Financial Risk Modeling for Accountants

1. Introduction to Financial Risk Modeling

1.1 Understanding Financial Risk: Definitions and Types

Financial risk refers to the possibility of losing money or facing financial uncertainty due to various factors affecting an organization’s financial health. For accountants, understanding financial risk is crucial as it directly impacts financial reporting, decision-making, and compliance.

What is Financial Risk?

Financial risk is the potential for financial loss or adverse financial outcomes resulting from internal or external factors. It can affect cash flows, profitability, asset values, and overall financial stability.

Types of Financial Risk

Financial risk can be broadly categorized into several types, each with distinct characteristics and implications:

Financial Risk Types Mind Map

Detailed Explanation of Key Risk Types

-

Market Risk: The risk of losses due to changes in market prices or rates.

- Example: An investment portfolio loses value because of a sudden drop in stock prices.

-

Credit Risk: The risk that a borrower or counterparty will fail to meet their financial obligations.

- Example: A corporate client defaults on a loan repayment.

-

Liquidity Risk: The risk that an entity cannot meet its short-term financial obligations due to the inability to convert assets into cash quickly.

- Example: A company cannot sell inventory fast enough to cover immediate expenses.

-

Operational Risk: Risks arising from failed internal processes, people, systems, or external events.

- Example: An accounting error leads to misstated financial statements.

-

Legal and Regulatory Risk: Risk of financial loss due to non-compliance with laws or regulations.

- Example: Penalties imposed for late tax filings.

-

Reputational Risk: Risk of loss resulting from damage to a firm’s reputation.

- Example: Negative publicity from a financial scandal reduces investor confidence.

Mind Map: Examples of Financial Risk in Accounting Context

Financial Risk Examples Mind Map

Simple Example: Understanding Credit Risk

Imagine an accountant managing accounts receivable for a mid-sized company. One client, a retail business, has been late on payments several times. The accountant assesses the credit risk by reviewing the client’s payment history, financial statements, and market conditions.

- If the client’s financial health deteriorates, the risk of default increases.

- The accountant might recommend setting a credit limit or requiring upfront payments to mitigate this risk.

This example illustrates how recognizing and quantifying credit risk helps accountants make informed decisions to protect the company’s financial interests.

Summary

Understanding financial risk and its types enables accountants to identify potential threats to financial stability and apply appropriate risk management strategies. Through clear definitions, categorized types, and practical examples, accountants can better integrate risk considerations into their daily work and financial reporting.

1.2 The Role of Accountants in Risk Modeling

Financial risk modeling is a critical process that helps organizations identify, assess, and manage potential financial risks. Accountants play a pivotal role in this process due to their deep understanding of financial data, regulatory requirements, and internal controls. This section explores the multifaceted role of accountants in risk modeling, supported by mind maps and practical examples.

Key Responsibilities of Accountants in Risk Modeling

Accountants contribute at various stages of risk modeling, from data preparation to interpretation of results and reporting. Their responsibilities include:

- Data Integrity and Validation: Ensuring the accuracy and completeness of financial data used in models.

- Regulatory Compliance: Aligning risk models with accounting standards and regulatory frameworks.

- Financial Analysis: Applying financial expertise to interpret model outputs and assess risk implications.

- Internal Controls: Designing controls to mitigate identified risks.

- Communication: Reporting risk findings clearly to stakeholders.

Mind Map: Roles and Responsibilities of Accountants in Risk Modeling

Example 1: Ensuring Data Integrity for Credit Risk Modeling

An accountant working in a bank is tasked with preparing financial data for a credit risk model. They identify discrepancies in the loan payment history data due to inconsistent entries. By implementing a rigorous data validation process—checking for missing values, duplicates, and logical inconsistencies—they ensure the model inputs are reliable. This reduces the risk of inaccurate credit risk predictions.

Mind Map: Data Integrity Process by Accountants

Example 2: Aligning Risk Models with Regulatory Standards

In an investment firm, accountants review the risk model outputs to ensure compliance with IFRS 9 requirements for expected credit loss calculations. They verify that the model assumptions and parameters align with regulatory guidelines and that the disclosures in financial statements accurately reflect the modeled risks.

Mind Map: Regulatory Compliance Role

Example 3: Communicating Risk Findings Effectively

After completing a market risk assessment, an accountant prepares a report summarizing the Value at Risk (VaR) results for senior management. Using clear visuals and straightforward language, they highlight key risk exposures and recommend mitigation strategies, facilitating informed decision-making.

Mind Map: Communication Workflow

Summary

Accountants are integral to financial risk modeling through their expertise in financial data management, regulatory compliance, analytical skills, internal control design, and communication. Their involvement ensures that risk models are built on accurate data, comply with standards, and produce actionable insights that support sound financial decision-making.

1.3 Overview of Risk Modeling Techniques

Financial risk modeling is a critical process that helps accountants and risk analysts quantify, analyze, and manage various types of financial risks. Understanding the different techniques available enables professionals to select the most appropriate model based on the risk type, data availability, and business context.

Key Risk Modeling Techniques

Below is a mind map illustrating the primary categories of risk modeling techniques:

Statistical Models

Description: These models use historical data and statistical techniques to estimate risk. They are foundational in financial risk modeling.

-

Regression Analysis: Helps in understanding relationships between variables. For example, predicting loan default probability based on financial ratios.

-

Time Series Analysis: Used for modeling and forecasting financial variables such as stock prices or interest rates.

-

Probability Distributions: Modeling risk factors using distributions like Normal, Lognormal, or Poisson to estimate likelihoods of different outcomes.

Example:

An accountant uses linear regression to estimate how changes in a company’s debt-to-equity ratio affect its probability of default. By analyzing past data, the accountant builds a model that predicts default risk based on this financial ratio.

Simulation Models

Description: These models generate a range of possible outcomes by simulating random variables, useful for capturing uncertainty.

-

Monte Carlo Simulation: Runs thousands of simulations to estimate the distribution of possible outcomes.

-

Bootstrapping: Resamples data to estimate the sampling distribution of a statistic.

Example:

To assess the operational risk of cash flow variability, an accountant runs a Monte Carlo simulation using historical cash flow data and assumptions about future volatility, generating a probability distribution of potential cash shortfalls.

Credit Risk Models

Description: Specifically designed to evaluate the risk of borrower default.

-

Credit Scoring Models: Use logistic regression or machine learning to score borrowers.

-

Structural Models: Based on the firm’s asset value dynamics (e.g., Merton model).

-

Reduced-Form Models: Focus on default intensity and hazard rates.

Example:

An accountant develops a credit scoring model using logistic regression, incorporating financial ratios like current ratio, profitability, and past payment history to predict the likelihood of default for corporate clients.

Market Risk Models

Description: Focus on risks arising from market movements.

-

Value at Risk (VaR): Estimates the maximum expected loss over a given time frame at a certain confidence level.

-

Conditional VaR (CVaR): Measures expected loss exceeding the VaR threshold.

-

Stress Testing: Evaluates model behavior under extreme but plausible scenarios.

Example:

An accountant calculates the 1-day 95% VaR for an investment portfolio using historical simulation, analyzing past price movements to estimate potential losses.

Liquidity Risk Models

Description: Assess the risk that a firm cannot meet its short-term financial obligations.

-

Cash Flow Forecasting: Projects inflows and outflows to identify liquidity gaps.

-

Liquidity Coverage Ratio Models: Measure the adequacy of liquid assets to cover short-term liabilities.

Example:

Using cash flow forecasting, an accountant identifies periods where the company may face liquidity shortages and recommends maintaining higher cash reserves during those times.

Operational Risk Models

Description: Address risks from internal processes, people, and systems.

-

Loss Distribution Approach: Uses historical loss data to model frequency and severity.

-

Scenario Analysis: Experts assess potential operational risk events and their impact.

Example:

An accountant collects data on past fraud incidents and uses the loss distribution approach to estimate potential future losses, helping the company set aside adequate reserves.

Emerging Machine Learning Models

Description: Advanced techniques that can capture complex patterns and interactions.

-

Decision Trees: Classify risk based on hierarchical decision rules.

-

Neural Networks: Model nonlinear relationships.

-

Support Vector Machines: Classify data points with maximum margin.

Example:

An accountant uses a decision tree model to classify loan applications into risk categories based on multiple financial indicators, improving the accuracy of credit risk assessment.

