EBITDA, Free Cash Flow, and Earnings Quality Analysis Essentials

1. Foundations for Cash and Earnings Quality Analysis

1.1 Define Performance Objectives and Decision Use Cases

Before you compute EBITDA, free cash flow, or earnings quality scores, you need to decide what “good” means for a specific decision. Otherwise, you end up with a spreadsheet full of numbers and no agreement on what they’re supposed to answer. Performance objectives translate analysis into questions like: “Can this business generate cash from operations consistently?” or “Are reported profits supported by cash, or are they mostly accounting timing?”

Start with the Decision, Not the Metric

A metric is a tool; a decision is the job. Common decision use cases include:

- Credit risk screening: Determine whether cash generation can cover interest and principal.

- Equity valuation support: Assess whether earnings are likely to persist and whether cash supports reinvestment.

- Operational diagnosis: Identify whether working capital or capex patterns explain cash shortfalls.

- Quality control for reporting: Detect aggressive adjustments that inflate earnings without cash backing.

Each use case implies different emphasis. For example, a credit decision cares more about cash coverage and downside resilience, while an operational diagnosis may focus on working capital drivers.

Define the Objective in Measurable Terms

Turn the broad goal into a measurable objective with a clear target and time horizon. A practical template:

- Decision: What decision will be made?

- Time horizon: Quarterly, annual, or multi-year.

- Success criterion: What threshold or pattern counts as acceptable?

- Evidence required: Which statements and line items must support the conclusion?

- Action link: What will you do if the evidence fails?

Example objective: “For the last four quarters, operating cash flow should generally track EBITDA, and free cash flow should remain positive after maintenance-like capex.” The phrase “generally track” forces you to define tolerances, not just eyeball charts.

Map Metrics to Evidence Types

To keep analysis coherent, classify each metric by what it measures and what it can miss.

- EBITDA: Approximates operating profitability before depreciation and amortization, but it ignores cash timing and working capital changes.

- Free Cash Flow: Captures cash after capex and working capital effects, but it depends heavily on capex classification and cash flow statement presentation.

- Earnings quality signals: Uses accrual behavior to judge whether earnings are supported by cash or by accounting timing.

A good workflow uses all three: EBITDA helps interpret operating performance, free cash flow tests cash reality, and earnings quality diagnostics explain the gap.

Mind Map: Objectives, Questions, and Evidence

Example: Choosing Objectives for Two Different Decisions

Consider the same company with strong EBITDA but weak free cash flow.

- Credit screening objective: “Assess whether cash from operations can cover interest after normal working capital swings.” Evidence focus: operating cash flow trend, receivables/payables changes, and interest coverage using cash.

- Equity analysis objective: “Assess whether earnings are likely to persist and whether reinvestment needs are sustainable.” Evidence focus: margin stability, capex intensity and classification, and accrual patterns in revenue and expenses.

Both decisions may use EBITDA and free cash flow, but the success criteria and the “why” behind the gap differ.

Define Your Tolerance for “Consistency”

Consistency is not a vibe; it’s a rule. Decide what counts as acceptable variation.

- If you’re evaluating cash coverage, define a minimum coverage ratio or a maximum number of consecutive weak periods.

- If you’re evaluating earnings quality, define what level of accrual-cash divergence triggers follow-up.

A simple rule for early screening: “Flag cases where operating cash flow is negative while EBITDA is positive for two consecutive quarters, unless working capital movements are clearly explained.” This turns a vague concern into a repeatable trigger.

Document Assumptions Before Calculations

Write down definitions and constraints that affect interpretation. For instance:

- Which capex categories are treated as maintenance-like versus growth-like.

- Whether you will adjust for discontinued operations or one-time items.

- How you will treat changes in accounting policies.

Even a short note prevents later confusion when two analysts compute different “free cash flow” versions and both claim they’re correct.

Case Study: A Clean Objective Statement

On 2026-04-05, an analyst is asked to support a lending decision for a mid-sized manufacturer. The objective is documented as: “Over the last four quarters, confirm that free cash flow after maintenance-like capex is non-negative in at least three quarters, and that the largest negative quarter has an identifiable working capital or capex explanation supported by statement line items.”

That objective dictates the evidence you must pull, the checks you must run, and the standard for concluding whether the business is cash-capable or merely accounting-profitable.

1.2 Distinguish Accounting Profit From Cash Generation

Accounting profit and cash generation measure different things. Profit is an accounting result shaped by recognition rules, estimates, and timing. Cash generation is the actual movement of money through the business. Confusing the two is how you end up praising “earnings strength” while the bank balance quietly files for divorce.

Profit Is Not Cash

Profit starts with revenues and expenses recognized under accrual accounting. Revenues are recorded when earned, not when cash is received. Expenses are recorded when incurred, not when paid. That means profit can rise even if cash is delayed, and profit can fall even if cash is temporarily strong.

A simple example: a company sells $1,000 of goods on credit in December. If the customer pays in January, December profit includes the $1,000 revenue, but December cash does not. The gap is not a moral failing; it’s a timing difference.

Cash Generation Is Not Profit

Cash generation comes from cash receipts and cash payments. It is affected by working capital movements, capital spending, taxes paid, and interest paid. A company can report solid profit while cash drains due to growing receivables, rising inventory, or large tax payments.

Consider a retailer that expands aggressively. It may record profit from higher sales, but it also buys inventory and extends credit to customers. If receivables and inventory increase faster than payables, cash can decline even while profit looks fine.

The Core Bridge: Accruals and Timing

The practical way to distinguish profit from cash is to track the accrual components that sit between them. Accruals typically show up in:

- Receivables: revenue recognized before cash collection.

- Inventory: costs recognized through cost of goods sold before cash is paid or after cash is paid depending on purchase timing.

- Payables and accrued expenses: expenses recognized before cash payment.

When these balances change, they influence cash from operations. If profit is high but receivables rise, cash from operations often lags.

Mind Map: Profit Versus Cash Signals

Worked Example: Same Profit, Different Cash

Assume a company reports $500 of accounting profit for the quarter. During the quarter:

- Receivables increase by $120 (cash not yet collected)

- Inventory increases by $60 (cash tied up in stock)

- Payables increase by $40 (cash payments delayed)

Net working capital effect on cash is typically negative: $120 + $60 − $40 = $140 of cash drag. Even with $500 profit, cash from operations may be closer to $360 before considering non-cash items like depreciation.

This is the key distinction: profit can be “earned” while cash is “still traveling.”

Worked Example: Cash Without Profit

Now flip the scenario. Suppose profit is $200, but the company collects $300 of prior-period receivables this quarter. Cash from operations can be strong even if current-period sales are weaker. That doesn’t mean the business is magically healthier; it means cash timing improved.

How to Tell the Difference in Practice

Use a consistent workflow:

- Start with profit from the income statement.

- Identify non-cash items that affect profit but not cash (for example, depreciation).

- Track working capital changes to see whether profit is converting into cash.

- Check cash flow classification so you don’t treat financing cash as operating cash.

A quick rule of thumb: if profit is rising while receivables and inventory also rise, expect cash conversion to be weaker unless payables rise enough to offset it.

Common Pitfalls to Avoid

- Equating EBITDA with cash: EBITDA removes depreciation and amortization, but it does not remove working capital effects.

- Ignoring tax and interest cash: profit includes tax expense and interest expense under accrual rules, while cash reflects what was actually paid.

- Treating one quarter as a verdict: timing differences can dominate short periods; patterns across quarters clarify whether the gap is structural or temporary.

Mini Case: A Single Line Item Can Explain the Gap

If a company’s profit is stable but cash from operations falls sharply, look first at receivables and inventory changes. A large receivables increase often explains a lot, because it directly signals that revenue recognized is not yet collected. That’s the cleanest way to distinguish “earned” from “received.”

1.3 Map Financial Statements to Cash Flow Mechanics

Mapping financial statements to cash flow mechanics is about tracing “what the numbers claim” to “what cash actually did.” The trick is to treat each statement as a different lens on the same underlying events: transactions first hit the income statement through accruals, then show up in the cash flow statement through timing, and finally settle in the balance sheet through working capital and non-cash items.

