Internal Audit Best Practices

1. Introduction to Internal Auditing

1.1 Understanding the Role of Internal Audit in Finance and Real Estate

Internal audit plays a crucial role in ensuring that organizations within the finance and real estate sectors operate efficiently, comply with regulations, and manage risks effectively. Its primary function is to provide independent assurance that an organization’s risk management, governance, and internal control processes are operating effectively.

Key Functions of Internal Audit in Finance and Real Estate

- Risk Management: Identifying, assessing, and mitigating risks that could impact financial performance or asset value.

- Compliance: Ensuring adherence to laws, regulations, and internal policies.

- Operational Efficiency: Evaluating processes to improve efficiency and reduce waste.

- Financial Accuracy: Verifying the accuracy and reliability of financial reporting.

- Fraud Prevention: Detecting and preventing fraudulent activities.

Mind Map: Role of Internal Audit

Why Internal Audit is Vital in Finance and Real Estate

- Complex Regulatory Environment: Both sectors face stringent regulations (e.g., SOX, SEC regulations for finance; local property laws for real estate).

- High-Value Transactions: Large sums and assets require thorough oversight to prevent errors and fraud.

- Market Volatility: Economic fluctuations impact asset values and financial stability.

- Stakeholder Assurance: Investors, regulators, and management rely on audit findings for decision-making.

Example: Internal Audit in a Real Estate Firm

A real estate company managing multiple commercial properties implemented an internal audit function to review lease agreements and rent collection processes. The audit identified inconsistencies in lease documentation and delayed rent payments. By recommending standardized lease templates and improved tracking systems, the firm reduced revenue leakage by 15% within six months.

Mind Map: Benefits of Internal Audit in Real Estate

Example: Internal Audit in a Finance Company

A mid-sized finance company used internal audit to assess its loan approval process. The audit revealed gaps in credit risk assessment and documentation. By introducing stricter credit checks and automated workflow approvals, the company reduced default rates by 10% and improved regulatory compliance.

Mind Map: Internal Audit Impact in Finance

Summary

Internal audit serves as a backbone for governance, risk management, and control in finance and real estate sectors. By systematically evaluating processes and controls, internal auditors help organizations safeguard assets, enhance operational efficiency, and maintain stakeholder confidence. Practical examples from both industries illustrate how internal audit not only identifies issues but also drives meaningful improvements.

1.2 Key Objectives and Benefits of Internal Auditing

Internal auditing plays a pivotal role in ensuring the robustness, transparency, and efficiency of an organization’s operations, particularly within the finance and real estate sectors. Understanding its key objectives and benefits helps accountants and auditors appreciate its value and apply best practices effectively.

Key Objectives of Internal Auditing

Internal auditing is designed to achieve several critical objectives that align with organizational goals and regulatory requirements:

- Risk Management: Identify, assess, and mitigate risks that could impact financial performance or compliance.

- Internal Control Evaluation: Assess the effectiveness and adequacy of internal controls to safeguard assets and ensure accurate financial reporting.

- Compliance Assurance: Verify adherence to laws, regulations, policies, and contractual obligations.

- Operational Efficiency: Evaluate processes and recommend improvements to enhance productivity and cost-effectiveness.

- Fraud Prevention and Detection: Detect irregularities and implement controls to prevent fraudulent activities.

- Governance Support: Provide assurance to management and the board on governance processes and ethical standards.

Benefits of Internal Auditing

Implementing a strong internal audit function offers numerous benefits, especially in complex industries like finance and real estate:

- Enhanced Risk Awareness: Organizations gain a clearer understanding of potential risks, enabling proactive management.

- Improved Financial Integrity: Accurate and reliable financial reporting builds stakeholder confidence.

- Regulatory Compliance: Avoid costly penalties and reputational damage by ensuring compliance.

- Operational Improvements: Identifying inefficiencies leads to streamlined processes and reduced waste.

- Fraud Reduction: Early detection and prevention mechanisms minimize financial losses.

- Strategic Decision Support: Auditors provide insights that inform strategic planning and resource allocation.

- Strengthened Corporate Governance: Transparent reporting and accountability foster trust among investors and regulators.

Practical Example: Real Estate Company Enhancing Compliance and Efficiency

A mid-sized real estate firm faced challenges with inconsistent lease contract management and regulatory compliance. The internal audit team was tasked with evaluating these areas.

- Objective: Ensure lease agreements comply with new local regulations and improve contract management efficiency.

- Approach: Conducted a risk assessment focusing on lease documentation and compliance controls.

- Findings: Identified gaps in contract approval workflows and missing documentation.

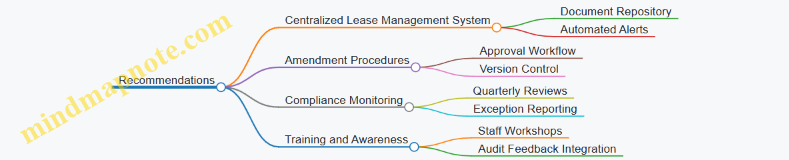

- Recommendations: Implemented a centralized lease management system with automated alerts for renewals and compliance deadlines.

- Outcome: Reduced compliance risks by 40% within six months and improved process efficiency, saving 15 hours per week in administrative tasks.

This example underscores how internal auditing objectives—risk management, compliance assurance, and operational efficiency—translate into tangible business benefits.

Summary

Internal auditing is not just a compliance exercise but a strategic function that drives risk mitigation, operational excellence, and governance. By clearly understanding and applying its key objectives and benefits, auditors in finance and real estate can add significant value to their organizations.

1.3 Overview of Regulatory and Compliance Requirements

Internal auditors in the finance and real estate sectors must have a comprehensive understanding of the regulatory landscape to ensure that their organizations remain compliant and avoid penalties. This section provides an overview of key regulatory and compliance requirements, illustrated with mind maps and practical examples.

Key Regulatory Frameworks in Finance and Real Estate

-

Finance Sector:

- Sarbanes-Oxley Act (SOX)

- Dodd-Frank Act

- Anti-Money Laundering (AML) Regulations

- Basel III

- Securities and Exchange Commission (SEC) Rules

-

Real Estate Sector:

- Fair Housing Act

- Real Estate Settlement Procedures Act (RESPA)

- Anti-Money Laundering (AML) in Real Estate

- Local Zoning and Environmental Regulations

- Financial Accounting Standards Board (FASB) Guidelines

Mind Map: Regulatory Requirements Overview

Practical Example 1: Sarbanes-Oxley Act (SOX) Compliance in a Finance Company

A mid-sized financial services firm implemented SOX compliance by establishing a robust internal control framework. The internal audit team conducted quarterly walkthroughs of financial reporting processes, tested controls such as segregation of duties and authorization protocols, and reported findings to the audit committee. This proactive approach helped identify control gaps early, reducing the risk of financial misstatements.

Practical Example 2: RESPA Compliance in a Real Estate Firm

A real estate company faced challenges ensuring compliance with RESPA, particularly in disclosing closing costs to clients. The internal audit team designed a checklist to verify that all disclosures were timely and accurate. They also reviewed contracts for prohibited kickbacks. As a result, the company improved transparency, reduced regulatory risk, and enhanced client trust.

Mind Map: Compliance Process Flow

Importance of Staying Updated

Regulatory requirements frequently evolve. Internal auditors should subscribe to regulatory updates, participate in industry forums, and maintain strong relationships with legal and compliance teams. For example, recent changes in lease accounting standards (ASC 842) require auditors in real estate to reassess lease classification and disclosure practices.

Summary

Understanding regulatory and compliance requirements is foundational for internal auditors. By integrating this knowledge into audit planning and execution, auditors can help their organizations mitigate risks, ensure legal compliance, and promote operational excellence.

