Financial Statement Auditing

1. Introduction to Financial Statement Auditing

1.1 Purpose and Importance of Financial Statement Audits

Financial statement audits serve as a cornerstone in ensuring the integrity, transparency, and reliability of financial information presented by organizations. They provide stakeholders—including investors, regulators, management, and the public—with confidence that the financial statements fairly represent the entity’s financial position and performance.

Mind Map: Purpose of Financial Statement Audits

Why Are Financial Statement Audits Important?

-

Enhance Credibility and Trust: Audited financial statements reduce information asymmetry between management and stakeholders, fostering trust.

-

Ensure Compliance: Audits verify that organizations comply with relevant accounting frameworks and legal requirements, reducing the risk of penalties.

-

Detect and Prevent Fraud: Through systematic examination, audits help uncover irregularities or fraudulent activities that could distort financial reporting.

-

Improve Internal Controls: Auditors assess the effectiveness of internal control systems, providing recommendations to strengthen financial processes.

-

Support Decision-Making: Reliable financial information enables investors, creditors, and government agencies to make informed decisions.

-

Promote Accountability: Audits hold management accountable for the stewardship of resources, especially critical in government and public sector entities.

Example 1: Audit in a Government Agency

A government agency responsible for public infrastructure submits its annual financial statements. An independent audit is conducted to ensure that public funds are accurately reported and used appropriately. The audit uncovers a minor misclassification of expenses, which the agency promptly corrects, thereby maintaining public trust and ensuring compliance with governmental accounting standards.

Example 2: Audit Impact on a Private Company

A mid-sized manufacturing company seeks a bank loan for expansion. The bank requires audited financial statements to assess creditworthiness. The audit confirms the company’s financial health, enabling the loan approval. Additionally, the audit identifies weaknesses in inventory controls, allowing management to implement improvements that reduce future risks.

Mind Map: Importance of Financial Statement Audits

In summary, financial statement audits are vital for maintaining the health and sustainability of both private and public sector organizations. They provide a structured, independent review that enhances the reliability of financial information, ultimately supporting economic stability and growth.

1.2 Overview of the Auditing Process

Financial statement auditing is a structured process designed to provide reasonable assurance that an organization’s financial statements are free from material misstatement, whether due to error or fraud. Understanding the auditing process is fundamental for accountants and auditors to execute their duties effectively.

Key Phases of the Auditing Process

The auditing process can be broadly divided into the following phases:

- Planning

- Risk Assessment

- Internal Controls Evaluation

- Substantive Testing

- Audit Evidence Collection

- Reporting

Below is a mind map illustrating these phases and their interconnections:

Auditing Process Mind Map

Detailed Explanation of Each Phase with Examples

Planning

Planning sets the foundation for an effective audit. Auditors gather preliminary information about the client’s business, industry, and environment. They define the audit scope and determine materiality thresholds.

Example: For a government finance department, the auditor reviews the department’s budget reports and prior audit findings to understand key focus areas such as grant management and procurement.

Risk Assessment

Auditors identify areas where financial misstatements are most likely to occur. They assess inherent risk (risk without controls) and control risk (risk that controls fail).

Example: In auditing a municipal government, the auditor identifies high risk in revenue recognition from property taxes due to complex billing cycles.

Internal Controls Evaluation

Auditors evaluate the design and effectiveness of internal controls to determine the extent of substantive testing required.

Example: Testing controls over payroll processing in a government agency by reviewing authorization procedures and payroll reconciliations.

Substantive Testing

This phase involves detailed testing of transactions and balances to detect material misstatements.

Example: Performing sample testing of vendor invoices and matching them with purchase orders and payment records to verify accuracy.

Audit Evidence Collection

Gathering sufficient and appropriate evidence is critical. This includes inspection of documents, confirmations from third parties, physical observations, and recalculations.

Example: Confirming bank balances directly with financial institutions to validate cash balances reported in the financial statements.

Reporting

The final phase involves compiling findings into an audit report, including the auditor’s opinion on the financial statements.

Example: Issuing an unqualified opinion for a government agency after concluding that the financial statements present a true and fair view.

Mind Map: Example of Audit Evidence Types

Integrated Example: Auditing a Government Grant

- Planning: Understand grant terms and compliance requirements.

- Risk Assessment: Identify risk of non-compliance or misstatement in grant revenue.

- Internal Controls: Evaluate controls over grant application and fund disbursement.

- Substantive Testing: Verify grant receipts and expenditures against supporting documents.

- Evidence Collection: Obtain confirmations from grantor and inspect related contracts.

- Reporting: Highlight any compliance issues or financial misstatements in the audit report.

By following this structured auditing process, auditors in finance and government sectors can ensure thoroughness, accuracy, and compliance, ultimately enhancing the credibility of financial statements.

1.3 Key Roles and Responsibilities of Auditors

Financial statement auditors play a critical role in ensuring the accuracy, reliability, and transparency of financial information. Their responsibilities extend beyond just verifying numbers—they help build trust in financial reporting, support regulatory compliance, and contribute to the overall governance of organizations.

Core Roles of Auditors

- Independent Examiner: Auditors provide an unbiased evaluation of financial statements to ensure they fairly represent the financial position and performance of an entity.

- Risk Assessor: They identify and assess risks of material misstatement due to error or fraud.

- Internal Controls Evaluator: Auditors review and test the effectiveness of an entity’s internal control systems.

- Evidence Gatherer: They collect sufficient and appropriate audit evidence to support their conclusions.

- Communicator: Auditors communicate findings, deficiencies, and recommendations to management, audit committees, and stakeholders.

Detailed Responsibilities

-

Planning the Audit:

- Understand the client’s business, industry, and environment.

- Assess risks and determine materiality levels.

- Develop an audit plan tailored to identified risks.

-

Conducting Fieldwork:

- Test internal controls through walkthroughs and sampling.

- Perform substantive testing on account balances and transactions.

- Use analytical procedures to identify unusual trends or inconsistencies.

-

Gathering and Evaluating Evidence:

- Obtain audit evidence from documents, confirmations, observations, and inquiries.

- Evaluate the sufficiency and appropriateness of evidence.

-

Reporting:

- Prepare audit reports expressing an opinion on the financial statements.

- Highlight any material misstatements or control weaknesses.

-

Ethical Compliance:

- Maintain independence and objectivity.

- Uphold confidentiality and professional skepticism.

Mind Map: Key Roles of Auditors

Mind Map: Responsibilities During Audit Phases

Example 1: Role as Independent Examiner

An auditor assigned to a municipal government reviews the financial statements to ensure that reported revenues from property taxes and grants are accurate. By independently verifying these figures against supporting documentation and third-party confirmations, the auditor helps stakeholders trust the municipality’s financial health.

Example 2: Risk Assessment Responsibility

While auditing a government healthcare agency, the auditor identifies a high risk of misstatement in payroll expenses due to complex overtime calculations. The auditor adjusts the audit plan to include detailed testing of payroll transactions and controls around timekeeping systems.

Example 3: Internal Controls Evaluation

In a financial audit of a state university, the auditor tests controls over procurement processes. By performing walkthroughs and sampling purchase orders, the auditor identifies weaknesses in approval workflows, recommending improvements to reduce fraud risk.

Example 4: Evidence Gathering and Documentation

During an audit of a government department, the auditor obtains bank confirmations directly from financial institutions to verify cash balances, ensuring the evidence is reliable and sufficient to support the audit opinion.

Example 5: Communication of Findings

After completing an audit of a public sector entity, the auditor prepares a report highlighting a material weakness in revenue recognition controls and discusses remediation steps with the audit committee to improve financial reporting accuracy.

