IFRS and GAAP Reporting

1. Introduction to IFRS and GAAP

1.1 Overview of IFRS and GAAP Frameworks

Understanding the foundational frameworks of IFRS (International Financial Reporting Standards) and GAAP (Generally Accepted Accounting Principles) is essential for accountants, auditors, and compliance officers working in finance and government sectors. Both frameworks guide the preparation and presentation of financial statements but differ in origin, structure, and application.

What is IFRS?

- Developed and maintained by the International Accounting Standards Board (IASB).

- Used in over 140 countries worldwide, including the European Union, Canada, and many Asian countries.

- Principles-based framework emphasizing transparency, comparability, and global consistency.

What is GAAP?

- Established by the Financial Accounting Standards Board (FASB) in the United States.

- Rules-based framework primarily used in the U.S.

- Focuses on detailed rules and guidelines to ensure consistency and comparability within the U.S. market.

Mind Map: IFRS Framework

Mind Map: GAAP Framework

Key Differences Between IFRS and GAAP

| Aspect | IFRS | GAAP |

|---|---|---|

| Origin | International Accounting Standards Board (IASB) | Financial Accounting Standards Board (FASB) |

| Approach | Principles-based | Rules-based |

| Inventory Valuation | Prohibits LIFO method | Allows LIFO method |

| Revenue Recognition | Single model (IFRS 15) | Detailed industry-specific guidance |

| Development Stage | Continuously evolving with global input | More established with detailed rules |

Practical Example: Basic Financial Statement Comparison

Consider a company recognizing revenue from a long-term contract.

- Under IFRS: Revenue is recognized based on the transfer of control over time or at a point in time, using a five-step model.

- Under GAAP: Revenue recognition follows similar principles but may include more prescriptive guidance depending on the industry.

Example: A software company sells a 12-month subscription for $12,000.

| Month | IFRS Revenue Recognition | GAAP Revenue Recognition |

|---|---|---|

| 1 | $1,000 | $1,000 |

| 6 | $6,000 | $6,000 |

| 12 | $12,000 | $12,000 |

Both frameworks recognize revenue evenly over the subscription period, demonstrating convergence in this area.

Summary

Understanding the IFRS and GAAP frameworks provides a foundation for accurate and compliant financial reporting. While IFRS offers a globally accepted, principles-based approach, GAAP provides detailed, rules-based guidance primarily for U.S. entities. Awareness of these frameworks’ characteristics helps finance professionals navigate reporting requirements effectively.

1.2 Key Differences Between IFRS and GAAP

Understanding the key differences between IFRS (International Financial Reporting Standards) and GAAP (Generally Accepted Accounting Principles) is essential for accountants, auditors, and compliance officers working in multinational environments or transitioning between frameworks. Below, we explore the primary distinctions with clear examples and mind maps to aid comprehension.

Overview Mind Map: IFRS vs GAAP Key Differences

Conceptual Approach

IFRS is principles-based, focusing on the spirit and intent of accounting standards, allowing more judgment and flexibility.

GAAP is rules-based, providing detailed rules and guidelines, which can limit flexibility but reduce ambiguity.

Example:

- Under IFRS, an accountant might apply judgment to classify a complex financial instrument based on its substance.

- Under GAAP, the classification might be strictly dictated by detailed rules, leaving less room for interpretation.

Financial Statement Presentation

| Aspect | IFRS | GAAP |

|---|---|---|

| Statement Format | Flexible; allows presentation choices | Prescribed formats (e.g., classified balance sheet) |

| Statement of OCI | Includes items like revaluation surplus | More limited OCI items |

Example:

- IFRS allows presenting expenses by nature (e.g., depreciation, raw materials) or by function (e.g., cost of sales, administrative expenses).

- GAAP generally requires presentation by function.

Revenue Recognition

Both IFRS 15 and GAAP ASC 606 follow a 5-step model but differ in application nuances.

Example:

- IFRS allows recognizing revenue when control transfers, which may happen over time or at a point in time.

- GAAP may have more detailed guidance on contract modifications and variable consideration.

Mind Map:

Inventory Accounting

| Aspect | IFRS | GAAP |

|---|---|---|

| Cost Formulas Allowed | FIFO, Weighted Average; LIFO prohibited | FIFO, Weighted Average, LIFO allowed |

| Write-downs | Reversal of write-downs allowed if value recovers | No reversal allowed |

Example:

- A company using LIFO inventory costing under GAAP must switch to FIFO or weighted average if reporting under IFRS.

- If inventory value recovers after a write-down, IFRS permits reversal, GAAP does not.

Lease Accounting

IFRS 16 requires lessees to recognize nearly all leases on the balance sheet as right-of-use assets and lease liabilities.

GAAP ASC 842 distinguishes between finance leases and operating leases, with different recognition and expense patterns.

Example:

- Under IFRS, a 3-year office lease must be capitalized on the balance sheet.

- Under GAAP, an operating lease may still be off-balance sheet with straight-line rent expense.

Impairment of Assets

| Aspect | IFRS | GAAP |

|---|---|---|

| Test Method | One-step: compare carrying amount to recoverable amount (higher of fair value less costs to sell and value in use) | Two-step: compare carrying amount to undiscounted cash flows, then measure impairment loss |

Example:

- IFRS impairment test may result in earlier recognition of impairment losses.

- GAAP requires an initial test before measuring impairment.

Development Costs

| Aspect | IFRS | GAAP |

|---|---|---|

| Treatment | Capitalize development costs if criteria met | Expense all development costs as incurred |

Example:

- IFRS allows capitalizing costs for developing a new product if technical feasibility and future economic benefits are demonstrated.

- GAAP requires expensing these costs immediately.

Summary Example: Inventory Accounting Comparison

Scenario: A company has 1,000 units of inventory purchased at $10 each, and 1,000 units purchased later at $12 each. The market value drops to $9 per unit.

-

Under IFRS:

- LIFO is not allowed; company uses FIFO.

- Inventory value is written down to $9 per unit.

- If market value recovers to $11, reversal of write-down is allowed.

-

Under GAAP:

- Company can use LIFO.

- Inventory is valued at the lower of cost or market.

- No reversal of write-down allowed if market value recovers.

Final Mind Map: Practical Impact on Reporting

This section equips finance professionals with a clear understanding of the fundamental differences between IFRS and GAAP, supported by practical examples and visual mind maps to enhance retention and application.

1.3 Importance of Compliance for Accountants and Auditors

Compliance with IFRS (International Financial Reporting Standards) and GAAP (Generally Accepted Accounting Principles) is critical for accountants and auditors to ensure the accuracy, transparency, and reliability of financial statements. Non-compliance can lead to legal penalties, loss of stakeholder trust, and financial misstatements that could severely impact an organization’s reputation and operations.

Why Compliance Matters

- Legal and Regulatory Requirements: Many jurisdictions mandate adherence to either IFRS or GAAP. Failure to comply can result in fines, sanctions, or legal action.

- Investor Confidence: Accurate and compliant financial reporting builds trust with investors, creditors, and other stakeholders.

- Audit Quality: Auditors rely on compliance to assess the fairness of financial statements and issue unqualified opinions.

- Internal Decision-Making: Management depends on compliant reports for strategic planning and operational control.

Mind Map: Importance of Compliance for Accountants and Auditors

Practical Example: Consequences of Non-Compliance

Scenario: An auditor discovers that a company has not properly recognized revenue according to IFRS 15, leading to overstated income.

- Impact:

- The financial statements are misleading.

- The auditor issues a qualified opinion.

- The company faces regulatory scrutiny and potential fines.

- Investor confidence drops, affecting stock price.

Best Practice: Accountants should ensure revenue recognition policies align with IFRS 15, and auditors should verify these policies during audits.

Mind Map: Compliance Process for Accountants and Auditors

Example: Compliance in Action – Revenue Recognition

Step 1: Accountant reviews contract terms to identify performance obligations.

Step 2: Applies IFRS 15 five-step model to recognize revenue appropriately.

Step 3: Auditor tests sample transactions to ensure revenue is recognized in the correct period.

Outcome: Financial statements reflect true economic activity, satisfying both IFRS and auditor requirements.

Summary

For accountants and auditors, compliance is not just about following rules but ensuring the integrity and usefulness of financial information. It safeguards the organization from risks and supports sound financial decision-making.

