Liquidity Engineering Across Supply Networks

1. Mapping Liquidity Flows Across Supply Networks

1.1 Defining Liquidity Engineering in Supply Chain Contexts

Liquidity engineering is the practice of designing how cash moves through a supply network so that payments happen on time, funding is available when needed, and disruptions don’t turn into a funding crisis. In supply chains, “liquidity” is not just a treasury concern; it’s the operational ability to pay invoices, settle disputes, and fund working capital across many parties with different incentives.

A useful starting point is to separate three ideas that often get mixed together:

- Liquidity availability: whether cash is present or can be sourced quickly.

- Liquidity timing: whether cash arrives before payment deadlines and before operational thresholds are breached.

- Liquidity quality: whether the cash is tied to valid invoices and correct settlement instructions, not to paperwork that will later be rejected.

When these three align, the supply network behaves like a well-tuned payment system rather than a collection of one-off transactions.

What Liquidity Engineering Changes in Practice

Liquidity engineering changes the rules of the game in four places.

- Who funds whom: A buyer may fund vendors earlier, a vendor may fund buyers through receivables, or an intermediary may fund both using a pool structure.

- What is eligible: Not every invoice should be financeable. Eligibility rules reduce funding tied to disputed or incomplete deliveries.

- When funding happens: Funding can be tied to invoice submission, proof of delivery, acceptance, or a scheduled payment date.

- How exceptions are handled: Disputes, partial deliveries, returns, and payment instruction errors need predefined workflows so liquidity doesn’t freeze.

A concrete example: a manufacturer receives raw materials from multiple suppliers. Without liquidity engineering, the manufacturer pays on its own schedule, vendors negotiate individually, and disputes cause delays. With liquidity engineering, the network defines invoice eligibility (including proof requirements), sets funding windows, and creates a dispute workflow that continues to move undisputed amounts. The result is fewer “cash surprises” and less time spent chasing paperwork.

Core Building Blocks

Think of liquidity engineering as assembling four blocks that must fit together.

- Flow map: the path from purchase order to delivery to invoice to payment, including who approves each step.

- Funding mechanism: the instrument or pool that provides cash, such as a receivables program or a payables funding structure.

- Risk controls: credit, operational, and legal controls that prevent funding from being based on unreliable data.

- Operational cadence: cutoffs, reconciliation routines, and escalation paths that keep the system moving.

If any block is missing, the system becomes fragile. For instance, a strong funding mechanism with weak eligibility rules can still fund invoices that later fail settlement, turning “liquidity” into a collection problem.

Stakeholder Roles and Their Liquidity Goals

Different parties optimize for different outcomes:

- Buyers want predictable payment timing, manageable working capital, and clean audit trails.

- Vendors want faster access to cash, clear acceptance criteria, and fewer payment delays caused by disputes.

- Intermediaries or program administrators want stable utilization, enforceable eligibility, and operational scalability.

- Banks and payment operators need correct instructions, consistent data formats, and exception handling that doesn’t create manual overload.

A practical way to align goals is to translate each party’s objective into measurable operational rules. For example, “vendors get paid faster” becomes “funding is triggered after invoice validation and proof-of-delivery acceptance, with a defined cutoff time.”

Mind Map: Liquidity Engineering in Supply Chain Contexts

Example: From Invoice Intake to Payment Without Surprises

Consider a vendor that submits invoices for delivered goods. Liquidity engineering starts at intake: the system checks invoice fields (invoice number, buyer reference, amounts, currency) and verifies that required delivery evidence is present. Next, eligibility rules determine whether the invoice can be funded immediately or only after acceptance. Then timing rules define the funding window and the expected value date. Finally, if a dispute is raised, the workflow specifies what happens to undisputed line items and what evidence is required to release disputed amounts.

This sequence matters because liquidity problems usually show up at boundaries: when data is incomplete, when acceptance is unclear, or when disputes are handled ad hoc. Liquidity engineering reduces those boundary failures by turning them into explicit rules.

A Simple Definition You Can Use Internally

Liquidity engineering in supply chain contexts is the design of eligibility, timing, funding mechanisms, and exception workflows so that cash movement matches the real state of goods, invoices, and approvals across multiple parties.

1.2 Identifying Liquidity Sources Uses and Constraints by Role

Liquidity engineering starts with a simple question: where does cash come from, where does it need to go, and what stops it from moving cleanly? In a supply network, “cleanly” is doing a lot of work. Different roles—buyers, vendors, logistics providers, banks, and program administrators—see different cash realities because they control different documents, payment triggers, and risk tolerances.

Role Based Liquidity Sources

Buyer side sources usually include operating cash, treasury credit lines, and working-capital facilities that convert invoices into earlier cash movements. A buyer may also have internal “payment timing” levers: payment calendars, approval workflows, and the ability to fund through centralized treasury rather than local accounts.

Vendor side sources often include receivables purchase programs, factoring arrangements, and short-term credit secured by invoice portfolios. Vendors typically care about speed and certainty: if an invoice is eligible and approved, cash should arrive on a predictable schedule.

Intermediary and program administrator sources include committed funding from banks or investors, plus internal liquidity buffers used to bridge timing gaps. Their job is to keep the program running even when invoices arrive late, disputes spike, or settlement instructions need correction.

Service providers such as logistics or inspection firms can indirectly affect liquidity by controlling proof-of-delivery or acceptance signals. Even when they do not fund directly, their operational outputs determine whether invoices become payable.

Role Based Liquidity Uses

Uses are where the cash must land, and they differ by role.

- Buyers use liquidity to pay suppliers on agreed terms while maintaining internal cash targets. They also use liquidity to manage exceptions: partial deliveries, invoice corrections, and dispute resolution.

- Vendors use liquidity to cover production costs, inventory replenishment, and payroll. Their “use” is often time-sensitive: a delay of a few days can force expensive short-term borrowing.

- Administrators use liquidity to fund eligible receivables, cover operational settlement timing, and maintain required reserves. They also use liquidity to absorb temporary mismatches between drawdowns and repayments.

- Banks and counterparties use liquidity to provide funding, manage credit exposure, and handle settlement rails. Their constraints show up as cutoffs, documentation requirements, and operational controls.

Constraints That Actually Matter

Constraints are not just risk limits; they are practical barriers that show up in daily operations.

- Eligibility constraints: Not every invoice can be funded. Common blockers include missing purchase order references, unclear delivery status, or incorrect tax treatment.

- Timing constraints: Value dates, cutoff times, and approval cycles can shift cash by days. A program that funds “on receipt” may still fund “after validation.”

- Credit constraints: Concentration limits by buyer, country, or industry restrict how much can be drawn. A sudden volume increase can exceed limits even if invoices are otherwise valid.

- Dispute constraints: Dispute windows, cure periods, and proof requirements determine whether cash is delayed or withheld.

- Operational constraints: Settlement instructions, bank account changes, and reconciliation rules can create funding holds.

A useful mental model is: sources generate capacity, uses consume capacity, constraints define the usable slice.

Mind Map: Liquidity Sources Uses and Constraints

Example: Same Invoice Different Outcomes

Consider an invoice for $250,000 dated 2026-02-26.

- The vendor submits it with a correct purchase order number and proof of delivery. If the invoice is eligible, the vendor expects funding within the program’s validation window.

- The buyer may have a payment approval workflow that requires confirmation of acceptance. If acceptance is not recorded by the cutoff, the buyer’s payment date shifts, which changes when the administrator receives repayment.

- The administrator checks eligibility and credit limits. If the buyer’s remaining credit cap is $180,000 for the month, only part of the invoice portfolio can be funded immediately.

- The bank handling settlement may require standardized remittance information. If the remittance reference is missing, repayment can be delayed even after the buyer pays.

The point is not that everyone is wrong; it’s that each role sees a different constraint surface. Liquidity engineering succeeds when those surfaces are mapped and managed together.

