Monte Carlo Forecasting for Corporate Financial Planning and Analysis

Chapter 1: Introduction to Monte Carlo Simulation in FP&A

1.1 Understanding Monte Carlo Simulation: Concepts and Terminology

Monte Carlo simulation is a method for understanding the impact of uncertainty in mathematical models. It uses random sampling to generate a range of possible outcomes, rather than a single fixed result. This approach helps financial planners and analysts see not just what might happen, but how likely different results are.

At its core, Monte Carlo simulation involves three key components:

- Inputs: Variables with uncertain values, often represented by probability distributions.

- Model: A formula or set of calculations that link inputs to outputs.

- Outputs: The results generated by running the model many times with different input values.

Key Terms

- Random Variable: A variable whose value is subject to randomness. For example, sales volume next quarter.

- Probability Distribution: A function that describes the likelihood of different values for a random variable. Common types include normal, uniform, and triangular distributions.

- Iteration: One complete run of the simulation, using a set of randomly sampled inputs.

- Simulation Run: The total number of iterations executed to build a distribution of outcomes.

- Outcome Distribution: The collection of results from all iterations, showing the range and likelihood of possible outcomes.

Mind Map: Core Concepts of Monte Carlo Simulation

How It Works: Step-by-Step

- Define uncertain inputs: For example, forecasted sales growth might be uncertain and modeled as a normal distribution with a mean of 5% and a standard deviation of 2%.

- Build the model: Use these inputs in your financial formula, such as projecting revenue by multiplying last year’s revenue by (1 + sales growth).

- Run iterations: Randomly sample values for sales growth according to its distribution and calculate revenue. Repeat this hundreds or thousands of times.

- Analyze outputs: Collect all revenue results to see the range of possible revenues and their probabilities.

Example: Forecasting Quarterly Revenue

Imagine you want to forecast revenue for the next quarter. You know last quarter’s revenue was $1 million. Sales growth is uncertain but expected to be around 5%, with some variability.

- Model sales growth as a normal distribution: mean = 5%, standard deviation = 2%.

- For each iteration, randomly pick a sales growth value from this distribution.

- Calculate revenue = $1,000,000 * (1 + sales growth).

- Repeat 1,000 times.

After running the simulation, you get a distribution of possible revenues. You might find that:

- 80% of outcomes fall between $1.03 million and $1.07 million.

- There’s a 5% chance revenue is below $1 million.

- The average simulated revenue is $1.05 million.

This information gives a clearer picture of risk and opportunity than a single point estimate.

Mind Map: Example Workflow for Revenue Forecasting

Why Use Monte Carlo Simulation?

Traditional forecasting often relies on single-point estimates, which can hide the range of possible outcomes and their likelihoods. Monte Carlo simulation exposes this uncertainty, allowing decision-makers to:

- Understand the probability of hitting targets.

- Identify risks and opportunities.

- Make informed decisions based on a spectrum of possible futures.

In financial planning, this means budgets and forecasts can better reflect real-world variability.

Summary

Monte Carlo simulation is a structured way to incorporate uncertainty into financial models. By defining inputs as probability distributions, running many iterations, and analyzing the resulting output distribution, FP&A professionals gain insight into the range and likelihood of financial outcomes. This approach supports more nuanced risk assessment and planning.

1.2 The Role of Probabilistic Forecasting in Corporate Financial Planning

Probabilistic forecasting introduces a way to represent uncertainty explicitly in financial planning. Unlike traditional point forecasts that provide a single expected value, probabilistic forecasts present a range of possible outcomes along with their likelihoods. This approach helps FP&A professionals understand not just what might happen, but how likely different scenarios are.

Why Probabilistic Forecasting Matters

Financial planning always involves uncertainty. Market conditions, customer behavior, supply chain disruptions, and regulatory changes all influence outcomes. Traditional forecasts often mask this uncertainty by focusing on a single “best guess.” This can lead to overconfidence and insufficient preparation for less likely but impactful events.

Probabilistic forecasting acknowledges uncertainty by modeling it directly. Instead of saying “Revenue will be $100 million,” a probabilistic forecast might say “Revenue has a 70% chance of falling between $95 million and $105 million, with a 10% chance it could be below $90 million.”

This richer information supports better decision-making, risk management, and communication with stakeholders.

Mind Map: Key Aspects of Probabilistic Forecasting in FP&A

Practical Example: Sales Forecasting with Probabilistic Approach

Imagine a company forecasting quarterly sales. A traditional forecast might predict $50 million in sales. However, sales depend on factors like customer demand, competitor actions, and economic conditions, all uncertain.

Using probabilistic forecasting, the FP&A team models these uncertainties as input variables with probability distributions. For example:

- Customer demand: Normally distributed with mean 100,000 units and standard deviation 10,000 units.

- Price per unit: Uniform distribution between $480 and $520.

Running simulations generates a distribution of possible sales outcomes rather than a single number. The team might find:

- 80% chance sales exceed $48 million.

- 10% chance sales fall below $45 million.

This insight helps management prepare contingency plans for lower sales scenarios and allocate marketing resources more effectively.

Mind Map: Differences Between Deterministic and Probabilistic Forecasting

How Probabilistic Forecasting Fits into Corporate Financial Planning

-

Budgeting: Probabilistic forecasts provide ranges for revenue, expenses, and cash flows, enabling flexible budgets that account for uncertainty.

-

Capital Allocation: Understanding the probability of different returns helps prioritize investments and manage risk.

-

Risk Management: Identifying the likelihood of adverse outcomes supports risk mitigation strategies.

-

Performance Monitoring: Comparing actual results against probabilistic forecasts highlights whether outcomes fall within expected ranges.

-

Communication: Presenting forecasts as distributions encourages realistic expectations among executives and investors.

Example: Cash Flow Forecasting with Probabilistic Inputs

A company forecasts monthly cash flow to ensure liquidity. Instead of assuming fixed payment timings and amounts, the FP&A team models:

- Customer payment delays as a probability distribution.

- Variability in supplier payment terms.

- Fluctuations in operating expenses.

Simulations reveal the probability of cash shortfalls in each month. This allows the treasury team to plan credit lines or delay discretionary spending proactively.

In summary, probabilistic forecasting shifts financial planning from a single-point estimate to a spectrum of possibilities. This approach equips FP&A teams to better understand risks, communicate uncertainty, and make decisions grounded in a fuller picture of potential outcomes.

1.3 Key Benefits of Monte Carlo Methods for FP&A Teams

Monte Carlo methods offer several clear advantages for FP&A teams aiming to improve financial forecasting and risk analysis. At their core, these methods provide a structured way to incorporate uncertainty into financial models, moving beyond single-point estimates to a range of possible outcomes. This shift helps teams understand not just what might happen, but how likely different scenarios are.

Key Benefits of Monte Carlo Methods for FP&A Teams

Quantifying Uncertainty

Monte Carlo simulation transforms uncertain inputs—like sales growth rates, cost fluctuations, or interest rates—into probability distributions. Instead of guessing a single number, the model runs thousands of simulations, each time sampling from these distributions. This process produces a spectrum of possible results, allowing FP&A professionals to see the likelihood of various financial outcomes.

Quantifying Uncertainty Mind Map

Example: Suppose a company estimates annual revenue growth at 5%, but actual growth can vary between 2% and 8%. Monte Carlo simulation models this range, showing the probability that revenue will fall below or exceed certain thresholds.

Improving Risk Assessment

Monte Carlo methods help identify the probability and impact of adverse financial events. This probabilistic approach allows FP&A teams to measure risks quantitatively, such as the chance of cash flow shortfalls or budget overruns. It also supports stress testing by simulating extreme but plausible scenarios.

Risk Assessment Mind Map

Example: An FP&A team can simulate the impact of a sudden 10% increase in raw material costs on operating margins, estimating the probability that margins fall below a critical level.

Enhancing Decision-Making with Probabilistic Insights

By providing a range of outcomes with associated probabilities, Monte Carlo simulation equips decision-makers with a clearer picture of risks and opportunities. This helps prioritize initiatives, allocate resources more effectively, and set realistic targets.

