Asset Management for Accountants

1. Introduction to Asset Management in Accounting

1.1 Understanding Asset Management: Definitions and Scope

Asset management is a systematic process of developing, operating, maintaining, upgrading, and disposing of assets in the most cost-effective manner. For accountants, asset management involves tracking and managing an organization’s assets to ensure accurate financial reporting, compliance, and optimization of asset utilization.

Definition of Asset Management

Asset management can be defined as:

“The coordinated activities of an organization to realize value from assets.”

This includes physical assets like machinery, buildings, and vehicles, as well as intangible assets such as patents, trademarks, and software licenses.

Scope of Asset Management in Accounting

The scope covers:

- Asset Identification: Recognizing and cataloging assets.

- Valuation: Determining the financial value of assets.

- Depreciation & Amortization: Allocating the cost of assets over their useful life.

- Maintenance & Optimization: Ensuring assets remain productive and cost-efficient.

- Disposal: Properly removing assets from the books when no longer useful.

- Reporting: Accurate financial statements and regulatory compliance.

Mind Map: Asset Management Overview

Why Asset Management Matters for Accountants

Accountants play a critical role in asset management because:

- They ensure accurate recording of assets for financial integrity.

- They help in compliance with accounting standards (e.g., IFRS, GAAP).

- They provide insights into asset utilization and profitability.

- They support tax planning through proper depreciation and capitalization.

Example: Asset Management in a Small Business

Imagine a small manufacturing company that purchases a new machine for $50,000.

- Identification: The accountant tags the machine with a unique ID and records it in the asset register.

- Valuation: The purchase price is recorded as the asset’s cost.

- Depreciation: Using straight-line depreciation over 10 years, the accountant allocates $5,000 annually as an expense.

- Maintenance: Maintenance costs are tracked and capitalized if they extend the machine’s life.

- Disposal: After 8 years, the machine is sold for $10,000. The accountant calculates gain/loss and removes it from the books.

This example demonstrates how asset management integrates with accounting processes to maintain accurate financial records.

Mind Map: Asset Management Lifecycle Example

Summary

Understanding asset management is foundational for accountants managing financial records. It ensures assets are properly tracked, valued, and reported, supporting organizational decision-making and compliance. Throughout this blog, we will explore best practices and real-world examples to help accountants excel in asset management.

1.2 The Role of Accountants in Asset Management

Asset management is a critical function within finance and accounting, where accountants play a pivotal role in ensuring that an organization’s assets are properly recorded, valued, maintained, and reported. Their responsibilities extend beyond bookkeeping to strategic oversight, compliance, and optimization of asset utilization.

Key Responsibilities of Accountants in Asset Management

- Accurate Asset Recording: Accountants ensure all assets are correctly identified, tagged, and entered into the asset register.

- Valuation and Depreciation: They apply appropriate valuation methods and calculate depreciation to reflect the true value of assets over time.

- Compliance and Reporting: Accountants ensure asset management complies with accounting standards (e.g., IFRS, GAAP) and regulatory requirements.

- Internal Controls: They design and monitor controls to safeguard assets against loss, theft, or misappropriation.

- Financial Analysis: Accountants analyze asset performance and provide insights to optimize asset utilization and investment decisions.

Mind Map: Core Roles of Accountants in Asset Management

Example 1: Accurate Asset Recording in Practice

Imagine a mid-sized manufacturing company acquiring new machinery worth $500,000. The accountant’s role includes:

- Verifying the purchase documentation.

- Assigning a unique asset tag number.

- Recording the asset details (cost, purchase date, useful life) in the asset register.

- Ensuring the asset is categorized correctly (e.g., machinery vs equipment).

This process ensures that the asset is tracked throughout its lifecycle and reflected accurately in financial statements.

Mind Map: Asset Recording Workflow

Example 2: Depreciation Calculation and Reporting

Consider an accountant managing a fleet of delivery vehicles. Using the straight-line depreciation method, they calculate annual depreciation to allocate the cost evenly over the vehicles’ useful life.

- Vehicle cost: $100,000

- Useful life: 5 years

- Annual depreciation: $100,000 / 5 = $20,000

The accountant records this depreciation expense each year, impacting the income statement and reducing the asset’s book value on the balance sheet.

Mind Map: Depreciation Process

Strategic Role: Advising on Asset Optimization

Accountants also provide strategic advice by analyzing asset utilization and recommending whether to repair, replace, or dispose of assets. For example, if maintenance costs for a machine exceed its productivity benefits, the accountant may suggest replacement to improve overall financial performance.

Mind Map: Strategic Asset Management by Accountants

Summary

Accountants are integral to asset management, combining technical accounting skills with strategic insights. Their role ensures assets are accurately recorded, valued, and managed in compliance with standards, while also supporting decision-making to maximize asset value and organizational efficiency.

1.3 Types of Assets: Tangible vs Intangible

In asset management, understanding the types of assets is fundamental for accurate accounting, valuation, and reporting. Assets are broadly classified into two main categories: Tangible Assets and Intangible Assets. Each type has distinct characteristics, accounting treatments, and management considerations.

Tangible Assets

Tangible assets are physical, measurable assets that can be seen and touched. They are often referred to as fixed or tangible property and are essential for the operations of a business.

Examples of Tangible Assets:

- Buildings

- Machinery and Equipment

- Vehicles

- Land

- Furniture and Fixtures

Key Characteristics:

- Physical existence

- Depreciable (except land)

- Used in production or operations

Example: A manufacturing company owns a fleet of delivery trucks. These trucks are tangible assets because they have a physical form, can be used over multiple accounting periods, and depreciate over time.

Intangible Assets

Intangible assets lack physical substance but provide long-term value to the business. They often represent legal rights or competitive advantages.

Examples of Intangible Assets:

- Patents

- Trademarks

- Goodwill

- Copyrights

- Software licenses

Key Characteristics:

- No physical form

- Amortizable over useful life

- Often arise from legal rights or contracts

Example: An accounting firm purchases a software license for a portfolio management system. This license is an intangible asset because it provides value but does not have a physical form.

Mind Map: Overview of Asset Types

Mind Map: Tangible Assets Breakdown

Note: While inventory, cash, and accounts receivable are tangible in nature, this section focuses on fixed tangible assets relevant to asset management.

Mind Map: Intangible Assets Breakdown

Practical Example: Differentiating Tangible and Intangible Assets in Accounting

Scenario: An accounting firm acquires the following:

- Office building

- Accounting software license

- Trademark for its brand

- Office furniture

Classification:

- Office building: Tangible asset (fixed asset)

- Accounting software license: Intangible asset

- Trademark: Intangible asset

- Office furniture: Tangible asset

Accounting Implications:

- Tangible assets like the building and furniture will be capitalized and depreciated over their useful lives.

- Intangible assets like the software license and trademark will be capitalized and amortized based on their estimated useful life or legal protection period.

Best Practice Tips for Accountants

- Maintain Clear Asset Registers: Separate registers for tangible and intangible assets help in tracking and reporting.

- Use Appropriate Valuation Methods: Tangible assets often use historical cost less depreciation, while intangible assets may require impairment testing.

- Review Useful Lives Regularly: Both asset types require periodic review to adjust depreciation/amortization schedules.

- Document Acquisition Details: Include proof of ownership, legal rights, and valuation reports.

Understanding the distinction between tangible and intangible assets enables accountants and portfolio managers to apply the correct accounting treatments, optimize asset utilization, and ensure compliance with financial reporting standards.

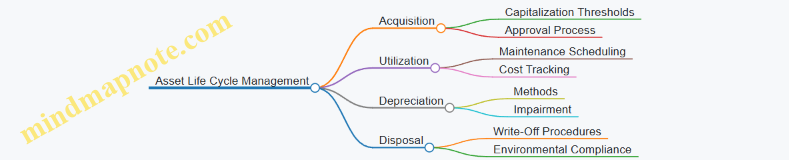

1.4 Overview of Asset Life Cycle Management

Asset Life Cycle Management (ALCM) is a comprehensive approach that tracks and manages an asset through all stages of its existence—from acquisition to disposal. For accountants, understanding ALCM is crucial to ensure accurate financial reporting, compliance, and optimization of asset value.

