Accounting for Intangible Assets

1. Introduction to Intangible Assets

1.1 Definition and Characteristics of Intangible Assets

Definition

Intangible assets are non-physical assets that provide long-term value to a business. Unlike tangible assets such as machinery or buildings, intangible assets lack a physical form but can be critical drivers of competitive advantage and revenue generation. They represent legal rights, intellectual property, or other non-monetary resources controlled by the company.

Key points:

- Non-monetary assets without physical substance

- Provide future economic benefits

- Controlled by the entity as a result of past events

Characteristics of Intangible Assets

Intangible assets have several defining characteristics that distinguish them from other asset types:

- Identifiability: The asset can be separated from the business and sold, transferred, licensed, rented, or exchanged, either individually or together with a related contract, identifiable asset, or liability.

- Control: The company has the power to obtain future economic benefits and restrict others’ access to those benefits.

- Future Economic Benefits: The asset is expected to generate cash flows or contribute to revenue generation in the future.

- Lack of Physical Substance: Unlike physical assets, intangible assets do not have a physical form.

Mind Map: Characteristics of Intangible Assets

Examples of Intangible Assets

| Asset Type | Description | Example Scenario |

|---|---|---|

| Patents | Exclusive rights to inventions | A tech company patents a new software algorithm |

| Trademarks | Brand names, logos, slogans | A startup registers its brand logo for protection |

| Copyrights | Rights over creative works | A software firm owns copyrights on its code |

| Customer Lists | Information about customers | A consulting firm’s database of clients |

| Goodwill | Excess paid over fair value in acquisitions | Purchase of a competitor with strong brand loyalty |

| Software | Internally developed or purchased software | Capitalized development costs for an app |

Practical Example

Consider a tech startup developing an innovative mobile app. The company files a patent for a unique algorithm embedded in the app. This patent is an intangible asset because:

- It is identifiable and separable (can be sold or licensed).

- The company controls the patent rights.

- It is expected to generate future economic benefits through licensing or exclusive use.

- It has no physical form.

Mind Map: Example - Patent as Intangible Asset

Summary

Understanding the definition and characteristics of intangible assets is fundamental for accountants and financial analysts. Recognizing these assets accurately ensures proper valuation, reporting, and strategic management within the finance and tech sectors.

1.2 Importance of Intangible Assets in Modern Business

Intangible assets have become a cornerstone of value creation in modern businesses, especially within the finance and technology sectors. Unlike tangible assets such as machinery or buildings, intangible assets are non-physical but often represent the most significant portion of a company’s market value.

Why Intangible Assets Matter

- Value Drivers: Intangible assets like intellectual property, brand reputation, and proprietary technology often drive competitive advantage and revenue growth.

- Market Differentiation: They help companies differentiate their products and services in crowded markets.

- Investor Perception: Investors increasingly focus on intangible assets when evaluating company potential, especially in tech-driven industries.

- Mergers & Acquisitions: Intangible assets frequently represent a large portion of acquisition premiums, such as goodwill and patents.

Mind Map: Key Roles of Intangible Assets in Business

Examples Demonstrating Importance

-

Tech Startup Example:

- A software startup develops a unique algorithm that significantly improves data processing speed.

- This algorithm is protected by patents (intangible asset) and forms the core product offering.

- Despite minimal physical assets, the startup’s valuation is driven by this intangible asset.

-

Brand Value in Consumer Tech:

- Apple Inc.’s brand is one of its most valuable intangible assets.

- The brand loyalty and recognition allow premium pricing and sustained revenue.

-

Pharmaceutical Industry:

- Patents on drugs provide exclusive rights, enabling companies to recoup R&D investments.

- The intangible asset of a patent can be worth billions and is critical in financial reporting.

Mind Map: Impact Areas of Intangible Assets

Practical Insight

For accountants and financial analysts, understanding the importance of intangible assets helps in:

- Accurately valuing companies, especially in tech and finance sectors where intangibles dominate.

- Advising on investment decisions by assessing the quality and sustainability of intangible assets.

- Ensuring compliance with accounting standards that govern recognition, measurement, and disclosure.

In summary, intangible assets are not just abstract concepts but vital components that shape business success and financial health in the modern economy.

1.3 Types of Intangible Assets: Identifiable vs. Unidentifiable

Intangible assets are non-physical assets that provide long-term value to a company. Understanding the distinction between identifiable and unidentifiable intangible assets is crucial for proper accounting treatment.

Identifiable Intangible Assets

An intangible asset is considered identifiable if it meets either of the following criteria:

- It is separable, meaning it can be separated or divided from the entity and sold, transferred, licensed, rented, or exchanged.

- It arises from contractual or other legal rights, regardless of whether those rights are transferable or separable.

Examples of Identifiable Intangible Assets:

- Patents

- Trademarks

- Copyrights

- Customer lists

- Software licenses

- Franchise agreements

Mind Map: Identifiable Intangible Assets

Example:

A tech company purchases a patent for a new algorithm. Since the patent is a legal right and can be sold or licensed, it is an identifiable intangible asset and should be recognized on the balance sheet.

Unidentifiable Intangible Assets

Unidentifiable intangible assets cannot be separated from the business and do not arise from contractual or legal rights. These assets are often internally generated and are typically recognized as goodwill during business combinations.

Examples of Unidentifiable Intangible Assets:

- Goodwill

- Brand reputation (when not legally protected)

- Workforce expertise

- Customer loyalty (when not separately identifiable)

Mind Map: Unidentifiable Intangible Assets

Example:

When a company acquires another business for a price higher than the fair value of its identifiable net assets, the excess amount is recorded as goodwill. This goodwill reflects unidentifiable assets such as brand reputation and employee expertise.

Summary Table

| Feature | Identifiable Intangible Assets | Unidentifiable Intangible Assets |

|---|---|---|

| Separability | Yes | No |

| Legal/Contractual Rights | Yes | No |

| Examples | Patents, Trademarks, Customer Lists | Goodwill, Brand Reputation, Workforce |

| Recognition on Balance Sheet | Yes | Only as Goodwill during acquisition |

Practical Example: Differentiating Intangible Assets in a Tech Startup

Imagine a tech startup that develops proprietary software and has a strong brand presence but no registered trademarks yet.

- The proprietary software code, if capitalized, is an identifiable intangible asset because it can be separated and licensed.

- The brand reputation, while valuable, is unidentifiable because it is not legally protected and cannot be sold separately.

This distinction affects how the startup reports these assets in its financial statements.

By clearly distinguishing between identifiable and unidentifiable intangible assets, accountants and financial analysts can apply the correct recognition, measurement, and disclosure principles, ensuring compliance with accounting standards and providing transparent financial information.

1.4 Overview of Accounting Standards Governing Intangibles (IAS 38, ASC 350)

Intangible assets are governed by specific accounting standards that provide guidance on recognition, measurement, amortization, and disclosure. The two primary frameworks are IAS 38 under IFRS and ASC 350 under US GAAP. Understanding these standards is essential for accountants and financial analysts to ensure compliance and accurate financial reporting.

IAS 38 - Intangible Assets (IFRS)

IAS 38 provides comprehensive guidance on accounting for intangible assets except those covered by other standards (e.g., goodwill, financial assets).