1.4 Practical Example: Comparing a Basic Financial Statement Under IFRS and GAAP

In this section, we will explore a practical example comparing a simple financial statement prepared under IFRS and GAAP. This will help accountants, auditors, and compliance officers understand the nuances and best practices when preparing financial reports under both frameworks.

Scenario:

A company, ABC Ltd., prepares a statement of financial position (balance sheet) as of December 31, 2023. We will compare how certain line items are presented and measured under IFRS and GAAP.

Key Differences Mind Map

Example Financial Statement Comparison

| Line Item | IFRS Presentation | GAAP Presentation | Notes/Best Practices |

|---|---|---|---|

| Cash and Cash Equivalents | Reported as current asset | Reported as current asset | Both frameworks treat similarly |

| Property, Plant and Equipment | Can be reported at cost or revalued amount | Reported at historical cost less depreciation | IFRS allows revaluation model; GAAP does not |

| Intangible Assets | Recognized if probable future benefits exist | Similar recognition criteria | IFRS more flexible on development costs |

| Deferred Tax Assets | Reported as non-current asset | Reported as non-current asset | Both require recognition of deferred taxes |

| Equity | Share capital, reserves, retained earnings | Common stock, additional paid-in capital, retained earnings | Terminology differs but concepts align |

Practical Example: Property, Plant and Equipment (PPE) Valuation

IFRS Approach:

- ABC Ltd. chooses the revaluation model.

- Original cost: $1,000,000

- Accumulated depreciation: $200,000

- Fair value at reporting date: $900,000

Calculation:

- Carrying amount under cost model = $1,000,000 - $200,000 = $800,000

- Carrying amount under revaluation model = $900,000 (fair value)

Presentation:

- PPE reported at $900,000

- Revaluation surplus recognized in Other Comprehensive Income (OCI)

GAAP Approach:

- PPE reported at historical cost less accumulated depreciation

- Carrying amount = $800,000

Best Practice:

- Clearly disclose the valuation method used.

- Provide reconciliation of carrying amounts.

Mind Map: Preparing Financial Statements Under IFRS and GAAP

Summary of Best Practices with Examples

| Best Practice | Example Scenario |

|---|---|

| Use consistent classification of assets/liabilities | Classify inventory as current asset under both IFRS and GAAP |

| Disclose accounting policies clearly | Note explaining use of revaluation model for PPE under IFRS |

| Reconcile differences when transitioning | Provide reconciliation schedule when moving from GAAP to IFRS |

| Use clear terminology for stakeholders | Use “Statement of Financial Position” for IFRS reports |

| Ensure fair value measurements are supported | Obtain independent valuation for PPE revaluation |

By integrating these examples and mind maps, professionals can better grasp the practical implications of preparing financial statements under IFRS and GAAP, ensuring accuracy, compliance, and clarity in reporting.

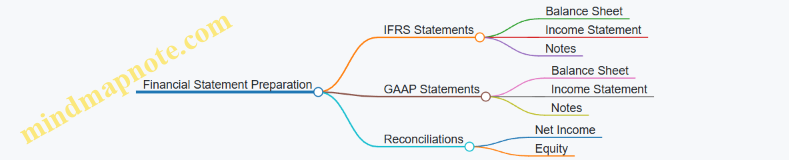

2. Financial Statement Presentation

2.1 IFRS Financial Statement Structure and Requirements

Overview

IFRS (International Financial Reporting Standards) provides a globally accepted framework for preparing financial statements. The structure and presentation requirements are designed to ensure transparency, comparability, and relevance of financial information.

Core Financial Statements under IFRS

IFRS requires the preparation of the following primary financial statements:

- Statement of Financial Position (Balance Sheet)

- Statement of Profit or Loss and Other Comprehensive Income

- Statement of Changes in Equity

- Statement of Cash Flows

- Notes to the Financial Statements

Mind Map: IFRS Financial Statement Components

Detailed Requirements

Statement of Financial Position

- Must classify assets and liabilities as current and non-current.

- Equity is presented separately from liabilities.

- IFRS does not prescribe a specific format but requires clear presentation.

Statement of Profit or Loss and Other Comprehensive Income

- Can be presented as a single statement or two separate statements.

- Must include all income and expenses recognized during the period.

- Other comprehensive income items include unrealized gains/losses, foreign exchange differences, etc.

Statement of Changes in Equity

- Shows movements in equity components during the reporting period.

- Includes transactions with owners (e.g., dividends, share issuance).

Statement of Cash Flows

- Must classify cash flows into operating, investing, and financing activities.

- IFRS allows the indirect or direct method for operating activities.

Notes to the Financial Statements

- Provide additional detail and explanation.

- Include significant accounting policies, judgments, and estimates.

Best Practices

- Use clear and consistent classification to enhance comparability.

- Provide reconciliations where necessary (e.g., equity changes).

- Ensure notes are comprehensive but concise.

Example: Simplified Statement of Financial Position (IFRS)

| Assets | Amount (USD) | Liabilities and Equity | Amount (USD) |

|---|---|---|---|

| Current Assets | 150,000 | Current Liabilities | 80,000 |

| Non-current Assets | 350,000 | Non-current Liabilities | 120,000 |

| Equity | 300,000 | ||

| Total Assets | 500,000 | Total Liabilities & Equity | 500,000 |

Example: Presentation of Other Comprehensive Income

| Description | Amount (USD) |

|---|---|

| Profit for the Year | 50,000 |

| Other Comprehensive Income: | |

| - Foreign Currency Translation | 5,000 |

| - Revaluation Surplus | 10,000 |

| Total Comprehensive Income | 65,000 |

Summary

Understanding the IFRS financial statement structure is crucial for compliance and effective communication of financial results. The flexibility in presentation allows entities to tailor disclosures to their circumstances while maintaining transparency and comparability.

For accountants and auditors, mastering these requirements ensures accurate reporting and facilitates smoother audits and reviews.

2.2 GAAP Financial Statement Structure and Requirements

Under Generally Accepted Accounting Principles (GAAP), financial statements follow a structured format designed to provide clear, consistent, and comparable financial information to users such as investors, creditors, and regulators. Understanding the structure and requirements of GAAP financial statements is essential for accountants, auditors, and compliance officers to ensure accuracy and compliance.

Key GAAP Financial Statements

GAAP requires the preparation of the following primary financial statements:

- Balance Sheet (Statement of Financial Position)

- Income Statement (Statement of Earnings or Profit & Loss Statement)

- Statement of Cash Flows

- Statement of Shareholders’ Equity

- Notes to the Financial Statements

Mind Map: GAAP Financial Statement Components

Balance Sheet (Statement of Financial Position)

The balance sheet presents an entity’s financial position at a specific point in time, showing what it owns (assets), what it owes (liabilities), and the residual interest of shareholders (equity).

GAAP Requirements:

- Assets and liabilities are classified as current or non-current.

- Assets are generally listed in order of liquidity.

- Liabilities are listed in order of maturity.

- Equity section includes common stock, additional paid-in capital, retained earnings, and treasury stock.

Example:

| Balance Sheet (As of Dec 31, 2023) | Amount (USD) |

|---|---|

| Assets | |

| Current Assets | 150,000 |

| Property, Plant & Equipment (net) | 350,000 |

| Total Assets | 500,000 |

| Liabilities | |

| Current Liabilities | 100,000 |

| Long-term Debt | 200,000 |

| Total Liabilities | 300,000 |

| Shareholders’ Equity | |

| Common Stock | 50,000 |

| Retained Earnings | 150,000 |

| Total Equity | 200,000 |

| Total Liabilities & Equity | 500,000 |

Income Statement (Statement of Earnings)

The income statement summarizes revenues, expenses, gains, and losses over a reporting period, culminating in net income or loss.

GAAP Requirements:

- Must follow the accrual basis of accounting.

- Expenses are matched with revenues.

- Presentation can be single-step or multi-step.

Example (Multi-step format):

| Income Statement (Year Ended Dec 31, 2023) | Amount (USD) |

|---|---|

| Revenues | 600,000 |

| Cost of Goods Sold | 350,000 |

| Gross Profit | 250,000 |

| Operating Expenses | 100,000 |

| Operating Income | 150,000 |

| Other Income and Expenses | (10,000) |

| Net Income Before Taxes | 140,000 |

| Income Tax Expense | 40,000 |

| Net Income | 100,000 |

Statement of Cash Flows

This statement reports cash inflows and outflows classified into operating, investing, and financing activities.

GAAP Requirements:

- Must use either direct or indirect method for operating activities (indirect is more common).