Key Stages of Asset Life Cycle Management

Stage 1: Acquisition

This is the initial phase where the asset is purchased or obtained. Accountants play a key role in verifying the purchase price, ensuring proper documentation, and deciding whether the asset should be capitalized or expensed.

Example: A company purchases a new office printer for $5,000. The accountant verifies the invoice, confirms it meets the capitalization threshold, and records it as a fixed asset rather than an expense.

Stage 2: Utilization

Once acquired, the asset is put into use. Maintenance and monitoring are essential to preserve asset value and functionality.

Example: The printer requires regular maintenance every six months. The accountant tracks maintenance costs and ensures these are correctly recorded, distinguishing between capital improvements and routine expenses.

Stage 3: Depreciation

Depreciation allocates the cost of the asset over its useful life. Accountants select appropriate methods (e.g., straight-line, declining balance) based on asset type and company policy.

Example: Using straight-line depreciation, the $5,000 printer with a useful life of 5 years will depreciate $1,000 annually.

Stage 4: Revaluation

Assets may require revaluation due to impairment or market value changes. Accountants must test for impairment and adjust asset values accordingly.

Example: If the printer becomes obsolete after 3 years, an impairment test may reveal a lower recoverable amount, requiring a write-down.

Stage 5: Disposal

Disposal involves removing the asset from the books through sale, write-off, or scrapping. Proper documentation and accounting treatment are essential.

Example: The company sells the printer for $500 after 5 years. The accountant records the sale, removes the asset from the books, and recognizes any gain or loss.

Integrated Example: Asset Life Cycle of a Company Vehicle

This example shows how accountants must manage each stage carefully to ensure accurate financial records and compliance.

Summary

Asset Life Cycle Management is a vital framework that helps accountants manage assets efficiently and accurately. By understanding each stage—from acquisition through disposal—and applying best practices with real-world examples, accountants can enhance asset control, optimize financial reporting, and support strategic decision-making.

1.5 Importance of Accurate Asset Tracking: A Practical Example

Accurate asset tracking is a cornerstone of effective asset management, especially for accountants who are responsible for maintaining precise financial records and ensuring compliance with regulatory standards. Without accurate tracking, organizations risk financial misstatements, asset misappropriation, and inefficient resource utilization.

Why Accurate Asset Tracking Matters

- Financial Accuracy: Ensures that asset values on the balance sheet reflect reality, supporting accurate depreciation and impairment calculations.

- Regulatory Compliance: Helps meet audit requirements and adhere to accounting standards such as IFRS and GAAP.

- Operational Efficiency: Enables timely maintenance, reduces downtime, and optimizes asset utilization.

- Risk Mitigation: Prevents theft, loss, or misuse of assets through proper oversight.

Mind Map: Key Benefits of Accurate Asset Tracking

Practical Example: Tracking IT Equipment in a Mid-Sized Accounting Firm

Scenario: A mid-sized accounting firm recently invested in new IT equipment, including laptops, servers, and networking devices. The accounting team is tasked with tracking these assets accurately to ensure proper capitalization, depreciation, and maintenance.

Step 1: Asset Identification and Tagging

- Each piece of equipment is assigned a unique asset tag number.

- Details such as purchase date, cost, vendor, and warranty period are recorded in the asset register.

Step 2: Asset Register Maintenance

- The asset register is updated monthly to reflect any changes such as new acquisitions, disposals, or transfers.

Step 3: Depreciation Tracking

- Depreciation is calculated using the straight-line method over the expected useful life.

- Monthly depreciation expenses are recorded in the accounting system.

Step 4: Maintenance and Repairs

- Maintenance activities are logged against each asset.

- Costs related to repairs are tracked separately to analyze asset performance.

Step 5: Disposal and Write-Off

- When equipment becomes obsolete, disposal is recorded with details of sale or write-off.

- Gain or loss on disposal is calculated and reflected in financial statements.

Mind Map: Asset Tracking Workflow Example

Example Impact of Poor Asset Tracking

Imagine if the accounting firm failed to tag and record some laptops:

- Financial Impact: Assets might be underreported, leading to understated depreciation expenses and overstated profits.

- Audit Risk: Auditors may flag discrepancies, causing delays and potential penalties.

- Operational Issues: Maintenance schedules might be missed, resulting in equipment failure and productivity loss.

Summary

Accurate asset tracking is vital for accountants to maintain financial integrity, comply with regulations, and support operational efficiency. By implementing systematic tracking processes, accountants can provide reliable data that informs strategic decisions and safeguards organizational assets.

2. Asset Identification and Classification

2.1 Best Practices for Asset Identification and Tagging

Effective asset identification and tagging are foundational steps in asset management that enable accurate tracking, valuation, and reporting. For accountants, mastering these practices ensures transparency, compliance, and efficient asset lifecycle management.

Why Asset Identification and Tagging Matter

- Provides a unique identity to each asset

- Facilitates accurate record-keeping and audit trails

- Enhances asset tracking and reduces loss or misplacement

- Enables streamlined maintenance and depreciation calculations

Best Practices for Asset Identification and Tagging

Assign Unique Asset IDs

- Use a standardized format (e.g., prefix + numeric code)

- Ensure IDs are non-repetitive and consistent across systems

Use Durable and Visible Tags

- Choose tags resistant to environmental conditions (waterproof, heat-resistant)

- Use barcode, QR code, or RFID tags depending on asset type and tracking needs

Maintain a Centralized Asset Register

- Record asset ID, description, location, acquisition date, cost, and custodian

- Update register promptly with any changes

Categorize Assets Clearly

- Group assets by type, department, or usage

- Helps in reporting and depreciation method selection

Integrate Technology for Efficiency

- Utilize asset management software with tagging capabilities

- Automate scanning and updating processes

Train Staff on Tagging Protocols

- Ensure consistent tagging and data entry

- Regularly audit tagging accuracy

Mind Map: Asset Identification and Tagging Best Practices

Example 1: Implementing Asset Tagging in a Mid-Sized Accounting Firm

Scenario: A mid-sized accounting firm wants to improve its fixed asset tracking to reduce discrepancies during audits.

Steps Taken:

- Developed a unique asset ID format: “ACCT-YYYY-XXX” (e.g., ACCT-2024-001).

- Purchased durable barcode tags and attached them to all computers, printers, and office furniture.

- Created a centralized Excel-based asset register capturing asset ID, description, purchase date, cost, location, and custodian.

- Trained the administrative team on scanning barcodes during asset movement.

- Conducted quarterly audits to verify tag presence and register accuracy.

Outcome:

- Reduced asset misplacement by 30% in the first year.

- Simplified depreciation tracking and improved audit readiness.

Example 2: Using RFID Tags for High-Value Assets in Portfolio Management

Scenario: A portfolio manager overseeing multiple client assets wants real-time tracking of high-value equipment.

Steps Taken:

- Selected RFID tags for their ability to be scanned without line-of-sight.

- Tagged all high-value assets such as servers and specialized software licenses.

- Integrated RFID scanning with asset management software to update asset location automatically.

- Set up alerts for unauthorized asset movement.

Outcome:

- Enhanced security and reduced asset loss.

- Improved real-time visibility of asset location and status.

Summary

Adopting best practices in asset identification and tagging empowers accountants and portfolio managers to maintain accurate, reliable asset records. This foundation supports better financial reporting, compliance, and operational efficiency.

For further reading, consider exploring asset tagging technologies and software solutions tailored for finance and asset management sectors.

2.2 Classification of Assets for Financial Reporting

Asset classification is a fundamental step in financial reporting that helps accountants and portfolio managers present a clear and accurate picture of an organization’s financial position. Proper classification ensures compliance with accounting standards and facilitates better decision-making.

What is Asset Classification?

Asset classification involves grouping assets into categories based on their characteristics, liquidity, usage, and expected life span. This grouping helps in applying appropriate accounting treatments such as depreciation, impairment, and disclosure.

Main Categories of Assets for Financial Reporting

- Current Assets

- Non-Current Assets (Fixed Assets)

- Intangible Assets

- Financial Assets

Mind Map: Asset Classification Overview

Current Assets

Definition: Assets expected to be converted into cash or used up within one operating cycle or one year, whichever is longer.