1.4 Example: How a Real Estate Firm Improved Compliance Through Internal Audit

Internal audits play a critical role in ensuring compliance within real estate firms, where regulatory requirements and operational complexities are high. This example illustrates how a mid-sized real estate company leveraged internal auditing to enhance compliance, reduce risks, and streamline processes.

Background

The firm managed a diverse portfolio of commercial and residential properties across multiple states. Due to varying local regulations and internal policy gaps, compliance issues were frequent, leading to fines and reputational risks.

Objectives of the Internal Audit

- Identify compliance gaps across property management and leasing operations.

- Evaluate effectiveness of existing controls.

- Recommend actionable improvements to reduce regulatory risks.

Mind Map: Compliance Improvement Process

Step 1: Risk Assessment and Audit Planning

The audit team began by mapping out all relevant regulatory requirements, including local housing laws, tenant rights, environmental regulations, and financial reporting standards. They then assessed internal policies to identify gaps or outdated procedures.

Example: They discovered that lease agreements in some states did not fully comply with recent tenant protection laws, exposing the firm to legal risks.

Step 2: Conducting Fieldwork

The auditors conducted detailed document reviews, including lease contracts, maintenance logs, and financial records. They also interviewed property managers and compliance officers to understand day-to-day practices.

Example: Sampling of lease agreements revealed inconsistent application of rent increase clauses, which conflicted with state regulations.

Step 3: Reporting Findings

The audit report clearly outlined compliance gaps, categorized by risk level. For example, high-risk findings included non-compliant lease clauses and inadequate documentation of property inspections.

Example: The report highlighted that 30% of properties lacked timely safety inspections, violating local ordinances.

Step 4: Recommendations and Implementation

Recommendations were practical and prioritized:

- Policy Updates: Revise lease templates to align with current laws.

- Training: Conduct workshops for property managers on compliance requirements.

- Automation: Implement a digital tracking system for inspections and lease renewals.

Example: After implementing an automated alert system, the firm reduced missed inspection deadlines by 90% within six months.

Step 5: Follow-Up and Continuous Improvement

The internal audit function established quarterly follow-ups to monitor progress and ensure sustained compliance.

Example: Quarterly reviews showed continuous improvement, with fewer compliance incidents reported.

Mind Map: Benefits Realized

Summary

This example demonstrates how a structured internal audit approach can significantly improve compliance in a real estate firm. By integrating risk assessment, thorough fieldwork, clear reporting, and actionable recommendations, internal auditors helped the firm mitigate risks and foster a culture of compliance.

Such practices are essential for accountants and auditors working in finance and real estate sectors to ensure that organizations not only meet regulatory demands but also operate efficiently and ethically.

2. Planning the Internal Audit

2.1 Establishing the Audit Universe and Risk Assessment

Internal auditing begins with a clear understanding of the audit universe and a thorough risk assessment. These foundational steps ensure that audit resources are focused on the areas of highest risk and greatest importance to the organization.

What is the Audit Universe?

The audit universe is a comprehensive list of all auditable entities within an organization. These entities can include departments, processes, systems, projects, subsidiaries, and controls. In finance and real estate sectors, the audit universe might cover areas such as:

- Financial reporting processes

- Lease and property management

- Investment portfolios

- Compliance with regulatory requirements

- IT systems supporting financial transactions

Example: A real estate company’s audit universe might include property acquisition, lease administration, tenant billing, and property maintenance.

Mind Map: Components of an Audit Universe

Risk Assessment: Prioritizing Audit Focus

Risk assessment involves identifying and evaluating risks that could impact the achievement of organizational objectives. It helps auditors prioritize which areas to audit based on the likelihood and impact of risks.

Key steps in risk assessment include:

- Identify Risks: Gather information from management, previous audits, industry trends, and regulatory changes.

- Assess Risks: Evaluate the likelihood (probability) and impact (consequence) of each risk.

- Prioritize Risks: Rank risks to determine audit priorities.

- Develop Risk-Based Audit Plan: Align audit activities with high-priority risks.

Example: In a finance company, risks such as fraud in accounts payable or inaccurate financial reporting may be rated high priority due to their potential financial impact.

Mind Map: Risk Assessment Process

Practical Example: Risk-Based Audit Planning in a Finance Company

Scenario: A mid-sized finance company wants to optimize its internal audit plan for the upcoming year.

-

The audit team compiles an audit universe including departments like Treasury, Accounts Payable, Compliance, and IT.

-

Through interviews and data analysis, they identify key risks such as:

- Treasury: Unauthorized transactions (High likelihood, High impact)

- Accounts Payable: Duplicate payments (Medium likelihood, Medium impact)

- Compliance: Regulatory non-compliance (Low likelihood, High impact)

- IT: Cybersecurity vulnerabilities (Medium likelihood, High impact)

-

Using this risk assessment, the audit team prioritizes Treasury and IT audits for the next cycle, ensuring resources are allocated effectively.

Best Practices for Establishing Audit Universe and Conducting Risk Assessment

- Engage Stakeholders: Collaborate with management and key personnel to gain insights.

- Use Data Analytics: Leverage data to identify unusual patterns or emerging risks.

- Regularly Update: The audit universe and risk assessment should be dynamic, reflecting organizational changes.

- Document Clearly: Maintain transparent records of how risks were identified and prioritized.

- Align with Strategic Objectives: Ensure audit priorities support the organization’s goals.

By carefully establishing the audit universe and conducting a thorough risk assessment, internal auditors in finance and real estate can focus their efforts where they matter most, enhancing audit effectiveness and organizational value.

2.2 Setting Audit Objectives and Scope

Setting clear audit objectives and defining the scope are critical steps in ensuring an internal audit is focused, efficient, and delivers value. This section explores how to establish meaningful objectives and appropriately limit the scope to align with organizational goals and risk priorities.

What Are Audit Objectives?

Audit objectives specify what the audit aims to achieve. They guide the audit process by defining the key questions to answer and the outcomes expected. Objectives should be SMART: Specific, Measurable, Achievable, Relevant, and Time-bound.

Example:

- Objective: “Evaluate the effectiveness of the lease approval process controls within the real estate division to ensure compliance with company policy and regulatory requirements by Q3 2024.”

Why Define Audit Scope?

The audit scope determines the boundaries of the audit, including the departments, processes, time periods, and types of transactions to be reviewed. Defining scope helps avoid audit creep and ensures resource optimization.

Example:

- Scope: “Review lease contracts signed between January 2023 and June 2024, focusing on approval workflows, documentation completeness, and compliance with internal policies.”

Mind Map: Setting Audit Objectives

Mind Map: Defining Audit Scope

Practical Example: Finance Sector

Scenario: An internal audit team in a financial services company plans to audit the loan approval process.

- Objective: Assess the adequacy and effectiveness of controls over loan approvals to mitigate credit risk and ensure compliance with lending policies.

- Scope: Review loan applications processed between January 2023 and December 2023, focusing on credit checks, approval limits, and documentation.

This clear objective and scope help auditors focus on critical risk areas and provide actionable insights.

Practical Example: Real Estate Sector

Scenario: An audit is planned for the property acquisition process in a real estate firm.

- Objective: Verify that property acquisitions comply with internal policies and regulatory requirements, and that financial approvals are properly documented.

- Scope: Examine all property acquisitions completed in the last 18 months, including contract reviews, approval workflows, and payment authorizations.

This scope ensures the audit covers relevant transactions while avoiding unrelated activities.

Tips for Effective Objective and Scope Setting

- Collaborate with management and process owners to understand priorities.

- Use risk assessments to focus on high-risk areas.

- Keep objectives concise but comprehensive.

- Avoid overly broad scopes that dilute audit effectiveness.

- Revisit and adjust objectives and scope if new risks emerge during the audit.

Summary

Setting audit objectives and scope is foundational to a successful internal audit. Clear, focused objectives aligned with organizational risks and a well-defined scope ensure efficient use of resources and meaningful audit outcomes.