- Must separately report cash flows from investing and financing activities.

Example (Indirect Method):

| Cash Flows from Operating Activities | Amount (USD) |

|---|---|

| Net Income | 100,000 |

| Adjustments for Non-cash Items | 20,000 |

| Changes in Working Capital | (15,000) |

| Net Cash Provided by Operating Activities | 105,000 |

| Cash Flows from Investing Activities | Amount (USD) |

|---|---|

| Purchase of Equipment | (50,000) |

| Sale of Investments | 10,000 |

| Net Cash Used in Investing Activities | (40,000) |

| Cash Flows from Financing Activities | Amount (USD) |

|---|---|

| Proceeds from Issuance of Debt | 30,000 |

| Dividends Paid | (20,000) |

| Net Cash Provided by Financing Activities | 10,000 |

| Net Increase in Cash | 75,000 |

Statement of Shareholders’ Equity

This statement reconciles the beginning and ending balances of equity accounts.

GAAP Requirements:

- Must disclose changes in common stock, retained earnings, treasury stock, and other equity components.

Example:

| Statement of Shareholders’ Equity (Year Ended Dec 31, 2023) | Amount (USD) |

|---|---|

| Beginning Retained Earnings | 120,000 |

| Add: Net Income | 100,000 |

| Less: Dividends | (20,000) |

| Ending Retained Earnings | 200,000 |

Notes to the Financial Statements

Notes provide essential disclosures about accounting policies, contingencies, commitments, and other relevant information.

GAAP Requirements:

- Must disclose significant accounting policies.

- Must provide details on contingencies, legal matters, and subsequent events.

Example:

Note 1: Summary of Significant Accounting Policies

The company prepares its financial statements in accordance with GAAP. Revenue is recognized when earned and realizable. Property, plant, and equipment are recorded at cost and depreciated over their useful lives using the straight-line method.

Best Practices for GAAP Financial Statement Preparation

- Consistency: Maintain consistent classification and presentation across periods.

- Clarity: Use clear headings and subheadings to improve readability.

- Disclosure: Provide comprehensive notes to explain judgments and estimates.

- Reconciliation: Ensure that totals and subtotals reconcile across statements.

- Review: Conduct thorough reviews and audits to ensure compliance.

Integrated Example: Preparing a GAAP Balance Sheet with Notes

Suppose a government finance department is preparing its year-end financial statements. They classify assets and liabilities carefully, ensuring current assets like cash and receivables are separated from long-term assets such as infrastructure.

Balance Sheet Snapshot:

| Assets | Amount (USD) |

|---|---|

| Cash and Cash Equivalents | 200,000 |

| Accounts Receivable | 150,000 |

| Infrastructure Assets | 1,000,000 |

| Total Assets | 1,350,000 |

| Liabilities | Amount (USD) |

|---|---|

| Accounts Payable | 100,000 |

| Bonds Payable | 500,000 |

| Total Liabilities | 600,000 |

| Equity | Amount (USD) |

|---|---|

| Fund Balance | 750,000 |

| Total Liabilities & Equity | 1,350,000 |

Note:

The infrastructure assets are valued at historical cost less accumulated depreciation. Bonds payable represent long-term debt issued to finance capital projects.

This detailed understanding of GAAP financial statement structure and requirements, combined with practical examples and mind maps, equips finance professionals to prepare compliant, transparent, and useful financial reports.

2.3 Best Practices for Preparing Comparative Financial Statements

Preparing comparative financial statements under IFRS and GAAP requires meticulous attention to detail, consistency, and clarity to ensure stakeholders can easily understand the financial position and performance across periods. Below are best practices integrated with practical examples and mind maps to guide accountants, auditors, and compliance officers.

Best Practices Overview

-

Consistent Presentation Format

- Use the same format and classification for each period presented.

- Align line items and headings to facilitate easy comparison.

-

Reconciliation and Restatement

- Clearly disclose any restatements or reclassifications made to prior period figures.

- Provide reconciliations between IFRS and GAAP figures if both are presented.

-

Clear Disclosure of Accounting Policies

- Include notes explaining any changes in accounting policies affecting comparability.

-

Use of Comparative Periods

- Present at least two periods side-by-side (current and prior) as required by IFRS and GAAP.

-

Highlight Material Changes and Variances

- Use variance analysis to explain significant differences between periods.

-

Ensure Compliance with Regulatory Requirements

- Follow specific disclosure and presentation requirements under IFRS IAS 1 and GAAP ASC 205.

-

Leverage Technology for Accuracy

- Use accounting software to automate comparative reporting and reduce errors.

Mind Map: Preparing Comparative Financial Statements

Practical Example: Comparative Statement of Financial Position

Scenario: A company prepares its balance sheet under both IFRS and GAAP for the years ended 2023 and 2022.

| Account | 2023 IFRS (USD) | 2022 IFRS (USD) | 2023 GAAP (USD) | 2022 GAAP (USD) |

|---|---|---|---|---|

| Cash and Cash Equivalents | 150,000 | 120,000 | 150,000 | 120,000 |

| Property, Plant & Equipment (PPE) | 500,000 | 480,000 | 490,000 | 470,000 |

| Lease Liabilities | 80,000 | 85,000 | 75,000 | 80,000 |

| Equity | 570,000 | 515,000 | 565,000 | 510,000 |

Best Practice Application:

- The company uses the same line items and order for both IFRS and GAAP statements.

- Notes disclose that PPE valuation differs due to IFRS revaluation model vs GAAP cost model.

- Lease liabilities reflect differences in lease classification standards.

- Prior year figures are restated to reflect new lease accounting under IFRS 16 and ASC 842.

Mind Map: Variance Analysis in Comparative Statements

Example: Explaining Variance in Lease Liabilities

Observation: Lease liabilities decreased from $85,000 in 2022 to $80,000 in 2023 under IFRS.

Explanation:

- The decrease is due to lease term modifications and early lease payments.

- Disclosed in notes with a reconciliation of opening and closing lease liability balances.

Additional Tips

- Always cross-check comparative figures for consistency.

- Use footnotes to explain any differences in measurement or presentation.

- Train staff regularly on updates to IFRS and GAAP standards affecting comparative reporting.

By following these best practices, professionals can ensure that comparative financial statements are accurate, transparent, and useful for decision-making.

2.4 Example: Preparing a Statement of Financial Position Under Both Standards

Preparing a Statement of Financial Position (also known as the Balance Sheet) under IFRS and GAAP involves understanding the structural and presentation differences between the two frameworks. This section will walk you through a detailed example, supported by mind maps, to clarify these differences and best practices.

Key Structural Differences Mind Map

Example Company Data

| Item | Amount (USD) |

|---|---|

| Cash and Cash Equivalents | 50,000 |

| Accounts Receivable | 40,000 |

| Inventory | 30,000 |

| Property, Plant & Equipment | 120,000 |

| Intangible Assets | 25,000 |

| Accounts Payable | 35,000 |

| Short-term Debt | 20,000 |

| Long-term Debt | 70,000 |

| Share Capital | 50,000 |

| Retained Earnings | 90,000 |

Step 1: Classify Assets and Liabilities

- IFRS Approach: Separate current and non-current assets/liabilities.

- GAAP Approach: Similar classification, but GAAP is more prescriptive on order.

Classification Mind Map

Step 2: Prepare IFRS Statement of Financial Position

| IFRS Statement of Financial Position | Amount (USD) |

|---|---|

| Assets | |

| Current Assets | 120,000 |

| - Cash and Cash Equivalents | 50,000 |

| - Accounts Receivable | 40,000 |

| - Inventory | 30,000 |

| Non-current Assets | 145,000 |

| - Property, Plant & Equipment | 120,000 |

| - Intangible Assets | 25,000 |

| Total Assets | 265,000 |

| Equity and Liabilities | |

| Equity | 140,000 |

| - Share Capital | 50,000 |

| - Retained Earnings | 90,000 |

| Non-current Liabilities | 70,000 |

| - Long-term Debt | 70,000 |

| Current Liabilities | 55,000 |

| - Accounts Payable | 35,000 |

| - Short-term Debt | 20,000 |

| Total Equity and Liabilities | 265,000 |

Step 3: Prepare GAAP Statement of Financial Position

| GAAP Statement of Financial Position | Amount (USD) |

|---|---|

| Assets | |

| Current Assets | 120,000 |

| - Cash and Cash Equivalents | 50,000 |

| - Accounts Receivable | 40,000 |

| - Inventory | 30,000 |

| Property, Plant & Equipment (Net) | 120,000 |

| Intangible Assets | 25,000 |

| Total Assets | 265,000 |

| Liabilities and Stockholders’ Equity | |

| Current Liabilities | 55,000 |

| - Accounts Payable | 35,000 |

| - Short-term Debt | 20,000 |

| Long-term Liabilities | 70,000 |

| - Long-term Debt | 70,000 |

| Stockholders’ Equity | 140,000 |

| - Common Stock | 50,000 |

| - Retained Earnings | 90,000 |

| Total Liabilities and Equity | 265,000 |

Step 4: Best Practices for Preparation

- Consistency: Use consistent classification year over year.