Practical Role Mapping Checklist

To identify sources, uses, and constraints without missing the obvious, map each role to three lists: what they can fund, what they must pay, and what can block movement. Then test the mapping with one real invoice lifecycle: submission, eligibility checks, funding decision, buyer approval, settlement, and reconciliation. If any step lacks an owner or a measurable rule, that gap will show up as a funding hold later—usually at the least convenient time.

1.3 Modeling Working Capital Cycles from Purchase Order to Settlement

Working capital modeling turns a messy chain of events into a timeline you can measure. The goal is simple: estimate how long cash is tied up from when a buyer commits to a purchase order until the moment the seller is paid and the buyer’s cash position reflects the settlement.

Core Timeline from Order to Cash Movement

Start with a sequence of states that every transaction can map onto. For a buyer, the cycle typically includes: purchase order issuance, goods receipt, invoice submission, invoice validation, payment scheduling, payment execution, and settlement confirmation. For a seller, the mirror image matters: order acceptance, fulfillment, invoice issuance, funding request, payment receipt, and reconciliation.

A practical modeling approach uses event dates and derives durations. For example, define:

- PO Date: when the buyer issues the purchase order.

- Receipt Date: when goods or services are accepted.

- Invoice Date: when the seller issues the invoice.

- Validation Date: when the buyer approves invoice for payment.

- Payment Date: when the buyer sends funds.

- Settlement Date: when funds are confirmed at the seller’s bank.

Then compute working capital drivers as differences between these dates. If you only track one metric, track Days Cash Tied Up: from PO Date to Settlement Date. If you track two, also track Invoice-to-Payment Lag: from Validation Date to Settlement Date.

Mind Map: Modeling Inputs and Outputs

Building the Model Step by Step

- Choose the unit of analysis. Use invoice-level records, not order-level, because payment usually follows invoices. If your business pays per milestone, model milestones as invoice-like events.

- Create a state machine. Each invoice moves through states such as Submitted, Validated, Scheduled, Paid, and Settled. This prevents mixing “sent” with “settled,” which is a common source of off-by-one-week errors.

- Map event dates to sources. PO dates come from procurement systems; receipt dates from warehouse or acceptance workflows; invoice dates from AP intake; validation dates from approval logs; payment and settlement from treasury and bank confirmations.

- Derive durations and cash timing. For payment terms, compute the contractual due date from the agreed reference point. Many programs use Receipt Date as the reference for Net terms; others use Invoice Date. Your model must encode which one applies.

- Handle discounts and partial payments. If terms include early payment discounts, compute two cashflow scenarios: discount taken vs. discount missed. For partial payments, split the invoice into payment tranches so the model doesn’t pretend the entire invoice settles at once.

Example with Concrete Numbers

Assume a buyer issues a PO on 2026-02-26. Goods are accepted on 2026-03-03. The seller submits the invoice on 2026-03-05. The buyer validates it on 2026-03-12. Payment terms are Net 30 from Receipt, so the contractual due date is 2026-04-02. The buyer schedules payment for 2026-03-28 to capture an operational preference, and the bank confirms settlement on 2026-03-31.

Derived durations:

- PO to Receipt: 5 days

- Receipt to Invoice: 2 days

- Invoice to Validation: 7 days

- Validation to Payment: 16 days

- Payment to Settlement: 3 days

Days Cash Tied Up for the buyer (PO to Settlement): from 2026-02-26 to 2026-03-31 is 33 days.

Modeling Exceptions Without Breaking the Timeline

Delays rarely come from one place. Add explicit exception states so you can measure where cash gets stuck:

- Invoice mismatch: validation paused due to quantity or price differences.

- Dispute: validation blocked until resolution.

- Missing references: invoice cannot be matched to PO.

- Bank cutoff: payment sent after cutoff shifts settlement by a business day.

When an exception occurs, keep the original planned dates and record the actual dates. That way, you can compute both “what should have happened” and “what did happen,” which is essential for improving the process rather than just reporting it.

Turning the Model into Decisions

Once the model produces stage durations and exception rates, you can identify bottlenecks. If Invoice-to-Validation is consistently long, focus on AP intake rules and matching tolerances. If Payment-to-Settlement is volatile, focus on cutoff calendars and payment rail selection. The model’s job is to point to the stage, not to blame a team—cash doesn’t care who pressed the button, but your controls should.

1.4 Segmenting Flows by Contract Type Payment Terms and Risk Drivers

Segmenting liquidity flows means grouping cash movements that behave similarly under stress. Instead of treating every invoice payment as the same event, you classify flows by contract type, payment terms, and the risk drivers that can change timing or certainty. The payoff is practical: you can set different pool rules, eligibility checks, and funding limits for each segment.

Foundational Building Blocks

Start with three attributes for every flow record (or every contract template):

- Contract type: what the legal and commercial relationship is doing. Examples include purchase orders with standard terms, supply agreements with rebates, framework contracts with call-offs, and consignment arrangements.

- Payment terms: when and how money moves. Examples include net 30, end-of-month, early payment discounts, milestone payments, and payment upon proof of delivery.

- Risk drivers: what can delay or reduce payment. Examples include disputes, delivery acceptance, credit concentration, currency mismatch, and regulatory withholding.

A simple way to keep this systematic is to map each flow to a “timing behavior” profile: does the contract anchor payment to an invoice date, a delivery event, or a calendar rule? Then map “certainty behavior”: does the contract create a clean path to payment, or does it require acceptance, reconciliation, or dispute resolution?

Segmenting by Contract Type

Contract type determines the event that starts the payment clock.

- Purchase order with invoice-based terms: payment often starts from invoice issuance. Liquidity is sensitive to invoice submission quality and completeness.

- Example: A buyer pays net 45 from invoice date. If vendors submit invoices late or with missing references, the cash-out shifts.

- Framework contract with call-offs: payment may start from each call-off delivery. Liquidity is sensitive to how call-offs are recorded and matched.

- Example: A buyer funds call-offs weekly; if call-off quantities are corrected after delivery, the payment date can move.

- Milestone or acceptance-based agreements: payment depends on acceptance. Liquidity is sensitive to dispute rates and acceptance turnaround.

- Example: A buyer pays 80% on acceptance and 20% after a warranty period. The pool should treat the 20% as a different segment with longer uncertainty.

- Rebates and deductions clauses: cash can be reduced after the fact. Liquidity is sensitive to reconciliation cycles.

- Example: A vendor issues invoices gross, but rebates are netted monthly. Segment the “netting window” separately so funding doesn’t assume full gross recovery.

Segmenting by Payment Terms

Payment terms control the cash calendar and the pool’s operational rhythm.

- Fixed tenor terms (net 30, net 60): timing is predictable, so focus on eligibility and dispute controls.

- Example: If most invoices are net 60, you can set a drawdown window aligned to that tenor.

- End-of-month terms: timing depends on month boundaries.

- Example: End-of-month net 30 means payment can cluster at month end. Pool liquidity should account for batch effects.

- Early payment discounts: timing is optional and can change behavior.

- Example: If a buyer offers 2%/10 net 30, the buyer may pay early when cash is available. Segment these invoices so the pool doesn’t overestimate funding duration.

- Payment upon proof of delivery: timing depends on operational events.

- Example: If proof of delivery is uploaded within two days, payment starts quickly; if not, funding certainty drops.

Segmenting by Risk Drivers

Risk drivers explain why two flows with the same tenor can behave differently.

- Dispute and chargeback likelihood: drives uncertainty in both timing and amount.

- Example: A segment with high dispute rates should require stronger proof of delivery and tighter submission rules.

- Credit concentration: drives pool fragility when one buyer dominates.

- Example: If 40% of eligible invoices come from one buyer, you set lower concentration limits and smaller draw sizes.

- Currency and withholding: drives payment amount variability.

- Example: Cross-border invoices with withholding tax can reduce net proceeds. Segment by tax treatment so eligibility reflects expected recoveries.

- Operational data quality: drives matching failures.

- Example: If invoice references are frequently incorrect, matching delays can mimic credit risk. Segment by data quality score.

