Private Equity Deal Structuring and Value Creation Essentials

1. Private Equity Value Creation Framework and Deal Lifecycle

1.1 Defining Value Creation Objectives Across Investment Phases

Value creation objectives should be written so they can survive contact with reality: diligence findings, lender questions, and the first month of operating changes. The goal is not to list wishes; it is to define measurable outcomes, the levers that drive them, and the timing of when each lever must start working.

Phase 1: Pre-Close Objectives That Reduce Uncertainty

Before closing, objectives focus on proving the business can generate the cash flow the deal depends on. Start with three categories.

-

Cash flow credibility: confirm that reported earnings convert to cash. A practical objective is “validate working capital behavior so the first 90 days do not drain cash.” For example, if the target has seasonal receivables, set a diligence objective to quantify days sales outstanding by month and tie it to the purchase price working capital target.

-

Risk containment: define what must be true to avoid value leakage. Example: “identify revenue contracts with termination rights tied to customer credit events and quantify exposure.” This turns legal review into a value question.

-

Financing readiness: ensure the capital structure can be serviced under realistic conditions. Example: “stress test debt service coverage under a downside margin scenario and confirm covenant headroom.” If the model shows thin headroom, the objective becomes negotiating covenants or adjusting purchase price mechanics.

Phase 2: Day One to 100-Day Objectives That Stabilize Performance

Early objectives should prevent avoidable damage while you gather operational truth. Write them as “stabilize, measure, and fix the obvious.”

- Stabilize cash: implement a cash collection cadence and approval limits for spending. Example: require weekly accounts receivable aging review and set a threshold for write-offs.

- Stabilize pricing and service: freeze discount authority until margin baselines are revalidated. Example: if sales teams can discount without approval, set a temporary rule that discounts above a defined band require sign-off.

- Stabilize reporting: produce a baseline KPI pack that matches how lenders and the board will monitor performance. Example KPIs: gross margin by product line, backlog coverage, and inventory turns.

These objectives are not about “big transformations.” They are about stopping the business from drifting while you measure what actually drives results.

Phase 3: 6- to 18-Month Objectives That Create Sustainable Improvements

Now the objectives shift from stabilization to improvement programs. Each objective should specify the operational lever, the metric, and the owner.

- Margin expansion: choose one or two drivers you can influence. Example: reduce expedited freight by improving order planning. The objective becomes “cut expedited freight cost as a percent of revenue by X points by month Y,” supported by a planning process change.

- Revenue retention and growth: focus on measurable commercial outcomes. Example: “increase renewal rate for top 50 customers from A% to B% by month Y,” paired with a customer success playbook and contract review cadence.

- Cost structure: target controllable costs with clear baselines. Example: “reduce controllable overhead by X% through procurement renegotiation and staffing plan changes,” with a monthly variance review.

A useful rule: if an objective cannot be tied to a metric that changes within the investment horizon, it belongs in a later phase or should be rewritten.

Phase 4: 18-Month to Exit Objectives That Protect the Sale Story

Exit objectives should make the business easier to diligence and easier to value. They focus on consistency, documentation, and normalization.

- Financial quality: ensure reporting is consistent and adjustments are supportable. Example: maintain a documented policy for one-time costs so EBITDA normalization is not a debate.

- Operational repeatability: prove that improvements are process-based, not hero-based. Example: if margin improved due to a new pricing tool, ensure the tool’s governance and training are documented.

- Customer and contract durability: keep churn and contract terms stable. Example: track renewal pipeline and ensure key contracts are not expiring without a plan.

Mind Map: Value Creation Objectives by Phase

Example: Turning Objectives Into a One-Page Scorecard

For a target with volatile receivables, a coherent objective set might look like this: pre-close validate monthly DSO and set working capital targets; day one implement AR aging and collection cadence; 6- to 18-month reduce DSO by improving dispute resolution; exit maintain consistent cash conversion so buyers do not discount earnings.

The scorecard stays simple: each objective has a metric, a target, a start date, and an owner. If you cannot assign an owner, the objective is probably not ready.

1.2 Mapping the Deal Lifecycle from Sourcing Through Exit

A private equity deal is easiest to manage when you treat it like a pipeline with handoffs, not a single event. The goal of mapping is to make every decision point traceable to a value driver, a financing constraint, and an operational plan.

Lifecycle Stages and What “Done” Means

1) Sourcing and Screening

You start with a thesis and filter targets using a short list of measurable value drivers: cash conversion, pricing power, churn, and cost structure. “Done” here means the team can explain why the business can improve and what would break the case.

2) Initial Diligence and Deal Shaping

Early diligence turns assumptions into questions. You validate revenue quality (recurring vs. one-time), customer concentration, and working-capital behavior. “Done” means you can propose a preliminary purchase price range and a financing approach that fits the likely cash profile.

3) Financing and Structuring

Capital structure is not a math exercise; it’s a constraint system. You align debt sizing with expected free cash flow, covenant headroom, and refinancing risk. “Done” means the model shows debt service coverage under base and downside cases, and the term sheet reflects those outcomes.

4) Definitive Diligence and Documentation

This is where legal terms meet operational reality. You confirm adjustments like working capital targets, normalize earnings, and refine earnout metrics if used. “Done” means the purchase agreement and disclosure schedules match what diligence actually found.

5) Closing and Day One Execution

Closing is a switch from “analysis” to “operations.” You finalize reporting cadence, confirm authority levels, and ensure systems can produce the KPIs used for covenant and management reporting. “Done” means the first operating review can run on time with reliable numbers.

6) Value Creation Execution

Value creation runs on a baseline and a rhythm. You track initiatives by KPI, not by activity, and you link spending to measurable outcomes. “Done” means each initiative has an owner, a timeline, and a metric that moves.

7) Monitoring, Governance, and Risk Control

Governance prevents surprises. You monitor liquidity, covenant compliance, and working capital trends, and you escalate issues with defined thresholds. “Done” means decisions are documented and consistent with the investment plan.

8) Exit Planning and Transaction Readiness

Exit starts long before the sale process. You maintain reporting quality, stabilize customer and employee retention, and keep the business narrative consistent with audited or supportable numbers. “Done” means a buyer can understand performance without hunting for explanations.

Mind Map: the Lifecycle Handoff Logic

Example: One Deal, Many Handoffs

Consider a mid-market manufacturer with 60% of revenue from repeat orders. During screening, the team flags two value drivers: improved gross margin through procurement discipline and better cash conversion by reducing inventory days.

In initial diligence, they discover that inventory spikes before seasonal demand but is funded by customer deposits that are recorded inconsistently across regions. That finding changes the working-capital adjustment approach in the purchase agreement and affects the financing model because cash timing is less stable than it looked.

During definitive diligence, they normalize earnings by separating one-time freight reimbursements from recurring logistics costs. They also define earnout metrics tied to gross margin and customer retention, with dispute-avoidance controls: clear measurement periods, data sources, and audit rights.

At closing, Day One readiness focuses on reporting definitions. If gross margin is calculated differently by plant, the KPI dashboard becomes a guessing game, and covenant monitoring suffers. The team standardizes the calculation and confirms the data feed before the first operating review.

In value creation, procurement initiatives are tracked by realized savings per SKU and by inventory turns, not by the number of supplier meetings. Governance adds a monthly working-capital review with a threshold: if inventory days move beyond a set band, the operating team must present corrective actions.

For exit readiness, the buyer narrative stays consistent: the same KPI definitions used internally are used in buyer materials, and the normalization logic is documented so diligence questions don’t derail the timeline.

Practical Mapping Checklist for the Team

- Every stage has a “done” definition tied to a value driver.

- Every handoff includes: data definitions, decision rights, and escalation triggers.

- Financing assumptions are revisited when operational facts change, not when the calendar forces it.

- Exit readiness is treated as maintaining quality of performance reporting, not just preparing a sale deck.

1.3 Establishing Key Performance Indicators and Value Drivers Before Closing

Before closing, you want two things to be true: (1) the business can be measured consistently, and (2) the measurements connect to the value creation plan you already modeled. Key performance indicators (KPIs) are the scoreboard; value drivers are the levers that move the score. When those two are linked, you can manage execution without guessing.