Decision-Making Mind Map

Example: When evaluating two investment projects, Monte Carlo simulation can reveal which project has a higher probability of meeting financial goals, rather than relying on average expected returns alone.

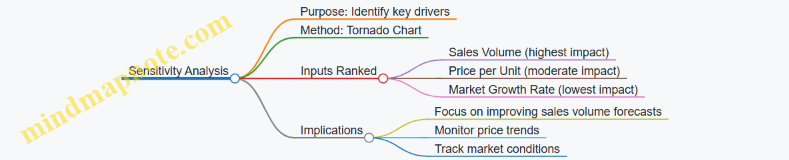

Supporting Sensitivity Analysis

Monte Carlo simulation naturally integrates sensitivity analysis by showing how changes in input assumptions affect output variability. This helps FP&A teams identify which variables drive the most uncertainty and deserve closer attention.

Sensitivity Analysis Mind Map

Example: A simulation may reveal that profit forecasts are highly sensitive to customer churn rates, prompting the team to focus on improving customer retention strategies.

Facilitating Communication and Transparency

Presenting financial forecasts as probability distributions rather than single numbers encourages more nuanced discussions with stakeholders. Monte Carlo outputs can be visualized with histograms, cumulative distribution functions, or tornado charts, making complex uncertainty easier to grasp.

Communication Mind Map

Example: Instead of stating “expected profit is $10 million,” the FP&A team can show there is a 70% chance profit will be between $8 million and $12 million, helping executives understand risk levels.

Flexibility Across Financial Planning Areas

Monte Carlo methods are adaptable to various FP&A tasks, including budgeting, forecasting, capital planning, and risk management. This versatility makes them a valuable tool for comprehensive financial analysis.

Application Areas Mind Map

Example: An FP&A team can use Monte Carlo simulation to forecast cash flows, analyze capital expenditure risks, and evaluate the impact of different economic scenarios on overall financial health.

In summary, Monte Carlo methods provide FP&A teams with a practical way to incorporate uncertainty into financial models, quantify risks, and communicate findings clearly. These benefits help organizations make better-informed decisions grounded in a realistic understanding of potential outcomes.

1.4 Overview of Financial Planning and Analysis Processes

Financial Planning and Analysis (FP&A) is the backbone of corporate decision-making, providing the data-driven insights that guide budgeting, forecasting, and strategic planning. At its core, FP&A involves collecting financial data, analyzing it, and using the results to support management in making informed business decisions. The process is cyclical and iterative, often involving multiple departments and stakeholders.

Core FP&A Processes

FP&A can be broken down into several key processes, each with distinct goals and activities:

- Budgeting: Setting financial targets and allocating resources for a specific period, usually annually.

- Forecasting: Updating financial expectations based on actual performance and changing conditions.

- Variance Analysis: Comparing actual results against budgets or forecasts to understand deviations.

- Financial Reporting: Preparing reports that summarize financial performance for internal and external audiences.

- Scenario and Sensitivity Analysis: Exploring how changes in assumptions impact financial outcomes.

- Strategic Planning Support: Providing financial insights to support long-term business strategies.

Mind Map: FP&A Core Processes

Budgeting

Budgeting is the process of translating strategic goals into quantifiable financial targets. It typically involves departments submitting planned expenses and revenue estimates, which are then consolidated into a company-wide budget. The budget acts as a financial roadmap for the upcoming period.

Example: A manufacturing company sets a budget for raw material costs based on expected production volumes and negotiated supplier prices. If the budget allocates $2 million for materials, this figure guides purchasing decisions and cost controls.

Forecasting

Forecasting updates the budget based on actual performance and new information. Unlike the fixed nature of budgets, forecasts are dynamic and often revised monthly or quarterly.

Example: Midway through the fiscal year, the same manufacturer notices a 10% increase in raw material prices. The FP&A team revises the forecast to reflect higher costs, adjusting profit expectations accordingly.

Variance Analysis

Variance analysis identifies differences between actual results and budgets or forecasts. It helps pinpoint where performance deviated and why.

Example: If the manufacturer spent $2.2 million on materials instead of the budgeted $2 million, variance analysis investigates whether higher prices, increased usage, or inefficiencies caused the overrun.

Financial Reporting

FP&A prepares reports that summarize financial results for management, investors, and regulatory bodies. These reports must be accurate, timely, and tailored to the audience.

Example: A monthly management report might include revenue, expenses, and profitability by product line, highlighting areas needing attention.

Scenario and Sensitivity Analysis

These analyses test how changes in key assumptions affect financial outcomes. Scenario analysis looks at distinct possible futures, while sensitivity analysis examines the impact of varying one factor at a time.

Example: The FP&A team models the impact on net income if sales volumes drop by 15% or if raw material prices rise by 20%, helping management prepare contingency plans.

Strategic Planning Support

FP&A supports long-term planning by building financial models that incorporate capital expenditures, financing options, and market conditions.

Example: Before launching a new product line, FP&A models the expected cash flows, break-even point, and return on investment to advise the executive team.

Mind Map: FP&A Workflow Example

Example: Monthly FP&A Cycle

- Data Collection: Gather actual financial results and operational metrics.

- Data Validation: Check for anomalies or errors.

- Forecast Update: Adjust forecasts based on new data.

- Variance Analysis: Identify and explain deviations.

- Reporting: Prepare management reports.

- Review Meeting: Discuss results and implications.

- Action Planning: Adjust plans or strategies as needed.

This cycle repeats monthly, ensuring the company stays aligned with financial goals and can respond quickly to changes.

In summary, FP&A processes form a structured approach to managing a company’s financial health. Each step builds on the previous one, creating a feedback loop that supports better decision-making. Monte Carlo simulation fits into this framework by enhancing forecasting and risk analysis, which will be explored in later chapters.

1.5 Common Challenges in Traditional Financial Forecasting

Traditional financial forecasting often relies on deterministic models that produce a single-point estimate, which can mask the inherent uncertainty in financial variables. This approach faces several common challenges that can limit the accuracy and usefulness of forecasts.

Challenge 1: Overreliance on Single-Point Estimates

Forecasts typically provide one expected value, such as a revenue figure or expense total, without indicating the range of possible outcomes. This can lead to overconfidence in the forecast and insufficient preparation for variability.

Example: A company forecasts $10 million in sales for the next quarter but does not account for the possibility that sales could be $8 million or $12 million. Decision-makers may treat the $10 million as a guaranteed figure, leading to tight budgets or missed opportunities.

Challenge 2: Ignoring Uncertainty and Variability

Financial inputs such as market demand, costs, and interest rates fluctuate. Traditional models often treat these inputs as fixed or use simple adjustments, failing to capture their probabilistic nature.

Example: A forecast assumes a fixed raw material cost of $50 per unit, ignoring historical price swings. If prices spike unexpectedly, the forecasted profit margins will be misleading.

Challenge 3: Inadequate Handling of Correlations

Variables in financial models are often interdependent. For example, sales volume and price discounts might be correlated. Traditional forecasting methods may overlook these relationships or treat variables independently.

Example: A forecast assumes sales volume increases independently of discount rates. In reality, higher discounts drive volume, so ignoring this correlation can distort revenue projections.

Challenge 4: Static Assumptions and Lack of Flexibility

Traditional forecasts often rely on fixed assumptions that are not updated dynamically as new information arrives. This rigidity can cause forecasts to become outdated quickly.

Example: A budget assumes a 3% inflation rate for the year, but mid-year inflation rises to 6%. The forecast does not adjust, leading to underestimated costs.

Challenge 5: Limited Scenario Analysis and Stress Testing

While some traditional models include scenario analysis, these are often limited to a few discrete cases rather than a continuous range of possibilities. This restricts understanding of risk exposure.

Example: A forecast includes a “best case” and “worst case” scenario but does not quantify the likelihood of each. Decision-makers cannot gauge how probable extreme outcomes are.

Challenge 6: Data Quality and Input Bias

Traditional forecasting depends heavily on historical data, which may be incomplete, outdated, or biased. Without mechanisms to account for data uncertainty, forecasts inherit these flaws.

