Equity Structure Design and Corporate Control Essentials

1. Foundations of Equity Structure and Corporate Control

1.1 Ownership Rights and Control Pathways

Ownership rights are not just about who holds shares. They determine who can decide, who can block, who can receive value, and who can influence the company when decisions get messy. Control pathways are the practical routes from ownership to outcomes, shaped by law, charter documents, and the specific terms attached to each equity class.

Ownership Rights as a Decision System

Start with the three core categories of rights.

- Voting rights decide matters submitted to shareholders. If a vote is required, the voting rights determine who can approve or reject.

- Economic rights determine who receives money or value, such as dividends, liquidation proceeds, and conversion value.

- Information and procedural rights determine who gets notified, who can inspect records, and what steps must occur for actions to be valid.

A useful way to think about control is: voting rights control decisions directly; economic rights control incentives indirectly; procedural rights control whether decisions can be taken at all.

Control Pathways: From Shareholder to Board to Company Actions

In most corporations, shareholders rarely run daily operations. Instead, they control the company through a chain.

- Shareholders elect directors and approve certain fundamental actions.

- Directors set strategy, oversee management, and approve major transactions.

- Management executes day-to-day operations under board oversight.

Ownership rights shape each link. For example, a shareholder with strong voting rights can influence board composition, which then influences board decisions on budgets, hiring executives, and approving financing.

The “Right” to Vote Versus the “Ability” to Vote

Not all votes are equal in practice.

- Record date mechanics determine which shareholders count for a vote. If someone buys after the record date, they may not vote even if they hold shares before the meeting.

- Quorum and meeting rules can prevent action if attendance thresholds are not met.

- Class voting means some decisions require approval by specific equity classes, not the entire cap table.

A control pathway fails when the documents require a vote that the controlling party cannot actually secure.

Protective Rights and Reserved Matters

Even when a shareholder can elect directors, they may still lack control over certain actions. Protective provisions and reserved matters carve out decisions that require additional approvals, often by class vote or supermajority.

This is where governance control becomes more than “who has the most shares.” It becomes “who can block specific categories of actions.”

Economic Rights That Influence Control

Economic rights can change behavior even when they do not directly vote.

- Liquidation preferences can make certain investors more focused on downside protection, which can affect how they push for financing terms.

- Conversion rights can shift voting power over time if conversion is triggered.

- Dividend terms can create pressure for cash management decisions.

Economic rights are incentive levers. They often explain why two groups with similar voting power still behave differently.

Mind Map: Ownership Rights and Control Pathways

Example: Two Investors with Different Control Profiles

Assume a company has 100 common shares.

- Investor A holds 55 common shares.

- Investor B holds 45 common shares.

If the charter requires a simple majority for director elections, Investor A can elect the full board. That looks like clear control.

Now add a reserved matter: issuing new preferred shares requires approval by a supermajority of the preferred class and a separate class vote of common. If Investor B later receives preferred with class voting rights, Investor B may block the financing even if Investor A controls board elections.

The key point: control is not a single number. It is the combination of voting thresholds, class structure, and reserved matters.

Example: Procedural Rights That Prevent “Control by Accident”

Suppose management wants to approve a major asset sale. The board votes, but the charter requires shareholder approval for transactions above a threshold.

If the company fails to provide proper notice or uses the wrong record date, the approval can be challenged. In that moment, procedural rights become a control pathway: they stop actions from becoming effective.

A Systematic Checklist for Mapping Control Pathways

To map ownership rights to control outcomes, identify:

- Which actions require shareholder votes, board votes, or both.

- Which equity classes vote on each action.

- What thresholds apply for each vote.

- What procedural steps must occur for validity.

- Which economic terms create incentive pressure on decision-makers.

Once you can answer those five items, you can explain control pathways in plain language: who can approve, who can block, and how value terms shape behavior.

1.2 Governance Mechanisms That Translate Equity Into Decisions

Equity only becomes “control” when governance mechanisms convert ownership into specific, repeatable decision outcomes. The key is to separate three layers: who has the authority, how decisions are made, and what happens when interests conflict. A well-designed system makes those layers explicit so the company can act without constant renegotiation.

Ownership to Authority

Start with the simplest mapping: equity class and voting rights determine who can approve or block certain actions. If founders hold common shares and investors hold preferred shares, the charter and investor rights agreement typically specify which class votes are required for major matters. For ordinary operations, the board usually acts on behalf of the company, while shareholders vote mainly on reserved matters.

A practical example: a company plans to issue new shares to fund a product launch. If the issuance would dilute investor economics, the documents may require a preferred class vote or a protective provision consent. Without that mechanism, investors might only complain after the fact, which is like trying to steer a car after the crash.

Board as the Decision Engine

The board translates equity into decisions through appointment rights, committee structure, and voting procedures. Appointment rights determine who sits on the board, and board composition determines which perspectives are present when tradeoffs arise.

A common pattern is a board with a majority of independent directors plus seats for founders and investors. Independence matters because it reduces the chance that a single shareholder bloc controls every outcome. Committees add focus: audit for financial oversight, compensation for executive pay, and sometimes governance or strategy for specific domains.

Example: if the company wants to adopt a new executive compensation plan, the compensation committee can review design choices, benchmark pay levels, and recommend approval. The board then votes, and the minutes record the rationale. This turns equity influence into a documented process rather than a series of informal conversations.

Reserved Matters and Protective Provisions

Reserved matters define the boundary between “management runs the business” and “owners must agree on major changes.” The mechanism is not just the list; it’s the threshold and the scope.

A good reserved matter clause is precise. Instead of “material transactions,” it specifies categories such as mergers, asset sales above a dollar threshold, incurring debt beyond a limit, changing the number of authorized shares, or amending the charter. Precision prevents disputes about whether something counts.

Example: a company sells a subsidiary. If the clause covers “sale of all or substantially all assets,” the board might still need investor consent if the sale is structured as multiple smaller transfers. Drafting should address aggregation and related-party structuring so the mechanism can’t be bypassed by paperwork gymnastics.

Voting Thresholds and Decision Rules

Decision rules determine how many votes are needed and which votes count. Thresholds can be simple majority, supermajority, or class vote requirements. The system should also specify whether abstentions count and how quorum is established.

Example: suppose a supermajority of the board is required to approve a related-party transaction. If one director abstains due to conflict, the quorum and voting rule determine whether the transaction can proceed. Clear rules reduce “interpretation fights” and keep decisions moving.

Information Rights and Effective Oversight

Oversight requires more than the right to vote. Information rights provide the inputs that make voting meaningful. These rights often include periodic financial statements, budgets, and notice of major events.

Example: an investor has protective consent rights over additional debt. If the company provides monthly cash flow and a quarterly budget, the investor can evaluate whether the debt is truly “necessary and reasonable” rather than reacting to a single press-release style update.

Conflict Management and Fiduciary Boundaries

Equity holders and directors may have conflicting incentives, especially when a decision affects their economics or control. Governance mechanisms handle this through conflict-of-interest policies, recusal requirements, and sometimes independent director approvals.

Example: if the company considers awarding a contract to a founder-affiliated vendor, the board can require disclosure, recusal of conflicted directors, and review by an independent committee. The goal is not to eliminate bias entirely, but to ensure the decision process is defensible.

Document Hierarchy and Consistency

Governance mechanisms live across multiple documents: charter, bylaws, shareholder agreements, and board policies. Consistency matters because contradictions create uncertainty about which rule applies.

