Introduction to Accounting Standards

1. Understanding Accounting Standards: Foundations and Importance

1.1 What Are Accounting Standards? Definition and Purpose

Accounting standards are a set of principles, rules, and guidelines established to govern how financial transactions and events are recorded, reported, and presented in financial statements. They ensure consistency, transparency, comparability, and reliability of financial information across different organizations and industries.

Definition

Accounting Standards: Formalized rules and guidelines issued by recognized standard-setting bodies that dictate how financial statements should be prepared and presented.

Purpose of Accounting Standards

- Consistency: Ensures that financial statements are prepared in a uniform manner across periods and entities.

- Comparability: Allows stakeholders to compare financial information between different organizations and time periods.

- Transparency: Provides clear and understandable financial information to users.

- Reliability: Enhances the trustworthiness of financial reports.

- Regulatory Compliance: Helps organizations comply with legal and regulatory requirements.

Mind Map: Understanding Accounting Standards

Example 1: Small Business Implementing Accounting Standards

Scenario: A small educational consultancy firm wants to prepare its financial statements to attract investors.

- Without standards: The firm records revenue inconsistently—sometimes when cash is received, sometimes when services are promised.

- With standards: The firm follows the revenue recognition principle, recording revenue when services are delivered.

Result: Investors can clearly understand the firm’s financial health and make informed decisions.

Mind Map: Purpose Illustrated Through Example

Example 2: Auditor’s Role in Ensuring Standards

An auditor reviews the financial statements of a university to ensure compliance with accounting standards.

- Checks if tuition fees are recognized properly.

- Verifies asset valuations for campus buildings.

- Confirms liabilities like loans are accurately reported.

This process ensures stakeholders receive trustworthy financial information.

Summary

Accounting standards form the backbone of reliable financial reporting. They guide accountants and auditors in preparing and reviewing financial statements, ensuring that users such as investors, regulators, and management can trust and compare financial data effectively.

1.2 Historical Evolution of Accounting Standards Globally

Accounting standards have evolved over centuries, shaped by economic, legal, and social changes worldwide. Understanding this evolution helps accountants and auditors appreciate the rationale behind current standards and anticipate future developments.

Early Beginnings: The Roots of Accounting

- Ancient Civilizations:

- Mesopotamia and Egypt used basic record-keeping for trade and taxation.

- Clay tablets and papyrus recorded transactions.

- Medieval Period:

- Double-entry bookkeeping emerged in 15th-century Italy, credited to Luca Pacioli (1494).

- This system laid the groundwork for modern accounting.

Example: A merchant in Renaissance Italy used double-entry bookkeeping to track sales and expenses, enabling better financial control.

Industrial Revolution and the Need for Standardization

- Rapid industrial growth increased business complexity.

- Companies raised capital from public investors, requiring transparent financial information.

- Early 20th century: Different countries developed their own accounting rules, leading to inconsistencies.

Example: A British manufacturing firm and a US competitor reported profits differently due to varying local accounting practices, confusing investors.

Formation of Professional Bodies and Early Standard-Setting

- Late 19th to early 20th century:

- Professional accounting organizations formed (e.g., AICPA in 1887).

- Voluntary guidelines and ethical codes introduced.

- 1930s:

- The Great Depression highlighted the need for formal standards.

- The U.S. established the Securities and Exchange Commission (SEC) in 1934, promoting standardized reporting.

Example: Following the 1929 stock market crash, the SEC required publicly traded companies to follow consistent accounting rules to protect investors.

Post-War Globalization and International Efforts

- Economic globalization increased cross-border investments.

- Need for harmonized accounting standards to facilitate comparability.

- 1973: The International Accounting Standards Committee (IASC) was formed.

- 2001: IASC restructured into the International Accounting Standards Board (IASB), issuing IFRS.

Example: A multinational corporation preparing consolidated financial statements for subsidiaries in different countries adopted IFRS to ensure uniform reporting.

Modern Era: Convergence and Technological Impact

- Efforts to converge IFRS and US GAAP to reduce differences.

- Increasing focus on transparency, sustainability, and digital reporting.

- Technology enables real-time compliance and automated disclosures.

Example: An accounting firm uses cloud-based software to automatically update financial reports according to the latest IFRS amendments.

Summary Mind Map

Best Practice Highlight:

- Stay informed about historical context to better interpret standards.

- Use historical examples to train junior accountants on why standards exist.

Practical Example:

- When explaining revenue recognition, reference how industrial revolution-era businesses struggled without consistent rules, emphasizing the importance of clear criteria today.

1.3 The Role of Accounting Standards in Financial Reporting

Accounting standards serve as the backbone of financial reporting, ensuring that financial statements are consistent, transparent, and comparable across different organizations and periods. Their role is critical in fostering trust among stakeholders such as investors, regulators, creditors, and management.

Why Accounting Standards Matter in Financial Reporting

- Consistency: They provide a uniform framework that companies must follow, making it easier to compare financial data across different entities and time periods.

- Transparency: Standards require clear disclosures, reducing ambiguity and enhancing the clarity of financial statements.

- Reliability: By enforcing strict guidelines, accounting standards ensure that financial information is accurate and dependable.

- Accountability: They hold organizations accountable by defining how transactions and events should be recorded and reported.

Mind Map: The Role of Accounting Standards in Financial Reporting

Practical Examples Illustrating the Role of Accounting Standards

Example 1: Consistency in Revenue Recognition

A university offering online courses must recognize revenue consistently each semester. By following IFRS 15 or ASC 606 (Revenue from Contracts with Customers), the university recognizes revenue when control of the educational service is transferred to the student, rather than when cash is received. This ensures that revenue is reported in the correct period, allowing stakeholders to accurately assess the university’s financial performance over time.

Example 2: Transparency in Asset Reporting

A finance company owns several investment properties. According to IAS 40 (Investment Property), the company must disclose the fair value of these properties and any changes during the reporting period. This transparency allows investors to understand the true value of the company’s assets and the risks involved.

Example 3: Reliability Through Audit and Compliance

An educational non-profit organization follows GAAP standards for its financial statements. Auditors verify that the organization’s financial reports comply with these standards, providing assurance to donors and grant providers that funds are used appropriately and reported accurately.

Best Practice: Embedding Accounting Standards into Financial Reporting Processes

- Regular Training: Ensure accounting and finance teams are up-to-date with current standards.

- Standardized Templates: Use reporting templates aligned with accounting standards to maintain consistency.

- Internal Controls: Implement checks to verify compliance before external reporting.

- Audit Readiness: Prepare documentation and disclosures in line with standards to facilitate smooth audits.

Summary

Accounting standards play a pivotal role in shaping financial reporting by promoting consistency, transparency, reliability, and accountability. They help create financial statements that stakeholders can trust and use to make informed decisions. By integrating these standards into everyday accounting practices, organizations in finance and education sectors can enhance the quality and credibility of their financial reports.

1.4 Key Regulatory Bodies and Standard-Setting Organizations

Accounting standards are developed, maintained, and enforced by various regulatory bodies and standard-setting organizations worldwide. Understanding these entities is crucial for accountants and auditors to ensure compliance and maintain the integrity of financial reporting.

Major Regulatory Bodies and Standard-Setting Organizations

Detailed Descriptions and Examples

International Accounting Standards Board (IASB)

- The IASB is an independent body responsible for developing IFRS, which are used in over 140 countries.

- Example: A multinational education company preparing consolidated financial statements uses IFRS to ensure comparability across its global operations.

Financial Accounting Standards Board (FASB)

- FASB issues US GAAP, which is the primary accounting framework in the United States.

- Example: A US-based finance firm follows FASB standards for revenue recognition and lease accounting.

Securities and Exchange Commission (SEC)

- The SEC enforces accounting standards for publicly traded companies in the US, ensuring transparency and investor protection.