Examples:

- Cash and Cash Equivalents: Physical cash, bank balances, money market funds.

- Accounts Receivable: Money owed by customers for goods or services delivered.

- Inventory: Raw materials, work-in-progress, and finished goods.

- Prepaid Expenses: Payments made in advance for services or goods.

Example Scenario: A company has $50,000 in cash, $120,000 in accounts receivable, $80,000 in inventory, and $10,000 prepaid insurance. These are all classified as current assets because they will be liquidated or consumed within the year.

Non-Current Assets (Fixed Assets)

Definition: Assets held for use in the production or supply of goods and services, expected to be used for more than one year.

Examples:

- Property, Plant, and Equipment (PPE): Buildings, machinery, vehicles.

- Investment Property: Real estate held for rental income or capital appreciation.

- Long-term Investments: Investments not intended to be sold within the next year.

Example Scenario: An accounting firm owns office equipment worth $200,000 and a building valued at $1,000,000. These are classified as non-current assets and depreciated over their useful lives.

Mind Map: Current vs Non-Current Assets

Intangible Assets

Definition: Non-monetary assets without physical substance but provide future economic benefits.

Examples:

- Goodwill: Value arising from acquisition of another company.

- Patents: Exclusive rights to use inventions.

- Trademarks: Brand names and logos.

Example Scenario: A portfolio manager evaluates a company that recently acquired a competitor. The excess purchase price over fair value of net assets is recorded as goodwill, an intangible asset.

Financial Assets

Definition: Assets representing contractual rights to receive cash or another financial instrument.

Examples:

- Stocks and bonds held for investment.

- Derivative instruments like options and futures.

Example Scenario: An accountant managing a client’s portfolio classifies shares of publicly traded companies as financial assets, recorded at fair value.

Mind Map: Intangible and Financial Assets

Best Practices for Asset Classification

- Consistency: Use consistent classification criteria across reporting periods.

- Documentation: Maintain clear documentation for classification decisions.

- Review: Periodically review asset classifications to reflect changes in use or intent.

- Compliance: Align classification with applicable accounting standards (e.g., IFRS, GAAP).

Integrated Example: Asset Classification in Practice

Scenario: An accountant at a mid-sized manufacturing company is preparing the year-end financial statements. The company owns:

- $100,000 in cash

- $250,000 in accounts receivable

- $500,000 in inventory

- $1,500,000 in machinery

- $300,000 in patents

- $200,000 in equity investments

Classification:

- Current Assets: Cash, Accounts Receivable, Inventory

- Non-Current Assets: Machinery

- Intangible Assets: Patents

- Financial Assets: Equity Investments

This classification ensures accurate presentation on the balance sheet and proper application of depreciation, amortization, and valuation methods.

By mastering asset classification, accountants and portfolio managers can enhance financial transparency, support compliance, and provide valuable insights for strategic asset management.

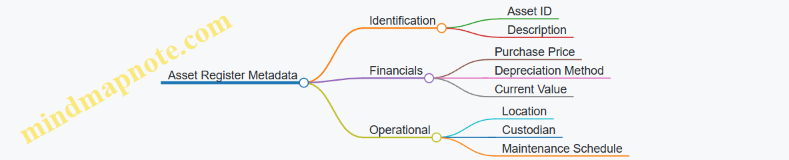

2.3 Using Asset Registers: Structure and Maintenance

An asset register is a comprehensive record of all the assets owned by an organization. For accountants, maintaining an accurate and up-to-date asset register is critical for financial reporting, compliance, and effective asset management.

What is an Asset Register?

An asset register is essentially a detailed database or ledger that tracks each asset’s key information, including acquisition details, valuation, depreciation, location, and status.

Importance of Asset Registers for Accountants

- Ensures accurate financial statements

- Facilitates depreciation and impairment calculations

- Supports audit and compliance requirements

- Helps in asset tracking and loss prevention

- Provides data for budgeting and capital planning

Structure of an Asset Register

A well-structured asset register typically contains the following fields:

- Asset ID/Tag Number: Unique identifier for each asset

- Asset Description: Clear description of the asset

- Category/Class: Classification such as machinery, vehicles, IT equipment

- Acquisition Date: Date when the asset was purchased or acquired

- Purchase Cost: Original cost of the asset

- Location: Physical location or department

- Custodian: Person responsible for the asset

- Useful Life: Estimated useful life for depreciation

- Depreciation Method: Method applied (e.g., straight-line)

- Accumulated Depreciation: Total depreciation charged to date

- Net Book Value: Current value after depreciation

- Status: Active, disposed, under maintenance

Mind Map: Asset Register Structure

Example: Sample Asset Register Entry

| Asset ID | Description | Category | Acquisition Date | Purchase Cost | Location | Custodian | Useful Life (Years) | Depreciation Method | Accumulated Depreciation | Net Book Value | Status |

|---|---|---|---|---|---|---|---|---|---|---|---|

| A-1001 | Dell Laptop XPS 13 | IT Equipment | 2022-01-15 | $1,200 | HQ Office | John Smith | 5 | Straight-Line | $240 | $960 | Active |

Maintenance of Asset Registers

Maintaining an asset register involves regular updates and audits to ensure data accuracy and completeness.

Best Practices for Maintenance:

- Regular Updates: Record acquisitions, disposals, transfers, and maintenance activities promptly.

- Periodic Physical Verification: Conduct physical asset counts to verify existence and condition.

- Reconciliation: Match physical counts with register data to identify discrepancies.

- Access Controls: Restrict editing rights to authorized personnel to prevent unauthorized changes.

- Backup and Security: Regularly back up the register and secure sensitive data.

Mind Map: Asset Register Maintenance

Example: Asset Register Maintenance Workflow

- Asset Acquisition: New asset purchased and details entered into the register.

- Tagging: Asset tagged with unique ID.

- Physical Verification: Quarterly physical count performed.

- Reconciliation: Differences between physical count and register investigated.

- Update Register: Corrections made to reflect accurate status.

- Disposal: When asset is sold or scrapped, disposal details recorded.

Practical Example: Using Excel for Asset Register

Many small to mid-sized firms use Excel to maintain their asset registers. Here’s a simple example of how to set it up:

- Create columns for each key field (Asset ID, Description, etc.)

- Use data validation for categories and status to maintain consistency

- Apply formulas to calculate accumulated depreciation and net book value

- Use conditional formatting to highlight assets nearing end of useful life

Example Formula: Straight-Line Depreciation in Excel

=IF(Status="Active", Purchase_Cost / Useful_Life * Years_Used, 0)

This formula calculates annual depreciation for active assets.

Summary

A well-maintained asset register is the backbone of effective asset management for accountants. It ensures transparency, compliance, and supports strategic financial decisions. By structuring the register properly and committing to regular maintenance, accountants can significantly enhance asset visibility and control within their organizations.

2.4 Example: Setting up an Asset Register for a Mid-Sized Firm

Setting up an asset register is a foundational step for effective asset management, especially for mid-sized firms where asset tracking can become complex without a structured approach. This section will guide you through the process of creating a comprehensive asset register, including best practices, practical examples, and mind maps to visualize the workflow.

What is an Asset Register?

An asset register is a detailed record of all the assets owned by a firm. It typically includes information such as asset description, acquisition date, cost, location, depreciation, and current status.

Why is it Important?

- Ensures accurate financial reporting

- Facilitates asset tracking and maintenance

- Supports compliance with accounting standards

- Helps in budgeting and forecasting

Step-by-Step Guide to Setting up an Asset Register

Step 1: Define Asset Categories

Start by classifying assets into categories that make sense for your firm. Common categories include:

- Property, Plant & Equipment (PPE)

- Vehicles

- IT Equipment

- Furniture & Fixtures

- Intangible Assets

Mind Map: Asset Categories

Step 2: Determine Required Data Fields

Identify the key data points to capture for each asset. Typical fields include:

- Asset ID (unique identifier)

- Description

- Category

- Purchase Date

- Purchase Cost

- Location

- Responsible Department/Person

- Depreciation Method

- Accumulated Depreciation

- Net Book Value

- Warranty/Service Information

Mind Map: Asset Data Fields

Step 3: Choose a Platform or Tool

For a mid-sized firm, options include:

- Excel or Google Sheets (for simplicity and flexibility)

- Dedicated Asset Management Software (for scalability and automation)

Step 4: Populate the Register

Begin by gathering existing asset information from invoices, purchase orders, and physical verification.