Example: Sales data from a period affected by an unusual event (e.g., supply chain disruption) is used unadjusted, skewing forecasts.

Challenge 7: Difficulty Communicating Uncertainty

Traditional forecasts often present a single number without context, making it hard for stakeholders to understand the risks and variability involved.

Example: A CFO receives a revenue forecast of $100 million but no indication of the confidence level or potential downside, leading to overly optimistic planning.

Summary Mind Map

Addressing these challenges requires moving beyond deterministic forecasts to approaches that explicitly model uncertainty and variability, such as Monte Carlo simulation. This shift helps FP&A teams produce more informative forecasts that better support decision-making under uncertainty.

1.6 Integrating Monte Carlo Simulation into Existing FP&A Frameworks

Integrating Monte Carlo simulation into existing FP&A frameworks involves carefully embedding probabilistic methods alongside traditional financial planning processes. The goal is to enhance forecasting accuracy and risk assessment without disrupting established workflows. This section outlines practical steps, considerations, and examples to help FP&A professionals make this integration smooth and effective.

Understanding the Current FP&A Framework

Before adding Monte Carlo simulation, it’s important to map out the existing planning cycle. Typical FP&A frameworks include:

- Data collection and cleansing

- Assumption setting

- Forecast model building (often deterministic)

- Scenario and sensitivity analysis

- Budget consolidation

- Reporting and communication

Monte Carlo simulation fits primarily into the forecasting and risk analysis phases but can influence assumptions and reporting.

Key Integration Points

Step 1: Align Input Data and Assumptions

Monte Carlo simulation requires defining probability distributions for uncertain inputs instead of single-point estimates. Start by reviewing your current assumptions:

- Identify which inputs are uncertain and can be modeled probabilistically (e.g., sales growth, cost inflation, FX rates).

- Gather historical data to estimate distribution parameters or use expert judgment when data is sparse.

- Document assumptions clearly to maintain transparency.

Example: Instead of assuming a fixed 5% sales growth, model it as a normal distribution with a mean of 5% and a standard deviation of 2%. This reflects real-world variability.

Step 2: Adapt Forecast Models to Accept Probabilistic Inputs

Most existing models are deterministic spreadsheets or software models. To integrate Monte Carlo:

- Modify formulas to accept random input samples rather than fixed values.

- Incorporate correlation structures where variables are interdependent.

- Use add-ins or scripting (e.g., Excel with @RISK, Python scripts) to automate repeated sampling and calculation.

Example: In a cash flow model, link revenue and cost drivers to their distributions and run thousands of iterations to generate a distribution of net cash flow outcomes.

Step 3: Run Simulations and Analyze Outputs

Set the number of iterations (commonly 5,000 to 10,000) to balance accuracy and computation time. Analyze outputs by:

- Examining output distributions (mean, median, percentiles).

- Identifying probabilities of meeting or missing targets.

- Performing sensitivity analysis to see which inputs drive output variability.

Example: A profit forecast might show a 70% chance of exceeding the target, helping management understand risk levels rather than relying on a single number.

Step 4: Integrate Results into Reporting and Decision-Making

Monte Carlo outputs should feed into regular FP&A reports:

- Present probabilistic forecasts alongside traditional numbers.

- Use charts like histograms, cumulative distribution functions, and tornado diagrams to communicate uncertainty and key drivers.

- Frame insights in terms of probabilities and risk, not just point estimates.

Example: Instead of reporting “Projected EBITDA: $10M,” report “Projected EBITDA ranges from $7M to $13M with a 90% confidence interval, and a 15% chance of falling below $8M.”

Step 5: Embed into Planning Cycles and Governance

To make Monte Carlo simulation a routine part of FP&A:

- Define clear roles and responsibilities for model maintenance and updates.

- Establish version control and documentation standards.

- Train team members on interpreting probabilistic results.

- Schedule simulation runs aligned with budgeting and forecasting timelines.

Practical Example: Integrating Monte Carlo into a Sales Forecast

Imagine a company forecasting quarterly sales. The traditional approach uses a single growth rate per quarter. To integrate Monte Carlo:

- Gather historical quarterly sales data and calculate variability.

- Define a probability distribution for quarterly growth rates (e.g., triangular distribution with minimum, most likely, and maximum values).

- Model correlations between quarters to reflect seasonality.

- Run 10,000 simulations generating a range of sales outcomes.

- Analyze the distribution to identify the probability of hitting sales targets.

- Present results in the quarterly forecast report with confidence intervals and risk commentary.

This approach provides a richer view of potential outcomes and helps sales and finance teams plan contingencies.

Summary

Integrating Monte Carlo simulation into existing FP&A frameworks is a stepwise process that respects current workflows while enhancing forecasting with probabilistic insights. By aligning data inputs, adapting models, analyzing outputs thoughtfully, and embedding results into reporting and governance, FP&A teams can improve decision-making without overhauling their entire process.

1.7 Practical Example: Comparing Deterministic vs. Monte Carlo Forecasts

When forecasting corporate financials, the choice between deterministic and Monte Carlo methods can significantly influence decision-making. This section walks through a clear example comparing the two approaches, highlighting their differences, strengths, and limitations.

Scenario: Forecasting Next Quarter’s Revenue for a Retail Company

The company expects revenue driven primarily by three factors:

- Number of customers

- Average purchase value

- Conversion rate (percentage of visitors who buy)

Each factor has some uncertainty, but traditional deterministic forecasting often uses single-point estimates.

Deterministic Forecast

Step 1: Define inputs as fixed values

| Factor | Estimate |

|---|---|

| Number of customers | 10,000 |

| Average purchase | $50 |

| Conversion rate | 20% (0.20) |

Step 2: Calculate revenue

Revenue = Number of customers × Conversion rate × Average purchase

= 10,000 × 0.20 × $50 = $100,000

Interpretation: The forecast is a single number: $100,000. This is straightforward but ignores variability.

Monte Carlo Forecast

Step 1: Define input distributions

Instead of fixed values, assign probability distributions reflecting uncertainty:

- Number of customers: Normal distribution, mean = 10,000, standard deviation = 1,000

- Average purchase: Triangular distribution, min = $45, mode = $50, max = $60

- Conversion rate: Beta distribution, alpha = 20, beta = 80 (mean = 0.20)

Step 2: Run simulations

For each iteration (e.g., 10,000 runs), randomly sample values from each distribution and calculate revenue.

Step 3: Analyze output

The simulation produces a distribution of possible revenues, not a single number.

Mind Map: Deterministic vs. Monte Carlo Forecast

Results Comparison

| Metric | Deterministic | Monte Carlo (Example Output) |

|---|---|---|

| Revenue Forecast | $100,000 | Mean: $99,500 |

| Median: $99,800 | ||

| 5th percentile: $85,000 | ||

| 95th percentile: $115,000 | ||

| Interpretation | Single value | Range with probabilities |

What Does This Mean?

- The deterministic forecast gives a clear target but no insight into risk or variability.

- The Monte Carlo forecast shows a range of plausible outcomes, allowing risk assessment.

- For example, there is a 5% chance revenue could be below $85,000, which deterministic ignores.

Mind Map: Benefits and Limitations

Practical Example: Sensitivity Analysis

Using the Monte Carlo output, we can identify which input contributes most to revenue variability.

- By correlating input samples with revenue outcomes, suppose we find:

- Number of customers explains 60% of variance

- Conversion rate explains 30%

- Average purchase explains 10%

This insight helps prioritize efforts to reduce uncertainty.

Summary

- Deterministic forecasts are straightforward but blind to uncertainty.

- Monte Carlo forecasts provide a fuller picture, showing a distribution of outcomes.

- Monte Carlo requires more input data and computational effort but supports better risk management.

- Incorporating Monte Carlo simulation into FP&A helps teams understand the range of possible financial futures rather than betting on a single point.

This example illustrates why Monte Carlo methods are valuable in financial planning and analysis, especially when uncertainty matters.