In summary, auditors serve as independent watchdogs who not only verify financial data but also assess risks, evaluate controls, gather evidence, and communicate findings effectively. Their multifaceted responsibilities are essential to maintaining confidence in financial statements within both finance and government sectors.

1.4 Regulatory Framework and Standards Governing Audits

Financial statement auditing is governed by a complex web of regulatory frameworks and professional standards designed to ensure consistency, reliability, and transparency in audit processes and reporting. Understanding these frameworks is essential for auditors working in both the finance and government sectors.

Key Regulatory Bodies and Frameworks

-

International Auditing and Assurance Standards Board (IAASB)

- Develops International Standards on Auditing (ISAs)

- Widely adopted globally, including by many government audit institutions

-

Public Company Accounting Oversight Board (PCAOB)

- Oversees audits of public companies in the United States

- Sets auditing standards and inspects audit firms

-

Government Accountability Office (GAO)

- Issues Government Auditing Standards (Yellow Book) for U.S. federal audits

- Focuses on audits of government entities and programs

-

Financial Accounting Standards Board (FASB)

- Sets accounting standards (US GAAP) which auditors verify compliance with

-

International Public Sector Accounting Standards Board (IPSASB)

- Develops standards for public sector accounting and auditing

Mind Map: Regulatory Framework Overview

International Standards on Auditing (ISAs)

ISAs provide a globally accepted framework for conducting high-quality audits. They cover all phases of the audit including planning, risk assessment, evidence gathering, and reporting.

Example:

- When auditing a multinational corporation, auditors follow ISAs to ensure consistency across different countries.

- ISA 315 requires auditors to identify and assess risks of material misstatement, which guides the entire audit strategy.

Government Auditing Standards (The Yellow Book)

The GAO’s Yellow Book provides standards specifically tailored for audits of government organizations, programs, activities, and functions.

Key Features:

- Emphasizes auditor independence and professional judgment

- Includes requirements for quality control and continuing professional education

Example:

- Auditing a state government’s financial statements requires adherence to the Yellow Book to ensure compliance with federal and state regulations.

PCAOB Standards

The PCAOB sets auditing standards for public company audits in the U.S., focusing on investor protection and audit quality.

Example:

- Auditors of a publicly traded financial institution must comply with PCAOB standards, including rigorous documentation and internal control testing.

Mind Map: Standards Application by Sector

Compliance and Enforcement

Auditors must not only understand these standards but also ensure strict compliance. Regulatory bodies conduct inspections and reviews to enforce adherence.

Example:

- A government auditor failing to comply with the Yellow Book may face sanctions or removal from audit engagements.

Summary

Understanding the regulatory framework and standards governing audits is foundational for auditors. It ensures audits are performed with integrity, consistency, and in accordance with legal and professional requirements.

Additional Example: Applying Standards in a Government Audit

Imagine auditing the financial statements of a city municipality. The auditor:

- Uses the Yellow Book to guide audit planning and reporting

- Applies IPSAS for public sector accounting principles

- Conducts risk assessments per ISA 315

- Documents findings in compliance with PCAOB documentation standards (if applicable)

This integrated approach ensures the audit meets all relevant regulatory and professional standards.

1.5 Common Challenges in Financial Statement Auditing

Financial statement auditing is a complex process that often presents auditors with various challenges. Understanding these common obstacles helps auditors prepare better strategies to ensure audit quality and compliance. Below, we explore key challenges, supported by mind maps and practical examples.

Challenge 1: Understanding Complex Financial Transactions

Auditors frequently encounter intricate financial transactions that require deep knowledge and expertise to interpret correctly.

- Mind Map: Understanding Complex Transactions

Example: An auditor reviewing a government entity’s lease agreements must distinguish between operating and finance leases under new accounting standards (e.g., GASB 87). Misclassification can lead to misstated liabilities and assets.

Challenge 2: Assessing and Testing Internal Controls

Evaluating the effectiveness of internal controls is critical but challenging due to the diversity and complexity of control environments.

- Mind Map: Internal Controls Challenges

Example: During an audit of a finance department, the auditor finds that segregation of duties is not properly implemented, increasing the risk of fraud. The auditor must design additional substantive procedures to compensate.

Challenge 3: Managing Audit Evidence Collection

Gathering sufficient, appropriate audit evidence can be difficult, especially when dealing with electronic records or third-party confirmations.

- Mind Map: Audit Evidence Challenges

Example: An auditor requests bank confirmations for cash balances but faces delays due to the bank’s internal policies. To mitigate this, the auditor uses alternative procedures such as reviewing bank statements and reconciliations.

Challenge 4: Detecting and Addressing Fraud Risks

Fraud is often concealed and requires auditors to be vigilant and skeptical throughout the audit.

- Mind Map: Fraud Risk Challenges

Example: In a government audit, unusual spikes in grant expenditures trigger suspicion. The auditor performs detailed transaction testing and uncovers fictitious vendor payments.

Challenge 5: Keeping Up with Regulatory Changes and Standards

Frequent updates to accounting and auditing standards require auditors to continuously update their knowledge and audit approaches.

- Mind Map: Regulatory and Standards Challenges

Example: An auditor must adapt audit procedures to comply with the latest GASB standards on revenue recognition, requiring additional training and revision of audit checklists.

Challenge 6: Time and Resource Constraints

Auditors often face tight deadlines and limited resources, which can impact the thoroughness of the audit.

- Mind Map: Time and Resource Constraints

Example: Due to a compressed audit timeline, the audit team prioritizes high-risk areas but must communicate the scope limitations clearly in the audit report.

Summary

Financial statement auditing involves navigating multiple challenges ranging from technical complexities to operational constraints. By understanding these challenges and applying best practices, auditors can enhance audit quality and deliver reliable financial insights.

2. Planning the Audit Engagement

2.1 Understanding the Client’s Business and Industry

Understanding the client’s business and industry is a foundational step in planning an effective financial statement audit. This knowledge enables auditors to identify key risk areas, tailor audit procedures, and provide valuable insights. Without a deep understanding of the client’s environment, auditors risk overlooking significant issues or misinterpreting financial data.

Why is Understanding the Client’s Business Important?

- Risk Identification: Different industries have unique risks. For example, a manufacturing company faces inventory valuation risks, while a government agency may have compliance risks related to grant funding.

- Tailored Audit Procedures: Knowing the business helps in designing relevant audit tests that focus on critical areas.

- Improved Communication: Understanding the client’s operations facilitates clearer discussions with management and stakeholders.

- Regulatory Compliance: Different industries are subject to different regulations which impact financial reporting.

Key Areas to Understand About the Client’s Business

Industry Context

Understanding the industry helps auditors anticipate common challenges and risks.

- Market Trends: For example, in the renewable energy sector, rapid technological changes and government incentives significantly impact financials.

- Regulatory Environment: Government agencies must comply with specific grant reporting requirements and budgetary constraints.

- Competitors: Knowing competitors helps assess market position and potential financial pressures.

Example: When auditing a public transportation authority, auditors must understand federal and state funding mechanisms, fare structures, and regulatory compliance related to safety and environmental standards.

Business Model

Understanding how the client generates revenue and incurs costs is critical.

- Revenue Streams: Are revenues from sales, grants, service fees, or a combination?

- Cost Structure: Fixed vs. variable costs, major expense categories.

- Key Products/Services: What drives the business? For example, a government agency may provide social services funded by multiple grants.

Example: An auditor working with a municipal water utility should understand billing cycles, rate structures, and capital investment plans.

Operational Processes

Mapping out core processes helps identify where errors or fraud might occur.

- Supply Chain: How are materials procured and inventoried?

- Sales Cycle: Order processing, invoicing, and collections.