Foundational Concepts That Prevent KPI Chaos

Start by separating KPIs into three layers.

- Value drivers describe what changes enterprise value: cash generation, growth, margin, and risk.

- Operational KPIs describe what the team can influence day to day: conversion rates, cycle times, defect rates, utilization.

- Financial KPIs translate operations into cash and profitability: gross margin, EBITDA, working capital, and debt service coverage.

A practical rule: every KPI should have an owner, a data source, a refresh frequency, and a clear “so what” statement. If you cannot explain why a KPI matters in one sentence, it probably belongs in a spreadsheet, not in the operating cadence.

Building the Value Driver Map

Use the value driver map to connect strategy to numbers. For a typical acquisition, the value drivers often cluster into four buckets.

- Revenue quality: retention, expansion, and contract terms that protect cash.

- Margin structure: gross margin and controllable cost lines.

- Working capital discipline: inventory turns, receivables aging, and payables timing.

- Risk and compliance: churn risk, warranty exposure, and customer concentration.

Then assign operational KPIs that explain each driver. For example, revenue quality is not just “sales growth.” It is retention rate, win rate, average contract duration, and billing accuracy.

KPI Selection with a Simple Test

Pick KPIs using a three-part test.

- Causality: does the KPI move before the financial outcome?

- Controllability: can management influence it within the planned holding period?

- Measurability: can you collect it reliably from existing systems without heroic effort?

Example: If your model assumes margin expansion, “gross margin” is a financial KPI. The operational KPIs might be product mix, scrap rate, and labor productivity. Those are measurable and actionable.

Data Readiness Before Closing

KPI integrity depends on data definitions. Before closing, confirm that the same metric means the same thing across teams and systems.

- Define terms: what counts as “active customer,” “on-time delivery,” or “recognized revenue.”

- Reconcile sources: compare ERP totals to accounting close numbers for at least two months.

- Document adjustments: if you use adjusted EBITDA, specify which lines are normalized and how often adjustments occur.

A small but effective practice is to run a “metric dry run” using last month’s data. If the KPI dashboard cannot be produced in a day, it will not survive month-end.

Mind Map: Value Drivers and KPI Linkages

Example KPI Set for a Typical Acquisition

Assume the investment thesis is to improve cash conversion and stabilize revenue. A coherent KPI set might look like this.

-

Revenue quality

- Retention rate by cohort (owner: commercial lead, monthly)

- Billing accuracy (owner: finance, monthly)

- Contract exception rate (owner: legal/ops, monthly)

-

Margin structure

- Pricing realization vs. list (owner: sales ops, weekly)

- Scrap and rework rate (owner: operations, weekly)

- Labor productivity (owner: plant/ops, weekly)

-

Working capital discipline

- Receivables aging by bucket (owner: finance, weekly)

- DSO trend (owner: finance, monthly)

- Inventory turns by SKU class (owner: supply chain, monthly)

Each KPI should connect to a value driver in your model. If the model assumes reduced DSO, then receivables aging and collection rate must be tracked with enough granularity to explain variances.

Targets and Thresholds That Match the Model

Targets should be consistent with the financial model, but not identical. Financial models often use annual averages; operational KPIs need interim thresholds.

Use three levels:

- Baseline: the last two months’ average.

- Target: the modeled improvement path.

- Threshold: a point where you trigger action, not a point where you panic.

Example: If receivables aging shows a growing 60–90 day bucket, set a threshold that forces a collection playbook review before the annual cash impact appears in the forecast.

Closing Checklist for KPI Readiness

Before closing, confirm the following are in place:

- KPI definitions are written and agreed.

- Data sources are accessible and reconciled.

- Owners are assigned with decision rights.

- A first-month dashboard can be produced without delays.

- KPI-to-value-driver mapping is documented so the operating team knows what they are moving.

When this is done, the post-close period starts with fewer surprises and more useful conversations. The scoreboard becomes a tool, not a mystery novel.

1.4 Building a Practical Workplan for Diligence Integration and Day One Readiness

A practical workplan turns diligence findings into actions that start on Day One, not “sometime after closing.” The goal is simple: ensure the team can run the business safely, accurately, and consistently from the first week, while the value plan begins immediately.

Foundational Inputs That Drive the Workplan

Start by consolidating four inputs into one operating view:

- Diligence outputs: risks, red flags, and quantified opportunities (for example, margin leakage, customer churn drivers, or working-capital traps).

- Deal terms and constraints: covenants, purchase price adjustments, earnout mechanics, and any closing conditions that affect operations.

- Value creation plan: the specific initiatives assumed in the model, with owners and target dates.

- Operating reality: current systems, reporting cadence, key roles, and where decisions actually get made.

A useful rule is to map every diligence finding to one of three buckets: fix before close, prepare for Day One, or manage after close. If a finding lands in “after close” but is critical to cash flow or compliance, it probably belongs in “prepare for Day One.”

Workplan Structure from Close to Day One

Build the workplan as a timeline with deliverables, not a list of tasks. A clean structure is:

- T-60 to T-30 days: finalize integration scope, confirm data access, and draft Day One operating procedures.

- T-30 to T-10 days: validate assumptions with management, run dry-runs for reporting and controls, and lock the KPI definitions.

- T-10 to Close: complete system access, confirm staffing coverage, and ensure legal and finance processes are ready.

- Day One to Day 30: execute the first operating cycle, track issues, and stabilize reporting.

Use a single “source of truth” tracker with columns for: initiative, diligence link, owner, dependencies, required artifacts, and acceptance criteria. Acceptance criteria prevent the classic problem where everyone agrees something is “in progress,” but nothing is actually usable.

Mind Map: Diligence Integration to Day One Readiness

Core Workstreams and What “Done” Looks Like

A workplan works best when it has a small set of workstreams with concrete deliverables.

-

Finance and Reporting Readiness

- Deliverables: KPI definitions, monthly close checklist, and a cash forecast template.

- Example: if diligence shows working capital volatility, define the exact inputs for the forecast (DSO, DPO, inventory turns) and set a weekly check-in during the first month.

-

Commercial and Customer Continuity

- Deliverables: pricing approval workflow, contract repository, and churn-risk customer list.

- Example: if contract terms vary by customer, Day One should include a rule for approvals so sales can quote without accidentally breaking discount or rebate constraints.

-

Operations and Controls

- Deliverables: standard operating procedures for purchasing, inventory counts, and quality checks.

- Example: if diligence flags inventory shrink, Day One should specify who signs off on cycle counts and how variances are investigated.

-

Legal, Compliance, and Contractual Mechanics

- Deliverables: covenant tracker, disclosure schedule owner list, and earnout metric governance.

- Example: for an earnout tied to revenue, define the revenue recognition basis and the dispute-resolution path before closing so the first measurement period is not a negotiation.

-

People and Decision Rights

- Deliverables: org chart, decision-rights matrix, and escalation rules.

- Example: if the CFO role is changing, assign a temporary “close owner” for the first month so the reporting cadence doesn’t slip.

Integrated Example: From Finding to Day One Action

Assume diligence identifies that month-end reporting is delayed by two weeks and that cash collections are tracked inconsistently.

- T-30 to T-10: finance creates a single collections tracker and defines aging buckets.

- T-10 to Close: IT grants access to the tracker and AP/AR exports; the close checklist is tested with last month’s data.

- Day One: the first weekly cash meeting uses the new tracker; exceptions are logged with owners.

- Day 30: the team compares actual collections to forecast and updates the working-capital assumptions used in the value model.

This is not “reporting for reporting’s sake.” It directly supports covenant monitoring and reduces the chance that value assumptions are based on stale information.

