Dynamic Pricing and Revenue Algorithms

1. Foundations of Revenue Management and Dynamic Pricing

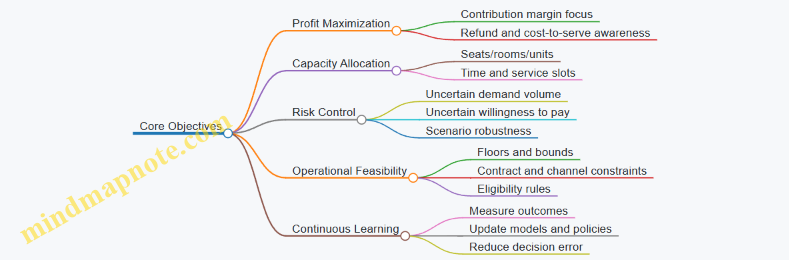

1.1 Core Objectives of Revenue Management and Pricing

Revenue management is the practice of deciding what to sell, to whom, for how much, and under what conditions—using limited capacity and uncertain demand. Pricing is the lever; revenue management is the system that decides how and when to pull it.

The Core Objectives

Maximize Expected Profit, Not Just Revenue. Revenue management often starts with revenue because it is easy to measure, but profit depends on costs, refunds, and service effort. A $120 booking that triggers heavy variable costs can be worse than a $110 booking with lower cost-to-serve.

Allocate Limited Capacity Intelligently. Capacity is not only seats, rooms, or units. It is also time on a service line, production slots, or bandwidth for delivery. The objective is to reserve capacity for higher-value demand while still selling enough to avoid empty capacity.

Control Risk Under Demand Uncertainty. Demand is uncertain in timing, volume, and willingness to pay. The system should avoid “all-or-nothing” decisions that look great in one scenario and fail badly in another.

Maintain Operational Feasibility. Pricing decisions must respect constraints like minimum margins, contractual rates, channel rules, and inventory availability. A theoretically optimal price that cannot be executed is just a fancy spreadsheet.

Improve Decision Quality Over Time. Objectives include learning from outcomes: if a price change consistently underperforms for a segment, the system should adjust. Learning is not a separate project; it is built into measurement and feedback.

Mind Map: Objectives and How They Connect

From Objectives to Decisions

A useful way to connect objectives to day-to-day decisions is to map each objective to a decision variable.

- Profit Maximization → Price and offer selection. If you can choose between a higher price with lower conversion and a lower price with higher conversion, you are optimizing expected profit.

- Capacity Allocation → Protection levels and inventory controls. You decide how much capacity to hold back for later or for higher-value segments.

- Risk Control → Guardrails and conservative policies. You limit how aggressively you change prices when uncertainty is high.

- Operational Feasibility → Constraints and eligibility logic. You ensure the system only proposes prices that can be honored.

- Continuous Learning → Measurement and feedback loops. You track whether the chosen policy actually performed as expected.

Example: A Simple Booking Scenario

Imagine an airline flight with 100 seats. You can offer two fare classes:

- Saver: $200, expected 60% chance of purchase if offered.

- Flex: $260, expected 35% chance of purchase if offered.

If you sell all seats at Saver, expected revenue is 100 × 0.60 × $200 = $12,000 (ignoring no-shows and assuming demand arrives until seats fill). If you restrict Saver and reserve seats for Flex, you trade off lower probability of selling each seat against higher value when demand is willing to pay.

A revenue-only mindset might chase the highest expected revenue per seat in isolation. A profit-aware mindset checks contribution margin and operational effects. For instance, if Flex bookings have lower refund rates or lower handling costs, Flex can be more attractive even when its raw purchase probability is lower.

Example: Capacity Allocation as a Protection Level

Suppose you expect two demand waves: early bookings are price-sensitive, late bookings are less price-sensitive. A protection level policy might reserve 20 seats for late demand.

- If early demand is strong, you still sell most early seats but stop selling Saver once you reach the protection threshold.

- If early demand is weak, you sell more early seats to avoid empty capacity.

This is risk control in action: you are not guessing one perfect outcome; you are choosing a rule that performs reasonably across multiple demand paths.

Objective Trade-Offs You Must Make Explicit

Revenue management is full of trade-offs, so the objectives should be stated in measurable terms.

- Revenue vs Profit: A higher price can reduce refunds or costs, improving profit even if revenue per seat drops.

- Sell-Through vs Value: Aggressive discounting increases sell-through but can cannibalize higher-value demand.

- Stability vs Responsiveness: Frequent price changes can improve fit but may create operational complexity and customer confusion.

When objectives are explicit, the system can justify decisions. When they are vague, the system becomes a collection of knobs with no clear target.

1.2 Demand Uncertainty and Capacity Constraints

Revenue management lives at the intersection of two realities: demand is not perfectly predictable, and capacity is not perfectly flexible. When you combine those, you get a simple but unforgiving rule—every unit of capacity you allocate today can’t be used later, and every pricing decision changes how many customers show up.

Demand Uncertainty as a Distribution, Not a Number

Instead of treating demand as a single forecast value, treat it as a range of outcomes. For a given time window (say, the next 14 days), demand might be 90, 110, or 140 units depending on seasonality, marketing effects, competitor actions, and random variation.

A practical way to think about this is: you choose a price, which influences demand, and then demand realizes from a distribution. Uncertainty matters because the “best” price under the average outcome can be worse under the tails.

Example: A hotel sets a nightly price for a weekend. If the price is too low, demand spikes and rooms sell out early, leaving later high-value demand unserved. If the price is too high, you may leave rooms empty, and empty rooms are lost revenue.

Capacity Constraints as a Hard Budget

Capacity constraints are usually modeled as a finite number of sellable units. The constraint is hard: you can’t sell more rooms than you have, and you can’t retroactively create capacity after the booking window closes.

There are two common forms of capacity constraints:

- Total capacity over a period: e.g., 500 seats available for a flight.

- Capacity by resource type: e.g., rooms by room type, or inventory by SKU and location.

When capacity is hard, the system must decide not only “what price should I offer,” but also “how much of my capacity should I reserve for later or for higher-value customers.”

The Booking Horizon and Time Coupling

Demand uncertainty is coupled across time. Early bookings reduce remaining capacity for later dates. That means your decision today affects the feasible set of decisions tomorrow.

A useful mental model is a booking horizon with a remaining inventory state. Each booking event updates the state, and future prices should be computed from the updated state.

Example: If you accept many low-fare bookings early, you may be forced to offer lower prices later because you still need to clear remaining inventory. If you protect capacity early, you can maintain higher prices later, but you risk unsold capacity if demand doesn’t materialize.

Protection Levels and Marginal Value

Protection levels convert uncertainty into a rule. The idea is to reserve some capacity for scenarios where demand is strong or customers are willing to pay more.

A common approach is to compare the expected value of selling one more unit now versus saving it for later. If the expected marginal value of selling now is lower than the value of keeping capacity, you protect.

Example: Suppose you have 100 seats. If you expect that later demand will likely support a higher fare, you might protect 20 seats. When a booking request arrives, you accept only if the fare exceeds the implied value of the protected seats.

Modeling Demand Under Capacity Limits

Demand models must respect capacity. If your demand model predicts 140 bookings for a 100-seat flight, the system can’t accept all 140. The accepted demand becomes the minimum of demand and remaining capacity.

This matters for evaluation. If you compute revenue using unconstrained demand, you’ll overestimate performance. You need constrained simulation or constrained optimization.

Example: A pricing policy might look great in a spreadsheet that assumes all demand converts. In reality, once capacity is exhausted, additional demand is lost. Your evaluation must include the “sell-out” behavior.

Practical Best Practices for Handling Uncertainty

- Use scenario-aware forecasts: Maintain multiple demand scenarios (low, base, high) rather than a single point estimate. Then compute expected outcomes across scenarios.

- Track uncertainty by segment: Uncertainty is not uniform. A last-minute business segment might be more predictable than a leisure segment that depends on travel plans.