- Example: A publicly listed auditing firm must file financial reports compliant with SEC regulations.

Governmental Accounting Standards Board (GASB)

- GASB sets accounting standards for US state and local governments.

- Example: A municipal education department follows GASB standards for budgeting and financial reporting.

Best Practice: Staying Updated with Regulatory Bodies

- Regularly visit official websites of IASB, FASB, SEC, and other relevant bodies.

- Subscribe to newsletters and updates on standard changes.

- Participate in webinars and training sessions offered by these organizations.

Mind Map: Overview of Key Regulatory Bodies

Mind Map: Key Regulatory Bodies

Example Scenario: Applying Knowledge of Regulatory Bodies

Scenario: An auditor working for a multinational finance company must prepare audit reports that comply with both IFRS and US GAAP due to the company’s dual listing.

Application:

- The auditor references IASB materials for IFRS compliance.

- Consults FASB pronouncements for US GAAP requirements.

- Reviews SEC regulations for disclosure requirements applicable to the US market.

- Uses PCAOB guidelines to ensure audit quality and compliance.

This integrated approach ensures the audit meets all regulatory expectations, minimizing risks of non-compliance.

By understanding the roles and scopes of these key regulatory bodies and standard-setting organizations, accountants and auditors can confidently navigate the complex landscape of accounting standards and ensure accurate, compliant financial reporting.

1.5 Best Practice: Aligning Accounting Processes with Standards from Day One

Aligning accounting processes with established accounting standards from the very beginning of an organization’s financial operations is crucial for ensuring accuracy, compliance, and transparency. This proactive approach minimizes costly adjustments later and builds trust with stakeholders such as auditors, investors, and regulatory bodies.

Why Align from Day One?

- Compliance Assurance: Early alignment helps avoid non-compliance penalties.

- Consistency: Establishes uniform accounting treatment across transactions.

- Efficiency: Streamlines reporting and auditing processes.

- Transparency: Enhances credibility with stakeholders.

Key Steps to Align Accounting Processes with Standards

Detailed Breakdown

-

Understand Applicable Standards:

- Identify which accounting standards apply to your organization (e.g., IFRS for multinational entities, GAAP for US-based companies).

- Stay informed about industry-specific guidelines.

-

Design the Chart of Accounts Accordingly:

- Structure accounts to reflect standard classifications (assets, liabilities, equity, income, expenses).

- Example: For an educational institution, separate accounts for tuition fees, grants, and donations to comply with revenue recognition standards.

-

Document Accounting Policies and Procedures:

- Create clear policy manuals referencing relevant standards.

- Include guidelines on revenue recognition, asset capitalization, depreciation, and lease accounting.

-

Implement Internal Controls:

- Segregate duties to prevent errors and fraud.

- Establish approval workflows aligned with accounting policies.

-

Train Accounting Staff:

- Conduct onboarding sessions focused on applicable standards.

- Provide continuous education on updates and interpretations.

-

Leverage Technology:

- Use accounting software configured to comply with standards.

- Automate routine compliance checks where possible.

-

Regular Monitoring and Review:

- Schedule periodic internal audits.

- Use checklists to ensure ongoing adherence.

Example: Small Educational Startup Aligning from Day One

-

Scenario: A new private tutoring company wants to ensure its accounting complies with IFRS.

-

Actions Taken:

- Selected IFRS as the reporting framework.

- Designed a chart of accounts separating tuition revenue, grants, and operational expenses.

- Documented revenue recognition policy recognizing tuition fees over the course duration.

- Trained the finance team on IFRS 15 (Revenue from Contracts with Customers).

- Implemented accounting software with IFRS templates.

- Established monthly internal reviews to verify compliance.

-

Outcome: Smooth audit process in the first year, accurate financial statements, and increased investor confidence.

Additional Mind Map: Training and Continuous Learning

Summary

Aligning accounting processes with standards from day one is a foundational best practice that pays dividends in compliance, efficiency, and stakeholder trust. By understanding applicable standards, designing processes thoughtfully, training staff, leveraging technology, and continuously monitoring compliance, organizations set themselves up for long-term financial integrity and success.

1.6 Example: How a Small Business Implements Basic Accounting Standards

Implementing accounting standards in a small business might seem daunting at first, but by breaking down the process into manageable steps and applying best practices, it becomes straightforward and highly beneficial. This example will guide you through how a small retail business, “Green Leaf Books,” applies basic accounting standards to ensure accurate and compliant financial reporting.

Step 1: Understanding Applicable Accounting Standards

Green Leaf Books decides to follow the local Generally Accepted Accounting Principles (GAAP) which emphasize the accrual basis of accounting, consistency, and prudence.

Step 2: Setting Up Accounting Policies

The business documents its accounting policies, including revenue recognition, inventory valuation, and expense recording, aligning with GAAP principles.

Step 3: Recording Transactions Using the Accrual Principle

- Revenue Recognition: Sales are recorded when books are delivered, not when cash is received.

- Expense Recognition: Expenses like rent and utilities are recorded in the period they relate to, not when paid.

Step 4: Maintaining Consistency

Green Leaf Books applies the same inventory valuation method (FIFO) every accounting period to ensure comparability.

Step 5: Applying Prudence

The business records potential bad debts conservatively, estimating doubtful accounts to avoid overstating assets.

Mind Map: Implementing Basic Accounting Standards in a Small Business

Example Transactions and Their Accounting Treatment

| Transaction Description | Accounting Treatment | Explanation |

|---|---|---|

| Sold 100 books worth $1,000 on credit | Record $1,000 revenue and accounts receivable | Revenue recognized when books delivered, not when cash received |

| Paid $500 rent for the month | Record $500 rent expense for the month | Expense recognized in the period it relates to, matching principle |

| Estimated $100 doubtful accounts from receivables | Record allowance for doubtful accounts of $100 | Prudence principle to avoid overstating assets |

Mind Map: Example Transactions and Principles Applied

Best Practice Tips for Small Businesses

- Maintain Clear Documentation: Keep detailed records of accounting policies and transaction evidence.

- Use Simple Accounting Software: Tools like QuickBooks or Xero help automate compliance with standards.

- Regular Reconciliation: Monthly bank and accounts reconciliation to ensure accuracy.

- Train Staff: Basic training on accounting principles for employees handling financial data.

Summary

By systematically applying accounting standards such as accrual accounting, consistency, and prudence, Green Leaf Books ensures its financial statements are reliable and compliant. This approach not only supports better decision-making but also prepares the business for audits and potential growth.

This example illustrates that even small businesses can successfully implement fundamental accounting standards with clear policies, consistent application, and practical tools.

2. Overview of Major Accounting Frameworks

2.1 International Financial Reporting Standards (IFRS): Scope and Application

Introduction to IFRS

International Financial Reporting Standards (IFRS) are a set of accounting principles developed and maintained by the International Accounting Standards Board (IASB). They provide a global framework for how public companies prepare and disclose their financial statements, ensuring transparency, accountability, and efficiency in financial markets worldwide.

Scope of IFRS

IFRS is designed to be applied by entities that prepare financial statements for external users, such as investors, creditors, regulators, and other stakeholders. It is widely adopted across more than 140 jurisdictions, including the European Union, Australia, Canada, and many countries in Asia, Africa, and South America.

Key Areas Covered by IFRS:

- Recognition, measurement, presentation, and disclosure of transactions and events in financial statements

- Specific standards for assets, liabilities, equity, income, and expenses

- Industry-specific guidance where applicable

Mind Map: IFRS Scope Overview

Application of IFRS

Applying IFRS involves adhering to the principles and detailed guidance laid out in the standards to prepare financial statements that faithfully represent the entity’s financial position and performance.

Best Practices in Applying IFRS:

- Understand the Entity’s Business Model: Tailor IFRS application to the specific nature of the business.

- Consistent Policy Selection: Choose accounting policies that comply with IFRS and apply them consistently.

