Cost Allocation Methods

1. Introduction to Cost Allocation

1.1 Understanding Cost Allocation: Definition and Importance

Cost allocation is the process of identifying, aggregating, and assigning costs to cost objects such as products, departments, or projects. It is a fundamental accounting practice that ensures costs are accurately traced or apportioned to the appropriate areas within an organization.

Definition

Cost Allocation refers to the systematic approach of distributing indirect costs (also known as overheads) to different cost centers or products based on a rational and consistent basis.

- Direct Costs: Costs that can be directly traced to a product or service (e.g., raw materials, direct labor).

- Indirect Costs: Costs that cannot be directly traced and need to be allocated (e.g., utilities, rent, administrative expenses).

Importance of Cost Allocation

- Accurate Product Costing: Helps determine the true cost of manufacturing a product or delivering a service.

- Pricing Decisions: Enables businesses to set competitive and profitable prices.

- Profitability Analysis: Identifies which products or departments are more or less profitable.

- Budgeting and Forecasting: Supports better financial planning and control.

- Regulatory Compliance: Ensures adherence to accounting standards and tax regulations.

- Resource Optimization: Helps in identifying cost-saving opportunities by understanding cost drivers.

Mind Map: Core Concepts of Cost Allocation

Example 1: Simple Cost Allocation in a Manufacturing Company

Scenario: A manufacturing company produces two products: Product A and Product B. The company incurs $10,000 in factory rent (an indirect cost) that needs to be allocated.

Step 1: Identify a cost driver. Suppose the factory floor space used by Product A is 60% and Product B is 40%.

Step 2: Allocate rent based on floor space:

- Product A: $10,000 x 60% = $6,000

- Product B: $10,000 x 40% = $4,000

This allocation ensures that each product bears a fair share of the rent expense based on usage.

Mind Map: Example 1 - Rent Allocation

Example 2: Cost Allocation for Service Departments

Scenario: A manufacturing firm has a maintenance department that supports production departments. The maintenance department costs $50,000 annually.

Step 1: Identify cost drivers, such as machine hours used by each production department.

- Department X uses 1,000 machine hours

- Department Y uses 500 machine hours

Step 2: Calculate total machine hours = 1,000 + 500 = 1,500

Step 3: Allocate maintenance costs:

- Department X: $50,000 x (1,000 / 1,500) = $33,333

- Department Y: $50,000 x (500 / 1,500) = $16,667

This allocation reflects the maintenance support each department consumes.

Mind Map: Example 2 - Maintenance Cost Allocation

Summary

Cost allocation is essential for transparent and accurate financial management in manufacturing and finance sectors. By understanding the types of costs and selecting appropriate cost drivers, accountants and cost analysts can ensure costs are fairly distributed, enabling better decision-making and operational efficiency.

1.2 Key Concepts: Direct vs Indirect Costs

Understanding the distinction between direct and indirect costs is fundamental for effective cost allocation in both finance and manufacturing sectors. These concepts help accountants and cost analysts accurately assign expenses to products, departments, or projects, ensuring precise financial reporting and informed decision-making.

What are Direct Costs?

Direct costs are expenses that can be directly traced to a specific cost object, such as a product, service, or department. These costs are easily identifiable and measurable.

Examples of Direct Costs:

- Raw materials used in manufacturing a product

- Direct labor wages paid to workers assembling a product

- Components purchased specifically for a particular product

Example: In an automobile manufacturing plant, the steel used to build car frames is a direct cost because it is directly attributable to each car produced.

What are Indirect Costs?

Indirect costs, also known as overheads, are expenses that cannot be directly traced to a single cost object. Instead, these costs support multiple products or departments and must be allocated using a systematic approach.

Examples of Indirect Costs:

- Factory rent

- Utilities (electricity, water)

- Salaries of supervisors and maintenance staff

- Depreciation of manufacturing equipment

Example: The electricity bill for the entire factory is an indirect cost because it supports all production activities and cannot be assigned to one specific product without allocation.

Mind Map: Direct vs Indirect Costs

Why is the Distinction Important?

- Accurate Product Costing: Direct costs provide a clear picture of the cost to produce a specific item, while indirect costs must be allocated to avoid under- or over-costing.

- Pricing Decisions: Knowing the true cost helps set competitive prices.

- Budgeting and Forecasting: Helps in planning resource allocation.

- Financial Reporting Compliance: Ensures adherence to accounting standards.

Best Practice: Clear Identification and Documentation

- Maintain detailed records to distinguish direct from indirect costs.

- Use cost codes and tracking systems.

- Regularly review cost classifications to reflect operational changes.

Example Scenario: Manufacturing a Custom Furniture Piece

- Direct Costs: Wood, nails, varnish, and wages of carpenters working on the piece.

- Indirect Costs: Factory lighting, rent, and salaries of security personnel.

In this case, direct costs are charged directly to the furniture piece, while indirect costs are allocated based on a reasonable driver, such as labor hours or machine hours.

Mind Map: Cost Allocation Flow

By mastering the concepts of direct and indirect costs, accountants and cost analysts can implement more precise cost allocation methods, leading to improved financial clarity and operational efficiency.

1.3 The Role of Cost Allocation in Finance and Manufacturing

Cost allocation plays a pivotal role in both finance and manufacturing sectors by enabling organizations to accurately assign costs to products, services, departments, or projects. This process is essential for effective budgeting, pricing, profitability analysis, and strategic decision-making.

Why Cost Allocation Matters

- Accurate Product Costing: Helps determine the true cost of manufacturing a product, including direct and indirect expenses.

- Profitability Analysis: Identifies which products or departments are profitable and which are not.

- Budgeting and Forecasting: Facilitates realistic budgeting by understanding cost behavior and drivers.

- Resource Optimization: Enables better allocation of resources by highlighting cost centers.

- Compliance and Reporting: Ensures adherence to accounting standards and regulatory requirements.

Mind Map: Role of Cost Allocation in Finance and Manufacturing

Example 1: Cost Allocation Impact on Pricing in Manufacturing

A company manufactures two products: Product A and Product B.

- Product A requires more machine hours but less labor.

- Product B requires more labor hours but fewer machine hours.

Using cost allocation based on machine hours alone would unfairly burden Product A with higher overhead costs, potentially leading to overpriced products and loss of competitiveness.

By allocating overhead costs using a combination of machine hours and labor hours, the company achieves a more accurate cost distribution, enabling better pricing decisions.

Mind Map: Example - Multi-Factor Cost Allocation

Example 2: Cost Allocation for Financial Reporting

In a manufacturing firm, indirect costs such as utilities, maintenance, and administrative salaries must be allocated to various departments to comply with financial reporting standards.

If these costs are not allocated properly, the financial statements may misrepresent the profitability of each department, leading to poor managerial decisions.

By using a step-down method to allocate service department costs (like maintenance and IT) to production departments, the company ensures transparency and accuracy in financial reporting.

Mind Map: Cost Allocation for Financial Reporting

Summary

Cost allocation is a foundational element that bridges finance and manufacturing functions. It ensures that costs are assigned logically and fairly, providing clarity for pricing, budgeting, and performance evaluation. By integrating best practices and using appropriate allocation bases, organizations can enhance financial accuracy and operational efficiency.

1.4 Overview of Cost Allocation Methods

Cost allocation is a fundamental process in both finance and manufacturing sectors, enabling organizations to assign indirect costs to products, services, or departments accurately. Understanding the various methods available helps accountants and cost analysts choose the most appropriate approach for their specific context.

Key Cost Allocation Methods

Below is a mind map summarizing the primary cost allocation methods:

Traditional Cost Allocation Methods

These methods allocate overhead costs based on a single cost driver, such as labor hours or machine hours. They are simple and widely used, especially in manufacturing environments with homogeneous products.

Example: A factory incurs $100,000 in overhead. It uses 10,000 direct labor hours across all products. Using the Direct Labor Hours method, the overhead rate is $10 per labor hour. If Product A uses 500 labor hours, it is allocated $5,000 of overhead.

Best Practice: Choose a cost driver that closely correlates with overhead consumption to improve accuracy.

Activity-Based Costing (ABC)

ABC assigns costs based on activities that drive costs, providing more precise allocation especially in complex environments with diverse products.

