Financial Systems Implementation

1. Introduction to Financial Systems Implementation

1.1 Understanding Financial Systems: Definitions and Scope

What is a Financial System?

A financial system is a structured framework that facilitates the management, processing, and reporting of financial data within an organization. It encompasses the tools, processes, policies, and technologies used to collect, store, and analyze financial information to support decision-making, compliance, and operational efficiency.

Financial systems are critical for organizations to maintain accurate records, ensure regulatory compliance, and provide timely insights into financial performance.

Mind Map: Core Components of Financial Systems

Scope of Financial Systems

The scope of financial systems extends beyond simple bookkeeping. It includes:

- Transaction Processing: Recording day-to-day financial transactions such as sales, purchases, payments, and receipts.

- Financial Reporting: Generating statutory and management reports to provide insights into financial health.

- Budgeting and Forecasting: Planning future financial activities and comparing actuals against budgets.

- Compliance Management: Ensuring adherence to regulatory requirements like GAAP, IFRS, SOX, and tax laws.

- Risk Management: Identifying and mitigating financial risks through controls and audits.

- Integration: Connecting with other enterprise systems such as HR, procurement, and inventory for seamless data flow.

Mind Map: Financial System Functions and Their Scope

Example 1: Small Business Financial System

A small retail business uses a cloud-based accounting software like QuickBooks to manage invoices, track expenses, and generate monthly profit and loss statements. The system integrates with the business’s bank account to automatically import transactions, reducing manual entry errors.

Best Practice: Automate bank feeds to improve data accuracy and save time.

Example 2: Large Enterprise Financial System

A multinational corporation implements an ERP system such as SAP or Oracle Financials. This system handles complex multi-currency transactions, consolidates financial data from various subsidiaries, supports regulatory reporting across different jurisdictions, and integrates with supply chain and HR modules.

Best Practice: Leverage modular architecture to customize financial processes while maintaining a unified data source.

Why Understanding Definitions and Scope Matters

For accountants and IT project managers, a clear understanding of what constitutes a financial system and its scope is essential to:

- Define accurate project requirements.

- Align system capabilities with business needs.

- Identify integration points and potential risks.

- Ensure compliance with financial regulations.

- Facilitate effective communication between finance and IT teams.

Summary

Financial systems are comprehensive platforms that support the entire financial management lifecycle within organizations. Their scope covers transaction processing, reporting, compliance, risk management, and integration with other enterprise systems. Understanding these elements helps stakeholders implement systems that are efficient, compliant, and scalable.

1.2 Importance of Financial Systems in Modern Organizations

Financial systems are the backbone of any modern organization, enabling efficient management of financial data, compliance with regulations, and informed decision-making. Their importance transcends simple bookkeeping, impacting strategic planning, operational efficiency, and competitive advantage.

Why Financial Systems Matter

- Accuracy and Reliability: Automated financial systems reduce human error, ensuring data integrity.

- Regulatory Compliance: Systems help organizations adhere to complex financial regulations and reporting standards.

- Real-Time Reporting: Enables timely insights into financial health, supporting agile decision-making.

- Cost Efficiency: Streamlines processes, reducing manual labor and operational costs.

- Scalability: Supports growth by handling increasing transaction volumes and complexity.

Mind Map: Core Benefits of Financial Systems

Example: Real-Time Reporting in Action

A mid-sized retail company implemented a cloud-based financial system that integrated sales, inventory, and accounting data. This integration allowed the CFO to access real-time dashboards showing cash flow, profit margins, and inventory costs. As a result, the company could quickly adjust pricing strategies during peak seasons, improving profitability by 15% within six months.

Mind Map: Impact Areas of Financial Systems

Example: Enhancing Operational Efficiency

An accounting firm adopted a financial system with automated invoicing and expense tracking. Previously, accountants spent hours manually entering data and reconciling accounts. Post-implementation, the firm reduced invoice processing time by 70%, freeing up staff to focus on advisory services and client engagement.

Mind Map: Stakeholders Benefiting from Financial Systems

Example: Supporting Compliance and Audit

A multinational corporation used an integrated financial system that automatically generated audit trails and compliance reports aligned with SOX and IFRS standards. This automation reduced audit preparation time by 50% and minimized compliance risks, enabling smoother regulatory reviews.

Summary

Financial systems are essential tools that empower organizations to maintain financial accuracy, comply with regulations, improve operational efficiency, and support strategic growth. By leveraging these systems, accountants and IT project managers can collaborate to deliver robust financial management solutions that drive business success.

1.3 Key Stakeholders: Accountants, IT Project Managers, and Beyond

In any financial systems implementation, understanding and engaging key stakeholders is critical to the project’s success. Stakeholders are individuals or groups who have an interest in the project outcome, influence its progress, or are impacted by the system.

Primary Stakeholders

- Accountants: They are the end-users who rely on the financial system for accurate reporting, compliance, and daily financial operations.

- IT Project Managers: Responsible for planning, executing, and closing the implementation project, ensuring it meets scope, time, and budget constraints.

Secondary Stakeholders

- Finance Managers and Controllers: Oversee financial operations and require system insights for decision-making.

- Internal Auditors: Ensure the system meets compliance and internal control standards.

- External Auditors: Validate financial data integrity and regulatory compliance.

- Vendors and Software Providers: Deliver the financial system and provide ongoing support.

- Executive Leadership: Sponsor the project and align it with strategic goals.

Mind Map: Stakeholders in Financial Systems Implementation

Roles and Responsibilities with Examples

Accountants

- Role: Primary users of the financial system, responsible for entering transactions, generating reports, and ensuring data accuracy.

- Example: During implementation, accountants participate in User Acceptance Testing (UAT) to validate that the system correctly processes payroll and accounts payable.

IT Project Managers

- Role: Lead the project team, manage timelines, coordinate between technical and business teams, and mitigate risks.

- Example: The IT Project Manager schedules weekly status meetings, tracks milestones, and resolves issues such as integration challenges between the new financial system and existing ERP software.

Finance Managers and Controllers

- Role: Provide requirements, review system outputs, and ensure the system supports financial planning and control.

- Example: Finance managers review customized dashboards that summarize budget variances and approve configuration changes to reporting modules.

Internal and External Auditors

- Role: Validate that the system complies with internal policies and external regulations.

- Example: Internal auditors test access controls within the system to ensure segregation of duties, while external auditors verify that financial reports generated meet GAAP standards.

Vendors and Software Providers

- Role: Deliver the software, provide training, and offer technical support.

- Example: The vendor conducts training sessions for accountants on new features such as automated invoice processing.

Executive Leadership

- Role: Provide project sponsorship, allocate resources, and ensure alignment with organizational strategy.

- Example: Executives review project dashboards and approve budget increases to address unforeseen customization needs.

Mind Map: Interaction Between Stakeholders

Example Scenario: Collaborative Success

In a mid-sized finance company implementing a new cloud-based financial system, the IT Project Manager organized cross-functional workshops involving accountants, finance managers, and auditors. Accountants provided detailed input on daily transaction workflows, which helped the vendor tailor the system’s interface for ease of use. Meanwhile, auditors identified critical control points that were incorporated into the system design early on. Executive leadership regularly reviewed progress reports, enabling timely decisions on resource adjustments. This collaboration led to a smooth implementation with minimal disruption and high user adoption.

Summary

Engaging all key stakeholders—accountants, IT project managers, finance managers, auditors, vendors, and executives—is essential for a successful financial systems implementation. Clear communication, defined roles, and collaborative decision-making ensure the system meets business needs, complies with regulations, and is adopted effectively by users.