Chapter 2: Foundations of Probability and Statistics for Monte Carlo Simulation

2.1 Basic Probability Concepts Relevant to Financial Forecasting

Probability is the backbone of Monte Carlo simulation. It quantifies uncertainty by assigning numbers to the likelihood of events. In financial forecasting, understanding probability helps us model outcomes that are not fixed but vary due to inherent risks and unknowns.

What is Probability?

Probability measures how likely an event is to occur, expressed as a number between 0 and 1. A probability of 0 means the event cannot happen; 1 means it is certain.

- Example: The probability that a company will meet its quarterly sales target might be 0.75, meaning there is a 75% chance of success.

Key Terms

- Experiment: A process with uncertain outcomes (e.g., forecasting next quarter’s revenue).

- Outcome: A possible result of an experiment (e.g., revenue is $1M, $1.2M, etc.).

- Event: One or more outcomes grouped together (e.g., revenue exceeding $1M).

Types of Probability

- Theoretical Probability: Based on known possibilities (e.g., rolling a fair die).

- Empirical Probability: Based on observed data (e.g., historical sales performance).

- Subjective Probability: Based on judgment or expert opinion (e.g., assessing risk of a new product launch).

Probability Rules

- Sum Rule: The total probability of all possible outcomes equals 1.

- Complement Rule: Probability of an event not occurring is 1 minus the probability it does.

Mind Map: Basic Probability Concepts

Probability Distributions

A probability distribution describes how probabilities are assigned to different outcomes.

- Discrete distributions: Outcomes are countable (e.g., number of sales calls made).

- Continuous distributions: Outcomes can take any value in a range (e.g., revenue amount).

Example: Modeling Sales Outcomes

Suppose a company expects the number of new clients next month to be 0, 1, or 2 with probabilities 0.2, 0.5, and 0.3 respectively. This is a discrete probability distribution.

Calculating Probabilities

If you want to know the chance of getting at least one new client, calculate:

P(at least 1) = P(1) + P(2) = 0.5 + 0.3 = 0.8

Mind Map: Probability Distributions

Conditional Probability

This is the probability of an event given another event has occurred.

-

Notation: P(A|B) means probability of A given B.

-

Example: Probability that sales exceed $1M given that marketing spend was above budget.

Independence

Two events are independent if the occurrence of one does not affect the probability of the other.

- Example: The chance of winning a contract is independent of the weather.

Mind Map: Conditional Probability and Independence

Practical Example: Forecasting Revenue with Probability

Imagine forecasting next quarter’s revenue with three possible outcomes:

| Revenue ($M) | Probability |

|---|---|

| 10 | 0.3 |

| 12 | 0.5 |

| 15 | 0.2 |

The expected revenue (mean) is:

E(Revenue) = 100.3 + 120.5 + 15*0.2 = 3 + 6 + 3 = 12 million

This expected value is a weighted average, reflecting the probabilities.

Summary

Probability concepts help translate uncertainty into numbers. They form the foundation for building models that reflect real-world variability in financial outcomes. Understanding these basics ensures that Monte Carlo simulations produce meaningful and actionable forecasts.

2.2 Probability Distributions: Types and Applications in FP&A

Probability distributions describe how the values of a random variable are spread or distributed. In financial planning and analysis (FP&A), understanding these distributions helps model uncertainties in revenue, costs, cash flows, and other financial metrics. Choosing the right distribution for each variable is crucial to generating realistic Monte Carlo simulations.

Common Types of Probability Distributions in FP&A

Below is a mind map summarizing key distributions and their typical applications:

Discrete Distributions

Binomial Distribution models the number of successes in a fixed number of independent trials, each with the same probability of success. For example, if an FP&A team wants to estimate how many out of 10 planned projects will get approved, assuming a 60% approval rate, the binomial distribution fits well.

Poisson Distribution is used to model the number of events occurring in a fixed interval of time or space when these events happen independently. For instance, estimating the number of warranty claims in a month can be modeled with a Poisson distribution.

Continuous Distributions

Normal Distribution is the classic bell curve. Many financial variables approximate this distribution when influenced by many small, independent factors. For example, forecast errors or deviations in monthly sales often fit a normal distribution. Its symmetry means values equally spread around the mean.

Lognormal Distribution applies when the variable cannot be negative and tends to be right-skewed. Revenue or stock prices often follow this pattern because growth compounds multiplicatively. If you model revenue growth rates as lognormal, you avoid unrealistic negative values.

Uniform Distribution assumes every value within a specified range is equally likely. This is useful when you have limited information but know the minimum and maximum possible values. For example, if a supplier quotes a cost range between $100,000 and $120,000 with no further detail, a uniform distribution can represent that uncertainty.

Triangular Distribution is a simple, intuitive distribution defined by minimum, most likely, and maximum values. It’s often used in early-stage estimates where data is scarce. For example, estimating project duration with a minimum of 3 months, most likely 5 months, and maximum 8 months.

Beta Distribution is flexible and bounded between 0 and 1, making it suitable for modeling probabilities or percentages. For example, modeling the probability of customer churn or the expected utilization rate of a resource.

Examples of Applying Distributions in FP&A

-

Revenue Forecasting with Lognormal Distribution

- Suppose historical monthly revenue growth rates show a right-skewed pattern with occasional high spikes. Modeling revenue growth as lognormal captures this skewness and prevents negative revenue forecasts.

-

Cost Estimation Using Triangular Distribution

- For a new product launch, the marketing team estimates the campaign cost as $50,000 minimum, $70,000 most likely, and $100,000 maximum. Using a triangular distribution in the simulation reflects this uncertainty without requiring detailed historical data.

-

Probability of Project Success with Binomial Distribution

- If the company historically approves 70% of submitted projects, and 5 projects are under review, the binomial distribution can estimate the probability of exactly 3 projects getting approved.

-

Modeling Forecast Errors with Normal Distribution

- Forecast errors in sales volume often cluster around zero with some variability. Assuming a normal distribution with mean zero and standard deviation derived from historical errors allows realistic simulation of forecast deviations.

Visualizing Distributions

Here’s a simple mind map to visualize how an FP&A professional might select distributions based on data characteristics:

Summary

In FP&A, selecting the right probability distribution is about matching the nature of the financial variable and the available data. Discrete distributions handle count and binary events, while continuous distributions model quantities with uncertainty. Using these distributions in Monte Carlo simulations allows FP&A teams to capture realistic variability and risk, leading to better-informed financial decisions.

2.3 Descriptive Statistics and Their Role in Data Analysis

Descriptive statistics summarize and organize data to make it easier to understand. In financial planning and analysis (FP&A), these statistics provide a snapshot of historical data and help frame assumptions for Monte Carlo simulations. They do not predict future outcomes but describe the characteristics of data sets, which is essential before applying probabilistic models.

Key Descriptive Statistics

-

Measures of Central Tendency: These describe the center point of a data set.

- Mean: The arithmetic average. For example, if quarterly sales were $100k, $120k, $110k, and $130k, the mean sales would be $(100 + 120 + 110 + 130) / 4 = 115k$.

- Median: The middle value when data is ordered. If sales were $100k, $110k, $115k, $130k, the median is the average of $110k$ and $115k$, which is $112.5k$.

- Mode: The most frequent value. If monthly expenses are $50k, $50k, $55k, $60k, the mode is $50k$.

-

Measures of Dispersion: These describe the spread or variability in data.

- Range: Difference between the maximum and minimum values. If profits ranged from $20k to $80k, the range is $60k$.

- Variance: Average of squared differences from the mean. It quantifies variability but is in squared units.

- Standard Deviation (SD): Square root of variance, expressed in the same units as data. A higher SD means more variability.

-

Shape of Distribution:

- Skewness: Measures asymmetry. Positive skew means a longer tail on the right; negative skew means a longer tail on the left.

- Kurtosis: Measures the “tailedness” or how heavy the tails are compared to a normal distribution.

Why Descriptive Statistics Matter in FP&A

- Data Quality Check: Identifying outliers or unusual values that could distort forecasts.

- Input Distribution Selection: Understanding the shape and spread helps choose appropriate probability distributions for simulation inputs.