The Core Link Between Statements

Start with the accounting identity: cash flow is driven by cash receipts and cash payments, while net income is driven by accrual recognition. That gap is not a flaw; it’s the reason the cash flow statement exists.

A practical mapping workflow looks like this:

- Identify the income statement line items that are mostly non-cash (depreciation, amortization, impairments, stock-based compensation).

- Identify the income statement line items that are cash-sensitive but timing-shifted (revenue, cost of sales, operating expenses).

- Use the balance sheet to measure timing shifts via changes in working capital accounts.

- Reconcile the result to the cash flow statement sections: operating, investing, and financing.

Operating Cash Flow Mechanics

Operating cash flow (OCF) is where the mapping gets most concrete. In the indirect method, OCF begins with net income and adjusts for:

- Non-cash expenses added back (e.g., depreciation)

- Non-cash gains subtracted (e.g., gains on asset sales)

- Changes in working capital that reflect timing differences

Working capital mapping is the bridge between accruals and cash. For example, if revenue is recognized before cash is received, accounts receivable rises and OCF falls relative to net income.

Example:

- Net income: $100

- Depreciation: +$20 (non-cash)

- Increase in accounts receivable: -$15 (cash not yet collected)

- Increase in accounts payable: +$5 (cash payments delayed)

- Other working capital changes net: -$3

Mapped OCF: 100 + 20 − 15 + 5 − 3 = $107. The income statement said “profit,” but the balance sheet said “timing,” and the cash flow statement reports the combined effect.

Investing Cash Flow Mechanics

Investing cash flow maps to changes in long-term assets and the cash effects of buying or selling them.

- Purchases of property, plant, and equipment (capex) reduce cash.

- Proceeds from asset sales increase cash.

- Acquisitions and divestitures show up as larger investing movements.

A common mapping pitfall is confusing depreciation with capex. Depreciation affects net income (non-cash), while capex affects cash (cash outflow). A company can show strong OCF while still spending heavily on capex, because the cash payment is recorded in investing activities.

Example:

- Depreciation expense: $20

- Capex during the year: $60

Even if net income is supported by depreciation, cash still left the business for new or maintained assets.

Financing Cash Flow Mechanics

Financing cash flow maps to capital structure actions and cash settlements with providers of capital.

- Issuing shares or repurchasing shares

- Borrowing or repaying debt

- Paying dividends

- Lease payments split between interest and principal depending on reporting conventions

Mapping here is about separating operating performance from capital structure effects. Interest expense appears in the income statement, but the cash paid for interest typically appears in financing or operating sections depending on reporting rules. The balance sheet helps confirm the cash settlement through changes in debt and accrued interest.

Mind Map: Statement to Cash Flow Mapping

A Systematic Mapping Checklist

Use this checklist to avoid gaps:

- For each major income statement item, ask: “Is this mostly non-cash, timing-shifted cash, or cash-settled?”

- For each working capital account, ask: “What accrual created this balance, and what cash movement would reverse it?”

- For each investing and financing line, ask: “Which balance sheet accounts changed, and does the cash flow match the settlement?”

Putting It Together with One Integrated Walkthrough

Take a year where net income is $100. Depreciation adds $20 to OCF. Receivables rise by $15, inventory rises by $8, and payables rise by $6. Those working capital changes explain why OCF might be lower than net income even after non-cash add-backs. Then capex of $60 appears in investing cash flow, and debt repayment of $25 appears in financing cash flow. The full mapping shows that “profit” and “cash” can move differently for understandable reasons: accrual timing, asset investment, and capital structure decisions.

When you can produce that walk-through from the statements alone, you’ve mapped financial statements to cash flow mechanics in a way that supports later EBITDA and earnings quality analysis.

1.4 Identify Common Misinterpretations of EBITDA and Earnings

EBITDA and earnings are often treated as interchangeable “performance” measures. They are not. EBITDA is a profitability proxy that removes interest, taxes, depreciation, and amortization; earnings are the accounting result after all those items and after accrual-based revenue and expense recognition. Misinterpretations usually come from mixing these different purposes into one mental model.

Mind Map: Where Misinterpretations Start

EBITDA Misread as Cash Generation

A common mistake is to assume that if EBITDA is rising, cash generation must be rising too. EBITDA can increase while cash falls when working capital consumes cash. For example, suppose a retailer reports EBITDA of $50 million, but accounts receivable increases by $20 million and inventory increases by $10 million during the year. Cash from operations will be pressured because customers paid later and goods sat longer. EBITDA did not “cause” cash; it only described earnings before certain non-cash and financing items.

Another frequent error is to ignore capital expenditures. EBITDA excludes depreciation, but depreciation is not the same thing as spending. A software company may show stable EBITDA while still investing heavily in servers, development, or platform upgrades. If those investments are expensed immediately, EBITDA may look strong while free cash flow is weak. If they are capitalized, EBITDA may look even stronger because expenses are deferred.

Earnings Misread as Sustainable Profit

Earnings are often treated as a direct measure of cash profitability and sustainability. Yet earnings can be supported by accruals that reverse later. Consider a construction firm that recognizes revenue when milestones are achieved. If billings lag collections, earnings can rise even as cash stays flat. Later, when the firm collects cash, earnings may not rise again because the revenue was already recognized.

Earnings can also be distorted by accounting choices that affect timing. A simple example: a company changes its estimate of bad debt expense. If it reduces the allowance for doubtful accounts, earnings improve immediately, even if cash collections have not improved. The “profit” is real in accounting terms, but the quality is questionable because it depends on assumptions.

Adjusted EBITDA and the Definition Problem

“Adjusted EBITDA” is where comparability goes to die—quietly. Companies may exclude restructuring costs, stock-based compensation, litigation expenses, or “non-recurring” items. The misinterpretation is treating adjusted EBITDA as a clean, objective measure. In practice, exclusions can be frequent enough to become recurring. If a firm reports adjusted EBITDA that removes restructuring every year, the adjustment is no longer a one-off; it is part of the business’s operating reality.

A practical check is to ask: “Would a rational investor still expect these exclusions to be absent in the future?” Even without forecasting, you can test whether the excluded items appear consistently in the notes or in the cash flow statement.

A Simple Earnings vs EBITDA Reality Check

Use a two-step logic: (1) identify what EBITDA and earnings include or exclude, then (2) identify what can still move cash.

- EBITDA excludes interest and taxes, so it can look strong even when financing costs are heavy.

- EBITDA excludes depreciation and amortization, so it can look strong even when asset replacement is costly.

- Earnings include interest and taxes, but they still rely on accrual timing for revenue and expenses.

Example: Same EBITDA, Different Cash Outcomes

Company A and Company B both report EBITDA of $100 million. Company A has stable working capital and moderate capex; its free cash flow is $70 million. Company B has EBITDA of $100 million but working capital consumes $40 million of cash and capex is $30 million; its free cash flow is $30 million. The misinterpretation would be to rank A and B by EBITDA alone. The integrated view is that cash depends on working capital and investment needs, not just on operating profitability before certain accounting items.

Example: Same Earnings, Different Quality

Company C reports net income of $60 million. Its accounts receivable rises sharply, and operating cash flow is only $20 million. The misinterpretation is to treat net income as high-quality profit. A more careful read connects the accruals: revenue recognized without cash collection often signals lower earnings quality, even if the income statement looks fine.

Mind Map: Quick Diagnostic Questions

Practical Takeaway

EBITDA and earnings are useful, but they answer different questions. EBITDA helps isolate operating profitability before financing and non-cash charges; earnings reflect accounting profit after accrual timing and financing/tax effects. Misinterpretations happen when you treat either measure as a direct proxy for cash without checking working capital, investment needs, and the consistency of definitions.

1.5 Establish an Evidence Based Workflow for Quality Assessment

A quality assessment is only as good as its evidence trail. The goal is simple: decide whether reported performance is likely to be repeatable, and explain why using items you can point to in the statements and notes. A good workflow moves from definitions to measurements, then to tests, and finally to a documented conclusion.

