Hedge Fund Strategies and Absolute Return Investing Essentials

1. Foundations of Absolute Return Investing

1.1 Defining Absolute Return and Risk Adjusted Performance

Absolute return means the portfolio aims to produce a positive result over a defined period regardless of whether the overall market is up or down. Risk adjusted performance means you do not just ask, “Did we make money?” You also ask, “How hard did we work for it, and what did it cost in risk?” A strategy can look great on raw returns and still be a poor fit if it required extreme drawdowns or relied on fragile assumptions.

Absolute Return: What It Really Measures

Absolute return is usually expressed as a percentage change in net asset value over a measurement window. The key detail is that it is portfolio-level, not a single trade-level outcome. For example, if a fund’s net value rises from 100 to 103 over a quarter, the absolute return is +3% for that quarter.

However, absolute return alone can mislead. A portfolio that earns +3% with a 20% peak-to-trough drawdown may be less attractive than one that earns +3% with a 6% drawdown. That is why risk adjusted performance matters.

Risk Adjusted Performance: The “Cost of Getting There”

Risk adjusted performance converts return into a score that accounts for volatility, drawdowns, or downside behavior. The most common inputs are:

- Volatility: how variable returns are over time.

- Downside risk: how bad losses can be, not just how often they happen.

- Drawdown: the size of the worst decline from a prior peak.

A simple example: Strategy A averages +8% annual return with 16% volatility, while Strategy B averages +8% with 8% volatility. Even if both have the same average return, Strategy B is typically preferred because its outcomes are more stable.

The Core Metrics You Will Use

Absolute return and risk adjusted performance are often summarized with a small set of metrics that complement each other.

1) Sharpe Ratio

Sharpe ratio compares excess return to volatility. If a strategy earns 10% and the risk-free rate is 4%, the excess return is 6%. If volatility is 12%, Sharpe is 6% / 12% = 0.5.

2) Sortino Ratio

Sortino replaces total volatility with downside deviation. This helps when upside swings are large but losses are the real concern.

3) Maximum Drawdown

Maximum drawdown measures the worst peak-to-trough decline. It is not a “forecast,” it is a historical stress snapshot of how the strategy behaved.

4) Calmar Ratio

Calmar ratio is annual return divided by maximum drawdown. If a strategy returns +12% and its maximum drawdown is -6%, Calmar is 12% / 6% = 2.

These metrics work best together. Sharpe can look fine even when drawdowns are uncomfortable; drawdown alone can ignore how quickly recovery happens.

A Practical Example with Integrated Reasoning

Consider two hypothetical quarterly outcomes:

- Portfolio X: +2% return, 5% volatility, -4% max drawdown.

- Portfolio Y: +2% return, 10% volatility, -12% max drawdown.

Both have the same absolute return, so the decision hinges on risk. Portfolio X shows tighter variability and a smaller worst decline, which usually improves investor experience and reduces the chance that risk limits force premature de-risking.

Now add one more nuance: if Portfolio Y’s drawdown occurs early in the quarter and recovery is slow, the strategy may trigger operational or mandate constraints even if the quarter ends positive. Absolute return can be positive while the path is still problematic.

Mind Map: Absolute Return and Risk Adjusted Performance

Putting It Into a Simple Working Definition

For practical use, treat absolute return as the outcome target and risk adjusted performance as the quality control. A strategy is “absolute return oriented” when it is designed to produce positive net results across varying market conditions, and it is “risk adjusted” when its evaluation explicitly penalizes volatility and drawdowns rather than pretending they do not exist.

1.2 Hedge Fund Role in Portfolio Construction and Diversification

Hedge funds are often used to improve a portfolio’s risk-adjusted performance, not by chasing the highest return, but by changing how risk is delivered. In portfolio construction, “diversification” means more than holding many positions; it means combining exposures that do not move together in the same way, at the same time, for the same reasons.

What Hedge Funds Add to a Portfolio

A typical hedge fund strategy can contribute one or more of these building blocks:

- Return sources that are not tied to a single market beta, such as relative value trades or event-driven spreads.

- Downside behavior that differs from equities, for example through hedging, market neutrality, or defined-risk structures.

- Diversified risk factors like volatility, credit spreads, or cross-asset relationships rather than only equity direction.

A useful mental model is to treat a hedge fund as an “exposure engine.” You want to know which exposures it runs (explicitly or implicitly), how those exposures respond under stress, and how they interact with the rest of your portfolio.

Diversification Beyond Correlation

Correlation is a starting point, but it can mislead when relationships change. Hedge fund diversification is better evaluated with three lenses:

- Sensitivity: How does the strategy’s P&L respond to equity moves, rates, credit spreads, and volatility?

- Path dependence: Does the strategy lose money during drawdowns even if the long-run average looks fine?

- Tail behavior: Are losses clustered in specific scenarios, such as liquidity gaps or funding stress?

For example, two strategies can both have low average correlation to equities, yet one may suffer large losses during equity selloffs while the other holds up due to hedged exposures.

Portfolio Construction Workflow

A systematic approach keeps the process from becoming a collection of opinions.

- Start with the portfolio’s current exposures

- Estimate factor exposures (equity beta, duration, credit sensitivity, volatility exposure) for your existing holdings.

- Translate the hedge fund into exposures

- Use historical returns, holdings data when available, and strategy mechanics to infer sensitivities.

- Set objectives and constraints

- Decide what “better” means: lower drawdown, steadier returns, reduced volatility, or improved performance net of fees.

- Run a risk-aware allocation

- Allocate based on marginal risk contribution, not just expected return.

- Stress test the combination

- Evaluate performance under scenarios that matter for the strategy’s failure modes.

A practical rule: if you cannot explain what the hedge fund is likely to be doing during a market shock, you are not ready to size it.

Mind Map: Hedge Fund Diversification in Practice

Example: Using a Market-Neutral Strategy

Suppose your portfolio is equity-heavy and has a high equity beta. You consider a market-neutral long-short equity strategy.

- What you want to confirm: the strategy’s equity beta is near zero, and its main exposures are stock-specific and sector-relative.

- What you test: performance during equity selloffs. If the strategy’s losses spike when volatility rises, you may be buying “equity neutrality” that breaks under stress.

- How you size: you allocate based on marginal contribution to portfolio drawdown, not on average correlation.

If the strategy reduces drawdowns but increases volatility modestly, it can still be a net improvement because the objective is risk-adjusted performance.

Example: Adding Relative Value to a Credit-Sensitive Portfolio

If your portfolio already has meaningful credit spread exposure, a relative value fixed income hedge fund may help by targeting spread mispricings rather than taking outright credit beta.

- What you want to confirm: the strategy’s duration and credit sensitivity are controlled, and the P&L is driven by spread relationships.

- What you test: whether the strategy hedges well when correlations between credit instruments rise.

In this case, diversification comes from changing the “where the risk lives” question: you want credit risk that is more selective and less directionally tied to the overall credit cycle.

Key Takeaway

Hedge funds earn their place in portfolio construction when they provide identifiable, testable exposure differences. Diversification is not a label; it is a measurable change in how risk is generated, experienced over time, and realized under stress.

1.3 Core Performance Metrics and Their Practical Interpretation

Absolute return sounds simple until you try to measure it. Metrics turn “it felt good” into numbers you can compare across strategies, time periods, and risk levels. The trick is to interpret each metric in context: what it rewards, what it hides, and what it assumes.

Performance Metrics Mind Map

Return Metrics That Set the Baseline

Total return answers a straightforward question: what did the strategy make over the measurement window? For example, if a portfolio grows from 100 to 112 over a year, total return is 12%. This metric is useful, but it ignores how bumpy the ride was.

Annualized return converts different time spans into a comparable rate. If the same 12% happened over 6 months, the annualized return is roughly 1.12² − 1 ≈ 25.4%. The practical point: annualization can make short, lucky periods look more impressive than they are.

Rolling return helps you see whether performance is stable or clustered. Suppose a strategy posts +2% per month for 10 months, then −15% in month 11, then +2% in month 12. Total return might still be positive, but rolling results reveal the “lumpiness” that risk metrics should capture.

Risk Metrics That Explain the Ride

Volatility measures dispersion of returns. If monthly returns average 1% with a standard deviation of 4%, volatility is 4% per month (convert to annual by multiplying by √12 for a rough estimate). Volatility is easy to compute, but it treats upside and downside symmetrically, which can be misleading for strategies that aim to avoid large losses.

