Advanced Commodity Trading Risk Management and Derivatives Hedging Strategies

1. Introduction to Commodity Trading and Risk Management

1.1 Overview of Commodity Markets and Trading Dynamics

Commodity markets form the backbone of the global economy, facilitating the exchange of raw materials that fuel industries and consumer demand. Understanding their structure and trading dynamics is essential for commodity traders and risk managers aiming to navigate these markets effectively.

What Are Commodity Markets?

Commodity markets are platforms where raw or primary products are exchanged. These products fall into two broad categories:

- Hard Commodities: Natural resources that are mined or extracted, such as crude oil, natural gas, metals (gold, copper, aluminum).

- Soft Commodities: Agricultural products or livestock, such as wheat, coffee, sugar, cattle.

These markets can be physical (spot markets) or derivative-based (futures, options, swaps).

Key Participants in Commodity Markets

- Producers: Entities that extract or grow commodities (e.g., oil companies, farmers).

- Consumers: Industries or companies that use commodities as inputs (e.g., airlines, food manufacturers).

- Speculators: Traders seeking profit from price movements.

- Hedgers: Participants aiming to reduce price risk exposure.

Trading Venues

- Exchanges: Centralized platforms like CME Group, ICE, LME where standardized contracts trade.

- Over-the-Counter (OTC): Customized bilateral contracts negotiated directly between parties.

Trading Dynamics Mind Map

Price Drivers and Market Influences

Commodity prices are influenced by a complex interplay of factors:

- Supply and Demand: Crop yields, mining output, consumption trends.

- Geopolitical Events: Conflicts, trade policies, sanctions.

- Weather Conditions: Droughts, floods affecting agricultural commodities.

- Economic Indicators: Inflation rates, currency fluctuations, interest rates.

Example: Crude Oil Market Dynamics

Consider crude oil, one of the most actively traded commodities:

- Supply Factors: OPEC production quotas, US shale output.

- Demand Factors: Global economic growth, transportation fuel consumption.

- Geopolitical Risks: Middle East tensions, sanctions on oil-producing countries.

- Market Impact: Sudden supply disruptions can cause sharp price spikes.

Best Practice: Mapping Market Dynamics for Risk Identification

A practical approach to managing risk is to create a dynamic mind map of the commodity market you trade. For example, a trader in agricultural commodities might map:

This visual tool helps identify potential risk triggers and informs hedging strategies.

Summary

Understanding commodity markets and their trading dynamics requires grasping the types of commodities, key participants, trading venues, and the multifaceted factors driving prices. Mind maps serve as an effective method to visualize these complex relationships and support risk management decisions.

Additional Example: Coffee Market

- Supply: Sensitive to weather in Brazil and Vietnam.

- Demand: Influenced by global consumption trends.

- Risks: Crop diseases, currency fluctuations.

Mapping these factors helps traders anticipate price movements and design appropriate hedges.

By mastering the overview of commodity markets and trading dynamics, commodity traders and risk managers lay a strong foundation for advanced risk management and derivatives hedging strategies.

1.2 Key Risks in Commodity Trading: Market, Credit, Operational, and Liquidity Risks

Commodity trading is inherently exposed to a variety of risks that can impact profitability and operational stability. Understanding these risks in detail is essential for effective risk management. Below, we explore the four primary categories of risks in commodity trading: Market Risk, Credit Risk, Operational Risk, and Liquidity Risk. Each section includes mind maps to visualize the risk components and practical examples to illustrate their real-world implications.

Market Risk

Market risk refers to the potential losses arising from adverse movements in commodity prices, interest rates, foreign exchange rates, and volatility. This is the most visible and actively managed risk in commodity trading.

Mind Map: Market Risk Components

Example:

A crude oil trader holds a large position expecting prices to rise. However, geopolitical developments cause oil prices to drop sharply. Without hedging, the trader faces significant losses. By using futures contracts to lock in prices, the trader can mitigate this price risk.

Credit Risk

Credit risk arises from the possibility that counterparties will fail to fulfill their contractual obligations, leading to financial losses.

Mind Map: Credit Risk Components

Example:

A metals trading firm enters into an OTC swap with a counterparty to hedge price exposure. If the counterparty defaults during a period when the swap is in-the-money for the firm, the firm incurs losses. To mitigate this, the firm requires collateral and sets credit limits.

Operational Risk

Operational risk involves losses resulting from inadequate or failed internal processes, people, systems, or external events.

Mind Map: Operational Risk Components

Example:

An agricultural commodity desk experiences a trade booking error where a large position is mistakenly recorded twice. This leads to an unintended oversized exposure. The error is caught during reconciliation, but it highlights the need for robust operational controls.

Liquidity Risk

Liquidity risk is the risk that a trader cannot buy or sell positions quickly enough without significantly impacting the market price or incurring losses.

Mind Map: Liquidity Risk Components

Example:

A trader holds a large position in a niche metal with low daily trading volume. When attempting to unwind the position, the trader faces wide bid-ask spreads and limited counterparties, resulting in a significant market impact and losses.

Summary Table of Key Risks with Examples

| Risk Type | Description | Example Scenario | Mitigation Practice |

|---|---|---|---|

| Market Risk | Losses from price, interest rate, FX, volatility changes | Crude oil price drop impacting unhedged positions | Use of futures/options to hedge price exposure |

| Credit Risk | Counterparty failure to meet obligations | OTC swap counterparty default | Collateral agreements, credit limits |

| Operational Risk | Failures in processes, people, systems, external events | Trade booking error leading to oversized exposure | Strong reconciliation and control processes |

| Liquidity Risk | Difficulty in executing trades without loss | Large position in illiquid metal causing market impact | Position limits, use of algorithmic trading |

By systematically identifying and understanding these key risks, commodity traders and risk managers can design comprehensive strategies to monitor, mitigate, and manage exposures effectively.

1.3 Importance of Risk Management in Commodity Trading

Commodity trading is inherently exposed to a wide array of risks due to the volatile nature of commodity prices, geopolitical factors, supply-demand imbalances, and operational complexities. Effective risk management is not just a regulatory or procedural requirement but a strategic imperative that safeguards profitability, ensures business continuity, and enhances competitive advantage.

Why Risk Management is Crucial in Commodity Trading

- Price Volatility: Commodity prices can fluctuate dramatically due to weather events, geopolitical tensions, or macroeconomic shifts.

- Market Uncertainty: Sudden changes in market sentiment or unexpected news can impact supply chains and pricing.

- Credit Risk: Exposure to counterparties who may default on contracts.

- Operational Risk: Errors in trade execution, settlement failures, or system breakdowns.

- Liquidity Risk: Difficulty in entering or exiting positions without significant price impact.

Mind Map: Core Reasons for Risk Management in Commodity Trading

Best Practice: Embedding Risk Management into Trading Strategy

Integrate risk management at every stage of the trading lifecycle—from trade idea generation, execution, to post-trade monitoring. This includes:

- Setting clear risk limits aligned with organizational risk appetite.

- Using real-time risk analytics to monitor exposures.

- Conducting regular scenario and stress testing.

- Establishing escalation protocols for breaches.

Practical Example: Managing Price Risk in Crude Oil Trading

A crude oil trading desk faces daily price swings driven by geopolitical events and supply disruptions. Without risk management, a sudden price drop could wipe out profits or cause losses.

Approach:

- The desk sets a maximum daily loss limit of $500,000.

- Uses futures contracts to hedge 60% of their open physical positions.

- Implements daily Value at Risk (VaR) reporting to track exposure.

- Conducts weekly stress tests simulating a 10% price drop.

Outcome:

- The hedging program reduces the impact of adverse price moves.

- Early detection of risk limit breaches allows timely trade adjustments.

- The firm avoids unexpected losses and maintains stable cash flows.

Mind Map: Risk Management Benefits Illustrated by the Example

Summary

Risk management in commodity trading acts as a shield against the inherent uncertainties of the markets. It enables traders and risk managers to anticipate, measure, and mitigate risks proactively rather than reactively. By embedding robust risk management practices, firms not only protect their financial health but also position themselves to capitalize on market opportunities with confidence and resilience.

1.4 Best Practices in Setting Up a Risk Management Framework

Setting up a robust risk management framework is essential for commodity traders and risk managers to effectively identify, assess, monitor, and mitigate risks inherent in commodity trading. This section outlines best practices, supported by clear examples and mind maps to help visualize the process.