Step 1: Fix Definitions Before You Touch the Numbers

Start by writing down what you mean by each metric you will use. For example, if you plan to compare EBITDA to free cash flow, you must choose a free cash flow definition and stick to it. A practical approach is to define free cash flow as operating cash flow minus capital expenditures, using the cash flow statement line items. Then define earnings quality signals you will test, such as accrual intensity, working capital drift, and cash tax behavior.

Example: Suppose a company reports EBITDA of $120 million and operating cash flow of $70 million. If you define free cash flow as $70 million minus $40 million of capex, you get $30 million. If you later use a different capex definition, your conclusion about cash conversion can flip.

Step 2: Build a Statement Map You Can Reconcile

Create a one-page map that links each metric to its source. Income statement items feed EBITDA; cash flow items feed free cash flow; balance sheet movements explain the “why” behind cash differences. This prevents the common mistake of treating EBITDA as a cash proxy without checking the mechanics.

Step 3: Collect Evidence with a Purpose, Not a Checklist

Evidence should answer specific questions. For earnings quality, the questions are usually: Are earnings supported by cash? Are accruals stable or erratic? Do working capital movements look like timing or like ongoing strain? Are capex levels consistent with the business model? Notes are where you confirm accounting policies and identify adjustments that may not be repeatable.

Example: If management excludes “non-recurring” items from EBITDA, record the exact line items they come from, the accounting basis, and whether similar items appeared in prior periods. If the exclusions cluster around the same type of charge every year, it is not truly non-recurring.

Step 4: Run Diagnostic Tests in a Logical Order

Use tests that build on each other.

-

Cash Conversion Test: Compare operating cash flow to EBITDA over multiple periods. Look for persistent gaps rather than one-off differences.

-

Accrual Intensity Test: Compute accruals as earnings minus operating cash flow. Large swings often indicate timing effects or aggressive recognition.

-

Working Capital Quality Test: Break down changes in receivables, inventory, and payables. A company can “earn” revenue while cash lags if collections slow, or it can generate cash by stretching payables.

-

Capex Quality Test: Check whether capex is maintenance-like or growth-like using disclosures and asset commentary. Also verify whether asset sales inflate cash.

-

Tax and Interest Cash Test: Reconcile tax expense to cash taxes paid and compare interest expense to cash interest. If cash taxes diverge sharply from accounting tax expense without explanation, earnings can be less reliable.

Example: A retailer shows stable EBITDA but recurring negative free cash flow. Working capital analysis reveals receivables rising faster than revenue, while inventory turns slow. That pattern points to collection and inventory management issues, not just accounting noise.

Step 5: Apply Decision Rules and Document the Reconciliation

Evidence becomes useful when you convert it into a decision. Create simple thresholds tied to your definitions. For instance, you might flag “quality concern” when free cash flow is negative for multiple consecutive years while EBITDA remains positive, or when accrual intensity is consistently large relative to earnings.

Then document the reconciliation: EBITDA to operating cash flow, and operating cash flow to free cash flow. Include the drivers you identified—working capital changes, capex, and cash taxes—so the conclusion is traceable.

Step 6: Produce a Clear Quality Conclusion

Write the conclusion as a short chain of evidence. Example structure: “EBITDA is positive, but operating cash flow trails due to receivables growth and slower inventory turnover. Capex is consistent with the business, and cash taxes track accounting taxes. Therefore, earnings appear less supported by cash in the current period.”

This keeps the analysis grounded: you are not guessing; you are connecting reported numbers to the cash mechanics that make them real.

2. EBITDA Construction and Interpretation in Financial Statements

2.1 Start with Reported Earnings and Reconcile to EBITDA

EBITDA starts life as a simple idea: take earnings from the income statement and remove items that are not meant to represent day-to-day operating performance. The key word is “meant.” Different companies define EBITDA differently, so your first job is to reconcile from reported earnings using a definition you can defend.

What Reported Earnings Means in Practice

Most companies report “net income” or “income before tax” and then include interest and other items. To reconcile to EBITDA, you typically begin with a pre-financing, pre-tax earnings measure such as operating income or earnings before tax, depending on the company’s starting point. If you start from net income, you must add back taxes, interest, and other non-operating items—more steps, more chances to mismatch.

A clean workflow is:

- Choose the starting line item that best matches the company’s EBITDA definition.

- Add back depreciation and amortization.

- Add back interest and taxes if they are excluded in the definition.

- Remove or adjust other items the company treats as “non-recurring” or “non-operating.”

- Confirm the math with a reconciliation table.

Mind Map: From Reported Earnings to EBITDA

A Systematic Reconciliation Method

Use a bridge that mirrors the income statement logic. The bridge should show each adjustment explicitly, not as a single lump sum.

Step 1: Pick the starting earnings line. If the company’s EBITDA is presented in the notes, it often starts from operating profit. If not, you can infer the starting point by testing which combination of add-backs lands you closest to the reported EBITDA.

Step 2: Add back depreciation and amortization. Depreciation and amortization are usually the largest and most stable adjustments. For example, if operating income is 120 and depreciation and amortization is 40, your interim total becomes 160 before considering interest and taxes.

Step 3: Handle interest and taxes according to the definition. If EBITDA is defined as earnings before interest and taxes, you add back interest expense and tax expense. Suppose interest expense is 15 and tax expense is 25. Adding both to 160 gives 200.

Step 4: Treat other adjustments carefully. Some companies adjust for restructuring, impairments, or gains/losses on asset sales. If you include these, you must use the same sign convention the company uses. For instance, an impairment charge reduces earnings; adding it back increases EBITDA.

Step 5: Validate with a tie-out. Your final EBITDA should match the company’s reported EBITDA within rounding. If it doesn’t, the mismatch usually comes from one of these issues:

- You started from the wrong earnings line.

- You missed a component of depreciation and amortization.

- You misread whether an item is included in operating income.

- You applied an adjustment with the wrong direction.

Example: A Worked Reconciliation

Assume a company reports:

- Operating income: 120

- Depreciation and amortization: 40

- Interest expense: 15

- Tax expense: 25

- Restructuring charge: 10 (included in operating income)

- Gain on asset sale: 6 (included in operating income)

If the company’s EBITDA definition excludes interest, taxes, and includes add-backs for restructuring while excluding gains on asset sales, the bridge is:

- Start with operating income: 120

- Add D&A: +40 → 160

- Add restructuring: +10 → 170

- Remove asset sale gain: −6 → 164

- Add interest: +15 → 179

- Add taxes: +25 → 204

So EBITDA is 204. If the company reports EBITDA of 203 due to rounding, you can accept the difference; if it reports 220, you need to revisit the starting line or the adjustment list.

Common Pitfalls That Break the Bridge

A reconciliation is only as good as its assumptions. Watch for:

- Double counting: If depreciation is already excluded in the starting line, adding it back again inflates EBITDA.

- Hidden components: Some companies split amortization into multiple lines; you must capture all relevant items.

- Inconsistent treatment across periods: If the company changes its EBITDA definition, you should reconcile each period using the same logic or clearly document the change.

Practical Output: What You Should Record

For each period, keep a short reconciliation table with the exact line items used and a note on the EBITDA definition source. This turns EBITDA from a number into a traceable calculation—useful when you later compare EBITDA to free cash flow and ask whether “operating performance” is actually paying its bills.

2.2 Understand Depreciation and Amortization Treatment

Depreciation and amortization are accounting methods for allocating the cost of long-lived assets over time. They matter for EBITDA because EBITDA adds back depreciation and amortization, but they matter for cash flow because the underlying assets still require real spending—either now (when purchased) or later (when replaced). A good analysis keeps two ideas in view: (1) the accounting expense is a timing allocation, and (2) the cash impact depends on capital spending and asset turnover.

What Depreciation and Amortization Actually Do

Depreciation applies to tangible assets like buildings, equipment, and vehicles. Amortization applies to intangible assets like patents, customer relationships, and software. Both reduce accounting profit without directly consuming cash in the period they are recorded.

