Integrated Finance with Effective Tax Rate Safe Harbour

1. Purpose Scope and Pillar Two Context for Effective Tax Rate Safe Harbour

1.1 Overview of Pillar Two and the Role of Effective Tax Rate Safe Harbour

Pillar Two is a group-level framework designed to reduce incentives to shift profits to low-tax jurisdictions. In practice, it asks a multinational group to compare its taxes to a baseline measure of profit for each relevant jurisdiction. If the comparison shows that the group’s effective tax rate is too low, additional top-up tax may be due.

The key idea is simple: Pillar Two does not start from “what tax did we pay?” alone. It starts from “what profit measure should we consider?” and then asks whether the taxes associated with that profit are sufficient under the framework’s rules. That means finance teams need a repeatable way to translate financial statement information into Pillar Two inputs.

How Pillar Two Creates a Calculation Chain

A practical way to understand the mechanics is to view them as a chain with checkpoints:

- Identify the scope: which entities and jurisdictions are in scope, and which reporting units matter.

- Build the profit measure: a standardized profit concept derived from financial statements with specified adjustments.

- Compute covered taxes: taxes that count for Pillar Two, mapped from tax expense and other tax-related items.

- Calculate an effective tax rate: covered taxes divided by the profit measure.

- Determine whether top-up applies: compare the effective tax rate to the relevant threshold.

Each step has failure modes. For example, if profit is measured inconsistently across entities, the effective tax rate comparison becomes unreliable even when the underlying tax payments are correct.

Where Safe Harbour Fits

Effective Tax Rate Safe Harbour is a simplification mechanism. Instead of performing the full, detailed Pillar Two computation for every jurisdiction, a group can use a standardized effective tax rate approach—provided it meets eligibility conditions and documentation requirements.

Think of it as a “fast lane” that still requires proof of fitness. The safe harbour does not remove the need for accurate data; it changes the method and reduces the number of moving parts. That matters because the detailed approach often requires more granular adjustments, more reconciliations, and more interpretation.

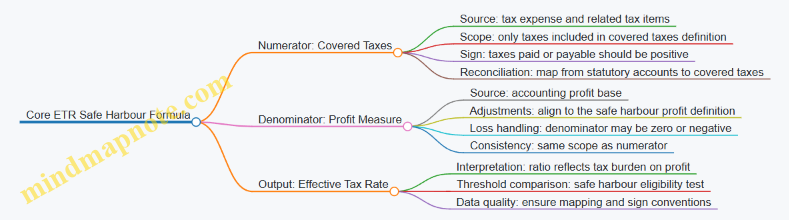

Mind Map: Pillar Two Logic and Safe Harbour Role

A Concrete Example of the Calculation Chain

Assume a jurisdiction has the following simplified inputs for the year:

- Profit measure: 100

- Covered taxes: 15

- Effective tax rate: 15 / 100 = 15%

If the relevant threshold is 15%, the jurisdiction meets the test and no top-up is expected under the effective tax rate approach. If covered taxes were 12 instead, the effective tax rate would be 12%, and the group would need to evaluate top-up tax under the framework.

Now consider why safe harbour is useful. In a detailed computation, the group might need to identify and treat multiple categories of adjustments and tax items carefully. With safe harbour, the group uses a standardized effective tax rate method, but it must still show that the inputs used are eligible and properly supported.

What Finance Teams Must Get Right

Safe harbour shifts effort rather than eliminating it. The most important work becomes:

- Mapping: ensuring the profit measure and covered taxes are derived from the same underlying financial statement logic every time.

- Consistency: using stable definitions for denominators and numerators across entities within the jurisdiction.

- Evidence: retaining reconciliations that show how tax expense and related items were transformed into covered taxes.

- Eligibility checks: confirming that the jurisdiction and reporting unit meet the safe harbour conditions before relying on it.

A small mapping error can still cause a misleading effective tax rate. For instance, if a tax item that should not be included in covered taxes is accidentally included, the effective tax rate may appear higher than it should be, leading to an incorrect conclusion.

A Simple Safe Harbour Workflow

A workable workflow for a single jurisdiction looks like this:

- Extract local trial balance and tax reporting data.

- Reconcile statutory tax expense to the components used for covered taxes.

- Compute the effective tax rate using the standardized safe harbour method.

- Run eligibility checks and document the basis.

- Produce a calculation pack with traceable links from source data to outputs.

This is the practical role of effective tax rate safe harbour: it reduces complexity in the calculation itself, while increasing the importance of disciplined data mapping, eligibility verification, and documentation quality.

1.2 Definitions That Drive Eligibility and Measurement

Effective Tax Rate Safe Harbour depends on definitions that are precise enough to be computed consistently, yet practical enough to be documented. This section sets the terms you will repeatedly use: what “covered” means, what “tax” includes, what “profit” measures, and how eligibility is checked.

Core Terms That Control Eligibility

Covered Taxes are the taxes you include in the numerator of an effective tax rate calculation. In practice, teams often start from the tax expense line items in the financial statements, then apply a filter: include taxes that are part of the group’s income tax burden for the period, and exclude items that do not represent income taxes on profits (for example, certain penalties or taxes that are not income-based). A simple rule of thumb is: if it is an income tax that would be expected to move with profit, it belongs; if it is a charge with a different economic purpose, it usually does not.

Profit Measure is the denominator used to compute the effective tax rate. It is not “revenue” and not “cash.” It is a profit concept that aligns with the Pillar Two measurement approach, typically based on accounting profit adjusted for relevant items. The key definition is that the denominator must be consistent with the numerator’s period and scope.

Relevant Period is the reporting period for which you compute the effective tax rate. Eligibility is assessed for that period, so mixing periods between numerator and denominator breaks the logic even if the numbers look reasonable.

Safe Harbour Outcome is the result of applying the eligibility test and then using the safe harbour conclusion in the Pillar Two computation workflow. The safe harbour is not a separate tax; it is a measurement shortcut that depends on the definitions above.

Measurement Definitions That Prevent “Good-Looking Wrong”

Effective Tax Rate is the ratio of Covered Taxes to the Profit Measure for the relevant period. The definition matters because sign conventions and zero-profit cases can change the interpretation. For example, if profit is negative, the effective tax rate can become misleading or undefined depending on the denominator rule used in your calculation pack.

Current Versus Deferred Components: Covered Taxes may include both current and deferred tax elements depending on the measurement definition used in your mapping. The practical implication is that you must define, in writing, which tax components are included and how they reconcile to the financial statement tax note.

Jurisdiction Scope: Eligibility is assessed at the level required by the safe harbour mechanics. Your definition must state whether you are testing per jurisdiction, per reporting unit, or another grouping. The easiest way to avoid confusion is to define the “unit of account” once and then enforce it in your data model.

Mind Map: Eligibility and Measurement Definitions

Example: Turning Financial Statement Lines Into Definitions

Assume an entity reports income tax expense of 120, made up of current tax of 140 and deferred tax credit of 20. Your definition register states that Covered Taxes include both current and deferred components that represent income taxes on profits for the period. Then Covered Taxes for the numerator are 120.

Next, your profit measure definition states that the denominator uses accounting profit before tax adjusted for specific items required by the Pillar Two measurement approach. Suppose adjusted profit is 600. The effective tax rate is 120 / 600 = 20%.

Now eligibility: if the safe harbour threshold test is based on this effective tax rate and the jurisdiction scope is “per jurisdiction for the relevant period,” you document that the test is applied to the jurisdiction totals for the same period. If your team accidentally uses profit measure from a different consolidation version or period, the effective tax rate will not match the documented reconciliation, and the safe harbour conclusion becomes hard to defend.

Example: Zero Profit and Sign Conventions

Consider a jurisdiction where adjusted profit measure is 0 because profit is fully offset by defined adjustments. If Covered Taxes are also 0, the effective tax rate is not informative, but the eligibility test still needs a defined rule. Your definition should specify how you treat this case in the calculation pack: whether you treat it as eligible by a specific rule, or whether you require additional checks. The point is not the arithmetic; it is that the definition removes ambiguity.