Maximum drawdown captures the worst peak-to-trough decline. Example: equity peaks at 120, then falls to 96 before recovering. Drawdown is (96/120 − 1) = −20%. Two strategies can share similar volatility but have very different drawdowns; investors usually feel drawdowns more than they feel volatility.

Tail risk focuses on extreme outcomes. A simple practical proxy is the worst 5% monthly loss (a quantile). If Strategy A’s worst 5% month is −8% and Strategy B’s is −15%, A has a better downside profile even if both have similar average returns.

Risk-Adjusted Metrics That Compare Apples to Apples

Sharpe ratio is the classic: (average excess return) / (return volatility). If monthly excess return averages 0.5% and monthly volatility is 3%, Sharpe ≈ 0.5/3 = 0.167 per month. Annualizing Sharpe is often done by multiplying by √12, giving about 0.58. Interpretation: higher Sharpe means more return per unit of total variability. Limitation: it penalizes upside volatility too.

Sortino ratio replaces total volatility with downside deviation. If average return is 0.5% monthly, but only months below 0% contribute to downside deviation, Sortino can reward strategies that generate upside without frequent deep negatives. Example: two strategies both have 3% volatility, but one has many small negative months and the other has occasional large losses; Sortino typically distinguishes them.

Calmar ratio uses annualized return divided by maximum drawdown magnitude. If annualized return is 10% and max drawdown is −25%, Calmar = 10/25 = 0.40. This metric is practical for absolute return because it directly links reward to the pain investors actually experience.

Information ratio compares active return versus a benchmark divided by tracking error. Even for “absolute return” strategies, you still need an opportunity-cost benchmark. Example: if a strategy earns 6% while a cash-like alternative earns 4%, the active return is 2%. If tracking error is 3%, information ratio ≈ 0.67. Interpretation: it measures consistency of outperformance, not just level.

Practical Interpretation Rules That Prevent Misreads

- Match frequency and compounding. If you compute Sharpe on daily returns but report annualized return from monthly compounding, you can create inconsistencies.

- Use net returns when fees matter. A strategy with strong gross metrics can look mediocre net if turnover is high. Example: if gross Sharpe is 1.2 but fees reduce average return by 0.3% per month, the net Sharpe can drop sharply.

- Beware small samples. A few months can inflate ratios. Rolling windows and confidence intervals (even simple ones) help you judge stability.

- Check for leverage effects. If leverage increases, volatility and drawdowns often rise nonlinearly. A metric that looks “better” might simply be taking more risk in disguise.

- Separate performance from risk timing. A strategy might have a good Sharpe but still fail during specific regimes. Drawdown and tail metrics catch that mismatch.

A Worked Example with Integrated Metrics

Assume a strategy over one year has: total return +8%, annualized return +8% (same window), monthly volatility 4%, maximum drawdown −12%, and average monthly excess return over cash +0.3%.

- Sharpe ≈ 0.3/4 = 0.075 per month; annualized Sharpe ≈ 0.075√12 ≈ 0.26.

- Calmar = 8/12 ≈ 0.67.

- If downside deviation is 2.5% (because losses are less frequent than gains), Sortino ≈ 0.3/2.5 = 0.12 per month; annualized Sortino ≈ 0.12√12 ≈ 0.42.

Interpretation: the strategy’s drawdowns are moderate relative to its return (Calmar is decent), but its total variability is still high enough that Sharpe remains modest. That combination often points to a strategy that produces gains but with enough volatility to dilute risk-adjusted performance.

Summary of Metric Roles

Return metrics tell you what happened. Risk metrics tell you how it happened. Risk-adjusted metrics tell you whether the outcome was worth the risk, given the measure’s assumptions. When you read them together—especially Sharpe with drawdown and tail—you get a coherent picture instead of a single number that can be gamed by luck.

1.4 Constraints and Objectives That Shape Strategy Design

Strategy design starts with a simple question: what must be true for the strategy to work in the real world? Objectives tell you what “work” means, while constraints tell you what you are not allowed to do. When these two are aligned, the rest of the design becomes a sequence of choices that are easier to justify and easier to test.

Objectives That Define Success

An objective is not just a target return. It is a statement about the shape of outcomes.

- Absolute return goal: You want positive performance over a defined horizon, even if markets are flat or choppy. Example: a strategy that targets +6% annually with monthly volatility around 4%.

- Risk-adjusted goal: You care about drawdowns, not only average returns. Example: “Keep maximum drawdown under 10%” forces the strategy to avoid fragile exposures.

- Liquidity and capacity goal: You need returns that survive trading at realistic sizes. Example: if your average position turnover implies $50 million of daily trading, you must ensure spreads and slippage stay within a cost budget.

- Implementation goal: You need operational feasibility. Example: if the strategy requires frequent corporate action handling, you must set a constraint on how complex the security universe can be.

A practical way to write objectives is to pair each one with a measurable metric and a review cadence. If you cannot measure it monthly, you probably cannot manage it monthly.

Constraints That Limit Feasible Designs

Constraints are the guardrails that prevent “paper strategies” from becoming “paper losses.” They come from markets, portfolios, and operations.

- Capital and leverage constraints: Margin rules, internal risk limits, and funding costs cap how much exposure you can take. Example: if leverage is capped at 2x, a strategy that needs 3x to reach its return target must be redesigned.

- Shorting and borrow constraints: Availability and borrow rates limit short positions. Example: a pair strategy that assumes unlimited borrow will fail during stress when borrow becomes scarce.

- Trading cost constraints: Spreads, commissions, and slippage reduce expected returns. Example: if the expected edge is 0.20% per trade and average round-trip costs are 0.18%, you have almost no room for execution slippage.

- Market impact constraints: Large orders move prices. Example: a momentum strategy that rebalances daily may breach impact limits when volatility spikes.

- Model and data constraints: Missing data, stale corporate actions, and regime shifts limit what signals can reliably do. Example: a factor model built on stale fundamentals may look stable in backtests and drift in live trading.

- Operational and compliance constraints: Trading restrictions, approval workflows, and settlement rules affect what you can trade and when. Example: if certain instruments require pre-trade approvals, you cannot assume instantaneous execution.

Turning Objectives and Constraints Into Design Choices

Once objectives and constraints are explicit, you can translate them into design parameters.

- Choose the risk budget first. If maximum drawdown is capped, you set position sizing and exposure limits accordingly.

- Select the strategy family that matches the constraints. If shorting is constrained, long-only or market-neutral-with-borrow-management may be more feasible than pure long-short.

- Define the execution policy that fits the cost budget. If turnover is high, you must use tighter cost controls or lower turnover.

- Set monitoring rules that trigger de-risking. Constraints are not only for initial construction; they must be enforced continuously.

Mind Map: Objectives and Constraints to Strategy Parameters

Example: A Momentum Strategy with a Cost Budget

Suppose your objective is +8% annual absolute return with a maximum drawdown of 12%. Your constraints include a cost budget of 0.30% per round trip and a leverage cap of 1.5x.

- If you rebalance daily, turnover is high and average round-trip costs might reach 0.35%, exceeding the budget. The design choice is not “try harder,” it is to change the rebalance frequency or reduce trading intensity.

- If you switch to weekly signals, turnover drops and costs might fall to 0.25% per round trip, leaving room for the expected edge.

- If drawdown still threatens the 12% limit, you adjust volatility scaling and stop rules so that position sizes shrink during high-volatility regimes.

The key is that each constraint forces a specific parameter change: frequency for cost, sizing for drawdown, and leverage for funding feasibility.

Example: Pair Trading Under Borrow Constraints

A market-neutral pair strategy aims for stable returns by hedging beta and holding a spread position. The objective is low drawdown, but the constraint is borrow availability.

- In backtests, the short leg is always available, so the strategy looks consistent.

- In live trading, borrow becomes expensive or unavailable for certain names, causing missed entries and forced exits.

Design fixes are concrete: restrict the universe to names with reliable borrow, cap borrow rates, and add a fallback rule such as holding the long leg only when the short leg cannot be established within a defined cost threshold.

When objectives and constraints are written down early, the strategy stops being a collection of clever ideas and becomes a set of enforceable rules that can be tested, monitored, and improved without surprises.