- Update beliefs with new data: As the booking window progresses, observed bookings reduce uncertainty. Your system should incorporate this update rather than sticking to a static forecast.

- Separate demand drivers from capacity effects: Capacity changes acceptance rates, which can look like demand changes. Keep these effects distinct in your measurement.

Mind Map: Demand Uncertainty and Capacity Constraints

Worked Mini-Example with Constraints

Assume 10 units of capacity and two price options.

- Price A: expected demand 8 units, but could be 5–11.

- Price B: expected demand 6 units, but could be 3–9.

If you ignore capacity, Price A seems better because its average demand is higher. With capacity, the high-demand tail for Price A causes sell-out, and the low-demand tail leaves units unused. Price B may yield steadier accepted volume, which can translate into higher expected revenue when the marginal value of late capacity is high.

The key point is not which price wins in this toy example; it’s that capacity converts demand uncertainty into a nonlinear outcome. Your algorithm must model both the distribution of demand and the hard cap on accepted units.

1.3 Price Elasticity and Revenue Sensitivity Concepts

Price elasticity tells you how much demand changes when price changes. Revenue sensitivity tells you how revenue responds to that same price move. They’re related, but not identical: elasticity is about quantity, sensitivity is about money.

Elasticity Basics Without the Math Panic

Elasticity is usually expressed as a ratio of percentage changes. If price goes up by 1% and quantity drops by 2%, demand is more elastic than if quantity drops by only 0.5%. In practice, you’ll estimate elasticity from historical data or experiments, then use it to reason about pricing moves.

A key sign convention: demand typically falls when price rises, so elasticity is often negative. Many teams use the absolute value for “how responsive” and keep the sign implicit.

Point Elasticity Versus Average Elasticity

Point elasticity describes responsiveness at a specific price level. Average elasticity summarizes across a range, which can hide important curvature. For example, a product might be fairly inelastic near the current price but elastic at higher prices where customers switch to alternatives.

The Demand Curve Shape Matters

Elasticity changes as you move along the demand curve. Near the steep part of the curve, small price changes can cause large quantity shifts. Near the flat part, quantity barely moves. This is why “one elasticity number” can be misleading if your pricing policy makes large jumps.

Revenue Sensitivity: When Quantity Loss Beats Price Gain

Revenue is price times quantity. If you raise price, revenue increases only if the quantity loss is not too large. A useful intuition: revenue is most sensitive when demand is near the boundary between “price wins” and “quantity wins.”

A Simple Rule of Thumb

For many smooth demand relationships, revenue tends to increase with price when demand is relatively inelastic and decrease with price when demand is relatively elastic. The exact threshold depends on how elasticity is defined and how the demand curve behaves, but the practical takeaway is consistent: elasticity magnitude determines whether price increases are likely to help or hurt revenue.

Local Sensitivity Versus Global Outcomes

Revenue sensitivity is local: it describes what happens for small changes around the current price. If you plan to move price a lot, you need to consider how elasticity changes across the range, not just at one point.

Connecting Elasticity to Revenue with Concrete Examples

Example: A Subscription with Low Elasticity

Suppose a subscription costs $20/month. Historical data suggests that a 1% price increase reduces monthly subscribers by about 0.3% (absolute elasticity 0.3). If you raise price by 1% to $20.20, revenue per month changes approximately by +1% from price and −0.3% from quantity, netting about +0.7% revenue. The quantity loss is small enough that price gain dominates.

Example: A Ticketed Event with Higher Elasticity

Now consider event tickets. If a 1% price increase reduces attendance by 1.6% (absolute elasticity 1.6), then the −1.6% quantity effect outweighs the +1% price effect. Revenue would likely drop for small price increases. This doesn’t mean “never raise price,” but it signals that you should expect revenue to be fragile around the current price.

Example: Elasticity Differences Across Segments

Elasticity is rarely uniform. Business travelers might have low elasticity because they value schedule certainty, while leisure customers might have higher elasticity because they can wait for discounts. If you average elasticity across both groups, you can end up with a policy that looks reasonable on paper but underperforms because one segment is harmed more than the other benefits.

Estimating Elasticity in a Way That Supports Decisions

Elasticity estimates are only useful if they match the decision you’re making.

Observational Estimation Pitfalls

If price changes are correlated with demand shocks (for example, you raise price during high-demand periods), naive estimates can confuse “demand caused by seasonality” with “demand caused by price.” A good best practice is to control for time effects, promotions, and availability so the remaining variation is closer to price-driven.

Experiment-Based Estimation

When you run a controlled test, you can compare demand under different prices while holding other factors steady. Even then, be careful about eligibility rules: if only certain users see the price, your elasticity is conditional on that selection.

Mind Map: Price Elasticity and Revenue Sensitivity

Practical Checklist for Using Elasticity

- Use elasticity that matches your price move size: local estimates for small adjustments, curve-aware reasoning for larger ones.

- Keep segment-level elasticity when segments have different behaviors; averages can mislead.

- Verify that your estimation controls for promotions, time effects, and availability so price effects aren’t mixed with other drivers.

- Translate elasticity into revenue sensitivity using the “price gain versus quantity loss” intuition, then sanity-check with a small numerical scenario.

Quick Numerical Sanity Check

If you’re unsure whether a price increase helps, do a one-line calculation: assume a 1% price increase causes an x% quantity decrease where x is the absolute elasticity. Net revenue change is roughly +1% − x%. If that number is negative, revenue is likely to fall for small increases; if positive, it’s likely to rise.

1.4 Data Requirements for Pricing and Yield Systems

Pricing and yield algorithms are only as good as the inputs they trust. This section lays out what data you need, why each piece matters, and how to structure it so decisions can be made consistently in real time.

What “Good Data” Means for Pricing

For pricing and yield systems, “good” usually means three things: (1) the data describes the decision context accurately, (2) it is aligned in time so the model sees what the decision-maker saw, and (3) it can be audited after the fact.

A simple test: pick one offer shown to a customer, then trace backward to the exact features used and forward to the outcome. If you cannot reconstruct that chain, you will struggle to debug revenue dips or explain why a policy changed.

Core Data Domains

Demand and Outcome Signals

You need outcomes that reflect customer response and inventory consumption.

- Impressions or offer exposures: when an offer was eligible and shown.

- Selections or bookings: what the customer chose, including “no purchase” when available.

- Cancellations and refunds: revenue is not final until these are settled.

- Time stamps: offer time, decision time, booking time, and cancellation time.

Easy example: a hotel shows two room rates. If you only log bookings, you miss that the cheaper rate was shown but not chosen. That missing “no” is often the difference between learning and guessing.

Inventory and Capacity State

Yield systems require a precise view of what can still be sold.

- Capacity by resource: rooms, seats, inventory units.

- Availability by time window: how many units remain for each stay date or departure.

- Release and hold rules: when inventory becomes sellable and when it is reserved.

- Overbooking policy parameters: limits and risk thresholds.

Easy example: if 10 seats remain but your system thinks 12 do, your algorithm will happily sell too much and then scramble later.

Offer Catalog and Eligibility Rules

Pricing decisions depend on what offers are allowed.

- Offer definitions: price, included terms, restrictions, and validity.

- Eligibility logic: channel, customer segment, geography, device, loyalty status.

- Lifecycle events: when an offer is created, updated, paused, or retired.

Easy example: if a promotion ends at 18:00 but your data still marks it active until midnight, you will attribute demand lift to the wrong policy.

Customer and Context Features

Features describe who the customer is and what situation they are in.

- Customer attributes: segment, loyalty tier, historical behavior.

- Session context: device, channel, referrer, search parameters.

- Temporal context: day of week, lead time, holiday flags.

- Geographic context: origin market, region, currency.

Easy example: lead time is not just “days until travel.” It must be computed consistently from the same time basis used in the decision.

Cost and Margin Inputs

If you optimize margin, you need cost to go with revenue.

- Variable costs: per unit sold, per booking, per service.

