Financial Statement Analysis and Corporate Finance Principles for Investment Professionals

1. Introduction to Financial Statement Analysis

1.1 Overview of Financial Statements: Balance Sheet, Income Statement, and Cash Flow Statement

Financial statements are the backbone of corporate financial analysis, providing a structured and standardized way to understand a company’s financial health, performance, and cash movements. For investment professionals, mastering these statements is essential for making informed decisions.

The Three Core Financial Statements

- Balance Sheet

- Income Statement

- Cash Flow Statement

Each statement serves a unique purpose and collectively offers a comprehensive picture of a company’s financial condition.

Mind Map: Core Financial Statements Overview

Balance Sheet: Snapshot of Financial Position

The balance sheet provides a snapshot of a company’s financial position at a specific point in time. It follows the fundamental accounting equation:

Assets = Liabilities + Equity

- Assets represent resources owned by the company.

- Liabilities are obligations owed to outsiders.

- Equity represents the owners’ residual interest.

Example:

Consider a company with:

- Cash and equivalents: $100,000

- Accounts receivable: $50,000

- Property, plant & equipment: $200,000

- Accounts payable: $40,000

- Long-term debt: $150,000

- Shareholders’ equity: $160,000

The balance sheet would confirm that $350,000 (assets) = $190,000 (liabilities) + $160,000 (equity).

Income Statement: Performance Over Time

The income statement summarizes revenues and expenses over a period, showing profitability.

Key components include:

- Revenue: Income from sales or services.

- Cost of Goods Sold (COGS): Direct costs of producing goods.

- Operating Expenses: Selling, general & administrative expenses.

- Net Income: Bottom-line profit after all expenses.

Example:

A company reports:

- Revenue: $500,000

- COGS: $300,000

- Operating expenses: $120,000

- Interest expense: $10,000

- Tax expense: $14,000

Net Income = $500,000 - $300,000 - $120,000 - $10,000 - $14,000 = $56,000

Cash Flow Statement: Cash Movement Insights

The cash flow statement explains changes in cash during a period, divided into three sections:

- Operating Activities: Cash from core business operations.

- Investing Activities: Cash used for or generated from investments in assets.

- Financing Activities: Cash flows from borrowing, repaying debt, or equity transactions.

Example:

- Cash from operations: $70,000

- Cash used in investing: -$30,000 (purchase of equipment)

- Cash from financing: $20,000 (new debt raised)

Net increase in cash = $70,000 - $30,000 + $20,000 = $60,000

Mind Map: Relationship Between Financial Statements

Integrated Example: Understanding a Company’s Financial Health

Imagine analyzing Company ABC:

- The balance sheet shows strong assets but high short-term liabilities.

- The income statement reveals growing revenues but shrinking profit margins.

- The cash flow statement indicates positive operating cash flow but heavy investing outflows.

Interpretation:

- The company is expanding (investing heavily), which may pressure short-term liquidity.

- Profit margin decline signals cost management issues.

- Positive operating cash flow is a good sign of core business strength.

Best Practices for Investment Professionals

- Always analyze the three statements together to get a holistic view.

- Pay attention to the timing differences between income recognition and cash flows.

- Use the balance sheet to assess financial stability and capital structure.

- Track trends over multiple periods rather than relying on a single snapshot.

- Validate data consistency across statements (e.g., net income should reconcile with cash flow from operations).

Mastering these fundamentals sets the foundation for deeper financial analysis and corporate finance decision-making.

1.2 Importance of Financial Statement Analysis in Investment Banking and Financial Analysis

Financial statement analysis is a cornerstone skill for investment bankers and financial analysts. It enables professionals to make informed decisions by interpreting the financial health, performance, and prospects of companies. This section explores why financial statement analysis is critical in these roles, supported by mind maps and practical examples.

Why Financial Statement Analysis Matters

- Investment Decision-Making: Helps determine the viability and risk of investments.

- Valuation Accuracy: Provides the quantitative foundation for company valuation.

- Credit Assessment: Assesses a company’s ability to meet debt obligations.

- Strategic Advisory: Supports M&A, restructuring, and capital raising decisions.

- Performance Monitoring: Tracks financial trends and operational efficiency.

Mind Map: Core Purposes of Financial Statement Analysis

Example 1: Investment Banking – Evaluating an M&A Target

An investment banker analyzing a potential acquisition target reviews the target’s financial statements to:

- Understand revenue growth and profit margins.

- Assess debt levels and liquidity to gauge financial risk.

- Identify any unusual accounting items that may distort earnings.

- Forecast future cash flows to estimate valuation.

Best Practice: Use common-size financial statements and ratio analysis to compare the target against industry peers, ensuring a relative perspective.

Mind Map: Financial Statement Analysis in M&A

Example 2: Financial Analyst – Credit Risk Assessment

A financial analyst at a credit rating agency examines a company’s financial statements to determine creditworthiness:

- Calculates interest coverage ratio to evaluate the ability to pay interest expenses.

- Analyzes cash flow from operations to ensure sufficient liquidity.

- Reviews maturity schedules of debt to anticipate refinancing needs.

Best Practice: Combine quantitative ratio analysis with qualitative factors such as industry outlook and management quality.

Mind Map: Financial Statement Analysis for Credit Risk

Summary

Financial statement analysis is indispensable for investment professionals. It provides a structured approach to decode complex financial data, enabling better investment decisions, accurate valuations, effective credit assessments, and strategic advisory services. Mastery of this skill, combined with best practices such as comparative analysis and integration of qualitative insights, equips professionals to add significant value in their roles.

1.3 Key Users of Financial Statements and Their Analytical Needs

Financial statements serve as a critical source of information for various stakeholders who rely on them to make informed decisions. Understanding who these key users are and what their specific analytical needs entail is fundamental for investment professionals such as investment bankers and financial analysts. This section explores the primary users of financial statements, their objectives, and the best practices for tailoring analysis to meet their requirements.

Mind Map: Key Users of Financial Statements

Investors

Equity Investors focus on the company’s ability to generate profits and grow shareholder value. They analyze earnings trends, dividend policies, and return ratios such as Return on Equity (ROE). For example, an equity investor reviewing a tech startup might prioritize revenue growth and R&D expenses to gauge future potential rather than just current profits.

Debt Investors (bondholders, banks) prioritize the company’s ability to meet interest and principal payments. They focus on liquidity ratios (current ratio, quick ratio), leverage ratios (debt-to-equity), and cash flow adequacy. For instance, a bank considering a loan to a manufacturing firm will analyze the firm’s operating cash flow and interest coverage ratio to assess repayment capacity.

Management

Management uses financial statements to evaluate operational efficiency and guide strategic decisions. They analyze cost structures, profitability by segment, and capital expenditure needs. For example, a CFO might use segment reporting to decide whether to expand or divest a business unit based on its profit margin and cash flow contribution.

Creditors and Lenders

Creditors assess the risk of lending by analyzing solvency and liquidity. They often require detailed covenant compliance reports and monitor financial ratios regularly. For example, a lender may impose a covenant requiring the company to maintain a minimum interest coverage ratio of 3.0x to reduce default risk.

Regulators

Regulatory bodies ensure companies comply with accounting standards and financial disclosure requirements. They analyze financial statements to detect irregularities or potential fraud. For example, the SEC reviews public companies’ filings to ensure transparency and protect investors.

Employees

Employees may use financial statements to assess job security and negotiate compensation. Profitability and cash flow trends can influence bonus schemes or profit-sharing plans. For example, union representatives might analyze the company’s earnings before negotiating wage increases.

Customers and Suppliers

Long-term customers and suppliers evaluate a company’s financial health to ensure continuity of business relationships. A supplier might review a retailer’s liquidity to decide on credit terms.

Analysts and Advisors

Financial analysts and advisors synthesize financial data to provide investment recommendations. They require comprehensive, accurate data and often perform ratio analysis, trend analysis, and valuation modeling.

Example: Tailoring Financial Analysis for Different Users

Consider a publicly traded consumer goods company:

- Equity Investor: Focuses on earnings growth, dividend payout ratio, and market valuation multiples like P/E ratio.

- Debt Investor: Concentrates on debt-to-equity ratio, interest coverage, and free cash flow to service debt.

- Management: Reviews segment profitability, operating margins, and capital expenditure efficiency.

- Lender: Monitors liquidity ratios and covenant compliance.

