Startup Funding and Venture Capital Strategies

1. Preparing Your Startup for Fundraising

1.1 Defining Your Fundraising Objectives and Funding Use Cases

Before you talk to investors, decide what you are trying to accomplish with the money. “Raise capital” is a task; fundraising objectives are measurable outcomes tied to specific use cases. When these are clear, your pitch becomes easier to write, your financial model becomes easier to defend, and your team stops arguing about priorities.

Start with Outcomes, Not Amounts

Pick 2–4 fundraising objectives that can be checked in the next 6–18 months. Each objective should map to a business bottleneck you can actually solve.

Common objective patterns:

- Revenue acceleration: reduce sales cycle time, improve conversion, or expand into a new customer segment.

- Product readiness: ship a feature set that unlocks a new pricing tier or reduces churn.

- Operational stability: hire key roles to prevent execution gaps, not just to “grow.”

- Market expansion: localize support, build a partner channel, or add compliance capacity.

Example: A B2B SaaS startup might set an objective of “increase net revenue retention from 92% to 105% by improving onboarding and support coverage.” That objective implies use cases like customer success capacity and product instrumentation, not generic “marketing.”

Translate Objectives into Funding Use Cases

A funding use case is a bucket of spending with a purpose, an owner, and a measurable result. Good use cases are specific enough that you can explain tradeoffs if the round is smaller.

Use case categories that cover most early-stage startups:

- People: engineering, product, sales, customer success, finance, and operations.

- Go-to-market execution: sales enablement, outbound tooling, events, partnerships, and customer acquisition experiments.

- Product and infrastructure: hosting, security reviews, analytics, QA, and key platform work.

- Customer validation: pilots, onboarding support, research, and service costs tied to learning.

- Legal and compliance: incorporation, IP work, contracts, and securities administration.

- Working capital: inventory (if relevant), payment terms buffers, and cash management.

Example: If your objective is “reduce churn,” a use case might be “hire a customer success lead and fund a structured onboarding program.” The measurable result could be “churn down by X points and time-to-value down by Y weeks.”

Define Success Metrics and Decision Rules

For each use case, define:

- Metric: what changes if the spending works.

- Baseline: what the number is today.

- Target: what “good” looks like.

- Time window: when you expect to see movement.

- Decision rule: what you do if progress is slower than expected.

Decision rules prevent endless spending. Example: “If onboarding activation does not improve within two months, we pause the additional CS headcount and reallocate to product changes that address the activation bottleneck.”

Avoid the Two Common Mistakes

- Listing expenses without purpose: “$120k for marketing” tells investors nothing about what will improve. Replace it with “$120k for sales enablement and outbound testing to improve demo-to-trial conversion from 18% to 25%.”

- Overstuffing objectives: If you have five objectives, you usually have none. Choose the bottleneck that most constrains execution right now.

Build a Simple Funding Use Case Map

Use the map below to connect objectives to use cases and metrics. Keep it to one page.

Mind Map: Fundraising Objectives

Convert the Map into a Funding Plan

Once the use cases are defined, estimate how much cash each one consumes and when it will be spent. A practical approach is to assign a rough monthly burn range per use case, then sum them into a total round size.

Example allocation for a $2.0M seed round:

- People (product and CS): $900k over 12 months

- Go-to-market execution: $550k over 10 months

- Product and infrastructure: $300k over 9 months

- Legal and compliance: $150k over 6 months

- Working capital buffer: $100k over 12 months

The buffer is not a “nice to have.” It prevents the plan from collapsing when hiring starts later than expected or when a customer pilot runs longer than the calendar promised.

Write Your Objective Statement

Create a short statement you can reuse in meetings and in your internal planning. It should include the bottleneck, the outcome, and the use cases.

Example objective statement:

“We are raising to improve net revenue retention by reducing churn drivers in onboarding and support. The funds will be used for customer success capacity, onboarding flow redesign, and security/compliance work needed for larger contracts, measured by activation rate and retention movement over the next two quarters.”

Quick Checklist Before You Pitch

- Do you have 2–4 objectives with measurable targets?

- Does each use case have an owner and a metric?

- Can you explain tradeoffs if the round is 20% smaller?

- Are you spending on bottlenecks, not categories?

When these answers are consistent, your fundraising story stops being a collection of slides and becomes a plan with logic investors can follow.

1.2 Building a Fundraising Readiness Checklist for Team Product and Metrics

A fundraising readiness checklist is not a list of chores. It’s a way to prove you can answer investor questions quickly, consistently, and with evidence. Start with what investors test first: the team’s ability to execute, the product’s ability to solve a real problem, and the metrics’ ability to describe reality without hand-waving.

Mind Map: Readiness Signals

Team Readiness Checklist

1. Roles and ownership. Write down who owns product, engineering, sales, and finance. Then add one sentence each: what that person is accountable for in the next 60 days. Example: “Product owns onboarding improvements and activation metrics; Engineering owns reliability and deployment cadence.” Investors don’t need job descriptions; they need clarity.

2. Execution history. Prepare a short “what we shipped” log with dates and outcomes. If you launched a feature, include what changed in usage. Example: “New onboarding reduced time-to-first-action from 9 minutes to 4 minutes over two weeks.” If you can’t quantify it, explain why and what you measured instead.

3. Hiring plan and gaps. List the top two roles you need and why they matter for the next milestone. Include what you will stop doing to make room. Example: “Hire a customer success lead to reduce churn; pause nonessential custom integrations.”

4. Decision cadence. Show how you make tradeoffs. A simple weekly operating rhythm works: product review, metrics review, and engineering status. Investors look for repeatable process, not heroics.

Product Readiness Checklist

1. Problem clarity. Create a one-page “problem statement” that includes who has the problem, how they describe it, and what they do today instead. Example: “Ops teams at mid-market firms struggle to reconcile invoices; they currently use spreadsheets and manual checks.”

2. Solution proof. Map each core feature to the user job it supports. Then add evidence: screenshots, short demo clips, or a written walkthrough of a typical workflow. Example: “Automated invoice matching supports the job of reducing manual reconciliation time.”

3. Customer feedback loop. Document how you collect feedback and how it changes the roadmap. Include at least three recent examples. Example: “Users requested export formats; we added CSV export and reduced support tickets about formatting.”

4. Roadmap discipline. Your roadmap should include milestones with measurable outcomes. Avoid vague goals like “improve engagement.” Use outcomes like “increase activation rate from 22% to 30% by improving onboarding steps 1–3.”

Metrics Readiness Checklist

1. Metric definitions that don’t drift. Write definitions for the metrics you’ll discuss: activation, retention, churn, revenue, and runway. Include the exact calculation and the data source. Example: “Activation is a user who completes the first successful workflow within 7 days of signup.”

2. Data quality checks. Add a small section called “How we know the numbers are right.” Include checks like deduping events, handling timezone issues, and reconciling analytics totals with billing totals. Example: “Monthly active users exclude test accounts; billing revenue reconciles to Stripe gross receipts minus refunds.”

3. Cohorts and retention evidence. Investors want to see whether users stick around. Provide cohort tables for at least two periods and explain what changed. Example: “Cohort retention improved after onboarding update because users reached the first workflow faster.”

4. Unit economics inputs. If you have revenue, show the inputs behind gross margin and customer acquisition cost. If you don’t, show the cost drivers you track anyway: support cost per active account, infrastructure cost per usage unit, and sales cycle length. Example: “Infrastructure cost per active workspace decreased 18% after optimizing queries.”

Evidence and Q and a Readiness

1. Data room completeness. Confirm you have the basics: cap table, incorporation documents, option plan details, key contracts, and financial statements. Add a “last updated” note for each file so you don’t repeat yourself.

2. Versioned artifacts. Keep pitch deck and metric definitions in one place with a clear version number. Example: “Deck v3.2 matches metrics sheet v3.2; both updated after the latest cohort export.”