- Semi-variable costs: costs that scale with volume but not perfectly linearly.

- Refund and chargeback costs: expected impact on contribution.

- Ancillary costs and fees: what you keep versus what you pass through.

Easy example: a low ticket price might still be profitable if the average cost is lower for that route or customer segment.

Data Quality Requirements That Prevent Silent Failures

Time Alignment and Event Ordering

Every training row should represent a decision at a specific time with a specific inventory state. If you join data by date only, you will mix “before” and “after” outcomes.

Consistent Identifiers and Join Keys

Use stable keys for customers, offers, inventory units, and transactions. If offer IDs change between systems, you will lose the ability to compare policies.

Coverage of the “No Decision” Case

You need a way to record when no offer was shown or when a customer was not eligible. Otherwise, the model learns that “missing” means “no demand,” which is rarely true.

Mind Map: Data Requirements for Pricing and Yield Systems

Example: Building a Single Training Row

Suppose you price a flight for a customer searching 30 days before departure.

- Decision time: record the exact moment the offer was generated.

- Inventory state: record remaining seats for that departure date and fare family.

- Offer details: record the exact price and restrictions shown.

- Customer context: record segment, channel, and lead time computed from the same time basis.

- Outcome: record whether the customer booked, and if so, capture cancellation later.

- Margin: attach expected variable cost and refund impact for that itinerary class.

If any of these fields are missing, you either drop the row or mark it explicitly. Dropping without tracking can bias results toward “easy” cases.

Practical Data Schema Checklist

- Event tables: offers shown, offers eligible, bookings, cancellations.

- State tables: inventory snapshots keyed by resource and time window.

- Reference tables: offer catalog, eligibility rules, cost tables.

- Feature store outputs: versioned features tied to decision timestamps.

- Decision logs: what the system recommended and what was actually served.

A pricing system is a chain. Data requirements are about making every link measurable, joinable, and explainable—so the algorithm can learn from reality instead of guessing at it.

1.5 Practical Example: Mapping Goals to Metrics

A revenue management system usually starts with a goal that sounds simple, like “maximize profit” or “improve fill rate.” The hard part is translating that goal into metrics that (1) can be measured reliably, (2) move when the pricing policy changes, and (3) don’t accidentally reward the wrong behavior. This example walks through a complete mapping from goals to metrics for a seat-based travel product.

Step 1: Write Goals in Decision Language

Assume the business goal is: increase contribution margin per departure while keeping customer experience stable. Break it into decision-relevant subgoals:

- Sell more seats at acceptable prices without exhausting inventory too early.

- Avoid selling at prices that are too low relative to variable costs and expected future demand.

- Prevent customer-visible issues like excessive price changes on the same itinerary.

Each subgoal should correspond to a lever the system can control: offer prices, offer eligibility, and booking limits.

Step 2: Choose Metric Families That Cover the Whole Loop

Use three metric families so you can see whether the system is winning for the right reasons.

- Outcome metrics measure what happened.

- Mechanism metrics measure how the system behaved.

- Guardrail metrics measure what must not degrade.

Here is the mapping for our example.

-

Outcome goal: contribution margin per departure

- Primary metric: contribution margin = (ticket price − variable cost − per-booking fees) × accepted bookings

- Secondary metric: margin per available seat (MPAS)

-

Outcome goal: sell more seats

- Primary metric: load factor (accepted bookings / available seats)

- Secondary metric: booking rate by time-to-departure bucket

-

Outcome goal: avoid too-low sales

- Primary metric: realized average price (or realized yield)

- Secondary metric: share of bookings in “low-price” bands

-

Guardrail goal: stable customer experience

- Primary metric: price change frequency for the same itinerary within a window

- Secondary metric: cancellation or refund rate attributable to price dissatisfaction signals (measured carefully)

-

Guardrail goal: operational safety

- Primary metric: offer rejection rate due to constraint violations

- Secondary metric: latency and decision failure rate

Step 3: Define Metrics with Clear Numerators and Denominators

Ambiguity is where good intentions go to die. For each metric, specify exactly what counts.

- Load factor: accepted bookings / total sellable seats for that departure.

- Realized average price: sum of accepted ticket prices / accepted bookings.

- Low-price band share: accepted bookings with price < threshold / accepted bookings.

- Price change frequency: number of distinct price updates shown to customers for an itinerary / number of itinerary views in the same window.

Pick thresholds using business policy, not vibes. For example, “low-price band” might be defined as below the variable-cost-plus-min-margin floor.

Step 4: Add a Small Example with Numbers

Suppose a departure has 100 seats. Over the booking horizon, the system accepts 78 bookings.

- Average accepted ticket price: 220

- Variable cost per booking: 60

- Per-booking fee: 5

Contribution margin = (220 − 60 − 5) × 78 = 155 × 78 = 12,090.

Now compare two pricing policies:

- Policy A: 78 bookings, realized average price 220 → margin 12,090

- Policy B: 80 bookings, realized average price 210 → margin = (210 − 65) × 80 = 145 × 80 = 11,600

Policy B sells more but earns less margin. That’s why you need both outcome and mechanism metrics: load factor alone would have picked the wrong winner.

Step 5: Mind Map of the Mapping Process

Mind Map: Mapping Goals to Metrics

Step 6: Sanity Checks Before You Trust the Metrics

Before running a full policy comparison, verify three things:

- Metric sensitivity: when you change the pricing policy in a controlled way, the metric moves in the expected direction.

- Metric integrity: the metric can be recomputed from logs without missing fields.

- Metric alignment: improving one metric doesn’t systematically worsen a guardrail.

If a metric fails any of these, it’s not “wrong” forever, but it is not ready to be a decision driver yet. In practice, this step prevents the system from optimizing a scoreboard that doesn’t match the business goal.

2. Pricing Data Engineering and Feature Construction

2.1 Event and Transaction Data Modeling for Pricing

Pricing systems live or die by the quality of their inputs. “Modeling” here means turning raw logs into a consistent set of entities, events, and measurements that can be joined, replayed, and audited. The goal is simple: every decision the system makes must be explainable in terms of what it knew at the time.

Start with the Decision Loop

A pricing decision usually follows this loop: an offer is shown, a user responds, and the system updates future decisions. To model this cleanly, define a decision timestamp and treat everything after it as outcome data.

Key modeling rule: store the decision context separately from the outcome. For example, the offer shown at 10:03:12 should not silently change if the user’s later session attributes are corrected.

Define Core Entities

Most pricing domains can be represented with a small set of entities.

- Subject: the thing being priced (seat, room night, SKU, subscription term).

- Customer: the identity or anonymous key used for segmentation.

- Channel: where the offer is surfaced (web, app, call center).

- Offer: the concrete price and terms presented (price, currency, fees included/excluded, restrictions).

- Transaction: the completed purchase or booking, including quantity and final paid amount.

Each entity needs a stable identifier and a time window. If you cannot define the window, you will eventually join the wrong facts.

Model Events with Clear Semantics

Events are what happened, in order. For pricing, you typically need:

- Offer Display Event: when an offer becomes eligible and is actually shown.

- Offer Interaction Event: clicks, add-to-cart, selection, or quote requests.

- Offer Acceptance Event: the moment the user commits to the offer terms.

- Transaction Completion Event: payment success, booking confirmation, or fulfillment start.

- Cancellation or Refund Event: reversals that affect realized margin.

A practical best practice is to attach a decision_id to each offer display and interaction. That way, you can trace outcomes back to the exact pricing logic that produced the offer.

Separate Offer Terms from Price Numbers

Offers are more than a single price. Two offers with the same price can differ in fees, cancellation rules, or included taxes. Model:

- Price components: base price, taxes, service fees, discounts.

- Terms: refundability, minimum stay, inventory rules.

- Eligibility: which segments and channels can see it.

Example: A hotel might show “$200 + $25 service fee” versus “$225 all-in.” If you store only one paid amount, you lose the ability to compute margin correctly when costs attach to specific components.