- Comprehensive Documentation: Maintain detailed records supporting judgments and estimates.

- Regular Training: Keep accounting and audit teams updated on IFRS changes.

Example: Applying IFRS 15 in an Educational Institution

An educational institution offers semester-based courses and receives tuition fees upfront. Under IFRS 15 (Revenue from Contracts with Customers), revenue recognition depends on the transfer of control of educational services.

- Step 1: Identify the contract with the student.

- Step 2: Identify performance obligations (e.g., delivery of lectures, access to resources).

- Step 3: Determine the transaction price (tuition fee).

- Step 4: Allocate the transaction price to performance obligations.

- Step 5: Recognize revenue as the institution delivers the educational services over the semester.

This means revenue is recognized over time, not just when fees are received, ensuring compliance with IFRS and reflecting the true economic activity.

Mind Map: IFRS 15 Application Example

Summary

IFRS provides a comprehensive framework that promotes consistency and comparability in financial reporting globally. Understanding its scope and correct application is essential for accountants and auditors to ensure compliance and provide stakeholders with reliable financial information.

For further reading, refer to the official IASB website and IFRS Foundation publications.

2.2 Generally Accepted Accounting Principles (GAAP): US and Other Variants

Generally Accepted Accounting Principles (GAAP) represent a set of accounting standards, principles, and procedures that companies and organizations follow when compiling their financial statements. While GAAP is often associated with the United States, many countries have their own versions or variants of GAAP tailored to their regulatory environments and business practices.

What is GAAP?

GAAP is a framework that ensures consistency, transparency, and comparability of financial reporting. It provides guidelines on how to recognize revenue, value assets, disclose liabilities, and present financial information.

US GAAP Overview

- Developed and maintained by the Financial Accounting Standards Board (FASB).

- Highly detailed and rules-based.

- Widely used by public companies in the United States.

Other GAAP Variants

- Canadian GAAP: Historically similar to US GAAP but evolving towards IFRS.

- Indian GAAP: Prescribed by the Institute of Chartered Accountants of India (ICAI), with gradual convergence to IFRS.

- Japanese GAAP: Overseen by the Accounting Standards Board of Japan (ASBJ), with some convergence efforts.

Mind Map: Overview of GAAP Variants

Key Differences Between US GAAP and Other Variants

| Aspect | US GAAP | Other GAAP Variants |

|---|---|---|

| Standard Setter | FASB | Various (e.g., ICAI, ASBJ) |

| Approach | Rules-based | Often principles-based or mixed |

| Revenue Recognition | Detailed guidance (ASC 606) | Varies; some follow IFRS principles |

| Financial Instruments | Complex classification rules | May be simpler or IFRS-aligned |

Best Practice: Understanding Local GAAP Requirements

When working internationally, accountants and auditors should:

- Familiarize themselves with the local GAAP variant.

- Identify key differences from US GAAP or IFRS.

- Adjust reporting and auditing procedures accordingly.

Example 1: Revenue Recognition under US GAAP vs Indian GAAP

Scenario: An education company in India offers subscription-based online courses.

- US GAAP: Revenue is recognized following ASC 606, focusing on the transfer of control and performance obligations.

- Indian GAAP: Revenue recognition may be based on the completion of services or receipt of payment, with less detailed guidance.

Implication: The company must carefully evaluate the timing and amount of revenue recognized to comply with the applicable GAAP.

Mind Map: Revenue Recognition Comparison

Example 2: Asset Valuation Differences

A Japanese manufacturing firm values its inventory.

- US GAAP: Inventory is valued at the lower of cost or market, with specific rules for cost flow assumptions (FIFO, LIFO, weighted average).

- Japanese GAAP: Similar valuation but LIFO is generally not permitted.

Implication: The firm must select an inventory costing method allowed under its local GAAP and disclose it properly.

Summary

Understanding the nuances of GAAP variants is essential for accountants and auditors working across borders. While US GAAP remains one of the most detailed and widely recognized frameworks, other countries maintain their own GAAP versions that may differ in principles, detail, and application.

Final Best Practice

Maintain a GAAP comparison checklist when preparing or auditing financial statements for entities operating under different GAAP systems. This checklist should include:

- Revenue recognition criteria

- Asset and liability measurement rules

- Disclosure requirements

- Recent updates or changes

This approach ensures compliance, reduces errors, and enhances the reliability of financial reporting.

2.3 Comparing IFRS and GAAP: Key Differences and Similarities

Understanding the differences and similarities between IFRS (International Financial Reporting Standards) and GAAP (Generally Accepted Accounting Principles) is crucial for accountants and auditors working in multinational environments or transitioning between frameworks. Both frameworks aim to provide transparent, consistent, and comparable financial information but differ in approach, detail, and application.

Key Similarities Between IFRS and GAAP

- Objective: Both frameworks aim to provide useful financial information to investors, creditors, and other stakeholders.

- Qualitative Characteristics: Emphasis on relevance, reliability, comparability, and understandability.

- Basic Accounting Principles: Both use accrual accounting and the going concern assumption.

- Financial Statements: Both require a balance sheet, income statement, statement of cash flows, and statement of changes in equity.

Key Differences Between IFRS and GAAP

| Aspect | IFRS | GAAP |

|---|---|---|

| Standard Setting Body | International Accounting Standards Board (IASB) | Financial Accounting Standards Board (FASB) |

| Approach | Principles-based | Rules-based |

| Inventory Valuation | Prohibits LIFO (Last In, First Out) method | Allows LIFO method |

| Revenue Recognition | Single comprehensive standard (IFRS 15) | Multiple industry-specific standards |

| Development Costs | Capitalized if criteria met | Generally expensed |

| Revaluation of Assets | Allowed for property, plant, and equipment | Generally prohibited |

| Extraordinary Items | Not recognized separately | Recognized separately |

| Financial Statement Presentation | Statement of comprehensive income can be combined or separate | Requires separate statements for income and comprehensive income |

Mind Map: IFRS vs GAAP Overview

Detailed Comparison with Examples

Inventory Valuation

- IFRS: Does not allow LIFO because it can distort the actual flow of inventory and financial position.

- GAAP: Permits LIFO, which can reduce taxable income during inflationary periods.

Example: A manufacturing company in the education sector uses LIFO under GAAP to manage tax liabilities. If it switches to IFRS, it must adopt FIFO or weighted average, potentially increasing reported profits.

Revenue Recognition

- IFRS 15: Provides a five-step model for recognizing revenue from contracts with customers, focusing on transfer of control.

- GAAP: Uses multiple standards depending on the industry, which can lead to inconsistencies.

Example: A financial services firm recognizing revenue from subscription services must apply the five-step IFRS model, ensuring revenue is recognized as services are delivered, whereas under GAAP, different rules might apply depending on contract terms.

Development Costs

- IFRS: Allows capitalization of development costs if certain criteria (technical feasibility, intention to complete, ability to use or sell) are met.

- GAAP: Generally requires expensing development costs as incurred.

Example: An educational software company developing a new learning platform can capitalize development costs under IFRS, improving asset base and profitability, but must expense these costs under GAAP, reducing short-term profits.

Asset Revaluation

- IFRS: Permits revaluation of property, plant, and equipment to fair value.

- GAAP: Revaluation is generally not allowed; assets are carried at historical cost less depreciation.

Example: A university owning land can revalue its property under IFRS to reflect current market value, enhancing balance sheet strength, but under GAAP, the land remains at historical cost.

Mind Map: Revenue Recognition Comparison

Best Practice Tips for Accountants and Auditors

- Stay Informed: Regularly update knowledge on both IFRS and GAAP changes.

- Documentation: Maintain clear documentation when transitioning between frameworks.

- Training: Conduct training sessions for finance teams on key differences.

- Use Technology: Leverage accounting software that supports multi-framework reporting.

