Financial Modelling for Accountants

1. Introduction to Financial Modelling

1.1 What is Financial Modelling? Definition and Scope

Financial modelling is the process of creating a mathematical representation of a company’s financial performance, operations, and future projections. It involves building structured models—usually in spreadsheet software like Microsoft Excel—that simulate real-world financial scenarios to aid decision-making, forecasting, and valuation.

Definition:

Financial Modelling is the art and science of constructing quantitative models that represent the financial aspects of a business or project, enabling accountants, financial analysts, and decision-makers to analyze historical data, forecast future performance, and evaluate financial outcomes under various assumptions.

Scope of Financial Modelling:

Financial modelling covers a broad range of applications including:

- Budgeting and forecasting

- Valuation of companies and projects

- Investment analysis

- Risk assessment and scenario planning

- Mergers and acquisitions

- Capital raising and financing decisions

- Performance measurement and ratio analysis

Mind Map: Core Components of Financial Modelling

Mind Map: Users and Benefits of Financial Modelling

Example 1: Simple Revenue Forecast Model

Imagine a retail company wants to forecast its revenue for the next year. The financial model might include:

- Inputs: Historical monthly sales data, expected growth rate (e.g., 5% increase per month), seasonality factors.

- Process: Apply growth rate and seasonality adjustments to historical data.

- Output: Projected monthly revenue for the next 12 months.

This simple model helps the accountant understand expected cash inflows and plan budgets accordingly.

Example 2: Valuation Model for a Tech Startup

A financial analyst builds a discounted cash flow (DCF) model to estimate the value of a tech startup:

- Inputs: Projected revenue growth, operating expenses, capital expenditures, discount rate.

- Process: Forecast free cash flows for 5 years, calculate terminal value, discount cash flows to present value.

- Output: Estimated enterprise value to support investment decisions.

This model guides investors and accountants in assessing whether the startup is a viable investment.

Summary

Financial modelling is a foundational skill for accountants and financial analysts, enabling them to translate complex financial data into actionable insights. By understanding its definition and scope, professionals can build models that support strategic planning, risk management, and effective communication across finance and tech sectors.

1.2 Importance of Financial Modelling in Accounting and Finance

Financial modelling is a cornerstone skill for accountants and financial analysts, serving as the backbone for informed decision-making, strategic planning, and performance evaluation. Its importance spans multiple facets of accounting and finance, providing clarity, accuracy, and foresight in complex financial environments.

Why Financial Modelling Matters

- Decision Support: Enables professionals to simulate financial outcomes based on various assumptions, helping stakeholders make data-driven decisions.

- Forecasting & Budgeting: Facilitates the projection of revenues, expenses, and cash flows, essential for budgeting and long-term planning.

- Valuation & Investment Analysis: Helps in valuing companies, projects, or assets, supporting investment decisions and capital allocation.

- Risk Management: Assists in identifying financial risks by analyzing different scenarios and their impact.

- Performance Monitoring: Tracks financial health through ratios and KPIs derived from the model.

Mind Map: Core Benefits of Financial Modelling

Example 1: Supporting a Business Expansion Decision

Imagine an accountant at a tech company tasked with evaluating whether to open a new office in a different city. Using financial modelling, they:

- Input assumptions such as expected revenue growth, operating costs, and capital expenditures.

- Create scenarios (base case, optimistic, pessimistic) to understand potential outcomes.

- Calculate projected cash flows and profitability.

- Present findings to management, highlighting risks and expected returns.

This model helps the company decide whether the expansion aligns with financial goals.

Mind Map: Financial Modelling in Business Expansion

Example 2: Budgeting and Forecasting for a Financial Year

An accountant in a manufacturing firm uses financial modelling to prepare the annual budget:

- Historical sales data is analyzed to forecast future sales.

- Variable and fixed costs are projected based on production plans.

- The model dynamically updates profit margins and cash flow forecasts.

- Enables the finance team to allocate resources efficiently and anticipate funding needs.

This proactive approach reduces surprises and aligns departments with financial targets.

Mind Map: Budgeting and Forecasting Process

Summary

Financial modelling empowers accountants and financial analysts to transform raw data into actionable insights. It enhances accuracy in forecasting, supports strategic decisions, and enables effective communication with stakeholders. Mastering financial modelling is therefore essential for professionals aiming to add value and drive financial success within their organizations.

1.3 Overview of Common Financial Models Used by Accountants

Financial models are essential tools that accountants use to analyze financial data, forecast future performance, and support decision-making. Understanding the common types of financial models helps accountants select and build the appropriate model for their specific needs. Below is an overview of the most frequently used financial models in accounting, along with mind maps and practical examples.

Common Financial Models Mind Map

Budgeting Models

Description: Budgeting models help accountants plan and control finances by estimating revenues, expenses, and cash flows for a future period.

Example: An accountant creates an operating budget model for the next fiscal year, projecting monthly sales, cost of goods sold, operating expenses, and net profit.

Practical Example:

- Input assumptions: monthly sales growth rate, fixed and variable costs.

- Output: monthly profit and loss statement.

Forecasting Models

Description: Forecasting models predict future financial outcomes based on historical data and assumptions.

Example: Revenue forecasting model using historical sales data and market growth rates to estimate next year’s revenue.

Practical Example:

- Use a linear growth assumption or seasonality adjustments.

- Output: projected revenue by product line.

Valuation Models

Description: Valuation models estimate the value of a business or asset.

Example: Discounted Cash Flow (DCF) model that calculates the present value of expected future cash flows.

Practical Example:

- Inputs: projected free cash flows, discount rate (WACC).

- Output: enterprise value.

Financial Statement Models

Description: These models integrate the three core financial statements to provide a comprehensive view of financial health.

Example: Integrated model linking income statement, balance sheet, and cash flow statement.

Practical Example:

- Calculate depreciation expense on fixed assets and link it to both income statement and balance sheet.

- Ensure the balance sheet balances after all transactions.

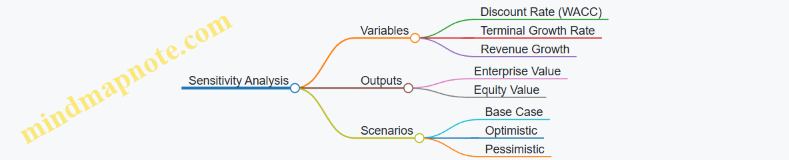

Scenario and Sensitivity Models

Description: These models test how changes in key assumptions affect financial outcomes.

Example: Scenario analysis with base, optimistic, and pessimistic sales forecasts.

Practical Example:

- Adjust sales growth rate and cost assumptions.

- Observe impact on net income and cash flow.

Cost Models

Description: Cost models analyze cost behavior and help in pricing and profitability decisions.

Example: Cost-Volume-Profit (CVP) model to determine break-even sales volume.

Practical Example:

- Inputs: fixed costs, variable cost per unit, sales price per unit.

- Output: break-even point in units and dollars.

Project Finance Models

Description: These models evaluate the financial viability of projects or investments.

Example: Capital budgeting model calculating Net Present Value (NPV) and Internal Rate of Return (IRR).

Practical Example:

- Inputs: initial investment, projected cash inflows, discount rate.

- Output: NPV and IRR to support investment decisions.

Summary

Accountants rely on a variety of financial models tailored to their specific tasks, whether budgeting, forecasting, valuation, or cost analysis. Mastering these models with clear assumptions and linked statements enhances accuracy and decision-making.

Additional Mind Map: Integrated Financial Statement Model

This comprehensive overview equips accountants with a foundational understanding of the financial models they use daily, supported by practical examples and visual mind maps for clarity.

1.4 Key Terminologies and Concepts in Financial Modelling

Financial modelling involves a variety of terms and concepts that are essential for accountants and financial analysts to understand. This section breaks down these key terminologies with clear explanations and examples, supported by mind maps to visualize relationships.

Key Terminologies

- Assumptions: Inputs or conditions set at the start of the model that drive calculations.

- Drivers: Variables that have a direct impact on financial outcomes (e.g., sales volume, growth rate).

- Outputs: Results generated by the model, such as financial statements or ratios.

- Scenarios: Different sets of assumptions to test various possible outcomes.

- Sensitivity Analysis: Technique to see how changes in drivers affect outputs.

- Circular Reference: A situation where a formula refers back to its own cell, often requiring iterative calculations.

- Linking: Connecting different parts of the model or different financial statements so changes propagate automatically.

