The Agentic Finance Revolution

1. Foundations of Agentic Finance

1.1 Defining Agentic Systems in Finance Operations

Agentic systems in finance operations are software that can carry out multi-step tasks toward a goal, using tools (like ERP actions, payment initiation, or risk calculations) and following rules about what it may do. The key difference from simple automation is that the system can decide the next step based on what it observes, rather than executing a fixed script from start to finish.

A practical way to define the scope is to start with the goal and work backward. For example, “prepare a cash forecast” is a goal. The system must then determine which inputs are required, which calculations to run, which assumptions to request or retrieve, and which checks to perform before publishing. If any check fails, the workflow must either correct the issue or route it to a human reviewer with a clear explanation.

Core Characteristics

- Goal orientation: The system is designed around an outcome, not a sequence of button clicks. In treasury, the outcome might be “submit a funding instruction that matches approved limits.”

- Tool use: It interacts with systems of record and systems of action. Examples include reading balances from a TMS, validating bank account details, and creating a payment draft.

- State and memory: It tracks what it has already done and what remains. For instance, it remembers which invoices were matched and which are still pending.

- Rule-based boundaries: It follows constraints such as approval thresholds, permitted counterparties, and data quality requirements.

- Evidence and traceability: It records the inputs, decisions, and actions so an auditor can reconstruct what happened.

Mind Map: What Makes It Agentic

From Automation to Agentic Workflows

A fixed workflow might say: “Pull last month’s cash, apply a fixed growth rate, publish.” An agentic workflow adds conditional steps: “If the growth rate inputs are missing, request them; if bank holidays affect settlement dates, adjust the calendar; if the forecast breaches a liquidity threshold, prepare an escalation package.” The system is still rule-governed, but it adapts to observed conditions.

A Simple Example: Payment Draft with Guardrails

Consider a workflow that prepares a payment draft for an approved vendor.

- Inputs: invoice amount, vendor bank account, payment currency, and due date.

- Perception: it checks whether the vendor is active and whether the bank account matches master data.

- Reasoning: it determines the correct payment method and settlement date rules.

- Actions: it creates a draft in the payment system.

- Safety checks: it verifies that the payment amount is within the approved invoice amount and that the beneficiary details match.

- Escalation: if the bank account differs from master data, it routes to a human with the discrepancy highlighted.

This example shows the “agentic” part: the next step changes based on what the system finds, while the boundaries remain explicit.

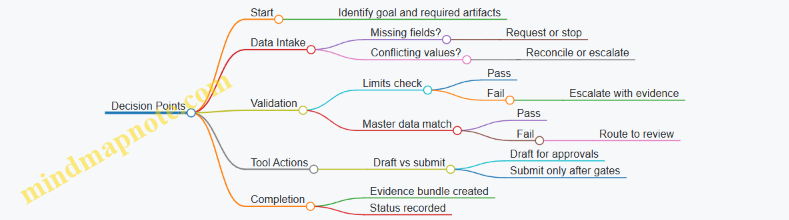

Defining the Boundaries Clearly

Agentic systems fail when the boundaries are vague. In finance operations, boundaries should be expressed as concrete rules:

- What it may do: permitted tool actions (read-only vs write operations).

- When it must ask: approval gates based on amount, counterparty, or risk flags.

- What it must verify: reconciliation checks, mandatory fields, and data freshness.

- How it handles uncertainty: if required data is missing, it should stop and request it rather than guess.

A useful test is to ask: “If the system sees conflicting data, what exact behavior occurs?” If the answer is not specific, the workflow needs refinement.

Mind Map: Decision Points in Finance Tasks

Practical Definition Summary

An agentic system in finance operations is a goal-driven workflow that observes the environment, plans the next step, uses authorized tools to act, and enforces governance rules with evidence capture. When you can describe the goal, the allowed actions, the decision points, and the escalation behavior in plain language, you have a definition that can be implemented and audited.

Mini Checklist for “Agentic”

- The workflow can choose the next step based on observed conditions.

- It uses tools to read and write in finance systems.

- It maintains state across steps.

- It enforces explicit approval and permission boundaries.

- It produces an audit-ready record of actions and decisions.

1.2 Distinguishing Automation From Agentic Workflows

Automation and agentic workflows both reduce manual effort, but they differ in how decisions are made, how work is planned, and how exceptions are handled. A useful rule of thumb: automation follows a script; agentic workflows coordinate a goal using tools, evidence, and guardrails.

Automation: Predictable Steps with Limited Choice

Automation is best when the process is stable and the “right action” is known in advance. The workflow typically has fixed inputs, deterministic transformations, and a clear success path.

What automation usually looks like

- Predefined triggers: “When invoice arrives, validate fields.”

- Fixed rules: “If tax ID is missing, reject.”

- Single-pass execution: The system does one round of checks and either passes or fails.

- Exception routing: Failures go to a queue with a reason code.

Treasury example A bank statement import runs nightly. It parses transactions, matches them to expected payment references, and flags unmatched items. If a payment reference is missing, the system marks the record as “needs review” and stops. The logic is clear, testable, and easy to audit because the decision boundaries are defined ahead of time.

Best-fit areas

- Repetitive reconciliations with stable formats

- Standard reporting calculations

- Straight-through processing where exceptions are rare and well categorized

Agentic Workflows: Goal-Driven Coordination with Tool Use

Agentic workflows are designed around a goal and the ability to choose actions. Instead of only applying a fixed set of rules, the workflow can plan steps, call tools, and adjust its path based on what it observes.

What agentic workflows usually look like

- Goal specification: “Prepare a cash position summary suitable for approval.”

- Dynamic planning: The workflow decides which data to fetch first.

- Tool use: It can query systems, compute metrics, and draft an approval package.

- Evidence gathering: It collects the facts needed to justify its output.

- Guardrails: It must respect limits, permissions, and required approvals.

Treasury example Suppose the cash forecast for next week is due. An agentic workflow starts by pulling current balances, then checks whether FX rates are available for the relevant currencies. If rates are missing, it requests the appropriate source data and reruns the forecast. If the forecast would breach an internal liquidity threshold, it prepares an escalation note with the specific assumptions and the exact limit that would be exceeded. The workflow doesn’t just “fail”; it actively assembles the information needed to move the process forward safely.

The Practical Distinction: Decision Timing and Recovery

The difference becomes obvious when something goes wrong.

- Automation recovery: Often limited to routing. The system detects an issue and hands it off.

- Agentic recovery: Can attempt structured remediation. It may try alternative data sources, re-run calculations, or propose an approval-ready explanation—while still requiring human signoff for high-impact actions.

A simple comparison for finance teams:

- If the workflow can be fully described as “if X then Y,” it’s likely automation.

- If the workflow must decide “what to do next” based on intermediate findings, it’s likely agentic.

Mind Map: Automation Versus Agentic Workflows

Example: Same Goal, Different Workflow Styles

Goal: “Create a payment batch for approval.”

- Automation approach: Generate a batch from a fixed file format, validate mandatory fields, and reject any record that fails validation. The approver receives a list of rejected items.

- Agentic approach: Generate the batch, but if a beneficiary account is inconsistent, the workflow checks master data, verifies whether an alternate account exists, and drafts a short justification for the approver. If the workflow cannot confirm the beneficiary, it routes the item with the exact missing evidence.

A Quick Checklist for Choosing the Right Style

- Stability: Are inputs and rules stable enough to predefine?

- Runtime choice: Does the workflow need to decide next steps after seeing results?

- Exception handling: Should the system only route issues, or also gather evidence and propose safe next actions?

- Approval requirements: Are high-impact actions gated by explicit human review?

When you can answer these questions clearly, the distinction stops being theoretical and becomes a design decision you can test with real finance scenarios.