Summary

While IFRS and GAAP share a common goal of transparent financial reporting, their differences in approach, detail, and application require accountants and auditors to carefully consider the framework applicable to their organization. Understanding these nuances ensures accurate financial statements and compliance across jurisdictions.

2.4 Other Regional and Industry-Specific Standards

Accounting standards are not only defined by global frameworks like IFRS and US GAAP but also by numerous regional and industry-specific standards tailored to meet local regulations and sectoral needs. Understanding these standards is crucial for accountants and auditors working in diverse environments, especially in finance and education sectors where compliance and reporting requirements can vary significantly.

Regional Accounting Standards

Different countries and regions have developed their own accounting standards to address local economic, legal, and cultural contexts. These standards often coexist with or complement IFRS or GAAP frameworks.

-

Examples of Regional Standards:

- Indian Accounting Standards (Ind AS): Converged with IFRS but with carve-outs to suit Indian economic conditions.

- Chinese Accounting Standards (CAS): Aligned closely with IFRS but include specific rules for state-owned enterprises.

- Japanese GAAP: Traditional standards with gradual IFRS adoption.

- Canadian GAAP: Transitioning towards IFRS but still used in some sectors.

Industry-Specific Accounting Standards

Certain industries require specialized accounting treatments due to their unique transactions, regulatory environments, or operational models. These standards ensure transparency and comparability within the industry.

-

Finance Sector:

- Banking and Financial Institutions: Standards like Basel III for capital adequacy and IFRS 9 for financial instruments.

- Insurance: IFRS 17 for insurance contracts, addressing recognition and measurement of insurance liabilities.

-

Education Sector:

- Non-Profit Accounting Standards: Such as FASB ASC 958 in the US, focusing on fund accounting and donor restrictions.

- Governmental Accounting Standards: GASB standards for public educational institutions.

Mind Map: Regional Accounting Standards

Mind Map: Industry-Specific Standards

Best Practice: Navigating Regional and Industry-Specific Standards

- Stay Updated: Regularly review updates from local standard-setting bodies.

- Integrate with Global Standards: Understand how regional standards interact with IFRS or GAAP.

- Customize Training: Provide industry-specific training for accounting teams.

- Use Checklists: Develop compliance checklists tailored to regional and industry requirements.

Examples

Example 1: Applying Ind AS in an Indian Educational Institution

An Indian university transitioning from Indian GAAP to Ind AS needs to recognize revenue differently, especially for government grants and student fees. Ind AS 115 (Revenue from Contracts with Customers) requires detailed contract analysis, which differs from previous practices. The accounting team implemented a step-by-step revenue recognition process aligned with Ind AS, ensuring compliance and transparency.

Example 2: Insurance Company Adopting IFRS 17

A finance company specializing in insurance products adopted IFRS 17 to better reflect the timing and uncertainty of insurance contract cash flows. The accounting department worked closely with actuaries to estimate liabilities and used new software tools to comply with the complex measurement models.

Example 3: Non-Profit Educational Organization Using FASB ASC 958

A non-profit school in the US follows FASB ASC 958 to manage donor-restricted funds separately from operational funds. This ensures clear reporting to donors and regulators, maintaining trust and eligibility for grants.

By understanding and effectively applying regional and industry-specific accounting standards, accountants and auditors can ensure accurate financial reporting, regulatory compliance, and enhanced stakeholder confidence across diverse sectors.

2.5 Best Practice: Choosing the Right Framework for Your Organization

Selecting the appropriate accounting framework is a critical decision that can significantly impact the accuracy, transparency, and comparability of your organization’s financial statements. This choice influences regulatory compliance, stakeholder trust, and operational efficiency. Below, we explore a structured approach to making this decision, supported by mind maps and practical examples.

Key Considerations When Choosing an Accounting Framework

Step 1: Understand Regulatory and Legal Requirements

Most jurisdictions mandate specific accounting frameworks. For example, public companies in the European Union must use IFRS, while U.S. companies typically follow US GAAP. Understanding these requirements ensures compliance and avoids penalties.

Example: A U.S.-based educational institution receiving federal funding must comply with US GAAP to meet audit requirements.

Step 2: Assess Organizational Size and Complexity

- SMEs: Often benefit from simplified frameworks like IFRS for SMEs or local GAAP variants designed to reduce complexity.

- Large Organizations: Typically require full IFRS or US GAAP to address complex transactions and provide detailed disclosures.

Example: A small accounting firm serving local clients might adopt IFRS for SMEs for streamlined reporting, while a multinational finance company would implement full IFRS.

Step 3: Evaluate Stakeholder Expectations

Consider who will use your financial statements:

- Investors may prefer internationally recognized standards like IFRS.

- Local banks might require compliance with local GAAP.

Example: An educational institution seeking international donors may choose IFRS to enhance credibility.

Step 4: Define Reporting Objectives

Clarify whether the focus is on external reporting, tax compliance, or internal management reporting. Different frameworks may better support these objectives.

Example: A finance company prioritizing detailed external reporting may select US GAAP, while an educational nonprofit focused on grant compliance might use local GAAP.

Step 5: Consider Cost and Resource Availability

Implementing complex frameworks requires trained staff and compatible software.

Example: A small auditor’s office might avoid full IFRS due to training costs and instead use a simplified framework.

Step 6: Plan for Future Growth

If expansion or cross-border operations are anticipated, adopting globally accepted standards like IFRS can ease future transitions.

Example: A regional finance firm planning to open offices abroad may adopt IFRS early to streamline consolidation.

Integrated Mind Map: Decision Flow for Selecting Accounting Framework

Practical Example: Choosing a Framework for an Educational Institution

Scenario: A mid-sized private university in Canada is evaluating whether to adopt IFRS or Canadian GAAP.

- Regulatory: Canadian public institutions must follow ASPE (Accounting Standards for Private Enterprises) or IFRS.

- Size & Complexity: Medium complexity with some international collaborations.

- Stakeholders: International students and donors expect IFRS-based reporting.

- Resources: Moderate budget for training and software.

- Growth: Plans to expand partnerships internationally.

Decision: Adopt IFRS to meet stakeholder expectations and support future growth.

Summary Checklist for Choosing the Right Framework

- Verify legal and regulatory requirements.

- Analyze organizational size and transaction complexity.

- Identify key stakeholders and their reporting expectations.

- Define primary reporting objectives.

- Assess resource availability and costs.

- Consider future expansion and international operations.

- Make an informed decision and plan implementation.

By following this structured approach and leveraging the mind maps provided, accountants and auditors can confidently select the accounting framework that best aligns with their organization’s needs, ensuring compliance, clarity, and operational efficiency.

2.6 Example: Transitioning from Local GAAP to IFRS in an Education Sector Entity

Transitioning from Local Generally Accepted Accounting Principles (GAAP) to International Financial Reporting Standards (IFRS) can be a complex but rewarding process for education sector entities. This example will walk through the key steps, challenges, and best practices involved in this transition, supported by mind maps and practical illustrations.

Understanding the Transition Context

Education sector entities, such as universities or private schools, often have unique financial reporting needs, including handling tuition fees, government grants, donations, and fixed assets like campus buildings. Transitioning to IFRS requires a thorough understanding of how these items are treated differently compared to Local GAAP.

Mind Map: Key Areas of Transition

Step 1: Assess Differences in Financial Statement Presentation

Local GAAP: May have different formats and line item classifications.

IFRS: Requires a clear distinction between current and non-current assets and liabilities, and presents comprehensive income.

Example: Under IFRS, the education entity must separate tuition fees receivable (current asset) from long-term receivables, if any.

Step 2: Revenue Recognition

Local GAAP: Tuition fees might be recognized on a cash basis or when invoiced.

IFRS (IFRS 15): Revenue is recognized when control of the promised service is transferred to the student, often over time.

Example: Tuition fees paid upfront for a semester are recognized proportionally over the semester rather than immediately.