Definition Register Checklist

A definition register is the practical artifact that keeps teams aligned. It should state: (1) which tax lines map to Covered Taxes, (2) which profit concept forms the denominator, (3) how current and deferred components are treated, (4) the jurisdiction scope rule, and (5) the handling of zero or negative profit scenarios. When these five items are explicit, eligibility checks become repeatable rather than interpretive.

1.3 Mapping Financial Statement Concepts to Tax Computation Inputs

Mapping is the step where “what the accounts say” becomes “what the tax computation needs.” The goal is not to replicate the tax return, but to produce consistent inputs for the Effective Tax Rate Safe Harbour calculation.

Start with the Computation Inputs, Not the Accounts

Begin by listing the tax computation fields you must populate, then trace each field back to the most reliable source in the financial statements. A practical approach is to create a one-page mapping table with three columns: Computation Field, Financial Statement Source, and Mapping Rule. The mapping rule should be explicit about whether you use a balance, a movement, or a component.

Example mapping decisions:

- Covered Taxes numerator often draws from tax expense components, but may require separating current tax from deferred tax depending on the safe harbour definition used in your methodology.

- Denominator profit measure typically uses a profit figure from the financial statements, adjusted for items that are excluded or treated differently for the computation.

Translate Financial Statement Components Into Tax Components

Financial statements group items by accounting logic, while tax computations group items by tax logic. The bridge is a set of consistent translations.

-

Tax Expense Line Items

- If your income statement shows a single “Income tax expense,” split it into current tax and deferred tax using the tax note disclosures.

- If the tax note provides only net deferred tax movement, ensure you can still identify the current tax amount used for the computation.

-

Deferred Tax Balances and Movements

- Deferred tax balances explain timing differences; the computation may require only the movement that corresponds to covered taxes.

- When the tax note includes valuation allowance or recognition changes, map those to the correct tax component so you do not accidentally double count.

-

Profit Before Tax and Adjustments

- Use profit before tax as a starting point, then apply computation-specific adjustments.

- Keep adjustments tied to identifiable financial statement lines, such as impairment, equity method results, or non-recurring items.

Use a “Source of Truth” Hierarchy

Not all accounting data is equally trustworthy for tax mapping. Set a hierarchy so the team knows what to use when numbers disagree.

- Primary source: audited trial balance and tax note reconciliations.

- Secondary source: consolidation adjustments and elimination schedules.

- Tertiary source: management accounts or reclassifications, only if they are reconciled to the primary source.

A simple rule prevents chaos: if a tax note reconciliation exists, it beats a spreadsheet reclass. If both exist, the mapping rule should state which one wins and why.

Mind Map: the Mapping Logic

Worked Example: From Tax Expense to Covered Taxes

Assume the income statement shows Income tax expense = 120. The tax note provides:

- Current tax = 90

- Deferred tax movement = 30

If your safe harbour numerator uses covered taxes equal to current tax plus qualifying deferred tax, you map:

- Covered taxes = 90 + 30 = 120

If instead your approach uses only current tax, then:

- Covered taxes = 90

The key is that the mapping rule must state which definition you are using. Otherwise, two teams can both be “correct” relative to their own assumptions, and the computation will not reconcile.

Worked Example: From Profit Before Tax to Denominator

Suppose profit before tax is 500. Your computation requires excluding a non-taxable equity method gain of 40.

- Denominator profit = 500 − 40 = 460

To keep this systematic, the mapping rule should point to the exact financial statement line where the equity method gain sits, and specify whether the exclusion is gross or net of related expenses.

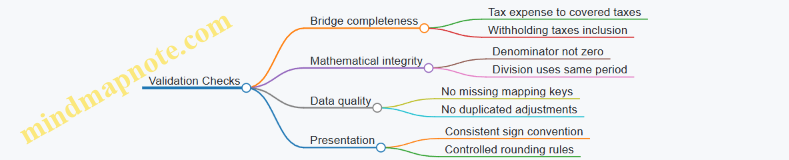

Validation Checks That Catch Mapping Errors Early

Use three checks that are hard to argue with:

- Tie-out check: mapped tax components should reconcile to the tax note totals.

- Sign check: losses and credits should follow the computation’s sign convention.

- Completeness check: every computation field has a documented source and rule.

When mapping is done this way, the safe harbour calculation becomes a controlled translation rather than a mystery tour through spreadsheets.

1.4 Boundaries Between Accounting Tax Expense and Covered Taxes

A clean boundary between accounting tax expense and Pillar Two covered taxes prevents the classic problem: the numbers look close, but the logic is different. Accounting tax expense is built for financial reporting, using accounting standards and presentation choices. Covered taxes are built for Pillar Two, using a defined set of taxes and a defined way to measure them.

What Accounting Tax Expense Is Measuring

Accounting tax expense typically includes current tax and deferred tax movements recognized in the income statement. It is influenced by items such as:

- Recognition timing of deferred tax assets and liabilities.

- Valuation allowances and recoverability assessments.

- Accounting classification and presentation choices.

Example: If a company records a deferred tax expense because a temporary difference reverses later than expected, the accounting tax expense changes even when the cash tax paid this period does not.

What Covered Taxes Are Measuring

Covered taxes focus on taxes that are relevant for Pillar Two calculations, measured using Pillar Two rules. They aim to represent the tax burden on profits in a consistent way across jurisdictions. Covered taxes are not automatically equal to the tax line in the financial statements because Pillar Two excludes or includes specific components.

Example: A jurisdiction may impose a levy that is recorded in accounting as part of operating expenses rather than income tax. Pillar Two may treat it as a covered tax if it meets the definition.

The Boundary Rule of Thumb

Use this rule of thumb to avoid mixing layers:

- Accounting tax expense is a financial reporting outcome.

- Covered taxes are a Pillar Two input.

Your job is to translate from the outcome to the input, using a mapping that is explicit, repeatable, and auditable.

Mind Map: Mapping Boundaries from Financial Statements to Covered Taxes

Systematic Boundary Workflow

- Start with the tax expense bridge: break the accounting tax expense into current and deferred components using the entity’s tax note or tax reconciliation.

- Identify the covered tax candidates: list taxes that could plausibly be covered based on jurisdictional tax types and how they are booked.

- Apply inclusion and exclusion logic: decide which components become covered taxes and which do not.

- Measure using Pillar Two measurement rules: adjust for differences in how accounting recognizes timing and classification.

- Reconcile back to the starting point: produce a schedule that explains every difference.

This workflow matters because it forces traceability. If you skip step 5, you may still compute a number, but you lose the ability to defend it.

Concrete Example: Current Tax Looks Right, Deferred Tax Does Not

Assume a company has:

- Accounting current tax expense: 120

- Accounting deferred tax expense: 30

- Total accounting tax expense: 150

In the Pillar Two covered taxes mapping, suppose only current taxes are included for the relevant measure, while deferred tax effects are excluded for the covered tax input.

Result:

- Covered taxes from this starting point: 120

- Difference explanation: 30 deferred tax excluded because it reflects accounting timing rather than the defined covered tax measure.

A common mistake is to use the full 150 because it is the “tax expense” line. That line includes deferred tax movements that are not meant to be treated as covered taxes.

Concrete Example: A Tax Expense Line Hides a Covered Tax

Assume the company records a “business tax” of 10 within operating expenses, not within income tax expense. The tax is legally linked to profits and meets the covered tax definition.

Boundary action:

- Do not rely on the accounting classification.

- Add 10 to covered taxes if it meets the definition.

Result:

- Covered taxes = mapped income tax components + 10 business tax

- Difference explanation: accounting classification differs from Pillar Two scope.

Advanced Boundary Detail: Sign Conventions and Netting

Covered taxes mapping should be consistent about signs:

- Tax expense increases are positive inputs.