Integrated Mind Map

Mind Map: Segmenting Flows by Contract Type, Payment Terms, and Risk Drivers

Example Segmentation Output

A practical output is a small set of segments with clear rules.

- Segment A: PO Invoice Net 45, Low Dispute

- Eligibility: complete invoice references, proof of delivery optional if historically low disputes.

- Pool rule: drawdown window aligned to net 45; standard concentration limits.

- Segment B: Acceptance-Based Milestones, Medium Dispute

- Eligibility: acceptance confirmation required; dispute history threshold enforced.

- Pool rule: shorter drawdown window and reduced advance rate to reflect acceptance delays.

- Segment C: Framework Call-Off End-of-Month Net 30, High Data Errors

- Eligibility: call-off linkage mandatory; data quality score minimum.

- Pool rule: funding only after successful matching; operational exception queue limits.

- Segment D: Cross-Border Invoices With Withholding

- Eligibility: tax treatment documented; expected net proceeds calculated.

- Pool rule: advance based on net recovery; separate limits by country and tax profile.

When you segment this way, every downstream decision has a reason. Eligibility checks stop being generic, pool limits stop being one-size-fits-all, and monitoring becomes targeted. The result is a liquidity system that behaves consistently with how contracts actually move cash.

1.5 Establishing a Data Inventory for Invoices Payments and Receivables

A liquidity pool lives or dies by data quality. If you cannot reliably answer “Which invoices are eligible, which payments are completed, and which receivables remain outstanding?” then every downstream decision becomes guesswork. A data inventory is the practical way to make those answers repeatable.

Start with the Inventory Purpose and Decision Questions

Before listing fields, write the decision questions the inventory must support. Typical questions include: Which invoices are submitted and within eligibility rules? Which invoices are funded and when? Which payments were made, matched, and settled? Which receivables are disputed, partially paid, or reversed? Each question maps to a data set and a minimum set of attributes.

Example: If your pool funds “approved invoices,” you need data that proves approval status, approval timestamp, and the approver identity or system event. Without timestamps, you cannot enforce cutoff calendars.

Define the Core Entities and Their Required Attributes

Use a small set of entities that cover the full lifecycle.

- Invoice: invoice identifier, buyer and vendor identifiers, invoice date, due date, currency, invoice amount, line items or total basis, goods or services reference, tax treatment indicators.

- Eligibility Event: eligibility status, eligibility decision timestamp, eligibility rule version, reason codes for rejection, and any required supporting documents references.

- Funding Event: funding request timestamp, funding amount, funding status, funding tranche or pool identifier, and settlement instructions used.

- Payment: payment identifier, payment date, value date, payment amount, payment currency, payment rail or method, bank account identifiers, and payment reference.

- Settlement and Reconciliation: match status, matched invoice(s), matched amount(s), tolerance thresholds, exception category, and reconciliation timestamp.

- Receivable: outstanding amount by invoice, aging bucket, dispute flag, dispute reason, dispute status, and expected resolution date.

A useful rule: every attribute should exist for a reason. If you cannot point to a decision question it supports, it probably belongs in a later enhancement.

Map Data Sources to Entities and Control Points

Data rarely comes from one place. Build a source-to-entity map that includes system of record and control points.

- ERP for invoice creation, due dates, and tax fields.

- AP/AR workflow for approval and dispute status.

- Treasury or payments platform for payment instructions and settlement confirmations.

- Bank feeds for actual payment events.

- Document systems for proof of delivery, credit notes, and dispute evidence.

Control points are where errors become expensive. For example, payment value date and currency must be validated against the payment platform and bank confirmation, not just the instruction record.

Establish Data Quality Rules with Concrete Examples

Quality rules should be testable.

- Uniqueness: invoice IDs must be unique within buyer-currency combinations. Example: two invoices with the same invoice number but different amounts should trigger a “duplicate candidate” exception.

- Completeness: funding cannot proceed without due date, currency, and buyer identifier. Example: if due date is missing, the invoice is held in “pending data” rather than rejected outright.

- Consistency: invoice total must equal sum of line items within tolerance. Example: a 0.02 currency unit difference might be allowed for rounding; a 20-unit difference is not.

- Timeliness: eligibility decisions must be recorded with timestamps. Example: if eligibility status changes after the cutoff, the system should tag it as “post-cutoff” for reporting.

Design the Inventory as a Traceable Lineage Chain

For liquidity engineering, traceability matters more than volume. Each funding decision should be traceable to: the invoice record, the eligibility decision, the funding event, the payment instruction, and the settlement match.

Include Exception Data as First-Class Inventory Items

Exceptions are not edge cases; they are the daily work of keeping pools accurate.

Inventory exception categories should include: dispute initiation and resolution, partial payment and allocation logic, credit notes and reversals, missing documentation, and mismatched bank references. For each category, define the minimum fields needed to resume normal processing.

Example: For a dispute, you need dispute reason code, dispute start timestamp, disputed amount, and the evidence reference. Without disputed amount, you cannot compute the remaining eligible receivable.

Set a Practical Implementation Scope and Naming Standards

A good inventory starts with a “minimum viable lineage.” For a first release, include the fields required to answer the four lifecycle questions: eligible or not, funded or not, paid or not, and outstanding or resolved.

Naming standards prevent confusion later. Use consistent prefixes such as inv_, elig_, fund_, pay_, setl_, and rcv_. Also standardize timestamps to a single time zone and store both event time and ingestion time.

Example: If you store elig_decision_ts and elig_ingest_ts, you can measure processing delays without guessing.

Validate the Inventory Using a Small End-to-End Sample

Pick a sample that includes normal and messy cases: one clean invoice, one with a credit note, one with a dispute, and one with a partial payment. Run the lifecycle questions end-to-end and confirm that every answer is supported by inventory data.

If the sample fails, fix the inventory before adding more fields. Data inventories are like payment rails: once you commit to a structure, retrofitting is expensive.

2. Designing Funding Pools for Vendors and Buyers

2.1 Selecting Pool Structures Based on Counterparty and Asset Eligibility

Pool structure is the part where “we can fund invoices” becomes “we can fund the right invoices, from the right counterparties, in the right way.” The goal is simple: match funding mechanics to (1) who is allowed to participate and (2) which assets are eligible to be financed.

Foundational Inputs

Start with two inventories.

Counterparty inventory lists every potential participant: buyers, vendors, and any intermediaries. For each, capture credit standing, dispute behavior, operational reliability, and legal capacity to assign or participate in receivables. A buyer with stable payment behavior can support a larger pool than a buyer with frequent invoice disputes.

Asset inventory lists every receivable type you might fund: standard invoices, credit notes, disputed invoices, and invoices with special delivery terms. Eligibility is not just “is it an invoice,” but also “is it provable, assignable, and matchable to purchase orders and delivery evidence.”

Eligibility Rules That Drive Structure

Eligibility rules determine the pool’s shape. Use them to decide whether you need a single pool, multiple pools, or a tiered structure.

- Proof strength: If invoices require proof of delivery, the pool must include workflow steps that block funding until proof is present. Weak proof pushes you toward shorter tenors and tighter draw limits.

- Dispute profile: If disputes are common, structure must separate “clean” invoices from “disputed” ones. Mixing them increases funding volatility and reconciliation workload.

- Assignment and setoff constraints: Some jurisdictions or contracts restrict assignment or allow setoff. When constraints exist, you may need buyer-specific sub-pools with tailored legal terms.

- Concentration tolerance: If one buyer represents most volume, you need concentration limits and possibly a cap per buyer or per country.

Pool Structure Options

Single Pool with Shared Eligibility

Use this when counterparties are similar and assets share the same eligibility requirements.

Example: A regional buyer group agrees to identical invoice formats, proof-of-delivery standards, and dispute windows. You create one pool where any eligible vendor invoice can be funded, subject to a single concentration cap per buyer.

Why it works: One set of rules reduces operational friction. When it fails: If one buyer’s dispute rate is materially higher, the pool’s risk profile becomes inconsistent.

Buyer-Specific Sub-Pools

Use this when legal terms, dispute behavior, or operational processes differ by buyer.