Mind Map:

Step 3: Accounting for Government Grants

Local GAAP: Grants may be recognized as income when received.

IFRS (IAS 20): Grants related to assets are recognized as deferred income and amortized over the life of the asset.

Example: A government grant to build a new library is initially recorded as deferred income and recognized in profit or loss over the useful life of the library.

Step 4: Asset Valuation and Depreciation

Local GAAP: May use historical cost or revaluation models inconsistently.

IFRS (IAS 16): Allows either cost model or revaluation model but requires consistency and detailed disclosures.

Example: The university opts to revalue its campus buildings every 3 years to reflect fair value.

Step 5: Lease Accounting

Local GAAP: Operating leases might not be capitalized.

IFRS (IFRS 16): Most leases are recognized on the balance sheet as right-of-use assets and lease liabilities.

Example: Leasing of classroom equipment is recognized as an asset and liability, impacting financial ratios.

Step 6: Employee Benefits

Local GAAP: May have simplified accounting for pensions and other benefits.

IFRS (IAS 19): Requires detailed actuarial valuations and recognition of defined benefit obligations.

Example: The education entity commissions an actuarial report to measure pension liabilities accurately.

Step 7: Disclosure Requirements

IFRS requires extensive disclosures to provide transparency.

Example: The entity prepares detailed notes on revenue recognition policies, grant accounting, and lease commitments.

Step 8: Reconciliation and Adjustments

Prepare reconciliations from Local GAAP equity and profit or loss to IFRS figures at the transition date.

Example: Adjustments for deferred revenue recognition on tuition fees and capitalization of leases are documented.

Mind Map: Transition Workflow

Best Practices for a Smooth Transition

- Engage Experts: Consult IFRS specialists familiar with the education sector.

- Staff Training: Conduct workshops to familiarize accounting and finance teams with IFRS requirements.

- Documentation: Maintain detailed records of all judgments and estimates made during transition.

- Communication: Keep stakeholders informed about changes and impacts.

- Phased Approach: Implement changes in stages to manage complexity.

Summary Example: Tuition Fee Revenue Recognition

| Period | Tuition Fee Invoiced | Revenue Recognized (IFRS) | Revenue Recognized (Local GAAP) |

|---|---|---|---|

| Month 1 | $12,000 | $2,000 | $12,000 |

| Month 2 | $0 | $2,000 | $0 |

| Month 3 | $0 | $2,000 | $0 |

| Month 4 | $0 | $2,000 | $0 |

| Month 5 | $0 | $2,000 | $0 |

| Month 6 | $0 | $2,000 | $0 |

IFRS spreads revenue evenly over the semester, whereas Local GAAP recognizes it immediately.

By following these steps and best practices, education sector entities can successfully transition from Local GAAP to IFRS, ensuring compliance, improved transparency, and enhanced comparability of financial statements.

3. Fundamental Accounting Principles Embedded in Standards

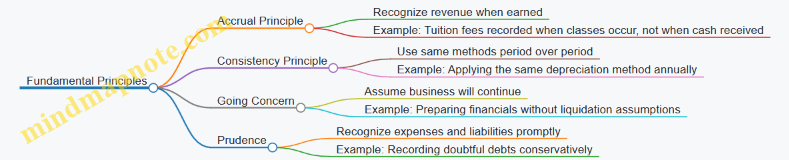

3.1 The Accrual Principle and Its Practical Implications

The Accrual Principle is one of the fundamental accounting concepts that requires revenues and expenses to be recorded when they are earned or incurred, regardless of when the cash is actually received or paid. This principle ensures that financial statements reflect the true financial position and performance of an organization during a specific period.

What is the Accrual Principle?

- Revenues are recognized when earned, not necessarily when cash is received.

- Expenses are recognized when incurred, not necessarily when cash is paid.

This contrasts with the cash basis of accounting, where transactions are recorded only when cash changes hands.

Why is the Accrual Principle Important?

- Provides a more accurate picture of financial health.

- Matches revenues with related expenses in the same period (matching principle).

- Helps stakeholders make better-informed decisions.

Mind Map: Overview of the Accrual Principle

Practical Implications of the Accrual Principle

- Revenue Recognition: Revenue must be recorded when the service is performed or goods delivered, even if payment is received later.

- Expense Recognition: Expenses must be recorded when they contribute to earning revenue, even if payment is made later.

- Adjusting Entries: At the end of accounting periods, accountants make adjusting entries to record accrued revenues and expenses.

Mind Map: Practical Steps for Applying the Accrual Principle

Example 1: Revenue Recognition in an Educational Institution

An online education platform delivers a 6-month course starting January 1st. The total fee is $1,200, paid upfront.

- Under accrual accounting, the platform recognizes $200 revenue each month (1/6 of $1,200), not the full $1,200 in January.

- This matches the revenue to the period when the service is actually delivered.

Adjusting Entry at Month-End:

- Debit Unearned Revenue $200

- Credit Revenue $200

Example 2: Expense Recognition for Utilities in a Finance Firm

A finance firm receives a utility bill of $900 for December, but the bill is paid in January.

- Under accrual accounting, the $900 expense is recorded in December when the utilities were consumed.

Adjusting Entry at Year-End:

- Debit Utilities Expense $900

- Credit Utilities Payable $900

Example 3: Accrued Salaries in an Educational Sector Entity

Employees earn $5,000 in salaries during the last week of December, but payment is scheduled for January 5th.

- Salaries expense must be recorded in December to reflect the period when employees provided their services.

Adjusting Entry:

- Debit Salaries Expense $5,000

- Credit Salaries Payable $5,000

Best Practices for Accountants and Auditors

- Regularly review contracts and service delivery timelines to accurately recognize revenue.

- Maintain detailed records of incurred expenses even if payment is pending.

- Implement a robust system for making adjusting entries at period-end.

- Train accounting teams on the importance and application of the accrual principle.

By adhering to the accrual principle, accountants and auditors ensure that financial statements present a true and fair view of an organization’s financial performance and position, which is critical for transparency and compliance with accounting standards.

3.2 The Consistency Principle: Ensuring Comparability Over Time

The Consistency Principle is a fundamental accounting concept that requires organizations to apply the same accounting methods and principles from one accounting period to the next. This principle ensures that financial statements are comparable over time, allowing stakeholders such as accountants, auditors, investors, and management to analyze trends, make informed decisions, and assess the financial health of an entity accurately.

Why is the Consistency Principle Important?

- Comparability: Enables users to compare financial data across different periods.

- Reliability: Builds trust in financial reports by maintaining uniformity.

- Transparency: Reduces confusion caused by frequent changes in accounting policies.

- Decision-Making: Assists management and external users in making sound financial decisions.

When Can Changes Be Made?

While consistency is critical, changes in accounting methods are allowed only when:

- Required by new accounting standards or regulations.

- The new method provides more reliable and relevant information.

In such cases, changes must be:

- Disclosed clearly in the financial statements.

- Explained in notes to the accounts.

- Adjusted retrospectively if applicable.

Mind Map: Core Concepts of the Consistency Principle

Best Practice: Documenting Accounting Policies

Maintain a comprehensive accounting policy manual that:

- Clearly states the chosen accounting methods.

- Records any changes and the rationale behind them.

- Ensures all team members and auditors are aware of the policies.

Example 1: Depreciation Method Consistency in an Educational Institution

Scenario: A university has been using the straight-line method to depreciate its computer equipment for the past five years.

- Application: The university continues using the straight-line method to ensure comparability of asset values and expenses over time.

- Change: If the university decides to switch to the declining balance method for better matching of expenses with usage, it must disclose this change in the financial statements and adjust prior periods retrospectively.

Result: Stakeholders can compare depreciation expenses year-over-year and understand the impact of the change.