Key Points of IAS 38:

-

Recognition Criteria:

- Identifiability (separable or arising from contractual/legal rights)

- Control over the asset

- Future economic benefits expected

- Cost can be reliably measured

-

Measurement:

- Initially measured at cost

- Subsequent measurement can be either:

- Cost model (cost less accumulated amortization and impairment)

- Revaluation model (fair value less accumulated amortization and impairment, if fair value can be reliably measured)

-

Amortization:

- Finite life intangibles amortized over useful life

- Indefinite life intangibles not amortized but tested annually for impairment

-

Impairment:

- Tested for impairment whenever there is an indication of impairment

-

Disclosures:

- Useful lives or amortization rates

- Amortization methods

- Gross carrying amount and accumulated amortization

- Reconciliation of carrying amount at beginning and end of period

ASC 350 - Intangibles - Goodwill and Other (US GAAP)

ASC 350 focuses on goodwill and other intangible assets, providing guidance on recognition, measurement, amortization, and impairment.

Key Points of ASC 350:

-

Recognition:

- Intangible assets acquired in a business combination are recognized separately from goodwill if they are identifiable

-

Measurement:

- Initially measured at fair value

- Subsequent measurement generally at cost less accumulated amortization and impairment

-

Amortization:

- Intangibles with finite lives amortized over useful life

- Indefinite-lived intangibles (including goodwill) not amortized but tested annually for impairment

-

Impairment:

- Two-step impairment test for goodwill (simplified in recent updates)

- Other intangibles tested for impairment when indicators exist

-

Disclosures:

- Description of intangible assets

- Amortization expense

- Remaining amortization period

- Impairment losses recognized

Mind Map: IAS 38 Overview

Mind Map: ASC 350 Overview

Practical Example: Applying IAS 38 and ASC 350

Scenario: A tech company acquires a patent and a trademark as part of a business combination.

-

Under IAS 38:

- The patent and trademark are identifiable intangible assets.

- They are initially recognized at cost (fair value at acquisition).

- The patent has a finite life of 15 years and will be amortized on a straight-line basis.

- The trademark is considered to have an indefinite life and is not amortized but tested annually for impairment.

-

Under ASC 350:

- Both patent and trademark are recognized at fair value at acquisition.

- The patent is amortized over its useful life.

- The trademark is classified as indefinite-lived and tested annually for impairment.

Best Practice: Maintain detailed documentation of the acquisition, valuation methods, useful life assessments, and impairment testing assumptions to ensure transparency and audit readiness.

Summary

Understanding IAS 38 and ASC 350 is critical for proper accounting of intangible assets. While both standards share common principles such as recognition criteria and impairment testing, differences exist in measurement and disclosure requirements. Accountants and financial analysts should stay updated with amendments and apply these standards consistently to reflect the true value of intangible assets in financial statements.

1.5 Practical Example: Identifying Intangible Assets in a Tech Startup

In this section, we will explore how a tech startup can identify its intangible assets, using clear examples and mind maps to visualize the process. Intangible assets are non-physical assets that provide future economic benefits to the company. For a tech startup, these assets are often critical to its value and competitive advantage.

Step 1: Understand the Business Model and Key Value Drivers

Before identifying intangible assets, it’s essential to understand what drives value in the startup. Typically, tech startups rely on innovation, intellectual property, user base, and proprietary technology.

Mind Map: Key Value Drivers in a Tech Startup

Step 2: Identify Potential Intangible Assets

Based on the value drivers, the startup should list all potential intangible assets. Here are common examples:

- Patents: If the startup has developed a novel technology or process and filed for patents.

- Trademarks: The startup’s brand name or logo that distinguishes its products.

- Copyrights: Software source code or original content created by the startup.

- Customer Lists/User Base: Databases of users or customers that have value.

- Domain Names: Unique website addresses owned by the startup.

- Proprietary Software: Custom-built software platforms or applications.

Mind Map: Potential Intangible Assets in a Tech Startup

Step 3: Apply Recognition Criteria

To recognize an intangible asset on the balance sheet, the startup must ensure that the asset:

- Is identifiable (can be separated or arises from contractual/legal rights)

- Is controlled by the company

- Will generate probable future economic benefits

- Has a measurable cost or value

Example: Identifying a Patent as an Intangible Asset

- The startup has filed a patent for a unique algorithm.

- The patent is legally protected (identifiable and controlled).

- The patent is expected to generate revenue through licensing or product sales.

- The costs incurred in filing and developing the patent are documented.

Conclusion: The patent qualifies as an intangible asset and should be recognized.

Example: User Base as an Intangible Asset

- The startup has a large user base acquired through marketing efforts.

- The user base is not legally protected or separable from the business.

- Future economic benefits are probable but difficult to measure reliably.

Conclusion: The user base may not qualify for recognition as an intangible asset but should be disclosed if material.

Step 4: Document the Identification Process

Maintaining clear documentation helps in audits and financial reporting.

Mind Map: Documentation for Intangible Asset Identification

Summary Table: Examples of Intangible Assets in a Tech Startup

| Intangible Asset | Recognition Criteria Met? | Example Details | Accounting Treatment |

|---|---|---|---|

| Patent | Yes | Patent filed for a unique algorithm | Capitalize development costs |

| Trademark | Yes | Brand name registered | Capitalize registration costs |

| Proprietary Software | Yes | Custom software developed in-house | Capitalize development costs |

| User Base | No | Large user database, no separable rights | Disclose, no capitalization |

| Domain Name | Yes | Purchased domain name with clear ownership | Capitalize purchase cost |

By following these steps and using the mind maps and examples above, accountants and financial analysts can systematically identify intangible assets in a tech startup, ensuring accurate recognition and reporting aligned with accounting standards.

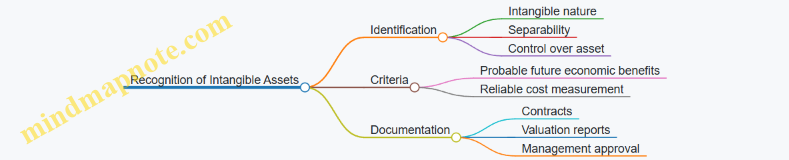

2. Recognition Criteria for Intangible Assets

2.1 Identifiability and Control: Key Recognition Principles

Intangible assets are non-physical assets that provide future economic benefits to a company. However, not all intangible items qualify for recognition on the balance sheet. Two fundamental principles guide the recognition of intangible assets: Identifiability and Control. Understanding these principles is crucial for accountants and financial analysts to ensure accurate and compliant financial reporting.

Identifiability

An intangible asset is identifiable if it meets either of the following criteria:

- Separability: The asset can be separated or divided from the entity and sold, transferred, licensed, rented, or exchanged, either individually or together with a related contract, identifiable asset, or liability.

- Arises from contractual or legal rights: The asset results from contractual or other legal rights, regardless of whether those rights are transferable or separable from the entity or from other rights and obligations.

Mind Map: Identifiability of Intangible Assets

Example:

A software company develops a proprietary algorithm. If the algorithm can be licensed to other companies independently of the business, it is separable and thus identifiable. Conversely, if the algorithm is embedded in the company’s overall technology and cannot be separated, it may not meet the separability criterion but could still be identifiable if protected by legal rights such as patents.

Control

Control refers to the company’s ability to obtain the future economic benefits flowing from the intangible asset and to restrict others’ access to those benefits. Control is typically established through legal rights but can also arise from other means.

Mind Map: Control Over Intangible Assets

Example:

A tech firm holds a patent for a unique data compression technology. This patent legally restricts competitors from using the technology, giving the firm control over the economic benefits derived from it. Alternatively, a customer list developed through internal efforts might be controlled through confidentiality agreements and access restrictions, even if not legally protected.

Integrating Identifiability and Control

For an intangible asset to be recognized, it must be both identifiable and controlled by the entity. Without identifiability, the asset cannot be reliably measured or separated from goodwill. Without control, the entity cannot guarantee future economic benefits.