2.3 Developing an Audit Plan and Schedule

Developing a comprehensive audit plan and schedule is a critical step in ensuring that the internal audit process is efficient, focused, and aligned with organizational goals. A well-structured plan helps auditors allocate resources effectively, manage time, and address the highest risks within the finance and real estate sectors.

Key Components of an Audit Plan

- Audit Objectives: Define what the audit aims to achieve.

- Scope: Specify the boundaries of the audit, including departments, processes, or systems.

- Risk Assessment: Prioritize areas based on risk levels.

- Resources: Identify the audit team, tools, and budget.

- Timeline: Establish start and end dates, milestones, and deadlines.

- Methodology: Outline the techniques and procedures to be used.

Mind Map: Components of an Audit Plan

Steps to Develop an Effective Audit Plan and Schedule

- Gather Preliminary Information: Understand the business environment, regulatory requirements, and previous audit findings.

- Perform Risk Assessment: Use risk matrices or scoring models to prioritize audit areas.

- Define Audit Objectives and Scope: Clearly articulate what will be audited and to what extent.

- Allocate Resources: Assign auditors with the right expertise and determine necessary tools.

- Develop the Schedule: Create a timeline considering resource availability and organizational priorities.

- Communicate the Plan: Share the plan with stakeholders for feedback and approval.

Mind Map: Steps to Develop Audit Plan and Schedule

Example: Developing an Audit Plan for a Real Estate Company

Scenario: A real estate firm wants to audit its lease management and property acquisition processes.

- Risk Assessment: Identified high risk in lease compliance and property valuation accuracy.

- Objectives: Ensure compliance with lease terms and verify accuracy of property valuations.

- Scope: Audit lease contracts from the last 2 years and recent property acquisitions.

- Resources: Two auditors with real estate expertise, data analytics software.

- Schedule: 6-week audit starting July 1st, with weekly progress reviews.

Result: The plan allowed the audit team to focus on critical areas, uncovering several lease compliance issues and recommending process improvements.

Mind Map: Real Estate Audit Plan Example

Tips for Scheduling Audits

- Balance Workload: Avoid overloading auditors; distribute audits evenly.

- Consider Business Cycles: Schedule audits during less busy periods to minimize disruption.

- Allow Flexibility: Build buffer time for unexpected issues or extended testing.

- Coordinate with Other Functions: Align with external audits or compliance checks when possible.

Example: Scheduling Audit in a Finance Department

A finance company schedules its internal audits around quarterly financial reporting periods to ensure findings can be incorporated before external audits. They allocate 3 weeks for each audit, with a 1-week buffer for follow-up.

Mind Map: Audit Scheduling Best Practices

By integrating these best practices and examples, internal auditors in finance and real estate can develop robust audit plans and schedules that optimize resources, mitigate risks, and add significant value to their organizations.

2.4 Example: Risk-Based Audit Planning in a Finance Company

Risk-based audit planning is a strategic approach that prioritizes audit resources on areas with the highest risk to the organization. This ensures that the internal audit function adds maximum value by focusing on critical business processes and controls.

Scenario Overview

A mid-sized finance company, FinSecure Inc., decided to adopt risk-based audit planning to improve the effectiveness of its internal audit function. The company operates in lending, investment advisory, and asset management.

Step 1: Establishing the Audit Universe

FinSecure first compiled a comprehensive list of auditable units and processes, including:

- Loan origination and approval

- Investment portfolio management

- Regulatory compliance

- IT systems and cybersecurity

- Financial reporting

- Customer onboarding and KYC (Know Your Customer)

Step 2: Conducting Risk Assessment

The audit team gathered input from management, reviewed past audit reports, and analyzed external factors such as regulatory changes and market conditions. They assessed risks based on:

- Likelihood of occurrence

- Potential financial impact

- Reputational damage

- Regulatory penalties

Mind Map: Risk Assessment Factors

Example: The loan origination process was identified as high risk due to increased default rates and regulatory scrutiny.

Step 3: Prioritizing Audit Areas

Based on the risk scores, the audit team prioritized areas for the upcoming audit cycle:

| Audit Area | Risk Level | Priority |

|---|---|---|

| Loan Origination | High | 1 |

| IT Systems and Cybersecurity | High | 2 |

| Investment Portfolio Management | Medium | 3 |

| Customer Onboarding (KYC) | Medium | 4 |

| Financial Reporting | Low | 5 |

Mind Map: Audit Prioritization

Step 4: Developing the Audit Plan

The audit plan was developed with clear objectives, scope, and resource allocation:

- Loan Origination Audit: Focus on credit approval controls, documentation completeness, and compliance with lending policies.

- IT Systems Audit: Evaluate cybersecurity controls, access management, and data integrity.

Example: For the loan origination audit, the team planned to sample 50 loan files from the last quarter to test adherence to approval workflows.

Step 5: Continuous Monitoring and Adjustment

The audit plan was reviewed quarterly to incorporate emerging risks such as changes in regulatory environment or market volatility.

Mind Map: Continuous Audit Planning

Key Takeaways from FinSecure’s Risk-Based Audit Planning

- Focus on High-Risk Areas: Prioritizing audits where risks are greatest improves resource efficiency.

- Engage Stakeholders: Involving management and using multiple data sources enriches risk assessment.

- Dynamic Planning: Regular updates to the audit plan ensure responsiveness to changing risk landscapes.

- Clear Documentation: Maintaining detailed audit plans and risk assessments supports transparency and accountability.

This example demonstrates how a finance company can implement risk-based audit planning to enhance its internal audit effectiveness, ensuring that critical risks are managed proactively.

2.5 Tools and Techniques for Effective Audit Planning

Effective audit planning is foundational to a successful internal audit. Leveraging the right tools and techniques not only streamlines the process but also enhances the accuracy and relevance of the audit outcomes. Below, we explore key tools and techniques with practical examples and mind maps to illustrate their application.

Key Tools and Techniques

-

Risk Assessment Matrices

- Helps prioritize audit areas based on risk impact and likelihood.

- Example: A real estate firm uses a risk matrix to identify high-risk lease contracts requiring detailed audit.

-

Audit Universe Mapping

- Visual representation of all auditable units/processes.

- Example: A finance company maps its departments and processes to ensure comprehensive coverage.

-

Stakeholder Analysis

- Identifies key stakeholders and their influence on audit scope.

- Example: Auditors engage with compliance officers to understand regulatory priorities.

-

Data Analytics Tools

- Software like ACL, IDEA, or Excel for analyzing large datasets.

- Example: Using data analytics to detect unusual transaction patterns in accounts payable.

-

Project Management Software

- Tools like MS Project, Trello, or Asana to track audit tasks and timelines.

- Example: Scheduling audit fieldwork and deliverables with clear deadlines.

-

Brainstorming and Workshops

- Collaborative sessions to identify risks and audit focus areas.

- Example: Conducting a workshop with finance and real estate teams to uncover emerging risks.

-

Mind Mapping

- Visual tool to organize audit planning thoughts and link related concepts.

- Example: Creating a mind map to break down audit scope into manageable components.

Mind Maps Examples in

Mind Map 1: Audit Universe Mapping

Mind Map 2: Risk Assessment Process

Mind Map 3: Audit Planning Workflow

Practical Example: Applying Tools in a Real Estate Audit Planning

A real estate company plans an internal audit focusing on lease compliance and asset valuation. The audit team begins by mapping the audit universe, listing all relevant departments and processes. Using a risk assessment matrix, they score lease contracts based on value and complexity, identifying high-risk leases for detailed review.

They organize a brainstorming workshop with property managers and finance staff to uncover potential risks such as inaccurate valuations or missed lease renewals. Data analytics tools are employed to analyze lease payment histories and detect anomalies.

Project management software is used to assign tasks, set deadlines, and monitor progress. Throughout, mind maps help the team visualize the audit scope and workflow, ensuring clarity and alignment.