A simple hierarchy rule can prevent chaos: charter controls over bylaws, and investor rights agreements specify additional class-level consent requirements. When drafting, map each governance action to the exact document section that governs it.

Mind Map: Equity to Decisions

Integrated Example: Funding a Product Launch

A company needs $10 million to launch a product. Management proposes a financing round.

- Authority check: The charter and investor rights agreement determine whether the issuance requires a preferred class vote due to protective provisions.

- Board process: The board reviews the budget, approves the financing terms, and assigns committee review if executive compensation or option grants are part of the package.

- Information inputs: Investors receive cash flow forecasts, use-of-proceeds detail, and the updated capitalization table.

- Conflict handling: If a director has an investment interest, disclosure and recusal rules apply.

- Decision rule: The vote threshold is applied exactly as written, with quorum and abstentions handled per the bylaws.

When these mechanisms work together, equity influence becomes predictable. The company can raise capital, investors can protect their rights, and the board can document decisions in a way that stands up to scrutiny.

1.3 Economic Rights and Their Interaction with Voting Power

Economic rights answer a simple question: “Who gets what, and when?” Voting power answers: “Who gets to decide?” In practice, the two are tightly linked because the people who control outcomes often also control the rules that determine outcomes.

The Core Economic Rights

Economic rights typically include dividends, liquidation proceeds, redemption or buyback rights, and participation in value on major events. For example, a preferred investor might receive a fixed dividend and a priority claim on liquidation proceeds, while common shareholders receive whatever remains after those priorities are satisfied.

A key nuance is that economic rights can be structured to influence behavior even when voting rights are limited. If a class receives priority economics, it may be less willing to approve actions that reduce its expected payout, even if it technically can’t block the decision.

How Voting Power Changes the Meaning of Economic Rights

Voting power determines which group can approve corporate actions that affect economic outcomes. Those actions include issuing new shares, changing dividend policy, approving mergers, authorizing redemptions, and amending charter terms.

Consider two scenarios:

-

Common shareholders hold most voting power, but preferred shareholders hold strong economic preferences. If the company wants to raise capital by issuing new shares, common may approve the issuance, but the preferred’s liquidation preference can reduce the value that common expects to receive. Common’s voting power then becomes a tool that can shift economics away from itself.

-

Preferred shareholders hold protective voting rights, even if they own a minority of equity. In that case, economic rights and voting rights reinforce each other. Preferred investors can block transactions that would worsen their payout position, such as issuing senior securities or changing conversion terms.

The interaction is easiest to see when you map “decision rights” to “economic impact.” Voting rights are the steering wheel; economic rights determine where the car ends up.

Priority Economics and Control Incentives

Liquidation preferences are the classic bridge between economics and control. A 1x non-participating preference means the preferred gets its principal back first, then common shares share the remainder. A participating preference means the preferred may take its principal and then also share in the remaining proceeds.

Example: Suppose a company sells for $100 million.

- Preferred has $30 million of 1x non-participating preference.

- Common owns the rest.

If the sale price is $100 million, preferred receives $30 million and common receives $70 million. If the sale price drops to $40 million, preferred still receives $30 million, leaving only $10 million for common. Common’s economic exposure becomes highly sensitive to downside outcomes.

Now connect that to voting. If common holds the votes to approve a sale, but preferred expects to be protected by its preference, common may still approve a sale that is “good for preferred” but “bad for common.” That mismatch is why many deals pair economic preferences with protective provisions or negotiation over conversion.

Conversion Rights and the Voting-Economics Loop

Conversion rights let preferred convert into common, usually at the investor’s option. Conversion changes both economics and voting power because converted shares typically vote with common.

Example: Preferred converts on a qualified financing or at a sale. If conversion is mandatory at a certain threshold, then the investor’s voting position can shift from protective-only to full voting participation. That means the company’s capital structure can change who effectively controls outcomes.

A practical way to reason about this is to ask: “At the decision point, is the investor likely to be converted or not?” If the investor is likely to convert, then its voting influence grows. If it is likely to stay preferred, its influence may be limited to protective votes.

Dividends and the Timing of Value

Dividends affect economics over time, not just at exit. Cumulative dividends can accumulate if unpaid, increasing the amount that must be satisfied before common receives anything in liquidation.

Example: Preferred has a $2 million annual cumulative dividend. If the company skips dividends for two years, the preference stack may grow by $4 million. Even if preferred does not vote on day-to-day matters, the accumulated dividend can change the economic stakes of approvals like refinancing, dividend policy changes, or liquidation.

This is where voting rights matter again: if the company needs approvals to change dividend policy or to authorize actions that affect whether dividends are paid, the group with voting leverage can influence the timing and size of economic claims.

Mind Map: Economic Rights Meet Voting Power

A Simple Integrated Example

Assume a company has common and preferred with a 1x non-participating liquidation preference. Preferred also has protective voting rights over issuing senior securities and changing conversion terms.

If the company proposes a new financing that would create another senior class, common might be tempted to approve because it needs capital. Preferred can block it because the new senior class would reduce preferred’s relative payout position. Economic rights therefore translate into voting leverage, even when preferred owns less equity.

The design goal is not to make one side “win,” but to ensure the voting structure matches the economic stakes. When those match, decisions are easier to justify internally, and the documents behave like they were meant to: clear on paper, coherent in outcomes.

1.4 Agency Risks and Misalignment Between Owners and Managers

Agency risk shows up when the people running the company (managers) do not bear the full consequences of their decisions, while owners do. The result is not that managers are “bad”; it’s that incentives, information, and decision rights can point in different directions.

Core Concept of Agency Risk

Agency risk has three ingredients: (1) a separation between ownership and control, (2) incomplete information about effort and quality, and (3) incentives that can be satisfied without maximizing owner value. When these ingredients combine, managers can choose actions that look rational under their personal goals but reduce long-term outcomes for owners.

A simple example: a manager’s bonus is tied to quarterly revenue. They may push aggressive discounting to hit targets. Revenue rises, but gross margin falls and customer churn increases. Owners experience lower long-term value even though the manager met the metric.

Where Misalignment Comes From

Misalignment usually starts with how decisions are measured and rewarded.

- Goal substitution: Managers optimize for what is tracked. If the company tracks “cost reduction” but not “service quality,” managers can cut maintenance and support until problems surface later.

- Information asymmetry: Owners cannot perfectly observe effort, risk-taking, or internal tradeoffs. Managers can present a selective picture, intentionally or not.

- Time horizon gaps: Owners may care about durable value; managers may care about near-term performance reviews. A manager who expects to be evaluated this year may underinvest in systems that pay off later.

- Risk shifting: If downside is limited for managers but upside is shared, managers may take risks that owners would avoid. For instance, if compensation is capped while losses reduce equity value, the manager’s personal downside is smaller than the owners’.

Mapping the Agency Problem to Decision Types

Not all decisions create the same agency risk. The risk is highest where outcomes are hard to observe and where managers have discretion.

- Investment decisions: Capital allocation, hiring, and product bets. These involve uncertainty and long payback periods.

- Operating decisions: Pricing, procurement, and staffing levels. These can be influenced by short-term targets.

- Financing decisions: Debt versus equity, refinancing timing, and covenant management. These affect risk distribution.

- Governance-facing decisions: Reporting quality, disclosure timing, and how performance is framed to the board.

A practical way to think about it: the more a decision depends on internal effort and judgment, the more agency risk matters.