Summary Mind Map: Linking Techniques to Risk Types

Final Notes

For accountants, selecting the right risk modeling technique depends on the specific risk being analyzed, data availability, and the desired level of model complexity. Combining multiple techniques often yields more robust risk assessments. Throughout this blog, we will explore these techniques with practical examples and best practices tailored for accounting professionals.

1.4 Importance of Integrating Best Practices in Risk Models

Financial risk modeling is a critical function for accountants, as it directly influences decision-making, compliance, and the overall financial health of an organization. Integrating best practices into risk models ensures accuracy, reliability, and transparency, which are essential for effective risk management.

Why Integrate Best Practices?

- Accuracy and Reliability: Best practices help reduce errors and biases in data handling and model construction.

- Regulatory Compliance: Many financial regulations require documented and validated risk models.

- Transparency and Communication: Clear models facilitate better communication with stakeholders and auditors.

- Adaptability: Best practices enable models to be flexible and scalable as business needs evolve.

- Risk Mitigation: Improved models lead to better identification and mitigation of financial risks.

Mind Map: Benefits of Integrating Best Practices in Risk Models

Core Best Practices to Integrate

-

Comprehensive Data Management

- Collecting high-quality, relevant data

- Regular data cleaning and validation

- Example: An accountant ensures that historical financial data is cross-verified with external credit ratings before modeling credit risk.

-

Clear Definition of Risk Metrics and Assumptions

- Explicitly stating assumptions used in models

- Defining risk metrics such as VaR, Expected Loss, etc.

- Example: When modeling market risk, an accountant documents the confidence level and time horizon used in VaR calculations.

-

Model Validation and Backtesting

- Regularly testing model predictions against actual outcomes

- Adjusting models based on validation results

- Example: After building a liquidity risk model, the accountant compares predicted cash flow shortages with actual occurrences over the last quarter.

-

Documentation and Transparency

- Keeping detailed records of model design, data sources, and assumptions

- Facilitating audits and stakeholder reviews

- Example: An accountant prepares a comprehensive report explaining the credit risk model’s methodology for the internal audit team.

-

Scenario Analysis and Stress Testing

- Testing models under extreme but plausible conditions

- Understanding model behavior under stress

- Example: Running a stress test on an investment portfolio to simulate the impact of a sudden market downturn.

Mind Map: Core Best Practices in Financial Risk Modeling

Practical Example: Integrating Best Practices in a Credit Risk Model

Scenario: An accountant is tasked with building a credit risk model to assess the likelihood of default for small business clients.

Step 1: Data Collection and Validation

- Collect financial statements, payment history, and external credit scores.

- Validate data by cross-checking with bank records and credit bureaus.

Step 2: Define Risk Metrics and Assumptions

- Use Probability of Default (PD) as the primary metric.

- Assume a one-year time horizon for default prediction.

Step 3: Model Development and Documentation

- Apply logistic regression to predict default probability.

- Document model variables, assumptions, and data sources.

Step 4: Validation and Backtesting

- Compare predicted defaults with actual defaults over the past year.

- Adjust model coefficients based on validation results.

Step 5: Scenario Analysis

- Test model under economic downturn conditions by adjusting macroeconomic variables.

Outcome: The accountant produces a robust, transparent credit risk model that meets regulatory standards and supports informed lending decisions.

Mind Map: Example Workflow for Best Practice Integration

Summary

Integrating best practices into financial risk models is not just a technical necessity but a strategic imperative for accountants. It enhances model credibility, supports compliance, and ultimately leads to better risk-informed decisions. By embedding these practices into everyday workflows, accountants can elevate their role as trusted advisors in financial risk management.

1.5 Simple Example: Assessing Credit Risk for a Small Business Loan

Assessing credit risk is a fundamental task for accountants involved in financial risk modeling. In this section, we will walk through a simple, easy-to-understand example of evaluating the credit risk associated with a small business loan application. This example will incorporate best practices and demonstrate how to use financial data effectively.

Step 1: Understand the Borrower’s Profile

Start by gathering essential information about the small business:

- Business type and industry

- Years in operation

- Loan amount requested

- Purpose of the loan

- Financial statements (balance sheet, income statement, cash flow)

Step 2: Key Financial Ratios for Credit Risk Assessment

Accountants use financial ratios to evaluate the borrower’s ability to repay the loan. Important ratios include:

- Debt-to-Equity Ratio (D/E): Measures leverage.

- Current Ratio: Measures liquidity.

- Interest Coverage Ratio: Ability to pay interest on debt.

- Net Profit Margin: Profitability indicator.

Step 3: Assigning Risk Scores Based on Ratios

Each ratio is compared against industry benchmarks or thresholds. Scores can be assigned as follows:

| Ratio | Threshold | Score (1-5) | Interpretation |

|---|---|---|---|

| Debt-to-Equity Ratio | < 1.5 | 5 | Low leverage |

| 1.5 - 3.0 | 3 | Moderate leverage | |

| > 3.0 | 1 | High leverage | |

| Current Ratio | > 1.5 | 5 | Strong liquidity |

| 1.0 - 1.5 | 3 | Adequate liquidity | |

| < 1.0 | 1 | Poor liquidity | |

| Interest Coverage | > 4 | 5 | Excellent coverage |

| 2 - 4 | 3 | Adequate coverage | |

| < 2 | 1 | Risk of default | |

| Net Profit Margin | > 10% | 5 | Highly profitable |

| 5% - 10% | 3 | Moderate profitability | |

| < 5% | 1 | Low profitability |

Step 4: Calculate an Overall Credit Risk Score

Sum the scores from each ratio and normalize to a scale of 0 to 100.

Example:

| Ratio | Score |

|---|---|

| Debt-to-Equity Ratio | 3 |

| Current Ratio | 5 |

| Interest Coverage | 3 |

| Net Profit Margin | 5 |

| Total | 16 |

Max possible score = 5 * 4 = 20

Normalized score = (16 / 20) * 100 = 80

Step 5: Decision Making Based on Score

- 80-100: Low credit risk – loan likely approved

- 50-79: Moderate risk – loan approved with conditions or higher interest

- <50: High risk – loan likely denied

Mind Map: Credit Risk Assessment Process

Example Walkthrough

Business: ABC Bakery

- Loan Amount: $100,000

- Years in Operation: 5

- Financial Ratios:

- Debt-to-Equity Ratio: 2.0 (Score: 3)

- Current Ratio: 1.8 (Score: 5)

- Interest Coverage Ratio: 3.5 (Score: 3)

- Net Profit Margin: 12% (Score: 5)

Total Score: 16/20 = 80%

Interpretation: ABC Bakery has a low credit risk and is a good candidate for loan approval.

Best Practices Highlighted

- Use multiple financial ratios to get a comprehensive view.

- Compare ratios against industry benchmarks.

- Normalize scores for easier interpretation.

- Combine quantitative scores with qualitative information (e.g., loan purpose).

- Document assumptions and thresholds clearly.

This simple example illustrates how accountants can apply financial risk modeling principles to assess credit risk effectively, using clear metrics and structured decision-making processes.

2. Data Collection and Preparation for Risk Models

2.1 Identifying Relevant Financial Data Sources

Financial risk modeling relies heavily on the quality and relevance of the data used. For accountants, understanding where to source accurate and comprehensive financial data is the first critical step in building robust risk models. This section explores the various types of financial data sources, how to evaluate their relevance, and practical examples to illustrate their use.

Why Identifying Relevant Data Sources Matters

- Accurate risk assessment depends on reliable data.

- Using irrelevant or poor-quality data can lead to misleading risk models.

- Accountants must balance data availability with data quality and relevance.

Categories of Financial Data Sources

Below is a mind map outlining the main categories of financial data sources relevant for risk modeling:

Internal Data Sources

1. Financial Statements:

These are the backbone of financial risk modeling for accountants. They provide historical and current snapshots of a company’s financial health.

- Example: Using balance sheet data to calculate debt-to-equity ratios for credit risk modeling.

2. Transaction Records:

Detailed records of sales, purchases, payments, and receipts help identify operational risks and cash flow volatility.

- Example: Analyzing payment delays in accounts receivable to assess liquidity risk.

3. Budget and Forecast Data:

Forward-looking data that can be used to model potential future risks.

- Example: Comparing forecasted revenues with actuals to identify variance risks.