By understanding these distinct needs, investment professionals can customize their analysis and reporting to provide relevant insights.

Best Practice

- Identify the primary user(s) before conducting analysis. This ensures the focus is aligned with their decision-making criteria.

- Use appropriate financial metrics and ratios tailored to each user’s needs. For example, prioritize cash flow metrics for creditors and growth metrics for equity investors.

- Communicate findings in a clear, concise manner emphasizing the aspects most relevant to the user.

This user-centric approach enhances the value of financial statement analysis and supports more effective corporate finance decisions.

1.4 Best Practices for Initial Financial Data Gathering and Validation

Financial data gathering and validation form the foundation of any robust financial statement analysis. For investment professionals, ensuring accuracy and completeness at this stage is critical to making informed decisions. This section outlines best practices, supported by clear examples and mind maps, to streamline the process.

Key Steps in Financial Data Gathering and Validation

Best Practice #1: Use Multiple Reliable Data Sources

Relying on a single source can lead to incomplete or biased data. Cross-checking financial statements from company filings (e.g., 10-K) with independent databases like Bloomberg or Capital IQ helps verify accuracy.

Example:

When analyzing Company ABC, an investment analyst first downloads the latest 10-K from the SEC EDGAR database. They then compare key figures such as total assets and net income with Bloomberg terminal data. Minor discrepancies prompt a review of the notes section, revealing a recent asset revaluation not yet reflected in Bloomberg.

Best Practice #2: Validate Data Consistency Across Statements

The balance sheet, income statement, and cash flow statement should reconcile logically. For instance, net income from the income statement should align with the change in retained earnings on the balance sheet.

Example:

An analyst notices that Company XYZ’s net income is $5 million, but retained earnings increased by only $3 million. Upon reviewing the notes, they discover a $2 million dividend payout, explaining the difference. This validation prevents misinterpretation of profitability.

Best Practice #3: Perform Ratio and Trend Analysis Early

Applying preliminary ratio analysis (e.g., current ratio, debt-to-equity) and trend analysis over multiple periods helps identify outliers or data entry errors.

Example:

While reviewing historical data for Company DEF, an analyst observes an unusual spike in the debt-to-equity ratio in the latest quarter. This triggers a deeper dive, revealing a recent debt issuance that was not clearly documented in the initial data set.

Best Practice #4: Document Data Sources and Maintain Version Control

Maintaining a clear audit trail of where data was sourced and tracking versions of datasets ensures transparency and facilitates updates.

Example:

An analyst creates a spreadsheet with tabs for raw data, cleaned data, and analysis. Each tab includes notes on data origin and date accessed. When new quarterly data arrives, the analyst updates the raw data tab and saves a new version, preserving prior work.

Mind Map: Validation Techniques

Summary

Initial financial data gathering and validation require a disciplined approach combining multiple data sources, consistency checks, and thorough documentation. By embedding these best practices into the workflow, investment professionals can build a reliable foundation for deeper financial analysis and corporate finance decision-making.

1.5 Example: Analyzing a Sample Company’s Financial Statements for the First Time

When approaching a company’s financial statements for the first time, it is crucial to have a structured framework to guide your analysis. This example will walk you through the initial steps of analyzing a hypothetical company, “TechNova Inc.”, using its Balance Sheet, Income Statement, and Cash Flow Statement.

Step 1: Understand the Company and Its Industry

- Gather background information about TechNova Inc.: sector, business model, competitors.

- Understand industry-specific financial characteristics (e.g., capital intensity, typical margins).

Step 2: Review the Financial Statements Overview

- Identify the reporting period.

- Note any accounting policies or changes disclosed in the notes.

Step 3: Analyze the Balance Sheet

Mind Map: Balance Sheet Analysis

Example:

- TechNova’s current assets are $150M, with cash of $40M, receivables of $60M, and inventory of $50M.

- Current liabilities total $100M, including $30M in accounts payable and $20M in short-term debt.

Initial Observations:

- Current Ratio = Current Assets / Current Liabilities = 150M / 100M = 1.5 (indicates reasonable liquidity).

Step 4: Analyze the Income Statement

Mind Map: Income Statement Analysis

Example:

- TechNova reports revenue of $500M.

- COGS is $300M, resulting in a gross profit of $200M.

- Operating expenses total $120M.

- Operating income is $80M.

- Interest expense is $10M, taxes are $15M.

- Net income is $55M.

Initial Observations:

- Gross Margin = 200M / 500M = 40%.

- Operating Margin = 80M / 500M = 16%.

- Net Profit Margin = 55M / 500M = 11%.

Step 5: Analyze the Cash Flow Statement

Mind Map: Cash Flow Statement Analysis

Example:

- Operating cash flow is $70M.

- Capital expenditures are $30M.

- Financing activities show $20M debt repayment and $5M dividends paid.

Initial Observations:

- Free Cash Flow = Operating Cash Flow - Capital Expenditures = 70M - 30M = $40M.

- Positive free cash flow indicates capacity to invest or return capital to shareholders.

Step 6: Synthesize Findings

Mind Map: Initial Financial Analysis Summary

Example:

- TechNova appears profitable with healthy margins.

- Liquidity is sufficient to cover short-term obligations.

- Generates positive free cash flow, supporting growth or shareholder returns.

Step 7: Next Steps and Best Practices

- Compare these metrics to industry peers for benchmarking.

- Review notes for off-balance sheet items or contingent liabilities.

- Look for trends by analyzing prior periods.

- Use ratio analysis to deepen insights.

Summary

This example demonstrates a systematic approach to analyzing a company’s financial statements for the first time. By breaking down each statement, calculating key metrics, and synthesizing insights, investment professionals can form a solid foundation for more advanced analysis and decision-making.

Remember: Always complement quantitative analysis with qualitative understanding of the company’s strategy, market position, and risks.

2. Understanding the Balance Sheet

2.1 Components of the Balance Sheet: Assets, Liabilities, and Equity

The balance sheet is a fundamental financial statement that provides a snapshot of a company’s financial position at a specific point in time. It is structured around the fundamental accounting equation:

Assets = Liabilities + Equity

Understanding each component is essential for investment professionals to analyze a company’s financial health, liquidity, and capital structure.

Assets

Assets represent the resources owned or controlled by a company that are expected to generate future economic benefits. They are typically classified into two categories:

- Current Assets: Assets expected to be converted into cash or used up within one year or the operating cycle, whichever is longer.

- Non-Current (Long-Term) Assets: Assets held for use over multiple years.

Common Current Assets:

- Cash and Cash Equivalents

- Accounts Receivable

- Inventory

- Prepaid Expenses

Common Non-Current Assets:

- Property, Plant, and Equipment (PP&E)

- Intangible Assets (e.g., patents, trademarks)

- Long-term Investments

Mind Map: Assets

Example:

Consider a manufacturing company with the following assets:

- Cash: $200,000

- Accounts Receivable: $150,000

- Inventory: $300,000

- PP&E: $1,200,000

- Patents: $100,000

Total Assets = $200,000 + $150,000 + $300,000 + $1,200,000 + $100,000 = $1,950,000

Liabilities

Liabilities are the company’s obligations or debts that it must settle in the future, usually through the transfer of assets or services. Like assets, liabilities are classified as:

- Current Liabilities: Obligations due within one year or the operating cycle.

- Non-Current (Long-Term) Liabilities: Obligations due beyond one year.

Common Current Liabilities:

- Accounts Payable

- Short-term Debt

- Accrued Expenses

- Current Portion of Long-Term Debt

Common Non-Current Liabilities:

- Long-Term Debt (e.g., bonds, bank loans)

- Deferred Tax Liabilities

- Pension Obligations

Mind Map: Liabilities

Example:

Using the same manufacturing company:

- Accounts Payable: $180,000

- Short-term Debt: $100,000

- Long-Term Debt: $700,000

Total Liabilities = $180,000 + $100,000 + $700,000 = $980,000

Equity

Equity represents the residual interest in the assets of the company after deducting liabilities. It reflects the owners’ claims and includes:

- Common Stock: Par value of shares issued.

- Additional Paid-In Capital: Amount paid by investors above par value.

- Retained Earnings: Accumulated net income not distributed as dividends.

- Treasury Stock: Shares repurchased by the company (contra equity account).