Key Components of a Risk Management Framework

A comprehensive risk management framework typically includes the following components:

- Risk Identification

- Risk Assessment and Measurement

- Risk Mitigation and Controls

- Risk Monitoring and Reporting

- Governance and Compliance

Below is a mind map illustrating these components:

Risk Management Framework Mind Map

Best Practice 1: Establish Clear Risk Appetite and Limits

Description: Define the organization’s risk appetite clearly to guide decision-making. Set quantitative limits for different risk types (e.g., maximum Value at Risk (VaR), credit exposure limits).

Example: A commodity trading firm sets a daily VaR limit of $1 million for its crude oil portfolio. If the VaR breaches this limit, trading activities are paused until risk mitigation actions are taken.

Best Practice 2: Implement Robust Risk Identification Processes

Description: Use a combination of quantitative tools and expert judgment to identify risks. Regularly update risk registers.

Example: A natural gas trading desk holds weekly risk review meetings where traders and risk managers discuss new market developments, potential operational risks, and counterparty credit exposures.

Best Practice 3: Use Quantitative and Qualitative Risk Assessment Methods

Description: Combine statistical models (VaR, stress tests) with qualitative assessments (expert opinions, scenario analysis) for a holistic view.

Example: The firm runs Monte Carlo simulations to estimate potential losses under normal market conditions and supplements this with scenario analysis for geopolitical events affecting oil supply.

Best Practice 4: Develop and Enforce Risk Mitigation Controls

Description: Deploy hedging strategies, set credit limits, and establish operational controls to reduce risk.

Example: To mitigate price risk, a metals trader uses futures contracts to hedge exposure. Credit limits are set per counterparty, and collateral agreements are enforced.

Best Practice 5: Continuous Risk Monitoring and Transparent Reporting

Description: Implement real-time risk monitoring systems and produce clear, actionable reports for stakeholders.

Example: A dashboard provides intraday updates on portfolio risk metrics, and daily reports highlight limit breaches and exceptions for senior management review.

Best Practice 6: Strong Governance and Compliance Framework

Description: Establish risk committees, define roles and responsibilities, and ensure compliance with regulations.

Example: A risk committee meets monthly to review risk exposures, approve limits, and oversee adherence to regulatory requirements such as EMIR or Dodd-Frank.

Integrated Mind Map: End-to-End Risk Management Framework with Examples

Summary

Setting up a risk management framework requires a structured approach combining clear policies, quantitative and qualitative tools, and strong governance. By following these best practices and continuously refining the framework with real-world examples, commodity traders and risk managers can effectively safeguard their portfolios against diverse risks.

1.5 Practical Example: Identifying and Categorizing Risks in a Crude Oil Trading Desk

In this section, we will explore how a crude oil trading desk identifies and categorizes the various risks it faces. Understanding these risks is fundamental to building an effective risk management framework.

Step 1: Overview of the Crude Oil Trading Desk

A crude oil trading desk typically engages in buying and selling physical crude oil and related derivatives such as futures, options, and swaps. The desk is exposed to multiple risk types that can impact profitability and operational stability.

Step 2: Identifying Key Risk Categories

The primary risk categories for a crude oil trading desk include:

- Market Risk: Price fluctuations in crude oil and related products.

- Credit Risk: Counterparty default risk.

- Operational Risk: Failures in processes, systems, or human errors.

- Liquidity Risk: Inability to enter or exit positions without significant cost.

- Legal and Regulatory Risk: Compliance with laws and regulations.

Step 3: Mind Map of Risk Categories

Step 4: Detailed Examples of Each Risk with Categorization

Market Risk

- Price Risk: The price of Brent crude oil drops unexpectedly due to geopolitical tensions easing.

- Example: The desk holds a long position in Brent futures; a price drop leads to mark-to-market losses.

- Basis Risk: The price difference between WTI and Brent crude widens unexpectedly.

- Example: The desk hedges WTI exposure using Brent futures, but the spread widens, causing imperfect hedge results.

Credit Risk

- Counterparty Default: A counterparty fails to deliver crude oil after the contract settlement date.

- Example: A physical supplier defaults, forcing the desk to buy oil at a higher spot price.

- Settlement Risk: Delay in payment or delivery from counterparties.

Operational Risk

- Trade Capture Errors: Incorrect data entry leads to wrong position reporting.

- Example: A trader enters a buy order for 10,000 barrels but mistakenly inputs 100,000 barrels.

- System Failures: Trading platform outage during volatile market conditions.

Liquidity Risk

- Market Liquidity: Difficulty in selling large crude oil futures positions without impacting price.

- Funding Liquidity: Insufficient cash or credit lines to meet margin calls.

Legal & Regulatory Risk

- Contractual Disputes: Ambiguities in delivery terms leading to disputes.

- Regulatory Compliance: Failure to comply with position limits or reporting requirements.

Step 5: Mind Map of Market Risk Subcategories with Examples

Step 6: Integrating Risk Identification into Daily Workflow

- Pre-Trade Analysis: Assess market conditions and counterparty creditworthiness.

- Real-Time Monitoring: Use risk dashboards to track exposures and P&L.

- Post-Trade Review: Confirm trade capture accuracy and compliance.

Step 7: Summary Table of Risks and Mitigation Approaches

| Risk Category | Description | Example Scenario | Mitigation Practice |

|---|---|---|---|

| Market Risk | Price and volatility fluctuations | Brent price drop impacting long futures | Use stop-loss orders, diversify hedges |

| Credit Risk | Counterparty default or settlement delays | Supplier fails to deliver crude oil | Perform credit checks, collateral agreements |

| Operational Risk | Errors in trade capture, system outages | Incorrect trade quantity entered | Implement trade validation, system backups |

| Liquidity Risk | Difficulty in executing large trades | Unable to exit large futures position quickly | Use limit orders, maintain cash reserves |

| Legal & Regulatory | Contract disputes and compliance failures | Breach of position limits | Regular legal reviews, compliance training |

This practical example illustrates how a crude oil trading desk systematically identifies and categorizes risks, supported by clear examples and mind maps to enhance understanding. This foundation enables the desk to apply targeted risk management strategies effectively.

2. Fundamentals of Derivatives in Commodity Markets

2.1 Types of Commodity Derivatives: Futures, Options, Swaps, and Forwards

Commodity derivatives are financial instruments whose value is derived from the price of an underlying commodity. They are essential tools for managing price risk in commodity trading. This section explores the four primary types of commodity derivatives — Futures, Options, Swaps, and Forwards — with clear explanations, mind maps, and practical examples.

Futures Contracts

Definition: A futures contract is a standardized agreement traded on an exchange to buy or sell a specific quantity of a commodity at a predetermined price on a specified future date.

Key Characteristics:

- Standardized terms (quantity, quality, delivery date)

- Traded on regulated exchanges (e.g., CME, ICE)

- Marked-to-market daily

- Requires margin deposits

Mind Map:

Example: A wheat farmer expects to harvest 10,000 bushels in 3 months. To lock in the selling price and protect against price drops, the farmer sells wheat futures contracts today at $6.00 per bushel. If the market price falls to $5.50 at harvest, the farmer still sells at $6.00 via the futures contract, effectively hedging the price risk.

Options Contracts

Definition: An option gives the buyer the right, but not the obligation, to buy (call option) or sell (put option) a commodity at a specified strike price before or on a certain expiration date.

Key Characteristics:

- Right without obligation

- Premium paid upfront

- Can be American (exercise anytime before expiry) or European (exercise only at expiry)

Mind Map:

Example: An oil refiner worried about rising crude oil prices buys call options with a strike price of $70/barrel, paying a premium of $2/barrel. If prices rise to $80, the refiner can exercise the option to buy at $70, saving $8/barrel (minus premium). If prices stay below $70, the refiner lets the option expire, losing only the premium.

Swaps

Definition: A commodity swap is a private agreement between two parties to exchange cash flows based on the price of a commodity over a specified period.

Key Characteristics:

- Over-the-counter (OTC) contract

- Customized terms

- Typically involves exchanging fixed price payments for floating price payments

Mind Map:

Example: A power company wants to stabilize fuel costs. It enters a swap agreement to pay a fixed price of $50 per MMBtu of natural gas while receiving payments based on the floating market price. If market prices rise above $50, the company benefits by paying only the fixed price, effectively hedging against price spikes.

Forwards

Definition: A forward contract is a customized agreement between two parties to buy or sell a commodity at a specified price on a future date. Unlike futures, forwards are OTC contracts and are not standardized or exchange-traded.

Key Characteristics:

- Customized terms (quantity, quality, delivery date)

- OTC trading

- Settlement at contract maturity

- Higher counterparty risk

Mind Map:

Example: A coffee importer agrees with a grower to buy 100,000 lbs of coffee beans in 6 months at $1.20 per lb. This forward contract locks in the price, protecting the importer from price increases and the grower from price decreases.