- Tax credits and refunds reduce covered taxes, but only when they meet the covered tax definition.

Also watch for netting. Accounting may present net tax expense after offsets. Pillar Two schedules often need gross components so you can apply inclusion/exclusion rules correctly.

Practical Checklist for the Boundary

- Every covered tax input has a documented source line or tax note reference.

- Every excluded component has a documented reason tied to the boundary logic.

- The reconciliation schedule ties covered taxes back to accounting tax expense with no unexplained gaps.

- Sign conventions are applied consistently across entities and jurisdictions.

When boundaries are treated as a mapping problem rather than a guess, the rest of the safe harbour computation becomes much easier to trust.

1.5 Practical Workflow From Data Capture to Safe Harbour Conclusion

A practical workflow for Effective Tax Rate Safe Harbour starts with collecting the right inputs once, then transforming them through a controlled sequence of checks until the final conclusion is defensible. Think of it as a pipeline: each stage produces outputs that the next stage can trust.

Step 1: Data Capture with Clear Ownership

Begin with a data request pack that lists exactly what you need, where it lives, and who signs off. For example, for the denominator you typically need profit measures from the reporting package, while for the numerator you need covered taxes aligned to the same scope.

Concrete example: Entity A reports profit before tax of 120 in local currency. Its tax expense in the statutory accounts is 28, but the covered taxes input requires separating items that are not in scope (for instance, certain penalties or non-income taxes). Your capture sheet should therefore include both the raw tax expense and the mapping to covered taxes.

Key control: every captured number must have a source pointer (trial balance line, tax return schedule, or consolidation adjustment reference) and a date-stamped extraction.

Step 2: Data Normalization Into a Standard Working Model

Once captured, normalize the data into a working model that uses consistent sign conventions, currency handling, and entity-to-reporting-unit mapping.

Concrete example: If Entity B has a tax credit recorded as a negative tax expense, your model should convert it into the covered taxes sign convention used for the safe harbour calculation. Otherwise, the effective tax rate can look “wrong” for reasons that are purely mechanical.

Key control: run a normalization checklist that verifies currency translation method, elimination of intercompany effects where required, and consistent treatment of losses.

Step 3: Reconciliation Between Financial Statements and Safe Harbour Inputs

This is where many teams lose time. The goal is not to force every number to match perfectly; it is to explain every difference.

Concrete example: Suppose statutory tax expense is 30, covered taxes are 26, and the difference is 4. Your reconciliation should break the 4 into categories such as non-covered taxes, permanent differences, and timing-related items that are treated differently in the safe harbour computation.

Key control: require a reconciliation “bridge” that ties each covered taxes component back to a captured source line or adjustment.

Step 4: Effective Tax Rate Computation with Guardrails

Compute the effective tax rate using the standardized numerator and denominator. Add guardrails so the calculation fails loudly when inputs are inconsistent.

Concrete example: If the denominator profit measure is zero or negative, document the chosen handling rule and ensure the output is flagged for review. A safe harbour conclusion should not be produced from a silent edge case.

Key control: implement checks such as denominator not missing, covered taxes not outside expected ranges, and rate inputs consistent with the jurisdiction mapping.

Step 5: Safe Harbour Eligibility Check with Evidence Assembly

Eligibility is not just a yes/no. It is a set of conditions that must be supported by evidence.

Concrete example: If the group uses a standardized reporting approach, you still need to confirm that the entity is within the scope of the safe harbour method and that the relevant tax profile meets the stated conditions. Your evidence pack should include the eligibility checklist, the computed effective tax rate, and the reconciliation bridge.

Key control: store evidence in a structured folder aligned to the checklist items, so reviewers can trace from conclusion back to inputs.

Step 6: Conclusion Drafting with Reviewable Logic

Draft the conclusion as a short narrative tied to the computation outputs and eligibility evidence. The conclusion should state what was calculated, which method was used, and why the eligibility conditions were met.

Concrete example: “Based on the standardized working model, Entity A’s effective tax rate safe harbour computation uses covered taxes of 26 and a profit denominator of 120, resulting in an effective tax rate of 21.7%. Eligibility conditions were met as evidenced by the completed eligibility checklist and reconciliation bridge.”

Key control: include a sign-off section with reviewer comments and resolution status for any exceptions.

Mind Map: End-to-End Workflow

Example: Mini Workflow for One Entity

- Capture: Entity A trial balance tax expense 30 and tax return schedules showing non-covered items 4.

- Normalize: convert tax credit signs to covered taxes convention; translate to group currency using the agreed rate.

- Reconcile: build a bridge showing 30 → 26 covered taxes with categories that match the capture pack.

- Compute: covered taxes 26 / profit denominator 120 = 21.7% effective tax rate.

- Check eligibility: complete the eligibility checklist and attach the reconciliation bridge.

- Conclude: produce a short conclusion statement and record reviewer sign-off.

This workflow keeps the process auditable without turning it into paperwork theater. Each step produces outputs that are both usable and reviewable, so the final safe harbour conclusion is grounded in traceable logic rather than guesswork.

2. Governance Operating Model and Controls for Integrated Finance

2.1 Responsibility Matrix for Tax Reporting Data Ownership

A responsibility matrix prevents the classic problem: everyone “owns” tax data in theory, and nobody can produce evidence in practice. For Effective Tax Rate Safe Harbour, the goal is simple—each input used in the computation has a named owner, a defined control, and a clear escalation path when numbers do not reconcile.

Foundational Ownership Principles

Start with three rules that keep the model stable across cycles:

- Ownership follows the data source, not the spreadsheet. If the trial balance is produced by Group Reporting, Group Reporting owns the base numbers.

- Every computation input has one accountable owner. If two teams can change the same cell, you will eventually get two different answers.

- Controls are attached to risk, not to convenience. Higher-risk fields—like covered taxes, profit measures, and rate inputs—require stronger evidence and review.

Responsibility Matrix Structure

Use a RACI-style matrix with roles that match how your organization actually works. Typical roles include:

- Data Owner: accountable for accuracy and completeness of a dataset.

- Process Owner: accountable for the end-to-end workflow and deadlines.

- Reviewer: verifies reasonableness and reconciliation outcomes.

- Approver: signs off on the final Safe Harbour pack.

- Consulted: provides technical interpretation of tax rules.

- Informed: receives outputs and status updates.

Responsibility Matrix Example

| Data Element | Data Owner | Process Owner | Reviewer | Approver | Evidence to Retain |

|---|---|---|---|---|---|

| Local trial balance totals | Group Reporting | Tax Reporting Lead | Tax Ops Reviewer | CFO or delegate | Trial balance extract, version ID |

| Current tax expense | Tax Accounting | Tax Reporting Lead | Tax Ops Reviewer | CFO or delegate | Tax return summary, GL mapping |

| Covered taxes adjustments | Tax Accounting | Tax Reporting Lead | Tax Ops Reviewer | CFO or delegate | Adjustment log, rationale |

| Denominator profit measure | Group Reporting | Tax Reporting Lead | Tax Ops Reviewer | CFO or delegate | Reconciliation to reporting profit |

| Safe Harbour eligibility checks | Tax Technical | Tax Reporting Lead | Tax Ops Reviewer | CFO or delegate | Eligibility checklist, sign-offs |

| Tax rate inputs | Tax Technical | Tax Reporting Lead | Tax Ops Reviewer | CFO or delegate | Rate source, calculation method |

Mind Map: Ownership and Controls

Workflow That Makes the Matrix Work

A matrix is only useful when paired with a workflow. A practical sequence:

- Data freeze date: lock the trial balance and tax return extracts for the cycle. For example, use a freeze date of two months ago from your current planning cadence, then keep it consistent.

- Mapping step: Data Owners map source lines to Safe Harbour inputs using a controlled mapping table.

- Computation build: Process Owner assembles the calculation pack from mapped inputs.

- Review step: Reviewer checks reconciliations and flags anomalies (for example, covered taxes that do not track with tax expense).