Mind Map: Equity

Example:

Continuing with the manufacturing company:

- Common Stock: $500,000

- Additional Paid-In Capital: $200,000

- Retained Earnings: $270,000

Total Equity = $500,000 + $200,000 + $270,000 = $970,000

Putting It All Together

| Component | Amount ($) |

|---|---|

| Assets | 1,950,000 |

| Liabilities | 980,000 |

| Equity | 970,000 |

Check: Assets = Liabilities + Equity

$1,950,000 = $980,000 + $970,000

This confirms the balance sheet equation holds true.

Best Practice: Analyzing Balance Sheet Components

- Assess Asset Quality: Understand the liquidity and valuation methods of assets. For example, inventory valuation methods (FIFO, LIFO) can affect asset values.

- Evaluate Liability Maturity: Distinguish between short-term and long-term obligations to assess liquidity risk.

- Examine Equity Composition: Review retained earnings trends and share issuances or buybacks.

Example: Quick Analysis of a Balance Sheet Snapshot

Imagine you are analyzing Company XYZ’s balance sheet:

- Current Assets: $500,000

- Non-Current Assets: $1,000,000

- Current Liabilities: $300,000

- Long-Term Liabilities: $400,000

- Equity: $800,000

Step 1: Calculate total assets = $500,000 + $1,000,000 = $1,500,000

Step 2: Calculate total liabilities = $300,000 + $400,000 = $700,000

Step 3: Verify equity = Assets - Liabilities = $1,500,000 - $700,000 = $800,000

This confirms the balance sheet is balanced and provides a clear picture of Company XYZ’s financial position.

Summary Mind Map: Balance Sheet Components

Understanding these components deeply enables investment professionals to perform thorough financial analysis, identify risks, and make informed decisions.

2.2 Asset Classification and Valuation Techniques

Understanding asset classification and valuation is fundamental for investment professionals analyzing a company’s financial health. Assets represent resources controlled by a company expected to generate future economic benefits. Proper classification and valuation ensure accurate financial reporting and sound investment decisions.

Asset Classification

Assets are broadly classified into two main categories:

- Current Assets

- Non-Current (Long-Term) Assets

Mind Map: Asset Classification

Current Assets

Current assets are expected to be converted into cash or used up within one operating cycle or one year, whichever is longer. Examples include:

- Cash and Cash Equivalents: Highly liquid assets like cash on hand and short-term investments.

- Accounts Receivable: Money owed by customers.

- Inventory: Raw materials, work-in-progress, and finished goods.

Non-Current Assets

Non-current assets provide long-term value and are not expected to be liquidated within a year. Examples include:

- Property, Plant, and Equipment (PP&E): Tangible fixed assets like buildings, machinery.

- Intangible Assets: Non-physical assets such as patents and goodwill.

Valuation Techniques

Accurate valuation of assets is critical for assessing company worth and making investment decisions. The valuation method depends on asset type and accounting standards.

Historical Cost Method

Assets are recorded at their original purchase price, less accumulated depreciation or amortization.

- Best Practice: Useful for PP&E where market value is stable.

Example: A machine purchased for $100,000 with a useful life of 10 years is recorded at $100,000 and depreciated annually.

Fair Value Method

Assets are recorded at their current market value.

- Best Practice: Used for marketable securities and investment properties.

Example: A portfolio of stocks purchased at $50,000 is reported at $60,000 if the market value increases.

Net Realizable Value (NRV)

Used primarily for inventory valuation, NRV is the estimated selling price minus costs to complete and sell.

- Best Practice: Ensures inventory is not overstated.

Example: Inventory costing $30,000 has an NRV of $25,000 due to obsolescence; it should be written down to $25,000.

Present Value Method

Used for long-term receivables or assets with future cash flows, discounting expected cash flows to present value.

- Best Practice: Important for valuing financial assets and intangible assets with measurable cash flows.

Example: A patent expected to generate $10,000 annually for 5 years is valued by discounting those cash flows to present value.

Mind Map: Asset Valuation Techniques

Integrated Example: Asset Classification and Valuation

Scenario: Company ABC’s balance sheet includes:

- Cash: $20,000

- Accounts Receivable: $50,000

- Inventory: $40,000 (NRV estimated at $35,000)

- Machinery (PP&E): Purchased for $200,000, accumulated depreciation $50,000

- Patent: Expected future cash flows discounted to $30,000

Analysis:

- Cash and Accounts Receivable: Classified as current assets, valued at face value.

- Inventory: Classified as current asset, valued at NRV ($35,000) due to obsolescence.

- Machinery: Non-current asset, valued at historical cost less depreciation ($150,000).

- Patent: Non-current intangible asset, valued using present value method ($30,000).

This classification and valuation provide a realistic picture of the company’s asset base for investment analysis.

Best Practices Summary

- Always classify assets based on liquidity and usage.

- Use valuation methods appropriate to asset type and industry standards.

- Regularly review asset values for impairment or obsolescence.

- Cross-check valuation with market data when available.

- Document assumptions used in valuation for transparency.

By mastering asset classification and valuation techniques, investment professionals can better assess a company’s financial position, identify risks, and make informed recommendations.

2.3 Liability Structures and Their Implications for Financial Health

Liabilities represent a company’s financial obligations and debts that it must settle in the future. Understanding the structure of liabilities is crucial for investment professionals because it directly impacts a firm’s liquidity, solvency, and overall financial health.

Types of Liabilities

Liabilities are generally classified into two main categories:

- Current Liabilities: Obligations due within one year.

- Non-Current Liabilities (Long-Term Liabilities): Obligations due beyond one year.

Mind Map: Liability Classification

Current Liabilities: Key Components and Implications

- Accounts Payable: Money owed to suppliers; reflects operational efficiency.

- Short-term Debt: Loans or borrowings due within a year; affects liquidity.

- Accrued Expenses: Expenses recognized but not yet paid; indicates timing of cash outflows.

- Current Portion of Long-term Debt: Portion of long-term debt due in the next year; important for cash flow planning.

Implications:

- High current liabilities relative to current assets may signal liquidity risk.

- Efficient management of payables and accruals can improve working capital.

Example:

Company A has current assets of $500,000 and current liabilities of $600,000. This results in a current ratio of 0.83, indicating potential liquidity issues since the company may struggle to cover short-term obligations.

Non-Current Liabilities: Key Components and Implications

- Long-term Debt: Loans and bonds payable beyond one year; affects leverage and interest expenses.

- Bonds Payable: Debt securities issued to investors; may have fixed or variable interest rates.

- Deferred Tax Liabilities: Taxes owed but deferred to future periods; impacts future cash outflows.

- Lease Obligations: Long-term lease commitments; recognized under accounting standards like IFRS 16.

Implications:

- Long-term liabilities influence the company’s capital structure and financial risk.

- Excessive long-term debt can increase bankruptcy risk but may also provide leverage benefits.

Example:

Company B has $2 million in long-term debt with an interest rate of 6%. If earnings before interest and taxes (EBIT) are $300,000, the interest coverage ratio is:

\[ \text{Interest Coverage Ratio} = \frac{EBIT}{Interest Expense} = \frac{300,000}{2,000,000 \times 0.06} = 2.5 \]

A ratio of 2.5 indicates moderate ability to cover interest payments but may be a warning sign if it declines.

Liability Structure and Financial Health

The composition and maturity profile of liabilities affect several key financial health indicators:

- Liquidity: Ability to meet short-term obligations.

- Solvency: Ability to meet long-term obligations.

- Financial Flexibility: Capacity to raise funds or restructure debt.

Mind Map: Liability Structure Impact on Financial Health

Best Practices for Analyzing Liability Structures

- Assess Maturity Profiles: Understand when liabilities come due to anticipate refinancing needs.

- Evaluate Interest Rates and Covenants: Fixed vs. variable rates affect risk; covenants may restrict operations.

- Compare to Industry Benchmarks: Contextualize leverage and liquidity ratios.

- Analyze Trends Over Time: Increasing liabilities without asset growth may indicate risk.

- Incorporate Off-Balance Sheet Liabilities: Such as operating leases or guarantees.