Build a Transaction Fact Table

A transaction fact table should represent realized outcomes, not just intent. Include:

- transaction_id

- subject_id and quantity

- final_paid_amount and currency

- cost components used for margin (variable fulfillment cost, payment processing, support cost)

- status (completed, canceled, refunded)

- timestamps (created, completed, refunded)

Then link it to the offer via offer_id or decision_id. If you only link by customer_id and time proximity, you will eventually misattribute outcomes.

Handle Time Zones and Late Arrivals

Pricing logs often arrive late due to buffering, retries, or batch exports. Use two timestamps:

- event_time: when the event occurred.

- ingest_time: when it was recorded.

For joins, prefer event_time for business logic and ingest_time for pipeline correctness. Also normalize time zones at ingestion so “10:00” means the same moment across systems.

Mind Map: Data Model for Pricing

Example: Joining Offer Displays to Realized Margin

Suppose a pricing service generates an offer for a seat. You store an offer_display event with decision_id, subject_id, and price components. Later, the transaction completes and you store final_paid_amount plus costs.

To compute realized margin for that decision, join:

- offer_display (decision_id, subject_id, event_time)

- transaction_facts (decision_id or offer_id, status, completion_time)

- cost components (variable_cost, processing_fee)

Then calculate margin as: final_paid_amount − variable_cost − processing_fee − refunds_adjustment. If a refund event arrives later, update the adjustment using refund timestamps, not the original completion timestamp.

Example: Preventing “Context Drift”

A common failure mode is recomputing features after the fact. If you store only raw customer attributes and rebuild features later, you might change the offer context for past decisions.

Best practice: snapshot the feature set used for the decision (or at least the key features) alongside decision_id. Then your audit trail can answer: “What did the system know when it chose this price?”

Validation Checklist for Modeling

Before you trust any pricing algorithm, validate the data model with checks that catch structural issues:

- Every offer_display has a decision_id.

- Every transaction links to exactly one accepted offer (or has a defined attribution rule).

- Currency is consistent within a transaction fact.

- Refunds and cancellations reduce realized margin using event_time ordering.

- No joins rely on “nearest timestamp” without an explicit rule.

When these constraints hold, your pricing analytics stop being a guessing game and become a measurable system.

2.2 Building Customer, Segment, and Channel Features

Good pricing decisions depend on features that describe who the customer is, what they are likely to do, and how they arrived. This section builds those features in a way that stays consistent from data collection to model input.

Customer Identity Features

Start with stable identifiers and basic behavioral summaries. Use them to create features that are meaningful even when some events are missing.

- Customer tenure: days since first purchase or first account creation.

- Recency: days since last purchase or last meaningful interaction.

- Purchase history counts: number of orders in the last 30/90/180 days.

- Typical basket size: rolling average of order value, plus a count of orders used to compute it.

- Product affinity: share of purchases in the last 90 days that belong to each major category.

Best practice: compute rolling windows with explicit denominators. For example, “average order value last 90 days” should also carry “number of orders last 90 days,” so the model can treat sparse customers differently.

Example: A customer with one order in the last 90 days gets a less confident “typical basket size” than a customer with 20 orders. The second feature (order count) lets the model learn that difference.

Segment Features That Generalize

Segments are not just labels; they are structured summaries that reduce noise. Build segments using rules that match how demand differs.

Common segment dimensions:

- Value tier: based on lifetime spend or average margin contribution.

- Engagement tier: based on browsing or search activity frequency.

- Price sensitivity proxy: based on historical response to discounts.

- Risk tier: based on refund rate, chargebacks, or cancellation frequency.

Best practice: keep segment definitions versioned. If you change the rule that defines “value tier,” you must know which definition was used for each training row.

Example: If “value tier” is defined by lifetime spend thresholds, store both the tier and the raw lifetime spend. The tier helps generalization; the raw value preserves ordering within tiers.

Channel Features That Explain Context

Channel features capture the path to the offer, which often changes both intent and constraints.

Channel dimensions to model:

- Acquisition channel: organic search, paid search, email, affiliate, direct.

- Device and platform: mobile web, iOS app, Android app, desktop.

- Session context: landing page type, referrer category, campaign identifier.

- Fulfillment context: delivery speed selection, pickup vs delivery.

Best practice: separate “channel” from “campaign.” Campaign identifiers can be sparse and short-lived; channel is usually more stable. When you include campaign, also include channel so the model can fall back when campaign data is missing.

Example: Two customers both arrive via “email,” but one is from a “10% off” campaign and the other is from a “back in stock” message. Channel features describe the shared baseline; campaign features describe the specific incentive.

Feature Engineering with Guardrails

Pricing features often fail in predictable ways: leakage, inconsistent timestamps, and mixing training and serving logic. Use these guardrails.

- Timestamp discipline: every feature must be computed using events strictly before the decision time.

- Missingness as information: include explicit flags like “no recent purchases” rather than imputing silently.

- Scale consistency: normalize continuous features (e.g., log-transform order value) and keep the same transformation at training and serving.

- Cardinality control: for high-cardinality fields (e.g., campaign id), use hashing or target-encoding with careful leakage prevention.

Example: If you compute “orders in last 30 days” at training time using the full dataset, you may accidentally include orders that happened after the price was shown. The fix is to compute features from an event stream with a strict cutoff at the decision timestamp.

Mind Map: Customer, Segment, and Channel Features

Practical Example: One Offer, Three Feature Views

Suppose you show a discount offer for a product category. Build three aligned feature sets for the same decision time.

- Customer view: recency, last 90-day category affinity, and order count in the last 90 days.

- Segment view: value tier and price sensitivity proxy derived from historical discount response.

- Channel view: acquisition channel, device type, and fulfillment context.

Then add guardrail features: a missingness flag for “no orders in last 90 days,” and a “feature computed from available history length” indicator. This makes the model robust when customers are new or when event logs are incomplete.

The result is a feature design that is interpretable, consistent, and resilient. It also gives the model multiple ways to explain demand differences without forcing one brittle definition to do all the work.

2.3 Handling Inventory, Availability, and Offer Lifecycles

Inventory and availability are the “what can be sold” layer, while offer lifecycles are the “how and when it can be sold” layer. If you treat them as one thing, you’ll eventually sell the wrong thing at the wrong time. The goal is to keep these concepts separate in your system design and then connect them with clear rules.

Inventory as State, Not a Number

Start with inventory as a state machine. A seat, room, or unit is either available, reserved, sold, or blocked. The system should track transitions, not just a remaining count. For example, a flight seat might be:

- Available: eligible for offers.

- Reserved: held for a user session or payment window.

- Sold: committed and no longer eligible.

- Blocked: unavailable due to operational reasons (crew changes, maintenance, manual holds).

Best practice: represent inventory events (reserve, release, sell, block) as append-only logs, then compute current availability from those events. This makes debugging far less painful than trying to infer history from a single number.

Availability as Eligibility Logic

Availability answers: “Given the current inventory state, which offers are eligible for a given user and context?” Eligibility depends on more than remaining units. It typically includes:

- Time windows: booking open/close, cutoff times, check-in deadlines.

- Channel rules: direct vs. partner access, contract restrictions.

- Offer validity: start/end timestamps, minimum stay or length-of-use.

- Segment constraints: age bands, membership tiers, corporate agreements.

Easy example: Suppose a hotel has 10 rooms. If 3 are reserved for a group that only accepts refundable rates, then the remaining 7 rooms may still not be eligible for a nonrefundable offer if the offer requires a specific cancellation policy.

Offer Lifecycles as Controlled Lifetimes

An offer is a priced, bookable option with a defined lifetime. Offers should not live forever, even if inventory does. Common lifecycle stages:

- Draft: computed but not yet shown.

- Published: visible to users and eligible for selection.

- Committed: selected and payment is underway.

- Expired: lifetime ended without commitment.

- Superseded: replaced by a newer offer due to inventory or price updates.