- Approval step: Approver signs off only after exceptions are resolved or formally accepted.

Concrete Example: Who Fixes a Broken Reconciliation

Assume the Safe Harbour pack shows covered taxes of 12.0 million, but the reconciliation to current tax expense shows a 0.6 million gap.

- Group Reporting (Data Owner) confirms whether the profit measure denominator was translated correctly and whether any consolidation eliminations were applied.

- Tax Accounting (Data Owner) checks whether current tax expense includes a one-off adjustment that should be excluded or reclassified for covered taxes.

- Tax Ops Reviewer verifies the adjustment log and ensures the gap is explained with evidence.

- Tax Reporting Lead (Process Owner) coordinates the fix, updates the mapping table if needed, and ensures the calculation pack version is consistent.

- Approver confirms the final numbers and records the resolution in the issue register.

Advanced Details Without the Headaches

To avoid ownership drift over time, add two practical mechanisms:

- Change control for mappings: if a mapping rule changes, require a short impact note and re-run the reconciliation for affected entities.

- Evidence completeness checks: before sign-off, run a checklist that confirms each input has a retained source document and a traceable mapping.

When these are in place, the responsibility matrix becomes a working tool: it tells people what to do, what to keep, and what to do when the numbers refuse to behave.

2.2 Control Objectives for Data Quality and Auditability

Control objectives for data quality and auditability answer two practical questions: “Can we trust this number?” and “Can we prove how we got it?” In Pillar Two effective tax rate safe harbour calculations, those questions apply to both the inputs (tax expense, covered taxes, profit measures) and the transformations (mapping, reclassifications, consolidations, and safe harbour eligibility checks).

Foundational Control Objectives

Accuracy and Completeness

- Every covered tax component used in the computation must be present and correctly classified.

- Example: If current tax expense is split across two GL accounts, the control should verify that both accounts are included in the covered taxes numerator, not just the one that “looks like tax.”

Consistency Across Periods and Entities

- The same mapping rules should produce comparable results across reporting periods and reporting units.

- Example: If an entity’s tax provision was previously mapped using a specific account range, a control should flag when the account range changes without an approved mapping update.

Traceability and Reproducibility

- A reviewer should be able to start from the final safe harbour calculation and trace back to source documents, mappings, and adjustments.

- Example: For an adjustment that moves deferred tax from one line to another, the control should retain the adjustment rationale and the source amounts used.

Timeliness and Controlled Change

- Data should be captured and transformed within defined cut-offs, and changes should be logged.

- Example: If a late consolidation adjustment is posted after the data freeze, the control should require a documented impact assessment and a recalculation of the affected schedules.

Auditability Controls That Make Reviews Efficient

Auditability is not just “having documents.” It is having the right documents in the right order, with enough structure to avoid detective work.

Evidence Packaging

- Maintain a calculation pack that includes: source trial balance extracts, mapping tables, adjustment schedules, rate selections, and reconciliation bridges.

- Example: A reconciliation bridge from statutory tax expense to covered taxes should show each reconciling item with sign conventions and a short reason.

Independent Review and Challenge

- Use a two-step review: a preparer check for completeness and a reviewer check for reasonableness.

- Example: The reviewer verifies that the effective tax rate denominator is not zero or negative without an explicit documented handling approach.

Reconciliation and Control Totals

- Use control totals to catch missing lines and mis-signing.

- Example: Sum of mapped covered taxes should reconcile to the total tax expense used in the group tax reporting pack within an agreed tolerance, with exceptions listed.

Mind Map: Data Quality and Auditability Controls

Systematic Control Design from Input to Output

Step 1: Define the “Data Contract”

- Specify which fields are required, where they come from, and how they are transformed.

- Example: “Covered taxes numerator” must be sourced from a defined set of GL accounts and adjustment schedules, not from a free-text spreadsheet entry.

Step 2: Validate Mappings Before Calculations

- Controls should confirm that each required input line has a mapping and that unmapped lines are either excluded with a reason or included via an exception workflow.

- Example: If a tax credit account appears in the trial balance but has no mapping, the control should stop the pack from finalizing until resolved.

Step 3: Reconcile Transformations

- Every transformation should have a reconciliation bridge: what went in, what came out, and why.

- Example: If intercompany tax effects are reclassified, the bridge should show the original amounts and the destination lines.

Step 4: Perform Output Reasonableness Checks

- Reasonableness checks should be tied to the computation logic, not generic “does it look right?”

- Example: If the effective tax rate safe harbour result implies a covered tax amount that is materially inconsistent with the reconciled tax expense, the control should require investigation.

Example Control Objective Set for One Entity

For a single reporting unit, a practical control objective set could be:

- Completeness: All mapped current and deferred tax components are included in covered taxes.

- Correctness: Signs and classifications match the mapping rules.

- Traceability: Each mapped component traces to a GL extract and, where applicable, an adjustment schedule.

- Consistency: Mapping rules match the prior period unless an approved change exists.

- Auditability: The reconciliation bridge from statutory tax expense to covered taxes is complete and documented.

When these objectives are met, the reviewer can reproduce the calculation from the source data without guessing, and the organization can explain any difference between statutory reporting and safe harbour inputs with clear, checkable evidence.

2.3 Standard Operating Procedures for Tax Data Collection

Standard Operating Procedures (SOPs) for tax data collection exist to prevent the classic problems: missing inputs, inconsistent definitions, and “we thought someone else had that file.” This SOP section sets a repeatable path from source data to the tax computation pack used for Effective Tax Rate Safe Harbour.

Purpose and Scope

The SOP defines who collects what, from where, and how the data is checked before it enters the computation. It covers covered taxes inputs, profit or loss denominators, and the rate inputs needed to interpret the effective tax rate. It applies to group reporting cycles and local statutory reporting cycles when those results feed the safe harbour pack.

Roles and Responsibilities

Assign roles so handoffs are explicit.

- Data Owner: provides source numbers and confirms definitions match the SOP.

- Tax Data Collector: extracts, maps, and prepares the calculation-ready dataset.

- Tax Reviewer: performs reconciliation checks and signs off on completeness.

- Finance Ops Coordinator: manages deadlines, versioning, and evidence storage.

A practical rule: the person who extracts data should not be the only person who reconciles it. That separation catches both arithmetic mistakes and mapping errors.

Inputs and Definitions

Before collecting, lock definitions in a short “input dictionary.” Each input should state:

- Source (trial balance, tax return, tax provision workpaper)

- Measure (current tax, deferred tax, total tax expense)

- Sign convention (tax expense positive, tax benefit negative)

- Scope (covered taxes only, excluding items outside the safe harbour computation)

Example: If the tax provision workpaper shows “income tax expense” as a net figure, the SOP must specify whether the collector uses that net figure directly or splits it into current and deferred components for mapping.

Collection Steps from Source to Staging

Use a consistent sequence so checks happen at the right time.

- Freeze the source: capture the trial balance and tax provision versions used for the reporting cycle.

- Extract covered tax components: pull current tax, deferred tax, and any relevant adjustments per the input dictionary.

- Extract denominator measures: pull the profit or loss measure used for the effective tax rate computation.

- Capture tax rate inputs: record the relevant statutory or effective rates used for interpretation, including how multiple taxes are handled.

- Stage in a controlled workbook or database: keep raw extracts separate from mapped fields.

A good SOP makes it hard to “fix” numbers silently. If a value changes, the evidence and reason must be recorded.

Mapping Rules and Reconciliation

Mapping rules translate financial statement lines into computation inputs.

- Chart of accounts mapping: map trial balance lines to computation categories.

- Tax return mapping: map tax return lines to current tax and adjustments.

- Provision mapping: map tax provision workpaper lines to covered taxes.

Reconciliation checks should be systematic:

- Balance check: mapped totals equal the source totals (within defined tolerances).

- Bridge check: differences are explained by known adjustments (for example, non-covered items).