Example: Buyer A allows assignment with minimal restrictions; Buyer B requires additional consent for certain contract types. You create two sub-pools, each with its own eligibility checklist and concentration limits.

Why it works: You isolate risk and simplify audit evidence. Tradeoff: More pools mean more administration and reporting.

Tiered Pools Based on Asset Cleanliness

Use this when you want to fund a broad range of invoices but with different risk levels.

Example: Tier 1 funds invoices with proof of delivery and no exceptions. Tier 2 funds invoices submitted with partial documentation but within a defined cure period. Tier 2 draws are smaller and priced higher to reflect the extra uncertainty.

Why it works: You keep vendors funded while controlling funding volatility. Key control: A clear cure mechanism that either upgrades the invoice to Tier 1 or removes it from eligibility.

Rolling Eligibility with Cutoff Windows

Use this when asset eligibility depends on time-bound events like delivery confirmation or dispute notice.

Example: Invoices become eligible only after delivery confirmation is received and matched to the purchase order. If confirmation arrives after the cutoff, the invoice waits for the next funding cycle.

Why it works: Eligibility becomes deterministic. Operational note: You must align cutoff times with bank value dates and internal approval workflows.

Mind Map: Pool Structure Selection

Practical Selection Workflow

- Group counterparties by eligibility similarity: If two buyers require different legal handling or have meaningfully different dispute rates, separate them.

- Group assets by proof and dispute handling: If some invoices can be funded only after proof arrives, treat them as a different eligibility tier or separate pool.

- Apply concentration constraints early: Decide caps before you finalize structure, because caps often force sub-pooling.

- Design workflow gates to match the structure: A tiered pool without cure rules is just a single pool with extra steps.

- Confirm operational matchability: If your systems cannot reliably match invoices to purchase orders and delivery evidence, choose the structure that minimizes funding before matching is complete.

Worked Example: Choosing Between Two Structures

Assume you have invoices from three buyers.

- Buyer X: low disputes, assignment allowed, consistent delivery proof.

- Buyer Y: moderate disputes, assignment allowed, delivery proof sometimes delayed.

- Buyer Z: high disputes, assignment restricted for certain contract types.

A single pool would require broad eligibility rules and would fund delayed-proof invoices alongside clean ones, creating reconciliation spikes.

A buyer-specific sub-pool plus tiering fits better: create sub-pools for X and Z, and within Y use Tier 1 for invoices with proof and Tier 2 for invoices within a cure period. This keeps funding steady for Y while preventing Z’s restricted contracts from contaminating the rest of the program’s eligibility.

2.2 Defining Pool Governance Roles and Decision Rights

A funding pool is only as steady as the decisions that run it. Governance defines who can approve eligibility, who can release funds, who can pause draws, and how disputes get resolved—without forcing every question into a meeting. The goal is simple: make decisions fast enough to fund invoices on time, and careful enough to avoid funding the wrong things.

Core Governance Principles

Start with three principles that shape every role.

- Separation of duties: the person who approves eligibility should not be the same person who can unilaterally release funds.

- Clear decision thresholds: small exceptions can be handled operationally; larger deviations require higher approval.

- Documented authority: every decision path must map to a record, so audits and internal reviews can trace “who decided what and why.”

A practical way to implement this is to define a decision catalog. Each decision type gets an owner, an approver, a reviewer, and an evidence requirement.

Role Set for a Typical Vendor Buyer Pool

Most pools can be governed with five role groups.

Pool Sponsor: sets the program objectives and approves the governance charter. In a buyer-sponsored pool, the buyer sponsor typically owns the eligibility policy and dispute tolerance.

Pool Administrator: runs day-to-day operations. This role validates submissions, checks eligibility rules, and prepares draw requests.

Credit and Risk Committee: approves credit policy changes, concentration limits, and any exception that increases risk. This committee should include risk and finance leadership, not only operations.

Legal and Contract Owner: ensures program terms match operational behavior, especially around assignment, setoff, and dispute handling.

Operations Escalation Desk: handles time-sensitive exceptions like missing proof of delivery or partial invoice corrections, within pre-set thresholds.

To keep things concrete, define what each role can do in one sentence. For example: the Pool Administrator can validate and stage draws, but cannot approve eligibility exceptions beyond the documented tolerance.

Decision Rights Matrix

Decision rights should be expressed as a matrix of decision types versus roles. Below is a compact template you can adapt.

| Decision Type | Pool Administrator | Credit and Risk Committee | Legal and Contract Owner | Operations Escalation Desk |

|---|---|---|---|---|

| Standard invoice eligibility check | Approve | - | - | - |

| Eligibility exception within tolerance | Recommend | Approve | - | Approve |

| New buyer or vendor onboarding | Recommend | Approve | Review | - |

| Concentration limit breach | Stop draw | Approve remediation | Review | - |

| Dispute classification and funding hold | Recommend | Approve hold extension | Review | Approve short hold |

| Contract term change | - | Review | Approve | - |

| Data model change affecting eligibility | Recommend | Review | Review | Approve if low risk |

The key is that “Approve” and “Recommend” are not synonyms. If the administrator recommends, the committee must be able to say yes or no with a defined evidence package.

Evidence and Approval Thresholds

Every decision needs evidence. For eligibility, evidence might include invoice fields, proof of delivery status, and contract term mapping. For risk exceptions, evidence should include buyer payment history, dispute rates, and any collateral or guarantees.

Set thresholds that prevent governance gridlock. A common pattern is:

- Operational threshold: small data corrections or short holds (handled by the Escalation Desk).

- Risk threshold: exceptions that change credit exposure or tenor (handled by the Credit and Risk Committee).

- Legal threshold: anything that changes rights, setoff, or assignment mechanics (handled by Legal).

If you need a date for governance records, use a fixed reference point such as 2026-02-15 for the initial charter effective date.

Mind Map: Governance Roles and Decision Rights

Example: Who Approves a Funding Hold

Assume a vendor submits an invoice and proof of delivery is missing for two line items due to a partial shipment.

- The Pool Administrator runs the standard eligibility check and flags the missing proof.

- The Escalation Desk approves a short hold for the affected line items because it falls within the operational threshold.

- The administrator continues processing the eligible portion so the vendor still receives funding on time.

- If the dispute classification later indicates a higher dispute risk category, the Credit and Risk Committee approves an extended hold and any remediation plan.

This example shows why governance matters: the pool keeps moving, but the riskier decisions still go through the right authority.

Example: Concentration Limit Breach Remediation

If a single buyer’s funded exposure exceeds a pre-set concentration limit, the system should trigger a draw stop. The administrator prepares a remediation package: current exposure, remaining eligible invoices, and options such as reducing future draws or tightening eligibility for that buyer.

The Credit and Risk Committee decides the remediation path, while Legal reviews whether any contractual levers exist for setoff or assignment adjustments. The sponsor is informed, but does not need to approve every operational remediation step.

Governance Outputs You Should Produce

To make governance usable, produce three artifacts:

- Decision catalog listing decision types, owners, approvers, and evidence.

- Decision thresholds defining what can be handled operationally versus committee-level.

- RACI-style matrix mapping roles to actions for eligibility, draws, holds, disputes, and contract changes.

With these in place, the pool can fund efficiently without turning governance into a bottleneck.

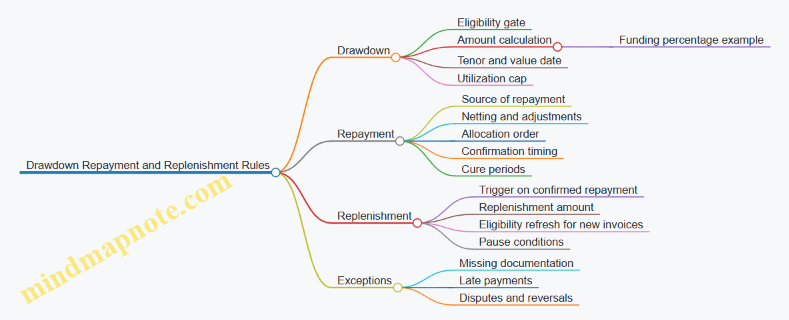

2.3 Setting Operational Rules for Drawdown Repayment and Replenishment

Operational rules turn a funding pool from a spreadsheet promise into a repeatable routine. The goal is simple: every drawdown has a clear repayment path, every repayment has a clear replenishment path, and exceptions are handled without inventing new rules under pressure.