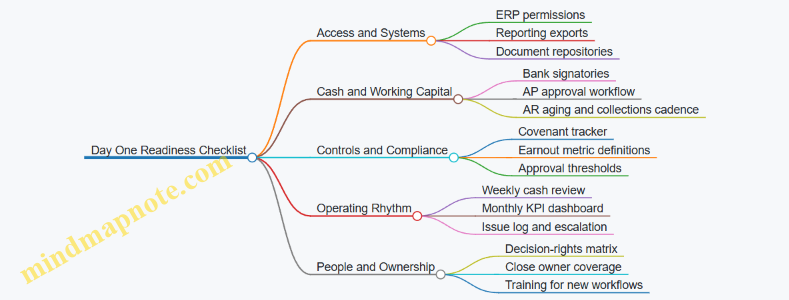

Mind Map: Day One Readiness Checklist

Practical Governance and Cadence

Set a meeting rhythm that matches the work:

- Twice weekly during T-30 to T-10: integration leads review blockers and confirm deliverables.

- Weekly during T-10 to Close: legal, finance, and commercial confirm readiness for the next milestone.

- First two weeks after close: daily standups for issues that affect cash, reporting, or customer continuity.

A simple acceptance test for each deliverable is: “Could a new person use this on Day One without asking the original author?” If the answer is no, the work is not ready.

Date Anchor for Planning

Use a planning anchor such as April 15 as the midpoint for T-30 activities, so teams can schedule dry-runs, access requests, and sign-offs without last-minute scrambling.

1.5 Aligning Stakeholders on Governance Reporting and Decision Rights

A deal’s early months can feel like a group project where everyone has a different definition of “done.” Governance reporting and decision rights fix that by making three things explicit: who decides, what they decide, and how information flows to support those decisions.

Foundational Concepts That Prevent Confusion

Start with decision rights. A simple rule works well: decisions that affect cash, risk, or performance get explicit owners. Everything else can be advisory.

Next comes governance reporting. Reporting is not “more dashboards.” It is a repeatable rhythm of facts that match the decisions being made. If the board reviews covenant risk monthly, the report must include covenant headroom and the actions underway to protect it.

Finally, define escalation. Escalation is the bridge between “we noticed” and “we acted.” Without it, issues become polite emails. With it, issues become tasks with owners and deadlines.

A Practical Governance Model for Private Equity

Use a three-layer structure.

- Board and investor governance: sets priorities, approves major actions, and monitors value creation progress.

- Management governance: runs the operating plan, manages tradeoffs, and proposes actions.

- Functional working groups: handle deep dives like pricing, procurement, or integration workstreams.

A useful starting point is a decision matrix. For each decision type, specify the approver, required inputs, and the threshold that triggers approval.

Decision Matrix Example

- Budget changes above 5%: Board approval; inputs include updated forecast, variance explanation, and cash impact.

- New debt draw or refinancing: Investor committee approval; inputs include lender term sheet, covenant impact, and liquidity forecast.

- Hiring replacement for a critical role: Management approval; inputs include role scope, cost, and timeline.

- Customer contract concessions beyond standard terms: Management approval with legal review; inputs include margin impact and churn risk assessment.

This keeps the board from micromanaging while ensuring material decisions do not slip through.

Reporting Rhythm That Matches Decision Needs

A clean reporting cadence reduces meeting time and increases action quality.

- Weekly: cash position, collections status, top operational blockers, and progress on critical workstreams.

- Monthly: KPI dashboard, variance analysis versus plan, covenant headroom, and a short “what we changed” section.

- Quarterly: re-forecast, integration or improvement progress review, and updated risk register.

The “what we changed” section matters because it turns reporting into decision support. If performance is off track, the report should state the specific corrective actions, not just the gap.

Mind Map: Governance Reporting and Decision Rights

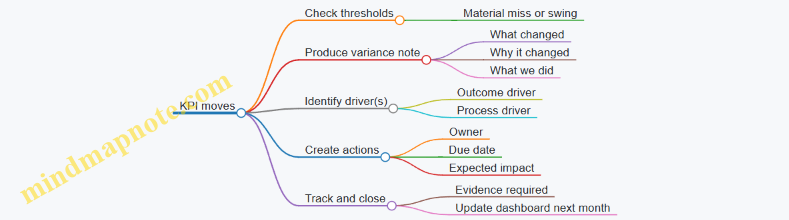

Example: Turning a KPI Miss Into a Governed Decision

Assume gross margin is trending below plan for two consecutive months.

- Management identifies the driver: a pricing discount pattern and higher freight costs.

- Reporting flags the threshold: the margin shortfall exceeds the agreed variance band.

- Escalation triggers: the CFO requests approval for a pricing policy change and a procurement renegotiation.

- Decision rights determine the approver: pricing policy beyond standard terms requires legal review and management approval; a procurement commitment above the cap requires board approval.

- Documentation is consistent: the board packet includes the margin bridge, cash impact, and timeline to implement.

The result is not just “a decision.” It is a decision with traceable inputs, clear ownership, and a timeline that can be monitored.

Example: Avoiding Covenant Surprise

Covenant headroom is often treated as a finance-only topic. Governance makes it everyone’s problem.

- Weekly reporting includes a simple covenant tracker with the latest forecast.

- The working group responsible for collections owns the action plan when headroom tightens.

- Escalation occurs when the forecast indicates a breach risk within the next reporting period.

This prevents the classic scenario where the first warning arrives in the same month the covenant is tested.

Implementation Checklist for Day One Readiness

- Confirm decision rights for cash, financing, capex, pricing concessions, and integration scope.

- Publish a one-page reporting calendar with owners and required metrics.

- Define escalation triggers and the exact information needed for approval requests.

- Run a first governance cycle using real data from the first month post-close.

When governance is designed this way, stakeholders spend less time arguing about what happened and more time deciding what to do next.

2. Target Screening and Diligence Planning for Structuring Decisions

2.1 Translating Investment Thesis Into Diligence Workstreams

An investment thesis is a promise about how value will be created, not a list of hopes. Diligence workstreams translate that promise into specific questions, evidence requests, and decision checkpoints. If you do it well, the diligence plan becomes a map from “what we believe” to “what we can prove.”

Start with Thesis Claims You Can Test

Write the thesis as 3–6 testable claims. Each claim should point to a measurable driver and a mechanism.

-

Claim example: “Margin expands because pricing discipline improves and costs stabilize.”

- Mechanism: pricing governance + reduced discount leakage + procurement renegotiation.

- Evidence you need: historical discount rates, quote approval workflows, supplier spend breakdown, and cost variance drivers.

-

Claim example: “Cash conversion improves because working capital is managed tightly.”

- Mechanism: tighter credit terms for new customers, faster invoice resolution, inventory turns improvement.

- Evidence you need: DSO, aging buckets, dispute rates, inventory aging, and replenishment policies.

This step prevents a common failure mode: diligence that collects data but cannot confirm or refute the thesis.

Convert Claims Into Workstreams

Group thesis claims into workstreams that match how the business actually runs. A practical set usually includes Commercial, Operations, Finance, Legal/Tax, People, and Integration/Exit readiness. Each workstream should have a purpose, key questions, and deliverables.

Commercial workstream focuses on revenue quality and retention mechanics.

- Key questions: Which customers drive revenue and margin? How stable are contracts? Where does revenue leakage occur?

- Deliverables: customer cohort retention view, contract term summary, pricing/discount governance assessment.

Operations workstream focuses on cost structure and execution capability.

- Key questions: What drives unit costs? Are there bottlenecks or quality issues? How repeatable are processes?

- Deliverables: process map of the main value chain, cost driver model, capacity and throughput constraints.

Finance workstream focuses on cash flow reality and accounting normalization.

- Key questions: What is recurring versus one-time? How reliable are forecasts? How does working capital behave in stress?

- Deliverables: quality of earnings memo, cash conversion bridge, covenant-relevant cash flow forecast.

Legal/Tax workstream focuses on risk that can break the plan.

- Key questions: Are there contract clauses that limit operational changes? Are there disputes, liens, or tax exposures?

- Deliverables: risk register with severity and remediation paths.

People workstream focuses on whether the operating plan has operators.

- Key questions: Who owns the processes behind the thesis? What is turnover risk? Are incentives aligned?

- Deliverables: org capability assessment, retention risk map, incentive gap analysis.

Define Evidence Standards and Decision Gates

Each workstream needs an evidence standard: what “good enough” looks like. For example, if the thesis depends on pricing discipline, you should not accept “we try to be consistent” as evidence.