- Production: Manufacturing steps, quality control.

Example: In auditing a government construction project, understanding contract management and progress billing is essential.

Financial Environment

Understanding the client’s accounting policies and financial health guides audit focus.

- Accounting Policies: Revenue recognition methods, depreciation policies.

- Funding Sources: Loans, grants, taxes.

- Financial Health: Liquidity, solvency, and profitability indicators.

Example: For a non-profit organization, auditors must understand donor restrictions and fund accounting.

Risks

Identifying risks specific to the client’s business and industry helps prioritize audit efforts.

- Industry-specific Risks: For example, healthcare entities face risks related to patient billing and regulatory compliance.

- Operational Risks: Process inefficiencies, fraud risks.

- Compliance Risks: Adherence to laws and regulations.

Example: Auditing a government agency that manages federal grants requires assessing risks of misallocation or non-compliance.

Practical Example: Understanding a Government Agency Client

Scenario: Auditing the financial statements of a state environmental protection agency.

- Industry Context: Subject to environmental regulations, funding from state and federal grants.

- Business Model: Provides regulatory oversight and environmental programs.

- Operational Processes: Grant management, contract administration, enforcement activities.

- Financial Environment: Multiple funding sources, restricted funds.

- Risks: Compliance with grant terms, revenue recognition of government appropriations.

This understanding informs audit procedures such as verifying grant expenditures, testing compliance with funding restrictions, and assessing revenue recognition.

Summary

A comprehensive understanding of the client’s business and industry is essential for effective audit planning and execution. It enables auditors to:

- Identify and assess risks accurately.

- Tailor audit procedures to client-specific circumstances.

- Communicate effectively with client management.

- Ensure compliance with relevant standards and regulations.

By integrating this knowledge early in the audit process, auditors enhance the quality and relevance of their work, ultimately providing greater assurance to stakeholders.

2.2 Risk Assessment and Materiality Determination

Overview

Risk assessment and materiality determination are foundational steps in planning an effective financial statement audit. They help auditors focus their efforts on areas with higher risk of material misstatement and ensure that audit resources are used efficiently.

Risk Assessment

Risk assessment involves identifying and analyzing risks that could lead to material misstatements in the financial statements, whether due to error or fraud.

Key Components of Risk Assessment:

- Inherent Risk: The susceptibility of an assertion to a misstatement before considering controls.

- Control Risk: The risk that a misstatement could occur and not be prevented or detected by internal controls.

- Detection Risk: The risk that audit procedures will not detect a material misstatement.

Mind Map: Risk Assessment Components

Example: Assessing Risk in a Government Grant Program

A government auditor is assessing the financial statements of a department managing multiple grant programs. The inherent risk is high due to complex compliance requirements and frequent changes in regulations. Control risk is moderate because the department has recently implemented new internal controls. Detection risk is managed by planning detailed substantive procedures.

Materiality Determination

Materiality is the threshold above which missing or incorrect information in financial statements is considered significant enough to influence decisions of users.

Factors Influencing Materiality:

- Quantitative factors such as size of the entity, total assets, revenues, or net income.

- Qualitative factors including nature of the item, regulatory requirements, or user expectations.

Mind Map: Materiality Determination

Example: Setting Materiality for a Municipal Audit

For a municipal government with $500 million in annual expenditures, the auditor sets materiality at 1% of total expenditures ($5 million). However, due to public sensitivity around certain programs, the auditor applies a lower performance materiality for those areas to ensure more thorough testing.

Integrated Approach: Combining Risk Assessment and Materiality

Auditors use risk assessment to identify high-risk areas and apply materiality thresholds to determine the extent of audit procedures.

Mind Map: Integrated Risk and Materiality Approach

Example: Audit Planning for a State Department

An auditor identifies payroll expenses as a high inherent risk area due to prior errors. Materiality for payroll is set lower than overall materiality to ensure detailed testing. The auditor plans additional substantive procedures and control testing focused on payroll transactions.

Best Practices

- Use a combination of quantitative and qualitative factors when determining materiality.

- Continuously update risk assessment as new information arises during the audit.

- Document all judgments and rationale for risk and materiality decisions.

- Engage with management and audit committees to understand areas of concern.

Summary

Effective risk assessment and materiality determination enable auditors to design focused and efficient audit procedures. By understanding where material misstatements are most likely, auditors can allocate resources wisely and enhance audit quality.

References

- International Standards on Auditing (ISA) 315: Identifying and Assessing the Risks of Material Misstatement

- ISA 320: Materiality in Planning and Performing an Audit

- Government Auditing Standards (Yellow Book)

2.3 Developing the Audit Strategy and Audit Plan

Developing a robust audit strategy and detailed audit plan is a critical step in ensuring a successful financial statement audit. This phase sets the foundation for how the audit will be conducted, focusing resources efficiently, addressing risks, and complying with regulatory requirements.

What is an Audit Strategy?

An audit strategy is a high-level approach that outlines the scope, timing, and direction of the audit. It considers the nature of the client’s business, risk factors, and the auditor’s objectives.

What is an Audit Plan?

The audit plan is a detailed roadmap derived from the audit strategy, specifying the nature, timing, and extent of audit procedures to be performed.

Key Components of Developing the Audit Strategy and Plan

- Understanding the entity and its environment

- Assessing risks of material misstatement

- Determining materiality levels

- Deciding on the nature, timing, and extent of audit procedures

- Allocating resources and assigning responsibilities

Mind Map: Developing the Audit Strategy and Plan

Step-by-Step Process

Understanding the Client

Before planning, auditors must gain a deep understanding of the client’s business, industry trends, regulatory environment, and internal processes.

Example: For a government finance department, understanding budget cycles, grant funding sources, and compliance requirements is essential.

Risk Assessment

Identify areas where material misstatements could occur due to error or fraud.

- Inherent Risk: Complexity of transactions, new accounting standards.

- Control Risk: Effectiveness of internal controls.

- Fraud Risk: Incentives or pressures to manipulate financials.

Example: A government agency receiving multiple grants may have higher inherent risk in revenue recognition.

Determining Materiality

Set thresholds for what is considered material to the financial statements.

- Overall materiality guides the audit scope.

- Performance materiality helps in designing tests.

Example: For a mid-sized municipal entity, overall materiality might be set at 1% of total expenditures.

Designing Audit Procedures

Decide on the nature (type), timing (when), and extent (how much) of audit procedures.

- Test of Controls: To evaluate if controls are operating effectively.

- Substantive Procedures: To detect material misstatements.

Example: If controls over procurement are strong, the auditor may reduce substantive testing on related expenses.

Resource Allocation

Assign audit team members based on expertise and availability.

- Schedule fieldwork and deadlines.

Example: Assign an auditor with IT audit experience to review electronic financial systems.

Documentation

Prepare an audit program outlining all planned procedures and maintain records of risk assessments.

Example Scenario: Developing an Audit Plan for a Government Grant Audit

Context: Auditing a government department that manages multiple federal grants.

- Understanding Client: Review grant agreements, compliance requirements, and financial reporting deadlines.

- Risk Assessment: High risk in grant revenue recognition and compliance with spending restrictions.

- Materiality: Set at 2% of total grant revenue.

- Audit Procedures:

- Test controls over grant approval and disbursement.

- Perform substantive testing on grant expenditures.

- Analytical procedures comparing grant revenue trends year-over-year.

- Resource Allocation: Assign team members with grant compliance experience.

- Documentation: Develop a detailed audit program specifying tests for each grant.

Additional Mind Map: Audit Procedures Design

Tips for Effective Audit Strategy and Planning

- Engage with client management early to clarify expectations.