- Dynamic Model: A model designed to update automatically when inputs change.

- Modularity: Structuring the model into separate, manageable sections or sheets.

- Error Checking: Processes to identify and correct mistakes in formulas or logic.

Mind Map: Core Concepts in Financial Modelling

Detailed Concepts with Examples

-

Assumptions & Drivers

-

Example: Assume a company expects 10% annual sales growth. This assumption drives revenue forecasts.

-

Mind Map:

- Assumptions

- Sales Growth Rate (10%)

- Cost Inflation Rate (3%)

- Tax Rate (25%)

- Drivers

- Sales Volume

- Price per Unit

- Assumptions

-

-

Outputs

- Example: The model outputs include projected Income Statement, Balance Sheet, and Cash Flow Statement.

- Mind Map:

- Outputs - Income Statement - Balance Sheet - Cash Flow Statement - Financial Ratios -

Scenarios & Sensitivity Analysis

-

Example: Create three scenarios: Base Case (10% growth), Optimistic (15% growth), Pessimistic (5% growth).

-

Sensitivity analysis might test how a 1% change in sales growth affects net income.

-

Mind Map:

- Scenario Analysis

- Base Case

- Optimistic

- Pessimistic

- Sensitivity Analysis

- Change in Sales Growth

- Impact on Net Income

- Scenario Analysis

-

-

Circular Reference

- Example: Interest expense depends on debt balance, but debt balance depends on cash flow, which includes interest expense. This circularity requires iterative calculation settings.

-

Linking & Modularity

- Example: Linking depreciation expense from the fixed asset schedule to the Income Statement.

- Modularity example: Separate sheets for Inputs, Calculations, Outputs.

-

Error Checking

- Example: Use Excel’s formula auditing tools to trace precedents and dependents, ensuring no broken links or incorrect formulas.

Summary Table of Terms and Examples

| Term | Definition | Example |

|---|---|---|

| Assumptions | Inputs that drive the model | Sales growth rate = 10% |

| Drivers | Variables affecting outputs | Sales volume, price per unit |

| Outputs | Results generated by the model | Projected Income Statement |

| Scenarios | Different sets of assumptions | Base, Optimistic, Pessimistic growth rates |

| Sensitivity Analysis | Testing impact of changes in drivers | Effect of 1% sales growth change on net income |

| Circular Reference | Formula refers back to itself | Interest expense linked to debt balance |

| Linking | Connecting model components | Depreciation linked from fixed assets to P&L |

| Modularity | Dividing model into sections | Separate sheets for Inputs, Calculations, Outputs |

| Error Checking | Identifying and fixing errors | Using Excel formula auditing |

By mastering these terminologies and concepts, accountants can build robust, transparent, and flexible financial models that support insightful analysis and decision-making.

1.5 Setting Objectives: Understanding the Purpose of Your Model

Setting clear objectives is the foundational step in building any financial model. Without a well-defined purpose, your model risks becoming overly complex, inaccurate, or irrelevant to the decision-making process. This section will guide you through how to set precise objectives and align your modelling efforts accordingly.

Why Setting Objectives Matters

- Focus: Objectives help you concentrate on relevant data and calculations.

- Efficiency: Saves time by avoiding unnecessary model components.

- Clarity: Facilitates communication with stakeholders.

- Accuracy: Ensures assumptions and outputs are aligned with the intended use.

Key Questions to Define Your Model’s Purpose

- What decision or analysis will this model support?

- Who is the primary user or audience?

- What is the time horizon (short-term, long-term)?

- What level of detail is required?

- What are the key outputs or deliverables?

Mind Map: Setting Objectives for Financial Models

Example 1: Objective Setting for a Budget Model

Scenario: An accountant is tasked with creating a budget model for the upcoming fiscal year.

- Purpose: To forecast revenues and expenses to guide spending decisions.

- Audience: Internal management team.

- Time Horizon: Monthly for 12 months.

- Outputs: Profit & Loss statement, cash flow forecast.

- Level of Detail: Detailed line items for major expense categories.

This clarity helps the accountant focus on relevant inputs like sales projections, cost of goods sold, operating expenses, and avoid unnecessary complexity like detailed tax schedules.

Example 2: Objective Setting for a Valuation Model

Scenario: A financial analyst needs to build a valuation model for a potential acquisition.

- Purpose: To estimate the fair market value of the target company.

- Audience: Investment committee and potential investors.

- Time Horizon: 5-year forecast.

- Outputs: Discounted cash flow (DCF) valuation, sensitivity analysis.

- Level of Detail: Detailed cash flow projections, capital expenditure, working capital assumptions.

Understanding this objective guides the analyst to focus on free cash flow calculations, discount rates, and scenario testing rather than operational budgeting.

Practical Tips for Setting Objectives

- Write down your objective in one or two sentences before starting.

- Confirm the objective with stakeholders to ensure alignment.

- Revisit and refine objectives as the model evolves.

- Use objectives to prioritize model features and data inputs.

Mind Map: Aligning Model Components with Objectives

By setting clear objectives upfront, accountants and financial analysts can build models that are not only accurate and reliable but also actionable and easy to communicate. This practice ultimately leads to better financial decision-making and stakeholder confidence.

1.6 Example: Building a Simple Revenue Forecast Model

In this section, we will walk through building a simple yet effective revenue forecast model. This example is designed to help accountants understand how to translate business assumptions into a dynamic financial model.

Step 1: Define the Objective

The goal is to forecast monthly revenue for a company over the next 12 months based on historical sales data and growth assumptions.

Step 2: Identify Key Inputs and Assumptions

- Historical monthly sales (units sold and price per unit)

- Expected monthly growth rate (%)

- Seasonality factors (if applicable)

Step 3: Structure the Model

We will organize the model into three main sections:

- Inputs: Where assumptions and historical data are entered

- Calculations: Where the forecast is computed

- Outputs: Where the forecasted revenue is summarized

Mind Map: Revenue Forecast Model Structure

Step 4: Example Data and Assumptions

| Month | Units Sold (Historical) | Price per Unit ($) |

|---|---|---|

| Jan | 1,000 | 50 |

| Feb | 1,100 | 50 |

| Mar | 1,200 | 50 |

- Growth Rate: 5% monthly

- Seasonality Factor: Assume no seasonality for simplicity

Step 5: Calculations

-

Forecast Units Sold:

Forecast for Month N = Previous Month Units Sold * (1 + Growth Rate)

-

Price per Unit:

Assume constant at $50

-

Monthly Revenue:

Revenue = Forecast Units Sold * Price per Unit

Step 6: Example Calculation Table

| Month | Units Sold Forecast | Price per Unit ($) | Revenue ($) |

|---|---|---|---|

| Jan | 1,000 (Historical) | 50 | 50,000 |

| Feb | 1,000 * 1.05 = 1,050 | 50 | 52,500 |

| Mar | 1,050 * 1.05 = 1,102.5 | 50 | 55,125 |

| Apr | 1,102.5 * 1.05 = 1,157.6 | 50 | 57,880 |

Step 7: Implementing in Excel (Example Formulae)

- Cell B2 (Units Sold Jan): 1000 (input)

- Cell B3 (Units Sold Feb):

=B2 * (1 + $E$1)where E1 contains growth rate 5% - Cell C2 (Price per Unit): 50 (input)

- Cell D2 (Revenue Jan):

=B2 * C2

Drag formulas down for subsequent months.

Step 8: Visualizing the Forecast

Create a line chart plotting months on the x-axis and revenue on the y-axis to visualize growth.

Mind Map: Forecast Calculation Flow

Step 9: Best Practices Highlighted

- Clear Inputs: Separate assumptions (growth rate, price) from calculations.

- Dynamic Formulas: Use cell references for easy updates.

- Documentation: Label inputs and calculations clearly.

- Validation: Cross-check forecast against historical trends.

Summary

This simple revenue forecast model provides a foundational approach for accountants to project future sales based on growth assumptions. By structuring inputs, calculations, and outputs clearly and using dynamic formulas, the model remains flexible and easy to update.

This example can be expanded to include seasonality, multiple products, or variable pricing to increase complexity as needed.

2. Planning and Structuring Your Financial Model

2.1 Understanding the Business and Financial Context

Before building any financial model, it is crucial for accountants and financial analysts to thoroughly understand the business and financial context in which the model will operate. This foundational step ensures that the assumptions, inputs, and outputs are relevant, accurate, and aligned with the company’s strategic goals.