Mind Map: Agency Risks and Misalignment

Mechanisms That Reduce Misalignment

Owners can’t eliminate agency risk, but they can reduce it by improving measurement, oversight, and alignment.

-

Better performance measurement

- Use a balanced scorecard that includes leading and lagging indicators.

- Example: pair revenue targets with retention or customer satisfaction metrics so discounting alone cannot carry the score.

-

Incentives that match time horizons

- Use vesting schedules and performance periods that extend beyond a single quarter.

- Example: if executives receive equity that vests over three years, they have a reason to avoid short-term actions that damage future value.

-

Board oversight with decision-specific questions

- The board should ask about assumptions, not just results.

- Example: when approving a hiring plan, require a simple model showing expected utilization and payback, plus what would trigger a pause.

-

Information rights that support verification

- Owners need timely, comparable reporting.

- Example: require monthly KPI packs with consistent definitions so “improved performance” can be checked rather than accepted.

-

Clear decision rights and escalation paths

- If managers can act freely on high-impact matters, agency risk rises.

- Example: reserve board approval for related-party transactions and major capital expenditures above a threshold.

Case Example: How Misalignment Plays Out

Imagine a company where managers are rewarded for EBITDA growth, and owners care about sustainable cash generation.

- Managers cut discretionary spend to raise EBITDA.

- They also delay vendor payments to preserve cash, which boosts near-term EBITDA but strains supplier relationships.

- Later, procurement costs increase and delivery reliability drops, hurting sales.

The fix is not “trust managers less.” It’s to align the measurement system with the outcome owners actually want: include cash conversion or supplier reliability indicators, and require board review for large discretionary cuts.

Practical Diagnostic Checklist

When you suspect misalignment, look for these signals:

- Metrics that can be improved without improving underlying economics.

- Decisions with long payback periods being judged on short-term results.

- Reporting that changes definitions or emphasizes favorable comparisons.

- Compensation that rewards upside while limiting personal exposure to downside.

- High-discretion areas where the board rarely asks for the assumptions behind the numbers.

Agency risk is a design problem: if owners define goals, measurement, and oversight well, managers can still run the company day to day without drifting away from owner value.

1.5 Scope of Equity Design Across Corporate Forms and Jurisdictions

Equity structure design is not one-size-fits-all because the legal “plumbing” differs by corporate form and jurisdiction. The same economic intent—say, protecting investors while keeping founders in control—can require different instruments, approval routes, and drafting language depending on whether the company is a Delaware corporation, a UK private company, or an LLC-like entity elsewhere.

Start with the Corporate Form First

Corporate form determines what equity can legally look like and how it can be governed.

- Corporations typically issue shares with defined classes. Voting rights, dividends, and liquidation outcomes are usually tied to share classes, and many governance actions require board and shareholder approvals.

- Partnership-style entities (including LLCs) often allow more contractual flexibility. Instead of “classes of stock,” you may see membership interests, profit allocations, and voting rights set through an operating agreement.

- Statutory hybrids in some jurisdictions can blend features, but still impose mandatory rules for certain matters like capital maintenance, distributions, and director duties.

A practical example: if you want investors to have a say over major financings, a corporation might implement this through preferred stock protective provisions plus class votes. An LLC might implement it through consent rights in the operating agreement tied to specific member actions.

Then Map Jurisdictional Constraints

Jurisdictions impose constraints that affect both drafting and enforceability.

- Mandatory corporate law can limit what you can contract around. For instance, some jurisdictions restrict the ability to create non-voting equity or to waive certain shareholder protections.

- Capital and distribution rules affect economic terms. Liquidation preferences and dividend mechanics must align with solvency tests and capital maintenance concepts.

- Fiduciary duties and governance formalities influence how board control and information rights are structured. Even if documents say one thing, courts may scrutinize governance practices.

- Tax classification rules can change the real-world effect of “economic rights.” A term that looks neutral legally might create unintended tax consequences.

A concrete example: a structure that relies on cumulative dividends may be treated differently across jurisdictions depending on whether dividends are legally “distributions” subject to solvency limits.

Identify the Design Surface Area

Equity design spans multiple layers, and each layer has different legal “failure modes.”

- Instrument layer: what is issued (shares, preferred, options, warrants, membership interests).

- Governance layer: who votes, who appoints, what requires class consent.

- Economic layer: how money flows on dividends, sale, or liquidation.

- Transfer layer: what happens when ownership changes hands.

- Process layer: how approvals are documented and recorded.

If you design only the instrument layer, you can still end up with governance gaps. For example, you might create a preferred class with protective provisions, but fail to ensure the charter/bylaws amendment process matches the class vote requirements.

Mind Map: Equity Design Scope Across Forms and Jurisdictions

Integrated Example: Same Goal, Different Implementation

Assume the goal is: “Investors get downside protection, founders keep day-to-day control, and major actions require investor consent.”

- In a corporation, you might use preferred shares with liquidation preference and protective provisions requiring investor class approval for actions like issuing senior securities, changing board composition, or approving a sale.

- In an LLC, you might use preferred-like economic rights through membership interest allocations and redemption features, while investor consent is handled through member voting thresholds for specified actions.

The key difference is not the intent; it’s the legal mechanism. In one form, the mechanism is share-class voting and charter amendments. In the other, it’s contractual consent and operating agreement provisions.

Practical Checklist for Scope Decisions

Before drafting term sheets, confirm these items in order:

- What corporate form is being used and what documents govern equity rights.

- Which jurisdiction’s mandatory rules apply to issuance, distributions, and voting.

- Which design layers must be aligned for your specific deal terms.

- What approval pathways are required for each reserved matter and amendment.

- How the economic terms interact with legal distribution limits.

When these checks are done, the rest of the equity design work becomes more precise. You are no longer guessing whether a term is “allowed” or whether it will be enforceable in the real governance process. You can then draft with fewer surprises and clearer accountability.

2. Mapping Stakeholders and Defining Control Objectives

2.1 Stakeholder Inventory and Role Clarification

A good equity structure starts with a simple question: who can influence outcomes, and how? Stakeholders are not just people with money; they are decision-makers, information receivers, and constraint enforcers. This section builds a practical inventory method and turns it into clear role definitions you can carry into governance documents.

Stakeholder Inventory: What You Are Actually Listing

Create an inventory that separates stakeholders by function rather than by title. A founder, for example, may be both an owner and an operator, which means they can affect both voting outcomes and day-to-day decisions.

Use five buckets:

- Equity holders: common, preferred, option holders, and any warrants.

- Governance actors: board members, board committees, and any designated observers.

- Management: CEO, CFO, and other executives who propose actions and manage execution.

- Contract counterparties: lenders, landlords, strategic partners, and counterparties with consent rights.

- Control constraints: regulators, auditors, and internal compliance functions that limit what can be approved.

For each bucket, record three fields: power, interest, and inputs. Power is the ability to block or approve. Interest is the reason they care. Inputs are what they provide—capital, expertise, approvals, or information.

Role Clarification: Turning Inventory Into Decision Logic

Once you list stakeholders, translate them into roles that map to governance mechanics.

Define these roles explicitly:

- Decision owner: the party whose approval is required for an action to proceed.

- Proposal owner: the party that drafts or initiates the action.

- Consulted party: the party whose input is required or expected before a decision.

- Informed party: the party that receives updates but does not approve.

- Constraint enforcer: the party whose rights limit the decision owner.

A common mistake is mixing roles. For instance, an investor may be “informed” through monthly reporting but also hold protective provisions that make them a “constraint enforcer” for certain reserved matters. Your documents should reflect that difference.