This integrated approach results in a focused, efficient audit plan that addresses the most critical risks with clear timelines and responsibilities.

Summary

Utilizing a combination of risk assessment matrices, audit universe mapping, stakeholder analysis, data analytics, project management tools, brainstorming, and mind mapping enables auditors to develop comprehensive and effective audit plans. These tools facilitate prioritization, collaboration, and clarity, ultimately enhancing audit quality and impact.

3. Conducting Fieldwork and Evidence Collection

3.1 Gathering and Documenting Audit Evidence

Gathering and documenting audit evidence is a cornerstone of the internal audit process. It ensures that auditors have sufficient, reliable, and relevant information to support their findings and conclusions. This section will explore best practices for collecting audit evidence, the types of evidence commonly used, and effective documentation techniques, all illustrated with practical examples.

What is Audit Evidence?

Audit evidence consists of all the information collected by auditors to evaluate the adequacy and effectiveness of controls, compliance, and risk management processes.

Types of Audit Evidence

- Physical Evidence: Tangible assets or documents (e.g., contracts, invoices, property deeds).

- Documentary Evidence: Records such as financial statements, policies, and reports.

- Testimonial Evidence: Information obtained through interviews or inquiries.

- Analytical Evidence: Data analysis, trends, and ratios.

Best Practices for Gathering Audit Evidence

- Plan Evidence Collection: Define what evidence is needed based on audit objectives.

- Use Multiple Sources: Corroborate findings by collecting evidence from different sources.

- Maintain Objectivity: Collect evidence impartially without bias.

- Ensure Timeliness: Gather evidence promptly to reflect current conditions.

- Secure Evidence: Protect confidentiality and integrity of evidence.

Mind Map: Key Steps in Gathering Audit Evidence

Methods of Collecting Audit Evidence

-

Inspection: Examining records, documents, or tangible assets.

- Example: Reviewing lease agreements in a real estate portfolio to verify terms.

-

Observation: Watching processes or procedures being performed.

- Example: Observing cash handling procedures at a finance department.

-

Inquiry: Asking questions of personnel to gain understanding.

- Example: Interviewing property managers about maintenance schedules.

-

Confirmation: Obtaining direct verification from third parties.

- Example: Confirming bank balances with financial institutions.

-

Recalculation: Verifying mathematical accuracy.

- Example: Recalculating depreciation expenses on fixed assets.

-

Analytical Procedures: Comparing financial data and ratios.

- Example: Analyzing trends in rental income over several quarters.

Mind Map: Methods of Evidence Collection

Documenting Audit Evidence

Proper documentation is essential to create a clear audit trail and support audit conclusions.

- Use Workpapers: Structured templates to record evidence, procedures, and findings.

- Detail Source Information: Include origin, date, and collector of evidence.

- Link Evidence to Objectives: Clearly connect evidence to audit criteria.

- Maintain Confidentiality: Store documentation securely.

Example: Documenting Evidence in a Real Estate Audit

An auditor reviewing lease compliance collects the following evidence:

- Copies of lease contracts (Inspection)

- Interview notes from tenant meetings (Inquiry)

- Maintenance logs (Observation)

- Rent payment confirmations from bank statements (Confirmation)

Each piece of evidence is logged in workpapers with dates, source names, and relevance notes, ensuring a comprehensive audit trail.

Practical Example: Detecting Anomalies Through Evidence Collection

In a finance company, auditors noticed discrepancies in vendor payments. Using a combination of inspection (reviewing invoices), confirmation (contacting vendors), and recalculation (verifying payment amounts), they uncovered duplicate payments caused by weak internal controls.

Summary

Gathering and documenting audit evidence requires a structured approach that combines multiple collection methods, ensures objectivity, and maintains thorough records. Applying these best practices enables auditors in finance and real estate sectors to produce credible, actionable audit results.

3.2 Interview Techniques and Stakeholder Engagement

Internal audits rely heavily on effective communication with stakeholders to gather accurate information, understand processes, and identify risks. Mastering interview techniques and stakeholder engagement is essential for auditors in finance and real estate sectors to ensure comprehensive and insightful audits.

Key Interview Techniques

- Preparation: Research the stakeholder’s role, background, and relevant processes before the interview.

- Open-Ended Questions: Encourage detailed responses to gain deeper insights.

- Active Listening: Show engagement through verbal and non-verbal cues; clarify and summarize to confirm understanding.

- Neutrality: Maintain an unbiased stance to foster honest communication.

- Documentation: Take clear notes or record (with permission) to capture critical information.

- Follow-Up Questions: Probe deeper based on initial answers to uncover hidden risks or controls.

Mind Map: Interview Techniques

Stakeholder Engagement Strategies

- Identify Key Stakeholders: Include finance managers, auditors, compliance officers, property managers, and external consultants.

- Build Rapport: Establish trust by explaining audit purpose and ensuring confidentiality.

- Tailor Communication: Adjust language and detail level based on stakeholder expertise.

- Schedule Convenient Meetings: Respect stakeholders’ time to encourage cooperation.

- Provide Feedback: Share preliminary findings to validate information and encourage collaboration.

Mind Map: Stakeholder Engagement

Example 1: Interviewing a Finance Manager in a Real Estate Firm

Scenario: An auditor is assessing lease revenue recognition controls.

- Preparation: Auditor reviews lease contracts and prior audit reports.

- Interview Approach: Uses open-ended questions like “Can you walk me through the process of recognizing lease revenue?” and probes with “How do you ensure that lease modifications are accurately reflected in the financial statements?”

- Engagement: Builds rapport by acknowledging the manager’s expertise and explaining the audit’s goal to improve controls.

- Outcome: The manager reveals a manual step prone to errors, which becomes a key audit finding.

Example 2: Engaging External Auditors During an Internal Audit

Scenario: Coordination between internal and external auditors to avoid duplication.

- Stakeholder Identification: External audit team lead.

- Engagement Strategy: Schedule a joint meeting to discuss scope and share preliminary findings.

- Communication: Use clear, jargon-free language and share timelines.

- Result: Enhanced cooperation reduces audit fatigue on finance staff and improves overall audit quality.

Best Practices Summary

- Always prepare thoroughly before interviews.

- Use open-ended and probing questions to uncover detailed information.

- Engage stakeholders respectfully and transparently.

- Document interviews meticulously for audit trail and follow-up.

- Foster ongoing communication to build trust and collaboration.

Mastering interview techniques and stakeholder engagement empowers internal auditors to collect accurate, relevant information and build strong relationships, ultimately enhancing audit effectiveness in the finance and real estate sectors.

3.3 Sampling Methods and Data Analysis

Internal auditors often face large volumes of data and transactions, making it impractical to review every item. Sampling methods and data analysis techniques help auditors efficiently and effectively gather evidence to form conclusions about the entire population.

Sampling Methods

Sampling is the process of selecting a subset of items from a population to draw conclusions about the whole. Choosing the right sampling method is critical to ensure the audit results are reliable and representative.

Common Sampling Methods:

- Random Sampling: Every item in the population has an equal chance of being selected.

- Systematic Sampling: Selecting every nth item from a list after a random start.

- Stratified Sampling: Dividing the population into subgroups (strata) and sampling from each subgroup.

- Judgmental (Non-Statistical) Sampling: Auditor selects items based on experience or risk assessment.

Mind Map: Sampling Methods Overview

Example: Applying Sampling in a Real Estate Audit

A real estate company has 5,000 lease contracts. Auditing all contracts is not feasible within the time frame. The auditor uses stratified sampling by dividing contracts into three strata based on lease value:

- High-value leases (top 10%)

- Medium-value leases (next 40%)

- Low-value leases (remaining 50%)

The auditor then selects a higher proportion of samples from the high-value stratum to focus on higher risk areas, ensuring efficient use of audit resources.