- Disclosure: Clearly disclose accounting policies related to asset classification.

- Presentation: Follow the prescribed order but tailor presentation to user needs.

- Reconciliation: When transitioning between IFRS and GAAP, provide reconciliations.

Visual Comparison Mind Map

Summary

This example demonstrates that while IFRS and GAAP share many similarities in preparing the Statement of Financial Position, subtle differences in classification and presentation exist. Accountants and auditors should apply best practices such as consistent classification, clear disclosures, and reconciliation to ensure compliance and transparency.

By using the example data and mind maps, professionals can better visualize and implement the requirements of both standards effectively.

3. Revenue Recognition Principles

3.1 IFRS 15 Revenue from Contracts with Customers Overview

IFRS 15, titled “Revenue from Contracts with Customers,” establishes the principles that an entity shall apply to report useful information to users of financial statements about the nature, amount, timing, and uncertainty of revenue and cash flows arising from a contract with a customer.

Key Objectives of IFRS 15

- Provide a comprehensive framework for revenue recognition.

- Align revenue recognition with the transfer of control of goods or services.

- Improve comparability across industries and capital markets.

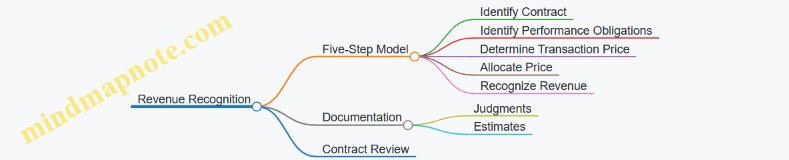

The Five-Step Model of IFRS 15

IFRS 15 introduces a five-step model to recognize revenue:

-

Step 1: Identify the contract(s) with a customer

- Contract must create enforceable rights and obligations.

- Example: A signed sales agreement for delivery of goods.

-

Step 2: Identify the performance obligations in the contract

- Distinct goods or services promised.

- Example: A software license and ongoing support counted as separate obligations.

-

Step 3: Determine the transaction price

- Amount of consideration expected.

- Consider variable consideration, discounts, rebates.

-

Step 4: Allocate the transaction price to the performance obligations

- Based on standalone selling prices.

-

Step 5: Recognize revenue when (or as) the entity satisfies a performance obligation

- Revenue recognized over time or at a point in time.

Mind Map: IFRS 15 Five-Step Model

Important Concepts in IFRS 15

- Contract: An agreement between two or more parties that creates enforceable rights and obligations.

- Performance Obligation: A promise to transfer a distinct good or service.

- Transaction Price: The amount of consideration an entity expects to be entitled to.

- Control: The ability to direct the use of and obtain substantially all of the remaining benefits from the asset.

Example: Software Subscription Service

A company sells a 12-month software subscription for $1,200, which includes:

- Access to the software (performance obligation 1)

- Customer support (performance obligation 2)

Step 1: Contract exists with customer.

Step 2: Two performance obligations identified: software access and support.

Step 3: Transaction price is $1,200.

Step 4: Allocate price based on standalone selling prices:

- Software access: $1,000

- Support: $200

Step 5: Recognize revenue over time:

- Software access: $83.33 per month

- Support: $16.67 per month

This ensures revenue is recognized in line with service delivery.

Best Practices for Applying IFRS 15

- Thoroughly review contracts to identify all performance obligations.

- Use reliable methods to estimate standalone selling prices.

- Document judgments made in determining transaction price and timing.

- Implement systems to track performance obligations and revenue recognition over time.

Mind Map: Best Practices for IFRS 15 Implementation

By understanding and applying the five-step model of IFRS 15, accountants, auditors, and compliance officers can ensure accurate, transparent, and consistent revenue recognition aligned with global standards.

3.2 GAAP ASC 606 Revenue Recognition Guidelines

The GAAP ASC 606 standard, titled “Revenue from Contracts with Customers,” provides a comprehensive framework for recognizing revenue in a consistent and transparent manner. It was introduced to align revenue recognition practices across industries and improve comparability of financial statements.

Core Principle

The core principle of ASC 606 is that an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services.

Five-Step Model for Revenue Recognition under ASC 606

Detailed Explanation of Each Step

-

Identify the contract(s) with a customer: A contract must create enforceable rights and obligations. Contracts can be written, oral, or implied by customary business practices.

-

Identify the performance obligations: These are promises to transfer distinct goods or services. If goods or services are highly interrelated or significantly modified, they may be combined into a single performance obligation.

-

Determine the transaction price: This is the amount the entity expects to receive. It includes fixed amounts, variable amounts (e.g., discounts, rebates, performance bonuses), and adjustments for the time value of money if the contract includes a significant financing component.

-

Allocate the transaction price: When there are multiple performance obligations, the total transaction price is allocated to each based on their relative standalone selling prices.

-

Recognize revenue when (or as) the entity satisfies a performance obligation: Revenue is recognized either over time (e.g., services rendered continuously) or at a point in time (e.g., delivery of a product) when control transfers to the customer.

Best Practices for Applying ASC 606

- Document contracts thoroughly to ensure clarity on performance obligations and pricing.

- Use consistent methods to estimate variable consideration and standalone selling prices.

- Evaluate contracts regularly for modifications that may affect revenue recognition.

- Implement robust internal controls to track performance obligations and revenue recognition timing.

Example: Software Subscription Service

A company sells a 12-month software subscription for $1,200, billed upfront. The subscription includes access to the software and ongoing customer support.

- Step 1: Contract exists with the customer for 12 months.

- Step 2: Two performance obligations identified: (1) access to software, (2) customer support.

- Step 3: Transaction price is $1,200 fixed.

- Step 4: Allocate price based on standalone selling prices: software access $1,000, support $200.

- Step 5: Recognize revenue over time as services are provided.

Revenue recognized monthly:

- Software access: $1,000 / 12 = $83.33 per month

- Customer support: $200 / 12 = $16.67 per month

Example: Construction Contract

A construction company enters into a contract to build a facility for $5 million. The contract specifies payments based on milestones.

- Step 1: Contract is enforceable.

- Step 2: Single performance obligation: completion of the facility.

- Step 3: Transaction price is $5 million fixed.

- Step 4: No allocation needed (single obligation).

- Step 5: Revenue recognized over time using input method (cost-to-cost) as work progresses.

If costs incurred to date are $2 million and total estimated costs are $4 million, revenue recognized to date = ($2M / $4M) * $5M = $2.5 million.

This structured approach ensures revenue is recognized in a manner that reflects the actual transfer of goods or services, providing transparency and consistency for stakeholders.

3.3 Step-by-Step Best Practices for Revenue Recognition

Revenue recognition is a critical area in both IFRS (IFRS 15) and GAAP (ASC 606) frameworks. Proper adherence ensures accurate financial reporting and compliance. Below is a detailed step-by-step guide with best practices, accompanied by mind maps and practical examples to facilitate understanding.

Step 1: Identify the Contract with the Customer

- Best Practice: Ensure the contract is legally enforceable and clearly defines the rights and obligations of both parties.

- Key Considerations: Written, oral, or implied contracts; collectability of consideration.

Example: A software company signs a written agreement with a client for a 12-month subscription. The contract specifies payment terms and service deliverables.

Step 2: Identify the Performance Obligations in the Contract

- Best Practice: Break down the contract into distinct goods or services promised to the customer.

- Key Considerations: Distinct goods/services, bundled offerings.

Example: The software subscription includes access to the platform and periodic updates. These are considered separate performance obligations if they are distinct.

Step 3: Determine the Transaction Price

- Best Practice: Calculate the amount the entity expects to receive, considering variable considerations, discounts, rebates, and financing components.

- Key Considerations: Fixed vs variable consideration, time value of money.

Example: The subscription fee is $1,200 annually, but the customer may receive a 10% rebate if usage exceeds a threshold.