Example Table (Excel Format):

| Asset ID | Description | Category | Purchase Date | Purchase Cost | Location | Department | Depreciation Method | Accumulated Depreciation | Net Book Value |

|---|---|---|---|---|---|---|---|---|---|

| A001 | Dell Laptop XPS 15 | IT Equipment | 2023-01-15 | $1,500 | HQ Office | IT | Straight Line | $250 | $1,250 |

| A002 | Office Desk | Furniture & Fixtures | 2022-06-10 | $300 | HQ Office | Admin | Straight Line | $60 | $240 |

Step 5: Implement Asset Tagging

Assign unique asset IDs physically to assets using barcode or QR code labels to facilitate tracking.

Step 6: Establish Update and Audit Procedures

Set regular intervals (e.g., quarterly) to update the register and conduct physical audits to ensure accuracy.

Practical Example: Setting Up the Asset Register for “MidCo Ltd”

Background: MidCo Ltd is a mid-sized marketing firm with 150 employees. They have recently expanded their IT infrastructure and office space.

Implementation:

- Categorized assets into IT Equipment, Furniture, and Leasehold Improvements.

- Created an Excel-based asset register with the fields outlined above.

- Assigned asset IDs starting with category codes (e.g., IT001, FUR001).

- Tagged all new laptops and office furniture with QR codes.

- Designated the Finance department to update the register monthly.

Sample Entry:

| Asset ID | Description | Category | Purchase Date | Purchase Cost | Location | Department | Depreciation Method | Accumulated Depreciation | Net Book Value |

|---|---|---|---|---|---|---|---|---|---|

| IT001 | MacBook Pro 16 inch | IT Equipment | 2024-03-01 | $2,400 | HQ Office | IT | Declining Balance | $200 | $2,200 |

Mind Map: Asset Register Setup Workflow

Tips for Accountants

- Maintain consistency in naming conventions and data entry.

- Use filters and pivot tables in Excel for easy reporting.

- Collaborate with IT and Operations for accurate asset information.

- Document procedures for onboarding new assets.

By following this structured approach, accountants can establish a reliable asset register that supports accurate financial reporting and efficient asset management in a mid-sized firm.

2.5 Leveraging Technology for Asset Identification

In today’s fast-paced financial and asset management environment, leveraging technology for asset identification is not just a convenience but a necessity. Accurate and efficient asset identification helps accountants and portfolio managers maintain up-to-date records, reduce errors, and streamline reporting processes.

Why Technology Matters in Asset Identification

- Accuracy: Automated systems reduce human error in recording asset details.

- Efficiency: Speeds up the process of tagging and tracking assets.

- Real-Time Updates: Enables instant updates to asset registers.

- Integration: Seamlessly connects with accounting and ERP systems.

Common Technologies Used for Asset Identification

- Barcode Systems

- Radio Frequency Identification (RFID)

- QR Codes

- GPS Tracking

- IoT Sensors

Mind Map: Technologies for Asset Identification

Example 1: Implementing Barcode Systems in a Mid-Sized Accounting Firm

Scenario: An accounting firm manages a fleet of laptops, printers, and office equipment across three locations. Manual tracking led to misplaced items and inaccurate asset records.

Solution:

- Each asset was tagged with a unique barcode.

- Staff used handheld barcode scanners to log asset movements.

- Asset register software automatically updated inventory levels.

Outcome:

- Reduced asset loss by 30% within six months.

- Improved audit readiness with accurate records.

Example 2: Using RFID for Asset Tracking in a Finance Company

Scenario: A finance company manages hundreds of physical documents and IT equipment. Manual tracking was time-consuming and prone to errors.

Solution:

- RFID tags were attached to high-value assets and document storage boxes.

- RFID readers installed at entry/exit points automatically logged asset movements.

- Integration with the accounting system provided real-time asset status.

Outcome:

- Asset check-in/check-out time reduced by 50%.

- Enhanced security and reduced asset misplacement.

Best Practices for Leveraging Technology

- Choose the Right Technology: Consider asset type, volume, and budget.

- Train Staff Thoroughly: Ensure everyone understands how to use the system.

- Integrate Systems: Connect asset identification tools with accounting and ERP software.

- Regularly Update Asset Data: Schedule periodic audits to verify accuracy.

- Plan for Scalability: Select solutions that can grow with your organization.

Mind Map: Best Practices for Technology-Driven Asset Identification

By embracing technology for asset identification, accountants and portfolio managers can significantly improve the accuracy, efficiency, and security of their asset management processes. This not only supports compliance and reporting requirements but also enhances decision-making and operational effectiveness.

3. Asset Valuation and Depreciation Methods

3.1 Principles of Asset Valuation in Accounting

Asset valuation is a fundamental aspect of accounting that ensures assets are recorded and reported at appropriate values on financial statements. Accurate valuation impacts decision-making, financial analysis, and compliance with accounting standards.

Key Principles of Asset Valuation

- Historical Cost Principle: Assets are recorded at their original purchase price, including all costs necessary to bring the asset to its intended use.

- Fair Value Principle: Assets are valued at the price they would fetch in an orderly transaction between market participants at the measurement date.

- Net Realizable Value (NRV): The estimated selling price of an asset in the ordinary course of business, less any costs of completion and disposal.

- Replacement Cost: The cost to replace an asset with a similar one at current market prices.

- Present Value: The current worth of future cash flows expected from the asset, discounted at an appropriate rate.

- Impairment Principle: Assets should be written down if their carrying amount exceeds their recoverable amount.

Mind Map: Principles of Asset Valuation

Explanation and Examples

-

Historical Cost Principle

- This is the most common valuation method used in accounting.

- Example: A company purchases machinery for $100,000 and pays $5,000 for installation. The asset is recorded at $105,000.

-

Fair Value Principle

- Used when assets are revalued or for financial instruments.

- Example: A portfolio manager revalues an investment property to its current market price of $500,000, up from the historical cost of $450,000.

-

Net Realizable Value (NRV)

- Often applied to inventory or receivables.

- Example: Inventory originally costing $20,000 is expected to sell for $18,000 after $2,000 in selling costs. NRV is $16,000.

-

Replacement Cost

- Useful for insurance or asset management decisions.

- Example: Replacing a delivery truck today costs $60,000, although its book value is $40,000.

-

Present Value

- Common in valuing long-term assets or investments.

- Example: A piece of equipment is expected to generate $10,000 annually for 5 years. Discounting these cash flows at 8% gives a present value of approximately $40,000.

-

Impairment Principle

- Applied when asset value declines unexpectedly.

- Example: A machine with a carrying amount of $30,000 is damaged and its recoverable amount is estimated at $18,000. The asset is impaired by $12,000.

Mind Map: Applying Valuation Principles in Practice

Practical Example: Valuing a Company Vehicle

- Purchase Price: $25,000

- Additional Costs (tax, registration): $2,000

- Estimated Useful Life: 5 years

- Residual Value: $5,000

Step 1: Initial Valuation

- Recorded at $27,000 (purchase price + additional costs)

Step 2: Depreciation (Straight-Line Method)

- Annual Depreciation = (27,000 - 5,000) / 5 = $4,400

Step 3: Fair Value Assessment After 3 Years

- Market value estimated at $15,000

- Carrying amount after 3 years = 27,000 - (4,400 * 3) = $13,800

Since fair value ($15,000) > carrying amount ($13,800), no impairment needed.

Summary

Understanding and applying the correct asset valuation principles ensures that financial statements reflect true and fair values. Accountants must select the appropriate valuation method based on asset type, purpose, and regulatory requirements, while documenting assumptions and calculations clearly.

For accountants and portfolio managers, mastering these principles enables better asset management, improved reporting accuracy, and informed strategic decisions.

3.2 Common Depreciation Methods: Straight-Line, Declining Balance, and Units of Production

Depreciation is a key accounting concept that allocates the cost of a tangible asset over its useful life. Understanding the different depreciation methods helps accountants accurately reflect asset value and expense recognition in financial statements. Below, we explore the three most common depreciation methods with detailed explanations, mind maps, and practical examples.