1.4 Overview of Implementation Lifecycle: From Planning to Go-Live

Implementing a financial system is a complex process that requires careful coordination between accountants, IT project managers, and other stakeholders. Understanding the implementation lifecycle is crucial to ensure a smooth transition and successful deployment. This section breaks down the lifecycle into key phases, illustrating best practices and providing easy-to-understand examples.

Implementation Lifecycle Phases

Planning Phase

Best Practice: Begin with a comprehensive needs assessment involving both finance and IT teams to align system capabilities with business goals.

Example: A mid-sized accounting firm conducted workshops with accountants and IT staff to identify pain points in their current system, such as slow reporting and lack of integration with payroll. This helped define clear objectives for the new system.

Requirements Gathering

Best Practice: Use interviews, surveys, and observation to gather detailed functional and non-functional requirements. Prioritize them to focus on critical features first.

Example: The project manager organized focus groups with senior accountants to document must-have features like multi-currency support and audit trail capabilities, ensuring these were prioritized in the system design.

Design & Customization

Best Practice: Decide early whether to configure existing system features or develop custom modules. Keep customization minimal to reduce complexity and future maintenance.

Example: A financial institution chose to configure the standard chart of accounts and reporting templates instead of building custom reports, saving time and reducing risk.

Data Migration

Best Practice: Assess data quality before migration and develop a detailed ETL (Extract, Transform, Load) plan. Validate data post-migration to ensure accuracy.

Example: Before migrating data from legacy spreadsheets, a company cleaned up duplicate entries and standardized account codes, which prevented errors during migration.

Testing

Best Practice: Conduct multiple testing stages including unit testing, integration testing, and user acceptance testing (UAT). Engage accountants in UAT to verify system meets business needs.

Example: During UAT, accountants discovered that the tax calculation module did not handle a new regulation correctly. This feedback allowed developers to fix the issue before go-live.

Training & Change Management

Best Practice: Develop role-specific training programs and communicate changes clearly to reduce resistance. Use simulations and hands-on workshops.

Example: An IT project manager created interactive training sessions for finance staff, including real-life transaction scenarios, which improved user confidence and adoption.

Deployment (Go-Live)

Best Practice: Choose a deployment strategy (big bang or phased) based on organizational readiness. Prepare infrastructure and have a go-live checklist.

Example: A company opted for a phased rollout starting with the accounts payable module, allowing the team to stabilize processes before full system deployment.

Mind Map: Go-Live Checklist

Summary

The financial systems implementation lifecycle is a structured approach that guides organizations from initial planning through to successful go-live and beyond. By following best practices and involving both accountants and IT project managers at every stage, organizations can minimize risks and maximize the benefits of their new financial system.

For accountants and IT project managers, understanding this lifecycle is the foundation for collaboration and successful project delivery.

1.5 Common Challenges and Risks in Financial Systems Implementation

Implementing a financial system is a complex endeavor that involves multiple stakeholders, intricate processes, and critical data. Understanding common challenges and risks upfront can help accountants and IT project managers mitigate issues and ensure a smoother implementation.

Key Challenges and Risks

Data Management Challenges

One of the most critical risks during implementation is related to data. Financial systems rely heavily on accurate, consistent, and complete data.

Example: A mid-sized company migrating from a legacy accounting system to a cloud-based ERP faced significant delays because the legacy data had inconsistent account codes and missing transaction histories. This required extensive data cleansing and validation before migration.

Best Practice: Conduct thorough data profiling and cleansing before migration. Use automated ETL (Extract, Transform, Load) tools to standardize data formats and validate data integrity.

Stakeholder Engagement Issues

Lack of involvement from key users, especially accountants who will use the system daily, can lead to misaligned expectations and resistance.

Example: In a financial system rollout for a multinational firm, the IT team selected features without consulting the finance department, resulting in a system that did not support essential reporting requirements. This caused frustration and delayed adoption.

Best Practice: Engage end users early and continuously through workshops, feedback sessions, and pilot testing. Communicate benefits clearly to reduce resistance.

Project Management Risks

Poor scope control, inadequate planning, and resource shortages can derail the project timeline and budget.

Example: An IT project manager underestimated the time needed for customization and integration, leading to multiple deadline extensions and budget overruns.

Best Practice: Develop a detailed project plan with realistic milestones. Use agile methodologies to manage scope and adapt to changes. Ensure resource availability and contingency planning.

Technical Issues

Integrating the new financial system with existing IT infrastructure can be complex, and performance or security issues may arise.

Example: During implementation, a bank experienced system slowdowns because the new financial software was not optimized for their existing database architecture, affecting transaction processing times.

Best Practice: Conduct thorough system compatibility assessments and performance testing. Implement robust security protocols and conduct vulnerability assessments.

Compliance and Regulatory Risks

Financial systems must comply with regulations such as SOX, GDPR, or industry-specific standards. Failure to do so can result in penalties.

Example: A company failed an audit because the new system did not maintain proper audit trails for financial transactions, violating SOX requirements.

Best Practice: Involve compliance experts during design and testing phases. Ensure the system supports audit trails, access controls, and reporting needed for regulatory compliance.

Summary Mind Map

By proactively identifying and addressing these challenges, accountants and IT project managers can significantly increase the chances of a successful financial systems implementation.

2. Planning and Preparation for Implementation

2.1 Conducting Needs Assessment: Aligning Business Goals with System Requirements

Conducting a thorough needs assessment is the foundational step in any successful financial systems implementation. This process ensures that the chosen system aligns perfectly with the organization’s strategic business goals and operational requirements. For accountants and IT project managers, understanding and executing a needs assessment effectively can save time, reduce costs, and improve system adoption.

What is a Needs Assessment?

A needs assessment is a systematic process used to determine and address gaps between the current state and desired future state of an organization’s financial systems. It involves gathering detailed information about business processes, pain points, and objectives to define clear system requirements.

Why is Needs Assessment Critical?

- Aligns Technology with Business Strategy: Ensures the system supports key financial goals.

- Identifies Stakeholder Needs: Captures input from accountants, finance teams, and IT.

- Prevents Scope Creep: Clear requirements reduce project overruns.

- Facilitates Better Vendor Selection: Helps in evaluating systems that meet actual needs.

Steps in Conducting a Needs Assessment

- Define Business Goals

- Map Current Financial Processes

- Identify Pain Points and Gaps

- Gather Stakeholder Input

- Translate Needs into System Requirements

- Prioritize Requirements

Mind Map: Needs Assessment Process

Example: Aligning Business Goals with System Requirements

Scenario: A mid-sized financial services company wants to implement a new financial system to improve reporting accuracy and reduce month-end closing time.

-

Business Goals:

- Reduce month-end close from 10 days to 5 days.

- Improve accuracy of financial reports.

- Ensure compliance with new regulatory standards.

-

Identified Pain Points:

- Manual consolidation of data from multiple sources.

- Lack of real-time reporting.

- Errors due to manual journal entries.

-

Derived System Requirements:

- Automated data consolidation from multiple ledgers.

- Real-time dashboard and reporting capabilities.

- Workflow automation for journal entry approvals.

-

Prioritization:

- Must-Have: Automated consolidation, real-time reporting.

- Nice-to-Have: Mobile access to dashboards.

- Future Enhancements: AI-driven anomaly detection.

Mind Map: Example Scenario Breakdown

Tips for Effective Needs Assessment

- Engage Cross-Functional Teams: Include accountants, finance managers, and IT early.

- Use Workshops and Interviews: Gather qualitative and quantitative data.

- Document Everything Clearly: Use diagrams, flowcharts, and mind maps.

- Validate Findings: Review requirements with stakeholders to ensure accuracy.

- Be Realistic and Prioritize: Focus on critical needs to avoid scope creep.