Foundational Concepts for Pool Operations

Start by defining three operational objects: drawdown, repayment, and replenishment.

- Drawdown is the pool’s advance to a vendor or buyer under agreed eligibility and documentation.

- Repayment is the cash return to the pool when the underlying invoices are paid, net of any agreed adjustments.

- Replenishment is the restoration of available capacity after repayments, so the pool can fund new eligible invoices.

A practical way to keep teams aligned is to map these objects to the pool’s lifecycle states: Available, Utilized, In Repayment, and Replenished. Each state should have a short checklist of what must be true before moving forward.

Core Operational Rules for Drawdown

Operational rules for drawdown should be strict enough to prevent accidental overfunding, but not so strict that they block normal invoice flow.

- Eligibility gate before funding: funding requests must reference eligible invoices and include required proof (for example, invoice number, buyer reference, and proof of delivery where applicable). If a field is missing, the request is rejected or queued, not partially funded.

- Amount calculation rule: define whether the drawdown equals invoice face value, a percentage, or a discounted amount. For example, if the pool funds 90% of eligible invoices, then a €100,000 invoice drawdown is €90,000.

- Tenor and value date rule: specify the expected repayment date window based on payment terms. If terms are “net 30,” set the expected repayment window to invoice date plus 30 days, plus a small operational buffer for settlement timing.

- Utilization cap: enforce a hard limit on total outstanding advances. If the cap is €50 million and utilization is already €49.2 million, a new request for €1.5 million can only proceed up to €0.8 million.

Repayment Rules That Prevent Cash Confusion

Repayment rules should define what counts as repayment and how it is applied.

- Source of repayment: repayment comes from buyer payments into a designated account or from a contractual remittance process. Mixing repayment sources without tagging creates reconciliation pain.

- Netting and adjustments: define how disputes, credit notes, and returns affect repayment. Example: if a buyer pays €95,000 on a €100,000 invoice and a €5,000 credit note is already confirmed, treat the €95,000 as full repayment for that invoice.

- Allocation order: when multiple invoices are funded, specify allocation order for partial payments. A common rule is FIFO by invoice maturity date, but the rule must be consistent and auditable.

- Repayment confirmation timing: set a rule for when repayment is considered confirmed. For instance, confirmation occurs when bank settlement is received and matched to invoice references.

- Cure periods for late payments: if repayment is late, define the cure window and what actions occur during it. Example: if payment is 5 days late, send a reminder; if 15 days late, require escalation and may pause new drawdowns for that buyer.

Replenishment Rules That Restore Capacity Safely

Replenishment rules should be the mirror image of drawdown rules, with additional safeguards.

- Replenishment trigger: capacity increases only after confirmed repayments, not after payment initiation. This avoids “phantom capacity” based on pending transfers.

- Replenishment amount calculation: replenishment should reflect the principal portion returned, not fees. Example: if a €90,000 drawdown repays €89,100 due to an agreed discount, replenishment should restore €89,100 of capacity, while fees are handled separately.

- Eligibility refresh requirement: after replenishment, new drawdowns must re-check eligibility for newly submitted invoices. Replenishment does not automatically validate future invoices.

- Operational pause conditions: define when replenishment continues but drawdowns pause. Example: if dispute rates exceed a threshold for a specific buyer, allow replenishment to keep the pool stable while preventing new utilization from that buyer.

Exception Handling Rules That Keep the System Honest

Exceptions should be categorized so teams respond consistently.

- Missing documentation: reject drawdown requests until corrected; do not “fund now, fix later.”

- Dispute opened after drawdown: define whether the outstanding advance is reduced immediately or after dispute confirmation. Example: reduce utilization only when the dispute is validated and supported by agreed evidence.

- Chargebacks or reversals: treat reversals as negative repayments with a defined timeline for re-collection or replacement invoices.

Mind Map: Drawdown Repayment and Replenishment Rules

Example Workflow with Concrete Numbers

Assume a pool funds 90% of eligible invoices and has a €50 million utilization cap.

- A vendor submits an eligible €100,000 invoice. Drawdown request is €90,000, and utilization becomes €49.2 million + €90,000.

- The buyer pays €95,000 on the invoice, and a €5,000 credit note is already confirmed. Repayment is treated as €100,000 principal settled, but replenishment restores only the funded principal portion: €90,000.

- If the payment arrives 12 days late, the cure period rule triggers escalation at day 10. New drawdowns for that buyer are paused, but replenishment continues once the bank settlement is confirmed.

These rules create a predictable rhythm: funding depends on eligibility, repayment depends on confirmed cash and agreed adjustments, and replenishment depends on verified principal return. The pool stays usable without turning reconciliation into a scavenger hunt.

2.4 Building Eligibility Criteria for Invoices Credit Notes and Disputes

Eligibility criteria are the rules that decide what can be funded, when it can be funded, and what evidence must exist to support the decision. In practice, they prevent the pool from paying for invoices that are not real, not payable, or not yet settled enough to be safe. The trick is to write criteria that are strict where it matters and flexible where it helps operations.

Eligibility Foundations That Keep the Pool Honest

Start with three baseline questions for every submission.

- Is the document eligible? The pool should accept only specific document types: invoices and credit notes, plus dispute records that meet defined thresholds. Everything else is rejected or routed to manual review.

- Is the underlying transaction eligible? Eligibility depends on contract terms, delivery status, service period, and whether the buyer has approved the goods or services.

- Is the counterparty and amount eligible? Limits should cover buyer credit standing, invoice amount bands, and concentration rules.

A simple example: a vendor submits an invoice for $120,000 dated 2026-02-15. The pool checks that the invoice is within the allowed age window, that the buyer is an approved counterparty, and that the contract includes the product category. If the invoice is outside the age window, it is not funded even if the buyer is approved.

Invoice Eligibility Criteria

Invoice criteria should be grouped into identity, commercial validity, and payment readiness.

Identity checks ensure the invoice is uniquely identifiable and internally consistent.

- Invoice number format and uniqueness within the pool.

- Buyer legal entity match to the pool’s master data.

- Currency match to supported currencies.

Commercial validity checks ensure the invoice reflects an actual transaction.

- Contract reference present and active.

- Goods receipt or service acceptance evidence available.

- No duplicate invoice for the same purchase order line items.

Payment readiness checks ensure the invoice is not already blocked.

- No existing dispute above the allowed tolerance.

- Not subject to legal setoff or termination clauses that would prevent payment.

- Payment terms within the pool’s supported tenor range.

Operationally, these checks should be applied in a predictable order so teams can explain outcomes. If identity fails, there is no need to evaluate delivery evidence.

Credit Note Eligibility Criteria

Credit notes are not just “negative invoices.” They change the net amount and can reverse prior funding exposure.

Key eligibility rules include:

- Credit note must reference an eligible invoice or a specific purchase order.

- Credit note must be approved by the buyer according to the same acceptance workflow used for invoices.

- Credit note effective date must fall within the pool’s adjustment window.

- Netting rules must be explicit: whether the pool reduces the funded amount immediately or waits until the next reconciliation cycle.

Example: A vendor’s invoice for $50,000 was funded. Two weeks later, the buyer issues a credit note for $5,000 due to a quantity correction. If the credit note is within the adjustment window and properly approved, the pool reduces the outstanding balance by $5,000 using the defined netting rule. If it is not approved, the pool keeps the original exposure until approval arrives.

Dispute Eligibility Criteria

Disputes are the part of the process where eligibility must be both fair and controlled. A dispute record should not automatically block everything, but it must prevent funding for the disputed portion.