Data Analysis in Internal Auditing

Data analysis enhances the auditor’s ability to identify anomalies, trends, and risks by examining large datasets systematically.

Key Data Analysis Techniques:

- Descriptive Analytics: Summarizing data using means, medians, frequencies.

- Trend Analysis: Identifying patterns over time.

- Ratio Analysis: Comparing financial ratios to benchmarks.

- Outlier Detection: Spotting unusual transactions or values.

- Data Visualization: Using charts and graphs to interpret data.

Mind Map: Data Analysis Techniques

Example: Using Data Analytics to Detect Anomalies in Real Estate Transactions

An auditor analyzes payment data for property management fees over the past year. Using outlier detection, they identify several unusually large payments made to a vendor outside the normal payment cycle. Further investigation reveals duplicate payments due to a system glitch, allowing the company to recover funds and improve controls.

Integrating Sampling and Data Analysis

Combining sampling with data analysis maximizes audit effectiveness. For example, auditors can use data analytics to identify high-risk transactions or unusual patterns and then apply targeted sampling to those areas.

Mind Map: Integrating Sampling and Data Analysis

Summary

- Sampling methods help auditors efficiently select representative data subsets.

- Data analysis techniques uncover trends, anomalies, and risks.

- Combining both approaches enhances audit quality and resource allocation.

- Real-world examples from finance and real estate illustrate practical application.

By mastering sampling and data analysis, internal auditors can provide deeper insights and more reliable assurance to stakeholders.

3.4 Example: Using Data Analytics to Detect Anomalies in Real Estate Transactions

Internal auditors in the real estate sector increasingly rely on data analytics to identify irregularities and potential fraud in transactions. By leveraging data-driven techniques, auditors can efficiently sift through large volumes of transaction data to pinpoint anomalies that warrant further investigation.

Understanding the Role of Data Analytics in Real Estate Audits

- Real estate transactions generate vast datasets including property details, buyer/seller information, pricing, payment schedules, and contractual terms.

- Manual review of these records is time-consuming and prone to oversight.

- Data analytics enables auditors to automate detection of unusual patterns, outliers, and inconsistencies.

Key Steps in Using Data Analytics for Anomaly Detection

Practical Example: Detecting Anomalies in Property Sale Prices

Scenario: An internal audit team is reviewing property sales over the last fiscal year to identify transactions that may indicate inflated prices or potential kickbacks.

Step 1: Data Gathering

- Extract all property sales data including sale price, property size, location, date of sale, and buyer/seller details.

Step 2: Data Cleaning

- Ensure all prices are in the same currency and format.

- Remove incomplete or duplicate records.

Step 3: Analytical Techniques

- Calculate average price per square foot for properties in each neighborhood.

- Identify transactions where price per square foot significantly exceeds the neighborhood average (e.g., 2 standard deviations above the mean).

Step 4: Visualization and Mind Mapping

Step 5: Example Findings

- Transaction #452: Sold at $750/sq ft in a neighborhood averaging $450/sq ft.

- Buyer and seller share common addresses, indicating potential conflict of interest.

Step 6: Reporting

- Document findings with supporting data and visualizations.

- Recommend further investigation or control improvements.

Additional Examples of Data Analytics Applications

-

Payment Pattern Analysis: Detecting unusual payment schedules or repeated late payments that may indicate financial distress or manipulation.

-

Duplicate Vendor Detection: Using fuzzy matching algorithms to identify duplicate or fictitious vendors in payment records.

-

Contract Compliance Checks: Comparing contract terms with actual transaction data to ensure adherence.

Best Practices for Effective Use of Data Analytics

- Collaborate with IT and data specialists to ensure data integrity.

- Use a combination of automated tools and auditor judgment.

- Continuously update analytical models to reflect market changes.

- Document assumptions, methodologies, and findings clearly.

By integrating data analytics into internal audit processes, auditors in the real estate sector can significantly enhance their ability to detect anomalies early, reduce risk exposure, and improve overall audit quality.

3.5 Maintaining Objectivity and Professional Skepticism

Maintaining objectivity and professional skepticism is fundamental to the integrity and effectiveness of internal auditing. These principles ensure that auditors remain impartial, unbiased, and critically evaluative throughout the audit process, which is especially crucial in the Finance and Real Estate sectors where complex transactions and regulatory requirements abound.

What is Objectivity?

Objectivity refers to the auditor’s ability to perform audit work without bias, conflict of interest, or undue influence from others. It requires auditors to base their conclusions solely on evidence and facts.

What is Professional Skepticism?

Professional skepticism is an attitude that includes a questioning mind and a critical assessment of audit evidence. It involves being alert to conditions that may indicate possible misstatement due to error or fraud and critically evaluating the sufficiency and reliability of audit evidence.

Mind Map: Maintaining Objectivity and Professional Skepticism

Practical Examples

Example 1: Detecting Unusual Real Estate Transaction Patterns An internal auditor noticed a series of property sales occurring at prices significantly above market value within a short period. Instead of accepting explanations at face value, the auditor applied professional skepticism by:

- Requesting additional documentation such as appraisal reports and contracts.

- Comparing transactions with independent market data.

- Interviewing involved parties to understand the rationale.

This approach uncovered potential related-party transactions intended to inflate asset values, prompting further investigation.

Example 2: Verifying Financial Data Beyond Face Value During an audit of a finance department, an auditor observed that reported revenue growth was unusually high compared to industry benchmarks. Maintaining objectivity, the auditor:

- Examined underlying contracts and payment schedules.

- Tested revenue recognition policies for compliance with accounting standards.

- Used data analytics to identify irregular revenue spikes.

This led to identifying premature revenue recognition, allowing management to correct financial statements.

Example 3: Challenging Optimistic Revenue Forecasts In a real estate company, management presented optimistic forecasts for rental income growth. The auditor, applying professional skepticism,:

- Reviewed historical performance against forecasts.

- Assessed market trends and economic indicators.

- Requested sensitivity analyses to understand forecast assumptions.

This critical evaluation helped highlight overly optimistic assumptions, resulting in more realistic budgeting.

Techniques to Maintain Objectivity and Professional Skepticism

- Rotate Audit Assignments: Regularly changing audit areas to avoid familiarity threats.

- Document Judgments: Clearly record the basis for conclusions to provide transparency.

- Seek Corroborative Evidence: Always look for multiple sources to support findings.

- Engage in Peer Reviews: Obtain feedback from colleagues to challenge assumptions.

- Stay Informed: Keep up-to-date with industry trends and emerging risks to better identify anomalies.

Summary

Maintaining objectivity and professional skepticism is essential for internal auditors to provide reliable and credible assurance. By fostering a questioning mindset, avoiding biases, and critically evaluating evidence, auditors can effectively identify risks and contribute to stronger governance and control environments in Finance and Real Estate organizations.

4. Evaluating Internal Controls

4.1 Frameworks for Assessing Internal Controls (COSO, COBIT)

Internal controls are the backbone of effective risk management and governance in any organization, especially within the finance and real estate sectors. To systematically assess these controls, auditors rely on established frameworks that provide structured guidance and best practices. Two of the most widely recognized frameworks are COSO (Committee of Sponsoring Organizations of the Treadway Commission) and COBIT (Control Objectives for Information and Related Technologies).

COSO Framework Overview

COSO is primarily focused on enterprise risk management and internal control over financial reporting. It helps organizations design, implement, and evaluate internal controls to achieve objectives related to operations, reporting, and compliance.

The COSO Framework consists of five interrelated components:

- Control Environment

- Sets the tone of the organization

- Influences control consciousness

- Risk Assessment

- Identifies and analyzes risks to achieving objectives

- Control Activities

- Policies and procedures to mitigate risks

- Information and Communication

- Supports the identification, capture, and exchange of information

- Monitoring Activities

- Ongoing evaluations to ensure controls are effective

Mind Map: COSO Framework Components

Example: A real estate company used the COSO framework to evaluate its lease approval process. By assessing the control environment, they identified a lack of segregation of duties between lease approval and payment processing. Implementing control activities such as dual approvals and regular reconciliations helped reduce errors and potential fraud.