Mind Map: Stakeholder Inventory to Governance Roles

Practical Example: Two Stakeholders, Different Roles

Consider a Series A investor and the CFO.

-

Series A investor

- Power: can approve reserved matters through class votes.

- Interest: protect downside and preserve control over major actions.

- Inputs: capital and governance oversight.

- Role mapping: constraint enforcer for specific actions; informed party for routine operations.

-

CFO

- Power: may not have voting power, but can influence outcomes through budgets and reporting.

- Interest: ensure financial controls and accurate disclosures.

- Inputs: forecasts, compliance reporting, and financial models.

- Role mapping: proposal owner for budgets and financial policies; consulted party for certain board decisions.

This separation prevents a frequent governance failure: treating investor rights as if they apply to everything, or treating management proposals as if they automatically become decisions.

Practical Example: Consent Rights That Change the Role

Suppose a lender agreement requires consent before the company issues additional debt. Even if the board would normally approve financing, the lender becomes a constraint enforcer for that specific action.

Your inventory should therefore include contract counterparties not as generic “stakeholders,” but as targeted rights holders tied to specific decision categories. When you later draft reserved matters, you can avoid duplicating rights and instead reference the correct decision pathway.

Inventory Output: A Role-Ready Checklist

To make this section usable, convert the inventory into a checklist you can reuse during drafting:

- For each stakeholder, list power, interest, and inputs.

- Assign one primary role for each governance layer: board decisions, management proposals, and document-level constraints.

- Identify where roles overlap and document the overlap explicitly.

- Mark actions that require class votes, board approval, management initiation, or third-party consent.

When the inventory is role-ready, the next step is straightforward: you can map these roles to voting rights, board appointment mechanics, and reserved matters without guessing who actually controls what.

2.2 Control Objectives for Founders Investors and Strategic Partners

Control objectives are the “why” behind governance design. They answer what each party is trying to protect, what decisions they must influence, and what tradeoffs they can tolerate. Founders typically optimize for speed and continuity; investors optimize for downside protection and accountability; strategic partners optimize for operational alignment and IP or commercial safeguards.

Control Objectives as Decision Filters

A useful way to structure objectives is to treat them as filters applied to a decision list. Start with three questions for each party: (1) What could go wrong if this decision is made poorly? (2) Who has the information needed to judge it? (3) How reversible is the decision if it turns out wrong?

Reversibility matters. Approving a new share class is hard to undo; approving a quarterly budget is easier to correct. That difference drives whether control should be exercised through voting rights, board oversight, or information rights.

Founders Control Objectives

Founders usually want control that preserves execution quality while preventing governance from becoming a bottleneck.

- Preserve decision speed for ordinary-course matters. Founders prefer that routine operating decisions sit with management and the board, without requiring investor-level consents.

Example: A founder-led company budgets marketing spend within an approved annual plan. The control objective is that management can reallocate within the plan without triggering a new approval cycle.

- Maintain continuity of strategy and leadership. Founders often seek stability around CEO appointment, removal, and succession planning.

Example: If a founder is also CEO, the objective is to avoid sudden leadership changes driven by short-term disagreement, while still allowing removal for defined cause.

- Protect against value leakage through capital structure changes. Founders may accept investor protections, but they want clear boundaries so financing terms cannot be used to force repeated renegotiations.

Example: Reserved matters define that any issuance of senior securities requires class approval, but ordinary equity grants under an approved plan do not.

Investor Control Objectives

Investors typically focus on preventing irreversible downside and ensuring accountability.

- Limit dilution and preserve economic expectations. Investors care about how new equity affects ownership and liquidation outcomes.

Example: A venture investor’s objective is that option pool expansions and new issuances follow a defined framework, so dilution is modeled and not handled ad hoc.

- Ensure governance accountability through board-level oversight. Investors often want board rights that translate into real monitoring: budgets, major contracts, and performance reporting.

Example: Board approval is required for entering contracts above a threshold, because those contracts can shift risk and cash flow materially.

- Control major structural events. Investors usually prioritize reserved matters for actions that change the company’s fundamental risk profile.

Example: Mergers, asset sales, and changes to liquidation preferences require supermajority or cross-class consent.

- Reduce information asymmetry. Investors use information rights to make voting meaningful.

Example: Monthly financials and quarterly KPI reporting are tied to specific decision points, like approving a new financing or revising the budget.

Strategic Partner Control Objectives

Strategic partners often care less about pure financial upside and more about operational alignment and protection of their contributions.

- Protect IP, data, and confidentiality. Strategic partners want governance hooks that prevent misuse or uncontrolled disclosure.

Example: Any transfer of core technology rights or changes to licensing terms require board approval.

- Ensure commercial commitments are honored. They may seek control over pricing, exclusivity, or termination rights in key agreements.

Example: A strategic partner’s objective is that the company cannot terminate a supply agreement without board review, because termination could harm both sides.

- Align decision-making on product roadmap and integration. Strategic partners may request input rights on decisions that affect integration scope.

Example: A board committee reviews integration milestones and approves changes that materially alter service levels.

Control Objectives Mind Map

Mind Map: Control Objectives by Party and Decision Type

Turning Objectives Into Governance Requirements

Once objectives are clear, convert them into three governance outputs: decision rights, thresholds, and documentation.

- Decision rights: Who decides—management, board, investor class, or specific board committee.

- Thresholds: What level of approval—simple majority, supermajority, or cross-class vote.

- Documentation: What must be produced—budgets, reports, valuation support, or contract terms.

Example: If the investor objective is accountability, the governance requirement might be board approval for annual budget and quarterly variance review, supported by a standard reporting pack.

Practical Example: A Control Objective to Clause Mapping

Example scenario: A company plans to issue new shares to fund a product expansion.

- Founder objective: keep financing execution efficient.

- Investor objective: prevent unexpected dilution and ensure terms are fair.

- Strategic partner objective: ensure the expansion does not compromise IP licensing obligations.

Integrated design: management proposes the financing; the board approves within a pre-agreed issuance framework; investor class consent is required only if the issuance crosses defined seniority or pricing thresholds; any change that affects the IP license terms is a reserved matter requiring board approval with the relevant committee review.

This approach keeps control where it matters, avoids blanket vetoes, and makes each party’s objective measurable in the governance process.

2.3 Decision Rights Framework for Board Management and Owners

A decision rights framework answers one practical question: who gets to decide, and what happens if the decision is wrong or delayed? In equity design, the board and owners share responsibility, but they should not share confusion. The goal is to map decisions to governance roles so that ownership control is real, not just ceremonial.

Foundational Concepts That Make Decisions Work

Start with three building blocks.

- Decision type

- Strategy: where to compete, what to build, and which risks to accept.

- Capital: raising money, issuing equity, changing the cap table.

- Operations: budgets, major contracts, hiring executives.

- Governance: amendments, reserved matters, committee structure.

- Decision authority

- Board approval means the board is accountable.

- Owner approval means owners vote as a class or as a whole.

- Management authority means executives decide within defined limits.

- Decision process

- Proposal: who brings the item forward.

- Review: who analyzes and challenges.

- Approval: what vote threshold applies.

- Implementation: who executes and reports back.

A useful rule of thumb: the more irreversible the decision, the more formal the approval path.

A Practical Rights Map from Owners to Management

Think of decision rights as a ladder.

- Owners set boundaries through charter-level reserved matters and class votes.