1.3 Core Components Including Tools Memory and Governance

Agentic finance workflows work only when three things are coordinated: the tools an agent can use, the memory it carries across steps, and the governance that decides what is allowed. Think of it as a controlled kitchen: tools are the appliances, memory is the recipe book and pantry labels, and governance is the rulebook for what can be cooked, by whom, and with which ingredients.

Tools the Action Surface

Tools are the concrete interfaces the agent can call to do work. In finance, they should be narrow, well-defined, and permissioned. A “tool” is not a vague capability; it is an operation with inputs, outputs, and an expected audit footprint.

Best practice is to design tools around stable business objects. For example, instead of one generic “payment” tool, use smaller tools:

- Create Payment Draft: validates required fields and formats beneficiary data.

- Request Payment Approval: routes a draft to the right approver group.

- Submit Payment to Bank: sends the final instruction and captures bank response codes.

- Query Payment Status: retrieves settlement state and exception reasons.

Easy example: If a treasury analyst asks the system to “prepare a EUR payment for vendor X,” the agent should call Create Payment Draft with vendor ID, amount, currency, and payment date. The tool returns a structured draft plus validation warnings (e.g., missing IBAN checksum). The agent then asks for approval only after the draft passes tool-level checks.

A practical rule: tools should fail loudly and predictably. If a tool cannot complete an operation, it should return an error category the agent can handle (validation error, permission error, upstream outage, or data not found).

Memory the Working Context

Memory is how the agent keeps track of what it has already learned or decided. In finance, memory must be explicit and bounded so it does not silently accumulate contradictions.

Use three memory layers:

- Session Memory stores the current workflow state, such as the payment draft ID or the risk limit record being reviewed.

- Reference Memory stores stable facts the workflow needs repeatedly, like counterparty master data fields or policy thresholds.

- Evidence Memory stores audit-relevant artifacts, such as tool outputs, approval decisions, and reconciliation results.

Easy example: For a cash forecast workflow, session memory holds the selected forecast horizon and the chosen scenario. Reference memory holds the company’s cash account mapping and historical seasonality parameters. Evidence memory stores the exact data extracts used and the reconciliation summary that confirms the forecast inputs match the general ledger totals.

To keep memory reliable, store memory as structured records, not free text. When the agent needs to “remember” something, it should retrieve the relevant record by key (workflow ID, draft ID, limit ID) and verify it matches the current request.

Governance the Permission and Policy Layer

Governance is the set of rules that constrains tool use and decision-making. It answers: What can the agent do, under which conditions, with what approvals, and how is it recorded?

Governance should be implemented as enforceable checks, not as instructions the agent merely follows. Typical governance gates include:

- Role and Segregation of Duties: the agent can draft but cannot submit without an approval gate.

- Policy Thresholds: certain actions require additional review when amounts exceed limits.

- Data Access Controls: the agent can read only the data domains it is authorized to use.

- Exception Handling Rules: if a tool returns a specific error category, the agent must route to a human queue.

Easy example: If a payment draft exceeds the “single payment approval threshold,” governance blocks submission and triggers Request Payment Approval. The approval record becomes part of evidence memory, so an auditor can trace the decision to the exact draft and the exact tool outputs.

Mind Map: Core Components

Putting It Together a Single Workflow Walkthrough

A coherent workflow shows the components interacting in order. Start with a request, use tools to produce structured outputs, store those outputs in evidence memory, and apply governance gates before any irreversible action.

Example: Payment Draft to Submission

- The agent receives payment details and calls Create Payment Draft.

- The tool returns a draft plus validation warnings; the agent resolves only warnings it can address via additional tool calls.

- The agent stores the draft ID and tool outputs in session and evidence memory.

- Governance checks whether the draft amount requires approval.

- If approval is required, the agent calls Request Payment Approval and waits for a signoff record.

- After signoff, the agent calls Submit Payment to Bank and stores the bank response in evidence memory.

- If bank submission returns an exception category, governance routes the workflow to human review instead of retrying blindly.

This structure prevents the most common failure mode: an agent that can “talk” about finance but cannot reliably execute it with traceable, permissioned actions.

1.4 Data Inputs Controls and Auditability Requirements

Agentic finance workflows live or die by their inputs. If the system cannot explain where a number came from, which rule transformed it, and who approved the action, then the workflow is just a fancy spreadsheet with better posture. This section lays out practical requirements for data inputs, control design, and auditability.

Data Inputs That Are Fit for Finance Work

Start with a simple principle: every input must have an owner, a definition, and a validation rule.

- Owner and purpose: For example, “Bank balance” is owned by Treasury Operations and used for cash forecasting. “Counterparty credit rating” is owned by Risk and used for exposure flags.

- Definition and units: Store currency, sign conventions, and time zones explicitly. A payment amount of “-250,000” is not the same as “250,000” unless the sign rule is documented.

- Validation rules: Apply checks before any agent action. Examples include schema validation (required fields present), referential integrity (account IDs exist), and range checks (interest rate within plausible bounds).

A useful pattern is to separate inputs into three buckets:

- Reference data: counterparties, accounts, instruments, payment templates.

- Transactional data: invoices, payment instructions, bank statements.

- Derived data: forecasts, risk metrics, reconciled balances.

Controls differ by bucket. Reference data needs change governance; transactional data needs completeness and reconciliation; derived data needs traceability to source fields.

Control Requirements Across the Data Lifecycle

Controls should be designed for the lifecycle: ingestion, transformation, decision, and action.

- Ingestion controls: Ensure the feed is complete and timely. Example: if a bank statement arrives late, the workflow should either pause or switch to a documented fallback source.

- Transformation controls: Every transformation should be deterministic where possible. Example: currency conversion must record the FX rate source, timestamp, and method.

- Decision controls: Decisions must be tied to explicit rules and thresholds. Example: “Approve funding transfer” only when projected liquidity after transfer stays above the minimum buffer.

- Action controls: Actions must be constrained by permissions and approval gates. Example: payment initiation requires a beneficiary match check and a second approval for amounts above a threshold.

A small but powerful best practice is to implement control coverage mapping: for each workflow step, list the required checks and the evidence they produce.

Auditability Requirements That Make Evidence Easy

Auditability is not a folder of screenshots; it is structured evidence that can be reconstructed.

Key requirements:

- Immutable logs: Record who/what initiated the workflow, the input snapshot identifiers, and the exact rule set version.

- Input snapshots: Store the data used for the run, not just a pointer to where it lived. Example: if a counterparty name changes later, the audit trail must still show the name used at decision time.

- Evidence bundles: For each action, capture the checks performed and their outcomes. Example: a payment evidence bundle includes beneficiary verification result, account validation result, and approval signoff.

- Reproducibility: A run should be re-executable in principle. That means versioned transformation logic and rule definitions.

When evidence is structured, auditors can answer questions quickly: “What did the system see?” “Which rule fired?” “Who approved?”

Mind Map: Data Inputs Controls and Auditability

Example: Payment Instruction with Evidence-First Controls

Consider a workflow that prepares a payment instruction.

- Input validation: Confirm beneficiary bank account ID exists in master data and that currency matches the payment template.

- Reconciliation check: Verify the payment amount matches the invoice total after applying the documented discount rule.

- Decision rule: If amount is above the approval threshold, require a second approver.

- Action constraints: Only allow the payment tool to submit to pre-approved bank endpoints.

- Evidence bundle: Store the input snapshot IDs, the invoice-to-payment mapping, the rule versions, the validation outcomes, and the approval signoffs.

If any validation fails, the workflow should stop with a clear reason and a record of which control failed. That record becomes the audit evidence and the operational troubleshooting trail.