Define disputes using these criteria:

- Dispute type: quantity, quality, pricing, or service period.

- Dispute status: submitted, under review, resolved.

- Dispute amount threshold: disputes below a tolerance may be funded with holdbacks; disputes above it trigger partial funding or full rejection.

- Evidence requirement: buyer must provide a reason code and supporting documentation.

- Timing rules: disputes must be raised within the allowed window after invoice submission or acceptance.

Example: The buyer disputes $8,000 of a $40,000 invoice for a delivery variance. If the pool’s tolerance is 20% and the dispute is 20% exactly, the pool may fund 80% immediately and hold the disputed amount until resolution. If the dispute is $12,000 (30%), the pool funds nothing until the dispute is resolved or falls below the threshold.

Advanced Details That Prevent Edge-Case Failures

Eligibility criteria should include how to handle common edge cases.

- Partial deliveries: allow funding based on accepted delivery quantities, not on the full purchase order value.

- Multiple invoices per purchase order: require line-level matching to avoid double counting.

- Amended invoices: treat amendments as new submissions with a clear rule for superseding prior versions.

- Reconciliation timing: specify whether eligibility is evaluated at submission time, funding time, or both.

A practical rule: evaluate eligibility at submission for speed, then re-check critical items at funding time for safety. This catches late disputes or late approval changes.

Mind Map: Eligibility Criteria for Invoices, Credit Notes, and Disputes

Example Workflow That Ties the Criteria Together

A vendor submits an invoice on 2026-02-10. The system checks identity and contract validity first. Next it verifies acceptance evidence. Then it checks whether a dispute exists and whether it is within tolerance. If eligible, the pool funds the accepted portion and records the holdback logic for any disputed portion. If a credit note arrives later, the system applies the adjustment window and netting rule to update the outstanding balance.

This approach keeps eligibility criteria actionable: every rule has a clear input, a clear decision, and a clear operational outcome.

2.5 Creating Standard Operating Procedures for Pool Administration

A pool works only if people can execute the same steps the same way, even when the invoice volume spikes or a counterparty sends “almost correct” documents. Standard Operating Procedures (SOPs) turn that consistency into a repeatable workflow: who does what, when they do it, what they check, and what happens when something doesn’t match.

SOP Scope and Operating Principles

Start by defining the SOP boundary: it covers pool administration tasks from intake of eligible invoices through funding, repayment, and exception handling. Then set operating principles that guide every step.

- Single source of truth: one system holds the pool rules, eligibility status, and funding decisions.

- Segregation of duties: the person who approves eligibility is not the person who releases funds.

- Traceability: every funding decision links to the exact eligibility evidence used.

- Time discipline: each step has a target turnaround time and a fallback path.

Example: If a vendor submits invoices via email, the SOP requires a manual intake step that creates a structured record in the system before any eligibility checks begin. This prevents “lost attachments” from becoming “mysterious funding gaps.”

Roles, Responsibilities, and Escalation Paths

Define roles in a way that matches real operations.

- Pool Administrator: maintains eligibility rules, monitors daily exceptions, and approves funding batches.

- Eligibility Analyst: validates invoice attributes, proof of delivery, and dispute flags.

- Treasury Operator: executes funding and repayment instructions.

- Compliance Reviewer: checks sanctions screening outcomes, tax documentation completeness, and contract term alignment.

- Dispute Coordinator: manages dispute intake, evidence requests, and resolution updates.

Escalation should be explicit. For example, if eligibility evidence is missing beyond a defined window, the SOP routes the item to “Hold” with a reason code and triggers a counterparty request workflow.

End-to-End Workflow for Funding and Repayment

Use a batch-oriented workflow so the pool can be administered predictably.

- Intake and normalization: invoices are converted into standardized fields (invoice number, buyer, amount, currency, due date, goods/service reference).

- Eligibility validation: checks include contract coverage, invoice status, dispute indicators, and required supporting documents.

- Credit and concentration checks: ensures the buyer and pool limits are not breached.

- Funding decision: eligibility analyst recommends; pool administrator approves.

- Funding execution: treasury sends payment instructions and records value dates.

- Reconciliation: compare funding confirmations to the batch ledger.

- Repayment tracking: repayment is scheduled based on contract terms and updated when settlement occurs.

- Closeout and reporting: exceptions are summarized with counts, amounts, and resolution status.

Example: A batch includes 500 invoices. If 12 invoices fail proof-of-delivery checks, the SOP funds the remaining 488 and places the 12 into a separate exception batch. This avoids delaying the entire vendor population for one missing document.

Eligibility Evidence Standards and Checklists

Eligibility checks must be measurable. Define evidence requirements per invoice type.

- Invoice completeness: required fields present and consistent with master data.

- Contract match: buyer and vendor are active under the pool agreement.

- Dispute status: disputes must be flagged with a reason and evidence; disputed invoices are excluded or partially funded per policy.

- Proof of delivery: acceptance documents must match the goods/service reference.

Checklist example for a goods shipment invoice:

- Purchase order reference matches buyer contract

- Delivery note number present

- Delivery date within allowed window

- Amount equals invoice line totals after tax handling rules

Exception Handling and Root Cause Discipline

Exceptions are inevitable; the SOP should make them structured.

- Category: data error, missing evidence, contract mismatch, dispute, payment failure, or reconciliation mismatch.

- Severity: block funding, allow partial funding, or allow post-funding correction.

- Resolution owner: assigns responsibility for each category.

- Evidence request template: standard messages reduce back-and-forth.

Example: If a buyer reports a dispute after funding, the SOP requires a dispute coordinator to record the dispute date, attach evidence, and trigger a defined adjustment path (e.g., hold future drawdowns and reconcile repayment timing).

Controls, Audit Trail, and Version Management

SOPs must survive audits.

- Approval controls: funding batch approval requires two-person sign-off.

- System controls: eligibility rule changes require change tickets and effective dates.

- Audit trail: each decision stores the rule version, evidence references, and approver identity.

- Retention: documents are retained for the contractually required period.

Use a versioning rule: “Rule set version X.Y applies to intake after the effective timestamp.” This prevents arguments like “we followed the old rules” when the system already moved on.

Mind Map: Pool Administration SOP

Practical Example SOP Runbook for One Day

On a typical day, the pool administrator starts with a batch queue review, then confirms that the eligibility analyst completed validations for the scheduled intake window. The treasury operator executes only the approved batch, records confirmations, and flags any payment failures immediately. By end of day, the dispute coordinator updates exception statuses, and the compliance reviewer checks that sanctions screening results and tax documentation completeness meet the defined thresholds.

Example: If payment confirmations arrive late, the SOP requires a reconciliation hold for that batch and a status update to finance so reporting doesn’t mix “sent” with “settled.”

3. Credit Underwriting for Receivables and Payables Programs

3.1 Underwriting Frameworks for Buyer Sponsored and Vendor Sponsored Programs

Underwriting is the discipline of deciding what you will fund, for whom, under what evidence, and what you will do when reality disagrees with the paperwork. In supply networks, the “reality” usually shows up as disputes, partial deliveries, late approvals, and invoices that look fine until you match them to a purchase order.

Core Underwriting Inputs

Start with the same three building blocks for both buyer sponsored and vendor sponsored programs:

- Counterparty quality: buyer creditworthiness for buyer sponsored programs, and vendor creditworthiness for vendor sponsored programs.

- Invoice quality: proof that the invoice corresponds to a valid obligation, including delivery or service acceptance.

- Program mechanics: eligibility rules, cure periods, dispute handling, and how quickly information flows from operational systems to treasury.

A simple way to keep teams aligned is to treat underwriting as a checklist that produces a decision outcome: approve, approve with limits, or decline. The checklist should be auditable, not just “someone’s judgment.”

Buyer Sponsored Underwriting Framework

In a buyer sponsored program, the buyer’s obligation is the anchor. The underwriting goal is to ensure that when vendors submit invoices, the buyer will pay or will resolve disputes in a controlled way.

Step 1: Buyer credit assessment

- Use financial indicators and payment history, but also check operational signals like billing disputes volume and approval cycle time.