- Baseline Understanding: Knowing average performance and variability sets realistic expectations.

- Communication: Summarized statistics provide clear, concise information for stakeholders.

Mind Map: Descriptive Statistics Overview

Example: Analyzing Monthly Revenue Data

Suppose an FP&A analyst has 12 months of revenue data (in $000s):

120, 130, 125, 140, 135, 150, 145, 155, 160, 158, 162, 170

-

Mean: Sum all values and divide by 12.

- Total = 1705

- Mean = 1705 / 12 ≈ 142.08

-

Median: Order data (already sorted), middle values are 135 and 140.

- Median = (135 + 140) / 2 = 137.5

-

Mode: No repeated values, so no mode.

-

Range: 170 - 120 = 50

-

Variance and SD:

- Calculate squared differences from mean, average them for variance.

- SD is square root of variance.

-

Skewness: Data is slightly right-skewed due to higher values at the end.

This analysis shows revenue is generally increasing with moderate variability. The positive skew suggests occasional higher revenues, which should be considered when modeling.

Mind Map: Applying Descriptive Statistics in FP&A

Practical Example: Using Descriptive Statistics to Choose a Distribution

Imagine you want to model monthly sales volume for a product. Historical data shows:

- Mean = 500 units

- SD = 50 units

- Skewness = 0 (approximately symmetric)

Given this, a normal distribution might be appropriate for simulation inputs. However, if skewness were positive, a lognormal or gamma distribution might better capture the data’s characteristics.

Summary

Descriptive statistics are the foundation for understanding financial data before applying Monte Carlo simulations. They help identify the central tendencies and variability, guide distribution selection, and ensure the data used in models reflects reality. Clear, concise descriptive summaries also improve communication within FP&A teams and with stakeholders.

2.4 Understanding Random Variables and Stochastic Processes

In financial planning and analysis, grasping the concepts of random variables and stochastic processes is essential for building reliable Monte Carlo simulations. These ideas help us model uncertainty and variability in financial outcomes.

Random Variables

A random variable is a numerical outcome of a random phenomenon. It assigns a number to each possible outcome of an experiment or event. For example, the future sales revenue of a product next quarter can be considered a random variable because it varies due to market conditions, customer demand, and other factors.

Random variables come in two types:

- Discrete random variables: These take on countable values, like the number of new customers acquired in a month (0, 1, 2, …).

- Continuous random variables: These can take any value within a range, such as the percentage growth rate of revenue, which might be 3.2%, 3.25%, or any number within an interval.

Mind Map: Random Variables

The expected value (or mean) of a random variable gives the average outcome if the experiment were repeated many times. The variance measures how spread out the outcomes are around the mean.

Example: Suppose the number of new customers next month is a discrete random variable with probabilities:

| Customers | Probability |

|---|---|

| 0 | 0.1 |

| 1 | 0.3 |

| 2 | 0.4 |

| 3 | 0.2 |

The expected number of new customers is:

E[X] = 00.1 + 10.3 + 20.4 + 30.2 = 0 + 0.3 + 0.8 + 0.6 = 1.7 customers.

Stochastic Processes

A stochastic process is a collection of random variables indexed by time or another parameter. It models how a system evolves over time under uncertainty. In FP&A, stochastic processes can represent how revenue, costs, or cash flows change month to month.

Think of a stochastic process as a random variable that changes its value at different points in time.

Mind Map: Stochastic Processes

Example: Discrete-Time Stochastic Process

Imagine quarterly revenue as a stochastic process \( {R_t} \), where \( t = 1, 2, 3, … \) represents quarters. Each \( R_t \) is a random variable representing revenue in quarter \( t \).

If revenue depends only on the previous quarter’s revenue plus some random shock, this process has the Markov property (future depends only on the present, not the past).

Example: Simple Revenue Model

\[ R_{t} = R_{t-1} + \epsilon_t \]

where \( \epsilon_t \) is a random variable representing unexpected changes (positive or negative).

This model captures the idea that revenue evolves over time with some randomness.

Why These Concepts Matter in Monte Carlo Forecasting

Monte Carlo simulation relies on sampling from random variables to generate many possible outcomes. When forecasting over multiple periods, stochastic processes help model how variables evolve, capturing temporal dependencies.

Understanding the difference between a single random variable and a stochastic process clarifies how to structure simulations:

- Use random variables to model uncertainty at a single point in time.

- Use stochastic processes to model sequences of uncertain outcomes over time.

Summary

- A random variable assigns numerical values to uncertain outcomes.

- Random variables can be discrete or continuous.

- The expected value and variance describe the average and variability.

- A stochastic process is a sequence of random variables indexed by time.

- Stochastic processes model how financial metrics evolve with uncertainty.

These concepts form the backbone of probabilistic financial forecasting and risk analysis.

2.5 Correlation and Dependency Structures in Financial Data

In financial forecasting, understanding how variables relate to each other is crucial. Correlation and dependency structures describe these relationships. They influence how risks and outcomes propagate through a model, affecting the accuracy and realism of Monte Carlo simulations.

What is Correlation?

Correlation measures the strength and direction of a linear relationship between two variables. It ranges from -1 to +1:

- +1 means perfect positive correlation (variables move together).

- 0 means no linear correlation.

- -1 means perfect negative correlation (variables move inversely).

Correlation is a simple but powerful tool to capture dependencies, especially in financial data where variables rarely move independently.

Why Correlation Matters in Monte Carlo Simulation

If you ignore correlation and treat inputs as independent, your simulation might underestimate risk or overstate diversification benefits. For example, sales in two related product lines might rise or fall together due to market conditions. Modeling them as independent could produce unrealistic combined outcomes.

Types of Dependency Structures

Correlation is one way to describe dependency, but it only captures linear relationships. Other structures include:

- Rank Correlation (Spearman’s rho, Kendall’s tau): Measures monotonic relationships, not just linear.

- Copulas: Functions that link multiple marginal distributions to form a joint distribution, capturing complex dependencies beyond correlation.

Mind Map: Understanding Dependency Structures

Calculating Correlation: A Simple Example

Suppose you have monthly revenue data for two product lines over a year:

| Month | Product A Revenue | Product B Revenue |

|---|---|---|

| Jan | 100 | 80 |

| Feb | 110 | 85 |

| Mar | 105 | 90 |

| Apr | 115 | 95 |

| May | 120 | 100 |

| Jun | 125 | 105 |

| Jul | 130 | 110 |

| Aug | 135 | 115 |

| Sep | 140 | 120 |

| Oct | 145 | 125 |

| Nov | 150 | 130 |

| Dec | 155 | 135 |

Calculating Pearson’s correlation coefficient for these two series would show a strong positive correlation close to 1, indicating that revenues move together.

Incorporating Correlation into Monte Carlo Models

To simulate correlated variables, you can use methods such as:

- Cholesky Decomposition: Transforms independent random variables into correlated ones using a correlation matrix.

- Copulas: Allows modeling of dependencies with different marginal distributions.

Mind Map: Incorporating Correlation in Simulation

Example: Using Cholesky Decomposition

Imagine you want to simulate two correlated variables: sales growth and marketing spend. Assume their correlation is 0.7.

- Define the correlation matrix:

| 1.0 0.7 |

| 0.7 1.0 |

- Generate two independent standard normal variables.

- Apply Cholesky decomposition to the correlation matrix.

- Multiply the independent variables by the Cholesky matrix to get correlated variables.

This process ensures that the simulated sales growth and marketing spend reflect the real-world correlation.

Dependency Beyond Correlation: Copulas

Correlation alone can miss tail dependencies—how variables behave during extreme events. Copulas help capture these nuances.

For example, during a market downturn, multiple financial metrics might simultaneously drop more than correlation suggests. Using a copula like the Clayton copula can model this stronger lower-tail dependence.

Mind Map: Copula Types and Uses

Practical Example: Correlation in Revenue and Cost Forecasting

Suppose a company forecasts revenue and cost for a product. Revenue and cost are positively correlated because higher sales volumes usually increase costs.

Ignoring this correlation might produce scenarios where revenue is high but costs remain low, which is unrealistic.