Example: Cash Forecast Inputs with Controlled Assumptions

A cash forecast run should capture:

- the bank balance snapshot used as the starting point,

- the forecast horizon and time zone,

- the assumption set version (for example, collection timing rules), and

- the reconciliation status of recent transactions.

If the reconciliation status is “partial,” the workflow can still produce a forecast, but it must label the derived outputs with the reconciliation condition and the specific controls that were bypassed or replaced. That keeps the forecast usable without pretending it is fully clean.

2. Architecture for Autonomous Financial Workflows

2.1 Reference Architecture for Agent Orchestration and Tool Use

Agent orchestration is the part of the system that decides what to do next, calls the right tools, and records evidence so finance teams can explain outcomes. A good reference architecture starts with a simple loop—plan, act, verify—and then adds the guardrails treasury, risk, and compliance require.

Core Loop and Responsibilities

- Intake and normalization: Convert a user request into a structured task with required fields (entities, dates, thresholds, and desired output format). Example: “Prepare the weekly cash forecast for EMEA” becomes a task with a date range, legal entities, and forecast granularity.

- Policy and control checks: Validate that the task is allowed for the requester and that it meets control requirements. Example: payment instructions require beneficiary verification and an approval gate above a configured amount.

- Planning and decomposition: Break the task into steps that map to tools. Example: forecasting might require retrieving historical balances, applying seasonality assumptions, and generating a variance report.

- Tool execution: Call deterministic tools for data retrieval, calculations, and system updates. Example: a “get bank balances” tool reads from TMS or banking APIs rather than relying on text generation.

- Verification and reconciliation: Check outputs against constraints and cross-source totals. Example: forecast totals must reconcile to the latest ledger snapshot within an allowed tolerance.

- Evidence capture and audit trail: Store inputs, tool calls, parameters, and verification results. Example: record the exact query filters used to compute exposure.

- Human review when required: Route exceptions and high-impact actions to approvers. Example: if a payment beneficiary is new, require a manual signoff.

Reference Architecture Components

- Orchestrator: The coordinator that manages the loop, step ordering, and retries.

- Task Schema: A strict structure for inputs and outputs, including required fields and validation rules.

- Tool Registry: A catalog of tools with schemas, permissions, and expected outputs.

- State Store: Persists intermediate results so the workflow can resume after failures.

- Policy Engine: Encodes segregation of duties, approval thresholds, and allowed actions.

- Evidence Store: Captures tool calls, parameters, and verification artifacts.

- Observability Layer: Tracks latency, failure rates, and reconciliation outcomes.

Mind Map: Orchestration and Tool Use

Tool Use Design Principles

1. Tools do the work; the orchestrator coordinates. Keep tool outputs structured so verification is straightforward. Example: a “calculate_fx_exposure” tool returns a table with currency, tenor, and sensitivity values.

2. Every tool call is permissioned. The tool registry should specify which roles can execute it. Example: only treasury operations can run “create_payment_batch,” while risk can run “compute_limit_utilization.”

3. Idempotency prevents double actions. For actions like posting or sending, include an idempotency key. Example: if a payment batch creation times out, rerunning with the same key returns the existing batch ID instead of creating a duplicate.

4. Verification is a first-class step. Define checks per workflow stage. Example: after retrieving bank balances, verify that the sum of sub-accounts equals the account total within tolerance.

Example Workflow: Payment Instruction with Controls

A payment request typically includes payee details, amount, currency, and execution date. The orchestrator should:

- Normalize the request into a task schema.

- Check policy: beneficiary verification required for new payees; approval required above a threshold.

- Plan steps: validate beneficiary, verify account format, generate payment file, and stage it for approval.

- Execute tools: run “validate_beneficiary,” “format_payment,” and “stage_payment_batch.”

- Verify: confirm amount precision, currency match, and remittance reference rules.

- Capture evidence: store tool call parameters and verification results.

- Human review: if beneficiary is new or amount exceeds threshold, pause and request approval.

Example Workflow: Risk Limit Monitoring with Reconciliation

For limit monitoring, the orchestrator should:

- Normalize inputs: portfolio scope, limit set, valuation date.

- Retrieve exposures via deterministic tools.

- Compute utilization and compare to limits.

- Reconcile totals to the latest risk ledger snapshot.

- If utilization breaches, generate an exception package with evidence and the exact computations used.

Minimal Diagram of Execution Flow

graph TD

A[Intake Request] --> B[Normalize Task Schema]

B --> C[Policy Checks]

C --> D[Plan Steps]

D --> E[Tool Execute]

E --> F[Verify and Reconcile]

F --> G[Capture Evidence]

G --> H{Human Review Required?}

H -->|No| I[Finalize Output]

H -->|Yes| J[Route to Approver]

J --> I

This architecture keeps orchestration predictable: the orchestrator manages order and controls, tools provide deterministic results, and verification plus evidence make the workflow explainable. That combination is what turns “it ran” into “it can be trusted.”

2.2 Integrating Enterprise Systems Including ERP TMS and Banking Platforms

Enterprise integration is where agentic finance stops being a clever workflow and becomes a reliable operating capability. The goal is simple: the agent must read the right facts, act through the right systems, and leave an audit trail that matches what auditors and operators expect.

Start with System Boundaries and Responsibilities

Treat each system as owning specific truths. ERP typically owns legal entity structure, vendor/customer master data, and accounting treatment. TMS owns payment instructions, remittance details, and payment status transitions. Banking platforms own account balances, cut-off rules, and settlement outcomes.

A practical rule: the agent should not “recreate” master data. Instead, it should request authoritative fields from the system that owns them, then cache only what it needs for the current workflow.

Example: When preparing a payment, the agent pulls beneficiary name and address from ERP vendor records, pulls payment method and remittance format from TMS configuration, and pulls available balance and bank account identifiers from the banking platform.

Define Integration Contracts for Inputs Outputs and Evidence

Integration contracts specify what the agent must provide and what it can trust back. For each action, define:

- Input fields with formats and validation rules (currency codes, bank routing formats, invoice references)

- Output fields with status semantics (e.g., “submitted,” “accepted,” “rejected,” “settled”)

- Evidence artifacts (request/response payload hashes, timestamps, approver IDs)

Example: For a payment submission, the contract requires the agent to send a normalized beneficiary record, then store the banking platform’s acceptance reference as evidence. If the platform returns a rejection reason, the agent must map it to a TMS status and trigger an exception workflow.

Choose Integration Patterns That Match the Workflow Shape

Not every workflow needs the same integration style.

- Synchronous calls fit validations that must block execution, like checking beneficiary bank details before submission.

- Asynchronous events fit status updates, like receiving settlement confirmations after cut-off.

- Batch reconciliation fits accounting alignment, like matching ERP posted entries to TMS payment records.

Example: The agent can synchronously validate bank account ownership before sending a payment, then rely on asynchronous webhooks to update payment status when the bank confirms settlement.

Build a Canonical Data Model for Cross-System Consistency

ERP and TMS often use different identifiers for the same business object. A canonical model reduces confusion by mapping each object to a stable internal key.

Include canonical entities such as:

- Legal entity and operating unit

- Counterparty and beneficiary

- Payment instruction and payment line

- Invoice or settlement reference

- Risk and compliance flags

Example: ERP might store vendor ID as V-1042, while TMS stores beneficiary as B-7781. The canonical model links both to a single internal counterparty key so the agent can join facts without guessing.

Implement Tooling Layers for Safe Execution

Use a tooling layer that wraps each system call with consistent behavior: authentication, retries, idempotency keys, and structured error handling.

Idempotency matters because payment submissions are not “safe to repeat.” The tooling layer should attach an idempotency key derived from payment instruction ID plus version.

Example: If the agent retries after a network timeout, the banking platform should recognize the idempotency key and avoid duplicate submissions. The tooling layer records whether the retry resulted in a new submission or a previously accepted one.