Straight-Line Depreciation

Definition: This method spreads the cost of an asset evenly over its useful life.

Formula:

\[ \text{Annual Depreciation Expense} = \frac{\text{Cost of Asset} - \text{Residual Value}}{\text{Useful Life (years)}} \]

Mind Map:

Example:

An accountant purchases office equipment costing $10,000 with an expected residual value of $1,000 after 5 years.

- Annual Depreciation = (10,000 - 1,000) / 5 = $1,800

Each year, $1,800 is recorded as depreciation expense.

Declining Balance Depreciation

Definition: This accelerated method applies a fixed depreciation rate to the book value of the asset each year, resulting in higher expenses in early years and lower expenses later.

Common Variant: Double Declining Balance (DDB) method uses twice the straight-line rate.

Formula (DDB):

\[ \text{Depreciation Expense} = 2 \times \frac{1}{\text{Useful Life}} \times \text{Book Value at Beginning of Year} \]

Mind Map:

Example:

A delivery truck costs $20,000 with a useful life of 5 years.

- Straight-line rate = 1/5 = 20%

- Double declining rate = 40%

| Year | Beginning Book Value | Depreciation Expense (40%) | Ending Book Value |

|---|---|---|---|

| 1 | $20,000 | $8,000 | $12,000 |

| 2 | $12,000 | $4,800 | $7,200 |

| 3 | $7,200 | $2,880 | $4,320 |

| 4 | $4,320 | $1,728 | $2,592 |

| 5 | $2,592 | $2,592* | $0 |

*In the final year, depreciation is adjusted to fully depreciate the asset.

Units of Production Depreciation

Definition: Depreciation is based on actual usage or output rather than time, ideal for assets whose wear depends on usage.

Formula:

\[ \text{Depreciation Expense} = \frac{\text{Cost} - \text{Residual Value}}{\text{Total Estimated Units}} \times \text{Units Produced in Period} \]

Mind Map:

Example:

A manufacturing machine costs $50,000 with a residual value of $5,000 and an estimated total usage of 100,000 hours.

If the machine is used 10,000 hours in the first year:

- Depreciation Expense = ((50,000 - 5,000) / 100,000) * 10,000 = $4,500

If usage varies each year, depreciation expense will adjust accordingly.

Summary Table of Methods

| Method | Expense Pattern | Best Used For | Example Asset |

|---|---|---|---|

| Straight-Line | Even over useful life | General assets with consistent use | Office equipment |

| Declining Balance | Accelerated (front-loaded) | Assets losing value quickly early | Vehicles, technology |

| Units of Production | Based on actual usage | Usage-dependent assets | Manufacturing machinery |

By understanding these methods, accountants can select the most appropriate depreciation approach to reflect asset consumption accurately, optimize tax benefits, and provide clear financial insights to portfolio managers and stakeholders.

3.3 Selecting the Appropriate Depreciation Method: Case Study

Selecting the right depreciation method is crucial for accurate financial reporting and tax compliance. Different assets and business contexts require different approaches. This section explores a detailed case study to illustrate how accountants can evaluate and choose the most appropriate depreciation method.

Case Study Overview: ABC Manufacturing Company

ABC Manufacturing recently purchased a new piece of machinery for $100,000. The machinery is expected to have a useful life of 10 years with a residual value of $10,000. The company wants to understand which depreciation method best reflects the asset’s usage and financial impact.

Step 1: Understanding Depreciation Methods

Here is a mind map summarizing the common depreciation methods:

Step 2: Applying Each Method to ABC’s Machinery

1. Straight-Line Method

- Formula: (Cost - Residual Value) / Useful Life

- Calculation: ($100,000 - $10,000) / 10 = $9,000 per year

2. Declining Balance Method (Double Declining)

- Rate: 2 / Useful Life = 2 / 10 = 20%

- Year 1 Depreciation: $100,000 x 20% = $20,000

- Year 2 Depreciation: ($100,000 - $20,000) x 20% = $16,000

- Depreciation decreases over time

3. Units of Production Method

- Assumes 100,000 units produced over life

- Depreciation per unit: ($100,000 - $10,000) / 100,000 = $0.90 per unit

- If 12,000 units produced in Year 1: 12,000 x $0.90 = $10,800

Step 3: Evaluating Which Method Fits Best

- Asset Usage Pattern

- Consistent usage each year?

- Yes: Straight-Line preferred

- Heavy usage in early years?

- Yes: Declining Balance preferred

- Usage varies significantly?

- Yes: Units of Production preferred

- Consistent usage each year?

- Financial Reporting Objectives

- Stable expenses for budgeting?

- Straight-Line

- Tax benefits from accelerated depreciation?

- Declining Balance

- Matching expense to actual wear?

- Units of Production

- Stable expenses for budgeting?

Step 4: Decision for ABC Manufacturing

- ABC expects consistent production levels each year.

- They prefer predictable expenses for budgeting.

- Therefore, Straight-Line Method is the most appropriate.

Step 5: Example Journal Entries (Straight-Line)

| Year | Depreciation Expense | Accumulated Depreciation | Book Value |

|---|---|---|---|

| 1 | $9,000 | $9,000 | $91,000 |

| 2 | $9,000 | $18,000 | $82,000 |

Journal Entry:

Dr Depreciation Expense $9,000

Cr Accumulated Depreciation $9,000

Summary

This case study demonstrates how understanding asset usage, financial goals, and accounting principles guides the selection of depreciation methods. Accountants must evaluate each asset individually and consider both financial and operational factors.

By applying these best practices, accountants and portfolio managers can ensure accurate asset valuation and reporting.

Additional Example: Choosing Declining Balance for Technology Equipment

- Tech equipment becomes obsolete quickly.

- Higher depreciation in early years matches rapid value loss.

- Accelerated depreciation also offers tax benefits.

Mind map:

Additional Example: Units of Production for Vehicle Fleet

- Vehicles’ wear depends on miles driven.

- Depreciation tied to actual usage reflects true value loss.

Mind map:

By integrating these examples and mind maps, accountants can better visualize and apply depreciation methods tailored to their asset portfolios.

3.4 Impairment Testing and Revaluation Procedures

Impairment testing and revaluation are critical components of asset management for accountants, ensuring that asset values reported in financial statements reflect their true economic value. This section will cover the concepts, procedures, and practical examples to help accountants effectively manage asset impairments and revaluations.

What is Asset Impairment?

Asset impairment occurs when the carrying amount of an asset exceeds its recoverable amount, meaning the asset is overvalued on the books and needs adjustment.

- Carrying Amount: The value at which the asset is recognized on the balance sheet.

- Recoverable Amount: The higher of an asset’s fair value less costs of disposal and its value in use.

When to Perform Impairment Testing?

- Annually for intangible assets with indefinite useful lives.

- When there is an indication that an asset may be impaired (e.g., physical damage, obsolescence, market decline).

Mind Map: Impairment Testing Process

Revaluation Procedures

Revaluation involves adjusting the carrying amount of an asset to its fair value, often used for property, plant, and equipment.

- Must be done regularly to ensure carrying amounts do not differ materially from fair value.

- Revaluation increases are credited to other comprehensive income and accumulated in equity under revaluation surplus.

- Revaluation decreases are recognized in profit or loss, unless reversing a previous revaluation surplus.

Mind Map: Revaluation Procedure

Practical Example 1: Impairment Testing of a Manufacturing Machine

Scenario: A manufacturing machine was purchased for $500,000 with accumulated depreciation of $200,000. Due to new technology, the machine’s market value has dropped significantly.

- Carrying amount: $500,000 - $200,000 = $300,000

- Fair value less costs to sell: $220,000

- Value in use (discounted cash flows): $250,000

Recoverable amount: Higher of $220,000 and $250,000 = $250,000

Impairment loss: $300,000 - $250,000 = $50,000

Accounting treatment: Recognize $50,000 impairment loss in profit and loss and reduce the carrying amount of the machine to $250,000.