Use decision gates to avoid late-stage surprises. Typical gates:

- Thesis validation gate after initial data review.

- Model confirmation gate after normalization and driver mapping.

- Risk resolution gate before final financing and purchase terms.

At each gate, require a short output: “What we believe,” “What we found,” “What changed,” and “What we need next.” Keep it crisp so the team can act.

Mind Map: Thesis to Diligence Workstreams

Example: Pricing-Led Margin Expansion Thesis

Suppose the thesis claims margin improves through pricing discipline and reduced discount leakage.

Commercial diligence tasks

- Request quote logs for the last 12–24 months.

- Compare quoted price vs. realized price by customer segment.

- Identify discount approval thresholds and exceptions.

Operations diligence tasks

- Confirm whether cost-to-serve varies by customer segment.

- Map how changes in pricing affect production planning and service levels.

Finance diligence tasks

- Normalize revenue recognition if discounts are tied to rebates or credits.

- Build a bridge from realized margin to cash margin after working capital impacts.

Legal diligence tasks

- Review contract clauses that restrict price changes or require notice periods.

People diligence tasks

- Identify who currently approves discounts and whether that role is stable.

Decision gate output

- If quote logs show realized pricing drift and approval controls are weak, the thesis is supported and the operating plan can specify governance changes.

- If realized pricing is stable but margin still varies, the thesis mechanism is wrong; you pivot to cost drivers instead of forcing pricing as the explanation.

This is the core discipline: diligence workstreams should be traceable to thesis claims, and each claim should have a clear path from evidence to decision.

2.2 Designing a Data Room Plan for Commercial Financial and Operational Inputs

A data room plan is a checklist with a purpose: it helps you collect the right evidence, in the right format, at the right time—so diligence doesn’t turn into a scavenger hunt. The goal is not volume; it’s traceability from commercial reality to financial results to operational drivers.

Step 1: Define the Questions the Data Room Must Answer

Start by writing diligence questions in plain language, then map each question to documents and owners. For example:

- “What drives revenue each month?” maps to customer contracts, pricing schedules, and billing reports.

- “Why did margins move?” maps to cost rollups, labor hours, supplier terms, and variance explanations.

- “Can the business deliver the forecast?” maps to capacity plans, lead times, quality metrics, and backlog.

A practical rule: every diligence workstream should have 5–10 questions. If you have 40 questions, you’ll drown in files.

Step 2: Organize the Room by Workstreams and Evidence Type

Use a consistent folder structure so reviewers can find things without asking. A common structure is:

- Commercial

- Financial

- Operational

- Legal and Tax (only if needed for this section)

- Management and Reporting

Within each workstream, split by evidence type:

- Contracts and policies

- Reports and dashboards

- Source data exports

- Support for adjustments and reconciliations

This structure reduces the “which version is correct?” problem when multiple teams work in parallel.

Step 3: Build a Document Inventory with Ownership and Freshness

For each item, record:

- Document name and system of origin

- Owner (who can answer questions)

- Frequency (monthly, quarterly, ad hoc)

- Last updated date

- Coverage period (for example, 24 months)

If a document is updated irregularly, include the last update date and explain the gap in a short note. For example, “Pricing exceptions report last updated 2024-04-15; exceptions are tracked in CRM and exported quarterly.” Use a date like 2024-04-15 rather than today.

Step 4: Specify the Minimum Commercial Inputs

Commercial diligence should connect customer behavior to revenue recognition and cash collection.

Include:

- Customer list by segment with contract start/end dates

- Pricing terms and discounting policy

- Top customers’ contracts and amendments

- Billing history by customer and invoice aging

- Revenue bridge from bookings to recognized revenue

- Churn and retention metrics with definitions

Example: If revenue is recognized over time, provide a schedule showing contract value, performance milestones, and recognized revenue by month. Then provide the billing report so the team can compare “what was billed” versus “what was recognized.”

Step 5: Specify the Minimum Financial Inputs

Financial diligence should support the adjusted EBITDA story and cash flow mechanics.

Include:

- Trial balance and general ledger exports

- Monthly P&L by cost center

- Balance sheet detail for working capital accounts

- Bank statements and debt schedules (if relevant)

- Reconciliation of reported to adjusted EBITDA

- Revenue and cost allocation methodology

Example: For working capital, provide a reconciliation of AR aging to the GL balance and explain any recurring adjustments. If AR includes disputed invoices, include the dispute log and resolution status.

Step 6: Specify the Minimum Operational Inputs

Operational diligence should show how the business produces the output that commercial teams sell.

Include:

- Production or service delivery process maps

- Capacity and utilization reports

- Quality metrics and defect or rework logs

- Inventory policy and inventory movement reports

- Procurement terms and supplier performance

- Staffing model with headcount, hours, and productivity measures

Example: If labor is a major cost driver, include a monthly labor hours report by role and a productivity metric (for example, units per labor hour). Then include a variance explanation template used internally so you can see how management already thinks about drivers.

Step 7: Add a “How to Read This” Layer

A data room without context creates endless questions. Add short readme documents:

- Definitions of metrics (churn, retention, backlog, utilization)

- Chart of accounts mapping

- Revenue recognition summary and key assumptions

- Adjustment policy for one-time items

Keep these to a few pages each. If a readme is longer than the document it explains, it’s not helping.

Step 8: Plan Q&A and Version Control

Set rules:

- Questions must reference folder paths and document names

- Answers must cite the document version used

- Updated files must be labeled with version numbers

A simple approach is to maintain a “Diligence Questions Log” spreadsheet with columns for question, workstream, document reference, status, and owner.

Mind Map: Data Room Plan for Commercial Financial and Operational Inputs

Example: A Minimal Yet Complete Commercial Folder Set

If you need a starting point, include these folders for each of the last 24 months:

- Customer contracts and amendments

- Pricing and discount policy

- Billing by customer and invoice aging

- Revenue bridge and recognition schedule

- Churn and retention report with definitions

Then add one “supporting export” folder that contains the raw extracts behind each report. Reviewers can trust the report, and they can reproduce it when something doesn’t match.

Example: Reconciling Revenue to Cash Without Guesswork

When revenue is recognized differently than cash is collected, provide:

- Monthly recognized revenue by customer

- Monthly cash receipts by customer

- AR aging by month

- A reconciliation note explaining timing differences

If a timing difference is driven by contract terms, point to the relevant clause in the contract folder. That single link can save hours of back-and-forth.

2.3 Assessing Quality of Earnings and Adjusted EBITDA Methodology

Quality of Earnings (QoE) is the discipline of asking, “How much of reported earnings is real, repeatable, and cash-supported?” In private equity deal structuring, this matters because purchase price, leverage capacity, and covenant headroom often hinge on Adjusted EBITDA. If the adjustment story is sloppy, the financing story will be too.

Foundational Concepts That Drive QoE

Start with the bridge from reported earnings to Adjusted EBITDA. Reported EBITDA is not a single number in the real world; it’s a moving target shaped by accounting policies, one-time items, and management judgment. QoE therefore focuses on three questions:

-

Is the underlying operating performance sustainable? Example: A company reports strong EBITDA after reversing an accrual. The reversal boosts earnings, but the cash reality is unchanged. QoE flags the reversal as non-recurring and checks whether the accrual was properly supported.

-

Do adjustments reflect economic reality, not accounting convenience? Example: “One-time consulting” that repeats every quarter is not one-time. QoE tests whether the spend is tied to ongoing projects or recurring functions.

-

Does Adjusted EBITDA correlate with cash generation? Example: EBITDA rises while operating cash flow falls due to working capital build. QoE examines whether the working capital movement is structural (e.g., longer receivable terms) or temporary.

The QoE Workflow from Evidence to Adjustments

A systematic QoE process prevents the common failure mode: building a persuasive adjustment list before verifying the facts.

Step 1: Normalize the Income Statement

Reconcile reported results to management’s “adjusted” version using a documented bridge.

- Identify recurring line items that are often adjusted (e.g., management fees, rent, stock-based compensation).

- Confirm whether the company’s accounting policies are consistent across periods.