Why Understanding the Business Context Matters

- Aligns the model with business objectives: Knowing what drives the business helps tailor the model to answer the right questions.

- Improves accuracy of assumptions: Industry-specific factors and company-specific nuances influence forecasting.

- Enhances stakeholder communication: Models built with context are easier to explain and justify.

Key Areas to Explore

-

Industry and Market Environment

- Market size and growth trends

- Competitive landscape

- Regulatory environment

-

Company Overview

- Business model and revenue streams

- Cost structure

- Key products or services

-

Financial History and Performance

- Historical financial statements

- Profitability and cash flow patterns

- Capital structure and financing

-

Strategic Goals and Risks

- Growth plans

- Potential risks and uncertainties

Mind Map: Understanding the Business and Financial Context

Example: Applying Business Context in a Financial Model

Scenario: You are building a financial model for a SaaS (Software as a Service) company.

- Industry Insight: SaaS companies typically have recurring revenue, high upfront customer acquisition costs, and relatively low variable costs.

- Business Model: Subscription-based revenue with monthly or annual billing.

- Financial History: Historical churn rate of 5% per month, average revenue per user (ARPU) of $50.

How this informs your model:

- Inputs should include churn rate and ARPU as key drivers.

- Revenue forecast should be based on subscriber growth and retention rather than one-time sales.

- Cost assumptions should reflect marketing spend for customer acquisition and fixed costs for platform maintenance.

Mind Map: SaaS Company Financial Model Context

Practical Tips

- Interview key stakeholders: Talk to sales, marketing, operations, and finance teams to gather insights.

- Review industry reports: Use third-party market research to validate assumptions.

- Analyze competitors: Benchmark financial metrics to understand positioning.

- Document findings: Keep a clear record of assumptions and context for future reference.

Summary

Understanding the business and financial context is the first and most critical step in financial modelling. It ensures that the model is relevant, accurate, and actionable. By mapping out the industry environment, company specifics, financial history, and strategic goals, accountants can build models that truly support decision-making and add value.

2.2 Defining Inputs, Assumptions, and Outputs Clearly

In financial modelling, clarity in defining inputs, assumptions, and outputs is critical to building a robust, transparent, and easily auditable model. This section will guide you through best practices for clearly distinguishing these components, supported by mind maps and practical examples.

Understanding the Components

- Inputs: Raw data or variables entered into the model. These are typically historical figures or user-defined parameters.

- Assumptions: Judgments or estimates about future conditions that influence the model. These often include growth rates, cost inflation, or discount rates.

- Outputs: The results generated by the model, such as financial statements, ratios, or forecasts.

Why Clear Definition Matters

- Ensures transparency and ease of review.

- Facilitates updates and scenario analysis.

- Reduces errors by isolating variable components.

Mind Map: Defining Inputs, Assumptions, and Outputs

Best Practices for Defining Inputs

- Create a dedicated ‘Inputs’ worksheet: Centralize all raw data and user variables.

- Use consistent formatting: Highlight input cells with a specific color (e.g., light blue) to differentiate them.

- Label inputs clearly: Use descriptive names and comments where necessary.

- Validate inputs: Use data validation tools (drop-down lists, ranges) to minimize errors.

Example: Inputs Sheet Snapshot

| Input Parameter | Value | Description |

|---|---|---|

| Historical Sales (2023) | 1,200,000 | Actual sales revenue for 2023 |

| Sales Growth Rate | 5% | Expected annual sales growth |

| Cost Inflation Rate | 3% | Annual inflation on costs |

Best Practices for Defining Assumptions

- Separate assumptions from inputs: While inputs are often historical or fixed data, assumptions are forward-looking estimates.

- Document the rationale: Provide notes or comments explaining the basis for each assumption.

- Use named ranges: This improves formula readability and reduces errors.

- Keep assumptions flexible: Design the model so assumptions can be easily modified for scenario analysis.

Example: Assumptions with Documentation

| Assumption | Value | Rationale |

|---|---|---|

| Discount Rate | 8% | Based on company WACC from recent analysis |

| Tax Rate | 25% | Current statutory corporate tax rate |

| Market Growth Rate | 4% | Industry forecast from market research |

Best Practices for Defining Outputs

- Organize outputs logically: Group outputs by financial statements or KPIs.

- Use clear labels and formatting: Highlight output cells with a distinct color (e.g., green).

- Link outputs to inputs and assumptions: Ensure outputs dynamically update when inputs or assumptions change.

- Include summary dashboards: Visualize key outputs for quick interpretation.

Example: Output Snapshot

| Output Metric | 2024 Forecast | 2025 Forecast | Notes |

|---|---|---|---|

| Revenue | 1,260,000 | 1,323,000 | Calculated using sales growth |

| Gross Profit | 756,000 | 793,800 | Revenue minus cost of goods sold |

| Net Income | 189,000 | 198,450 | After tax and expenses |

Mind Map: Workflow from Inputs to Outputs

Integrated Example: Simple Revenue Forecast Model

-

Inputs:

- Historical Sales: $1,000,000

- Sales Growth Rate: 6%

-

Assumptions:

- Growth rate remains constant for 3 years

-

Outputs:

- Year 1 Revenue = Historical Sales * (1 + Growth Rate) = $1,060,000

- Year 2 Revenue = Year 1 Revenue * (1 + Growth Rate) = $1,123,600

- Year 3 Revenue = Year 2 Revenue * (1 + Growth Rate) = $1,191,016

This simple example illustrates how clearly defined inputs and assumptions feed into outputs that update dynamically.

Summary Checklist

- Separate inputs, assumptions, and outputs into distinct sections or sheets.

- Use consistent and intuitive formatting to differentiate components.

- Document assumptions with clear rationale.

- Validate inputs to reduce errors.

- Link outputs dynamically to inputs and assumptions.

- Use mind maps or flowcharts to visualize relationships.

By following these practices, accountants can build financial models that are transparent, flexible, and easy to maintain.

2.3 Best Practice: Designing a Logical and Modular Model Structure

Designing a logical and modular structure is fundamental to building effective financial models. A well-structured model is easier to understand, update, audit, and scale. It reduces errors and improves collaboration among accountants and financial analysts.

Why Modular Structure Matters

- Clarity: Separates inputs, calculations, and outputs for easy navigation.

- Flexibility: Allows individual sections to be updated without affecting the entire model.

- Error Reduction: Isolates errors to specific modules.

- Reusability: Modules can be reused across different models or projects.

Core Principles of Logical and Modular Modelling

-

Segregate Inputs, Calculations, and Outputs

- Inputs: Raw data and assumptions.

- Calculations: Processing logic and formulas.

- Outputs: Reports, summaries, and dashboards.

-

Use Separate Worksheets or Sections

- Clearly label each sheet/tab (e.g., “Inputs”, “Calculations”, “Outputs”).

-

Consistent Naming Conventions

- Use descriptive names for sheets, ranges, and variables.

-

Avoid Hardcoding Values in Formulas

- Reference input cells instead of embedding numbers directly.

-

Build in Checks and Balances

- Include error checks and reconciliation modules.

-

Document Assumptions and Logic

- Use comments and a dedicated assumptions sheet.

Mind Map: Logical and Modular Model Structure

Example: Modular Structure in Practice

Imagine you are building a financial model for a mid-size tech company. Here’s how you might organize it:

| Worksheet Name | Purpose |

|---|---|

| Inputs | All raw data and assumptions (e.g., sales growth, cost percentages) |

| Revenue Forecast | Calculation of projected revenues based on inputs and historical trends |

| Expense Forecast | Breakdown of fixed and variable expenses calculations |

| Working Capital | Calculations related to receivables, payables, and inventory |

| Depreciation & Tax | Depreciation schedules and tax computations |

| Financial Statements | Consolidated Income Statement, Balance Sheet, and Cash Flow Statement |

| Ratios & KPIs | Key financial ratios and performance indicators |

| Checks | Error checks, balance reconciliations, and validation formulas |

| Documentation | Explanation of assumptions, version notes, and model instructions |

Example Walkthrough: Revenue Forecast Module

-

Inputs Sheet:

- Sales growth rate: 10%

- Historical sales data for 3 years

-

Revenue Forecast Sheet:

- Formula references sales growth from Inputs

- Calculates Year 1 Revenue = Last Year Historical Sales * (1 + Sales Growth Rate)

- Extends forecast for 5 years

-

Benefits:

- Easy to update growth assumptions in one place

- Revenue calculations are isolated, making troubleshooting straightforward

Visual Mind Map for Revenue Forecast Module

Tips for Implementation

- Use color coding to differentiate inputs (e.g., blue), calculations (black), and outputs (green).