Summary Mind Map: Commodity Derivatives Overview

Best Practice: Choosing the Right Derivative

- Understand the specific risk exposure (price volatility, timing, quantity)

- Consider liquidity and market availability

- Evaluate counterparty risk (exchange-traded vs OTC)

- Match derivative terms closely with underlying exposure to minimize basis risk

By mastering these four types of commodity derivatives and their applications, traders and risk managers can effectively design hedging strategies tailored to their unique risk profiles.

2.2 Pricing Basics and Market Conventions

Understanding pricing basics and market conventions is fundamental for effective commodity trading and risk management. This section breaks down key concepts, pricing mechanisms, and standard market practices with clear examples and mind maps to facilitate comprehension.

Pricing Basics in Commodity Markets

Commodity prices are influenced by supply and demand dynamics, geopolitical factors, weather conditions, and market sentiment. Pricing in commodity derivatives markets typically revolves around the spot price, futures price, and the concept of cost of carry.

Key Pricing Terms:

- Spot Price: The current market price for immediate delivery of the commodity.

- Futures Price: The agreed price today for delivery of the commodity at a future date.

- Cost of Carry: The cost associated with holding the physical commodity until the futures contract delivery date, including storage, insurance, and financing costs.

- Contango: A market condition where futures prices are higher than the spot price.

- Backwardation: A market condition where futures prices are lower than the spot price.

Mind Map: Pricing Basics

Market Conventions in Commodity Pricing

Market conventions standardize how prices and contracts are quoted, traded, and settled. These conventions vary by commodity and exchange but generally cover contract size, tick size, delivery terms, and trading hours.

Common Market Conventions:

- Contract Size: Standardized quantity of the commodity per contract (e.g., 1,000 barrels for crude oil futures).

- Tick Size: Minimum price fluctuation allowed (e.g., $0.01 per barrel).

- Delivery Terms: Specifications on quality, location, and timing for physical delivery.

- Trading Hours: Defined periods when contracts can be traded.

Mind Map: Market Conventions

Pricing Formula: Futures Price and Cost of Carry Model

The futures price can be derived from the spot price using the cost of carry model:

\[ F = S \times e^{(r + c - y) \times T} \]

Where:

- \(F\) = Futures price

- \(S\) = Spot price

- \(r\) = Risk-free interest rate

- \(c\) = Storage cost rate

- \(y\) = Convenience yield (benefit of holding the physical commodity)

- \(T\) = Time to maturity (in years)

Example:

Suppose the spot price of gold is $1,800 per ounce, the risk-free rate is 2% annually, storage costs are 0.5% annually, convenience yield is 0.3%, and the futures contract expires in 6 months (0.5 years).

Calculate the futures price:

\[ F = 1800 \times e^{(0.02 + 0.005 - 0.003) \times 0.5} = 1800 \times e^{0.011} \approx 1800 \times 1.0111 = 1819.98 \]

So, the futures price is approximately $1,820 per ounce.

Example: Pricing a Crude Oil Futures Contract

- Spot price of crude oil: $70 per barrel

- Risk-free rate: 3% per annum

- Storage cost: 1% per annum

- Convenience yield: 0.5% per annum

- Time to maturity: 3 months (0.25 years)

Calculate the futures price:

\[ F = 70 \times e^{(0.03 + 0.01 - 0.005) \times 0.25} = 70 \times e^{0.00875} \approx 70 \times 1.00879 = 70.62 \]

The futures price is approximately $70.62 per barrel.

Practical Considerations

- Impact of Convenience Yield: Commodities with high convenience yields (e.g., agricultural products during harvest) often exhibit backwardation.

- Seasonality: Many commodities have seasonal price patterns affecting futures pricing.

- Exchange-Specific Conventions: Always verify contract specifications on the exchange website (e.g., CME, ICE).

Summary Mind Map: Pricing and Market Conventions Overview

By mastering these pricing basics and market conventions, commodity traders and risk managers can better interpret market signals, price derivatives accurately, and design effective hedging strategies.

2.3 Role of Derivatives in Risk Mitigation

Derivatives are financial instruments whose value is derived from an underlying asset, such as commodities, currencies, or interest rates. In commodity trading, derivatives play a crucial role in managing and mitigating various types of risks, primarily price volatility risk. By using derivatives, traders and risk managers can hedge exposures, lock in prices, and stabilize cash flows, thereby reducing uncertainty and potential losses.

Mind Map: Role of Derivatives in Risk Mitigation

Key Functions of Derivatives in Risk Mitigation

-

Price Risk Management

- Commodity prices are highly volatile due to supply-demand imbalances, geopolitical events, weather conditions, and other factors.

- Derivatives allow traders to lock in prices or set price floors/ceilings to protect against unfavorable price movements.

-

Hedging Strategies

- Derivatives enable the creation of hedging positions that offset the risk of the underlying commodity exposure.

- Examples include perfect hedges (using the exact underlying asset), cross hedges (using a related asset), and dynamic hedges (adjusting hedge ratios over time).

-

Risk Transfer

- Derivatives facilitate transferring risk from one party to another willing to bear it, often for a premium (e.g., option premiums).

-

Liquidity Management

- Futures and options markets provide liquidity, allowing traders to enter and exit positions efficiently without impacting the physical market.

-

Speculation vs Hedging

- While derivatives can be used for speculation, their primary risk management role is to hedge exposures and stabilize financial outcomes.

Practical Examples

Example 1: Hedging with Futures Contracts

A crude oil refiner expects to purchase 100,000 barrels of crude oil in three months. Concerned about rising prices, the refiner sells crude oil futures contracts today to lock in the current price.

- If prices rise, losses on the physical purchase are offset by gains on the futures contracts.

- If prices fall, the refiner pays more on the futures contracts but benefits from lower physical prices.

This hedge reduces price uncertainty and stabilizes budgeting.

Example 2: Using Options for Price Protection

A wheat farmer wants to protect against a price drop but also wants to benefit if prices rise.

- The farmer buys put options on wheat futures, which give the right to sell at a strike price.

- If prices fall below the strike, the farmer exercises the option, limiting downside.

- If prices rise, the farmer lets the option expire and sells at the higher market price.

This strategy provides asymmetric protection.

Example 3: Cross-Hedging with Related Commodities

A trader holds exposure to a rare metal with no active futures market but a correlated base metal futures market exists.

- The trader uses futures on the base metal to hedge price risk, accepting some basis risk.

This approach mitigates risk when direct hedging instruments are unavailable.

Mind Map: Example of Hedging with Futures

Summary

Derivatives are indispensable tools in commodity trading risk management. They provide mechanisms to mitigate price volatility, transfer risk, and enhance liquidity. By carefully selecting and applying derivatives, traders and risk managers can protect their portfolios, optimize cash flows, and improve financial stability in uncertain markets.

2.4 Best Practice: Selecting the Appropriate Derivative Instrument for Specific Commodity Risks

Selecting the right derivative instrument is crucial for effectively managing commodity risks. Each derivative type—futures, options, swaps, and forwards—has unique characteristics that make it suitable for different risk profiles and trading objectives. This section provides a structured approach to choosing the appropriate derivative instrument, supported by mind maps and practical examples.

Understanding Commodity Risks and Derivative Instruments

Before selecting a derivative, it is essential to understand the nature of the commodity risk you face:

- Price Risk: Exposure to adverse price movements.

- Basis Risk: Risk arising from imperfect correlation between the hedged item and the derivative.

- Volatility Risk: Risk related to fluctuations in price volatility.

- Liquidity Risk: Risk of not being able to enter or exit positions easily.

Each derivative instrument offers different ways to mitigate these risks.

Mind Map: Derivative Instrument Selection Based on Risk Type

Mind Map: Decision Flow for Selecting Derivative Instruments

Practical Examples

Example 1: Hedging Wheat Price Exposure with Futures

A grain trader expects to sell 10,000 bushels of wheat in three months. The trader is exposed to price risk and wants a straightforward hedge.

- Instrument Chosen: Wheat futures contract on the Chicago Board of Trade (CBOT).

- Reason: Futures are standardized, highly liquid, and allow locking in a price.

- Outcome: The trader sells futures contracts equivalent to 10,000 bushels, offsetting price risk.

Example 2: Protecting Against Oil Price Spike Using Options

An airline company wants to protect against rising jet fuel prices but still benefit if prices fall.

- Instrument Chosen: Call options on crude oil futures.