COBIT Framework Overview

COBIT is a comprehensive framework for IT governance and management, particularly useful for auditing IT controls within organizations. It aligns IT goals with business objectives and provides detailed control objectives for IT processes.

COBIT’s core components include:

- Governance System and Components

- Governance and Management Objectives

- Performance Management

- Processes and Activities

COBIT organizes IT processes into domains such as:

- Evaluate, Direct and Monitor (EDM)

- Align, Plan and Organize (APO)

- Build, Acquire and Implement (BAI)

- Deliver, Service and Support (DSS)

- Monitor, Evaluate and Assess (MEA)

Mind Map: COBIT Domains and Key Processes

Example: In a finance company, the internal audit team used COBIT to assess IT controls related to financial reporting systems. They focused on DSS05 (Manage Security Services) to evaluate access controls and data protection measures. By identifying gaps in user access reviews, they recommended implementing automated periodic access certification, which enhanced system security and compliance.

Integrating COSO and COBIT in Internal Audits

While COSO provides a broad framework for internal controls across the enterprise, COBIT offers detailed guidance on IT-specific controls. For auditors in finance and real estate sectors, combining both frameworks ensures comprehensive coverage of financial, operational, and IT risks.

Mind Map: Integration of COSO and COBIT

Example: A real estate firm conducting an internal audit on its property management software applied COSO to evaluate overall control environment and risk assessment, while using COBIT to drill down into IT governance, security, and system development lifecycle controls. This integrated approach uncovered both process and IT control gaps, leading to a robust remediation plan.

Summary of Best Practices for Using Frameworks

- Tailor frameworks to organizational context: Adapt COSO and COBIT components to fit the size, complexity, and risk profile of the organization.

- Use risk-based approach: Prioritize controls based on risk assessment outcomes.

- Document findings clearly: Map audit observations to specific framework components.

- Leverage technology: Use audit management tools to track controls and testing results.

- Continuous monitoring: Implement ongoing evaluation mechanisms aligned with framework monitoring activities.

By mastering COSO and COBIT frameworks, internal auditors in finance and real estate can systematically assess controls, identify weaknesses, and provide actionable recommendations that enhance organizational resilience and compliance.

4.2 Identifying Control Weaknesses and Risks

Identifying control weaknesses and risks is a critical step in the internal audit process. It allows auditors to pinpoint areas where the organization’s internal controls may fail to prevent or detect errors, fraud, or inefficiencies. This section will guide you through practical approaches, supported by examples and mind maps, to effectively identify these vulnerabilities within finance and real estate sectors.

Understanding Control Weaknesses

Control weaknesses occur when controls are missing, improperly designed, or not operating effectively. These weaknesses can be categorized as:

- Design Weaknesses: Controls that are inadequately designed to mitigate risks.

- Operational Weaknesses: Controls that are well designed but not implemented or followed correctly.

Mind Map: Types of Control Weaknesses

Risk Identification Process

-

Understand the Business Processes: Gain a thorough understanding of the processes under audit. For example, in real estate lease management, understand how leases are approved, recorded, and monitored.

-

Perform Risk Assessment: Identify risks that could impact financial reporting, compliance, or operational efficiency.

-

Evaluate Existing Controls: Assess whether current controls address identified risks adequately.

-

Test Controls: Perform walkthroughs and sample testing to verify control effectiveness.

-

Document Findings: Clearly document any control gaps or failures.

Mind Map: Risk Identification Steps

Example: Identifying Control Weaknesses in a Real Estate Lease Management Process

Scenario: An internal auditor is reviewing the lease approval process in a real estate company.

- Observation: The auditor finds that lease agreements are sometimes approved verbally without formal documentation.

- Risk: This may lead to unauthorized leases, financial losses, or compliance breaches.

- Control Weakness: Lack of a formal approval control (design weakness) and inconsistent enforcement of approval procedures (operational weakness).

Action: Recommend implementing a mandatory written approval workflow with electronic signatures and periodic review of lease approvals.

Common Risks and Associated Control Weaknesses in Finance and Real Estate

| Risk Area | Example Risk | Typical Control Weakness |

|---|---|---|

| Financial Reporting | Misstatement of revenue | Inadequate reconciliation controls |

| Compliance | Non-adherence to regulatory requirements | Lack of updated policies and training |

| Fraud | Unauthorized transactions | Weak segregation of duties |

| Asset Management | Misappropriation of property assets | Poor physical access controls |

| IT Systems | Data breaches or system downtime | Insufficient IT access controls and monitoring |

Mind Map: Common Risks and Control Weaknesses

Practical Tips for Auditors

- Use process flowcharts to visualize controls and identify gaps.

- Conduct interviews with process owners to uncover informal practices.

- Leverage data analytics to detect anomalies indicating control failures.

- Prioritize risks based on impact and likelihood to focus audit efforts.

Example: Using Data Analytics to Identify Risks in Finance

An auditor uses transaction data to identify duplicate payments in accounts payable. By applying filters and pattern recognition, the auditor uncovers multiple instances where invoices were paid twice due to weak invoice matching controls.

Result: The auditor recommends implementing automated three-way matching controls and periodic data reviews to prevent recurrence.

By systematically identifying control weaknesses and associated risks, internal auditors can provide valuable insights that strengthen organizational controls, reduce risk exposure, and enhance overall governance.

4.3 Testing Control Effectiveness

Testing control effectiveness is a critical step in the internal audit process to ensure that internal controls are functioning as intended and mitigating risks effectively. This section will guide you through the methodologies, best practices, and practical examples to test controls within finance and real estate sectors.

What is Control Effectiveness Testing?

Control effectiveness testing evaluates whether the control activities are operating as designed and are capable of preventing or detecting errors or fraud in a timely manner.

Key Steps in Testing Control Effectiveness

Mind Map: Testing Control Effectiveness Steps

Common Testing Techniques

Mind Map: Control Testing Techniques

Example: Testing Control Effectiveness in Lease Approval Process (Real Estate)

Control Objective: Ensure all lease agreements are properly authorized before execution.

Testing Approach:

- Inquiry: Interview lease managers to understand the approval workflow.

- Inspection: Review a sample of lease agreements for signatures and approval stamps.

- Reperformance: Select a few lease agreements and verify if the approval process was followed by tracing back through system logs or email trails.

Findings:

- 95% of sampled leases had proper approvals.

- 5% lacked documented authorization, indicating a control gap.

Action: Recommend reinforcing approval documentation and periodic refresher training for lease managers.

Example: Testing Control Effectiveness in Expense Reimbursement (Finance)

Control Objective: Ensure all employee expense reimbursements are valid, approved, and comply with company policy.

Testing Approach:

- Observation: Observe the process of submitting and approving expense reports.

- Inspection: Examine a random sample of expense reports for receipts, approval signatures, and policy compliance.

- Reperformance: Recalculate expense totals and verify approval dates.

Findings:

- All sampled reports had valid receipts.

- Two instances of late approvals were noted, which could delay detection of errors.

Action: Suggest implementing automated reminders for timely approvals.

Best Practices for Testing Control Effectiveness

Mind Map: Best Practices

Tips for Sample Selection

- Use statistical sampling for large populations to ensure unbiased results.

- For smaller populations, consider 100% testing if feasible.

- Focus on high-risk transactions or controls with past deficiencies.

Common Pitfalls to Avoid

- Relying solely on inquiry without corroborating evidence.

- Testing too few samples, leading to unreliable conclusions.

- Ignoring the design of the control and focusing only on execution.

By integrating these testing methodologies and examples, internal auditors in finance and real estate can confidently assess control effectiveness, identify gaps, and contribute to stronger risk management frameworks.