Step 4: Allocate the Transaction Price to Performance Obligations

- Best Practice: Allocate based on standalone selling prices of each distinct good or service.

- Key Considerations: Estimation methods if standalone prices are not directly observable.

Example: Access to the platform is valued at $1,000, updates at $200; allocate the $1,200 accordingly.

Step 5: Recognize Revenue When (or As) Performance Obligations Are Satisfied

- Best Practice: Recognize revenue when control of the good or service transfers to the customer, either over time or at a point in time.

- Key Considerations: Indicators of transfer of control, input vs output methods for measuring progress.

Example: Revenue for the software subscription is recognized ratably over the 12-month period, reflecting continuous access.

Practical Example: Recognizing Revenue for a Software Subscription Service

Scenario:

- Contract: 12-month subscription for $1,200

- Performance Obligations: Access to software platform + Updates

- Standalone Prices: Platform access $1,000, Updates $200

- Payment: Upfront payment

Application:

- Contract identified and enforceable.

- Two performance obligations identified.

- Transaction price is $1,200 fixed.

- Allocate $1,000 to platform access and $200 to updates.

- Recognize revenue over time, $100/month for platform access and $16.67/month for updates.

Summary Mind Map

By following these structured steps and applying the best practices, accountants, auditors, and compliance officers can ensure accurate and compliant revenue recognition under both IFRS and GAAP standards.

3.4 Example: Recognizing Revenue for a Software Subscription Service

Revenue recognition for software subscription services is a common and practical scenario where both IFRS 15 and GAAP ASC 606 standards apply the five-step model to recognize revenue. This example will break down the process with clear explanations, mind maps, and illustrative examples.

Step 1: Identify the Contract with the Customer

- A subscription agreement is signed between the software provider and the customer.

- The contract specifies the subscription period, pricing, and services included.

Step 2: Identify the Performance Obligations

- The software provider promises to deliver access to the software over the subscription period.

- Additional services like customer support or updates may be separate performance obligations if distinct.

Step 3: Determine the Transaction Price

- The total subscription fee agreed upon (e.g., $1,200 for a 12-month subscription).

Step 4: Allocate the Transaction Price to Performance Obligations

- If the contract includes multiple obligations (software access + support), allocate price based on standalone selling prices.

- In a simple subscription, the entire fee is allocated to software access.

Step 5: Recognize Revenue When (or As) the Entity Satisfies a Performance Obligation

- Revenue is recognized over time, typically on a straight-line basis over the subscription period.

Mind Map: Revenue Recognition Process for Software Subscription

Practical Example

Scenario:

- Company ABC sells a 12-month software subscription for $1,200.

- The subscription includes software access and email support.

- Standalone selling price: Software access $1,000, Email support $200.

Step-by-step recognition:

- Identify contract: Signed 12-month subscription agreement.

- Performance obligations: Software access and email support are distinct.

- Transaction price: $1,200 total.

- Allocate price:

- Software access: ($1,000 / $1,200) * $1,200 = $1,000

- Email support: ($200 / $1,200) * $1,200 = $200

- Recognize revenue:

- Software access revenue recognized evenly over 12 months: $1,000 / 12 = $83.33 per month.

- Email support revenue recognized evenly over 12 months: $200 / 12 = $16.67 per month.

Journal entries example for month 1:

| Account | Debit | Credit |

|---|---|---|

| Accounts Receivable | 100 | |

| Revenue - Software Access | 83.33 | |

| Revenue - Email Support | 16.67 |

Mind Map: Allocation and Recognition Example

Additional Considerations and Best Practices

- Contract Modifications: If the subscription is extended or upgraded, reassess the contract and performance obligations.

- Variable Consideration: Discounts or refunds should be estimated and included in the transaction price.

- Disclosure: Clearly disclose revenue recognition policies and significant judgments in financial statements.

- Automation: Use accounting software to automate revenue recognition schedules and reduce errors.

This example demonstrates how to apply IFRS 15 and GAAP ASC 606 principles in a straightforward subscription service context, ensuring compliance and transparency in revenue reporting.

4. Lease Accounting

4.1 IFRS 16 Lease Accounting Model

Overview

IFRS 16, effective from January 1, 2019, introduced a single lessee accounting model, eliminating the previous distinction between operating and finance leases for lessees. Under IFRS 16, lessees recognize assets and liabilities for almost all leases, providing greater transparency about lease obligations.

Key Principles of IFRS 16

- Right-of-Use Asset (ROU Asset): Represents the lessee’s right to use the leased asset during the lease term.

- Lease Liability: Represents the lessee’s obligation to make lease payments.

- Lease Term: Includes non-cancellable periods, renewal options if reasonably certain to be exercised, and termination options if reasonably certain not to be exercised.

- Measurement: Initial measurement of lease liability is the present value of lease payments; ROU asset is initially measured at cost.

Mind Map: IFRS 16 Lease Accounting Model

Recognition and Measurement

Initial Recognition

- Lease Liability: Calculate the present value of lease payments over the lease term discounted using the interest rate implicit in the lease or the lessee’s incremental borrowing rate.

- Right-of-Use Asset: Initially measured at the amount of the lease liability, adjusted for lease prepayments, initial direct costs, and restoration costs.

Subsequent Measurement

- Lease Liability: Increase by interest expense and decrease by lease payments made.

- ROU Asset: Depreciated over the lease term or useful life if ownership transfers.

Example: Lessee Accounting for Office Lease

Scenario: A company leases office space for 5 years. Annual lease payments are $50,000, payable at the end of each year. The incremental borrowing rate is 5%.

Step 1: Calculate Lease Liability (Present Value of Lease Payments)

| Year | Payment ($) | PV Factor @5% | Present Value ($) |

|---|---|---|---|

| 1 | 50,000 | 0.9524 | 47,620 |

| 2 | 50,000 | 0.9070 | 45,350 |

| 3 | 50,000 | 0.8638 | 43,190 |

| 4 | 50,000 | 0.8227 | 41,135 |

| 5 | 50,000 | 0.7835 | 39,175 |

| Total | 216,470 |

Step 2: Initial Recognition

- Lease Liability = $216,470

- Right-of-Use Asset = $216,470 (assuming no initial direct costs or prepayments)

Step 3: Subsequent Measurement

- Depreciate ROU asset on a straight-line basis: $216,470 / 5 = $43,294 per year

- Interest expense for Year 1: $216,470 * 5% = $10,824

- Lease payment reduces liability: $50,000 - $10,824 = $39,176

- Lease liability at end of Year 1: $216,470 - $39,176 = $177,294

Mind Map: Lease Liability Amortization Example

Practical Best Practices

- Identify Lease Components: Carefully review contracts to identify lease and non-lease components.

- Determine Lease Term: Assess options to extend or terminate leases based on reasonable certainty.

- Select Appropriate Discount Rate: Use the interest rate implicit in the lease if known; otherwise, use incremental borrowing rate.

- Document Judgments and Assumptions: Maintain clear documentation for estimates such as lease term and discount rate.

- Use Lease Accounting Software: Automate calculations and disclosures to reduce errors.

Common Challenges and Solutions

- Variable Lease Payments: Only payments linked to an index or rate are included in lease liability; others are expensed as incurred.

- Lease Modifications: Reassess lease liability and ROU asset when lease terms change.

- Short-term and Low-value Leases: Consider exemptions to simplify accounting.

Summary

IFRS 16 requires lessees to bring most leases onto the balance sheet, enhancing transparency and comparability. Understanding the recognition, measurement, and presentation requirements, supported by practical examples and clear documentation, is essential for compliance and accurate financial reporting.

4.2 GAAP ASC 842 Lease Accounting Model

Overview

ASC 842, issued by the Financial Accounting Standards Board (FASB), represents the updated lease accounting standard under US GAAP. It requires lessees to recognize most leases on the balance sheet, improving transparency and comparability.

Key Components of ASC 842

- Lease Definition: A contract that conveys the right to control the use of identified property, plant, or equipment (an identified asset) for a period of time in exchange for consideration.

- Lease Classification: Leases are classified as either finance leases or operating leases.

- Recognition: Lessees recognize a right-of-use (ROU) asset and a lease liability for virtually all leases.

- Measurement: Lease liability is measured at the present value of lease payments; ROU asset is based on the lease liability adjusted for prepaid or accrued lease payments, initial direct costs, and lease incentives.