Orchestrate Status Lifecycles Across ERP TMS and Banking

A common failure mode is mismatched status definitions. Define a single lifecycle model and map each system’s statuses into it.

Example lifecycle:

- Draft in TMS

- Approved in TMS

- Submitted to bank

- Accepted by bank

- Settled at bank

- Posted in ERP

The agent updates the lifecycle only when it receives evidence from the owning system. If ERP posting lags, the agent continues to monitor without re-posting.

Add Control Points Without Breaking Throughput

Integration should include control points that are enforceable and observable.

- Pre-submission checks: beneficiary verification, payment format validation, and required approvals

- Post-submission checks: bank acceptance reference captured, rejection reasons categorized

- Reconciliation checks: ERP posting matched to TMS payment ID

Example: If the bank rejects a payment due to an invalid routing number, the agent marks the instruction as “Rejected—Data Issue,” requests corrected bank details from ERP, and routes it back to the approval gate.

Mind Map: Integration of ERP TMS and Banking Platforms

Case Study: Payment Submission with Evidence Capture

A multinational uses ERP for vendor records, TMS for payment instructions, and a banking platform for submission and settlement confirmations.

- The agent selects invoices in ERP and creates a payment draft in TMS.

- Before approval, it synchronously validates beneficiary bank details by requesting the banking platform’s account metadata and comparing it to the canonical beneficiary record.

- After approval, it submits the payment through the tooling layer using an idempotency key tied to the TMS payment instruction ID.

- When the bank returns acceptance, the agent stores the acceptance reference and updates TMS status to “Accepted.”

- When settlement arrives, the agent updates TMS to “Settled,” then triggers a reconciliation check that ensures ERP posting exists for the same payment instruction ID.

The result is not just a working payment. It is a chain of evidence that ties each decision and action to the system that owns the truth.

2.3 Designing Task Decomposition for Transactional and Analytical Work

Task decomposition is how you turn a messy business goal into a sequence of actions that an agent can execute safely. The trick is to separate what must be executed exactly (transactional work) from what can be reasoned about (analytical work), then connect them with explicit handoffs. If you skip that separation, you get either brittle automation or vague analysis that never reaches a decision.

Foundational Principle: Separate Execution from Reasoning

Transactional tasks require deterministic outputs, strict validation, and clear stop conditions. Analytical tasks require structured inputs, assumptions, and traceable calculations. A good decomposition makes those differences visible.

A practical way to start is to define three layers:

- Inputs: the data and documents the workflow needs.

- Decisions: the rules that determine what happens next.

- Actions: the system operations that change state, such as creating a payment instruction or updating a risk limit status.

When you map a workflow, every step should answer: What data is required? What decision gates exist? What action is performed, and what evidence is recorded?

Mind Map: Decomposition Building Blocks

Transactional Decomposition: Payment and Instruction Work

Transactional workflows should be decomposed into small, testable steps with explicit validation after each step. A typical payment workflow can be broken into:

- Intake and Normalization: Parse invoice or payment request data into a canonical structure. Example: convert “1,250.00 USD” and “1250 USD” into a single numeric amount with currency code.

- Reference Resolution: Map vendor, bank account, and payment purpose to master data. Example: if the vendor has two active bank accounts, require the workflow to select the one tied to the invoice’s remittance reference.

- Control Checks: Apply rules before any state change. Example: verify beneficiary name matches the account owner on file; if it doesn’t, route to manual review.

- Instruction Drafting: Create the payment instruction payload without submitting it. Example: generate the SWIFT/SEPA fields and validate length and allowed characters.

- Approval Gate: For high-value or new-beneficiary cases, require a human signoff. Example: if amount exceeds a threshold or the beneficiary is first-time, pause and request approval.

- Submission and Confirmation: Submit to the banking interface and capture confirmation identifiers. Example: store the bank’s message ID and timestamp.

- Post-Action Reconciliation: Confirm that the payment appears in the expected ledger or status feed. Example: match instruction ID to settlement status; if missing after a defined window, open an exception ticket.

Notice how each step produces evidence. That evidence is what makes the workflow auditable and debuggable.

Analytical Decomposition: Forecasting and Risk Work

Analytical workflows should be decomposed into computations that can be validated independently. A risk monitoring workflow might follow:

- Scope Definition: Choose the portfolio, time horizon, and scenario set. Example: “last 30 business days, base and stress scenarios.”

- Data Preparation: Filter and align positions, rates, and exposures. Example: ensure all instruments use the same valuation date; if not, reconcile or exclude.

- Metric Computation: Compute exposures, sensitivities, or limit utilization. Example: calculate FX exposure by currency netting across entities.

- Assumption Traceability: Record assumptions used in the calculation. Example: document how missing rates were handled (e.g., interpolation method and source).

- Decision Logic: Compare metrics to thresholds and determine actions. Example: if limit utilization exceeds 90%, recommend escalation; if it exceeds 100%, require approval.

- Output Packaging: Produce a structured report for downstream systems. Example: include metric values, threshold levels, and the exact rules triggered.

Analytical steps should not directly change operational state. They should produce recommendations and evidence, then hand off to an execution workflow.

Handoffs: The Glue Between Analytical and Transactional Work

The handoff is where many designs fail. A clean handoff includes:

- A decision payload: what to do next and why.

- An evidence bundle: inputs, calculations, and rule triggers.

- A control context: which approvals or permissions apply.

Example: A cash forecast analysis recommends a funding action. The execution workflow then:

- Re-validates the required fields (available cash, target liquidity, funding instrument constraints).

- Applies the same control checks used for other funding actions.

- Records the forecast evidence ID so auditors can trace the recommendation to the executed action.

Example: Decomposing One Use Case End to End

Use case: “If FX exposure breaches a limit, propose hedging and then draft the hedge instruction.”

- Analytical steps produce: exposure breach details, suggested hedge size, and the rule that triggered escalation.

- Transactional steps consume: suggested hedge size, eligible instruments list, and beneficiary or counterparty constraints.

- Validation gates ensure: the hedge instruction is consistent with master data and approval requirements.

This decomposition keeps reasoning honest and execution controlled. The agent can be helpful without pretending it can skip the parts where mistakes are expensive.

2.4 Implementing Human in the Loop Review and Approval Gates

Human-in-the-loop gates are the part of an agentic workflow where responsibility becomes explicit. The goal is not to slow everything down; it is to ensure that high-impact actions are reviewed with the right evidence, by the right people, at the right time.

Start with Decision Types and Risk Levels

Before you design approvals, classify actions by consequence and reversibility.

- Low-impact, reversible: e.g., drafting a payment instruction for review. You can allow straight-through execution with logging.

- Medium-impact, partially reversible: e.g., updating a beneficiary name that affects future payments. Require review of the specific fields.

- High-impact, hard to reverse: e.g., submitting a payment, changing bank account details, or overriding risk limits. Require explicit approval.

A practical rule: if the action can cause money movement, regulatory exposure, or limit breaches, treat it as high-impact until proven otherwise.

Define Gate Triggers and Evidence Requirements

Each gate needs two things: when it triggers and what evidence the reviewer must see.

- Trigger examples

- Payment amount exceeds a threshold.

- Beneficiary account differs from master data.

- Forecast suggests a liquidity action outside normal ranges.

- Risk metric breaches a configured limit.

- Evidence examples

- Source data references (transaction IDs, forecast inputs).

- Calculations summary (what changed and why).

- Control checks performed (e.g., sanctions screening status, duplicate detection).

- Proposed action payload (exact fields to be sent).

Keep evidence structured so reviewers can scan quickly. A reviewer should not have to reverse-engineer the agent’s reasoning from raw logs.

Choose Gate Placement Along the Workflow

Gates work best when placed at natural boundaries.