Integrated Example: Liability Structure Analysis of Company C

Company C’s balance sheet shows:

- Current Liabilities: $800,000

- Current Assets: $1,200,000

- Long-term Debt: $3,000,000 at 5% interest

- EBIT: $400,000

- Equity: $4,000,000

Step 1: Liquidity Analysis

- Current Ratio = $1,200,000 / $800,000 = 1.5 (healthy liquidity)

Step 2: Leverage Analysis

- Debt-to-Equity = ($800,000 + $3,000,000) / $4,000,000 = 0.95 (moderate leverage)

Step 3: Interest Coverage

- Interest Expense = $3,000,000 * 5% = $150,000

- Interest Coverage Ratio = $400,000 / $150,000 = 2.67 (adequate coverage)

Step 4: Interpretation

- Company C maintains a balanced liability structure with sufficient liquidity and manageable leverage.

- The interest coverage ratio suggests the company can comfortably meet interest payments.

Summary

Understanding liability structures enables investment professionals to:

- Evaluate short-term liquidity risks and long-term solvency.

- Assess financial flexibility and risk exposure.

- Make informed recommendations on capital structure optimization.

By integrating detailed liability analysis with other financial statement components, professionals can form a comprehensive view of a company’s financial health.

2.4 Equity Analysis: Shareholder’s Equity and Retained Earnings

Overview

Shareholder’s equity represents the residual interest in the assets of a company after deducting liabilities. It is a critical component of the balance sheet and provides insight into the company’s net worth from the shareholders’ perspective. Understanding equity and retained earnings helps investment professionals assess the company’s financial stability, growth potential, and dividend capacity.

Components of Shareholder’s Equity

- Common Stock: Par value of shares issued to shareholders.

- Additional Paid-In Capital (APIC): Amount paid by investors above the par value.

- Retained Earnings: Cumulative net income retained in the business after dividends.

- Treasury Stock: Shares repurchased by the company, reducing equity.

- Other Comprehensive Income: Gains/losses excluded from net income but affecting equity.

Mind Map: Components of Shareholder’s Equity

Understanding Retained Earnings

Retained earnings reflect the accumulated profits that have been reinvested in the company rather than distributed as dividends. It is calculated as:

\[ \text{Retained Earnings}_{end} = \text{Retained Earnings}_{beginning} + \text{Net Income} - \text{Dividends Paid} \]

This figure is crucial for evaluating how much profit a company has reinvested to fuel growth.

Mind Map: Retained Earnings Calculation

Best Practice: Analyzing Changes in Equity

Investment professionals should analyze changes in shareholder’s equity over time to understand capital raising activities, dividend policies, and profitability retention. Key steps include:

- Review Equity Statement: Examine the statement of changes in equity for detailed movements.

- Identify Capital Issuances or Buybacks: Note any new share issuances or treasury stock transactions.

- Analyze Dividend Trends: Understand how dividends impact retained earnings.

- Assess Profitability Impact: Correlate net income trends with retained earnings growth.

Example 1: Interpreting Shareholder’s Equity Movements

Company ABC’s equity section (in $ millions):

| Item | Year 1 | Year 2 |

|---|---|---|

| Common Stock | 100 | 100 |

| Additional Paid-In Capital | 200 | 250 |

| Retained Earnings | 300 | 350 |

| Treasury Stock | (50) | (50) |

| Total Shareholder’s Equity | 550 | 650 |

Analysis:

- APIC increased by $50 million, indicating new capital raised.

- Retained earnings grew by $50 million, reflecting net income retention.

- Treasury stock remained constant.

- Overall equity increased by $100 million, signaling strengthening financial position.

Example 2: Calculating Retained Earnings

Given:

- Beginning retained earnings: $500 million

- Net income for the year: $120 million

- Dividends paid: $40 million

Calculation:

\[ 500 + 120 - 40 = 580 \text{ million} \]

Interpretation: Retained earnings increased to $580 million, indicating the company retained a significant portion of its earnings for reinvestment.

Equity Analysis in Decision-Making

- Dividend Policy: A high retained earnings balance may indicate capacity to pay dividends or reinvest.

- Financial Health: Increasing equity generally signals financial strength.

- Capital Structure: Changes in equity affect leverage ratios and cost of capital.

Mind Map: Equity Analysis for Investment Professionals

Summary

Equity analysis, particularly understanding shareholder’s equity and retained earnings, is vital for investment professionals to evaluate a company’s financial foundation and growth trajectory. By combining quantitative calculations with qualitative insights, professionals can make informed recommendations on investments, capital structure, and dividend policies.

2.5 Best Practice: Assessing Liquidity and Solvency Using Balance Sheet Data

Assessing a company’s liquidity and solvency is fundamental for investment professionals to understand its short-term financial health and long-term viability. The balance sheet provides critical data to perform these assessments effectively.

Understanding Liquidity and Solvency

- Liquidity refers to a company’s ability to meet its short-term obligations using its most liquid assets.

- Solvency refers to the company’s capacity to meet long-term obligations and sustain operations over time.

Key Metrics for Liquidity Assessment

- Current Ratio = Current Assets / Current Liabilities

- Quick Ratio (Acid-Test Ratio) = (Current Assets - Inventories) / Current Liabilities

- Cash Ratio = Cash and Cash Equivalents / Current Liabilities

Key Metrics for Solvency Assessment

- Debt to Equity Ratio = Total Debt / Total Equity

- Interest Coverage Ratio = EBIT / Interest Expense

- Debt Ratio = Total Debt / Total Assets

Mind Map: Liquidity Assessment

Mind Map: Solvency Assessment

Step-by-Step Best Practice Approach

-

Gather Balance Sheet Data

- Extract current assets, inventories, cash, current liabilities, total debt, total equity, EBIT, and interest expense.

-

Calculate Liquidity Ratios

- Compute current, quick, and cash ratios.

- Compare against industry benchmarks.

-

Calculate Solvency Ratios

- Compute debt to equity, interest coverage, and debt ratios.

- Analyze trends over multiple periods.

-

Interpret Results

- Identify potential liquidity crunches or solvency risks.

- Consider qualitative factors such as industry cyclicality.

-

Integrate with Broader Financial Analysis

- Combine with cash flow and income statement insights for a holistic view.

Example: Assessing Liquidity and Solvency for XYZ Corp

Balance Sheet Extract (in $ millions):

| Item | Amount |

|---|---|

| Current Assets | 500 |

| Inventories | 150 |

| Cash and Equivalents | 100 |

| Current Liabilities | 400 |

| Total Debt | 700 |

| Total Equity | 800 |

Income Statement Extract:

| Item | Amount |

|---|---|

| EBIT | 200 |

| Interest Expense | 40 |

Calculations:

- Current Ratio = 500 / 400 = 1.25 (Healthy liquidity)

- Quick Ratio = (500 - 150) / 400 = 350 / 400 = 0.875 (Acceptable liquidity)

- Cash Ratio = 100 / 400 = 0.25 (Moderate cash buffer)

- Debt to Equity Ratio = 700 / 800 = 0.875 (Moderate leverage)

- Interest Coverage Ratio = 200 / 40 = 5 (Strong ability to cover interest)

- Debt Ratio = 700 / (700 + 800) = 700 / 1500 = 0.467 (Less than 50% assets financed by debt)

Interpretation:

- XYZ Corp shows solid liquidity with current and quick ratios above typical thresholds.

- Cash ratio is lower, suggesting limited immediate cash but acceptable given other liquid assets.

- Solvency ratios indicate moderate leverage and strong interest coverage, implying manageable long-term debt risk.

Summary

- Use multiple ratios to get a comprehensive picture.

- Always benchmark against industry standards.

- Analyze trends over time, not just single-period data.

- Combine quantitative analysis with qualitative insights for robust conclusions.

This best practice approach enables investment professionals to confidently assess a company’s financial health and make informed decisions.

2.6 Example: Interpreting a Real-World Balance Sheet to Identify Financial Strengths and Weaknesses

In this section, we will walk through a practical example of analyzing a real-world balance sheet to uncover a company’s financial strengths and weaknesses. This exercise is essential for investment bankers and financial analysts who need to make informed decisions based on a company’s financial health.

Step 1: Overview of the Balance Sheet

Let’s consider the simplified balance sheet of XYZ Corporation (all figures in millions):

| Assets | Amount | Liabilities & Equity | Amount |

|---|---|---|---|

| Current Assets | 500 | Current Liabilities | 300 |

| - Cash and Equivalents | 150 | - Accounts Payable | 120 |

| - Accounts Receivable | 200 | - Short-term Debt | 180 |

| - Inventory | 150 | Long-term Debt | 400 |

| Non-Current Assets | 1000 | Shareholders’ Equity | 800 |

| - Property, Plant & Equip | 700 | - Common Stock | 300 |

| - Intangible Assets | 300 | - Retained Earnings | 500 |

| Total Assets | 1500 | Total Liabilities & Equity | 1500 |

Step 2: Mind Map - Key Areas to Analyze

Step 3: Analyze Liquidity

Liquidity measures the company’s ability to meet short-term obligations.