Mind Map: Recognition Principles for Intangible Assets

Practical Example: Recognizing a Customer List

A software-as-a-service (SaaS) company acquires another firm and obtains its customer list.

- Identifiability: The customer list can be separated from the acquired business and sold or licensed independently.

- Control: The company has exclusive rights to use the customer data and restrict others from accessing it.

Therefore, the customer list qualifies as an intangible asset and should be recognized separately from goodwill.

Best Practice Tips

- Document the basis for identifiability: Maintain clear evidence on whether the intangible asset is separable or arises from contractual/legal rights.

- Assess control carefully: Review legal agreements, patents, licenses, and internal policies to confirm control.

- Use examples and analogies: When training teams, use relatable examples such as trademarks or software licenses to illustrate these principles.

- Coordinate with legal teams: Collaborate closely with legal counsel to understand the scope of rights and control.

By thoroughly applying the principles of identifiability and control, accountants and financial analysts can ensure that intangible assets are recognized accurately, enhancing the reliability and transparency of financial statements.

2.2 Future Economic Benefits: Assessing Probable Cash Flows

Understanding and assessing the future economic benefits of intangible assets is a cornerstone of their recognition and valuation in accounting. This section explores how accountants and financial analysts can evaluate the probable cash flows that an intangible asset is expected to generate, ensuring compliance with accounting standards such as IAS 38 and ASC 350.

What Are Future Economic Benefits?

Future economic benefits refer to the potential inflows of cash or other assets that an entity expects to derive from the use or sale of an intangible asset. These benefits justify the capitalization of the asset rather than expensing the cost immediately.

Key Considerations in Assessing Future Economic Benefits

- Probability of Cash Flows: The expected cash inflows must be probable, meaning more likely than not to occur.

- Direct Link to the Asset: Cash flows should be directly attributable to the intangible asset.

- Time Frame: Consider the period over which the benefits will be realized.

- Market and Industry Factors: External conditions affecting the asset’s ability to generate benefits.

Mind Map: Assessing Future Economic Benefits

Practical Example 1: Assessing Future Benefits of a Software License

A tech company acquires a software license for $500,000. To assess future economic benefits, the financial analyst:

- Projects incremental revenue from new clients using the software.

- Estimates cost savings from improved operational efficiency.

- Considers the license term of 5 years.

- Evaluates market demand for the software.

The company forecasts annual incremental cash inflows of $150,000, which is probable based on existing contracts and market analysis. Hence, the license meets the recognition criteria.

Mind Map: Example 1 - Software License Cash Flow Assessment

Practical Example 2: Evaluating a Trademark’s Economic Benefits

A retail company develops a new trademark expected to enhance brand recognition. To assess probable cash flows:

- The marketing team forecasts a 10% increase in sales attributable to the trademark.

- The finance team estimates the incremental profit margin on increased sales.

- The expected useful life of the trademark is 10 years.

- Market research supports sustained brand loyalty.

Based on these, the company capitalizes the trademark cost, anticipating future economic benefits.

Mind Map: Example 2 - Trademark Economic Benefit Assessment

Best Practices for Assessing Future Economic Benefits

- Use Reliable and Supportable Data: Base forecasts on verifiable market data and historical trends.

- Document Assumptions Clearly: Maintain transparency for auditors and stakeholders.

- Involve Cross-Functional Teams: Collaborate with marketing, sales, and finance for comprehensive insights.

- Regularly Review Estimates: Update cash flow projections as market conditions evolve.

- Apply Conservative Judgments: Avoid over-optimistic forecasts to mitigate impairment risks.

Summary

Assessing probable future economic benefits involves a careful, evidence-based evaluation of expected cash flows directly attributable to the intangible asset. By integrating quantitative forecasts with qualitative market insights and maintaining thorough documentation, accountants and financial analysts can ensure accurate recognition and valuation aligned with accounting standards.

2.3 Cost Measurement: Initial Recognition at Cost

When accounting for intangible assets, the initial recognition is crucial because it sets the foundation for all subsequent accounting treatments. The fundamental principle is that intangible assets should be recognized initially at cost.

What Constitutes Cost?

Cost includes all expenditures directly attributable to preparing the asset for its intended use. This can be broken down into:

- Purchase price (including import duties and non-refundable taxes)

- Costs of preparing the asset for use (e.g., legal fees, registration costs)

- Directly attributable costs necessary to bring the asset to working condition

Mind Map: Components of Initial Cost

Practical Example 1: Acquiring a Patent

A tech company purchases a patent from another firm for $150,000. Additional costs include:

- Legal fees for registration: $5,000

- Patent search and valuation fees: $3,000

- Training employees on the patent technology: $2,000

Accounting Treatment:

- Initial cost = Purchase price + Legal fees + Valuation fees

- Training costs are expensed as incurred and not capitalized.

Calculation:

$150,000 + $5,000 + $3,000 = $158,000

The patent is recognized at $158,000 on the balance sheet.

Mind Map: Example Breakdown for Patent Acquisition

Practical Example 2: Internally Developed Software

A software company develops a new application internally. Costs incurred:

- Research phase costs: $50,000

- Development phase costs: $200,000

- Testing costs before launch: $30,000

Accounting Treatment:

- Research costs are expensed as incurred.

- Development and testing costs that meet recognition criteria are capitalized.

Calculation:

Capitalized cost = $200,000 + $30,000 = $230,000

The intangible asset is recognized at $230,000.

Mind Map: Cost Recognition for Internally Developed Software

Best Practices for Cost Measurement

- Maintain detailed documentation: Track all costs related to acquisition or development separately.

- Distinguish between research and development: Only capitalize development costs meeting recognition criteria.

- Exclude non-qualifying costs: Advertising, training, and general overhead should be expensed.

- Review contracts carefully: Ensure all directly attributable costs are captured.

- Use consistent policies: Apply uniform cost recognition policies across the organization.

Summary

Initial recognition at cost ensures that intangible assets are recorded based on the actual resources expended to acquire or prepare them for use. Understanding which costs to include or exclude is essential for accurate financial reporting and compliance with accounting standards such as IAS 38 and ASC 350.

2.4 Practical Example: Recognizing a Patent Acquired Through Purchase

When a company acquires a patent through purchase, it must recognize the patent as an intangible asset on its balance sheet, provided it meets the recognition criteria under accounting standards such as IAS 38 or ASC 350. This section walks through the step-by-step process of recognizing such a patent, supported by mind maps and practical examples.

Step 1: Identify the Asset

- The patent is an identifiable intangible asset because it is separable and arises from legal rights granted by a government authority.

- The company has control over the patent, meaning it can restrict others from using the invention.

Patent Recognition Mind Map

Step 2: Determine the Cost of the Patent

- The cost includes the purchase price and any directly attributable costs necessary to prepare the patent for use (e.g., legal fees, registration fees).

Example:

- Purchase price: $500,000

- Legal fees for transfer: $20,000

- Registration fees: $5,000

Total cost to capitalize: $525,000

Cost Components Mind Map

Step 3: Recognition Criteria Check

- Identifiability: Patent is identifiable.

- Control: Company has exclusive rights.

- Future Economic Benefits: Expected licensing fees or cost savings.

- Reliable Measurement of Cost: Purchase price and fees are documented.

Since all criteria are met, the patent can be recognized as an intangible asset.

Step 4: Initial Recognition in Financial Statements

- Record the patent as an intangible asset at $525,000.

- Debit: Intangible Assets – Patents $525,000

- Credit: Cash/Payable $525,000

Step 5: Subsequent Measurement and Amortization

- Determine useful life (e.g., 10 years).

- Amortize cost over useful life using straight-line method.