- Reason: Options provide the right to buy at a strike price, limiting upside cost while retaining downside benefit.

- Outcome: The airline pays a premium for call options, capping fuel costs without losing potential savings.

Example 3: Managing Long-Term Natural Gas Price Exposure with Swaps

A utility company has a 2-year natural gas supply contract with variable pricing.

- Instrument Chosen: Natural gas price swap.

- Reason: Swaps allow fixing the price over the contract period, providing cash flow certainty.

- Outcome: The utility pays a fixed price and receives floating market prices, stabilizing costs.

Example 4: Custom Forward Contract for Specialty Metal Delivery

A manufacturer requires a specific grade of rare metal delivered in six months.

- Instrument Chosen: Forward contract negotiated OTC.

- Reason: Futures markets do not exist for this metal; forwards allow customization of quantity, quality, and delivery.

- Outcome: The manufacturer locks in price and delivery terms, mitigating price and supply risks.

Summary Best Practices

- Match instrument to risk profile: Use futures for standardized, short-term price risk; options for asymmetric risk management; swaps and forwards for long-term or customized needs.

- Consider liquidity: Prefer exchange-traded instruments for liquidity; use OTC instruments when customization is essential.

- Evaluate cost vs protection: Options require premium payments but offer flexibility; futures and swaps have no upfront premium but may require margin.

- Monitor basis risk: When cross-hedging or using non-standard instruments, assess basis risk carefully.

By systematically analyzing the commodity risk and understanding the characteristics of each derivative instrument, traders and risk managers can select the most effective hedging tool to protect their portfolios.

2.5 Practical Example: Using Futures Contracts to Hedge Wheat Price Exposure

Introduction

Hedging wheat price exposure using futures contracts is a fundamental strategy employed by commodity traders and risk managers to mitigate the risk of adverse price movements. This example will walk through the process of setting up a hedge, calculating hedge ratios, and monitoring the position over time.

Step 1: Understanding the Exposure

A wheat farmer expects to harvest 10,000 bushels of wheat in 3 months. The current spot price is $6.00 per bushel, but the farmer fears that prices might decline by the time of harvest, which would reduce revenue.

Objective: Lock in a selling price today to protect against price drops.

Step 2: Selecting the Hedging Instrument

The farmer decides to use Chicago Board of Trade (CBOT) wheat futures contracts, each representing 5,000 bushels.

- Number of contracts needed = Exposure (bushels) / Contract size

- = 10,000 / 5,000 = 2 contracts

Step 3: Executing the Hedge

The farmer takes a short position in 2 wheat futures contracts at the current futures price of $6.05 per bushel (slightly above spot due to carry costs).

Mind Map: Hedging Wheat Price Exposure with Futures

Step 4: Price Movement and Hedge Outcome

Assume that at harvest, the spot price has dropped to $5.50 per bushel.

-

Without Hedge:

- Revenue = 10,000 bushels * $5.50 = $55,000

-

With Hedge:

- Loss on spot sale = (6.00 - 5.50) * 10,000 = $5,000 loss

- Gain on futures = (6.05 - 5.50) * 10,000 = $5,500 gain

- Net revenue = $60,500 (approximate, ignoring transaction costs)

The futures position offsets the loss in the physical market, effectively locking in a price close to $6.00 per bushel.

Step 5: Hedge Ratio and Basis Risk

In real scenarios, the hedge ratio may not be exactly 1 due to:

- Differences in contract size vs exposure

- Basis risk (difference between spot and futures prices at settlement)

Mind Map: Factors Affecting Hedge Effectiveness

Step 6: Adjusting the Hedge

If the farmer’s expected quantity changes or the harvest date shifts, the hedge position should be adjusted accordingly.

Example: If the farmer expects only 8,000 bushels, the hedge would be:

- 8,000 / 5,000 = 1.6 contracts

- Since partial contracts aren’t possible, the farmer may hedge 1 or 2 contracts and accept some residual risk.

Step 7: Monitoring and Closing the Hedge

As the harvest approaches, the farmer monitors the basis and futures prices.

-

At harvest, the farmer delivers the wheat and closes the futures position by buying back the contracts.

-

The combined cash flows from the physical sale and futures position realize the locked-in price.

Summary Mind Map: Futures Hedging Process

Additional Example: Hedging a Wheat Buyer

A food processing company expects to purchase 15,000 bushels of wheat in 4 months and fears price increases.

-

The company takes a long position in 3 CBOT wheat futures contracts (15,000 / 5,000).

-

If prices rise, gains on futures offset higher spot prices.

-

If prices fall, losses on futures are offset by cheaper physical purchases.

This demonstrates how futures contracts can hedge both short and long commodity exposures.

Conclusion

Using futures contracts to hedge wheat price exposure is a practical and effective risk management strategy. By understanding contract specifications, calculating appropriate hedge ratios, and monitoring basis risk, traders and risk managers can protect against unfavorable price movements while maintaining flexibility.

References

- CME Group CBOT Wheat Futures Specifications

- Hull, J. C. (2018). Options, Futures, and Other Derivatives.

- Commodity Markets Council: Hedging Best Practices

3. Advanced Hedging Strategies Using Commodity Derivatives

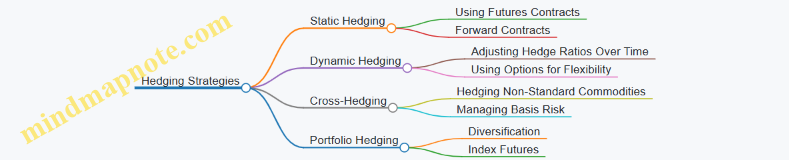

3.1 Static vs Dynamic Hedging: Concepts and Applications

Introduction

In commodity trading, hedging is a fundamental risk management technique used to protect against adverse price movements. Two primary hedging approaches are static hedging and dynamic hedging. Understanding their concepts, applications, and differences is crucial for traders and risk managers aiming to optimize risk mitigation strategies.

What is Static Hedging?

Static hedging involves establishing a hedge position that remains unchanged or fixed over the hedge horizon. Once the hedge is placed, it is not actively adjusted in response to market movements.

-

Key Characteristics:

- One-time hedge setup

- Minimal ongoing management

- Simplicity and lower transaction costs

-

When to Use:

- When the underlying exposure is stable

- When transaction costs are high

- When the hedge instrument closely matches the exposure

Example of Static Hedging:

A wheat farmer expects to sell 10,000 bushels in 6 months. To protect against price drops, the farmer sells wheat futures contracts now and holds them until delivery. No adjustments are made regardless of price fluctuations.

What is Dynamic Hedging?

Dynamic hedging involves continuously adjusting the hedge position in response to changes in market conditions, underlying exposure, or risk parameters.

-

Key Characteristics:

- Frequent rebalancing of hedge positions

- More complex and resource-intensive

- Better risk alignment in volatile markets

-

When to Use:

- When exposure or market conditions are volatile

- When the hedge instrument is imperfect or the underlying exposure changes

- When managing options or nonlinear risks

Example of Dynamic Hedging:

An energy trader holds options on crude oil. Since option delta changes with price and time, the trader continuously buys or sells futures contracts to maintain a delta-neutral position, adjusting the hedge as market prices move.

Mind Map: Static vs Dynamic Hedging Overview

Mind Map: Applications and Considerations

Practical Example: Comparing Static and Dynamic Hedging for Natural Gas Exposure

Scenario: A utility company expects to consume 1 million MMBtu of natural gas over the next 3 months. The company wants to hedge price risk.

-

Static Hedge Approach:

- The company sells futures contracts covering 1 million MMBtu at current prices.

- The hedge remains unchanged regardless of consumption variations or price movements.

- Pros: Simple, low cost.

- Cons: If consumption changes or prices move significantly, the hedge may become ineffective.

-

Dynamic Hedge Approach:

- The company adjusts futures positions weekly based on updated consumption forecasts and market prices.

- If consumption is lower than expected, futures are bought back; if higher, more futures are sold.

- Pros: More precise risk management.

- Cons: Increased transaction costs and operational complexity.

Best Practices for Choosing Between Static and Dynamic Hedging

- Assess the volatility and predictability of the underlying exposure.

- Evaluate transaction costs and operational capabilities.

- Consider the complexity of the derivative instruments involved.

- Use static hedging for straightforward, stable exposures.

- Employ dynamic hedging for options or when exposures are uncertain or highly volatile.