Example: A manufacturing company identifies activities such as setup, inspection, and packaging. Setup costs total $20,000, driven by the number of setups. If Product B requires 10 setups out of 100 total, it is allocated $2,000 of setup costs.

ABC Example Mind Map

Best Practice: Ensure thorough identification of activities and accurate measurement of cost drivers.

Time-Driven Activity-Based Costing (TDABC)

TDABC simplifies ABC by estimating the time required for activities and assigning costs based on time.

Example: If the capacity cost rate is $50 per hour and Product C requires 3 hours of assembly and 2 hours of quality check, the allocated cost is (3 + 2) * $50 = $250.

TDABC Mind Map

Best Practice: Regularly update time estimates and capacity rates to maintain accuracy.

Joint Product Cost Allocation

Used when multiple products are produced from a common process and costs must be split.

Example: A chemical plant produces Product X and Product Y from the same batch costing $100,000. Using market value at split-off, if Product X is worth $60,000 and Product Y $40,000, costs are allocated proportionally: $60,000 to X and $40,000 to Y.

Service Department Cost Allocation

Allocates costs from service departments (e.g., maintenance, IT) to production departments.

Methods:

- Direct: Allocates service costs directly to production departments.

- Step-Down: Allocates service costs sequentially, considering some inter-service usage.

- Reciprocal: Fully recognizes mutual services among service departments.

Example: Maintenance costs $30,000 and IT costs $20,000. Using the step-down method, maintenance costs are allocated first, then IT costs including a portion of maintenance.

Summary

Selecting the right cost allocation method depends on the complexity of operations, accuracy required, and resources available. Traditional methods offer simplicity, while ABC and TDABC provide precision. Joint and service department allocations address specific scenarios common in manufacturing and finance.

By understanding these methods and applying best practices with clear examples, accountants and cost analysts can enhance cost visibility and support better decision-making.

1.5 Best Practice: Aligning Cost Allocation with Organizational Goals

Aligning cost allocation methods with organizational goals is critical for ensuring that financial data drives strategic decision-making, operational efficiency, and overall business success. When cost allocation reflects the company’s objectives, it provides clearer insights into product profitability, resource utilization, and cost control.

Why Alignment Matters

- Supports Strategic Decision-Making: Accurate cost data helps management prioritize products, services, and projects that align with long-term goals.

- Enhances Accountability: Departments and cost centers understand their financial impact and are motivated to optimize costs.

- Improves Resource Allocation: Resources are directed toward high-value activities, reducing waste.

- Facilitates Performance Measurement: Cost allocation tied to goals enables better tracking of progress and outcomes.

Steps to Align Cost Allocation with Organizational Goals

Example 1: Manufacturing Company Focusing on Product Profitability

A mid-sized manufacturing firm aims to increase profitability by focusing on high-margin products. Previously, overhead was allocated using a simple direct labor hour method, which distorted costs for automated product lines.

Best Practice Applied:

- The company identified that machine hours and setup times were significant cost drivers.

- They shifted to an Activity-Based Costing (ABC) approach, allocating overhead based on actual machine usage and setup activities.

- This realignment provided clearer insights into product costs, revealing that some low-volume products were consuming disproportionate resources.

Outcome:

- Management discontinued unprofitable product lines.

- Resources were reallocated to optimize production of high-margin products.

- Profitability improved by 12% within one year.

Example 2: Finance Department Supporting Cost Control Initiatives

A manufacturing firm’s finance department wanted to support the company’s goal of reducing operational costs by 10%.

Best Practice Applied:

- The finance team collaborated with operations to identify major cost centers and their drivers.

- They implemented a step-down method to allocate service department costs more accurately.

- Cost reports were tailored to highlight variances against budget aligned with cost-saving targets.

Outcome:

- Department managers became more aware of their cost impact.

- Targeted cost reduction initiatives were launched.

- The company achieved a 9.5% reduction in operational costs within the fiscal year.

Mind Map: Benefits of Aligning Cost Allocation with Goals

Tips for Effective Alignment

- Engage Cross-Functional Teams: Include finance, operations, and strategy teams in designing cost allocation.

- Use Relevant Cost Drivers: Ensure allocation bases reflect actual resource consumption tied to goals.

- Maintain Flexibility: Be ready to adjust methods as organizational priorities evolve.

- Document Policies: Clear documentation helps maintain consistency and transparency.

- Leverage Technology: Use costing software to simulate and analyze different allocation scenarios.

By embedding organizational goals into cost allocation practices, accountants and cost analysts can provide more actionable insights, driving better financial and operational outcomes.

1.6 Example: Basic Cost Allocation in a Manufacturing Setup

In this section, we will explore a straightforward example of cost allocation in a manufacturing environment. This example will help accountants and cost analysts understand how to allocate indirect costs (overhead) to products using basic allocation methods.

Scenario Overview

A manufacturing company produces two products: Product A and Product B. The company incurs the following costs for the month:

- Direct materials: $50,000

- Direct labor: $30,000

- Manufacturing overhead (indirect costs): $20,000

The overhead costs include utilities, depreciation of equipment, and factory rent.

The direct labor hours worked for each product are:

- Product A: 1,000 hours

- Product B: 500 hours

The goal is to allocate the $20,000 overhead to Product A and Product B based on direct labor hours.

Step 1: Identify the Cost Pool and Allocation Base

- Cost Pool: Manufacturing Overhead ($20,000)

- Allocation Base: Direct Labor Hours (1,000 + 500 = 1,500 hours total)

Step 2: Calculate the Overhead Rate

\[ \text{Overhead Rate} = \frac{\text{Total Overhead}}{\text{Total Direct Labor Hours}} = \frac{20,000}{1,500} = 13.33 \text{ per direct labor hour} \]

Step 3: Allocate Overhead to Each Product

- Product A: 1,000 hours × $13.33 = $13,333

- Product B: 500 hours × $13.33 = $6,667

Step 4: Calculate Total Product Costs

| Cost Component | Product A | Product B |

|---|---|---|

| Direct Materials | $30,000 | $20,000 |

| Direct Labor | $20,000 | $10,000 |

| Allocated Overhead | $13,333 | $6,667 |

| Total Cost | $63,333 | $36,667 |

Note: Direct materials and labor split assumed proportional to overhead allocation for simplicity.

Mind Map: Basic Cost Allocation Process

Additional Example: Using Machine Hours as Allocation Base

Suppose instead the company decides to allocate overhead based on machine hours.

-

Machine hours:

- Product A: 600 hours

- Product B: 900 hours

-

Total machine hours = 1,500

Overhead Rate:

\[ \frac{20,000}{1,500} = 13.33 \text{ per machine hour} \]

Allocated Overhead:

- Product A: 600 × 13.33 = $8,000

- Product B: 900 × 13.33 = $12,000

This changes the overhead allocation significantly, demonstrating the importance of choosing an appropriate allocation base.

Mind Map: Choosing an Allocation Base

Summary

This example illustrates the fundamental steps in allocating manufacturing overhead costs to products using a simple and commonly used method — direct labor hours. It also highlights how the choice of allocation base can impact the cost assigned to each product, affecting pricing, profitability analysis, and decision-making.

By applying these basic principles, accountants and cost analysts can ensure more accurate product costing and better financial insights in manufacturing environments.

2. Traditional Cost Allocation Methods

2.1 Overview of Traditional Methods

Traditional cost allocation methods have been the backbone of cost accounting for decades, especially in manufacturing and finance sectors. These methods primarily allocate indirect costs (overheads) to products or departments based on a single cost driver, such as labor hours or machine hours. While simpler than modern approaches like Activity-Based Costing (ABC), traditional methods remain widely used due to their straightforwardness and ease of implementation.

Key Characteristics of Traditional Methods:

- Use a single, volume-based cost driver

- Easy to understand and apply

- Suitable for homogeneous production environments

- May oversimplify cost behavior leading to less accurate product costing

Common Traditional Cost Allocation Methods

Direct Labor Hours Method

This method allocates overhead costs based on the number of labor hours worked on a product. It assumes that labor hours are the primary driver of overhead costs.

Example:

A manufacturing company has $100,000 in overhead costs and 5,000 direct labor hours for the month.

- Overhead rate = $100,000 / 5,000 hours = $20 per labor hour

- If Product A requires 10 labor hours, overhead allocated = 10 x $20 = $200

Best Practice: Use this method when labor is a major component of production and overhead costs correlate strongly with labor time.

