Accounting Information Systems

1. Introduction to Accounting Information Systems

1.1 Definition and Importance of AIS in Modern Finance

What is an Accounting Information System (AIS)?

An Accounting Information System (AIS) is a structured framework that collects, stores, manages, processes, retrieves, and reports financial data to support decision-making and control in an organization. It integrates accounting principles with information technology to streamline financial operations and ensure accuracy, compliance, and efficiency.

Mind Map: Core Definition of AIS

Importance of AIS in Modern Finance

-

Accuracy and Reliability

- AIS automates data entry and processing, significantly reducing human errors.

- Example: A multinational corporation uses AIS to automatically reconcile bank statements daily, minimizing discrepancies.

-

Efficiency and Speed

- Automated workflows speed up transaction processing and reporting.

- Example: An e-commerce company processes thousands of sales transactions per hour using AIS, enabling real-time financial tracking.

-

Regulatory Compliance

- AIS helps organizations comply with financial regulations by maintaining audit trails and generating required reports.

- Example: A publicly traded company uses AIS to ensure Sarbanes-Oxley (SOX) compliance by tracking changes in financial data.

-

Improved Decision Making

- Provides timely and relevant financial information to stakeholders.

- Example: CFOs use AIS dashboards to monitor cash flow and profitability trends, enabling strategic planning.

-

Cost Reduction

- Reduces manual labor and paper-based processes.

- Example: A small business reduces accounting overhead by adopting cloud-based AIS, eliminating the need for physical storage and manual bookkeeping.

-

Internal Controls and Fraud Prevention

- AIS incorporates controls like segregation of duties and access restrictions.

- Example: A manufacturing firm uses AIS to restrict invoice approvals to authorized personnel only, preventing fraudulent payments.

Mind Map: Importance of AIS in Modern Finance

Example Scenario: AIS Impact in a Mid-Sized Accounting Firm

A mid-sized accounting firm implemented an integrated AIS to handle client bookkeeping, payroll, and tax reporting. Before AIS, accountants manually entered data into spreadsheets, leading to delays and errors. Post-implementation:

- Data entry errors dropped by 85% due to validation rules.

- Monthly financial closing time reduced from 10 days to 3 days.

- Real-time client reports improved transparency and client satisfaction.

- Compliance with tax regulations became automated, reducing audit risks.

This example illustrates how AIS transforms financial operations by enhancing accuracy, efficiency, and compliance.

Summary

Accounting Information Systems are vital in modern finance for automating and securing financial data management. By integrating accounting with technology, AIS empowers accountants and IT specialists to deliver accurate, timely, and compliant financial information, driving better business decisions and operational excellence.

1.2 Key Components of AIS: People, Processes, and Technology

Accounting Information Systems (AIS) are complex frameworks designed to collect, store, and process financial and accounting data. To understand how AIS functions effectively, it is essential to break down its three fundamental components: People, Processes, and Technology. Each component plays a critical role and must work in harmony to ensure accurate, timely, and secure financial information.

People

People are the backbone of any AIS. They include all individuals who interact with the system, from data entry clerks to accountants, auditors, and IT specialists. Their roles and responsibilities vary but are crucial for the system’s success.

- Accountants: Interpret financial data, ensure compliance, and use AIS outputs for decision-making.

- IT Specialists: Manage the technical infrastructure, maintain system security, and customize software.

- Management: Use AIS reports for strategic planning and performance evaluation.

- End Users: Input data and use AIS tools for daily operations.

Best Practice Example:

A mid-sized manufacturing company assigns clear roles where accountants validate data entries and IT specialists regularly update security protocols. This segregation ensures data integrity and reduces errors.

Mind Map: People in AIS

Processes

Processes refer to the procedures and workflows that govern how data is collected, processed, and reported within the AIS. Well-defined processes ensure accuracy, consistency, and efficiency.

Key process elements include:

- Data Input: Capturing financial transactions accurately.

- Data Processing: Classifying, summarizing, and validating data.

- Data Storage: Organizing data securely for easy retrieval.

- Information Output: Generating reports and dashboards for stakeholders.

Best Practice Example:

A retail company implements automated invoice processing where scanned invoices are automatically entered into the AIS, reducing manual errors and speeding up accounts payable.

Mind Map: Processes in AIS

Technology

Technology encompasses the hardware, software, and networks that enable AIS to function. It includes accounting software, databases, cloud services, and security tools.

- Accounting Software: Tools like QuickBooks, SAP, or Oracle Financials that automate accounting tasks.

- Databases: Structured storage systems that hold financial data securely.

- Networks: Facilitate data sharing and remote access.

- Security Technologies: Firewalls, encryption, and access controls protect sensitive information.

Best Practice Example:

An IT firm integrates cloud-based AIS software allowing accountants to access real-time financial data remotely, improving collaboration and decision-making.

Mind Map: Technology in AIS

Integrated Example: How People, Processes, and Technology Work Together

Consider a healthcare provider implementing a new AIS:

- People: Accountants input patient billing data; IT specialists configure the system.

- Processes: Automated billing processes validate insurance claims before submission.

- Technology: Cloud-based software stores data securely and generates financial reports.

This integration ensures timely billing, reduces errors, and supports compliance with healthcare regulations.

Summary

| Component | Role | Best Practice Example |

|---|---|---|

| People | Execute and manage AIS tasks | Clear role definitions in a manufacturing firm |

| Processes | Define workflows for data handling | Automated invoice processing in retail |

| Technology | Provide tools and infrastructure | Cloud-based AIS in IT firm |

Understanding these components and their interplay is vital for accountants and IT specialists to design, implement, and maintain effective AIS solutions.

1.3 Overview of AIS Roles for Accountants and IT Specialists

Accounting Information Systems (AIS) serve as the backbone for financial data management and decision-making in organizations. Both Accountants and IT Specialists play crucial, yet distinct, roles in ensuring that AIS operates efficiently, securely, and aligns with business objectives. Understanding these roles helps foster collaboration and optimize system performance.

Mind Map: Roles in AIS

Accountants’ Roles in AIS

-

Data Entry & Validation

- Accountants ensure accurate and timely input of financial transactions.

- Example: An accountant verifies invoices before entering them into the AIS to prevent errors.

-

Financial Reporting

- They generate reports such as balance sheets, income statements, and cash flow statements.

- Example: Preparing monthly financial summaries for management review using AIS reporting tools.

-

Compliance & Audit

- Accountants ensure AIS outputs comply with regulatory standards like GAAP or IFRS.

- Example: Using AIS audit trails to verify transaction authenticity during internal audits.

-

Internal Controls

- They design and monitor controls to prevent fraud and errors.

- Example: Implementing segregation of duties within AIS to ensure no single user can both approve and process payments.

-

User Training & Support

- Accountants often train end-users on AIS functionalities related to finance.

- Example: Conducting workshops for junior accountants on how to use the AIS for expense reporting.

Mind Map: Accountants’ AIS Responsibilities

IT Specialists’ Roles in AIS

-

System Design & Development

- IT specialists develop or customize AIS software to meet organizational needs.

- Example: Creating a custom module for automated payroll processing.

-

Database Management

- They manage the databases that store financial data, ensuring integrity and availability.

- Example: Regularly backing up AIS databases and optimizing query performance.

-

Security & Access Control

- IT ensures that only authorized personnel can access sensitive financial data.

- Example: Implementing multi-factor authentication and role-based access controls.

-

System Maintenance & Updates

- They apply patches, upgrades, and troubleshoot system issues.

- Example: Scheduling downtime to update AIS software without disrupting business operations.

-

Technical Support

- IT specialists provide ongoing support to AIS users.

- Example: Resolving login issues or software bugs reported by accountants.

Mind Map: IT Specialists’ AIS Responsibilities

Collaborative Examples

-

Example 1: Implementing a New AIS Feature

- Accountants identify the need for enhanced expense tracking.