- Lock or protect sheets that contain formulas to prevent accidental changes.

- Regularly review and refactor the model structure as complexity grows.

- Use named ranges for key inputs to improve formula readability.

By adhering to these best practices and modular design principles, accountants can create financial models that are robust, transparent, and easy to maintain — ultimately supporting better financial decision-making.

2.4 Example: Structuring a Profit and Loss Forecast Model

Creating a well-structured Profit and Loss (P&L) forecast model is a foundational skill for accountants. This section will guide you through the step-by-step process of structuring a P&L forecast model with clear best practices and illustrative examples, supported by mind maps to visualize the model’s architecture.

Understanding the P&L Forecast Model Structure

A P&L forecast model projects revenues, costs, and expenses over a future period to estimate profitability. The model typically includes the following components:

- Revenue Streams

- Cost of Goods Sold (COGS)

- Gross Profit

- Operating Expenses

- Operating Profit (EBIT)

- Interest, Taxes

- Net Profit

Mind Map: High-Level Structure of a P&L Forecast Model

Step 1: Define Inputs and Assumptions

Best Practice: Separate all inputs and assumptions on a dedicated worksheet or clearly defined input section. This makes the model easier to update and audit.

Example Inputs:

| Parameter | Value | Description |

|---|---|---|

| Sales Growth Rate | 8% | Annual growth in sales revenue |

| COGS as % of Revenue | 55% | Cost of goods sold percentage |

| Operating Expenses | $50,000 | Fixed operating expenses per year |

| Tax Rate | 25% | Corporate tax rate |

Step 2: Project Revenue

Use historical data and growth assumptions to forecast revenue.

Example:

| Year | 2023 | 2024 | 2025 |

|---|---|---|---|

| Revenue | $500,000 | $540,000 | $583,200 |

Calculation:

Revenue_2024 = Revenue_2023 * (1 + Sales Growth Rate) = 500,000 * 1.08 = 540,000

Step 3: Calculate Cost of Goods Sold (COGS)

COGS is typically a percentage of revenue.

Example:

| Year | 2023 | 2024 | 2025 |

|---|---|---|---|

| Revenue | $500,000 | $540,000 | $583,200 |

| COGS (%) | 55% | 55% | 55% |

| COGS | $275,000 | $297,000 | $320,760 |

Calculation:

COGS_2024 = Revenue_2024 * COGS % = 540,000 * 0.55 = 297,000

Step 4: Compute Gross Profit

Gross Profit = Revenue - COGS

Example:

| Year | 2023 | 2024 | 2025 |

|---|---|---|---|

| Revenue | $500,000 | $540,000 | $583,200 |

| COGS | $275,000 | $297,000 | $320,760 |

| Gross Profit | $225,000 | $243,000 | $262,440 |

Step 5: Include Operating Expenses

Operating expenses can be fixed or variable. For simplicity, assume fixed expenses.

Example:

| Year | 2023 | 2024 | 2025 |

|---|---|---|---|

| Operating Expenses | $50,000 | $50,000 | $50,000 |

Step 6: Calculate Operating Profit (EBIT)

EBIT = Gross Profit - Operating Expenses

Example:

| Year | 2023 | 2024 | 2025 |

|---|---|---|---|

| Gross Profit | $225,000 | $243,000 | $262,440 |

| Operating Exp | $50,000 | $50,000 | $50,000 |

| EBIT | $175,000 | $193,000 | $212,440 |

Step 7: Account for Interest and Taxes

Assume interest expense is zero for this example.

Tax Expense = EBIT * Tax Rate

Example:

| Year | 2023 | 2024 | 2025 |

|---|---|---|---|

| EBIT | $175,000 | $193,000 | $212,440 |

| Tax Rate | 25% | 25% | 25% |

| Tax Expense | $43,750 | $48,250 | $53,110 |

Step 8: Calculate Net Profit

Net Profit = EBIT - Tax Expense

Example:

| Year | 2023 | 2024 | 2025 |

|---|---|---|---|

| EBIT | $175,000 | $193,000 | $212,440 |

| Tax Expense | $43,750 | $48,250 | $53,110 |

| Net Profit | $131,250 | $144,750 | $159,330 |

Mind Map: Detailed P&L Forecast Model Flow

Best Practices Highlighted in This Example

- Separation of Inputs: All assumptions are centralized to allow easy updates without digging through formulas.

- Modular Calculations: Each step builds logically on the previous one, making the model easy to audit and troubleshoot.

- Use of Clear Labels: Tables and sections are clearly labeled for readability.

- Scenario Flexibility: By changing input assumptions (e.g., sales growth or COGS %), the entire forecast updates dynamically.

Summary

Structuring a P&L forecast model involves clearly defining inputs, logically sequencing calculations, and presenting outputs in an understandable format. Using mind maps helps visualize the model’s architecture, ensuring no component is overlooked. This approach not only improves accuracy but also enhances communication with stakeholders.

Next Steps: In the following sections, we will explore how to link this P&L forecast model with balance sheet and cash flow models to create a comprehensive financial model.

2.5 Documenting Assumptions and Sources for Transparency

In financial modelling, documenting assumptions and sources is a critical best practice that ensures transparency, facilitates model auditing, and enhances stakeholder confidence. Clear documentation helps users understand the rationale behind the numbers, enables easier updates, and reduces the risk of errors or misinterpretations.

Why Document Assumptions and Sources?

- Transparency: Stakeholders can trace back figures to their origins.

- Auditability: Facilitates internal and external reviews.

- Update Efficiency: Simplifies model adjustments when assumptions change.

- Credibility: Builds trust in the model’s outputs.

Best Practices for Documenting Assumptions

-

Create a Dedicated Assumptions Sheet:

- Centralize all key assumptions in one place.

- Use clear labels and organize by category (e.g., revenue, costs, growth rates).

-

Use Comments and Notes:

- Add cell comments explaining the source or reasoning.

- Highlight assumptions that are estimates or require validation.

-

Link to External Sources:

- Include hyperlinks or references to reports, databases, or websites.

- Store copies of key documents in a shared folder for easy access.

-

Version Control:

- Track changes to assumptions over time.

- Maintain a change log with dates and reasons.

-

Use Consistent Formatting:

- Differentiate assumptions from calculated outputs using color coding.

- Use data validation to restrict input types.

Mind Map: Documenting Assumptions and Sources

Example 1: Assumptions Sheet Layout

| Assumption Category | Description | Value | Source/Notes |

|---|---|---|---|

| Revenue Growth | Annual revenue growth rate | 8% | Historical CAGR from 2018-2023 (Company Annual Report) |

| Cost Inflation | Annual cost inflation rate | 3% | Based on Consumer Price Index forecast (Bureau of Labor Statistics) |

| Tax Rate | Corporate tax rate | 25% | Current statutory tax rate as per government website |

| Discount Rate | Weighted Average Cost of Capital (WACC) | 10% | Calculated using CAPM model; see Appendix A |

Note: Each value is linked to a source or explanation, making it easy for reviewers to verify assumptions.

Example 2: Using Cell Comments for Transparency

In Excel, you can right-click a cell containing an assumption and add a comment like:

“Source: IMF World Economic Outlook, April 2024. Assumption based on projected GDP growth for relevant region.”

This comment appears when hovering over the cell, providing immediate context without cluttering the sheet.

Example 3: Change Log for Assumptions

| Date | Assumption | Previous Value | New Value | Reason for Change | Updated By |

|---|---|---|---|---|---|

| 2024-05-01 | Revenue Growth | 7% | 8% | Updated based on latest quarterly results | J. Smith |

| 2024-05-15 | Discount Rate | 9.5% | 10% | Revised WACC after new debt issuance | A. Lee |

Maintaining this log helps track the evolution of the model and supports transparency.

Mind Map: Example Workflow for Documenting Assumptions

Summary

Documenting assumptions and sources is not just a formality but a foundational element of robust financial modelling. By centralizing assumptions, linking to credible sources, using clear notes, and maintaining version control, accountants and financial analysts can build models that are transparent, reliable, and easy to maintain.

