Revenue Recognition Mastery

1. Revenue Recognition Foundations for Practical Application

1.1 Scope and Core Principles Under ASC 606 And IFRS 15

Revenue recognition is less about “when to be optimistic” and more about “when the customer gets what they paid for.” ASC 606 and IFRS 15 are built on the same five-step model, but they live in different rule ecosystems. This section sets the boundary lines so you know what the model covers, what it does not, and how the core principles guide judgment when contracts get messy.

What the Standards Cover

Both standards apply to contracts with customers, meaning an agreement that creates enforceable rights and obligations. The standards focus on revenue from ordinary activities, not on gains from selling nonrecurring items like property held for investment.

A practical way to test scope is to ask three questions:

- Is there a contract? If the agreement is not enforceable, the model may not apply.

- Is the counterparty a customer? A customer is a party that has contracted to obtain goods or services that are an output of the entity’s ordinary activities.

- Is the transaction revenue? If it is outside the revenue definition, you do not force it into the model.

Example: Scope Triage for a Service Agreement

A software company signs a contract to provide subscription access and implementation support. The customer can enforce delivery of access and support, and the company’s ordinary activities include providing these services. The contract is in scope.

If the same company sells an old server as scrap, that sale is not an output of ordinary activities. Even if cash is received, it is not revenue from contracts with customers under the model.

The Core Principles That Drive the Model

Both ASC 606 and IFRS 15 revolve around a single idea: recognize revenue to depict the transfer of promised goods or services to the customer in an amount that reflects the consideration the entity expects to be entitled to.

That idea becomes three practical principles.

Principle 1: Identify the Promised Goods or Services

Revenue is not recognized for “having a contract.” It is recognized for delivering specific promises. If a contract includes multiple promises, each promise may be a separate performance obligation depending on whether it is distinct.

Principle 2: Measure Revenue Based on Consideration Expected

Transaction price is not automatically the invoice amount. Variable consideration, constraints, and noncash consideration can change the amount you recognize.

Principle 3: Recognize Revenue When Control Transfers

The timing depends on whether the customer controls the asset as it is created or delivered. Control is broader than physical possession; it includes the ability to direct use and obtain benefits.

How the Standards Treat Judgment

Both frameworks require judgment, but they also require discipline. Judgment is used to determine what the contract promises, how much consideration is expected, and whether control transfers over time or at a point in time.

A helpful mindset is to separate contract interpretation from accounting mechanics:

- Contract interpretation answers: What did we promise and what can the customer enforce?

- Accounting mechanics answers: How does that promise translate into revenue timing and measurement?

Example: Contract Interpretation Before Numbers

A consulting contract states: “We will provide training and a final report.” The customer can enforce delivery of both training sessions and the final report. Even if the report is delivered at the end, you still identify it as a promised service. Only after that identification do you decide whether revenue is recognized over time or at a point in time.

Mind Map: Scope and Core Principles

A Quick Integrated Walkthrough

Consider a contract signed on 2026-03-15 to deliver a customized analytics dashboard plus ongoing data updates for one year.

- Scope check: The customer is obtaining outputs of the entity’s ordinary activities, and the contract is enforceable.

- Promises: The customized dashboard and the data updates are typically separate promises because the updates provide ongoing service benefits.

- Transaction price: If the contract includes a usage-based component, you estimate variable consideration and apply the constraint so you do not recognize amounts that may reverse.

- Timing: The dashboard may be recognized over time if the customer controls the asset as it is built; updates are recognized as the service is provided.

At the end of the day, ASC 606 and IFRS 15 ask you to connect contract promises to customer control, and connect customer control to the amount you expect to be entitled to. That connection is the core principle, and everything else is implementation detail.

1.2 The Five Step Model and How to Apply It to Real Contracts

The five-step model is easiest to use when you treat it like a checklist with evidence requirements. You start with what the contract promises, then you decide how much consideration you expect, then you match that amount to the promises, and finally you decide when revenue is recognized.

Step 1: Identify the Contract with a Customer

A contract exists when there are enforceable rights and obligations. In practice, you look for (1) approval and commitment, (2) identifiable rights for each party, (3) payment terms, (4) commercial substance, and (5) collectability.

Example: A software vendor signs an agreement with a customer for a 12-month subscription. The customer pays within 30 days of invoice. The vendor has a history of collecting from this customer and the contract is enforceable. This passes Step 1.

If collectability is uncertain, you don’t “recognize revenue anyway.” Instead, you reassess whether the arrangement qualifies as a contract under the standard and adjust your accounting accordingly.

Step 2: Identify the Performance Obligations

Performance obligations are promises to transfer distinct goods or services. A promise is distinct if the customer can benefit from it on its own and it is separately identifiable from other promises.

Example: The subscription includes (a) access to the platform and (b) onboarding sessions. If the customer can use the platform without the onboarding and the onboarding is not highly integrated with the platform access, onboarding is likely distinct. If the onboarding is essentially a setup activity that does not provide a separate benefit, it may be part of the platform service.

Step 3: Determine the Transaction Price

Transaction price is the amount of consideration you expect to receive. It includes fixed amounts and variable consideration, and it excludes amounts collected on behalf of third parties.

Variable consideration is estimated using either the expected value method or the most likely amount method, depending on which better predicts the amount.

Example: A construction-related contract has a fixed fee of $500,000 plus a performance bonus of $100,000 if milestones are met. The vendor estimates a 60% chance of meeting milestones. Using the expected value approach, the variable consideration estimate is $60,000 (60% × $100,000). The transaction price estimate becomes $560,000, subject to the constraint.

Constraint in plain terms: you include variable consideration only to the extent it is highly probable that a significant reversal will not occur when uncertainty resolves.

Step 4: Allocate the Transaction Price to Performance Obligations

You allocate based on relative standalone selling prices. If standalone selling prices are observable, use them. If not, estimate them using methods such as adjusted market assessment or expected cost plus margin.

Example: The contract includes platform access (standalone $300,000) and onboarding (standalone $50,000). Total standalone selling price is $350,000. If the transaction price is $280,000, allocation is:

- Platform access: $280,000 × (300,000 / 350,000) = $240,000

- Onboarding: $280,000 × (50,000 / 350,000) = $40,000

If a discount relates specifically to one obligation, you allocate it to that obligation first, as long as the criteria are met.

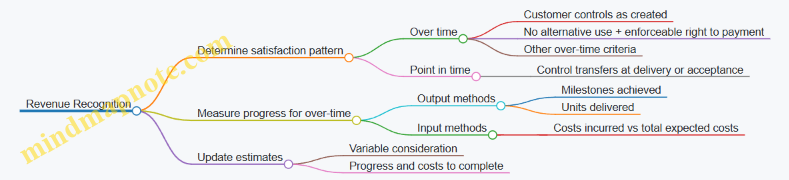

Step 5: Recognize Revenue When (Or As) Performance Obligations Are Satisfied

Revenue timing depends on whether control transfers over time or at a point in time.

Over time recognition is used when one of the over-time criteria is met, such as when the customer controls the asset as it is created or when the asset has no alternative use and the entity has an enforceable right to payment for performance completed to date.

Example: A managed service contract requires the vendor to provide continuous support over 12 months. The customer receives and consumes benefits as the service is performed, so revenue is recognized over time.

To measure progress, you use an output method (such as milestones or units delivered) or an input method (such as costs incurred relative to total expected costs). You update estimates as facts change.