- Board translates boundaries into company-level decisions and oversight.

- Management runs the business within board-approved policies.

To keep this ladder from wobbling, define three categories of items.

- Reserved matters for owners

These are actions that change the economic or control bargain. Examples include creating new share classes with different voting rights, approving a merger that changes consideration, or amending investor protective provisions.

- Reserved matters for the board

These are actions that materially affect risk, capital structure, or long-term direction but do not require owner votes. Examples include approving annual budgets, entering credit facilities above a threshold, or adopting equity incentive plan terms.

- Management decisions within limits

These are operational choices that management can make without repeated approvals. Examples include routine hiring below an executive level, signing contracts within a dollar cap, or adjusting pricing within approved ranges.

Vote Thresholds and Decision Hygiene

A threshold is not just a number; it is a control signal. Use consistent patterns so people can predict outcomes.

- Simple majority for ordinary board actions.

- Supermajority for sensitive board actions like issuing equity outside a plan.

- Class vote or cross-class vote when the action affects a specific class’s rights.

Decision hygiene prevents “silent vetoes.” Require written materials, define quorum rules, and specify when abstentions count. If a board member has a conflict, state the process for recusal and how the remaining vote is counted.

Mind Map: Decision Rights Framework

Example: Mapping Rights for a Typical Financing

Assume a company issues preferred shares to new investors.

- Owners approve charter amendments that create the new preferred class and its voting protections.

- Board approves the financing terms, subject to board reserved matters thresholds.

- Management prepares the offering documents and runs the process, but cannot change key economics like liquidation preference without board approval.

If the financing also includes an option pool increase, the framework should specify whether that increase is a board reserved matter or an owner reserved matter. The clean approach is: if the increase meaningfully dilutes existing holders beyond a defined band, require owner approval.

Example: Handling a Major Acquisition

For a proposed acquisition:

- Management evaluates targets, negotiates terms, and drafts the deal memo.

- Board approves entering the definitive agreement and sets conditions for closing.

- Owners vote only if the transaction triggers reserved matters, such as a change of control that affects protective provisions or requires class consent.

To avoid delays, define a timeline: when management must deliver materials, when the board committee reviews, and when the vote must occur.

Example: Preventing Control Drift in Ordinary Operations

Suppose management wants to sign a long-term customer contract.

- If the contract is within the board-approved dollar cap and does not create unusual risk, management decides.

- If it exceeds the cap or includes terms that could materially affect leverage or covenants, it becomes a board reserved matter.

This is how the framework balances control with speed: owners and the board focus on decisions that change the company’s risk and ownership bargain, while management handles the rest with clear boundaries.

2.4 Constraints from Existing Agreements and Corporate Charters

When you design equity and control, you’re not starting on a blank whiteboard. Existing charters, bylaws, investor rights agreements, option plan documents, and side letters already define what can be done, who must approve it, and what wording must be used. Treat these constraints like the rules of the road: they don’t change because you prefer a different route.

Step 1: Inventory the Documents That Bind the Company

Start with a document map, not a negotiation map. Create a list of every instrument that can affect governance or economics, then tag each one by its “binding force.”

- Corporate charter and bylaws: set baseline governance, board structure, and amendment mechanics.

- Investor rights agreements: often add consent rights, information rights, and class vote requirements.

- Voting agreements and ROFR/Co-sale agreements: control transfers and sometimes voting behavior.

- Equity plan and option agreements: govern option pool approvals, vesting, and award issuance.

- Prior financing documents: can include protective provisions, anti-dilution terms, and conversion mechanics.

Example: A company plans to issue a new class of preferred stock with different voting rights. The charter may allow preferred stock issuance, but the investor rights agreement may require each affected class to approve any “materially adverse” change. If you skip the inventory step, you may draft a term sheet that cannot be implemented.

Step 2: Identify the “Decision Gate” for Each Action

Not every action needs the same approvals. Constraints usually show up as decision gates: board approval, stockholder approval, class vote, or specific investor consent.

Create a simple action-to-approval table in your head:

- Board-level actions: budgets, hiring executives, approving equity grants within plan limits.

- Stockholder-level actions: charter amendments, mergers, major asset sales.

- Class vote actions: changes that affect rights of a specific class of stock.

- Contract consent actions: actions that trigger investor rights under side agreements.

Example: Issuing additional shares might be board-approved under the charter, but if the issuance triggers anti-dilution adjustments or changes the relative economics of an existing preferred class, class vote or investor consent may be required.

Step 3: Translate Constraints Into Drafting Requirements

Constraints aren’t just approval thresholds; they also dictate how terms must be written.

Common drafting constraints include:

- Defined terms: “Change of Control,” “Major Transaction,” “Qualified Financing,” and “Original Issue Date” often appear in multiple documents. If definitions differ, you get inconsistent triggers.

- Amendment hierarchy: some agreements require charter amendments for certain changes, while others can be amended by contract consent.

- Notice and recordkeeping: meeting notices, written consent procedures, and timing requirements can invalidate actions.

Example: A protective provision might say a class vote is required for “any amendment that adversely affects the liquidation preference.” If your new financing changes the cap table in a way that indirectly affects liquidation outcomes, you need to decide whether the change is “adverse” under the existing definition and how to document that analysis.

Step 4: Check for Hidden Interactions Between Documents

Constraints often collide in ways that are easy to miss.

- Equity plan vs. financing: option pool increases may require board approval, but investor rights may require consent if the pool is “material” or if it affects anti-dilution calculations.

- Transfer restrictions vs. new issuance: ROFR and co-sale rights can apply to transfers by founders, which affects who can actually hold the new securities.

- Conversion mechanics vs. voting outcomes: conversion ratios can change voting power, which can indirectly affect reserved matters.

Example: A company wants to add a founder-friendly voting structure. If existing preferred stock has conversion terms that increase common voting power upon conversion, the “reserved matters” thresholds might be met or missed depending on conversion timing.

Mind Map: Constraints Workflow and Where They Show Up

Step 5: Produce an Approval Matrix and a Constraint List

Before negotiating new terms, convert constraints into two practical artifacts.

- Approval matrix: each planned action mapped to required approvals (board, stockholder, class vote, investor consent) and the relevant document section.

- Constraint list: the exact phrases and thresholds that cannot be changed without specific approvals.

Example: If the charter requires a supermajority for charter amendments, and the investor rights agreement requires class consent for changes to protective provisions, your matrix will show that a “simple” charter amendment is not simple. It becomes a coordinated process: draft language, confirm class vote mechanics, and align notice timing.

Step 6: Use Clear “What Changes What” Language in Negotiations

When you propose new equity terms, explicitly state which existing rights are being preserved, modified, or replaced. This reduces the chance that counterparties interpret your proposal as a broader change than intended.

Example: Instead of saying “we’ll update protective provisions,” specify: “We are adding a new reserved matter category, but we are not changing the approval thresholds for existing categories.” That sentence forces the conversation into concrete territory and makes it easier to confirm compliance with the existing amendment rules.

2.5 Document Checklist for Governance and Equity Instruments

A good equity structure is only as reliable as the documents that implement it. This checklist moves from the “who decides” basics to the “what happens if” details, so you can trace every control right to a specific clause and every economic term to a specific instrument.

Governance Core Documents

Start with the documents that define the company’s decision-making machinery.

- Charter or Articles of Incorporation: Confirm the authorized share classes, any class votes, and any special rights that must live at the charter level.

- Bylaws: Verify board meeting rules, officer roles, notice and quorum mechanics, and how amendments are handled.