1.5 Practical Example: Mapping Objectives to Strategy Choices

You can’t pick a hedge fund strategy by vibes. You start with objectives, translate them into constraints, and then match those constraints to what each strategy can realistically deliver. Here’s a systematic example that moves from foundational choices to implementation details.

Step 1: Write the Objective in Measurable Terms

Assume an investor wants:

- Target return: 6% annualized

- Risk tolerance: maximum 8% peak-to-trough drawdown

- Liquidity need: monthly subscriptions and redemptions

- Capital stability: avoid strategies that require frequent large leverage changes

A practical best practice is to convert “risk” into something you can monitor daily or weekly. For instance, you can translate drawdown tolerance into a volatility budget and a de-risking rule (for example, reduce gross exposure when portfolio volatility breaches a threshold).

Step 2: Translate Objectives Into Constraints

From the objective set, you derive constraints that will later eliminate unsuitable strategies.

- Drawdown constraint implies you need either (a) naturally defensive exposures, (b) hedges that respond quickly, or (c) position sizing that scales down during stress.

- Monthly liquidity implies you should avoid strategies with settlement or execution cycles that make pricing stale or trading too slow.

- Leverage stability implies you prefer strategies where risk can be managed through sizing and hedging rather than constant leverage rebalancing.

Step 3: Map Constraints to Strategy Families

Different strategy families “solve” different parts of the problem. The mapping below is intentionally blunt: it helps you decide what to test first.

Mind Map: Objective to Strategy Mapping

Step 4: Choose a Shortlist Using a Simple Scoring Rubric

A quick rubric prevents endless debate. Score each strategy family from 1 to 5 on each criterion, then sum.

Example criteria aligned to the constraints:

- Drawdown control (can the strategy reduce risk quickly?)

- Liquidity and pricing timeliness (can you trade and value consistently?)

- Leverage stability (can risk be managed without constant leverage swings?)

- Cost realism (can you model trading and hedging costs without hand-waving?)

Suppose you score:

- Market Neutral Equity: 5 (drawdown control), 4 (liquidity), 4 (leverage stability), 3 (cost realism) → 16

- Long Short Equity: 4, 4, 3, 3 → 14

- Fixed Income Relative Value: 4, 5, 4, 4 → 17

- Volatility Options: 3, 3, 4, 2 → 12

The top two are Fixed Income Relative Value and Market Neutral Equity. That doesn’t mean they’re “best,” only that they match the objective constraints more closely.

Step 5: Turn the Choice Into an Implementation Plan

Now you define the rules that make the strategy behave like the objective.

Example A: Market Neutral Equity sleeve

- Risk budget: target portfolio volatility of 6% with a hard cap at 8%.

- Sizing rule: scale gross exposure inversely with estimated idiosyncratic volatility.

- Hedge rule: maintain factor neutrality using a small set of liquid factors (for example, sector and style) and rebalance when exposures drift beyond thresholds.

- De-risking: if realized volatility breaches the cap for two consecutive weeks, cut gross exposure by 25% and tighten stop conditions.

Concrete example: if a pair trade’s spread z-score suggests entry but the factor exposure drift exceeds the threshold, you skip the trade or reduce size. This is how you prevent “good signals” from breaking the risk budget.

Example B: Fixed Income Relative Value sleeve

- Risk budget: limit key rate duration and spread risk so the sleeve contributes a controlled fraction of total portfolio drawdown.

- Scenario stress: run historical spread widening and rate shock scenarios, then set position limits so losses stay within the sleeve’s drawdown budget.

- Execution rule: trade in liquid tenors first, and cap turnover to keep transaction costs predictable.

Concrete example: if a curve trade looks attractive on carry but the scenario set shows that spread widening dominates, you reduce position size or choose a different maturity pair with better stress behavior.

Step 6: Validate the Mapping with Backtests That Respect Constraints

Finally, you test whether the strategy choices actually honor the constraints when costs and timing are included.

- Use realistic bid-ask and slippage assumptions.

- Include delays for signal formation and rebalancing.

- Apply the same de-risking rules used in the plan.

If the backtest shows drawdowns exceeding the 8% target even after de-risking, the mapping is wrong. The fix is not “try harder,” it’s to adjust the strategy choice, the risk budget, or the hedging and sizing rules.

Step 7: Produce the Decision Artifact

You end with a one-page mapping summary:

- Objective metrics

- Derived constraints

- Shortlisted strategy families

- Scoring rubric results

- Implementation rules for sizing, hedging, and de-risking

That artifact is what keeps the strategy selection coherent when real trading starts behaving like real trading.

2. Market Microstructure and Trading Mechanics

2.1 Order Types Execution Paths and Cost Implications

Order execution is where “strategy” meets “reality.” The order type you choose determines how your intent is routed through the market, how quickly it can be filled, and what costs you’ll likely pay. Those costs show up as explicit fees and implicit frictions like spread, slippage, and market impact.

Execution Path Basics

An order typically moves through three stages: submission, matching, and post-trade processing. Submission includes routing to a venue and choosing how the order behaves while it waits. Matching is where the order interacts with the limit order book or with auction mechanisms. Post-trade processing covers settlement and reporting, which affects operational cost but not trading P&L directly.

The key idea: different order types change your “interaction style” with liquidity. A market order aggressively seeks immediate execution, while a limit order offers a price and waits for counterparties who like that price.

Market Orders

A market order is executed against the best available prices until the order quantity is filled or liquidity runs out. The execution path is straightforward: it consumes liquidity at the top of the book and then walks the book if needed.

Cost implication: you pay the spread in expectation because you cross it immediately. If the order is large relative to visible depth, you also pay additional levels of the book, which shows up as slippage.

Example: Suppose the best bid is 100.00 and best ask is 100.01. A buy market order for 10 shares likely fills at 100.01 first. If the ask depth at 100.01 is only 4 shares, the remaining 6 shares fill at the next ask level, say 100.02. Your average fill becomes 100.014, not 100.01.

Limit Orders

A limit order specifies the worst acceptable price. A buy limit at 100.00 will only execute at 100.00 or lower. The execution path depends on whether the market reaches your price and whether your order becomes the best available offer or bid.

Cost implication: you avoid crossing the spread, so you typically reduce immediate slippage. The trade-off is fill probability. If price moves away, you may get partial fills or none.

Example: You place a buy limit at 100.00 for 10 shares. If the market trades down to 100.00 for a moment, you might get a partial fill at 100.00 and then stop. If it never returns, you pay no trading cost but also achieve no position.

Limit vs Market Under Volatility

Volatility changes the balance between speed and price. In fast markets, market orders tend to fill quickly but with worse average prices due to book walking. Limit orders can protect price but may miss the move entirely.

A practical best practice is to align order aggressiveness with your signal horizon. If your edge depends on being in quickly, you accept higher expected costs. If your edge tolerates waiting, you can use limit orders to control price.

Time-in-Force and Queue Position

Time-in-force (TIF) controls how long the order stays active. Common choices include Day (expires at end of session) and Good-Til-Cancelled (remains until canceled). Queue position matters: earlier orders at the same price generally get matched first.

Cost implication: a longer-lived limit order can improve fill probability, but it also increases exposure to adverse selection if the market moves against you while you wait.

Example: Two traders submit buy limits at 100.00 for 10 shares. Trader A submits at 10:00:01, Trader B at 10:00:05. If the price touches 100.00 for 3 seconds with enough sell liquidity, Trader A is more likely to get filled first, reducing the chance of partial fills.

Routing and Venue Selection

Routing determines where your order is sent and how it’s exposed to liquidity. Some venues may have tighter spreads or deeper books for a given instrument, while others may have different fee schedules.

Cost implication: the same order type can produce different results across venues because of fee differences and available depth.

Example: A limit order routed to a venue with a narrower spread may execute at a better price, even if the maker fee is slightly higher. Conversely, a venue with deeper depth can reduce slippage for market orders.

Partial Fills and Average Price

Partial fills are not a failure; they’re a cost profile. Your realized execution quality depends on the sequence of fills and the evolving book.

Best practice: track average execution price versus the prevailing mid at submission time. If average price deteriorates quickly, your order type may be too aggressive for the current liquidity.