- Example: If a buyer’s dispute rate spikes after a new ERP rollout, you may still approve, but you tighten eligibility and shorten the funding window.

Step 2: Invoice eligibility and evidence

- Require matching fields such as purchase order number, line item identifiers, and delivery confirmation.

- Example: For a shipment-based contract, fund only invoices with a proof-of-delivery reference and a delivery date within the contract window.

Step 3: Dispute and cure design

- Define what counts as a valid dispute and how quickly the buyer must notify.

- Example: If the buyer disputes within 5 business days, you pause further funding for that invoice and route it to a resolution workflow; if not, you treat it as accepted.

Step 4: Limits and concentration controls

- Set limits by buyer, country, and contract type.

- Example: Cap exposure to a single buyer at a percentage of program capacity, and reduce the cap for higher dispute categories like services without acceptance milestones.

Vendor Sponsored Underwriting Framework

In a vendor sponsored program, the vendor’s ability to originate clean receivables becomes central. The underwriting goal is to ensure that the vendor can consistently produce eligible invoices and manage disputes.

Step 1: Vendor credit and operational reliability

- Assess vendor financial stability and, just as importantly, invoice origination discipline.

- Example: A vendor with stable margins but frequent invoice corrections may still be eligible, but you require stricter matching and longer review for first-time contracts.

Step 2: Receivable quality controls

- Validate that invoices are supported by contract terms, delivery/service acceptance, and correct tax treatment.

- Example: For maintenance services, require acceptance sign-off or ticket closure evidence, not just invoice submission.

Step 3: Program governance and data integrity

- Underwrite the workflow: who submits, who approves, and how exceptions are handled.

- Example: If the vendor’s system sometimes omits tax IDs, you can approve the vendor but block funding until corrected master data is in place.

Step 4: Limits based on performance history

- Use early performance to adjust limits.

- Example: If early batches show low dispute rates and fast resolution, you expand eligibility; if not, you tighten evidence requirements.

Mind Map: Underwriting Logic Across Sponsorship Models

Integrated Example: Same Invoice, Different Underwriting Emphasis

Imagine a vendor submits an invoice for delivered components.

- Buyer sponsored: You focus on whether the buyer is likely to pay and how quickly disputes are raised. If the buyer typically disputes late, you shorten the funding window and require stricter proof-of-delivery.

- Vendor sponsored: You focus on whether the vendor reliably links invoices to the correct purchase order and delivery evidence. If invoice corrections are common, you require additional matching fields before funding.

Both models use the same evidence categories, but they weight them differently because the risk sits with different parties.

Practical Underwriting Artifacts

To keep underwriting operational, produce three artifacts for each program:

- Eligibility rulebook: what qualifies, what is blocked, and what triggers review.

- Dispute playbook: dispute categories, required evidence, and cure timelines.

- Limit schedule: how exposure changes with performance and concentration.

When these artifacts exist, underwriting becomes repeatable. It also makes exceptions easier to handle, because everyone knows which lever to pull and why.

3.2 Assessing Invoice Quality Including Dispute Rates and Proof of Delivery

Invoice quality is the practical bridge between “we funded it” and “we can defend it.” In receivables and payables programs, quality assessment should answer three questions: Is the invoice valid, is it payable under the program rules, and will it survive the dispute process? The goal is not to predict every dispute, but to reduce avoidable ones by catching the common failure modes early.

Foundational Quality Signals

Start with invoice identity and completeness. A high-quality invoice has a consistent invoice number, correct buyer and seller identifiers, a clear invoice date, and a line-item structure that matches the underlying commercial agreement. As a simple example, if an invoice lists 120 units but the purchase order line shows 100 units, the mismatch is not a “minor clerical issue”—it is a dispute magnet. Similarly, missing tax fields, absent currency codes, or unclear service periods should trigger a hold until corrected.

Next, validate commercial alignment. Compare invoice terms to the contract or purchase order: unit prices, quantities, discounts, and payment terms. If the invoice applies a discount that the contract does not allow, the buyer may dispute even if the invoice is otherwise accurate. A good rule of thumb: if the invoice requires interpretation to determine what was agreed, it is not ready for funding.

Dispute Rate Assessment

Dispute rate is a quality metric that turns messy human behavior into something you can manage. Compute it at multiple levels: by buyer, by vendor, by program, and by invoice type (goods vs. services, domestic vs. cross-border). Use a consistent definition, such as “disputed invoices divided by submitted invoices” over a fixed window.

Example: Suppose Vendor A submits 1,000 invoices in a quarter and 35 are disputed. The dispute rate is 3.5%. If Vendor B submits 1,000 invoices and 10 are disputed, its dispute rate is 1.0%. The difference is actionable only if you also categorize dispute reasons. If Vendor A’s disputes are mostly “quantity mismatch,” you can tighten proof-of-delivery requirements. If they are mostly “pricing disputes,” you can tighten price validation against the contract.

To make dispute rates useful, separate “early disputes” from “late disputes.” Early disputes often indicate preventable data issues. Late disputes can indicate process gaps, such as delayed buyer review or late delivery confirmations. Both matter, but they point to different fixes.

Proof of Delivery as Evidence Quality

Proof of delivery (PoD) is the evidence that the goods or services were actually delivered or accepted. PoD quality is not binary; it has gradations. A delivery note with missing delivery dates is weaker than one with delivery dates, reference numbers, and recipient confirmation.

A practical approach is to score PoD completeness and traceability. Completeness covers whether required fields exist. Traceability covers whether the PoD can be linked to the invoice and the underlying order line.

Example: A warehouse scan system records a pallet ID and delivery timestamp, but the invoice references only the order number. If the mapping from pallet ID to order line is not stored, the PoD becomes hard to use during a dispute. The invoice may still be funded, but it should be funded with a lower confidence score or with tighter monitoring.

Integrated Quality Workflow

Quality assessment should be systematic: validate, score, decide, and record. The workflow below keeps decisions consistent across teams.

- Step 1: Validate structure: required fields, formats, and identifiers.

- Step 2: Validate commercial alignment: prices, quantities, terms, and tax.

- Step 3: Validate PoD linkage: delivery/service evidence matches invoice lines.

- Step 4: Compute quality score: combine structural, commercial, and PoD scores.

- Step 5: Decide funding action: approve, approve with conditions, or hold.

- Step 6: Record outcomes: dispute reason codes and resolution status.

A conditional example: If PoD is present but missing recipient confirmation, you might allow funding with a reduced advance rate and require an updated PoD within a defined cure window.

Mind Map: Invoice Quality Assessment

Example: Putting It Together with a Quality Score

Assume a simple scoring model with three components: structure (0–40), commercial alignment (0–40), and PoD linkage (0–20). An invoice with perfect structure (40), correct pricing and quantities (35), and PoD linked to the order line but missing recipient confirmation (12) totals 87. If your program threshold for standard funding is 90, you can either hold it for the missing confirmation or fund with a condition.

The key is that the score is explainable. When a dispute happens, you can trace it back to the component that was weakest. If most disputes occur on invoices with PoD linkage under 15, you tighten PoD requirements rather than blaming the entire invoice process.

Evidence Recording for Dispute Handling

Finally, record dispute outcomes in a way that supports future assessment. Store the dispute reason code, the disputed line items, the missing or incorrect fields, and whether PoD was the root cause. Over time, this turns dispute rates from a retrospective statistic into a targeted quality control system that reduces avoidable disputes without slowing down every invoice.

3.3 Evaluating Concentration Limits by Buyer Vendor Country and Industry

Concentration limits answer one practical question: “How much of our pool can depend on a small set of counterparties or geographies before a single disruption becomes expensive?” In liquidity engineering, concentration is not just a credit metric; it directly shapes funding stability, operational workload, and recovery time when invoices fail to perform.

Start with the basics. A concentration limit is a cap on exposure measured over a defined window (for example, outstanding funded amount, committed amount, or expected cash inflow). The window matters because a pool can look diversified on paper while still being fragile during a short settlement cycle.