Machine Hours Method

This method allocates overhead based on machine hours used, ideal for automated or machine-intensive manufacturing.

Example:

A factory incurs $150,000 overhead with 3,000 machine hours.

- Overhead rate = $150,000 / 3,000 hours = $50 per machine hour

- Product B uses 8 machine hours, overhead allocated = 8 x $50 = $400

Best Practice: Choose this method when machine usage drives overhead costs more than labor.

Material Cost Method

Allocates overhead based on the cost of materials used in production.

Example:

Overhead costs: $80,000

Total material cost: $400,000

- Overhead rate = $80,000 / $400,000 = 20%

- Product C uses $5,000 in materials, overhead allocated = 20% x $5,000 = $1,000

Best Practice: Use when material consumption is a significant driver of overhead.

Direct Labor Cost Method

Allocates overhead based on the total labor cost rather than hours.

Example:

Overhead: $120,000

Total labor cost: $600,000

- Overhead rate = $120,000 / $600,000 = 20%

- Product D labor cost: $10,000

- Overhead allocated = 20% x $10,000 = $2,000

Best Practice: Useful when labor cost variability better reflects overhead consumption than labor hours.

Summary Mind Map

Conclusion

Traditional cost allocation methods offer simplicity and ease of use, making them suitable for many manufacturing environments with relatively uniform production processes. However, their reliance on a single cost driver can lead to inaccuracies when overhead costs are driven by multiple factors. Accountants and cost analysts should carefully evaluate their production environment and overhead cost behavior to select the most appropriate traditional method or consider more sophisticated approaches when necessary.

2.2 Direct Labor Hours Method: Principles and Application

Overview

The Direct Labor Hours (DLH) method is one of the most traditional and widely used cost allocation techniques in manufacturing and finance. It allocates overhead costs based on the number of labor hours directly involved in producing a product or service. This method assumes that the consumption of overhead resources is directly proportional to the labor hours worked.

Principles of the Direct Labor Hours Method

- Cost Driver: Direct labor hours serve as the cost driver.

- Assumption: Overhead costs increase with labor hours.

- Applicability: Best suited for labor-intensive manufacturing environments.

- Calculation: Overhead Rate = Total Overhead Costs / Total Direct Labor Hours

Mind Map: Principles of Direct Labor Hours Method

Step-by-Step Application

- Identify Total Overhead Costs: Sum all indirect manufacturing costs (e.g., utilities, rent, depreciation).

- Measure Total Direct Labor Hours: Aggregate all labor hours spent on production.

- Calculate Overhead Rate: Divide total overhead by total direct labor hours.

- Allocate Overhead: Multiply the overhead rate by the direct labor hours for each product/job.

Example 1: Basic Overhead Allocation

Scenario:

- Total Overhead Costs: $120,000

- Total Direct Labor Hours: 10,000 hours

- Product A: 200 direct labor hours

- Product B: 300 direct labor hours

Calculation:

- Overhead Rate = $120,000 / 10,000 = $12 per direct labor hour

- Overhead allocated to Product A = 200 * $12 = $2,400

- Overhead allocated to Product B = 300 * $12 = $3,600

Mind Map: Example 1 Breakdown

Best Practices When Using the Direct Labor Hours Method

- Ensure Accurate Labor Tracking: Use timekeeping systems to capture precise labor hours.

- Review Overhead Components: Confirm that overhead costs are relevant and consistently categorized.

- Evaluate Method Suitability: Use DLH primarily in labor-intensive environments; consider alternative methods if automation dominates.

- Regularly Update Rates: Overhead rates should be recalculated periodically to reflect cost changes.

Example 2: Application in a Manufacturing Plant

Scenario: A furniture manufacturer wants to allocate overhead costs for two products: Chairs and Tables.

- Total Overhead Costs: $250,000

- Total Direct Labor Hours: 20,000 hours

- Chairs: 8,000 direct labor hours

- Tables: 12,000 direct labor hours

Calculation:

- Overhead Rate = $250,000 / 20,000 = $12.50 per direct labor hour

- Overhead allocated to Chairs = 8,000 * $12.50 = $100,000

- Overhead allocated to Tables = 12,000 * $12.50 = $150,000

Interpretation: The overhead allocation reflects the labor intensity of each product, helping management understand cost structure and pricing.

Mind Map: Example 2 Application

Advantages of the Direct Labor Hours Method

- Simple to understand and implement.

- Relies on easily measurable data (labor hours).

- Provides a reasonable allocation in labor-intensive settings.

Limitations

- May be inaccurate in automated or capital-intensive environments.

- Assumes overhead correlates only with labor hours, ignoring other drivers.

- Can distort product costs if labor hours do not reflect actual resource consumption.

Summary

The Direct Labor Hours method remains a foundational cost allocation technique, especially effective in environments where labor is a primary driver of overhead. By understanding its principles, applying best practices, and using clear examples, accountants and cost analysts can leverage this method to enhance cost accuracy and support managerial decision-making.

2.3 Machine Hours Method: When and How to Use

Overview

The Machine Hours Method is a traditional cost allocation technique that assigns overhead costs based on the number of machine hours consumed by a product or production process. This method is particularly useful in manufacturing environments where machinery plays a central role in production, and machine usage is a significant driver of overhead costs.

When to Use the Machine Hours Method

- High Machine Intensity: When production relies heavily on machines rather than manual labor.

- Overhead Costs Linked to Machine Usage: When overhead costs such as maintenance, depreciation, electricity, and repairs are closely related to machine operation.

- Consistent Machine Usage: When machine hours can be reliably tracked and are a consistent measure across products.

- Simpler Cost Structures: When the production process is relatively straightforward, and machine hours serve as a reasonable proxy for overhead consumption.

Mind Map: When to Use Machine Hours Method

How to Use the Machine Hours Method

- Identify Total Overhead Costs: Collect all indirect costs related to production that need allocation.

- Determine Total Machine Hours: Calculate the total machine hours used during the period.

- Calculate Overhead Rate per Machine Hour: \[ \text{Overhead Rate} = \frac{\text{Total Overhead Costs}}{\text{Total Machine Hours}} \]

- Allocate Overhead to Products: Multiply the overhead rate by the machine hours consumed by each product.

Mind Map: How to Use Machine Hours Method

Example 1: Basic Application in a Manufacturing Plant

Scenario: A manufacturing plant has total overhead costs of $120,000 for the month. The total machine hours recorded across all products are 4,000 hours.

Step 1: Calculate the overhead rate per machine hour:

\[ \text{Overhead Rate} = \frac{120,000}{4,000} = 30 \text{ USD per machine hour} \]

Step 2: Product A used 150 machine hours, and Product B used 250 machine hours.

Step 3: Allocate overhead:

- Product A: 150 hours × $30 = $4,500

- Product B: 250 hours × $30 = $7,500

This allocation reflects the overhead costs based on machine usage.

Example 2: Applying Machine Hours Method with Multiple Products

Scenario: A factory produces three products: X, Y, and Z. Overhead costs total $200,000, and total machine hours are 5,000.

| Product | Machine Hours Used |

|---|---|

| X | 1,200 |

| Y | 2,000 |

| Z | 1,800 |

Step 1: Calculate overhead rate:

\[ \frac{200,000}{5,000} = 40 \text{ USD per machine hour} \]

Step 2: Allocate overhead:

- Product X: 1,200 × $40 = $48,000

- Product Y: 2,000 × $40 = $80,000

- Product Z: 1,800 × $40 = $72,000

Best Practices for Using Machine Hours Method

- Accurate Tracking: Ensure machine hours are recorded accurately using automated systems or reliable logs.

- Review Overhead Components: Confirm that overhead costs are indeed driven by machine usage to avoid misallocation.

- Combine with Other Methods if Needed: For complex environments, consider supplementing with other allocation bases like labor hours.

- Regular Updates: Recalculate overhead rates periodically to reflect changes in costs or machine usage.

Mind Map: Best Practices

Summary

The Machine Hours Method is a straightforward and effective cost allocation technique when overhead costs are closely tied to machine usage. By carefully tracking machine hours and overhead costs, accountants and cost analysts can allocate costs fairly and support better pricing, budgeting, and financial decision-making in manufacturing environments.