Putting It Together with One Integrated Walkthrough

Consider a contract dated 2026-03-15 for $500,000 fixed consideration for platform access plus $50,000 for implementation. Implementation is distinct because the customer can benefit from platform access immediately, and implementation is separately identifiable. The transaction price is $550,000. Standalone selling prices are $480,000 for access and $120,000 for implementation, totaling $600,000.

Allocation:

- Access: $550,000 × (480,000 / 600,000) = $440,000

- Implementation: $550,000 × (120,000 / 600,000) = $110,000

Timing:

- Access is recognized over the subscription period.

- Implementation is recognized over time if the customer controls the work as it is performed; otherwise, it may be recognized at a point in time upon acceptance.

The model works best when you keep the evidence trail tight: contract terms for Step 1 and 2, estimation support for Step 3, standalone selling price logic for Step 4, and control/progress evidence for Step 5.

1.3 Identifying a Contract with a Customer and Assessing Collectability

Identifying A Contract With A Customer

A “contract” for revenue recognition purposes is not just a signed document. It’s an agreement that creates enforceable rights and obligations. In practice, you’re looking for four things: (1) approval and commitment, (2) identifiable rights and payment terms, (3) commercial substance, and (4) collectability is probable. If any of these are missing, you don’t get to start recognizing revenue just because work has begun.

Approval and Commitment

Approval can be explicit (signed master agreement) or implicit (a purchase order accepted by the supplier, or a customer’s order that the supplier fulfills without objection). The key is that both parties are committed to the arrangement. For example, if a customer emails “Please quote,” and you respond with a price, that’s not yet a contract. If the customer then issues a purchase order and you accept it, the commitment is clearer.

Identifiable Rights and Payment Terms

You need enough detail to determine what each party must do and what the customer must pay. Rights and obligations include delivery timing, service scope, acceptance criteria, and how changes are handled. Payment terms include the amount, due dates, and whether payment is contingent on something.

Example: A contract states “Implementation services for Customer X” but never specifies deliverables or acceptance. If the scope is so vague that you can’t identify what the customer is entitled to, you may not have a contract for revenue recognition purposes.

Commercial Substance

Commercial substance exists when the arrangement is expected to change the entity’s future cash flows in a meaningful way. If the “deal” is effectively a wash—no real economic effect—then revenue recognition is not appropriate.

Example: A customer requests a “swap” where you deliver nothing new and receive nothing of value beyond reimbursement of costs with no margin. Even if paperwork exists, you may struggle to show commercial substance.

Collectability Assessment

Collectability is the probability that the entity will collect substantially all of the consideration to which it expects to be entitled. This is assessed at contract inception and updated when facts change.

Collectability is not “will we eventually get paid?” It’s “are we likely to collect substantially all of what we’re entitled to?” The assessment should consider the customer’s ability and intent to pay, including past payment history, credit risk, and whether amounts are disputed.

Practical Mindset for Collectability

Treat collectability as a decision gate. If collectability is not probable, you generally do not recognize revenue for the expected consideration. Instead, you may recognize consideration only when it is received or when collectability becomes probable, depending on the facts and the nature of the arrangement.

Mind Map: Contract Identification and Collectability

Assessing Collectability Systematically

A good collectability assessment is repeatable. Start with a checklist, then document the reasoning.

Step 1: Gather Credit and Payment Evidence

Use information available at inception: credit ratings, internal credit scores, payment history with the customer, and whether the customer has a track record of paying invoices on time. If the customer is new, rely more heavily on available credit indicators and any guarantees or collateral.

Example: A long-standing customer with consistent on-time payments typically supports a “probable” conclusion, assuming no new adverse facts.

Step 2: Identify Contractual Barriers to Collection

Look for terms that make payment uncertain. Common examples include customer rights to withhold payment for reasons unrelated to performance, broad refund rights, or pricing that is heavily contingent on events controlled by the customer.

Example: A contract requires payment only after the customer’s internal acceptance process, and the customer can delay acceptance indefinitely without objective criteria. That can weaken collectability.

Step 3: Evaluate Disputes and Offsets

If the customer has a history of disputing invoices or if there is an active dispute about amounts already billed, collectability may not be probable for the disputed portion. The assessment should focus on whether you expect to collect substantially all of the consideration.

Example: You bill $100,000 for services delivered. The customer disputes $40,000 and has not paid any portion. If you expect to collect only part of the disputed amount, collectability may fail for the unpaid consideration.

Step 4: Consider Mitigating Factors

Some arrangements include credit enhancements such as guarantees, letters of credit, or prepayments. These can support collectability because they reduce the risk of nonpayment.

Example: If a customer pays 50% upfront and the remaining 50% is due upon delivery, and the customer has a reasonable payment history, collectability for the remaining consideration may be probable even if the customer’s credit is not perfect.

Integrated Example: When a Contract Exists and When It Doesn’t

A software vendor signs a master agreement with a customer. The customer issues a purchase order for a subscription and implementation. The vendor accepts the order. The agreement specifies the subscription term, implementation deliverables, and payment schedule. The customer has paid prior invoices on time. Collectability is probable because the vendor expects to collect substantially all consideration.

Now change one fact: the customer’s credit deteriorates sharply, and the customer informs the vendor it will not pay unless acceptance occurs, but acceptance criteria are subjective and the customer can delay indefinitely. Even with a signed agreement, collectability may not be probable at inception. In that case, revenue recognition should be constrained until collectability improves or the arrangement is structured to support it.

Documentation That Holds Up Under Review

Document the conclusion on collectability and the evidence used. Include: the assessment date, key facts about the customer, any contractual terms affecting payment, and the rationale for “probable” or “not probable.” If the conclusion changes, document the trigger and the updated assessment. This turns a judgment call into a traceable process—less guesswork, fewer surprises.

1.4 Determining the Contract Term and Accounting for Contract Modifications

Contract Term Basics That Drive Revenue Timing

The contract term is the period over which the parties have enforceable rights and obligations. In practice, it matters because it determines when performance is required, when consideration is due, and what happens if the customer changes plans. Start by separating three time concepts: (1) the stated contract period, (2) the period of enforceable rights and obligations, and (3) the period over which you expect to perform. Revenue accounting uses the enforceable rights and obligations, not the marketing-friendly “term” on the signature page.

A common example is a one-year master agreement with purchase orders issued as needed. The master agreement may set pricing and ordering rules, but the enforceable obligation to deliver specific goods or services often exists only when a purchase order is issued. If the master agreement does not create enforceable delivery obligations for future orders, then the contract term for revenue recognition is effectively tied to each purchase order’s enforceable scope.

When Contract Term Includes Renewal Options

Renewal options can extend the contract term, but only if they create enforceable rights and obligations. The key question is whether the option is within the customer’s control and whether the supplier has a substantive right to prevent renewal. If the customer can renew without paying an additional amount that reflects the supplier’s expected costs and risks, the renewal may be part of the enforceable term.

Example: A software hosting agreement runs for 12 months and includes an automatic renewal unless the customer gives notice 30 days before the end of the term. If the customer can avoid renewal by giving notice, the renewal is not automatically enforceable. However, if the supplier has a substantive right to charge a penalty or otherwise prevent the customer from avoiding renewal, the renewal period may be included in the contract term.