Example:

- Annual amortization expense = $525,000 / 10 = $52,500

Summary Mind Map

Additional Example

Scenario: A tech company acquires a patent for a new software algorithm for $300,000, with $15,000 legal fees.

- Total capitalized cost: $315,000

- Estimated useful life: 8 years

- Annual amortization: $315,000 / 8 = $39,375

This example illustrates how to apply the recognition and measurement principles practically.

Best Practice Tips

- Always document purchase agreements and related costs meticulously.

- Confirm the useful life with technical experts to ensure accurate amortization.

- Review impairment indicators regularly to assess if the patent’s carrying amount remains recoverable.

By following these steps and using the examples and mind maps above, accountants and financial analysts can confidently recognize patents acquired through purchase in compliance with accounting standards.

2.5 Best Practice: Documenting the Recognition Process for Audit Trail

Proper documentation of the recognition process for intangible assets is critical to ensure transparency, compliance, and ease of audit. This best practice helps accountants and financial analysts provide clear evidence that recognition criteria have been met, supports internal controls, and facilitates external audits.

Why Documenting Recognition Matters

- Audit Readiness: Clear documentation provides auditors with a traceable path to verify the recognition of intangible assets.

- Regulatory Compliance: Ensures adherence to accounting standards such as IAS 38 and ASC 350.

- Internal Controls: Supports management in monitoring and validating intangible asset recognition.

- Decision Support: Helps stakeholders understand the rationale behind capitalization decisions.

Key Elements to Document in the Recognition Process

Step-by-Step Documentation Workflow

- Identify the Asset: Document the nature and description of the intangible asset.

- Assess Recognition Criteria: Record how identifiability, control, and future economic benefits are evaluated.

- Measure Cost: Detail the cost components included and the valuation method used.

- Gather Supporting Documents: Attach contracts, invoices, legal rights, and valuation reports.

- Management Review: Obtain formal approval from responsible personnel.

- Record Accounting Entries: Log journal entries with references to supporting documentation.

- Store Documentation: Maintain all records in a centralized, accessible system.

Practical Example: Documenting Recognition of a Purchased Patent

- Asset Description: Patent for a new software algorithm acquired from a third party.

- Recognition Criteria:

- Identifiability: Patent is legally registered and separable.

- Control: Company holds exclusive rights.

- Future Economic Benefits: Expected to generate licensing revenue.

- Cost Measurement: Purchase price of $500,000 plus legal fees of $20,000.

- Supporting Documents: Purchase agreement, patent registration certificate, legal invoices.

- Approvals: CFO and Head of Accounting sign-off on recognition.

- Accounting Entry: Debit Intangible Assets $520,000; Credit Cash/Payables $520,000.

- Storage: All documents saved in the company’s financial document management system with audit trail enabled.

Mind Map: Documentation Components for Patent Recognition

Tips for Effective Documentation

- Use standardized templates to ensure consistency.

- Include version control to track changes.

- Link electronic documents directly to accounting entries.

- Train staff on the importance and methods of documentation.

- Periodically review documentation practices for improvements.

By thoroughly documenting the recognition process, organizations not only comply with accounting standards but also build a robust audit trail that supports reliable financial reporting and enhances stakeholder confidence.

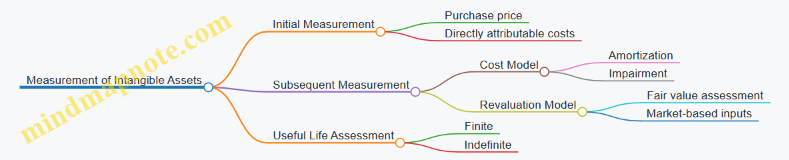

3. Valuation and Measurement of Intangible Assets

3.1 Initial Measurement: Cost Components and Capitalization

When accounting for intangible assets, the initial measurement is a critical step that determines how the asset will be recorded on the balance sheet. According to IAS 38 and ASC 350, intangible assets should be initially recognized at cost if certain recognition criteria are met. Understanding the components of cost and the rules around capitalization ensures accuracy and compliance.

What Constitutes the Cost of an Intangible Asset?

The cost of an intangible asset includes all expenditures directly attributable to preparing the asset for its intended use. This typically encompasses:

- Purchase price (including import duties and non-refundable taxes)

- Professional fees (legal, consulting, valuation)

- Costs of preparing the asset for use (e.g., testing, installation)

- Borrowing costs (if capitalization criteria are met)

Costs that are not directly attributable, such as general administrative expenses or training costs, should be expensed as incurred.

Mind Map: Components of Initial Cost

Capitalization vs. Expense

Capitalization means recording the cost as an asset on the balance sheet, while expensing means recognizing the cost immediately in the income statement. Only costs that meet the recognition criteria and are directly attributable to bringing the intangible asset to working condition should be capitalized.

Practical Example 1: Acquiring a Patent

A tech company purchases a patent for $100,000. Additional costs include legal fees of $5,000 and registration fees of $2,000. The company also incurs $3,000 in training costs for employees to use the technology.

- Purchase price: $100,000

- Legal fees: $5,000

- Registration fees: $2,000

- Training costs: $3,000 (expensed)

Capitalized cost: $100,000 + $5,000 + $2,000 = $107,000

Expensed: $3,000

Mind Map: Example Breakdown for Patent Acquisition

Practical Example 2: Internally Developed Software

A software company develops a new application. The development costs include:

- Salaries of developers during development phase: $200,000

- Costs of testing the software: $20,000

- Research phase costs: $50,000

- Marketing costs: $30,000

According to accounting standards, research costs are expensed immediately, while development costs that meet capitalization criteria can be capitalized.

- Capitalized costs: $200,000 + $20,000 = $220,000

- Expensed costs: $50,000 + $30,000 = $80,000

Mind Map: Software Development Cost Components

Best Practices for Initial Measurement and Capitalization

- Maintain detailed documentation: Keep clear records of all costs incurred and their nature to support capitalization decisions.

- Separate research and development phases: Properly distinguish these phases to comply with capitalization rules.

- Review contracts and invoices carefully: Ensure all directly attributable costs are identified and included.

- Consult accounting standards regularly: Stay updated on changes in IAS 38 and ASC 350.

- Use expert valuations when necessary: For complex intangibles, professional valuation can help determine cost components.

By carefully identifying and measuring the cost components of intangible assets, accountants and financial analysts can ensure accurate capitalization, leading to more reliable financial statements and better decision-making.

3.2 Subsequent Measurement Models: Cost Model vs. Revaluation Model

When accounting for intangible assets after initial recognition, companies must choose an appropriate subsequent measurement model. The two primary models are the Cost Model and the Revaluation Model. Understanding the differences, applications, and implications of each model is critical for accurate financial reporting and compliance with accounting standards such as IAS 38.

Cost Model

Under the cost model, intangible assets are carried at their initial cost less any accumulated amortization and any accumulated impairment losses.

-

Key Features:

- Simplicity and ease of application.

- No revaluation to fair value after initial recognition.

- Amortization and impairment losses reduce the carrying amount.

-

When to Use:

- Most intangible assets are accounted for using the cost model.

- Especially when fair value is not reliably measurable.

-

Example:

- A software license purchased for $100,000 is amortized over its 5-year useful life. After 2 years, the carrying amount is $60,000 ($100,000 - 2 x $20,000 amortization).

Revaluation Model

The revaluation model allows intangible assets to be carried at a revalued amount, being its fair value at the date of revaluation less any subsequent amortization and impairment losses.

-

Key Features:

- Fair value must be reliably measurable.

- Revaluations must be done regularly to ensure carrying amount does not differ materially from fair value.