A simple example: a company buys a machine for $1,000,000. If it is depreciated straight-line over 10 years, the income statement shows $100,000 depreciation each year. Cash leaves at purchase, not at the moment the expense is recognized. That’s why EBITDA can look strong while free cash flow is weak.

The Mechanics Behind the Expense

Depreciation and amortization require three inputs:

- Cost basis: what the asset cost (net of any salvage value for depreciation).

- Useful life: how long the company expects to benefit from the asset.

- Method: how the expense is allocated (commonly straight-line; sometimes units-of-production or declining balance).

If useful life changes, the accounting expense changes too. For instance, extending a useful life from 8 to 10 years lowers annual depreciation, improving earnings and EBITDA (since EBITDA adds it back anyway, the effect shows up more in net income and operating profit). The cash story doesn’t magically improve; it reflects whether the company is still investing at a similar pace.

Where It Appears in Financial Statements

Depreciation and amortization usually show up in operating expenses, cost of revenue, or both. They also reduce the carrying value of assets on the balance sheet through accumulated depreciation or amortization.

A practical check: if depreciation expense rises but capital expenditures are flat, the company may be running down older assets or changing estimates. If both rise, the company may be investing heavily and ramping production capacity. If depreciation falls while capex rises, the company might be shifting toward assets with different useful lives or capitalization policies.

How EBITDA Treatment Can Mislead

EBITDA adds back depreciation and amortization to remove non-cash charges. That is reasonable for comparing operating performance across firms with different capital intensity, but it becomes misleading when depreciation is a proxy for “how much the business has been investing.”

Example: Company A has $50 million depreciation and $10 million capex. Company B has $50 million depreciation and $60 million capex. Even if EBITDA is identical, Company B is funding replacement and growth through cash outflows, while Company A may be under-investing relative to its asset base. The accounting expense alone can’t tell you which situation you’re in; you need the link to cash.

Mind Map: Depreciation and Amortization Treatment

Advanced Details That Change the Numbers

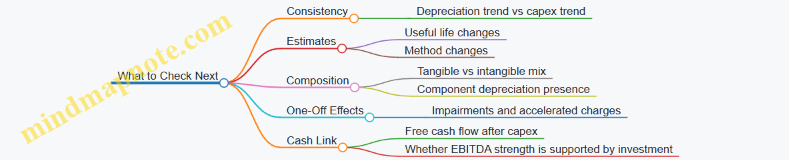

1. Componentization and major parts. Some companies depreciate major components separately. A building might have a structure and a roof with different useful lives. Componentization increases the likelihood that depreciation changes as parts are replaced.

2. Impairments. If an asset is impaired, accounting charges can accelerate the expense pattern. Depreciation may not fully capture the economic wear-and-tear if impairment losses are significant.

3. Capitalization policies. Costs can be expensed or capitalized depending on accounting rules and management judgment. If more costs are capitalized, future depreciation rises while current expenses fall. That can make EBITDA look better in the short run because fewer operating expenses are recognized.

4. Reassessments of useful lives. Changes in estimates alter the expense schedule. Two firms with the same asset base can report different depreciation simply due to different assumptions.

Example: Linking Depreciation to Asset Replacement

Assume a firm reports $30 million depreciation and $25 million capex in a year.

- If capex is mostly maintenance, depreciation roughly matches the consumption of the asset base, and free cash flow is more likely to be stable.

- If capex is mostly growth, depreciation may lag behind the new asset base, and future depreciation could rise even if cash spending continues.

Now add one more check: if depreciation is rising while capex is falling, the firm may be relying on an older asset base and not replacing it. That pattern can still produce positive EBITDA, but it often shows up as weaker free cash flow once working capital and capex needs catch up.

Mind Map: What to Check Next

Depreciation and amortization are not “fake” expenses, but they are not cash expenses either. Treat them as a structured way to allocate past spending, then test whether the company’s current cash spending supports the asset base that generates earnings.

2.3 Analyze Interest Taxes and Other Non Operating Items

EBITDA is often treated as a “clean” operating measure, but it still depends on what the income statement labels as operating versus non operating. This section helps you analyze interest, taxes, and other non operating items so you can interpret EBITDA adjustments without accidentally mixing operating performance with financing or accounting artifacts.

Start with the Income Statement Labels

Begin by locating three lines (or their equivalents): interest expense, income tax expense, and any other non operating items such as gains or losses on investments, foreign exchange, or restructuring. The key best practice is to treat these lines as separate “sources of variation” rather than noise. If EBITDA is meant to reflect operations, then interest and taxes should not be driving your operating conclusions.

A simple check: if a company’s EBITDA margin is stable while net income swings sharply, the swing likely sits in interest, taxes, or non operating items. That’s not a guarantee, but it’s a useful first filter.

Interest Expense: Financing Cost, Not Operating Cost

Interest expense reflects capital structure and borrowing terms. Two companies can have identical operations but different interest expense due to leverage or interest rates. When you reconcile from earnings to EBITDA, you typically add back interest expense (and sometimes other financing-related items depending on the definition used).

Easy example: Company A reports earnings of 100, interest expense of 20, and tax expense of 30. If EBITDA is computed as earnings + interest + taxes + depreciation and amortization (plus any standard adjustments), then interest is explicitly excluded from EBITDA. If Company A’s interest expense rises from 20 to 35 while earnings stay similar, EBITDA should not be interpreted as deteriorating unless operating lines also change.

Advanced detail: interest can be split between continuing operations and discontinued operations, or between “interest expense” and “other income/expense.” If you only add back the interest line but the company nets interest elsewhere, your reconciliation will be inconsistent.

Income Tax Expense: The Cash Reality Behind the Accrual

Tax expense is an accrual-based measure that can differ from cash taxes due to timing differences, tax credits, and valuation allowances. For EBITDA analysis, taxes are usually excluded, but you still need to understand why tax expense is moving.

Practical approach:

- Compare tax expense to earnings before tax to infer the effective tax rate.

- Check whether the company discloses discrete items such as one-time tax benefits, jurisdictional mix changes, or valuation allowance adjustments.

Example: Company B has earnings before tax of 200 and tax expense of 10, implying a very low effective tax rate. If EBITDA is steady, the low tax expense may be driven by discrete tax benefits rather than improved operating performance. Your reconciliation should reflect that taxes are excluded from EBITDA, but your interpretation of net income should note the tax driver.

Other Non Operating Items: Gains, Losses, and Accounting Timing

“Other non operating items” can include:

- Gains or losses on asset sales

- Impairments and reversals

- Foreign exchange gains or losses

- Equity method earnings

- Restructuring charges presented outside operating profit

The best practice is to classify each item by its economic nature and its placement on the income statement. If an item is recurring and tied to operations, excluding it from EBITDA may distort operating performance. If it is truly non operating or non recurring, excluding it can improve comparability.

Example: Company C reports a large gain from selling a property. Net income jumps, but EBITDA does not. If you only look at net income, you might conclude profitability improved. If you look at the non operating gain, you correctly attribute the jump to a one-time transaction.

Mind Map: How to Analyze Interest, Taxes, and Non Operating Items

A Worked Reconciliation Mini-Example

Assume Company D reports:

- Earnings: 120

- Interest expense: 18

- Tax expense: 42

- Depreciation and amortization: 60

- Non operating gain on asset sale: -25 (a gain reduces expense)

If EBITDA is defined as earnings + interest + taxes + depreciation and amortization, then EBITDA = 120 + 18 + 42 + 60 = 240. The asset sale gain affects net income but not EBITDA under this definition because it is not part of operating profit. Your interpretation should explicitly note that net income includes a non operating gain, while EBITDA excludes it.

Common Pitfalls to Avoid

-

Mixing financing items into operating adjustments. If you adjust EBITDA for items that are actually financing-related, you lose the point of excluding interest.

-

Treating tax expense as a proxy for operating quality. Taxes can be driven by jurisdictional mix or discrete items, not by operational improvements.

-

Ignoring where the company hides non operating items. A gain or loss may appear in “other income/expense” rather than a dedicated line, so your reconciliation must follow the company’s presentation.

By the end of this step, you should be able to explain why net income differs from EBITDA using three buckets: interest, taxes, and other non operating items—each with a clear, evidence-based reason.