3. Red flag handling. Prepare short explanations for known issues: churn spikes, delayed launches, or a mismatch between pipeline and bookings. The goal is not to hide problems; it’s to show you can explain them precisely.

Process Checklist for the Fundraising Window

Assign owners for every recurring task: updating metrics, responding to diligence questions, and coordinating legal review. Then set a simple workflow: questions arrive, owner triages, response is drafted, and evidence is attached. Example: “If an investor asks about retention, the metrics owner answers and links the cohort export and definition sheet.”

Example Readiness Scorecard

| Area | Evidence You Have | What’s Missing | Owner | Target Date |

|---|---|---|---|---|

| Team | Ship log, org ownership | Hiring plan detail | Head of Product | 2026-02-15 |

| Product | Workflow demo, roadmap milestones | Customer feedback examples | PM | 2026-02-15 |

| Metrics | Definitions, cohort exports | Revenue reconciliation notes | Finance | 2026-02-18 |

| Evidence | Data room folder structure | Versioning for deck | Ops | 2026-02-18 |

A good checklist ends with accountability. When every item has an owner and a target date, fundraising stops being a vague project and becomes a controlled process.

1.3 Establishing Your Company Structure and Cap Table Baseline

A cap table is not just a spreadsheet; it’s the ledger of who owns what, how ownership changes, and what investors will later ask you to prove. Before you raise money, you want a structure that is legally coherent, operationally manageable, and easy to explain in one page.

Start with the Corporate Form and Governance Basics

Most venture-backed startups incorporate as a C-Corp (common in the US). The practical reason is simple: preferred stock and standard venture financing mechanics fit cleanly. If you’re outside that norm, the same principles apply—choose a structure that supports equity issuance, option grants, and investor preferred rights.

Governance basics should be set early:

- Board and consent process: define how decisions are made (board meetings vs written consents).

- Authorized shares: confirm the number of shares the company can issue without amending the charter.

- Stock classes and rights: decide what exists today (common stock) and what will exist later (preferred stock).

Example: If your charter authorizes 10,000,000 shares but you only track 1,000,000 issued, you still need a clear record of what happened to the remaining authorized shares. Investors will ask, and your answer must match the charter.

Create a Cap Table Baseline Snapshot

A baseline snapshot is the state of the cap table at a specific moment, with documents that support every line item. Build it from primary records, not memory.

Include at minimum:

- Issued shares by holder (founders, employees, any existing investors)

- Vesting status for founders and employees (if applicable)

- Option pool size and what portion is reserved vs granted

- Any SAFEs or notes outstanding (even if they are not equity yet)

- Any transfers, cancellations, or repurchases

Use a consistent naming convention for holders and securities so you can reconcile later.

Example: Two founders each have 3,000,000 common shares, but one has a repurchase agreement for unvested shares. Your baseline should show the vesting schedule and the repurchase terms, not just the current share count.

Align Equity with Vesting and Founder Agreements

Equity that is “owned” but not “earned” causes problems during fundraising. The baseline should reflect vesting and any acceleration rules.

Common setup:

- Founders receive common stock subject to vesting

- Unvested shares are subject to repurchase at cost if the founder leaves

- Vesting typically spans multiple years with monthly vesting after an initial cliff

Example: A founder starts on Day 1 and leaves after 10 months. If you issued fully vested shares without a repurchase mechanism, you may need to unwind ownership later. If you used vesting with repurchase, you can cancel or repurchase unvested shares and update the cap table cleanly.

Establish an Option Pool Plan Before You Need It

An option pool is reserved equity for future hires. Even if you plan to hire later, you want the baseline to show how much equity is available and how it will be granted.

Key baseline components:

- Board-approved equity incentive plan

- Option pool size (reserved shares)

- Granting policy and approval workflow

- Standard option terms (exercise price, vesting, expiration)

Example: You reserve 1,500,000 shares for options. Later you grant 300,000 options to an early engineer. Your cap table baseline should already know the pool size and show remaining reserved shares after the grant.

Document Everything That Changes Ownership

Ownership changes come from a small set of events. Your baseline should be backed by documents for each event type.

Common event categories:

- Issuance: stock purchase agreements, subscription agreements

- Vesting: vesting schedules, board approvals for grants

- Repurchase or cancellation: repurchase agreements, cancellation records

- Transfers: stock transfer forms and board consents

- Rights conversion: SAFEs/notes documentation and conversion mechanics

If you have any SAFEs or notes, record them as separate line items with their terms. Even without conversion, investors will want to see what could become equity.

Mind Map: Cap Table Baseline Work

A Practical Baseline Checklist

Treat this as a “numbers plus proof” exercise.

- Confirm charter and authorized shares match your intended issuance plan.

- List every holder and security type currently outstanding.

- For each founder, include vesting and repurchase details.

- For the option pool, show reserved shares and what has been granted.

- Record any SAFEs/notes as separate items with terms.

- Reconcile totals: issued shares + reserved options + any other equity instruments should align with your authorized share framework.

Example: If your cap table says 6,000,000 shares issued and your charter authorizes 10,000,000, you still need to show how the remaining 4,000,000 is treated—reserved for options, unissued, or otherwise allocated.

Common Mistakes That Break Fundraising

- Missing repurchase terms for unvested founder equity.

- Option pool reserved shares not matching the approved plan.

- Cap table built from a founder’s memory instead of board records.

- SAFEs/notes omitted from the baseline because “they aren’t equity yet.”

A clean baseline makes later steps faster: diligence questions become straightforward, and term sheet negotiations start from accurate facts rather than guesswork.

1.4 Organizing Financial Records and Data Rooms for Investor Review

Investors don’t review your company; they review evidence. A well-organized financial record set and data room turns “Can you show me?” into “Got it.” The goal is not to impress with volume, but to reduce friction: clear documents, consistent numbers, and a trail that matches your story.

Start with a Single Source of Truth

Before you create folders, decide what system owns each number. For example, if your accounting software produces revenue and expenses, treat it as the source for the income statement. If you track customer usage in a separate billing system, treat that as the source for usage metrics, then reconcile it to revenue.

A simple rule prevents chaos: every metric used in your pitch deck should be traceable to a document in the data room. If a slide says “MRR grew from $40k to $55k,” the data room should contain the MRR calculation method and the underlying export or report.

Build Your Data Room Structure Like a Filing Cabinet

Use a consistent folder hierarchy so investors can navigate without asking you to explain the layout. A practical structure:

- 00 Cover And Index

- Data room index with document descriptions

- Investor Q&A log template

- 01 Corporate

- Charter, bylaws, cap table, stock ledger

- 02 Financial Statements

- Monthly P&L, balance sheet, cash flow (or closest equivalent)

- General ledger trial balance exports

- 03 Revenue And Billing

- Billing reports, churn/retention calculations, revenue recognition notes

- 04 Expenses And Payroll

- Payroll summaries, contractor payment summaries, major expense categories

- 05 Bank And Cash

- Bank statements, cash reconciliation worksheet

- 06 Tax And Compliance

- Tax filings, sales tax reports if applicable

- 07 Contracts And Legal Financial Impact

- Customer master agreements, key vendor contracts

Investors often start with financials, then jump to contracts that explain why the numbers look the way they do. Keeping contracts near the financial impact reduces back-and-forth.

Create a Reconciliation Layer for Every “Why”

Numbers rarely match perfectly across systems. Your job is to explain differences with a reconciliation worksheet.

Example: Revenue Reconciliation

- Billing system shows invoiced amounts.

- Accounting system shows recognized revenue.

- Reconciliation worksheet includes:

- Invoiced vs recognized delta

- Timing differences (prepaid months, annual contracts)

- Credits and refunds

If you have a monthly revenue chart, include a one-page explanation of the calculation method and the reconciliation approach. That one page saves hours of investor time.