- Pre-commit gate: before the system sends instructions to a bank or ERP.

- Pre-change gate: before master data updates that affect future operations.

- Post-commit monitoring gate: after submission, to verify confirmations and handle exceptions.

For example, a payment workflow can draft and validate automatically, then stop right before submission for approval, then resume to reconcile confirmation messages.

Implement Role-Based Approvals with Clear Authority

Approvals should map to roles that already exist in finance operations.

- Requester: initiates the workflow (often treasury ops).

- Reviewer: checks evidence and approves or rejects.

- Approver: required only for high-impact actions.

- Exception handler: resolves failures and documents remediation.

A simple but effective pattern is two-step approval for high-impact actions: one reviewer verifies correctness, and a second approver confirms policy alignment (such as limit compliance).

Use Deterministic Gate Logic and Avoid Ambiguous States

Gate logic must be deterministic: the system should always know whether it is waiting for approval, ready to proceed, or blocked.

- Statuses: Drafted, Awaiting Approval, Approved, Rejected, Submitted, Reconciliation Pending, Resolved.

- No silent fallthrough: if evidence is missing, the workflow must stop and request the missing inputs.

This prevents the classic failure mode where an agent “continues anyway” because a field was empty.

Mind Map: Human in the Loop Gates

Example: Payment Submission Gate with Field-Level Checks

Scenario: the agent drafts a payment for approval.

- Automatic steps

- Validate mandatory fields.

- Check beneficiary against master data.

- Run sanctions screening status check.

- Compute totals and fees.

- Gate trigger

- Payment amount is above the “single-approval” threshold.

- Beneficiary bank account differs from master data.

- Evidence shown to reviewer

- Payment draft payload with highlighted differences.

- Master data record reference and the exact mismatch fields.

- Screening status and timestamp.

- Calculation summary of amount and fees.

- Approval outcome

- If approved, the system submits the payment and records the approval ID.

- If rejected, the workflow returns to Drafted with a required correction note.

The key is that the reviewer approves a specific payload, not a vague plan.

Example: Risk Limit Breach Gate with Escalation Path

Scenario: the agent monitors limits and detects a breach.

- Automatic steps

- Recalculate exposure using the latest positions.

- Identify which component drove the breach.

- Compare against limit configuration.

- Gate trigger

- Breach severity is “hard limit.”

- Evidence shown to reviewer

- Exposure breakdown by instrument and counterparty.

- Limit definition and effective date.

- Control checks confirming data completeness.

- Approval outcome

- Reviewer can approve an action that reduces exposure.

- If no reduction action is approved, the workflow blocks further limit-impacting tasks and routes to exception handling.

This keeps the system from treating “breach detected” as permission to proceed.

Operationalizing Rejections and Exception Handling

Rejections should be actionable. Require a structured reason code (e.g., Missing evidence, Payload mismatch, Policy conflict) and a correction target (which field or which input set).

For exception handling, the workflow should capture:

- the failing step and error details,

- the remediation action taken,

- the evidence supporting the remediation,

- whether a new approval is required.

That way, the audit trail reflects both the decision and the correction path, without forcing reviewers to guess what happened.

2.5 Logging Traceability and Evidence Capture for Every Action

Agentic finance workflows only earn trust when you can reconstruct what happened, why it happened, and who (or what) approved it. Logging traceability is the record; evidence capture is the proof package. Together they let treasury, risk, compliance, and audit teams answer the same questions with the same facts—without chasing screenshots.

What “Every Action” Means in Practice

Treat an “action” as any step that changes state or creates a decision artifact. Examples include:

- Creating a payment draft and generating a beneficiary record.

- Calling a bank API to submit an instruction.

- Applying a risk limit rule and producing an approval or rejection.

- Marking a compliance check as passed and assembling an evidence bundle.

- Escalating an exception to a human reviewer.

A useful rule: if the step could affect money, risk posture, or regulatory standing, it must be logged with enough detail to replay the reasoning.

Traceability Model from Inputs to Outcomes

Start with a simple chain: input facts → decision logic → tool calls → outputs → approvals → final state. Each link needs identifiers and consistent fields.

Minimum trace fields for every action:

- Correlation identifiers: workflow_id, run_id, action_id.

- Actor: system component name and version; human reviewer identity when applicable.

- Trigger: event source (e.g., “monthly cash forecast run” or “payment exception detected”).

- Inputs snapshot: references to data versions and the exact parameters used.

- Decision record: rule/model name, version, and key outputs (not just a final label).

- Tool calls: endpoint/system name, request parameters (redacted), response status, and timestamps.

- Outputs: artifact IDs (payment instruction ID, risk report ID, evidence bundle ID).

- Approvals and overrides: who approved, what changed, and the reason code.

- Outcome: success/failure, error codes, and remediation path.

To keep logs readable, store large payloads (like full API responses) in an evidence store and log pointers plus hashes.

Evidence Capture as a Proof Package

Evidence is not “whatever we logged.” It is the subset that an auditor or control owner can verify. Build evidence bundles per action type.

Evidence bundle contents (tailored by action):

- Payment submission: payment instruction payload (redacted), bank response, timestamp, and approval record.

- Risk limit decision: exposure inputs, limit definition version, computed metrics, and the rule evaluation trace.

- Compliance check: policy version, mapping to the specific control, transaction attributes used, and pass/fail rationale.

- Exception escalation: exception classification, recommended action, reviewer decision, and final disposition.

Use stable naming and include a “bundle manifest” that lists included items and their hashes. That manifest becomes the anchor for later verification.

Logging Granularity and Redaction

Logs must be detailed enough to reconstruct, but not so detailed that they leak sensitive data.

A practical approach:

- Log identifiers and computed metrics freely.

- Redact secrets and personal data (account numbers, names, credentials) while preserving referential integrity (e.g., last-4 digits and internal IDs).

- Record data provenance (source system, extraction batch, transformation version) so you can explain why a value was used.

Mind Map: Traceability and Evidence Capture

Example: Payment Exception with Evidence Bundle

Assume a payment draft is created, then rejected by the bank due to beneficiary details.

Logged action sequence

action_id=pay_draft_createrecords workflow_id/run_id, payment fields (redacted), and the draft artifact ID.action_id=bank_submitlogs the bank endpoint, request parameters (redacted), response statusREJECTED, and bank error code.action_id=exception_classifystores the exception category, the rule name used, and the recommended fix (e.g., “verify beneficiary reference format”).action_id=human_approvalcaptures reviewer identity, approval decision, and reason code.action_id=evidence_bundle_creategeneratesbundle_id=EVB-2026-02-15-1042with a manifest listing the draft artifact hash, bank response hash, and approval record hash.

The key detail: the evidence bundle is created after the final disposition, but it references the exact artifacts produced earlier.

Example: Risk Limit Decision with Evaluation Trace

For a limit check, log the computed exposure metrics and the specific rule evaluation path.

- Record

limit_definition_versionand the metric inputs used. - Store the rule evaluation trace as structured data (e.g., which threshold was compared, and the resulting branch).

- If the decision is “approve with conditions,” log the condition set as an explicit output artifact ID.

This prevents the classic problem where logs show “approved” but not the math or the rule path that led there.

Operational Checks That Keep Logs Useful

- Consistency tests: every action must have correlation IDs and an outcome.

- Completeness checks: evidence bundles must include the manifest and hashes for referenced artifacts.

- Redaction verification: ensure sensitive fields are never written to the log store.

- Replay readiness: a control owner should be able to trace from a final artifact back to inputs and approvals using only IDs.

When these checks are in place, traceability stops being a compliance chore and becomes a practical debugging tool—one that works even when the original run is long gone.