Mind Map: ASC 842 Lease Accounting Model

Detailed Explanation

Lease Classification Criteria

ASC 842 classifies leases into two categories:

-

Finance Lease: Similar to capital leases under ASC 840, these leases transfer substantially all risks and rewards of ownership to the lessee.

-

Operating Lease: Leases that do not meet finance lease criteria.

Finance Lease Criteria (Any one of the following):

- Ownership transfers to lessee by end of lease term.

- Lease contains a purchase option reasonably certain to be exercised.

- Lease term is for the major part (generally 75% or more) of the asset’s economic life.

- Present value of lease payments equals or exceeds substantially all (generally 90% or more) of the fair value of the asset.

- The asset is specialized and has no alternative use to the lessor.

Initial Recognition and Measurement

At lease commencement, lessees recognize:

-

Lease Liability: Measured as the present value of lease payments not yet paid, discounted using the rate implicit in the lease or the lessee’s incremental borrowing rate.

-

Right-of-Use Asset: Initially measured at the amount of the lease liability, adjusted for lease payments made at or before commencement, initial direct costs, and lease incentives received.

Subsequent Measurement

-

Finance Lease: Interest on lease liability is recognized using the effective interest method; ROU asset is amortized generally on a straight-line basis.

-

Operating Lease: Single lease expense recognized on a straight-line basis over the lease term, combining interest on lease liability and amortization of ROU asset.

Disclosure Requirements

Lessees must disclose qualitative and quantitative information about leases, including:

- Lease terms and conditions

- Maturity analysis of lease liabilities

- Expense related to leases

Example: Accounting for an Operating Lease under ASC 842

Scenario:

Company ABC enters into a 5-year lease for office equipment. Annual lease payments are $20,000, payable at the end of each year. The incremental borrowing rate is 6%. The lease does not transfer ownership, nor does it contain a purchase option.

Step 1: Lease Classification

- Lease term = 5 years

- Asset economic life = 10 years

- Lease term is 50% of asset life (less than 75%)

- No ownership transfer or purchase option

- Present value of payments (PV) calculation:

\[ PV = 20,000 \times \frac{1 - (1 + 0.06)^{-5}}{0.06} = 20,000 \times 4.21236 = 84,247 \]

Assuming fair value of asset is $100,000, PV is 84.2% of fair value (less than 90%).

Conclusion: Operating lease.

Step 2: Initial Recognition

- Lease Liability = $84,247

- ROU Asset = $84,247 (assuming no prepaid payments or initial direct costs)

Step 3: Subsequent Measurement

- Lease expense each year = $20,000 (straight-line)

Journal Entries at commencement:

| Account | Debit | Credit |

|---|---|---|

| Right-of-Use Asset | 84,247 | |

| Lease Liability | 84,247 |

Year 1 Lease Payment:

| Account | Debit | Credit |

|---|---|---|

| Lease Liability | 14,093 | |

| Interest Expense | 5,054 | |

| Cash | 20,000 |

Note: Interest Expense = 6% × $84,247 = $5,054; Lease Liability reduction = $20,000 - $5,054 = $14,946 (rounded here as $14,093 for illustration; actual amortization schedule needed).

Lease Expense Recognition:

- Recognized on a straight-line basis: $20,000 per year.

Mind Map: Operating Lease Accounting Example

Best Practices for Compliance with ASC 842

- Thorough Contract Review: Identify all lease components and embedded leases.

- Accurate Discount Rate Determination: Use implicit rate if known; otherwise, incremental borrowing rate.

- Lease Term Assessment: Consider renewal and termination options reasonably certain to be exercised.

- Consistent Classification: Apply criteria uniformly across leases.

- Robust Systems: Use lease accounting software to track and calculate lease liabilities and ROU assets.

- Comprehensive Disclosures: Ensure all required qualitative and quantitative information is included.

Summary

ASC 842 significantly changes lease accounting by requiring lessees to bring most leases onto the balance sheet, improving financial statement transparency. Understanding classification criteria, measurement principles, and disclosure requirements is essential for compliance. Practical examples and structured mind maps help clarify the application of these complex rules.

4.3 Best Practices for Lease Classification and Measurement

Lease accounting under IFRS 16 and GAAP ASC 842 requires careful classification and measurement to ensure accurate financial reporting. Below are best practices to help accountants, auditors, and compliance officers navigate this complex area effectively.

Best Practices Overview

- Understand the Lease Definition Clearly: Confirm whether a contract contains a lease by assessing the right to control the use of an identified asset.

- Accurate Lease Classification: Distinguish between finance (IFRS) / capital (GAAP) leases and operating leases based on criteria such as transfer of ownership, lease term, and present value of lease payments.

- Comprehensive Data Collection: Gather all relevant lease terms, including lease term, renewal options, variable payments, and discount rates.

- Use Appropriate Discount Rates: Apply the rate implicit in the lease or the lessee’s incremental borrowing rate consistently.

- Regularly Review Lease Modifications: Assess modifications for reclassification or remeasurement.

- Maintain Detailed Documentation: Keep clear records of judgments, assumptions, and calculations.

Mind Map: Lease Classification Process

Mind Map: Lease Measurement Steps

Practical Example 1: Lease Classification

Scenario: A company leases a machine for 6 years. The machine’s economic life is 8 years. The lease agreement does not transfer ownership, and there is no purchase option. The present value of lease payments is 85% of the machine’s fair value.

Analysis:

- Lease term (6 years) is 75% of economic life (8 years) → meets threshold.

- Present value of payments (85%) exceeds 90% threshold? No.

- Ownership transfer? No.

- Purchase option? No.

Conclusion: Under IFRS 16 and GAAP ASC 842, this lease would likely be classified as a finance/capital lease because the lease term criterion is met, despite the present value being slightly below 90%. Judgment is required.

Practical Example 2: Lease Measurement

Scenario: Company ABC enters into a 5-year lease for office space with annual fixed payments of $50,000 payable at the end of each year. The incremental borrowing rate is 6%.

Step 1: Calculate Lease Liability

Using present value of an annuity formula:

PV = Pmt × [(1 - (1 + r)^-n) / r]

PV = $50,000 × [(1 - (1 + 0.06)^-5) / 0.06] ≈ $50,000 × 4.21236 = $210,618

Step 2: Recognize Right-of-Use Asset

Initial ROU asset = Lease liability = $210,618 (assuming no initial direct costs or incentives)

Step 3: Subsequent Measurement

- Lease liability amortized using effective interest method.

- ROU asset amortized on a straight-line basis over 5 years.

Mind Map: Common Pitfalls and Controls

Summary

Adhering to these best practices ensures compliance with IFRS and GAAP lease accounting standards, reduces risk of misstatement, and enhances transparency. Using clear classification criteria, precise measurement techniques, and thorough documentation supported by practical examples helps finance professionals maintain accuracy and confidence in lease reporting.

4.4 Example: Accounting for Operating vs Finance Leases

Understanding the distinction between operating leases and finance leases is critical for accurate financial reporting under both IFRS 16 and GAAP ASC 842. This section provides a detailed example, supported by mind maps, to clarify the accounting treatment for each lease type.

Mind Map: Lease Classification Criteria

Example Scenario

Company ABC enters into a 5-year lease agreement for machinery with the following terms:

- Fair value of machinery: $100,000

- Lease term: 5 years

- Economic life of machinery: 7 years

- Annual lease payment: $22,000, payable at year-end

- Interest rate implicit in lease: 6%

- No transfer of ownership or bargain purchase option

Step 1: Determine Lease Classification

- Lease term (5 years) is approximately 71% of economic life (7 years), which is considered a major part.

- Present value of lease payments calculation:

\[ PV = 22,000 \times \left(1 - (1 + 0.06)^{-5}\right) / 0.06 \approx 22,000 \times 4.21236 = 92,691 \]

- Present value ($92,691) is about 93% of fair value ($100,000), close to the asset’s fair value.

Conclusion: Under IFRS and GAAP, this lease qualifies as a Finance Lease (or Capital Lease).