Summary

A well-executed needs assessment bridges the gap between business objectives and technical solutions. By methodically defining goals, mapping processes, and gathering stakeholder input, accountants and IT project managers can collaboratively craft a clear, prioritized set of system requirements. This alignment is essential for selecting and implementing a financial system that drives efficiency, accuracy, and compliance.

Further Reading

- Business Analysis for Accountants: Bridging Finance and IT by Jane Doe

- The Project Manager’s Guide to Financial Systems Implementation by John Smith

- Articles on effective requirements gathering at PMI.org

2.2 Building a Cross-Functional Implementation Team: Roles and Responsibilities

Successful financial systems implementation hinges on assembling a well-rounded, cross-functional team that brings together diverse expertise and perspectives. This team ensures that both technical and business requirements are met, risks are managed, and the project stays aligned with organizational goals.

Why a Cross-Functional Team?

- Holistic Understanding: Combines finance knowledge with IT expertise.

- Improved Communication: Bridges gaps between departments.

- Efficient Problem Solving: Diverse perspectives lead to innovative solutions.

- Ownership and Accountability: Shared responsibility increases commitment.

Core Roles and Their Responsibilities

Below is a mind map illustrating the key roles typically involved in a financial systems implementation team, along with their primary responsibilities.

Example: Building a Team for a Mid-Sized Company Financial System Implementation

Scenario: A mid-sized company is implementing a new ERP financial module. The project manager assembles the following team:

- Project Sponsor: CFO, who ensures alignment with financial strategy.

- Project Manager: IT Project Manager with experience in ERP rollouts.

- Business Analyst: Senior Accountant familiar with current workflows.

- IT Architect: Internal IT lead responsible for system integration.

- Data Specialist: Database administrator handling legacy data migration.

- QA Lead: IT tester coordinating UAT with finance staff.

- Training Manager: HR representative developing user training.

- End Users: Accounts payable and receivable clerks engaged for feedback.

This team meets weekly to discuss progress, risks, and upcoming milestones. The business analyst translates accounting needs into technical requirements, while the IT architect ensures the system fits the company’s infrastructure. The QA lead organizes testing sessions with end users to validate functionality.

Mind Map: Responsibilities Breakdown

Best Practices for Team Building

- Define Clear Roles and Responsibilities: Avoid overlap and gaps.

- Select Members with Relevant Expertise: Both technical and business knowledge.

- Foster Open Communication: Regular meetings and transparent updates.

- Encourage Collaboration: Use collaborative tools and shared documentation.

- Empower End Users: Involve them early to increase buy-in.

- Provide Leadership Support: Ensure executives are engaged and supportive.

Example: Communication Flow in a Cross-Functional Team

Summary

Building a cross-functional implementation team is critical for the success of financial systems projects. By clearly defining roles, fostering collaboration, and involving both finance and IT professionals, organizations can navigate complexities effectively and deliver systems that truly meet business needs.

2.3 Budgeting and Resource Allocation: Best Practices with Real-World Examples

Effective budgeting and resource allocation are critical to the success of any financial systems implementation. Without a clear understanding of costs and resource needs, projects risk delays, scope creep, and budget overruns. This section explores best practices for budgeting and resource allocation, supported by real-world examples and mind maps to visualize key concepts.

Best Practices for Budgeting

-

Define Clear Project Scope

- Understand all components of the financial system implementation.

- Avoid scope creep by documenting requirements and changes.

-

Identify All Cost Categories

- Software licensing and subscriptions

- Hardware and infrastructure

- Consulting and implementation services

- Training and change management

- Contingency reserves

-

Use Historical Data and Benchmarks

- Leverage data from previous implementations or industry standards.

- Adjust estimates based on organizational size and complexity.

-

Involve Cross-Functional Stakeholders

- Collaborate with finance, IT, and operations teams to capture all cost perspectives.

-

Plan for Contingencies

- Allocate 10-20% of the total budget for unforeseen expenses.

-

Regularly Review and Update Budget

- Track actual spending against budget.

- Adjust allocations as project evolves.

Best Practices for Resource Allocation

-

Identify Required Skill Sets

- Accountants for financial process expertise

- IT project managers for technical oversight

- Data migration specialists

- Trainers and change management experts

-

Assign Clear Roles and Responsibilities

- Use RACI matrices to clarify accountability.

-

Balance Internal and External Resources

- Determine which tasks require consultants vs. internal staff.

-

Optimize Resource Utilization

- Avoid overallocation to prevent burnout.

- Use resource leveling techniques.

-

Plan for Training and Knowledge Transfer

- Ensure internal teams gain skills for post-implementation support.

Mind Map: Budgeting Components for Financial Systems Implementation

Mind Map: Resource Allocation Strategy

Real-World Example 1: Mid-Sized Financial Firm Implementation

Scenario: A mid-sized financial firm planned to implement a new ERP financial module.

Budgeting Approach:

- Defined scope including core accounting, budgeting, and reporting modules.

- Estimated software licensing at $150,000 annually.

- Allocated $75,000 for consulting services.

- Set aside $25,000 for training sessions.

- Included a 15% contingency ($37,500).

Outcome:

- The firm completed implementation within 5% of budget.

- Early involvement of accountants helped identify hidden training needs, preventing costly rework.

Real-World Example 2: Large Bank’s Cloud-Based Financial System Rollout

Scenario: A large bank transitioned its financial systems to a cloud platform.

Resource Allocation:

- Created a cross-functional team with 10 IT project managers, 15 accountants, 5 data migration experts, and 3 change management specialists.

- Used a RACI matrix to assign responsibilities, ensuring no overlap.

- Balanced internal staff with external consultants for specialized cloud expertise.

- Scheduled phased training to avoid overwhelming staff.

Outcome:

- Smooth deployment with minimal downtime.

- Effective resource leveling prevented burnout during peak phases.

Summary

Budgeting and resource allocation are foundational to financial systems implementation success. By clearly defining scope, involving stakeholders, planning contingencies, and strategically assigning resources, organizations can mitigate risks and optimize outcomes. The mind maps above provide a visual framework to organize these efforts, while real-world examples demonstrate practical application.

Actionable Tips

- Start budgeting early and revisit regularly.

- Use mind maps to visualize budget and resource components.

- Engage both finance and IT teams in planning.

- Document roles clearly to avoid confusion.

- Monitor resource utilization to maintain team health.

This approach ensures that accountants and IT project managers collaborate effectively, aligning financial and technical perspectives for a successful financial systems implementation.

2.4 Selecting the Right Financial System: Criteria and Evaluation Techniques

Selecting the right financial system is a critical decision that can significantly impact an organization’s efficiency, compliance, and overall financial health. This section will guide you through essential criteria and evaluation techniques, supported by practical examples and mind maps to help visualize the decision-making process.

Key Criteria for Selecting a Financial System

When evaluating financial systems, consider the following core criteria:

- Functionality: Does the system cover all necessary financial processes such as general ledger, accounts payable/receivable, budgeting, and reporting?

- Scalability: Can the system grow with your organization’s needs?

- Integration: How well does the system integrate with existing software (e.g., ERP, CRM, payroll)?

- User Experience: Is the interface intuitive for accountants and finance professionals?

- Compliance and Security: Does it support regulatory requirements and protect sensitive financial data?

- Cost: What are the total costs including licensing, implementation, training, and maintenance?

- Vendor Support and Reputation: Is the vendor reliable with strong customer support?

Mind Map: Financial System Selection Criteria

Evaluation Techniques

Requirements Mapping

Start by mapping your organization’s specific financial needs against the features offered by potential systems. This ensures alignment and helps identify any gaps.

Example: A mid-sized company requires multi-currency support and automated tax calculations. During evaluation, they score each system on these features to shortlist options.

Request for Proposal (RFP)

Prepare an RFP detailing your requirements and send it to vendors. Evaluate responses based on how well they meet your criteria.