2.4 Material Cost Method: Allocation Based on Material Usage

Overview

The Material Cost Method is a traditional cost allocation approach where overhead costs are allocated to products based on the amount of material cost each product consumes. This method assumes that material usage is the primary driver of overhead costs, making it particularly useful in manufacturing environments where material consumption significantly influences indirect costs.

Why Use the Material Cost Method?

- Simplicity: Easy to calculate and understand.

- Relevance: Effective when material costs form a large portion of total costs.

- Fairness: Allocates overhead in proportion to material consumption.

How It Works

- Determine Total Overhead Costs: Sum all indirect costs to be allocated.

- Calculate Total Material Costs: Aggregate material costs for all products.

- Compute Allocation Rate: \[ \text{Overhead Allocation Rate} = \frac{\text{Total Overhead Costs}}{\text{Total Material Costs}} \]

- Allocate Overhead to Each Product: \[ \text{Overhead Allocated to Product} = \text{Material Cost of Product} \times \text{Overhead Allocation Rate} \]

Mind Map: Material Cost Method

Example: Applying Material Cost Method in a Manufacturing Plant

Scenario: A furniture manufacturer produces two types of chairs: Wooden Chairs and Metal Chairs.

- Total overhead costs for the month: $40,000

- Material costs:

- Wooden Chairs: $120,000

- Metal Chairs: $80,000

Step 1: Calculate total material costs

\[ 120,000 + 80,000 = 200,000 \]

Step 2: Compute overhead allocation rate

\[ \frac{40,000}{200,000} = 0.20 \]

Step 3: Allocate overhead to each product

- Wooden Chairs: $120,000 x 0.20 = $24,000

- Metal Chairs: $80,000 x 0.20 = $16,000

Interpretation: The overhead is allocated proportionally to the material costs, reflecting the assumption that products consuming more materials incur more overhead.

Best Practices for Material Cost Method

- Validate Assumptions: Confirm that overhead costs are indeed driven by material consumption.

- Combine Methods: If overhead costs are influenced by multiple factors, consider blending material cost method with other allocation bases.

- Regular Review: Periodically reassess the allocation base to ensure continued relevance.

- Transparency: Document the rationale and calculations clearly for audit and reporting purposes.

Additional Mind Map: Best Practices in Material Cost Allocation

Limitations

- Overhead costs may not always correlate with material costs.

- Can distort product costing if labor or machine usage is a more significant driver.

- Less suitable for service-heavy or labor-intensive manufacturing.

Summary

The Material Cost Method is a straightforward and effective cost allocation technique when material consumption is a key driver of overhead. By allocating overhead proportionally to material costs, companies can achieve a fair distribution of indirect costs, aiding in accurate product costing and pricing decisions.

2.5 Best Practice: Choosing the Right Traditional Method for Your Business

Selecting the appropriate traditional cost allocation method is crucial for accurate cost management and informed decision-making in manufacturing and finance sectors. The choice depends on the nature of your production processes, cost behavior, and the availability of reliable data. Below, we explore best practices to guide you through this selection process, supported by mind maps and practical examples.

Key Considerations When Choosing a Traditional Cost Allocation Method

Step 1: Understand Your Production Process and Cost Drivers

- Direct Labor Hours are ideal when labor is the primary driver of overhead costs.

- Machine Hours suit highly automated processes where machinery usage drives costs.

- Material Cost allocation works well when material consumption significantly influences overhead.

Example: A small furniture manufacturer relies heavily on skilled carpenters. Since labor is the main cost driver, allocating overhead based on direct labor hours provides a more accurate reflection of resource consumption.

Step 2: Evaluate Data Availability and Reliability

Choose a method supported by accurate and readily available data.

- If machine usage data is logged precisely, machine hours method is feasible.

- If labor hours are tracked through timesheets, direct labor hours method is practical.

- If material costs are well documented per product, material cost allocation is effective.

Example: An electronics manufacturer uses automated machines with digital logs of machine hours, making the machine hours method both reliable and easy to implement.

Step 3: Balance Accuracy and Simplicity

While more detailed methods can improve accuracy, they may increase complexity and administrative burden.

- For small to medium enterprises, simpler methods like direct labor hours may suffice.

- Larger firms with diverse products might benefit from more precise methods.

Example: A startup manufacturing custom apparel opts for direct labor hours due to limited resources and simpler operations, while a large automotive plant uses machine hours for better precision.

Step 4: Test and Review the Method

Implement the chosen method on a trial basis and analyze its impact on cost accuracy and decision-making.

- Compare allocated costs with actual resource consumption.

- Adjust the method if discrepancies are significant.

Example: A food processing company initially used material cost allocation but found overhead allocation skewed. After testing, they switched to machine hours, which better matched actual overhead usage.

Summary Table of Traditional Methods and Best Use Cases

| Method | Best Used When | Data Needed | Pros | Cons |

|---|---|---|---|---|

| Direct Labor Hours | Labor-intensive production | Labor hours | Simple, easy to track | Less accurate if labor not main driver |

| Machine Hours | Automated, machine-driven processes | Machine usage hours | Reflects machine overhead well | Requires reliable machine data |

| Material Cost | Material-heavy production | Material cost per product | Aligns overhead with material use | May ignore labor/machine impact |

Practical Example: Choosing a Method for a Manufacturing Firm

Scenario: A medium-sized electronics manufacturer produces multiple product lines. The production process is a mix of automated assembly and manual inspection.

- Labor accounts for 30% of overhead.

- Machines consume 60% of overhead.

- Material costs are 10% of overhead.

Decision: Machine hours method is preferred due to the dominant machine-related overhead. However, labor hours can be tracked for secondary analysis.

Implementation:

- Collect machine hour data from automated logs.

- Allocate overhead proportionally based on machine hours.

Outcome: More accurate product costing, better pricing decisions, and improved profitability analysis.

Final Best Practice Tips

- Regularly review cost drivers and allocation bases as business processes evolve.

- Engage cross-functional teams (accountants, cost analysts, production managers) to validate assumptions.

- Document the rationale for method selection and maintain transparency.

- Use pilot studies to test methods before full-scale implementation.

By carefully considering these factors and applying the outlined best practices, accountants and cost analysts can select the most appropriate traditional cost allocation method tailored to their business needs, ensuring accuracy, efficiency, and strategic insight.

2.6 Example: Allocating Overhead Using Direct Labor Hours in a Factory

Overview

Allocating overhead costs using direct labor hours is one of the most traditional and widely used methods in manufacturing. This method assumes that overhead costs are incurred in proportion to the amount of direct labor hours worked.

Step-by-Step Example

Scenario: A factory produces two products: Product A and Product B.

- Total overhead costs for the period: $120,000

- Total direct labor hours worked: 6,000 hours

- Direct labor hours for Product A: 4,000 hours

- Direct labor hours for Product B: 2,000 hours

Objective: Allocate the $120,000 overhead to Product A and Product B based on their direct labor hours.

Step 1: Calculate the Overhead Rate per Direct Labor Hour

\[ \text{Overhead Rate} = \frac{\text{Total Overhead Costs}}{\text{Total Direct Labor Hours}} = \frac{120,000}{6,000} = 20 \text{ per direct labor hour} \]

Step 2: Allocate Overhead to Each Product

- Product A Overhead = 4,000 hours * $20 = $80,000

- Product B Overhead = 2,000 hours * $20 = $40,000

Step 3: Summarize Allocation

| Product | Direct Labor Hours | Overhead Allocated |

|---|---|---|

| Product A | 4,000 | $80,000 |

| Product B | 2,000 | $40,000 |

| Total | 6,000 | $120,000 |

Mind Map: Direct Labor Hours Overhead Allocation

Best Practices Highlighted

- Use accurate labor hour tracking: Ensure direct labor hours are recorded precisely to avoid misallocation.

- Review overhead drivers: Confirm that direct labor hours are a reasonable driver of overhead costs in your factory.

- Combine with other methods if needed: For complex operations, consider supplementing with machine hours or activity-based costing.

Additional Example: Impact of Changing Labor Hours

Suppose Product B increases production, raising its direct labor hours to 3,000, while Product A drops to 3,000 hours.

- New total labor hours = 3,000 + 3,000 = 6,000

- Overhead rate remains $20 per hour.

Allocated overhead:

- Product A: 3,000 * $20 = $60,000

- Product B: 3,000 * $20 = $60,000

This shows how changes in labor hours directly impact overhead allocation.