-

Current Ratio = Current Assets / Current Liabilities = 500 / 300 = 1.67

- Interpretation: A current ratio above 1 indicates the company can cover its short-term liabilities with current assets, which is a positive sign.

-

Quick Ratio = (Current Assets - Inventory) / Current Liabilities = (500 - 150) / 300 = 350 / 300 = 1.17

- Interpretation: Excluding inventory, the company still has more than enough liquid assets to cover current liabilities.

Mind Map - Liquidity Analysis

Step 4: Analyze Solvency

Solvency assesses the company’s long-term financial stability.

-

Debt-to-Equity Ratio = Total Debt / Shareholders’ Equity = (300 + 400) / 800 = 700 / 800 = 0.875

- Interpretation: Less than 1, indicating the company uses less debt than equity to finance assets, which is generally conservative.

-

Interest Coverage Ratio (Assuming EBIT of 150 million and interest expense of 50 million):

- EBIT / Interest Expense = 150 / 50 = 3

- Interpretation: The company earns 3 times its interest expense, which is acceptable but could be improved.

Mind Map - Solvency Analysis

Step 5: Asset Quality and Composition

-

Intangible Assets represent 300 million out of 1000 million non-current assets (30%).

- High intangible assets may indicate strong brand value or intellectual property but can be less liquid and harder to value.

-

Inventory at 150 million is 30% of current assets.

- Inventory management efficiency should be monitored to avoid obsolescence.

Mind Map - Asset Quality

Step 6: Equity Position

- Retained Earnings of 500 million indicate accumulated profits reinvested in the company.

- Common Stock of 300 million reflects shareholder capital.

A strong equity base supports financial stability and growth potential.

Step 7: Summary of Financial Strengths and Weaknesses

| Strengths | Weaknesses |

|---|---|

| Healthy liquidity ratios (Current and Quick) | Moderate interest coverage ratio (3x) |

| Conservative debt-to-equity ratio (0.875) | Significant intangible assets (valuation risk) |

| Strong cash reserves (150 million) | Inventory concentration (risk of obsolescence) |

| Solid retained earnings supporting equity | Reliance on short-term debt (180 million) |

Step 8: Final Mind Map - Holistic View

Conclusion

By carefully interpreting the balance sheet of XYZ Corporation, investment professionals can identify that the company demonstrates solid liquidity and a conservative capital structure, which are financial strengths. However, attention should be paid to the moderate interest coverage ratio and the relatively high proportion of intangible assets and inventory, which pose potential risks.

This comprehensive approach, combining ratio analysis, asset composition review, and equity evaluation, equips investment bankers and financial analysts with actionable insights to support investment decisions, credit assessments, or corporate finance strategies.

3. Income Statement Analysis

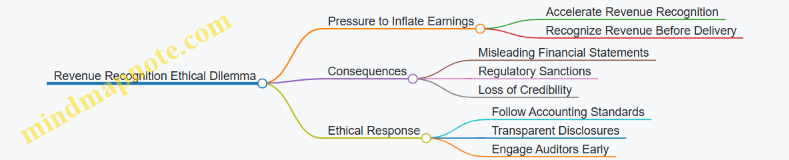

3.1 Revenue Recognition and Its Impact on Financial Results

Revenue recognition is a fundamental accounting principle that determines the specific conditions under which income becomes realized as revenue. For investment professionals, understanding revenue recognition is critical because it directly affects the reported earnings, valuation, and financial health of a company.

What is Revenue Recognition?

Revenue recognition refers to the process and timing by which a company records revenue in its financial statements. The key principle is to recognize revenue when it is earned and realizable, not necessarily when cash is received.

Why It Matters for Financial Analysis

- Earnings Quality: Proper revenue recognition ensures earnings reflect the true economic activity.

- Comparability: Consistent revenue recognition policies allow for meaningful comparisons across companies and periods.

- Valuation Impact: Revenue drives profitability and cash flow forecasts, influencing valuation models.

Core Principles of Revenue Recognition (IFRS 15 / ASC 606)

- Identify the contract(s) with a customer

- Identify the performance obligations in the contract

- Determine the transaction price

- Allocate the transaction price to the performance obligations

- Recognize revenue when (or as) the entity satisfies a performance obligation

Mind Map: Revenue Recognition Process

Common Revenue Recognition Methods

| Method | Description | Example |

|---|---|---|

| Point in Time | Revenue recognized when control transfers | Retail sale when customer takes possession |

| Over Time | Revenue recognized over contract duration | Construction project progress billing |

| Completed Contract | Revenue recognized at contract completion | Custom software development |

Example 1: Software Company with Subscription Model

Scenario: A SaaS company sells annual subscriptions for $1,200.

- Cash received upfront: $1,200

- Revenue recognized monthly: $100

Impact: Although cash is received upfront, revenue is recognized ratably over the subscription period to match service delivery.

Financial Statement Effect:

- Income Statement: $100 revenue per month

- Balance Sheet: Deferred revenue liability of $1,100 initially, decreasing monthly

Mind Map: Impact of Revenue Recognition on Financial Statements

Example 2: Construction Company Using Percentage-of-Completion Method

Scenario: A construction firm enters a $10 million contract expected to last 2 years.

- Year 1: 40% complete

- Revenue recognized in Year 1: $4 million

Impact: Revenue and profit are recognized based on progress, providing a more accurate reflection of economic activity.

Financial Statement Effect:

- Income Statement: $4 million revenue in Year 1

- Balance Sheet: Construction in progress asset and billings on account

Best Practices for Investment Professionals

- Review Revenue Recognition Policies: Always examine the notes to financial statements for the company’s revenue recognition methods.

- Analyze Deferred Revenue: Large deferred revenue balances may indicate future revenue streams but also potential risks.

- Watch for Changes in Policy: Changes can signal aggressive accounting or shifts in business model.

- Compare Across Peers: Ensure consistency in revenue recognition to make valid comparisons.

Summary

Revenue recognition is a cornerstone of financial reporting that directly influences a company’s reported earnings and financial position. Investment professionals must understand the timing and methods of revenue recognition to accurately interpret financial results, assess earnings quality, and make informed investment decisions.

3.2 Cost of Goods Sold, Operating Expenses, and Profit Margins

Understanding the components of the income statement is crucial for investment professionals analyzing a company’s profitability and operational efficiency. This section delves into Cost of Goods Sold (COGS), Operating Expenses (OPEX), and Profit Margins, explaining their definitions, relationships, and implications with practical examples and mind maps.

What is Cost of Goods Sold (COGS)?

COGS represents the direct costs attributable to the production of the goods sold by a company. This includes raw materials, direct labor, and manufacturing overhead directly tied to production.

- Direct Materials: Raw materials used in production.

- Direct Labor: Wages of employees directly involved in manufacturing.

- Manufacturing Overhead: Indirect costs like factory utilities and depreciation of production equipment.

Example: A furniture manufacturer buys wood and fabric for $50,000 and pays $20,000 in wages to factory workers in a quarter. The factory electricity bill is $5,000. The COGS for that quarter would be $75,000.

What are Operating Expenses (OPEX)?

Operating expenses are costs required to run the business that are not directly tied to production. They include selling, general, and administrative expenses (SG&A).

- Selling Expenses: Marketing, sales commissions, distribution costs.

- General & Administrative Expenses: Salaries of office staff, rent, utilities, office supplies.

Example: The same furniture company spends $15,000 on marketing, $10,000 on administrative salaries, and $3,000 on office rent in the same quarter. These total $28,000 in operating expenses.

Profit Margins Explained

Profit margins measure the percentage of revenue that remains after certain costs are deducted. They help assess profitability at different stages.