- IT specialists design and develop the feature.

- Both teams collaborate on testing and training.

-

Example 2: Responding to a Security Incident

- IT detects unusual access patterns.

- Accountants review affected transactions.

- Jointly, they update controls and educate users.

Summary

The synergy between Accountants and IT Specialists is vital for a robust AIS. Accountants bring domain expertise and ensure financial accuracy and compliance, while IT Specialists provide the technical foundation and security. Together, they enable organizations to leverage AIS for strategic advantage.

1.4 Best Practice: Aligning AIS with Organizational Goals - Example of a Mid-Sized Firm

Aligning an Accounting Information System (AIS) with organizational goals is critical to ensure that the system supports the company’s strategic objectives, improves operational efficiency, and provides accurate financial information for decision-making. This section explores best practices for achieving this alignment, illustrated with a practical example from a mid-sized manufacturing firm.

Why Align AIS with Organizational Goals?

- Supports Strategic Decision-Making: AIS provides timely and relevant financial data that helps management steer the company.

- Enhances Operational Efficiency: Tailoring AIS to business processes reduces redundant tasks and errors.

- Ensures Compliance and Risk Management: Aligning AIS with regulatory requirements protects the organization.

- Improves User Adoption: Systems designed with organizational context in mind are easier for staff to use.

Best Practices for Alignment

-

Understand Organizational Goals Clearly

- Engage stakeholders from finance, operations, and IT.

- Document short-term and long-term objectives.

-

Map Business Processes to AIS Functions

- Identify key processes like order-to-cash, procure-to-pay, and payroll.

- Ensure AIS modules support these processes seamlessly.

-

Customize AIS Features to Reflect Business Needs

- Configure reporting formats to match management requirements.

- Automate workflows that align with company policies.

-

Establish Continuous Feedback Loops

- Regularly collect user feedback to refine AIS.

- Monitor KPIs to assess system impact on goals.

-

Train Users on AIS in the Context of Organizational Objectives

- Provide role-based training emphasizing how AIS supports their tasks.

Mind Map: Aligning AIS with Organizational Goals

Example: Mid-Sized Manufacturing Firm “TechParts Inc.”

Background: TechParts Inc. produces electronic components and has about 200 employees. The company aims to improve financial transparency, reduce manual errors, and speed up month-end closing.

Step 1: Understanding Goals

- Management wants real-time cost tracking per product line.

- The finance team requires automated reconciliation to reduce errors.

- Compliance with industry-specific tax regulations is mandatory.

Step 2: Mapping Processes

- Order-to-Cash: From sales orders to revenue recognition.

- Procure-to-Pay: Managing supplier invoices and payments.

- Inventory Management: Tracking raw materials and finished goods.

Step 3: Customizing AIS

- Implemented a module for real-time cost allocation per product.

- Automated bank reconciliation workflows.

- Customized tax reporting templates aligned with regulations.

Step 4: Feedback and KPIs

- Monthly surveys collected from finance and operations teams.

- KPIs monitored: Reduction in closing time (from 10 to 5 days), error rate in invoices (reduced by 60%).

Step 5: Training

- Conducted workshops focusing on how AIS features help achieve faster closing and error reduction.

Mind Map: TechParts Inc. AIS Alignment

Key Takeaways

- Aligning AIS with organizational goals ensures the system delivers maximum value.

- Collaboration between accountants and IT specialists is essential for effective customization.

- Continuous feedback and training help maintain alignment as business needs evolve.

This approach not only improves system efficiency but also empowers users by making the AIS a strategic tool rather than just a transactional system.

1.5 Case Study: Transition from Manual to Automated AIS

Overview

This case study explores the journey of a mid-sized manufacturing company, “Acme Manufacturing,” as it transitioned from a fully manual accounting system to an automated Accounting Information System (AIS). The goal was to improve accuracy, reduce processing time, and enhance reporting capabilities.

Background

Acme Manufacturing relied on paper-based ledgers, manual invoice processing, and spreadsheet-based financial reporting. This led to frequent errors, delayed month-end closes, and limited real-time financial insights.

Challenges Faced

- Data Entry Errors: Manual input caused frequent mistakes.

- Time-Consuming Processes: Invoice approvals and reconciliations took days.

- Limited Reporting: Financial reports were generated monthly with limited detail.

- Lack of Integration: Disconnected systems led to redundant work.

Transition Objectives

- Automate data entry and transaction processing.

- Implement internal controls to reduce errors and fraud.

- Enable real-time financial reporting.

- Integrate accounting with inventory and sales systems.

Step-by-Step Transition Process

Mind Map: Transition Process from Manual to Automated AIS

Best Practices Applied

-

Comprehensive Needs Assessment

- Example: Conducted workshops with accounting and IT teams to list all manual processes and pain points.

-

Stakeholder Collaboration

- Example: Accountants and IT specialists jointly selected an AIS platform that supports integration with existing inventory software.

-

Phased Implementation

- Example: Started automation with accounts payable before moving to general ledger and payroll.

-

Parallel Testing

- Example: Ran manual and automated systems simultaneously for one month to validate accuracy.

-

User Training and Support

- Example: Created role-based training sessions and a dedicated helpdesk for early adopters.

Example: Automated Invoice Processing Workflow

Mind Map: Automated Invoice Processing

This automation reduced invoice processing time from 5 days to 1 day and decreased errors by 80%.

Results and Benefits

- Accuracy Improved: Data entry errors dropped significantly due to validation controls.

- Efficiency Gains: Month-end close shortened from 10 days to 4 days.

- Real-Time Reporting: Management accessed dashboards with up-to-date financial metrics.

- Enhanced Security: Segregation of duties and audit trails reduced fraud risk.

- Employee Satisfaction: Staff shifted focus from repetitive tasks to analysis and decision support.

Lessons Learned

- Early involvement of end-users is critical for adoption.

- Parallel runs help build confidence and identify hidden issues.

- Continuous training and feedback loops improve system utilization.

Summary

The transition from manual to automated AIS at Acme Manufacturing demonstrates how thoughtful planning, collaboration between accountants and IT specialists, and adherence to best practices can transform accounting operations. This case highlights the tangible benefits of automation, including improved accuracy, efficiency, and strategic insight.

For accountants and IT specialists embarking on similar transitions, this case study underscores the importance of clear communication, phased rollouts, and ongoing support to ensure a successful AIS implementation.

2. Core Functionalities of Accounting Information Systems

2.1 Data Collection and Input Controls - Best Practices with Real-World Examples

Introduction

Data collection and input controls are foundational to the accuracy and reliability of any Accounting Information System (AIS). Properly designed input controls ensure that the data entered into the system is complete, accurate, and authorized, minimizing errors and fraud.

Key Concepts of Data Collection and Input Controls

- Data Collection: The process of gathering financial and transactional data from various sources.

- Input Controls: Mechanisms to validate and verify data before it is processed by the AIS.

Best Practices for Data Collection and Input Controls

Validation Checks

- Definition: Automated checks that verify data accuracy and completeness at the point of entry.

- Examples: Range checks, format checks, consistency checks.

Authorization Controls

- Ensuring only authorized personnel can input or modify data.

- Use of role-based access controls (RBAC).

Automated Data Capture

- Using technologies like barcode scanners, OCR (Optical Character Recognition), and EDI (Electronic Data Interchange) to reduce manual entry errors.

Segregation of Duties

- Separating responsibilities between data entry, approval, and reconciliation to prevent fraud.

Audit Trails

- Maintaining logs of who entered or modified data and when.

Mind Map: Data Collection and Input Controls Best Practices

Real-World Examples

Example 1: Retail Company Using Barcode Scanning

A retail company implemented barcode scanning at the point of sale to capture sales data directly into their AIS. This automated data collection reduced manual entry errors significantly.