Document Your Accounting Policies in Plain Language

Investors don’t need accounting textbooks; they need consistent definitions. Include a short “Accounting Notes” document covering:

- Revenue recognition approach at a high level

- Treatment of refunds, credits, and discounts

- How you handle prepaid revenue

- How you classify expenses (especially one-time items)

Example: One-Time Expense Labeling If you had a $25,000 legal expense that won’t repeat, label it clearly as non-recurring in your monthly reporting package and explain why it occurred. Investors can then adjust their own models without guessing.

Prepare a Monthly Reporting Package That Stays Stable

A stable monthly package reduces investor questions because the format doesn’t change.

Include:

- Income statement with clear line items

- Balance sheet

- Cash reconciliation summary

- Headcount and payroll summary

- Variance notes for major changes (for example, “Marketing spend increased due to annual contract start”)

Use a consistent naming convention, such as YYYY-MM_PnL, YYYY-MM_CashReconciliation, and YYYY-MM_Headcount. Consistency beats cleverness.

Mind Map: Data Room Readiness

Example: A Clean Index Entry That Works

Your index should describe what a document contains and how it connects to a metric.

Example Index Entry

- 02 Financial Statements / 2026-02 Monthly P&L

- Contains: revenue, COGS, operating expenses by category

- Ties to: investor deck “Monthly burn” and “Gross margin”

- Notes: includes non-recurring legal expense line item

This level of specificity prevents the classic problem: investors download a file but still can’t tell what it means.

Version Control and Access Hygiene

Use a single “final” version per month per document type. If you revise a reconciliation, update the index entry and mark the revised file clearly.

Also, avoid mixing drafts with finals. A simple approach:

- Drafts live in a separate internal folder

- Only finals are uploaded

- File names include the month and document type

Close the Loop with a Q and a Log

Add a lightweight Q&A log template in the data room. When an investor asks a question, record:

- Question summary

- Where the answer lives in the data room

- Date answered (for example, 2026-02-15)

This keeps you from re-explaining the same reconciliation every time someone new joins the diligence call.

1.5 Selecting the Right Funding Path for Your Stage and Business Model

Choosing a funding path is mostly about matching cash needs to investor expectations. Investors care less about the label of the round and more about whether your current evidence supports the risk they’re taking.

Start with two foundational questions: What are you building, and what proof can you produce soon? A product with fast customer feedback can often raise earlier because you can generate evidence quickly. A product that depends on long sales cycles or complex compliance usually needs more runway and clearer milestones before investors feel comfortable.

Step 1: Match Stage to Evidence

Early stage typically means you’re still proving something fundamental: demand, repeatability, or technical feasibility. Funding paths differ in how much uncertainty they tolerate.

- Pre-revenue or early revenue: Investors expect learning velocity. Your metrics should show progress toward a repeatable motion, not just raw growth.

- Revenue with early retention: Investors expect unit economics to be directionally correct. They want to see that customers keep coming back and that costs don’t scale faster than value.

- Scaling revenue: Investors expect predictable execution. Your funding plan should support hiring, sales capacity, and operational scaling without losing control of margins.

A practical example: if you run a B2B service with manual onboarding, you may show revenue quickly but still lack scalable delivery. That’s a sign to fund with a path that supports process refinement, not one that assumes immediate automation.

Step 2: Match Business Model to Cash Flow

Your business model determines how quickly cash returns.

- Subscription or usage-based: Cash often comes in recurring intervals, so investors look for retention, churn, and cohort behavior.

- Marketplace: Cash depends on liquidity and take rate. Investors look for supply and demand balance and whether incentives are sustainable.

- One-time sales: Cash may arrive in bursts. Investors focus on pipeline quality, sales cycle consistency, and gross margin stability.

- Hardware or regulated products: Cash needs are front-loaded. Investors expect milestones tied to manufacturing, approvals, or clinical/technical gates.

Example: a SaaS company with monthly churn of 6% might still be fundable early, but a SaaS company with churn of 25% usually needs product and pricing work before equity investors will underwrite the risk.

Step 3: Choose the Funding Instrument That Fits the Risk

Different instruments shift risk between founders and investors.

- Equity rounds: Best when you can articulate valuation logic and you have enough evidence to justify ownership transfer now. Equity also simplifies future fundraising because the cap table is straightforward.

- Convertible notes: Useful when you want speed and expect a priced round soon. They add complexity through interest and maturity, so you need a plan for what happens if the next round takes longer than expected.

- SAFEs: Similar intent to notes but typically simpler. They still require clarity on conversion mechanics and how you’ll handle future pricing.

A simple rule: if you can credibly reach a priced round milestone within the instrument’s expected timeline, convertibles can be efficient. If not, equity may reduce the chance of an awkward maturity event.

Step 4: Pick the Round Size and Milestones Together

Funding paths fail when the round size is chosen without linking it to what you’ll prove.

Create a milestone map with three layers:

- Product proof (what users do, not just what they say)

- Commercial proof (repeatable acquisition and retention)

- Operational proof (unit economics, delivery capacity, and cash discipline)

Example: for a seed round, you might set milestones like “reduce onboarding time from 10 days to 3” and “reach cohort retention of X at a defined price.” For a Series A, you might set “improve gross margin to Y” and “demonstrate sales efficiency with a stable sales cycle.”

Step 5: Use a Decision Mind Map

Mind Map: Selecting the Right Funding Path

Step 6: Validate with a “Fit Check”

Before you commit, run a fit check using three tests.

- Evidence test: Can you show the metric that justifies the instrument and stage within the next 6–12 weeks?

- Cash test: Does the funding path cover the time needed to reach the next milestone without forcing emergency decisions?

- Complexity test: Does the added paperwork and negotiation effort match your current bandwidth?

If you fail any test, adjust the plan: either narrow the milestones, change the instrument, or delay the round until the evidence is stronger.

A final practical note: the “right” funding path is the one that lets you keep building while staying consistent with what investors will ask for next. When your next milestone is clear and your metrics are measurable, the funding conversation becomes less about persuasion and more about verification.

2. Understanding Venture Capital and Investor Decision Making

2.1 Mapping Venture Capital Firm Structures and Investment Mandates

Venture capital firms are not just “money with opinions.” Their internal structure determines how fast decisions happen, what gets prioritized, and which founders get a meeting in the first place. Mapping a firm’s structure and mandate helps you predict the questions you’ll face and the terms you’re likely to see.

Core Firm Structures

Most VC firms fit one of these patterns, and each changes how deals are sourced and approved.

- Single-fund partnership: A small team runs one main fund. Fewer people means faster alignment, but the mandate can be narrow because the team is accountable to a specific strategy.

- Multi-fund platform: The firm manages multiple funds across stages. You may meet a partner who invests early, but the “real decision” could involve a partner aligned to the specific fund that matches your round.

- Fund-of-funds or feeder structures: Some firms allocate to other managers. Their mandate is about manager selection, so they rarely lead startup rounds directly.

- Corporate venture arms: These sit inside a corporate group. They often have a strategic lens, which can affect diligence depth, timelines, and governance expectations.

A practical way to map structure is to identify who signs the investment, who leads diligence, and who sets the investment committee agenda.

Investment Mandates That Actually Matter

A mandate is more than a one-line description like “seed to Series A.” It usually includes constraints that show up in meetings.

- Stage: Seed, Series A, growth, or a narrow band like “pre-seed with revenue.” Stage affects what evidence investors expect.

- Check size: A firm that writes $2–5M checks will ask different questions than one that writes $250k–$1M checks.

- Geography: Some firms are global; others are tied to a region. Even remote-friendly firms may prefer founders who can meet in person.

- Sector focus: “Software” can mean anything from developer tools to fintech. The mandate often specifies subcategories.