- Increases in value are credited to other comprehensive income and accumulated in equity under revaluation surplus.

- Decreases are recognized in profit or loss unless reversing a previous revaluation surplus.

-

When to Use:

- Intangible assets with active markets (rare).

- Examples include certain trademarks or licenses with observable market prices.

-

Example:

- A trademark initially recognized at $500,000 is revalued after 3 years to $600,000 based on market evidence. The $100,000 increase is credited to revaluation surplus.

Mind Map: Subsequent Measurement Models

Practical Considerations and Best Practices

-

Reliable Fair Value Measurement:

- For the revaluation model, ensure access to active markets or use valuation techniques like discounted cash flows.

- Engage valuation experts when necessary.

-

Frequency of Revaluation:

- Conduct revaluations regularly (e.g., annually) to avoid material discrepancies.

-

Consistency:

- Apply the chosen model consistently to the entire class of intangible assets.

-

Disclosure:

- Disclose the measurement model used, revaluation methods, and effects on financial statements.

Example Scenario: Choosing Between Cost and Revaluation Models

Company A owns a patent with no active market but expects significant cash flows. They choose the cost model because fair value is not reliably measurable.

Company B owns a trademark actively traded in a market. They opt for the revaluation model to reflect current market values, enhancing transparency.

Mind Map: Decision Factors for Subsequent Measurement Model

By understanding and applying these models appropriately, accountants and financial analysts can ensure that intangible assets are reported accurately, reflecting their economic value and providing meaningful information to stakeholders.

3.3 Fair Value Measurement Techniques and Challenges

Fair value measurement is a critical aspect of accounting for intangible assets, especially when companies opt for the revaluation model or during impairment testing. Fair value represents the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

Key Fair Value Measurement Techniques

There are three primary approaches to measuring the fair value of intangible assets:

Mind Map: Fair Value Measurement Techniques

Detailed Explanation and Examples

-

Market Approach

- This approach relies on observable market data. It is often the preferred method when active markets exist.

- Example: A tech company wants to value its brand name. The accountant researches recent sales of similar brands in the same sector and adjusts for differences in market reach and brand strength.

-

Income Approach

- This approach estimates the present value of expected future economic benefits.

- Example: For a patented technology, the company estimates future cash flows generated by the patent and discounts them using an appropriate discount rate.

- Relief-from-Royalty Method: Commonly used for trademarks and brands. The company estimates the royalty payments it would have to pay if it did not own the trademark and discounts these savings.

-

Cost Approach

- This approach estimates the cost to replace or reproduce the asset.

- Example: A software development company estimates the cost to recreate a proprietary software application, including labor, materials, and overhead.

Challenges in Fair Value Measurement

Mind Map: Challenges in Fair Value Measurement

Practical Example: Valuing a Trademark Using Relief-from-Royalty Method

A software company owns a trademark for its flagship product. To estimate the fair value:

- The company estimates annual sales attributable to the trademark: $10 million

- Industry royalty rate for similar trademarks: 5%

- Expected useful life of the trademark: 10 years

- Discount rate: 12%

Steps:

- Calculate annual royalty savings: $10 million * 5% = $500,000

- Discount these savings over 10 years at 12%

- Sum the present values to arrive at the fair value

This method helps quantify the economic benefit of owning the trademark rather than licensing it.

Best Practice Tips

- Use multiple valuation approaches when possible to cross-verify results.

- Document all assumptions and methodologies clearly for audit and regulatory review.

- Engage qualified valuation experts for complex or high-value intangible assets.

- Regularly update valuations to reflect market changes and new information.

By understanding and applying these fair value measurement techniques and recognizing the associated challenges, accountants and financial analysts can ensure more accurate and reliable intangible asset valuations that enhance financial reporting quality.

3.4 Practical Example: Valuing a Trademark Using Relief-from-Royalty Method

The Relief-from-Royalty (RFR) method is a widely accepted valuation technique for intangible assets such as trademarks. It estimates the value of a trademark based on the royalties a company would have to pay if it did not own the trademark and instead licensed it from a third party.

Step-by-Step Process to Value a Trademark Using the Relief-from-Royalty Method

Step 1: Estimate Forecasted Revenues

Forecast the future revenues generated by the product or service associated with the trademark. These revenues form the base on which the royalty rate will be applied.

Example:

- Year 1 Revenue: $10 million

- Year 2 Revenue: $12 million

- Year 3 Revenue: $14 million

- Year 4 Revenue: $16 million

- Year 5 Revenue: $18 million

Step 2: Determine Appropriate Royalty Rate

Identify a reasonable royalty rate based on industry benchmarks, licensing agreements, or comparable transactions.

Example:

- Industry average royalty rate for similar trademarks: 5%

Step 3: Calculate Royalty Savings

Multiply forecasted revenues by the royalty rate to estimate the royalty payments saved by owning the trademark.

Example:

| Year | Revenue ($ million) | Royalty Rate | Royalty Savings ($ million) |

|---|---|---|---|

| 1 | 10 | 5% | 0.5 |

| 2 | 12 | 5% | 0.6 |

| 3 | 14 | 5% | 0.7 |

| 4 | 16 | 5% | 0.8 |

| 5 | 18 | 5% | 0.9 |

Step 4: Apply Discount Rate

Discount the royalty savings to present value using an appropriate discount rate that reflects the risk profile of the trademark and the business.

Example:

- Discount rate: 10%

Step 5: Calculate Trademark Value

Sum the discounted royalty savings to arrive at the estimated trademark value.

Calculation:

- Present value of royalty savings = 0.45 + 0.50 + 0.53 + 0.55 + 0.56 = $2.59 million

Summary Mind Map

Best Practice Tips:

- Use Reliable Revenue Projections: Base forecasts on historical data, market research, and realistic growth assumptions.

- Benchmark Royalty Rates: Use industry-specific royalty rates from licensing databases or comparable agreements.

- Select Appropriate Discount Rate: Reflect the trademark’s risk, industry volatility, and company-specific factors.

- Document Assumptions: Maintain clear documentation for all inputs and rationale to support audit and review processes.

- Review Periodically: Update valuations regularly to reflect changes in market conditions or business performance.

This example demonstrates how the Relief-from-Royalty method provides a practical and intuitive approach to valuing trademarks, helping accountants and financial analysts accurately reflect intangible asset values on the balance sheet.

3.5 Best Practice: Engaging Valuation Experts for Complex Intangibles

When dealing with complex intangible assets, such as patents, trademarks, customer relationships, or proprietary technology, engaging valuation experts is a best practice that ensures accuracy, compliance, and credibility in financial reporting. These experts bring specialized knowledge, methodologies, and market insights that internal accounting teams may lack.

Why Engage Valuation Experts?

- Specialized Knowledge: Valuation experts understand industry-specific factors and intangible asset nuances.

- Methodological Rigor: They apply accepted valuation approaches (income, market, cost) with precision.

- Regulatory Compliance: Experts ensure valuations meet IFRS, US GAAP, and local regulatory standards.

- Audit Readiness: Independent valuations strengthen audit defense and stakeholder confidence.

Key Steps When Working with Valuation Experts

Common Valuation Approaches for Intangible Assets

Practical Example: Valuing a Patent Using a Valuation Expert

Scenario: A tech company acquires a patent related to a novel software algorithm. The patent is complex, with uncertain future cash flows and no direct market comparables.

Process:

- Engage Expert: The company hires a valuation specialist with experience in software patents.

- Data Collection: The expert collaborates with R&D and finance teams to gather projected revenue, market potential, and legal status of the patent.