Easy example: If depreciation is adjusted upward because “maintenance capex is higher than reported,” QoE checks capex invoices and asset lives rather than accepting the narrative.

Step 2: Validate Each Adjustment Category

Treat adjustments like evidence-based claims.

- One-time items: Obtain support for the event (contract termination, severance plan, litigation settlement).

- Non-operating items: Separate financing effects, taxes, and unusual gains/losses from core operations.

- Non-cash items: Confirm stock-based compensation and non-cash charges are correctly classified.

- Run-rate adjustments: Only apply if you can show the change has already occurred and is measurable.

Easy example: A company adjusts for “customer churn impact” after a pricing change. QoE verifies churn data before and after the change and checks whether the adjustment period matches the actual timing.

Step 3: Test Cash Conversion and Working Capital

Adjusted EBITDA is an earnings metric; lenders and investors care about cash.

- Compare EBITDA to operating cash flow over multiple periods.

- Analyze working capital drivers: receivables aging, inventory turns, and payables terms.

Easy example: If Adjusted EBITDA is stable but cash drops, QoE checks whether revenue recognition is front-loaded (e.g., bill-and-hold) or whether collections are slipping.

Step 4: Assess Revenue Quality and Margin Integrity

QoE should include revenue and gross margin checks because EBITDA can look fine while revenue quality deteriorates.

- Review customer concentration and contract terms.

- Inspect returns, credits, and allowances.

- Validate whether gross margin changes are explained by product mix, pricing, or cost inflation.

Easy example: A company “adjusts out” higher freight costs as non-recurring. QoE checks freight invoices and whether the cost increase is tied to ongoing logistics changes.

Adjusted EBITDA Methodology That Holds Up Under Scrutiny

A robust Adjusted EBITDA methodology uses consistent definitions and clear rules.

Define the Baseline

- Start from reported EBITDA (or operating income plus D&A, depending on the company’s reporting).

- Ensure the starting point is consistent across periods.

Use a Controlled Adjustment Policy

Create categories with rules:

- Allowed adjustments: clearly evidenced, truly non-recurring, and supported by documentation.

- Conditioned adjustments: require a run-rate justification (e.g., a new pricing model already in effect).

- Disallowed adjustments: recurring costs disguised as one-time.

Easy example: “Restructuring” is allowed only if it is tied to a defined plan with end dates and measurable severance/contract costs.

Document the Bridge and Ownership

For each adjustment, capture:

- rationale,

- period(s) affected,

- documentation,

- whether it is recurring or non-recurring,

- impact on cash (if relevant).

Mind Map: QoE and Adjusted EBITDA Logic

Example: Building a Credible Adjustment Bridge

Assume reported EBITDA is $10.0m. Management proposes $1.2m of adjustments.

- $0.6m severance from a documented restructuring plan with end dates.

- $0.3m legal settlement tied to a specific dispute.

- $0.2m “consulting” that is actually recurring project support with invoices every quarter.

- $0.1m stock-based compensation.

A QoE-driven outcome:

- Keep severance and legal settlement as allowed.

- Reclassify the recurring consulting as disallowed (or treat as a reforecasted baseline cost rather than an adjustment).

- Keep stock-based compensation as non-cash if consistently treated.

Result: Adjusted EBITDA becomes $10.0m + $0.6m + $0.3m + $0.1m = $11.0m, not $11.2m. That difference is small in this example, but it’s exactly the kind of gap that can matter for leverage and covenant calculations.

Practical Output for Deal Structuring

The deliverable is not just a revised EBITDA number. It’s a defensible bridge with categories, evidence, and cash checks. When the financing model uses Adjusted EBITDA, it should reference the same definitions and adjustment policy so the lender and investment committee are evaluating the same story.

2.4 Evaluating Customer Revenue Mix and Contract Terms for Cash Flow Visibility

Cash flow visibility starts with two questions: who pays, and when they pay. Revenue mix answers “who,” while contract terms answer “when.” Together they determine how predictable collections are, how much cash is tied up in receivables, and how sensitive cash is to churn, disputes, and billing mechanics.

Revenue Mix Foundations That Affect Cash

Start by classifying revenue into buckets that behave differently in cash collection.

- Recurring vs. transactional: Subscription-like revenue usually bills on a schedule; transactional revenue often follows project milestones or usage.

- Contracted vs. uncommitted: Contracted revenue has defined pricing and billing rules; uncommitted revenue may be subject to renewals, rate changes, or customer behavior.

- Concentration by customer and segment: A small number of customers can dominate collections timing. If one customer pays late, the cash forecast moves.

- Revenue by payment pattern: Some customers pay net 30, others net 60 or require approvals. Even with the same revenue amount, cash timing differs.

A simple check: compute weighted average days sales outstanding (DSO) using each customer’s payment terms and actual historical payment behavior. If DSO is drifting upward, revenue recognition may look fine while cash quietly deteriorates.

Contract Terms That Drive Timing and Collectability

Contract terms determine whether revenue is “collectible” in practice, not just “recognized” in accounting.

- Payment terms: Net days, invoicing triggers, and whether invoices require acceptance. Example: a contract that invoices only after customer acceptance can create a two-step delay.

- Billing cadence: Monthly in advance, monthly in arrears, milestone-based, or usage-based. Example: usage-based billing can lag actual consumption, especially if metering or reporting is monthly.

- Price protection and indexation: Rate changes can cause disputes or delayed approvals. Example: if pricing updates require customer sign-off, collections may pause until paperwork is complete.

- Dispute and credit provisions: Look for clauses that allow deductions, credits, or withholding. Example: if customers can withhold 10% for “service quality” without a defined cure process, cash becomes less certain.

- Termination and renewal mechanics: Early termination rights, notice periods, and renewal timing affect churn risk. Example: a 90-day notice requirement can reduce sudden cash drops, but only if the company has strong renewal execution.

- Service level and remedies: Credits tied to performance can be predictable if measurement is clear; they are unpredictable if measurement is ambiguous.

Building a Cash Flow Visibility View from Contracts

Create a collections map that links each revenue bucket to cash timing.

- Inventory contract types: list the main contract templates and any major customer-specific deviations.

- Extract billing triggers: define what starts invoicing and what stops it.

- Assign expected collection lags: use historical payment data by customer and contract type.

- Model deductions and disputes: estimate expected net collections after typical credits or chargebacks.

- Stress the weak links: focus on customers with long payment terms, high dispute rates, or complex acceptance procedures.

A practical example: suppose 40% of revenue is milestone-based with invoices issued at delivery, but acceptance takes 45 days on average. Even if accounting recognizes revenue upon delivery, cash may arrive closer to 75–90 days after delivery depending on net terms. Your forecast should reflect that gap.

Mind Map: Revenue Mix to Cash Outcomes

Example: Two Contracts, Same Revenue, Different Cash

Consider a software services company with $10M annual revenue.

- Contract A: monthly in arrears, net 30, acceptance is automatic, credits limited to documented SLA misses.

- Contract B: quarterly milestones, net 60, customer acceptance required, credits can be applied for “ongoing issues” with broad discretion.

Even if both contracts recognize revenue similarly, Contract B will likely produce higher receivables balances and more variability in collections. In a forecast, you would reflect longer invoicing-to-cash timing for B and apply a higher expected deduction rate based on historical disputes.

Example: Turning Contract Language into Forecast Inputs

When reviewing a contract, convert clauses into measurable forecast assumptions.

- “Invoices are issued after customer acceptance” becomes acceptance lag days.

- “Customer may withhold amounts for disputes” becomes expected withholding percentage and dispute resolution timing.

- “Credits apply for service level failures” becomes credit frequency and credit magnitude.

If the contract does not define measurement or cure steps, treat the related cash impact as uncertain and rely on historical outcomes from similar customers. The goal is not perfection; it’s a forecast that reflects how cash actually moves.

2.5 Identifying Key Risks That Affect Purchase Price Allocation and Financing

Purchase price allocation (PPA) and financing are tightly connected: the way you assign value to assets and liabilities changes taxable income, future depreciation and amortization, and sometimes the cash flows that lenders rely on. The goal in diligence is not to list every possible risk, but to identify the few that can materially change (1) the PPA outcome, (2) the debt capacity, or (3) the post-close cash available for debt service.