3. Treasury Operations with Agentic Execution

3.1 Cash Forecasting Workflows With Structured Assumptions

Cash forecasting is easiest to trust when assumptions are explicit, testable, and tied to observable drivers. A structured workflow turns “best guesses” into a chain of inputs that can be reviewed, challenged, and audited.

The Goal of Structured Assumptions

A cash forecast should answer three practical questions: What cash movements are expected? When do they occur? What assumptions would make the forecast wrong? Structured assumptions make the third question answerable without rewriting the whole model.

Start by separating assumptions into three layers:

- Transaction drivers: what creates cash movements (invoices, payroll cycles, debt coupons, payment terms).

- Timing rules: how dates shift (cutoff times, settlement lags, holiday calendars, bank processing windows).

- Behavioral adjustments: what changes the pattern (collection rates by aging bucket, supplier payment prioritization, one-off events).

A useful rule of thumb: if an assumption can’t be traced to a driver, it probably belongs in a “review needed” bucket rather than the forecast.

Workflow from Inputs to Forecast

Step 1: Define the Forecast Scope

Choose the cash scope and horizon before touching assumptions. For example, decide whether you forecast only bank balances or also include intercompany settlements and intraday liquidity. Then set the horizon granularity, such as daily for the next 30 days and weekly beyond.

Example: A company forecasts daily cash for the next 45 days to manage payment deadlines, and weekly for the next quarter to plan funding capacity.

Step 2: Build an Assumption Inventory

Create a list of assumptions with owners, sources, and review frequency. Each assumption should include:

- Assumption statement: “Collections for 31–45 day receivables occur 70% in week 1.”

- Source: last 6 months of collection history.

- Update cadence: monthly.

- Confidence or variability: derived from historical dispersion.

- Impact path: which forecast line items it affects.

This inventory prevents the common failure mode where assumptions live in spreadsheets with no clear lineage.

Step 3: Map Assumptions to Cash Movement Types

Cash forecasts usually combine recurring and non-recurring movements. Map assumptions to categories so reviewers know where to look.

- Operating inflows: customer collections by aging and payment method.

- Operating outflows: vendor payments by terms and scheduled runs.

- Payroll and taxes: fixed calendars with known variability windows.

- Financing: interest, principal, revolver draws, lease payments.

- Investing and other: capex disbursements, dividends, intercompany settlements.

Example: Payroll timing is calendar-driven, while vendor payments are terms-driven with a “payment run” timing rule.

Step 4: Encode Timing Rules Explicitly

Timing rules are where forecasts quietly drift. Capture them as deterministic rules first, then add variability.

Common timing rules include:

- Settlement lag: invoice date to expected cash receipt date.

- Cutoff and processing windows: payments initiated before a cutoff settle sooner.

- Non-business days: shift to next business day.

- Bank holidays: apply bank-specific calendars.

Example: If a payment is submitted after 3:00 PM local cutoff, assume settlement shifts by one business day.

Step 5: Apply Behavioral Adjustments with Guardrails

Behavioral adjustments should be bounded. Instead of “collections will be higher,” use aging-bucket adjustments with caps.

Example: If historical collections for 0–30 day receivables average 85%, set a cap at 92% and a floor at 75% for the next month unless a documented reason changes it.

Guardrails reduce the chance that a single optimistic assumption dominates the forecast.

Step 6: Reconcile with Actuals and Close the Loop

At each refresh, reconcile forecasted vs. actual cash movements. Use variance analysis to update assumptions that are truly wrong.

A practical approach:

- Compute variance by cash movement type.

- Attribute variance to timing vs. amount.

- Update only the assumptions implicated by the attribution.

This avoids “model churn,” where everything changes because someone wants the forecast to look better.

Mind Map: Structured Assumptions

Example: Collections Assumptions That Don’t Drift

Suppose the company forecasts customer collections from receivables aging. Use a structured assumption set:

- Driver: receivables balance by aging bucket.

- Timing rule: expected cash receipt date = invoice due date + settlement lag.

- Behavioral adjustment: collection rate by bucket.

Example: For the 31–45 day bucket, assume 70% collected in week 1 and 30% in week 2. If actuals show week 1 collections at 60%, attribute variance to amount (collection rate) rather than timing unless receipts consistently arrive earlier or later than expected.

The result is a forecast that can be explained in plain language: “We expected 70% of that bucket in week 1; actual was 60%, so the forecast is short by the difference, not because the calendar suddenly changed.”

Practical Checklist for Reviewers

Before approving a forecast run, verify:

- Every assumption has a source and an owner.

- Timing rules are calendar-aware and bank-aware.

- Behavioral adjustments have caps, floors, and a reason.

- Variance analysis is ready for the next refresh.

If any item fails, the forecast can still be produced, but it should be labeled as “needs review” so the team knows where attention belongs.

3.2 Liquidity Management Including Cash Concentration and Sweeps

Liquidity management answers one question: “Do we have the right cash, in the right place, at the right time?” Cash concentration and sweeps are the practical mechanisms that move cash from where it sits idle to where it is needed, while keeping controls, tax, and banking constraints in view.

Core Concepts and Why Location Matters

Start with the basics. Cash concentration pools balances from multiple legal entities or bank accounts into fewer “hub” accounts. Sweeps then automate movement of balances based on rules, such as end-of-day thresholds. The key nuance is that liquidity is not just an amount; it is also a location tied to bank accounts, currencies, and legal entities.

A simple example: Entity A has $5 million in an operating account overnight, while Entity B needs $2 million for payroll the next morning. Without concentration, B may borrow or delay. With concentration and a sweep, A’s excess can be transferred to the hub, and then made available to B through internal funding or direct sweep logic.

Cash Concentration Models and Their Tradeoffs

Common concentration structures include:

- Physical concentration: balances are transferred to a hub account. This reduces idle cash but creates more movement and requires careful reconciliation.

- Notional concentration: balances are offset for interest calculation without moving principal. This can reduce transfer volume, but interest allocation and bank reporting must be precise.

A best-practice approach is to map each entity’s cash behavior. If an entity’s balance is volatile and unpredictable, sweeping it aggressively can increase exceptions. If an entity’s balance is consistently above a minimum, it is a strong candidate for concentration.

Sweep Mechanics and Rule Design

Sweeps typically run on a schedule, often end-of-day, and follow rules. Good rules are explicit about inputs, thresholds, and exceptions.

Consider a threshold-based sweep:

- If available balance exceeds a target buffer (e.g., $500,000), sweep the excess to the hub.

- If the balance is below the buffer, do nothing.

The “available balance” definition matters. It should exclude amounts reserved for payments already queued, such as scheduled wires or payroll files. Otherwise, the sweep can create avoidable payment failures.

A second rule handles minimums for operational continuity. For example, a subsidiary may need a $200,000 intraday buffer to cover card settlements. The sweep should respect that buffer even if the end-of-day balance looks temporarily high.

Controls That Prevent Costly Surprises

Liquidity automation is only as safe as its guardrails. Build controls around three failure modes: wrong direction, wrong amount, and wrong timing.

- Wrong direction: ensure the sweep direction is tied to a clear “excess vs. deficit” condition. For deficit scenarios, decide whether you want a reverse sweep, an internal loan, or no action.

- Wrong amount: enforce rounding rules and maximum transfer caps. For example, cap daily sweeps at $3 million to avoid large transfers caused by data errors.

- Wrong timing: align sweep execution with cutoffs for payment files. If your bank cutoff is 3:00 PM local time, schedule sweeps after the cutoff or coordinate with payment processing.

Reconciliation is the fourth control. Each sweep should produce an evidence record: source account balance, computed sweep amount, transfer reference, and resulting hub balance.

Mind Map: Liquidity Concentration and Sweeps

Example: End-of-Day Excess Sweep with Payment Reservations

Assume three entities share a hub in the same currency.