- Method Selection: The expert chooses the Relief-from-Royalty method, estimating the royalties saved by owning the patent.

- Valuation Execution: Using industry royalty rates and projected revenues, the expert calculates the patent’s fair value.

- Reporting: The expert delivers a detailed report explaining assumptions, methodology, and conclusions.

- Accounting Integration: The company records the patent at the expert’s valuation, documenting the process for audit purposes.

Additional Example: Valuing Customer Relationships in a SaaS Company

- Challenge: Customer relationships are intangible and lack direct market comparables.

- Expert Role: The valuation expert applies the Multi-Period Excess Earnings Method (MPEEM) to estimate the value based on expected future cash flows from existing customers.

- Outcome: The valuation supports the purchase price allocation in an acquisition and informs amortization schedules.

Tips for Maximizing the Value of Valuation Experts

- Involve experts early in the acquisition or asset recognition process.

- Provide comprehensive and accurate data to reduce assumptions.

- Maintain open communication to clarify business context and strategic plans.

- Review valuation reports critically with internal finance and legal teams.

- Keep documentation thorough to support audit and regulatory reviews.

By integrating valuation experts into the accounting process for complex intangible assets, companies enhance the reliability and defensibility of their financial statements, ultimately supporting better decision-making and stakeholder trust.

4. Internally Generated Intangible Assets

4.1 Research vs. Development Phases: Accounting Distinctions

Understanding the distinction between the research and development (R&D) phases is crucial for accountants and financial analysts when accounting for internally generated intangible assets. This distinction determines whether costs can be capitalized or must be expensed immediately.

Definitions:

- Research Phase: The original and planned investigation undertaken with the prospect of gaining new scientific or technical knowledge and understanding.

- Development Phase: The application of research findings or other knowledge to a plan or design for the production of new or substantially improved materials, devices, products, processes, systems, or services before commercial production or use.

Key Accounting Distinctions:

| Aspect | Research Phase | Development Phase |

|---|---|---|

| Objective | Discovery of new knowledge | Applying knowledge to create a product |

| Accounting Treatment | Costs expensed as incurred | Costs capitalized if criteria met |

| Capitalization Criteria | Not capitalized | Capitalize if all recognition criteria are fulfilled (technical feasibility, intention to complete, ability to use or sell, probable future economic benefits, availability of resources, ability to measure costs reliably) |

Mind Map: Research vs. Development Phases

Practical Example 1: Software Development in a Tech Firm

Scenario: A tech company is developing a new software product.

-

Research Phase: The company spends 6 months investigating new algorithms and conducting feasibility studies. These costs include salaries of researchers and costs of experiments.

- Accounting Treatment: All research costs are expensed as incurred.

-

Development Phase: After confirming technical feasibility, the company begins coding, testing, and preparing the software for launch.

- Accounting Treatment: Development costs such as coding salaries, testing, and software licenses are capitalized as intangible assets, provided the company expects to generate probable future economic benefits.

Mind Map: Capitalization Criteria for Development Costs

Practical Example 2: Pharmaceutical Company

Scenario: A pharmaceutical company incurs costs in discovering a new drug.

-

Research Phase: Initial laboratory research and clinical trials to discover new compounds.

- Accounting Treatment: All research costs are expensed immediately.

-

Development Phase: After successful trials, the company begins regulatory approval processes and manufacturing setup.

- Accounting Treatment: Development costs related to regulatory approval and manufacturing setup can be capitalized once the company meets the recognition criteria.

Best Practices

- Clear Documentation: Maintain detailed records distinguishing research activities from development activities.

- Regular Review: Periodically assess projects to determine phase transitions.

- Cross-Functional Collaboration: Work closely with R&D and legal teams to understand technical feasibility and patent status.

- Consistent Application: Apply capitalization criteria consistently to avoid misstatements.

Summary

The accounting distinction between research and development phases significantly impacts financial reporting. Research costs are always expensed, reflecting uncertainty and lack of guaranteed future benefits. Development costs, however, can be capitalized if strict criteria are met, recognizing the asset’s future economic value. Proper classification ensures compliance with accounting standards such as IAS 38 and ASC 350, and provides stakeholders with transparent and reliable financial information.

4.2 Criteria for Capitalizing Development Costs

Capitalizing development costs is a critical accounting decision that impacts the balance sheet and profit & loss statements. Unlike research costs, which are expensed as incurred, development costs can be capitalized if certain criteria are met. This section explains these criteria in detail, supported by mind maps and practical examples to help accountants and financial analysts apply them effectively.

Understanding Development Costs

Development costs refer to expenditures incurred in the application of research findings or other knowledge to a plan or design for the production of new or substantially improved products, processes, systems, or services before the start of commercial production or use.

Criteria for Capitalization (According to IAS 38 / ASC 350)

The main criteria that must be met to capitalize development costs are:

- Technical Feasibility: The project must demonstrate that it is technically feasible to complete the intangible asset so it will be available for use or sale.

- Intention to Complete and Use or Sell: Management must intend to complete the asset and either use it internally or sell it.

- Ability to Use or Sell: The company must have the ability to use or sell the asset once completed.

- Probable Future Economic Benefits: The asset is expected to generate probable future economic benefits, such as increased revenue or cost savings.

- Availability of Resources: Adequate technical, financial, and other resources must be available to complete the development and use or sell the asset.

- Reliable Measurement of Costs: The costs attributable to the asset during its development can be reliably measured.

Mind Map: Criteria for Capitalizing Development Costs

Practical Example 1: Software Development in a Tech Firm

Scenario: A software company is developing a new SaaS platform.

- Technical Feasibility: The development team has completed a working prototype and passed internal testing.

- Intention to Complete: The management has approved the project roadmap and allocated budget.

- Ability to Use or Sell: The platform will be launched commercially to customers.

- Probable Future Economic Benefits: Market research forecasts significant subscription revenue.

- Availability of Resources: The company has dedicated developers and financial resources.

- Reliable Cost Measurement: All development hours and related costs are tracked through project management software.

Conclusion: The company can capitalize the development costs incurred from the point technical feasibility is established.

Practical Example 2: Pharmaceutical Drug Development

Scenario: A pharmaceutical company is developing a new drug.

- Technical Feasibility: Clinical trials have successfully passed Phase II.

- Intention to Complete: Management plans to complete Phase III and seek regulatory approval.

- Ability to Use or Sell: The drug will be marketed upon approval.

- Probable Future Economic Benefits: Forecasted sales indicate strong profitability.

- Availability of Resources: Funding secured for remaining trials.

- Reliable Cost Measurement: Costs are tracked by clinical trial phases.

Conclusion: Development costs from Phase III onward can be capitalized.

Best Practices for Capitalizing Development Costs

- Maintain Detailed Documentation: Keep records of feasibility studies, management approvals, and resource allocation.

- Use Project Management Tools: Track costs and progress to ensure reliable measurement.

- Regularly Review Criteria: Reassess capitalization eligibility at each reporting period.

- Coordinate with Auditors: Ensure compliance with accounting standards and transparency.

By applying these criteria and best practices, accountants and financial analysts can accurately capitalize development costs, improving financial reporting and providing stakeholders with a clearer picture of the company’s intangible asset value.

4.3 Expense Recognition for Research Costs

In accounting for intangible assets, distinguishing between research and development costs is crucial because research costs are expensed as incurred, while certain development costs may be capitalized. This section focuses on the principles and best practices for recognizing research costs as expenses.

Understanding Research Costs

Research costs refer to the original and planned investigation undertaken with the prospect of gaining new scientific or technical knowledge and understanding. These costs are incurred before the entity can demonstrate the technical feasibility and commercial viability of the project.