- Best Practice Applied: Automated Data Capture

- Impact: Improved accuracy, faster processing, and real-time inventory updates.

Example 2: Financial Firm Implementing Validation Checks

A financial services firm integrated validation rules into their AIS to ensure that all invoice amounts entered were within expected ranges and that invoice dates were not in the future.

- Best Practice Applied: Validation Checks

- Impact: Reduced data entry errors and prevented processing of invalid invoices.

Example 3: Manufacturing Company Segregating Duties

In a manufacturing company, the data entry clerk inputs purchase orders, but only the purchasing manager can approve them. The AIS enforces this segregation through access controls.

- Best Practice Applied: Segregation of Duties & Authorization Controls

- Impact: Reduced risk of unauthorized purchases and fraud.

Example 4: Non-Profit Organization Maintaining Audit Trails

A non-profit organization uses their AIS to maintain detailed audit trails for all donations entered, including who entered the data and when, to comply with regulatory requirements.

- Best Practice Applied: Audit Trails

- Impact: Enhanced transparency and accountability.

Additional Mind Map: Example Scenario - Invoice Data Entry Controls

Summary

Implementing robust data collection and input controls is essential for maintaining the integrity of an AIS. By combining validation checks, authorization controls, automated data capture, segregation of duties, and audit trails, organizations can significantly reduce errors and fraud, leading to more reliable financial reporting and decision-making.

2.2 Processing Transactions: Accuracy and Efficiency Techniques

Processing transactions accurately and efficiently is at the heart of any Accounting Information System (AIS). This section explores best practices and techniques to ensure transaction processing maintains data integrity, minimizes errors, and accelerates workflows.

Key Objectives in Transaction Processing

- Accuracy: Ensuring data entered and processed is correct and consistent.

- Efficiency: Minimizing time and resources needed to process transactions.

- Auditability: Maintaining clear trails for verification and compliance.

Best Practices for Accuracy and Efficiency

Automated Data Validation

Automated validation rules check data as it is entered, reducing human error.

- Example: Invoice entry fields automatically validate vendor IDs against the master database.

Use of Standardized Transaction Templates

Templates ensure consistent data capture and reduce omissions.

- Example: A standardized purchase order form with mandatory fields.

Batch Processing with Error Handling

Grouping transactions for batch processing improves efficiency, while error logs help isolate issues.

- Example: Payroll transactions processed nightly with automatic flagging of anomalies.

Real-Time Processing for Critical Transactions

For time-sensitive transactions, real-time processing ensures immediate updates.

- Example: Real-time bank reconciliations for cash management.

Segregation of Duties and Dual Controls

Splitting transaction processing tasks reduces fraud and errors.

- Example: One employee enters transactions, another approves them.

Mind Map: Techniques to Ensure Accuracy in Transaction Processing

Mind Map: Techniques to Improve Efficiency in Transaction Processing

Detailed Examples

Example 1: Automated Invoice Processing in a Retail Company

A retail company implemented an AIS module that automatically scans and extracts invoice data using Optical Character Recognition (OCR). The system validates vendor codes and purchase order numbers against the database before posting the transaction.

- Accuracy: Automated validation reduced invoice entry errors by 85%.

- Efficiency: Processing time dropped from 3 days to a few hours.

Example 2: Payroll Batch Processing with Error Handling

A mid-sized firm processes payroll in batches every two weeks. The AIS flags any employee record missing tax information or with inconsistent hours worked.

- Accuracy: Errors are caught before payment runs.

- Efficiency: Payroll staff focus only on flagged records, saving time.

Example 3: Real-Time Bank Reconciliation

A financial institution uses real-time transaction feeds to reconcile bank statements instantly. Any discrepancies trigger alerts for immediate investigation.

- Accuracy: Immediate detection of mismatches.

- Efficiency: Reduced month-end reconciliation workload.

Summary

By combining automated validation, standardized templates, batch and real-time processing, and segregation of duties, organizations can significantly improve the accuracy and efficiency of transaction processing within their AIS. These techniques not only reduce errors and fraud risk but also accelerate financial workflows, enabling better decision-making and compliance.

For accountants and IT specialists, understanding and implementing these techniques is critical to maintaining robust and reliable accounting systems.

2.3 Information Storage and Retrieval: Database Management Best Practices

Effective information storage and retrieval are foundational to the success of any Accounting Information System (AIS). Proper database management ensures data integrity, accessibility, and security, enabling accountants and IT specialists to generate accurate financial reports and make informed decisions.

Key Concepts in Database Management for AIS

- Data Integrity: Ensuring accuracy and consistency of data over its lifecycle.

- Data Accessibility: Enabling authorized users to retrieve data efficiently.

- Data Security: Protecting sensitive financial information from unauthorized access.

- Backup and Recovery: Safeguarding data against loss or corruption.

Best Practices for Database Management in AIS

-

Use a Relational Database Management System (RDBMS)

- Most AIS utilize RDBMS like SQL Server, Oracle, or MySQL.

- Example: A retail company uses SQL Server to store transactional data, ensuring relationships between invoices, customers, and payments are maintained.

-

Normalize Data to Reduce Redundancy

- Organize data into tables to minimize duplication.

- Example: Separating customer details and sales transactions into different tables linked by customer ID.

-

Implement Strong Access Controls

- Role-based access ensures only authorized personnel can view or modify data.

- Example: Accountants have read/write access to financial records, while auditors have read-only access.

-

Regular Backup and Disaster Recovery Plans

- Schedule automated backups and test recovery procedures.

- Example: A manufacturing firm performs nightly backups and stores copies offsite.

-

Use Indexing to Improve Query Performance

- Index frequently queried fields like invoice numbers or dates.

- Example: Indexing the invoice date column speeds up monthly sales reports.

-

Audit Trails and Logging

- Track changes to data for compliance and troubleshooting.

- Example: Logging every update to payment records with user ID and timestamp.

-

Data Encryption

- Encrypt sensitive data both at rest and in transit.

- Example: Encrypting customer credit card information stored in the database.

Mind Map: Database Management Best Practices in AIS

Example: Implementing Database Management in a Mid-Sized Accounting Firm

Scenario: A mid-sized accounting firm wants to improve its AIS database to handle increasing client data securely and efficiently.

Steps Taken:

- Migrated from a flat-file system to an RDBMS (PostgreSQL).

- Normalized data into tables: Clients, Transactions, Invoices, Payments.

- Established role-based access: Accountants, Auditors, IT Admins.

- Enabled encryption for sensitive fields like Social Security Numbers.

- Set up nightly backups with offsite replication.

- Created indexes on client ID and invoice date for faster report generation.

- Implemented audit logging to track data changes.

Outcome:

- Faster data retrieval for monthly financial reports.

- Enhanced data security and compliance with regulations.

- Reduced data redundancy and errors.

Mind Map: Example Implementation Workflow

Tips for IT Specialists and Accountants

- IT Specialists: Focus on designing a scalable, secure database architecture that supports business needs.

- Accountants: Collaborate closely with IT to define data requirements and validate data integrity.

By following these best practices, organizations can ensure their AIS databases are robust, secure, and optimized for efficient financial data management.

2.4 Reporting and Decision Support Systems in AIS

Accounting Information Systems (AIS) play a crucial role not only in processing transactions but also in generating insightful reports and supporting decision-making processes. Reporting and Decision Support Systems (DSS) within AIS enable accountants and IT specialists to transform raw financial data into actionable information that drives strategic business decisions.

What are Reporting and Decision Support Systems in AIS?

- Reporting Systems: These systems generate financial statements, management reports, compliance reports, and customized dashboards that summarize the organization’s financial health.

- Decision Support Systems (DSS): These are interactive software tools that help users analyze data, model scenarios, and make informed decisions based on accounting and operational data.

Importance of Reporting and DSS in AIS

- Provide timely and accurate financial information.