Accounting Treatment Under IFRS 16 / GAAP ASC 842

| Aspect | Finance Lease (Capital Lease) | Operating Lease |

|---|---|---|

| Recognition | Recognize Right-of-Use (ROU) asset and lease liability | Recognize ROU asset and lease liability |

| Initial Measurement | ROU asset and liability measured at present value of lease payments | Same as finance lease |

| Subsequent Measurement | ROU asset depreciated; lease liability amortized with interest expense | Lease expense recognized on straight-line basis |

Mind Map: Accounting Entries for Finance vs Operating Lease

Detailed Journal Entries for Year 1 (Finance Lease)

| Date | Account | Debit ($) | Credit ($) |

|---|---|---|---|

| Lease start | Right-of-Use Asset | 92,691 | |

| Lease start | Lease Liability | 92,691 | |

| Year-end | Interest Expense | 5,561 | |

| Year-end | Lease Liability | 16,439 | |

| Year-end | Cash | 22,000 | |

| Year-end | Depreciation Expense | 18,538 | |

| Year-end | Accumulated Depreciation | 18,538 |

Note: Lease liability amortization = Lease payment - Interest expense = 22,000 - 5,561 = 16,439

Detailed Journal Entries for Year 1 (Operating Lease)

| Date | Account | Debit ($) | Credit ($) |

|---|---|---|---|

| Lease start | Right-of-Use Asset | 92,691 | |

| Lease start | Lease Liability | 92,691 | |

| Year-end | Lease Expense | 22,000 | |

| Year-end | Cash | 22,000 |

Note: Lease expense is recognized on a straight-line basis; no separate interest or depreciation expense is recorded.

Summary Table: Key Differences in Accounting

| Feature | Finance Lease | Operating Lease |

|---|---|---|

| Asset Recognition | ROU asset capitalized | ROU asset capitalized |

| Liability Recognition | Lease liability at PV of payments | Lease liability at PV of payments |

| Expense Recognition | Interest + Depreciation expenses | Single lease expense (straight-line) |

| Balance Sheet Impact | Higher initial liabilities and assets | Similar initial recognition but different expense pattern |

Practical Tips for Compliance Officers and Auditors

- Verify lease classification by carefully assessing lease terms against criteria.

- Confirm accuracy of present value calculations using correct discount rates.

- Ensure proper segregation of interest and depreciation expenses for finance leases.

- Review lease disclosures to confirm transparency about lease commitments and accounting policies.

This example demonstrates how understanding the nuances of lease classification directly impacts financial reporting and compliance under IFRS and GAAP frameworks.

5. Financial Instruments and Fair Value Measurement

5.1 IFRS 9 Classification and Measurement of Financial Instruments

IFRS 9 Financial Instruments is a comprehensive standard that addresses the classification, measurement, impairment, and hedge accounting of financial instruments. This section focuses on the classification and measurement aspects, which are critical for accountants, auditors, and compliance officers in ensuring accurate financial reporting.

Overview of IFRS 9 Classification

IFRS 9 classifies financial assets into three main categories based on the entity’s business model for managing the financial assets and the contractual cash flow characteristics of the financial asset:

- Amortized Cost

- Fair Value Through Other Comprehensive Income (FVOCI)

- Fair Value Through Profit or Loss (FVTPL)

Financial liabilities are generally measured at amortized cost, with some exceptions measured at fair value.

Mind Map: IFRS 9 Classification of Financial Assets

Step 1: Assess the Business Model

The business model assessment determines how the financial asset is managed to generate cash flows:

- Hold to Collect: The objective is to hold financial assets to collect contractual cash flows.

- Hold to Collect and Sell: The objective is both to collect contractual cash flows and sell financial assets.

- Other: Financial assets held for trading or other purposes.

Step 2: Assess the Contractual Cash Flow Characteristics (SPPI Test)

The cash flows must consist solely of payments of principal and interest on the principal amount outstanding. If the cash flows include other elements (e.g., equity-like features), the asset fails the SPPI test.

Classification Outcomes

| Business Model | SPPI Test Result | Classification | Measurement Basis |

|---|---|---|---|

| Hold to Collect | Pass | Amortized Cost | Amortized Cost |

| Hold to Collect and Sell | Pass | FVOCI | Fair Value Through OCI |

| Any Other | Fail or Any | FVTPL | Fair Value Through P&L |

Mind Map: Measurement Basis

Practical Example 1: Classification of a Corporate Bond

Scenario: A company purchases a corporate bond with fixed interest payments and principal repayment at maturity. The company’s business model is to hold the bond to collect contractual cash flows.

- Business Model: Hold to collect

- SPPI Test: Pass (fixed interest and principal)

- Classification: Amortized Cost

Measurement: The bond is measured at amortized cost using the effective interest method.

Practical Example 2: Classification of Equity Investment

Scenario: A company invests in equity shares of another company and intends to actively trade these shares.

- Business Model: Other (trading)

- SPPI Test: Not applicable (equity instruments do not have contractual cash flows of principal and interest)

- Classification: FVTPL

Measurement: The investment is measured at fair value with changes recognized in profit or loss.

Practical Example 3: Debt Instrument Held for Both Collecting and Selling

Scenario: A company holds government bonds to collect interest and occasionally sells them to manage liquidity.

- Business Model: Hold to collect and sell

- SPPI Test: Pass

- Classification: FVOCI

Measurement: Fair value changes are recognized in OCI, with interest income recognized in profit or loss.

Summary of Best Practices

- Document Business Model: Maintain clear documentation of the business model for managing financial assets.

- Perform SPPI Testing Thoroughly: Analyze contractual terms carefully to determine SPPI compliance.

- Regularly Review Classification: Reassess classification if business models change.

- Use Examples to Train Teams: Incorporate practical examples in training to enhance understanding.

By following these guidelines and understanding the classification criteria, finance professionals can ensure compliance with IFRS 9 and enhance the accuracy and transparency of financial reporting.

5.2 GAAP ASC 320 and ASC 825 Overview

Under U.S. GAAP, accounting for financial instruments is primarily governed by two key Accounting Standards Codification (ASC) topics:

- ASC 320: Investments—Debt and Equity Securities

- ASC 825: Financial Instruments

These standards provide guidance on classification, measurement, impairment, and disclosure requirements for financial instruments.

ASC 320: Investments—Debt and Equity Securities

ASC 320 focuses on the accounting and reporting for investments in debt and equity securities. It classifies securities into three categories based on management’s intent and ability:

- Held-to-Maturity (HTM)

- Trading Securities

- Available-for-Sale (AFS) Securities

Mind Map: ASC 320 Classification and Measurement

Example: Classification of a Corporate Bond

Company A purchases a corporate bond with a maturity of 5 years.

- If Company A intends and is able to hold the bond until maturity, classify as HTM and measure at amortized cost.

- If Company A buys the bond to actively trade, classify as Trading and measure at fair value with changes in earnings.

- If Company A neither intends to hold to maturity nor actively trade, classify as AFS and measure at fair value with changes in OCI.

ASC 825: Financial Instruments

ASC 825 provides guidance on the recognition and measurement of financial instruments not covered by other specific standards, including the option to measure certain financial assets and liabilities at fair value.

Key aspects include:

- Fair Value Option (FVO): Permits entities to elect fair value measurement for eligible financial instruments to reduce accounting mismatches.

- Disclosure Requirements: Requires extensive disclosures about fair value measurements, risks, and methods.

Mind Map: ASC 825 Key Provisions

Example: Using the Fair Value Option

Company B holds a loan receivable that is not classified under ASC 320. To better reflect economic reality and reduce volatility, Company B elects the fair value option under ASC 825 at initial recognition.

- The loan is measured at fair value on the balance sheet.

- Changes in fair value are recognized in earnings each reporting period.

Integrated Best Practices for ASC 320 and ASC 825

- Classification Accuracy: Ensure securities are classified based on management’s intent and ability, documented clearly.

- Consistent Application: Apply measurement methods consistently across reporting periods.

- Fair Value Measurement: Use reliable valuation techniques and document inputs for fair value measurements.

- Disclosure Transparency: Provide clear disclosures about classification, measurement methods, and risks.

Mind Map: Best Practices for GAAP Financial Instruments

Summary

ASC 320 and ASC 825 together provide a comprehensive framework for accounting for financial instruments under GAAP. Understanding the classification criteria, measurement bases, and disclosure requirements is essential for accountants, auditors, and compliance officers to ensure accurate and transparent financial reporting.

By integrating practical examples and mind maps, professionals can better visualize and apply these standards in real-world scenarios.

5.3 Best Practices for Fair Value Measurement and Disclosure

Fair value measurement is a critical aspect of financial reporting under both IFRS and GAAP. Proper measurement and transparent disclosure ensure that financial statements reflect the true economic value of financial instruments and other assets, enhancing decision-making for stakeholders.