- Stockholders Agreement: Check voting agreements, transfer restrictions, and any drag or tag mechanics that bind stockholders.

- Board Consent and Minutes Template: Ensure you have a consistent recordkeeping approach for approvals that require board action.

Example: If preferred stock requires class approval for a financing, the charter should state the class vote threshold, while the stockholders agreement should not silently override it.

Equity Instrument Set

Next, inventory the documents that create and govern the equity itself.

- Stock Purchase Agreements: Tie each investor’s purchase to the exact class, number of shares, and representations.

- Preferred Stock Terms or Certificate of Designation: Confirm voting, dividends, liquidation, conversion, and protective provisions are fully specified.

- Investor Rights Agreement: Validate information rights, registration rights if applicable, and any consent rights.

- Voting Agreement or Irrevocable Proxy: If used, confirm scope, duration, and revocation mechanics.

- Option Plan and Option Grant Documents: Ensure the plan authorizes the pool, and grants match the plan terms.

Example: If an option plan says vesting is four years with a one-year cliff, but a grant letter says otherwise, you will eventually litigate the mismatch.

Decision Rights and Reserved Matters

Document the “reserved matters” so they are enforceable and operational.

- Reserved Matters Schedule: List each action requiring investor or class approval, such as issuing new senior securities, changing board size, or altering dividend terms.

- Approval Threshold Matrix: Specify whether approvals are by majority of the board, majority of the class, supermajority, or cross-class vote.

- Information Rights Trigger List: Identify what information must be delivered and when, including financial statements and budget approvals.

Example: A reserved matter clause that says “material transactions” without a definition is like a seatbelt labeled “important.” Add objective thresholds.

Transfer, Liquidity, and Control Boundaries

Transfer restrictions should be consistent across every document that touches ownership.

- ROFR and Co-Sale Clauses: Confirm notice procedures, timing, and how price and terms are matched.

- Drag-Along Rights: Verify who can trigger, what vote is required, and what protections apply to minority holders.

- Permitted Transfers: List affiliates, estate planning, and internal reorganizations with conditions.

- Change of Control Definition: Ensure it matches the company’s governance intent and any investor consent rights.

Example: If “change of control” includes asset sales in one document but not another, you can end up with investors who are bound to a drag but not to the consent that should have preceded it.

Amendment and Consent Management

Finally, make sure you can actually run the governance process without chaos.

- Amendment Hierarchy: Confirm which rights live in charter vs bylaws vs investor agreements, and which require class vote.

- Consent Mechanics: Specify notice, response periods, quorum, and whether consents can be delivered electronically.

- Waiver Rules: Confirm whether waivers require the same threshold as approvals.

- Document Version Control: Maintain a single “current” set of executed documents and a change log.

Example: If an amendment requires preferred class approval, but the company’s internal checklist treats it as a board matter, you have a governance failure waiting for a signature.

Mind Map: the Checklist

Practical Execution Checklist

Use this short run-through before closing a financing or issuing new equity.

- Confirm each investor right has a home document and a clause reference.

- Verify every reserved matter appears in the correct agreement and matches the voting thresholds.

- Cross-check transfer restrictions across charter, stockholders agreement, and investor rights.

- Ensure option plan terms and grant letters match exactly.

- Record the executed versions and update the cap table assumptions used for governance decisions.

Example: If you update conversion mechanics in a certificate of designation, also confirm any investor agreement provisions that reference conversion outcomes still align with the new terms.

3. Core Equity Instruments and Their Governance Effects

3.1 Common Stock Preferred Stock and Hybrid Securities

Equity instruments are not just “ownership.” They are bundles of rights that determine who gets paid first, who votes on which matters, and how control can shift when things get expensive—financially or legally. This section builds a clean mental model: start with common stock, add preferred stock, then connect both to hybrid securities that mix features.

Common Stock as the Baseline Ownership Unit

Common stock is the default equity class in most corporations. It typically carries:

- Residual economics: common shareholders receive what remains after creditors and preferred holders are paid.

- Voting rights: common votes elect directors and approve major corporate actions, subject to charter and statutory rules.

- Participation in upside: if the company grows, common holders generally benefit through price appreciation and dividends if declared.

A simple example: Company A has $10 million in assets and $6 million in debt. If the company is sold for $10 million, creditors get $6 million. If there is no preferred stock, the remaining $4 million is distributed to common shareholders based on their ownership percentages.

Common stock is also the “control anchor.” If a company has multiple classes, common often becomes the reference point for voting thresholds, board elections, and consent mechanics.

Preferred Stock as the Payment Priority Tool

Preferred stock is designed to change the order and terms of economic outcomes. It commonly includes:

- Liquidation preference: preferred holders are paid before common on a sale or liquidation.

- Dividend rights: dividends may be cumulative or non-cumulative, and may be fixed or adjustable.

- Limited voting: preferred may vote only on specific matters, often called protective provisions.

Example: Company B issues preferred stock with a 1x liquidation preference. In a sale, proceeds after debt are $50 million. Preferred is $20 million. Preferred holders receive $20 million first, and the remaining $30 million goes to common.

If dividends are cumulative, unpaid dividends can accumulate and must be satisfied before common receives anything in a liquidation scenario. If dividends are non-cumulative, missed dividends generally do not create a liquidation claim.

Preferred stock can also include conversion rights. Conversion turns preferred into common on a specified basis, which matters for control because converted shares may carry full voting rights.

Hybrid Securities as the Rights Mixer

Hybrid securities combine features of equity and debt-like instruments. They exist to solve a specific negotiation problem: investors want downside protection or priority, while founders want flexibility and less immediate dilution.

Common hybrid patterns include:

- Convertible preferred: preferred with conversion into common, often at the investor’s option.

- Redeemable preferred: company can be required or permitted to redeem shares after a period, which can affect long-term ownership stability.

- Preferred with participation: preferred holders may receive their preference plus an additional share of remaining proceeds.

Example: Company C issues convertible preferred with a 1x preference and a conversion ratio that effectively prices the preferred at a negotiated valuation. If the company later raises a new round at a higher valuation, conversion may be attractive because preferred holders can participate in greater upside. If the company sells at a lower valuation, the liquidation preference still provides a floor.

Control Implications You Can Actually Track

Economic priority and voting control do not always move together. A company can grant preferred holders strong economic rights while limiting their voting, or it can give them voting rights only when certain reserved matters occur.

To design control that stays stable, you typically map three layers:

- Economics: who gets paid first and how dividends work.

- Voting: who votes for directors and on reserved matters.

- Conversion and transfer mechanics: how shares change class status and who can hold them.

A practical example: If preferred holders have limited voting but strong liquidation preferences, they may not control day-to-day decisions. However, they can still influence outcomes through protective provisions tied to major actions like issuing senior securities, changing charter terms, or approving mergers.

Mind Map: Rights and Outcomes Across Equity Classes

Example: Three Outcomes from One Cap Table Snapshot

Assume Company D has:

- $60 million sale proceeds after debt

- $20 million preferred with 1x liquidation preference

- $40 million common

Outcome A: No participation and no conversion

- Preferred gets $20 million

- Common gets $40 million

Outcome B: Participation where preferred also shares remaining proceeds

- Preferred gets $20 million first

- Remaining $40 million is split per participation formula (for example, preferred receives an additional 20% of remaining proceeds, common receives the rest)

Outcome C: Conversion into common before sale

- Preferred converts to common based on the conversion ratio

- Total proceeds are distributed across the enlarged common base, changing who receives the residual

These three outcomes show why “common vs preferred” is not a label game. The charter terms decide the math, and the math decides who has leverage.