Next, define exposure consistently. For invoice-based programs, exposure is typically the funded principal outstanding. For payables programs, exposure can be the net amount due to the pool participant. Use the same currency basis across countries by converting at the invoice currency spot rate used for funding, then track FX movements separately so concentration limits do not accidentally “move” just because rates changed.

Now choose the concentration dimensions. Buyer concentration is usually the first lever because buyer default or payment suspension stops cash inflow. Vendor concentration matters when the pool relies on a narrow set of suppliers whose delivery performance drives dispute rates. Country concentration matters because payment rails, legal enforceability, and tax friction vary by jurisdiction. Industry concentration matters because contract norms differ: some sectors see higher dispute rates, longer proof-of-delivery cycles, or more frequent contract amendments.

A simple foundation is a three-layer limit set:

- Buyer-level cap: maximum funded exposure per buyer.

- Country-level cap: maximum funded exposure per buyer country and per vendor country.

- Industry-level cap: maximum funded exposure per industry segment, often mapped from buyer and vendor industries.

Then add cross-dimension caps. A buyer in a high-risk country can be riskier than the same buyer in a stable country, so you need a combined view such as “Buyer Country × Buyer” or “Buyer Country × Industry.” This prevents a pool from passing individual caps while still concentrating risk in a specific corner.

Mind Map: Concentration Limit Design

Example: Buyer Country Concentration with a Concrete Threshold

Assume a pool has a total funding capacity of 100 million. You set a buyer-level cap of 12% (12 million) and a buyer-country cap of 35% (35 million). The pool currently has:

- Buyer A (Germany): 10 million

- Buyer B (Germany): 9 million

- Buyer C (Germany): 8 million

- Buyer D (France): 20 million

- Remaining buyers: 53 million

Germany exposure totals 27 million, which is under the 35 million country cap. Even if Buyer A is under its 12 million cap, the pool is still reasonably diversified by country. Now suppose a new onboarding adds 15 million from Buyer E (Germany). Germany becomes 42 million, exceeding the country cap. The correct response is not “reject everything,” but apply a structured action: reduce the new drawdown amount, require additional credit enhancement, or pause onboarding until Germany exposure falls below the cap.

Example: Industry Concentration Using Dispute Rate as a Risk Weight

Concentration limits can be sharpened by risk weighting. Suppose the pool uses a base exposure cap by industry, but industries with historically higher dispute rates get tighter caps. For instance:

- “Industrial Components” dispute rate: 1.5%

- “Construction Services” dispute rate: 4.5%

If both industries share the same base industry cap of 30 million, you might tighten “Construction Services” to 20 million because disputes delay cash inflow and increase operational exception handling. This is not a prediction; it is a disciplined use of observed behavior in the same program design.

Example: Cross-Dimension Cap Preventing Hidden Fragility

Consider a pool where buyer-level caps are respected and country caps are respected. Yet the pool is still fragile if many exposures cluster in one buyer country and one industry combination. Example:

- Buyer-level: all buyers are below 12 million

- Country-level: no country exceeds 35%

- But “Germany × Construction Services” totals 30 million, while your cross-dimension cap is 18 million.

In this case, the pool fails the cross-dimension cap because the same operational failure mode—proof-of-delivery disputes and contract change cycles—tends to occur together. The cross-dimension cap forces the program to treat this combination as a single risk bucket.

Operationalizing Limits Without Creating a Paper Exercise

Monitoring frequency should match settlement cadence. If funding draws and repayments occur weekly, concentration checks should run at least daily against the latest invoice register and payment status. When limits are breached, define cure actions in advance: partial funding, delayed drawdown until eligibility is confirmed, or temporary suspension for specific onboarding batches.

Finally, document the rationale for each cap so exceptions are explainable. A limit that exists only because “someone set it” will be hard to defend during audits and hard to adjust during onboarding. A limit that ties to exposure definition, observed dispute behavior, and governance thresholds stays usable even when the pool grows.

3.4 Structuring Credit Enhancements Such as Guarantees and Overcollateralization

Credit enhancements are the “extra layer” that makes a funding pool behave better when invoices don’t pay on time, disputes linger, or a buyer’s credit weakens. The key is to structure them so they are enforceable, measurable, and operationally usable—otherwise they become paperwork with good intentions.

Foundations for Choosing the Right Enhancement

Start with three inputs: (1) what risk you are covering, (2) who can trigger the enhancement, and (3) how quickly the pool needs relief.

- Risk covered: late payment, non-payment, dispute losses, or a mix. For example, if disputes are common, a guarantee that pays only after final adjudication may be too slow.

- Trigger timing: enhancements should activate on objective events such as delinquency days, dispute aging, or failure to replenish.

- Operational usability: the enhancement must specify the exact calculation method for losses and the payment mechanics.

A practical rule: if your enhancement cannot be calculated from data you already receive daily, it will not work when you need it.

Guarantees and Letters of Credit

A guarantee is a promise by a third party to cover defined losses. A letter of credit is a payment instrument that can be drawn under specified conditions.

Example: Buyer delinquency guarantee

- A buyer participates in a receivables pool.

- The enhancement is triggered when invoices become delinquent for 15 business days.

- The guarantor pays the pool for the unpaid invoice amount net of any amounts already recovered.

To keep this enforceable, define:

- Eligible invoices: only invoices that meet proof-of-delivery and invoice format rules.

- Loss definition: unpaid principal only, or principal plus approved fees.

- Claim package: what documents prove delinquency and eligibility.

Overcollateralization as a buffer Overcollateralization means the pool holds more value than the amount funded. It absorbs losses without requiring immediate third-party payment.

Example: 10% overcollateralization

- Pool funds $900 for eligible receivables.

- It holds $100 of additional collateral (cash or highly liquid instruments).

- If $60 of receivables are ultimately uncollectible, the buffer covers it, and the pool remains solvent.

This is especially useful when disputes take time to resolve, because the buffer is available immediately.

Structuring Overcollateralization Mechanics

Overcollateralization needs rules for how it changes over time.

- Initial ratio: set at onboarding based on historical dispute and delinquency rates.

- Dynamic ratio: adjust when credit quality changes or when dispute rates rise.

- Release schedule: specify when excess collateral can be returned.

Example: release schedule tied to dispute aging

- Collateral ratio starts at 12%.

- When disputes on a batch move from “open” to “resolved in favor of the pool,” the pool releases collateral back toward 8%.

- If disputes worsen, the ratio returns to 12%.

This avoids the common failure mode where collateral is released too early, then replenishment becomes urgent and expensive.

Combining Enhancements Without Double Counting

Many programs use both guarantees and overcollateralization. The goal is to prevent overlap that confuses loss recovery.

A clean approach is to define priority of coverage:

- First, use the overcollateralization buffer.

- Then, draw on the guarantee for losses beyond the buffer.

Example: layered coverage

- Overcollateralization covers losses up to $2 million.

- Any additional losses are covered by a guarantee up to $5 million.

- The claim clause states that the guarantor pays only the excess after buffer utilization.

Mind Map: Credit Enhancements Design

Mini Case Study: Dispute Heavy Environment

Assume a pool funds invoices from multiple buyers, and disputes are frequent due to delivery documentation issues.

- The program uses 8% overcollateralization to cover timing gaps.

- It adds a guarantee that triggers when unresolved disputes exceed a defined threshold for a buyer.

- The claim clause requires proof that the invoice met eligibility rules at funding time.

Result: the pool can absorb losses while disputes are processed, and the guarantee prevents the buffer from being drained by repeated documentation failures.

Practical Checklist for Implementation

- Define triggers using measurable events, not vague “credit deterioration.”

- Specify loss calculations and netting rules.

- Set claim documentation requirements that match your operational reality.

- Use layered coverage with explicit priority to avoid conflicting recoveries.

- Maintain ledgers for collateral, funded amounts, and realized losses so governance decisions are auditable.

3.5 Documenting Underwriting Evidence for Audits and Ongoing Monitoring