Mind Map: Order Types and Cost Drivers

Practical Example: Choosing an Order Type

Assume you want to buy 1,000 shares and the instrument’s top-of-book depth at the best ask is 300 shares. If you use a market order, you will likely consume multiple price levels, increasing slippage. If you use a limit order at the best ask, you may get only the 300 shares initially, then wait for additional sellers to appear at your price.

A systematic approach is to estimate visible depth and decide whether you prefer predictable price with uncertain timing (limit) or predictable timing with uncertain price (market). Then set TIF to match your tolerance for waiting, and route to venues that offer the best combination of depth and fees for that order type.

2.2 Liquidity Measurement and Trading Venue Selection

Liquidity is not one number; it’s a set of frictions that show up as spreads, depth, and the way prices move when you trade. Venue selection is the practical step where those frictions become real costs.

Liquidity Components That Actually Matter

Start with three observable pieces:

- Bid-ask spread: the immediate cost of crossing from one side to the other. If you buy at the ask and later sell at the bid, the spread is your first hurdle.

- Order book depth: how much size is available near the top of book. Thin depth means your order walks the book, widening your effective spread.

- Price impact: how much the midprice shifts due to your trade. Impact depends on size relative to typical order flow and on how quickly liquidity replenishes.

A useful mental model: spread is the “cover charge,” depth is the “how many seats are left,” and impact is the “how much the room changes when you sit down.”

Measuring Liquidity with Practical Metrics

Use metrics that connect to execution, not just market snapshots.

- Effective spread: compare execution price to mid at the time of trade. For a buy, effective spread is roughly \(2 \times (\text{exec price} - \text{mid})\). This captures both spread and microstructure noise.

- Depth at distance: measure cumulative size within a few basis points from mid (for example, within 1 bp and 5 bp). This helps estimate how far your order will travel if you join the book.

- Volume at price and replenishment: track how quickly the book refills after trades. A venue with similar depth can still be worse if replenishment is slow.

- Realized slippage vs. size: bucket trades by participation rate (your order size divided by venue volume over the interval) and compute average slippage. This turns “liquidity” into a size-dependent cost curve.

Venue Selection Framework

Venue choice should be driven by the execution objective.

- If you need immediacy: prioritize venues with lower effective spread and lower short-horizon impact for your typical order size.

- If you can wait: prioritize venues with strong replenishment and sufficient depth near mid, since you’ll often trade via passive orders.

- If you trade across venues: compare not only prices but also how quickly your order can be filled without moving the market.

A simple decision rule is to estimate expected total execution cost for each venue:

\(\text{Expected cost} = \text{Expected spread component} + \text{Expected impact component} + \text{Expected adverse selection component}\)

Adverse selection is the risk that your trade hits informed flow; it shows up as worse-than-expected execution relative to mid.

Mind Map: Liquidity Measurement and Venue Selection

Example: Choosing Between Two Venues

Assume you trade 200,000 shares of a liquid equity.

- Venue A shows a quoted spread of 1.0 bp, but depth within 1 bp is only 50,000 shares. Your order likely walks the book.

- Venue B shows a quoted spread of 1.3 bp, but depth within 1 bp is 250,000 shares and replenishment is fast.

If you place a passive order, Venue B can yield a lower effective spread because your order fills without moving far from mid. If you must cross immediately, Venue A might win because the smaller quoted spread reduces the crossing cost, even if depth is thin.

To make this concrete, compute for each venue:

- expected fill price using depth buckets,

- expected impact using slippage vs participation from recent executions,

- and compare the sum.

Example: Participation Rate as the Bridge Between Liquidity and Impact

Suppose your typical interval volume on Venue A is 10 million shares, and your order is 200,000 shares. Participation is 2%. If historical data shows that at 2% participation, average slippage is 2.5 bp on Venue A and 1.8 bp on Venue B, then Venue B is cheaper for your usual urgency level.

If you later change order size to 600,000 shares (6% participation), the impact curve may steepen. Venue selection should follow the new participation regime rather than the old one.

Operational Checks That Prevent “Good Theory, Bad Fills”

Before routing decisions become policy, verify:

- Time-of-day effects: liquidity often changes across the session, so compute metrics by time buckets.

- Instrument-specific behavior: depth and impact can differ even for similar tick sizes.

- Consistency of midprice reference: ensure you use the same mid definition when computing effective spread.

A venue that looks best on a random snapshot can lose once you account for how your order size interacts with depth and replenishment.

2.3 Slippage Modeling and Transaction Cost Estimation

Slippage is the difference between the price you intended and the price you actually get. Transaction costs are broader: they include explicit fees and implicit costs like spread and market impact. Modeling both matters because a strategy that looks profitable on mid-price can quietly lose money once you pay the bill.

Core Concepts and What They Mean in Practice

Start with three price references:

- Mid-price: average of best bid and best ask. It’s a convenient “fair” reference.

- Execution price: where your order actually fills.

- Realized cost: execution price minus the reference, adjusted for direction (buy vs sell).

A simple way to think about costs for a buy order is:

- Half-spread cost: if you cross the spread, you effectively pay the ask; relative to mid, that’s about half the spread.

- Adverse selection: if you trade when the market is about to move against you, you pay more than the spread alone.

- Market impact: your order changes prices, especially when size is large relative to liquidity.

A good model separates these components so you can test which lever actually improves results.

Building a Slippage Model from Observable Inputs

A practical slippage model uses observable market data and a few strategy parameters:

- Order aggressiveness: market order vs limit order, and how quickly you cancel.

- Trade size: shares/contracts relative to typical volume.

- Liquidity: spread width and depth near the best quotes.

- Volatility: faster markets tend to widen realized costs.

- Time of day: liquidity and volatility vary across the session.

Mind Map: Slippage Modeling Components

Estimating Spread and Fees First

Before impact modeling, compute the easy parts.

- Spread cost: estimate using historical average bid-ask spread at the time you would trade. If you use mid-price in backtests, you can convert to a more realistic reference by subtracting half the spread for buys and adding half the spread for sells.

- Fees: use your venue schedule. Even if fees are small, leaving them out can distort comparisons between strategies with different turnover.

Example: Suppose the average spread at your execution times is 10 bps (0.10%). If your backtest assumes mid-price, a market buy will typically cost about 5 bps relative to mid, before impact.

Modeling Market Impact with a Size-to-Liquidity Lens

Market impact grows with order size and with how quickly you trade. A common approach is to relate impact to participation rate:

- Participation rate = your order size / typical volume over the order’s time window.

Then estimate impact as a function of participation and volatility. A simple, robust form is:

- Impact ≈ k × (participation rate)^α × volatility

Where:

- k scales the level for your instrument and venue,

- α controls curvature (often between 0.3 and 1.0 in practice),

- volatility can be measured as short-horizon realized volatility.

You don’t need a perfect formula to be useful. You need a model that responds correctly when liquidity worsens.

Example: Impact Sensitivity with Two Trade Sizes

Assume:

- short-horizon volatility proxy = 1.0% per day,

- α = 0.6,

- k chosen so that a 10% participation trade costs 0.20%.

If you double participation to 20%, impact scales by (2^0.6) ≈ 1.52, so cost becomes about 0.30%. That’s the key behavior you want: bigger trades cost disproportionately more.

Adverse Selection and Timing Effects

Adverse selection captures the idea that your order may execute when the market is already moving against you. A workable method is to estimate slippage conditional on short-term price movement:

- Compute the return over a short window around execution (for example, from 1 minute before to 1 minute after).

- Regress realized execution price vs that movement, separately for buys and sells.

If buys tend to fill after upward moves, you’ll see negative adverse selection for buys (you paid more than expected). If the sign flips, your model should reflect it rather than assuming a constant bias.

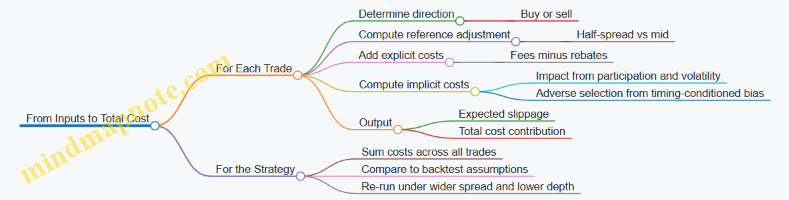

Putting It Together for Total Transaction Cost Estimation

For each simulated trade, estimate:

-

Reference adjustment from spread

-

Fees

-

Impact from participation and volatility

-

Adverse selection from timing-conditioned bias

Then sum across trades, including rebalancing and any hedges. A strategy with frequent small trades may have low impact but still lose to spread and fees. A low-turnover strategy may look great until you model impact on the occasional large rebalance.