Summary

| Aspect | Static Hedging | Dynamic Hedging |

|---|---|---|

| Hedge Adjustment | None after initial setup | Continuous or periodic adjustments |

| Complexity | Low | High |

| Transaction Costs | Lower | Higher |

| Suitability | Stable, predictable exposures | Volatile, nonlinear exposures |

| Risk Mitigation | Basic, may leave residual risk | More precise, reduces residual risk |

Understanding these approaches and their appropriate applications enables commodity traders and risk managers to tailor hedging strategies that best fit their risk profiles and market conditions.

3.2 Cross-Hedging Techniques for Non-Standard Commodities

Cross-hedging is a powerful risk management technique used when direct hedging instruments for a specific commodity are unavailable, illiquid, or too costly. It involves using derivatives of a related but different commodity to hedge price risk. This technique is especially relevant for non-standard commodities—those that may not have active futures markets or standardized contracts.

What is Cross-Hedging?

Cross-hedging is the practice of hedging a commodity exposure by taking a position in a different but correlated commodity’s derivative. The goal is to reduce price risk by leveraging the price relationship between the two commodities.

Key Points:

- Used when direct hedging instruments are unavailable or inefficient.

- Relies on correlation between the commodity to be hedged and the hedging instrument.

- Basis risk (the risk that the hedge does not perfectly offset the exposure) is a critical consideration.

Mind Map: Cross-Hedging Overview

Selecting a Proxy Commodity for Cross-Hedging

The effectiveness of cross-hedging depends largely on the selection of an appropriate proxy commodity. This involves:

- Correlation Analysis: Statistical measurement of price movements between the target commodity and potential proxies.

- Fundamental Linkages: Supply chain relationships, substitution effects, or shared demand drivers.

- Liquidity and Market Depth: The proxy should have a liquid derivatives market.

Mind Map: Proxy Commodity Selection

Practical Example 1: Cross-Hedging Rare Earth Metals with More Liquid Base Metals

Scenario: A trader holds exposure to a rare earth metal (e.g., Neodymium) which lacks a liquid futures market.

Approach: Use futures contracts on a more liquid base metal like Copper or Aluminum as a proxy hedge.

Steps:

- Analyze historical price correlation between Neodymium and Copper.

- Determine hedge ratio based on volatility and correlation.

- Enter a short futures position in Copper to offset price risk in Neodymium holdings.

- Monitor basis risk and adjust hedge dynamically.

Example Calculation:

- Neodymium price volatility: 30%

- Copper price volatility: 20%

- Correlation coefficient: 0.75

Hedge ratio = (Volatility of Neodymium / Volatility of Copper) * Correlation = (0.30 / 0.20) * 0.75 = 1.125

This means for every 1 unit exposure in Neodymium, the trader takes a 1.125 unit position in Copper futures.

Practical Example 2: Cross-Hedging Specialty Agricultural Products Using Corn or Soybean Futures

Scenario: A risk manager for a company trading specialty grains like millet or sorghum needs to hedge price risk but finds no direct futures contracts.

Approach: Use corn or soybean futures as proxies due to similar growing conditions and overlapping demand.

Steps:

- Conduct correlation and regression analysis between millet/sorghum prices and corn/soybean prices.

- Calculate optimal hedge ratio.

- Implement hedge using futures or options on corn or soybeans.

- Continuously monitor and rebalance hedge positions.

Mind Map: Cross-Hedging Process

Managing Basis Risk in Cross-Hedging

Basis risk arises because the proxy commodity’s price movements do not perfectly offset the target commodity’s price changes. To manage basis risk:

- Regularly update correlation and hedge ratios to reflect current market conditions.

- Use dynamic hedging strategies that adjust positions as relationships evolve.

- Combine multiple proxies if appropriate to better capture price movements.

- Incorporate scenario and stress testing to understand potential hedge performance under different market conditions.

Best Practices for Cross-Hedging

- Perform thorough quantitative and qualitative analysis before selecting proxy instruments.

- Maintain ongoing monitoring of correlation and basis risk.

- Use a combination of derivatives (futures, options) to tailor risk profiles.

- Educate trading and risk teams on the nuances and limitations of cross-hedging.

- Document hedge rationale and assumptions clearly for audit and compliance.

Summary

Cross-hedging is an essential strategy for managing price risk in non-standard commodities where direct hedging instruments are unavailable. By carefully selecting proxy commodities based on correlation and fundamental linkages, calculating appropriate hedge ratios, and actively managing basis risk, commodity traders and risk managers can effectively reduce exposure and improve portfolio stability.

Additional Resources

- Hull, J. C. (2018). Options, Futures, and Other Derivatives. Pearson.

- Geman, H. (2005). Commodities and Commodity Derivatives: Modeling and Pricing for Agriculturals, Metals and Energy. Wiley.

- CME Group: Educational materials on commodity futures and options.

3.3 Basis Risk Management and Minimization Strategies

Introduction to Basis Risk

Basis risk arises when the price of a hedging instrument (usually a futures contract) does not move perfectly in line with the price of the underlying physical commodity or exposure being hedged. This imperfect correlation creates residual risk even after hedging, known as basis risk.

Why Basis Risk Matters:

- It can lead to unexpected gains or losses despite a hedge.

- It affects the effectiveness of hedging strategies.

- Managing basis risk is critical for accurate risk control and profit stability.

Mind Map: Understanding Basis Risk

Sources of Basis Risk

- Location Differences: Physical commodity prices vary by delivery location, while futures contracts are tied to specific delivery points.

- Quality Differences: The physical commodity may differ in grade or quality from the standardized futures contract.

- Timing Differences: Mismatches between the timing of the physical transaction and futures contract expiration.

- Contract Specifications: Variations in contract size, delivery terms, or settlement methods.

Measuring Basis Risk

- Historical Basis Analysis: Calculate the difference between spot price and futures price over time to understand typical basis behavior.

- Correlation Coefficient: Statistical measure of how closely the futures price moves with the spot price.

- Basis Volatility: Standard deviation of the basis over a given period.

Mind Map: Basis Risk Measurement Techniques

Strategies to Manage and Minimize Basis Risk

Selecting the Most Appropriate Futures Contract

- Choose contracts with delivery locations and specifications closely matching the physical exposure.

- Example: A natural gas trader in Henry Hub region should use Henry Hub futures rather than a distant hub.

Using Basis Contracts or Swaps

- Instruments designed to hedge basis risk specifically, such as basis swaps that exchange floating basis for fixed.

- Example: An electricity producer hedges the difference between local spot prices and regional futures using basis swaps.

Cross-Hedging

- When no exact futures contract exists, hedge with a related commodity or contract with high correlation.

- Example: Hedging jet fuel exposure with crude oil futures, while monitoring basis risk closely.

Timing Alignment

- Match the hedge duration and delivery timing as closely as possible to the physical exposure.

- Rolling futures positions carefully to avoid gaps.

Dynamic Hedge Adjustments

- Continuously monitor basis and adjust hedge ratios or instruments accordingly.

- Use statistical models or AI tools to predict basis changes.

Geographical Arbitrage and Logistics Optimization

- Manage physical logistics to reduce location basis risk.

- Example: Adjusting delivery points or storage to align better with futures contract locations.

Mind Map: Basis Risk Minimization Strategies

Practical Examples

Example 1: Basis Risk in Wheat Hedging

- A grain trader in Kansas hedges wheat exposure using Chicago Board of Trade (CBOT) wheat futures.

- Basis risk arises because local Kansas wheat prices can differ from CBOT prices due to transportation costs and local demand.

- The trader monitors historical basis and adjusts hedge ratios monthly.

- Uses local cash market data to estimate basis trends and employs a partial hedge to balance risk and cost.

Example 2: Managing Basis Risk in Crude Oil

- An oil refiner hedges using NYMEX WTI futures but sources crude from a different region (e.g., Brent crude).

- The basis between Brent and WTI fluctuates due to regional supply-demand differences.

- The refiner uses a cross-hedge with Brent futures and applies a basis swap to manage residual risk.

- Regularly reviews correlation and basis volatility to adjust hedge strategy.

Example 3: Timing Basis Risk in Natural Gas

- A utility company hedges winter natural gas demand with futures contracts expiring in December.

- Actual consumption peaks in January and February, creating timing basis risk.

- The company staggers futures contracts across multiple months and uses storage options to align physical and financial exposures.

Best Practices Summary

- Always analyze and understand the sources of basis risk before implementing a hedge.

- Use historical data and statistical tools to quantify basis risk.

- Select hedging instruments that closely align with physical exposure in location, quality, and timing.

- Employ specialized instruments like basis swaps when available.

- Continuously monitor and adjust hedges dynamically.

- Integrate physical logistics considerations into risk management.