4. Audit Reports:

Provide insights into internal controls and potential risk areas flagged by auditors.

- Example: Using audit findings to adjust operational risk parameters.

External Data Sources

1. Market Data:

Includes prices and rates that affect asset values and liabilities.

- Example: Using historical stock price volatility to model market risk exposure.

2. Credit Ratings:

Ratings from agencies like Moody’s or S&P provide an external assessment of creditworthiness.

- Example: Incorporating credit rating changes into credit risk models.

3. Macroeconomic Indicators:

Economic conditions influence financial risks broadly.

- Example: Using inflation rates to adjust cash flow forecasts.

4. Industry Reports:

Provide sector-specific insights and benchmarks.

- Example: Comparing a company’s financial ratios to industry averages to identify risk outliers.

5. Regulatory Filings:

Public disclosures required by regulators can reveal risk exposures.

- Example: Using SEC filings to gather data on contingent liabilities.

Alternative Data Sources

Emerging data types that can supplement traditional sources.

-

Example: Using social media sentiment analysis to anticipate reputational risk.

-

Example: Satellite data to monitor supply chain disruptions.

Practical Example: Identifying Data Sources for Credit Risk Modeling

| Step | Data Source Type | Specific Data | Purpose |

|---|---|---|---|

| 1 | Internal | Financial Statements (Balance Sheet, Income Statement) | Calculate financial ratios like debt coverage and profitability |

| 2 | External | Credit Ratings from Moody’s | Assess borrower creditworthiness |

| 3 | External | Macroeconomic Indicators (GDP growth, unemployment) | Adjust risk parameters based on economic environment |

| 4 | Internal | Transaction Records (Payment history) | Identify payment behavior and default risk |

Summary

Identifying relevant financial data sources is foundational for effective financial risk modeling. Accountants should combine internal financial data with external market and economic data, and where appropriate, alternative data sources to build comprehensive and accurate risk models.

By systematically mapping out and evaluating these data sources, accountants can ensure their risk assessments are grounded in robust and relevant information.

2.2 Data Cleaning and Validation Best Practices

Data cleaning and validation are foundational steps in financial risk modeling. Accurate, consistent, and reliable data ensures that the risk models produce meaningful and actionable insights. For accountants, who often work with large volumes of financial data, mastering these best practices is critical.

Why Data Cleaning and Validation Matter

- Garbage in, garbage out: Poor data quality leads to misleading risk assessments.

- Regulatory compliance: Accurate data supports audit trails and regulatory reporting.

- Model robustness: Clean data reduces noise and improves model stability.

Key Steps in Data Cleaning

Best Practices for Data Cleaning

Handling Missing Data

- Identify: Use summary statistics or visualization to locate missing values.

- Impute: Depending on context, fill missing values with mean, median, mode, or predictive methods.

- Remove: If missing data is excessive or random, consider removing affected records.

Example: A dataset of loan applications has missing values in the “Annual Income” field. Since income is critical for credit risk, imputing missing values with the median income of applicants in the same job category preserves data integrity without skewing results.

Detecting and Treating Outliers

- Detect: Use boxplots, z-scores, or interquartile range (IQR) methods.

- Analyze: Determine if outliers are errors or valid extreme cases.

- Treat: Correct errors, cap values, or exclude outliers based on business rules.

Example: An operational risk dataset shows a transaction loss of $10 million, far above typical values. Investigation reveals a data entry error (extra zero). Correcting this to $1 million aligns the data with reality and improves model accuracy.

Removing Duplicates

- Identify duplicate records using unique identifiers (e.g., invoice numbers, client IDs).

- Remove duplicates to avoid double counting risks.

Example: Two entries for the same client loan appear in the dataset due to system sync issues. Removing the duplicate prevents overstating credit exposure.

Ensuring Consistency

- Standardize date formats, currency units, and categorical labels.

- Cross-check related fields for logical consistency (e.g., loan start date should precede end date).

Example: Dates in a dataset appear as MM/DD/YYYY and DD-MM-YYYY. Standardizing all dates to ISO format (YYYY-MM-DD) avoids parsing errors during modeling.

Validating Accuracy

- Cross-verify data against original sources or external references.

- Use reconciliation reports to identify discrepancies.

Example: Accountants compare reported revenue figures with bank statements to confirm accuracy before feeding data into market risk models.

Validation Techniques

Best Practices for Data Validation

- Range Checks: Ensure numerical values fall within expected limits.

- Format Checks: Confirm data types and formats match requirements.

- Referential Integrity: Validate relationships between datasets.

- Duplicate Checks: Enforce uniqueness where applicable.

- Business Rules Validation: Apply domain-specific rules (e.g., interest rates cannot be negative).

Example: In credit risk modeling, validate that the “Credit Score” field is between 300 and 850. Any value outside this range triggers a data review.

Integrated Example: Cleaning and Validating a Loan Dataset

- Initial Inspection: Identify missing “Employment Status” and outliers in “Loan Amount”.

- Cleaning: Impute missing employment statuses using mode of similar applicants; cap loan amounts at the 99th percentile.

- Validation: Check that “Loan Start Date” precedes “Loan End Date”; confirm all loan IDs are unique.

- Outcome: A clean, validated dataset ready for credit risk modeling.

Summary

Effective data cleaning and validation involve systematic identification and treatment of missing data, outliers, duplicates, and inconsistencies. For accountants, applying these best practices with clear examples ensures the reliability of financial risk models and supports sound decision-making.

2.3 Handling Missing and Outlier Data with Practical Examples

Handling missing and outlier data is a critical step in financial risk modeling, especially for accountants who rely on accurate and clean data to make informed decisions. Poor handling of such data can lead to biased models, inaccurate risk assessments, and ultimately flawed financial strategies.

Understanding Missing Data

Missing data occurs when no value is stored for a variable in an observation. In financial datasets, missing data can arise due to errors in data entry, system failures, or unavailability of information.

Types of Missing Data:

- MCAR (Missing Completely at Random): The missingness is unrelated to any data.

- MAR (Missing at Random): The missingness is related to observed data.

- MNAR (Missing Not at Random): The missingness is related to unobserved data.

Understanding Outliers

Outliers are data points that differ significantly from other observations. They can be due to measurement errors, data entry mistakes, or genuine but rare events.

Mind Map: Handling Missing Data

Mind Map: Handling Outliers

Practical Example 1: Handling Missing Data in Financial Statements

Scenario: An accountant is analyzing quarterly financial statements of multiple companies to assess credit risk. Some companies have missing values in ‘Accounts Receivable’ and ‘Inventory’ columns.

Step 1: Identify Missing Data

- Use a missing data matrix or heatmap to visualize missingness.

Step 2: Determine Missingness Type

- Check if missingness correlates with company size or industry.

Step 3: Choose Imputation Method

- For ‘Accounts Receivable’ (continuous variable), use median imputation to reduce skew impact.

- For ‘Inventory’, use regression imputation based on related variables like ‘Cost of Goods Sold’.

Step 4: Validate Imputation

- Compare distributions before and after imputation.

Code Snippet (Python/Pandas):

import pandas as pd

from sklearn.linear_model import LinearRegression

# Median imputation for Accounts Receivable

median_ar = df['Accounts_Receivable'].median()

df['Accounts_Receivable'].fillna(median_ar, inplace=True)

# Regression imputation for Inventory

train = df[df['Inventory'].notnull()]

test = df[df['Inventory'].isnull()]

X_train = train[['Cost_of_Goods_Sold']]

y_train = train['Inventory']

model = LinearRegression()

model.fit(X_train, y_train)

X_test = test[['Cost_of_Goods_Sold']]

df.loc[df['Inventory'].isnull(), 'Inventory'] = model.predict(X_test)

Practical Example 2: Detecting and Treating Outliers in Risk Ratios

Scenario: A risk analyst is reviewing the Debt-to-Equity ratios of clients to identify potential credit risks. Some values appear unusually high.

Step 1: Visualize Data

- Use boxplots to detect outliers.

Step 2: Quantify Outliers

- Calculate IQR and define outliers as values outside 1.5 * IQR.

Step 3: Investigate Outliers

- Check if high ratios are due to data entry errors or genuine financial distress.

Step 4: Treat Outliers

- For confirmed errors, correct or remove.

- For genuine values, consider winsorizing to reduce impact on model.