Mind Map: From Inputs to Total Cost

Validation That Doesn’t Lie

Validate the model against historical executions or realistic proxy fills. Check three things:

- Level: does predicted average slippage match observed averages?

- Shape: does slippage increase with size and worsen in low-liquidity periods?

- Direction: do buy and sell costs behave differently when the market moves?

If the model matches level but not shape, your backtest may still be misleading. If it matches shape but not level, your assumptions about fees, spread, or scaling are off. Either way, fixing it improves the strategy’s cost realism without changing the core trading logic.

2.4 Market Impact and Turnover Management

Market impact is the price change caused by your own trading. Turnover is how often you trade, usually measured as traded value divided by average portfolio value. Together, they determine whether a strategy’s expected edge survives real trading costs—or gets quietly eaten by the market.

Why Market Impact Matters

Even if your signal is correct, execution can shift your realized entry and exit prices. Impact tends to rise when liquidity is thin, when orders are large relative to typical volume, and when urgency is high. A useful mental model is: you trade, the order book adjusts, and the adjustment becomes part of your cost.

A simple decomposition helps: total trading cost is roughly (i) explicit costs like commissions and fees, (ii) implicit costs like bid-ask spread, and (iii) impact costs from moving the price. Turnover management mainly targets the third component, but it also changes how often you pay spread and fees.

Foundational Building Blocks

- Order size vs. liquidity: If your order is a noticeable fraction of the average volume over your execution window, impact is more likely to be meaningful.

- Execution speed: Faster execution usually increases impact because you consume liquidity quickly.

- Participation rate: A common control variable is the fraction of market volume you intend to trade during a time slice.

- Order type and aggressiveness: Market orders typically pay more impact than passive limit orders, but passive orders can face adverse selection and fill uncertainty.

Impact Models in Practice

You don’t need a PhD-level model to manage impact. A practical approach is to estimate a cost-per-share (or cost-per-dollar) that increases with size and urgency.

A common structure is:

- Temporary impact: cost that depends on how quickly you execute.

- Permanent impact: longer-lasting price effects that may persist after your trade.

For day-to-day execution planning, temporary impact is often the main driver. You can approximate it by scaling observed slippage with participation rate and volatility.

Turnover Management as a Cost Control System

Turnover management is not “trade less” as a slogan. It is choosing a trading frequency that matches signal decay and rebalancing needs.

- If a signal changes slowly, frequent rebalancing just adds spread and impact without improving outcomes.

- If a signal changes quickly, delaying trades can reduce edge, but executing too aggressively can also destroy it.

A systematic workflow:

- Define a target rebalance rule: e.g., rebalance when weight deviates by a threshold or on a schedule.

- Estimate incremental cost per rebalance: include expected spread and impact.

- Compare incremental benefit to incremental cost: if the expected improvement is smaller than the cost, the rebalance rule is too sensitive.

Concrete Example: Rebalance Threshold vs. Execution Cost

Suppose you run a strategy that targets a 5% position in a liquid stock. Your average daily volume is $200 million, and your typical portfolio value is $50 million.

- Aggressive schedule: rebalance daily back to target. If you trade $2.5 million per day (5% of $50m), your participation rate is about 1.25% of daily volume.

- Threshold schedule: rebalance only when the position drifts by more than 0.5 percentage points. If drift is usually small, you might trade only 2–3 times per week.

Even if the stock is liquid, the threshold approach reduces the number of times you cross the spread and reduces how often you create short-term price pressure. The key is that you’re not changing the signal; you’re changing how often you convert it into trades.

Mind Map: Market Impact and Turnover Management

Advanced Details Without the Confusion

Participation rate targeting: Instead of “execute quickly,” set a participation rate cap. If you cap participation, you implicitly slow down execution when liquidity is low.

Slice and schedule: Break a large order into smaller slices and distribute them across time windows with better liquidity. This reduces peak pressure.

Avoiding adverse selection: Passive orders can be filled by counterparties who know something you don’t. A balanced approach uses limit orders when spreads are stable and switches to more aggressive execution when fill risk becomes too high.

Turnover-aware portfolio rules: Weight-based thresholds, banded rebalancing, and volatility-scaled position updates all reduce unnecessary trading. The best rules are the ones that are measurable: you can compute expected drift, expected trade size, and expected cost.

Practical Checklist for Execution Planning

- Estimate expected trade size and participation rate.

- Choose order type based on liquidity and urgency.

- Use slicing to reduce peak impact.

- Apply rebalance thresholds to avoid churn.

- Validate with realized slippage and cost attribution by trade bucket.

When impact and turnover are treated as first-class design constraints, execution stops being a post-trade surprise and becomes part of the strategy’s cost-aware logic.

2.5 Practical Example: Building a Trade Cost Budget

A trade cost budget is a simple, disciplined way to decide whether a strategy’s expected edge can survive real-world frictions. The goal is not to predict the future perfectly; it’s to set a cost ceiling that your execution must beat, and to quantify what “beat” means.

Step 1: List Cost Components in Plain Categories

Start with costs you can estimate before trading:

- Explicit costs: commissions, exchange fees, clearing fees.

- Implicit costs: bid-ask spread, slippage from price movement during execution.

- Market impact: price pressure caused by your own orders, especially for larger trades.

- Operational costs: failed orders, late cancels, re-quotes, and any systematic delays.

A useful rule: if a cost is small but frequent, include it; if it’s rare but huge, include it too. Either way, your budget should reflect the strategy’s trading pattern.

Step 2: Choose a Unit of Measurement

Pick one consistent unit so comparisons are meaningful. Common choices:

- Cost per share (good for single-name equity trades)

- Cost per notional dollar (good for cross-asset)

- Cost per trade (good for event-driven)

For this example, use basis points (bps) of notional so it scales cleanly.

Step 3: Build a Numeric Example for One Trade

Assume a strategy trades $1,000,000 notional of a liquid stock.

Inputs (illustrative, but realistic in structure):

- Commission and fees: $2,500 per trade

- Average bid-ask spread: $0.02 per share

- Average price: $50

- Shares traded: $1,000,000 / $50 = 20,000 shares

- Slippage from execution timing: 0.8 bps

- Market impact allowance: 1.2 bps

Convert the spread into bps. If you cross the spread once on average, the spread cost is roughly half-spread to full-spread depending on execution. Use a conservative midpoint assumption: 0.75 of the spread.

- Spread dollars per share: $0.02

- Spread cost per share: 0.75 × 0.02 = $0.015

- Spread cost total: 20,000 × 0.015 = $300

- Spread cost in bps of notional: ($300 / $1,000,000) × 10,000 = 3.0 bps

Commission and fees in bps: ($2,500 / $1,000,000) × 10,000 = 25 bps

Now sum the budget components:

- Fees: 25.0 bps

- Spread: 3.0 bps

- Slippage: 0.8 bps

- Market impact: 1.2 bps

Total trade cost budget = 30.0 bps.

If your strategy’s expected gross alpha per trade is, say, 35 bps, then the net edge is 5 bps before taxes, financing, and any model error. If expected gross alpha is 25 bps, the trade is structurally unprofitable under this cost ceiling.

Step 4: Translate the Budget Into Execution Requirements

A budget is only useful if it becomes actionable. Turn the total into constraints:

- If fees are fixed, the remaining “execution allowance” is 30.0 − 25.0 = 5.0 bps.

- That 5.0 bps must cover spread, slippage, and impact.

- If your historical slippage is trending toward 2.5 bps, you must reduce impact via smaller slices, better timing, or more selective liquidity.

Step 5: Add a Simple Stress Check

Costs are not constant. Add a stress scenario that increases slippage and impact while leaving fees unchanged.

- Base: slippage 0.8 bps, impact 1.2 bps

- Stress: slippage 1.6 bps, impact 2.4 bps

Recompute: fees 25.0 + spread 3.0 + slippage 1.6 + impact 2.4 = 32.0 bps.

Your strategy must still clear the threshold under stress, or you need to adjust position sizing, execution style, or signal selectivity.