- Facilitate compliance with regulatory requirements.

- Support budgeting, forecasting, and strategic planning.

- Enhance transparency and accountability within organizations.

Mind Map: Components of Reporting and DSS in AIS

Best Practices for Reporting and DSS in AIS

-

Automate Report Generation

- Example: A manufacturing company uses AIS to automatically generate monthly financial statements and send them to management, reducing manual errors and saving time.

-

Customize Reports for Different Stakeholders

- Example: Accountants receive detailed ledger reports, while executives get high-level dashboards focusing on KPIs.

-

Integrate Real-Time Data Visualization

- Example: A retail chain implements dashboards that update sales and expense data in real time, enabling quick response to market changes.

-

Use Scenario Modeling for Strategic Decisions

- Example: An IT firm uses DSS to model the financial impact of investing in new software development projects.

-

Ensure Data Accuracy and Consistency

- Example: Regular data reconciliation processes are embedded within AIS to maintain report integrity.

Example: Implementing a Decision Support System in a Mid-Sized Accounting Firm

Scenario: The firm wants to improve its budgeting process and better forecast cash flows.

- The AIS is configured to collect historical financial data automatically.

- Using built-in DSS tools, accountants perform trend analysis on past revenues and expenses.

- The system enables “what-if” scenario modeling, such as projecting cash flow impacts if client payments are delayed by 30 days.

- Customized dashboards display forecasted cash positions and alert accountants when projected cash falls below a threshold.

Outcome: The firm can proactively manage cash reserves and make informed decisions about expenditures and client credit terms.

Mind Map: Example Workflow of Reporting and DSS in AIS

Tools and Technologies Supporting Reporting and DSS in AIS

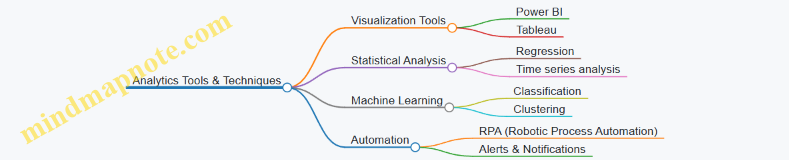

- Business Intelligence (BI) Tools: Power BI, Tableau, QlikView

- Accounting Software with Built-in Reporting: QuickBooks, SAP Business One, Oracle NetSuite

- Data Analytics Platforms: Microsoft Excel (advanced), Python with Pandas, R

Summary

Reporting and Decision Support Systems are integral to maximizing the value of AIS. By leveraging automated reporting, real-time dashboards, and scenario modeling, organizations empower accountants and IT specialists to make data-driven decisions that enhance financial performance and strategic agility.

2.5 Example: Implementing Automated Invoice Processing in a Retail Company

Automated invoice processing is a critical functionality within Accounting Information Systems (AIS) that enhances efficiency, reduces errors, and accelerates the accounts payable cycle. In this section, we explore a detailed example of how a retail company can implement an automated invoice processing system, highlighting best practices and practical steps.

Background

RetailCo, a mid-sized retail chain with multiple outlets, faced challenges with manual invoice processing:

- High volume of paper invoices causing delays

- Frequent data entry errors leading to payment discrepancies

- Difficulty in tracking invoice status and approvals

To address these issues, RetailCo decided to implement an automated invoice processing system integrated into their AIS.

Step 1: Understanding the Invoice Processing Workflow

Before automation, the workflow involved:

- Receiving paper or PDF invoices via mail/email

- Manual data entry into the accounting system

- Physical routing for approval

- Manual matching of invoices with purchase orders and receipts

- Payment processing

Mind Map: Manual Invoice Processing Workflow

Step 2: Designing the Automated Invoice Processing System

RetailCo aimed to automate the following:

- Capture invoice data automatically using Optical Character Recognition (OCR)

- Validate invoice data against purchase orders and receipts

- Route invoices electronically for approval

- Update AIS in real-time

- Generate alerts for exceptions

Mind Map: Automated Invoice Processing Workflow

Step 3: Implementation Best Practices

-

Stakeholder Collaboration: Accountants and IT specialists worked together to define requirements and map workflows.

-

Choosing the Right Technology: RetailCo selected an OCR tool compatible with their AIS and ERP system.

-

Pilot Testing: The system was tested with a subset of invoices to identify issues.

-

Training: Staff were trained on new processes and exception handling.

-

Continuous Monitoring: KPIs such as processing time and error rates were tracked.

Step 4: Example Scenario

- An invoice arrives via email as a PDF.

- The OCR engine extracts key data: invoice number, date, vendor, line items, amounts.

- The system automatically matches the invoice to a purchase order and goods receipt.

- If matched, the invoice is routed electronically to the purchasing manager for approval.

- Upon approval, the AIS updates the accounts payable ledger and schedules payment.

- If discrepancies arise, the system flags the invoice for manual review.

Mind Map: Invoice Processing Exception Handling

Benefits Realized by RetailCo

- 60% reduction in invoice processing time

- Significant decrease in data entry errors

- Improved visibility into invoice status

- Enhanced compliance and audit trail

Summary

Automating invoice processing within an AIS framework transforms a traditionally manual, error-prone task into a streamlined, efficient workflow. By leveraging OCR technology, electronic approvals, and real-time system updates, RetailCo improved operational efficiency and accuracy, demonstrating a best practice example for other retail and finance organizations.

3. Designing and Implementing an Effective AIS

3.1 Requirements Gathering: Collaborating Between Accountants and IT Specialists

Requirements gathering is a critical first step in designing an effective Accounting Information System (AIS). It involves collecting detailed information about what the system must do to meet the needs of both accounting professionals and IT specialists. Successful collaboration between these two groups ensures the system is both functionally robust and technically feasible.

Why Collaboration Matters

- Accountants understand the financial processes, compliance requirements, and reporting needs.

- IT Specialists bring expertise in system architecture, data security, and technology integration.

Together, they ensure the AIS supports accurate financial management while being scalable, secure, and user-friendly.

Key Steps in Requirements Gathering

- Stakeholder Identification

- Identify all users and stakeholders (e.g., accountants, auditors, IT staff, management).

- Interviews and Workshops

- Conduct interviews and joint workshops to understand workflows and pain points.

- Documenting Business Processes

- Map out current accounting processes and identify areas for automation or improvement.

- Defining Functional Requirements

- Specify what the AIS must do (e.g., ledger management, tax calculations, audit trails).

- Defining Non-Functional Requirements

- Include performance, security, usability, and compliance needs.

- Prioritization and Validation

- Prioritize requirements and validate them with stakeholders.

Mind Map: Requirements Gathering Process

Example: Collaborative Requirements Gathering for a Payroll System

Scenario: A mid-sized company wants to implement an AIS module for payroll.

-

Accountants’ Input:

- Need accurate tax calculations based on local regulations.

- Require automated deduction of benefits and retirement contributions.

- Must generate reports for compliance and auditing.

-

IT Specialists’ Input:

- System must integrate with existing HR software.

- Data encryption is required for sensitive employee information.

- Support for multi-platform access (desktop and mobile).

Collaboration Outcome:

- Joint workshops identified the need for an API to connect payroll with HR.

- Accountants and IT agreed on security protocols and user roles.

- Prioritized features included automated tax updates and real-time reporting.

Mind Map: Payroll System Requirements Collaboration

Best Practices for Effective Collaboration

- Establish Clear Communication Channels: Use collaborative tools like Slack, Microsoft Teams, or shared documentation platforms.

- Create Cross-Functional Teams: Include representatives from accounting and IT in all phases.

- Use Visual Aids: Flowcharts, mind maps, and prototypes help clarify complex requirements.

- Iterative Feedback: Regularly review requirements with stakeholders to refine and adjust.

- Document Everything: Maintain detailed records of decisions and requirements for future reference.