- Ownership expectations: Many firms target a certain level of influence. This shows up in board expectations and protective provisions.

- Follow-on behavior: Some firms reserve capital for later rounds; others invest opportunistically. Your fundraising plan should match their likely participation.

When you map these constraints, you can translate them into meeting prep. If a firm’s mandate emphasizes retention, expect deeper questions on cohorts and churn. If it emphasizes enterprise sales, expect diligence on pipeline quality and sales cycle length.

Decision Flow Inside the Firm

Investment committees and partner approvals vary, but the logic is consistent: risk is reduced through internal review.

- Sourcing: A partner or associate brings the deal. The first meeting often tests fit with the mandate.

- Pre-diligence: The team checks basic viability: team credibility, market clarity, and whether the numbers are internally consistent.

- Diligence ownership: Different partners may own different diligence tracks, such as product, market, or legal.

- Investment committee: The committee decides whether to proceed and under what terms. If the firm has multiple funds, the committee may route the deal to the appropriate fund.

A useful founder habit is to ask, early and politely, “Which fund would this typically be allocated to?” That question is grounded in how the firm operates, not in curiosity for its own sake.

Mind Map: Firm Structure and Mandate

Example Mapping in Practice

Example 1: Multi-fund platform with a narrow stage band You’re raising a seed round for a B2B SaaS product with early revenue. The partner you meet says “seed is our focus,” but their firm is a multi-fund platform. In the second meeting, you ask which fund would invest. You learn it would be routed to a specific seed fund that emphasizes retention. That explains why they ask for cohort charts and why they want a clear plan for improving net revenue retention.

Example 2: Corporate venture arm with strategic governance You’re pitching an infrastructure startup to a corporate venture group. Their mandate includes a sector match, but their internal process includes additional stakeholders from the corporate side. In diligence, they request more documentation around security posture and integration timelines. Even if the economics look fine, the governance expectations may be stricter because the corporate parent needs predictable risk management.

Turning Mapping into Meeting Preparation

Once you map structure and mandate, you can tailor your materials and questions without guessing. Prepare a one-page “fit summary” that ties your stage, traction evidence, and funding use to the constraints you identified. Then align your questions to the decision flow: ask about fund routing, diligence ownership, and expected timeline for committee review.

This approach keeps the conversation grounded. It also reduces the chance that you spend time pitching to a firm that is structurally capable of investing, but mandate-incompatible with your specific round.

2.2 Understanding Partner Roles and How Deals Get Approved

Venture capital firms are not monoliths. Even when the same partner meets you, the decision is usually shaped by a small group with different jobs: sourcing, diligence, investment committee preparation, and final approval. Knowing who does what helps you answer questions the right way and at the right time.

Partner Roles That Actually Touch Your Deal

Start with the simplest mental model: partners are accountable for outcomes, but they operate through a pipeline.

- Sourcing partner: Often the first person you meet. They translate your story into the firm’s internal language and decide whether it’s worth spending diligence time.

- Diligence lead: Sometimes the same person, sometimes not. They coordinate the information requests, pressure-test assumptions, and ensure the firm’s internal checklist is satisfied.

- Industry or functional specialist: A partner or senior associate who focuses on a domain like fintech, developer tools, or healthcare. They may not run the whole process, but they can veto weak technical or market reasoning.

- Investment committee partner: The person who helps package the deal for approval. They care about consistency: does the round fit the firm’s mandate, and is the risk profile coherent with the proposed terms?

- Operations or legal partner: Not always a “partner” in the meeting sense, but they influence feasibility. They flag issues like option pool mechanics, cap table cleanliness, or contract gaps that could delay closing.

A useful rule: if you only impress the sourcing partner, you may still lose later. If you satisfy the diligence lead and the committee partner, you’re much more likely to move.

How Deals Get Approved Inside a Firm

Most firms follow a repeatable sequence. The names vary, but the logic is consistent.

- Initial screen: The firm checks fit with stage, geography, and sector. If you’re outside the mandate, the process stops early.

- Partner alignment: The sourcing partner confirms internal interest and identifies who must sign off.

- Diligence sprint: The firm requests documents and runs structured questions. This is where weak metrics, unclear ownership, or inconsistent unit economics get caught.

- Investment memo: A written summary is prepared for the committee. It includes the thesis, risks, and how the proposed terms address those risks.

- Investment committee: The committee debates the memo, compares it to portfolio needs, and decides whether to approve, revise, or pass.

- Term negotiation and closing: If approved, the firm negotiates terms and coordinates legal execution.

A practical implication: your answers should map to the memo. If you can’t explain your numbers clearly, you’re forcing the diligence lead to guess, and committees dislike guessing.

Mind Map: Partner Roles and Approval Flow

Partner Roles and Deal Approval Mind Map

Example: How the Same Meeting Plays Differently Across Roles

Imagine you’re raising a Seed round.

- In the first meeting, the sourcing partner asks, “Why now, and why you?” They want a coherent narrative and a reason the firm should spend time.

- During the diligence sprint, the diligence lead asks, “Show the retention cohort math and explain churn drivers.” They’re not judging your ambition; they’re checking whether the evidence supports the plan.

- In the specialist review, a partner might ask, “How defensible is your distribution?” They look for concrete differentiation, not just a claim.

- At the investment committee, the committee partner focuses on whether the proposed terms match the risk. If your traction is real but your revenue model is fragile, they may push for protections or a smaller check.

If you treat every question as a chance to tell your story, you’ll miss the point. Each role is asking for a different kind of proof.

Example: A Clean Path to Approval Through Targeted Evidence

Suppose an investor asks for customer references and you provide two calls plus a short summary of outcomes. That helps, but it’s not enough if the diligence lead also needs contract clarity.

A stronger approach is to bundle evidence by question type:

- Commercial proof: retention and usage metrics with cohort definitions

- Legal proof: signed customer agreements and IP assignment confirmations

- Financial proof: reconciled revenue numbers and burn calculation notes

When your evidence is organized this way, the diligence lead can write the memo faster, and the committee can focus on substance rather than chasing documents.

What to Watch for in Partner Behavior

Even without knowing internal names, you can infer roles from behavior.

- If someone asks for documents early, they’re likely driving diligence.

- If someone summarizes your thesis and asks about terms, they’re likely preparing for committee.

- If someone focuses on feasibility and closing mechanics, they’re likely connected to operations or legal.

Your job is to respond with the right evidence for the role that’s currently “holding the steering wheel.”

2.3 Reading Investment Thesis Fit Through Sector Stage and Geography

A venture firm’s thesis is not a slogan; it’s a set of constraints that shapes what they can underwrite quickly and defend internally. Your job is to translate your startup into those constraints using evidence, not persuasion.

Sector Fit Starts with What They Can Actually Evaluate

Sector fit usually means the firm has a repeatable way to judge customer pain, buying behavior, and competitive dynamics. Begin with three questions you can answer in your first meeting:

- Who is the buyer and how do they decide? If you sell to procurement, show how deals get approved and what blocks them.

- What is the workflow your product changes? Investors look for a clear “before and after,” even if you’re early.

- What evidence counts in this sector? In B2B, it might be pilot-to-contract conversion; in marketplaces, it might be liquidity and retention.

Example: A seed investor focused on developer tools will ask about adoption loops and integration effort. If you instead lead with revenue charts but can’t explain how developers evaluate and switch, you’ll feel “off-thesis” even if your numbers are strong.

Stage Fit Means Matching Their Decision Tempo

Stage fit is about how much uncertainty the firm is willing to carry and how they structure support. Early-stage investors often accept messy metrics if you can show learning velocity. Later-stage investors expect clearer unit economics, repeatable sales motion, and governance readiness.

Use a simple mapping:

- Pre-product: evidence of problem clarity, early design partners, and iteration cadence.