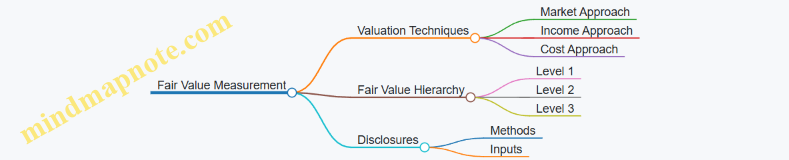

Key Principles of Fair Value Measurement

- Market-Based Measurement: Use observable market data whenever available rather than entity-specific inputs.

- Hierarchy of Inputs: Follow the three-level fair value hierarchy:

- Level 1: Quoted prices in active markets for identical assets or liabilities.

- Level 2: Inputs other than quoted prices that are observable either directly or indirectly.

- Level 3: Unobservable inputs based on the entity’s own assumptions.

- Consistency: Apply consistent valuation techniques and assumptions over reporting periods.

- Documentation: Maintain comprehensive documentation supporting valuation methods, inputs, and judgments.

Mind Map: Fair Value Measurement Best Practices

Best Practices in Disclosure

- Disclose the fair value hierarchy level for each class of assets and liabilities measured at fair value.

- Explain the valuation techniques and inputs used, especially for Level 2 and Level 3 measurements.

- Provide reconciliation of Level 3 measurements from the beginning to the end of the period, including gains/losses recognized.

- Include sensitivity analysis showing how changes in unobservable inputs affect fair value.

- Describe any changes in valuation techniques or inputs from prior periods and the reasons for those changes.

Mind Map: Fair Value Disclosure Requirements

Practical Example: Valuing Equity Securities at Fair Value

Scenario: A government entity holds equity securities in a publicly traded company.

- Level 1 Measurement: The securities are traded on an active stock exchange.

- Valuation: Use the quoted closing price on the reporting date.

- Disclosure:

- State that Level 1 inputs were used.

- Provide the fair value amount.

- No significant judgment or estimation uncertainty involved.

Example Disclosure Extract:

“Equity securities are measured at fair value using quoted prices in active markets (Level 1 inputs). As of December 31, 2023, the fair value of these securities was $5 million. There were no transfers between levels during the period.”

Practical Example: Valuing Complex Derivative Instruments

Scenario: A financial institution holds over-the-counter (OTC) derivatives with no active market.

- Level 2 or Level 3 Measurement: Use valuation models incorporating observable inputs such as interest rates and credit spreads (Level 2), and unobservable inputs like counterparty credit risk adjustments (Level 3).

- Best Practice:

- Use multiple valuation techniques for cross-validation.

- Document all assumptions and model inputs.

- Perform sensitivity analysis on unobservable inputs.

- Disclosure:

- Describe the valuation models and inputs.

- Reconcile Level 3 balances.

- Present sensitivity analysis results.

Example Disclosure Extract:

“Derivative financial instruments are measured at fair value using discounted cash flow models incorporating observable market data (Level 2 inputs) and adjustments for counterparty credit risk (Level 3 inputs). The Level 3 fair value balance at December 31, 2023, was $12 million, with a sensitivity analysis indicating a $1 million increase/decrease in fair value for a 10% change in credit risk assumptions.”

Summary Checklist for Fair Value Measurement and Disclosure

- Identify appropriate valuation technique based on asset/liability type.

- Determine the correct fair value hierarchy level.

- Use observable market data where available.

- Document all assumptions, inputs, and methodologies.

- Consistently apply valuation methods across periods.

- Disclose hierarchy levels and valuation techniques clearly.

- Provide reconciliations and sensitivity analyses for Level 3 inputs.

- Update disclosures to reflect any changes in valuation approaches.

By following these best practices, accountants, auditors, and compliance officers can ensure that fair value measurements are accurate, reliable, and transparent, thereby enhancing the credibility and usefulness of financial reports.

5.4 Example: Valuing Equity Securities at Fair Value

Valuing equity securities at fair value is a critical task under both IFRS and GAAP, especially for financial instruments classified as available-for-sale or held-for-trading. This section provides a detailed example, illustrating best practices and the application of fair value measurement principles.

Understanding Fair Value Measurement

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

Key considerations:

- Use of market data when available

- Hierarchy of inputs (Level 1, Level 2, Level 3)

- Consistency and transparency in valuation methods

Mind Map: Fair Value Measurement Process

Example Scenario

Company A holds 10,000 shares of Company B’s publicly traded stock as of December 31, 2023. The shares are classified as financial assets at fair value through profit or loss (IFRS 9) or trading securities (GAAP).

- Market price on December 31, 2023: $50 per share

- No significant transaction costs

Objective: Determine the fair value of the equity securities and record the appropriate journal entries.

Step 1: Identify the Fair Value

Since Company B’s shares are actively traded on a stock exchange, the fair value is based on the quoted market price (Level 1 input).

Fair value calculation:

Fair Value = Number of Shares × Market Price

Fair Value = 10,000 × $50 = $500,000

Step 2: Journal Entries for Initial Recognition

Assuming the shares were purchased at $45 per share:

Dr Equity Securities (Asset) $450,000

Cr Cash $450,000

Step 3: Adjusting to Fair Value at Reporting Date

At December 31, 2023, the fair value is $500,000, so an unrealized gain of $50,000 must be recognized.

- Under IFRS 9 (fair value through profit or loss):

Dr Equity Securities (Asset) $50,000

Cr Unrealized Gain on Investments (P&L) $50,000

- Under GAAP (trading securities):

Dr Equity Securities (Asset) $50,000

Cr Unrealized Gain on Investments (Income Statement) $50,000

Step 4: Disclosure Best Practices

- Disclose the fair value hierarchy level (Level 1 in this case).

- Describe valuation techniques and inputs.

- Provide sensitivity analysis if Level 3 inputs are used.

Mind Map: Disclosure Requirements for Fair Value of Equity Securities

Additional Example: Valuing Equity Securities Without Active Market

Scenario: Company A holds 5,000 shares of a private company (Company C) with no active market.

- Recent transaction price: $30 per share six months ago

- Adjustments for changes in financial performance and market conditions

Valuation approach: Use Level 3 inputs with an income approach (discounted cash flow).

Steps:

- Estimate future cash flows of Company C.

- Determine appropriate discount rate.

- Calculate present value.

- Adjust for lack of marketability.

Example calculation:

- Estimated fair value per share: $28

- Total fair value = 5,000 × $28 = $140,000

Journal entry to adjust carrying amount:

If carrying amount was $150,000:

Dr Unrealized Loss on Investments (P&L) $10,000

Cr Equity Securities (Asset) $10,000

Summary

Valuing equity securities at fair value requires:

- Identifying the appropriate input level

- Applying consistent valuation techniques

- Recognizing unrealized gains or losses appropriately

- Providing transparent disclosures

By following these best practices, accountants and auditors can ensure compliance with IFRS and GAAP while providing stakeholders with reliable financial information.

6. Impairment of Assets

6.1 IFRS IAS 36 Impairment Testing Procedures

IFRS IAS 36 outlines the procedures for impairment testing to ensure that assets are carried at no more than their recoverable amount. When an asset’s carrying amount exceeds its recoverable amount, an impairment loss must be recognized.

Key Concepts of IAS 36

- Carrying Amount: The amount at which an asset is recognized in the balance sheet after deducting accumulated depreciation and accumulated impairment losses.

- Recoverable Amount: The higher of an asset’s fair value less costs of disposal and its value in use.

- Impairment Loss: The amount by which the carrying amount of an asset exceeds its recoverable amount.

When to Perform Impairment Testing?

- Indicators of impairment include significant decline in market value, adverse changes in the business environment, physical damage, or underperformance compared to expectations.

- Annual impairment testing is mandatory for intangible assets with indefinite useful lives and goodwill.

Step-by-Step Impairment Testing Procedure

Detailed Explanation of Each Step

-

Identify Indicators of Impairment

- Review both external and internal sources for signs that the asset may be impaired.

-

Calculate Recoverable Amount

- Fair Value Less Costs of Disposal (FVLCD): The price obtainable from selling the asset in an arm’s length transaction minus costs associated with disposal.

- Value in Use (VIU): Present value of estimated future cash flows expected to arise from the asset.

-

Compare Carrying Amount and Recoverable Amount

- If carrying amount > recoverable amount, impairment loss exists.

-

Recognize and Measure Impairment Loss

- Impairment loss = Carrying amount - Recoverable amount.

- Charge the loss to profit or loss immediately.

-