Code Snippet (Python/Pandas):

Q1 = df['Debt_to_Equity'].quantile(0.25)

Q3 = df['Debt_to_Equity'].quantile(0.75)

IQR = Q3 - Q1

lower_bound = Q1 - 1.5 * IQR

upper_bound = Q3 + 1.5 * IQR

# Identify outliers

outliers = df[(df['Debt_to_Equity'] < lower_bound) | (df['Debt_to_Equity'] > upper_bound)]

# Winsorize outliers

df['Debt_to_Equity'] = df['Debt_to_Equity'].clip(lower=lower_bound, upper=upper_bound)

Summary of Best Practices

- Always understand the nature of missingness and outliers before deciding on treatment.

- Use visualization tools to detect issues early.

- Prefer imputation methods that preserve data distribution and relationships.

- Document all decisions and rationale for transparency.

- Validate the impact of handling missing and outlier data on model performance.

By carefully handling missing and outlier data using these best practices and examples, accountants and risk analysts can improve the reliability and accuracy of their financial risk models.

2.4 Data Normalization and Transformation Techniques

Data normalization and transformation are critical steps in preparing financial data for risk modeling. These techniques help ensure that data is on a comparable scale, reduce bias, and improve the performance and interpretability of risk models. In this section, we will explore the most common normalization and transformation methods, their applications in financial risk modeling, and practical examples tailored for accountants.

Why Normalize and Transform Data?

- Financial data often comes from diverse sources with different units and scales.

- Normalization ensures variables contribute equally to the analysis.

- Transformation can help meet model assumptions (e.g., normality).

- Improves convergence and stability of quantitative models.

Common Data Normalization Techniques

Mind Map: Data Normalization Techniques

Example: Min-Max Scaling of Debt-to-Equity Ratio

Suppose you have the following debt-to-equity ratios for five companies:

| Company | Debt-to-Equity Ratio |

|---|---|

| A | 0.5 |

| B | 1.2 |

| C | 0.8 |

| D | 2.0 |

| E | 1.5 |

- Minimum = 0.5, Maximum = 2.0

- For Company B: (1.2 - 0.5) / (2.0 - 0.5) = 0.7 / 1.5 = 0.4667

This scaled value now fits between 0 and 1, making it easier to compare across metrics.

Common Data Transformation Techniques

Mind Map: Data Transformation Techniques

Example: Log Transformation of Revenue

Consider annual revenues (in millions) for five clients:

| Client | Revenue |

|---|---|

| 1 | 10 |

| 2 | 100 |

| 3 | 1000 |

| 4 | 5000 |

| 5 | 20000 |

- Raw data is heavily skewed.

- Applying log transformation:

- log(10) = 1

- log(100) = 2

- log(1000) = 3

- log(5000) ≈ 3.7

- log(20000) ≈ 4.3

This compresses the range and reduces skewness, making it easier for models to interpret.

When to Use Which Technique?

Mind Map: Choosing Normalization and Transformation

Practical Tips and Best Practices

- Always visualize data before and after transformation (histograms, boxplots).

- Avoid applying log transformation to zero or negative values; consider shifting data if necessary.

- Document all transformations for audit and reproducibility.

- Combine normalization with feature engineering for improved risk model performance.

Integrated Example: Preparing Financial Ratios for Credit Risk Model

- Collect financial ratios such as Current Ratio, Debt-to-Equity, and Return on Assets.

- Use Min-Max scaling for ratios bounded between 0 and an upper limit (e.g., Current Ratio).

- Apply Z-score standardization for ratios with no fixed upper bound (e.g., Return on Assets).

- For highly skewed metrics like Debt-to-Equity, apply log transformation after adding a small constant to avoid zero values.

- Validate the transformed data with summary statistics and visualizations.

By mastering these normalization and transformation techniques, accountants can significantly enhance the quality and reliability of financial risk models, leading to better risk assessment and decision-making.

2.5 Case Study: Preparing Historical Financial Statements for Market Risk Analysis

In this section, we will walk through a detailed case study that demonstrates how accountants can prepare historical financial statements effectively for market risk analysis. This process involves data collection, cleaning, normalization, and transformation to ensure the data is accurate and suitable for risk modeling.

Step 1: Understanding the Objective

The goal is to analyze the market risk exposure of a publicly traded company by using its historical financial statements. Market risk typically involves risks arising from fluctuations in market prices, interest rates, and foreign exchange rates.

Step 2: Collecting Historical Financial Statements

- Gather at least 5 years of quarterly financial statements (Income Statement, Balance Sheet, Cash Flow Statement).

- Source data from reliable platforms such as company filings (e.g., SEC EDGAR), financial databases (Bloomberg, Reuters), or internal accounting systems.

Step 3: Data Cleaning and Validation

- Check for missing data: Identify any missing quarters or incomplete reports.

- Validate consistency: Ensure that line items are consistent across periods (e.g., revenue categories, expense classifications).

- Remove duplicates: Eliminate any repeated entries.

Step 4: Data Normalization and Transformation

- Convert all figures to a consistent currency and unit (e.g., USD in thousands).

- Adjust for any restatements or accounting policy changes.

- Calculate relevant financial ratios that impact market risk, such as:

- Debt-to-Equity Ratio

- Current Ratio

- Interest Coverage Ratio

Step 5: Organizing Data for Market Risk Modeling

- Structure the data in a time-series format suitable for statistical analysis.

- Align financial data with corresponding market data (e.g., stock prices, interest rates).

Mind Map: Preparing Historical Financial Statements for Market Risk Analysis

Example: Cleaning and Normalizing Revenue Data

| Quarter | Reported Revenue (in USD) | Notes |

|---|---|---|

| Q1 2019 | 1,200,000 | Complete |

| Q2 2019 | 1,250,000 | Complete |

| Q3 2019 | Missing | Data not reported |

| Q4 2019 | 1,300,000 | Complete |

Approach:

- For Q3 2019, estimate revenue using linear interpolation:

- Q3 Revenue = (Q2 Revenue + Q4 Revenue) / 2 = (1,250,000 + 1,300,000) / 2 = 1,275,000

This maintains continuity and avoids gaps in the dataset.

Example: Calculating Debt-to-Equity Ratio Over Time

| Quarter | Total Debt (USD) | Shareholders’ Equity (USD) | Debt-to-Equity Ratio |

|---|---|---|---|

| Q1 2020 | 800,000 | 1,600,000 | 0.50 |

| Q2 2020 | 850,000 | 1,550,000 | 0.55 |

| Q3 2020 | 900,000 | 1,500,000 | 0.60 |

This ratio helps assess the company’s leverage and sensitivity to market interest rate changes.

Mind Map: Data Cleaning and Normalization Techniques

Step 6: Final Preparation for Market Risk Analysis

- Export the cleaned and normalized dataset into formats compatible with risk modeling tools (e.g., CSV, Excel).

- Document all assumptions and adjustments made during preparation.

- Collaborate with risk analysts to ensure the dataset meets model requirements.

Summary

Preparing historical financial statements for market risk analysis is a critical step that requires meticulous attention to data quality and consistency. By following best practices such as thorough cleaning, normalization, and proper organization, accountants can provide reliable inputs that enhance the accuracy of market risk models.

This case study illustrated practical methods and examples that accountants can apply in their daily work to support robust financial risk management.

3. Quantitative Techniques in Financial Risk Modeling

3.1 Statistical Methods for Risk Assessment

Financial risk assessment relies heavily on statistical methods to quantify, analyze, and predict potential losses or uncertainties. For accountants, understanding these methods is crucial to accurately model risks and support decision-making.

Key Statistical Methods in Risk Assessment

- Descriptive Statistics: Summarizing data characteristics

- Probability Distributions: Modeling uncertainties

- Hypothesis Testing: Validating assumptions

- Regression Analysis: Exploring relationships between variables

- Correlation Analysis: Measuring dependencies

- Time Series Analysis: Analyzing data over time

Mind Map: Overview of Statistical Methods for Risk Assessment

Descriptive Statistics

Descriptive statistics provide a summary of the financial data used in risk models.

- Mean (Average): Central tendency of data.

- Variance and Standard Deviation: Measure of data dispersion, essential for understanding volatility.

Example:

An accountant analyzing monthly returns of a portfolio calculates the mean return (5%) and standard deviation (2%). The standard deviation indicates the typical deviation from the mean, helping to understand risk.