Additional Example: Using Mind Mapping Tools

A financial services firm used mind mapping software (e.g., XMind, MindMeister) during requirements sessions. This visual approach helped uncover overlooked needs such as:

- Automated reconciliation alerts.

- Multi-currency handling.

- Audit trail customization.

The mind maps were shared with all stakeholders, ensuring transparency and alignment before development began.

In summary, requirements gathering is a collaborative, iterative process where accountants provide domain expertise and IT specialists translate those needs into technical specifications. Using structured approaches like mind maps and joint workshops ensures the AIS is designed to meet real-world business needs effectively.

3.2 System Design Principles: Scalability and Flexibility

Designing an Accounting Information System (AIS) that can grow with your organization and adapt to changing requirements is crucial for long-term success. Scalability and flexibility are two foundational principles that ensure your AIS remains effective, efficient, and relevant.

Understanding Scalability in AIS

Scalability refers to the system’s ability to handle increasing amounts of work, data, or users without performance degradation. In accounting systems, scalability ensures that as transaction volumes grow or as more users access the system, the AIS continues to operate smoothly.

Key aspects of scalability:

- Vertical scalability: Enhancing the system’s capacity by upgrading hardware or software resources.

- Horizontal scalability: Adding more machines or instances to distribute the load.

Example: A growing e-commerce company initially processes 1,000 transactions daily. As sales increase, the AIS must handle 10,000+ transactions without slowing down invoice generation or financial reporting.

Understanding Flexibility in AIS

Flexibility is the system’s ability to adapt to new business processes, regulatory changes, or integration requirements without extensive rework.

Key aspects of flexibility:

- Modular design allowing components to be added or modified independently.

- Configurable workflows that can be adjusted without coding.

- Support for multiple accounting standards or currencies.

Example: A multinational corporation needs its AIS to support different tax regulations and currencies across countries. A flexible system allows easy configuration for each region without building separate systems.

Mind Map: Scalability and Flexibility in AIS

Best Practices for Designing Scalable and Flexible AIS

-

Adopt a Modular Architecture:

- Break down the AIS into independent modules such as General Ledger, Accounts Payable, and Reporting.

- Example: Using microservices architecture where each accounting function is a separate service that can be scaled independently.

-

Use Cloud-Based Infrastructure:

- Cloud platforms like AWS or Azure offer on-demand resources to scale vertically and horizontally.

- Example: A startup uses a cloud AIS solution that automatically scales during peak financial periods like month-end closing.

-

Implement Configurable Workflows:

- Allow users to modify approval processes or reporting formats without developer intervention.

- Example: An accounting team configures a multi-level invoice approval workflow as the company grows.

-

Design for Integration:

- Use standardized APIs and middleware to connect AIS with ERP, CRM, or payroll systems.

- Example: Integrating AIS with a CRM system to automatically sync customer billing data.

-

Plan for Data Growth:

- Use scalable databases (e.g., NoSQL or sharded SQL databases) to handle increasing transaction volumes.

- Example: A retail chain implements a sharded database to distribute sales data across regions.

-

Continuous Performance Monitoring:

- Monitor system response times and transaction throughput to identify bottlenecks early.

- Example: IT specialists set up dashboards to track AIS performance metrics in real-time.

Example Scenario: Designing a Scalable and Flexible Payroll System

Context: A mid-sized company with 200 employees plans to expand to multiple countries.

- Scalability: The payroll module is designed to handle up to 5,000 employees by using cloud infrastructure that can add computing resources during payroll processing peaks.

- Flexibility: The system supports multiple tax jurisdictions and currencies, allowing HR to configure payroll rules per country without custom coding.

Mind Map:

Summary

Designing AIS with scalability and flexibility in mind helps organizations avoid costly system overhauls and downtime. By adopting modular architectures, leveraging cloud technologies, and enabling configurability, both accountants and IT specialists can ensure the AIS supports current needs and future growth seamlessly.

3.3 Best Practice: Using Flowcharts and Data Models - Example of a Payroll System

When designing an Accounting Information System (AIS), particularly for complex processes like payroll, visual tools such as flowcharts and data models are invaluable. They help both accountants and IT specialists understand, communicate, and optimize system workflows and data structures before implementation.

Why Use Flowcharts and Data Models?

- Clarity: Visual representations simplify complex processes.

- Collaboration: Bridges communication gaps between accountants and IT teams.

- Error Reduction: Early identification of bottlenecks or missing steps.

- Documentation: Provides a reference for future audits and system updates.

Example Scenario: Payroll System

A payroll system manages employee salary calculations, tax deductions, benefits, and payment disbursements. Designing this system requires clear mapping of processes and data relationships.

Flowchart for Payroll Processing

flowchart TD

A[Start: Collect Employee Work Hours] --> B[Validate Hours]

B -->|Valid| C[Calculate Gross Pay]

B -->|Invalid| D[Flag Error and Notify]

C --> E[Calculate Deductions]

E --> F[Calculate Net Pay]

F --> G[Generate Payslip]

G --> H[Disburse Payment]

H --> I[Update Payroll Records]

I --> J[End]

Explanation:

- The process starts with collecting employee work hours.

- Validation ensures data accuracy.

- Gross pay is calculated based on hours and pay rate.

- Deductions (taxes, benefits) are applied.

- Net pay is computed.

- Payslips are generated and payments disbursed.

- Records are updated for accounting and audit purposes.

Data Model for Payroll System (Entity-Relationship Diagram)

Explanation:

- Employees entity stores employee details.

- TimeRecords track hours worked per date.

- Payroll aggregates payment information per pay period.

- Deductions detail various deduction types linked to payroll.

Practical Example: Applying the Flowchart and Data Model

Step 1: Data Collection

- Employee John Doe logs 40 hours for the week.

- TimeRecords entry created with EmployeeID = 001, Date = 2024-06-01, HoursWorked = 40.

Step 2: Validation

- System checks if hours are within allowable limits.

- If valid, proceed; if not, notify payroll officer.

Step 3: Gross Pay Calculation

- John’s pay rate = $25/hour.

- Gross Pay = 40 * $25 = $1,000.

Step 4: Deductions Calculation

- Tax deduction = 15% of gross pay = $150.

- Health insurance = $50.

- Total deductions = $200.

Step 5: Net Pay Calculation

- Net Pay = $1,000 - $200 = $800.

Step 6: Payslip Generation and Payment

- Payslip generated with all details.

- Payment disbursed via direct deposit.

Step 7: Record Update

- Payroll record updated with all payment details.

Tips for Creating Effective Flowcharts and Data Models

- Use standard symbols (e.g., rectangles for processes, diamonds for decisions).

- Keep flowcharts simple and modular.

- Validate models with end-users (accountants and payroll staff).

- Update diagrams as system requirements evolve.

By integrating flowcharts and data models early in the payroll system design, organizations can ensure smoother implementation, reduce errors, and foster better collaboration between accounting and IT teams.

3.4 Implementation Strategies: Phased vs. Big Bang Approach

Implementing an Accounting Information System (AIS) is a critical step that can significantly impact an organization’s operational efficiency and financial accuracy. Choosing the right implementation strategy is essential to minimize risks, control costs, and ensure user adoption. Two primary strategies dominate AIS implementation: the Phased Approach and the Big Bang Approach.

Phased Implementation Approach

The phased approach involves rolling out the AIS in stages or modules over a period of time. This method allows organizations to gradually transition from the old system to the new one, reducing disruption and allowing for continuous feedback and adjustments.

Key Characteristics:

- Incremental deployment of system components

- Parallel running of old and new systems during transition

- Easier troubleshooting and risk management

Mind Map: Phased Implementation Approach

Example: A mid-sized manufacturing company decided to implement their AIS using a phased approach. They first deployed the payroll module, allowing HR and finance teams to get accustomed to the new system. After successfully running payroll for two cycles without issues, they moved on to implement accounts payable, followed by general ledger and financial reporting. This incremental rollout helped identify and fix issues early, minimizing operational disruptions.