- Completeness check: every required input has a value or a documented “not applicable” reason.

Example: Suppose trial balance shows income tax expense of 120, but the tax return indicates current tax of 110 and deferred tax of 15. The SOP requires a bridge explaining why the net differs from the mapped covered taxes (for example, excluded items or classification differences).

Evidence Capture and Audit Trail

Evidence should be collected at the same time as the numbers.

- Store the source version identifiers (reporting period, workbook version, tax return version).

- Save mapping outputs showing the transformation from source to computation fields.

- Record review notes with dates and reviewer names.

If a date is required in the evidence log, use a stable reference such as 2026-03-15.

Quality Checks and Sign Off

Quality checks prevent late surprises.

- Consistency checks: sign conventions, currency, and entity identifiers match the input dictionary.

- Outlier checks: flag unusual ratios or zero denominators for review.

- Reperformance: reviewer recalculates key totals from staged inputs.

Sign off should be explicit: the reviewer confirms completeness, reconciliation, and correct mapping, then approves the dataset for the safe harbour computation pack.

Mind Map: Tax Data Collection SOP

Example Workflow for One Entity and One Jurisdiction

Assume Entity A in Jurisdiction X.

- The collector freezes the trial balance version used for group reporting.

- The collector extracts current tax and deferred tax from the tax provision workpaper and records sign conventions.

- The collector maps trial balance tax expense lines to covered taxes categories and stages both raw and mapped values.

- The reviewer reconciles mapped covered taxes to the tax provision totals and documents any bridge items.

- The reviewer confirms the denominator measure is present and not zero without a documented reason.

- The reviewer signs off, and the dataset is released to the safe harbour calculation pack.

This workflow keeps the “why” attached to the “what,” so the computation pack can be trusted without heroic detective work.

2.4 Evidence Requirements for Supporting Calculations

Evidence requirements are what make a calculation defensible when someone asks, “Where did that number come from?” In Effective Tax Rate Safe Harbour work, evidence must support both the inputs (data) and the logic (how the data became the calculation).

Evidence Principles That Keep Audits Calm

Start with three principles. First, traceability: every figure in the calculation should map to a source document or system extract. Second, completeness: the evidence set should cover the full scope of covered taxes and the profit measure used in the computation. Third, consistency: the same mapping rules should be applied across entities and periods, so reviewers see a repeatable method rather than a one-off effort.

A practical way to test these principles is to pick any line item in the safe harbour pack and follow it backward to its origin, then forward to its final use. If you cannot do that in one sitting, the evidence is not yet ready.

Evidence Inventory from Source to Submission

Build an evidence inventory that mirrors the calculation pack structure.

-

Source evidence for financial statement numbers

- Trial balance extracts by entity and period.

- General ledger detail for tax expense and relevant profit components.

- Consolidation adjustments that affect the profit measure.

-

Source evidence for covered taxes

- Current tax computation schedules used for statutory reporting.

- Tax return summaries showing tax paid or payable where applicable.

- Deferred tax roll-forward supporting any deferred components included in the computation.

-

Evidence for adjustments and reclassifications

- Mapping tables showing how each statutory line maps to covered tax categories.

- Reclassification worksheets explaining why an amount was included or excluded.

-

Evidence for rate inputs

- Jurisdiction tax rate documentation used for the computation.

- Selection rationale when multiple rates apply.

-

Evidence for controls and review

- Completed checklists and sign-offs.

- Review notes resolving discrepancies.

- Version history showing what changed and why.

Mind Map: Evidence Chain for Safe Harbour Calculations

How to Make Evidence Traceable Without Creating Paperwork Purgatory

Evidence should be organized so a reviewer can reperform the calculation without guessing.

- Use stable identifiers: entity code, jurisdiction code, reporting period, and a calculation pack version.

- Name files to match the pack: if the pack has “Covered Taxes Reconciliation,” the evidence should contain the same phrase so the mapping is obvious.

- Keep reconciliation totals aligned: totals in the reconciliation should tie to the underlying financial statement totals, with differences explained.

A common failure mode is having detailed evidence for each component but missing the bridge totals. Reviewers can tolerate complexity; they cannot tolerate missing bridges.

Example: Evidence for a Covered Taxes Reconciliation

Assume an entity reports tax expense of 120 in the local financial statements. The safe harbour computation requires covered taxes of 110.

Evidence set should include:

- A reconciliation worksheet showing:

- Starting point: tax expense 120.

- Adjustments: exclusions of 10 due to non-covered items.

- Ending point: covered taxes 110.

- Supporting evidence for the 10 exclusion:

- A mapping table linking the excluded statutory line to the non-covered category.

- A short reclassification note stating the reason for exclusion.

- A tie-out to the general ledger:

- The tax expense total 120 traced to the relevant GL accounts.

If the reconciliation worksheet exists but the GL tie-out does not, the evidence chain breaks at the first question.

Example: Evidence for Rate Selection When Multiple Rates Apply

Suppose two tax rates apply in the same jurisdiction due to different activities. The safe harbour pack uses a blended rate for the profit measure.

Evidence should include:

- The rate selection worksheet showing the basis for weighting (for example, profit by activity).

- The activity-level profit source from management reporting or statutory segmentation.

- A check that the weighted rate reproduces the blended rate used in the computation.

This prevents a reviewer from concluding the blended rate was chosen by convenience rather than method.

Advanced Details Reviewers Expect to See

Evidence quality improves when you include “how we know” notes for edge cases.

- Loss or near-zero profit: show the denominator logic and confirm whether any special handling was applied.

- Currency translation: include the exchange rate source and the translation method used for both profit and tax amounts.

- Intercompany effects: show whether elimination entries affect the profit measure and whether the evidence reflects the final consolidated position.

Finally, evidence should be complete for the period and scope claimed. If the pack states it covers all reporting units in a jurisdiction, the evidence inventory should show coverage for each unit, not just the ones with material amounts.

Evidence Mindset for Review Sign-Off

A sign-off is credible when it is backed by evidence coverage and a repeatable method. The goal is simple: if someone else repeats the steps using the evidence set, they should arrive at the same safe harbour computation.

2.5 Change Management for Tax Rates and Reporting Templates

Change management for tax rates and reporting templates is where “we calculated it once” turns into “we can calculate it again, consistently, and with evidence.” This section sets a practical approach that connects governance, template design, rate data, and control testing.

Start with What Changes and Why It Matters

Tax rate changes typically come from statutory updates, administrative guidance, or internal re-mapping of which rate applies to which income stream. Reporting template changes come from new schedules, revised mapping logic, or altered reconciliation steps.

A useful first step is to classify each change request into one of three types:

- Rate logic change: the rate selection rule changes (for example, different treatment for withholding taxes).

- Rate data change: the rule stays the same, but the numeric rate input changes.

- Template change: the computation structure changes (for example, new lines for covered taxes or a different denominator input).

Example: If a jurisdiction introduces a reduced corporate rate for qualifying profits, that is a rate data change if the selection rule already supports “qualifying vs non-qualifying.” If the template previously assumed one rate per jurisdiction, it becomes a template change plus a rate data change.

Define Ownership and Decision Rights

Assign clear roles before touching spreadsheets.

- Rate owner: validates statutory basis and rate effective dates.

- Template owner: ensures the reporting structure matches the computation logic.

- Finance controller: approves the change package and confirms controls are updated.

- Reporting operator: implements the change in the calculation pack.

A simple rule prevents chaos: no one role can both change logic and approve it. The operator prepares; the controller signs.

Use a Standard Change Package

Every change should be traceable through a consistent package. Include:

- Change summary: what changed and where it appears in the pack.

- Effective period: which reporting periods are impacted.

- Source evidence: statutory text or internal interpretation memo.

- Mapping impact: which entities, jurisdictions, or tax components are affected.

- Control impact: which checks must be updated or re-run.

Example: A template update that adds a new “withholding taxes included in covered taxes” line requires updating the reconciliation check that previously compared only two totals.