Visual Mind Map: Impact of Labor Hour Changes

Summary

Allocating overhead using direct labor hours is straightforward and effective when labor is a primary cost driver. It provides clear visibility into how overhead is distributed based on workforce effort. However, accountants and cost analysts should evaluate if this method aligns with their factory’s cost structure and consider alternative methods when overhead is influenced by other factors such as machine usage or complexity of operations.

3. Activity-Based Costing (ABC)

3.1 Introduction to Activity-Based Costing (ABC)

Activity-Based Costing (ABC) is a refined approach to cost allocation that assigns overhead and indirect costs to products and services based on the activities that generate those costs. Unlike traditional costing methods that allocate costs broadly (e.g., based on labor hours or machine hours), ABC provides a more accurate reflection of resource consumption by identifying specific activities and their cost drivers.

Why ABC Matters in Finance and Manufacturing

- Accuracy: ABC helps in pinpointing the true cost of producing a product or delivering a service by focusing on activities.

- Decision-Making: Enables better pricing, budgeting, and cost control decisions.

- Cost Management: Identifies non-value-added activities that can be optimized or eliminated.

Core Concepts of ABC

How ABC Works: Step-by-Step

- Identify Activities: Break down the production or service process into distinct activities (e.g., setup, inspection, material handling).

- Assign Costs to Activities: Collect costs related to each activity to form cost pools.

- Determine Cost Drivers: Identify factors that cause the cost of each activity (e.g., number of setups, inspection hours).

- Calculate Activity Rates: Divide total activity cost by total cost driver units.

- Assign Costs to Products: Multiply activity rates by the amount of cost driver consumed by each product.

Example: Applying ABC in a Manufacturing Environment

Scenario: A company produces two products, Product A and Product B. Both products use the same machine but differ in setup time and inspection requirements.

| Activity | Cost Pool ($) | Cost Driver | Total Driver Units | Product A Usage | Product B Usage |

|---|---|---|---|---|---|

| Machine Setup | 10,000 | Number of setups | 50 | 30 | 20 |

| Inspection | 5,000 | Inspection hours | 100 | 60 | 40 |

| Machine Usage | 15,000 | Machine hours | 1,000 | 600 | 400 |

Step 1: Calculate activity rates:

- Setup rate = $10,000 / 50 setups = $200 per setup

- Inspection rate = $5,000 / 100 hours = $50 per inspection hour

- Machine usage rate = $15,000 / 1,000 hours = $15 per machine hour

Step 2: Assign costs to products:

- Product A: (30 setups * $200) + (60 inspection hours * $50) + (600 machine hours * $15) = $6,000 + $3,000 + $9,000 = $18,000

- Product B: (20 setups * $200) + (40 inspection hours * $50) + (400 machine hours * $15) = $4,000 + $2,000 + $6,000 = $12,000

This example illustrates how ABC allocates overhead more precisely based on actual activity consumption rather than a single broad measure.

Best Practice Tips for Introducing ABC

- Start with high-overhead areas where traditional costing is less accurate.

- Engage cross-functional teams to identify relevant activities.

- Use software tools to simplify data collection and analysis.

- Regularly review and update cost drivers to reflect process changes.

Additional Mind Map: Benefits vs Challenges of ABC

By adopting Activity-Based Costing, accountants and cost analysts in finance and manufacturing sectors can gain deeper insights into cost behavior, enabling more strategic financial management and operational improvements.

3.2 Identifying Activities and Cost Drivers

In Activity-Based Costing (ABC), accurately identifying activities and their corresponding cost drivers is fundamental to allocating costs precisely. This process ensures that overhead and indirect costs are traced to products or services based on the actual consumption of resources.

What Are Activities?

Activities are the specific tasks or processes that consume resources within an organization. They represent what causes costs to be incurred.

Examples of Activities in Manufacturing:

- Machine setup

- Quality inspection

- Material handling

- Assembly

- Packaging

What Are Cost Drivers?

Cost drivers are factors that cause changes in the cost of an activity. They serve as the basis for assigning costs to products or services.

Examples of Cost Drivers:

- Number of setups

- Inspection hours

- Number of material moves

- Assembly labor hours

- Number of packages

Mind Map: Identifying Activities

Mind Map: Identifying Cost Drivers

Step-by-Step Process to Identify Activities and Cost Drivers

- Conduct Process Analysis: Map out all processes involved in production or service delivery.

- List All Activities: Break down processes into discrete activities that consume resources.

- Determine Resource Consumption: Understand how each activity uses resources.

- Identify Cost Drivers: Find measurable factors that directly influence the cost of each activity.

- Validate with Data: Use historical data or time studies to confirm the relevance of cost drivers.

Example 1: Identifying Activities and Cost Drivers in a Furniture Manufacturing Plant

| Activity | Description | Cost Driver |

|---|---|---|

| Machine Setup | Preparing machines for production | Number of setups |

| Assembly | Putting parts together | Labor hours |

| Quality Inspection | Checking product quality | Number of inspections |

| Packaging | Packing finished goods | Number of packages |

Explanation:

- The number of setups drives the cost of machine setup because each setup requires time and resources.

- Labor hours are a good driver for assembly since labor intensity varies with assembly time.

- Quality inspection costs are driven by how many inspections are performed.

- Packaging costs depend on the quantity of packages used.

Example 2: Identifying Activities and Cost Drivers in an Electronics Manufacturing Company

| Activity | Description | Cost Driver |

|---|---|---|

| Component Testing | Testing electronic components | Testing hours |

| PCB Assembly | Assembling printed circuit boards | Number of PCBs |

| Rework | Correcting defects | Number of rework hours |

| Shipping | Preparing and sending products | Number of shipments |

Explanation:

- Testing hours directly affect the cost of component testing.

- The number of PCBs assembled drives PCB assembly costs.

- Rework hours reflect the effort spent fixing defects.

- Shipping costs are influenced by the number of shipments.

Best Practice Tips for Identifying Activities and Cost Drivers

- Engage Cross-Functional Teams: Involve personnel from production, finance, and operations to get a comprehensive view.

- Use Time and Motion Studies: Collect data on how long activities take to improve accuracy.

- Focus on Cause-and-Effect Relationships: Ensure cost drivers logically influence the cost of activities.

- Keep It Manageable: Avoid excessive granularity that complicates the system without adding value.

By carefully identifying activities and their cost drivers, accountants and cost analysts can build a robust ABC system that enhances cost accuracy and supports better decision-making.

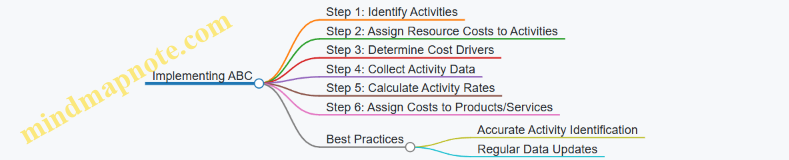

3.3 Steps to Implement Activity-Based Costing (ABC) in Manufacturing

Implementing Activity-Based Costing (ABC) in a manufacturing environment involves a structured approach to accurately trace overhead and indirect costs to products based on the activities that generate those costs. Below is a detailed step-by-step guide, complemented by mind maps and practical examples to help accountants and cost analysts understand and apply ABC effectively.

Step 1: Identify and Define Activities

The first step is to identify all the significant activities involved in the manufacturing process. Activities are tasks or functions that consume resources and incur costs.

Example: In a furniture manufacturing plant, activities might include cutting, assembling, finishing, quality inspection, and packaging.

Mind Map:

Step 2: Assign Resource Costs to Activities

Once activities are identified, assign the costs of resources (labor, materials, utilities, depreciation) to each activity. This creates activity cost pools.

Example: The electricity cost for running cutting machines is assigned to the “Cutting” activity cost pool.

Mind Map:

Step 3: Identify Cost Drivers for Each Activity

Cost drivers are factors that cause the cost of an activity to increase or decrease. Selecting appropriate cost drivers is critical for accurate allocation.

Example: Number of machine hours for “Cutting”, number of inspections for “Quality Inspection”, or number of setups for “Machine Setup”.

Mind Map:

Step 4: Collect Activity Data

Gather data on the frequency or intensity of each cost driver for the period under analysis.

Example: During the month, the cutting machines ran for 1,200 hours, and there were 300 quality inspections conducted.