Big Bang Implementation Approach

The big bang approach involves switching over from the old system to the new AIS all at once, on a predetermined date. This method aims for a rapid transition, eliminating the need to maintain two systems simultaneously.

Key Characteristics:

- Complete system cutover at once

- Requires extensive preparation and testing

- High risk but potentially faster realization of benefits

Mind Map: Big Bang Implementation Approach

Example: A financial services firm opted for a big bang implementation of their new AIS to meet regulatory deadlines. They conducted extensive user training and system testing over six months. On a weekend, they switched off the legacy system and activated the new AIS. Although the transition was challenging, the firm was able to quickly leverage the new system’s advanced reporting and compliance features.

Comparative Mind Map: Phased vs. Big Bang

Best Practices for Choosing an Implementation Strategy

- Assess Organizational Readiness: Evaluate staff expertise, change management capacity, and IT infrastructure.

- Consider System Complexity: More complex systems often benefit from phased implementation.

- Evaluate Risk Tolerance: Organizations with low risk tolerance should prefer phased rollout.

- Plan Thorough Training: Regardless of approach, comprehensive user training is critical.

- Develop Contingency Plans: Prepare rollback strategies and support resources.

Summary

Both phased and big bang approaches have their merits and challenges. The phased approach offers controlled, incremental change with lower risk but requires more time and resources. The big bang approach provides rapid deployment and immediate benefits but comes with higher risk and demands meticulous preparation. Selecting the right strategy depends on organizational needs, resources, and risk appetite.

Additional Example: Payroll System Implementation

Phased: Implement core payroll processing first, then add tax filing and benefits management modules later.

Big Bang: Deploy the entire payroll system including processing, tax filing, and benefits management simultaneously on a single go-live date.

By understanding these strategies and applying best practices, accountants and IT specialists can collaborate effectively to ensure a smooth AIS implementation that supports the organization’s financial and operational goals.

3.5 Real-Life Example: Successful AIS Implementation in a Non-Profit Organization

Background

A mid-sized non-profit organization focused on community development faced challenges with its manual accounting processes. The organization struggled with data accuracy, delayed financial reporting, and difficulty in tracking donations and grants. To address these issues, they decided to implement an Accounting Information System (AIS) tailored to their unique needs.

Objectives of AIS Implementation

- Automate financial transactions and reporting

- Improve accuracy and reduce errors

- Enhance donor and grant tracking

- Ensure compliance with regulatory requirements

- Facilitate real-time financial insights for decision-making

Implementation Process

-

Needs Assessment and Requirement Gathering

- Collaboration between accountants and IT specialists to identify pain points

- Prioritized features: donation tracking, grant management, expense allocation

-

System Selection and Customization

- Chose a cloud-based AIS with modules for non-profit accounting

- Customized chart of accounts to reflect fund accounting principles

-

Data Migration and Validation

- Transferred historical financial data from spreadsheets

- Conducted thorough data validation to ensure accuracy

-

Training and Change Management

- Role-based training sessions for finance staff and program managers

- Created user manuals and FAQs

-

Go-Live and Continuous Support

- Phased rollout starting with core accounting functions

- Established helpdesk support for troubleshooting

Mind Map: AIS Implementation Workflow

Best Practices Applied with Examples

-

Collaborative Requirement Gathering: Accountants and IT specialists held joint workshops to ensure all functional needs were captured. For example, program managers requested custom reports to track fund utilization per project.

-

Phased Implementation: Instead of switching all functions at once, the organization first automated accounts payable and receivable, then moved to grant tracking. This reduced risk and allowed staff to adapt gradually.

-

Role-Based Training: Finance staff received in-depth training on journal entries and reconciliations, while program managers were trained on generating financial reports relevant to their projects.

-

Data Validation: Before going live, sample transactions were entered and cross-checked with legacy data to ensure accuracy, preventing costly errors post-implementation.

-

Continuous Feedback Loop: After implementation, monthly meetings were held to gather user feedback and prioritize system enhancements, such as adding automated email alerts for grant deadlines.

Example: Donation Tracking Module

- Problem: Previously, donations were tracked manually, leading to missed acknowledgments and reporting delays.

- Solution: The AIS integrated a donation tracking module that automatically records donor details, donation amounts, and generates receipts.

- Outcome: Improved donor relations and compliance with tax regulations.

Mind Map: Donation Tracking Process

Results and Impact

- Reduced monthly financial closing time by 40%

- Increased accuracy in financial reports, reducing audit findings

- Enhanced transparency with real-time dashboards for board members

- Improved donor engagement through timely communication

Lessons Learned

- Early involvement of end-users is critical to capture all requirements

- Investing in comprehensive training ensures smoother adoption

- Continuous system evaluation and updates keep the AIS aligned with organizational needs

This real-life example demonstrates how a well-planned and collaboratively executed AIS implementation can transform financial management in a non-profit organization, driving efficiency, accuracy, and transparency.

4. Internal Controls and Security in AIS

4.1 Understanding Internal Controls in Accounting Systems

Internal controls are essential mechanisms embedded within Accounting Information Systems (AIS) to ensure the accuracy, reliability, and security of financial data. They help prevent errors, detect fraud, and ensure compliance with laws and regulations. For both accountants and IT specialists, understanding internal controls is critical to maintaining the integrity of financial reporting and safeguarding organizational assets.

What Are Internal Controls?

Internal controls are policies, procedures, and activities designed to provide reasonable assurance that an organization’s objectives related to financial reporting, operations, and compliance are achieved.

Key Objectives of Internal Controls:

- Reliability of Financial Reporting

- Effectiveness and Efficiency of Operations

- Compliance with Applicable Laws and Regulations

Types of Internal Controls in AIS

Preventive Controls

These controls aim to stop errors or fraud before they occur.

-

Access Controls: Restrict system access to authorized users only.

- Example: Using role-based access control (RBAC) so that only accountants can approve journal entries.

-

Authorization Procedures: Require approval for transactions.

- Example: A purchase order must be approved by a manager before processing.

-

Segregation of Duties (SoD): Dividing responsibilities so no single individual can execute all parts of a transaction.

- Example: One employee enters invoices, another approves payments.

Detective Controls

These controls identify errors or irregularities after they have occurred.

-

Reconciliations: Regularly comparing records to detect discrepancies.

- Example: Monthly bank reconciliations to verify cash balances.

-

Exception Reports: Automated reports highlighting unusual transactions.

- Example: A report showing all payments above a certain threshold for review.

-

Audit Trails: Logs that record transaction details for review.

- Example: Tracking who modified a financial record and when.

Corrective Controls

These controls help fix problems detected by detective controls.

-

Backup and Recovery Procedures: Regular data backups to restore information after data loss.

- Example: Daily backups of the AIS database stored offsite.

-

Incident Response: Steps to address security breaches or system failures.

- Example: Immediate account lockout after multiple failed login attempts.

-

System Updates and Patches: Applying software updates to fix vulnerabilities.

- Example: Regularly updating AIS software to protect against cyber threats.

Example Scenario: Segregation of Duties in a Small Business AIS

In a small business, the accountant enters vendor invoices into the AIS. To prevent fraud, the business owner reviews and approves payments before they are processed. This separation ensures no single person can both create and pay fraudulent invoices.

Summary

Understanding and implementing internal controls within AIS is vital for safeguarding assets, ensuring data integrity, and maintaining regulatory compliance. Both accountants and IT specialists must collaborate to design, implement, and monitor these controls effectively.

Further Reading:

- COSO Internal Control Framework

- COBIT for IT Governance

- Sarbanes-Oxley Act (SOX) Compliance Guidelines

4.2 Best Practice: Segregation of Duties with Practical Examples

Segregation of Duties (SoD) is a fundamental internal control designed to prevent errors and fraud by dividing responsibilities among different individuals. In Accounting Information Systems (AIS), SoD ensures that no single person has control over all aspects of any critical financial transaction.

Why Segregation of Duties Matters

- Risk Mitigation: Reduces the risk of intentional fraud or unintentional errors.

- Checks and Balances: Creates a system of checks and balances within financial processes.

- Accountability: Enhances accountability by clearly defining roles.

Core Principles of Segregation of Duties

- Authorization of transactions should be separate from recording.

- Custody of assets should be separate from accounting.

- Reconciliation and review should be performed independently.

Mind Map: Segregation of Duties in AIS

Practical Example 1: Accounts Payable Process

Scenario: In a mid-sized company, the accounts payable process involves multiple steps where SoD is critical.

| Role | Responsibility |

|---|---|

| Purchase Requester | Initiates purchase requests |

| Purchase Approver | Approves purchase orders |

| Accounts Payable | Processes invoices and payments |

| Receiving Clerk | Confirms receipt of goods/services |

| Internal Auditor | Reviews transactions periodically |

How SoD is applied:

- The Purchase Approver cannot process payments.

- The Receiving Clerk is separate from Accounts Payable to verify goods before payment.

- Internal Auditor reviews the entire process independently.

Mind Map: Accounts Payable Segregation of Duties

Practical Example 2: Payroll System

Scenario: In an organization, payroll processing involves sensitive data and payments.

| Role | Responsibility |

|---|---|

| HR Department | Maintains employee records |

| Payroll Processor | Calculates and processes payroll |

| Finance Department | Approves payroll disbursement |

| IT Department | Manages payroll system access |

SoD Implementation:

- HR updates employee data but cannot process payroll.

- Payroll Processor runs payroll but cannot modify employee data.

- Finance approves payroll payments but does not process or modify payroll data.

- IT controls system access and monitors for unauthorized changes.

Mind Map: Payroll Segregation of Duties

Practical Example 3: Cash Handling and Recording

Scenario: A retail company manages cash transactions daily.

| Role | Responsibility |

|---|---|

| Cashier | Collects cash from customers |

| Cash Count Team | Counts and verifies cash at shift end |

| Accountant | Records cash transactions in AIS |

| Internal Auditor | Performs surprise cash counts |

SoD Highlights:

- Cashiers do not record transactions in AIS.

- Accountants record transactions but do not handle cash.

- Cash Count Team verifies physical cash independently.

- Internal Auditor performs unannounced checks.

Mind Map: Cash Handling Segregation of Duties

Implementing Segregation of Duties in AIS

- Role-Based Access Control (RBAC): Assign system permissions based on job roles.

- Automated Alerts: Configure AIS to flag conflicting duties or unusual activities.

- Regular Reviews: Periodically review user access and transaction logs.

- Cross-Training: Ensure multiple employees can perform tasks to avoid bottlenecks but maintain SoD.

Summary

Segregation of Duties is a critical control in AIS that protects organizations from fraud and errors. By clearly defining and separating responsibilities, companies can create a robust control environment. Practical implementation through role definitions, system access controls, and independent reviews ensures the effectiveness of SoD.

For accountants and IT specialists, understanding and applying SoD principles within AIS not only safeguards financial integrity but also enhances operational efficiency and compliance.

4.3 Data Security Measures: Encryption, Access Controls, and Authentication

In Accounting Information Systems (AIS), protecting sensitive financial data is paramount. Data security measures such as encryption, access controls, and authentication form the backbone of safeguarding information from unauthorized access, tampering, and breaches. This section explores these critical components with practical examples and mind maps to help accountants and IT specialists understand and implement best practices effectively.

Encryption

Encryption is the process of converting data into a coded format that can only be read by someone who has the decryption key. It ensures that even if data is intercepted, it remains unreadable to unauthorized users.

Types of Encryption:

- Symmetric Encryption: Same key for encryption and decryption.

- Asymmetric Encryption: Public and private key pairs.

Example: A finance department uses AES (Advanced Encryption Standard) to encrypt sensitive payroll data before storing it in the cloud. Even if the cloud storage is compromised, the encrypted data remains protected.

Mind Map: Encryption in AIS

Access Controls

Access controls restrict who can view or use resources in a computing environment. They are essential to ensure that only authorized personnel can access financial data.

Types of Access Controls:

- Discretionary Access Control (DAC): Access based on user identity and permissions.

- Mandatory Access Control (MAC): Access based on fixed policies.

- Role-Based Access Control (RBAC): Access based on user roles.

Best Practice Example: A company implements RBAC in their AIS where accountants have access to financial reporting modules, while IT specialists have access to system configuration but not sensitive financial records.

Mind Map: Access Controls

Authentication

Authentication verifies the identity of a user or system before granting access. Strong authentication mechanisms prevent unauthorized access to AIS.

Common Authentication Methods:

- Passwords and PINs

- Multi-Factor Authentication (MFA)

- Biometric Authentication (fingerprint, facial recognition)

Example: An accounting firm requires employees to use MFA when accessing the AIS remotely. After entering their password, users must also provide a one-time code sent to their mobile device.

Mind Map: Authentication Methods

Integrated Example: Securing Payroll Data in an AIS

- Encryption: Payroll files are encrypted using AES before storage.

- Access Controls: Only HR and payroll accountants have RBAC permissions to access payroll modules.

- Authentication: Employees accessing payroll remotely must use MFA.

This layered approach ensures confidentiality, integrity, and availability of sensitive payroll information.

Summary

Implementing encryption, access controls, and authentication in AIS is critical for protecting financial data. By combining these measures, organizations can create a robust security framework that mitigates risks from both external threats and insider misuse.

For accountants and IT specialists, understanding these concepts and applying them with practical tools and policies is essential to maintaining trust and compliance in financial reporting systems.

4.4 Case Study: Preventing Fraud Through AIS Controls in a Manufacturing Company

Fraud prevention is a critical concern for manufacturing companies due to the complexity of their operations and the large volume of transactions. This case study explores how a mid-sized manufacturing company successfully implemented Accounting Information System (AIS) controls to detect and prevent fraud, ensuring financial integrity and operational efficiency.

Background

The company, “ABC Manufacturing,” faced challenges with unauthorized transactions, inventory misappropriation, and inaccurate financial reporting. Their legacy AIS lacked robust internal controls, making them vulnerable to fraud.

Objectives

- Strengthen internal controls within the AIS

- Improve segregation of duties

- Enhance transaction monitoring and approval processes

- Implement real-time fraud detection mechanisms

AIS Controls Implemented

Segregation of Duties (SoD)

- Description: Dividing responsibilities among different employees to reduce risk of error or fraud.

- Example: The employee responsible for inventory management cannot approve purchase orders.

Automated Approval Workflows

- Description: Transactions above a certain threshold require multiple levels of approval within the AIS.

- Example: Purchase orders over $10,000 require approval from both the Purchasing Manager and the CFO.

Access Controls and User Permissions

- Description: Restricting system access based on roles.

- Example: Only authorized personnel can modify vendor master data.

Real-Time Transaction Monitoring

- Description: AIS flags suspicious transactions based on predefined rules.

- Example: Duplicate invoice numbers or unusual payment amounts trigger alerts.

Audit Trails and Logging

- Description: Every transaction and change is logged with user ID and timestamp.

- Example: If a payment is modified, the system records who made the change and when.

Mind Map: AIS Controls for Fraud Prevention

Implementation Process

- Assessment: Conducted a risk assessment to identify vulnerable areas.

- Design: Developed control policies aligned with business processes.

- Configuration: Configured AIS modules to enforce controls.

- Training: Educated employees on new processes and fraud awareness.