- Entity A: operating account balance $6,200,000; reserved payments $1,000,000

- Entity B: operating account balance $1,100,000; reserved payments $900,000

- Entity C: operating account balance $450,000; reserved payments $50,000

Rules:

- Target buffer: $500,000 per entity

- Available balance = current balance minus reserved payments

- Sweep excess to hub at end of day

Compute available balances:

- A: $6,200,000 − $1,000,000 = $5,200,000 excess over buffer $500,000 → sweep $4,700,000

- B: $1,100,000 − $900,000 = $200,000 below buffer → sweep $0

- C: $450,000 − $50,000 = $400,000 below buffer → sweep $0

This example shows why reservations are non-negotiable. If you sweep based on the raw balance, Entity A would transfer too much and create payment failures.

Example: Handling Exceptions Without Breaking the System

Define exceptions so operations can respond quickly and consistently.

Common exceptions include:

- Missing or late balance feeds

- Unavailable hub account due to bank maintenance

- Currency mismatch where the sweep requires conversion

A practical response rule is to stop sweeping for the affected entity and route it to manual review. For instance, if Entity C’s balance feed is missing, keep its funds in place and document the reason. That prevents “silent” failures where the system appears to run but does not move cash as intended.

Operational Checklist for Reliable Sweeps

A reliable liquidity setup includes: clear definitions of available balance, entity-specific buffers, cutoff-aware scheduling, caps and rounding rules, exception triggers, and reconciliation evidence for every sweep. When these pieces are consistent, concentration becomes a controlled plumbing system rather than a daily guessing game.

3.3 Debt and Funding Operations Including Rollovers and Notices

Debt and funding operations are where “paper decisions” meet cash reality. The goal is simple: keep funding available, keep costs within policy, and ensure every notice and rollover is executed with the right approvals and evidence.

Core Concepts That Drive Reliable Execution

Start with three inputs: the debt instrument terms, the funding calendar, and the decision rules. Terms include maturity dates, coupon reset schedules, call or put features, notice periods, and any covenants that affect refinancing options. The funding calendar lists upcoming maturities, interest payment dates, rate reset dates, and required notice deadlines. Decision rules define what actions are allowed, who approves them, and which conditions trigger exceptions.

A practical best practice is to represent each obligation as a structured record with fields for maturity, currency, instrument type, benchmark and spread, settlement instructions, and notice windows. For example, a $50 million USD term loan due 2026-06-30 with a 30-day notice period for prepayment should carry a computed “earliest notice date” and “latest safe notice date” based on your operational cutoffs.

Rollover Workflow from Intake to Execution

Rollover is the controlled replacement of maturing funding with a new instrument or extension. A systematic workflow prevents last-minute scrambling.

- Instrument intake and validation: Confirm the instrument identity, currency, and maturity. Validate that settlement accounts and payment calendars match the treasury bank setup.

- Eligibility check: Verify whether the instrument can be rolled over under current authority limits and any covenant constraints. If the debt is tied to a credit agreement, ensure the relevant covenant status is current.

- Funding option preparation: Generate candidate actions such as refinancing with a new loan, extending the existing facility, or using short-term funding to bridge. Each option should map to expected cash flows and operational steps.

- Cost and risk comparison: Compare options using the same assumptions you use elsewhere in treasury. For instance, if you compare a 3-month bill bridge versus a 12-month rollover, use consistent day count conventions and include fees.

- Approval gate: Route the selected action to the correct approver based on amount, tenor, and instrument type. Evidence should include the option set, the selected rationale, and the approval record.

- Execution and confirmation: Submit instructions to the bank or counterparty, then capture confirmations. For a rollover, confirmations often include revised maturity dates, new interest terms, and updated settlement details.

A concrete example: On 2026-04-10, you identify a maturity on 2026-06-30. Your notice window is 30 days. Your “latest safe notice date” is 2026-05-31 after accounting for internal review and bank processing. If approval is required by 2026-05-20, the workflow should flag any missing approvals as early as 2026-05-15.

Notice Management That Prevents Missed Deadlines

Notices are time-bound communications that can be strict. Treat them as first-class work items with deadlines, templates, and evidence requirements.

A notice workflow should include:

- Notice type: maturity extension, prepayment election, rate reset notice, or conversion election.

- Deadline computation: derive the deadline from the instrument terms and your operational cutoffs.

- Content assembly: populate required fields such as reference numbers, amounts, effective dates, and payment instructions.

- Review and signoff: ensure the notice is reviewed by the appropriate role and signed according to policy.

- Delivery proof: store proof of delivery such as email logs, portal submission receipts, or courier tracking.

Example: A bondholder notice requires the “principal amount to be redeemed” and an “effective redemption date.” If the redemption date falls on a non-business day, your notice should reflect the correct adjusted date per the instrument’s business day convention.

Mind Map: Debt and Funding Operations

Controls and Evidence That Make Audits Boring

To keep operations clean, tie every rollover and notice to an evidence bundle: the computed deadlines, the approved action, the executed instruction, and the received confirmation. Reconcile the confirmation against the original terms you expected to change. If the confirmation differs, route it to an exception workflow rather than silently updating records.

A final practical rule: never let “deadline passed” be the first time someone learns about a problem. Your process should surface risks when the notice window is still wide enough to correct content, approvals, or settlement details.

3.4 Bank Account Management and Payment Instruction Governance

Bank account management is where “finance operations” meets “systems reality.” If the account list is wrong, every downstream payment workflow becomes a confidence problem. Governance is the set of rules that keeps the account master accurate, the payment instructions consistent, and the audit trail complete.

Foundational Concepts for Account Governance

Start with three objects: (1) the legal entity that owns the account, (2) the bank account record, and (3) the payment instruction template. A bank account record should include immutable identifiers (bank country, bank code, account number or tokenized reference, account holder name, currency, and account type). Payment instruction templates should include what changes frequently (beneficiary reference formatting, remittance fields mapping, and payment method constraints).

A practical best practice is to treat account records as “slow-moving” and instruction templates as “faster-moving.” For example, the account number rarely changes, but the way you populate remittance lines can evolve with customer billing formats.

Master Data Controls for Bank Accounts

Use a single source of truth for bank accounts, with strict lifecycle states: Draft, Active, Suspended, and Closed. Only Active accounts can be selected in payment creation. Suspended accounts remain visible for investigation and reconciliation, but they block new payments.

Validation rules should be explicit and testable:

- Format checks: bank code length by country, IBAN checksum where applicable, currency match.

- Consistency checks: account holder name must match the legal entity’s registered name or a controlled alias list.

- Uniqueness checks: prevent duplicate active records for the same bank account reference and currency.

Example: If a user tries to add a USD account for Entity A but the record’s currency is EUR, the system should stop the workflow before any payment instruction is generated.

Role-Based Access and Segregation of Duties

Governance requires separation between “requesting” and “approving” changes. A common pattern:

- Account requester: proposes changes and provides supporting documentation.

- Account approver: validates documentation and activates or suspends the account.

- Payment operator: creates payments using Active accounts but cannot modify account master data.

This separation prevents a single person from both changing the destination and approving the payment. If your organization uses a single approval group, at least require two distinct approvals for high-risk fields such as account number, bank code, and account holder name.

Payment Instruction Governance for Accuracy

Payment instructions are where errors become expensive. Define a mapping layer between payment fields and instruction fields, and enforce it through templates.

Key governance controls:

- Template selection rules: payment method and currency determine which template is allowed.

- Mandatory fields: beneficiary name, beneficiary bank identifiers, and remittance mapping must be present.

- Field-level immutability: once a payment is submitted for execution, critical fields should be locked.