4.4 Example: Control Evaluation in Lease Management Processes

Internal audit plays a critical role in evaluating controls within lease management processes, especially in the real estate sector where lease agreements, payments, and compliance are complex and high-value. This example demonstrates how auditors can assess controls effectively, identify weaknesses, and recommend improvements.

Understanding Lease Management Controls

Lease management involves multiple control points to ensure accuracy, compliance, and risk mitigation. Typical controls include:

- Lease agreement approval and documentation

- Rent calculation and invoicing

- Payment collection and reconciliation

- Lease renewal and termination procedures

- Compliance with regulatory and accounting standards (e.g., IFRS 16 / ASC 842)

Mind Map: Key Control Areas in Lease Management

Step-by-Step Control Evaluation Example

-

Review Lease Documentation Controls:

- Verify that all lease agreements are properly authorized by management.

- Check for completeness and accuracy of contract terms.

- Example: An auditor found that 15% of lease contracts lacked proper signature approvals, indicating a control gap.

-

Assess Rent Calculation and Invoicing Controls:

- Test the accuracy of rent calculations against contract terms.

- Evaluate automated invoicing systems for consistency.

- Example: In one audit, discrepancies in rent escalation clauses led to underbilling by 8%, highlighting the need for better system controls.

-

Evaluate Payment Collection and Reconciliation:

- Confirm that payments are recorded timely and reconciled with bank statements.

- Review procedures for handling late or missed payments.

- Example: An auditor discovered delays in payment posting, causing cash flow forecasting issues.

-

Examine Lease Renewal and Termination Controls:

- Check if lease renewals are reviewed and approved before expiry.

- Verify that terminations are documented and financial impacts accounted for.

- Example: A real estate firm improved lease renewal tracking after auditors identified lapses causing revenue loss.

-

Test Compliance with Regulatory and Accounting Standards:

- Ensure lease accounting complies with IFRS 16 or ASC 842.

- Review audit trails for changes in lease terms.

- Example: Auditors recommended enhanced controls after finding inconsistent lease classification affecting financial statements.

Mind Map: Control Weaknesses and Recommendations

Practical Example: Improving Controls in a Real Estate Company

Scenario: A mid-sized real estate company faced recurring issues with lease renewals being overlooked, resulting in lost rental income and tenant dissatisfaction.

Audit Findings:

- No formal tracking system for lease expiration dates.

- Renewal approvals were often delayed or undocumented.

- Manual processes led to inconsistent rent adjustments.

Actions Taken:

- Implemented a lease management software with automated alerts for upcoming renewals.

- Established a formal approval workflow requiring documented sign-offs.

- Integrated rent escalation clauses into the system to automate recalculations.

Outcome:

- Lease renewals increased by 25% within six months.

- Revenue leakage reduced significantly.

- Improved tenant relationships due to proactive communication.

Summary

Evaluating controls in lease management processes requires a thorough understanding of the lease lifecycle, associated risks, and regulatory requirements. By systematically assessing documentation, rent management, payment processes, renewals, and compliance, internal auditors can identify control gaps and recommend practical improvements. Using mind maps helps visualize complex control areas and focus audit efforts effectively.

This example highlights the importance of integrating technology, formalizing workflows, and continuous monitoring to strengthen lease management controls and safeguard organizational assets.

4.5 Best Practices for Reporting Control Deficiencies

Reporting control deficiencies effectively is critical to ensuring that management understands the risks and takes appropriate corrective actions. Clear, concise, and actionable reports help bridge the gap between auditors and stakeholders, fostering transparency and continuous improvement.

Key Best Practices for Reporting Control Deficiencies

Reporting Control Deficiencies Mind Map

Detailed Explanation with Examples

-

Clarity & Conciseness

- Use straightforward language to describe the deficiency.

- Example: Instead of “The internal control environment exhibits weaknesses in segregation of duties,” say “The same employee approves and processes vendor payments, increasing risk of error or fraud.”

-

Prioritization

- Categorize deficiencies by severity to help management focus on the most critical issues first.

- Example: Label a missing approval on a $1 million transaction as “High Risk,” while a minor documentation lapse could be “Low Risk.”

-

Evidence-Based Findings

- Support your findings with concrete evidence such as transaction samples, screenshots, or audit logs.

- Example: “Out of 50 lease agreements reviewed, 12 lacked proper authorization signatures, as shown in Appendix A.”

-

Actionable Recommendations

- Provide clear steps to remediate the deficiency.

- Example: “Implement a dual-approval process for all vendor payments exceeding $10,000 by Q3 2024. Assign responsibility to the Finance Manager.”

-

Impact Explanation

- Explain why the deficiency matters.

- Example: “Without proper segregation of duties, there is an increased risk of unauthorized payments leading to financial loss.”

-

Balanced Tone

- Maintain professionalism to encourage cooperation.

- Example: Use phrases like “Opportunity for improvement” instead of “Failure to comply.”

-

Follow-Up Mechanism

- Define how and when the issue will be re-evaluated.

- Example: “A follow-up audit will be conducted in six months to verify implementation of recommended controls.”

-

Stakeholder Communication

- Tailor the report to the audience’s level of understanding.

- Example: Provide a high-level summary for the Audit Committee and detailed findings for operational managers.

Example Report Snippet

Control Deficiency: Lack of Segregation of Duties in Vendor Payment Process

Description: The same employee is responsible for both approving and processing vendor payments, which increases the risk of unauthorized or fraudulent transactions.

Risk Level: High

Evidence: Review of 30 payment transactions showed 100% were approved and processed by the same individual (see Appendix B).

Impact: This control weakness could lead to financial loss and reputational damage if fraudulent payments occur.

Recommendation: Implement a dual-approval process where one employee approves payments and another processes them. Assign the Finance Manager to oversee implementation by September 30, 2024.

Follow-Up: A follow-up audit will be conducted in Q4 2024 to assess compliance.

Tone: This presents an opportunity to strengthen internal controls and reduce risk exposure.

By integrating these best practices, internal auditors can deliver reports that not only highlight deficiencies but also drive meaningful improvements within finance and real estate organizations.

5. Reporting Audit Findings

5.1 Structuring Clear and Concise Audit Reports

An effective audit report is a critical communication tool that conveys the results of the internal audit in a clear, concise, and actionable manner. For accountants and auditors in finance and real estate sectors, structuring the audit report properly ensures that stakeholders understand the findings, risks, and recommendations, facilitating timely decision-making and corrective actions.

Key Components of a Clear and Concise Audit Report

Detailed Explanation of Each Component

-

Introduction

- Clearly state the purpose of the audit (e.g., compliance, operational efficiency).

- Define the scope and boundaries (departments, processes, time frame).

- Example: “This audit covers lease management processes from January to June 2024 to assess compliance with internal controls and regulatory requirements.”

-

Executive Summary

- Provide a snapshot of the most critical findings.

- Summarize the overall audit opinion (e.g., satisfactory, needs improvement).

- Highlight key recommendations.

- Example: “The audit identified significant control gaps in rent collection processes, exposing the company to potential revenue leakage. Immediate corrective actions are recommended.”

-

Detailed Findings

- Present each observation with clarity.

- Use a consistent format: Observation, Criteria, Cause, Effect, Recommendation.

- Include management’s response and action plans.

- Example:

- Observation: Inadequate segregation of duties in payment processing.

- Criteria: Company policy requires separation of payment initiation and approval.

- Cause: Limited staffing led to overlapping responsibilities.

- Effect: Increased risk of unauthorized payments.

- Recommendation: Assign distinct roles to different employees to strengthen controls.

-

Conclusion

- Recap audit objectives and whether they were met.

- Provide final thoughts on the audit’s impact.

-

Appendices

- Attach relevant documents, data analysis, or definitions.