Why Are Research Costs Expensed?

- Uncertainty of Future Benefits: Research activities are exploratory and may not lead to a commercially viable product.

- Conservatism Principle: Accounting standards require a cautious approach, avoiding capitalization of costs without assured future economic benefits.

- Accounting Standards Guidance: IAS 38 and ASC 730 mandate expensing research costs immediately.

Key Accounting Standards

- IAS 38 (Intangible Assets): Paragraph 54 states research costs shall be recognized as an expense when incurred.

- ASC 730 (Research and Development): Requires research and development costs to be expensed as incurred.

Mind Map: Expense Recognition for Research Costs

Examples of Research Costs Expensed

-

Laboratory Research on New Materials: A tech company spends $100,000 on experimenting with new semiconductor materials. Since the outcome is uncertain, this cost is expensed immediately.

-

Market Research for Product Viability: A financial services firm conducts a $50,000 survey to understand customer demand for a new app feature. This cost is expensed as it relates to research.

-

Feasibility Studies: A software company investigates the feasibility of a new algorithm. The $75,000 cost is expensed because it is part of research.

Best Practices for Expense Recognition of Research Costs

- Segregate Research from Development: Maintain detailed project accounting to clearly separate research activities from development.

- Document Decision Criteria: Keep records explaining why costs are classified as research.

- Regular Review: Periodically review projects to reassess classification as they progress.

- Use Mind Maps and Flowcharts: Visual tools help teams understand and communicate expense recognition policies.

Mind Map: Best Practices for Research Cost Expense Recognition

Practical Scenario

Scenario: A tech startup is developing an innovative AI-driven analytics platform. The initial phase involves researching new machine learning models.

- Costs incurred: $120,000 on experiments and data collection.

- Accounting treatment: These costs are expensed immediately as research costs.

- Documentation: The finance team maintains detailed records separating these costs from later development costs, which may be capitalized once feasibility is demonstrated.

Summary

Recognizing research costs as expenses ensures compliance with accounting standards and reflects the inherent uncertainty of research activities. Proper documentation, segregation, and periodic review are essential to maintain clarity and accuracy in financial reporting.

4.4 Practical Example: Capitalizing Software Development Costs in a Tech Firm

Capitalizing software development costs is a critical accounting practice for tech firms, enabling them to recognize internally generated intangible assets on their balance sheets. This section walks through a detailed example illustrating how a tech company can identify, measure, and capitalize software development costs in compliance with accounting standards such as IAS 38 and ASC 350.

Understanding the Phases: Research vs. Development

Before capitalizing costs, it’s essential to distinguish between the research phase (costs expensed) and the development phase (costs potentially capitalized).

Example:

A tech firm, “Innovatech,” is developing a new SaaS platform. The initial feasibility study and prototyping (research phase) cost $200,000 and are expensed immediately. Once the project moves into detailed design and coding (development phase), costs incurred can be capitalized if certain criteria are met.

Criteria for Capitalization

According to IAS 38 and ASC 350, development costs can be capitalized if the company can demonstrate:

- Technical feasibility of completing the software

- Intention and ability to complete and use or sell the software

- Ability to generate probable future economic benefits

- Availability of adequate resources to complete development

- Ability to reliably measure the costs attributable to the software

Step-by-Step Capitalization Example

- Project Overview: Innovatech starts detailed development on January 1, 2024.

- Costs Incurred: Salaries of developers ($500,000), software licenses ($50,000), and testing expenses ($30,000).

- Assessment: Innovatech confirms technical feasibility, has committed resources, and expects to launch in 12 months.

- Capitalization: The $580,000 development costs are capitalized as an intangible asset.

- Amortization: The software has an estimated useful life of 5 years; amortization begins upon product launch.

Mind Map: Capitalization Process

Additional Examples

-

Example 1: Innovatech incurs $100,000 on market research for the software concept. This cost is expensed immediately as it falls under the research phase.

-

Example 2: After product launch, Innovatech spends $40,000 on routine maintenance and bug fixes. These costs are expensed as incurred because they do not enhance the software’s functionality.

-

Example 3: Innovatech purchases a third-party software module for $150,000 to integrate into their platform. This cost is capitalized as a separately identifiable intangible asset.

Best Practices for Capitalizing Software Development Costs

- Maintain detailed documentation segregating research and development activities.

- Track costs by project and phase to ensure accurate capitalization.

- Regularly review the project’s progress and reassess capitalization criteria.

- Collaborate with technical teams to confirm technical feasibility.

- Ensure amortization schedules reflect the software’s expected useful life.

By following these guidelines and examples, accountants and financial analysts can accurately capitalize software development costs, enhancing the transparency and reliability of financial statements for tech firms.

4.5 Best Practice: Establishing Clear Policies for Internal Intangibles

Establishing clear and comprehensive policies for accounting internal intangible assets is critical for ensuring consistency, compliance, and accurate financial reporting. Internal intangible assets, such as internally developed software, trademarks, or proprietary processes, often pose challenges due to the difficulty in distinguishing research from development phases and measuring costs reliably.

Why Clear Policies Matter

- Consistency: Uniform treatment across projects and departments.

- Compliance: Alignment with accounting standards like IAS 38 and ASC 350.

- Audit Readiness: Clear documentation supports audit trails.

- Financial Accuracy: Proper capitalization avoids misstating expenses or assets.

Key Components of Internal Intangible Asset Policies

Mind Map: Components of Internal Intangible Asset Policies

Practical Example: Policy for Software Development Costs

Scenario: A technology company develops a new software product internally.

- Research Phase: Activities like feasibility studies, prototyping, and concept formulation are expensed as incurred.

- Development Phase: Once technical feasibility is established, costs such as coding, testing, and implementation are capitalized.

- Costs Included: Salaries of developers, software licenses used in development, and allocated overhead.

- Costs Excluded: General administrative costs and training expenses.

- Documentation: Timesheets linked to development tasks, project approval forms, and cost tracking reports.

- Approval: Capitalization decisions reviewed quarterly by finance and project management teams.

Mind Map: Software Development Cost Policy

Additional Examples

- Trademark Creation: Costs related to designing and registering a trademark are capitalized once the trademark is legally registered.

- Customer Lists: Costs to acquire customer lists internally are capitalized if they meet identifiability and control criteria.

- Proprietary Processes: Documented development costs of unique manufacturing processes can be capitalized if future economic benefits are probable.

Tips for Implementing Clear Policies

- Train Employees: Ensure project managers and finance staff understand capitalization criteria.

- Use Templates: Standardize documentation forms for cost tracking and approvals.

- Regular Reviews: Periodically revisit policies to incorporate regulatory updates or business changes.

- Cross-Department Collaboration: Encourage communication between R&D, finance, and legal teams.

Summary

Establishing clear policies for internal intangible assets helps organizations accurately capture the value of their innovations while maintaining compliance with accounting standards. Well-defined criteria, thorough documentation, and consistent review processes are the pillars of effective intangible asset management.

For more detailed guidance, refer to IAS 38 “Intangible Assets” and ASC 350 “Intangibles—Goodwill and Other.”

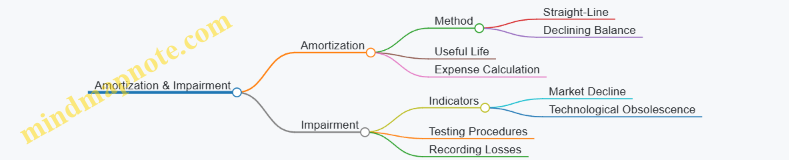

5. Amortization of Intangible Assets

5.1 Determining Useful Life: Finite vs. Indefinite

Understanding the useful life of intangible assets is a critical step in their accounting treatment. The useful life determines how the asset will be amortized or tested for impairment, impacting both the balance sheet and income statement.