Next up: 2.6 Using Flowcharts and Diagrams to Map Model Logic

2.6 Using Flowcharts and Diagrams to Map Model Logic

Financial modelling can quickly become complex, especially when dealing with multiple interconnected components such as revenues, expenses, financing, and forecasting assumptions. Using flowcharts and diagrams to map out your model logic before or during the build process can significantly improve clarity, reduce errors, and enhance communication with stakeholders.

Why Use Flowcharts and Diagrams?

- Visual Clarity: They provide a visual representation of how different parts of the model interact.

- Error Reduction: Mapping logic helps identify potential circular references or missing links.

- Improved Collaboration: Stakeholders and team members can understand the model’s structure without diving into formulas.

- Documentation: Acts as a reference for future updates or audits.

Common Diagram Types for Financial Modelling

- Flowcharts: Show the sequence of calculations or processes.

- Mind Maps: Illustrate relationships between assumptions, inputs, calculations, and outputs.

- Data Flow Diagrams: Highlight how data moves through the model.

Example Mind Map: Revenue Forecast Model

Revenue Forecast Model Mind Map

This mind map breaks down the revenue forecast into inputs, calculations, and outputs, helping you organize your model logically.

Example Flowchart: Profit & Loss Statement Logic

Profit & Loss Statement Flowchart

graph TD;

A0[Start] --> A1[Input Revenue Data] --> A2[Calculate Cost of Goods Sold] --> A3[Compute Gross Profit] --> A4[Calculate Operating Expenses] --> A5[Compute Operating Income] --> A6[Calculate Interest and Taxes] --> A7[Compute Net Income] --> A8[End]

This linear flowchart shows the step-by-step calculation process in the P&L statement, ensuring each step feeds correctly into the next.

Detailed Mind Map: Comprehensive Financial Model Structure

Comprehensive Financial Model Mind Map

This mind map helps visualize the entire model’s architecture, making it easier to assign responsibilities and track dependencies.

Practical Tips for Creating Flowcharts and Diagrams

- Start Simple: Begin with high-level components before drilling down into details.

- Use Consistent Symbols: For example, rectangles for processes, diamonds for decision points.

- Leverage Software Tools: Use tools like Microsoft Visio, Lucidchart, or even Excel’s SmartArt for creating diagrams.

- Integrate with Documentation: Embed diagrams within your model documentation or Excel sheets.

- Update Regularly: Keep diagrams current as the model evolves.

Example: Creating a Flowchart in Excel

- Go to the Insert tab.

- Select Shapes and choose flowchart symbols (e.g., Process, Decision).

- Arrange shapes to represent the model logic.

- Use arrows to indicate flow direction.

- Add text to describe each step.

This simple approach allows accountants to create quick visual guides without needing specialized software.

Summary

Using flowcharts and diagrams to map your financial model logic is a best practice that enhances understanding, reduces errors, and improves communication. By visually organizing inputs, calculations, and outputs, you create a blueprint that guides model construction and review.

Start incorporating these visual tools early in your modelling process to build more robust and transparent financial models.

3. Data Collection and Input Management

3.1 Identifying Reliable Data Sources for Financial Models

Reliable data is the backbone of any robust financial model. As accountants and financial analysts, ensuring the integrity, accuracy, and relevance of your data sources is critical to building trustworthy models that drive sound business decisions.

Why Reliable Data Sources Matter

- Accuracy: Incorrect data leads to flawed forecasts and poor decision-making.

- Consistency: Consistent data allows for meaningful trend analysis and comparisons.

- Transparency: Knowing your data sources builds confidence among stakeholders.

Types of Data Sources for Financial Models

Internal Data Sources

-

Accounting Systems (e.g., QuickBooks, SAP, Oracle Financials):

- Provide detailed transactional data, general ledger entries, and trial balances.

- Example: Extracting monthly revenue and expense data directly from your ERP ensures accuracy and timeliness.

-

Historical Financial Statements:

- Past income statements, balance sheets, and cash flow statements form the foundation for trend analysis and forecasting.

- Example: Using the last 3 years of audited financials to establish baseline assumptions for revenue growth.

-

Customer Relationship Management (CRM) Systems:

- Useful for sales pipeline data, customer segmentation, and churn rates.

- Example: Pulling sales forecast data from Salesforce to estimate future revenues.

External Data Sources

-

Market Data Providers:

- Sources like Yahoo Finance, Google Finance, or specialized providers offer stock prices, market indices, and commodity prices.

- Example: Using historical stock price data to model cost of equity or beta in a valuation model.

-

Government Publications:

- Economic data such as inflation rates, unemployment figures, and GDP growth from agencies like the Bureau of Economic Analysis (BEA) or the Federal Reserve.

- Example: Incorporating inflation forecasts from government reports to adjust expense projections.

-

Industry Reports:

- Published by consulting firms (e.g., McKinsey, Deloitte) or industry associations, these reports provide benchmarks and market trends.

- Example: Using industry average profit margins to validate your company’s projected margins.

-

Competitor Financials:

- Publicly available financial statements of competitors can provide valuable benchmarking data.

- Example: Comparing your company’s revenue growth rate against competitors to assess reasonableness.

Third-Party Data Sources

-

Financial Databases (Bloomberg, Reuters, Capital IQ):

- Comprehensive datasets including financials, market data, and news.

- Example: Pulling credit ratings and debt maturity schedules for debt modelling.

-

Credit Rating Agencies (Moody’s, S&P):

- Provide credit risk assessments and outlooks.

- Example: Using credit ratings to estimate borrowing costs.

-

Analyst Reports:

- Equity research reports offer forecasts, valuation multiples, and qualitative insights.

- Example: Incorporating consensus analyst revenue growth estimates.

-

News Feeds and Press Releases:

- Timely information on company events, regulatory changes, or market disruptions.

- Example: Adjusting forecasts based on announced mergers or regulatory fines.

Best Practices for Selecting Data Sources

- Verify Authenticity: Always confirm the credibility of the source.

- Check Timeliness: Use the most recent data available to maintain relevance.

- Cross-Reference: Validate data by comparing multiple sources where possible.

- Document Sources: Maintain a data log for transparency and audit trails.

Example: Selecting Data Sources for a Revenue Forecast Model

| Data Type | Source | Purpose | Notes |

|---|---|---|---|

| Historical Sales Data | Internal ERP System | Base revenue figures | Extract monthly sales for last 3 years |

| Market Growth Rates | Industry Reports (Deloitte) | Benchmark revenue growth | Use to validate internal growth assumptions |

| Economic Indicators | Government Publications (BEA) | Adjust for macroeconomic impact | Incorporate GDP growth and inflation |

| Competitor Performance | Public Financial Statements | Competitive benchmarking | Compare revenue growth and margins |

Summary

Identifying and leveraging reliable data sources is essential for building accurate and credible financial models. Combining internal data with well-vetted external and third-party sources ensures your models reflect reality and provide actionable insights.

Next up: 3.2 Best Practice: Creating Input Sheets for Easy Updates

3.2 Best Practice: Creating Input Sheets for Easy Updates

Creating well-structured input sheets is a cornerstone of effective financial modelling. Input sheets serve as the centralized location where all assumptions, historical data, and variables are entered. This approach not only simplifies updates but also reduces the risk of errors and enhances model transparency.

Why Use Dedicated Input Sheets?

- Centralization: All key assumptions and data points are in one place.

- Ease of Updates: Changing assumptions does not require hunting through complex formulas.

- Error Reduction: Minimizes accidental overwrites of formulas.

- Auditability: Facilitates review and validation by others.

- Scenario Management: Enables quick switching between different sets of assumptions.

Key Principles for Designing Input Sheets

- Clear Labeling: Use descriptive labels for each input.

- Consistent Formatting: Use consistent font, colors, and cell styles.

- Data Validation: Restrict inputs to valid ranges or lists.

- Separation of Inputs and Calculations: Avoid mixing inputs with formulas.

- Use of Named Ranges: Assign names to key inputs for easier formula referencing.

- Documentation: Include comments or notes explaining each input.

Mind Map: Structure of an Effective Input Sheet

Example: Simple Input Sheet Layout

| Parameter | Value | Description |

|---|---|---|

| Revenue Growth Rate | 5% | Annual expected revenue increase |

| Cost Inflation Rate | 3% | Expected increase in costs |

| Tax Rate | 25% | Corporate tax rate |

| Initial Sales (Units) | 10,000 | Units sold in the base year |

- Use blue fill color for input cells to visually distinguish them.

- Lock formula cells to prevent accidental edits.