Mind Map: Trade Cost Budget Workflow

Example: Budgeting for a Different Execution Style

If instead of crossing you use passive orders and achieve a better fill, the spread component can drop. Suppose spread cost falls from 3.0 bps to 1.5 bps, but slippage rises from 0.8 bps to 1.4 bps due to waiting.

New total: fees 25.0 + spread 1.5 + slippage 1.4 + impact 1.2 = 28.1 bps.

The budget tells you whether passive execution is actually improving net cost. If it doesn’t, you don’t “try harder”; you change the assumptions or the execution approach.

Step 6: Record the Budget and Compare to Realized Costs

For each trade, store:

- Notional

- Realized effective spread (or proxy)

- Realized slippage vs decision price

- Any impact proxy you track

- Total realized cost in bps

Then compare realized costs to the budget ceiling. If realized costs are consistently above budget, the issue is usually one of three things: the spread proxy is wrong, slippage is underestimated, or impact is larger than assumed for your trade size and venue.

A good trade cost budget is boring in the best way: it turns “execution matters” into numbers you can manage.

3. Portfolio Construction for Hedge Fund Style Returns

3.1 Risk Factor Decomposition and Exposure Management

Risk factor decomposition turns “the portfolio is risky” into a map of what is actually driving returns and losses. In practice, you start with a factor model, estimate exposures, and then manage those exposures so the portfolio behaves the way you intend under different market conditions.

Core Idea: Separate Return Drivers from Random Noise

A factor model expresses portfolio returns as a combination of systematic components plus idiosyncratic noise. The systematic components are the ones you can manage; the noise is the part you can only reduce by diversification and better estimation.

A simple linear form is:

- Portfolio return ≈ sum of (factor exposure × factor return) + residual

If your residual is large, your strategy is relying on things you cannot reliably forecast. If your factor exposures are unstable, your risk control will be inconsistent even if your backtest looks fine.

Step 1: Choose a Factor Set That Matches Your Strategy

Factor sets should be practical, not encyclopedic. For equity long-short, common categories include:

- Market beta (broad equity direction)

- Style factors (value, growth, size, momentum)

- Sector or industry factors

- Quality or profitability proxies

- Volatility or liquidity proxies

For absolute return goals, you typically want to control broad direction and style drift while allowing controlled idiosyncratic selection.

Example: If your long-short book is meant to be market neutral, you still need to decide whether “neutral” means beta-neutral only, or also neutral across size and sector. Beta-neutral alone can still leave you exposed to sector swings.

Step 2: Estimate Exposures Using Holdings and Factor Loadings

Exposure estimation links what you hold to how those holdings behave. You can estimate factor exposures using:

- Factor loadings per security (from a regression or vendor model)

- Portfolio weights (including long and short positions)

- Optional adjustments for corporate actions, borrow costs, and liquidity constraints

A practical workflow:

- Compute net weights by factor-relevant dimensions (e.g., sector, style).

- Convert those into factor exposures using the chosen factor loadings.

- Validate exposures by checking whether predicted factor PnL explains realized PnL during recent windows.

Example: Suppose you hold 60% long and 60% short with equal gross exposure. If your factor model shows a +0.20 market beta exposure, the book is not neutral; it is directionally tilted even if the gross is balanced.

Step 3: Manage Exposures with Explicit Targets and Limits

Exposure management is not “minimize risk” in the abstract. It is “keep exposures within ranges that match your mandate.” Typical controls include:

- Target exposures (e.g., beta = 0, sector net = 0)

- Hard limits (e.g., |value factor exposure| ≤ 0.05)

- Soft penalties (e.g., discourage concentration in a single sector)

- Turnover-aware constraints (to avoid rebalancing that breaks cost assumptions)

Example: You run a market-neutral strategy. You set:

- Market beta target: 0

- Sector exposure limits: ±0.02 per sector

- Momentum exposure limit: ±0.03

If a new trade candidate increases momentum exposure beyond the limit, you either reduce its size, pair it with an offsetting position, or reject it.

Step 4: Account for Estimation Error and Model Risk

Factor models are approximations. Two common failure modes are:

- Factor loadings drift over time

- Correlations among factors change, making exposures harder to interpret

Mitigations that fit naturally into the workflow:

- Use rolling windows for loadings and exposures

- Monitor factor exposure stability (not just level)

- Stress-test exposure changes under plausible shocks to factor returns

Example: If your value factor exposure is near zero today but has been swinging between -0.10 and +0.10, you should treat it as unstable and tighten limits or improve the estimation method.

Step 5: Translate Factor Exposures Into Risk Budgeting

Risk budgeting connects exposures to expected volatility and drawdown behavior. A common approach is to use a factor covariance matrix:

- Factor risk ≈ exposure vector × factor covariance × exposure vector

- Add residual risk from idiosyncratic variance

Then you allocate risk budgets across sleeves or strategies.

Example: If your total risk budget is 8% annualized volatility and your equity sleeve consumes 6%, you can cap its factor-driven risk while allowing controlled residual risk from stock selection.

Mind Map: Risk Factor Decomposition and Exposure Management

Worked Example: From Holdings to Controlled Exposure

Assume a long-short equity book with net market beta target 0.

- Current portfolio market beta exposure: +0.12

- Target: 0

- Allowed band: ±0.03

You identify a candidate trade that would add +0.04 beta exposure if added alone. Instead of rejecting immediately, you check whether pairing it with an offsetting position reduces net beta to within the band. If the pair brings beta to +0.02 while keeping sector exposure within limits, the trade is acceptable. If it fixes beta but pushes sector exposure beyond its limit, you adjust the pair or reduce size.

The key is that every decision is evaluated against the same exposure framework, so risk control stays consistent as the portfolio evolves.

3.2 Position Sizing Methods for Volatility and Drawdown Control

Position sizing is where “good ideas” meet “survivable reality.” The goal is simple: scale exposure so losses stay within a drawdown budget while still allowing enough size to matter when signals work. This section builds from volatility basics to drawdown-aware sizing, then turns it into implementable rules.

Core Concepts That Drive Sizing

Volatility sizing starts with the idea that risk is not constant. If a strategy’s returns swing more, the same notional position can produce larger losses. Drawdown control adds a second layer: even if average risk looks fine, clustering of losses can push the portfolio into unacceptable territory.

A practical way to connect these ideas is to treat sizing as a mapping from forecasted risk to allowed loss. You can do this with either (1) volatility targeting, (2) drawdown budgeting, or (3) a hybrid that uses both.

Volatility Targeting with a Clear Loss Budget

Volatility targeting chooses position size so the expected contribution to portfolio volatility matches a target. A common starting point uses realized volatility over a recent window.

Example: Suppose you trade an equity long/short sleeve and estimate the sleeve’s 20-day annualized volatility at 25%. Your portfolio volatility target for this sleeve is 10% annualized. If the sleeve’s return stream is roughly proportional to position size, scale by:

- Size multiplier ≈ target_vol / current_vol = 10% / 25% = 0.4

If you would normally allocate $1,000,000 notional, you allocate $400,000 instead. The “why” is straightforward: when volatility rises, the multiplier shrinks, reducing the chance that a normal signal produces an outsized loss.

Best practice: use a volatility estimate that is stable enough to avoid whipsaw. A shorter window reacts faster but can overreact to noise; a longer window is steadier but slower to respond.

Volatility Targeting with Correlation-Aware Scaling

Portfolio risk is not just the sleeve’s own volatility; it’s also how it moves with the rest. If your sleeve is correlated with existing exposures, the same notional can increase portfolio volatility more than you expect.

Example: You already hold a factor-tilted book. Your new sleeve has 25% standalone volatility, but its correlation with your factor book is 0.6. If you ignore correlation, you may size too large. A correlation-aware approach estimates the incremental portfolio variance contribution and scales to keep the incremental contribution near the target.

A simple approximation uses covariance:

- Incremental variance ≈ w_new^2 * var_new + 2 * w_new * w_existing * cov(new, existing)

Then solve for w_new that yields the desired incremental variance. Even a rough covariance estimate improves sizing discipline.

Drawdown-Aware Sizing That Reacts to Loss Clustering

Volatility targeting controls typical risk, but drawdowns are about the path of returns. Drawdown-aware sizing reduces exposure after losses accumulate, even if volatility is unchanged.