Probability Distributions

Modeling the likelihood of different outcomes is fundamental.

- Normal Distribution: Assumes data clusters around a mean; widely used in finance.

- Binomial Distribution: Useful for modeling binary outcomes, e.g., default/no default.

- Poisson Distribution: Models the number of events in a fixed interval, e.g., number of fraud cases.

Example:

To estimate the probability of a client defaulting on a loan, an accountant might use a binomial distribution where each loan is either defaulted or not.

Hypothesis Testing

Used to validate assumptions about financial data.

- Formulate a null hypothesis (e.g., “The average loss is less than $10,000”).

- Use sample data to accept or reject the hypothesis.

Example:

An accountant tests whether a new risk mitigation strategy reduces average losses by comparing pre- and post-implementation loss data.

Regression Analysis

Explores relationships between dependent and independent variables.

- Linear Regression: Predicts continuous outcomes.

- Logistic Regression: Predicts binary outcomes (e.g., default or no default).

Example:

Using logistic regression, an accountant predicts the probability of loan default based on financial ratios such as debt-to-equity and current ratio.

Mind Map: Regression Analysis in Risk Modeling

Correlation Analysis

Measures the strength and direction of the relationship between two variables.

- Pearson Correlation: Measures linear relationships.

- Spearman Correlation: Measures monotonic relationships.

Example:

An accountant finds a strong positive correlation (0.85) between interest rate hikes and loan default rates, indicating rising rates increase risk.

Time Series Analysis

Analyzes data points collected or recorded at specific time intervals.

- Useful for forecasting future financial risks.

- Techniques include moving averages and autoregressive models.

Example:

An accountant uses a moving average to smooth out daily cash flow data to better understand liquidity risk trends.

Integrated Example: Assessing Credit Risk Using Statistical Methods

- Data Summary: Calculate mean and standard deviation of historical default rates.

- Distribution Fit: Confirm default rates follow a binomial distribution.

- Hypothesis Test: Test if recent default rates differ significantly from historical averages.

- Regression Model: Use logistic regression with financial ratios to predict default probability.

- Correlation Check: Analyze correlation between macroeconomic indicators and default rates.

- Time Series Forecast: Forecast future default rates using autoregressive models.

This integrated approach helps accountants build robust risk models supported by sound statistical methods.

Summary

Statistical methods form the backbone of financial risk assessment. Accountants equipped with these tools can better quantify, analyze, and communicate risks, ultimately supporting more informed financial decisions.

3.2 Introduction to Probability Distributions in Finance

Probability distributions are fundamental to financial risk modeling because they describe how likely different outcomes are in uncertain environments. Understanding these distributions helps accountants and risk analysts quantify risk, forecast potential losses, and make informed decisions.

What is a Probability Distribution?

A probability distribution is a mathematical function that provides the probabilities of occurrence of different possible outcomes in an experiment. In finance, these outcomes could be asset returns, credit defaults, or operational losses.

Why Are Probability Distributions Important in Finance?

- Risk Quantification: They help measure the likelihood of extreme losses or gains.

- Modeling Uncertainty: Financial markets are inherently uncertain; distributions capture this variability.

- Decision Making: They enable scenario analysis and stress testing.

Common Probability Distributions Used in Finance

Below is a mind map summarizing the key probability distributions frequently applied in financial risk modeling:

Example 1: Normal Distribution in Asset Returns

Scenario: An accountant is analyzing the daily returns of a stock portfolio.

- The returns are assumed to follow a normal distribution with a mean (μ) of 0.1% and a standard deviation (σ) of 2%.

- Using this distribution, the accountant can calculate the probability that the portfolio will lose more than 3% in a day.

Calculation:

- Calculate the Z-score: \( Z = \frac{-3\% - 0.1\%}{2\%} = \frac{-3.1\%}{2\%} = -1.55 \)

- Using standard normal tables, the probability of Z < -1.55 is approximately 6.0%.

Interpretation: There is a 6% chance the portfolio will lose more than 3% in a single day.

Example 2: Binomial Distribution for Credit Defaults

Scenario: A risk analyst wants to model the probability that exactly 2 out of 5 loans default within a year.

- Each loan has a default probability (p) of 10%.

- The number of defaults follows a binomial distribution: ( B(n=5, p=0.1) ).

Calculation:

-

Probability of exactly 2 defaults:

\[ P(X=2) = \binom{5}{2} (0.1)^2 (0.9)^3 = 10 \times 0.01 \times 0.729 = 0.0729 \]

Interpretation: There is a 7.29% chance that exactly 2 loans will default.

Visual Mind Map: Understanding Distribution Characteristics

Best Practices for Using Probability Distributions in Financial Risk Modeling

- Validate Distribution Assumptions: Always test if your data fits the assumed distribution using goodness-of-fit tests (e.g., Kolmogorov-Smirnov test).

- Use Heavy-Tailed Distributions for Financial Returns: Normal distribution often underestimates extreme losses; consider Student’s t or other fat-tailed distributions.

- Incorporate Empirical Data: When possible, use historical data to estimate distribution parameters.

- Combine Distributions for Complex Risks: For example, use a mixture of distributions to model multi-modal data.

Summary

Probability distributions provide the mathematical foundation for quantifying and managing financial risks. By understanding their properties and applying them appropriately, accountants and risk analysts can build more robust risk models that better capture the realities of financial markets.

Next Section Preview: In 3.3, we will explore how regression analysis leverages probability distributions to predict financial outcomes and enhance risk models.

3.3 Using Regression Analysis to Predict Financial Outcomes

Regression analysis is a powerful statistical tool used to understand relationships between variables and predict financial outcomes based on historical data. For accountants and risk analysts, mastering regression techniques can enhance forecasting accuracy, support decision-making, and improve risk assessment.

What is Regression Analysis?

Regression analysis estimates the relationship between a dependent variable (the outcome we want to predict) and one or more independent variables (predictors).

- Simple Linear Regression: One independent variable.

- Multiple Linear Regression: Multiple independent variables.

Why Use Regression in Financial Risk Modeling?

- Predict future cash flows based on historical trends.

- Estimate credit risk by analyzing borrower characteristics.

- Forecast market risk factors like stock prices or interest rates.

- Identify key drivers of financial performance.

Mind Map: Key Concepts in Regression Analysis

Regression Analysis Mind Map

Step-by-Step Example: Predicting Company Revenue Using Multiple Linear Regression

Scenario: An accountant wants to predict next quarter’s revenue based on advertising spend, number of sales calls, and economic index.

| Variable | Description |

|---|---|

| Revenue (Y) | Quarterly revenue (in $ thousands) |

| Advertising Spend (X1) | Amount spent on advertising ($ thousands) |

| Sales Calls (X2) | Number of sales calls made |

| Economic Index (X3) | Economic health indicator (index value) |

Step 1: Collect Data

| Quarter | Revenue (Y) | Advertising Spend (X1) | Sales Calls (X2) | Economic Index (X3) |

|---|---|---|---|---|

| Q1 | 500 | 50 | 200 | 100 |

| Q2 | 550 | 55 | 220 | 102 |

| Q3 | 580 | 60 | 230 | 105 |

| Q4 | 600 | 65 | 250 | 107 |

Step 2: Build the Regression Model

The regression equation:

\[ Revenue = \beta_0 + \beta_1 \times AdvertisingSpend + \beta_2 \times SalesCalls + \beta_3 \times EconomicIndex + \epsilon \]

Step 3: Interpret Coefficients

| Coefficient | Interpretation |

|---|---|

| \(\beta_0\) (Intercept) | Base revenue when all predictors are zero |

| \(\beta_1\) (Advertising Spend) | Expected increase in revenue per $1k spent on advertising |

| \(\beta_2\) (Sales Calls) | Expected increase in revenue per additional sales call |

| \(\beta_3\) (Economic Index) | Expected revenue change per unit increase in economic index |

Step 4: Make Predictions

If next quarter’s advertising spend is $70k, sales calls are 260, and economic index is 108, plug into the model to predict revenue.

Mind Map: Regression Workflow for Financial Prediction

Best Practices for Accountants Using Regression Analysis

- Ensure Data Quality: Accurate and relevant data improves model reliability.

- Check Model Assumptions: Violations can lead to misleading results.

- Avoid Overfitting: Use only necessary variables to maintain model generalizability.

- Interpret Results in Context: Coefficients should make business sense.