Best practice: tie offer expiration to both time and state changes. If inventory changes materially (e.g., a unit is sold elsewhere), mark affected offers as superseded immediately rather than waiting for their timer.

Reservation Windows and Consistency

Reservations prevent overselling during the gap between “user clicks” and “payment confirms.” The tricky part is consistency across services.

A practical approach:

- When an offer is selected, create a reservation with an expiration timestamp.

- Lock the reservation to the exact inventory unit(s) or to a capacity bucket with a clear reconciliation rule.

- If payment fails or the reservation expires, release inventory back to availability.

Example: A booking request arrives at 10:00:05. You reserve capacity for 90 seconds. If payment confirms at 10:01:20, the reservation becomes a sale. If it confirms at 10:02:10, the reservation has expired, so the system must reject or reprice.

Handling Cancellations and Repricing Safely

Cancellations create new inventory, but they also create new opportunities for offers. The safe rule is: inventory release should trigger availability recomputation, and availability recomputation should trigger offer refresh only for impacted segments.

Example: If a cancellation returns 1 seat to a fare family, you may need to:

- Update the remaining capacity for that fare family.

- Recompute bid prices or protection levels for the affected time bucket.

- Invalidate offers that depended on the previous capacity.

Do not silently keep old offers active. Users will notice when the system “accepts” a selection and then fails at confirmation.

Mind Map: Inventory, Availability, and Offer Lifecycles

Example: End-to-End Flow for a Single Offer

Consider a train ticket offer for a specific departure date.

- Compute eligibility: check booking window, channel access, and segment constraints.

- Check inventory state: confirm capacity is available for the relevant fare bucket.

- Publish offer: assign a price and an expiration time (e.g., 2 minutes).

- User selects: create a reservation tied to the offer and inventory bucket.

- Payment confirms: convert reservation to sold and finalize the booking.

- Payment fails or expires: release reservation and mark the offer expired.

- Concurrent updates: if another sale reduces capacity before confirmation, supersede the offer so the user must see updated eligibility.

This flow keeps the system honest: inventory changes drive availability, availability drives offer eligibility, and offer lifecycles control what users can actually do at any moment.

2.4 Data Quality Controls for Real Time Pricing Inputs

Real time pricing decisions are only as good as the inputs they consume. In practice, “data quality” means more than accuracy; it includes timeliness, completeness, consistency, and whether the data matches the decision being made. This section lays out a systematic control stack that starts with basic checks and ends with decision-time safeguards.

Data Quality Goals for Pricing Decisions

A pricing engine typically needs features such as availability, demand signals, customer context, and offer eligibility. Quality controls should therefore target four failure modes:

- Wrong value: a feature is incorrect (e.g., inventory shows 12 when 2 are actually sellable).

- Missing value: a feature is absent (e.g., channel is null, so eligibility rules can’t run).

- Stale value: a feature is old (e.g., inventory updated 30 minutes ago but the decision is now).

- Inconsistent meaning: the same field is interpreted differently across systems (e.g., “booking date” means local time in one pipeline and UTC in another).

A useful mindset is to treat each feature as having a “contract”: what it represents, its allowed range, its freshness expectation, and how it should be handled when it fails.

Foundational Checks Before Any Modeling

Start with checks that are cheap and deterministic.

Schema and type validation ensures the incoming payload matches expectations. For example, if price_floor arrives as a string instead of a number, the engine should fail fast or coerce safely.

Range and constraint checks catch impossible values. If availability can’t be negative, enforce availability >= 0. If lead time is computed from timestamps, enforce lead_time_minutes >= 0.

Completeness checks verify required fields exist for the decision path. If the pricing policy depends on customer_segment, then missing segment should trigger a defined fallback segment or a “no-offer” response.

Freshness checks compare event timestamps to the decision timestamp. A practical rule is to define a maximum acceptable delay per feature. Inventory might tolerate seconds; a weekly promotion flag might tolerate hours.

Consistency Controls Across Systems

Consistency problems are subtle because each system can be “correct” locally.

Key alignment ensures joins use the same identifiers. A classic failure is joining by product_id in one table and sku_id in another, producing silent mismatches.

Time zone normalization prevents off-by-one-day errors. If a booking window is defined in local time, convert all timestamps into that same frame before computing lead time or cutoff eligibility.

Unit normalization avoids mixing currencies, weights, or quantities. If costs are stored in cents but revenue features are in dollars, you’ll get confidently wrong margins.

Decision-Time Guardrails

Even with pipeline controls, you still need safeguards at the moment of decision.

Eligibility gating should be the first step. If required inputs fail validation, do not attempt to optimize; instead, apply a conservative policy such as returning the last known safe offer or withholding offers.

Fallback strategies must be explicit and testable. Example: if demand_signal is missing, use a neutral default (e.g., baseline demand index) rather than reusing an old value.

Rate limiting for updates prevents thrashing when upstream systems briefly glitch. If inventory changes by an extreme amount in a short window, clamp the change and log the anomaly.

Logging and Traceability That Actually Helps

Controls without observability are just hope with extra steps.

Log the following for every pricing decision:

- Feature validation outcomes (pass/fail per feature)

- Freshness deltas (how late each feature was)

- Fallbacks used (which defaults were applied)

- The final offer inputs (so you can reproduce the decision)

A simple rule: if you can’t explain why an offer was withheld, you don’t have enough logging.

Mind Map: Data Quality Controls for Real Time Pricing Inputs

Example: Inventory Freshness and Fallback

Suppose an airline pricing request arrives at 2026-02-26 10:05:00 UTC. The pricing engine requires sellable_seats and expects inventory freshness within 60 seconds.

- Upstream inventory timestamp: 10:03:00 UTC

- Freshness delta: 120 seconds

- Validation result: stale inventory

Best practice: do not use the stale value. Instead, apply a fallback such as:

- Use the last inventory snapshot that is within freshness tolerance, if available.

- If none exists, withhold offers for that cabin and log the reason.

This avoids a common failure where the system “works” but sells seats that are already gone.

Example: Unit Normalization for Margin Inputs

A hotel margin policy needs variable cost per booking. Costs arrive from finance in cents, while the pricing engine expects dollars.

- Incoming

variable_cost_cents = 1250 - Engine expects

variable_cost_dollars

Control: enforce a unit contract at ingestion. Convert cents to dollars (12.50) before any margin computation. If conversion is missing, margin optimization can systematically bias prices while still producing plausible numbers.

Example: Consistency Through Time Zone Normalization

A retail promotion ends at 23:00 local time. The promotion service stores timestamps in local time; the pricing engine uses UTC.

Control: normalize both to the same time zone before computing whether the offer is eligible. Without this, customers near midnight can see offers that should have expired, and the engine will “correct” itself later with inconsistent behavior.

Summary of the Control Stack

Use deterministic checks first, then cross-system consistency, then decision-time guardrails, and finally traceability. When each feature has a contract and every failure path is defined, real time pricing becomes predictable in the only way that matters: the system behaves the same way under both normal and messy inputs.

2.5 Practical Example: Designing a Pricing Feature Store

A pricing feature store is the place where raw signals become consistent, reusable inputs for forecasting, optimization, and real time price control. The goal is simple: the same customer, time, and context should produce the same features across teams and systems, with clear freshness rules.

Step 1: Define Feature Contracts

Start with a contract that every downstream model can trust. For each feature, specify: meaning, grain, allowed values, time window, and update cadence.

- Meaning: what the feature measures (e.g., “days until departure”).

- Grain: the unit each row represents (e.g., offer_id × request_time).

- Time window: how far back history is used (e.g., last 7 days).

- Freshness: when the feature becomes valid (e.g., updated every 15 minutes).

Example: If you store days_to_event, compute it at the request timestamp, not at midnight. Otherwise, two requests a few hours apart can disagree.

Step 2: Choose the Store Layout

A practical layout separates features by purpose and update frequency.

- Static attributes: rarely change (e.g., customer tier, route). Update daily.