A workable method is to define a drawdown budget and scale down when the portfolio drawdown breaches thresholds.

Example: Let your maximum tolerable drawdown for the sleeve be 8% from its recent peak. Create two bands:

- Band A: drawdown 0%–4% → 100% size

- Band B: drawdown 4%–8% → linearly scale from 100% to 50%

If the sleeve drawdown reaches 6%, the scale factor is 75%. A $1,000,000 notional becomes $750,000. This prevents “normal” sizing from turning a temporary slump into a portfolio-level problem.

Best practice: use a rolling peak definition (e.g., peak over the last N trading days) so the drawdown measure resets in a controlled way.

Hybrid Approach Combining Volatility and Drawdown

The most robust practical sizing rules often combine both controls: volatility targeting sets the baseline size, and drawdown control applies a risk-off multiplier.

Example: Baseline volatility targeting gives a multiplier of 0.4. The drawdown band multiplier at the moment is 0.75. Final multiplier = 0.4 * 0.75 = 0.3. If you would allocate $1,000,000 notional, you allocate $300,000.

This hybrid avoids two common failure modes: volatility-only sizing that ignores loss streaks, and drawdown-only sizing that ignores changing market regimes.

Implementation Mind Map

Mind Map: Position Sizing for Volatility and Drawdown Control

Practical Guardrails That Prevent Accidental Overconfidence

- Cap leverage and notional changes: Even with correct formulas, sudden sizing jumps can create execution stress.

- Use consistent units: Volatility estimates, targets, and multipliers must align (annualized vs daily).

- Separate signal strength from sizing: If your signal is weak, sizing should not compensate by increasing risk.

- Validate with backtests that include transaction costs: Sizing changes alter turnover, which changes net returns.

Mini Example with All Steps Together

Assume:

- Baseline notional: $1,000,000

- Volatility estimate: 30% annualized

- Sleeve volatility target: 12% annualized

- Current drawdown band multiplier: 0.7

Step 1: volatility multiplier = 12% / 30% = 0.4

Step 2: final multiplier = 0.4 * 0.7 = 0.28

Final notional = $280,000

That’s the whole point: the position size is a computed response to measurable risk conditions, not a guess.

3.3 Correlation Estimation and Regime Aware Risk Controls

Correlation is a relationship, not a law of physics. In hedge fund portfolios, the practical question is: “When correlation changes, do our risk controls still behave the way we intended?” This section builds a workflow that estimates correlation carefully, then uses regime awareness to keep risk limits meaningful.

Start with What Correlation Actually Measures

Correlation between two return series is a standardized co-movement over a chosen window. If you estimate it on the wrong horizon, you can get a “high correlation” that only exists during a specific market behavior. For risk controls, you typically need correlation that is stable enough to guide sizing, but responsive enough to avoid being blindsided.

A useful mental model is to separate three layers:

- Sampling layer: window length, missing data, and outliers.

- Model layer: how you estimate correlation and whether you adjust for noise.

- Control layer: how you translate correlation into limits and de-risking actions.

Mind Map: Correlation Estimation and Regime Aware Controls

Estimate Correlation Without Fooling Yourself

Begin with clean, aligned returns. If one series has stale prices or different trading calendars, correlation can look “real” while actually reflecting data artifacts.

Next, choose an estimation method. The raw sample correlation matrix can be noisy, especially with short windows or many assets. A common best practice is shrinkage: blend the sample covariance with a structured target (like equal correlations or factor-implied covariance). This reduces estimation error and makes risk limits less jumpy.

A simple example: suppose you estimate correlation between two equity sectors using 20 trading days. If one sector has a single idiosyncratic shock, the 20-day correlation can swing dramatically. Shrinkage dampens that swing by pulling the estimate toward a more stable structure.

Finally, run diagnostics. Compute correlation stability by rolling the window and tracking how often correlations change sign or exceed thresholds. If your correlation estimate is wildly unstable, your risk control will be too.

Regime Awareness That Actually Helps

Regimes are not mystical states; they are operational buckets that correspond to different market behavior. For correlation, regimes often relate to volatility and stress.

A practical regime definition uses observable variables:

- Volatility level: e.g., rolling realized volatility above a threshold.

- Market stress: e.g., credit spreads widening beyond a level.

- Broad risk-on or risk-off: e.g., index trend strength.

Then decide how to apply regimes:

- Hard switching: use one correlation matrix per regime.

- Soft weighting: blend matrices using probabilities of being in each regime.

Soft weighting is usually smoother. Hard switching is simpler and can be effective when regimes are clearly separated.

Example: Regime-Specific Correlation for a Long Short Portfolio

Imagine a portfolio holding long positions in Quality stocks and short positions in Value stocks. In calm markets, these sleeves might have modest correlation because idiosyncratic selection dominates. During stress, both sleeves can move together as liquidity and risk appetite dominate.

Workflow:

- Estimate two correlation matrices using different windows:

- Calm regime: 60-day window when volatility is below threshold.

- Stress regime: 60-day window when volatility is above threshold.

- Compute portfolio risk using the appropriate matrix.

- Add a control rule: if the portfolio’s estimated risk under the stress matrix exceeds a limit, reduce gross exposure or tighten position caps.

Concrete control logic: if the stress-matrix risk is 12% annualized and your limit is 10%, cut gross by 15% and re-check. This is not prediction; it is conditional risk budgeting.

Mind Map: Regime Mapping to Risk Controls

Advanced Details That Prevent Common Failure Modes

Two failure modes show up often.

First: regime leakage. If your regime signal is computed using the same data window as the correlation estimate, you can create circularity. Use a signal window that is earlier than the correlation estimation window, or compute the regime signal from a separate set of observations.

Second: mismatched horizons. If your correlation matrix is estimated on daily returns but your rebalancing is weekly, the correlation used for risk might not match the holding period. Align estimation horizon, rebalancing frequency, and the risk metric horizon.

Operationalizing the Control Loop

A clean implementation loop looks like this:

- Recompute regime classification on a schedule.

- Update correlation estimates per regime using shrinkage.

- Recalculate portfolio risk and factor exposures.

- Apply limits and de-risking rules consistently.

- Monitor correlation drift and limit breach frequency to ensure the system is behaving as designed.

When done well, regime-aware correlation controls turn “correlation changed” from an uncomfortable surprise into a structured input for risk decisions. And yes, it’s still correlation—just with better manners.

3.4 Leverage Use and Margin Constraints in Practice

Leverage turns small equity into larger exposure, but margin rules decide how much leverage you can actually use. In practice, “allowed leverage” is not a single number; it’s the result of margin requirements, haircuts, liquidity terms, and how your broker or prime broker treats your positions. The goal is to size leverage so the portfolio can survive normal volatility and still meet margin calls without forced liquidation.

Leverage Basics That Matter for Margin

Start with the simplest mapping: equity is what you post, exposure is what you control. If you hold $1 of equity and borrow $4, your gross exposure is $5, and your leverage is 5x on a gross basis. Margin constraints then cap borrowing by requiring collateral coverage. Two portfolios with the same leverage can behave very differently if one uses instruments with higher haircuts or less favorable margin treatment.

A practical way to think about margin is as a buffer equation:

Margin buffer = Equity − Required Margin

Required margin rises when prices move against you, when volatility increases, or when the broker applies larger haircuts to certain assets. If the buffer goes negative, you get a margin call and must add collateral or reduce positions.

Margin Types and Why They Change

Margin requirements typically depend on:

- Initial margin: posted at trade entry.

- Variation margin: posted as mark-to-market P&L changes.

- Haircuts: reductions applied to collateral value, often higher for less liquid or more volatile assets.

- Concentration and liquidity adjustments: extra margin for large positions or hard-to-fund instruments.

Even if your strategy is “market neutral,” margin can still bite. A long-short equity book may have low net market exposure, but if both legs are volatile or correlated in stress, the broker may increase margin requirements for the gross positions.

A Systematic Sizing Workflow

Use a repeatable process that connects strategy risk to margin capacity.

- Choose a target risk level: for example, a maximum expected drawdown over a holding period.

- Convert risk into position volatility: estimate how much P&L moves per unit of exposure.

- Translate exposure into required margin: apply instrument-specific margin rates and haircuts.

- Add a buffer: require that equity covers required margin under a stress move, not just under today’s prices.