By mastering basis risk management and minimization strategies, commodity traders and risk managers can significantly enhance hedge effectiveness, reduce unexpected losses, and improve overall portfolio stability.

3.4 Best Practice: Constructing a Dynamic Hedge for Volatile Natural Gas Prices

Managing price volatility in natural gas markets requires a flexible and adaptive hedging strategy. A dynamic hedge adjusts the hedge ratio and instruments over time in response to market conditions, reducing risk exposure while optimizing cost efficiency.

Understanding Dynamic Hedging

Dynamic hedging involves continuously monitoring the natural gas price movements and adjusting the hedge position accordingly. Unlike static hedging, which sets a fixed hedge ratio for a period, dynamic hedging responds to price volatility, seasonality, and market liquidity.

Key Components of a Dynamic Hedge for Natural Gas

- Hedge Ratio Adjustment: Modifying the percentage of exposure hedged based on risk tolerance and market signals.

- Instrument Selection: Using a mix of futures, options, and swaps to tailor risk coverage.

- Rebalancing Frequency: Determining how often to review and adjust hedge positions.

- Market Indicators: Incorporating volatility indices, weather forecasts, and inventory reports.

Mind Map: Dynamic Hedging Framework for Natural Gas

Step-by-Step Example: Constructing a Dynamic Hedge

Scenario: A natural gas trading desk has an exposure of 10,000 MMBtu per month for the next 6 months. The market is highly volatile due to unpredictable weather patterns.

-

Initial Hedge Setup:

- Hedge 70% of exposure using NYMEX natural gas futures for the next 3 months.

- Buy call options to protect against price spikes for the remaining 30%.

-

Monitoring Market Volatility:

- Use the CBOE Natural Gas Volatility Index (NGVIX) to track market turbulence.

- When NGVIX rises above a threshold (e.g., 40%), increase hedge ratio to 85% by purchasing additional futures.

-

Adjusting for Weather Forecasts:

- If a cold snap is forecasted, increase call option positions to benefit from potential price spikes.

- If mild weather is expected, reduce hedge ratio to 60% to avoid over-hedging.

-

Rebalancing Frequency:

- Review hedge positions weekly.

- Adjust futures and options holdings based on updated market data and exposure changes.

-

Risk and Cost Optimization:

- Monitor margin requirements and liquidity to avoid excessive costs.

- Use options to cap downside risk while allowing upside participation.

Mind Map: Example Dynamic Hedge Adjustment Cycle

Practical Tips for Effective Dynamic Hedging

- Use Real-Time Data Feeds: Ensure access to up-to-date price, volatility, and weather data.

- Set Clear Thresholds: Define triggers for hedge adjustments to avoid emotional decision-making.

- Leverage Technology: Utilize risk management software for scenario analysis and automated alerts.

- Maintain Flexibility: Be prepared to shift between instruments as market conditions evolve.

- Document Decisions: Keep detailed records of hedge adjustments and rationale for audit and learning.

Summary

Constructing a dynamic hedge for volatile natural gas prices involves a continuous process of monitoring, analysis, and adjustment. By combining futures and options, leveraging market indicators like volatility indices and weather forecasts, and maintaining disciplined rebalancing, traders can effectively manage price risk while optimizing hedging costs.

This approach not only reduces unexpected losses but also provides opportunities to capitalize on favorable market movements, making it a best practice for natural gas risk management.

3.5 Practical Example: Cross-Hedging Aluminum Exposure with Copper Futures

Cross-hedging is a risk management strategy used when a direct hedge instrument is unavailable or illiquid. In commodity trading, this often occurs when the commodity you want to hedge (the exposure) does not have a liquid futures market or the futures contracts are too expensive or impractical to use. Instead, you use a related commodity’s futures contract to hedge your position.

Scenario Overview

Suppose you are a commodity trader with a significant exposure to aluminum prices, but the aluminum futures market is either illiquid or unavailable for your desired contract size or delivery location. Copper futures, on the other hand, are highly liquid and actively traded on major exchanges such as the COMEX.

You decide to use copper futures to hedge your aluminum price risk, leveraging the historical price correlation between aluminum and copper.

Step 1: Understanding the Relationship Between Aluminum and Copper

- Both aluminum and copper are base metals used extensively in industrial applications.

- Their prices often move in tandem due to similar demand drivers (e.g., construction, manufacturing) and supply factors.

- However, the correlation is not perfect, so basis risk exists.

Mind Map: Relationship Between Aluminum and Copper Prices

Step 2: Calculating the Hedge Ratio

The hedge ratio determines how many copper futures contracts you need to hedge your aluminum exposure effectively.

Formula:

\[ \text{Hedge Ratio} = \rho \times \frac{\sigma_{Al}}{\sigma_{Cu}} \]

Where:

- \(\rho\) = correlation coefficient between aluminum and copper prices

- \(\sigma_{Al}\) = standard deviation (volatility) of aluminum prices

- \(\sigma_{Cu}\) = standard deviation (volatility) of copper prices

Example Calculation:

- Correlation (\(\rho\)) = 0.75

- Aluminum volatility (\(\sigma_{Al}\)) = 4.5% monthly

- Copper volatility (\(\sigma_{Cu}\)) = 6.0% monthly

\[ \text{Hedge Ratio} = 0.75 \times \frac{4.5}{6.0} = 0.75 \times 0.75 = 0.5625 \]

This means for every 1 unit of aluminum exposure, you hedge approximately 0.56 units of copper futures.

Step 3: Determining the Number of Futures Contracts

Assume:

- Aluminum exposure: 100 metric tons

- Aluminum price: $2,000 per metric ton

- Copper futures contract size: 25 metric tons

- Copper futures price: $9,000 per metric ton

Calculate the dollar exposure:

- Aluminum exposure value = 100 tons * $2,000 = $200,000

Calculate the equivalent copper exposure using hedge ratio:

- Equivalent copper exposure = $200,000 * 0.5625 = $112,500

Calculate number of copper futures contracts:

-

One copper futures contract value = 25 tons * $9,000 = $225,000

-

Number of contracts = $112,500 / $225,000 = 0.5 contracts

Since you cannot trade half a contract, you round to the nearest whole number, usually rounding up to 1 contract for better risk coverage.

Step 4: Executing the Hedge

- Sell 1 copper futures contract to hedge the aluminum exposure.

- Monitor the hedge effectiveness regularly, adjusting the hedge ratio and number of contracts as market conditions and correlations change.

Step 5: Monitoring and Managing Basis Risk

Because aluminum and copper prices do not move perfectly together, there is residual risk (basis risk) after hedging.

Mind Map: Managing Basis Risk in Cross-Hedging

Summary Table

| Step | Action | Example Values |

|---|---|---|

| 1. Analyze correlation | Correlation between aluminum and copper | 0.75 |

| 2. Calculate hedge ratio | \(0.75 \times (4.5\% / 6.0\%) = 0.5625\) | 0.5625 |

| 3. Determine contracts | Aluminum exposure = $200,000 | Copper futures contract = $225,000 |

| Equivalent copper exposure = $112,500 | Number of contracts = 0.5 → 1 | |

| 4. Execute hedge | Sell 1 copper futures contract | Ongoing monitoring |

| 5. Manage basis risk | Regular updates and risk controls | Use regression and scenario tests |

Key Takeaways

- Cross-hedging allows risk mitigation when direct futures are unavailable or illiquid.

- Calculating an accurate hedge ratio based on correlation and volatility is critical.

- Basis risk is inherent and must be actively managed.

- Regular monitoring and adjustment ensure hedge effectiveness.

This practical example demonstrates how commodity traders and risk managers can apply cross-hedging with copper futures to manage aluminum price risk effectively, balancing liquidity and risk control.

4. Quantitative Risk Measurement and Analytics

4.1 Value at Risk (VaR) Models for Commodity Portfolios

Value at Risk (VaR) is a fundamental quantitative risk measurement tool widely used in commodity trading to estimate the potential loss in value of a portfolio over a defined period for a given confidence interval. It helps traders and risk managers understand the maximum expected loss under normal market conditions.

What is VaR?

- Definition: VaR answers the question: “What is the worst loss that can be expected over a given time horizon at a certain confidence level?”

- Example: A 1-day VaR of $1 million at 95% confidence means there is a 5% chance that losses will exceed $1 million in one day.

Key Components of VaR

Mind Map: Components of VaR

VaR Methodologies Explained

-

Parametric (Variance-Covariance) Method

- Assumes returns are normally distributed.

- Uses mean and variance-covariance matrix of returns.

- Fast and simple but may underestimate risk if returns are not normal.