Foundational Risk Categories That Drive PPA and Financing

Start with the risks that sit closest to the accounting mechanics.

-

Valuation input risk: If the purchase price is allocated using weak or inconsistent inputs, the resulting asset values can swing. Example: a customer list valued using outdated churn assumptions can lead to an overstatement of intangible assets, which then changes amortization expense and affects lender-focused cash flow metrics.

-

Classification risk: Some items are easy to misclassify between goodwill, identifiable intangibles, and assumed liabilities. Example: a long-term service contract that is actually transferable and separable may be treated as goodwill if diligence fails to document transferability and customer-specific economics.

-

Measurement risk: PPA requires estimates for useful lives, impairment indicators, and the timing of cash flows. Example: if you assume a 10-year useful life for a technology intangible but the underlying contracts and staffing model support only 5 years, amortization will be understated in the early years.

-

Liability completeness risk: Understated liabilities can inflate equity value and distort both PPA and financing. Example: an unrecorded warranty reserve can reduce future cash, lowering debt service coverage and increasing covenant pressure.

-

Working capital and cash conversion risk: Financing models often assume a working capital target. If the target is wrong because of hidden receivables quality issues, the first months after close can be cash-draining. Example: receivables include a large portion of disputed invoices; the seller may show “current” balances, but collections lag and the buyer funds the gap.

Risk Mapping to PPA Outcomes

Use a simple logic chain: risk → accounting estimate → PPA line item → cash flow impact → financing impact.

- Customer-related risk (churn, contract terms, transferability) can change the valuation of customer relationships and thus amortization.

- Technology-related risk (roadmap feasibility, IP ownership, staffing continuity) can change the valuation and useful life of developed technology.

- Brand-related risk (market evidence, trademark ownership, marketing spend sustainability) can shift value between goodwill and identifiable intangibles.

- Contingent liability risk (litigation, tax exposures, environmental matters) can change assumed liabilities and reduce purchase price allocation to assets.

A practical diligence habit: for each risk, document the specific evidence you will use to support the estimate. If the evidence is thin, treat the risk as material until you can strengthen it or adjust the financing assumptions.

Risk Mapping to Financing Constraints

Lenders care about cash generation and downside protection. Identify risks that can change cash flow timing or covenant headroom.

- Debt capacity risk: If EBITDA is adjusted for one-time items incorrectly, debt capacity can be overstated. Example: “one-time” legal costs recur annually due to a recurring compliance issue.

- Covenant risk: If amortization and interest are modeled inconsistently with the expected PPA, covenant calculations can be off. Example: a higher intangible valuation increases amortization, lowering EBITDA-based covenants depending on the covenant definition.

- Liquidity risk: If working capital is not truly normal, the buyer may need additional cash to fund operations. Example: inventory turns are slower than reported because of obsolete stock hidden in “finished goods.”

Mind Map: Of Key Risks and Their Effects

Concrete Examples of Risk Identification in Diligence

Example 1: Customer relationships misvaluation

- Observation: churn is reported as “industry average,” but the company’s top 20 customers are on different contract terms.

- Risk: classification and valuation input risk.

- Diligence action: reconcile churn by cohort and contract type; confirm whether contracts are transferable or dependent on the seller’s relationships.

- Financing effect: if customer intangibles are overstated, amortization may be higher than modeled, and covenant headroom can shrink.

Example 2: Warranty reserve understatement

- Observation: warranty expense is low relative to peers, but returns data shows a lag.

- Risk: liability completeness and working capital risk.

- Diligence action: test returns and warranty claims after period end; review historical claim development.

- Financing effect: cash shortfalls can force covenant waivers or additional equity funding.

Example 3: Working capital target mismatch

- Observation: the seller proposes a working capital target based on “average” balances.

- Risk: cash conversion risk.

- Diligence action: normalize receivables aging, identify disputed invoices, and separate seasonal inventory.

- Financing effect: the buyer’s first-quarter cash flow can miss lender thresholds even if long-run EBITDA looks fine.

A Systematic Diligence Workflow to Keep Risks Actionable

- List estimates that feed PPA: intangibles, useful lives, contingent liabilities, and working capital true-ups.

- Attach evidence to each estimate: contracts, IP registrations, claim development, aging reports, and board minutes.

- Quantify sensitivity where it matters: focus on risks that change amortization, assumed liabilities, or cash conversion.

- Translate to financing impacts: map each quantified risk to covenant definitions, debt capacity, and liquidity buffers.

- Decide how to manage: strengthen diligence evidence, adjust purchase price mechanics, or revise financing assumptions and protections.

When this workflow is followed, the risk list stops being a spreadsheet of worries and becomes a set of decisions that directly shape both PPA outcomes and the financing plan.

3. Acquisition Financing Fundamentals and Capital Structure Design

3.1 Choosing the Acquisition Capital Stack and Understanding Its Tradeoffs

A capital stack is the order of who gets paid first, second, and last when cash comes in or the business runs into trouble. In an acquisition, the stack typically combines equity, senior secured debt, and sometimes mezzanine or preferred equity. The choice is not just about “how much debt” but about how risk and control are allocated across parties.

Core Building Blocks

Equity is the residual claim. If the business performs, equity captures upside; if it underperforms, equity absorbs losses first. Equity is flexible on timing, but it is expensive in return terms because lenders will not take the same risk.

Senior secured debt is paid before other claims and is usually backed by collateral. It tends to have lower interest rates than riskier layers, but it comes with covenants and limits on actions like additional borrowing, dividend payments, and sometimes asset sales.

Mezzanine debt or preferred equity sits between senior debt and common equity. It often carries higher interest or preferred return and may include equity-like features such as warrants or conversion rights. It can reduce the amount of common equity needed, but it increases fixed obligations and can tighten operating flexibility.

Tradeoffs That Actually Matter

-

Cash flow sensitivity: Fixed payments (interest, preferred returns, amortization) reduce the room for operational swings. A stack with heavy fixed obligations can still work, but the model must show coverage under realistic downside assumptions.

-

Covenants and operational constraints: Senior debt covenants can force management to act early—sometimes before the business is ready. For example, a covenant tied to leverage may trigger if EBITDA dips due to one-time costs or customer churn.

-

Priority in distress: In a downside scenario, the stack determines who takes the hit. If lenders have strong security and enforcement rights, equity may be effectively “out of the game” even before a formal default.

-

Flexibility for value creation: Operational improvement often requires spending and timing. If the stack restricts capex, working capital movements, or acquisitions, the plan can stall.

-

Negotiation leverage: More senior debt can mean more lender involvement in reporting and approvals. That can be helpful for discipline, but it can also slow decisions.

A Systematic Selection Process

Start with the business’s cash generation profile. Then match it to the payment profile of each layer.

- If cash flows are stable and predictable, senior secured debt can be the workhorse layer.

- If cash flows are lumpy due to seasonality or project-based revenue, the stack should include more flexibility, such as interest-only periods, longer maturities, or a smaller fixed-payment burden.

- If the acquisition requires near-term investment to realize synergies, avoid a stack that forces immediate deleveraging at the expense of execution.

Next, test the stack against covenant mechanics. A common mistake is modeling only interest coverage while ignoring leverage covenants and liquidity requirements. For instance, a company might cover interest comfortably but still breach a leverage threshold after working capital absorbs cash.

Finally, align the stack with the value creation plan. If the plan depends on reducing working capital, the stack should not punish the period when cash is temporarily tied up. If the plan depends on margin expansion, the stack should tolerate the ramp period.

Mind Map: Capital Stack Components and Tradeoffs

Example: Choosing Between Two Stacks

Consider a target with EBITDA of $50 million and expected annual free cash flow conversion of 70% after normalization. Two financing options are on the table.

Stack A uses more senior secured debt and less equity. The interest rate is lower, but the leverage covenant is tight: it requires leverage below a set threshold each quarter. During the first year, the operating plan includes inventory reduction and pricing resets. Inventory reduction can temporarily increase cash needs, and pricing resets can delay margin improvement. The model shows interest coverage stays above 2.5x, but leverage breaches in Q3 due to EBITDA normalization timing.