Practical Drafting Checklist for This Section

When you review or draft terms, confirm that the documents align on:

- Liquidation preference type: 1x vs multiple, and whether it is participating.

- Dividend structure: cumulative vs non-cumulative and payment priority.

- Voting scope: what preferred votes on, and what it does not.

- Conversion mechanics: triggers, ratios, and whether conversion is automatic or optional.

- Interaction with reserved matters: whether protective provisions cover charter amendments that change economics or voting.

If these items are consistent, the equity structure becomes predictable. If they conflict, control can shift in ways that neither side expected—usually at the worst possible moment.

3.2 Voting Rights Classes and Protective Provisions

Voting rights classes translate ownership into decision power, while protective provisions define which decisions require extra consent. Together, they prevent “majority rule” from becoming “majority takeover,” and they prevent minority holders from being ignored when decisions affect the economic deal.

Voting Rights Classes: The Basics That Matter

A voting rights class is a set of shares with a defined voting behavior. The most common levers are (1) who gets votes, (2) how many votes each share gets, and (3) which matters those votes cover.

Start with the simplest model: one share, one vote, for ordinary matters. This is easy to administer and easy for everyone to understand. The moment you introduce multiple classes, you should also introduce a clear map of which matters are ordinary and which are reserved.

Common Voting Structures

Single class with protective provisions. All shares vote equally for director elections and shareholder votes, but certain actions require a separate class vote or a supermajority. This keeps control straightforward while still protecting key rights.

Dual class with different voting power. Founder shares may carry higher votes per share than investor shares. This can preserve long-term strategy, but it must be paired with reserved matters so that high-vote holders cannot change the rules that govern investor economics.

Preferred shares with class votes. Preferred stock often votes as a class on matters that affect liquidation preference, conversion, or seniority. This is the cleanest way to ensure the preferred holders’ core economics are not altered without their consent.

Protective Provisions: What They Actually Do

Protective provisions are contractual and charter-based constraints. They typically require one or more of the following: a supermajority of the affected class, a separate class vote, or consent of a specified investor group.

A useful way to think about protective provisions is: they define “no surprises” boundaries. If a decision changes the risk profile or the economic bargain, it should trigger heightened approval.

Reserved Matters Categories

Protective provisions usually cluster into a few categories. Each category should be drafted with precision so the company can operate without constant consent requests.

- Capital structure changes. Issuing senior securities, creating new classes with priority, or changing the number of authorized shares.

- Economic term changes. Altering liquidation preference, dividend rights, conversion ratios, or participation features.

- Control and governance changes. Changing board size, removing directors appointed under rights agreements, or amending voting rights.

- Fundamental transactions. Mergers, asset sales, or dissolutions that would change the company’s form or the value of the security.

- Transfer and enforcement mechanics. Waiving rights, changing transfer restrictions, or modifying consent requirements.

Thresholds and Drafting Precision

Common thresholds include: (a) majority of the outstanding shares of the affected class, (b) two-thirds or three-quarters supermajority, or (c) a separate class vote plus an overall shareholder vote. The key is consistency: if a matter is “reserved,” the approval path should be unambiguous.

Ambiguity often comes from vague terms like “materially adversely affects.” A better approach is to list the specific rights that cannot be changed without consent, and to define what counts as an adverse change.

Mind Map: Voting Classes and Protective Provisions

Integrated Example: How the Pieces Work Together

Assume a company issues Preferred A and Common. Preferred A has class voting rights and protective provisions.

- Ordinary decision: approve an annual budget. Common and Preferred vote together as a single class for this matter.

- Reserved decision: issue new preferred stock that ranks senior to Preferred A. This triggers a Preferred A class vote requiring approval of a supermajority of Preferred A outstanding.

- Reserved decision: amend the charter to change conversion ratios for Preferred A. This also triggers a Preferred A class vote.

Now add a twist: the company also has a dual-class structure where founder common has higher votes per share. Without reserved matters, the high-vote founder could pass governance changes that indirectly alter investor economics. With reserved matters, the founder’s voting strength cannot override changes that affect Preferred A’s liquidation preference, conversion mechanics, or seniority.

Practical Example: Drafting a Protective Provision Without Overreach

A common failure mode is drafting reserved matters so broadly that routine operations require consent. Instead, tie the reserved matter to specific outcomes.

Example approach for capital structure: reserve “issuance of securities senior to Preferred A” rather than “any financing.” That allows the company to raise money through junior instruments without triggering class consent, while still preventing the seniority bargain from being diluted.

Case Study: Board Elections Versus Board Composition Changes

Consider two related but distinct actions.

- Board election. If preferred holders have voting rights for director elections, the charter should specify whether they vote with common or separately.

- Board composition change. If the company wants to change board size or remove a director appointed under investor rights, that should be a reserved matter requiring the affected class vote or investor consent.

This separation matters because elections are about choosing representatives, while composition changes can restructure control permanently. Treating them differently keeps governance workable and protections meaningful.

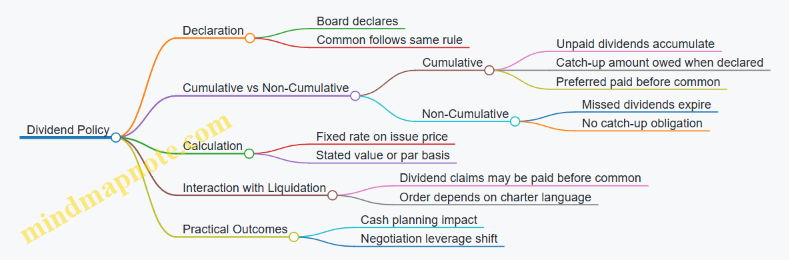

3.3 Dividend Rights Liquidation Preferences And Participation

Dividend rights and liquidation preferences answer two different questions: who gets paid first when cash is available, and who gets paid first when the company is sold or otherwise exits. Participation determines whether preferred holders stop after their preference or keep sharing alongside common. Together, these terms shape both control incentives and economic outcomes.

Dividend Rights: When Cash Flows Before Exit

Dividend rights can be cumulative or non-cumulative. With non-cumulative dividends, if the company skips a dividend in a given year, preferred holders generally cannot claim the missed amount later. With cumulative dividends, unpaid dividends accrue and must be paid before common receives anything. A simple example: a preferred series has a 6% cumulative dividend on a $10 million original issue price. If the company declares no dividends for two years and later pays $1.2 million, the preferred holders typically receive $1.2 million first (6% of $10 million per year), and only then does common participate in any remaining distribution.

Dividend payment mechanics also matter. Some deals require dividends only when declared by the board, which means governance and board composition indirectly affect dividend outcomes. Others include a “mandatory” dividend trigger tied to specific events or financial thresholds. Even when dividends are “optional,” the presence of cumulative dividends can create pressure to manage cash carefully, because the preference balance grows while common waits.

Liquidation Preferences: Who Gets Paid First on Exit

Liquidation preference is usually expressed as a multiple of the original issue price. A 1x non-participating preference means preferred holders receive the greater of their preference amount or the amount they would receive if they converted to common, but they do not share further. A 2x preference means they receive twice the original issue price before common gets anything, subject to the deal’s participation and conversion rules.