Practical Example 2: Revaluation of Office Building

Scenario: An office building originally recorded at $1,000,000 with accumulated depreciation of $100,000 is revalued based on a recent appraisal.

- Appraised fair value: $1,200,000

- Carrying amount before revaluation: $900,000

Revaluation increase: $1,200,000 - $900,000 = $300,000

Accounting treatment: Increase the asset’s carrying amount to $1,200,000 and credit $300,000 to revaluation surplus in equity.

Update depreciation based on the new carrying amount and remaining useful life.

Key Best Practices

- Perform impairment reviews regularly and when triggers are identified.

- Document assumptions and calculations thoroughly.

- Use qualified appraisers for revaluations.

- Communicate changes clearly in financial reports.

- Coordinate with portfolio managers to understand asset utilization and market conditions.

By integrating impairment testing and revaluation procedures into your asset management practices, accountants can ensure financial statements reflect accurate asset values, supporting better decision-making and compliance with accounting standards.

3.5 Practical Example: Calculating Depreciation for a Fleet of Vehicles

Depreciation is a key accounting process that allocates the cost of an asset over its useful life. For accountants managing a fleet of vehicles, understanding how to calculate depreciation accurately is essential for financial reporting and tax purposes.

Step 1: Gather Asset Information

Before calculating depreciation, collect the following details for each vehicle:

- Purchase cost

- Estimated useful life (in years or mileage)

- Residual (salvage) value

- Date of acquisition

Example:

| Vehicle | Purchase Cost | Useful Life (Years) | Residual Value | Acquisition Date |

|---|---|---|---|---|

| Car A | $30,000 | 5 | $5,000 | Jan 1, 2023 |

| Car B | $45,000 | 7 | $7,000 | Mar 15, 2023 |

Step 2: Choose Depreciation Method

Common depreciation methods include:

- Straight-Line Method

- Declining Balance Method

- Units of Production Method

For simplicity, we will use the Straight-Line Method in this example.

Step 3: Calculate Annual Depreciation Expense

Formula:

\[ \text{Annual Depreciation} = \frac{\text{Cost} - \text{Residual Value}}{\text{Useful Life}} \]

Calculations:

-

Car A:

\[ \frac{30,000 - 5,000}{5} = \frac{25,000}{5} = 5,000\text{ per year} \]

-

Car B:

\[ \frac{45,000 - 7,000}{7} = \frac{38,000}{7} \approx 5,429\text{ per year} \]

Step 4: Record Depreciation Journal Entries

At the end of each accounting period:

| Account | Debit | Credit |

|---|---|---|

| Depreciation Expense | $5,000 | |

| Accumulated Depreciation | $5,000 |

(For Car A, similarly for Car B with $5,429)

Mind Map: Depreciation Calculation Process

Step 5: Consider Partial Year Depreciation

If a vehicle is acquired partway through the year, calculate depreciation proportionally.

Example: Car B acquired on March 15, 2023.

-

Number of months in service in 2023: 10.5 months (March 15 to Dec 31)

-

Monthly depreciation = $5,429 / 12 = $452.42

-

Partial year depreciation = $452.42 * 10.5 ≈ $4,750

Mind Map: Partial Year Depreciation

Step 6: Example Summary Table

| Vehicle | Annual Depreciation | Months in Service | Partial Year Depreciation |

|---|---|---|---|

| Car A | $5,000 | 12 | $5,000 |

| Car B | $5,429 | 10.5 | $4,750 |

Additional Tips for Accountants Managing Vehicle Fleets

- Maintain an updated asset register including acquisition dates and costs.

- Review residual values annually to reflect market conditions.

- Consider using fleet management software to automate depreciation calculations.

- Coordinate with tax advisors to align depreciation methods with tax regulations.

This practical example demonstrates how straightforward depreciation calculations can be when broken down step-by-step, helping accountants provide accurate financial information and support portfolio managers in asset valuation and decision-making.

4. Asset Acquisition and Capitalization Policies

4.1 Defining Capital vs Expense: Accounting Best Practices

Understanding the distinction between capital expenditures (CapEx) and operating expenses (OpEx) is fundamental for accountants managing asset accounting. This section explores the definitions, accounting treatments, and best practices with clear examples and mind maps to clarify the concepts.

What is Capital Expenditure (CapEx)?

Capital expenditures are funds used by a company to acquire, upgrade, or extend the life of long-term assets. These assets provide benefits over multiple accounting periods.

- Examples: Purchase of machinery, building renovations, software licenses with multi-year use.

- Accounting Treatment: Capitalized on the balance sheet and depreciated or amortized over the asset’s useful life.

What is Operating Expense (OpEx)?

Operating expenses are the costs required for the day-to-day functioning of the business. These expenses are consumed within the current accounting period.

- Examples: Rent, utilities, office supplies, routine maintenance.

- Accounting Treatment: Expensed immediately on the income statement.

Mind Map: Capital vs Expense Decision Factors

Best Practices for Defining Capital vs Expense

-

Establish Clear Capitalization Thresholds

- Define a minimum dollar amount for capitalizing assets (e.g., $5,000).

- Example: A $4,000 purchase of office chairs is expensed, while a $6,000 purchase is capitalized.

-

Evaluate Asset Life Expectancy

- Capitalize expenditures that provide benefit beyond one year.

- Example: Software license for 3 years is capitalized; monthly subscription is expensed.

-

Assess Nature of the Expenditure

- Distinguish between improvements (capitalize) and repairs (expense).

- Example: Replacing an engine in a delivery truck extends life → capitalize; oil change → expense.

-

Document Policies and Train Staff

- Maintain written policies to ensure consistency.

- Provide training to procurement and accounting teams.

-

Review Regularly

- Periodically review thresholds and policies to align with business needs and regulations.

Example 1: Capitalizing a New Computer Purchase

Scenario: A company buys a laptop for $1,200 with an expected useful life of 3 years.

- Threshold: $1,000

- Since $1,200 > $1,000 and useful life > 1 year, capitalize.

Accounting Treatment:

- Record as an asset on the balance sheet.

- Depreciate over 3 years using straight-line method.

Example 2: Expensing Office Supplies

Scenario: The company purchases office supplies worth $300.

- Threshold: $1,000

- Since $300 < $1,000, expense immediately.

Accounting Treatment:

- Record as an expense on the income statement.

Mind Map: Accounting Treatment Flow

Summary

Distinguishing capital expenditures from operating expenses ensures accurate financial reporting, compliance with accounting standards, and effective asset management. By applying clear thresholds, evaluating asset life, and documenting policies, accountants can make consistent and informed decisions.

For further reading, accountants can refer to IAS 16 (Property, Plant and Equipment) or ASC 360 (Property, Plant, and Equipment) depending on their jurisdiction.

4.2 Establishing Capitalization Thresholds

What is a Capitalization Threshold?

A capitalization threshold is the minimum dollar amount at which an asset purchase is recorded as a capital asset rather than an expense. This threshold helps organizations determine which purchases should be capitalized and depreciated over time versus which should be expensed immediately in the income statement.

Why Establish Capitalization Thresholds?

- Consistency: Ensures uniform treatment of asset purchases across the organization.

- Materiality: Avoids tracking and depreciating insignificant assets that do not materially impact financial statements.

- Efficiency: Reduces administrative burden by limiting the number of assets that require detailed tracking.

Factors to Consider When Setting Capitalization Thresholds

Mind Map: Factors Influencing Capitalization Thresholds

Common Practices and Examples

| Company Type | Typical Capitalization Threshold | Rationale |

|---|---|---|

| Small Business | $1,000 - $5,000 | Minimize tracking of low-value assets |

| Medium Enterprise | $5,000 - $10,000 | Balance between control and efficiency |

| Large Corporation | $10,000+ | Focus on material assets, reduce admin load |

Example 1:

A mid-sized accounting firm sets a capitalization threshold of $5,000. A new office printer costing $4,200 is expensed immediately, while a $7,500 server purchase is capitalized and depreciated over its useful life.

Example 2:

A portfolio management company with many intangible assets sets a lower threshold of $2,000 to capture software licenses and subscriptions as capital assets.