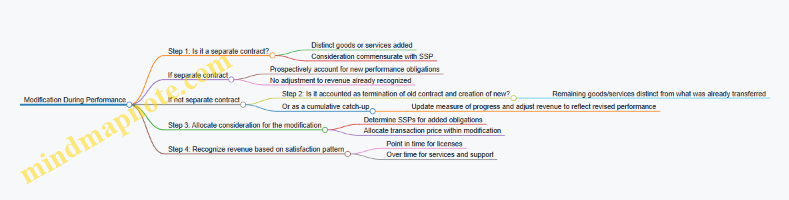

Contract Modifications That Change the Accounting

A contract modification is a change in scope and/or price (or both) that is approved by the parties. The accounting depends on whether the modification adds distinct goods or services and whether those goods or services are priced separately from the original contract.

Think of modifications as one of three outcomes:

- Separate addition: The modification adds distinct goods or services at a price that reflects what the customer would pay on a standalone basis.

- Cumulative adjustment: The modification does not add distinct goods or services, so you update the accounting for the remaining performance.

- No meaningful change: The change is administrative or clarifies terms without changing scope or price.

Step-by-Step Decision Process for Modifications

Use a consistent sequence so the conclusion is defensible:

- Confirm it is a modification: Is there an approved change in scope and/or price? If it’s just a timing change for delivery with no scope or price impact, it may not be a modification.

- Identify the added goods or services: What exactly is changing? Break the change into deliverables, not just “more work.”

- Assess distinctness: Are the added goods or services separately identifiable and capable of being distinct? A deliverable is distinct if the customer can benefit from it on its own or with readily available resources.

- Determine whether the modification is priced separately: If the added goods or services are priced at a standalone selling price (or close enough using your allocation approach), that supports separate accounting.

- Apply the correct accounting model:

- If distinct and priced separately: treat as a separate contract for the added portion.

- Otherwise: treat as part of the existing contract and adjust revenue prospectively (or as required for the remaining performance).

Practical Example: Modification During Performance

Assume a managed services contract begins January 1. The original contract includes monthly service for 12 months at $120,000, with revenue recognized over time.

- Original scope: 12 months of service.

- Modification: On April 1, the customer requests an additional security monitoring module starting July 1.

- Distinctness: The module is separately identifiable and the customer can benefit from it with its existing systems.

- Pricing: The module is priced at $30,000, which aligns with its standalone selling price.

Result: Account for the added module as a separate contract for the July 1 onward period, while continuing to recognize the original contract’s revenue based on the original performance obligations.

Now change one fact: suppose the module is not separately identifiable because it requires reconfiguring the entire service and cannot be used independently. Even if the customer pays an additional amount, the modification likely does not add distinct goods or services. In that case, you adjust the remaining performance obligation accounting for the existing contract, using updated estimates of progress and total consideration.

Mind Map: Contract Term and Modifications

Documentation That Makes the Conclusion Hold Up

To keep the accounting consistent across quarters, document three items for every modification: (1) the approval evidence and what changed, (2) the distinctness rationale tied to customer benefit, and (3) the pricing basis used to judge whether the added goods or services are priced separately. When these are clear, the modification accounting becomes less of a debate and more of a repeatable process—like assembling furniture with the right screws, not guessing which pile is “probably the right one.”

1.5 Common Data Inputs and Documentation Requirements for Audit Readiness

Audit readiness starts with boring inputs and ends with traceable conclusions. In revenue recognition, “traceable” means you can start at a contract term, follow it to a policy decision, and land on a journal entry (or a disclosure) with supporting calculations.

Data Inputs You Need Before You Touch Accounting

Contract and Commercial Terms

Collect the contract itself and the commercial terms that drive the five-step model: customer identity, contract start and end dates, pricing, payment terms, delivery terms, renewal rights, and any change-control language. If the contract is silent on something that affects performance obligations or timing, document the gap and how you resolved it (for example, through standard terms, correspondence, or internal approvals).

Performance Obligation Details

For each promised good or service, capture what is delivered, when it is delivered, and what makes it distinct. If the contract includes setup, implementation, training, or ongoing support, record whether these are separate promises or part of a combined deliverable. The audit trail should show the “distinctness” reasoning and the evidence used.

Transaction Price Components

Variable consideration requires more than a number. Capture the type of variability (rebates, refunds, performance bonuses, usage-based fees), the estimation method you used, and the constraint rationale. Also capture any consideration payable to a customer and whether it is treated as a reduction of transaction price.

Standalone Selling Prices and Allocation Inputs

If you estimate standalone selling prices, store the method and the inputs. For example, if you use an adjusted market assessment, keep the market data sources and the adjustments. If you use expected cost plus margin, keep cost assumptions and margin logic.

Contract Balances and Billing Data

Revenue accounting depends on what has been billed and what has been recognized. Capture billing schedules, invoice dates, amounts, and any credit memos. Also capture contract assets and contract liabilities movements so the reconciliation is not a guessing game.

Documentation Requirements That Make Auditors Happy

A Contract Review Memo That Connects Terms to Accounting

Create a standardized memo per contract that includes: (1) identified performance obligations, (2) transaction price components, (3) allocation approach, (4) revenue recognition pattern and progress measurement, and (5) key judgments. Keep it short enough to be used, but complete enough to stand alone.

Evidence Packs for Key Judgments

Auditors typically focus on judgments, not the mechanics. Build an evidence pack for each judgment area: contract enforceability, distinctness, variable consideration estimation, and over-time measurement. Evidence can include signed agreements, amendments, emails that confirm scope, and internal approval records.

Calculation Workpapers with Version Control

Workpapers should show the calculation steps, not just the final number. Include assumptions, intermediate outputs, and the date of preparation. Version control matters because variable consideration and progress estimates change as facts update.

Reconciliation Between Subledger and General Ledger

Maintain a reconciliation that ties contract-level activity to GL postings. The reconciliation should explain differences such as timing, rounding, tax handling, and write-offs. If you cannot reconcile within a reasonable tolerance, you do not have audit readiness—you have a mystery.

Systematic Mind Map of Audit-Ready Inputs

Mind Map: Audit-Ready Revenue Recognition Inputs

Integrated Examples That Show the Trail

Example: Variable Consideration with a Constraint

A software contract includes a $100,000 base fee plus a $20,000 performance bonus if uptime exceeds a threshold. You estimate the bonus using the expected value of likely outcomes based on historical performance and current implementation status. You then apply the constraint by documenting why it is not probable that a significant reversal will occur. In the workpaper, you store: the probability inputs, the expected value calculation, and the constraint conclusion tied to the specific facts.

Example: Allocation When Standalone Selling Prices Are Uncertain

A customer buys a bundled package: implementation ($60,000 list) and ongoing support ($30,000 list). The contract grants a $20,000 discount for the bundle. If standalone selling prices are not directly observable, you estimate them using adjusted market assessment for implementation and expected cost plus margin for support. You document the discount allocation method and show the allocated amounts per performance obligation, then link those allocations to the revenue recognition schedule.

Example: Over-Time Progress with Cost Updates

A construction-related service is recognized over time using an input method based on labor hours. You capture the labor rate assumptions, the estimated total hours, and the current period hours. When estimates update, you document the change in total hours and the reason (for example, scope clarification). The journal entry is supported by the updated progress calculation and the reconciliation to contract balances.

Practical Documentation Checklist for Audit Readiness

- Contract terms mapped to accounting judgments

- Performance obligations and distinctness evidence stored per contract

- Variable consideration estimation method and constraint rationale documented

- Standalone selling price method and inputs saved with calculations

- Progress measurement method and cost-to-complete assumptions retained

- Workpapers with assumptions, intermediate steps, and version dates

- Subledger-to-GL reconciliation completed and reviewed

- Approval trail for exceptions and policy deviations

A good audit trail is like a well-labeled file cabinet: it does not make the work exciting, but it makes the work finishable.