Mind Map: Input Sheet Best Practices

Example: Using Data Validation for Input Control

- For the “Tax Rate” cell, restrict input to between 0% and 50%.

- For “Scenario” selection, create a drop-down list with options: Base, Optimistic, Pessimistic.

Steps in Excel:

- Select the input cell.

- Go to Data > Data Validation.

- Choose “Decimal” between 0 and 0.5 for tax rate.

- For scenario, select “List” and enter options separated by commas.

Example: Named Ranges for Inputs

- Define named ranges such as

RevenueGrowth,CostInflation, andTaxRate. - Use these names in formulas instead of cell references, e.g.,

=InitialSales * (1 + RevenueGrowth).

This improves formula readability and makes model updates easier.

Mind Map: Linking Input Sheet to Model Calculations

Summary

Creating a dedicated input sheet with clear structure, data validation, and documentation is a best practice that enhances the usability, accuracy, and maintainability of financial models. By applying these principles, accountants can ensure their models remain flexible and reliable as assumptions evolve.

3.3 Handling Historical Data: Cleaning and Validation Techniques

Historical data forms the backbone of any reliable financial model. Accurate, clean, and validated historical data ensures that forecasts and analyses are based on solid foundations. In this section, we will explore best practices for cleaning and validating historical financial data, accompanied by practical examples and mind maps to visualize the process.

Why Clean and Validate Historical Data?

- Accuracy: Prevents errors from propagating into forecasts.

- Consistency: Ensures data follows uniform formats and standards.

- Reliability: Builds confidence in model outputs.

Common Issues in Historical Data

- Missing values

- Duplicates

- Inconsistent formats (dates, currencies)

- Outliers and anomalies

- Incorrect or outdated entries

Mind Map: Historical Data Cleaning Process

Step 1: Handling Missing Values

Techniques:

- Deletion: Remove rows or columns with excessive missing data.

- Imputation: Fill missing values using:

- Mean or median of the column

- Forward fill (previous period’s value)

- Domain-specific assumptions

Example: A sales dataset has missing monthly sales figures for February 2023.

- Forward fill from January 2023 sales: If January sales were $100,000, use $100,000 for February.

- Alternatively, use the average sales of January and March.

Step 2: Removing Duplicates

Duplicates can distort totals and averages.

Example: Two identical expense entries for $5,000 in March 2023 found in the dataset.

- Use Excel’s

Remove Duplicatesfeature or SQLDISTINCTclause to eliminate duplicates.

Step 3: Standardizing Formats

Dates: Convert all date entries to a consistent format (e.g., ISO 8601 YYYY-MM-DD).

Currency: Ensure all monetary values are in the same currency and format.

Example:

A dataset contains dates in MM/DD/YYYY and DD-MM-YYYY formats.

- Use Excel’s

DATEVALUEor Power Query to standardize.

Step 4: Detecting Outliers

Outliers can indicate data entry errors or genuine anomalies.

Techniques:

- Statistical methods: Z-score, IQR (Interquartile Range)

- Visual methods: Box plots, scatter plots

Example: A reported expense of $1,000,000 in a category where typical expenses range between $10,000-$50,000.

- Investigate source documents or flag for review.

Step 5: Data Validation

Validation Rules:

- Data type checks (e.g., numbers in numeric fields)

- Range checks (e.g., percentages between 0 and 100)

- Cross-validation with external reports or trial balances

Example: Validate that total assets equal total liabilities plus equity in the balance sheet data.

Mind Map: Data Validation Techniques

Practical Example: Cleaning a Historical Sales Dataset

| Date | Sales Amount | Currency | Notes |

|---|---|---|---|

| 01/15/2023 | 100000 | USD | |

| 02/15/2023 | USD | Missing value | |

| 03/15/2023 | 105000 | USD | |

| 03/15/2023 | 105000 | USD | Duplicate entry |

| 04-15-2023 | 110000 | USD | Different date format |

Cleaning Steps:

- Impute missing February sales using average of January and March: (100,000 + 105,000)/2 = 102,500

- Remove duplicate March 15 entry

- Standardize April date to

2023-04-15

Result:

| Date | Sales Amount | Currency | Notes |

|---|---|---|---|

| 2023-01-15 | 100000 | USD | |

| 2023-02-15 | 102500 | USD | Imputed value |

| 2023-03-15 | 105000 | USD | |

| 2023-04-15 | 110000 | USD | Standardized date |

Summary

Cleaning and validating historical data is critical for building trustworthy financial models. By systematically addressing missing values, duplicates, format inconsistencies, outliers, and validation checks, accountants can ensure their models are robust and reliable.

Adopting these best practices will reduce errors, improve forecasting accuracy, and enhance stakeholder confidence in your financial analyses.

3.4 Example: Input Sheet for Sales and Expense Data

Creating a well-structured input sheet is a cornerstone of effective financial modelling. It ensures data consistency, ease of updates, and reduces the risk of errors. In this section, we will walk through an example of designing an input sheet specifically for sales and expense data, incorporating best practices and clear examples.

Key Objectives for the Input Sheet:

- Centralize all raw data inputs in one dedicated sheet.

- Use clear labels and organized layout.

- Separate assumptions from actual data.

- Implement data validation to minimize input errors.

- Use consistent formatting for ease of reading.

Mind Map: Structure of an Input Sheet for Sales and Expense Data

Step-by-Step Example: Building the Input Sheet

Define Sales Data Inputs

| Parameter | Description | Example Value | Notes |

|---|---|---|---|

| Product Category | Type of product sold | Electronics | Dropdown list for consistency |

| Month | Reporting month | Jan 2024 | Use date format |

| Sales Volume | Number of units sold | 1,000 | Numeric input only |

| Unit Price | Price per unit | $150 | Currency format |

| Growth Rate | Expected monthly growth rate (%) | 2% | Input as decimal or percentage |

Define Expense Data Inputs

| Parameter | Description | Example Value | Notes |

|---|---|---|---|

| Expense Type | Category of expense | Rent | Dropdown list recommended |

| Month | Reporting month | Jan 2024 | Consistent with sales data |

| Amount | Expense amount | $5,000 | Currency format |

| Inflation Rate | Expected inflation on expenses | 1.5% | Used for forecasting |

Example Input Sheet Layout (Simplified)

| Sales Inputs | ||||

|---|---|---|---|---|

| Month | Product Category | Sales Volume | Unit Price | Growth Rate |

| Jan 2024 | Electronics | 1,000 | $150 | 2% |

| Feb 2024 | Electronics | 1,020 | $150 | 2% |

| Expense Inputs | ||||

|---|---|---|---|---|

| Month | Expense Type | Amount | Inflation Rate | |

| Jan 2024 | Rent | $5,000 | 1.5% | |

| Jan 2024 | Marketing | $2,000 | 1.5% |

Best Practices Demonstrated in This Example

-

Use of Dropdown Lists: For fields like Product Category and Expense Type, dropdown menus reduce errors and standardize inputs.

-

Consistent Time Periods: Aligning months across sales and expense data simplifies linking and aggregation.

-

Separation of Assumptions: Growth rates and inflation rates are input separately to allow easy scenario adjustments.

-

Clear Formatting: Currency and percentage formats help users understand the data type at a glance.

-

Documentation: Adding comments or notes in cells can guide users on expected inputs.

Additional Mind Map: Data Validation and Error Prevention

Example: Implementing a Dropdown List in Excel

- Select the cells under ‘Product Category’.

- Go to Data > Data Validation.

- Choose ‘List’ and input the categories: Electronics, Software, Services.

- Click OK.

This ensures only valid product categories are entered.

Summary

An input sheet designed with clarity, validation, and modularity in mind forms the foundation for reliable financial models. By organizing sales and expense data systematically and incorporating best practices like dropdowns and consistent formatting, accountants can build models that are easy to update, audit, and communicate.

3.5 Using Data Validation and Drop-down Lists to Minimize Errors

In financial modelling, accuracy and consistency of input data are critical. One common source of errors is manual data entry, which can lead to typos, inconsistent formats, or invalid values. To minimize these errors, Excel offers powerful features such as Data Validation and Drop-down Lists that restrict inputs to predefined criteria, ensuring data integrity and improving model reliability.

What is Data Validation?

Data Validation is a feature in Excel that allows you to control the type of data or the values that users can enter into a cell. It helps prevent invalid data entry by setting rules such as:

- Restricting input to numbers within a range

- Allowing only dates within a specific timeframe

- Limiting text length

- Providing a list of acceptable values via drop-down menus

Benefits of Using Data Validation and Drop-down Lists

- Error Reduction: Prevents users from entering invalid or inconsistent data.