Mind Map: Example - Depreciation Method Consistency

Example 2: Revenue Recognition in a Finance Firm

Scenario: A finance company recognizes revenue when cash is received (cash basis).

- Consistency: The company applies the cash basis consistently for all contracts.

- Change: To comply with IFRS 15, the company switches to accrual basis revenue recognition.

- Action: The company discloses the change, explains the reasons, and adjusts previous financial statements to reflect the accrual basis.

Result: Financial reports become more comparable and aligned with international standards.

Mind Map: Example - Revenue Recognition Consistency

Summary

The Consistency Principle is vital for maintaining the integrity and usefulness of financial statements. By applying accounting methods consistently and transparently managing any changes, accountants and auditors ensure that financial information remains reliable and comparable over time, ultimately supporting better financial analysis and decision-making.

3.3 The Going Concern Assumption in Financial Statements

The Going Concern Assumption is a fundamental accounting principle that assumes a company will continue its operations into the foreseeable future and has no intention or need to liquidate or significantly curtail its business activities. This assumption underpins the preparation of financial statements, allowing assets and liabilities to be recorded on the basis that the business will remain operational.

Why is the Going Concern Assumption Important?

- It justifies the use of historical cost accounting rather than liquidation values.

- It impacts asset valuation, depreciation, and amortization schedules.

- It influences the classification of liabilities as current or long-term.

Mind Map: Going Concern Assumption Overview

Indicators That May Threaten Going Concern

Accountants and auditors must evaluate whether there are any signs that a business might not continue as a going concern. Common indicators include:

- Recurring operating losses or negative cash flows

- Inability to meet debt obligations

- Loss of major customers or suppliers

- Legal or regulatory issues

- Plans to liquidate or cease operations

Best Practice: Assessing Going Concern Status

- Conduct regular financial health checks focusing on liquidity and solvency ratios.

- Review management’s forecasts and plans for future operations.

- Document all findings and judgments clearly.

- Communicate concerns promptly to stakeholders.

Example 1: Going Concern Assessment for a University

A mid-sized private university has experienced declining enrollment over the past three years, resulting in operating losses and increased reliance on short-term borrowing. The finance team prepares the financial statements assuming the university will continue operating but notes the following:

- Cash flow projections show potential liquidity issues in the next 12 months.

- Management has a plan to increase enrollment and reduce costs.

- There is no intention to close or sell the university.

Application: The accountants disclose a going concern uncertainty note in the financial statements, explaining the risks and management’s mitigation plans. They continue to prepare the statements on a going concern basis but highlight the potential risks.

Mind Map: Going Concern Assessment Process

Example 2: Auditor’s Role in Going Concern Evaluation

An accounting firm audits a small finance company facing significant losses and overdue debts. The auditor:

- Reviews management’s assessment of going concern.

- Examines cash flow forecasts and debt covenants.

- Identifies material uncertainties about the company’s ability to continue.

Outcome: The auditor includes an emphasis of matter paragraph in the audit report to highlight the going concern uncertainty, ensuring users of the financial statements are aware of the risks.

Practical Tips for Accountants and Auditors

- Always question assumptions behind management’s going concern evaluation.

- Use both quantitative data (financial ratios, forecasts) and qualitative factors (market trends, legal issues).

- Keep communication transparent with management and audit committees.

- Update assessments regularly, especially during volatile economic conditions.

Summary

The going concern assumption is critical for accurate financial reporting. Accountants and auditors must vigilantly assess whether this assumption remains valid and disclose any uncertainties to maintain transparency and trust in financial statements.

3.4 The Prudence (Conservatism) Principle: Balancing Optimism and Caution

The Prudence Principle, also known as the Conservatism Principle, is a fundamental accounting concept that guides accountants to exercise caution when faced with uncertainty. It emphasizes that potential expenses and liabilities should be recognized promptly, while gains should only be recorded when they are assured. This principle helps prevent the overstatement of financial health and ensures that financial statements provide a realistic and reliable picture of an organization’s financial position.

Key Concepts of the Prudence Principle

- Cautious Recognition: Recognize losses and liabilities as soon as they are foreseeable.

- Delayed Recognition of Gains: Record revenues and gains only when they are realized or virtually certain.

- Avoid Over-Optimism: Prevent overestimating assets or income.

- Ensuring Reliability: Financial statements should not mislead stakeholders by presenting an overly optimistic view.

Mind Map: Prudence Principle Overview

Practical Examples of the Prudence Principle

Example 1: Provision for Bad Debts

An education services company has several outstanding tuition fee payments. Some students have delayed payments beyond the due date, and there is uncertainty about their ability to pay. Applying the prudence principle, the accountant estimates a provision for bad debts to cover potential losses rather than waiting until the debts are confirmed as uncollectible.

- Best Practice: Use historical data and current economic conditions to estimate the provision conservatively.

Example 2: Inventory Valuation

A finance firm holds technology equipment as inventory. Due to rapid technological changes, some equipment may become obsolete. The prudence principle requires the firm to write down the value of inventory to the lower of cost or net realizable value, reflecting potential losses early.

- Best Practice: Regularly review inventory for obsolescence and adjust valuations accordingly.

Example 3: Litigation Contingency

An auditor is aware of a pending lawsuit against a client that may result in a financial penalty. Although the outcome is uncertain, the prudence principle dictates recognizing a provision if the loss is probable and can be reasonably estimated.

- Best Practice: Collaborate with legal advisors to assess the likelihood and estimate the potential loss conservatively.

Mind Map: Applying Prudence in Financial Reporting

Balancing Prudence with Other Principles

While prudence encourages caution, it must be balanced with the Faithful Representation and Relevance principles to avoid excessive conservatism that could distort financial information.

-

Example: Over-provisioning for bad debts might understate profits and mislead stakeholders.

-

Best Practice: Regularly review estimates and provisions to ensure they remain reasonable and reflect current conditions.

Summary

The Prudence Principle is essential for maintaining trust and reliability in financial reporting. By recognizing potential losses early and gains only when certain, accountants and auditors help present a balanced and cautious view of an organization’s financial health.

Additional Mind Map: Summary of Prudence Principle Benefits

3.5 Best Practice: Documenting Accounting Policies to Reflect Principles

Documenting accounting policies is a critical best practice that ensures consistency, transparency, and compliance with fundamental accounting principles. Well-documented policies serve as a reference for accountants, auditors, and stakeholders, helping to maintain uniformity in financial reporting and facilitating easier audits.

Why Document Accounting Policies?

- Consistency: Ensures that accounting treatments are applied uniformly across periods.

- Transparency: Provides clear guidance on how transactions are recognized and measured.

- Compliance: Demonstrates adherence to accounting standards and principles.

- Training: Acts as a resource for onboarding new accounting staff.

Key Elements to Include in Accounting Policy Documentation

- Policy Objective: What the policy aims to achieve.

- Scope: Which transactions or accounts the policy covers.

- Accounting Principle: The fundamental principle(s) the policy is based on (e.g., accrual, prudence).

- Measurement Basis: How values are measured (e.g., historical cost, fair value).

- Recognition Criteria: When and how transactions are recognized.

- Disclosure Requirements: Information to be disclosed in financial statements.

- Examples: Practical illustrations to clarify application.

Mind Map: Components of Accounting Policy Documentation

Mind Map: Benefits of Documenting Accounting Policies

Example 1: Documenting Revenue Recognition Policy for an Educational Institution

Policy Objective: To recognize revenue from tuition fees in accordance with the accrual principle and IFRS 15.

Scope: Applies to all tuition fee income from students.

Accounting Principle: Accrual principle — revenue recognized when earned, not when cash is received.

Measurement Basis: Transaction price agreed in enrollment contracts.

Recognition Criteria: Revenue is recognized over the period of instruction delivery.

Disclosure Requirements: Total tuition revenue recognized, deferred revenue balances.

Example: If a student pays $12,000 for a 12-month course upfront, the institution recognizes $1,000 revenue each month.