Consider an exit of $50 million with $20 million of preferred at 1x. If the preferred is non-participating, preferred holders receive $20 million first, leaving $30 million for common. If the preferred is participating, the preferred may receive $20 million first and then also share in the remaining $30 million with common, often on an as-converted basis. Participation is where economics can shift dramatically.

Participation: Stop After Preference or Share Again

Participation comes in two common flavors: participating and non-participating. Non-participating preferred holders typically choose between taking the preference or converting to common, whichever yields more. Participating preferred holders often take the preference and then share the rest, sometimes with a cap.

A capped participating structure limits how much the preferred can receive in total. Example: preferred has a 1x participating preference with a 2x cap. If the company exits for a very large amount, preferred holders receive their 1x preference and then participate until their total payout reaches 2x of original issue price. After the cap is reached, remaining proceeds go to common. This prevents the preferred from effectively absorbing most upside while still preserving a downside floor.

A practical way to see the difference: suppose preferred original issue price is $10 million, common ownership is 50% on an as-converted basis, and exit proceeds are $30 million.

- Non-participating: preferred receives $10 million, common receives $20 million.

- Participating uncapped: preferred receives $10 million, then shares the remaining $20 million with common. If preferred and common split the remaining $20 million 50/50 on an as-converted basis, preferred receives another $10 million, totaling $20 million.

That second $10 million is the “participation” effect. It can be fair when the preferred is meant to behave partly like equity, but it can also reduce common’s incentive to support growth if the preferred’s upside is too strong.

Conversion Interactions: The Choice That Changes Everything

Many preferred series include an automatic conversion right or mandatory conversion at certain thresholds. Conversion is often evaluated by comparing the preference payout to the as-converted common payout. For non-participating preferred, this comparison is the core economic decision. For participating preferred, conversion may be less relevant if participation already grants sharing, but conversion can still matter for voting and for how future rounds treat the series.

A clean example: if the exit is high enough that converting yields more than taking the preference, non-participating preferred will convert. If the exit is modest, the preference dominates and conversion is not chosen. This is why liquidation preference and participation must be read together with conversion triggers and any caps.

Mind Map: Dividend Rights Liquidation Preferences and Participation

Example: Putting It Together in One Exit Scenario

Assume Series A preferred has a 1x non-participating preference, and Series B preferred has a 1x participating preference with a 2x cap. Total preferred original issue price across both series is $30 million. The company exits for $60 million.

- Series A non-participating receives $15 million (1x on its share) and does not share further.

- Series B participating receives its $15 million preference first, then shares the remaining proceeds with common until it reaches its 2x cap. If the cap is reached, any additional proceeds go to common rather than continuing to feed the preferred.

This structure creates a clear hierarchy: both series get a floor, but only the participating series can share, and only up to a defined limit. That limit is often the difference between “preferred as a risk-mitigating instrument” and “preferred as a second common,” so it deserves careful attention during drafting.

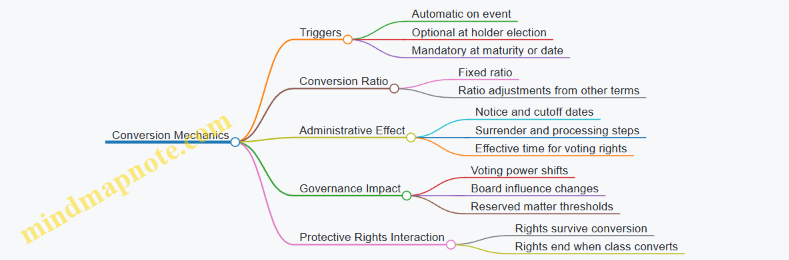

3.4 Conversion Mechanics and Their Control Implications

Conversion mechanics decide when and how one security becomes another, and that timing directly shapes who can influence corporate decisions. The key control question is simple: does conversion change voting power, board influence, or protective consent thresholds at moments that matter?

Conversion Basics That Control the Timeline

Most conversion provisions specify four moving parts: the trigger, the ratio, the method, and the administrative effect.

- Trigger: conversion may be automatic on an event (like a qualified financing) or optional at the holder’s election.

- Ratio: the conversion rate determines how many common shares a converted holder receives.

- Method: conversion may require notice, surrender of certificates, or a conversion form.

- Administrative effect: the charter and stock ledger rules determine when voting rights attach after conversion.

A practical example: if preferred converts automatically at closing, the company must ensure the cap table and voting record reflect the new common ownership immediately for any shareholder vote scheduled around that closing.

Control Implications of Conversion Triggers

Conversion triggers can be designed to prevent “surprise control” while still allowing investors to participate in upside.

- Automatic conversion on a financing tends to shift control quickly. If the new common shares are large enough, the investor group may gain voting influence right when the company is also making major approvals.

- Optional conversion at holder election spreads control changes over time. That can be helpful when the company wants stability for near-term governance, but it requires careful tracking of when holders exercise the option.

- Mandatory conversion at maturity or a fixed date creates a predictable governance transition. The company can plan board composition and reserved matters approvals around that date.

Example: A preferred series converts mandatorily on a specific date unless a protective condition is met. If the company schedules a shareholder vote shortly after that date, the voting threshold calculations must use the post-conversion ownership.

Conversion Ratios and Voting Power Math

The conversion ratio is where control often lives. Even small ratio differences can swing outcomes when votes are close.

Consider a simplified scenario:

- Preferred shares: 1,000

- Conversion ratio: 1.0 common per preferred

- If converted, the holder receives 1,000 common shares.

Now compare a second scenario:

- Preferred shares: 1,000

- Conversion ratio: 1.5 common per preferred

- If converted, the holder receives 1,500 common shares.

If the company has 10,000 common shares outstanding, the holder’s voting share becomes 10% versus 15%. That difference can matter for reserved matters requiring supermajority approvals.

Conversion Administration and Ledger Timing

Control is not only legal; it is operational. The company’s recordkeeping determines which votes are valid.

- Notice windows: if conversion requires notice, the company can define a cutoff date for inclusion in a meeting record.

- Surrender requirements: holders may need to surrender certificates or submit forms, which can delay conversion effectiveness.

- Effective time: documents should state whether conversion is effective upon notice, upon issuance of shares, or upon ledger update.

Example: If a holder submits a conversion notice after the record date for a meeting, the holder may not be counted for that meeting even if conversion is later processed. That is a governance control lever, intentionally or not.

Interaction with Protective Provisions

Conversion can change the class composition of the shareholder base, which can affect which protective provisions apply.

Two common design patterns:

- Protective provisions that survive conversion: some rights remain even after conversion, preventing holders from losing protections due to conversion.

- Protective provisions tied to class ownership: if protections apply only while preferred remains outstanding, conversion can reduce the group that holds those veto rights.

Example: A reserved matter might require approval by the preferred class “so long as any preferred remains outstanding.” Once conversion completes, that veto disappears. That can be acceptable if the company’s governance plan anticipates the transition, but it should be explicit.

Mind Map: Conversion Mechanics and Control Implications

Example: Designing Conversion to Avoid Governance Whiplash

Suppose a company issues preferred with optional conversion. The company wants stable voting for the next two quarters while it completes a restructuring. The documents can:

- require conversion notices to be delivered with a defined lead time,

- specify that voting rights attach only after the company updates the ledger,

- and clarify whether reserved matters require preferred approval only while preferred remains outstanding.

This approach doesn’t stop conversion; it prevents conversion from being used as a last-minute voting tactic during a meeting where the record date has already been set.

Example: Conversion Ratio That Aligns Incentives