- Validate Model: Use holdout samples or cross-validation.

Additional Example: Predicting Loan Default Probability Using Logistic Regression

While linear regression predicts continuous outcomes, logistic regression predicts probabilities, such as the likelihood of loan default.

- Dependent Variable: Default (Yes=1, No=0)

- Independent Variables: Debt-to-Income Ratio, Credit Score, Employment Length

This example demonstrates how regression techniques adapt to different financial risk modeling needs.

Summary

Regression analysis is an essential technique for accountants and risk analysts to predict financial outcomes and quantify relationships between variables. By following best practices and understanding the underlying assumptions, professionals can build robust models that support risk management and strategic planning.

3.4 Monte Carlo Simulations: Concepts and Applications

Monte Carlo simulations are a powerful quantitative technique used in financial risk modeling to assess the impact of uncertainty and variability in financial outcomes. This method relies on repeated random sampling to simulate a wide range of possible scenarios, allowing accountants and risk analysts to better understand potential risks and make informed decisions.

What is a Monte Carlo Simulation?

At its core, a Monte Carlo simulation models the probability of different outcomes in a process that cannot easily be predicted due to the intervention of random variables. It is particularly useful when dealing with complex financial systems where multiple uncertain factors interact.

Key Concepts:

- Random Sampling: Generating random inputs based on defined probability distributions.

- Iterations: Running thousands or millions of simulations to cover a broad spectrum of possible outcomes.

- Probability Distributions: Defining how input variables behave (e.g., Normal, Lognormal, Uniform distributions).

- Output Analysis: Aggregating results to estimate probabilities, expected values, and risk measures.

Mind Map: Monte Carlo Simulation Overview

Step-by-Step Process of Monte Carlo Simulation

- Define the Problem: Identify the financial variable or risk to model (e.g., portfolio value, credit loss).

- Model Inputs: Determine the uncertain variables and assign appropriate probability distributions.

- Generate Random Samples: Use random number generators to create input scenarios.

- Run Simulations: Calculate the output for each set of inputs over many iterations.

- Analyze Results: Summarize outcomes using statistics such as mean, variance, percentiles, and Value at Risk (VaR).

Example: Simulating Future Portfolio Value

Imagine an accountant wants to estimate the future value of an investment portfolio over one year. The portfolio return is uncertain and assumed to follow a normal distribution with a mean annual return of 8% and a standard deviation of 15%.

Step 1: Define the initial portfolio value: $100,000.

Step 2: Model the annual return as a Normal(0.08, 0.15).

Step 3: Generate 10,000 random returns from this distribution.

Step 4: Calculate portfolio value for each return:

Portfolio Value = Initial Value * (1 + Simulated Return)

Step 5: Analyze the distribution of simulated portfolio values.

Outcome:

- Mean portfolio value

- Probability portfolio value falls below a threshold (e.g., $80,000)

- Value at Risk (VaR) at 95% confidence level

Mind Map: Monte Carlo Simulation Example - Portfolio Value

Applications of Monte Carlo Simulations in Financial Risk Modeling

- Credit Risk: Simulating default probabilities and loss given default to estimate potential credit losses.

- Market Risk: Estimating the distribution of portfolio returns to calculate VaR and Expected Shortfall.

- Operational Risk: Modeling the frequency and severity of operational loss events.

- Liquidity Risk: Simulating cash flow variability under different market conditions.

Best Practices for Accountants Using Monte Carlo Simulations

- Accurate Input Distributions: Use historical data and expert judgment to define realistic probability distributions.

- Sufficient Iterations: Run enough simulations (typically thousands) to ensure stable results.

- Scenario Validation: Cross-check simulation outputs with known scenarios or stress tests.

- Documentation: Clearly document assumptions, inputs, and methodology for transparency and audit purposes.

- Software Tools: Utilize reliable tools like Excel with add-ins, R, Python, or specialized risk software.

Example: Monte Carlo Simulation in Excel

Accountants can implement a simple Monte Carlo simulation in Excel using the following steps:

- Use the

NORM.INV(RAND(), mean, standard_deviation)function to generate random returns. - Calculate portfolio values based on these returns.

- Repeat the process down a column for thousands of rows.

- Use Excel functions like

PERCENTILEandAVERAGEto analyze the results.

This approach provides an accessible way for accountants to start applying Monte Carlo simulations without advanced programming.

Summary

Monte Carlo simulations offer accountants a robust framework to quantify financial risk by modeling uncertainty through random sampling. By integrating best practices and leveraging accessible tools, accountants can enhance their risk assessment capabilities, providing valuable insights to support financial decision-making.

3.5 Example: Modeling Operational Risk Using Monte Carlo Simulation

Operational risk refers to the risk of loss resulting from inadequate or failed internal processes, people, systems, or external events. Unlike market or credit risk, operational risk is often less quantifiable and more complex to model. Monte Carlo simulation offers a powerful technique to estimate potential losses by simulating a wide range of possible outcomes based on probabilistic inputs.

Step 1: Define the Scope of Operational Risk

Operational risk can arise from various sources such as fraud, system failures, legal risks, or human error. For this example, we focus on fraud risk within an accounting department.

Mind Map: Operational Risk Scope

Step 2: Identify Key Risk Factors and Loss Distribution

To model fraud risk, we need to identify:

- Frequency of fraud events (how often fraud occurs)

- Severity of fraud losses (financial impact per event)

Assume:

- Fraud events follow a Poisson distribution with an average of 2 events per year.

- Loss severity follows a Lognormal distribution with a mean loss of $50,000 and a standard deviation of $20,000.

Mind Map: Risk Factors for Fraud

Step 3: Monte Carlo Simulation Process

Monte Carlo simulation involves the following steps:

- Simulate the number of fraud events in a year using the Poisson distribution.

- For each simulated event, generate a loss amount from the Lognormal distribution.

- Sum the losses for all events to get the total annual loss.

- Repeat steps 1-3 for a large number of iterations (e.g., 10,000) to build a distribution of total losses.

Mind Map: Monte Carlo Simulation Steps

Step 4: Implementing the Simulation (Example in Excel or Python)

Excel Approach:

- Use

POISSON.DISTor generate Poisson random numbers with VBA or add-ins. - Use

LOGNORM.INV(RAND(), mean, std_dev)to generate loss severity. - Sum losses per iteration.

Python Snippet:

import numpy as np

np.random.seed(42) # For reproducibility

iterations = 10000

lambda_poisson = 2

mean_loss = 50000

std_loss = 20000

# Convert mean and std to lognormal parameters

mu = np.log(mean_loss**2 / np.sqrt(std_loss**2 + mean_loss**2))

sigma = np.sqrt(np.log(1 + (std_loss**2 / mean_loss**2)))

total_losses = []

for _ in range(iterations):

num_events = np.random.poisson(lambda_poisson)

losses = np.random.lognormal(mu, sigma, num_events)

total_losses.append(losses.sum())

# Analyze results

percentile_95 = np.percentile(total_losses, 95)

print(f"95th Percentile Loss: ${percentile_95:,.2f}")

Step 5: Interpreting the Results

- The simulation output is a distribution of possible annual losses due to fraud.

- The 95th percentile loss represents a loss level that will not be exceeded 95% of the time — useful for setting risk limits or capital reserves.

Mind Map: Interpreting Simulation Results

Step 6: Best Practices for Operational Risk Modeling Using Monte Carlo

- Accurate Data Collection: Use historical loss data to calibrate frequency and severity distributions.

- Distribution Selection: Choose appropriate statistical distributions that fit the data.

- Sufficient Iterations: Run enough simulations (e.g., 10,000+) for stable results.

- Scenario Analysis: Combine Monte Carlo with stress testing for extreme events.

- Model Validation: Backtest simulation outputs against actual loss experience.

Summary Example

| Parameter | Value |

|---|---|

| Event Frequency (λ) | 2 events/year |

| Loss Severity Mean | $50,000 |

| Loss Severity Std Dev | $20,000 |

| Simulation Iterations | 10,000 |

| 95th Percentile Loss | $XXX,XXX (output from sim) |

This example demonstrates how accountants and risk analysts can use Monte Carlo simulation to quantify operational risk, enabling better-informed decisions about risk controls and capital allocation.