Example: An IT project manager drafts an RFP emphasizing integration capabilities and user training support. Vendors respond with tailored proposals, which are then scored.

Demo and Trial Periods

Arrange product demonstrations and trial periods to allow end-users (accountants) to interact with the system firsthand.

Example: Accountants test the reporting module during a 30-day trial to assess usability and reporting flexibility.

Scoring Models

Use weighted scoring models to objectively compare systems across multiple criteria.

Example: Assign weights to criteria like functionality (30%), cost (25%), integration (20%), user experience (15%), and support (10%). Each system is scored accordingly, and the highest total score indicates the best fit.

Mind Map: Evaluation Techniques

Practical Example: Selecting a Financial System for a Growing Startup

Scenario: A startup with 50 employees is looking for a financial system that supports rapid growth, multi-department budgeting, and integrates with their existing CRM.

Process:

- Requirements Gathering: The finance team lists critical features: multi-department budgeting, real-time reporting, and CRM integration.

- RFP Preparation: The IT project manager sends out an RFP emphasizing these needs.

- Demo Sessions: The team tests three shortlisted systems, focusing on ease of use and integration.

- Scoring Model: They assign weights prioritizing integration (35%) and functionality (30%).

- Decision: Based on scores and user feedback, they select a cloud-based system with strong CRM integration and scalable features.

Tips for Successful Selection

- Involve End Users Early: Accountants and finance professionals should participate in demos and trials.

- Consider Future Needs: Choose a system that can adapt as your organization evolves.

- Evaluate Vendor Stability: Long-term vendor viability ensures ongoing support.

- Balance Cost and Value: The cheapest option may not deliver the best ROI.

By following these criteria and evaluation techniques, organizations can confidently select a financial system that aligns with their operational needs and strategic goals, ensuring a smoother implementation and greater long-term success.

2.5 Developing a Detailed Project Plan: Milestones, Timelines, and Deliverables

Creating a detailed project plan is a cornerstone of successful financial systems implementation. It acts as a roadmap that guides the team through each phase, ensuring alignment, accountability, and timely delivery. This section will walk you through best practices for developing a project plan, enriched with practical examples and mind maps to visualize the process.

Why a Detailed Project Plan Matters

- Clarity: Defines what needs to be done, by whom, and when.

- Risk Mitigation: Identifies potential bottlenecks early.

- Communication: Keeps stakeholders informed and engaged.

- Resource Management: Allocates budget, personnel, and tools efficiently.

Key Components of a Project Plan

- Milestones: Significant checkpoints or achievements.

- Timelines: Scheduling of tasks and phases.

- Deliverables: Tangible outputs or results expected.

Step 1: Define Project Milestones

Milestones mark critical points in the project lifecycle. For financial systems implementation, typical milestones include:

- Project Kickoff

- Requirements Sign-Off

- System Design Completion

- Data Migration Completion

- User Acceptance Testing (UAT) Completion

- Go-Live

- Post-Implementation Review

Example Milestone Mind Map

Step 2: Establish Timelines

Timelines break down the project into manageable phases with start and end dates. Use Gantt charts or timeline tools for visualization.

Best Practice Example:

- Phase 1: Planning & Analysis – 4 weeks

- Phase 2: Design & Customization – 6 weeks

- Phase 3: Data Migration – 3 weeks

- Phase 4: Testing – 4 weeks

- Phase 5: Training & Change Management – 2 weeks

- Phase 6: Deployment & Go-Live – 1 week

- Phase 7: Post-Implementation Support – Ongoing

Timeline Mind Map

Step 3: Specify Deliverables

Deliverables are concrete outputs that demonstrate progress. Examples include:

- Requirements Specification Document

- System Design Blueprint

- Data Migration Plan

- Test Cases and Results

- Training Materials

- Deployment Checklist

Deliverables Mind Map

Integrating Milestones, Timelines, and Deliverables

To build a cohesive project plan, link milestones to timelines and deliverables. For example:

| Milestone | Timeline | Deliverable |

|---|---|---|

| Requirements Sign-Off | Weeks 1-4 | Requirements Specification |

| Design Completion | Weeks 5-10 | System Design Document |

| Data Migration Completion | Weeks 11-13 | Data Migration Plan & Reports |

| UAT Completion | Weeks 14-17 | Test Cases & UAT Sign-Off |

| Go-Live | Week 18 | Deployment Checklist |

Practical Example: Mid-Sized Finance Firm

Scenario: A mid-sized finance firm is implementing a new ERP financial module.

- Milestone: Data Migration Completion

- Timeline: Weeks 10-12

- Deliverables: Cleaned and validated data migrated to the new system, migration report.

Approach:

- Conduct data profiling in Week 10.

- Perform trial migration in Week 11.

- Validate migrated data with finance team in Week 12.

This phased approach ensures data integrity and minimizes disruption.

Tools to Support Project Planning

- Microsoft Project: For detailed Gantt charts and resource allocation.

- Trello or Jira: Agile boards for task tracking.

- MindMeister or XMind: For creating mind maps.

- Smartsheet: Combines spreadsheets with project management features.

Summary Mind Map of Developing a Detailed Project Plan

By following these structured steps and leveraging visual tools like mind maps, accountants and IT project managers can collaboratively develop a detailed, transparent, and actionable project plan that drives financial systems implementation success.

3. Requirements Gathering and Analysis

3.1 Engaging End Users: Techniques for Effective Requirement Elicitation

Effective requirement elicitation is a cornerstone of successful financial systems implementation. Engaging end users—primarily accountants and finance professionals—is essential to gather accurate, relevant, and actionable requirements. This section explores practical techniques to involve end users actively, supported by mind maps and easy-to-understand examples.

Why Engage End Users?

- Ensure the system meets actual business needs

- Increase user adoption and satisfaction

- Identify hidden requirements and pain points

- Reduce costly rework and scope creep

Techniques for Effective Requirement Elicitation

Interviews

- One-on-one or small group discussions

- Focused questions to understand workflows, pain points, and expectations

Example: An IT project manager interviews a senior accountant to understand month-end closing challenges. The accountant explains manual reconciliation steps that could be automated.

Workshops

- Collaborative sessions with multiple stakeholders

- Brainstorming, prioritization, and consensus building

Example: A workshop with accountants, auditors, and IT staff to map out the invoice processing workflow and identify bottlenecks.

Surveys and Questionnaires

- Structured data collection from a larger user base

- Quantitative and qualitative insights

Example: A survey sent to all finance department employees asking about their satisfaction with current reporting tools and desired features.

Observation and Job Shadowing

- Watching users perform their tasks in real-time

- Identifying implicit requirements and inefficiencies

Example: An IT analyst shadows an accounts payable clerk to observe manual data entry and discover opportunities for automation.

Document Analysis

- Reviewing existing process documents, reports, and system manuals

- Understanding current state and compliance requirements

Example: Analyzing the company’s financial policy documents to ensure the new system supports regulatory controls.

Prototyping

- Creating mock-ups or wireframes to gather user feedback

- Iterative refinement of requirements

Example: Presenting a dashboard prototype to accountants to validate key performance indicators (KPIs) and layout preferences.

Mind Maps

Mind Map 1: Techniques for Engaging End Users

Mind Map 2: Benefits of End User Engagement

Mind Map 3: Example Scenario - Invoice Processing Workshop

Practical Example: Interview Technique in Action

Context: A mid-sized company is implementing a new financial system. The IT project manager schedules interviews with key accounting staff.

Process:

- Prepare open-ended questions about daily tasks and challenges

- Ask about specific pain points with current systems

- Document suggestions for automation or reporting

Outcome: The interviews reveal that manual bank reconciliations take excessive time and are prone to errors. This insight leads to prioritizing automated reconciliation features in the system design.