Manage Effective Dates and Versioning

Effective dates are where mistakes hide. Use a versioning convention that ties template and rate inputs together.

- Template version: changes to schedules, line items, or mapping logic.

- Rate version: changes to rate values or selection rules.

When both change, keep them aligned by using a single “submission-ready” bundle. If you must separate them, document the dependency explicitly.

Example: For a reporting cycle covering 2025, a rate reduction effective 2025-04-01 means the pack must support partial-year logic or a documented approximation rule. If the pack cannot support partial-year, the change request should include a decision on how to handle it, not just the new rate number.

Update Templates Without Breaking Reconciliations

Template changes should preserve the ability to reconcile old and new outputs.

A safe approach is to introduce changes in layers:

- Add new lines or schedules while keeping existing totals intact.

- Update mapping logic to populate the new lines.

- Re-run reconciliation checks to confirm totals still tie.

- Only then retire old lines in the next cycle.

Example: If you add a new schedule for “covered taxes adjustments,” keep the original “covered taxes total” line for one cycle so you can compare outputs and explain differences.

Test Controls and Evidence Before Approval

Controls should be tested at two levels.

- Data controls: rate inputs exist, are within expected ranges, and match the effective date.

- Computation controls: totals tie, sign conventions are consistent, and denominator inputs are not accidentally swapped.

Run a “before vs after” test for a small set of entities. The goal is not to prove the math is correct in theory; it is to prove the pack behaves correctly with real data.

Example: If a rate selection rule changes from “jurisdiction-level” to “entity-level,” test one entity that previously used the jurisdiction rate and one that had a different local tax profile.

Communicate Changes in a Way Operators Can Follow

Operators need instructions that map to actions.

- What to update (which cells, which tabs, which schedules).

- What to verify (which checks and expected outcomes).

- What to document (which evidence to attach).

Keep the communication short and operational. If a change requires a judgment call, specify the exact decision rule.

Mind Map: Change Management for Tax Rates and Reporting Templates

Worked Example for a Controlled Template Update

Assume a template update adds a new schedule for “covered taxes adjustments.” The change request states that the schedule must roll into the existing “covered taxes total” line.

- Before: covered taxes total equals current tax expense plus/minus a single adjustment.

- After: covered taxes total equals current tax expense plus/minus the same adjustment, but split into two components for clarity.

Testing steps:

- Select one entity in the affected jurisdiction.

- Populate the new schedule using the same underlying inputs.

- Confirm covered taxes total matches the before version within rounding.

- Update the reconciliation check to compare the new split components to the original adjustment total.

If the totals do not tie, the pack should fail the control check and require a fix before approval. That’s the point: the evidence trail should be boring, consistent, and complete.

3. Data Architecture for Standardized Reporting Across Entities

3.1 Entity Mapping from Legal Entities to Reporting Units

Entity mapping is the bridge between what the legal entities do and what Pillar Two reporting units need. If the bridge is shaky, the calculations will still run, but the numbers will be attached to the wrong people—an error that is hard to spot because it looks tidy in spreadsheets.

Foundational Concepts

A legal entity is the statutory company that files local accounts and pays local taxes. A reporting unit is the unit used for Pillar Two measurement and safe harbour computations. Mapping is the controlled process of assigning each legal entity’s relevant financial and tax inputs to the correct reporting unit.

Start with a simple rule: every legal entity must have exactly one primary reporting unit mapping for a given reporting period, unless your methodology explicitly supports split mappings with documented rationale and consistent data handling.

Inputs and Outputs

Inputs typically include:

- Legal entity master data (name, tax identifiers, jurisdiction, consolidation status)

- Local trial balance and tax expense components

- Entity-level tax attributes used for covered taxes and rate inputs

- Group consolidation structure and elimination logic

Outputs typically include:

- A mapping table from legal entity to reporting unit

- A mapping rationale log for exceptions

- A control-ready dataset that downstream templates can consume

Systematic Mapping Workflow

Step 1: Establish the Mapping Key

Use a stable key such as legal entity ID plus reporting period. Avoid relying on names alone; names change, IDs usually do not.

Step 2: Determine the Reporting Unit Basis

Define the basis your group uses for reporting units. In practice, this often aligns with how the group groups entities for Pillar Two measurement, which may be jurisdictional or based on a defined set of reporting boundaries.

Step 3: Perform the Default Mapping

Apply the default rule to most entities. For example, if your reporting unit is jurisdiction-based, map all legal entities in Germany to the Germany reporting unit.

Step 4: Handle Exceptions with Evidence

Exceptions are where mapping quality is won or lost. Examples include:

- Entities with different tax profiles than their jurisdiction peers

- Entities that are consolidated but have distinct reporting boundaries

- Entities with discontinued operations where you still need consistent period treatment

For each exception, record:

- Why the default mapping is not appropriate

- What alternative reporting unit is used

- Which data fields are affected (financials, covered taxes, or both)

Step 5: Validate Completeness and Uniqueness

Run two checks:

- Completeness: every legal entity in scope has a mapping

- Uniqueness: no legal entity maps to multiple reporting units without an approved split method

Step 6: Lock the Mapping for the Cycle

Freeze the mapping before calculation packs are finalized. If changes occur, require a controlled re-run and an audit trail of what changed and why.

Mind Map: Entity Mapping Logic

Concrete Example: Default Mapping with One Exception

Assume a group has three legal entities:

- DECo GmbH (Germany)

- DEHold GmbH (Germany)

- FRCo SARL (France)

Your reporting unit basis is jurisdiction-based, so the default mapping is:

- DECo GmbH → Germany reporting unit

- DEHold GmbH → Germany reporting unit

- FRCo SARL → France reporting unit

Now suppose DEHold GmbH has a distinct tax treatment because it is a holding entity with a different covered taxes profile and you apply a documented split method for reporting units. The exception mapping becomes:

- DEHold GmbH → Germany holding reporting unit

The mapping table must reflect this split, and the rationale log must state the basis for the split and confirm which inputs are routed to each reporting unit.

Control Checklist for Mapping Quality

- Mapping table includes all in-scope legal entities

- No duplicate mappings without approved split logic

- Jurisdiction and reporting unit labels are consistent across cycles

- Exception rationale is complete and references the affected entities

- Downstream templates reference the mapping by ID, not by name

Example: Mapping Table Structure

A practical mapping table contains:

- LegalEntityID

- LegalEntityName

- Jurisdiction

- ReportingUnitID

- ReportingUnitName

- MappingMethod (Default or Exception)

- ExceptionReasonCode (blank if Default)

- EffectiveFromPeriod

- EffectiveToPeriod (blank if current)

This structure supports both calculation and audit. When someone asks, “Why did this entity land in that reporting unit?”, the answer is already in the table instead of living in someone’s memory.

3.2 Chart of Accounts Alignment With Tax Data Needs

A chart of accounts (CoA) is the bridge between accounting results and tax computations. If the CoA is aligned to tax data needs, you can produce consistent inputs for Effective Tax Rate Safe Harbour without heroic spreadsheet surgery. The goal is not to redesign accounting, but to ensure that the accounts you already post to can be reliably mapped to the “covered taxes” and the profit denominator used in Pillar Two calculations.

Foundational Principle: Map Once, Reuse Often

Start by defining what the tax computation needs at the level of granularity you can support from the CoA. For Safe Harbour, you typically need covered taxes by jurisdiction and a profit measure that corresponds to the computation base. Then you create a mapping layer that links CoA accounts to tax input categories. Once the mapping is stable, every reporting cycle becomes a controlled extraction rather than a fresh interpretation.

Step 1: Identify Tax Input Categories

Create a short list of tax input categories that your computation requires, such as:

- Current tax expense

- Deferred tax movements that affect the covered tax view (if applicable to your approach)

- Withholding taxes and other taxes that qualify as covered taxes

- Tax credits or reliefs that reduce taxes (captured consistently)

- Profit denominator components (the profit measure you use for the effective tax rate)

Example: If your CoA has “Income tax expense” and “Deferred tax expense,” you can map them to current and deferred categories. If you also have “Withholding tax on dividends,” map that to the withholding category.