2. Contract Identification and Customer Agreements in Complex Environments

2.1 Contract Combination Rules and When to Treat Agreements as One

Revenue standards often start with a simple question: “What is the contract?” In practice, companies sign multiple documents that look separate but behave like one deal. Contract combination rules prevent companies from recognizing revenue too early by splitting what is economically one arrangement.

Foundational Concept: One Customer, One Economic Arrangement

A “contract” is an agreement that creates enforceable rights and obligations. When multiple agreements are entered with the same customer (or related parties) around the same time, you evaluate whether they should be combined. The key idea is whether the agreements are linked in a way that changes the substance of the arrangement.

Step 1: Identify the Agreements to Evaluate

Start by listing all agreements with the customer that are signed or modified within the relevant timeframe. Include:

- Master agreements and statements of work

- Purchase orders and acceptance confirmations

- Side letters that change pricing, scope, or delivery terms

- Renewal or extension documents that modify the original deal

If the documents are clearly independent—different customers, different pricing logic, and no shared performance terms—combination is usually unnecessary.

Step 2: Apply the Combination Criteria

Combine agreements when they are negotiated as a package with a single commercial objective, or when the consideration in one agreement depends on the other. Also consider whether the goods or services promised in one agreement are effectively part of the same overall performance.

A practical way to test this is to ask two questions:

- If you removed Agreement B, would Agreement A still make commercial sense on its own?

- Do the documents reference each other’s pricing, scope, or delivery conditions?

If both answers are “no” or “yes, they reference each other,” you likely have one combined contract.

Step 3: Evaluate the Timing and Negotiation Link

Even when documents are signed on different dates, they can still be negotiated as a package. Look for evidence such as:

- A single bid or proposal covering multiple documents

- One set of commercial terms that gets split into separate paperwork

- Delivery schedules that interlock across documents

If the company can show that the later document was negotiated after the earlier one was fully priced and committed independently, combination becomes less likely.

Step 4: Consider Contract Modifications Separately

Combination is not the same as modification. If a later document changes the scope or price of an existing contract, you may need modification accounting instead of combining contracts from the start. A helpful rule of thumb:

- Combination: agreements are linked from the outset as one package.

- Modification: the original contract exists, and later changes alter it.

Mind Map: Contract Combination Decision Flow

Example: Two Documents That Should Be Combined

Company A signs a master services agreement with Customer C for “implementation and ongoing support.” Two weeks later, it issues a statement of work for implementation. The statement of work states that the monthly support fee in the master agreement is reduced by 20% if implementation milestones are missed, and it references the same milestone schedule.

Even though the documents are separate, the support consideration depends on implementation performance. Removing the statement of work would change how the support fee works. Under the combination criteria, treat them as one contract so the performance obligations and revenue timing reflect the interdependent deal.

Example: Two Documents That Should Not Be Combined

Company B enters a one-year software license agreement with Customer D. Three months later, Customer D purchases additional training under a separate order with a separate price and a separate delivery schedule. The training order does not reference the license pricing, does not change the license scope, and does not affect any enforceable rights under the license.

Here, the later agreement does not appear negotiated as a package and the consideration does not depend on the earlier contract. Treat the training order as a separate contract unless other facts show interdependence.

Example: When Cross-References Are the Tie That Binds

Company E signs a framework agreement for “future modules.” It also signs a specific module agreement that sets delivery dates and a fixed price. The framework agreement states that the fixed price applies only if the customer commits to purchasing at least two modules under the framework.

The customer’s commitment under the framework affects the economics of the specific module agreement. That dependency is a strong indicator to combine the agreements into a single contract for revenue recognition purposes.

Practical Takeaway: Document the Reasoning

For audit-ready work, record:

- Which agreements were evaluated

- The specific facts supporting “package” or “dependency”

- Why the agreements are interdependent or independent

- Whether later documents are combinations or modifications

When the paperwork looks messy, the substance usually isn’t. The combination rules are essentially a consistency check: the revenue pattern should match the commercial reality of how the customer and company actually bargained.

2.2 Contract Segmentation for Multiple Performance Obligations

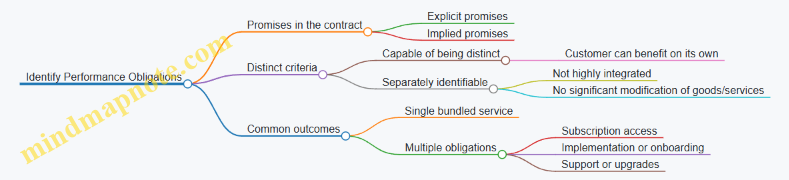

Contract segmentation is the step where you decide whether a customer agreement contains one performance obligation or several. The goal is practical: you want revenue to reflect what the customer actually receives, not just what the contract happens to say.

Foundational Idea: Promises Become Performance Obligations

A performance obligation is a promise to transfer a distinct good or service. Segmentation starts by listing the promises in the contract. Then you test each promise for distinctness. If multiple promises are distinct, you segment the contract into multiple performance obligations and account for them separately.

A useful mental model is “what the customer can benefit from on its own.” If the customer can use a promised item without relying on other promises, that item is a strong candidate for being distinct.

Step 1: Inventory Promises and Group Them Intentionally

Begin with a promise inventory, not a revenue schedule. Create a list of each deliverable and each service activity that the contract commits you to perform. Examples include software licenses, implementation services, training, ongoing support, and hardware delivery.

Then group promises into clusters that are likely to be distinct. For instance, “license + implementation” might be one cluster if the implementation is required to make the license functional. “Training + support” might be separate if training is optional or can be delivered independently.

Step 2: Apply Distinctness Criteria to Each Promise

A promise is distinct if both of the following are true:

- The customer can benefit from the good or service on its own or together with other readily available resources.

- The promise is separately identifiable from other promises in the contract.

The first criterion is about usefulness. The second is about separateness in the contract’s structure.

Readily Available Resources in Plain Terms

Readily available resources are things the customer already has or can obtain without your help. For example, a customer that purchases a standard software license and already has IT staff can often benefit from the license without your implementation.

Separately Identifiable in Plain Terms

Separately identifiable means the promise is not highly integrated with other promises such that it effectively becomes one combined output. If the contract is written so that you are delivering a single combined result, segmentation may be limited.

Mind Map: Contract Segmentation Logic

Example: Bundled Software License and Setup

Assume a contract states:

- You provide a software license for $120,000.

- You provide “setup” for $30,000.

- Setup includes configuration and data migration.

If the customer can use the license immediately with its own resources, the license is distinct. Now consider setup: if setup is required to make the license functional and the configuration is highly dependent on the license, setup may be separately identifiable only if it does not significantly modify the license into a combined output.

A practical way to decide is to ask: “Is setup a service the customer could reasonably buy from someone else, or is it part of delivering a single combined system?” If setup is a standard service and can be performed independently, segmentation into two performance obligations is more likely.

Example: Managed Service with Integrated Reporting

Now assume:

- You provide a managed service for $200,000.

- The contract includes monthly reporting and ongoing monitoring.

If the reporting is not a separate deliverable the customer can benefit from without the monitoring, and the monitoring activities are what generate the reporting, then reporting is likely not separately identifiable. In that case, the managed service and reporting may be one performance obligation.