Steps to Establish Capitalization Thresholds

Mind Map: Steps to Establish Capitalization Thresholds

Practical Example: Setting a Capitalization Threshold Policy

Scenario:

An accounting firm with annual revenues of $50 million wants to establish a capitalization threshold that balances administrative efficiency with accurate financial reporting.

Process:

- Review past asset purchases and identify that most assets under $3,000 have minimal impact on financial statements.

- Benchmark shows similar firms use $5,000 as a threshold.

- Consult tax advisors to ensure compliance.

- Set threshold at $5,000.

- Draft policy stating all asset purchases above $5,000 are capitalized.

- Policy approved by CFO and audit committee.

- Communicate policy to procurement and accounting teams.

Outcome:

- The firm capitalizes IT equipment, furniture, and software licenses above $5,000.

- Smaller purchases are expensed immediately, reducing tracking burden.

Tips for Accountants

- Regularly review thresholds to reflect inflation and business growth.

- Coordinate with tax professionals to align accounting and tax capitalization policies.

- Document all decisions and rationale for audit purposes.

- Use asset management software to automate threshold enforcement.

Summary

Establishing capitalization thresholds is a critical best practice that ensures consistent, efficient, and compliant asset management. By considering company size, industry norms, regulatory requirements, and administrative capacity, accountants can set thresholds that optimize financial reporting and operational workflows.

4.3 Documentation and Approval Processes for Asset Acquisition

Asset acquisition is a critical process in asset management that requires thorough documentation and a clear approval workflow to ensure accountability, compliance, and proper financial recording. For accountants, understanding and implementing best practices in documentation and approval helps maintain transparency and control over company resources.

Importance of Documentation and Approval

- Ensures asset purchases align with budget and strategic goals.

- Provides audit trail for internal and external reviews.

- Prevents unauthorized or unnecessary acquisitions.

- Facilitates accurate capitalization and financial reporting.

Key Components of Documentation

-

Purchase Request Form

- Initiated by the department needing the asset.

- Details asset description, quantity, estimated cost, and justification.

-

Vendor Quotations and Selection

- Multiple quotes to ensure competitive pricing.

- Documentation of vendor evaluation and selection criteria.

-

Purchase Order (PO)

- Official document authorizing the purchase.

- Includes terms, delivery dates, and payment conditions.

-

Receiving Report

- Confirms delivery and condition of the asset.

- Signed by the receiving department.

-

Invoice and Payment Records

- Invoice matched against PO and receiving report for payment approval.

-

Asset Registration Form

- Captures asset details for the asset register (serial numbers, location, custodian).

Approval Workflow Best Practices

- Multi-level Approval: Depending on asset value, approvals may be required from department heads, finance managers, and senior executives.

- Segregation of Duties: Different individuals handle request initiation, approval, purchasing, and receiving to reduce fraud risk.

- Digital Approval Systems: Use of electronic workflows to track approvals and reduce processing time.

Mind Map: Asset Acquisition Documentation and Approval Process

Example Workflow: From Purchase Request to Capitalization

Scenario: An accounting firm needs to acquire new laptops for its portfolio management team.

-

Purchase Request: The IT department submits a purchase request form detailing 10 laptops, specifications, and justification citing outdated equipment impacting productivity.

-

Vendor Quotes: Procurement obtains three vendor quotes. Vendor A offers the best price and warranty.

-

Approval: The department head reviews and approves the request. The finance manager confirms budget availability and approves.

-

Purchase Order: A PO is issued to Vendor A with agreed terms.

-

Receiving: Upon delivery, the IT department verifies the laptops against the PO and creates a receiving report.

-

Invoice & Payment: The finance team matches the invoice with the PO and receiving report, then processes payment.

-

Asset Registration: The laptops are tagged and entered into the asset register with details including serial numbers, purchase date, and assigned users.

-

Capitalization: The accountant applies the firm’s capitalization policy and records the laptops as fixed assets in the financial system.

Mind Map: Example Laptop Acquisition Workflow

Tips for Accountants

- Maintain a centralized digital repository for all asset acquisition documents.

- Regularly review approval thresholds and update workflows accordingly.

- Train staff on the importance of each documentation step to avoid delays.

- Use checklists to ensure no documentation step is missed.

By following structured documentation and approval processes, accountants can ensure asset acquisitions are transparent, compliant, and efficiently integrated into financial records, supporting sound asset management practices.

4.4 Example Workflow: From Purchase Request to Capitalization

Managing asset acquisition efficiently is critical for accountants to ensure accurate capitalization and compliance with accounting standards. Below is a detailed example workflow illustrating the process from the initial purchase request to the capitalization of the asset.

Step 1: Purchase Request Initiation

- Trigger: Department identifies the need for a new asset (e.g., new office laptops).

- Action: Submit a purchase request form including asset description, estimated cost, justification, and preferred vendor.

Example:

The IT department submits a purchase request for 10 laptops estimated at $1,200 each, citing the need to replace outdated equipment to improve productivity.

Step 2: Review and Approval

- Trigger: Purchase request is received by the finance or asset management team.

- Action: Review request for budget availability, necessity, and compliance with capitalization policy.

- Decision Points: Approve, reject, or request more information.

Example:

The finance team verifies the budget and confirms the laptops meet the capitalization threshold of $1,000 per unit. The request is approved.

Step 3: Purchase Order and Procurement

- Trigger: Approved purchase request.

- Action: Generate purchase order (PO) and send to vendor.

- Follow-up: Track order delivery and verify receipt.

Example:

A PO is created for 10 laptops and sent to the preferred vendor. Upon delivery, the receiving department verifies the quantity and condition.

Step 4: Asset Receipt and Inspection

- Trigger: Delivery of asset.

- Action: Inspect asset for quality and conformity to order.

- Documentation: Record serial numbers, condition, and receipt date.

Example:

The receiving team confirms all 10 laptops are delivered, serial numbers are recorded, and no damages are found.

Step 5: Asset Tagging and Registration

- Trigger: Asset inspection complete.

- Action: Assign asset tags and enter details into the asset register.

Example:

Each laptop is tagged with a unique barcode and entered into the asset register with purchase date and cost.

Step 6: Capitalization and Accounting Entry

- Trigger: Asset registered.

- Action: Capitalize asset according to accounting policies.

- Accounting Entries: Debit Asset Account, Credit Accounts Payable/Cash.

Example:

The total cost of $12,000 (10 laptops x $1,200) is capitalized. Straight-line depreciation over 3 years is selected. Journal entry:

- Debit: Office Equipment $12,000

- Credit: Accounts Payable $12,000

Step 7: Post-Capitalization Monitoring

- Trigger: Asset is capitalized.

- Action: Monitor asset for depreciation, maintenance, and eventual disposal.

Example:

Accountants schedule monthly depreciation entries and coordinate with IT for maintenance updates.

Summary Mind Map of Entire Workflow

This workflow ensures that asset acquisitions are properly documented, approved, and recorded, enabling accountants to maintain accurate financial records and comply with regulatory requirements. Integrating these steps into your asset management process improves transparency, accountability, and financial control.

4.5 Managing Leased Assets and Their Accounting Implications

Leased assets play a significant role in many organizations’ asset portfolios, especially when companies prefer operational flexibility or want to avoid large upfront capital expenditures. For accountants, understanding how to manage leased assets and their accounting treatment is critical to ensure compliance with accounting standards and accurate financial reporting.

Understanding Lease Types

Leases are generally classified into two main types under accounting standards such as IFRS 16 and ASC 842:

- Finance Lease (Capital Lease): Transfers substantially all risks and rewards of ownership to the lessee.

- Operating Lease: Does not transfer substantially all risks and rewards; lessee uses the asset without ownership.

Mind Map: Lease Classification

Accounting Treatment for Leased Assets

Finance Lease:

- Recognize Right-of-Use (ROU) Asset and Lease Liability on the balance sheet.

- Depreciate the ROU asset over the useful life or lease term.

- Interest expense on lease liability recognized separately.

Operating Lease:

- Lease payments are recognized as an expense on a straight-line basis over the lease term.

- No asset or liability recognized on the balance sheet (under previous standards; under IFRS 16 and ASC 842, most leases are recognized on balance sheet).