- Slow changing: update hourly or daily (e.g., rolling average conversion rate).

- Fast changing: update near real time (e.g., current inventory availability, active promotions).

This separation prevents a common failure mode: recomputing everything for every request.

Step 3: Build a Minimal Feature Set First

Resist the urge to store every possible metric. Start with features that map cleanly to pricing decisions.

Core demand context

days_to_eventday_of_weekseason_bucketlead_time_bucket

Offer and channel context

channel_idoffer_typeprice_position_in_ladderis_promo_active

Inventory and availability context

remaining_capacitycapacity_utilizationsold_out_flag

Customer and segment context

segment_idloyalty_statusrecent_purchase_count_30d

Example: For a travel product, capacity_utilization might be sold / (sold + remaining) computed at the same time window as remaining_capacity so the model doesn’t see contradictory signals.

Step 4: Implement Time-Aware Joins

Features often come from different pipelines. The store must join them using the request timestamp.

- Use as-of joins: each feature value must be the latest one not after the request time.

- Apply lookback windows consistently (e.g., “last 14 days” means 14×24 hours ending at request time).

Example: If promotions are logged with start and end times, compute is_promo_active by checking whether request_time falls within the interval.

Step 5: Add Guardrails for Data Quality

Quality checks should run before features are served.

- Schema checks: correct types, no missing required fields.

- Range checks:

days_to_eventmust be non-negative for future events. - Distribution drift checks: detect sudden spikes in missingness.

When a check fails, decide a policy: drop the request, fall back to last known good, or use a default with a “fallback_used” flag.

Mind Map: Pricing Feature Store Design

Step 6: Version Features and Log Decisions

Versioning prevents silent changes from breaking model behavior.

- Feature version: increment when logic changes.

- Model version: record which model consumed which feature version.

- Decision logging: store request context, features used, and chosen price.

Example: If you change capacity_utilization from “sold/(sold+remaining)” to “sold/total_capacity,” you must bump the feature version and keep old values for backtesting.

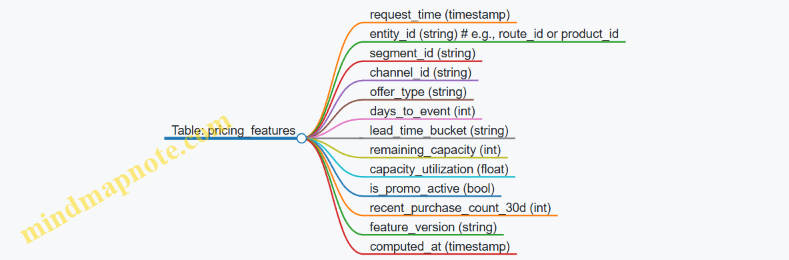

Step 7: Example Feature Store Schema

A simple schema keeps things understandable.

Step 8: End-to-End Example Flow

- A pricing request arrives with

request_time,entity_id,segment_id, andchannel_id. - The store retrieves static, slow, and fast features using as-of logic.

- Guardrails validate ranges and missingness; if needed, a fallback flag is set.

- The pricing model consumes the feature vector and outputs a candidate price.

- The system logs the feature_version and the chosen price for later evaluation.

This workflow makes debugging practical: if revenue drops, you can check whether the feature inputs changed, whether freshness lagged, or whether the model saw a different capacity state.

3. Demand Forecasting for Yield Management

3.1 Forecasting Targets and Granularity Choices

Forecasting starts with two decisions that quietly control everything else: what you forecast (the target) and at what level you forecast it (the granularity). If either is wrong, the model can be perfectly trained and still produce decisions that miss the mark—like measuring a marathon with a ruler.

Define Forecasting Targets

A forecasting target is the quantity your system will use downstream to choose prices, protect capacity, or decide which offers to show. Common targets include:

- Demand volume: expected number of bookings or units sold in a time window.

- Arrival process: expected number of customers arriving per day or per hour.

- Conversion rate: probability an eligible user books given an offer.

- Revenue or margin per booking: expected value conditional on booking.

In yield and dynamic pricing, demand volume and conversion rate are usually the workhorses. Revenue and margin are often computed after the fact using the chosen price and cost rules, because those depend on the decision you’re trying to make.

A practical best practice is to forecast the “decision-relevant” quantity. For example, if your pricing algorithm selects among discrete price points, you typically need demand (or conversion) as a function of price. If you only forecast total revenue historically, you’ll struggle to attribute changes to price versus mix.

Choose Granularity Levels

Granularity is the “where” and “when” of the forecast. Typical axes are:

- Time: day, hour, or booking horizon buckets (e.g., 0–3 days before arrival).

- Customer segment: channel, geography, loyalty tier, device type, or past behavior bucket.

- Product or offer: SKU, fare family, room type, seat bucket, or bundle.

- Channel: direct web, call center, partner marketplace.

The goal is to match granularity to operational control. If your system can only change prices once per day, forecasting hourly demand won’t help much; it may even create noise that looks like signal. Conversely, if you update offers every few minutes, daily granularity can hide short-lived demand spikes.

A useful rule: forecast at the finest granularity you can support with stable data, then aggregate upward for decisions that don’t require finer control.

Mind Map: Target and Granularity Design

Booking Horizon Versus Calendar Time

Many revenue systems forecast by booking horizon—time remaining until the service date—because demand patterns often change as the departure date approaches. Calendar time captures seasonality, but horizon captures urgency and planning behavior.

A systematic approach is to include both:

- Use calendar time features to represent macro effects like weekends.

- Use horizon buckets to represent the “how close are we” effect.

Example: A hotel might see strong weekend demand, but the last 3 days before check-in also behave differently from 30 days out. If you forecast only by calendar day, you’ll mix these effects and force the model to learn a complicated relationship it doesn’t need.

Segment Granularity and Data Sufficiency

Segmenting too aggressively creates sparse data. Sparse data leads to unstable estimates of conversion or demand, which then causes erratic pricing.

A best practice is to start with a segmentation that is both operationally meaningful and statistically supported. For instance:

- If you can route customers by channel, start with channel.

- If you can only observe loyalty tier reliably for returning customers, keep a “known loyalty” bucket and an “unknown” bucket.

Example: Suppose you split web traffic into 20 micro-segments by device and referrer. If each segment has only a few thousand eligible impressions per week, conversion estimates will swing with random variation. A safer approach is to group devices into fewer buckets and keep referrer categories broader.

Target Choice: Volume Versus Conversion

When you have clear eligibility rules (who sees which offer), conversion rate can be more stable than raw demand volume because it factors out exposure.

Example: Two channels may generate the same number of impressions, but one channel’s users are more likely to book. Forecasting conversion rate per channel lets your pricing logic respond to willingness to pay rather than being distracted by differences in traffic volume.

If you forecast volume directly, you must ensure the model accounts for both traffic and conversion. That’s doable, but it increases the number of moving parts.

Evaluation at Multiple Levels

Granularity choices should be validated where decisions happen. Backtesting only at the most aggregated level can hide problems.

Example: A model might predict total bookings correctly for the week, but fail for a specific fare family near the end of the booking horizon. The aggregated metric looks fine, while the protection logic quietly breaks.

A systematic evaluation set includes:

- Accuracy metrics at the decision granularity (e.g., fare family by horizon bucket).

- Calibration checks for conversion probabilities.

- Error decomposition by segment to locate where the model is consistently off.

Practical Example: Designing a Forecasting Setup

Imagine an airline with discrete fare classes and frequent offer updates. A coherent setup is:

- Target: conversion rate per fare class and booking horizon bucket.

- Granularity:

- Time: booking horizon buckets (e.g., 0–3, 4–7, 8–14, 15–30 days).

- Segment: channel (direct vs partner) and a coarse loyalty tier.

- Product: fare class.

Then compute expected bookings by multiplying predicted conversion by eligible impressions (or eligible customer arrivals) for each bucket. This keeps the forecast aligned with what the pricing system actually controls: which fare class is offered and at what price.