- Monitoring: Established continuous monitoring and periodic audits.

Results and Benefits

- Reduction in Fraud Incidents: Reported fraud cases dropped by 70% within the first year.

- Improved Compliance: Enhanced adherence to regulatory requirements.

- Increased Transparency: Management gained real-time visibility into transactions.

- Operational Efficiency: Automated workflows reduced manual errors and processing time.

Example Scenario: Detecting Duplicate Invoices

- Situation: The AIS flagged two invoices with identical invoice numbers but different amounts.

- Action: The system automatically sent alerts to the Accounts Payable team.

- Outcome: Investigation revealed an attempt to process a fraudulent invoice; payment was stopped.

Best Practices Highlighted

- Integrate AIS Controls Early: Embedding controls during system design prevents costly fixes later.

- Regularly Update Control Rules: Fraud tactics evolve; AIS rules should adapt accordingly.

- Cross-Functional Collaboration: Accountants and IT specialists must work together to balance security and usability.

- Leverage Technology: Utilize AI and machine learning for advanced anomaly detection.

This case study illustrates how a well-designed AIS with robust controls can serve as a powerful tool to prevent fraud in manufacturing companies, safeguarding assets and ensuring trustworthy financial reporting.

4.5 Disaster Recovery and Business Continuity Planning for AIS

Disaster Recovery (DR) and Business Continuity Planning (BCP) are critical components in safeguarding Accounting Information Systems (AIS) against unexpected disruptions. These disruptions can range from natural disasters, cyberattacks, hardware failures, to human errors. For accountants and IT specialists, understanding and implementing robust DR and BCP strategies ensures the integrity, availability, and confidentiality of financial data, minimizing downtime and financial loss.

Key Concepts in Disaster Recovery and Business Continuity Planning

- Disaster Recovery (DR): Focuses on restoring IT systems and data access after a disruption.

- Business Continuity Planning (BCP): Ensures that critical business functions continue during and after a disaster.

Mind Map: Core Components of DR and BCP for AIS

Best Practice: Conducting a Risk Assessment with Example

Example: A mid-sized accounting firm identifies the following risks:

- Power outages affecting server availability

- Ransomware attacks encrypting financial data

- Flooding in the data center location

Action: They prioritize risks based on likelihood and impact, focusing first on ransomware and power outages.

Data Backup Strategies with Practical Example

Example: A retail company using AIS implements:

- Daily incremental backups stored on a secure cloud service.

- Weekly full backups saved on encrypted external drives stored off-site.

This layered approach ensures minimal data loss and quick recovery.

Mind Map: Recovery Objectives and Strategies

Communication Plan Example

Scenario: After a ransomware attack, the IT team must notify:

- Senior management

- Accounting department

- External auditors

- Clients (if data breach affects them)

Best Practice: Use predefined communication templates and assign clear roles to ensure timely and accurate information dissemination.

Testing and Maintenance

- Schedule quarterly disaster recovery drills simulating AIS failure.

- Document lessons learned and update the DR/BCP plan accordingly.

Example: An accounting firm conducts a simulated data center outage, successfully switching operations to a cloud-based AIS backup within the RTO.

Integrated Example: Disaster Recovery Plan for a Financial Institution’s AIS

- Risk Assessment: Identified threats include cyberattacks and hardware failures.

- Backup Strategy: Real-time replication of AIS data to a geographically distant data center.

- RPO & RTO: Set at 1 hour and 30 minutes respectively.

- Communication: Automated alerts to IT and finance teams.

- Testing: Bi-annual failover tests to validate recovery procedures.

This comprehensive approach minimizes financial risk and ensures regulatory compliance.

Summary

Disaster Recovery and Business Continuity Planning for AIS require a proactive, well-documented, and regularly tested approach. By combining risk assessments, strategic backups, clear recovery objectives, effective communication, and continuous improvement, organizations can protect their critical accounting systems and maintain trust with stakeholders even in the face of adversity.

5. Integration of AIS with Other Enterprise Systems

5.1 ERP Systems and AIS: Understanding the Connection

Enterprise Resource Planning (ERP) systems and Accounting Information Systems (AIS) are two critical components in modern business operations, especially within finance and IT sectors. Understanding their connection is essential for accountants and IT specialists to optimize financial processes, improve data accuracy, and enhance decision-making.

What is an ERP System?

An ERP system is an integrated software platform used by organizations to manage and automate core business processes across various departments such as finance, human resources, procurement, supply chain, and manufacturing.

What is an AIS?

An Accounting Information System is a subset of ERP focused specifically on collecting, storing, and processing financial and accounting data to produce meaningful reports for stakeholders.

How ERP and AIS Connect

- Integration: AIS is often a module within an ERP system or tightly integrated with it.

- Data Flow: ERP systems provide a centralized database where AIS accesses real-time financial data.

- Process Automation: ERP automates workflows that involve accounting, such as invoicing, payroll, and budgeting.

Mind Map: ERP and AIS Connection Overview

Example 1: ERP with Integrated AIS in a Manufacturing Company

Scenario: A manufacturing company uses an ERP system that includes an AIS module. When raw materials are purchased, the procurement module records the transaction, which automatically updates the AIS module for accounts payable.

Best Practice: This integration eliminates duplicate data entry, reduces errors, and ensures that financial statements reflect real-time inventory costs.

Mind Map: Data Flow Example in ERP-AIS Integration

Example 2: ERP-AIS Integration in a Retail Chain

Scenario: A retail chain uses an ERP system where the sales module records transactions at the point of sale. This data flows directly into the AIS module, updating revenue accounts and inventory simultaneously.

Best Practice: Real-time synchronization allows finance teams to monitor daily sales performance and inventory turnover without manual reconciliation.

Benefits of ERP and AIS Integration

- Improved Data Accuracy: Single source of truth reduces discrepancies.

- Enhanced Reporting: Consolidated data enables comprehensive financial and operational reports.

- Streamlined Processes: Automation reduces manual workload and accelerates closing cycles.

- Better Compliance: Integrated audit trails support regulatory requirements.

Mind Map: Benefits Summary

Conclusion

For accountants and IT specialists, understanding the connection between ERP systems and AIS is crucial for designing efficient financial workflows and ensuring data integrity. Leveraging ERP’s broad capabilities alongside AIS’s specialized financial functions creates a powerful ecosystem that supports strategic business decisions.

Quick Tips for Implementation

- Ensure clear communication between finance and IT teams during ERP selection and customization.

- Prioritize modules that tightly integrate AIS functions for seamless data flow.

- Regularly train users on how ERP and AIS modules interact to maximize system benefits.

- Use real-world scenarios to test integration points before full deployment.

5.2 Best Practice: Seamless Data Flow Between AIS and CRM Systems - Example Scenario

In today’s interconnected business environment, seamless data flow between Accounting Information Systems (AIS) and Customer Relationship Management (CRM) systems is crucial for improving operational efficiency, enhancing customer experience, and ensuring accurate financial reporting. This section explores best practices for integrating AIS and CRM systems, supported by a detailed example scenario and mind maps to visualize the process.

Why Integrate AIS and CRM?

- Unified Customer Data: Consolidates financial and customer interaction data.

- Improved Billing Accuracy: Automates invoicing based on CRM sales data.

- Enhanced Reporting: Combines sales pipeline and revenue recognition.

- Streamlined Processes: Reduces manual data entry and errors.

Best Practices for Seamless Data Flow

-

Define Clear Data Mapping:

- Identify which data fields in CRM correspond to AIS (e.g., customer ID, invoice amount).

- Establish standardized data formats to avoid discrepancies.

-

Use Middleware or APIs:

- Employ integration platforms or APIs to enable real-time or scheduled data synchronization.

-

Implement Data Validation and Error Handling:

- Validate data before transfer to prevent corrupt or incomplete records.

- Set up alerts for synchronization failures.

-