By including a positive correlation (say 0.6) in the simulation inputs, the model generates more plausible joint outcomes, improving forecast reliability.

Summary

- Correlation quantifies linear relationships and is essential for realistic simulations.

- Dependency structures can be more complex than correlation; copulas offer advanced modeling.

- Incorporating correlation prevents underestimation of risk and unrealistic scenario generation.

- Tools like Cholesky decomposition help generate correlated random variables for simulations.

Understanding and correctly modeling dependencies in financial data is a foundational step toward accurate Monte Carlo forecasting.

2.6 Sampling Techniques and Their Importance in Simulation

Sampling is the process of selecting representative values from a probability distribution to use as inputs in a Monte Carlo simulation. Since Monte Carlo forecasting relies on repeated random sampling to estimate outcomes, the quality and method of sampling directly affect the accuracy and reliability of the simulation results.

Why Sampling Matters

Imagine you want to forecast sales revenue, but your input variable—customer demand—is uncertain and described by a probability distribution. To simulate possible outcomes, you need to draw values from this distribution. If your samples don’t represent the distribution well, your forecast will be biased or misleading.

Sampling techniques help ensure that the values drawn reflect the true characteristics of the underlying distribution, such as its shape, spread, and any dependencies with other variables.

Common Sampling Techniques

Here is a mind map summarizing key sampling methods used in Monte Carlo simulations:

Simple Random Sampling

This is the most straightforward approach. Each sample is drawn independently and randomly from the entire distribution. It’s easy to implement but can require a large number of samples to cover the distribution evenly.

Example: If you want to simulate monthly sales, you generate random values from the sales distribution for each month independently.

Stratified Sampling

The distribution is divided into distinct strata or segments, and samples are drawn from each stratum proportionally. This ensures that all parts of the distribution are represented.

Example: Suppose customer demand varies by region. You could stratify the demand distribution by region and sample from each, ensuring regional variability is captured.

Latin Hypercube Sampling (LHS)

LHS divides the cumulative distribution into equal probability intervals and samples once from each interval. It ensures better coverage of the input space with fewer samples compared to simple random sampling.

Example: For a forecast of product price sensitivity, LHS ensures that low, medium, and high price points are all sampled, preventing clustering of samples in one region.

Importance Sampling

This technique focuses sampling on the most critical parts of the distribution that have the greatest impact on the outcome, often the tails.

Example: When assessing risk of extreme losses, importance sampling draws more samples from the tail of the loss distribution to better estimate rare but impactful events.

Systematic Sampling

Samples are drawn at regular intervals from an ordered list of possible values. It’s simpler than random sampling and can be effective if the data is well-ordered.

Example: If you have a sorted list of historical sales figures, you might pick every 10th value to represent the distribution.

Quasi-Random Sampling

Also called low-discrepancy sequences, this method generates samples that are more evenly spaced than purely random samples, improving convergence speed.

Example: Using Sobol sequences to sample input variables in a financial model to reduce variance in simulation results.

Visualizing Sampling Methods

Here’s a mind map illustrating how different sampling methods cover a distribution:

Practical Example: Sampling for Revenue Forecast

Suppose you model monthly revenue with a triangular distribution: minimum $80k, most likely $100k, maximum $130k.

- Using simple random sampling, you might get many samples near $100k but few near the extremes.

- With stratified sampling, you ensure samples from low, medium, and high revenue ranges.

- Latin Hypercube Sampling guarantees that each segment of the distribution is sampled, improving the reliability of your forecast.

Running 1,000 iterations with LHS often yields a more stable estimate of expected revenue and risk than 1,000 simple random samples.

Correlated Sampling

When input variables are correlated, sampling must preserve these relationships. Ignoring correlation can produce unrealistic scenarios.

Example: If sales volume and price are negatively correlated, sampling them independently might generate unlikely combinations (high price and high volume). Techniques like copula functions or Cholesky decomposition help generate correlated samples.

Summary

Sampling techniques are the foundation of Monte Carlo simulation. Choosing the right method can improve simulation efficiency, accuracy, and insight. Simple random sampling is easy but may require many iterations. Stratified and Latin Hypercube Sampling improve coverage with fewer samples. Importance sampling targets critical regions. Correlated sampling preserves relationships between variables. Understanding these techniques helps FP&A professionals build robust financial models that better reflect uncertainty.

2.7 Practical Example: Defining Input Distributions for Revenue Forecasting

When building a Monte Carlo simulation for revenue forecasting, one of the first and most critical steps is defining the input distributions for the uncertain variables. These inputs represent the range and likelihood of possible values that key revenue drivers can take. Getting this right ensures the simulation produces meaningful and actionable results.

Step 1: Identify Key Revenue Drivers

Before assigning distributions, list the main factors influencing revenue. Common drivers include:

- Sales volume (units sold)

- Price per unit

- Market growth rate

- Customer churn or retention rates

- Seasonal effects

Each of these drivers can vary, and their uncertainty must be captured.

Step 2: Choose Appropriate Probability Distributions

Not all distributions fit every variable. The choice depends on the nature of the data and business context. Here’s a quick mind map to organize common distributions and their typical uses:

Step 3: Gather Data and Expert Input

Historical data helps estimate parameters like mean and standard deviation. When data is sparse, expert judgment can fill gaps, especially for minimum, most likely, and maximum values used in triangular distributions.

Step 4: Define Distributions for Each Driver

Let’s consider a simplified revenue model:

- Sales Volume: Historical data shows sales vary between 900 and 1,100 units monthly, with a most likely value around 1,000. A triangular distribution fits well here.

- Price per Unit: Prices fluctuate slightly around $50, with a standard deviation of $2. A normal distribution is appropriate.

- Market Growth Rate: Uncertain but expected between -2% and 5%, with no strong reason to favor any value. A uniform distribution suits this.

Step 5: Visualize the Distributions

Visualizing helps confirm the chosen distributions reflect reality.

-

Sales Volume (Triangular)

- Min: 900

- Mode: 1000

- Max: 1100

-

Price per Unit (Normal)

- Mean: 50

- Std Dev: 2

-

Market Growth Rate (Uniform)

- Min: -0.02

- Max: 0.05

Step 6: Mind Map of Revenue Forecast Inputs

Step 7: Example Calculation Setup

The revenue for a given month can be modeled as:

Revenue = Sales Volume × Price per Unit × (1 + Market Growth Rate)

Each variable is sampled from its distribution during simulation iterations.

Step 8: Checking Correlations

If sales volume and price per unit are correlated (e.g., higher sales when prices are lower), this dependency should be modeled. Ignoring correlations can distort results. For this example, assume independence for simplicity.

Step 9: Summary

Defining input distributions involves:

- Understanding the business context and drivers

- Selecting distributions that match data characteristics

- Using historical data or expert estimates to set parameters

- Visualizing and validating assumptions

This foundation allows the Monte Carlo simulation to produce a realistic range of revenue outcomes, supporting better financial planning and risk assessment.

Chapter 3: Building Monte Carlo Models for Financial Forecasting

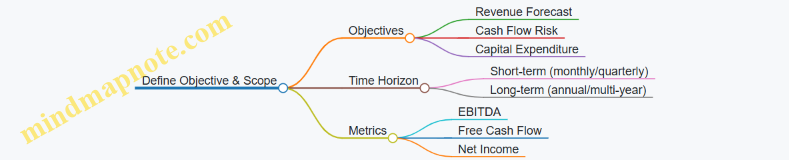

3.1 Defining Model Objectives and Scope in FP&A Context

When starting a Monte Carlo simulation project for financial planning and analysis (FP&A), the first step is to clearly define what the model is supposed to achieve and the boundaries within which it will operate. This clarity helps avoid wasted effort and ensures the simulation delivers actionable insights.

Why Define Objectives and Scope?

Without a well-defined objective, a model can become a vague exercise in number crunching. The objective guides the selection of variables, the design of input distributions, and the interpretation of results. Scope limits the model’s complexity and keeps it manageable, ensuring it aligns with business needs.