- Seed: early traction that proves demand and a credible plan to reach the next milestone.

- Series A: stronger retention or conversion, clearer pricing logic, and a sales process that doesn’t rely on founder magic.

Example: If you’re raising a seed round but your deck reads like a Series A plan—complete with mature churn cohorts and enterprise procurement timelines—some investors will assume you’re mis-staged. Others may still invest, but you’ll spend time correcting their mental model.

Geography Fit Is Mostly About Network and Execution

Geography is often less about where you live and more about where the firm’s partners can reach customers, talent, and follow-on capital. It affects how quickly they can validate claims and help with hiring.

To assess geography fit, check:

- Where are your first customers located? If your buyers are concentrated in one region, align your narrative to that reality.

- Where do you already have credibility? Advisory boards, early hires, and customer references in the target region matter.

- How will the firm add value locally? If they can’t introduce you to relevant operators or buyers, they may still invest, but they’ll be slower.

Example: A firm headquartered in Europe may still fund a US startup if your early customers are in Europe and you can show local traction. If your traction is US-only and your team is US-only, you’ll need stronger proof that the firm’s network is still useful.

Mind Map: Thesis Fit Signals

Turning Fit into a Practical Pitch Structure

A thesis-fit pitch should reduce investor effort. Use a three-part sequence:

- One-sentence positioning: “We help [buyer] do [workflow] by [mechanism].”

- Evidence in their language: pick one metric or customer story that matches how they judge this sector.

- Fit justification: explain why your stage and geography match their pattern, or acknowledge the mismatch and show why it won’t block execution.

Example: If you’re raising seed for a B2B compliance product, don’t just say “we’re growing.” Show a pilot conversion story, then connect it to the firm’s sector evidence standard. If your customers are outside the firm’s home region, show how you already built local credibility through a specific customer relationship and a hiring plan that supports that region’s go-to-market.

Common Misreads That Make Fit Look Worse Than It Is

Investors sometimes label “not a fit” when the pitch doesn’t map to their internal checklist. Watch for these avoidable issues:

- Sector mismatch by framing: using consumer metrics for a B2B sales cycle.

- Stage mismatch by expectations: presenting late-stage claims without the underlying retention or sales process.

- Geography mismatch by omission: ignoring where customers are and how you’ll operate there.

A good rule: if you can’t point to one concrete example that supports sector, stage, and geography fit, your thesis alignment is still mostly hope. Replace hope with evidence, one claim at a time.

2.4 Evaluating Risk Factors Investors Screen for in Early Deals

Early-stage investors are not trying to be pessimists. They’re trying to avoid predictable failure modes using limited information. Risk screening is therefore a structured process: identify what can break, estimate how likely it is, and check whether the team has already built evidence that the break is unlikely.

The Risk Map Investors Use

Most risk checks fall into five buckets that show up repeatedly across seed and Series A conversations: market risk, product risk, traction risk, execution risk, and financial risk. Each bucket has observable signals, and each signal has a “what would I expect to see if this is going well?” counterpart.

Market Risk

Market risk asks whether customers actually have the problem and whether the company can reach them. Investors look for problem clarity first: can the team describe who feels the pain, how they currently solve it, and what makes the current workaround expensive in time or money?

A simple example: a founder says, “We sell to HR teams.” That’s a category, not a customer. A stronger signal is, “We sell to mid-market companies with 200–800 employees that are rolling out performance reviews and need audit-ready documentation.” The second statement implies a buying trigger and a path to identifying prospects.

Investors also test customer access. They look for evidence that the team can find and engage the target buyer without heroic effort. If the only channel is “we’ll do outbound,” the risk is that the company has no proof of message-market fit. A practical counter-signal is a short list of target accounts with documented outreach results and conversion rates.

Product Risk

Product risk is about whether the solution works well enough to be adopted. Investors typically focus on three things: solution fit, reliability, and differentiation.

Solution fit shows up as repeatable value delivery. For a B2B SaaS product, that might be “time-to-first-value” measured from signup to the first completed workflow. If customers take weeks to get value, adoption becomes fragile.

Reliability is often overlooked in early demos. Investors ask questions like: how often does the product fail, what are the top support tickets, and what percentage of sessions complete successfully. Even basic metrics help. For example, “99.2% successful workflow runs over the last 30 days” is more useful than “it’s stable.”

Differentiation is not a slogan. It’s a defensible mechanism: data advantage, workflow integration, switching costs, or a technical constraint that competitors can’t easily replicate. Investors look for “why you” that can be explained without hand-waving.

Traction Risk

Traction risk is whether early interest turns into consistent usage or revenue. Investors screen for leading indicators, not just totals.

For usage-based products, they look at retention and cohort behavior. A common red flag is high initial signups with flat or declining week-4 usage. A counter-signal is improving retention after onboarding changes, with a clear before-and-after explanation.

For revenue-based products, they look at sales cycle signals and deal quality. Investors ask: are deals small because the product is weak, or small because the market is early? They also check whether revenue is recurring or one-time. A concrete example: “10 customers, $30k MRR, churn is 2% monthly” is a different risk profile than “10 customers, $30k annual contracts, no renewal history.”

Execution Risk

Execution risk is whether the team can build and sell the product under real constraints. Investors evaluate capability through past work, but they also evaluate judgment through current decisions.

They look for a realistic hiring plan tied to milestones. If the roadmap requires three engineering hires and one sales hire, investors expect the plan to match the timeline and budget. They also look for operational discipline: do you track bugs, measure onboarding steps, and run experiments with documented outcomes?

A helpful example is onboarding iteration. If the team can explain how they reduced time-to-first-value from 14 days to 5 days by changing a specific workflow step, that shows learning velocity.

Financial Risk

Financial risk is about survival and capital efficiency. Investors screen runway because it determines how many mistakes you can afford. They also screen burn rate against milestones: spending should correlate with measurable progress.

Unit economics matter even early. Investors don’t require perfect numbers, but they require coherent assumptions. For instance, if customer acquisition cost is estimated from a small sample, the team should state the sample size and what would change the estimate.

A practical checklist investors use:

- Runway in months at current burn

- Burn breakdown by category (engineering, sales, cloud, contractors)

- Revenue or usage trend with a defined metric

- Evidence that spending is tied to a milestone (not just “we need time”)

Putting It Together with a Risk Scorecard

Investors often translate the buckets into a scorecard that supports consistent decision-making. The goal is not to “grade” the startup; it’s to identify which risk is currently dominant.

Risk Scorecard

- Market: 1–5 (problem clarity, access proof)

- Product: 1–5 (fit, reliability signals, differentiation)

- Traction: 1–5 (retention/usage or recurring revenue quality)

- Execution: 1–5 (milestones, learning velocity, operational discipline)

- Finance: 1–5 (runway, burn-to-milestone alignment, coherent assumptions)

Dominant risk: the lowest score with the least evidence

Mitigation evidence: what the team has already done to reduce it

When founders can point to mitigation evidence—like improved onboarding metrics, documented conversion rates, or clearer customer access—the screening conversation shifts from “what could go wrong?” to “what have you already proven you can handle?”

2.5 Knowing Common Deal Terms and What They Signal

Deal terms are the investor’s way of translating risk into structure. The same word can mean different things across firms, so treat each term as a signal about priorities: control, downside protection, alignment, and how the investor expects to get paid.

The Core Economic Terms

Valuation and Price Per Share Valuation sets the starting point for ownership. If an investor pushes a low valuation, they’re pricing in more perceived risk or expecting stronger downside protection elsewhere. Example: a seed round at a $6M pre-money means the new investors receive a larger slice than a $10M pre-money round, even if the round size is identical.

Round Size and Ownership Target Investors often aim for a specific ownership percentage. If the round is small relative to the company’s needs, the investor may be trying to keep dilution limited for themselves while still gaining meaningful influence.