This is where segmentation prevents a common mistake: treating every named deliverable as separate when the contract is really promising one continuous service outcome.

Common Segmentation Pitfalls and How to Avoid Them

- Treating every line item as distinct: A named deliverable can still be part of a combined output.

- Ignoring customer benefit: If the customer cannot benefit from a promise without other promises, distinctness is weaker.

- Overlooking integration language: Contract wording about a single system, single outcome, or interdependence often signals limited separability.

- Forgetting practical delivery reality: If your delivery process shows one combined output, that supports treating promises as one performance obligation.

Practical Output: What You Should Document

For each promise, document:

- The promise description in plain language.

- The distinctness conclusion for each criterion.

- The key facts supporting that conclusion.

- The resulting performance obligation grouping.

When segmentation is done well, the next steps—price allocation and revenue timing—become straightforward because each performance obligation has a clear “what” and “when.”

2.3 Handling Framework Agreements and Purchase Orders

Framework agreements set the rules of the relationship, while purchase orders (POs) are the specific orders that trigger delivery and payment. The accounting question is whether each PO is a separate contract or whether the framework agreement already contains enforceable rights and obligations for specific goods or services. The answer affects when revenue begins, how performance obligations are identified, and how contract modifications are recognized.

Foundational Concept: What Makes Something a Contract

A contract exists when there are enforceable rights and obligations. In practice, framework agreements often include pricing, general terms, and ordering procedures, but they may not specify the exact goods or services until a PO is issued. Collectability and approval rights matter too: if the supplier can refuse orders without penalty, the “obligation” may not be enforceable until the PO is accepted.

Practical rule of thumb: treat the framework as the “container” for terms, then determine whether the PO creates enforceable rights for specific performance.

Step 1: Read the Framework Like a Contract Lawyer with a Spreadsheet

Focus on five areas:

- Ordering mechanics: Are POs binding when issued, or only after acceptance?

- Pricing and payment terms: Are they fixed or subject to later negotiation?

- Delivery and acceptance: Are delivery dates and acceptance criteria defined per PO?

- Customer obligations: Does the customer commit to minimum quantities or pay for cancellations?

- Supplier obligations: Is the supplier required to fulfill each PO?

If the framework states that each PO is a binding order and the supplier has no substantive right to avoid performance, the PO typically creates enforceable rights and obligations for the specific goods or services.

Step 2: Decide Whether to Combine or Separate

Under the contract combination concept, you combine agreements only when they are entered into at or near the same time with the same customer and meet the criteria for being negotiated as a package. Framework agreements and POs are usually not “negotiated as a package” each time; instead, the framework sets baseline terms and the PO specifies the transaction.

Common outcome: the framework is not a contract by itself for revenue purposes; each PO is the contract for the goods or services ordered, unless the framework already creates enforceable rights for specific items.

Step 3: Determine the Contract Term for Each PO

Even if each PO is a separate contract, the framework can still affect the contract term by defining:

- how long orders can be placed,

- how long the supplier must deliver,

- and how changes are handled.

If a PO includes a delivery schedule spanning months, the PO contract term drives the timing of revenue recognition and the measurement of progress (if over-time criteria apply).

Step 4: Identify Performance Obligations Within the PO

Framework agreements often bundle multiple items or service levels across POs. For each PO, identify promised goods or services that are distinct. If the PO includes a product plus installation, you assess whether installation is separately identifiable and whether the customer can benefit from the product on its own.

Step 5: Handle Changes Without Creating Accidental Modifications

Changes can occur at two levels:

- Framework-level changes that affect future POs (usually not modifications of already-issued POs).

- PO-level changes that alter scope, price, or delivery for that specific order.

A PO modification is accounted for based on whether the change adds distinct goods or services and whether the remaining goods or services are accounted for as a continuation of the original contract.

Mind Map: Framework Agreements and Purchase Orders

Example: Framework Sets Terms, PO Creates the Contract

A supplier signs a framework agreement with a customer on 2026-03-15. The framework states that the customer may issue POs for specific equipment, and each PO is binding upon issuance. The supplier must fulfill accepted POs and cannot cancel without a contractual penalty. Pricing is fixed by a rate card in the framework.

When the customer issues PO-1001 for 10 units delivered in April, the PO specifies the goods and delivery dates. Revenue for PO-1001 begins based on the PO’s performance obligations and timing. The framework merely provides the enforceable terms that make the PO binding.

Example: PO Not Binding Until Acceptance

Same facts, except the framework says the supplier may reject any PO without penalty and only accepted POs are binding. In this case, enforceable rights and obligations for the specific goods generally arise upon acceptance. Revenue recognition should not start merely because a PO is issued; it starts when the supplier has an enforceable obligation.

Example: Framework-Level Change Does Not Modify Prior POs

The framework includes a clause allowing the supplier to update service rates for future POs with 30 days’ notice. The supplier issues the update on 2026-03-30. POs already issued before the update keep their original rates unless the PO terms incorporate the updated rates. Accounting treats the update as affecting future contracts, not modifications of completed or in-progress POs.

Example: PO-Level Change Creates a Modification

A PO for a managed service includes a monthly fee and a defined scope. Midway through the quarter, the customer requests additional reporting dashboards under the same service. If the dashboards are distinct services, the change is accounted for as an added performance obligation. If they are not distinct and represent a change to the existing service pattern, the modification is treated as a continuation with updated estimates and allocation as required.

Documentation That Prevents Confusion Later

For each PO type, document:

- whether the PO is binding on issuance or acceptance,

- which framework clauses establish enforceable rights,

- how you conclude the contract is formed,

- and how PO revisions map to modification accounting.

This keeps the accounting consistent across months of orders, instead of turning each PO into a mini debate with the same facts.

2.4 Assessing Enforceable Rights and Obligations in Contract Terms

Enforceable rights and obligations are the backbone of the “contract” concept in revenue recognition. If the parties can’t enforce key terms, you may have something closer to a plan than an agreement—and the accounting can change. The goal is not to predict behavior; it’s to determine what each party can legally demand and what each party must legally perform.

Step 1: Start with What Is Actually Promised

Read the contract as if you were drafting a checklist for a dispute. Identify the promised goods or services, the delivery timing, and the consideration. Then mark which terms are operational (what gets delivered) and which are conditional (what must happen for delivery or payment).

Example: A software vendor signs an agreement to provide “implementation services.” The contract states the customer will pay $120,000 “upon completion of milestones.” If the contract also says either party may terminate “at any time without cause,” the enforceability of the milestones and payment triggers becomes a central question.

Step 2: Determine Whether Each Party’s Rights Are Enforceable

Enforceability is about legal rights, not business expectations. Look for terms that give one party the ability to compel performance or demand payment.

Key indicators to evaluate:

- Payment rights: Is the customer required to pay, or is payment optional?

- Performance rights: Can the vendor be required to deliver, or can it walk away without consequence?

- Remedies: Are there consequences for nonperformance that suggest enforceable obligations (for example, damages, refund obligations, or specific performance clauses)?

- Termination and cancellation: Does termination require a substantive reason, or is it freely exercisable?

Example: A customer signs a one-year service agreement but the contract allows the customer to cancel monthly “for convenience” with no penalty. If the vendor has no enforceable right to continued service or payment beyond the cancellation date, the agreement may not meet the contract criteria for the full term.