Stack B uses less senior debt and more mezzanine or equity. The fixed return is higher, but the covenant headroom is wider and liquidity buffers are larger. The same operating plan now fits the covenant calendar because the business has time to complete the pricing and cost initiatives before leverage tightens.

The point is not that one stack is “better.” Stack A can be attractive when execution is fast and cash conversion is reliable. Stack B can be safer when timing matters more than headline cost of capital.

Practical Checklist for the Deal Team

- Confirm which covenants exist and when they are tested.

- Map each value creation initiative to the months it affects cash flow.

- Ensure the model includes working capital timing, not just EBITDA.

- Check whether the stack restricts actions needed for execution.

- Verify that the lender reporting package matches the operating cadence.

A well-chosen stack is the one that keeps the business running while the plan runs its course. If the stack forces management to manage the covenant instead of the business, it will eventually cost more than it saves.

3.2 Modeling Debt Capacity Using Cash Flow and Covenant Constraints

Debt capacity is the amount of borrowing a business can support while staying within lender rules and still paying for day-to-day operations. In practice, you model it by combining (1) cash flow available for debt service and (2) covenant headroom, then translating both into a maximum sustainable debt level.

Step 1: Start with Cash Flow That Actually Pays Debt

Use a cash flow view, not just earnings. A simple starting point is:

- EBITDA (or operating cash proxy)

- Less cash taxes (based on normalized earnings and tax structure)

- Less maintenance capital expenditures (the “keep the lights on” number)

- Less required working capital investment (inventory, receivables, payables)

- Equals cash available for debt service (before interest and principal)

Easy example: Suppose a target generates $20.0m EBITDA. Normalized cash taxes are $3.0m, maintenance capex is $2.0m, and working capital consumes $1.5m per year. Cash available for debt service is $20.0m − $3.0m − $2.0m − $1.5m = $13.5m.

This $13.5m is the pool you test against interest-only and amortization requirements. If your model assumes aggressive working capital releases or underestimates maintenance capex, you’ll overstate capacity. Lenders tend to notice when cash flow assumptions are “creative.”

Step 2: Translate Cash Flow Into Debt Service Coverage

Most deals use one or more coverage ratios. Common ones include:

- Interest Coverage: EBITDA or operating cash divided by interest expense

- Debt Service Coverage: cash available for debt service divided by total debt service (interest + scheduled principal)

A practical approach is to model debt service explicitly:

- Interest expense = opening debt × interest rate (with any hedges modeled)

- Scheduled principal = amortization schedule

- Total debt service = interest + principal

Then compute coverage:

- Debt Service Coverage = cash available for debt service ÷ total debt service

Easy example: If cash available for debt service is $13.5m and total debt service is $10.0m, coverage is 1.35x. If the covenant requires 1.25x, you have 0.10x headroom.

Step 3: Model Covenant Mechanics, Not Just Ratios

Covenants are rules with definitions. The same ratio can behave differently depending on how EBITDA is adjusted, how cash taxes are treated, and whether the lender uses trailing twelve months or a forward-looking test.

Key covenant modeling choices:

- Test period timing: monthly/quarterly, trailing twelve months, or annual

- EBITDA definition: add-backs, exclusions, and whether they are capped

- Leverage vs. coverage: leverage covenants often use net debt

- Net debt definition: includes cash netting rules and treatment of restricted cash

- Cure rights: whether you can fix a breach via equity injection or asset sales

A simple modeling habit: create a “covenant definition” tab that mirrors the credit agreement language in plain numbers. Then reference it in the main model so you don’t accidentally use the wrong EBITDA.

Step 4: Build a Debt Capacity Waterfall

Debt capacity is rarely a single number. Use a waterfall that shows how constraints reduce the maximum.

Waterfall example:

- Start with a “cash flow limit” based on coverage.

- Apply a “covenant limit” based on the strictest covenant test.

- Apply a “liquidity limit” if the credit agreement requires a minimum cash balance or limits restricted payments.

- The smallest result is your maximum sustainable debt.

Step 5: Identify the Binding Constraint with Period-by-Period Testing

Capacity can be highest in year 3 and lowest in year 1 because of ramp-up costs, one-time working capital needs, or covenant test timing. Model at least quarterly (or monthly if the credit agreement tests that way) for the first year.

Easy example: A company plans a $2.0m inventory build in the first quarter to support a new contract. Even if annual cash flow looks fine, the covenant test might fail in that quarter because working capital consumes cash and reduces coverage.

Step 6: Stress the Assumptions That Actually Move Covenants

Instead of random sensitivity noise, stress the drivers that change covenant math:

- Revenue and gross margin (affects EBITDA)

- Working capital days (affects cash available for debt service)

- Maintenance capex (affects cash available)

- Interest rate (affects debt service)

- Amortization schedule (affects principal)

Example: If interest rate increases by 100 bps on $60m debt, annual interest rises by about $0.6m. If coverage headroom is only $0.4m, the covenant becomes the binding constraint.

Step 7: Convert Maximum Debt Into a Structuring Output

Once you have maximum sustainable debt, translate it into structuring terms:

- Debt amount and tranche mix (term loan vs. revolver)

- Amortization level and expected paydown

- Interest rate assumptions and hedging treatment

- Equity contribution timing to preserve covenant headroom

A clean final check: ensure the model shows covenant compliance under the base case and that the “worst quarter” has measurable headroom. If headroom is negative, the structure is not merely “tight”—it’s structurally inconsistent with lender definitions.

3.3 Structuring Equity Contributions and Managing Return Profiles

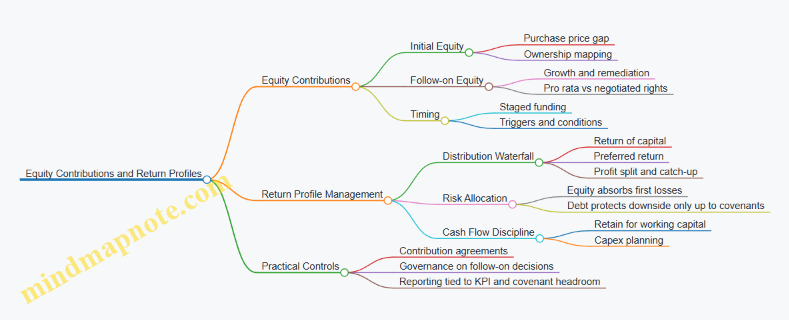

Equity is the part of the capital stack that takes the first hit and gets the last payoff. That sounds dramatic, but it’s actually useful: it forces you to be explicit about what risks you’re paying for and what outcomes you’re targeting. Structuring equity contributions means deciding (1) how much equity goes in, (2) when it goes in, (3) what rights it carries, and (4) how returns are measured and distributed.

Foundational Concepts for Equity Design

Start with three building blocks: ownership, timing, and priority.

- Ownership determines who benefits from value creation. If you and a co-investor contribute different amounts, you need a mechanism that maps contributions to ownership or to economic entitlements.

- Timing matters because equity invested earlier compounds longer. A delayed equity tranche can be cheaper in nominal terms but expensive in return terms.

- Priority determines who gets paid first when cash is distributed. In many deals, equity is not one bucket; it’s split into classes or layers with different distribution rules.

A practical way to keep this grounded is to tie equity structure to the cash flow story you already built in the financing model: what cash is available for debt service, what remains for distributions, and what must be retained for working capital and capex.

Equity Contribution Mechanics

Equity contributions typically come in two forms: initial equity at closing and follow-on equity later.

- Initial equity covers the purchase price gap after debt and any seller financing. Example: A sponsor buys a company for $100 million. Debt provides $70 million. The remaining $30 million is equity. If the sponsor brings $25 million and a partner brings $5 million, the economic deal must reflect that split.

- Follow-on equity funds growth, repairs, or covenant headroom. Example: After closing, the business needs $6 million for a new ERP rollout and working capital build. If the original equity investors fund it pro rata, distributions later may be reduced until the new capital is repaid under the deal’s return rules.