- Gross Profit Margin: (Revenue - COGS) / Revenue

- Operating Profit Margin: (Operating Income) / Revenue

- Net Profit Margin: (Net Income) / Revenue

Example: If the furniture company has revenue of $150,000 in the quarter:

-

Gross Profit = $150,000 - $75,000 = $75,000

-

Gross Margin = $75,000 / $150,000 = 50%

-

Operating Income = Gross Profit - Operating Expenses = $75,000 - $28,000 = $47,000

-

Operating Margin = $47,000 / $150,000 ≈ 31.3%

-

Assuming interest and taxes total $7,000, Net Income = $40,000

-

Net Margin = $40,000 / $150,000 ≈ 26.7%

Mind Maps

Mind Map 1: Components of Income Statement Costs

Mind Map 2: Profit Margin Types

Best Practices for Analysis

- Analyze COGS Trends: Rising COGS as a percentage of sales may indicate increasing production costs or inefficiencies.

- Evaluate Operating Expenses: Compare OPEX to industry benchmarks to identify cost control effectiveness.

- Use Common-Size Statements: Express COGS and OPEX as a percentage of sales for easier comparison across periods or companies.

- Assess Profit Margins Over Time: Look for consistent or improving margins as a sign of operational strength.

Example: Analyzing a Retail Company’s Income Statement

Company ABC Retail reports the following for the fiscal year:

| Item | Amount ($) |

|---|---|

| Revenue | 2,000,000 |

| Cost of Goods Sold | 1,200,000 |

| Operating Expenses | 400,000 |

| Interest Expense | 50,000 |

| Taxes | 70,000 |

Calculations:

-

Gross Profit = $2,000,000 - $1,200,000 = $800,000

-

Gross Margin = 800,000 / 2,000,000 = 40%

-

Operating Income = $800,000 - $400,000 = $400,000

-

Operating Margin = 400,000 / 2,000,000 = 20%

-

Net Income = $400,000 - $50,000 - $70,000 = $280,000

-

Net Margin = 280,000 / 2,000,000 = 14%

Interpretation:

- The company retains 40% of revenue after direct costs, which is healthy for retail.

- Operating expenses consume 20% of revenue, indicating moderate overhead.

- Net margin of 14% suggests solid profitability after all costs.

Investment professionals can use these insights to compare ABC Retail with peers, evaluate operational efficiency, and assess potential investment risks or opportunities.

Summary

- COGS directly impacts gross profit and reflects production efficiency.

- Operating Expenses affect operating income and indicate management’s cost control.

- Profit Margins provide layered insights into profitability at different stages.

- Using mind maps and examples helps clarify these concepts and supports robust financial analysis for investment decisions.

3.3 Non-Operating Items and Their Effects on Earnings

Non-operating items are revenues, expenses, gains, or losses that are not related to a core business operations of a company. Understanding these items is crucial for investment professionals because they can significantly distort the true operating performance and profitability of a company if not analyzed properly.

What Are Non-Operating Items?

- Definition: Items that arise from activities outside the primary business operations.

- Common Types:

- Interest income and expense

- Gains or losses on asset sales

- Restructuring charges

- Impairment losses

- Foreign exchange gains or losses

- Litigation settlements

Why Are Non-Operating Items Important?

- They can inflate or deflate earnings temporarily.

- They affect comparability across periods and companies.

- Analysts need to adjust earnings to reflect sustainable operating performance.

Mind Map: Classification of Non-Operating Items

Effects of Non-Operating Items on Earnings

| Effect Type | Description | Example |

|---|---|---|

| Earnings Volatility | Sudden spikes or drops due to one-time items | Gain from sale of a subsidiary |

| Misleading Profitability | Operating profit appears higher or lower than actual core business results | Large restructuring charge in a quarter |

| Impact on Valuation | Distorts metrics like EPS, P/E ratio | Foreign exchange gain boosting net income |

Example 1: Impact of Asset Sale Gain on Earnings

Scenario:

Company ABC sells a piece of machinery for $1 million. The book value of the machinery was $700,000.

- Gain on sale = $1,000,000 - $700,000 = $300,000

- This gain is recorded as a non-operating income item.

Effect:

- The net income will increase by $300,000 in the period.

- Operating income remains unaffected.

- Analysts should exclude this gain when assessing ongoing profitability.

Mind Map: Adjusting Earnings for Non-Operating Items

Example 2: Restructuring Charges and Their Impact

Scenario:

Company XYZ incurs a $5 million restructuring charge to close an underperforming division.

- This charge is recorded as a non-operating expense.

- It reduces net income significantly in the current period.

Effect:

- Operating income excludes this charge, so it better reflects ongoing operations.

- Analysts may adjust earnings by adding back the restructuring charge (net of tax) to evaluate normalized earnings.

Best Practices for Analysts

- Identify Non-Operating Items: Carefully review income statement and notes.

- Adjust Earnings: Calculate adjusted earnings excluding non-operating items for better comparability.

- Consider Tax Impact: Adjustments should reflect after-tax amounts.

- Evaluate Recurrence: Determine if items are truly one-time or recurring.

- Use Segment Reporting: Helps isolate operating vs. non-operating results.

Summary

Non-operating items can significantly affect reported earnings, often masking the true operating performance of a company. Investment professionals must identify, analyze, and adjust for these items to make informed decisions about profitability, valuation, and financial health.

Additional Example: Foreign Exchange Gain Impact

Scenario:

A multinational company reports a $2 million foreign exchange gain due to currency fluctuations.

- This gain is non-operating and can vary widely from period to period.

- Including it in earnings may overstate profitability.

Analyst Action:

- Exclude the $2 million gain when calculating adjusted net income.

- Focus on operating income and cash flows for sustainable performance analysis.

3.4 Earnings Quality and Sustainable Profitability Assessment

Earnings quality refers to the degree to which reported income reflects the company’s true economic performance and is free from distortion or manipulation. Sustainable profitability assesses whether a company can maintain its earnings over the long term without relying on one-time gains or accounting gimmicks.

Understanding earnings quality and sustainable profitability is crucial for investment professionals because it helps distinguish between companies with genuine operational strength and those with potentially misleading financial results.

Key Factors Affecting Earnings Quality

Components of Sustainable Profitability

Best Practices to Assess Earnings Quality

-

Analyze the Composition of Earnings:

- Separate recurring operating income from non-recurring items such as gains on asset sales or restructuring charges.

- Example: A company reports a 20% increase in net income, but 5% is from selling a subsidiary. Adjusted earnings growth is 15%, reflecting core operations.

-

Evaluate Cash Flow vs. Net Income:

- High-quality earnings typically correlate with strong operating cash flows.

- Example: Company A reports net income of $10 million but operating cash flow is only $2 million, signaling potential earnings quality issues.

-

Review Changes in Accounting Policies:

- Identify if changes in revenue recognition or expense capitalization inflate earnings.

- Example: A firm switches from cash to accrual accounting, increasing reported revenue without actual cash inflow.

-

Detect Earnings Management:

- Look for unusual accruals, reserves, or timing of expenses.

- Example: A company defers maintenance expenses to inflate current period profits.

-

Use Financial Ratios:

- Accruals ratio, cash conversion ratio, and quality of earnings ratio help quantify earnings quality.

Example: Assessing Earnings Quality of XYZ Corp

XYZ Corp reported the following for fiscal year 2023:

| Metric | Amount (in $ millions) |

|---|---|

| Net Income | 50 |

| Operating Cash Flow | 45 |

| Non-Recurring Gains | 5 |

| Revenue Growth | 10% |

| Change in Accounting Policy | None |

- Step 1: Adjust net income by removing non-recurring gains: $50M - $5M = $45M

- Step 2: Compare adjusted net income ($45M) to operating cash flow ($45M) — strong alignment indicates high earnings quality.

- Step 3: No accounting policy changes reported.

Conclusion: XYZ Corp demonstrates high earnings quality with sustainable profitability driven by core operations.

Mind Map: Steps to Evaluate Earnings Quality and Sustainable Profitability

Summary

For investment bankers and financial analysts, distinguishing between high and low-quality earnings is essential to making informed investment decisions. Sustainable profitability ensures that earnings are not only strong today but can be maintained or grown in the future. Combining quantitative analysis with qualitative insights provides a comprehensive view of a company’s financial health.

3.5 Best Practice: Using Common-Size Income Statements for Comparative Analysis

What is a Common-Size Income Statement?

A common-size income statement expresses each line item as a percentage of total revenue (sales). This standardization allows investment professionals to compare companies of different sizes or analyze a single company’s performance over time, eliminating the distortion caused by absolute dollar amounts.

Why Use Common-Size Income Statements?