Example 2: Documenting Asset Depreciation Policy

Policy Objective: To systematically allocate the cost of tangible fixed assets over their useful lives.

Scope: Applies to all tangible fixed assets such as computers, furniture, and vehicles.

Accounting Principle: Matching principle — expenses recognized in the same period as related revenues.

Measurement Basis: Historical cost less residual value.

Recognition Criteria: Depreciation expense recognized monthly using the straight-line method.

Disclosure Requirements: Depreciation methods, useful lives, accumulated depreciation.

Example: A computer purchased for $1,200 with a useful life of 3 years and no residual value will be depreciated at $33.33 per month.

Practical Tips for Effective Documentation

- Use clear, simple language avoiding jargon.

- Include flowcharts or diagrams where helpful.

- Regularly review and update policies to reflect changes in standards.

- Involve cross-functional teams (finance, audit, operations) to ensure completeness.

- Store policies in an accessible digital repository.

Mind Map: Steps to Create Accounting Policy Documentation

By thoroughly documenting accounting policies aligned with fundamental principles, organizations empower their accounting and audit teams to produce reliable, consistent, and compliant financial reports. This practice reduces ambiguity, supports training, and strengthens internal controls, ultimately enhancing stakeholder confidence.

3.6 Example: Applying the Accrual Principle in Revenue Recognition for Educational Services

The accrual principle is fundamental in accounting, requiring that revenue be recognized when it is earned, regardless of when the cash is received. In the context of educational services, this means recognizing tuition fees and other revenues in the period the educational services are delivered, not necessarily when the payment is made.

Mind Map: Accrual Principle in Educational Revenue Recognition

Scenario 1: Tuition Fees Paid in Advance

Situation: A university charges $12,000 for a semester-long course. A student pays the full amount upfront on January 1st, but the semester runs from February 1st to June 30th.

Accrual Principle Application:

- The university should recognize revenue monthly from February through June, $2,400 per month ($12,000 / 5 months).

- Even though cash was received in January, revenue is not recognized until the service is delivered.

Journal Entries:

| Date | Account | Debit | Credit |

|---|---|---|---|

| Jan 1 | Cash | 12,000 | |

| Jan 1 | Unearned Revenue (Liability) | 12,000 | |

| Feb 28 | Unearned Revenue | 2,400 | |

| Feb 28 | Tuition Revenue | 2,400 | |

| Mar 31 | Unearned Revenue | 2,400 | |

| Mar 31 | Tuition Revenue | 2,400 | |

| … | … | … | … |

Scenario 2: Monthly Payment Plan

Situation: Another student opts to pay $2,400 monthly for the same semester, paying at the beginning of each month.

Accrual Principle Application:

- Revenue is recognized each month as the service is provided.

- Since payment coincides with service delivery, revenue recognition and cash receipt align.

Journal Entries (Monthly):

| Date | Account | Debit | Credit |

|---|---|---|---|

| Feb 1 | Cash | 2,400 | |

| Feb 1 | Tuition Revenue | 2,400 |

Scenario 3: Conditional Grants for Educational Programs

Situation: An educational institution receives a $50,000 grant on March 1st to develop a new online course. The grant is conditional upon delivering the course by August 31st.

Accrual Principle Application:

- The grant revenue is recognized only when the condition is met (i.e., course delivery).

- Until then, the grant is recorded as deferred income.

Journal Entries:

| Date | Account | Debit | Credit |

|---|---|---|---|

| Mar 1 | Cash | 50,000 | |

| Mar 1 | Deferred Grant Income | 50,000 | |

| Aug 31 | Deferred Grant Income | 50,000 | |

| Aug 31 | Grant Revenue | 50,000 |

Summary Table: Revenue Recognition Timing

| Revenue Type | Payment Timing | Revenue Recognition Timing | Accrual Principle Impact |

|---|---|---|---|

| Tuition Paid in Advance | Before service | Over service period | Recognize revenue as service is delivered |

| Tuition Monthly Plan | During service | Monthly as service is delivered | Revenue recognition aligns with cash receipt |

| Conditional Grants | Before condition met | After condition fulfillment | Revenue deferred until conditions are met |

Best Practices for Accountants and Auditors

- Maintain clear schedules of service delivery periods to accurately match revenue recognition.

- Use deferred revenue accounts to track payments received before service delivery.

- Document all conditions attached to grants or donations to determine proper recognition timing.

- Regularly review contracts and payment terms to ensure compliance with the accrual principle.

By applying the accrual principle carefully, educational institutions can produce financial statements that accurately reflect their financial performance and position, providing stakeholders with reliable and timely information.

4. Detailed Exploration of Key Accounting Standards

4.1 Revenue Recognition Standards: Criteria and Timing

Revenue recognition is a fundamental aspect of accounting standards that determines when and how revenue should be recorded in the financial statements. Proper revenue recognition ensures that financial reports accurately reflect an entity’s financial performance and position.

Key Principles of Revenue Recognition

The most widely adopted framework for revenue recognition is IFRS 15 / ASC 606, which follows a five-step model to recognize revenue from contracts with customers.

Five-Step Revenue Recognition Model Mind Map

Criteria for Revenue Recognition

- Contract Existence: There must be a valid contract with enforceable rights.

- Identification of Performance Obligations: Distinct goods or services must be identified.

- Transaction Price Determination: The amount expected to be received must be measurable.

- Allocation of Price: The transaction price must be allocated to each performance obligation.

- Satisfaction of Performance Obligations: Revenue is recognized when control of goods or services transfers to the customer.

Timing of Revenue Recognition

Revenue can be recognized:

- At a point in time: When control of the asset transfers to the customer (e.g., delivery of goods).

- Over time: When the customer simultaneously receives and consumes the benefits (e.g., services rendered over a period).

Mind Map: Timing of Revenue Recognition

Best Practices for Revenue Recognition

- Document Contracts Clearly: Ensure contracts specify performance obligations and payment terms.

- Use Consistent Methods: Apply the same recognition method consistently across similar contracts.

- Regularly Review Estimates: Update variable consideration and progress measurements as new information arises.

- Train Staff: Keep accounting and sales teams informed about revenue recognition rules.

Examples

Example 1: Educational Services Subscription

An online education platform sells annual subscriptions for access to courses.

- Contract: One year subscription.

- Performance Obligation: Access to educational content over 12 months.

- Transaction Price: $1,200.

- Recognition: Revenue is recognized ratably over the subscription period as the service is delivered.

Example 2: Sale of Accounting Software License

A finance firm sells a software license with a one-time fee.

- Contract: One-time sale.

- Performance Obligation: Delivery of software license.

- Transaction Price: $5,000.

- Recognition: Revenue recognized at the point in time when the license is delivered and control transfers.

Example 3: Customized Financial Consulting Services

An auditor provides a customized consulting service over 6 months.

- Contract: Consulting engagement.

- Performance Obligation: Delivery of consulting services.

- Transaction Price: $60,000.

- Recognition: Revenue recognized over time based on milestones or percentage of completion.

Summary

Understanding the criteria and timing for revenue recognition is critical for accurate financial reporting. Following the five-step model ensures compliance with accounting standards and provides transparency to stakeholders.

For accountants and auditors in finance and education sectors, mastering revenue recognition standards helps in avoiding misstatements and supports better decision-making.

4.2 Standards on Asset Valuation and Impairment

Asset valuation and impairment are critical components of accounting standards, ensuring that the financial statements reflect a true and fair view of an entity’s financial position. This section explores the key principles, methodologies, and examples to help accountants and auditors accurately apply these standards.

Understanding Asset Valuation

Asset valuation refers to the process of determining the monetary value of an asset at a given point in time. Accounting standards provide guidance on how to measure assets initially and subsequently.

Key Valuation Bases:

- Historical Cost: The original purchase price of the asset.