-

Historical Simulation

- Uses actual historical returns to simulate portfolio losses.

- No assumption about return distribution.

- Dependent on the quality and length of historical data.

-

Monte Carlo Simulation

- Generates a large number of random price paths based on statistical models.

- Flexible and can incorporate complex risk factors.

- Computationally intensive.

Mind Map: VaR Methodologies

Example: Calculating Parametric VaR for a Crude Oil Portfolio

- Portfolio Value: $10 million

- Daily Return Mean: 0%

- Daily Return Std Dev: 2%

- Confidence Level: 95% (Z-score ≈ 1.65)

Calculation:

VaR = Portfolio Value × Z-score × Std Dev

VaR = $10,000,000 × 1.65 × 0.02 = $330,000

Interpretation: There is a 5% chance that the portfolio could lose more than $330,000 in one day.

Example: Historical Simulation VaR for a Wheat Trading Portfolio

- Collect last 250 trading days’ daily returns of wheat futures.

- Sort returns from worst to best.

- At 95% confidence, identify the 13th worst return (5% of 250).

- Suppose the 13th worst return is -3.5%.

- Portfolio Value: $5 million

VaR = 3.5% × $5,000,000 = $175,000

Interpretation: Based on historical data, there is a 5% chance the portfolio could lose more than $175,000 in one day.

Best Practices for VaR in Commodity Portfolios

- Use multiple VaR methodologies to cross-validate risk estimates.

- Incorporate stress testing alongside VaR to capture extreme events.

- Regularly update input data and parameters to reflect current market conditions.

- Adjust for non-normality and fat tails in commodity price returns.

- Combine VaR with other risk metrics like Expected Shortfall for a fuller picture.

Mind Map: Best Practices for VaR

Summary

Value at Risk is a powerful tool for quantifying potential losses in commodity portfolios. Understanding its methodologies, assumptions, and limitations is crucial for effective risk management. By integrating VaR with practical examples and best practices, commodity traders and risk managers can better prepare for market uncertainties and make informed hedging decisions.

4.2 Stress Testing and Scenario Analysis in Commodity Trading

Stress testing and scenario analysis are critical tools in commodity trading risk management. They help traders and risk managers understand how extreme but plausible events could impact their portfolios, enabling proactive mitigation strategies.

What is Stress Testing?

Stress testing involves applying hypothetical or historical extreme market conditions to a commodity portfolio to evaluate potential losses beyond normal market fluctuations.

- Purpose: Identify vulnerabilities under adverse conditions.

- Scope: Can be applied to price shocks, volatility spikes, liquidity crunches, or operational disruptions.

What is Scenario Analysis?

Scenario analysis examines the impact of specific, often complex, events or combinations of events on a portfolio.

- Purpose: Understand the effects of multi-factor events.

- Scope: Includes geopolitical crises, regulatory changes, supply chain disruptions, or demand shocks.

Mind Map: Stress Testing Framework in Commodity Trading

Mind Map: Scenario Analysis Examples

Best Practices for Stress Testing and Scenario Analysis

- Use Multiple Scenarios: Combine historical shocks with hypothetical events to cover a wide risk spectrum.

- Incorporate Correlations: Account for how commodity prices and related risk factors move together under stress.

- Regular Updates: Refresh scenarios frequently to reflect evolving market conditions and emerging risks.

- Integrate with Risk Limits: Use stress test results to adjust trading limits and hedging strategies.

- Communicate Clearly: Present findings in an understandable format for decision-makers.

Practical Example 1: Stress Testing a Crude Oil Portfolio

Context: A trading desk holds a diversified crude oil portfolio including futures, options, and swaps.

Stress Test Scenario: Sudden 30% drop in Brent crude prices within one week due to unexpected global demand slowdown.

Steps:

- Reprice all instruments using the shocked price.

- Calculate portfolio loss.

- Assess impact on margin requirements and liquidity.

Outcome: The portfolio shows a potential loss of $15 million, exceeding the desk’s risk limit.

Action: Increase hedging using put options and reduce open positions.

Practical Example 2: Scenario Analysis for Agricultural Commodities

Scenario: Severe drought in a major wheat-producing region combined with a trade embargo on exports.

Impact Analysis:

- Wheat prices spike by 40% due to supply shortage.

- Corn and soy prices increase due to substitution effects.

- Currency depreciation in importing countries affects demand.

Portfolio Effect: Long positions in wheat futures gain value, but short positions in corn suffer losses.

Risk Management Response: Adjust portfolio to reduce exposure to correlated commodities and increase monitoring of geopolitical developments.

Visualizing Scenario Impact: Mind Map

Summary

Stress testing and scenario analysis provide commodity traders and risk managers with a structured approach to anticipate and prepare for extreme market events. By combining quantitative rigor with practical examples, these techniques enhance resilience and support informed decision-making.

4.3 Greeks and Sensitivity Analysis for Commodity Options

Understanding the Greeks is essential for effective risk management and hedging in commodity options trading. The Greeks measure the sensitivity of an option’s price to various factors such as changes in the underlying commodity price, volatility, time decay, and interest rates. This section delves into the key Greeks relevant to commodity options and demonstrates how sensitivity analysis can be applied to manage risk.

Key Greeks in Commodity Options

- Delta (Δ): Measures the rate of change of the option price with respect to changes in the underlying commodity price.

- Gamma (Γ): Measures the rate of change of Delta with respect to changes in the underlying price; indicates convexity.

- Vega (ν): Measures sensitivity of the option price to changes in the volatility of the underlying commodity.

- Theta (Θ): Measures the sensitivity of the option price to the passage of time (time decay).

- Rho (ρ): Measures sensitivity to changes in the risk-free interest rate.

Mind Map: Overview of Greeks

Practical Example 1: Calculating Delta for a Crude Oil Call Option

Suppose you hold a call option on crude oil with the following parameters:

- Current crude oil price: $70/barrel

- Strike price: $75

- Time to expiration: 30 days

- Volatility: 25%

- Risk-free rate: 2%

Using an option pricing model (e.g., Black-Scholes adapted for commodities), you calculate Delta to be approximately 0.35. This means that for every $1 increase in crude oil price, the option price increases by $0.35.

Interpretation: If crude oil price rises from $70 to $71, the option price should increase by roughly $0.35, all else equal.

Mind Map: Delta and Gamma Relationship

Practical Example 2: Using Gamma to Adjust Hedging

Continuing the crude oil option example, suppose Gamma is 0.05. If the underlying price moves from $70 to $71, Delta will increase from 0.35 to approximately 0.40 (0.35 + 0.05). This means your hedge ratio needs to be adjusted to maintain a delta-neutral position.

Vega and Volatility Sensitivity

Volatility is a critical factor in commodity options pricing due to the often volatile nature of commodity markets.

- Vega is highest for at-the-money options and decreases as options move in- or out-of-the-money.

- A rise in implied volatility increases option premiums.

Practical Example 3: Vega Impact on Natural Gas Option

Consider a natural gas call option with a Vega of 0.12. If implied volatility rises from 30% to 35%, the option price increases by approximately 0.12 * 5 = $0.60.

Mind Map: Vega and Volatility

Theta and Time Decay

Options lose value as expiration approaches, all else equal. Theta quantifies this time decay.

- Theta is generally negative for long options.

- Time decay accelerates as expiration nears.

Practical Example 4: Theta Effect on Corn Option

A long call option on corn has a Theta of -0.03. This means the option loses $0.03 in value each day, assuming no change in other factors.

Mind Map: Theta and Time Decay

Rho and Interest Rate Sensitivity

Rho measures sensitivity to interest rate changes but is generally less impactful in commodity options compared to equity options.

Integrated Sensitivity Analysis Example

Imagine a portfolio holding multiple commodity options on gold and oil. By calculating the Greeks for each option, the risk manager can:

- Use Delta to hedge directional price risk.

- Monitor Gamma to understand how hedge ratios will change with price movements.

- Use Vega to assess exposure to volatility spikes, especially during geopolitical events.

- Track Theta to manage time decay, deciding when to roll or close positions.

Best Practice: Using Greeks for Dynamic Hedging

- Regularly compute Greeks for all option positions.

- Adjust hedge ratios dynamically based on Gamma and Delta changes.

- Monitor Vega to protect against volatility risk.

- Factor in Theta to avoid unexpected erosion of option value.

Summary

Greeks provide a powerful toolkit for measuring and managing the sensitivities of commodity options. By integrating Greeks into daily risk management and hedging strategies, commodity traders and risk managers can better anticipate price movements, volatility changes, and time decay effects, leading to more effective risk mitigation and optimized portfolio performance.