Tips for Successful End User Engagement

- Build trust and communicate the value of their input

- Use simple language, avoiding technical jargon

- Encourage honest feedback, including negative experiences

- Schedule sessions at convenient times to maximize participation

- Follow up with summaries and confirm understanding

By applying these techniques thoughtfully, IT project managers and accountants can collaboratively define requirements that ensure the financial system truly supports business objectives and daily operations.

3.2 Documenting Functional and Non-Functional Requirements

Documenting requirements is a critical step in the financial systems implementation process. Clear, well-structured documentation ensures that all stakeholders—accountants, IT project managers, developers, and end users—have a shared understanding of what the system must do and how it should perform.

Understanding Functional vs. Non-Functional Requirements

- Functional Requirements describe what the system should do. They define specific behaviors, features, and functions.

- Non-Functional Requirements specify how the system performs those functions, including constraints and quality attributes.

Why Documenting Both Matters

- Functional requirements ensure the system meets business needs.

- Non-functional requirements ensure usability, reliability, security, and performance.

Mind Map: Overview of Requirements Documentation

Functional Requirements: Key Elements and Examples

- Business Processes

- Example: “The system shall process invoice approvals within 48 hours.”

- User Roles and Permissions

- Example: “Accountants can create and edit financial reports; auditors have read-only access.”

- Data Handling

- Example: “The system shall import bank transaction data in CSV format daily.”

- Reporting

- Example: “Generate monthly profit and loss statements automatically.”

- Workflow Automation

- Example: “Automatically route expense reports to managers for approval.”

Mind Map: Functional Requirements Breakdown

Non-Functional Requirements: Key Elements and Examples

- Performance

- Example: “The system shall handle 1,000 concurrent users without degradation.”

- Security

- Example: “All financial data must be encrypted at rest and in transit.”

- Usability

- Example: “The system shall provide an intuitive dashboard accessible to non-technical users.”

- Scalability

- Example: “The system must support a 20% annual increase in transaction volume.”

- Compliance

- Example: “The system shall comply with SOX and GDPR regulations.”

Mind Map: Non-Functional Requirements Breakdown

Best Practices for Documenting Requirements

- Use Clear, Concise Language: Avoid ambiguity.

- Involve Stakeholders: Validate requirements with accountants, IT managers, and end users.

- Use Visual Aids: Mind maps, flowcharts, and diagrams help clarify complex requirements.

- Prioritize Requirements: Identify must-haves vs. nice-to-haves.

- Maintain Traceability: Link requirements to business objectives and test cases.

Example: Documenting a Functional Requirement

| ID | FR-001 |

|---|---|

| Title | Invoice Approval Workflow |

| Description | The system shall allow accountants to submit invoices for approval and route them automatically to the relevant manager based on department. |

| Priority | High |

| Acceptance Criteria | - Invoice submitted triggers notification to manager. - Manager can approve or reject within 48 hours. - System logs all actions for audit purposes. |

Example: Documenting a Non-Functional Requirement

| ID | NFR-001 |

|---|---|

| Title | Data Encryption |

| Description | All sensitive financial data must be encrypted using AES-256 encryption both at rest and during transmission. |

| Priority | Critical |

| Acceptance Criteria | - Data stored in database is encrypted. - Data transmitted over network uses TLS 1.2 or higher. - Encryption keys are managed securely. |

Summary

Documenting both functional and non-functional requirements with clarity and precision is essential for successful financial systems implementation. Using mind maps and examples helps bridge communication between accountants and IT project managers, ensuring that the system meets business needs while maintaining performance, security, and compliance.

3.3 Prioritizing Requirements: Balancing Needs and Constraints

Prioritizing requirements is a critical step in financial systems implementation. It ensures that the most valuable features and functionalities are delivered first, while balancing time, budget, and resource constraints. Effective prioritization helps avoid scope creep, reduces risk, and aligns the project with business goals.

Why Prioritize Requirements?

- Maximize Business Value: Focus on features that deliver the highest ROI.

- Manage Constraints: Time, budget, and resource limitations require trade-offs.

- Improve Stakeholder Satisfaction: Address critical needs early to build trust.

- Reduce Risk: Early delivery of core functionality mitigates project failure.

Common Prioritization Techniques

| Technique | Description | Example Use Case |

|---|---|---|

| MoSCoW | Categorizes requirements into Must, Should, Could, Won’t have | Must: Regulatory reporting; Could: Custom dashboards |

| Kano Model | Classifies features by customer satisfaction impact | Must: Accurate ledger entries; Delighters: AI-driven insights |

| Weighted Scoring | Assigns scores based on criteria like cost, benefit, risk | Scoring features based on impact on month-end close |

| 100-Point Method | Stakeholders distribute 100 points across requirements | Team allocates points to prioritize integration features |

Mind Map: Prioritization Framework

Example: Applying MoSCoW in a Financial System Implementation

Scenario: A mid-sized company is implementing a new ERP financial module. The team must prioritize features for the first release.

-

Must Have:

- General ledger functionality

- Regulatory compliance reporting (e.g., tax filings)

- Accounts payable and receivable

-

Should Have:

- Automated bank reconciliation

- Budgeting and forecasting tools

-

Could Have:

- Customizable dashboards

- Mobile access for expense approvals

-

Won’t Have:

- Integration with legacy CRM in first phase

This clear categorization helps the team focus on delivering core financial operations first, ensuring compliance and basic functionality before adding enhancements.

Mind Map: MoSCoW Prioritization Example

Balancing Needs and Constraints: Practical Tips

- Engage Stakeholders Early: Include accountants and IT project managers to understand critical needs and technical feasibility.

- Use Data-Driven Decisions: Leverage historical data on pain points, compliance deadlines, and financial impact.

- Iterative Prioritization: Revisit priorities regularly as project progresses and new information emerges.

- Document Trade-Offs: Clearly record decisions and rationale to maintain transparency.

- Focus on Minimum Viable Product (MVP): Deliver a working system with essential features before expanding.

Example: Weighted Scoring for Month-End Close Features

| Requirement | Business Impact (1-5) | Complexity (1-5) | Compliance (1-5) | Total Score (Impact - Complexity + Compliance) |

|---|---|---|---|---|

| Automated Journal Entries | 5 | 3 | 4 | 6 |

| Real-Time Financial Reporting | 4 | 4 | 3 | 3 |

| Multi-Currency Support | 3 | 5 | 2 | 0 |

The team selects Automated Journal Entries first due to its high net score, balancing impact and complexity.

Mind Map: Weighted Scoring Approach

Summary

Prioritizing requirements in financial systems implementation is about balancing what the business needs most with what is feasible within constraints. Using structured techniques like MoSCoW, Kano, or Weighted Scoring, combined with stakeholder engagement and iterative review, ensures that the project delivers maximum value efficiently and effectively.

3.4 Using Use Cases and User Stories: Practical Examples from Finance Teams

In financial systems implementation, capturing clear and actionable requirements is crucial. Two powerful techniques to achieve this are Use Cases and User Stories. Both help translate business needs into system functionalities, ensuring that the implemented system aligns with user expectations.

What Are Use Cases?

Use cases describe interactions between users (actors) and the system to achieve a specific goal. They provide a detailed narrative that outlines the steps involved in a process.

Example Use Case:

- Title: Process Vendor Invoice Payment

- Actors: Accountant, Financial System

- Goal: Successfully record and pay vendor invoices

Basic Flow:

- Accountant logs into the financial system.

- Accountant selects ‘Invoice Payment’ module.

- Accountant enters invoice details (vendor, amount, due date).

- System validates invoice data.

- Accountant submits payment request.

- System processes payment and updates ledger.

- System generates payment confirmation.

Alternate Flow:

- If invoice data is invalid, system prompts for correction.