Key Questions to Define Objectives

- What specific financial question or decision is the simulation intended to support?

- Which financial metrics or KPIs are most relevant?

- What time horizon does the forecast cover?

- What level of detail is required (e.g., company-wide, business unit, product line)?

- What uncertainties or risks need to be captured?

Example Objective Statements

- “Estimate the probability distribution of next year’s operating cash flow to support liquidity planning.”

- “Assess the range of possible EBITDA outcomes for a new product launch over 18 months.”

- “Quantify the risk of budget overruns in the capital expenditure plan for the upcoming fiscal year.”

Defining Scope

Scope involves setting boundaries on what is included in the model and what is left out. This might mean focusing on certain revenue streams, excluding minor cost categories, or limiting the forecast to a single business unit.

A well-scoped model balances detail with usability. Too broad, and it becomes unwieldy; too narrow, and it may miss critical factors.

Mind Map: Defining Model Objectives and Scope

Practical Example: Cash Flow Forecasting Model

Objective: Forecast the distribution of monthly cash flow over the next 12 months to identify the probability of cash shortfalls.

Scope: Include major cash inflows (sales receipts, financing) and outflows (operating expenses, debt service). Exclude minor one-time expenses and non-cash items.

This objective and scope focus the model on the cash flow drivers that matter most for liquidity management, avoiding unnecessary complexity.

Steps to Define Objectives and Scope

- Engage Stakeholders: Understand what decisions the model should inform.

- List Financial Metrics: Identify which KPIs or financial statements are relevant.

- Determine Time Frame: Choose a forecast horizon that matches planning cycles.

- Identify Key Drivers and Risks: Pinpoint variables with significant uncertainty.

- Set Boundaries: Decide what to include or exclude based on impact and data availability.

- Document Assumptions: Clearly record what the model covers and what it does not.

Example Mind Map: Stakeholder Engagement for Objective Setting

Why This Matters

A clear objective and scope prevent the model from becoming a black box. They help focus data collection, simplify communication, and ensure the simulation results are relevant and trusted. Without this foundation, even a technically sound Monte Carlo simulation may fail to influence decisions.

In summary, defining model objectives and scope is the blueprint stage of Monte Carlo forecasting in FP&A. It sets the direction, limits complexity, and aligns expectations. Taking time here pays off in clarity and usefulness down the line.

3.2 Identifying Key Financial Drivers and Uncertainties

Identifying key financial drivers and uncertainties is a critical step in building a Monte Carlo simulation model for financial forecasting. These elements form the foundation of your model’s inputs and directly influence the accuracy and usefulness of your simulation outcomes.

What Are Financial Drivers?

Financial drivers are the variables that have a direct impact on your financial results. They can be internal factors like sales volume, pricing, or cost of goods sold, or external factors such as market demand, interest rates, or exchange rates. Pinpointing the right drivers means focusing on those variables that significantly affect your financial statements.

What Are Uncertainties?

Uncertainties represent the range of possible values that a financial driver can take. Unlike fixed assumptions, uncertainties acknowledge that real-world outcomes vary. For example, sales growth might be uncertain due to market competition or economic conditions.

Why Is This Important?

Monte Carlo simulation thrives on variability. Without identifying key drivers and their uncertainties, your model risks being either too simplistic or too complex, leading to misleading results or unnecessary complications.

Steps to Identify Key Financial Drivers and Uncertainties

-

Map the Business Model and Financial Statements Start by understanding how money flows through the business. Break down revenue streams, cost structures, capital expenditures, and financing.

-

List Potential Drivers Brainstorm all variables that could influence your financial outcomes. Include both controllable factors (like marketing spend) and uncontrollable ones (like commodity prices).

-

Prioritize Drivers by Impact Use historical data, expert judgment, or preliminary analysis to rank drivers by their influence on key metrics such as EBITDA, cash flow, or net income.

-

Define Uncertainty Ranges For each key driver, determine the plausible range of outcomes. This can be based on historical volatility, market research, or scenario analysis.

-

Consider Correlations Identify relationships between drivers. For example, sales volume and marketing spend might be positively correlated.

Mind Map: Identifying Key Financial Drivers

Mind Map: Uncertainties Associated with Drivers

Example 1: Identifying Drivers for a Retail Company

- Revenue Drivers: Number of stores, average transaction value, customer footfall.

- Cost Drivers: Cost of goods sold (COGS), rent per store, staffing costs.

- Uncertainties: Seasonal fluctuations in footfall, supplier price changes, rent increases.

In this case, the Monte Carlo model might simulate footfall as a random variable with a seasonal pattern, while COGS could be modeled with a distribution reflecting supplier price volatility.

Example 2: Identifying Drivers for a Manufacturing Firm

- Revenue Drivers: Production volume, unit selling price.

- Cost Drivers: Raw material costs, labor hours, machine maintenance.

- Uncertainties: Raw material price swings due to commodity markets, machine downtime variability.

Here, raw material costs might be modeled using historical price distributions, while production volume could be linked to demand forecasts with uncertainty.

Tips for Effective Identification

- Use historical data to quantify variability where possible.

- Engage cross-functional teams to capture diverse perspectives on what drives financial outcomes.

- Keep the model manageable by focusing on drivers that materially affect results.

- Document assumptions clearly to support model transparency.

Identifying the right financial drivers and their uncertainties is less about guessing and more about structured analysis. This clarity sets the stage for building a Monte Carlo model that reflects the true range of possible financial futures.

3.3 Selecting Appropriate Probability Distributions for Inputs

Selecting appropriate probability distributions for inputs is a crucial step in building a Monte Carlo simulation model for financial forecasting. The choice of distribution affects how uncertainty is represented and ultimately influences the reliability of your forecasts. This section explains common distributions, how to select them, and provides practical examples to clarify the concepts.

Understanding the Role of Distributions

In Monte Carlo simulation, each uncertain input is modeled as a random variable with a probability distribution. This distribution captures the range of possible values and their likelihood. For example, sales growth might vary between -5% and +15%, but some values are more probable than others. Assigning a distribution allows the simulation to generate realistic scenarios reflecting that uncertainty.

Common Probability Distributions in FP&A

Here is a mind map summarizing common distributions and their typical applications:

How to Choose the Right Distribution

-

Understand the nature of the variable: Is it continuous or discrete? Does it have natural bounds? For example, probabilities must lie between 0 and 1, so beta distribution fits well.

-

Consider data availability: If you have historical data, analyze its distribution shape. If data is limited, use expert judgment to define plausible ranges.

-

Match distribution properties to the variable: For symmetric variables fluctuating around a mean, normal distribution often works. For skewed data, lognormal or beta might be better.

-

Keep it simple when possible: Triangular and uniform distributions are easy to understand and implement, especially when data is scarce.

-

Validate your choice: Run sensitivity tests to see how different distributions affect results.

Practical Examples

Example 1: Modeling Sales Growth

Suppose historical sales growth rates are roughly symmetric around 5%, with occasional dips and spikes. The data shows a mean of 5%, standard deviation of 3%. Here, a normal distribution fits well.

- Mean (μ): 5%

- Standard deviation (σ): 3%

This allows the simulation to generate growth rates mostly between -4% and 14%, capturing typical variability.

Example 2: Estimating Project Costs

A project manager estimates costs with a minimum of $90,000, most likely $100,000, and maximum $130,000. No detailed data exists.

A triangular distribution suits this scenario:

- Minimum: $90,000

- Mode (most likely): $100,000

- Maximum: $130,000

This reflects the manager’s judgment and bounds the cost realistically.

Example 3: Forecasting Market Share

Market share is a percentage between 0 and 100%. Historical data shows it fluctuates between 20% and 40%, with a tendency to cluster near 30%.

A beta distribution can model this well. By scaling beta to the 0.2–0.4 range and adjusting shape parameters, you capture the skew and bounds.

Visualizing Distributions

Here’s a mind map to help visualize the decision process:

Summary

Choosing the right probability distribution is about matching the mathematical properties of the distribution to the real-world behavior of the variable. Use data when available, rely on expert judgment when not, and prefer simple models unless complexity is justified. This approach ensures your Monte Carlo simulation produces meaningful and actionable forecasts.