Mind Map: Accounting Treatment

Practical Example: Accounting for a Finance Lease

Scenario: A company leases machinery for 5 years. The lease payments are $20,000 annually, paid at year-end. The present value of lease payments is $85,000. The useful life of the machinery is 7 years.

Accounting Steps:

-

Initial Recognition:

- Debit Right-of-Use Asset: $85,000

- Credit Lease Liability: $85,000

-

Depreciation:

- Depreciate ROU asset over 5 years (lease term): $85,000 / 5 = $17,000 per year

-

Lease Payment:

- Each year, record interest expense on lease liability (using effective interest method)

- Reduce lease liability by the principal portion of the payment

-

Journal Entry Example (Year 1):

- Debit Interest Expense (e.g., $6,800)

- Debit Lease Liability (principal portion, e.g., $13,200)

- Credit Cash $20,000

-

Depreciation Entry:

- Debit Depreciation Expense $17,000

- Credit Accumulated Depreciation $17,000

Managing Lease Documentation and Controls

Maintaining accurate lease documentation is essential for compliance and audit readiness. Best practices include:

- Keeping signed lease agreements centralized and accessible.

- Tracking lease terms, renewal options, and payment schedules.

- Regularly reviewing lease classification and reassessing if terms change.

Mind Map: Lease Management Best Practices

Example: Lease Reassessment Due to Contract Modification

Scenario: A company initially classified a lease as an operating lease with a 3-year term. After 1 year, the lease term is extended by 2 years.

Accounting Implication:

- Reassess lease classification considering the extended term.

- Adjust ROU asset and lease liability to reflect new lease payments and term.

- Recognize any gain or loss if applicable.

Tax Implications of Leased Assets

- Lease payments under operating leases are generally deductible as expenses.

- Finance leases may allow depreciation deductions on the ROU asset.

- Tax treatment varies by jurisdiction; accountants must coordinate with tax professionals.

Summary

Managing leased assets requires a clear understanding of lease classification, accounting treatment, and ongoing management. Accountants should leverage technology to track leases, maintain documentation, and ensure compliance with evolving standards.

Additional Resources

- IFRS 16 Leases Standard

- ASC 842 Leases Guidance

- Lease Accounting Software Tools

By mastering leased asset management, accountants can provide accurate financial insights and support strategic decision-making.

5. Asset Maintenance and Optimization Strategies

5.1 Importance of Maintenance in Asset Longevity and Valuation

Maintenance plays a pivotal role in preserving the value and extending the useful life of assets. For accountants and portfolio managers, understanding how maintenance impacts asset longevity and valuation is crucial for accurate financial reporting, budgeting, and strategic decision-making.

Why Maintenance Matters

- Preserves Asset Functionality: Regular maintenance ensures assets operate efficiently, reducing the risk of unexpected breakdowns.

- Extends Useful Life: Proper upkeep can delay asset obsolescence, spreading costs over a longer period.

- Maintains Asset Value: Well-maintained assets retain higher market and book values.

- Reduces Repair Costs: Preventive maintenance is typically less costly than major repairs or replacements.

- Compliance and Safety: Maintenance ensures assets meet regulatory and safety standards, avoiding penalties.

Mind Map: Importance of Maintenance

Impact on Asset Valuation

Accountants must consider how maintenance affects asset valuation on financial statements:

- Book Value: Regular maintenance can justify the carrying amount by preventing impairment.

- Depreciation: Maintenance costs are generally expensed, but capital improvements can increase asset value and affect depreciation schedules.

- Impairment Testing: Poor maintenance may trigger impairment losses due to reduced asset utility.

Example: Maintenance Impact on a Manufacturing Machine

A manufacturing firm owns a machine valued at $500,000 with an expected useful life of 10 years. Without maintenance, the machine may fail after 6 years, requiring replacement.

- Scenario A (No Maintenance): Machine fails early, resulting in a $500,000 write-off and unplanned capital expenditure.

- Scenario B (Regular Maintenance): Scheduled maintenance costing $10,000/year extends machine life to 10 years, preserving value and spreading depreciation.

Accounting Implication: In Scenario B, the firm avoids impairment losses and benefits from predictable depreciation expenses, improving financial stability.

Mind Map: Maintenance Impact on Asset Valuation

Best Practices for Maintenance Management

- Develop a Maintenance Schedule: Plan preventive maintenance based on manufacturer recommendations and usage.

- Track Maintenance Costs: Record all maintenance expenses to analyze cost-effectiveness.

- Integrate with Asset Register: Link maintenance records to asset details for comprehensive tracking.

- Use Technology: Employ asset management software to automate reminders and reporting.

- Review and Adjust: Periodically assess maintenance effectiveness and adjust schedules accordingly.

Example: Maintenance Cost Tracking

An accounting team implements a spreadsheet to track maintenance expenses for office equipment:

| Asset | Maintenance Date | Cost | Description |

|---|---|---|---|

| Laptop #123 | 2024-03-15 | $150 | Battery replacement |

| Printer #45 | 2024-04-10 | $75 | Ink cartridge refill |

| HVAC System | 2024-05-01 | $500 | Annual servicing |

This tracking helps the team budget accurately and supports asset valuation discussions.

Summary

Maintenance is not just a technical necessity but a financial imperative. For accountants and portfolio managers, incorporating maintenance considerations into asset management practices ensures assets retain their value, supports accurate financial reporting, and optimizes operational costs.

By adopting structured maintenance programs and integrating them with accounting processes, organizations can maximize asset longevity and enhance overall financial health.

5.2 Integrating Maintenance Schedules with Accounting Records

Effective asset management goes beyond just acquisition and depreciation; it requires ongoing maintenance to preserve asset value and ensure operational efficiency. For accountants, integrating maintenance schedules with accounting records is critical to accurately track costs, forecast expenses, and comply with financial reporting standards.

Why Integrate Maintenance Schedules with Accounting Records?

- Accurate Cost Allocation: Maintenance costs can be capitalized or expensed depending on the nature of the work. Integration helps in proper classification.

- Improved Budgeting & Forecasting: Knowing when maintenance is due allows better cash flow management.

- Enhanced Asset Valuation: Regular maintenance can extend asset life, affecting depreciation schedules.

- Audit Trail & Compliance: Detailed records support audits and regulatory compliance.

Key Components of Integration

Step-by-Step Process for Integration

-

Define Maintenance Types and Their Accounting Treatment

- Preventive maintenance is usually expensed.

- Major repairs or upgrades may be capitalized.

-

Implement a Maintenance Scheduling System

- Use CMMS or calendar-based tools to schedule and record maintenance activities.

-

Link Maintenance Records to Asset Ledger

- Each maintenance event should reference the specific asset ID.

-

Record Costs in Accounting Software

- Maintenance expenses are coded correctly (expense vs capital).

-

Adjust Depreciation if Necessary

- Capitalized maintenance may require recalculating depreciation.

-

Generate Reports for Review

- Regularly review maintenance costs and asset performance.

Example: Integrating Maintenance for Office Equipment

Scenario: A mid-sized accounting firm manages a fleet of printers and computers.

- Maintenance Schedule: Preventive maintenance every 6 months.

- Accounting Treatment: Routine maintenance expensed; major repairs capitalized.

Process:

- The IT department logs maintenance tasks in a CMMS.

- Each task is linked to an asset ID (e.g., Printer #23).

- Maintenance costs are automatically pushed to the accounting system.

- Routine maintenance costs appear as expenses in the Profit & Loss statement.

- A major repair costing $5,000 is capitalized, increasing the asset’s book value.

- Depreciation schedules are updated to reflect the capitalized cost.

Result: The firm has clear visibility on maintenance costs, asset conditions, and accurate financial reporting.

Mind Map: Example Workflow for Maintenance-Accounting Integration

Practical Tips for Accountants

- Collaborate closely with maintenance teams to understand the nature of work.

- Establish clear policies on what qualifies as capital expenditure.

- Use integrated software solutions to minimize manual data entry errors.

- Regularly reconcile maintenance records with accounting entries.

- Train staff on the importance of accurate and timely data capture.

By integrating maintenance schedules with accounting records, accountants can provide more accurate financial insights, support asset longevity, and contribute to better organizational decision-making.

5.3 Cost-Benefit Analysis of Preventive vs Corrective Maintenance