Liquidation Preference This term determines who gets paid first if the company is sold or liquidated. A 1x non-participating preference means investors get their money back before common holders, but they don’t also share in the remaining proceeds. A participating preference lets them get their preference and then share again, which can heavily reduce outcomes for founders and employees. Signal: participating terms usually indicate a stronger preference for downside certainty.

Participation Cap If participation exists, a cap limits how much investors can receive. A cap is a compromise: it protects investors from worst-case scenarios while preserving some upside for others.

The Conversion and Anti-Dilution Terms

Convertible Notes and SAFEs Notes convert into equity later, usually at a discount or with a valuation cap. SAFEs convert similarly but typically without interest. Signal: a discount or cap suggests the investor expects the next priced round to be higher, and they want a built-in adjustment.

Discount Rate A discount (for example, 20%) means conversion happens as if the next round price were lower. Example: if the next priced round values shares at $2.00, a 20% discount converts at $1.60.

Valuation Cap A cap sets a maximum valuation for conversion. Example: with a $8M cap, even if the next round values the company at $12M, the SAFE converts as if the company were worth $8M.

Anti-Dilution Protection Anti-dilution adjusts conversion terms if the company issues equity at a lower price later. A “weighted average” approach is generally less punitive than “full ratchet.” Signal: full ratchet indicates a strong concern that the company may need to raise at a lower valuation.

Control and Governance Terms

Board Composition and Voting Rights Board seats and voting thresholds shape how decisions get made. If an investor requests board control early, they’re signaling a desire to actively manage risk. Example: a board with two investor directors and one founder director can shift outcomes on budgets and hiring.

Protective Provisions Protective provisions require investor approval for major actions like issuing new shares, changing the charter, or taking on debt. Signal: extensive protective provisions indicate the investor wants veto power over events that could dilute or change risk.

Information Rights These specify what the company must share and how often. Signal: frequent reporting requests often correlate with a hands-on investor style or a need to monitor cash closely.

Liquidation, Exit, and Transfer Terms

Drag-Along Rights Drag-along rights allow a majority (often including preferred holders) to force minority holders to participate in a sale. Signal: drag rights reduce holdout risk for investors and acquirers.

Pro Rata Rights Pro rata rights let investors maintain their ownership by participating in future rounds. Signal: pro rata rights show the investor expects to stay involved and wants to avoid dilution.

ROFR and Transfer Restrictions Right of first refusal and restrictions on share transfers control who can buy shares. Signal: these terms reduce surprises in the cap table and help investors manage who becomes a new shareholder.

Mind Map: Deal Terms and Their Signals

Putting It Together with a Practical Example

Imagine a seed round where the term sheet includes a 1x non-participating liquidation preference, a valuation cap on a SAFE, and standard protective provisions.

- The 1x non-participating preference signals downside protection without stacking extra upside on top.

- The valuation cap signals the investor expects a higher priced round later and wants a fair conversion anchor.

- Standard protective provisions signal they want control over major risk events, but not day-to-day interference.

Now compare that to a term sheet with participating preference, full ratchet anti-dilution, and broad veto rights. The combination signals stronger fear of downside and a higher likelihood the investor expects the company to face pricing pressure later.

Quick Term-to-Question Checklist

When you see a term, ask what it changes in a real scenario:

- If there’s a preference, who gets paid first and how much?

- If there’s a cap or discount, what happens if the next round price is higher or lower?

- If there are protective provisions, which future actions become harder?

- If there are pro rata rights, how much future dilution is effectively pre-allocated?

This approach keeps the discussion grounded in mechanics, not vibes, and it makes negotiation more precise.

3. Choosing the Right Capital Instruments

3.1 Comparing Equity Rounds Convertible Notes and SAFEs

When founders compare equity rounds, convertible notes, and SAFEs, they’re really comparing three ways to handle one question: what happens between “we need money now” and “we can agree on a valuation later.” The differences show up in timing, pricing mechanics, investor protections, and how much paperwork you’ll manage.

Mind Map: Funding Instrument Decision

Foundational Mechanics

Equity rounds sell shares at a stated price. Investors become shareholders immediately, and the company’s cap table reflects the new ownership right away. This clarity is useful when you already have enough traction to justify a valuation and when you want clean governance from day one.

Convertible notes start as a loan. The note accrues interest, and it has a maturity date. If the company raises a priced equity round before maturity, the note converts into equity using agreed conversion terms. If not, the maturity date can force repayment or renegotiation.

SAFEs (Simple Agreement for Future Equity) are not debt and typically do not include interest or maturity. They convert into equity when a triggering event occurs, most commonly a priced equity round. The conversion math is governed by discount and/or a valuation cap.

Conversion Triggers and What They Mean

In practice, the biggest operational difference is what triggers conversion.

- In an equity round, there is no conversion event. The deal is already equity.

- In a note, conversion is usually tied to a future equity financing, and the note’s maturity date still matters if that financing is delayed.

- In a SAFE, conversion is also tied to a future equity financing, but without maturity pressure.

A simple example: suppose you raise $1,000,000 and expect a priced round in 12 months.

- With an equity round, you agree on valuation now, and everyone knows their ownership.

- With a note, you agree on conversion rules now, but the note also accrues interest during those 12 months.

- With a SAFE, you agree on conversion rules now, and the agreement avoids interest and maturity, so the company’s cash planning is simpler.

Pricing: Discount, Valuation Cap, and Effective Price

Convertible notes and SAFEs often use the same two levers: a discount and a valuation cap.

- A discount gives the investor a lower effective price than the price paid by new investors in the next priced round.

- A valuation cap sets a maximum valuation used to calculate conversion.

Consider a priced round where new investors pay $2.00 per share.

- If an instrument has a 20% discount, it converts at $1.60 per share.

- If it has a $10M valuation cap, conversion uses the cap valuation to compute the share price, which may be lower than the priced round price.

If both are present, the agreement usually uses whichever produces the lower conversion price. That “whichever is lower” detail matters because it determines how much equity the investor receives.

Investor Protections and Founder Tradeoffs

Equity rounds typically include protective provisions and governance rights negotiated as part of the share purchase. The tradeoff is time: agreeing on valuation and terms can take longer, and the cap table changes immediately.

Convertible notes often include additional investor protections because they are debt-like. Interest accrual increases the eventual conversion amount, and the maturity date can create leverage for investors if fundraising stalls.

SAFEs reduce complexity by removing debt mechanics. However, investors still negotiate conversion terms and sometimes additional rights. The tradeoff is that SAFEs can be less precise about certain economic outcomes than a fully priced equity round, so founders must be careful about how the conversion math interacts with future financing.

Paperwork and Cap Table Impact

A clean rule of thumb: the earlier you sell equity, the more immediate the cap table work; the later you convert, the more you must track conversion math.

- Equity round: immediate share issuance and straightforward ownership records.

- Convertible note: you track principal, interest accrual, and conversion upon trigger.

- SAFE: you track the SAFE amount and conversion calculation, usually without interest.

Mind Map: Practical Comparison Checklist

Choosing the Instrument for the Moment

If your company can support a credible valuation and you want immediate shareholder alignment, an equity round is the cleanest path.

If you need speed and prefer to postpone valuation while still accepting debt-like mechanics, a convertible note can fit, but founders should treat maturity and interest as real economic variables, not fine print.

If you want a simpler instrument that postpones valuation without debt mechanics, a SAFE is often the most straightforward option, provided you model conversion outcomes carefully for the next priced round.

A practical closing example: imagine two founders raising at the same time.

- Founder A raises an equity round at a $12M valuation.

- Founder B raises a SAFE with a $12M valuation cap and a 20% discount.