- Comparability: Enables apples-to-apples comparison between companies regardless of scale.

- Trend Analysis: Highlights changes in cost structure and profitability over time.

- Benchmarking: Helps identify operational efficiencies or inefficiencies relative to peers.

How to Prepare a Common-Size Income Statement

- Take each line item from the income statement.

- Divide the line item by total revenue (net sales).

- Express the result as a percentage.

Example:

| Income Statement Item | Amount ($) | % of Revenue |

|---|---|---|

| Revenue | 1,000,000 | 100% |

| Cost of Goods Sold | 600,000 | 60% |

| Gross Profit | 400,000 | 40% |

| Operating Expenses | 200,000 | 20% |

| Operating Income | 200,000 | 20% |

| Interest Expense | 20,000 | 2% |

| Net Income | 150,000 | 15% |

Mind Map: Common-Size Income Statement Analysis

Example: Comparative Analysis Using Common-Size Income Statements

Consider two companies in the retail sector:

| Item | Company A ($) | % of Revenue A | Company B ($) | % of Revenue B |

|---|---|---|---|---|

| Revenue | 2,000,000 | 100% | 5,000,000 | 100% |

| Cost of Goods Sold | 1,200,000 | 60% | 3,750,000 | 75% |

| Gross Profit | 800,000 | 40% | 1,250,000 | 25% |

| Operating Expenses | 400,000 | 20% | 750,000 | 15% |

| Operating Income | 400,000 | 20% | 500,000 | 10% |

| Net Income | 300,000 | 15% | 350,000 | 7% |

Insights:

- Company A has a lower cost of goods sold percentage (60% vs. 75%), indicating better cost control or supplier terms.

- Company A’s operating income margin is double that of Company B (20% vs. 10%), suggesting more efficient operations.

- Despite Company B’s higher absolute revenue, Company A is more profitable relative to sales.

Mind Map: Interpreting Comparative Common-Size Income Statements

Tips for Investment Professionals

- Always pair common-size analysis with absolute figures to understand scale.

- Use industry averages as benchmarks to contextualize percentages.

- Track common-size percentages over multiple periods to identify trends.

- Combine with ratio analysis (e.g., gross margin, operating margin) for deeper insights.

Summary

Using common-size income statements is a best practice that allows investment bankers and financial analysts to perform meaningful comparative analysis across companies and time periods. By converting income statement line items into percentages of revenue, professionals can uncover insights about cost structures, profitability, and operational efficiency that raw numbers alone might obscure.

3.6 Example: Evaluating Profitability Trends in a Competitive Industry

In this section, we will walk through a detailed example of evaluating profitability trends for a company operating in a highly competitive industry — the consumer electronics sector. This example will demonstrate how investment professionals can analyze income statements, apply best practices, and interpret profitability metrics to make informed decisions.

Step 1: Understanding the Industry Context

Competitive industries often experience pressure on pricing, margins, and innovation cycles. Profitability analysis must consider these factors alongside raw financial data.

Mind Map: Industry Context and Profitability Factors

Step 2: Collecting and Reviewing Income Statement Data

Consider Company A, a mid-sized consumer electronics manufacturer. Below is a simplified income statement for the last three years (in millions):

| Year | Revenue | Cost of Goods Sold (COGS) | Operating Expenses | Operating Income | Net Income |

|---|---|---|---|---|---|

| 2021 | 1,000 | 700 | 200 | 100 | 70 |

| 2022 | 1,100 | 770 | 220 | 110 | 77 |

| 2023 | 1,200 | 840 | 260 | 100 | 65 |

Step 3: Calculating Profitability Metrics

Key profitability metrics include:

- Gross Profit Margin = (Revenue - COGS) / Revenue

- Operating Profit Margin = Operating Income / Revenue

- Net Profit Margin = Net Income / Revenue

| Year | Gross Profit Margin | Operating Profit Margin | Net Profit Margin |

|---|---|---|---|

| 2021 | (1000-700)/1000 = 30% | 100/1000 = 10% | 70/1000 = 7% |

| 2022 | (1100-770)/1100 = 30% | 110/1100 = 10% | 77/1100 = 7% |

| 2023 | (1200-840)/1200 = 30% | 100/1200 = 8.33% | 65/1200 = 5.42% |

Step 4: Analyzing Trends and Identifying Drivers

- Gross Profit Margin remains stable at 30%, indicating consistent cost control on production.

- Operating Profit Margin declines from 10% to 8.33%, suggesting rising operating expenses.

- Net Profit Margin declines more sharply, from 7% to 5.42%, possibly due to increased interest, taxes, or other non-operating expenses.

Mind Map: Profitability Trend Analysis

Step 5: Benchmarking Against Competitors

Compare Company A’s margins with Industry Averages:

| Metric | Company A (2023) | Industry Average (2023) |

|---|---|---|

| Gross Profit Margin | 30% | 32% |

| Operating Profit Margin | 8.33% | 9.5% |

| Net Profit Margin | 5.42% | 6.5% |

Company A is slightly below industry averages, indicating potential operational inefficiencies or higher costs.

Step 6: Applying Best Practices

- Use Common-Size Income Statements: Express all line items as a percentage of revenue to facilitate comparison.

- Analyze Expense Breakdown: Drill down into operating expenses to identify areas of cost increase.

- Consider Non-Recurring Items: Adjust net income for one-time expenses or gains.

- Review Notes and Disclosures: Look for explanations about margin changes.

Step 7: Example Conclusion and Recommendations

- Company A maintains stable gross margins, showing effective production cost control.

- Operating expenses are rising faster than revenue growth, pressuring operating margins.

- Net margins are declining, possibly due to increased financial costs or non-operating expenses.

Recommendations:

- Conduct a detailed expense audit to identify controllable costs.

- Evaluate pricing strategies to improve revenue growth without sacrificing market share.

- Explore refinancing options to reduce interest expenses.

- Monitor competitor moves and market trends to anticipate further margin pressures.

This example illustrates how investment professionals can systematically evaluate profitability trends by combining quantitative analysis with qualitative insights, enabling better investment decisions in competitive industries.

4. Cash Flow Statement and Its Strategic Importance

4.1 Structure of the Cash Flow Statement: Operating, Investing, and Financing Activities

The cash flow statement is a crucial financial document that provides insights into a company’s cash inflows and outflows over a specific period. Unlike the income statement, which shows profitability, the cash flow statement reveals the actual liquidity position by categorizing cash movements into three main activities: Operating, Investing, and Financing. Understanding these categories helps investment professionals assess the company’s cash generation ability, investment strategy, and financing decisions.

Mind Map: Overview of Cash Flow Statement Structure

Operating Activities

Operating activities reflect the core business operations that generate cash. This section adjusts net income for non-cash items and changes in working capital to arrive at cash generated or used by operations.

Key Components:

- Cash received from customers

- Cash paid to suppliers and employees

- Interest paid

- Income taxes paid

- Adjustments for non-cash expenses (depreciation, amortization)

- Changes in working capital (accounts receivable, inventory, accounts payable)

Best Practice: When analyzing operating cash flow, focus on the consistency and quality of cash generated relative to net income. A company with strong operating cash flow is generally more financially stable.

Example: Consider a retail company with a net income of $500,000. It reports depreciation expense of $50,000 (non-cash), an increase in accounts receivable of $30,000, and an increase in accounts payable of $20,000.

Operating cash flow calculation:

- Start with net income: $500,000

- Add back depreciation: +$50,000

- Subtract increase in accounts receivable: -$30,000

- Add increase in accounts payable: +$20,000

Operating Cash Flow = $500,000 + $50,000 - $30,000 + $20,000 = $540,000

This indicates the company generated $540,000 in cash from its core operations.

Investing Activities

Investing activities capture cash flows related to the acquisition and disposal of long-term assets and investments.

Key Components:

- Purchase of fixed assets (capital expenditures)

- Sale of fixed assets

- Purchase or sale of investments (e.g., securities, subsidiaries)

Best Practice: Analyze investing cash flows to understand the company’s growth strategy. Negative cash flow here often indicates investment in future growth, while positive cash flow may indicate asset sales.

Example: A manufacturing firm purchases new machinery for $200,000 and sells an old vehicle for $30,000 during the period.

Investing cash flow calculation:

- Cash outflow for machinery: -$200,000

- Cash inflow from vehicle sale: +$30,000

Net Investing Cash Flow = -$170,000

This suggests the company is investing heavily in its production capacity.