Example: For SEPA credit transfers, ensure the template enforces IBAN-based beneficiary details and restricts remittance fields to the allowed character limits. If a remittance reference exceeds the limit, the system should either truncate using a defined rule or reject with a clear message.

Change Management with Evidence Capture

Every account change should produce an evidence bundle: request form, documentation (bank confirmation letter or signed mandate), approver identity, and timestamps. Store evidence in a way that can be retrieved during reconciliation and audits.

A useful operational rule is to require evidence for both activation and deactivation. Deactivation often happens during investigations, and missing evidence turns a simple closure into a long explanation.

Example: When an account is suspended after a suspected mismatch, capture the reason code, the approver, and the reconciliation outcome that triggered the suspension.

Exception Handling and Reconciliation Loops

Governance must include what happens when reality disagrees with the master data. Define exception categories:

- Payment rejected by bank due to beneficiary details.

- Payment returned due to incorrect remittance or beneficiary mismatch.

- Account master mismatch discovered during reconciliation.

For each category, specify the allowed actions. For instance, if a payment is rejected due to beneficiary bank identifiers, you may update the instruction template mapping only after an approver reviews the underlying account record.

Mind Map: Bank Account Management and Payment Instruction Governance

Example Workflow: Adding and Using a New Account

- A requester submits a new bank account record for Entity A with documentation and a proposed activation date.

- The system validates country-specific formats and checks for duplicates against existing Active records.

- An approver reviews evidence and approves the activation; the record transitions from Draft to Active.

- Payment operators can now select the account when creating payments, but they cannot edit account identifiers.

- If a payment fails due to beneficiary mismatch, the exception workflow checks whether the account record or the instruction template mapping is responsible, then routes the remediation to the correct approver.

This structure keeps the account list trustworthy and ensures payment instructions remain consistent with the governed master data.

4. Payments and Working Capital Optimization

4.1 Payment Lifecycle Management From Draft to Settlement

Payment lifecycle management is the boring part that keeps money from going to the wrong place. This section describes a practical end-to-end flow, with controls at the moments where errors are most likely: when data is created, when it is approved, when it is sent, and when it is reconciled.

Payment Lifecycle Stages

Draft and Data Capture

A payment draft starts as a structured request, not a free-form email. The draft should include: payee identity, payment method, currency, amount, value date, payment reference, and supporting documents. A simple best practice is to require the draft to reference a source record such as an invoice or contract line, so the payment can be traced back to the business reason.

Example: A buyer submits a draft for an invoice of $48,250.00. The draft pulls vendor bank details from master data, sets the payment reference to the invoice number, and records the value date as 2026-02-15.

Validation and Pre-Send Checks

Before approval, the system should run deterministic checks that catch common issues without needing judgment. Typical checks include:

- Amount and currency consistency with the source invoice

- Mandatory fields present, including beneficiary name and account identifiers

- Payment reference format rules

- Bank account validity rules, such as checksum or country-specific formatting

- Duplicate detection using a combination of payee, amount, currency, and reference

Example: The system flags a draft where the invoice currency is USD but the payment currency is EUR, and blocks submission until the mismatch is corrected.

Approval and Authorization

Approval should be role-based and risk-based. Low-value payments might require one approval, while high-value or new-beneficiary payments require additional review. The key is to define approval gates that match control objectives: preventing unauthorized payments, preventing tampering after approval, and ensuring segregation of duties.

Best practice: lock the payment fields that affect settlement once approved. If a user changes the amount or beneficiary after approval, the workflow should revert to a new approval cycle.

Example: A payment over a threshold requires two approvals. The first approval validates the business basis; the second confirms beneficiary details. If the beneficiary bank account is edited, the second approval is invalidated.

Payment File Creation and Transmission

For bank connectivity, payments are often sent as files or via an API. The lifecycle should include a clear separation between the approved payment record and the transmitted instruction. Generate the payment file from the approved dataset, then compute and store a file hash or checksum for integrity.

Example: After approval, the system generates a SEPA credit transfer file, stores the checksum, and transmits it to the bank. If transmission fails, the draft remains in a “ready to send” state rather than being marked as sent.

Bank Response Handling and Status Updates

Banks respond with acknowledgements and later settlement confirmations. Your workflow should map bank messages into internal statuses such as: accepted, rejected, pending, returned, or settled. Each status change should be tied to the original payment instruction and the bank message identifier.

Example: A payment is accepted by the bank but later returned due to beneficiary account closure. The system records the return reason code and triggers an exception workflow.

Exception Management and Corrections

Exceptions are not failures of the process; they are branches that must still be controlled. Common exceptions include missing remittance details, beneficiary validation failures, insufficient funds, and formatting errors.

Best practice: treat exceptions as structured work items with required fields for resolution. For instance, a returned payment should capture the return reason, the action taken (reissue, cancel, or manual settlement), and the evidence supporting the decision.

Example: A returned payment due to an invalid beneficiary account triggers a workflow to update master data, re-validate the account, and re-approve the corrected payment before re-sending.

Settlement Confirmation and Reconciliation

Settlement is where accounting reality meets bank reality. Reconciliation should match payments to bank statements using reference fields and amounts, then update ledger entries and payment statuses. The control objective is to ensure every settled payment has a corresponding accounting entry and every accounting entry has a bank settlement.

Example: The system reconciles a settled payment by matching the bank statement reference to the invoice number stored in the payment reference field. Any unmatched items become reconciliation exceptions with assigned owners.

Integrated Example Walkthrough

A finance team processes a $48,250.00 USD invoice payment.

- The draft is created from the invoice record, auto-filling beneficiary details from master data and setting the value date to 2026-02-15.

- Pre-send checks confirm currency match, required fields, and reference format, and run duplicate detection.

- The payment is approved by two roles because it exceeds the threshold.

- The system generates a bank file from the approved snapshot, stores a checksum, and transmits it.

- The bank accepts the instruction; the status updates to accepted.

- Later, the bank settles the payment; the system reconciles it to the invoice reference and posts the accounting entry.

- If the bank had returned it, the workflow would require beneficiary validation, evidence capture for the correction, and re-approval before re-sending.

Control Checklist for This Stage

- Draft references a source record

- Pre-send checks are deterministic and blocking

- Approval gates match risk and segregation of duties

- Approved fields are locked against post-approval edits

- Transmission stores integrity evidence and outcomes

- Bank messages map to internal statuses with identifiers

- Exceptions are structured and require re-approval when fields change

- Settlement reconciliation matches bank and ledger with clear exception handling

4.2 Exception Handling for Failed Payments and Missing Remittances

Failed payments and missing remittances are the two sides of the same coin: money didn’t arrive as expected, and the ledger needs a story that matches reality. The goal of exception handling is not just to “fix” the payment, but to (1) classify what went wrong, (2) gather evidence, (3) decide the correct next action, and (4) close the loop in accounting and controls.

Exception Handling Foundations

Start with a consistent exception taxonomy so every case follows the same workflow. Use three labels:

- Failure type: rejected, returned, delayed, or partially settled.

- Scope: beneficiary bank issue, intermediary network issue, internal data issue, or unknown.

- Accounting impact: requires reversal, requires reclassification, or requires only reconciliation.

A practical example: a supplier payment is submitted, but the bank returns it with a “beneficiary account closed” reason. That is a rejected/returned failure type, beneficiary bank issue scope, and accounting impact of reversal plus a new payment attempt after updated beneficiary details.

Detection and Triage Workflow

Detection should combine operational signals and ledger checks. Operational signals include bank status messages, payment confirmations, and remittance advice feeds. Ledger checks include “payment sent but not cleared” aging and “invoice paid but not matched” flags.

Triage should happen in a fixed order:

- Validate identifiers: payment reference, invoice number, beneficiary account, and currency.

- Check timing: compare expected settlement windows to actual timestamps.