The result is a forecast that is not just accurate in hindsight, but useful in the exact places where pricing decisions are made.

3.2 Time Series Models for Booking and Arrival Processes

Booking and arrival processes are time-indexed systems: demand arrives over time, inventory is consumed, and the remaining capacity changes what future demand can do. A good time series model respects three realities: (1) arrivals are not evenly spaced, (2) booking behavior changes as the departure date approaches, and (3) price and availability affect what gets booked, even if you model them separately.

Core Time Axis Choices

Start by deciding what “time” means in your dataset. For bookings, common axes are booking timestamp (when the customer books) and stay/usage start date (when the customer uses the product). For arrivals, you often model the usage start date as the event time.

A practical rule: use one axis for the event you care about (arrival or usage start) and another for the lead time (days before arrival). Lead time is usually the more stable structure because it captures the approach to departure.

Modeling Arrival Counts

Let \( A_t \) be the number of arrivals in time bucket \(t\) (for example, per day). The simplest baseline treats (A_t) as a count process. A Poisson model assumes the variance equals the mean; real booking data usually has extra variance, so a Negative Binomial model is often a better starting point.

Best practice: fit a baseline model per segment or per route/channel, then check residual patterns by lead time. If residuals cluster near the departure date, your model is missing the “last-minute” shape.

Lead Time Effects and Nonstationarity

Booking behavior is strongly nonstationary: early lead times look different from late lead times. Instead of forcing one stationary process across all lead times, represent time as lead time \(L\) and model \(A(L)\) or booking intensity as a function of \(L\).

A simple and effective approach is a two-stage structure:

- Model the arrival intensity by lead time.

- Convert intensity into expected arrivals for each future day.

This keeps the model interpretable and makes it easier to apply booking controls later.

Intensity Models for Booking Curves

Many revenue systems use an intensity view: the probability of a booking happening in a small interval depends on the current lead time and current conditions (like price and remaining inventory). Even if you don’t model inventory directly, you can still model the baseline intensity.

A common form is:

- Expected arrivals in bucket \(t\): \(\mathbb{E}[A_t] = \lambda(t)\)

- Where \(\lambda(t)\) is a smooth function of lead time and calendar features.

Calendar features matter because demand has weekly and seasonal cycles. Include day-of-week and holiday indicators, and treat them as exogenous inputs rather than letting the model “discover” them from noise.

Seasonality and Calendar Features

Seasonality can be handled with either explicit features or seasonal components. Explicit features are often easier to debug:

- Day of week (categorical)

- Month or week-of-year (categorical or cyclic)

- Holiday flags

- Local events if you have them

Best practice: keep holiday effects separate from general seasonality. Otherwise, the model may smear a sharp holiday spike into nearby days and distort protection levels.

Autocorrelation and Residual Structure

Arrivals are correlated across time buckets because demand is not independent. If you ignore autocorrelation, your forecast intervals will be too narrow and your booking control will be overconfident.

A standard approach is to use autoregressive terms on residuals or to adopt a state-space model. For example, an AR component can capture short-term correlation after accounting for lead time and calendar.

Check this systematically:

- Fit the model.

- Plot residuals by lead time and by calendar position.

- If residuals show a repeating pattern, your seasonality representation is incomplete.

State-Space Models for Evolving Behavior

State-space models represent the system as a hidden state that evolves over time. In booking, the hidden state can represent “current demand level” or “market momentum” after controlling for lead time and calendar.

A useful mental model: the observed arrivals are noisy measurements of an underlying demand state. As new data arrives, the state updates, which naturally supports rolling forecasts.

This is especially helpful when you need forecasts that update frequently during the booking horizon.

Practical Example: Modeling Daily Arrivals by Lead Time

Suppose you forecast arrivals for a product with departure date \(D\). For each historical booking, compute lead time (\(L = D - \text{booking date}\)). Aggregate arrivals by lead time bucket (e.g., 0–6 days, 7–13 days, etc.) and by day-of-week of departure.

Then:

- Fit \(\lambda(L, \text{dow})\) using a Negative Binomial regression.

- Include holiday indicators for departure date.

- Add a small autoregressive correction on daily residuals within each departure day-of-week group.

Finally, generate expected arrivals for each future departure day by summing expected intensity across lead time buckets.

Mind Map: Time Series Modeling for Booking and Arrival Processes

Validation Checklist That Actually Helps

Before you trust the forecast, verify that the model reproduces the booking curve shape. A quick sanity test is to compare predicted and actual arrivals aggregated by lead time buckets. If the model matches the curve but misses day-to-day variation, you can still use it for booking control, provided your uncertainty estimates reflect the remaining variance.

If the model matches day-to-day variation but misses the curve shape, your protection levels will be wrong near the departure date. In that case, fix lead time representation first, then revisit autocorrelation.

Example: A Simple Baseline with Clear Failure Modes

Start with a Negative Binomial regression for arrival counts using lead time buckets and day-of-week of departure. If forecasts systematically underpredict late lead times, add a flexible term for lead time (more buckets or a smooth spline). If forecasts overpredict holiday spikes, separate holiday indicators from general seasonality and refit.

This “fit, inspect, adjust” loop keeps the model grounded in observable structure rather than hoping the algorithm figures out the booking curve on its own.

3.3 Incorporating Price and Promotion Effects in Forecasts

Forecasting demand without accounting for price and promotions is like planning a trip while ignoring traffic lights. You can still arrive, but you’ll keep “mysteriously” missing your timing. This section explains how to incorporate price and promotion effects systematically, from basic modeling choices to practical validation.

Price and Promotion Effects as Forecast Inputs

Start by separating two roles that price and promotions play in forecasting:

- They shift demand: a higher effective price usually reduces quantity demanded, while promotions can increase it.

- They change the composition of buyers: promotions may attract more price-sensitive customers or different purchase timing.

In practice, you need forecast features that represent the effective price customers face at the moment they decide, plus promotion context such as discount depth, duration, and whether the offer is active.

Defining Effective Price and Promotion Variables

Effective price should reflect what the customer actually pays after discounts and fees. A simple example for retail:

- List price: $100

- Coupon: 20% off

- Net price: $80

For forecasting, represent this as a numeric feature (net price) rather than only a “promo yes/no” flag. Promotions also need structure:

- Discount depth: percent off or absolute off

- Promo type: coupon, , bundle, free shipping

- Promo phase: first day, middle, last day

- Promo intensity: discount depth multiplied by availability (if you have it)

If you only have a binary promo indicator, you can still model lift, but you’ll lose the ability to forecast different discount levels accurately.

Modeling Approaches That Work in Real Systems

Use a modeling approach that matches your data and decision granularity.

Baseline Demand Model

First build a baseline that captures non-price effects:

- seasonality (day-of-week, month)

- trend (slow drift)

- calendar effects (holidays)

- channel effects (web vs store)

This baseline should forecast demand when price and promotions are “normal.”

Additive Lift Model

A straightforward method is:

- Forecast = Baseline + Promotion Lift

Price can be included as an additional term, for example:

- Forecast = Baseline + α · (Net Price) + β · (Promo Indicator)

This is easy to interpret, but it assumes linear relationships and can struggle when demand response is nonlinear.

Multiplicative Response Model

A more stable alternative is to model demand as a multiplier:

- Forecast = Baseline × (1 + Promotion Lift Rate)

For price, you can use a log-linear form:

- log(Demand) = baseline terms + γ · log(Net Price) + …

This often behaves better because demand changes tend to scale rather than shift by a constant amount.

Avoiding Common Data Traps

Price and promotions are rarely random. They are often set in response to demand signals, which can bias estimates.

- Confounding by intent: if promotions are triggered when demand is already weak, a naive model may think promotions reduce demand.

- Selection effects: certain segments see different offers, so “promo” is not comparable across customers.

- Stockouts and availability: if items are out of stock during a promo, observed demand won’t reflect the offer’s true effect.

Practical mitigations:

- Include availability indicators or filter out periods with stockouts.