- Use prior year audit findings to inform risk assessment.

- Incorporate technology tools to streamline planning and documentation.

- Regularly update the audit plan as new information emerges.

Developing a comprehensive audit strategy and plan ensures that auditors focus on the most significant risks, allocate resources efficiently, and deliver high-quality audit outcomes. Integrating real-world examples and structured mind maps helps auditors visualize and implement best practices effectively.

2.4 Establishing Timelines and Resource Allocation

Effective audit planning hinges on establishing clear timelines and allocating resources efficiently. This ensures the audit progresses smoothly, meets deadlines, and maintains quality standards.

Importance of Timelines and Resource Allocation

- Timelines help manage client expectations and coordinate audit team activities.

- Resource allocation ensures the right skills and manpower are assigned to audit tasks, optimizing productivity and risk coverage.

Steps to Establish Timelines

-

Understand the Scope and Complexity

- Review audit scope and identify high-risk areas.

- Determine the volume of transactions and complexity of accounts.

-

Set Key Milestones

- Planning completion

- Fieldwork start and end dates

- Draft report preparation

- Final report issuance

-

Consider External Deadlines

- Regulatory filing dates

- Client reporting requirements

-

Build in Contingency Time

- Account for unexpected delays or additional procedures.

Mind Map: Establishing Audit Timelines

Resource Allocation Best Practices

- Identify Required Skills: Match audit tasks with team members’ expertise (e.g., IT audit specialists for system controls).

- Determine Team Size: Balance workload to avoid burnout and ensure thoroughness.

- Assign Roles Clearly: Define responsibilities such as lead auditor, field auditors, and quality reviewers.

- Leverage Technology: Utilize audit software to reduce manual effort.

Mind Map: Resource Allocation in Auditing

Example: Establishing Timelines and Resource Allocation for a Government Agency Audit

Scenario: Auditing the annual financial statements of a mid-sized government agency with a 3-month deadline.

-

Timeline Setup:

- Planning: 2 weeks

- Fieldwork: 6 weeks

- Draft report: 2 weeks

- Final report: 2 weeks

- Contingency: 1 week buffer included within fieldwork

-

Resource Allocation:

- Lead Auditor: Oversees entire audit

- 2 Field Auditors: Conduct transaction testing and control evaluation

- IT Specialist: Reviews internal control systems

- Data Analyst: Supports substantive testing with data analytics

-

Outcome:

- Clear deadlines communicated to the team and client

- Balanced workload with specialized roles

- Use of audit software to streamline testing

Tips for Successful Implementation

- Regularly review progress against the timeline.

- Adjust resource allocation dynamically if delays or issues arise.

- Communicate proactively with the client and audit team.

By carefully establishing timelines and allocating resources, auditors can enhance efficiency, reduce risks, and deliver high-quality audit reports on schedule.

2.5 Example: Planning an Audit for a Government Agency Financial Statement

Planning an audit for a government agency financial statement requires a tailored approach that considers the unique regulatory environment, funding sources, and public accountability aspects. This section will walk through a detailed example of how to plan such an audit, integrating best practices and practical examples.

Step 1: Understand the Entity and Its Environment

- Objective: Gain a comprehensive understanding of the government agency’s operations, funding, and regulatory framework.

- Example: Suppose the agency is a state transportation department responsible for managing highways and public transit.

Key considerations:

- Funding sources (state budget allocations, federal grants, user fees)

- Regulatory compliance requirements (Government Accounting Standards Board - GASB)

- Organizational structure and key personnel

Mind Map: Understanding the Entity

Step 2: Assess Risks and Materiality

- Objective: Identify areas with higher risk of misstatement and determine materiality thresholds.

- Example: The agency receives multiple federal grants with strict compliance requirements, increasing risk in grant revenue recognition.

Risk factors to consider:

- Complexity of grant agreements

- Changes in funding levels

- Prior audit findings

Materiality:

- Quantitative: Set materiality based on total budget or expenditures (e.g., 1% of total expenditures)

- Qualitative: Consider public interest and sensitivity of certain programs

Mind Map: Risk Assessment & Materiality

Step 3: Develop the Audit Strategy and Plan

- Objective: Outline the overall approach, including the nature, timing, and extent of audit procedures.

Example:

- Plan to perform substantive testing on grant revenues and expenditures.

- Schedule interim testing to review internal controls over procurement.

Key components:

- Scope of audit (financial statements and compliance)

- Timing (interim vs. year-end procedures)

- Resource allocation (assign specialists for grant compliance)

Mind Map: Audit Strategy & Plan

Step 4: Establish Communication Protocols

- Objective: Define how the audit team will communicate with agency management and oversight bodies.

Example:

- Schedule entrance and exit conferences.

- Agree on reporting timelines with the audit committee.

Mind Map: Communication Protocols

Step 5: Document the Audit Plan

- Objective: Create a comprehensive audit plan document that includes all the above elements.

Example:

- The audit plan includes detailed procedures for testing grant compliance, timelines, assigned personnel, and risk assessments.

Summary Example: Planning for the State Transportation Department Audit

| Step | Action Item | Example Detail |

|---|---|---|

| Understand Entity | Review organizational chart and funding sources | State appropriations and federal highway grants |

| Assess Risks & Materiality | Identify high-risk grant revenue areas | Federal grants with complex compliance terms |

| Develop Audit Strategy | Schedule interim control testing | Procurement controls testing in Q3 |

| Communication | Set meeting dates with management and oversight | Entrance conference scheduled for July 1 |

| Document Plan | Compile audit plan with assigned responsibilities | Assign grant specialist to revenue testing team |

This example demonstrates how a structured and detailed planning phase sets the foundation for an effective financial statement audit of a government agency. By integrating risk assessment, regulatory considerations, and clear communication, auditors can ensure a focused and efficient audit process.

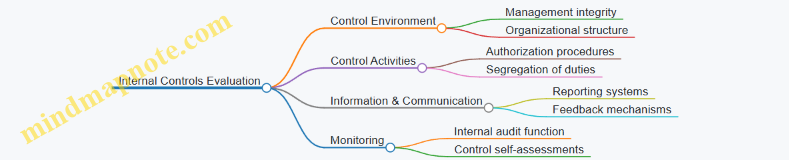

3. Internal Controls Evaluation

3.1 Importance of Internal Controls in Auditing

Internal controls are the backbone of any organization’s financial integrity and operational efficiency. In the context of financial statement auditing, understanding and evaluating internal controls is crucial for auditors to assess the reliability of financial reporting and to design effective audit procedures.

What Are Internal Controls?

Internal controls are processes, policies, and procedures implemented by an organization to ensure the achievement of objectives in the following areas:

- Reliability of financial reporting

- Compliance with applicable laws and regulations

- Effectiveness and efficiency of operations

Why Are Internal Controls Important in Auditing?

- Risk Mitigation: Strong internal controls reduce the risk of material misstatements, whether due to error or fraud.

- Audit Efficiency: When controls are effective, auditors can reduce the extent of substantive testing, focusing efforts where risks are higher.

- Compliance Assurance: Controls help ensure that financial statements comply with accounting standards and regulatory requirements.

- Fraud Prevention and Detection: Controls such as segregation of duties and authorization procedures help prevent and detect fraudulent activities.

Mind Map: Importance of Internal Controls in Auditing

Example: Segregation of Duties in a Government Finance Department

In a government finance department, segregation of duties is a critical internal control. For instance, the person who approves payments should not be the same individual who processes or records those payments. This separation helps prevent unauthorized disbursements and reduces the risk of fraud.

During an audit, the auditor evaluates this control by:

- Reviewing organizational charts and job descriptions.