4. Credit Risk Modeling for Accountants

4.1 Fundamentals of Credit Risk and Its Measurement

Credit risk is the possibility that a borrower or counterparty will fail to meet their financial obligations as agreed, leading to a financial loss for the lender or investor. For accountants, understanding credit risk is crucial because it directly impacts the valuation of assets, provisioning for bad debts, and overall financial health of an organization.

What is Credit Risk?

- Definition: The risk of loss due to a borrower’s failure to repay a loan or meet contractual obligations.

- Key Players: Banks, financial institutions, corporate lenders, investors.

- Types of Credit Risk:

- Default Risk: Borrower fails to make scheduled payments.

- Counterparty Risk: Risk that the other party in a financial contract defaults.

- Concentration Risk: Excessive exposure to a single borrower or sector.

Mind Map: Components of Credit Risk

Key Metrics in Credit Risk Measurement

- Probability of Default (PD): The likelihood that a borrower will default within a given time frame.

- Loss Given Default (LGD): The amount of loss a lender incurs if the borrower defaults, expressed as a percentage of exposure.

- Exposure at Default (EAD): The total value exposed to loss at the time of default.

- Expected Loss (EL): Calculated as EL = PD × LGD × EAD.

Mind Map: Credit Risk Metrics

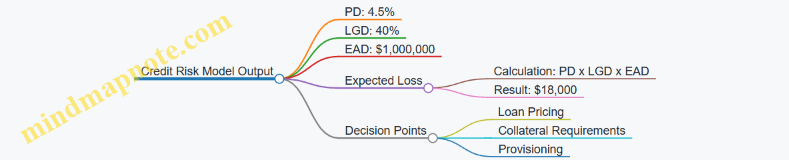

Example 1: Calculating Expected Loss for a Corporate Loan

Scenario:

- Loan amount (EAD): $1,000,000

- Probability of Default (PD): 2% (0.02)

- Loss Given Default (LGD): 40% (0.40)

Calculation:

Expected Loss (EL) = PD × LGD × EAD

EL = 0.02 × 0.40 × $1,000,000 = $8,000

This means the lender expects to lose $8,000 on average due to credit risk on this loan.

Credit Risk Assessment Process

- Data Collection: Gather borrower financials, credit history, market data.

- Credit Scoring: Use quantitative models to assign a credit score.

- Credit Rating: Assign a rating based on score and qualitative factors.

- Risk Quantification: Calculate PD, LGD, EAD, and EL.

- Decision Making: Approve, reject, or adjust terms based on risk.

Mind Map: Credit Risk Assessment Workflow

Example 2: Simple Credit Scoring Model

Suppose an accountant is evaluating a small business loan application. The scoring criteria might include:

| Factor | Score Range | Applicant Score |

|---|---|---|

| Payment History | 0-40 | 35 |

| Debt-to-Income Ratio | 0-30 | 25 |

| Length of Credit | 0-20 | 15 |

| Collateral | 0-10 | 8 |

Total Score: 35 + 25 + 15 + 8 = 83 out of 100

Interpretation: A score above 75 might indicate low credit risk, guiding the accountant to recommend loan approval with standard terms.

Best Practices for Accountants in Credit Risk Measurement

- Use Multiple Data Points: Combine quantitative data with qualitative insights.

- Regularly Update Models: Reflect changes in market conditions and borrower status.

- Document Assumptions: Maintain transparency for audits and regulatory compliance.

- Stress Test Models: Evaluate how models perform under adverse scenarios.

- Collaborate with Risk Analysts: Leverage expertise to refine models and interpretations.

Summary

Understanding the fundamentals of credit risk and its measurement equips accountants to better evaluate financial exposures, make informed decisions, and contribute to robust risk management frameworks. By mastering key metrics like PD, LGD, EAD, and expected loss, accountants can quantify risk effectively and support organizational financial health.

4.2 Credit Scoring Models: Logistic Regression and Beyond

Credit scoring models are essential tools used by accountants and risk analysts to evaluate the creditworthiness of borrowers. These models help predict the likelihood that a borrower will default on their obligations, enabling informed lending decisions and risk management.

What is Credit Scoring?

Credit scoring is a statistical technique that assigns a score to potential borrowers based on their financial and personal characteristics. This score reflects the probability of default or the risk level associated with lending to that individual or entity.

Logistic Regression: The Foundation of Credit Scoring

Logistic regression is the most widely used method for credit scoring due to its simplicity, interpretability, and effectiveness in binary classification problems (e.g., default vs. non-default).

- Concept: Logistic regression models the probability that a borrower defaults (target variable = 1) based on predictor variables such as income, debt-to-income ratio, credit history, etc.

- Output: Probability value between 0 and 1, which can be converted into a credit score.

Logistic Regression Formula:

\[ P(Y=1|X) = \frac{1}{1 + e^{-(\beta_0 + \beta_1 X_1 + \beta_2 X_2 + … + \beta_n X_n)}} \]

Where:

- \(P(Y=1|X)\) is the probability of default given predictors \(X\)

- \(\beta_0\) is the intercept

- \(\beta_i\) are coefficients for predictors \(X_i\)

Mind Map: Logistic Regression in Credit Scoring

Example: Building a Simple Logistic Regression Model

Scenario: An accountant wants to predict whether a corporate client will default on a loan based on two variables: Debt-to-Income Ratio (DTI) and Number of Late Payments.

| Client | DTI (%) | Late Payments | Default (1=Yes, 0=No) |

|---|---|---|---|

| A | 30 | 1 | 0 |

| B | 55 | 3 | 1 |

| C | 40 | 0 | 0 |

| D | 70 | 4 | 1 |

Using logistic regression, the accountant fits the model and obtains:

\[ \text{logit}(P) = -4 + 0.05 \times \text{DTI} + 0.8 \times \text{Late Payments} \]

For Client B:

\[ \text{logit}(P) = -4 + 0.05 \times 55 + 0.8 \times 3 = -4 + 2.75 + 2.4 = 1.15 \]

Probability of default:

\[ P = \frac{1}{1 + e^{-1.15}} \approx 0.76 \]

This means Client B has a 76% chance of defaulting, indicating high risk.

Beyond Logistic Regression: Advanced Credit Scoring Models

While logistic regression is foundational, more complex models can capture nonlinear relationships and interactions, improving predictive power.

Decision Trees

- Split data based on feature thresholds to classify borrowers.

- Easy to interpret.

Random Forests

- Ensemble of decision trees to reduce overfitting.

- Handles large datasets well.

Gradient Boosting Machines (GBM)

- Sequentially builds trees to correct errors.

- High accuracy but less interpretable.

Support Vector Machines (SVM)

- Finds optimal boundary to separate classes.

- Effective in high-dimensional spaces.

Neural Networks

- Mimics human brain structure.

- Captures complex patterns but requires large data.

Mind Map: Advanced Credit Scoring Models

Example: Comparing Logistic Regression and Random Forest

Scenario: Using the same dataset, the accountant tries both logistic regression and random forest to predict defaults.

| Model | Accuracy | Interpretability | Use Case |

|---|---|---|---|

| Logistic Regression | 78% | High | When transparency is key |

| Random Forest | 85% | Medium | When accuracy is prioritized |

The accountant chooses logistic regression for regulatory reporting due to its transparency but uses random forest internally for risk monitoring.

Best Practices for Credit Scoring Models

- Feature Selection: Choose relevant financial ratios, payment history, and demographic data.

- Data Quality: Ensure clean, complete, and up-to-date data.

- Model Validation: Use cross-validation and backtesting to assess model performance.

- Interpretability: Balance between model complexity and explainability, especially for regulatory compliance.

- Regular Updates: Periodically retrain models with new data to maintain accuracy.

Summary

Logistic regression remains a cornerstone in credit scoring for accountants due to its balance of simplicity and effectiveness. However, exploring advanced models like random forests and gradient boosting can enhance predictive accuracy. Integrating best practices and understanding model trade-offs ensures robust credit risk assessment.

Additional Resources

- Hosmer, D.W., Lemeshow, S., & Sturdivant, R.X. (2013). Applied Logistic Regression.

- James, G., Witten, D., Hastie, T., & Tibshirani, R. (2013). An Introduction to Statistical Learning.

- Credit Scoring and Its Applications, Thomas, Crook, & Edelman (2017).

4.3 Best Practices in Building Credit Risk Models

Building robust credit risk models is essential for accountants aiming to accurately assess the likelihood of default and manage credit exposures effectively. Below are key best practices, supported by mind maps and practical examples to facilitate understanding.