What Are User Stories?

User stories are short, simple descriptions of a feature told from the perspective of the end user. They focus on the ‘who’, ‘what’, and ‘why’ to keep requirements user-centric.

User Story Format:

As a [type of user], I want [an action] so that [a benefit].

Example User Stories from Finance Teams:

- As an Accountant, I want to generate monthly financial reports so that I can review company performance quickly.

- As a Finance Manager, I want to approve expense claims via mobile so that I can expedite reimbursements while on the go.

- As an Auditor, I want to access transaction logs so that I can verify compliance with regulations.

Mind Map: Use Cases vs User Stories

Practical Example: Capturing Requirements for Expense Management Module

| Requirement Type | Description | Example |

|---|---|---|

| Use Case | Detailed process of submitting and approving expenses | Accountant submits expense claim → Manager reviews → Finance processes reimbursement |

| User Story | Simple user need description | As an Accountant, I want to submit expense claims online so that I can avoid paperwork. |

Use Case Mind Map:

User Story Mind Map:

Tips for Writing Effective Use Cases and User Stories in Finance Teams

- Engage real users: Collaborate with accountants and finance managers to capture authentic workflows.

- Keep it simple: Avoid jargon; use language familiar to finance professionals.

- Prioritize requirements: Focus on high-impact features first.

- Validate regularly: Review with stakeholders to ensure accuracy.

- Use visuals: Mind maps and flowcharts help clarify complex processes.

Summary

Use cases and user stories are complementary tools that help bridge the gap between finance professionals and IT project teams. By incorporating practical examples and visual aids like mind maps, teams can ensure a shared understanding and successful financial systems implementation.

3.5 Validating Requirements with Stakeholders to Avoid Scope Creep

Validating requirements with stakeholders is a critical step in financial systems implementation to ensure the project stays on track and within scope. This process helps confirm that the documented requirements accurately reflect the needs and expectations of all parties involved, minimizing misunderstandings and preventing scope creep.

Why Validate Requirements?

- Ensures alignment between business goals and system capabilities.

- Identifies gaps or inconsistencies early.

- Builds stakeholder confidence and buy-in.

- Reduces costly changes during later phases.

Key Stakeholders to Involve

- Accountants and Finance Teams (end users)

- IT Project Managers

- Compliance Officers

- External Auditors (if applicable)

- Executive Sponsors

Best Practices for Validating Requirements

- Collaborative Workshops: Bring stakeholders together to review and discuss requirements.

- Prototyping: Use wireframes or mockups to visualize requirements.

- Requirement Reviews: Conduct formal walkthroughs and inspections.

- Use Cases and User Stories: Validate through real-world scenarios.

- Sign-off Process: Obtain formal approval to freeze requirements.

Mind Map: Validating Requirements Process

Example Scenario: Avoiding Scope Creep in a Financial Reporting Module

Context: A mid-sized company is implementing a new financial system. During requirements gathering, the finance team requests a complex, customizable reporting feature.

Validation Steps:

- The project manager organizes a workshop including finance, IT, and compliance.

- A prototype of the reporting interface is presented.

- Stakeholders discuss and realize some requested features overlap with existing tools.

- The team agrees to prioritize core reporting features for the initial release and defer advanced customization to a later phase.

- Formal sign-off is obtained on this scope.

Outcome: This validation prevented adding extensive customization that would delay the project and increase costs, effectively avoiding scope creep.

Mind Map: Example Scenario Breakdown

Tips to Maintain Validation Momentum

- Schedule regular requirement review sessions throughout the project.

- Use collaborative tools (e.g., JIRA, Confluence) to track feedback and changes.

- Encourage open communication and document all decisions.

- Educate stakeholders on the impact of scope changes.

By systematically validating requirements with all relevant stakeholders, organizations can ensure clarity, reduce misunderstandings, and keep financial systems implementation projects aligned with business objectives — ultimately avoiding costly scope creep and project delays.

4. System Design and Customization

4.1 Translating Requirements into System Architecture

Translating business and technical requirements into a coherent system architecture is a critical step in financial systems implementation. This process ensures that the final solution aligns with organizational goals, supports user needs, and integrates seamlessly with existing infrastructure.

Understanding the Requirements

Before designing the architecture, it’s essential to thoroughly understand both functional and non-functional requirements gathered from stakeholders, especially accountants and IT project managers. These include:

- Functional Requirements: Transaction processing, reporting, compliance features, multi-currency support.

- Non-Functional Requirements: Performance, scalability, security, maintainability.

Step-by-Step Approach to Translating Requirements

- Categorize Requirements: Group requirements into logical domains such as data management, user interface, integration, security, and reporting.

- Define System Components: Identify major components or modules that will fulfill these requirements.

- Establish Relationships: Map how components interact and communicate.

- Select Architectural Style: Choose between layered, microservices, event-driven, or hybrid architectures based on needs.

- Document Architecture: Use diagrams and models to represent the design clearly.

Mind Map: Translating Requirements into System Architecture

Example: Translating a Requirement for Multi-Currency Support

Requirement: The system must support transactions and reporting in multiple currencies with real-time exchange rate updates.

Translation into Architecture:

- Component: Currency Management Module within the Business Logic Layer.

- Integration: Connects to external exchange rate APIs (Integration Layer).

- Data Layer: Stores currency data and historical exchange rates.

- User Interface: Allows users to select currency preferences and view reports in chosen currencies.

- Security: Ensures secure API communication and data integrity.

Mind Map for Multi-Currency Support:

Example: Mapping Reporting Requirements to Architecture

Requirement: Generate real-time financial reports with drill-down capabilities.

Translation:

- Reporting Module: Part of the Business Logic Layer responsible for aggregating and formatting data.

- Data Warehouse: Optimized storage in the Data Layer for fast query performance.

- Presentation Layer: Interactive dashboards and report viewers.

- Integration: Connects with transactional systems for real-time data.

Mind Map for Reporting Architecture:

Best Practices

- Engage Stakeholders Continuously: Validate architectural decisions with accountants and IT project managers to ensure alignment.

- Use Visual Models: Diagrams and mind maps help clarify complex relationships.

- Prioritize Scalability and Security: Financial systems handle sensitive data and high transaction volumes.

- Iterate Architecture: Refine design as new requirements emerge or constraints change.

By systematically translating requirements into a well-defined architecture, teams can build financial systems that are robust, scalable, and user-friendly, ultimately supporting organizational success.

4.2 Customization vs. Configuration: Making Informed Decisions

When implementing a financial system, one of the critical decisions project teams face is whether to customize the software or simply configure it to meet business needs. Understanding the difference, benefits, risks, and practical implications of each approach is essential for accountants and IT project managers to ensure a successful implementation.

Definitions

- Configuration refers to adjusting the settings and options provided by the financial system out-of-the-box without altering the underlying code. It involves using built-in tools to tailor workflows, reports, user roles, and interfaces.

- Customization involves modifying or extending the software’s source code or adding new modules to create features not originally provided by the vendor.

Mind Map: Customization vs Configuration Overview

Benefits and Risks

| Aspect | Configuration | Customization |

|---|---|---|

| Flexibility | Limited to vendor-provided options | High, can meet unique requirements |

| Cost | Generally lower, no development needed | Higher, requires development and testing |

| Time to Deploy | Faster, uses existing tools | Longer, involves coding and validation |

| Maintenance | Easier, supported by vendor updates | Complex, may require rework during upgrades |

| Upgrade Impact | Minimal, vendor patches usually compatible | High risk, custom code may break with new versions |

Example 1: Configuration in Practice

Scenario: A mid-sized company needs to restrict access to sensitive financial data based on user roles.