- Observing workflows and interviewing staff.

- Testing a sample of transactions to verify that duties are appropriately segregated.

If the control is effective, the auditor may reduce detailed testing of payment transactions, focusing instead on controls testing.

Mind Map: Example - Segregation of Duties

Example: Authorization Controls in Expense Reimbursements

An organization requires all employee expense reimbursements to be approved by a manager before payment. This internal control ensures expenses are valid and comply with company policies.

The auditor tests this control by:

- Selecting a sample of expense reimbursements.

- Verifying that each reimbursement has the required approval.

- Checking for compliance with expense policies.

If the control is found to be reliable, the auditor can place reliance on it, potentially reducing the need for extensive substantive testing on expense transactions.

Mind Map: Example - Authorization Controls

Summary

Internal controls form the foundation for a reliable financial reporting system. For auditors, understanding and evaluating these controls is essential to:

- Identify areas of higher risk

- Design efficient and effective audit procedures

- Provide assurance on the accuracy and completeness of financial statements

By integrating examples such as segregation of duties and authorization controls, auditors can better appreciate how internal controls operate in real-world settings and how they impact the audit process.

3.2 Techniques for Assessing Control Environment

The control environment is the foundation of an organization’s internal control system. It sets the tone at the top and influences the control consciousness of its people. Assessing the control environment is critical for auditors to understand the overall risk and design effective audit procedures.

Key Components of the Control Environment

- Integrity and ethical values

- Commitment to competence

- Management’s philosophy and operating style

- Organizational structure

- Assignment of authority and responsibility

- Human resource policies and practices

Techniques for Assessing the Control Environment

Inquiry and Interviews

- Conduct interviews with management and key personnel to understand the tone at the top.

- Ask about ethical standards, communication channels, and management’s attitude towards controls.

Example: An auditor interviews the CFO and internal audit manager to gauge their commitment to ethical financial reporting and how they communicate expectations to staff.

Observation

- Observe the organization’s operations and employee behavior.

- Look for evidence of ethical conduct, adherence to policies, and management oversight.

Example: During a site visit, the auditor notes that employees openly discuss compliance issues and management regularly holds team meetings emphasizing control importance.

Document Review

- Review organizational charts, policies, codes of conduct, and procedural manuals.

- Evaluate whether the documentation supports a strong control environment.

Example: The auditor reviews the company’s code of ethics and notes that it is comprehensive, regularly updated, and distributed to all employees.

Walkthroughs

- Trace transactions through the accounting system to observe control points.

- Verify that controls are embedded in processes and consistently applied.

Example: The auditor performs a walkthrough of the procurement process, observing approval hierarchies and segregation of duties.

Analytical Procedures

- Analyze trends in control-related metrics such as error rates, incident reports, or employee turnover.

- Identify unusual patterns that may indicate control weaknesses.

Example: An auditor notices a spike in expense report exceptions and investigates whether this reflects a lapse in control enforcement.

Mind Map: Techniques for Assessing Control Environment

Integrated Example: Assessing Control Environment in a Government Finance Department

Scenario: An auditor is assigned to assess the control environment of a government finance department responsible for budget management and expenditure.

Steps Taken:

- Inquiry: The auditor interviews the department head and finance officers to understand their commitment to ethical standards and control policies.

- Observation: During on-site visits, the auditor observes regular team briefings where management reinforces compliance and accountability.

- Document Review: The auditor examines the department’s organizational chart, noting clear segregation of duties, and reviews the ethics policy which is prominently displayed.

- Walkthrough: A walkthrough of the budget approval process confirms that multiple levels of approval are required before funds are released.

- Analytical Procedures: The auditor reviews past audit reports and incident logs, finding a low rate of control exceptions over the past year.

Outcome: The auditor concludes that the control environment is strong, supported by management’s ethical tone, well-defined responsibilities, and effective communication.

Summary

Assessing the control environment requires a combination of qualitative and quantitative techniques. By integrating inquiry, observation, document review, walkthroughs, and analytical procedures, auditors can form a comprehensive understanding of the control environment’s strength and its impact on financial statement reliability.

3.3 Testing Control Effectiveness: Walkthroughs and Sampling

Testing the effectiveness of internal controls is a critical step in financial statement auditing. It helps auditors determine whether the controls designed by the organization are operating as intended and can be relied upon to prevent or detect material misstatements.

Walkthroughs: Understanding and Validating Control Processes

A walkthrough is a step-by-step tracing of a transaction from initiation through the accounting system to its inclusion in the financial statements. This process helps auditors gain a deep understanding of the control environment and verify that controls are implemented as described.

Key Objectives of Walkthroughs:

- Confirm the design and implementation of controls

- Identify potential control gaps or weaknesses

- Understand the flow of transactions and data

Mind Map: Walkthrough Process

Example:

Consider an auditor performing a walkthrough of the revenue cycle in a government agency:

- The auditor selects a sample sales transaction.

- They trace the transaction from the receipt of the purchase order, through approval by the finance department, to recording in the accounting system.

- At each stage, the auditor observes controls such as authorization signatures, system access restrictions, and reconciliations.

- The auditor interviews staff to confirm control procedures are consistently applied.

This walkthrough confirms whether controls over revenue recognition are designed and operating effectively.

Sampling: Testing Controls on a Representative Basis

Since it is often impractical to test every transaction or control instance, auditors use sampling techniques to test a subset that represents the entire population.

Types of Sampling:

- Statistical Sampling: Uses probability theory to select and evaluate samples, allowing quantification of sampling risk.

- Non-Statistical Sampling: Based on auditor judgment without formal statistical measures.

Mind Map: Sampling Approach

Example:

An auditor testing controls over invoice approvals might:

- Define the population as all invoices processed in the last quarter.

- Determine a sample size of 40 invoices based on assessed risk.

- Randomly select invoices and verify each has the required approval signatures and supporting documentation.

- Find 2 exceptions where approvals were missing.

- Evaluate whether the exceptions indicate a control weakness or isolated errors.

If exceptions are material or frequent, the auditor may conclude the control is not effective and increase substantive testing.

Integrating Walkthroughs and Sampling

Walkthroughs provide qualitative understanding and validation of control design and implementation, while sampling provides quantitative evidence about control operation over time.

Mind Map: Combined Approach

Example:

In auditing payroll controls:

- The auditor performs a walkthrough to understand the payroll process and control points such as time approval and payroll authorization.

- Then, the auditor samples payroll transactions over several months to test whether controls were consistently applied.

- If walkthroughs show strong design but sampling reveals exceptions, the auditor investigates further to assess risk.

Best Practices for Testing Control Effectiveness

- Clearly document walkthrough procedures and findings.

- Use a risk-based approach to determine sample sizes.

- Combine qualitative insights from walkthroughs with quantitative sampling results.

- Communicate control deficiencies promptly to management.

- Use technology tools to assist in sampling and documentation.

By effectively applying walkthroughs and sampling, auditors can confidently assess the reliability of internal controls, reducing audit risk and enhancing the quality of financial statement audits.

3.4 Documenting Internal Control Findings

Documenting internal control findings is a critical step in the financial statement auditing process. Proper documentation ensures transparency, supports audit conclusions, and provides a clear trail for review and future audits. This section will guide you through best practices for documenting internal control findings, supplemented with mind maps and practical examples to enhance understanding.

Why Document Internal Control Findings?

- Provides evidence of the auditor’s work and conclusions

- Facilitates communication with management and stakeholders

- Helps identify areas for improvement and risk mitigation

- Supports compliance with auditing standards and regulatory requirements

Key Elements to Document

- Description of the Control: What is the control designed to do?

- Control Owner: Who is responsible for the control?