4.4 Best Practice: Integrating VaR and Stress Testing into Daily Risk Reporting

Effective risk management in commodity trading hinges on timely, accurate, and comprehensive risk reporting. Integrating Value at Risk (VaR) and stress testing into daily risk reports empowers traders and risk managers to understand potential losses under normal and extreme market conditions, enabling proactive decision-making.

Why Integrate VaR and Stress Testing Daily?

- Real-time risk visibility: Daily updates provide a current snapshot of portfolio risk.

- Early warning signals: Detect emerging vulnerabilities before losses materialize.

- Regulatory compliance: Many regulators require regular risk reporting.

- Informed hedging decisions: Helps optimize hedging strategies based on risk exposure.

Key Components of Daily Risk Reporting with VaR and Stress Testing

Step-by-Step Implementation Example

Scenario: A natural gas trading desk wants to integrate VaR and stress testing into its daily risk report.

-

Calculate Daily VaR:

- Use a 99% confidence level and 1-day horizon.

- Apply historical simulation using 1-year price data.

- Result: VaR = $2 million loss potential.

-

Perform Stress Tests:

- Historical scenario: 2008 natural gas price spike.

- Hypothetical scenario: sudden 20% price drop due to geopolitical event.

- Result: Potential losses of $5 million and $3.5 million respectively.

-

Create Risk Dashboard:

- Display VaR and stress test results side-by-side.

- Show current exposure vs. risk limits.

- Include trend charts of VaR over past 30 days.

-

Distribute Report:

- Automated email to traders, risk managers, and senior management.

- Upload to risk management system for audit trail.

Mind Map: Daily Risk Reporting Workflow

Practical Tips for Best Practice Implementation

- Automate data feeds: Ensure market data and positions update in real-time to avoid stale inputs.

- Standardize scenarios: Use a consistent set of stress scenarios relevant to your commodity portfolio.

- Visualize effectively: Use charts and heatmaps to highlight risk concentrations and trends.

- Set thresholds and alerts: Trigger notifications when VaR or stress losses approach risk limits.

- Document assumptions: Clearly state models, confidence levels, and scenario rationales in reports.

- Regularly validate models: Backtest VaR and review stress scenarios for relevance.

Example Visualization Ideas

- VaR Trend Chart: Line chart showing daily VaR over the past month.

- Stress Test Impact Table: Tabular display of scenario names and corresponding loss estimates.

- Risk Limit Gauge: Dial or bar showing current VaR as a percentage of the risk limit.

Summary

Integrating VaR and stress testing into daily risk reporting creates a robust framework for monitoring commodity trading risks. By combining statistical risk measures with scenario analysis, traders and risk managers gain a comprehensive view of potential losses under both normal and extreme conditions. Automation, clear visualization, and consistent communication are key to embedding this best practice successfully into daily operations.

4.5 Practical Example: Calculating Delta and Vega for Crude Oil Options

Understanding the Greeks—particularly Delta and Vega—is crucial for effective risk management and hedging in commodity options trading. This section walks through a detailed example of calculating Delta and Vega for a crude oil call option, illustrating how these sensitivities inform trading decisions.

What are Delta and Vega?

- Delta (Δ): Measures the sensitivity of the option’s price to a $1 change in the underlying asset price.

- Vega (ν): Measures the sensitivity of the option’s price to a 1% change in the implied volatility of the underlying asset.

Step 1: Define the Option Parameters

| Parameter | Value |

|---|---|

| Underlying Price (S) | $70 per barrel |

| Strike Price (K) | $75 per barrel |

| Time to Maturity (T) | 3 months (0.25 years) |

| Risk-Free Rate (r) | 2% per annum |

| Implied Volatility (σ) | 30% (0.30) |

| Option Type | European Call Option |

Step 2: Calculate d1 and d2 (Black-Scholes Model)

\[ \begin{aligned} d_1 &= \frac{\ln(\frac{S}{K}) + (r + \frac{\sigma^2}{2}) T}{\sigma \sqrt{T}} \\ d_2 &= d_1 - \sigma \sqrt{T} \end{aligned} \]

- Calculate \( d_1 \):

\[ \begin{aligned} d_1 &= \frac{\ln(70/75) + (0.02 + 0.5 \times 0.3^2) \times 0.25}{0.3 \times \sqrt{0.25}} \\ &= \frac{\ln(0.9333) + (0.02 + 0.045) \times 0.25}{0.3 \times 0.5} \\ &= \frac{-0.069 + 0.01625}{0.15} = \frac{-0.05275}{0.15} = -0.3517 \end{aligned} \]

- Calculate \( d_2 \):

\[ d_2 = -0.3517 - 0.3 \times 0.5 = -0.3517 - 0.15 = -0.5017 \]

Step 3: Calculate Delta

- For a European call option, Delta is given by:

\[ \Delta = N(d_1) \]

where \( N(\cdot) \) is the cumulative distribution function (CDF) of the standard normal distribution.

- Using standard normal tables or a calculator:

\[ N(-0.3517) = 1 - N(0.3517) \approx 1 - 0.6377 = 0.3623 \]

So,

\[ \Delta = 0.3623 \]

Interpretation: The option price will increase by approximately $0.36 for every $1 increase in crude oil price.

Step 4: Calculate Vega

- Vega formula:

\[ \text{Vega} = S \times \sqrt{T} \times n(d_1) \]

where \( n(\cdot) \) is the probability density function (PDF) of the standard normal distribution.

- Calculate \( n(d_1) \):

\[ n(d_1) = \frac{1}{\sqrt{2\pi}} e^{-\frac{d_1^2}{2}} = \frac{1}{2.5066} e^{-\frac{(-0.3517)^2}{2}} = 0.375 \]

- Calculate Vega:

\[ \text{Vega} = 70 \times 0.5 \times 0.375 = 13.125 \]

Interpretation: The option price will increase by approximately $13.13 for every 1.0 (or 100%) increase in implied volatility. For a 1% increase in volatility, the option price changes by approximately $0.1313.

Mind Map: Understanding Delta and Vega for Crude Oil Options

Example: Using Delta and Vega in Hedging

Scenario: A trader holds 100 crude oil call options with the parameters above.

-

Delta Hedge:

- Total Delta = 100 options × 0.3623 = 36.23

- To hedge price risk, short 36.23 barrels of crude oil futures.

-

Vega Risk:

- Total Vega = 100 × 13.125 = 1,312.5

- If implied volatility rises by 1%, option value increases by $1,312.50.

- Trader may consider volatility derivatives or options spreads to hedge this risk.

Summary

| Greek | Value | Meaning | Practical Use |

|---|---|---|---|

| Delta | 0.3623 | Price sensitivity to $1 move in crude oil | Hedge underlying price risk |

| Vega | 13.125 | Price sensitivity to 100% change in volatility | Manage volatility exposure |

By calculating Delta and Vega, commodity traders and risk managers can better understand and hedge their exposure to price and volatility risks in crude oil options, enabling more informed and effective risk management strategies.

5. Credit Risk Management in Commodity Trading

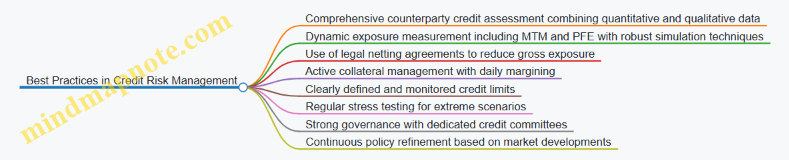

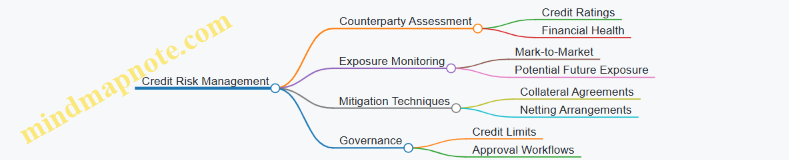

5.1 Counterparty Credit Risk and Exposure Measurement

Counterparty credit risk is the risk that the counterparty to a commodity trading transaction will default before the final settlement of the transaction’s cash flows. This risk is particularly significant in over-the-counter (OTC) derivative transactions where the exposure is bilateral and not guaranteed by an exchange.

Understanding Counterparty Credit Risk

- Definition: The possibility that the counterparty fails to fulfill its contractual obligations.

- Importance: Unmanaged credit risk can lead to significant financial losses and liquidity issues.

Key Components of Counterparty Credit Risk

Mind Map: Counterparty Credit Risk Components

Exposure Measurement