Best Practices for Writing Audit Reports

Example: Clear and Concise Audit Report Excerpt

Executive Summary:

The internal audit of the accounts payable process revealed that while invoice approvals are generally timely, there is a lack of formal documentation for vendor verification, increasing the risk of fraudulent payments. We recommend implementing a standardized vendor onboarding checklist and periodic vendor audits.

Detailed Finding:

- Observation: Vendor verification procedures are informal and inconsistent.

- Criteria: Company policy mandates documented verification for all new vendors.

- Cause: Absence of a formal checklist and training.

- Effect: Potential exposure to fraudulent or unqualified vendors.

- Recommendation: Develop and enforce a vendor onboarding checklist; train staff accordingly.

- Management Response: Agreed. The procurement team will implement the checklist by Q3 2024.

Tips for Enhancing Readability

- Use bullet points and numbered lists for clarity.

- Break long paragraphs into smaller sections.

- Highlight key terms in bold or italics.

- Use consistent formatting throughout the report.

By following these structured guidelines and incorporating real-world examples, auditors can produce reports that not only inform but also drive meaningful improvements within finance and real estate organizations.

5.2 Prioritizing Findings Based on Risk and Impact

Prioritizing audit findings is a critical step in ensuring that internal audit efforts are focused on the most significant risks and issues that could affect the organization’s objectives. By assessing the risk and impact associated with each finding, auditors can help management allocate resources effectively and address vulnerabilities that pose the greatest threat.

Why Prioritize Findings?

- Efficient Resource Allocation: Focus on high-risk areas that could cause significant financial loss or reputational damage.

- Effective Risk Mitigation: Address critical control weaknesses before they escalate.

- Clear Communication: Help management understand which issues require immediate attention.

Key Factors in Prioritization

- Risk Likelihood: How probable is the risk event?

- Impact Severity: What is the potential consequence if the risk materializes?

- Control Environment: Are there existing controls mitigating the risk?

- Regulatory and Compliance Implications: Does the finding relate to legal or regulatory requirements?

- Financial Impact: Potential monetary loss or cost.

- Operational Impact: Effect on business processes or service delivery.

Mind Map: Prioritizing Audit Findings

Step-by-Step Approach to Prioritization

- Identify and Document Findings: Collect all audit observations with detailed descriptions.

- Assess Risk Likelihood: Evaluate how often the risk might occur based on historical data or expert judgment.

- Evaluate Impact Severity: Determine the potential damage or loss if the risk occurs.

- Consider Control Effectiveness: Review if existing controls reduce the risk.

- Assign Priority Levels: Categorize findings into High, Medium, or Low priority.

- Communicate Priorities: Clearly present prioritized findings in the audit report.

Example: Prioritizing Findings in a Real Estate Audit

Scenario: During an internal audit of a real estate company’s lease management process, several findings were identified:

| Finding ID | Description | Risk Likelihood | Impact Severity | Control Effectiveness | Priority |

|---|---|---|---|---|---|

| F1 | Missing lease agreement documentation | Medium | High | Low | High |

| F2 | Delayed rent payment tracking | High | Medium | Medium | Medium |

| F3 | Minor discrepancies in utility expense reports | Low | Low | High | Low |

Explanation:

- F1 is prioritized as High because missing documentation can lead to legal disputes and financial loss.

- F2 is Medium priority due to frequent delays but partially mitigated by existing controls.

- F3 is Low priority as discrepancies are minor and controls are effective.

Mind Map: Example Prioritization for Real Estate Audit Findings

Best Practices for Prioritizing Findings

- Use a Risk Matrix to visually map likelihood vs. impact.

- Engage with stakeholders to understand business context.

- Regularly update priorities as new information emerges.

- Document the rationale behind prioritization decisions.

- Integrate prioritization with audit follow-up to track remediation.

Example: Risk Matrix for Prioritization

| Impact \ Likelihood | Low | Medium | High |

|---|---|---|---|

| High | Medium Priority | High Priority | High Priority |

| Medium | Low Priority | Medium Priority | High Priority |

| Low | Low Priority | Low Priority | Medium Priority |

Summary

Prioritizing audit findings based on risk and impact ensures that internal audit resources are directed towards the most critical issues. This approach not only enhances the value of the audit function but also supports management in making informed decisions to strengthen controls and mitigate risks effectively.

5.3 Communicating with Management and the Audit Committee

Effective communication with management and the audit committee is a cornerstone of successful internal auditing. It ensures that audit findings are understood, risks are appropriately addressed, and recommendations are implemented. This section explores best practices for communication, supported by mind maps and practical examples.

Key Objectives of Communication

- Ensure transparency and clarity of audit findings

- Facilitate timely decision-making and corrective actions

- Build trust and credibility between auditors, management, and the audit committee

- Promote a culture of continuous improvement and risk awareness

Mind Map: Communication Flow in Internal Audit

Best Practices for Communicating with Management

-

Know Your Audience

- Tailor communication style and detail level based on the management role.

- Example: Senior executives prefer high-level summaries with key risks, while operational managers need detailed findings.

-

Be Clear and Concise

- Use straightforward language avoiding jargon.

- Highlight key risks, impacts, and recommended actions.

-

Use Visual Aids

- Incorporate charts, graphs, and dashboards to illustrate trends and control gaps.

- Example: A heat map showing risk severity across departments.

-

Engage in Two-Way Dialogue

- Encourage questions and clarifications.

- Schedule follow-up meetings to discuss progress.

-

Provide Actionable Recommendations

- Recommendations should be specific, measurable, achievable, relevant, and time-bound (SMART).

Mind Map: Effective Communication with Management

Best Practices for Communicating with the Audit Committee

-

Provide Executive Summaries

- Summarize audit scope, key findings, and risk implications.

- Example: A one-page dashboard highlighting top 3 risks and their mitigation status.

-

Be Objective and Balanced

- Present both strengths and areas for improvement.

- Avoid overly technical language.

-

Highlight Strategic Risks

- Link audit findings to organizational objectives and strategic risks.

-

Prepare for Questions

- Anticipate concerns and have supporting data ready.

-

Ensure Timely Reporting

- Deliver reports aligned with the audit committee’s meeting schedule.

Mind Map: Communicating with the Audit Committee

Example Scenario: Communicating a Significant Control Deficiency

Context: During an audit of lease management processes in a real estate firm, auditors identified a significant control deficiency related to unauthorized lease modifications.

Communication to Management:

- Delivered a detailed report outlining the deficiency, potential financial impact, and risk of regulatory non-compliance.

- Included a heat map showing the frequency and severity of unauthorized changes.

- Recommended implementing automated approval workflows and periodic reconciliations.

- Scheduled a workshop with the lease management team to discuss findings and action plans.

Communication to Audit Committee:

- Presented an executive summary highlighting the risk to revenue recognition and compliance.

- Emphasized the strategic importance of strengthening controls to protect company assets.

- Provided a timeline for remediation and follow-up audit plans.

- Addressed committee questions regarding resource allocation and monitoring.

Summary

Effective communication with management and the audit committee requires clarity, relevance, and engagement. By tailoring messages, using visual tools, and fostering dialogue, auditors can ensure their findings lead to meaningful improvements and strengthen organizational governance.

5.4 Example: Crafting Actionable Recommendations for a Finance Department

Crafting actionable recommendations is a critical step in the internal audit process. It ensures that audit findings translate into practical improvements that management can implement effectively. Below is a detailed guide, supported by mind maps and examples, to help auditors develop clear, concise, and actionable recommendations for a finance department.

Understanding the Problem

Before crafting recommendations, fully understand the root cause of the issue identified during the audit.

Mind Map: Understanding the Problem

Example:

Finding: Delays in monthly financial close process causing late reporting.

Root Cause: Manual data consolidation from multiple systems without standardized procedures.

Characteristics of Actionable Recommendations

Recommendations should be: