Financial Compliance for Accountants

1. Introduction to Financial Compliance

1.1 Understanding Financial Compliance: Definition and Importance

Financial compliance refers to the adherence to laws, regulations, guidelines, and specifications relevant to financial activities and reporting. For accountants, compliance ensures that financial records are accurate, transparent, and meet the standards set by regulatory bodies.

What is Financial Compliance?

- Definition: The process of conforming to external regulatory requirements and internal policies related to financial management.

- Scope: Includes financial reporting, tax filings, anti-money laundering (AML), fraud prevention, and data protection.

Why is Financial Compliance Important?

- Legal Obligations: Avoid penalties, fines, or legal action.

- Reputation Management: Builds trust with investors, clients, and regulators.

- Operational Efficiency: Streamlines financial processes and reduces risks.

- Financial Accuracy: Ensures reliable and truthful financial statements.

Mind Map: Core Components of Financial Compliance

Example 1: Compliance in Action - Timely Tax Filing

Scenario: An accountant at a mid-sized firm ensures all tax returns are filed before the deadline.

Best Practice: Using a compliance calendar and automated reminders to avoid late submissions.

Outcome: The firm avoids penalties and maintains a good standing with tax authorities.

Mind Map: Importance of Financial Compliance

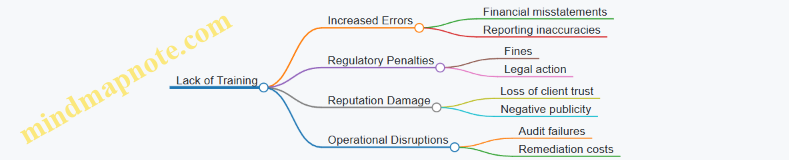

Example 2: Consequences of Non-Compliance

Scenario: A company fails to comply with AML regulations, resulting in a regulatory investigation.

Impact: Heavy fines, reputational damage, and operational disruptions.

Lesson: Proactive compliance monitoring and employee training are essential.

Summary

Financial compliance is a foundational pillar for accountants, ensuring that financial activities are lawful, ethical, and transparent. Understanding its definition and importance helps accountants implement best practices that protect their organizations from risks and build long-term trust.

For accountants and compliance officers, mastering financial compliance is not just about meeting requirements but fostering a culture of integrity and accountability.

1.2 Regulatory Bodies and Frameworks: An Overview

Financial compliance is governed by a complex network of regulatory bodies and frameworks designed to ensure transparency, accountability, and integrity within financial markets. For accountants, understanding these entities and their requirements is critical to maintaining compliance and avoiding penalties.

Key Regulatory Bodies

Below is a mind map illustrating some of the primary regulatory bodies that influence financial compliance globally:

Example: An accountant working for a multinational corporation must comply with SEC regulations if the company is listed on a US stock exchange, while also adhering to IASB standards for international financial reporting.

Important Regulatory Frameworks

These frameworks provide the rules and guidelines that accountants must follow:

Example: Under SOX, accountants must ensure internal controls over financial reporting are robust and documented, reducing the risk of fraud.

Mind Map: Relationship Between Regulatory Bodies and Frameworks

Practical Example: Navigating Multiple Jurisdictions

Consider an accountant at a European subsidiary of a US-based company. They must:

- Prepare financial statements according to IFRS (European requirement).

- Ensure compliance with the Sarbanes-Oxley Act for the parent company’s SEC filings.

- Follow GDPR guidelines when handling customer data.

This scenario illustrates the importance of understanding how regulatory bodies and frameworks intersect and impact daily accounting tasks.

Summary

Understanding regulatory bodies and frameworks is foundational for accountants to:

- Identify which rules apply to their organization.

- Implement appropriate internal controls.

- Prepare accurate and compliant financial reports.

- Mitigate risks related to non-compliance.

By integrating knowledge of these entities into their workflows, accountants can proactively manage compliance and support organizational integrity.

1.3 The Role of Accountants in Ensuring Compliance

Accountants play a pivotal role in ensuring financial compliance within organizations. Their responsibilities extend beyond traditional bookkeeping and financial reporting to include safeguarding the organization against regulatory risks and fostering a culture of transparency and accountability.

Key Responsibilities of Accountants in Compliance

- Accurate Financial Reporting: Ensuring all financial statements are prepared in accordance with applicable laws and standards.

- Internal Controls Implementation: Designing and monitoring controls to prevent errors and fraud.

- Regulatory Monitoring: Staying updated with changes in financial regulations and adapting processes accordingly.

- Risk Assessment: Identifying compliance risks and recommending mitigation strategies.

- Documentation and Record-Keeping: Maintaining thorough records to support audits and investigations.

- Ethical Conduct: Upholding integrity and ethical standards in all financial dealings.

Mind Map: Core Roles of Accountants in Financial Compliance

Practical Example 1: Ensuring Accurate Reporting

Scenario: An accountant at a mid-sized company notices discrepancies in the revenue recognition timing compared to the contract terms.

Action: The accountant reviews the contracts, consults the relevant accounting standards (e.g., IFRS 15), and adjusts the revenue recognition schedule accordingly.

Outcome: This proactive approach ensures compliance with revenue recognition rules, avoiding potential regulatory penalties and maintaining stakeholder trust.

Mind Map: Steps to Ensure Accurate Financial Reporting

Practical Example 2: Implementing Internal Controls

Scenario: An accountant identifies that the same person is responsible for both approving payments and reconciling bank statements.

Action: The accountant recommends segregation of duties by assigning reconciliation to a different team member and implements a dual-approval process for payments.

Outcome: This reduces the risk of fraud and errors, strengthening the organization’s internal control environment.

Mind Map: Internal Controls Best Practices

Practical Example 3: Staying Updated with Regulatory Changes

Scenario: New AML regulations require enhanced customer due diligence.

Action: The accountant attends training sessions, updates the compliance checklist, and works with the compliance team to integrate new procedures.

Outcome: The company remains compliant with AML laws, reducing the risk of fines and reputational damage.

Mind Map: Regulatory Monitoring Process

Summary

Accountants serve as the frontline defenders of financial compliance. Through accurate reporting, robust internal controls, continuous regulatory monitoring, and ethical conduct, they help organizations navigate complex regulatory landscapes effectively. Embedding these practices into daily workflows not only ensures compliance but also builds trust with stakeholders and regulators alike.

1.4 Common Compliance Challenges Faced by Accountants

Financial compliance is a critical aspect of an accountant’s role, but it comes with a variety of challenges that can complicate adherence to regulations. Understanding these challenges helps accountants proactively address potential issues and maintain robust compliance frameworks.

Mind Map: Common Compliance Challenges

Regulatory Complexity

Accountants often face the challenge of navigating a labyrinth of regulations that vary by jurisdiction, industry, and organizational size. For example, a multinational company must comply with both local tax laws and international standards like IFRS or SOX.

Example: A mid-sized firm struggled to keep up with quarterly updates to tax codes. This led to late filings and penalties. By subscribing to a regulatory update service and assigning a compliance officer, they improved their adherence and avoided fines.

Data Management

Maintaining accurate and complete financial data is fundamental but challenging. Errors in data entry or incomplete documentation can lead to compliance breaches.

Example: An accountant manually entered expense reports without verification, resulting in duplicate reimbursements. Implementing automated expense management software with validation rules helped eliminate these errors.

Internal Controls

Weak internal controls can expose organizations to fraud and non-compliance. Accountants must ensure proper segregation of duties and regular control testing.

Example: In a small firm, the same person was responsible for both approving and processing payments, increasing fraud risk. Introducing a dual-approval process reduced this risk significantly.

Technology Limitations

Outdated or incompatible financial systems can hinder compliance efforts, especially when regulatory reporting requires specific formats or real-time data.

Example: A company relied on legacy accounting software that could not generate reports compliant with new SOX requirements. Upgrading to a cloud-based solution with built-in compliance features streamlined reporting.

Human Factors

Lack of training and ethical challenges can cause inadvertent or intentional compliance violations.

Example: An accountant unaware of recent AML regulations failed to flag suspicious transactions. Regular training sessions and clear ethical guidelines helped raise awareness and reduce risks.

Communication Gaps

Poor communication between departments or with external auditors can lead to misunderstandings and compliance failures.

Example: Finance and legal teams worked in silos, causing delays in implementing new compliance policies. Establishing cross-functional compliance committees improved coordination and policy rollout.

Summary

Accountants face multifaceted compliance challenges ranging from regulatory complexity to human factors. Addressing these challenges requires a combination of updated knowledge, robust internal controls, effective technology use, and clear communication channels. Proactively managing these areas helps ensure sustained compliance and reduces organizational risk.

1.5 Case Study: Consequences of Non-Compliance in Financial Reporting

Financial reporting non-compliance can lead to severe consequences for organizations, accountants, and stakeholders. This section explores a detailed case study illustrating these impacts, supported by mind maps and practical examples to enhance understanding.

Case Study Overview: The XYZ Corporation Scandal

XYZ Corporation, a mid-sized publicly traded company, failed to comply with financial reporting standards by intentionally misstating revenue figures to appear more profitable. This non-compliance was uncovered during an external audit, leading to significant repercussions.

Mind Map: Consequences of Non-Compliance in Financial Reporting

Detailed Breakdown of Consequences

-

Legal Penalties

- XYZ Corporation was fined $10 million by the Securities and Exchange Commission (SEC) for violating the Sarbanes-Oxley Act.

- Several executives faced lawsuits for fraudulent reporting.

-

Financial Impact

- Following the scandal, XYZ’s stock price dropped by 40% within two weeks.

- Investors withdrew funding, and the company faced higher interest rates on loans.

-

Reputational Damage

- Media outlets extensively covered the scandal, damaging XYZ’s brand.

- Key clients reconsidered partnerships, affecting revenue streams.

-

Operational Disruptions

- The CFO and several accounting staff were replaced.

- The company had to allocate significant resources to overhaul compliance systems.

-

Personal Consequences for Accountants

- The lead accountant involved lost their CPA license.

- Several team members faced internal disciplinary actions.

Example: How Non-Compliance Occurred

- XYZ Corporation recognized revenue prematurely by recording sales before delivery.

- This inflated quarterly earnings, misleading stakeholders.

- The accounting team bypassed internal controls to conceal discrepancies.

Mind Map: Preventive Best Practices to Avoid Non-Compliance

Practical Example: Applying Best Practices

- XYZ Corporation, post-scandal, implemented a robust internal control system including automated revenue recognition software.

- They conducted quarterly training sessions for accountants on compliance and ethics.

- An anonymous whistleblower hotline was established, encouraging early detection of irregularities.

Summary

This case study highlights the critical importance of financial compliance. Non-compliance not only risks legal and financial penalties but also damages reputations and careers. Accountants play a pivotal role in upholding compliance through adherence to best practices, continuous education, and ethical vigilance.

2. Key Financial Regulations and Standards

2.1 Overview of Sarbanes-Oxley Act (SOX) Compliance

The Sarbanes-Oxley Act of 2002 (SOX) is a United States federal law enacted in response to major corporate and accounting scandals such as Enron and WorldCom. Its primary goal is to protect investors by improving the accuracy and reliability of corporate disclosures and financial statements.

Key Objectives of SOX

- Enhance corporate responsibility

- Increase financial disclosures

- Combat corporate and accounting fraud

Who Must Comply?

- Publicly traded companies in the U.S.

- Their wholly owned subsidiaries

- Accounting firms auditing these companies

Core Sections Relevant to Accountants

- Section 302: Corporate Responsibility for Financial Reports

- Section 404: Management Assessment of Internal Controls

- Section 906: Corporate Responsibility for Financial Reports (Criminal Penalties)

Mind Map: SOX Compliance Essentials

Best Practices for Accountants under SOX

-

Maintain Accurate Financial Records

- Example: Ensure all journal entries are supported by proper documentation to avoid misstatements.

-

Implement and Document Internal Controls

- Example: Use checklists to verify segregation of duties, such as separating authorization and payment functions.

-

Regular Testing of Controls

- Example: Conduct quarterly walkthroughs of key financial processes to identify control weaknesses early.

-

CEO and CFO Certification Preparation

- Example: Prepare detailed reports and evidence supporting the accuracy of financial statements for executive sign-off.

-

Coordinate with External Auditors

- Example: Provide timely access to documentation and respond promptly to audit inquiries.

Mind Map: Internal Controls under SOX Section 404

Example Scenario: Applying SOX Compliance in a Mid-Sized Company

Situation: A mid-sized publicly traded company is preparing for its annual SOX compliance audit.

Actions:

- The accounting team documents all financial processes and internal controls.

- They perform a risk assessment identifying areas prone to errors, such as revenue recognition.

- Quarterly testing is conducted on controls related to cash disbursements and payroll.

- The CFO reviews and certifies the financial statements with supporting evidence.

- External auditors are given full access to documentation and control test results.

Outcome: The company passes the SOX audit with minimal findings, demonstrating effective compliance.

Summary

SOX compliance is critical for maintaining investor confidence and ensuring the integrity of financial reporting. Accountants play a central role by establishing, documenting, and testing internal controls, preparing accurate financial reports, and facilitating audits. Understanding the key sections and best practices of SOX helps accountants navigate compliance efficiently and effectively.

2.2 Understanding Anti-Money Laundering (AML) Requirements

Anti-Money Laundering (AML) refers to a set of laws, regulations, and procedures intended to prevent criminals from disguising illegally obtained funds as legitimate income. For accountants, understanding AML requirements is critical to ensure compliance, detect suspicious activities, and protect the integrity of financial systems.

What is Money Laundering?

Money laundering is the process of making large amounts of money generated by a criminal activity, such as drug trafficking or terrorist funding, appear to have come from a legitimate source. The goal is to hide the illegal origin of the money.

Why AML Matters for Accountants

- Accountants often handle client funds and financial records, making them key players in identifying suspicious transactions.

- Regulatory bodies require firms to implement AML programs to detect and report money laundering activities.

- Failure to comply can result in severe penalties, reputational damage, and legal consequences.

Core Components of AML Requirements

Customer Due Diligence (CDD)

CDD is the process of verifying the identity of clients and assessing the risk they may pose.

- Know Your Customer (KYC): Collecting and verifying personal information such as name, address, and identification documents.

- Enhanced Due Diligence (EDD): Applied to higher-risk customers, such as politically exposed persons (PEPs) or clients from high-risk jurisdictions.

Example: An accountant onboarding a new corporate client must verify the beneficial owners of the company and understand the nature of the business to assess risks.

Monitoring and Reporting Suspicious Activities

Accountants should monitor transactions for unusual patterns that may indicate money laundering.

- Transaction Monitoring: Automated or manual review of transactions to detect anomalies.

- Suspicious Activity Reports (SARs): Reporting suspicious transactions to the relevant authorities.

Example: A client suddenly deposits a large sum inconsistent with their usual business activity. The accountant investigates and files a SAR if justified.

Record Keeping

Maintaining detailed records of transactions, customer identification, and due diligence efforts is essential.

- Records must be kept for a minimum period (typically 5-7 years).

- Documentation should be easily accessible for audits or investigations.

Example: An accountant ensures all client identification documents and transaction records are securely stored and retrievable.

AML Compliance Program

Organizations must establish a comprehensive AML compliance program that includes:

- Written policies and procedures

- Appointment of a compliance officer

- Regular training for staff

- Independent audits of the AML program

Example: A mid-sized accounting firm appoints a dedicated AML compliance officer and conducts quarterly training sessions for all employees.

Mind Map: AML Compliance Workflow

Practical Example: Applying AML in an Accounting Scenario

Scenario: An accountant is managing the accounts of a new client who operates an import-export business. During routine monitoring, the accountant notices multiple large cash deposits that do not align with the client’s declared business activities.

Steps Taken:

- Enhanced Due Diligence: The accountant requests additional documentation and clarifies the source of funds.

- Risk Assessment: Determines the client is from a jurisdiction with high money laundering risk.

- Transaction Monitoring: Flags the unusual deposits for further review.

- Reporting: Files a Suspicious Activity Report (SAR) with the financial intelligence unit as per regulatory requirements.

This example highlights how accountants integrate AML requirements into their daily work to detect and prevent illicit financial activities.

Summary

Understanding AML requirements is vital for accountants to:

- Identify and verify clients properly.

- Monitor and report suspicious transactions.

- Maintain thorough records.

- Implement and support an effective AML compliance program.

By embedding these practices into their workflows, accountants not only comply with legal obligations but also contribute to the global fight against financial crime.

2.3 Compliance with International Financial Reporting Standards (IFRS)

International Financial Reporting Standards (IFRS) are a set of accounting standards developed by the International Accounting Standards Board (IASB) that provide a global framework for how public companies prepare and disclose their financial statements. Compliance with IFRS ensures transparency, accountability, and efficiency in financial markets worldwide.

Why IFRS Compliance Matters for Accountants

- Global Consistency: Facilitates comparability of financial statements across international boundaries.

- Investor Confidence: Enhances trust among investors and stakeholders by ensuring reliable and transparent reporting.

- Regulatory Requirement: Many countries mandate IFRS compliance for listed companies.

Key Principles of IFRS

- Fair Presentation: Financial statements must faithfully represent the financial position, performance, and cash flows.

- Going Concern: Assumes the entity will continue its operations in the foreseeable future.

- Accrual Basis: Transactions are recorded when they occur, not when cash is received or paid.

- Materiality and Aggregation: Only material items are presented separately.

- Consistency: Presentation and classification should be consistent over time.

Mind Map: Core Components of IFRS Compliance

Practical Example: Revenue Recognition under IFRS 15

Scenario: A software company sells a subscription service bundled with installation and customer support.

IFRS 15 Approach:

- Identify the contract with the customer.

- Identify distinct performance obligations (subscription, installation, support).

- Determine the transaction price.

- Allocate the transaction price to each performance obligation.

- Recognize revenue when (or as) each performance obligation is satisfied.

Example:

- Subscription: Recognized over time as the service is delivered.

- Installation: Recognized at the point in time when installation is complete.

- Customer Support: Recognized over the support period.

This ensures revenue is recognized accurately and reflects the economic reality.

Mind Map: Steps for Applying IFRS 15 Revenue Recognition

Best Practices for Accountants to Ensure IFRS Compliance

- Stay Updated: Regularly review IASB updates and amendments.

- Detailed Documentation: Maintain thorough records of judgments and estimates.

- Training: Conduct ongoing training sessions on IFRS standards.

- Use Checklists: Implement IFRS compliance checklists during financial close.

- Leverage Technology: Use accounting software with IFRS modules.

Example: Transition from Local GAAP to IFRS

Company: A mid-sized manufacturing firm transitioning from local Generally Accepted Accounting Principles (GAAP) to IFRS.

Challenges:

- Differences in asset valuation methods.

- Recognition of leases under IFRS 16.

- Adjusting revenue recognition policies.

Approach:

- Conduct a gap analysis between local GAAP and IFRS.

- Train accounting staff on IFRS requirements.

- Restate prior period financials for comparability.

- Communicate changes to stakeholders.

Outcome:

- Improved financial statement transparency.

- Enhanced ability to attract foreign investment.

Mind Map: Transition Process from Local GAAP to IFRS

Summary

Compliance with IFRS is critical for accountants working in an increasingly globalized financial environment. By understanding the core principles, applying standards like IFRS 15 correctly, and following best practices during transitions, accountants can ensure accurate, transparent, and compliant financial reporting.

For further reading, refer to the official IFRS Foundation website and IASB publications.

2.4 The General Data Protection Regulation (GDPR) and Financial Data

The General Data Protection Regulation (GDPR) is a comprehensive data protection law enacted by the European Union (EU) that came into effect on May 25, 2018. It aims to protect the personal data and privacy of EU citizens and residents, impacting how organizations worldwide handle financial data.

Why GDPR Matters for Accountants

Accountants regularly process sensitive financial data that often includes personal information such as names, addresses, bank details, and transaction histories. GDPR compliance is essential to avoid hefty fines, reputational damage, and legal consequences.

Key GDPR Principles Relevant to Financial Data

- Data Minimization: Only collect data necessary for the specific financial purpose.

- Purpose Limitation: Use financial data only for the stated purpose.

- Accuracy: Keep financial data accurate and up to date.

- Storage Limitation: Retain data only as long as necessary.

- Integrity & Confidentiality: Protect data against unauthorized access and breaches.

- Lawfulness, Fairness & Transparency: Process data legally and inform data subjects about usage.

Practical Example: GDPR Compliance in Payroll Processing

Scenario: An accounting firm processes payroll for multiple clients across the EU.

- Data Minimization: Collect only employee names, tax IDs, bank account numbers, and salary details necessary for payroll.

- Purpose Limitation: Use this data solely for payroll and tax reporting.

- Transparency: Inform employees via privacy notices about how their data will be used.

- Security Measures: Encrypt payroll data and restrict access to authorized personnel.

- Data Retention: Retain payroll records for the legally required period, then securely delete.

Rights of Data Subjects Under GDPR

Accountants must be prepared to handle requests such as:

- Right to Access: Providing clients or employees with copies of their financial data.

- Right to Rectification: Correcting inaccurate financial records promptly.

- Right to Erasure: Deleting personal financial data when no longer necessary or upon request.

Example: Handling a Data Subject Access Request (DSAR)

Scenario: A client requests a copy of all their personal financial data held by the accounting firm.

Best Practice Steps:

- Verify the identity of the requester to prevent unauthorized disclosure.

- Compile all relevant financial data including invoices, statements, and correspondence.

- Provide the data in a clear, commonly used electronic format within the one-month timeframe.

- Document the request and response for audit purposes.

GDPR Compliance Best Practices for Accountants

- Conduct Data Audits: Regularly review what financial data is collected and processed.

- Implement Data Protection Policies: Define clear guidelines on data handling.

- Train Staff: Ensure all team members understand GDPR obligations.

- Encryption & Access Controls: Protect data both at rest and in transit.

- Maintain Records: Document data processing activities as required by GDPR.

- Incident Response Plans: Prepare for potential data breaches with clear procedures.

Example: Encryption in Financial Data Handling

An accounting firm uses encryption software to secure client financial files stored on cloud servers. Access is restricted via multi-factor authentication, ensuring only authorized accountants can view sensitive data. This practice aligns with GDPR’s integrity and confidentiality principle, reducing the risk of data breaches.

Summary

GDPR significantly impacts how accountants manage financial data, emphasizing data protection, transparency, and respect for individual rights. By integrating GDPR principles into daily financial processes, accountants not only comply with legal requirements but also build trust with clients and stakeholders.

For accountants, understanding and applying GDPR to financial data is not optional but a critical component of modern financial compliance.

2.5 Practical Example: Applying GAAP vs IFRS in Financial Statements

Understanding the differences between GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards) is crucial for accountants working in multinational environments or dealing with cross-border financial reporting. This section provides a practical example of how these two frameworks impact the preparation and presentation of financial statements.

Mind Map: Key Differences Between GAAP and IFRS

Practical Example Scenario

Company: ABC Manufacturing

Situation: ABC Manufacturing is preparing its annual financial statements. It operates in the United States but plans to expand to Europe, requiring IFRS-compliant reporting.

Focus Areas: Revenue recognition, inventory valuation, and development costs.

Revenue Recognition

- GAAP Approach: ABC recognizes revenue when all criteria under ASC 606 are met, including detailed guidance for specific industries.

- IFRS Approach: ABC applies IFRS 15, focusing on the transfer of control to the customer.

Example: ABC sells machinery with installation services.

| Aspect | GAAP Treatment | IFRS Treatment |

|---|---|---|

| Timing of Revenue | Recognize separately for machinery and installation | Recognize combined if services are not distinct |

| Measurement | Based on standalone selling price | Allocate transaction price based on relative standalones |

Mind Map:

Inventory Valuation

- GAAP: ABC uses LIFO method to value inventory, which can reduce taxable income during inflation.

- IFRS: LIFO is prohibited; ABC must use FIFO or weighted average.

Example: Inventory costing $100,000 under FIFO is $90,000 under LIFO.

| Aspect | GAAP Treatment | IFRS Treatment |

|---|---|---|

| Inventory Method | LIFO allowed | LIFO prohibited |

| Impact on Profit | Lower profit during inflation (LIFO) | Higher profit (FIFO or weighted average) |

Mind Map:

Development Costs

- GAAP: ABC expenses all development costs as incurred.

- IFRS: ABC capitalizes development costs if specific criteria (technical feasibility, intention to complete, ability to use or sell, etc.) are met.

Example: ABC incurs $500,000 in development costs.

| Aspect | GAAP Treatment | IFRS Treatment |

|---|---|---|

| Treatment of Costs | Expense immediately | Capitalize if criteria met |

| Impact on Financials | Lower assets, higher expenses | Higher assets, lower expenses initially |

Mind Map:

Summary Table: GAAP vs IFRS Impact on ABC Manufacturing

| Financial Statement Item | GAAP Treatment | IFRS Treatment | Impact on Financials |

|---|---|---|---|

| Revenue Recognition | Separate recognition | Combined recognition possible | Timing and amount of revenue recognized |

| Inventory Valuation | LIFO allowed | LIFO prohibited | Inventory value and profit margins differ |

| Development Costs | Expense immediately | Capitalize if criteria met | Asset base and expenses differ |

Conclusion

For accountants, understanding these differences is essential to ensure accurate and compliant financial reporting. When transitioning from GAAP to IFRS or vice versa, companies should carefully evaluate the impact on financial statements and communicate changes to stakeholders.

By applying these practical examples, accountants can better navigate the complexities of dual reporting frameworks and maintain compliance with relevant standards.

3. Internal Controls and Risk Management

3.1 Designing Effective Internal Controls for Financial Processes

Internal controls are the backbone of financial compliance, ensuring accuracy, reliability, and prevention of fraud or errors in financial processes. Designing effective internal controls requires a structured approach that aligns with organizational goals and regulatory requirements.

What Are Internal Controls?

Internal controls are policies, procedures, and activities implemented to safeguard assets, ensure financial data integrity, and promote operational efficiency.

Key Objectives of Internal Controls

- Accuracy: Ensure financial data is recorded correctly.

- Completeness: All transactions are captured.

- Authorization: Only approved transactions are processed.

- Compliance: Adherence to laws and regulations.

- Fraud Prevention: Detect and prevent unauthorized activities.

Mind Map: Core Components of Internal Controls

Designing Internal Controls: Step-by-Step Approach

-

Identify Key Financial Processes

- Examples: Accounts payable, payroll, revenue recognition.

-

Assess Risks in Each Process

- Example: Risk of duplicate payments in accounts payable.

-

Define Control Objectives

- Example: Prevent unauthorized disbursements.

-

Develop Control Activities

- Example: Require dual approval for payments over $5,000.

-

Assign Responsibilities

- Example: Accounts payable clerk prepares invoices; finance manager approves.

-

Implement Monitoring Mechanisms

- Example: Monthly reconciliation of bank statements.

-

Document Controls and Procedures

- Maintain clear manuals and workflows.

Mind Map: Example - Accounts Payable Controls

Example: Implementing Segregation of Duties

Scenario: In a small firm, the same person processes invoices and approves payments, increasing fraud risk.

Best Practice: Separate these duties so one employee processes invoices and another approves payments.

Result: Reduces risk of unauthorized payments and increases accountability.

Example: Automated Controls with Software

Using accounting software that automatically flags duplicate invoice numbers or mismatched purchase orders helps reduce manual errors and enforce control policies.

Tips for Effective Internal Controls

- Keep controls simple and practical.

- Regularly review and update controls.

- Train staff on control importance and procedures.

- Use technology to enhance control effectiveness.

By carefully designing internal controls tailored to your organization’s financial processes, accountants can significantly reduce risks and ensure compliance with regulatory standards.

3.2 Risk Assessment Techniques for Accountants

Risk assessment is a fundamental part of financial compliance, enabling accountants to identify, evaluate, and prioritize risks that could impact the accuracy, integrity, and legality of financial reporting and operations. Effective risk assessment helps prevent fraud, errors, and regulatory breaches.

Understanding Risk Assessment

Risk assessment involves systematically analyzing potential threats to financial processes and controls. For accountants, this means evaluating both internal and external risks that could affect compliance.

Key Risk Assessment Techniques

-

Risk Identification

- Recognize potential risks related to financial transactions, reporting, and controls.

- Example: Identifying risks of misstatement in revenue recognition.

-

Risk Analysis

- Determine the likelihood and impact of identified risks.

- Example: Assessing the probability of a data breach affecting financial data confidentiality.

-

Risk Evaluation

- Prioritize risks based on their severity and likelihood.

- Example: Prioritizing risks related to cash handling over minor documentation errors.

-

Risk Mitigation Planning

- Develop strategies to manage or reduce risks.

- Example: Implementing dual authorization for payments to reduce fraud risk.

Mind Map: Risk Assessment Process

Common Risk Assessment Techniques for Accountants

Checklists

- Use standardized checklists to ensure all common risk areas are reviewed.

- Example: A checklist covering revenue recognition, expense recording, and asset valuation.

Interviews and Questionnaires

- Engage with staff and management to identify potential risks.

- Example: Interviewing accounts payable staff to uncover risks in invoice processing.

Process Mapping

- Visualize financial processes to identify control gaps and risk points.

- Example: Mapping the procurement-to-payment cycle to spot where fraud could occur.

Data Analytics

- Analyze financial data patterns to detect anomalies or unusual transactions.

- Example: Using software to flag duplicate payments or unusual vendor activity.

Scenario Analysis

- Evaluate how different scenarios could impact financial compliance.

- Example: Assessing the impact of a sudden regulatory change on reporting timelines.

Mind Map: Risk Assessment Techniques

Practical Example: Risk Assessment in Accounts Receivable

Step 1: Identify Risks

- Risk of unrecorded sales

- Risk of incorrect customer credit limits

- Risk of delayed collections impacting cash flow

Step 2: Analyze Risks

- Unrecorded sales: Likelihood - Medium; Impact - High

- Incorrect credit limits: Likelihood - Low; Impact - Medium

- Delayed collections: Likelihood - High; Impact - High

Step 3: Evaluate and Prioritize

- Focus on delayed collections and unrecorded sales as top risks.

Step 4: Mitigate Risks

- Implement automated sales recording systems.

- Regularly review and update customer credit policies.

- Set up alerts for overdue accounts.

Mind Map: Example - Accounts Receivable Risk Assessment

Best Practices for Accountants Conducting Risk Assessments

- Regular Updates: Risk assessments should be updated periodically to reflect changes in business or regulatory environment.

- Documentation: Maintain clear documentation of risk assessment processes and findings.

- Collaboration: Work closely with compliance officers, auditors, and other stakeholders.

- Use Technology: Leverage risk management software and data analytics tools.

- Training: Ensure all accounting staff understand risk factors and their role in mitigation.

By integrating these risk assessment techniques into daily accounting practices, accountants can proactively manage compliance risks, safeguard financial integrity, and support organizational governance.

3.3 Best Practices for Segregation of Duties

Segregation of Duties (SoD) is a fundamental internal control designed to prevent errors and fraud by dividing responsibilities among different individuals. This practice ensures that no single person has control over all aspects of any critical financial transaction.

Why Segregation of Duties Matters

- Risk Reduction: Minimizes the risk of intentional fraud or unintentional errors.

- Checks and Balances: Creates a system of checks and balances within financial processes.

- Accountability: Enhances accountability by clearly defining roles.

Core Principles of Segregation of Duties

- Authorization of transactions

- Custody of assets

- Recording and reconciliation of transactions

Mind Map: Key Components of Segregation of Duties

Best Practices for Implementing Segregation of Duties

-

Define Clear Roles and Responsibilities

- Assign specific tasks to individuals based on their job descriptions.

- Avoid overlapping duties that could compromise control.

-

Implement Role-Based Access Controls (RBAC)

- Use software systems to restrict access based on roles.

- Regularly review and update access permissions.

-

Rotate Duties Periodically

- Rotate employees in sensitive roles to reduce risk of collusion.

- Example: Rotate the person responsible for bank reconciliations every 6 months.

-

Use Compensating Controls When Segregation Isn’t Possible

- Introduce additional reviews or approvals.

- Example: If one person handles both recording and custody, require a supervisor to review transactions.

-

Regular Monitoring and Auditing

- Conduct periodic audits to ensure SoD policies are followed.

- Use exception reports to detect violations.

Mind Map: Best Practices Workflow

Practical Examples

Example 1: Payroll Processing

- Scenario: One employee processes payroll, another authorizes payments, and a third reconciles payroll accounts.

- Benefit: Prevents any single employee from manipulating payroll for personal gain.

Example 2: Vendor Payments

- Scenario: Employee A creates vendor records, Employee B approves invoices, Employee C processes payments.

- Benefit: Reduces risk of fraudulent vendors or unauthorized payments.

Example 3: Cash Handling in Retail

- Scenario: Cashiers collect payments, supervisors perform cash counts, and accountants record transactions.

- Benefit: Ensures cash is properly accounted for and discrepancies are detected early.

Summary

Segregation of Duties is a critical control that protects organizations from fraud and errors. By clearly defining roles, implementing access controls, rotating duties, applying compensating controls, and continuously monitoring compliance, accountants can uphold the integrity of financial processes and contribute to a robust compliance environment.

3.4 Monitoring and Testing Controls: Practical Approaches

Effective monitoring and testing of internal controls are critical components of a robust financial compliance program. These activities ensure that controls are functioning as intended, risks are mitigated, and any weaknesses are identified and addressed promptly.

Key Objectives of Monitoring and Testing Controls

- Verify the effectiveness of internal controls

- Detect control failures or weaknesses early

- Ensure compliance with regulatory requirements

- Support continuous improvement of control processes

Practical Approaches to Monitoring Controls

-

Ongoing Monitoring

- Continuous supervision embedded in daily operations

- Examples: Automated system alerts, exception reports

-

Separate Evaluations

- Periodic independent assessments (internal audit, compliance teams)

- Examples: Quarterly control reviews, surprise audits

-

Use of Technology

- Leverage software tools for real-time monitoring and data analytics

- Examples: ERP system dashboards, compliance management software

Mind Map: Monitoring Controls

Practical Approaches to Testing Controls

-

Design Effectiveness Testing

- Assess whether controls are properly designed to mitigate risks

- Example: Reviewing control documentation and process flowcharts

-

Operating Effectiveness Testing

- Verify if controls are operating as intended over a period

- Example: Sampling transactions to check approval signatures

-

Walkthroughs

- Trace a transaction through the system to observe control points

- Example: Following an invoice from receipt to payment

-

Data Analytics and Sampling

- Use statistical sampling or full population testing where feasible

- Example: Using software to identify duplicate payments

Mind Map: Testing Controls

Examples of Monitoring and Testing Controls

Example 1: Monitoring Segregation of Duties (SoD)

- Scenario: An accounting firm wants to ensure no single employee can both initiate and approve payments.

- Monitoring Approach: Use system-generated SoD conflict reports monthly.

- Testing Approach: Sample payment transactions quarterly to verify approval signatures are from authorized personnel.

Example 2: Testing Expense Reimbursement Controls

- Scenario: Company policy requires receipts for all employee expense claims.

- Monitoring Approach: Automated flagging of claims without attached receipts.

- Testing Approach: Periodic audit of expense reports to ensure compliance with documentation requirements.

Example 3: Monitoring Journal Entry Controls

- Scenario: To prevent fraudulent adjustments, all journal entries above a threshold require dual approval.

- Monitoring Approach: Real-time alerts for entries exceeding the threshold.

- Testing Approach: Walkthrough of journal entry process and sampling of entries to confirm approvals.

Best Practices for Effective Monitoring and Testing

- Establish clear control objectives and criteria

- Use a risk-based approach to prioritize controls

- Document all monitoring and testing activities thoroughly

- Communicate findings promptly to relevant stakeholders

- Integrate feedback loops for continuous control improvement

By systematically monitoring and testing controls using these practical approaches, accountants can proactively manage compliance risks and strengthen their organization’s financial integrity.

3.5 Example: Implementing a Fraud Prevention Control System

Implementing a fraud prevention control system is a critical step for accountants to safeguard financial integrity and ensure compliance. This example will walk through the key components, best practices, and practical steps to develop and maintain an effective fraud prevention system.

Step 1: Risk Assessment and Identification

- Identify areas vulnerable to fraud (e.g., cash handling, procurement, payroll).

- Evaluate historical data and past incidents.

- Engage stakeholders to understand potential risks.

Mind Map: Fraud Risk Assessment

Example: A mid-sized company discovered through risk assessment that expense reimbursements were frequently manipulated due to lack of verification.

Step 2: Designing Internal Controls

- Segregation of duties to prevent conflicts of interest.

- Authorization and approval workflows.

- Regular reconciliations and verifications.

- Access controls and system permissions.

Mind Map: Internal Controls for Fraud Prevention

Example: Implementing a policy where no single employee can both create and approve vendor payments.

Step 3: Monitoring and Detection Mechanisms

- Use of data analytics to identify anomalies.

- Continuous transaction monitoring.

- Exception reporting.

- Surprise audits and spot checks.

Mind Map: Monitoring and Detection

Example: Using software to flag duplicate invoice numbers or payments exceeding predefined thresholds.

Step 4: Reporting and Whistleblower Policies

- Establish confidential reporting channels.

- Protect whistleblowers from retaliation.

- Encourage ethical behavior through training.

Mind Map: Reporting Mechanisms

Example: A company sets up an anonymous hotline where employees can report suspicious activities without fear.

Step 5: Response and Remediation

- Investigate reported incidents promptly.

- Document findings and corrective actions.

- Update controls based on lessons learned.

Mind Map: Response and Remediation

Example: After detecting a fraudulent reimbursement, the company revised its approval process and conducted refresher training.

Summary Table: Fraud Prevention Control System Components

| Component | Description | Practical Example |

|---|---|---|

| Risk Assessment | Identifying fraud-prone areas | Expense reimbursement vulnerabilities identified |

| Internal Controls | Segregation of duties, approvals | Separate employees for payment creation and approval |

| Monitoring & Detection | Data analytics, audits | Software flags duplicate invoices |

| Reporting Mechanisms | Whistleblower policies, confidential channels | Anonymous hotline for fraud reporting |

| Response & Remediation | Investigation and corrective actions | Revising approval workflows after fraud detection |

By integrating these components into a cohesive fraud prevention control system, accountants can proactively mitigate risks, ensure compliance, and protect organizational assets effectively.

4. Financial Reporting and Documentation

4.1 Accurate Record-Keeping and Documentation Standards

Accurate record-keeping and documentation are foundational pillars of financial compliance. For accountants, maintaining precise, timely, and well-organized records not only ensures adherence to regulatory requirements but also supports transparency, audit readiness, and effective decision-making.

Why Accurate Record-Keeping Matters

- Regulatory Compliance: Many regulations, such as SOX, IFRS, and AML, mandate detailed documentation to verify transactions and controls.

- Audit Preparedness: Well-maintained records simplify internal and external audits, reducing risks of penalties or reputational damage.

- Financial Integrity: Accurate records help prevent errors, fraud, and misstatements in financial reporting.

- Operational Efficiency: Organized documentation facilitates smoother workflows and quicker retrieval of information.

Key Principles of Record-Keeping

- Completeness: Every financial transaction must be fully recorded without omissions.

- Accuracy: Data entered must reflect the true nature and value of transactions.

- Timeliness: Records should be updated promptly to reflect current financial status.

- Consistency: Use standardized formats and procedures across all documentation.

- Security: Protect records from unauthorized access or tampering.

- Retention: Follow legal and regulatory guidelines on how long to keep records.

Mind Map: Core Components of Accurate Record-Keeping

Best Practices for Documentation Standards

-

Use Standardized Templates and Formats

- Example: Implement a uniform invoice template that captures all required fields such as date, amount, vendor details, and approval signatures.

-

Maintain Supporting Documentation

- Attach receipts, contracts, and correspondence to each transaction record.

- Example: For a purchase transaction, keep the purchase order, vendor invoice, and payment confirmation together.

-

Implement a Document Management System (DMS)

- Digitize records to improve accessibility and reduce physical storage risks.

- Example: Use cloud-based DMS with version control and audit trails.

-

Regular Reconciliation and Review

- Schedule periodic checks to compare ledger entries with bank statements and other source documents.

- Example: Monthly bank reconciliations to detect discrepancies early.

-

Ensure Proper Authorization and Approval

- Record who authorized transactions and when.

- Example: Use electronic approval workflows that log approver identity and timestamp.

-

Train Staff on Documentation Protocols

- Conduct regular training sessions emphasizing the importance of accuracy and compliance.

Mind Map: Best Practices Workflow

Practical Examples

Example 1: Handling Expense Reports

- An accountant receives an expense report from a team member.

- They verify the report against receipts and company policy.

- The accountant uses a standardized form ensuring all necessary fields are completed.

- The report is digitally stored in the DMS with scanned receipts attached.

- Approval is logged electronically before reimbursement is processed.

Example 2: Correcting a Data Entry Error

- During a monthly review, an accountant notices a payment recorded twice.

- They trace the error to manual entry and document the correction with a clear explanation.

- The correction is authorized by a supervisor and logged in the system.

- This transparent documentation prevents audit issues and maintains data integrity.

Example 3: Retention Compliance

- A firm follows a policy to retain financial records for 7 years.

- The accountant uses automated alerts to review and archive or securely delete records after this period.

- This ensures compliance with tax and regulatory requirements.

Summary

Accurate record-keeping and documentation standards are critical for financial compliance. By adhering to principles of completeness, accuracy, timeliness, consistency, security, and retention, accountants can safeguard their organizations against compliance risks. Leveraging standardized templates, technology, and regular training further strengthens these efforts, ensuring that financial records are reliable, auditable, and compliant with regulatory demands.

4.2 Preparing Compliant Financial Statements: Step-by-Step

Preparing financial statements that comply with regulatory standards is a critical responsibility for accountants. This process ensures transparency, accuracy, and trustworthiness in financial reporting. Below is a detailed step-by-step guide, complemented by mind maps and practical examples to illustrate best practices.

Step 1: Understand Applicable Financial Reporting Standards

Before preparing financial statements, identify the relevant accounting framework (e.g., GAAP, IFRS) based on your jurisdiction and the organization’s requirements.

Mind Map: Understanding Reporting Standards

Example: A US-based company listed on the NYSE must prepare statements according to US GAAP, while a multinational may need to use IFRS for consolidated reports.

Step 2: Collect and Verify Source Data

Gather all financial transactions, invoices, bank statements, and other relevant documents. Verify their accuracy and completeness.

Mind Map: Data Collection & Verification

Example: An accountant cross-checks the sales invoices against bank deposits to ensure all revenue is recorded.

Step 3: Record Transactions Accurately

Enter transactions into the accounting system using the correct accounts, ensuring proper classification (assets, liabilities, equity, income, expenses).

Mind Map: Recording Transactions

Example: A payment for office supplies is recorded as an expense under ‘Office Supplies’ rather than as an asset.

Step 4: Adjust Entries and Reconcile Accounts

Make necessary adjustments such as accruals, deferrals, depreciation, and reconcile accounts to reflect true financial position.

Mind Map: Adjustments & Reconciliation

Example: An accountant accrues unpaid salaries at the end of the reporting period to comply with matching principles.

Step 5: Prepare the Trial Balance

Compile a trial balance to ensure that total debits equal total credits, which is a fundamental check for accuracy.

Mind Map: Trial Balance Preparation

Example: If the trial balance does not balance, the accountant investigates missing entries or incorrect postings.

Step 6: Draft the Financial Statements

Prepare the core financial statements:

- Balance Sheet (Statement of Financial Position)

- Income Statement (Profit & Loss Statement)

- Statement of Cash Flows

- Statement of Changes in Equity

Mind Map: Financial Statements Components

Example: The income statement clearly separates operating expenses from non-operating expenses to enhance transparency.

Step 7: Ensure Compliance with Disclosure Requirements

Include all required notes and disclosures such as accounting policies, contingent liabilities, related party transactions, and subsequent events.

Mind Map: Disclosure Requirements

Example: Disclosing a pending lawsuit as a contingent liability in the notes to the financial statements.

Step 8: Review and Obtain Approvals

Conduct a thorough review for accuracy and compliance, then obtain necessary approvals from management or audit committees.

Mind Map: Review & Approval Process

Example: The CFO reviews and signs off on the financial statements before external audit submission.

Step 9: Publish and File Financial Statements

Distribute the financial statements to stakeholders and file with regulatory bodies within prescribed deadlines.

Mind Map: Publication & Filing

Example: Filing the annual report with the SEC electronically before the deadline to avoid penalties.

Summary Table: Step-by-Step Process

| Step | Action | Key Focus | Example |

|---|---|---|---|

| 1 | Understand Standards | GAAP, IFRS, Regulations | US GAAP for NYSE-listed company |

| 2 | Collect & Verify Data | Accuracy & Completeness | Cross-check invoices with bank deposits |

| 3 | Record Transactions | Correct Classification | Recording office supplies as expense |

| 4 | Adjust & Reconcile | Accruals, Depreciation | Accruing unpaid salaries |

| 5 | Prepare Trial Balance | Debit = Credit | Investigate imbalance in trial balance |

| 6 | Draft Financial Statements | Balance Sheet, Income Stmt | Separating operating and non-operating exp |

| 7 | Disclosures | Notes & Policies | Disclosing contingent liabilities |

| 8 | Review & Approvals | Accuracy & Compliance | CFO sign-off |

| 9 | Publish & File | Stakeholders & Regulators | Filing with SEC on time |

By following these steps carefully, accountants can ensure that financial statements are not only accurate but also fully compliant with relevant regulations, thereby maintaining stakeholder trust and avoiding legal penalties.

4.3 Ensuring Transparency and Disclosure Requirements

Transparency and disclosure are fundamental principles in financial compliance that ensure stakeholders have access to accurate, timely, and complete information about an organization’s financial health and activities. For accountants, mastering these requirements is critical to maintaining trust, meeting regulatory obligations, and avoiding legal repercussions.

What is Transparency in Financial Reporting?

Transparency means providing clear, understandable, and accessible financial information that reflects the true state of an organization’s finances without hiding or distorting facts.

Disclosure Requirements Explained

Disclosure involves the act of making relevant financial information available to users, including investors, regulators, creditors, and the public. This includes:

- Financial statements

- Notes to financial statements

- Management discussion and analysis (MD&A)

- Risk factors

- Related party transactions

Mind Map: Key Elements of Transparency and Disclosure

Best Practices for Ensuring Transparency and Disclosure

-

Complete and Accurate Reporting

Ensure all financial data is recorded and reported without omissions or errors. -

Timely Disclosure

Provide financial reports and disclosures within the deadlines set by regulatory bodies. -

Clear Presentation

Use straightforward language and well-organized formats to make disclosures understandable. -

Consistent Application of Accounting Policies

Apply accounting standards consistently to avoid misleading comparisons. -

Disclose Material Information

Include any information that could influence decision-making by stakeholders.

Example 1: Disclosure of Contingent Liabilities

Scenario: A company is involved in a lawsuit that might result in a financial loss.

Best Practice: The accountant should disclose the nature of the lawsuit, the possible financial impact, and the likelihood of loss in the notes to the financial statements.

Why: This transparency allows investors and creditors to assess potential risks.

Mind Map: Disclosure of Contingent Liabilities

Example 2: Related Party Transactions Disclosure

Scenario: The company has conducted significant transactions with a business owned by a family member of an executive.

Best Practice: Disclose the relationship, transaction nature, amounts involved, and terms in the financial statement notes.

Why: This prevents conflicts of interest and maintains stakeholder trust.

Mind Map: Related Party Transactions Disclosure

Practical Tips for Accountants

- Regularly review regulatory guidelines (e.g., SEC, IFRS, GAAP) for disclosure requirements.

- Collaborate with legal and compliance teams to identify sensitive or material information.

- Use checklists to ensure all required disclosures are included before finalizing reports.

- Train staff on the importance of transparency and how to identify reportable information.

- Leverage financial reporting software that supports standardized disclosure templates.

Summary

Ensuring transparency and meeting disclosure requirements is a continuous process that demands diligence, accuracy, and ethical commitment from accountants. By following best practices and learning from real-world examples, accountants can help their organizations build credibility and comply with financial regulations effectively.

4.4 Using Technology to Enhance Reporting Accuracy

In today’s fast-paced financial environment, leveraging technology is crucial for accountants to enhance the accuracy and reliability of financial reporting. Technology not only reduces human error but also streamlines processes, improves data integrity, and ensures compliance with regulatory standards.

Key Technologies in Financial Reporting

- Accounting Software: Tools like QuickBooks, Xero, and Sage automate bookkeeping and generate accurate financial statements.

- Enterprise Resource Planning (ERP) Systems: Integrated platforms such as SAP and Oracle consolidate financial data across departments.

- Data Analytics Tools: Power BI, Tableau, and Excel advanced analytics help identify anomalies and trends.

- Robotic Process Automation (RPA): Automates repetitive tasks like data entry and reconciliations.

- Cloud Computing: Enables real-time access and collaboration on financial data.

Mind Map: Technology Tools Enhancing Reporting Accuracy

How Technology Improves Reporting Accuracy

-

Automation of Data Entry and Calculations

- Reduces manual errors.

- Example: Using RPA bots to input invoice data directly into accounting systems, eliminating transcription mistakes.

-

Real-Time Data Processing

- Enables up-to-date financial reports.

- Example: ERP systems updating financial dashboards instantly when transactions occur.

-

Standardization of Reporting Formats

- Ensures consistency across reports.

- Example: Accounting software templates that comply with GAAP or IFRS standards.

-

Enhanced Data Validation and Error Checking

- Automated alerts for inconsistencies.

- Example: Data analytics tools flagging unusual expense patterns for review.

-

Improved Audit Trails

- Digital logs track changes and approvals.

- Example: Cloud-based systems maintaining immutable records of report modifications.

Mind Map: Benefits of Technology in Financial Reporting

Practical Examples

Example 1: Automating Month-End Close with ERP

- A mid-sized company implemented an ERP system that automated data consolidation from multiple departments.

- Result: Month-end close time reduced from 10 days to 4 days, with fewer reconciliation errors.

Example 2: Using Data Analytics to Detect Reporting Anomalies

- An accounting team used Power BI to analyze expense reports.

- The tool flagged a sudden spike in travel expenses, prompting investigation that uncovered duplicate reimbursements.

Example 3: Cloud-Based Collaboration for Financial Reporting

- A multinational firm adopted cloud accounting software allowing teams in different countries to work simultaneously on financial statements.

- Result: Improved accuracy due to immediate feedback and version control.

Best Practices for Implementing Technology

- Choose Scalable Solutions: Ensure software can grow with your organization.

- Train Staff Thoroughly: Proper training minimizes user errors.

- Integrate Systems: Avoid data silos by connecting accounting, ERP, and analytics tools.

- Regularly Update Software: Stay compliant with the latest standards and security patches.

- Maintain Data Security: Implement strong access controls and backups.

By thoughtfully integrating technology into financial reporting processes, accountants can significantly enhance accuracy, reduce risks, and deliver timely, compliant financial information to stakeholders.

4.5 Example: Correcting Errors in Financial Reports Without Breaching Compliance

Correcting errors in financial reports is a critical task for accountants, as inaccuracies can lead to regulatory penalties, loss of stakeholder trust, and potential legal consequences. However, the correction process must be handled carefully to maintain compliance with financial regulations and standards.

Key Principles for Correcting Financial Report Errors

- Transparency: Always disclose the nature and impact of the error.

- Timeliness: Correct errors as soon as they are identified.

- Documentation: Maintain detailed records of the error and correction process.

- Approval: Obtain necessary approvals from management or audit committees.

- Compliance: Follow relevant accounting standards (e.g., GAAP, IFRS) and regulatory requirements.

Mind Map: Steps to Correct Financial Report Errors

Example Scenario: Correcting a Revenue Recognition Error

Situation: An accountant discovers that revenue from a $100,000 contract was recognized prematurely in the previous quarter, violating revenue recognition principles.

Step-by-Step Correction Process:

- Identification: The error was found during a routine review.

- Assessment: The $100,000 is material relative to the quarterly revenue.

- Communication: The accountant informs the CFO and external auditors.

- Correction:

- Reverse the premature revenue recognition entry.

- Recognize revenue in the correct period.

- Documentation: Detailed memo prepared explaining the error, impact, and correction.

- Approval: CFO and audit committee review and approve the correction.

- Disclosure: Financial statements include a note explaining the restatement.

Mind Map: Example of Revenue Recognition Error Correction

Best Practices Illustrated by the Example

- Materiality Assessment: Ensures only significant errors trigger restatements.

- Clear Communication: Keeps stakeholders informed and involved.

- Proper Documentation: Creates an audit trail for transparency.

- Regulatory Compliance: Aligns with SEC and accounting standards for restatements.

Additional Example: Correcting a Clerical Error in Expense Reporting

Situation: An accountant notices that an expense of $5,000 was recorded twice.

Correction Approach:

- Since the error is immaterial, the accountant reverses the duplicate entry in the current period without restating prior financial statements.

- Records a brief note in internal documentation.

- Informs the finance manager.

This approach avoids unnecessary restatements while maintaining accurate records.

Mind Map: Handling Immaterial Errors

Summary

Correcting errors in financial reports requires a structured approach that balances accuracy with compliance. By assessing materiality, maintaining transparency, documenting thoroughly, and following approval protocols, accountants can correct errors effectively without breaching compliance requirements. Real-world examples, such as revenue recognition errors and clerical mistakes, demonstrate how best practices can be applied in everyday accounting scenarios.

5. Compliance Audits and Reviews

5.1 Planning and Preparing for Financial Compliance Audits

Financial compliance audits are critical checkpoints that ensure an organization adheres to regulatory requirements and internal policies. Proper planning and preparation can significantly streamline the audit process, minimize disruptions, and improve outcomes.

Key Steps in Planning and Preparing for Financial Compliance Audits

Define Audit Scope and Objectives

Start by clearly defining the scope of the audit. This includes identifying which financial processes, departments, or transactions will be reviewed. The objectives should align with regulatory requirements and internal compliance goals.

Example: A mid-sized accounting firm plans a SOX compliance audit focusing on internal controls over financial reporting for the last fiscal year. The objective is to verify that all controls are operating effectively to prevent material misstatements.

Identify Applicable Regulations

Understanding which regulations apply to your organization is vital. This could include SOX, AML, IFRS, GAAP, or industry-specific rules.

Example: A financial institution preparing for an AML audit identifies the key regulations such as the Bank Secrecy Act (BSA) and FinCEN guidelines to ensure all anti-money laundering controls are reviewed.

Gather Documentation and Evidence

Collect all relevant financial records, policies, procedures, and previous audit reports. Proper documentation supports transparency and helps auditors verify compliance.

Example: An accountant compiles bank statements, transaction logs, internal control manuals, and training records to prepare for an upcoming compliance audit.

Assign Roles and Responsibilities

Designate team members responsible for different parts of the audit preparation and execution. Clear accountability ensures tasks are completed efficiently.

Example: The compliance officer is assigned to coordinate with external auditors, while the accounting manager prepares the financial statements and supporting documents.

Conduct Pre-Audit Risk Assessment

Identify areas with higher risk of non-compliance or errors. This helps prioritize audit focus and allocate resources effectively.

Example: A company identifies revenue recognition and expense reporting as high-risk areas based on prior audit findings and recent process changes.

Schedule Audit Timeline

Develop a realistic timeline that includes preparation, fieldwork, reporting, and remediation phases. Communicate this schedule to all stakeholders.

Example: The audit team sets a four-week schedule, with one week for document collection, two weeks for fieldwork, and one week for reporting.

Notify Stakeholders and Prepare the Audit Team

Inform all relevant departments and personnel about the upcoming audit. Provide training or refresher sessions to ensure everyone understands their role.

Example: The compliance officer holds a briefing session for the finance team to review audit procedures and expectations.

Utilize Tools and Resources

Leverage compliance management software, checklists, and templates to organize the audit process and ensure nothing is overlooked.

Example: Using a compliance checklist app, the audit coordinator tracks completion of document submissions, control testing, and issue resolution.

Mind Map: Detailed Audit Preparation Workflow

Summary

Planning and preparing for financial compliance audits involves a structured approach that includes defining scope, gathering documentation, assigning roles, assessing risks, scheduling, and effective communication. By following these best practices and using appropriate tools, accountants can facilitate smoother audits, reduce compliance risks, and demonstrate organizational commitment to regulatory adherence.

5.2 Conducting Internal Audits: Best Practices

Internal audits are a critical component of financial compliance, enabling organizations to assess the effectiveness of their internal controls, identify risks, and ensure adherence to regulatory requirements. For accountants, mastering internal audit best practices is essential to maintain transparency, accuracy, and trustworthiness in financial reporting.

Key Steps in Conducting Internal Audits

Best Practices Explained with Examples

Thorough Planning and Scoping

- Best Practice: Clearly define the audit scope and objectives to focus efforts on high-risk areas.

- Example: An accountant planning an audit of accounts payable might scope the audit to include vendor selection, invoice approval, and payment processing to detect potential fraud or errors.

Risk-Based Approach

- Best Practice: Prioritize audit activities based on risk assessment to allocate resources efficiently.

- Example: During an internal audit, the accountant identifies that cash handling processes have a higher risk of misappropriation than fixed asset management, so more time is devoted to testing cash controls.

Use of Checklists and Standardized Procedures

- Best Practice: Employ checklists to ensure consistency and completeness across audits.

- Example: Using a checklist for compliance with SOX Section 404, the accountant verifies documentation of control activities, segregation of duties, and IT system access controls.

Effective Data Collection and Testing

- Best Practice: Collect relevant data through sampling, observation, and interviews; test controls for operating effectiveness.

- Example: The auditor selects a random sample of expense reports to verify proper approval and supporting documentation, identifying any deviations.

Clear and Objective Reporting

- Best Practice: Document findings clearly, avoid jargon, and provide actionable recommendations.

- Example: Instead of stating “controls are weak,” the report specifies “lack of dual authorization on payments exceeding $10,000 increases risk of unauthorized disbursements” and recommends implementing dual approvals.

Follow-up and Monitoring

- Best Practice: Track remediation efforts and re-assess controls to ensure issues are resolved.

- Example: After identifying a gap in IT access controls, the accountant schedules a follow-up audit in six months to verify implementation of new access policies.

Mind Map: Internal Audit Best Practices

Practical Example: Conducting an Internal Audit on Expense Reimbursements

- Planning: Define the audit scope to cover expense reimbursements over the past 6 months.

- Risk Assessment: Identify risks such as fraudulent claims, lack of receipts, or policy non-compliance.

- Data Collection: Obtain a list of all expense reimbursements and supporting documents.

- Testing: Select a sample of 30 reimbursements and verify:

- Proper approval by supervisors

- Valid receipts attached

- Compliance with company policy

- Reporting: Document findings, e.g., “5 out of 30 reimbursements lacked proper approval,” and recommend stricter enforcement of approval policies.

- Follow-up: Schedule a review in 3 months to ensure corrective actions are implemented.

Summary

Conducting internal audits effectively requires a structured approach emphasizing planning, risk assessment, thorough testing, clear reporting, and diligent follow-up. By integrating these best practices, accountants can strengthen financial compliance, mitigate risks, and enhance organizational governance.

5.3 Working with External Auditors: Roles and Responsibilities

Financial compliance relies heavily on the collaboration between accountants and external auditors. Understanding the roles and responsibilities of each party ensures a smooth audit process, accurate reporting, and adherence to regulatory standards.

Roles of External Auditors

- Independent Assessment: External auditors provide an unbiased evaluation of the financial statements, verifying accuracy and compliance with applicable standards.

- Risk Identification: They assess areas of potential risk or misstatement, focusing audit efforts accordingly.

- Compliance Verification: Auditors ensure that the organization adheres to relevant laws, regulations, and internal policies.

- Reporting: They issue audit reports that communicate findings, including any material misstatements or control weaknesses.

Responsibilities of Accountants When Working with External Auditors

- Preparation of Documentation: Accountants must prepare and organize financial records, supporting documents, and reconciliations.

- Facilitating Access: Providing auditors with timely access to systems, personnel, and data.

- Clarifying Transactions: Explaining complex or unusual transactions to auditors.

- Implementing Recommendations: Acting on audit findings to improve controls and compliance.

Mind Map: Collaboration Between Accountants and External Auditors

Best Practices for Effective Collaboration

- Early Engagement: Involve external auditors early in the financial reporting cycle to address potential issues proactively.

- Clear Communication: Maintain open, transparent communication channels to resolve queries quickly.

- Documentation Accuracy: Ensure all financial records are complete, accurate, and well-organized.

- Responsiveness: Respond promptly to auditor requests and provide detailed explanations.

- Continuous Improvement: Use audit feedback to strengthen internal controls and compliance processes.

Example Scenario: Preparing for an External Audit