Step 3: Evaluate Consideration That Is Not Yet Due

Contracts often include amounts that depend on future events. The question is whether the parties have enforceable rights to those amounts.

Consider whether the consideration is:

- Unconditional (due regardless of future events),

- Conditional (due only if specified conditions occur), or

- At the discretion of one party (for example, amounts the vendor can decide not to invoice).

Example: A contract includes a $50,000 “success fee” if the customer’s project reaches a defined outcome. If the outcome definition is objective and the vendor has a right to the fee when achieved, the right is enforceable. If the vendor can decide whether the outcome is “satisfactory” without objective criteria, enforceability is weaker.

Step 4: Assess Whether the Contract Has Substance

Even if terms exist on paper, enforceability can be undermined by practical barriers. Evaluate whether the contract is effectively executable.

Common issues:

- No clear approval process for pricing or scope changes,

- Ambiguous acceptance criteria that allow one party to avoid performance,

- Unilateral change rights that let one party alter key terms without the other’s agreement.

Example: A purchase order references “rates per attached schedule,” but the schedule is missing and the vendor can later set rates unilaterally. If the customer cannot enforce the rates and the vendor cannot enforce delivery at known prices, the enforceable rights and obligations are not sufficiently defined.

Step 5: Use a Consistent Evidence Approach

Document your reasoning using contract excerpts and a short conclusion for each enforceability area: payment, performance, termination, and remedies. Consistency matters because teams often interpret the same clause differently.

A practical way to structure your assessment:

- Quote the clause.

- State the enforceable right or obligation it creates.

- Identify the counterparty’s ability to avoid that obligation.

- Conclude whether the contract criteria are met for the relevant portion.

Mind Map: Enforceable Rights and Obligations Assessment

Example: Putting It Together with a Clause-by-Clause Conclusion

Assume a contract includes: (1) a $200,000 base fee, (2) monthly service delivery, and (3) a termination-for-convenience clause allowing the customer to cancel with 30 days’ notice and no penalty.

- Payment: If the contract requires payment for services performed up to the cancellation date, payment for that period is enforceable.

- Performance: The vendor is obligated to provide services during the notice period, but not beyond cancellation.

- Termination: The customer’s free cancellation limits enforceable rights for the remaining months.

Result: You treat the enforceable portion as the period through the cancellation notice, because beyond that point the parties lack enforceable rights and obligations.

Quick Self-Check Before You Move On

If you can’t point to a clause that gives each party enforceable rights and obligations for the relevant period, pause. Revenue recognition depends on what the parties can compel, not what they hope will happen.

2.5 Practical Checklist for Contract Review and Evidence Collection

A contract review is only as good as the evidence behind it. The goal is to reach defensible conclusions about (1) what the customer and company promised, (2) how much consideration is expected, and (3) when and how those promises are satisfied. Use this checklist to move from basic contract facts to the specific judgments required by the revenue model.

Step 1: Capture the Contract Record

Start by building a clean contract “source file” so you can trace every accounting conclusion back to wording.

- Contract identifiers: legal entity, counterparty name, contract number, effective date, and any amendments.

- Document set: master agreement, statements of work, order forms, pricing schedules, and side letters.

- Version control: record the latest executed version and list superseded documents.

- Evidence of approval: signatures, email approvals, or documented authority.

Example: If a master agreement exists but pricing is only in a separate rate card, store both in the same source file and note which document controls pricing.

Step 2: Confirm Contract Existence and Enforceability

Revenue accounting depends on whether the agreement creates enforceable rights and obligations.

- Identify the parties and scope of the agreement.

- Verify enforceability indicators: payment terms, delivery terms, and remedies for nonperformance.

- Assess collectability: document the basis for concluding the company expects to collect consideration.

- Note termination rights: whether termination is at the customer’s option, the company’s option, or mutual.

Example: If the contract allows the customer to cancel without penalty, document whether the company has enforceable rights to payment for work performed or only for delivered items.

Step 3: Identify Performance Obligations

This step turns contract language into a structured list of promises.

- List each promised good or service explicitly stated.

- Scan for implicit promises: setup, implementation, onboarding, training, and ongoing support.

- Determine whether promises are distinct by documenting:

- The customer can benefit from the item on its own or with readily available resources.

- The item is separately identifiable in the contract.

- Record any “series” or bundling logic if multiple deliverables are treated as a single performance obligation.

Example: A contract may bundle “installation” with “software subscription.” If installation is required to make the software functional and is not separately identifiable, you may treat it as part of the subscription promise. Capture the exact clauses supporting that conclusion.

Step 4: Determine Transaction Price and Variable Consideration

Judgments here are often the audit focus, so evidence must be specific.

- Extract consideration terms: fixed fees, usage fees, milestones, rebates, credits, and refunds.

- Identify variable consideration triggers: performance bonuses, penalties, service-level credits, and customer acceptance provisions.

- Document estimation method: expected value or most likely amount, and why it fits the contract.

- Apply the constraint: document the reason the company expects it will not reverse revenue significantly.

- Capture payment terms and timing: due dates, invoicing cadence, and dispute processes.

Example: If service-level credits reduce consideration when uptime falls below a threshold, document how historical performance and the contract’s credit mechanism support the estimate and constraint.

Step 5: Allocate Transaction Price to Performance Obligations

Allocation requires standalone selling prices and a defensible method.

- Determine standalone selling price (SSP) method for each performance obligation:

- Observable prices, adjusted market assessment, or expected cost plus margin.

- Document discount allocation logic: confirm whether discounts relate to specific performance obligations.

- Record allocation outcomes and rounding approach.

Example: If a discount is granted for a bundle of subscription plus implementation, document whether the discount is specifically attributable to one or both promises based on contract terms.

Step 6: Determine Revenue Recognition Pattern

This step links performance obligation nature to timing.

- For each performance obligation, decide point in time vs over time.

- If over time, document which criterion is met:

- Customer controls the asset as created.

- Asset has no alternative use and the company has an enforceable right to payment.

- Customer simultaneously receives and consumes benefits.

- Document progress measurement method:

- Output measures (deliverables, milestones) or input measures (costs, labor hours).

- Capture how estimates are updated and who approves changes.

Example: For a managed service, if progress is measured by labor hours, keep a schedule showing how hours are tracked and reconciled to billing.

Step 7: Collect Evidence for Contract Costs and Presentation

Even if the contract review is “revenue-first,” evidence should cover related accounting.

- Incremental costs of obtaining a contract: document why they qualify and the amortization period.

- Costs to fulfill: document capitalization criteria and amortization basis.

- Principal vs agent: document control indicators such as responsibility for fulfillment and pricing latitude.

- Presentation: ensure revenue and related expenses are presented consistently with principal/agent conclusions.

Example: If the company pays a sales commission only when a contract is signed, store the policy and the contract clause that triggers payment.

Step 8: Build the Audit-Ready Evidence Pack

Evidence should be organized so a reviewer can follow the logic without hunting.

- Create a one-page summary per contract: promises, transaction price components, allocation, timing, and key judgments.

- Attach supporting schedules:

- Variable consideration estimate worksheet.

- SSP calculation or rationale.

- Progress measurement and update log.

- Contract modification log if applicable.

- Maintain a judgment log with:

- The judgment.

- The specific contract language or data supporting it.

- The accounting conclusion.

- The approver and date of approval.

Example: A contract with milestones and service credits should have (a) a milestone schedule, (b) a service-level credit calculation, (c) an allocation worksheet, and (d) a progress update log. If any of these are missing, the accounting may still be correct, but the evidence trail is incomplete—like having the right destination without the map.