- Control Frequency: How often is the control performed?

- Testing Procedures: How was the control tested?

- Findings: What were the results of the testing?

- Impact Assessment: What is the potential impact of control deficiencies?

- Recommendations: Suggestions for remediation or improvement

Mind Map: Internal Control Findings Documentation

Best Practices for Documentation

- Be Clear and Concise: Use straightforward language avoiding jargon.

- Use Standardized Templates: Ensures consistency across audit teams.

- Include Evidence References: Link findings to supporting documents or test results.

- Highlight Severity: Clearly indicate the severity of any control weaknesses.

- Maintain Objectivity: Document facts without bias or assumptions.

- Ensure Timeliness: Document findings promptly after testing.

Example: Documenting a Control Over Revenue Recognition

Description of Control: The finance department reviews and approves all sales invoices before recording revenue to ensure accuracy and completeness.

Control Owner: Accounts Receivable Manager

Control Frequency: Performed daily for all sales transactions.

Testing Procedures: Walkthrough of the invoice approval process and sampling of 20 invoices for approval signatures and accuracy.

Findings: 18 out of 20 invoices were properly approved. Two invoices lacked approval signatures.

Impact Assessment: The missing approvals represent a control deficiency that could lead to inaccurate revenue reporting, though no misstatements were identified in the sample.

Recommendations: Reinforce training on invoice approval procedures and implement a checklist to ensure all invoices are reviewed before recording.

Mind Map: Example Documentation for Revenue Recognition Control

Tips for Using Technology in Documentation

- Utilize audit management software to store and link documentation.

- Employ digital checklists and forms to standardize data capture.

- Use version control to track changes and updates.

- Incorporate screenshots or scanned copies of evidence.

Proper documentation of internal control findings not only strengthens the audit quality but also builds trust with clients and stakeholders by demonstrating thoroughness and professionalism.

3.5 Example: Evaluating Controls Over Revenue Recognition

Evaluating controls over revenue recognition is a critical aspect of financial statement auditing because revenue is often a key performance indicator and a common area for misstatement or fraud. This section will walk through best practices for assessing these controls, supported by clear examples and mind maps to illustrate the process.

Understanding Revenue Recognition Controls

Revenue recognition controls are designed to ensure that revenue is recorded accurately, completely, and in the correct accounting period. These controls typically include:

- Authorization of sales transactions

- Accurate invoicing and billing procedures

- Cut-off controls to record revenue in the proper period

- Reconciliation of sales records to general ledger

- Monitoring and review by management

Mind Map: Key Components of Revenue Recognition Controls

Step-by-Step Evaluation Process

-

Obtain and Review Documentation

- Review company policies on revenue recognition.

- Obtain flowcharts or narratives describing the revenue process.

-

Walkthrough Testing

- Select a sample sales transaction.

- Trace the transaction from initiation (order) through invoicing and recording.

- Confirm controls are operating as described.

-

Test of Controls

- Test authorization controls by verifying approval signatures or system access logs.

- Check accuracy of invoices against shipping documents.

- Review cut-off procedures by examining transactions near period-end.

-

Evaluate Control Deficiencies

- Identify any breakdowns or exceptions.

- Assess the potential impact on financial statements.

-

Document Findings

- Maintain clear records of tests performed, results, and conclusions.

Example Scenario: Evaluating Revenue Controls at a Government Agency

Background: A government agency receives grant funding and service fees. Revenue recognition policies require revenue to be recorded when services are rendered or grant conditions met.

Control Evaluation:

- Authorization: All service contracts require approval by the finance director.

- Recording: Invoices are generated automatically upon service completion.

- Cut-off: Revenue is recognized based on service completion dates, supported by service logs.

- Reconciliation: Monthly reconciliation between service logs and revenue recorded.

Testing:

- Selected 5 service contracts and confirmed finance director approval.

- Verified invoices matched service completion dates.

- Reviewed transactions around year-end to ensure revenue was recorded in the correct period.

- Confirmed monthly reconciliation reports were prepared and reviewed by management.

Outcome: Controls were operating effectively, with minor timing discrepancies corrected promptly.

Mind Map: Testing Controls Over Revenue Recognition

Common Control Weaknesses and Examples

-

Lack of Proper Authorization: Sales contracts signed without required approvals.

- Example: An auditor found multiple contracts lacking finance director approval, increasing risk of unauthorized sales.

-

Inaccurate Cut-off Procedures: Revenue recorded in incorrect periods.

- Example: Revenue for services completed in January was recorded in December, overstating prior year revenue.

-

Inadequate Reconciliation: Sales ledger not reconciled to general ledger regularly.

- Example: Missing reconciliations led to undetected duplicate revenue entries.

Best Practices Summary

- Establish clear, documented revenue recognition policies.

- Implement strong authorization controls.

- Use system-generated invoices tied to service/shipment evidence.

- Perform regular cut-off testing, especially near period-end.

- Conduct timely reconciliations and management reviews.

- Document all control evaluations and testing results thoroughly.

By integrating these practices and examples, auditors can effectively evaluate controls over revenue recognition, reducing the risk of material misstatement and enhancing audit quality.

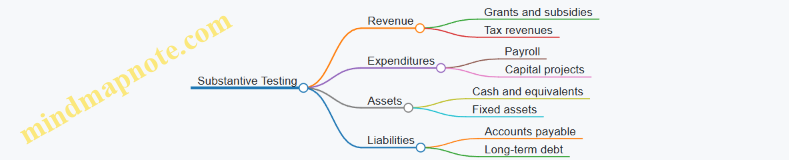

4. Substantive Testing Procedures

4.1 Designing Substantive Tests Based on Risk Assessment

Substantive testing is a critical phase in financial statement auditing that involves verifying the accuracy and completeness of account balances and transactions. Designing effective substantive tests begins with a thorough risk assessment, which helps auditors focus their efforts on areas with higher risk of material misstatement.

Understanding Risk Assessment

Risk assessment involves identifying and analyzing risks that could lead to material misstatements in financial statements. These risks can be inherent (due to the nature of the business or transactions), control risks (due to weaknesses in internal controls), or detection risks (related to the audit procedures).

Key components:

- Inherent Risk: Risk of material misstatement without considering controls.

- Control Risk: Risk that controls will fail to prevent or detect misstatements.

- Detection Risk: Risk that audit procedures will not detect existing misstatements.

Steps to Design Substantive Tests Based on Risk Assessment

- Identify Significant Accounts and Disclosures: Focus on accounts with high balances or complex transactions.

- Assess Inherent and Control Risks: Use knowledge of the client’s industry, prior audits, and internal control evaluations.

- Determine Materiality Levels: Define thresholds for what constitutes a material misstatement.

- Develop Audit Procedures: Tailor tests to address identified risks, including analytical procedures and detailed tests.

- Decide on Sample Sizes and Techniques: Based on assessed risk and materiality.

Mind Map: Designing Substantive Tests

Types of Substantive Tests

- Analytical Procedures: Comparing financial data with expectations based on trends, budgets, or industry data.

- Test of Details: Verifying individual transactions or balances through inspection, confirmation, or recalculation.

Example: Designing Substantive Tests for Accounts Receivable

Scenario: A government finance auditor is auditing the accounts receivable balance of a municipal department.

Risk Assessment:

- Inherent risk is high due to the complexity of billing and collection processes.

- Control risk is moderate; controls exist but have some weaknesses.

Materiality: $100,000 threshold based on total receivables.

Substantive Tests Designed:

- Analytical Procedure: Compare current year receivables aging report with prior year and budgeted amounts to identify unusual trends.

- Test of Details: Select a sample of receivable balances over $10,000 and send confirmation requests to debtors.