Step 2: Classify CoA Accounts by Tax Role

For each CoA account, assign a tax role:

- Direct tax input account: already represents a tax line you need

- Tax adjustment account: represents an item that must be reclassified into a tax input category

- Profit denominator account: represents profit components used in the base

- Non-relevant account: does not feed the computation

Example: “Legal and professional fees” is non-relevant for covered taxes, even though it may affect profit. “Tax penalties” might be non-covered or excluded; you decide the role based on your covered tax definition and document it.

Step 3: Define Mapping Rules and Sign Conventions

Mapping is where errors breed. Document rules for:

- Sign conventions (expenses as positive or negative)

- Treatment of reversals and credit notes

- Whether the mapping is based on account only or account plus transaction attributes

Example: If your system posts tax refunds as negative “Income tax expense,” your mapping rule must still place them in the correct covered tax category. Otherwise, the effective tax rate denominator might look fine while the numerator flips.

Step 4: Use Dimensions to Avoid CoA Explosion

Instead of creating dozens of new CoA lines for every tax nuance, use dimensions such as jurisdiction, tax type, and entity. Keep CoA stable and let dimensions carry the tax specificity.

Example: “Income tax expense” stays one account. Jurisdiction is captured via a dimension. Withholding taxes can be separated by a “tax type” dimension rather than by creating separate CoA accounts for each withholding category.

Step 5: Validate with Reconciliations

Validation should be systematic:

- Reconcile mapped tax inputs back to the tax-related ledger totals

- Reconcile profit denominator mapped accounts back to the profit measure used in the computation

- Check that excluded accounts do not leak into the numerator

Example: If the ledger shows total “Income tax expense” of 10,000, but your mapped covered taxes sum to 9,200, you need a documented reason for the 800 difference (e.g., excluded penalties or non-covered taxes).

Mind Map: CoA Alignment Workflow

Example: Practical Mapping Table

| CoA Account | Typical Description | Tax Role | Mapping Category | Notes |

|---|---|---|---|---|

| 4000 | Income tax expense | Direct tax input | Current tax | Use jurisdiction dimension |

| 4100 | Deferred tax expense | Tax adjustment | Deferred component | Include only if your covered tax definition requires it |

| 4200 | Withholding tax on dividends | Direct tax input | Withholding taxes | Map refunds using same category |

| 4300 | Tax penalties | Tax adjustment | Excluded from covered taxes | Document exclusion rule |

| 8000 | Revenue | Profit denominator | Profit base | Included via profit measure mapping |

| 8100 | Operating expenses | Profit denominator | Profit base | Included net of exclusions |

Step 6: Handle Edge Cases Without Breaking the Model

Edge cases usually come from mixed postings:

- A single account used for both covered and non-covered taxes

- Tax items posted through journals that bypass standard dimensions

- Intercompany tax settlements posted to non-tax accounts

Example: If “Other taxes” includes both covered and non-covered items, split by a “tax type” dimension and enforce it in journal templates. If you cannot enforce it, create a temporary mapping override with documented criteria and a reconciliation check.

When the CoA alignment is done this way, the tax computation becomes a repeatable extraction plus a small set of documented adjustments. That’s the difference between “we can calculate it” and “we can calculate it consistently under review.”

3.3 Data Dictionaries for Covered Taxes and Relevant Adjustments

A data dictionary is the group’s single source of truth for what “covered taxes” means in your calculations, how each number is sourced, and how adjustments are classified. Without it, teams end up with spreadsheets that look consistent but quietly disagree on definitions. The goal here is practical: make every field in your safe harbour pack traceable to a financial system object and a documented rule.

Start with the Covered Taxes Vocabulary

Begin by listing the tax concepts you will actually compute. For each concept, define three things: (1) the accounting source, (2) the computation role, and (3) the sign convention.

Example vocabulary entries:

- Current tax expense: sourced from the income tax note or tax provision ledger; used as a base component; typically positive when expense increases profit.

- Deferred tax movements: sourced from deferred tax rollforward; used only if your covered taxes definition includes it; sign must match the computation template.

- Withholding taxes: sourced from tax withholding ledgers; used depending on whether they are treated as covered taxes in your mapping.

A good dictionary also states what is not included. If a tax is excluded, record the reason category (for example, “not a covered tax type” or “excluded due to jurisdiction mapping”).

Define Fields as “Business Meaning + System Path”

For each dictionary field, include:

- Field name: the label used in the calculation pack.

- Definition: one sentence describing the business meaning.

- Source system and object: where the number comes from (trial balance account, tax ledger, subledger journal type).

- Transformation rule: how raw data becomes the field value (currency conversion, aggregation level, sign flip).

- Validation checks: what must be true for the value to be accepted.

- Owner and evidence: who confirms it and what document proves it.

This structure prevents the classic problem where two teams both say “tax expense” but one uses the tax provision and the other uses the tax payable movement.

Classify Relevant Adjustments with Rule Types

Adjustments should not be a pile of one-off exceptions. Classify them into rule types so the pack can be reviewed consistently.

Common rule types:

- Reclassification: move amounts between categories without changing the underlying economic amount.

- Inclusion/Exclusion: remove or add specific components based on covered tax rules.

- Timing alignment: map items to the correct reporting period when systems post differently.

- Aggregation standardization: combine multiple accounts into a single dictionary field.

Example adjustment rule:

- Rule type: Reclassification

- Dictionary field affected: “Current tax expense included in covered taxes”

- Trigger: tax provision ledger includes a component booked to a non-covered account

- Action: re-map that component to the covered category using a mapping table.

Mind Map for Dictionary Design

Example Dictionary Entries That Work in Practice

Example: “Covered Taxes Current”

- Definition: the portion of current tax expense included in the covered taxes numerator.

- Source: income tax provision ledger account group “Current Tax”.

- Transformation: sum by reporting unit and period; convert to reporting currency using the group average rate used in the safe harbour pack; apply sign convention so expense is positive.

- Validation: value must reconcile to the tax expense line within a tolerance; if not, require a mapping break explanation.

- Evidence: tax provision trial balance extract and the mapping table version used.

Example: “Excluded Taxes Category”

- Definition: amounts that are tax-like but not included in covered taxes.

- Source: tax ledger account group “Non-covered levies”.

- Transformation: carry forward as excluded; no sign flip.

- Validation: excluded total must equal the sum of excluded account balances; if a new account appears, block submission until it is classified.

Validation Logic That Prevents Silent Errors

A dictionary is only as good as its checks. Build validations around three failure modes:

- Mapping gaps: an account exists in the ledger but has no dictionary field mapping.

- Sign mismatches: a credit/debit convention flips the numerator or denominator.

- Reconciliation drift: totals no longer tie to the tax note or provision ledger.

Use dictionary-driven checks inside your pack so reviewers see issues as soon as data is loaded, not after calculations are finalized.

Versioning and Change Records

Store a dictionary version with each safe harbour calculation cycle. Record what changed, why it changed, and which entities it affects. A simple change log entry should include the affected field names and the mapping table version. This keeps reviews grounded: when numbers move, you can point to the rule change rather than guessing.

A dictionary that is consistent, testable, and versioned turns tax data from “spreadsheet content” into “controlled inputs,” which is exactly what integrated finance needs.

3.4 Handling Currency Translation and Consolidation Effects

Currency translation is where “same numbers, different stories” tends to happen. For Effective Tax Rate Safe Harbour inputs, the goal is not to mirror consolidation accounting perfectly; it is to produce consistent, traceable covered-tax and profit measures in the reporting currency used for Pillar Two calculations.

Foundational Principles for Safe Harbour Currency Consistency

Start with two rules.