2.4 Evaluate EBITDA Margin and Trend Using Consistent Bases

EBITDA margin is a ratio: EBITDA divided by a revenue base. The “consistent bases” part matters because EBITDA itself can be computed in multiple ways, and the denominator can be defined differently across companies and even across periods. If you mix definitions, the margin trend becomes a story about accounting choices rather than operating performance.

Start with a Single EBITDA Definition

Pick one EBITDA definition and stick to it for the entire analysis. A practical approach is to begin with reported operating profit (or net income) and reconcile to EBITDA using the same adjustment logic each period. For example, if you exclude restructuring charges in one year, you should exclude them in every year. If you include stock-based compensation in EBITDA (common in many reported EBITDA figures), keep that treatment consistent.

A quick sanity check: compute EBITDA margin for two adjacent years using your chosen definition. If the margin swings wildly while the business description suggests stability, you likely changed the EBITDA build or missed an item that moved between “operating” and “non-operating.”

Choose a Revenue Base That Matches the Business

EBITDA margin uses a revenue denominator. Common choices include:

- Total revenue (most straightforward)

- Revenue from continuing operations only (if discontinued operations exist)

- Segment revenue for a segment-level view

Consistency rule: the denominator should match the scope of the EBITDA numerator. If EBITDA is built from continuing operations, the revenue base should also be continuing operations revenue.

Example: Company A reports a discontinued business in 2024. If you compute EBITDA using only continuing operations but divide by total revenue including the discontinued business, the margin will look artificially low in 2024 and artificially high in 2023.

Normalize for Currency, Consolidation, and Reporting Changes

Even with a fixed EBITDA definition, trends can be distorted by structural changes:

- Currency translation: use the same currency basis across periods (often reported currency, or a consistent constant-currency approach if you choose it)

- Consolidation changes: acquisitions and disposals can shift margins even if the core business is stable

- Reporting reclassifications: companies sometimes move items between cost of revenue and operating expenses

Consistency rule: when you see a reporting change, either restate the prior period using the company’s own restatement (if provided) or keep the original reported figures and explicitly note the scope change in your working papers.

Use a Margin Trend with a Clear Time Window

A one-year comparison is fragile. A three- to five-year window usually reveals whether margin movement is persistent or a one-off. The goal is not to predict; it is to understand whether the margin change is systematic.

A simple method:

- Compute EBITDA margin for each year.

- Compute year-over-year change in margin.

- Separate “level shifts” from “gradual drift.”

Level shift example: EBITDA margin jumps from 12% to 18% in one year. That often points to a one-time cost reduction, a pricing change, or a structural change in revenue mix.

Gradual drift example: margin moves from 12% to 13% to 13.5% over several years. That can reflect steady operating leverage, cost discipline, or gradual mix changes.

Break Margin Into Drivers Using a Consistent Bridge

EBITDA margin can be decomposed into revenue growth and EBITDA margin components. A clean way is to build a bridge from revenue to EBITDA using consistent line items.

Worked Example with Consistent Bases

Assume Company B reports:

- 2023 revenue: 1,000

- 2024 revenue: 1,100

- EBITDA (your consistent definition): 150 in 2023, 180 in 2024

EBITDA margin:

- 2023: 150 / 1,000 = 15.0%

- 2024: 180 / 1,100 = 16.4%

Interpretation with discipline:

- Margin increased by 1.4 percentage points, not just because revenue grew.

- To understand why, you would next examine whether EBITDA grew faster than revenue, and whether the change came from recurring cost structure or from adjustments you included consistently.

If, instead, you had divided 2024 EBITDA by a different revenue base (say, revenue including a discontinued unit), the margin might have fallen, and you would incorrectly conclude that profitability weakened.

Common Pitfalls and How to Avoid Them

- Mixing EBITDA definitions across years: fix by locking the adjustment policy.

- Using total revenue when EBITDA is from continuing operations: fix by matching scope.

- Ignoring reporting changes: fix by documenting scope and consolidation effects in your margin worksheet.

- Overreacting to a single-year spike: fix by using a multi-year window and checking for level shifts.

A consistent margin trend is less about finding the “right” number and more about ensuring the number is comparable. Once comparability is solid, the margin trend becomes a reliable starting point for deeper earnings quality work.

2.5 Use EBITDA Bridge Techniques with Worked Examples

An EBITDA bridge is a structured reconciliation that shows how you move from a reported earnings figure to an EBITDA figure, and then how you explain the main drivers of change across periods. Done well, it prevents two common errors: (1) treating EBITDA as a magic number, and (2) explaining period-to-period movement with vague “adjustments” instead of traceable components.

Core Bridge Logic

Start with a base earnings measure and add back items that EBITDA excludes, then subtract items EBITDA excludes that are not already handled. A practical bridge usually includes these buckets:

- Starting point: Operating profit or net income, depending on the company’s reporting conventions.

- Depreciation and amortization: Added back because EBITDA excludes it.

- Interest: Added back because EBITDA excludes financing effects.

- Taxes: Added back because EBITDA excludes tax effects.

- Other non-operating items: Added back or excluded depending on how the company defines EBITDA.

- Adjustments: Added back only if they are consistent with the definition and supported by disclosures.

A bridge should also include directional checks. If EBITDA rises while depreciation stays flat and revenue is stable, something else must be moving—usually margins, cost structure, or adjustments.

EBITDA Bridge Mind Map

Mind Map: Bridge Components

Worked Example 1: Building EBITDA from Operating Profit

Assume a company reports the following for Year 1 (in $ millions):

- Operating profit: 120

- Depreciation and amortization: 40

- Interest expense: 25

- Income tax expense: 30

- Other items included in operating profit: 5 (net expense)

A simple bridge from operating profit to EBITDA can be written as:

- Starting point: Operating profit = 120

- Add back depreciation and amortization: +40 → 160

- Add back interest: +25 → 185

- Add back taxes: +30 → 215

- Adjust for other items included in operating profit: -5 → 210

EBITDA (Year 1) = 210.

Notice the small but important step: if the “other items” are already embedded in operating profit and are not part of EBITDA’s definition, you need to remove them. If you skip that, your bridge will still “work,” but it will be wrong in a way that becomes obvious only when you compare to the company’s reported EBITDA.

Worked Example 2: Explaining EBITDA Change Across Two Years

Now compare Year 2 to Year 1. Suppose the company reports:

- EBITDA Year 1: 210

- EBITDA Year 2: 240

- Depreciation and amortization Year 2: 42 (up by 2)

- Interest expense Year 2: 20 (down by 5)

- Taxes Year 2: 28 (down by 2)

- Adjustments Year 2: restructuring expense 18 (Year 1 had 10)

A driver-style bridge focuses on what changed in the components:

- Starting point: EBITDA Year 1 = 210

- Depreciation and amortization effect: +2 (added back more) → 212

- Interest effect: -5 (added back less) → 207

- Tax effect: -2 (added back less) → 205

- Restructuring adjustment effect: +8 (18 vs 10) → 213

- Remaining difference: 27

That remaining difference is not a nuisance; it’s a prompt. It tells you the bridge is incomplete unless you reconcile the remaining 27 through either:

- operating profit changes not captured by the listed line items, or

- other adjustments and non-operating components that were omitted.

A good bridge therefore includes an “other” line that is not a black box. You either break it into specific categories (e.g., impairments, litigation, one-time gains) or you explicitly reconcile it to the change in the starting earnings measure.

Bridge Quality Checks That Prevent Self-Inflicted Confusion

- Definition consistency: If the company changes how it treats stock-based compensation or restructuring, the bridge must reflect that change.

- Materiality discipline: Include every adjustment that is large enough to move EBITDA meaningfully; smaller items can be grouped if disclosures support it.

- Direction sanity: If EBITDA increases but depreciation increases and interest and taxes decrease, the net effect must still be explained by operating performance or adjustments.

- Reconciliation completeness: Every bridge should reconcile exactly to the reported EBITDA for each period.