Solution: Using the financial system’s role-based access control (RBAC) configuration, the IT project manager sets permissions for different accountant groups without any code changes.

Outcome: The system meets security requirements quickly, with minimal cost and no impact on future upgrades.

Example 2: Customization in Practice

Scenario: A multinational corporation requires a specialized currency conversion feature that accounts for real-time exchange rates and custom rounding rules.

Solution: The IT team develops a custom module integrated into the financial system to handle these unique calculations.

Outcome: While the feature perfectly fits business needs, the team must allocate additional resources for testing and future upgrades to ensure compatibility.

Mind Map: Decision Factors for Customization vs Configuration

Best Practices for Making the Decision

- Thoroughly Analyze Requirements: Engage accountants and finance teams to identify which needs can be met through configuration.

- Prioritize Configuration First: Always attempt to use configuration options before considering customization.

- Evaluate Long-Term Impact: Consider how customization will affect system upgrades and maintenance.

- Prototype and Test: If customization is necessary, develop prototypes to validate feasibility and impact.

- Document Customizations: Maintain detailed documentation to support future troubleshooting and upgrades.

Summary

Choosing between customization and configuration is a balancing act between meeting unique business needs and maintaining system stability and upgradeability. By understanding the trade-offs and applying best practices, accountants and IT project managers can make informed decisions that align with organizational goals and resources.

4.3 Designing User Interfaces for Accountants and Finance Professionals

Designing user interfaces (UI) for accountants and finance professionals requires a deep understanding of their workflows, priorities, and the complexity of financial data. A well-designed UI enhances productivity, reduces errors, and improves user satisfaction.

Key Principles for UI Design in Financial Systems

- Simplicity and Clarity: Financial data can be complex; the UI should present information clearly without overwhelming the user.

- Consistency: Use consistent layouts, colors, and terminology to reduce cognitive load.

- Accessibility: Ensure the interface is usable by all users, including those with disabilities.

- Responsiveness: The UI should perform well on different devices and screen sizes.

- Error Prevention and Handling: Provide clear feedback and prevent common input errors.

Mind Map: Core UI Design Considerations for Finance Professionals

Example 1: Dashboard Design for Quick Financial Insights

Best Practice: Use dashboards to provide accountants with a snapshot of key financial metrics such as cash flow, outstanding invoices, and budget variances.

Example:

- A dashboard with widgets showing:

- Real-time cash position

- Accounts receivable aging

- Expense trends

- Alerts for overdue payments

Why it works: This allows accountants to quickly identify issues without navigating multiple screens.

Mind Map: Dashboard Components for Accountants

Example 2: Data Entry Form Design

Best Practice: Minimize manual input and use validation rules to reduce errors.

Example:

- Auto-fill vendor details when vendor ID is entered.

- Drop-down menus for account codes to avoid typos.

- Real-time validation for date formats and amounts.

Why it works: Streamlines data entry and ensures data integrity.

Mind Map: Data Entry Form Features

Example 3: Report Generation Interface

Best Practice: Allow users to customize reports with filters and export options.

Example:

- A report interface where accountants can select date ranges, departments, and account types.

- Preview pane to view report before export.

- Export options including PDF, Excel, and CSV.

Why it works: Provides flexibility and supports diverse reporting needs.

Mind Map: Report Interface Features

Additional Tips for UI Design

- Use Familiar Terminology: Use accounting and finance terms familiar to users to reduce learning curves.

- Provide Keyboard Shortcuts: Accountants often prefer keyboard navigation for speed.

- Include Audit Trails: Display change history clearly to support compliance.

- Offer Contextual Help: Tooltips and help icons assist users without cluttering the interface.

Summary

Designing user interfaces for accountants and finance professionals is about balancing complexity with usability. By focusing on clarity, automation, and customization, financial systems can empower users to perform their tasks efficiently and accurately.

4.4 Integration with Existing IT Infrastructure: Best Practices and Pitfalls

Integrating a new financial system with an organization’s existing IT infrastructure is a critical step that can determine the overall success of the implementation. Proper integration ensures seamless data flow, reduces manual intervention, and enhances operational efficiency. However, it also presents challenges such as compatibility issues, data inconsistencies, and security risks.

Best Practices for Integration

-

Conduct a Thorough IT Infrastructure Assessment

- Understand existing hardware, software, network architecture, and security protocols.

- Identify legacy systems that need to interface with the new financial system.

-

Define Clear Integration Objectives and Scope

- Determine which systems require integration (e.g., ERP, CRM, payroll, tax software).

- Set measurable goals such as real-time data synchronization or batch processing.

-

Choose the Right Integration Approach

- Point-to-Point Integration: Direct connections between systems; simple but can become complex with scale.

- Middleware/Enterprise Service Bus (ESB): Acts as a central hub to manage communication; scalable and flexible.

- API-Based Integration: Using RESTful or SOAP APIs for modular and secure data exchange.

-

Ensure Data Consistency and Integrity

- Establish data mapping and transformation rules.

- Implement validation checks to prevent corrupt or incomplete data transfer.

-

Prioritize Security and Compliance

- Use encryption for data in transit and at rest.

- Implement role-based access controls and audit trails.

-

Test Integration Thoroughly

- Perform unit, system, and end-to-end integration testing.

- Include real-world scenarios and edge cases.

-

Plan for Scalability and Maintenance

- Design integration to accommodate future system upgrades and expansions.

- Document integration architecture and processes for ongoing support.

Common Pitfalls to Avoid

- Underestimating Complexity: Assuming integration is straightforward can lead to overlooked dependencies.

- Ignoring Legacy System Limitations: Older systems may lack modern interfaces, requiring custom adapters.

- Poor Communication Between Teams: Lack of collaboration between IT and finance teams can cause misaligned expectations.

- Inadequate Testing: Skipping thorough testing increases risk of failures post-deployment.

- Neglecting Security: Weak security measures can expose sensitive financial data.

Mind Map: Integration Planning and Execution

Mind Map: Common Pitfalls in Integration

Practical Example: Integrating a Cloud-Based Financial System with On-Premise ERP

Scenario: A mid-sized manufacturing company is implementing a cloud-based financial system that must integrate with their existing on-premise ERP system for inventory and procurement.

Approach:

- The IT team conducts a detailed assessment of the ERP system’s integration capabilities.

- They decide to use an API-based integration approach, leveraging RESTful APIs exposed by the ERP.

- Middleware is introduced to handle data transformation and orchestration between systems.

- Data mapping is established to align financial transactions with inventory movements.

- Security protocols include VPN tunnels and OAuth 2.0 for API authentication.

- Extensive testing is performed, including simulated procurement cycles.

Outcome:

- Real-time synchronization of purchase orders and invoices.

- Reduced manual data entry errors.

- Improved financial reporting accuracy.

Practical Example: Pitfall Avoidance in Integration

Scenario: An accounting firm integrates a new financial reporting tool with their legacy tax software.

Challenge: The legacy system only supports batch data exports in a proprietary format.

Solution:

- The project team develops a custom adapter to convert batch exports into a format compatible with the new system.

- They schedule nightly batch transfers to minimize disruption.

- Regular communication between IT and accounting teams ensures alignment.

- Comprehensive testing uncovers data mismatches early.

Lesson Learned: Understanding legacy system constraints upfront and fostering cross-team collaboration prevented costly delays and data errors.

By following these best practices and learning from real-world examples, accountants and IT project managers can navigate the complexities of integrating financial systems with existing IT infrastructure, ensuring a smooth, secure, and efficient implementation.

4.5 Case Study: Customizing a Financial System for a Mid-Sized Enterprise

Background

A mid-sized enterprise in the manufacturing sector, “ABC Manufacturing,” decided to implement a new financial system to replace their legacy software. Their goal was to improve financial reporting accuracy, streamline accounts payable and receivable, and integrate with their existing inventory management system.