3.4 Constructing the Simulation Model: Step-by-Step Approach

Constructing a Monte Carlo simulation model involves a clear, methodical approach that turns financial uncertainties into quantifiable outcomes. This section breaks down the process into manageable steps, illustrated with mind maps and practical examples to keep things grounded.

Step 1: Define the Objective and Scope

Start by clarifying what you want to achieve with the simulation. Are you forecasting revenue, cash flow, or assessing risk exposure? Defining the scope helps focus the model and avoid unnecessary complexity.

Example: Suppose your goal is to forecast next year’s operating cash flow for a mid-sized manufacturing company, focusing on sales volume, price variability, and cost fluctuations.

Step 2: Identify Key Variables and Uncertainties

List all the financial drivers that influence your forecast. Separate deterministic inputs (fixed values) from uncertain variables that will be modeled probabilistically.

Example: Sales volume fluctuates seasonally, prices may vary due to market conditions, and raw material costs can be volatile.

Step 3: Choose Probability Distributions for Inputs

Assign appropriate probability distributions to each uncertain variable based on historical data, expert judgment, or industry benchmarks.

Example: Sales volume might follow a normal distribution centered around the average monthly sales with a standard deviation reflecting past variability. Price could use a triangular distribution with minimum, most likely, and maximum values.

Step 4: Establish Relationships and Formulas

Define how variables interact. This includes formulas linking inputs to outputs, such as revenue = sales volume × price, and profit = revenue - costs.

Example: If sales volume increases, revenue rises, but variable costs also increase proportionally.

Step 5: Incorporate Correlations Between Variables

Some variables move together. Ignoring correlations can distort results. Use correlation matrices or copulas to model dependencies.

Example: If raw material costs rise, prices might increase to maintain margins, indicating a positive correlation.

Step 6: Build the Simulation Logic

Translate the relationships and distributions into a computational model. This often involves setting up random sampling for each input and calculating outputs per iteration.

Example: For each iteration, randomly sample sales volume, price, and costs, then compute profit.

Step 7: Validate the Model

Check that the model behaves as expected. Test with known inputs, verify output ranges, and ensure correlations are preserved.

Example: Run the model with fixed inputs to confirm deterministic results, then with distributions to check output variability.

Step 8: Document Assumptions and Limitations

Clear documentation ensures transparency and helps users understand the model’s boundaries.

Example: Note that the model assumes stable economic conditions and does not account for sudden market shocks.

Practical Example: Constructing a Simple Cash Flow Model

- Objective: Forecast monthly operating cash flow for 12 months.

- Variables: Sales volume (uncertain), price per unit (uncertain), variable costs (uncertain), fixed costs (deterministic).

- Distributions: Sales volume ~ Normal(1000, 150), Price ~ Triangular(9, 10, 11), Variable costs ~ Lognormal(2, 0.3), Fixed costs = $50,000.

- Formulas:

- Revenue = Sales volume × Price

- Total costs = Variable costs × Sales volume + Fixed costs

- Cash flow = Revenue - Total costs

- Correlations: Assume sales volume and price are slightly negatively correlated (-0.2).

- Simulation: Run 10,000 iterations sampling inputs and calculating cash flow each time.

- Validation: Check that cash flow distribution aligns with expectations and that correlation is reflected.

- Documentation: Record assumptions about distributions, correlation, and fixed costs.

This step-by-step approach ensures the model is transparent, grounded in data, and useful for decision-making.

3.5 Incorporating Correlations and Dependencies Between Variables

In Monte Carlo simulation for financial forecasting, treating input variables as independent often oversimplifies reality. Many financial drivers move together, influenced by common factors or direct relationships. Ignoring these dependencies can lead to misleading results, either underestimating or overestimating risk and uncertainty.

Why Correlations Matter

Consider two variables: sales volume and marketing spend. If marketing spend increases, sales volume often rises too. If you simulate these variables independently, you might generate scenarios where marketing spend is high but sales volume is low, which is unlikely. Capturing the correlation ensures the simulation reflects realistic joint behavior.

Dependencies can be positive (variables move in the same direction) or negative (one increases while the other decreases). Some relationships are nonlinear or more complex, but linear correlation is a common starting point.

Mind Map: Understanding Variable Dependencies

Measuring Correlation

The Pearson correlation coefficient (ranging from -1 to 1) quantifies linear relationships. For example, an r of 0.8 between sales and marketing spend indicates a strong positive linear relationship. Zero means no linear correlation, but variables could still be related nonlinearly.

In practice, historical data helps estimate correlations. If data is limited, expert judgment or industry benchmarks may guide assumptions.

Incorporating Correlations: Techniques

Correlation Matrix

A correlation matrix lists pairwise correlations between all input variables. For example:

| Variable | Sales Volume | Marketing Spend | Price |

|---|---|---|---|

| Sales Volume | 1.0 | 0.75 | -0.3 |

| Marketing Spend | 0.75 | 1.0 | 0.0 |

| Price | -0.3 | 0.0 | 1.0 |

This matrix guides the simulation to generate correlated random samples.

Cholesky Decomposition

This mathematical method transforms independent random variables into correlated ones based on the correlation matrix. It’s widely used because it’s straightforward and efficient.

Copulas

Copulas model dependencies beyond linear correlation, capturing tail dependencies and nonlinear relationships. They are more complex but useful when variables exhibit such behavior.

Practical Example: Simulating Correlated Variables Using Cholesky Decomposition

Imagine you want to simulate sales volume and marketing spend, which have a correlation of 0.7. Both variables are normally distributed with means and standard deviations estimated from historical data.

Step 1: Define means and standard deviations.

- Sales Volume: mean = 1000 units, std dev = 100 units

- Marketing Spend: mean = $50,000, std dev = $5,000

Step 2: Define correlation matrix:

[ [1.0, 0.7],

[0.7, 1.0] ]

Step 3: Generate two independent standard normal random variables.

Step 4: Apply Cholesky decomposition to the correlation matrix to get matrix L.

Step 5: Multiply L by the vector of independent variables to get correlated standard normal variables.

Step 6: Scale and shift these to the original means and standard deviations.

Result: Simulated pairs of sales volume and marketing spend that reflect the 0.7 correlation.

This process ensures that when marketing spend is high in a simulation run, sales volume tends to be high as well.

Mind Map: Steps to Incorporate Correlations in Monte Carlo Simulation

Example: Impact of Ignoring Correlation

Suppose you simulate profit as revenue minus costs, where revenue and costs are correlated (e.g., higher sales lead to higher variable costs). If you simulate revenue and costs independently, you might get unrealistic scenarios with high revenue and low costs or vice versa.

This can inflate the variance of profit artificially. Including correlation aligns simulated scenarios with business logic, producing more reliable risk assessments.

Validating Correlations in Simulation Output

After running simulations with correlated inputs, check that the simulated variables maintain the intended correlation. Calculate the sample correlation of simulated outputs and compare to the input matrix. Large deviations may indicate errors in implementation.

Summary

Incorporating correlations between variables in Monte Carlo simulation is essential for realistic financial forecasting. The correlation matrix and Cholesky decomposition offer practical tools to achieve this. Properly modeling dependencies reduces the risk of misleading conclusions and supports better decision-making.

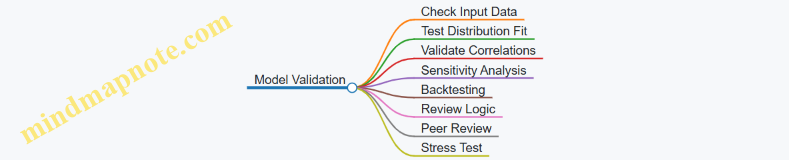

3.6 Validating Model Assumptions and Data Inputs

Validating model assumptions and data inputs is a critical step in building a reliable Monte Carlo simulation for financial forecasting. Without proper validation, the model risks producing misleading results that can lead to poor decision-making. This section breaks down the key validation tasks and illustrates them with practical examples and mind maps to clarify the process.

Why Validate?