- Fair Value: The price that would be received to sell an asset in an orderly transaction between market participants.

- Net Realizable Value: The estimated selling price in the ordinary course of business minus costs to complete and sell.

- Value in Use: The present value of future cash flows expected from the asset.

Mind Map: Asset Valuation Methods

Impairment of Assets

Impairment occurs when the carrying amount of an asset exceeds its recoverable amount, indicating that the asset’s value has declined.

Key Concepts:

- Carrying Amount: The value at which an asset is recognized on the balance sheet.

- Recoverable Amount: The higher of an asset’s fair value less costs to sell and its value in use.

- Indicators of Impairment: External (market decline, legal changes) and internal (obsolescence, physical damage).

Mind Map: Asset Impairment Process

Best Practices for Asset Valuation and Impairment

- Regular Review: Conduct periodic impairment tests, especially when indicators are present.

- Use Reliable Data: Base valuations on observable market data whenever possible.

- Document Assumptions: Clearly record assumptions used in value in use calculations.

- Collaborate with Experts: Engage valuation specialists for complex assets.

- Consistent Application: Apply valuation methods consistently across reporting periods.

Example 1: Valuing a Building for an Educational Institution

An educational institution purchased a building for $2,000,000 five years ago. The building is recorded at historical cost less accumulated depreciation. Due to changes in the local real estate market, the fair value of the building is now estimated at $1,500,000.

- Step 1: Determine carrying amount (historical cost minus depreciation).

- Step 2: Assess indicators of impairment (market value decline).

- Step 3: Calculate recoverable amount (higher of fair value less costs to sell and value in use).

- Step 4: If carrying amount > recoverable amount, recognize impairment loss.

Outcome: The institution recognizes an impairment loss of $X, reducing the carrying amount to the recoverable amount.

Example 2: Impairment Testing for Financial Instruments in a Finance Firm

A finance firm holds bonds classified as financial assets. Due to a downgrade in the issuer’s credit rating, the fair value of the bonds has declined significantly.

- Step 1: Identify impairment indicators (credit rating downgrade).

- Step 2: Measure recoverable amount (fair value less costs to sell).

- Step 3: Compare with carrying amount.

- Step 4: Recognize impairment loss if applicable.

Outcome: The firm records an impairment loss in the income statement, reflecting the reduced recoverable amount.

Summary

Understanding and applying asset valuation and impairment standards ensures that financial statements provide accurate and reliable information. Regular reviews, proper documentation, and adherence to best practices help accountants and auditors maintain compliance and support sound financial decision-making.

4.3 Accounting for Liabilities and Provisions

Accounting for liabilities and provisions is a critical aspect of financial reporting that ensures organizations accurately represent their obligations and potential future outflows. This section will cover the definitions, recognition criteria, measurement, and disclosure requirements for liabilities and provisions, along with best practices and practical examples tailored for accountants and auditors in the finance and education sectors.

Understanding Liabilities and Provisions

- Liabilities: Present obligations arising from past events, the settlement of which is expected to result in an outflow of resources.

- Provisions: A type of liability of uncertain timing or amount, recognized when a present obligation exists but the exact amount or timing is uncertain.

Mind Map: Classification of Liabilities

Recognition Criteria for Provisions (IAS 37 / Relevant GAAP Guidance)

- There must be a present obligation (legal or constructive) as a result of a past event.

- It is probable (more likely than not) that an outflow of resources will be required to settle the obligation.

- A reliable estimate can be made of the amount of the obligation.

Best Practice: Maintain detailed documentation of the events leading to the obligation and the rationale for recognizing provisions.

Measurement of Liabilities and Provisions

- Liabilities are generally measured at the amount expected to be paid to settle the obligation.

- Provisions are measured at the best estimate of the expenditure required to settle the present obligation at the reporting date.

- When the effect of the time value of money is material, provisions should be discounted to present value.

Mind Map: Steps to Account for Provisions

Example 1: Warranty Provision in an Educational Equipment Supplier

An educational equipment supplier sells devices with a 1-year warranty. Based on past experience, 3% of devices sold require repairs costing an average of $200 each.

- Scenario: 1,000 devices sold in the year.

- Calculation: 1,000 devices * 3% failure rate = 30 devices expected to require repair.

- Provision Amount: 30 devices * $200 = $6,000.

Accounting Entry:

| Account | Debit | Credit |

|---|---|---|

| Warranty Expense | $6,000 | |

| Provision for Warranty | $6,000 |

Best Practice: Regularly update the provision based on actual warranty claims and revise estimates accordingly.

Example 2: Legal Provision for a Pending Lawsuit at a University

A university is involved in a lawsuit related to a contractual dispute. Legal counsel estimates a 70% chance the university will have to pay damages estimated between $50,000 and $80,000.

- Since the outflow is probable and estimable, a provision should be recognized.

- Use the best estimate or the midpoint: ($50,000 + $80,000) / 2 = $65,000.

Accounting Entry:

| Account | Debit | Credit |

|---|---|---|

| Legal Expense | $65,000 | |

| Provision for Lawsuit | $65,000 |

Best Practice: Disclose the nature of the provision and uncertainties in the notes to the financial statements.

Handling Contingent Liabilities

- Contingent liabilities are possible obligations that arise from past events but whose existence will be confirmed only by uncertain future events.

- They are not recognized but disclosed unless the possibility of outflow is remote.

Mind Map: Distinguishing Provisions vs Contingent Liabilities

Best Practices Summary

- Documentation: Keep thorough records of all assumptions, estimates, and judgments.

- Regular Review: Update provisions at each reporting date to reflect new information.

- Communication: Work closely with legal and operational teams to assess obligations.

- Disclosure: Provide transparent notes explaining the nature, timing, and uncertainties of liabilities and provisions.

Example 3: Provision for Restructuring in a Finance Firm

A finance firm plans to close a branch office, incurring employee termination costs estimated at $120,000.

- The firm has communicated the plan to employees and has a detailed formal plan.

- Recognition of a restructuring provision is appropriate.

Accounting Entry:

| Account | Debit | Credit |

|---|---|---|

| Restructuring Expense | $120,000 | |

| Provision for Restructuring | $120,000 |

Best Practice: Ensure the provision only includes direct costs related to the restructuring.

By integrating these concepts, mind maps, and examples, accountants and auditors can confidently apply accounting standards related to liabilities and provisions, ensuring accurate and compliant financial reporting.

4.4 Standards Governing Leases and Lease Accounting

Lease accounting has undergone significant changes with the introduction of new standards such as IFRS 16 and ASC 842. These standards aim to increase transparency and comparability by requiring lessees to recognize most leases on their balance sheets.

Key Concepts in Lease Accounting

- Lease Definition: A contract that conveys the right to use an asset for a period of time in exchange for consideration.

- Lessor vs Lessee: The lessor owns the asset; the lessee obtains the right to use it.

- Types of Leases: Finance (capital) leases and operating leases.

- Recognition: Lessees recognize a right-of-use (ROU) asset and lease liability.

Mind Map: Overview of Lease Accounting Standards

IFRS 16 and ASC 842: Core Requirements

| Aspect | IFRS 16 | ASC 842 |

|---|---|---|

| Lessee Accounting | Recognize ROU asset and lease liability for almost all leases | Same as IFRS 16, with some exceptions for short-term leases |

| Lease Classification | No distinction for lessees; all leases capitalized | Operating vs Finance leases classification retained |

| Lessor Accounting | Similar to IAS 17; operating and finance leases | Similar to previous standards |

| Lease Term Definition | Non-cancellable period + options likely to be exercised | Similar approach |

Best Practice: Assessing Lease Contracts Thoroughly

- Review lease terms carefully to identify embedded leases.

- Determine lease term including renewal and termination options.

- Use consistent discount rates for lease liability measurement.

- Document judgments and assumptions clearly.

Example 1: University Campus Building Lease