Example Mind Map for a Two-Year Bridge

A well-constructed EBITDA bridge is less about producing a number and more about producing an explanation that survives scrutiny. If the bridge leaves a large unexplained residual, the analysis is not finished—it’s just waiting for the missing components to be named.

3. Free Cash Flow Measurement and Cash Conversion

3.1 Define Free Cash Flow Variants and Choose a Consistent Definition

Free Cash Flow (FCF) is not one number. It’s a family of definitions built from the same raw materials—cash from operations, capital spending, and sometimes interest or leases. The goal of this section is simple: pick a definition you can compute consistently, explain clearly, and defend when the numbers don’t behave.

Start with the foundation: most FCF variants begin with cash generated by the core business and then subtract cash required to maintain or grow the asset base. The differences come from two choices: (1) what you treat as “operating” cash, and (2) what you treat as “investment” cash.

Core Building Blocks

- Operating cash generation: usually based on cash flow from operations (CFO). CFO already reflects working capital changes and non-cash items converted into cash.

- Capital spending: typically cash paid for property, plant, and equipment (capex). Some definitions also include capitalized software or other investing outflows.

- Financing-related items: interest and principal payments can be treated as either operating or financing depending on the purpose of the metric.

If you keep these building blocks separate, you can swap variants without losing logic.

Mind Map: Free Cash Flow Variants

The Most Used Variants

1) Levered Free Cash Flow (FCF to Equity, common in practice)

- Typical form: FCF = CFO − Capex

- Why it’s used: it’s easy to compute from the cash flow statement and reflects cash available after reinvestment, before financing decisions.

- What it hides: it doesn’t explicitly separate interest burden from operating performance.

Example: A company has CFO of 120, capex of 60, so FCF is 60. If interest payments rise later, CFO may fall even if operations are stable, and the FCF change will reflect that mix.

2) Unlevered Free Cash Flow (FCF to Firm)

- Typical form: FCF to Firm = (Operating cash after taxes) − Net investment in operating assets

- Why it’s used: it aims to measure cash generation independent of capital structure.

- What it requires: more careful handling of interest and taxes, sometimes using EBIT-based adjustments or explicit tax/interest cash mapping.

Example: If you compute operating cash after taxes as 150, subtract net investment of 70, you get FCF to Firm of 80. This number is intended to be comparable across firms with different debt levels.

3) Free Cash Flow After Maintenance Capex

- Typical form: FCF after maintenance = CFO − Maintenance capex

- Why it’s used: it distinguishes “keep the lights on” spending from growth spending.

- What it requires: a maintenance vs growth split, usually inferred from disclosures, historical patterns, and segment behavior.

Example: If total capex is 90 but maintenance is estimated at 60, then FCF after maintenance is CFO − 60. If CFO is 100, the metric is 40, not 10. The difference matters when growth spending is temporarily elevated.

Choosing a Definition That Stays Defensible

Pick the variant that matches your question.

- If you’re assessing cash available to reinvest and absorb shocks without isolating financing effects, CFO − capex is usually the cleanest starting point.

- If you’re comparing operating cash strength across different leverage levels, use an unlevered approach.

- If you’re evaluating profit sustainability, maintenance capex is often the most informative, but only if you can justify the split.

Then lock the definition.

Consistency rules that prevent accidental metric drift:

- Use the same capex scope each period (PP&E only, or PP&E plus capitalized software).

- Use the same lease treatment each period (especially if reporting changes).

- Avoid mixing net and gross capex across years. If you subtract capex only, don’t later subtract capex net of asset sales.

- State the definition in one sentence you can reuse in your model documentation.

A Practical Decision Checklist

- What is the metric’s purpose: equity cash, firm cash, or sustainability after maintenance?

- What line items will you use: CFO, capex, and any explicit adjustments?

- Are there accounting changes that affect comparability (lease classification, software capitalization, discontinued operations)?

- Can you reproduce the number from the cash flow statement with minimal interpretation?

When these answers are clear, the definition becomes a tool rather than a debate.

Worked Mini-Scenario with Two Definitions

Assume:

- CFO = 200

- Cash capex = 120

- Asset sales proceeds = 20

- Cash interest = 30

If you use FCF = CFO − capex, you get 80. If you use a variant that nets asset sales with investment outflows, you might compute FCF = CFO − (capex − asset sales proceeds) = 200 − (120 − 20) = 100.

Both can be reasonable, but only one matches your stated definition. The difference is not math—it’s interpretation. Choose one, document it, and keep it steady.

3.2 Compute Operating Cash Flow and Adjust for Working Capital

Operating cash flow (OCF) starts with the cash generated by day-to-day operations. In practice, most companies report OCF using the indirect method, which begins with net income and then adjusts for non-cash items and working capital changes. The goal is simple: translate accrual-based earnings into cash timing.

Core Idea from Net Income to Cash

Net income includes revenues earned and expenses incurred, even when cash hasn’t moved yet. Working capital accounts—receivables, inventory, payables, and other current items—capture those timing gaps. If receivables rise, customers paid later than the revenue was recognized, so cash is lower than earnings suggest. If payables rise, the company recognized expenses before paying suppliers, so cash is higher than earnings suggest.

Step 1: Start with Net Income

Use the income statement net income for the period. If the company reports discontinued operations, decide whether to keep them consistent with your analysis scope. For a clean bridge, match the net income line you will use with the cash flow line you will reconcile.

Step 2: Add Back Non-Cash Expenses

Common non-cash adjustments include depreciation and amortization, stock-based compensation, impairment charges (when non-cash), and deferred taxes (depending on presentation). These items reduce net income but do not consume cash in the period.

Example: Suppose net income is $10.0 million, depreciation is $4.0 million, and stock-based compensation is $1.0 million. Before working capital, you have $15.0 million of cash-related earnings.

Step 3: Remove Non-Cash Gains

If the company records gains that do not generate cash in the period—such as gains on asset sales—subtract them. This prevents double counting: the gain increased net income, but the cash impact is already captured elsewhere in the cash flow statement.

Step 4: Adjust for Working Capital Changes

Working capital adjustments convert accrual timing into cash timing. The indirect method typically shows these as changes in current assets and current liabilities.

- Increase in accounts receivable: subtract (cash outflow)

- Decrease in accounts receivable: add (cash inflow)

- Increase in inventory: subtract (cash outflow)

- Decrease in inventory: add (cash inflow)

- Increase in accounts payable: add (cash inflow)

- Decrease in accounts payable: subtract (cash outflow)

A practical way to avoid sign mistakes is to think in terms of cash movement: if the balance grows, cash usually went into that asset; if the balance shrinks, cash usually came out.

Worked Example with Clear Signs

Assume:

- Net income: $10.0

- Depreciation: $4.0

- Stock-based compensation: $1.0

- Gain on asset sale: $0.5 (non-cash in this simplified example)

- Accounts receivable increased by $2.0

- Inventory increased by $1.0

- Accounts payable increased by $1.5

Compute:

- Net income + depreciation + stock comp − gain = $10.0 + 4.0 + 1.0 − 0.5 = $14.5

- Working capital adjustment = −2.0 −1.0 +1.5 = −1.5

- Operating cash flow = $14.5 − 1.5 = $13.0 million

Notice how the cash story is consistent: earnings were strong, but customers paid later and inventory grew, which absorbed cash; suppliers were paid later too, which partially offset the drag.

Step 5: Handle Other Current Items Carefully

Other current assets and liabilities can include prepaid expenses, accrued revenue, accrued expenses, contract assets, and contract liabilities. Treat them the same way: determine whether the balance increase represents cash paid earlier than expense recognition, or cash received earlier than revenue recognition.

Example: If contract liabilities (deferred revenue) increase, cash was received before revenue was recognized, so OCF typically benefits.

Mind Map: Operating Cash Flow and Working Capital

Common Pitfalls and How to Stay Consistent

First, don’t mix definitions: if you use net income from continuing operations, use the corresponding cash flow scope. Second, keep sign discipline by mapping each working capital line to a cash direction. Third, when a company presents working capital changes net of certain items, mirror that presentation in your model rather than forcing a different breakdown.