Mind Map:

Step 5: Calculate Activity Rates

Divide the total cost in each activity cost pool by the total quantity of its cost driver to get the activity rate.

Formula: \[ \text{Activity Rate} = \frac{\text{Total Activity Cost}}{\text{Total Cost Driver Quantity}} \]

Example: If the total cost assigned to the Cutting activity is $60,000 and total machine hours are 1,200, then:

\[ \text{Cutting Activity Rate} = \frac{60,000}{1,200} = 50 \text{ per machine hour} \]

Mind Map:

Step 6: Assign Costs to Products Based on Activity Usage

Multiply the activity rate by the amount of cost driver consumed by each product to allocate costs accurately.

Example: Product A used 100 machine hours in Cutting, 150 labor hours in Assembling, and underwent 20 inspections.

- Cutting Cost = 100 hours * $50 = $5,000

- Assembling Cost = 150 hours * $50 = $7,500

- Quality Inspection Cost = 20 inspections * $50 = $1,000

Total overhead allocated to Product A = $5,000 + $7,500 + $1,000 = $13,500

Mind Map:

Step 7: Analyze and Review Results

Review the cost allocations for accuracy and reasonableness. Compare ABC results with traditional costing methods to identify discrepancies and areas for improvement.

Example: If traditional costing allocated $10,000 overhead to Product A but ABC shows $13,500, investigate the reasons such as higher activity consumption.

Mind Map:

Summary Example: Applying ABC in a Small Manufacturing Plant

| Activity | Total Cost | Cost Driver | Total Driver Quantity | Activity Rate | Product A Usage | Product A Cost Allocation |

|---|---|---|---|---|---|---|

| Cutting | $60,000 | Machine Hours | 1,200 hours | $50/hour | 100 hours | $5,000 |

| Assembling | $40,000 | Labor Hours | 800 hours | $50/hour | 150 hours | $7,500 |

| Quality Inspection | $15,000 | Number of Inspections | 300 inspections | $50/inspection | 20 inspections | $1,000 |

Total overhead allocated to Product A = $13,500

By following these steps, manufacturing firms can implement ABC to gain more accurate insights into product costs, enabling better pricing, budgeting, and strategic decision-making.

3.4 Best Practice: Ensuring Accurate Activity Identification

Accurate activity identification is the cornerstone of effective Activity-Based Costing (ABC). Without correctly identifying the activities that consume resources, cost allocation will be flawed, leading to poor decision-making and distorted product or service costs. This section explores best practices to ensure precise activity identification, supported by illustrative mind maps and practical examples.

Why Accurate Activity Identification Matters

- Activities represent the fundamental units where costs are incurred.

- Misidentification can lead to under- or over-costing products.

- Enables better understanding of cost drivers and resource consumption.

Best Practices for Accurate Activity Identification

-

Engage Cross-Functional Teams

- Include representatives from production, finance, operations, and quality control.

- Diverse perspectives help uncover hidden or overlooked activities.

-

Use Process Mapping Techniques

- Visualize workflows to identify discrete activities.

- Helps in breaking down complex processes into manageable components.

-

Conduct Interviews and Observations

- Talk to employees performing the work.

- Observe daily operations to capture implicit activities.

-

Classify Activities by Level

- Unit-level: Activities performed for each unit produced.

- Batch-level: Activities performed for a batch of units.

- Product-level: Activities related to specific products.

- Facility-level: Activities supporting overall operations.

-

Validate Activities with Data

- Use historical cost data and time logs.

- Confirm that identified activities correspond to actual resource consumption.

-

Iterate and Refine

- Activity identification is not one-time; revisit periodically.

- Adjust as processes and products evolve.

Mind Map: Steps to Identify Activities Accurately

Example 1: Activity Identification in a Manufacturing Plant

Scenario: A manufacturer produces custom furniture and wants to implement ABC.

- Step 1: Cross-functional team formed including production supervisors, accountants, and quality inspectors.

- Step 2: Process mapping revealed activities such as cutting, sanding, assembling, finishing, and quality inspection.

- Step 3: Interviews uncovered additional activities like machine setup and maintenance.

- Step 4: Activities classified:

- Unit-level: sanding, assembling

- Batch-level: machine setup

- Product-level: design customization

- Facility-level: factory cleaning

- Step 5: Time logs and cost data validated the frequency and resource consumption of each activity.

- Outcome: Accurate activity list enabled precise overhead allocation, revealing that machine setup was a significant cost driver for small batches.

Mind Map: Example Activities in Custom Furniture Manufacturing

Example 2: Activity Identification in a Cost Analyst Role

Scenario: A cost analyst at an electronics manufacturer is tasked with identifying activities for ABC implementation.

- Step 1: Analyst reviews production workflows and consults with line managers.

- Step 2: Observes assembly line and documents activities such as component testing, soldering, packaging.

- Step 3: Identifies support activities like equipment calibration and inventory management.

- Step 4: Classifies activities and assigns preliminary cost drivers.

- Step 5: Uses software to track time spent on each activity for validation.

- Outcome: The analyst discovers that equipment calibration, previously overlooked, is a significant cost driver affecting product quality and warranty costs.

Tips for Accountants and Cost Analysts

- Always corroborate activity lists with multiple data sources.

- Avoid overly broad activities; specificity improves cost accuracy.

- Document assumptions and rationale for activity identification.

- Use technology tools like workflow software and time-tracking systems to enhance accuracy.

By following these best practices, finance and manufacturing professionals can ensure that their ABC systems reflect true resource consumption, leading to better cost control, pricing strategies, and profitability analysis.

3.5 Example: Applying ABC to Allocate Overhead in a Multi-Product Environment

Activity-Based Costing (ABC) is particularly useful in multi-product environments where overhead costs are not uniformly consumed by all products. This example demonstrates how ABC can allocate overhead more accurately by tracing costs to activities and then to products based on their actual consumption.

Scenario Overview:

A manufacturing company produces two products: Product A and Product B. The company incurs the following overhead costs:

- Machine Setup Costs: $50,000

- Quality Inspection Costs: $30,000

- Material Handling Costs: $20,000

The company identifies three main activities driving overhead costs:

- Machine Setups

- Quality Inspections

- Material Handling

The cost drivers and their usage by each product are:

| Activity | Cost Driver | Product A Usage | Product B Usage |

|---|---|---|---|

| Machine Setups | Number of Setups | 100 setups | 50 setups |

| Quality Inspections | Number of Inspections | 200 inspections | 100 inspections |

| Material Handling | Weight of Materials | 10,000 kg | 30,000 kg |

Step 1: Calculate Cost Driver Rates

For each activity, calculate the cost per unit of the cost driver:

- Machine Setup Rate = $50,000 / (100 + 50) setups = $50,000 / 150 = $333.33 per setup

- Quality Inspection Rate = $30,000 / (200 + 100) inspections = $30,000 / 300 = $100 per inspection

- Material Handling Rate = $20,000 / (10,000 + 30,000) kg = $20,000 / 40,000 = $0.50 per kg

Step 2: Allocate Overhead to Products

Multiply the cost driver rate by the usage for each product:

| Activity | Product A Allocation | Product B Allocation |

|---|---|---|

| Machine Setups | 100 setups * $333.33 = $33,333 | 50 setups * $333.33 = $16,667 |

| Quality Inspections | 200 inspections * $100 = $20,000 | 100 inspections * $100 = $10,000 |

| Material Handling | 10,000 kg * $0.50 = $5,000 | 30,000 kg * $0.50 = $15,000 |

Step 3: Total Overhead Allocated

- Product A Total Overhead = $33,333 + $20,000 + $5,000 = $58,333

- Product B Total Overhead = $16,667 + $10,000 + $15,000 = $41,667

Mind Map: ABC Overhead Allocation Process

Best Practice Tips:

- Identify Relevant Activities: Focus on activities that significantly consume overhead resources.

- Use Accurate Cost Drivers: Select drivers that closely correlate with the consumption of resources.

- Gather Reliable Data: Ensure the usage data for each product is accurate and up-to-date.

- Review Periodically: Regularly update cost drivers and rates to reflect changes in operations.