- Standardization: Ensures uniform data formats and values.

- User Guidance: Makes it easier for users to input data correctly.

- Improved Model Integrity: Reduces the risk of model breakage due to unexpected inputs.

How to Create a Drop-down List Using Data Validation

-

Prepare the List of Valid Entries:

- Create a list of acceptable values in a separate range or worksheet.

- Example: A list of departments – “Sales”, “Marketing”, “Finance”, “IT”.

-

Select the Input Cells:

- Highlight the cells where you want to restrict input.

-

Apply Data Validation:

- Go to the Data tab → Data Validation → Data Validation.

- In the Settings tab, choose List under Allow.

- In the Source box, select the range containing your list.

- Click OK.

-

Test the Drop-down:

- Click on the validated cell and select from the drop-down list.

Example: Creating a Drop-down List for Expense Categories

Suppose you are building an expense input sheet and want to restrict the “Category” column to predefined options.

-

Step 1: In a separate sheet named “Lists”, enter the categories in cells A1:A5:

- Travel

- Office Supplies

- Salaries

- Marketing

- Utilities

-

Step 2: Select the “Category” column in your expense input sheet.

-

Step 3: Apply Data Validation with the source as

=Lists!$A$1:$A$5. -

Step 4: Now users can only select one of the five categories, reducing input errors.

Mind Map: Data Validation and Drop-down Lists

Advanced Tips

-

Dynamic Drop-down Lists: Use Excel tables or OFFSET formulas to create drop-down lists that automatically update when you add new items.

-

Dependent Drop-down Lists: Create cascading drop-downs where the selection in one list filters the options in another. For example, selecting a country filters the list of cities.

-

Custom Error Messages: Customize error alerts to provide clear instructions when invalid data is entered.

-

Input Messages: Display helpful messages when a user selects a cell to guide correct data entry.

Example: Custom Error Message Setup

- When setting up Data Validation, go to the Error Alert tab.

- Choose Stop style to prevent invalid entries.

- Enter a title like “Invalid Entry” and a message such as “Please select a category from the drop-down list.”

This helps users understand what went wrong and how to fix it.

Summary

Using Data Validation and Drop-down Lists is a best practice in financial modelling to ensure data accuracy and consistency. By restricting inputs to valid options, accountants and financial analysts can reduce errors, save time on data cleaning, and build more robust models.

Quick Reference Table

| Feature | Purpose | Example Use Case |

|---|---|---|

| Data Validation - List | Restrict input to predefined options | Expense categories |

| Data Validation - Date | Allow only dates within a range | Project start/end dates |

| Input Message | Guide users on valid input | “Select a department from list” |

| Error Alert | Prevent invalid data entry | Custom error message on invalid category |

By integrating these techniques into your financial models, you enhance data quality and reduce the risk of costly mistakes.

3.6 Automating Data Imports with Excel and Other Tools

Automating data imports is a critical step in financial modelling, especially for accountants and financial analysts who deal with large volumes of data from multiple sources. Automation reduces manual errors, saves time, and ensures your model is always up-to-date with the latest information.

Why Automate Data Imports?

- Accuracy: Minimizes human error during data entry.

- Efficiency: Saves hours of manual work.

- Consistency: Ensures data is imported in a uniform format.

- Scalability: Handles large datasets effortlessly.

Common Data Sources for Financial Models

- Excel files (internal reports, historical data)

- CSV files (exported from accounting software)

- Databases (SQL Server, Access)

- Web data (stock prices, exchange rates)

- ERP and accounting systems (SAP, Oracle, QuickBooks)

Tools and Techniques for Automating Data Imports

Excel’s Built-in Features

- Power Query: A powerful ETL (Extract, Transform, Load) tool integrated into Excel that allows you to import, clean, and transform data from various sources.

- Data Connections: Link Excel directly to external databases or files.

- Macros/VBA: Automate repetitive import tasks with custom scripts.

Third-Party Tools

- Microsoft Power BI: For advanced data integration and visualization.

- Python Scripts: Using libraries like

pandasandopenpyxlto automate data extraction and transformation. - R Programming: For statistical data processing and automation.

Mind Map: Automating Data Imports Workflow

Step-by-Step Example: Automating Data Import Using Power Query

Scenario: Import monthly sales data from a CSV file into your financial model.

- Open Excel and go to the Data tab.

- Click on Get Data > From File > From Text/CSV.

- Select your CSV file and click Import.

- Power Query Editor opens showing a preview of your data.

- Apply transformations if needed (e.g., change data types, remove columns).

- Click Close & Load to import data into a new worksheet.

- To refresh data when the CSV updates, simply click Refresh All in the Data tab.

Best Practice: Save your Power Query steps so you can reuse or modify them easily when data sources change.

Example: Automating Data Import Using VBA Macro

Sub ImportCSV()

Dim ws As Worksheet

Dim csvPath As String

csvPath = "C:\Data\MonthlySales.csv"

Set ws = ThisWorkbook.Sheets("SalesData")

ws.Cells.Clear

With ws.QueryTables.Add(Connection:="TEXT;" & csvPath, Destination:=ws.Range("A1"))

.TextFileParseType = xlDelimited

.TextFileCommaDelimiter = True

.Refresh BackgroundQuery:=False

End With

MsgBox "CSV Data Imported Successfully"

End Sub

This macro clears the existing data in the “SalesData” sheet and imports fresh data from the specified CSV file. Running this macro automates the import process with a single click.

Mind Map: VBA Automation for Data Import

Integrating Data from Databases Using Excel Data Connections

- Go to Data > Get Data > From Database.

- Choose your database type (e.g., SQL Server).

- Enter server and database credentials.

- Select the required tables or write a SQL query.

- Load data directly into Excel.

- Refresh data as needed.

Example: Importing a trial balance from a SQL database into your model for real-time updates.

Automating Web Data Imports

Using Power Query, you can import data from web pages such as stock prices or exchange rates:

- Go to Data > Get Data > From Other Sources > From Web.

- Enter the URL of the web page.

- Select the relevant table or data element.

- Load data into Excel.

Example: Automatically importing daily currency exchange rates for currency conversion in your financial model.

Tips for Effective Automation

- Always validate imported data for accuracy.

- Use named ranges and structured tables to simplify referencing.

- Document your data import process within the model.

- Schedule regular refreshes if using tools like Power BI or Excel Online.

- Backup your model before applying automation scripts.

By integrating these automation techniques into your financial modelling workflow, you can significantly improve the reliability and efficiency of your models, allowing you to focus more on analysis and decision-making rather than manual data handling.

4. Building Core Financial Statements in the Model

4.1 Constructing the Income Statement: Step-by-Step

The income statement, also known as the profit and loss statement, is a fundamental financial report that summarizes a company’s revenues, expenses, and profits over a specific period. For accountants, constructing an accurate income statement within a financial model is essential to assess profitability and support decision-making.

Step 1: Understand the Structure of the Income Statement

The income statement typically follows this structure:

- Revenue (Sales)

- Cost of Goods Sold (COGS)

- Gross Profit (Revenue - COGS)

- Operating Expenses (Selling, General & Administrative Expenses, Depreciation, etc.)

- Operating Income (EBIT) (Gross Profit - Operating Expenses)

- Other Income and Expenses (Interest, Gains/Losses)

- Pre-Tax Income

- Income Tax Expense

- Net Income

Step 2: Define Inputs and Assumptions

Before building the income statement, gather the following inputs:

- Historical sales data or forecasted sales volumes and prices

- Cost structure details (variable and fixed costs)

- Operating expenses estimates

- Tax rates

- Interest expenses or income

Step 3: Build the Revenue Section

Start by projecting revenues. For example, if you forecast sales volume and price:

Mind Map: Revenue Calculation

Example:

| Month | Units Sold | Price per Unit | Revenue |

|---|---|---|---|

| Jan | 1,000 | $50 | $50,000 |

| Feb | 1,200 | $50 | $60,000 |

Formula in Excel: =Units_Sold * Price_per_Unit

Step 4: Calculate Cost of Goods Sold (COGS)

COGS represents the direct costs attributable to the production of goods sold.