Objectives

- Enhance financial reporting capabilities with customizable dashboards.

- Automate invoice processing to reduce manual errors.

- Integrate financial data with inventory and sales systems.

- Ensure compliance with industry-specific tax regulations.

Mind Map: Key Customization Areas

Step 1: Requirement Gathering and Analysis

The project team conducted workshops with accountants and IT staff to identify pain points and desired features.

Example: Accountants requested a dashboard showing real-time cash flow and overdue invoices to prioritize collections.

Step 2: Customizing Reporting Modules

The system’s reporting module was customized to include:

- Drag-and-drop dashboard builder.

- Pre-built widgets for cash flow, profit & loss, and balance sheets.

Example: A custom widget was created to highlight invoices overdue by more than 30 days, enabling proactive follow-up.

Mind Map: Reporting Customization Workflow

Step 3: Automating Invoice Processing

Automation was introduced to:

- Automatically capture invoice data using OCR (Optical Character Recognition).

- Route invoices for approval based on predefined thresholds.

Example: Invoices under $5,000 were auto-approved, while higher amounts required manager sign-off.

Mind Map: Invoice Automation Process

Step 4: Integration with Inventory and Sales Systems

The financial system was integrated via APIs to sync:

- Inventory valuations for accurate cost of goods sold (COGS).

- Sales data to update revenue figures in real-time.

Example: When a sale was recorded in the sales system, the financial system automatically updated revenue and adjusted inventory levels.

Step 5: Ensuring Compliance

Customization included configuring tax rules specific to the manufacturing sector and enabling audit trails for all financial transactions.

Example: The system flagged transactions that required additional documentation for tax audits.

Results and Benefits

- Reduced month-end closing time by 30% due to automated processes.

- Improved accuracy of financial reports with real-time data.

- Enhanced collaboration between finance and operations through integrated systems.

- Strengthened compliance posture with built-in audit capabilities.

Summary Mind Map: Customization Impact

This case study illustrates how thoughtful customization tailored to the specific needs of a mid-sized enterprise can significantly enhance the value derived from a financial system implementation. By involving both accountants and IT project managers throughout the process, ABC Manufacturing achieved a solution that was both technically robust and aligned with business goals.

5. Data Migration and Management

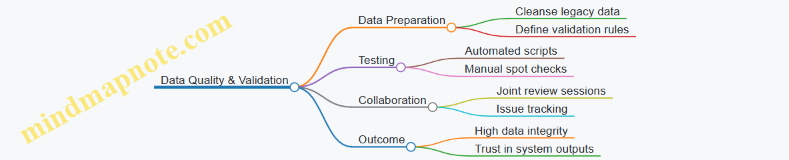

5.1 Assessing Data Quality and Readiness for Migration

Implementing a new financial system often hinges on the quality and readiness of the data being migrated. Poor data quality can lead to inaccurate financial reporting, compliance issues, and operational disruptions. Therefore, a thorough assessment of data quality and readiness is a critical first step in the migration process.

Key Dimensions of Data Quality

To assess data quality effectively, focus on the following dimensions:

- Accuracy: Is the data correct and free from errors?

- Completeness: Are all required data fields populated?

- Consistency: Does data align across different systems and datasets?

- Timeliness: Is the data up-to-date and relevant?

- Validity: Does the data conform to defined formats and business rules?

- Uniqueness: Are there duplicate records that need to be resolved?

Mind Map: Data Quality Dimensions

Steps to Assess Data Quality and Readiness

-

Data Profiling

- Use automated tools to scan datasets for anomalies, missing values, and inconsistencies.

- Example: Running SQL queries to identify null values in critical financial fields like invoice amounts or account codes.

-

Data Cleansing

- Correct or remove inaccurate, incomplete, or irrelevant data.

- Example: Standardizing date formats from MM/DD/YYYY to ISO 8601 (YYYY-MM-DD) to ensure compatibility.

-

Data Validation Against Business Rules

- Verify data adheres to financial policies and regulatory requirements.

- Example: Ensuring all transactions have valid GL account codes as per the chart of accounts.

-

Stakeholder Review

- Engage accountants and finance managers to validate data relevance and accuracy.

- Example: Cross-checking vendor master data with procurement teams to confirm active vendors.

-

Readiness Checklist

- Confirm data is complete, cleansed, and validated.

- Ensure backups and rollback plans are in place.

Mind Map: Data Quality Assessment Process

Example Scenario: Assessing Data Quality for Invoice Migration

A mid-sized company is migrating its invoice data to a new cloud-based financial system. During data profiling, the project team discovers:

- 5% of invoices have missing customer IDs.

- Several invoice dates are in the future, which is invalid.

- Duplicate invoice numbers exist due to legacy system errors.

Actions Taken:

- Missing customer IDs are flagged for manual review by the finance team.

- Future dates are corrected after verifying transaction dates with source documents.

- Duplicate invoices are consolidated or removed based on transaction history.

This process ensures that only accurate and reliable invoice data is migrated, reducing post-migration reconciliation efforts.

Tips for Accountants and IT Project Managers

- Collaborate early: Accountants provide domain knowledge essential for identifying data anomalies.

- Use specialized data profiling tools like Talend, Informatica, or open-source options.

- Document all data quality issues and resolutions to maintain transparency.

- Plan for iterative cleansing cycles; data quality improvement is rarely a one-time activity.

Summary

Assessing data quality and readiness is foundational to a successful financial systems implementation. By systematically profiling, cleansing, validating, and reviewing data, organizations can mitigate risks, ensure compliance, and enable smooth migration. Incorporating cross-functional collaboration and leveraging appropriate tools enhances the accuracy and reliability of the migrated data.

5.2 Developing a Data Migration Strategy: Step-by-Step Approach

Data migration is a critical phase in financial systems implementation, ensuring that valuable financial data moves accurately and securely from legacy systems to the new platform. A well-crafted data migration strategy minimizes risks, reduces downtime, and ensures data integrity.

Step 1: Assess and Analyze Source Data

- Inventory Data Sources: Identify all systems and databases containing financial data.

- Data Profiling: Evaluate data quality, completeness, and consistency.

- Identify Sensitive Data: Pinpoint personally identifiable information (PII) and confidential financial records.

Example: A mid-sized accounting firm discovered duplicate customer records and inconsistent invoice formats during data profiling, which informed their cleansing plan.

Step 2: Define Migration Scope and Objectives

- Determine Data to Migrate: Decide which data sets are essential for the new system.

- Set Success Criteria: Define what successful migration looks like (e.g., zero data loss, minimal downtime).

- Plan for Archival: Decide what legacy data will be archived rather than migrated.

Example: An IT project manager prioritized migrating current fiscal year transactions and archived older records to reduce system load.

Step 3: Design the Migration Approach

- Choose Migration Method: Options include Big Bang (all at once) or Phased (incremental).

- Select Tools and Technologies: ETL tools, custom scripts, or vendor-provided utilities.

- Plan for Data Transformation: Map source data formats to target system requirements.

Example: A financial institution used a phased migration approach with ETL tools to gradually move data, minimizing operational disruption.

Step 4: Develop a Detailed Migration Plan

- Create Timeline and Milestones: Schedule extraction, transformation, loading, and validation phases.

- Assign Roles and Responsibilities: Define who handles data extraction, validation, and issue resolution.

- Risk Management: Identify potential risks and mitigation strategies.

Example: The project team scheduled weekend migration windows to avoid impacting daily financial operations.

Step 5: Execute Data Migration

- Extract Data: Pull data from legacy systems.

- Transform Data: Cleanse, normalize, and format data as per target system.

- Load Data: Import data into the new financial system.

- Monitor Progress: Track migration status and log issues.