Financing Activities

Financing activities reflect cash flows related to changes in the company’s capital structure.

Key Components:

- Proceeds from issuing shares or debt

- Repayment of debt

- Payment of dividends

- Share repurchases

Best Practice: Evaluate financing cash flows to understand how the company funds its operations and growth, and how it returns value to shareholders.

Example: A company issues $100,000 in new debt, repays $40,000 of existing loans, and pays dividends of $10,000.

Financing cash flow calculation:

- Debt issuance: +$100,000

- Debt repayment: -$40,000

- Dividends paid: -$10,000

Net Financing Cash Flow = $50,000

This indicates the company raised more capital than it repaid and paid out dividends.

Mind Map: Detailed Cash Flow Activities

Summary

The cash flow statement’s tripartite structure provides a comprehensive view of how a company generates and uses cash. For investment professionals, dissecting each section with an eye on best practices and real examples enables a deeper understanding of liquidity, operational efficiency, investment strategy, and financing decisions.

By mastering the cash flow statement structure, analysts and bankers can better forecast future cash flows, assess financial health, and make informed investment or financing recommendations.

4.2 Free Cash Flow Calculation and Interpretation

Free Cash Flow (FCF) is a critical financial metric that investment professionals use to assess a company’s ability to generate cash after accounting for capital expenditures necessary to maintain or expand its asset base. Understanding and accurately calculating FCF helps in valuation, credit analysis, and strategic decision-making.

What is Free Cash Flow?

Free Cash Flow represents the cash a company generates from its operations minus the capital expenditures (CapEx) required to maintain or grow its asset base. It reflects the cash available to all capital providers, including debt and equity holders.

Formula:

\[ \text{Free Cash Flow} = \text{Operating Cash Flow} - \text{Capital Expenditures} \]

Alternatively, starting from Net Income:

\[ \text{FCF} = \text{Net Income} + \text{Non-Cash Charges} + \text{Changes in Working Capital} - \text{Capital Expenditures} \]

Why is Free Cash Flow Important?

- Valuation: FCF is the foundation for Discounted Cash Flow (DCF) valuation models.

- Financial Health: Indicates the company’s ability to generate cash to pay dividends, repay debt, or reinvest.

- Investment Decisions: Helps assess whether a company can sustain growth or requires external financing.

Mind Map: Components of Free Cash Flow

Step-by-Step Calculation Example

Company ABC’s Financial Data (in $ millions):

| Item | Amount |

|---|---|

| Net Income | 120 |

| Depreciation & Amortization | 30 |

| Increase in Accounts Receivable | (10) |

| Increase in Inventory | (5) |

| Increase in Accounts Payable | 8 |

| Capital Expenditures | 40 |

Step 1: Calculate Changes in Working Capital

\[ \text{Changes in Working Capital} = (\Delta \text{Accounts Receivable}) + (\Delta \text{Inventory}) - (\Delta \text{Accounts Payable}) \]

\[ = (-10) + (-5) - 8 = -10 - 5 - 8 = -23 \]

Note: Since Accounts Payable increase is a source of cash, it is subtracted here because of the sign convention; alternatively, some analysts add increases in payables.

Step 2: Calculate Operating Cash Flow (OCF)

\[ \text{OCF} = \text{Net Income} + \text{Depreciation} + \text{Changes in Working Capital} \]

\[ = 120 + 30 + (-23) = 127 \]

Step 3: Calculate Free Cash Flow (FCF)

\[ \text{FCF} = \text{OCF} - \text{Capital Expenditures} = 127 - 40 = 87 \]

Interpretation:

Company ABC generated $87 million in free cash flow, indicating strong cash generation after reinvesting in its assets.

Mind Map: Interpreting Free Cash Flow

Best Practices for FCF Calculation and Analysis

- Use Consistent Definitions: Different firms may report CapEx differently; verify what is included.

- Adjust for Non-Recurring Items: Remove one-time gains or losses to get normalized FCF.

- Analyze Over Multiple Periods: Look for trends rather than single-period snapshots.

- Compare with Net Income and Earnings: Large discrepancies may indicate accounting differences or cash flow issues.

- Consider Industry Norms: Capital intensity varies; benchmark against peers.

Example: Comparing Two Companies Using FCF

| Metric | Company X ($M) | Company Y ($M) |

|---|---|---|

| Net Income | 200 | 150 |

| Operating Cash Flow | 250 | 180 |

| Capital Expenditures | 100 | 90 |

| Free Cash Flow | 150 | 90 |

Analysis:

- Company X has higher net income and FCF, indicating more cash available after investments.

- Company Y’s lower FCF relative to net income suggests either higher reinvestment or less efficient cash conversion.

- Investment bankers might view Company X as having greater financial flexibility.

Summary

Free Cash Flow is a vital metric that bridges accounting profits and actual cash generation. For investment professionals, mastering FCF calculation and interpretation enables more accurate valuation, risk assessment, and strategic financial decisions.

4.3 Cash Flow vs. Earnings: Identifying Discrepancies

Understanding the differences between cash flow and earnings is critical for investment professionals. While earnings (net income) reflect profitability under accrual accounting, cash flow shows the actual liquidity generated or consumed by the business. Discrepancies between these two can reveal important insights about a company’s financial health, quality of earnings, and potential risks.

Key Concepts

- Earnings (Net Income): Profit reported on the income statement, calculated using accrual accounting principles. Includes non-cash items like depreciation, amortization, and accruals.

- Operating Cash Flow (OCF): Cash generated from core business operations, reported on the cash flow statement.

- Discrepancies: Differences between net income and operating cash flow that can indicate earnings quality issues, aggressive revenue recognition, or working capital management.

Mind Map: Cash Flow vs. Earnings Discrepancies

Why Discrepancies Matter

- Quality of Earnings: A company reporting strong net income but weak or negative operating cash flow may be inflating earnings through aggressive accounting or facing collection issues.

- Liquidity Insight: Cash flow reveals the actual cash available to meet obligations, pay dividends, or invest in growth.

- Risk Identification: Persistent negative cash flow despite reported profits can signal financial distress.

Example 1: Identifying Earnings Quality Issues

Scenario:

- Company A reports net income of $10 million.

- Operating cash flow is only $2 million.

Analysis:

- Investigate working capital changes: large increase in accounts receivable (+$8 million) suggests sales booked but cash not collected.

- Check for non-cash expenses: depreciation is $3 million, which reduces net income but doesn’t affect cash.

Conclusion: Earnings may be overstated due to aggressive revenue recognition or collection delays.

Mind Map: Analytical Approach to Discrepancies

Example 2: Positive Earnings but Negative Cash Flow

Scenario:

- Company B reports net income of $5 million.

- Operating cash flow is negative $3 million.

Investigation:

- Large inventory build-up of $7 million indicates cash tied up in unsold goods.

- Accounts payable decreased by $2 million, meaning the company paid off suppliers faster.

Implication:

- Despite profitability, cash is being consumed, which may affect the company’s ability to fund operations or service debt.

Best Practices for Investment Professionals

- Always analyze operating cash flow alongside net income to assess earnings quality.

- Use cash flow to net income ratio as a quick check (ideal ratio is close to or above 1).

- Investigate significant changes in working capital accounts for cash flow impacts.

- Adjust earnings for non-cash items to get a clearer picture of cash-generating ability.

- Be cautious of companies with persistent divergence between earnings and cash flow.

Summary Table: Common Causes of Discrepancies

| Cause | Effect on Earnings | Effect on Cash Flow | Notes |

|---|---|---|---|

| Depreciation & Amortization | Decreases earnings (non-cash) | No cash impact | Normal accounting adjustment |

| Increase in Accounts Receivable | Increases earnings (revenue recognized) | Decreases cash | Cash not yet collected |

| Increase in Inventory | No immediate earnings impact | Decreases cash | Cash tied up in stock |

| Decrease in Accounts Payable | No immediate earnings impact | Decreases cash | Paying suppliers faster |

| One-time Gains (Asset Sales) | Increases earnings | Increases cash | May distort ongoing earnings |

By mastering the analysis of cash flow versus earnings discrepancies, investment professionals can better evaluate the true financial performance and sustainability of a company, leading to more informed investment decisions.

4.4 Best Practice: Forecasting Cash Flows for Valuation and Credit Analysis