Mind Map: COGS Components

Example:

If direct materials cost $20 per unit and direct labor is $10 per unit:

| Month | Units Sold | Direct Materials | Direct Labor | Total COGS |

|---|---|---|---|---|

| Jan | 1,000 | $20,000 | $10,000 | $30,000 |

Formula: =Units_Sold * (Direct_Materials_per_Unit + Direct_Labor_per_Unit)

Step 5: Compute Gross Profit

Gross Profit = Revenue - COGS

Example:

| Month | Revenue | COGS | Gross Profit |

|---|---|---|---|

| Jan | $50,000 | $30,000 | $20,000 |

Step 6: Estimate Operating Expenses

Operating expenses include selling, general & administrative expenses (SG&A), depreciation, and other operating costs.

Mind Map: Operating Expenses

Example:

| Expense Type | Monthly Cost |

|---|---|

| Selling Expenses | $5,000 |

| General Admin | $3,000 |

| Depreciation | $2,000 |

| Total | $10,000 |

Step 7: Calculate Operating Income (EBIT)

Operating Income = Gross Profit - Operating Expenses

Example:

| Month | Gross Profit | Operating Expenses | Operating Income |

|---|---|---|---|

| Jan | $20,000 | $10,000 | $10,000 |

Step 8: Include Other Income and Expenses

Add interest income or expense, gains or losses from non-operating activities.

Example:

| Item | Amount |

|---|---|

| Interest Expense | -$1,000 |

| Other Income | $500 |

| Net Other Income | -$500 |

Step 9: Calculate Pre-Tax Income

Pre-Tax Income = Operating Income + Net Other Income

Example:

| Month | Operating Income | Net Other Income | Pre-Tax Income |

|---|---|---|---|

| Jan | $10,000 | -$500 | $9,500 |

Step 10: Calculate Income Tax Expense

Apply the tax rate to pre-tax income.

Example:

Assuming a tax rate of 30%:

| Month | Pre-Tax Income | Tax Rate | Income Tax Expense |

|---|---|---|---|

| Jan | $9,500 | 30% | $2,850 |

Formula: =Pre_Tax_Income * Tax_Rate

Step 11: Calculate Net Income

Net Income = Pre-Tax Income - Income Tax Expense

Example:

| Month | Pre-Tax Income | Income Tax Expense | Net Income |

|---|---|---|---|

| Jan | $9,500 | $2,850 | $6,650 |

Summary Mind Map of Income Statement Construction

Mind Map: Income Statement Construction

Best Practices Integrated in This Section

- Modular Design: Separate inputs (sales volume, prices, costs) from calculations for easy updates.

- Use of Named Ranges: Improves formula readability.

- Documentation: Clearly label each section and assumptions.

- Error Checking: Use subtotals and cross-checks (e.g., Gross Profit = Revenue - COGS).

- Dynamic Formulas: Use cell references instead of hardcoding numbers.

By following these steps and integrating the examples and mind maps, accountants can build a clear, flexible, and accurate income statement within their financial models.

4.2 Building the Balance Sheet with Linked Accounts

A balance sheet is a snapshot of a company’s financial position at a specific point in time. It comprises three main sections: Assets, Liabilities, and Equity. Building a balance sheet within a financial model requires careful linking of accounts to ensure accuracy and consistency with other financial statements, especially the Income Statement and Cash Flow Statement.

Key Concepts in Building the Balance Sheet

- Assets: Resources owned by the company (e.g., cash, accounts receivable, inventory, fixed assets).

- Liabilities: Obligations the company owes to others (e.g., accounts payable, loans).

- Equity: Owner’s residual interest in the company after liabilities are deducted from assets.

Best Practice: Linking Accounts Dynamically

Linking balance sheet accounts dynamically means that changes in one part of the model automatically update related accounts. This reduces errors and improves model integrity.

- Link Assets to Operating Activities: For example, accounts receivable should be linked to sales and collections assumptions.

- Link Liabilities to Expenses and Financing: Accounts payable should reflect purchases and payment terms.

- Link Equity to Retained Earnings: Retained earnings should update based on net income and dividends.

Mind Map: Structure of a Linked Balance Sheet

Step-by-Step Example: Building a Linked Balance Sheet

Step 1: Set Up Asset Accounts

| Account | Formula / Link Example |

|---|---|

| Cash | Link to ending cash balance from Cash Flow Statement |

| Accounts Receivable | = Previous AR + Sales on Credit - Collections |

| Inventory | = Previous Inventory + Purchases - Cost of Goods Sold |

| PP&E | = Previous PP&E + Capital Expenditures - Depreciation |

Step 2: Set Up Liability Accounts

| Account | Formula / Link Example |

|---|---|

| Accounts Payable | = Previous AP + Purchases on Credit - Payments |

| Short-term Debt | Link to financing schedule or loan repayment plan |

Step 3: Set Up Equity Accounts

| Account | Formula / Link Example |

|---|---|

| Retained Earnings | = Previous Retained Earnings + Net Income - Dividends |

Mind Map: Linking Retained Earnings

Practical Example in Excel

Suppose you have the following data:

| Period | Sales | Collections | Purchases | Payments | Net Income | Dividends |

|---|---|---|---|---|---|---|

| Jan | 10000 | 9000 | 4000 | 3500 | 2000 | 500 |

| Feb | 12000 | 11000 | 4500 | 4200 | 2500 | 600 |

-

Accounts Receivable (AR) Calculation:

- Jan AR = Previous AR + Sales on Credit - Collections

- If Previous AR = 2000, Jan AR = 2000 + 10000 - 9000 = 3000

-

Accounts Payable (AP) Calculation:

- Jan AP = Previous AP + Purchases - Payments

- If Previous AP = 1500, Jan AP = 1500 + 4000 - 3500 = 2000

-

Retained Earnings Calculation:

- Jan Retained Earnings = Previous RE + Net Income - Dividends

- If Previous RE = 10000, Jan RE = 10000 + 2000 - 500 = 11500

By linking these calculations dynamically in Excel, when sales or payments change, the balance sheet updates automatically.

Tips for Effective Linking

- Use consistent naming conventions for accounts.

- Separate input assumptions from calculations.

- Use cell references instead of hardcoding numbers.

- Regularly audit links using Excel’s formula auditing tools.

Summary

Building a balance sheet with linked accounts ensures your financial model is robust, accurate, and easy to update. By connecting assets, liabilities, and equity accounts to their respective drivers and other financial statements, accountants can create dynamic models that reflect real-time changes and support better decision-making.

4.3 Developing the Cash Flow Statement from Operating Activities

The cash flow statement is a critical financial document that shows how changes in the balance sheet and income affect cash and cash equivalents. The operating activities section specifically reflects the cash generated or used by a company’s core business operations.

Understanding Cash Flow from Operating Activities

Operating cash flow (OCF) starts with net income and adjusts for non-cash items and changes in working capital. This section helps accountants and financial analysts understand the liquidity generated from regular business operations.

Key Components of Cash Flow from Operating Activities

- Net Income: Starting point, derived from the income statement.

- Adjustments for Non-Cash Items: Includes depreciation, amortization, impairment, and provisions.

- Changes in Working Capital: Adjustments for changes in current assets and liabilities such as accounts receivable, inventory, accounts payable.

Mind Map: Components of Operating Cash Flow

Step-by-Step Example: Building Operating Cash Flow

Scenario:

A company reports the following data for the year:

| Item | Amount (USD) |

|---|---|

| Net Income | 120,000 |

| Depreciation Expense | 15,000 |

| Increase in Accounts Receivable | (10,000) |

| Increase in Inventory | (5,000) |

| Increase in Accounts Payable | 8,000 |

Step 1: Start with Net Income

- $120,000

Step 2: Add back Non-Cash Expenses

- Depreciation is a non-cash expense, so add $15,000

Step 3: Adjust for Changes in Working Capital

- Increase in Accounts Receivable is a use of cash: subtract $10,000

- Increase in Inventory is a use of cash: subtract $5,000

- Increase in Accounts Payable is a source of cash: add $8,000

Step 4: Calculate Net Cash Provided by Operating Activities

Operating Cash Flow = Net Income + Depreciation - Increase in AR - Increase in Inventory + Increase in AP

Operating Cash Flow = 120,000 + 15,000 - 10,000 - 5,000 + 8,000 = 128,000

Mind Map: Example Calculation Flow

Best Practices for Modelling Cash Flow from Operating Activities

- Link Directly to Financial Statements: Pull net income from the income statement and working capital balances from the balance sheet to ensure consistency.

- Use Clear Labels and Separate Sections: Distinguish between non-cash adjustments and working capital changes.