Additional Example: Simplified ABC for a Furniture Manufacturer

- Activities: Wood Cutting, Assembly, Finishing

- Overhead Costs: $60,000 (Wood Cutting), $40,000 (Assembly), $20,000 (Finishing)

- Cost Drivers: Machine Hours, Labor Hours, Number of Finishing Batches

| Activity | Cost Driver | Product X Usage | Product Y Usage |

|---|---|---|---|

| Wood Cutting | Machine Hours | 300 hours | 700 hours |

| Assembly | Labor Hours | 500 hours | 500 hours |

| Finishing | Number of Batches | 20 batches | 30 batches |

Calculate rates and allocate costs similarly to the main example.

This example highlights how ABC provides a nuanced and fair allocation of overhead costs, improving product costing accuracy and supporting better pricing and profitability decisions in multi-product manufacturing environments.

3.6 Benefits and Challenges of Activity-Based Costing (ABC)

Activity-Based Costing (ABC) is a powerful method for allocating overhead costs more accurately by linking costs to specific activities and cost drivers. While ABC offers many advantages, it also presents certain challenges that organizations need to consider.

Benefits of ABC

-

Improved Cost Accuracy

- ABC assigns overhead costs based on actual activities, reducing distortions caused by traditional allocation methods.

- This leads to more precise product costing and better pricing decisions.

-

Enhanced Decision-Making

- By understanding the true cost drivers, managers can identify inefficient processes and areas for cost reduction.

- Supports strategic decisions such as product mix, outsourcing, and process improvements.

-

Better Resource Allocation

- ABC highlights high-cost activities, enabling more focused resource management.

-

Supports Continuous Improvement

- Provides detailed insights into activities, facilitating lean initiatives and process optimization.

-

Facilitates Profitability Analysis

- Helps identify profitable and unprofitable products, customers, or services.

Challenges of ABC

-

Complexity and Implementation Effort

- ABC requires detailed data collection on activities and cost drivers, which can be time-consuming.

- Implementation may need cross-departmental collaboration and training.

-

Data Maintenance

- Maintaining up-to-date activity data and cost drivers requires ongoing effort.

-

Cost of Implementation

- Initial setup and software tools can be expensive.

-

Resistance to Change

- Employees and managers may resist new costing methods due to unfamiliarity or perceived complexity.

-

Potential Overhead

- In some cases, the level of detail may not justify the benefits, especially for smaller organizations.

Mind Map: Benefits of ABC

Mind Map: Challenges of ABC

Example 1: Improved Cost Accuracy in a Multi-Product Manufacturing Plant

A manufacturing company produces three products: A, B, and C. Traditional costing allocated overhead based on direct labor hours, resulting in Product A appearing highly profitable while Product C seemed marginal.

Using ABC, the company identified that Product C required more machine setups and quality inspections, which were costly activities not captured by labor hours alone. By allocating overhead based on actual activities, Product C’s cost increased, revealing its true profitability and prompting management to reconsider pricing and process improvements.

Example 2: Challenge of Data Collection

A mid-sized electronics manufacturer attempted to implement ABC but found that tracking every activity and its drivers was overwhelming. The finance team had to collect data from multiple departments, leading to delays and incomplete information. To address this, they prioritized key activities that consumed the most resources and simplified the ABC model, balancing accuracy with practicality.

Summary

While ABC provides detailed and accurate cost information that can significantly improve financial insights and decision-making, it requires careful planning, commitment, and resources to implement effectively. Organizations should weigh the benefits against the challenges and consider starting with a pilot project or simplified ABC model before full-scale adoption.

4. Time-Driven Activity-Based Costing (TDABC)

4.1 Understanding TDABC and Its Evolution from ABC

Time-Driven Activity-Based Costing (TDABC) is an advanced cost allocation methodology that evolved from the traditional Activity-Based Costing (ABC) system. While ABC focuses on identifying multiple activities and assigning costs based on various cost drivers, TDABC simplifies this process by using time as the primary cost driver, making it more practical and easier to implement, especially in complex manufacturing and finance environments.

What is Activity-Based Costing (ABC)?

ABC assigns overhead and indirect costs to products or services based on the activities required to produce them. It involves:

- Identifying activities that consume resources

- Determining cost drivers for each activity

- Allocating costs based on the usage of these drivers

Example: In a manufacturing plant, activities might include machine setups, inspections, and material handling. Costs are allocated based on how many setups or inspections each product requires.

Limitations of Traditional ABC

- Complexity: Requires detailed data collection on numerous activities and cost drivers.

- Time-consuming: Frequent updates needed to keep cost drivers accurate.

- High implementation and maintenance costs.

These limitations led to the development of TDABC.

What is Time-Driven Activity-Based Costing (TDABC)?

TDABC simplifies ABC by focusing on two parameters:

- Capacity Cost Rate: The cost of supplying resource capacity per unit of time (e.g., cost per minute or hour).

- Time Estimates: The time required to perform each activity.

Costs are allocated by multiplying the capacity cost rate by the time required for each activity.

Mind Map: Evolution from ABC to TDABC

How TDABC Works: Step-by-Step

-

Calculate Capacity Cost Rate:

- Determine total cost of resources (e.g., labor, equipment) available.

- Estimate practical capacity (e.g., available minutes per period).

- Capacity Cost Rate = Total Resource Cost / Practical Capacity.

-

Estimate Time for Activities:

- Measure or estimate the time required to perform each activity.

-

Assign Costs:

- Multiply the time estimate by the capacity cost rate to allocate costs.

Example: Applying TDABC in an Assembly Line

Scenario: A manufacturing company wants to allocate overhead costs for its assembly line.

- Total overhead cost for assembly workers: $600,000 per year.

- Practical capacity: 120,000 minutes per year (accounting for breaks, maintenance).

Step 1: Calculate Capacity Cost Rate

- Capacity Cost Rate = $600,000 / 120,000 minutes = $5 per minute.

Step 2: Estimate Time per Product

- Product A requires 10 minutes of assembly.

- Product B requires 15 minutes of assembly.

Step 3: Allocate Costs

- Product A overhead cost = 10 minutes * $5 = $50.

- Product B overhead cost = 15 minutes * $5 = $75.

This method provides a straightforward and transparent way to allocate overhead based on time, reducing complexity compared to traditional ABC.

Mind Map: TDABC Components

Benefits of TDABC Over ABC

- Simplicity: Requires fewer data points, focusing mainly on time.

- Flexibility: Easier to update as time estimates or capacity change.

- Accuracy: Reflects actual resource consumption more closely when time is a reliable driver.

- Cost-Effective: Lower implementation and maintenance costs.

Practical Tips for Accountants and Cost Analysts

- Use time studies or historical data to estimate activity times accurately.

- Regularly review capacity assumptions to reflect changes in workforce or equipment availability.

- Combine TDABC with other costing methods if certain activities are not time-driven.

Summary

TDABC represents a practical evolution of ABC, focusing on time as the primary cost driver to simplify and improve cost allocation. It is particularly useful in manufacturing environments where time spent on activities directly correlates with resource consumption. By understanding and implementing TDABC, accountants and cost analysts can achieve more accurate product costing with less complexity.

4.2 Calculating Capacity Cost Rate

The Capacity Cost Rate (CCR) is a fundamental component of Time-Driven Activity-Based Costing (TDABC). It represents the cost of supplying capacity for a resource per unit of time, typically expressed as cost per minute or cost per hour. Calculating the CCR accurately allows organizations to assign costs based on the actual time resources are available and used, leading to more precise cost allocation.

What is Capacity Cost Rate?

- Definition: The cost to supply one unit of resource capacity for a given period.

- Purpose: To translate resource costs into a time-based rate that can be applied to activities.

Formula for Capacity Cost Rate

\[ \text{Capacity Cost Rate} = \frac{\text{Total Cost of Resource Supply}}{\text{Practical Capacity of the Resource}} \]

- Total Cost of Resource Supply: Includes salaries, benefits, equipment depreciation, utilities, and other overheads related to the resource.

- Practical Capacity: The actual time the resource is available for productive work, excluding breaks, downtime, and non-productive periods.

Step-by-Step Calculation Process

- Identify the Resource: Determine the resource or department whose capacity cost rate you want to calculate (e.g., machine, labor group).

- Calculate Total Resource Cost: Sum all costs associated with the resource for a specific period (usually annually).

- Determine Practical Capacity: Calculate the total available working time minus non-productive time.

- Compute Capacity Cost Rate: Divide total resource cost by practical capacity.