If the next priced round values the company at $20M, Founder B’s effective conversion price will be lower due to the cap and/or discount, resulting in more shares for the SAFE holders than Founder A’s investors received for their $12M valuation. That’s not good or bad by itself; it’s the direct consequence of deferring valuation and setting conversion rules.

3.2 Using Preferred Stock Terms to Balance Control and Economics

Preferred stock is the “grown-up” version of equity: it keeps the upside of ownership while adding rules that protect investors when outcomes are uneven. The trick is balancing control (who can steer decisions) with economics (who gets paid first and how much).

Foundational Concepts Investors Care About

Start with three baseline questions.

-

What happens if the company does well? Preferred terms should still allow common holders to participate meaningfully, usually through conversion.

-

What happens if the company struggles? Investors want downside protection, typically via liquidation preference and anti-dilution.

-

Who decides? Governance rights determine whether investors can block actions that affect value, like issuing new shares or selling the company.

A useful mental model is: economics set the payment order; control sets the decision order. You can have strong economics with limited control, or vice versa, but the combination should match the risk the investor is taking.

Economics Terms That Shape Payouts

Liquidation Preference

Liquidation preference defines the payout waterfall if the company is sold, liquidated, or otherwise exits. Common structures include:

- 1x non-participating: Investor gets their original investment back first; then remaining proceeds split according to conversion to common.

- 1x participating: Investor gets their preference first and then also shares in the remaining proceeds.

Example: An investor puts in $5M for preferred. In a $30M acquisition, a 1x non-participating preferred typically converts and shares like common, so founders and employees still benefit. With 1x participating, the investor may receive $5M first and then still share, reducing what’s left for everyone else.

Conversion Rights

Most preferred converts to common, either automatically at an IPO or at the investor’s option. Conversion is how investors participate in upside without giving up protection.

Example: If the preferred converts at a 1:1 ratio, then in a strong exit the preferred behaves like common. If conversion is adjusted by anti-dilution, the effective conversion rate can improve for investors after down rounds.

Anti-Dilution

Anti-dilution protects investors when the company issues shares at a lower valuation later.

- Full ratchet: The conversion price resets to the lowest price paid in a later round. This can be harsh to founders and employees.

- Weighted average: Adjusts conversion price using a formula that considers both the new price and the amount of new shares.

Example: Suppose preferred converts at $2.00 per share. A later round prices new shares at $1.50. With weighted average, the conversion price moves down but not all the way to $1.50 unless the new issuance is large enough to justify it.

Control Terms That Shape Decision Power

Preferred stock often comes with protective provisions. These are not “day-to-day control,” but they can block major actions.

Typical protective matters include:

- Issuing senior or pari passu securities

- Changing charter documents in ways that affect investor rights

- Authorizing new share classes or increasing option pool beyond agreed limits

- Selling the company or merging

Example: If the company wants to raise a bridge round that includes new preferred with senior liquidation preference, protective provisions can require investor consent. That prevents a scenario where new money changes the payout order midstream.

The Balance: How Terms Interact

Preferred terms rarely operate in isolation. A common pattern is:

- Stronger economics (participating preference, aggressive anti-dilution) often comes with fewer governance rights.

- Stronger control (more protective provisions, board seats) can be paired with less aggressive economics.

Example: A seed investor might accept a 1x non-participating preference but request board observation and consent on major financings. A later-stage investor might accept fewer consent rights if the liquidation preference and anti-dilution are already protective.

Mind Map: Control and Economics Tradeoffs

Practical Negotiation Examples

Example: Choosing Between Participating and Non-Participating

If the company expects a range of outcomes, non-participating is often easier to justify because it preserves upside for common holders after the investor is made whole.

Example: In a $50M exit, a participating preference can cause the investor to receive more than their original investment plus a share of the remainder, leaving less for employees. Non-participating typically results in conversion and a more “common-like” outcome.

Example: Anti-Dilution Standard Selection

Weighted average is usually the compromise because it protects investors without fully resetting conversion based on a single later price.

Example: If a down round happens due to temporary market conditions, weighted average reduces the chance that one financing event permanently rewrites the economics for everyone.

A Simple Term Checklist for Founders

Before signing, verify that each term answers a concrete question:

- Payment order: Is the liquidation preference non-participating or participating?

- Upside participation: Under what conditions does preferred convert?

- Downside protection: Is anti-dilution full ratchet or weighted average?

- Decision power: Which actions require investor consent?

- Consistency: Do the control rights match the level of economic protection?

When these pieces align, preferred stock becomes a structured compromise rather than a surprise mechanism. The goal is not to eliminate investor protection, but to make it predictable and proportional to the risk being priced.

3.3 Applying Valuation Methods for Early Stage Rounds

Early stage valuation is less about finding a single “correct” number and more about choosing a method that matches what you can prove today. Investors are usually underwriting three things: the risk that the product won’t work, the speed at which traction can compound, and the dilution they’ll experience if the company needs more capital later. Your job is to make those risks measurable, then translate them into valuation logic.

Start with What You Can Actually Measure

Before any math, separate evidence into three buckets:

- Current traction: revenue, usage, retention, pipeline, or signed pilots.

- Execution capacity: team capability, delivery milestones, and operational cadence.

- Market access: distribution channels, customer segments, and sales cycle reality.

If you only have an idea and a prototype, valuation methods will rely more heavily on comparable deals and risk adjustments. If you have repeatable revenue or strong retention, you can justify valuation with unit economics and growth rates.

Mind Map: Early Stage Valuation Inputs

Comparable Deal Method with Realistic Adjustments

The comparable method starts with recent seed and Series A transactions in similar sectors and geographies. The key is to adjust for differences that change risk, not just scale.

Use a simple adjustment checklist:

- Stage alignment: compare companies with similar traction quality, not just “seed.”

- Business model alignment: usage-based SaaS behaves differently from services or marketplaces.

- Geography and hiring intensity: cost structure affects how quickly milestones can be reached.

- Customer proof: pilots with no repeat usage are not the same as retention-backed revenue.

Example: If a comparable company raised at a $10M pre-money with monthly retention of 80% and you have 50%, you should expect a lower valuation unless your growth rate or margins compensate. Investors often express this as a discount to reflect higher uncertainty.

Venture Capital Method with a Clear Exit Assumption

The venture capital method works backward from an expected exit value. It’s popular because it forces you to state what “success” means and how much ownership investors need to earn.

Core steps:

- Choose an exit multiple or exit value based on comparable outcomes.

- Estimate the time to exit and the probability-weighted success path.

- Apply an investor required return to compute the maximum price today.

Example: Suppose an investor expects a $60M exit in 5 years and targets a 3x to 5x return on their money. If they want to own 20% to 30% post-money to achieve that outcome, the implied pre-money valuation range becomes constrained. If your current traction suggests a longer path to exit or higher failure probability, the same exit assumption yields a lower present valuation.

This method is not about predicting the future; it’s about stress-testing whether your story can support the ownership and return math.

Discounted Cash Flow with Guardrails

DCF can be misleading early because cash flows are uncertain and often negative. Still, it can be useful if you apply guardrails that prevent false precision.

Guardrails:

- Use scenario-based projections rather than a single forecast.

- Discount using a rate that reflects early-stage uncertainty.

- Tie projections to measurable drivers like retention, conversion, and gross margin.

Example: If you forecast revenue growth based on improving retention, show the chain: retention affects expansion, expansion affects revenue per customer, and revenue per customer affects total revenue. If you can’t connect those links, DCF becomes decorative.

A practical approach is to use DCF as a sanity check against other methods. If DCF suggests a valuation far above comparable deals without stronger evidence, you likely assumed too much too soon.

Scorecard and Risk Factor Adjustments Without Hand-Waving

Scorecard methods start from a baseline valuation for comparable deals, then adjust for factors like team strength, market size, product differentiation, and traction quality.