- Cut-off Testing: Verify transactions recorded near year-end to ensure proper period recognition.

Mind Map: Substantive Testing for Accounts Receivable

Best Practices

- Align substantive tests directly with identified risks.

- Use a combination of analytical procedures and tests of details for comprehensive coverage.

- Document rationale for chosen procedures and sample sizes.

- Continuously update risk assessment based on audit findings.

Additional Example: Substantive Testing for Payroll Expenses

Scenario: Auditing payroll expenses in a government department with a large workforce.

Risk Assessment:

- Inherent risk is moderate due to standardized payroll systems.

- Control risk is low with strong automated controls.

Substantive Tests:

- Perform analytical procedures comparing payroll expenses to prior periods and budget.

- Select a sample of payroll transactions and verify against personnel records and timesheets.

- Recalculate payroll tax withholdings and benefits.

Mind Map: Substantive Testing for Payroll Expenses

By integrating risk assessment into the design of substantive tests, auditors can optimize their efforts, focusing on areas with the greatest potential for material misstatement and ensuring a more effective and efficient audit process.

4.2 Analytical Procedures for Financial Statement Review

Analytical procedures are essential tools in financial statement auditing that help auditors understand the client’s business, identify areas of potential risk, and detect unusual transactions or trends. These procedures involve evaluating financial information through analysis of plausible relationships among both financial and non-financial data.

What Are Analytical Procedures?

Analytical procedures consist of comparisons, ratios, trend analyses, and reasonableness tests used to assess the consistency and validity of financial data. They are typically performed at three stages of an audit:

- Planning Stage: To help identify risk areas and plan the nature, timing, and extent of audit procedures.

- Substantive Testing Stage: To obtain audit evidence about particular assertions related to account balances or classes of transactions.

- Final Review Stage: To assess the overall financial statement presentation and identify any unusual items.

Mind Map: Types of Analytical Procedures

Common Analytical Procedures Explained with Examples

-

Comparison of Current Period to Prior Period

Example: An auditor compares the current year’s sales revenue of a government department to the previous year. If sales increased by 50% without a corresponding increase in service delivery or funding, this flags a need for further investigation.

-

Budget vs Actual Comparison

Example: In auditing a municipal finance statement, the auditor compares the budgeted expenses for public works with actual expenses. Significant deviations may indicate misstatements or inefficiencies.

-

Ratio Analysis

- Liquidity Ratio Example: Current Ratio = Current Assets / Current Liabilities. A sudden drop in the current ratio may indicate liquidity problems.

- Profitability Ratio Example: Net Profit Margin = Net Income / Revenue. A declining margin could suggest cost control issues.

-

Trend Analysis

Example: An auditor performs horizontal analysis on the last five years of expenditure data for a government agency to identify abnormal spikes or declines.

-

Reasonableness Tests

Example: Using regression analysis, an auditor predicts expected payroll expenses based on employee headcount and compares this to reported payroll expenses to detect anomalies.

Mind Map: Steps to Perform Analytical Procedures

Best Practices for Analytical Procedures

- Understand the Entity and Its Environment: Knowledge of the business model, regulatory environment, and economic factors is crucial.

- Use Reliable Data Sources: Ensure data integrity before analysis.

- Develop Clear Expectations: Base expectations on historical data, budgets, industry norms, or other relevant benchmarks.

- Investigate Unusual Variances: Follow up on significant deviations with additional audit procedures.

- Document Thoroughly: Record the rationale, methods, results, and conclusions of analytical procedures.

Integrated Example: Analytical Procedures in Action

Scenario: An auditor is reviewing the financial statements of a government-funded healthcare provider.

- Step 1: The auditor compares current year patient service revenue to prior years and budgeted amounts.

- Step 2: Ratio analysis reveals a sudden drop in the provider’s operating margin.

- Step 3: Trend analysis shows a steady increase in administrative expenses over three years.

- Step 4: Reasonableness tests predict payroll expenses based on staff numbers, but actual payroll is significantly higher.

Outcome: These analytical procedures highlight potential issues such as overstaffing or misallocation of funds, prompting the auditor to perform detailed substantive testing on payroll and expense accounts.

Analytical procedures are powerful tools that, when applied thoughtfully and systematically, enhance the auditor’s ability to detect material misstatements and improve audit efficiency.

4.3 Detailed Transaction Testing and Account Balances Verification

Detailed transaction testing and account balances verification are critical components of substantive audit procedures. These processes help auditors obtain sufficient and appropriate evidence to support the accuracy and completeness of financial statement assertions.

What is Detailed Transaction Testing?

Detailed transaction testing involves examining individual transactions recorded in the accounting system to verify their validity, accuracy, and compliance with applicable accounting standards.

What is Account Balances Verification?

Account balances verification focuses on confirming the ending balances of accounts reported in the financial statements, ensuring they are free from material misstatement.

Objectives

- Confirm the existence and occurrence of transactions

- Verify the accuracy and completeness of recorded amounts

- Ensure transactions are recorded in the correct period

- Validate account balances against supporting documentation

Mind Map: Detailed Transaction Testing

Mind Map: Account Balances Verification

Step-by-Step Approach to Detailed Transaction Testing

-

Define the Scope and Objectives: Identify which accounts and transaction types require detailed testing based on risk assessment.

-

Select Sample Transactions: Use sampling techniques such as random or risk-based sampling to select transactions for testing.

-

Gather Supporting Documentation: Obtain invoices, contracts, purchase orders, and other relevant documents.

-

Verify Transaction Details: Check that the transaction amount, date, and description match the supporting documents.

-

Test Authorization and Approvals: Confirm that transactions were properly authorized according to company policies.

-

Check Cut-off Procedures: Ensure transactions are recorded in the correct accounting period.

-

Recalculate Amounts: Verify mathematical accuracy of invoices, discounts, taxes, and totals.

-

Document Findings: Record any discrepancies or exceptions found during testing.

Example: Testing a Purchase Transaction

Scenario: An auditor is testing a purchase transaction recorded in the accounts payable ledger.

- Step 1: Select a sample purchase invoice dated near year-end.

- Step 2: Obtain the purchase order, receiving report, and invoice.

- Step 3: Verify the invoice amount matches the purchase order and receiving report.

- Step 4: Confirm the transaction was authorized by the purchasing manager.

- Step 5: Check the invoice date to ensure it is recorded in the correct period.

- Step 6: Recalculate the invoice total including taxes and discounts.

- Step 7: Document the results and note any exceptions.

Step-by-Step Approach to Account Balances Verification

-

Identify Significant Accounts: Focus on accounts with high balances or risk.

-

Obtain Confirmations: Send external confirmations to banks, customers, or vendors.

-

Perform Reconciliations: Match subsidiary ledgers to the general ledger.

-

Conduct Analytical Procedures: Analyze trends and ratios to identify unusual fluctuations.

-

Perform Physical Verification: Count inventory or inspect fixed assets where applicable.

-

Investigate Discrepancies: Follow up on any differences or anomalies.

-

Document Evidence: Maintain clear records of verification procedures and outcomes.

Example: Verifying Accounts Receivable Balance

Scenario: An auditor is verifying the accounts receivable balance at the end of the fiscal year.

- Step 1: Obtain the accounts receivable aging report.

- Step 2: Select a sample of customer balances for confirmation.

- Step 3: Send confirmation requests to customers and track responses.

- Step 4: Reconcile confirmed balances with subsidiary ledger.

- Step 5: Analyze aging to identify potentially uncollectible accounts.

- Step 6: Review subsequent cash receipts to verify collection.

- Step 7: Document all findings and adjust audit risk accordingly.