3. Performance Obligations and Bundled Promises

3.1 Identifying Promises in Contracts and Distinguishing Goods from Services

Revenue recognition starts with a simple question: what exactly did the customer promise to buy, and what did the company promise to deliver? The contract may look like one deal, but it can contain multiple promises. The accounting answer depends on whether each promise is a good or a service, and whether the promise is distinct.

Core Concept of a Promise

A promise is a unit of performance that the company has committed to the customer. In practice, promises come from explicit contract language, but they can also arise from implied commitments created by customary business practices, published policies, or specific statements made during sales.

A useful way to test whether something is a promise is to ask: if the company did not perform it, would the customer still receive what it bargained for? If the customer would not, the item is likely a promise.

Goods Versus Services

A good is generally something the customer can control as an asset, such as a product, software delivered in a way that the customer can use, or a physical deliverable. A service is generally a performance obligation to provide an activity or access over time, such as implementation, ongoing support, or hosting.

The distinction matters because it often drives the timing of revenue recognition. Goods frequently lead to point-in-time recognition, while services often lead to over-time recognition, though the final timing depends on the “over time” criteria.

Systematic Steps to Identify Promises

- List deliverables and activities stated in the contract. Start with the obvious: products, licenses, installation, training, support, and any reporting.

- Identify what the customer can reasonably expect. Consider marketing materials only if they are incorporated into the contract or create specific commitments.

- Separate deliverables from administrative tasks. Internal steps like project management, invoicing, or internal approvals are usually not promises.

- Assess whether each promise is capable of being distinct. Even if something is a promise, it may not be distinct from other promises.

- Classify each promise as a good or a service. Use the control and nature of performance as the guide.

Mind Map: Promises and Goods Versus Services

Examples That Show the Reasoning

Example 1: Hardware Plus Setup

A contract states: “We will deliver 10 servers and provide installation.” The servers are goods because the customer can control the servers as an asset once delivered. Installation is a service because it is an activity performed to bring the servers into working condition.

If the contract instead says: “We will deliver servers preconfigured and ready to run,” installation may be minimal and could be part of delivering the servers as a good. The key is whether the customer is buying a separate activity or simply receiving a configured item.

Example 2: Software License with Implementation

A company licenses software “for use by the customer.” The license itself is typically a good if the customer receives a right to use the software as an asset. Implementation is a service if it involves configuring, integrating, or training to enable the customer to use the software.

If implementation is purely technical assistance that does not change the customer’s ability to use the software, it may still be a service promise, but it could be not distinct from the license depending on how tightly it is integrated.

Example 3: Hosting and Support

A contract provides “cloud hosting and help desk support.” Hosting is usually a service because the customer receives access to an activity over time rather than an asset delivered at a point in time. Help desk support is also a service because it is ongoing performance.

A common mistake is to treat “support” as a warranty. If the contract promises to fix defects only to assure the product meets specifications, that may be assurance-type. If it promises ongoing assistance, it is a service promise.

Practical Classification Checklist

- Does the customer control an item or right at delivery? Likely a good.

- Is the company performing an activity or providing access over time? Likely a service.

- Is the deliverable an internal step with no customer benefit? Usually not a promise.

- Would nonperformance deprive the customer of the benefit of the contract? Likely a promise.

Once promises are identified and classified, the next step is to determine which promises are distinct and how that affects the timing and measurement of revenue. For now, the goal is to be precise about what the contract requires the company to do—and whether that requirement looks like delivering an asset or performing an activity.

3.2 Determining Whether Promises Are Distinct Under The Practical Criteria

A performance obligation is “distinct” when (1) the customer can benefit from the good or service on its own, and (2) the promise is separately identifiable from other promises in the contract. The practical criteria are designed to prevent over-splitting (creating too many obligations) and under-splitting (bundling unrelated promises). Think of it as asking two questions in order: “Would the customer still want it?” and “Is it really a separate deliverable?”

Step 1: Customer Can Benefit from the Promise

A customer can benefit if the good or service is capable of being used or consumed on its own, or together with other readily available resources. “Readily available” means the customer can obtain the resources without the seller needing to provide a custom integration service.

Example 1: Standalone software license

A contract includes a one-year software license and a separate training session. The license can be used immediately without the training, and the customer can access user guides and support materials. Even if training improves results, the license is capable of being used on its own. The training may or may not be distinct depending on the second criterion, but the license clearly passes the first.

Example 2: Custom installation that is not required

A contract sells a piece of equipment plus optional installation. If the equipment can be installed by the customer’s technicians (or third parties) without the seller’s involvement, the equipment promise can benefit on its own. If the contract requires the seller to perform a unique installation that cannot be replicated easily, the analysis shifts toward whether the promises are separately identifiable.

Step 2: Promise Is Separately Identifiable

Separately identifiable is assessed using indicators that look at how the promises interact. The goal is to determine whether the seller is, in substance, providing a combined item rather than multiple deliverables.

Indicator A: The seller does not provide a combined output

If the promises result in a single integrated deliverable, they may not be distinct. For instance, a “turnkey” system where hardware, software, and configuration are interdependent can be one combined service.

Example 3: Managed service with integrated reporting

A contract includes ongoing data processing and a customized dashboard. The dashboard is not functional without the ongoing processing, and the processing is tailored to the dashboard’s design. The customer cannot benefit from the dashboard without the processing service. Even if the dashboard could be viewed as a separate item, the interdependence suggests the promises may not be separately identifiable.

Indicator B: The good or service is not highly interdependent or interrelated

Interdependence is about whether one promise significantly affects the other. If the seller must substantially modify one deliverable to make the other work, that is a strong sign they are not distinct.

Example 4: Implementation that materially changes the product

A SaaS vendor sells a base subscription plus “implementation” that configures workflows unique to the customer and changes the subscription’s functionality. If the implementation is required to make the subscription usable and the subscription cannot operate as sold without it, the promises may be one performance obligation.

Indicator C: The promise is not significantly modifying or customizing another promise

Customization can be a clue that the promises are linked. The key is whether the customization is so substantial that it effectively merges the promises into a single combined output.

Example 5: Setup that is routine

A contract includes a subscription and a standard onboarding package that configures default settings and provides basic access. If the onboarding does not materially alter the subscription’s functionality and the subscription remains usable without it (even if less efficient), the onboarding may still be distinct.

Practical Decision Flow

flowchart TD

A[Start: Identify each promise] --> B{Can the customer benefit from the promise on its own or with readily available resources?}

B -- Yes --> C{Is the promise separately identifiable from other promises?}

B -- No --> D[Not distinct: combine with related promises]

C -- Yes --> E[Distinct performance obligation]

C -- No --> F[Not distinct: combine with related promises]

Use a structured approach to avoid “gut feel” conclusions.

Mind Map: Distinctness Under the Practical Criteria

Integrated Example: Multi-Element Contract

A vendor sells a cloud subscription, a data migration service, and a custom analytics module. The subscription can be used immediately, but the analytics module requires migrated data and specific configuration. The migration service is tailored to the analytics module, and the module is not functional without it.

- Subscription: passes Criterion 1 because it is usable on its own. Separately identifiable is likely supported if the analytics module does not significantly modify the subscription.

- Migration and Analytics Module: likely fail distinctness together because the analytics module cannot benefit without migration, and the migration is customized to enable the module. In substance, the customer is buying a combined capability.