-

Choose the measurement currency early. Decide whether the Safe Harbour computation is performed in the group reporting currency (common) or in local currency per jurisdiction and then translated. Either approach can work, but mixing approaches across entities creates avoidable reconciliation noise.

-

Translate components using the same logic every time. Covered taxes and the profit denominator must follow a consistent translation method across the group. If you translate taxes at one rate and profit at another without a documented rationale, your effective tax rate can shift even when underlying economics did not.

A practical baseline is:

- Profit denominator: translate using the average rate for the period.

- Covered taxes: translate using the rate applicable to the tax amount recognition basis (often the average rate for the period for simplicity, or a weighted approach if your tax amounts are materially time-phased).

Consolidation Effects That Change the Inputs

Consolidation can affect both numerator and denominator through eliminations and reclassifications.

Intercompany Transactions

Intercompany interest, royalties, and service charges can move profit between entities. If the Safe Harbour inputs are built from local financial statements before eliminations, the denominator may reflect local profit allocation rather than group profit.

Best practice is to align the Safe Harbour inputs with the consolidation stage you use for Pillar Two:

- If Pillar Two is computed on consolidated covered taxes and consolidated profit, then build inputs from the consolidation ledger after intercompany eliminations.

- If Pillar Two is computed per jurisdiction, then keep local profit and local covered taxes, but still apply jurisdiction-level eliminations consistently.

Foreign Exchange Differences

FX differences can appear in profit but may not correspond to tax effects in a clean way. For Safe Harbour, treat FX differences as part of the profit denominator if they are included in the consolidated profit measure you are using. The key is to ensure the tax numerator corresponds to the same profit basis.

Deferred Tax and Translation

Deferred tax balances are often translated using closing rates, but Safe Harbour focuses on covered taxes for the period. Avoid translating deferred tax movements directly into covered taxes unless your mapping explicitly supports it. Instead, map covered taxes from the period tax expense/current tax components that your reporting framework defines.

Systematic Workflow for Translation and Consolidation

- Lock the rate set for the reporting period (average and closing rates, plus any weighted rates used for tax timing).

- Translate local trial balance to the computation currency using the chosen method.

- Apply consolidation adjustments that affect profit and taxes (intercompany eliminations, reclassifications).

- Reconcile to consolidation totals using control checks: numerator totals, denominator totals, and sign conventions.

- Document the mapping from local line items to covered taxes and profit denominator, including the translation method used for each component.

Mind Map: Currency Translation and Consolidation Effects

Example: Two Entities, One Reporting Currency

Assume the group reporting currency is EUR.

-

Entity A (functional currency EUR):

- Profit denominator (local): 10,000 EUR

- Covered taxes (local): 2,000 EUR

-

Entity B (functional currency USD):

- Profit denominator (local): 12,000 USD

- Covered taxes (local): 3,000 USD

- Average rate for the period: 0.90 EUR per USD

Translation using the baseline method:

- Entity B profit denominator: 12,000 × 0.90 = 10,800 EUR

- Entity B covered taxes: 3,000 × 0.90 = 2,700 EUR

Group totals before intercompany eliminations:

- Denominator: 10,000 + 10,800 = 20,800 EUR

- Numerator: 2,000 + 2,700 = 4,700 EUR

- Effective tax rate: 4,700 / 20,800 = 22.60%

Now suppose there is an intercompany service fee from A to B that increases B profit by 500 USD and reduces A profit by the equivalent amount, with no direct tax effect in the mapping used for covered taxes. After consolidation eliminations, the denominator changes, but the covered taxes remain the same. Your effective tax rate moves because the denominator moved—this is correct as long as both numerator and denominator come from the same consolidation stage.

Control Checks That Prevent Silent Errors

- Rate consistency check: confirm the same average rate set is used for all profit denominator translations in the period.

- Component alignment check: verify that covered taxes are translated using the same rate logic as defined in your mapping.

- Sign and rounding check: ensure negative profits and tax credits follow the same sign convention across currencies.

- Reconciliation check: tie translated totals back to the consolidation pack totals within an agreed tolerance.

A good rule of thumb: if a change in exchange rates alone moves the effective tax rate, you should be able to point to exactly which component was translated and which rate method was applied.

3.5 Building a Reusable Data Model for Safe Harbour Computations

A reusable data model turns Safe Harbour calculations from a one-off spreadsheet exercise into a repeatable pipeline. The goal is simple: the same definitions, mappings, and checks should work across entities, jurisdictions, and reporting cycles, with minimal manual rework.

Foundational Design Principles

Start with stable “source-of-truth” tables. For Safe Harbour, the model needs (1) financial statement amounts, (2) tax amounts that qualify as covered taxes, (3) profit measures used as denominators, and (4) tax rate inputs where required. If you treat these as separate layers, you can change mappings without rewriting calculations.

Next, define canonical keys. Use consistent identifiers for entity, reporting unit, jurisdiction, and period. A common mistake is to let the same entity appear under different names across systems; the model should normalize names into keys once, then reuse them everywhere.

Finally, design for traceability. Every computed output should be explainable back to input lines and adjustment rules. That means storing not only final numbers, but also the rule used to produce them.

Data Model Layers

Layer 1: Raw Inputs

- Trial balance or statutory tax return extracts by entity and period.

- Consolidation adjustments that affect profit measures.

- Tax expense components and current/deferred splits where available.

Layer 2: Standardized Measures

- Covered taxes measure, built from eligible tax components.

- Profit measure used for the effective tax rate denominator.

- Optional components for reconciliation, such as “tax expense per accounts” and “covered taxes per model.”

Layer 3: Safe Harbour Calculation Outputs

- Effective tax rate computation.

- Eligibility flags and documentation completeness indicators.

- Output schedules that can be exported into a calculation pack.

Layer 4: Controls and Evidence

- Mapping confidence checks (for example, missing jurisdiction tags).

- Reconciliation tolerances.

- Evidence pointers to supporting schedules.

Canonical Definitions and Mapping Rules

Define covered taxes once, then reuse. For example, if your group includes current corporate income tax and excludes certain penalties, represent that as a rule: “Covered taxes = current tax + qualifying taxes − excluded items.”

Example: Suppose Entity A reports tax expense of 120, made of current tax 110 and deferred tax 10. If your Safe Harbour covered taxes definition includes only current tax, then covered taxes becomes 110, not 120. The model should store both numbers so the reconciliation is automatic rather than reconstructed later.

For the denominator, decide whether you use profit before tax, profit after tax, or another profit measure consistent with your Safe Harbour approach. The model should treat the denominator as a standardized measure, not a direct copy from one report.

Example: If consolidation introduces an intercompany elimination that reduces profit before tax by 5, the standardized profit measure should reflect the consolidated view used for Safe Harbour. Keep the local profit and the consolidation-adjusted profit as separate standardized measures so you can explain differences.

Reusability Through Parameterization

Parameterize by jurisdiction and reporting unit. The same calculation logic can run for multiple jurisdictions if you store jurisdiction-specific items as parameters: tax rate selection rules, included tax types, and exclusions.

Example: Jurisdiction B has both corporate income tax and a payroll-related levy that is excluded from covered taxes. Instead of hardcoding exclusions in formulas, store “levy excluded” as a parameter tied to tax type codes.

Mind Map: Data Model Components

Worked Example: Minimal End-to-End Flow

Assume a reporting period of 2026-03-31 and Entity A in Jurisdiction X.

- Raw inputs load trial balance lines for profit before tax and tax expense components.

- Mapping rules convert tax expense lines into tax type codes.

- Covered taxes rule selects only current tax lines, excluding penalties.

- Denominator rule selects the consolidated profit measure for the reporting unit.

- Effective tax rate is computed as covered taxes divided by the denominator.

- Controls verify that covered taxes reconcile to tax expense per accounts within tolerance and that jurisdiction tags are present.

If the denominator is zero, the model should still produce an output record with a clear status (for example, “denominator zero”) rather than leaving blanks. That keeps downstream reporting consistent.