Quick Consistency Check

After computing OCF, compare it to net income. A persistent pattern of OCF far below net income often signals working capital absorption or aggressive revenue timing. A persistent pattern of OCF far above net income often signals delayed payments or early cash collection. Either way, the working capital bridge explains the gap rather than leaving it as a mystery.

3.3 Incorporate Capital Expenditures and Disposals Correctly

Free cash flow (FCF) is sensitive to how you treat capital expenditures (capex) and asset disposals. The goal is simple: measure cash spent to keep the business running and to grow it, then adjust for cash received when assets are sold. If you get the classification wrong, your FCF can look healthier or weaker than the underlying economics.

Core Concept: Capex Is Cash Used for Long-Term Assets

Capex is cash paid to acquire or improve long-lived assets. In practice, you’ll usually start from the cash flow statement line items, then reconcile them to notes and schedules. A common pitfall is mixing accounting “capitalization” with cash timing. Capitalized costs may not all be paid in the same period, and some cash payments may be expensed depending on the accounting policy.

A practical rule: use the cash flow statement for the cash amount, then use the notes to understand what the cash represents.

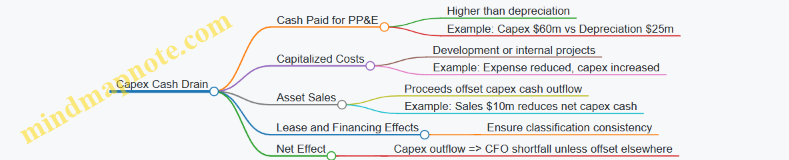

Step 1: Identify Capex from the Cash Flow Statement

Look for “Payments for property, plant and equipment” (or similar) and “Payments for intangible assets.” If the statement is netted or grouped, you may need note disclosures to split maintenance versus growth.

Example: A company reports:

- Cash paid for PP&E: 120

- Cash paid for intangibles: 30

- Proceeds from sale of assets: 15

If your FCF definition is:

- FCF = Operating cash flow − capex + proceeds from disposals then capex cash outflow is 150, and disposals add 15.

Step 2: Treat Disposals as Cash Inflows, Not Negative Capex

Disposals are not “negative capex” in an accounting sense; they are cash inflows from selling assets. In FCF, you typically add proceeds to offset the net cash impact of investing activity.

Why this matters: a company can sell an asset and temporarily boost FCF even if it is not investing enough to replace capacity. That’s not fraud; it’s a measurement choice. Your job is to interpret it consistently.

Step 3: Separate Maintenance and Growth When Evidence Exists

When notes provide enough detail, you can split capex into maintenance and growth. If you cannot, you still incorporate total capex correctly, but you should avoid claiming maintenance-only conclusions.

Example with evidence:

- Management discloses maintenance capex as “required to sustain production capacity.”

- Growth capex is tied to new lines or expansions.

If maintenance capex is 70 and growth capex is 80, and operating cash flow is 200, then:

- FCF after maintenance = 200 − 70 + proceeds

- FCF after total capex = 200 − 150 + proceeds

This distinction helps explain why EBITDA might stay stable while cash generation changes.

Step 4: Handle Asset Sales, Impairments, and “Non-Cash” Adjustments

Impairments reduce accounting earnings but do not automatically create cash. Disposals create cash, but the gain or loss on sale is an accounting result that may differ from the cash proceeds.

Example: The company sells equipment for 15 cash. The book value was 20, so it records a loss of 5. In FCF, you use the 15 cash proceeds, not the accounting loss.

Step 5: Watch for Leases and Financing-Style Investing

Some companies present lease-related payments differently across jurisdictions and reporting standards. If lease payments are included in operating cash flow, you must not treat them as capex. Instead, focus on the specific cash lines that represent purchases of PP&E and intangibles.

A quick sanity check: if capex is low but the company’s asset base is expanding, review whether investments are being done through leases, joint ventures, or acquisitions.

Step 6: Reconcile Capex with Notes and Movement Schedules

To avoid “mystery capex,” reconcile:

- Beginning and ending PP&E and intangibles

- Additions

- Disposals

- Depreciation/amortization

- FX effects (if applicable)

If the cash paid for PP&E is 120 but the note shows additions of 140, the gap can come from unpaid invoices, timing differences, or reclassifications. Your FCF should still use the cash paid, but the reconciliation tells you whether the period is unusually cash-heavy or cash-light.

Mind Map: Capex and Disposals Integration Logic

Example: Building a Clean FCF Bridge from Investing Cash

Assume:

- Operating cash flow: 260

- Cash paid for PP&E: 110

- Cash paid for intangibles: 25

- Proceeds from sale of assets: 10

Then:

- Total capex cash outflow = 135

- Net investing cash impact = −135 + 10 = −125

- FCF = 260 − 125 = 135

Now add interpretation:

- If proceeds are recurring and capex is consistently low, FCF may reflect asset turnover rather than sustained reinvestment.

- If capex rises while operating cash flow stays steady, FCF compresses even if EBITDA looks unchanged.

Correct incorporation is the foundation; the reconciliation and interpretation are what keep the numbers honest.

3.4 Calculate Free Cash Flow Yield and Cash Conversion Ratios

Free Cash Flow (FCF) is a cash-based measure of what a business generates after funding its operating needs and capital spending. Yield and conversion ratios turn that raw cash number into something comparable across companies, time periods, and capital structures.

Core Definitions and Why Ratios Matter

Start with a consistent FCF definition. A common approach is:

- FCF = Operating Cash Flow − Capital Expenditures

Then compute two families of ratios:

- FCF Yield: relates FCF to a valuation base (most often enterprise value).

- Cash Conversion Ratios: relate FCF to accounting earnings or revenue, showing how much profit becomes cash.

A useful mental model: yield answers “how much cash per unit of value,” while conversion answers “how much of the reported performance becomes cash.” Both are needed because a company can look cheap on yield yet have weak conversion.

Free Cash Flow Yield Calculation

Step 1: Choose the valuation base.

- Enterprise Value (EV) is typically preferred because it reflects the value of operations before financing choices.

Step 2: Use a consistent time horizon.

- Use trailing twelve months (TTM) FCF for stability, or use the same period as the EV snapshot.

Step 3: Compute the ratio.

- FCF Yield = FCF / EV

Example:

- FCF (TTM): $120 million

- EV: $1,200 million

- FCF Yield = 120 / 1,200 = 10%

Interpretation is comparative, not absolute. If the company’s yield is higher than its own history or peers, the market is assigning less value per dollar of cash generated.

Cash Conversion Ratios That Connect Profit to Cash

Conversion ratios help you test whether earnings quality is supported by cash. Use at least one earnings-based and one revenue-based view.

FCF to Net Income Conversion

- FCF Conversion to Net Income = FCF / Net Income

Example:

- FCF: $120 million

- Net income: $90 million

- FCF / Net income = 120 / 90 = 1.33

A ratio above 1 means cash exceeds accounting profit for the period. A ratio below 1 suggests cash is lagging earnings, which can be caused by working capital build, aggressive revenue timing, or higher-than-expected capital needs.

FCF to Operating Cash Flow Conversion

This ratio checks whether “free” is truly free.

- FCF Conversion to Operating Cash Flow = FCF / Operating Cash Flow

Example:

- Operating cash flow: $200 million

- Capex: $80 million

- FCF: $120 million

- 120 / 200 = 0.60

If this ratio is consistently low, the business may require heavy reinvestment just to maintain operations.

FCF to Revenue Conversion

- FCF Margin in Cash Terms = FCF / Revenue

Example:

- Revenue: $800 million

- FCF: $120 million

- 120 / 800 = 15%

This is especially helpful when comparing firms with different accounting margins but similar cash economics.

Mind Map: What You Calculate and What It Means

Practical Data Checks That Prevent Ratio Errors

- Capex classification: Ensure capital expenditures are consistently defined (cash paid for capex vs accounting capex can differ). If you mix definitions, your conversion ratios will “drift” for reasons unrelated to business performance.

- EV consistency: EV should be computed using the same treatment of cash, debt, and minority interests across periods. A small EV mismatch can swing yield meaningfully.