The practical takeaway is simple: remove one promise in your mind and ask whether the remaining promises still provide a usable outcome to the customer without the seller’s additional work. If the answer is “no,” you probably have a combined performance obligation rather than separate ones.

3.3 Series Guidance and When Multiple Deliverables Are Treated as One

Some contracts look like a menu: “Deliver A, then B, then C.” Others look like a subscription: “Deliver ongoing updates until the customer stops paying.” Revenue recognition needs a consistent answer to one question: are these promised items a single performance obligation (a series) or separate performance obligations?

A series is not a “vibe.” It’s a specific pattern: multiple promised goods or services that are substantially the same and transferred to the customer in the same way over time. When the pattern fits, the accounting can treat the promises as one performance obligation, which simplifies timing and measurement.

Core Series Criteria in Plain Language

A series exists when all of the following are true:

- The promises are substantially the same. The customer is getting the same type of deliverable repeatedly. Differences in size or timing don’t automatically break “substantially the same,” but major differences in nature usually do.

- The pattern of transfer is the same. Each deliverable is transferred to the customer in a similar manner—often over time as the service is performed.

- Each deliverable meets the “over time” requirement. If the contract includes deliverables that are point-in-time while others are over-time, you generally cannot treat everything as one series.

If any deliverable is materially different in nature, or transferred differently, you split the contract into separate performance obligations.

How to Think About “Substantially the Same”

Use a practical test: ask whether the customer would reasonably view each deliverable as the same “thing,” just delivered at different times.

- Usually substantially the same: monthly software updates, recurring managed service tickets, periodic compliance reports with the same scope.

- Often not substantially the same: one deliverable is a basic report, another is a full implementation project; one is a license grant, another is a custom build.

A helpful internal check is to compare the deliverables’ inputs and outputs. If the outputs are the same type and the inputs follow the same process, the deliverables are likely substantially the same.

How to Think About “Same Pattern of Transfer”

The pattern of transfer is about how the customer obtains control. If each deliverable is transferred as it is performed (for example, the customer receives and consumes the service as the vendor performs), that supports a series.

If control transfers only when a milestone is reached—say, when a final report is accepted—then each milestone may be point-in-time, which usually prevents series treatment across the board.

Measuring Progress When It’s One Series

When you treat the series as a single performance obligation, you measure progress for the entire series, not each individual deliverable separately.

- Output method example: “We deliver 1,000 hours of support; we recognize revenue based on hours provided.”

- Input method example: “We recognize based on labor costs incurred relative to total expected labor.”

The key is consistency: the measurement method should reflect the transfer of control for the series as a whole.

Example: Monthly Updates Under a Managed Service Contract

A vendor provides “Security Updates” each month for 12 months. Each month includes the same update package, delivered through the customer’s environment as the vendor completes it. The contract states the customer can benefit from each month’s update as received.

- Deliverables are substantially the same: same type of update.

- Transfer pattern is the same: updates are delivered over time as performed.

- Each month’s update meets the over-time requirement.

Result: treat the 12 monthly updates as a single series performance obligation and measure progress over the contract term.

Example: Implementation Milestones Mixed with Ongoing Support

Now the contract includes:

- Phase 1: implementation (a custom build) delivered at acceptance (point-in-time).

- After acceptance, ongoing support delivered monthly over time.

The implementation phase is not over time, and it’s not substantially the same as the monthly support.

Result: split into at least two performance obligations: one for the implementation milestone and one series for the monthly support.

Mind Map: Series Guidance Decision Path

Practical Documentation Tips That Prevent Rework

When you conclude “series,” document the reasoning in three bullets: (1) what makes deliverables substantially the same, (2) how control transfers in the same way, and (3) why each deliverable qualifies over time. When you conclude “not a series,” document the specific criterion that fails, such as a point-in-time acceptance milestone or a deliverable with a different nature.

That’s the whole game: series treatment is a structured conclusion, not a shortcut. It reduces complexity only when the contract’s deliverables truly behave as one continuous pattern.

3.4 Explicit and Implicit Promises Including Setup and Implementation

Revenue recognition starts with what you promised, not with what you delivered. In practice, contracts often include a mix of explicit promises (stated clearly) and implicit promises (reasonable expectations created by your conduct, customary practices, or specific contract language). The goal is to identify each promised good or service that is distinct, then decide whether it is satisfied over time or at a point in time.

Explicit Promises in Plain Language

Explicit promises are the easiest to spot because they are written or stated directly. They can appear as line items, service descriptions, or milestones.

Example 1: Explicit setup service

A software vendor signs a contract for a subscription plus “implementation services including configuration and user training.” The contract lists “Implementation” as a deliverable with a defined scope. That is an explicit promise.

Practical accounting habit: when you read the contract, highlight every verb that implies performance—“configure,” “install,” “train,” “migrate,” “support,” “deliver.” If the contract ties those verbs to the vendor’s obligations, treat them as candidates for performance obligations.

Implicit Promises That Customers Reasonably Expect

Implicit promises arise when the contract context and the vendor’s established practices create a valid expectation that the vendor will perform a service, even if the contract does not list it as a separate deliverable.

Example 2: Implicit implementation from past practice

A company sells an equipment warranty that includes “preventive maintenance.” The contract does not mention installation support, but the vendor’s standard operating procedure for this equipment always includes site readiness checks and commissioning assistance. If customers typically rely on that practice to make the equipment operational, commissioning assistance can be an implicit promise.

Reasoning rule: an implicit promise must be grounded in evidence. Evidence can include consistent historical behavior, published service descriptions, or specific contract language that references “implementation” without detailing every step.

Setup and Implementation as a Promise, Not a Cost Bucket

Setup and implementation are common sources of confusion because they are often treated as internal activities. Under the revenue model, the question is whether those activities result in a promised good or service to the customer.

Step 1: Map Setup Activities to Customer Benefits

Ask what the customer receives because of your setup work.

- If setup produces a deliverable the customer can benefit from (for example, a configured system, migrated data, or trained users), it is likely a promised service.

- If setup is merely internal preparation with no separate customer benefit, it may not be a promised service.

Example 3: Setup that is a promised service

A cloud provider sells “Managed onboarding” for $20,000. The onboarding includes data mapping, configuration, and a go-live checklist. The customer can point to a completed configuration and a defined onboarding outcome. Treat onboarding as a promised service.

Example 4: Setup that is internal preparation

A vendor’s contract says the subscription begins on the contract start date, and the vendor will “perform internal setup to enable service.” There is no customer deliverable, no acceptance milestone, and no separate scope. The internal setup may be part of fulfilling the subscription rather than a separate performance obligation.

Step 2: Determine Whether Setup Is Distinct

Even if setup is a promised service, it must be distinct to be a separate performance obligation.

Distinct criteria in practice:

- The customer can benefit from the setup on its own or with other readily available resources.

- The setup is not highly integrated with the subscription such that it significantly modifies or customizes the subscription.

Example 5: Integrated implementation

A contract for a customized manufacturing system states that implementation is required to tailor the system and that the subscription cannot function as promised without the implementation work. The implementation is highly integrated, so it may not be distinct from the overall system service.

Example 6: Distinct training

A contract includes a subscription and a separate “training session” with a scheduled agenda and attendance list. The training can be used by the customer’s staff immediately, and it does not significantly modify the subscription. Training is likely distinct.

Mind Map: Promises and Setup/Implementation

Putting It Together with a Mini Walkthrough