- Use lagged price/promo features when decisions are made before purchase.

- Fit at the right level of aggregation so that price/promo exposure is comparable.

Example: Forecasting with Net Price and Promo Depth

Suppose you forecast weekly units for a product. You have:

- Baseline seasonality already modeled.

- Net price varies due to s.

- Promotions occur for 2 weeks with varying discount depth.

A workable feature set for each week:

- NetPrice

- PromoDepthPercent (0 when no promo)

- PromoWeekIndex (1, 2 during the promo, 0 otherwise)

- DaysSinceLastPromo

- AvailabilityRate

Then you fit a response model where promotion lift depends on depth and phase. For instance, you might find:

- Each additional 5% discount increases units by a smaller amount later in the promo window.

- The first promo week has higher lift because customers notice and act sooner.

This matters because your forecast for a future promo must reflect the phase, not just the discount.

Mind Map: Price and Promotion Effects in Forecasts

Validation That Confirms You’re Modeling the Right Thing

After fitting, validate in ways that directly test price and promo behavior.

- Scenario backtests: compare forecasts under historical promo depths to actual outcomes.

- Residual patterns: check whether errors systematically grow during promo periods or at specific discount levels.

- Stability checks: verify that the model’s response to price doesn’t flip sign when you change aggregation level.

A model that predicts “average lift” but fails at different discount depths is still useful for rough planning, but it will mislead when you need to forecast specific offers.

Practical Integration into the Forecast Pipeline

To keep the system coherent:

- Compute effective price and promo features at the same time granularity as the demand target.

- Ensure the baseline model is trained with consistent definitions of “normal” periods.

- Fit the response layer using the same exposure logic you will use in production.

- Log the exact features used for each forecast so you can reproduce results when a promo changes.

If you do these steps, your forecast becomes a controlled calculation rather than a black box that happens to match last month.

3.4 Calibration and Backtesting for Forecast Reliability

Forecasts are only useful if they behave like the truth when you test them. Calibration answers “are we systematically too high or too low?” Backtesting answers “does the forecast drive good decisions when the world changes?” Together they turn a demand model from a number generator into a decision tool.

Calibration Targets and Error Types

Start by defining what “reliable” means for your use case. For yield management, you usually care about booking volume by time bucket and the implied availability consumption.

Common calibration checks:

- Level calibration: predicted totals match observed totals.

- Distribution calibration: predicted uncertainty bands contain the right fraction of outcomes.

- Segment calibration: errors are not concentrated in one channel or customer group.

Use two complementary error views:

- Point accuracy: compare predicted mean demand to realized demand.

- Probabilistic accuracy: compare predicted quantiles or intervals to realized demand.

A practical rule: if your point forecasts are biased, your optimization will consistently protect too much or too little capacity.

Backtesting Design That Respects Time

Backtesting fails when it accidentally “peeks” at the future. Use a rolling-origin design.

- Choose an evaluation horizon, such as the next 14 days of bookings.

- Pick multiple cutoffs spaced through time, for example weekly.

- For each cutoff, train using only data available up to that cutoff.

- Generate forecasts for the horizon and compare to what actually happened.

This produces a set of forecast errors across time, which you can summarize with stability metrics.

Building a Backtesting Dataset

Your dataset should mirror production inputs. That means the same feature logic, the same price/promo encoding, and the same handling of missing values.

Best practices that prevent silent failures:

- Lock feature definitions: freeze transformations used during training.

- Reproduce availability logic: if inventory constraints affect observed bookings, ensure the model sees the same constraints.

- Separate training and evaluation segments: do not mix post-cutoff outcomes into feature aggregates.

Concrete example: if you compute “recent search volume” using a rolling window, ensure the window ends at the cutoff date for each backtest run.

Calibration Metrics That Actually Help

For point forecasts, use metrics that align with operational decisions.

- MAE for interpretability in units of bookings.

- Weighted MAPE when some buckets matter more, such as near departure.

- Bias as mean(predicted − actual) to detect systematic over/under forecasting.

For probabilistic forecasts, use:

- Coverage: fraction of actuals within predicted 80% or 90% intervals.

- Calibration curves: group predictions by predicted quantile levels and compare empirical frequencies.

If you only track one number, track bias plus coverage. Bias tells you which direction to correct; coverage tells you whether your uncertainty is too tight or too wide.

Correcting Miscalibration Without Breaking the Model

Calibration is not just a report card; it can be a fix.

Two common correction layers:

- Post-hoc bias correction: adjust predicted means by a learned offset per segment or per horizon bucket.

- Uncertainty scaling: widen or narrow prediction intervals using an error-based scale factor.

Example: suppose your model predicts demand too high for last-minute bookings. You can estimate a horizon-specific bias term by averaging residuals for the last 3 days before arrival, then subtract it from future predictions for that horizon.

Keep corrections simple and auditable. Overfitting calibration to a single backtest window is a classic way to get “good-looking” metrics that fail in production.

Mind Map: Calibration and Backtesting Workflow

Example: Rolling Backtest with Horizon Buckets

Assume you forecast daily bookings for the next 7 days. You run backtests with weekly cutoffs for 8 weeks.

For each cutoff:

- Predict bookings for day 1 through day 7.

- Store predicted mean and predicted 80% interval.

After collecting all runs, compute:

- Bias by day: average residual for day 1, day 2, … day 7.

- Coverage by day: fraction of actuals within the 80% interval for each day.

Interpretation example:

- If day 1 bias is +6 bookings and day 1 coverage is 90%, your model is too high and also too uncertain. Bias correction should reduce the mean; uncertainty scaling should narrow intervals.

- If bias is near zero but coverage is 60%, your mean is fine but your uncertainty is too optimistic. Increase interval width.

Example: Decision-Linked Backtesting

Forecast reliability matters because it feeds optimization. A forecast that is “accurate” by MAE can still cause poor capacity decisions.

To connect forecasts to decisions:

- For each backtest cutoff, run your booking control policy using the forecast.

- Compare realized outcomes to a baseline policy.

- Track decision quality metrics such as accepted bookings vs. lost sales, and margin impact if costs vary.

This catches cases where errors cancel out numerically but still shift the timing of protection levels.

Practical Checklist for Reliability

- Use rolling-origin backtests with fixed horizons.

- Ensure feature and availability logic match production.

- Track bias and coverage by horizon bucket.

- Apply minimal correction layers when calibration fails.

- Validate that decision-linked backtesting improves outcomes, not just forecast metrics.

When calibration and backtesting agree—errors are small, intervals contain the right outcomes, and decisions improve—you can trust the forecast enough to optimize with confidence.

3.5 Practical Example: Forecasting Demand Under Multiple Price Scenarios

A good demand forecast for dynamic pricing answers one question: “If we change the price, what happens to bookings or sales volume, and how does that ripple through inventory and time?” This example builds that capability step by step, using a small but realistic workflow.

Step 1: Define the Decision Set and the Time Grain

Pick a time grain that matches how you sell. Suppose you sell seats for a route with departures every day. You decide prices once per day for the next 14 days.

Create a price scenario table for each day t:

- Scenario A: Keep current price

- Scenario B: Reduce price by 5%

- Scenario C: Increase price by 5%

Best practice: keep scenarios small and interpretable. A 5% move is large enough to measure, but not so large that demand behavior changes in weird ways.

Step 2: Choose the Demand Target and the Modeling Form

Let y(t) be daily demand (bookings) for a given segment, say “business travelers.” You also track price p(t) and a few drivers that affect demand regardless of price: day-of-week, lead time, and a simple availability proxy.

A practical modeling form is a log-linear response:

- log(E[y(t)]) = β0 + βp log(p(t)) + βdow[dow(t)] + βL leadTime(t) + βa availability(t)

Why this works well in practice: the coefficient βp behaves like an elasticity. If βp is -1.2, then a 1% price increase reduces expected demand by about 1.2% (before accounting for other terms).

Step 3: Fit the Model on Historical Data with Consistent Features