- Set a leverage cap: the cap should be the minimum of (a) strategy-driven leverage and (b) margin-driven leverage.

Here’s a concrete example. Suppose you manage $10,000,000 equity. Your broker requires initial margin of 8% of gross exposure for liquid equities, and you plan a gross exposure of $120,000,000. Required margin is 0.08 × 120,000,000 = $9,600,000. Your margin buffer is $10,000,000 − $9,600,000 = $400,000.

Now assume a stress move reduces your equity by $600,000 before you can rebalance. Your buffer would be negative, triggering a margin call. To avoid that, you either reduce gross exposure or increase equity buffer. If you want at least a $1,000,000 buffer after a $600,000 drawdown, you need required margin ≤ 10,000,000 − 1,000,000 + 600,000 = $9,600,000. In this setup, you can’t increase gross exposure beyond $120,000,000; in fact, you may need to lower it if margin rates rise during stress.

Margin Stress Testing That Doesn’t Lie

Margin stress tests should include both P&L moves and margin-rate changes. A common mistake is to test only price moves while keeping margin requirements fixed. Instead, run scenarios where:

- prices move against your positions,

- volatility increases,

- haircuts widen,

- and concentration penalties apply.

Then compute whether the margin buffer stays positive through the rebalancing window. If your rebalancing window is two business days, you need the buffer to survive two days of mark-to-market and operational delays.

Mind Map: Leverage and Margin Constraints

Operational Controls in Practice

Sizing is not enough; you need controls that prevent accidental over-leverage.

- Pre-trade margin checks: block trades that would reduce the margin buffer below a minimum threshold.

- Gross exposure limits: cap gross and per-instrument exposure, not just net exposure.

- De-risking triggers: define actions when buffer falls, such as reducing the largest gross leg first.

- Collateral planning: keep a dedicated liquidity reserve so variation margin can be met without selling at the worst time.

Example: De-Risking Rule for a Long-Short Book

Assume the same $10,000,000 equity and $120,000,000 gross exposure setup. Set a buffer warning at $300,000 and a hard limit at $100,000. If mark-to-market pushes the buffer to $250,000, you reduce gross exposure by 10% by trimming the leg with the highest marginal contribution to required margin. If the buffer hits $90,000, you cut another 10% and pause new trades until the buffer recovers.

This rule works because it ties action to the margin buffer, not to a subjective “feels risky” moment. It also respects the fact that margin requirements often increase when volatility rises, so the safest time to reduce exposure is before the hard limit.

3.5 Practical Example Constructing a Risk Balanced Portfolio

A risk-balanced portfolio aims to keep the risk contribution of each sleeve (or factor bucket) aligned with a target, rather than forcing equal dollar weights. The easiest way to see why this matters is to compare two sleeves: one that is volatile but uncorrelated, and another that is stable but highly correlated with the rest. Equal weights can still produce uneven risk.

Step 1: Define the Sleeves and the Risk Model

Assume you want an absolute return portfolio with three sleeves:

- Equity Long Short (LS): expected to be moderately volatile and equity-factor sensitive.

- Statistical Arbitrage (SA): lower volatility, designed to be market-neutral.

- Fixed Income Relative Value (RV): typically smoother returns but can react to rate shocks.

For each sleeve, you need a volatility estimate and a correlation matrix. Use a rolling window (for example, 60 trading days) to estimate:

- \(\sigma_{LS}\), \(\sigma_{SA}\), \(\sigma_{RV}\)

- Correlations \(\rho_{ij}\) between sleeve returns.

A simple covariance matrix is \(\Sigma_{ij} = \rho_{ij}\sigma_i\sigma_j\). This is the engine for risk budgeting.

Step 2: Choose a Risk Budget Target

Pick target risk contributions that reflect your intent. A common starting point is equal risk contribution across sleeves:

- Target risk shares: \(b = [1/3, 1/3, 1/3]\)

Risk contribution for sleeve \(i\) is computed from weights \(w\):

- Portfolio variance: \(\sigma_p^2 = w^T\Sigma w\)

- Marginal contribution: \(m_i = (\Sigma w)_i\)

- Risk contribution: \(RC_i = w_i m_i\)

Then normalize: \(RC_i / \sum_j RC_j\) should match \(b_i\).

Step 3: Solve for Weights with a Practical Constraint Set

In real portfolios you rarely allow unconstrained weights. Add constraints such as:

- Long-only for RV sleeve: \(w_{RV} \ge 0\)

- Gross exposure cap: \(\sum |w_i| \le 1.5\)

- Minimum allocation to avoid “zombie” sleeves: \(w_i \ge 0.05\) for SA and RV

If you allow shorting in LS, you might set \(w_{LS}\) to be positive or negative depending on your implementation, but for this example assume \(w_{LS} \ge 0\) and the sleeve itself handles its internal hedging.

Step 4: Work a Concrete Numeric Example

Suppose estimated volatilities and correlations are:

- \(\sigma_{LS}=12\%\), \(\sigma_{SA}=6\%\), \(\sigma_{RV}=4\%\)

- \(\rho_{LS,SA}=0.20\), \(\rho_{LS,RV}=0.10\), \(\rho_{SA,RV}=0.30\)

Then the covariance matrix (in decimal units) is:

- \(\Sigma_{LS,LS}=0.12^2=0.0144\)

- \(\Sigma_{SA,SA}=0.06^2=0.0036\)

- \(\Sigma_{RV,RV}=0.04^2=0.0016\)

- \(\Sigma_{LS,SA}=0.20\cdot0.12\cdot0.06=0.00144\)

- \(\Sigma_{LS,RV}=0.10\cdot0.12\cdot0.04=0.00048\)

- \(\Sigma_{SA,RV}=0.30\cdot0.06\cdot0.04=0.00072\)

Now choose weights \(w=[w_{LS},w_{SA},w_{RV}]\) to target equal risk contributions. A reasonable solution under these assumptions is approximately:

- \(w_{LS}=0.45\), \(w_{SA}=0.35\), \(w_{RV}=0.20\)

Why these numbers make sense: LS is the most volatile, so it gets less weight than SA would under equal-dollar logic. RV is the least volatile, so it gets the smallest weight, but not zero, because its correlation with SA is not negligible.

Step 5: Validate with Realized Behavior and Stress Checks

Before trusting the weights, sanity-check them:

- Risk contribution check: compute \(RC_i\) using \(\Sigma\) and confirm each sleeve contributes close to one-third of total variance.

- Scenario check: apply a simple shock by increasing correlations (for example, multiply off-diagonal correlations by 1.2) and re-evaluate risk shares. If one sleeve suddenly dominates, your diversification assumption is fragile.

- Turnover check: if weights change sharply from the prior rebalance, add a smoothing rule such as limiting weight changes to 20% per rebalance.

A portfolio that passes these checks is not “perfect,” but it is coherent: the risk budget is consistent with the covariance model, and the constraints prevent accidental concentration.

Mind Map: Risk Balanced Portfolio Construction

Example: Interpreting the Result

If after rebalancing you observe that LS contributes more than half the portfolio variance, the issue is usually one of three things: the volatility estimate for LS is too high, correlations are higher than expected, or constraints forced the optimizer to violate the risk budget. The fix is not to “guess harder,” but to update \(\Sigma\) with a more stable estimation window or adjust constraints so the risk budget can actually be achieved.

This example shows the core workflow: define sleeves, estimate covariance, set a risk budget, solve under constraints, then validate with both contribution math and simple stress logic.

4. Statistical Tools for Signal Generation and Backtesting

4.1 Data Preparation Cleaning Corporate Actions and Survivorship Bias

Good backtests fail for boring reasons: the data is inconsistent, the universe changes without telling you, and corporate actions quietly rewrite history. Data preparation is where you make the past behave like a real trading environment.

Data Foundations That Prevent Hidden Errors

Start by defining what each row means. For example, decide whether your dataset is “end-of-day prices,” “adjusted close,” or “intraday bars.” Mixing definitions creates phantom returns. Next, standardize identifiers: map tickers to a stable security ID so that splits, renames, and symbol changes don’t look like new assets.

A practical check is to verify monotonic time ordering per security and to confirm there are no duplicate timestamps. If you see duplicates, you need a rule: keep the last observation, average them, or drop them—just don’t let the rule vary across securities.

Corporate Actions Cleaning That Keeps Returns Honest