Mind Map: Calculating Capacity Cost Rate

Example 1: Calculating CCR for a Machine Operator Group

- Resource: Machine Operators

- Total Annual Cost: $600,000 (including wages, benefits, and overheads)

- Working Hours per Year: 2,000 hours (based on 40 hours/week × 50 weeks)

- Non-productive Time: 10% (breaks, meetings, training)

Step 1: Calculate Practical Capacity

\[ \text{Practical Capacity} = 2,000 \times (1 - 0.10) = 1,800 \text{ hours} \]

Step 2: Calculate Capacity Cost Rate

\[ \text{CCR} = \frac{600,000}{1,800} = 333.33 \text{ dollars per hour} \]

Interpretation: Each hour of machine operator capacity costs the company $333.33.

Mind Map: Example 1 Breakdown

Example 2: Calculating CCR for a CNC Machine

- Resource: CNC Machine

- Total Annual Cost: $120,000 (depreciation, maintenance, electricity)

- Available Hours: 2,500 hours/year

- Downtime: 15% (maintenance, setup)

Step 1: Calculate Practical Capacity

\[ \text{Practical Capacity} = 2,500 \times (1 - 0.15) = 2,125 \text{ hours} \]

Step 2: Calculate Capacity Cost Rate

\[ \text{CCR} = \frac{120,000}{2,125} \approx 56.47 \text{ dollars per hour} \]

Interpretation: Operating the CNC machine costs approximately $56.47 per hour of available capacity.

Mind Map: Example 2 Breakdown

Best Practices for Calculating Capacity Cost Rate

- Use Practical Capacity, Not Theoretical: Avoid using 100% capacity; account for realistic downtime.

- Include All Relevant Costs: Factor in all costs related to the resource, including indirect costs.

- Regularly Update Data: Capacity and costs can change; update CCR calculations periodically.

- Segment Resources if Needed: Differentiate CCRs for different shifts or resource types if costs vary significantly.

Summary

Calculating the Capacity Cost Rate is a critical step in TDABC, enabling organizations to assign costs based on the actual time resources are available. By accurately determining the total cost and practical capacity, accountants and cost analysts can improve cost transparency and support better decision-making.

4.3 Assigning Time Estimates to Activities

Assigning accurate time estimates to activities is a critical step in Time-Driven Activity-Based Costing (TDABC). This process involves estimating how much time each activity consumes per unit of cost driver, which then helps in allocating costs more precisely based on actual resource usage.

Why Assign Time Estimates?

- Time is the primary cost driver in TDABC.

- Accurate time estimates ensure fair and realistic cost allocation.

- Helps identify inefficiencies and areas for process improvement.

Steps to Assign Time Estimates

-

Identify Activities Clearly

- Break down processes into discrete activities.

- Example: In a manufacturing line, activities could be “Machine Setup,” “Assembly,” “Quality Inspection.”

-

Determine Time per Activity Unit

- Measure the average time required to complete each activity for one unit of output or per transaction.

- Use direct observation, time studies, or historical data.

-

Validate Time Estimates

- Cross-check estimates with employees and supervisors.

- Adjust for variability and exceptions.

-

Document and Update Regularly

- Keep time estimates transparent and revisit periodically to reflect process changes.

Mind Map: Assigning Time Estimates to Activities

Example 1: Assembly Line Activity

Scenario: A manufacturing company wants to allocate costs for the “Assembly” activity.

- Observation shows it takes 15 minutes on average to assemble one unit.

- The capacity cost rate for the assembly resource is $40 per hour.

Calculation:

- Time per unit = 15 minutes = 0.25 hours

- Cost allocated per unit = 0.25 hours * $40/hour = $10

This means $10 of overhead is allocated to each unit for assembly.

Example 2: Customer Order Processing in Finance Department

Scenario: The finance department processes customer orders, and the activity “Order Verification” takes approximately 10 minutes per order.

- Capacity cost rate for finance staff is $60 per hour.

Calculation:

- Time per order = 10 minutes = 1/6 hour

- Cost allocated per order = (1/6) * $60 = $10

This helps allocate the finance department’s overhead accurately to each processed order.

Best Practices for Assigning Time Estimates

- Use a combination of methods (time studies, interviews, system logs) for accuracy.

- Consider variability by using average times or ranges.

- Engage employees in validating time estimates to improve buy-in and accuracy.

- Regularly update time estimates to reflect process improvements or changes.

Mind Map: Best Practices

By carefully assigning time estimates to each activity, organizations can leverage TDABC to gain a granular and realistic view of cost consumption, leading to better decision-making and cost control.

4.4 Best Practice: Simplifying Cost Allocation with TDABC

Time-Driven Activity-Based Costing (TDABC) offers a streamlined approach to cost allocation by focusing on the time required to perform activities and the cost per unit of time. This method simplifies the traditional ABC process by reducing the complexity involved in identifying numerous cost drivers and activities.

Key Principles to Simplify Cost Allocation with TDABC

- Calculate Capacity Cost Rate: Determine the cost of supplying capacity per time unit (e.g., cost per minute or hour).

- Estimate Time for Activities: Assign time estimates to each activity or process step.

- Multiply Time by Capacity Cost Rate: Allocate costs based on the actual time consumed.

- Minimize Data Collection Complexity: Use time estimates instead of detailed driver data.

Mind Map: Simplifying Cost Allocation with TDABC

Example 1: Assembly Line Cost Allocation

A manufacturing company wants to allocate overhead costs for its assembly line.

-

Step 1: Calculate Capacity Cost Rate

- Total overhead costs for assembly line resources: $600,000 per year

- Practical capacity: 120,000 minutes per year

- Capacity cost rate = $600,000 / 120,000 minutes = $5 per minute

-

Step 2: Estimate time per product

- Product A requires 10 minutes of assembly time

- Product B requires 15 minutes of assembly time

-

Step 3: Allocate overhead costs

- Product A overhead = 10 minutes x $5 = $50

- Product B overhead = 15 minutes x $5 = $75

This simple calculation replaces complex driver analysis and provides clear, actionable cost data.

Mind Map: Assembly Line TDABC Example

Best Practice Tips for Simplifying TDABC Implementation

- Start with High-Level Activities: Focus on major activities before drilling down.

- Use Practical Capacity: Base calculations on realistic available time, not theoretical maximums.

- Leverage Technology: Use time-tracking software or process monitoring tools to gather accurate time data.

- Regularly Update Time Estimates: Reflect changes in processes or resource availability.

- Communicate Clearly: Ensure all stakeholders understand the time-based allocation approach.

Example 2: Maintenance Department Cost Allocation

A maintenance department supports multiple production lines. Instead of tracking numerous cost drivers, the company estimates the average time spent on maintenance per line.

-

Total maintenance cost: $300,000

-

Practical capacity: 60,000 minutes

-

Capacity cost rate: $300,000 / 60,000 = $5 per minute

-

Maintenance time per line:

- Line 1: 2,000 minutes

- Line 2: 3,000 minutes

-

Allocated costs:

- Line 1: 2,000 x $5 = $10,000

- Line 2: 3,000 x $5 = $15,000

This approach reduces the administrative burden and improves transparency.

Mind Map: Maintenance Department TDABC Example

By focusing on time as the primary cost driver and simplifying data collection, TDABC enables finance and manufacturing professionals to allocate costs more efficiently and accurately. This best practice fosters better decision-making and cost management without the complexity of traditional ABC methods.

4.5 Example: Using TDABC to Allocate Costs in an Assembly Line

Time-Driven Activity-Based Costing (TDABC) simplifies cost allocation by assigning costs based on the time required to perform activities, multiplied by the cost per time unit of capacity. This method is particularly effective in environments like assembly lines where time and resource usage can be precisely measured.

Step 1: Calculate Capacity Cost Rate

The capacity cost rate is the cost of supplying capacity divided by the practical capacity of the resource (usually expressed in minutes or hours).

Example:

- Total cost of assembly line resources (labor, equipment, overhead): $600,000 per year

- Practical capacity: 120,000 minutes per year (e.g., 2,000 hours * 60 minutes)

Capacity Cost Rate = $600,000 / 120,000 minutes = $5 per minute

Step 2: Estimate Time Required for Each Activity

Identify key activities on the assembly line and estimate the time each takes per unit.

| Activity | Time per Unit (minutes) |

|---|---|

| Component Assembly | 10 |

| Quality Inspection | 5 |