To manage return profiles, you also decide whether equity is paid-in fully at closing or staged. Staging can reduce early cash outlay, but it increases the need for clear triggers: what conditions require the follow-on, and what happens if they are not met.

Return Profile Basics and Distribution Logic

Return profiles are governed by distribution waterfalls. Even without getting lost in legal drafting, you can think in terms of three steps: return of capital, preferred return, and catch-up or split.

- Return of capital: investors get their contributed equity back before profits are split.

- Preferred return: investors earn an agreed rate on unreturned capital.

- Profit split: after the above, remaining proceeds are shared between investors and the sponsor.

Example with simple numbers: Suppose investors contribute $30 million. Preferred return is 8% annually, and the deal exits in year 4 with $45 million of equity proceeds available for distribution after debt and transaction costs. If the preferred return and return of capital are satisfied, the remaining $15 million becomes the profit pool subject to the negotiated split. The exact split depends on the waterfall design, but the logic stays consistent.

Mind Map: Equity Contributions and Return Profiles

Advanced Details That Prevent Misalignment

-

Pro Rata vs Non-Pro Rata Follow-On: If follow-on is not pro rata, you need a clear economic adjustment. Example: Investor A funds an extra $3 million to keep the company compliant with a liquidity covenant. If Investor B doesn’t fund, Investor A may receive additional units or a higher share of future distributions. Without this, the non-funding investor can benefit from the funding without paying for it.

-

Equity Rights and Control: Equity structure can include voting rights tied to major decisions, such as approving budgets, incurring debt, or changing business plans. Example: If the company wants to increase capex beyond the approved plan, the sponsor may require investor consent. This protects equity from being diluted by operational decisions that shift risk.

-

Return Measurement Consistency: Use the same basis for return calculations across modeling and documentation. Example: If your model assumes transaction costs are deducted from exit proceeds, but the legal waterfall treats them differently, the realized return can diverge from what was underwritten.

-

Linking Equity to Operational Milestones: Follow-on funding can be tied to measurable conditions. Example: Release $2 million only after the business hits a working capital target for two consecutive quarters. This reduces the chance that equity becomes a blank check.

Worked Example: Two Investors, One Deal, Different Timing

Assume a $100 million purchase with $70 million debt and $30 million equity. Investor X contributes $20 million at closing; Investor Y contributes $10 million at closing. In year 1, a $5 million follow-on is required. Investor X funds the full $5 million; Investor Y funds $2 million and declines $3 million.

If the deal is pro rata, Investor Y would have funded $2.5 million, so declining $0.5 million creates a mismatch. A well-structured agreement resolves this by either (a) issuing additional equity to Investor X for the shortfall, or (b) adjusting the distribution waterfall so Investor X receives a larger share until the economics catch up. The key is that the return profile reflects both the timing and the risk each investor actually took.

The goal of equity structuring is not to make returns look pretty on paper. It’s to ensure that when cash moves—at closing, during follow-ons, and at exit—the economics match the contributions and the decisions that created or protected value.

3.4 Selecting Interest Rate and Amortization Structures for Predictable Cash Flows

Predictable cash flows start with two knobs: the interest rate path and the amortization schedule. Together they determine how much cash goes to debt service each period, how sensitive that cash is to rate changes, and how quickly principal is paid down. The goal is not “lowest cost,” but “manageable variability” that still supports the equity return target.

Foundational Concepts That Drive Cash Predictability

Interest rate type controls payment sensitivity.

- Fixed rate: the interest portion stays constant (ignoring fees and step-ups). This is easiest for budgeting.

- Floating rate: interest changes with a reference rate (often SOFR or similar). Predictability depends on how much the reference rate can move and how quickly the loan reprices.

Amortization structure controls principal paydown timing.

- Straight-line amortization: principal reduces evenly over time, producing a smoother decline in interest expense.

- Back-ended amortization: little principal early, larger payments later. This can preserve early cash but concentrates repayment risk.

- Bullet maturity: principal paid at the end. Interest-only periods can look great on a cash flow statement until the maturity wall arrives.

A practical rule: if your operating plan is sensitive to demand swings, prefer structures that keep debt service stable even when revenue is not.

Choosing Between Fixed and Floating Rates

Start with a simple question: “How much payment variability can the business absorb without breaking covenants or forcing equity injections?” Then map that to the loan’s rate mechanics.

Example: fixed vs floating on the same debt amount

- Debt: $50 million

- Margin over reference: 4.00%

- Reference rate today: 5.00%

- Term: 5 years

If fixed is set at 9.50% all-in, annual interest is about $4.75 million. With floating, if the reference rate rises to 6.50% while margin stays the same, the all-in rate becomes 10.50% and annual interest becomes about $5.25 million. That extra $0.50 million per year is not theoretical; it directly competes with operating cash for working capital and capex.

To keep the decision grounded, model at least two reference-rate scenarios and check covenant headroom under each.

Selecting Amortization That Matches Operating Reality

Amortization should mirror how quickly the business can reliably generate excess cash.

Example: straight-line amortization for stable cash generation

- Debt: $30 million

- Term: 6 years

- Straight-line principal: $5 million per year

Interest declines each year as principal reduces. Early years still have meaningful interest, but the principal schedule prevents a large maturity payment. This is often a good fit for businesses with steady recurring revenue.

Example: back-ended amortization for early cash preservation

- Debt: $30 million

- Term: 6 years

- Principal: $1 million per year for years 1–5, $25 million in year 6

Early debt service is lower, which can support an operational improvement plan. However, the year-6 payment must be funded through refinancing, sale proceeds, or a large cash build. If your exit plan relies on a sale, confirm that the sale proceeds timing aligns with the maturity date.

Example: bullet maturity when exit timing is certain

Bullet structures can be rational when the business has a clear path to refinance or exit at maturity. If that path depends on multiple moving parts, bullet risk becomes a cash-flow planning problem rather than a financing choice.

Coordinating Rate and Amortization in the Debt Service Profile

Interest rate and amortization interact. A floating-rate loan with back-ended amortization can create a “double squeeze”: higher interest during years when principal is still large. Conversely, a fixed-rate loan with straight-line amortization often produces the most stable debt service profile.

Use a debt service schedule to compare structures period by period.

Simple comparison framework

- Build a monthly or quarterly debt service schedule.

- Apply interest mechanics (fixed or floating with repricing dates).

- Apply principal schedule (straight-line, back-ended, bullet).

- Compute coverage ratios and covenant compliance for each scenario.

Practical Modeling Steps for Deal Teams

Step 1: Define the “cash available” metric consistently

Use the same cash measure that the covenants or internal targets reference (for example, cash flow available for debt service). Inconsistent definitions create false comfort.

Step 2: Model repricing timing for floating rates

If the loan reprices quarterly, don’t assume annual averages. Payment timing affects liquidity.

Step 3: Include fees and interest capitalization only when contractually allowed

Upfront fees reduce net proceeds; capitalization changes when cash leaves the business. Both matter for predictability.

Step 4: Stress the combination, not just each part

Run scenarios that change both reference rates and operating cash. A stable operating plan with a rising rate is one thing; a weaker operating plan with a rising rate is the real test.

Mind Map: Interest Rate and Amortization Choices

Example: Turning the Choice Into a Decision Rule

If the business can only tolerate limited variability in cash available for debt service, choose either (a) fixed rate with back-ended amortization capped by a realistic refinancing plan, or (b) floating rate only when amortization is front-to-mid loaded enough to reduce principal risk early. If the operating plan is volatile, avoid bullet structures unless the exit proceeds timing is contractually and operationally supported.

The “best” structure is the one that keeps the debt service profile within the business’s cash reality across the scenarios you actually care about.

3.5 Coordinating Financing Terms with Purchase Price and Closing Conditions

Financing terms and deal economics are not separate workstreams; they are one system. If you coordinate them early, you avoid the classic problem where the purchase price looks fine on paper, but the lender’s conditions force a lower cash contribution, a different timing of payments, or a working-capital target that quietly changes the effective price.

Start with the Cash Waterfall Logic