Best Practices

- Use a combination of sampling methods tailored to risk and materiality.

- Maintain a clear audit trail with detailed documentation.

- Leverage technology and data analytics to identify unusual transactions.

- Communicate findings promptly with the audit team and client.

- Continuously update testing procedures based on prior audit experience and emerging risks.

By integrating detailed transaction testing with thorough account balances verification, auditors can significantly enhance the reliability of their audit conclusions and provide greater assurance on the financial statements.

4.4 Using Data Analytics to Enhance Substantive Testing

Data analytics has become an indispensable tool in modern financial statement auditing, particularly in enhancing substantive testing. By leveraging large volumes of financial data, auditors can identify anomalies, trends, and patterns that might not be evident through traditional audit methods. This section explores how data analytics can be integrated into substantive testing with practical examples and mind maps to illustrate key concepts.

What is Data Analytics in Auditing?

Data analytics refers to the process of examining, transforming, and modeling data to discover useful information, draw conclusions, and support decision-making. In auditing, it helps auditors to:

- Increase audit coverage and depth

- Improve risk assessment accuracy

- Detect potential fraud or errors

- Enhance efficiency and effectiveness of audit procedures

Mind Map: Data Analytics in Substantive Testing

Key Techniques for Using Data Analytics in Substantive Testing

-

Trend Analysis: Examining financial data over time to identify unusual fluctuations.

-

Ratio Analysis: Comparing financial ratios to industry benchmarks or prior periods.

-

Duplicate Payment Detection: Using algorithms to find duplicate transactions.

-

Benford’s Law Analysis: Applying statistical distribution to detect anomalies in numerical data.

-

Outlier Detection: Identifying transactions or balances that deviate significantly from the norm.

-

Sampling Optimization: Using data analytics to select more representative samples for detailed testing.

Example 1: Using Data Analytics to Test Accounts Receivable

Scenario: An auditor is testing the completeness and accuracy of accounts receivable balances for a government agency.

Approach:

- Extract the full accounts receivable ledger data.

- Use data analytics software to perform the following:

- Aging Analysis: Categorize receivables by age to identify overdue accounts.

- Trend Analysis: Compare monthly receivables balances over the past year to detect unusual spikes.

- Duplicate Invoice Detection: Identify invoices with identical amounts and dates.

Outcome:

- The auditor identifies several overdue accounts that require further investigation.

- A duplicate invoice is detected, indicating a potential error or fraud.

- Trend analysis reveals an unexpected spike in receivables in the last quarter, prompting additional substantive testing.

Mind Map: Data Analytics Workflow for Accounts Receivable Testing

Example 2: Benford’s Law Application in Expense Testing

Scenario: Auditing expense transactions of a government department to detect irregularities.

Approach:

- Extract all expense transaction amounts.

- Apply Benford’s Law to analyze the distribution of the leading digits.

- Compare the observed distribution with the expected Benford distribution.

Outcome:

- Significant deviations from Benford’s expected distribution highlight suspicious transactions.

- Auditor selects these transactions for detailed substantive testing.

Best Practices for Integrating Data Analytics in Substantive Testing

- Understand the Data: Ensure data completeness, accuracy, and relevance before analysis.

- Define Clear Objectives: Tailor analytics procedures to specific audit assertions and risks.

- Combine Analytics with Professional Judgment: Use analytics as a complement, not a replacement, for auditor expertise.

- Document Procedures and Findings: Maintain clear records of analytics methods, results, and follow-up actions.

- Train Audit Teams: Equip auditors with data analytics skills and tools.

Summary

Data analytics significantly enhances substantive testing by enabling auditors to analyze entire data populations, identify risks more effectively, and increase audit efficiency. Through practical applications like aging analysis, duplicate detection, and Benford’s Law, auditors can uncover insights that traditional sampling methods might miss. Integrating these techniques with professional judgment and robust documentation ensures a higher quality audit outcome.

4.5 Example: Substantive Testing of Accounts Receivable

Substantive testing of accounts receivable is a critical audit procedure aimed at verifying the existence, accuracy, and valuation of receivables reported on the financial statements. This section provides a detailed example of how auditors perform substantive tests on accounts receivable, integrating best practices and illustrative examples.

Objectives of Substantive Testing for Accounts Receivable

- Confirm existence and occurrence of receivables

- Verify accuracy of recorded amounts

- Assess valuation and collectability

- Ensure proper cutoff and classification

Step 1: Understanding the Accounts Receivable Process

Step 2: Designing Substantive Procedures

- Accounts Receivable Confirmations: Sending direct confirmation requests to customers to verify balances.

- Aging Analysis Review: Examining the aging report to identify overdue accounts.

- Subsequent Cash Receipts Testing: Verifying payments received after year-end against outstanding balances.

- Cutoff Testing: Ensuring transactions near the period-end are recorded in the correct period.

- Review of Allowance for Doubtful Accounts: Evaluating management’s estimate for bad debts.

Step 3: Performing the Tests – Detailed Example

Example Scenario:

A government finance auditor is auditing the accounts receivable of a municipal utility company with a year-end balance of $5 million.

-

Accounts Receivable Confirmations:

- Auditor selects a sample of 50 customer balances from the accounts receivable ledger.

- Confirmation letters are sent directly to customers requesting verification of balances.

- Responses are received for 40 customers; discrepancies noted in 3 cases.

-

Aging Analysis Review:

- The auditor reviews the aging report and notes that $500,000 is over 90 days past due.

- Auditor investigates these overdue balances by reviewing correspondence and payment history.

-

Subsequent Cash Receipts:

- For balances outstanding at year-end, auditor tests cash receipts in the first quarter of the following year.

- Confirms that 80% of the overdue amounts were collected within 60 days.

-

Cutoff Testing:

- Auditor tests invoices issued in the last week of the fiscal year and the first week of the new fiscal year.

- Verifies that sales and receivables are recorded in the correct period.

-

Allowance for Doubtful Accounts:

- Auditor reviews the methodology used by management to estimate the allowance.

- Compares historical write-offs and current economic conditions.

- Tests the mathematical accuracy of the allowance calculation.

Step 4: Evaluating Results and Forming Conclusions

- Discrepancies in confirmations are investigated and resolved.

- Aging analysis and subsequent receipts support the collectability of receivables.

- Cutoff testing confirms transactions are recorded in the appropriate period.

- Allowance for doubtful accounts is deemed reasonable based on evidence.

Step 5: Documenting Findings

- Detailed working papers include confirmation letters, aging reports, cash receipt testing results, and allowance calculations.

- Auditor’s conclusions on the fairness of accounts receivable balances are clearly stated.

Summary

Substantive testing of accounts receivable involves a combination of confirmation, analytical review, and detailed transaction testing. By following a structured approach and using examples like the municipal utility company, auditors can effectively assess the accuracy and collectability of receivables, thereby supporting a reliable audit opinion.

For further reading, auditors can refer to ISA 505 (External Confirmations) and ISA 330 (The Auditor’s Responses to Assessed Risks) for detailed guidance on substantive procedures.

5. Audit Evidence Collection and Documentation

5.1 Types of Audit Evidence and Their Reliability

Audit evidence is the information collected by auditors to form a basis for their audit opinion. Understanding the types of audit evidence and their reliability is crucial for effective auditing. This section explores the various types of audit evidence, their characteristics, and how auditors assess their reliability.

Types of Audit Evidence

Audit evidence can be broadly classified into the following categories:

- Physical Evidence

- Documentary Evidence

- Oral Evidence

- Analytical Evidence

- Electronic Evidence

Mind Map: Types of Audit Evidence

Physical Evidence

Physical evidence involves the direct inspection or observation of tangible assets or processes.