Understand the Business Context

Before building any model, it’s critical to grasp the lending environment, borrower profiles, and regulatory requirements.

Mind Map: Understanding Business Context

Example: A bank focusing on SME loans must understand sector-specific risks and typical cash flow cycles to tailor the credit risk model accordingly.

Data Quality and Feature Selection

High-quality, relevant data is the foundation of any credit risk model. Feature selection improves model accuracy and interpretability.

Mind Map: Data Quality & Feature Selection

Example: Using a borrower’s debt-to-equity ratio and payment history as features can significantly improve prediction of default risk.

Choose Appropriate Modeling Techniques

Select models that balance predictive power with explainability, especially important for regulatory compliance.

Mind Map: Modeling Techniques

Example: Logistic regression is often preferred for credit scoring due to its transparency, while random forests can be used to capture complex nonlinear relationships.

Model Validation and Backtesting

Regular validation ensures the model remains accurate over time and adapts to changing conditions.

Mind Map: Model Validation

Example: After building a credit risk model, use a holdout sample to test predictive accuracy and monitor performance quarterly to detect model degradation.

Incorporate Regulatory and Ethical Considerations

Ensure models comply with regulations and avoid bias.

Mind Map: Regulatory & Ethical Considerations

Example: Avoid using protected attributes such as race or gender in the model and provide clear explanations of credit decisions to customers.

Documentation and Communication

Maintain thorough documentation and communicate findings effectively to stakeholders.

Mind Map: Documentation & Communication

Example: Prepare a report summarizing the credit risk model’s methodology and results, including visualizations like score distributions and default probabilities.

Integrated Example: Building a Credit Risk Model for Corporate Clients

- Step 1: Gather financial statements, payment history, and macroeconomic data.

- Step 2: Clean data, handle missing values, and select features such as debt-to-equity ratio, current ratio, and payment delays.

- Step 3: Use logistic regression to develop the credit scoring model.

- Step 4: Validate the model using cross-validation and calculate AUC.

- Step 5: Ensure compliance with Basel III and exclude any sensitive attributes.

- Step 6: Document the process and present findings to risk management and credit committees.

This approach ensures a transparent, accurate, and compliant credit risk model tailored to the accountant’s role in financial risk management.

4.4 Integrating Financial Ratios into Credit Risk Assessment

Financial ratios are essential tools for accountants when assessing credit risk. They provide quantifiable insights into a company’s financial health, operational efficiency, and ability to meet debt obligations. Integrating these ratios into credit risk models enhances the accuracy and reliability of creditworthiness evaluations.

Key Financial Ratios for Credit Risk Assessment

-

Liquidity Ratios: Measure the ability to meet short-term obligations.

- Current Ratio

- Quick Ratio

-

Leverage Ratios: Indicate the level of debt relative to equity or assets.

- Debt-to-Equity Ratio

- Debt Ratio

-

Profitability Ratios: Reflect the company’s ability to generate profits.

- Return on Assets (ROA)

- Return on Equity (ROE)

- Net Profit Margin

-

Efficiency Ratios: Show how well the company uses its assets.

- Asset Turnover Ratio

- Inventory Turnover

-

Coverage Ratios: Assess the ability to service debt.

- Interest Coverage Ratio

Mind Map: Financial Ratios in Credit Risk Assessment

Best Practices for Using Financial Ratios in Credit Risk Models

-

Use Multiple Ratios Together: No single ratio provides a complete picture. Combining liquidity, leverage, and profitability ratios offers a holistic view.

-

Benchmark Against Industry Standards: Compare ratios to industry averages or peer companies to contextualize the results.

-

Trend Analysis: Analyze ratios over multiple periods to detect improving or deteriorating financial conditions.

-

Adjust for Seasonality and One-Off Events: Normalize ratios to avoid misleading conclusions from temporary fluctuations.

-

Incorporate Ratios into Quantitative Models: Use ratios as input variables in logistic regression or machine learning models for credit scoring.

Example: Integrating Financial Ratios into a Credit Risk Score

Consider a mid-sized manufacturing company applying for a loan. The accountant calculates the following ratios:

| Ratio | Value | Industry Average | Interpretation |

|---|---|---|---|

| Current Ratio | 1.8 | 1.5 | Good liquidity |

| Debt-to-Equity Ratio | 1.2 | 1.0 | Slightly higher leverage |

| Return on Assets (ROA) | 6% | 5% | Above average profitability |

| Interest Coverage Ratio | 4.5x | 3.0x | Strong ability to cover interest |

Step 1: Normalize the ratios by comparing to industry averages.

Step 2: Assign weights based on their importance in credit risk (e.g., liquidity 30%, leverage 25%, profitability 25%, coverage 20%).

Step 3: Calculate a composite credit risk score.

Step 4: Use the score to classify the company’s credit risk (e.g., low, medium, high).

This approach helps the accountant provide a data-driven recommendation to lenders.

Mind Map: Example Workflow for Financial Ratio Integration

Additional Example: Using Ratios in Logistic Regression Model

Accountants can incorporate financial ratios as independent variables in a logistic regression model to predict the probability of default (PD).

Variables:

- Current Ratio

- Debt-to-Equity Ratio

- ROA

- Interest Coverage Ratio

Model Output: Probability that the borrower will default within the next year.

Interpretation: Higher current ratio and interest coverage reduce PD, while higher debt-to-equity increases PD.

This quantitative approach, combined with qualitative insights, strengthens credit risk assessment.

Summary

Integrating financial ratios into credit risk assessment empowers accountants to make informed, objective evaluations of a borrower’s creditworthiness. By combining multiple ratios, benchmarking, trend analysis, and embedding these metrics into statistical models, accountants can enhance the predictive power and transparency of credit risk models.

4.5 Practical Example: Developing a Credit Risk Model for Corporate Clients

In this section, we will walk through a practical example of developing a credit risk model tailored for corporate clients. This example integrates best practices and uses clear, easy-to-understand steps to help accountants grasp the modeling process.

Step 1: Define the Objective

The primary goal is to predict the probability of default (PD) for corporate clients applying for credit, helping the finance team make informed lending decisions.

Step 2: Data Collection

Collect relevant data points including:

- Financial ratios (e.g., Debt-to-Equity, Current Ratio)

- Payment history

- Credit scores

- Industry sector

- Company size (revenue, employees)

- Macroeconomic indicators

Step 3: Feature Selection and Engineering

Identify the most predictive variables using domain knowledge and statistical techniques.

Mind Map: Feature Selection Process

Example: Calculate Debt-to-Equity Ratio = Total Liabilities / Shareholders’ Equity

Step 4: Model Choice

Commonly used models for credit risk include logistic regression, decision trees, and more advanced machine learning models. For this example, we will use logistic regression due to its interpretability.

Step 5: Model Building

- Split data into training and testing sets (e.g., 70% train, 30% test).

- Train the logistic regression model using the training data.

- Use financial ratios and payment history as independent variables.

Example:

| Variable | Coefficient (β) | Interpretation |

|---|---|---|

| Debt-to-Equity Ratio | 1.5 | Higher ratio increases default risk |

| Current Ratio | -0.8 | Higher liquidity reduces default risk |

| Days Past Due | 2.0 | More days past due increases risk |

Step 6: Model Evaluation

Evaluate the model using metrics such as:

- Accuracy

- Precision and Recall

- Area Under the ROC Curve (AUC)

Example: The model achieves an AUC of 0.85, indicating good discrimination between default and non-default clients.

Step 7: Risk Scoring and Decision Making

Convert the logistic regression output (log-odds) into a probability score representing the likelihood of default.

Mind Map: Risk Scoring Workflow

Example: A client with a PD of 18% would be classified as high risk, prompting additional collateral requirements or credit denial.

Step 8: Model Validation and Monitoring

- Perform backtesting using historical data to verify predictive power.

- Monitor model performance regularly to detect drift.

Summary Table: Example Corporate Client Data and Model Output

| Client ID | Debt-to-Equity | Current Ratio | Days Past Due | Predicted PD (%) | Risk Category |

|---|---|---|---|---|---|

| 101 | 2.5 | 1.2 | 0 | 4.5 | Low Risk |

| 102 | 4.0 | 0.8 | 15 | 22.0 | High Risk |