- Net income distortions: Net income can include non-cash items and one-time charges. If conversion to net income looks poor, confirm whether the denominator is temporarily depressed or inflated.

Worked Mini-Template for a Single Company

Assume:

- Revenue: $800m

- Operating cash flow: $200m

- Capex: $80m

- Net income: $90m

- EV: $1,200m

Compute:

- FCF = 200 − 80 = $120m

- FCF Yield = 120 / 1,200 = 10%

- FCF / Net Income = 120 / 90 = 1.33

- FCF / Operating Cash Flow = 120 / 200 = 0.60

- FCF / Revenue = 120 / 800 = 15%

Use the set together: yield tells you how the market values the cash stream, while conversion ratios tell you whether that cash stream is supported by earnings and how much reinvestment is required to keep it coming.

3.5 Validate Free Cash Flow With Statement Level Reconciliations

Free cash flow (FCF) is only as trustworthy as the path you used to get there. Validation means proving that your FCF math is consistent with the cash flow statement and the balance sheet movements that feed it. Think of it as a three-way handshake: income statement logic, balance sheet timing, and cash flow presentation.

Core Validation Idea

Start with a definition you can defend. A common approach is:

- FCF = Operating Cash Flow − Capital Expenditures

Then validate each component using statement-level reconciliations.

Step 1: Reconcile Operating Cash Flow to Accrual Earnings

Operating cash flow (OCF) is derived from net income plus non-cash items and working capital changes. Validation checks whether your working capital adjustments match the balance sheet.

Example: Suppose a company reports:

- Net income: 100

- Depreciation and amortization: 40

- Accounts receivable increase: +15

- Accounts payable increase: +10

- Other working capital items net: −5

If you compute OCF as:

- 100 + 40 − 15 + 10 − 5 = 130 Then your statement-level validation is: does the cash flow statement show OCF of 130 (or very close after rounding)? If not, you likely missed a working capital line, mis-signed a change, or used a different “other” bucket than the company uses.

Practical rule: For each working capital line on the cash flow statement, map it to the exact balance sheet line and confirm whether the cash flow statement uses “increase is negative” conventions.

Step 2: Reconcile Changes in Working Capital Using Balance Sheet Movements

Working capital changes are where many FCF errors hide because they depend on timing.

Example: If accounts receivable rises from 200 to 215, the change is +15. On the indirect method, that typically reduces OCF by 15 because cash hasn’t been collected yet.

Validation checklist:

- Confirm the beginning and ending balance sheet dates match the cash flow period.

- Check whether the company presents netting (for example, receivables net of allowances).

- Ensure discontinued operations are treated consistently across statements.

If the cash flow statement shows a different working capital impact than your balance sheet math, reconcile the difference by identifying reclassifications, FX effects, or acquisitions/disposals that alter balances without corresponding operating cash.

Step 3: Reconcile Capital Expenditures to Cash Flow Investing Lines

FCF subtracts capex, but capex can be presented in multiple ways. Validation ensures you’re using the same capex concept as the cash flow statement.

Example: A cash flow statement may show:

- “Capital expenditures” of −60

- “Proceeds from sale of property, plant, and equipment” of +5 If your FCF definition subtracts only capex, you subtract 60. If your definition subtracts net capex, you subtract 55.

Best practice: Choose one definition and stick to it. Then validate by matching your capex input to the investing cash flow lines, or to the notes if the company provides a capex reconciliation.

Step 4: Validate the Bridge from OCF to FCF Using a Statement-Level Ledger

Create a simple reconciliation ledger that shows how you move from OCF to FCF and how the remainder ties back to the cash flow statement.

Example ledger (illustrative):

- OCF (from cash flow statement): 130

- Less capex (from investing section): 60

- FCF: 70

Then sanity-check whether the company’s net cash change roughly aligns with FCF plus financing and other investing items. You’re not forcing a perfect match (timing and other items exist), but you should understand the major drivers.

Step 5: Use Variance Checks to Catch Data and Classification Issues

Validation is incomplete without variance checks.

Common variance sources:

- Rounding differences between statements.

- “Other investing” cash flows that include items you treated as capex or vice versa.

- Lease payments: some companies classify certain lease cash flows differently.

- Changes in cash due to FX translation on cash and cash equivalents.

Example: If your computed FCF is 70 but your spreadsheet shows 62, the first suspect is capex classification. Confirm whether you subtracted gross capex or net of asset sales.

Mind Map: Statement-Level Reconciliation Workflow

Mini Case Example: Spotting a Capex Definition Mismatch

A company reports:

- OCF: 200

- Investing cash flow shows “Purchases of property, plant, and equipment” of −90

- Notes mention asset sales of +10 If you subtract only 90, FCF is 110. If you mistakenly subtract net (90−10=80), FCF becomes 120. The reconciliation ledger immediately reveals the mismatch: your capex input doesn’t match your chosen definition.

Validation ends when every input has a clear statement-level source and every major difference is explained, not ignored. Once that’s done, FCF becomes a measurement you can compare across periods with confidence.

4. Earnings Quality Framework Using Accruals and Cash Alignment

4.1 Understand Accrual Accounting and Its Implications

Accrual accounting records economic events when they occur, not when cash changes hands. That single design choice explains why earnings can look strong while cash looks weak, and why the reverse can also happen. If you want to judge earnings quality, you need to understand what accruals are doing under the hood.

Core Idea and Why It Exists

Accrual accounting matches revenues with the expenses incurred to generate them. For example, if a company delivers services in March but invoices in April, accrual accounting records revenue in March and creates an accounts receivable balance. The goal is timing consistency: performance is measured by activity, not by payment.

This approach is useful, but it introduces estimates. Many accruals depend on judgment about timing, collectability, and allocation. Those estimates are not automatically wrong, but they are where earnings quality can vary.

The Main Accrual Mechanisms

Accrual accounting typically creates four recurring “bridges” between the income statement and the cash flow statement.

- Revenue recognition creates receivables or deferred revenue.

- Expense recognition creates payables or accrued expenses.

- Depreciation and amortization allocate past cash outflows across future periods.

- Provisions and estimates create liabilities that may later be adjusted.

A quick example: suppose a firm signs a contract for $120,000 in January, delivers the work evenly over four months, and bills at delivery. Under accrual accounting, revenue is recognized each month even though cash arrives later. The cash flow timing depends on billing and collections.

Mind Map: Accrual Accounting Implications

How Accruals Move Through the Statements

The income statement reports earnings after including non-cash items and estimated timing effects. The cash flow statement then reconciles earnings to cash from operations.

Consider a simple scenario for a retailer:

- In March, the retailer sells $1,000 of goods on credit.

- It recognizes $1,000 revenue in March.

- It records $1,000 in accounts receivable.

- In April, it collects the cash.

March earnings include the revenue, but March operating cash flow is reduced by the increase in receivables. When cash arrives in April, operating cash flow increases as receivables decrease. This is not a flaw; it is the expected pattern of accrual accounting.

Where Earnings Quality Can Diverge

Accrual accounting becomes a quality issue when accruals do not behave as expected.

1. Receivables that don’t convert to cash. If sales are recorded but collections lag far beyond normal terms, accounts receivable grows. That can indicate overly optimistic revenue recognition, weak credit control, or insufficient allowance for doubtful accounts.

2. Expenses that are delayed. If costs are recognized later than the period in which related benefits are consumed, earnings can be overstated. A common signal is persistently low expense ratios relative to revenue growth, paired with rising accrued liabilities or shrinking payables.

3. Depreciation that doesn’t reflect reality. Depreciation is an allocation, not a cash payment. If useful lives are set too long, depreciation expense may be understated, boosting earnings while cash needs show up later through higher future capex.

4. Provisions that are adjusted opportunistically. Provisions for warranties, litigation, or restructuring rely on estimates. If the company repeatedly releases provisions without corresponding changes in underlying risk, earnings can look smoother than cash generation.

Example: A Small Accrual Story with Numbers

Assume a software firm recognizes $500,000 of subscription revenue in a quarter. It collects only $420,000 cash and records $80,000 in accounts receivable.

- Income statement: revenue increases earnings by $500,000.