To avoid hand-waving, define each factor with observable criteria:

- Team: prior relevant execution, ability to ship, and customer-facing competence.

- Market: clear segment definition and evidence of willingness to pay.

- Product: measurable engagement or retention, not just feature lists.

- Traction: growth rate, churn, and pipeline conversion.

Example: Two startups both raise at seed. Startup A has strong retention but weak sales conversion; Startup B has decent conversion but churns quickly. A scorecard can justify different valuations by weighting the factor that most limits near-term cash generation.

Converging on a Valuation Range Investors Can Defend

In practice, strong rounds converge on a range that multiple methods support. A common workflow:

- Use comparable deals to set a baseline.

- Use venture capital method to check whether the implied ownership and return requirements are consistent with your traction and timeline.

- Use DCF only as a guardrail, ensuring projections are driver-based.

- Use scorecard adjustments to explain why your company deserves a higher or lower position within the range.

When you present valuation, focus on the reasoning chain: evidence → risk assessment → method choice → implied ownership. That’s what makes the number feel earned rather than guessed.

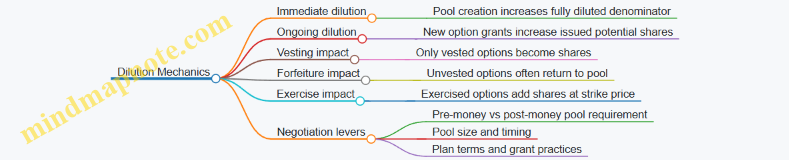

3.4 Designing Option Pools and Understanding Dilution Mechanics

An option pool is a pre-allocated slice of a company’s equity reserved for hiring and retaining people. Investors care because the pool affects ownership percentages, and founders care because the pool affects how much equity you can grant without constantly renegotiating terms. The trick is to size the pool correctly and understand how dilution works when the pool is created and when options are later exercised.

Option Pool Basics and Why It Exists

Start with the purpose: you need a mechanism to grant equity to employees and sometimes advisors. Without a pool, every grant either reduces the founder’s and existing holders’ percentages immediately or requires amendments and approvals that slow hiring.

A simple mental model: the pool is created first, then individual option grants happen over time. The pool is not “spent” all at once; it’s a budget.

Mind Map: Option Pool Components

Sizing the Pool Without Guessing

Sizing is not a single number; it’s a set of assumptions. Use a hiring plan and translate it into equity needs.

- Estimate headcount growth. Example: you plan to hire 6 people over 18 months.

- Assign typical grant ranges. Example: early engineers might receive 0.5%–1.0% each, while a senior hire might receive 1.0%–2.0% depending on level and market.

- Account for forfeiture. Options often return to the pool when employees leave before vesting.

- Decide whether you want a refresh. If you plan another hiring wave, you may need a larger pool now or a smaller pool with a later increase.

A practical approach: build a “grant budget” table for roles and expected start dates, then add a buffer for attrition. If your plan is vague, investors will assume the worst-case and push for a bigger pool.

Fully Diluted Shares and the Dilution Equation

Dilution is about percentages changing as new shares enter the cap table. Option pools are usually expressed as a percentage of “fully diluted” shares, meaning the denominator includes shares that could be issued under existing instruments.

When you create an option pool, you typically increase the share count immediately, even though options are granted later. That creates immediate dilution for existing holders.

Example: Suppose the company has 10,000,000 fully diluted shares before the pool. You create a 10% option pool on a fully diluted basis. The pool effectively increases the denominator, so existing holders’ percentages drop even before any individual grant.

A useful way to compute it: if the pool is X% of post-pool fully diluted shares, then the pre-pool holders’ ownership becomes (1 − X). In the example, existing holders collectively become 90% of the post-pool fully diluted capitalization.

Pre-Round Versus Post-Round Pool Creation

Whether the pool is created before or after a financing changes who bears the dilution.

- Pre-round pool: founders and existing holders absorb dilution before new investors come in.

- Post-round pool: new investors may effectively share the dilution because they buy into a capitalization that already includes the pool.

Example: If investors require a 10% pool, they may negotiate whether that 10% is carved out of the pre-money or post-money capitalization. The difference affects both founder ownership and investor economics.

Vesting, Forfeiture, and How the Pool “Recycles”

Options usually vest over time, often with a four-year schedule and a one-year cliff. If someone leaves before vesting, unvested options typically expire and return to the pool.

This matters for dilution mechanics because the pool percentage is based on the total options authorized, not on how many ultimately vest. Over time, forfeitures reduce the number of shares that actually get issued.

Example: You grant 100,000 options to an employee. If they leave after 9 months, only the cliff portion vests (often zero), and the remaining options return to the pool. The pool authorization stays the same, but the issued shares are lower than the maximum.

Mind Map: Dilution Mechanics

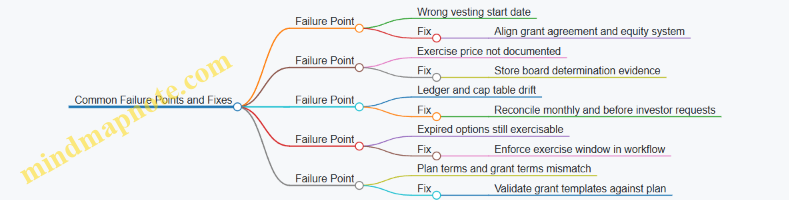

Common Mistakes and How to Avoid Them

- Oversizing the pool “just in case.” It dilutes everyone immediately and can make future hiring harder to justify.

- Undersizing the pool and then increasing it later without a clear plan. Investors may treat later increases as a signal that the original assumptions were weak.

- Ignoring role-based grant sizes. A pool sized for 6 hires at one equity level will not work if you later hire a different profile.

- Treating the pool as a one-time event. If your hiring cadence changes, your pool strategy should change too, but with clear reasoning.

A Simple Worked Example for Founder Ownership

Assume pre-round fully diluted shares are 10,000,000. You negotiate a 10% option pool created pre-round. After pool creation, existing holders collectively hold 90% of the post-pool fully diluted shares.

If you later grant and vest options that result in shares being issued, your ownership percentage can drop further. The key is that the first drop happens when the pool is created, and the next drops happen as options vest and are exercised.

Designing the pool well means you can explain both steps: why the pool size is reasonable, and how the company will manage grants so the pool is used efficiently rather than inflated.

3.5 Selecting Investor Rights and Protective Provisions

Investor rights are the “how we communicate and how we prevent surprises” layer of a financing. Protective provisions are the “you can’t change these basics without investor consent” layer. Together, they shape day-to-day governance and define which decisions require a vote, which require notice, and which are simply off-limits.

Start with a simple principle: the more rights investors have, the more operational friction you should expect. That friction isn’t automatically bad—especially when it prevents value leakage—but it should match the risk investors are taking. Early rounds often grant fewer rights than later rounds, and strategic investors sometimes negotiate more than financial investors.

Mind Map: Investor Rights and Protective Provisions

Information Rights That Actually Help

Information rights typically include periodic updates and notice of significant events. Monthly reporting is common, but the content should be realistic for your team. A practical package might include: cash on hand, net burn for the month, runway based on current burn, and a KPI table tied to your operating plan. If you don’t have clean KPI definitions yet, investors will still ask—so define them before you promise them.

Notice rights matter when they prevent investors from learning about major issues through the market or employees. For example, if you enter a contract that materially changes customer economics, investors may want advance notice. The key is to define “material” with a threshold, such as a percentage of annual revenue or a fixed dollar amount, so you’re not negotiating every time a contract is signed.

Governance Rights That Define Decision Flow

Governance rights cover board structure and voting mechanics. Preferred investors often request board seats proportional to their ownership or a minimum number of seats. Even if you keep board seats limited, you still need to specify what happens when the board can’t agree.