What is Useful Life?

Useful life is the period over which an intangible asset is expected to contribute to the cash flows of the entity. It can be either finite or indefinite.

Finite Useful Life

- Definition: The intangible asset has a limited period during which it is expected to generate economic benefits.

- Accounting Treatment: Amortized systematically over its useful life.

- Examples: Patents, copyrights, customer contracts, software licenses.

Indefinite Useful Life

- Definition: No foreseeable limit to the period over which the asset is expected to generate economic benefits.

- Accounting Treatment: Not amortized but tested annually for impairment.

- Examples: Goodwill, certain trademarks, brand names.

Mind Map: Determining Useful Life of Intangible Assets

Factors Influencing Useful Life Determination

- Legal, Regulatory, or Contractual Provisions: For example, a patent’s legal life is 20 years, but technological obsolescence might shorten its useful life.

- Expected Usage: How long the company expects to use the asset.

- Obsolescence: Technological or market changes that reduce the asset’s value.

- Maintenance and Renewal: Ability to extend the asset’s life through maintenance or renewal.

- Other Economic Factors: Competition, demand, and economic environment.

Example 1: Finite Useful Life - Patent

A tech company acquires a patent with a legal life of 20 years. Due to rapid technological changes, the company estimates the patent will generate economic benefits for 10 years.

- Useful life: 10 years (finite)

- Accounting: Amortize the patent cost over 10 years using straight-line amortization.

Example 2: Indefinite Useful Life - Trademark

A well-established brand owns a trademark with no legal expiration and a strong market presence expected to last indefinitely.

- Useful life: Indefinite

- Accounting: No amortization; perform annual impairment tests to ensure carrying value is recoverable.

Practical Best Practices

- Document Assumptions: Clearly record the rationale behind useful life estimates.

- Regular Review: Reassess useful life annually or when significant events occur.

- Cross-Functional Input: Collaborate with legal, marketing, and R&D teams to understand asset longevity.

- Use Industry Benchmarks: Compare with similar companies or industry standards.

Mind Map: Best Practices for Determining Useful Life

Summary

Determining whether an intangible asset has a finite or indefinite useful life is foundational for correct accounting treatment. Finite-life assets are amortized over their useful life, while indefinite-life assets require annual impairment testing. Applying a structured approach with clear documentation and regular reviews ensures compliance and accurate financial reporting.

5.2 Amortization Methods: Straight-Line and Other Approaches

Amortization is the systematic allocation of the cost of an intangible asset over its useful life. Choosing the appropriate amortization method is crucial for accurately reflecting the consumption of economic benefits derived from the asset.

Common Amortization Methods

- Straight-Line Method

- Units of Production Method

- Declining Balance Method

- Sum-of-the-Years’-Digits Method

Straight-Line Method

This is the most commonly used amortization method due to its simplicity and consistency. It allocates an equal amount of amortization expense each accounting period over the asset’s useful life.

Formula:

\[ \text{Amortization Expense} = \frac{\text{Cost of Intangible Asset} - \text{Residual Value}}{\text{Useful Life}} \]

Example:

A company acquires a patent for $120,000 with a useful life of 10 years and no residual value.

- Annual amortization expense = $120,000 / 10 = $12,000

Each year, the company will expense $12,000 until the patent is fully amortized.

Mind Map:

Units of Production Method

This method allocates amortization based on the actual usage or output related to the intangible asset, making it useful when the asset’s economic benefits vary with usage.

Formula:

\[ \text{Amortization Expense} = \frac{\text{Cost} - \text{Residual Value}}{\text{Total Estimated Units}} \times \text{Units Used in Period} \]

Example:

A software license costing $50,000 is expected to be used for 100,000 user sessions. In the first year, 20,000 sessions occur.

- Amortization expense = ($50,000 / 100,000) * 20,000 = $10,000

Mind Map:

Declining Balance Method

An accelerated amortization method where higher amortization expenses are recognized in the earlier years of the asset’s life, decreasing over time.

Formula:

\[ \text{Amortization Expense} = \text{Book Value at Beginning of Period} \times \text{Declining Rate} \]

Example:

An intangible asset costing $100,000 with a 5-year useful life uses a double declining balance rate of 40%.

- Year 1: $100,000 * 40% = $40,000

- Year 2: ($100,000 - $40,000) * 40% = $24,000

Mind Map:

Sum-of-the-Years’-Digits Method

Another accelerated amortization method that allocates amortization based on a fraction that decreases each year.

Formula:

\[ \text{Amortization Expense} = (\text{Cost} - \text{Residual Value}) \times \frac{\text{Remaining Life}}{\text{Sum of the Years’ Digits}} \]

Where sum of the years’ digits for n years = n(n+1)/2

Example:

An intangible asset costing $90,000 with a 5-year useful life and no residual value.

- Sum of digits = 5+4+3+2+1 = 15

- Year 1 expense = $90,000 * (5/15) = $30,000

- Year 2 expense = $90,000 * (4/15) = $24,000

Mind Map:

Choosing the Right Method: Best Practices

- Match amortization method to asset usage: Use straight-line for consistent benefits; use units of production or accelerated methods when usage or benefit consumption varies.

- Review useful life and residual value regularly: Adjust amortization if estimates change.

- Document assumptions and rationale: Maintain clear records for audit and compliance.

Summary Mind Map

5.3 Practical Example: Amortizing Customer Lists Over Contract Period

Amortization of intangible assets like customer lists is a critical accounting practice to systematically allocate the cost of the asset over its useful life. Customer lists typically have a finite useful life, often linked to contract durations or expected customer retention periods.

Understanding Amortization of Customer Lists

- Customer List as an Intangible Asset: Represents the value of a company’s existing customer relationships.

- Finite Useful Life: Usually determined by the length of contracts or historical customer retention data.

- Amortization Purpose: To match the expense recognition with the economic benefits derived from the customer list.

Step-by-Step Example

Scenario:

A tech company acquires a customer list for $120,000. The contract period associated with these customers is 4 years. The company decides to amortize the customer list over the 4-year contract period using the straight-line method.

Step 1: Determine Useful Life

- Useful life = 4 years (contract period)

Step 2: Select Amortization Method

- Straight-line amortization (equal expense each year)

Step 3: Calculate Annual Amortization Expense

- Annual amortization = Cost of asset / Useful life

- Annual amortization = $120,000 / 4 = $30,000

Step 4: Record Amortization Expense

- Each year, the company records $30,000 as amortization expense.

Journal Entry:

Dr Amortization Expense $30,000

Cr Accumulated Amortization - Customer List $30,000

Step 5: Review and Adjust

- At the end of each year, review the useful life and adjust if necessary.

Mind Map: Amortizing Customer Lists

Additional Example: Variable Amortization

If the customer list is expected to generate more benefits in the first two years, the company might choose an accelerated amortization method, such as the double-declining balance.

- Cost: $120,000

- Useful life: 4 years

- Year 1 amortization: $120,000 x 2/4 = $60,000

- Year 2 amortization: ($120,000 - $60,000) x 2/4 = $30,000

- Year 3 amortization: Remaining balance amortized accordingly

This approach better matches expenses with economic benefits when customer value declines over time.

Best Practice Tips

- Align Useful Life with Contract Terms: Use contract periods or historical data to estimate useful life accurately.

- Choose Appropriate Amortization Method: Straight-line is simple; accelerated methods may better reflect economic reality.

- Regularly Review Asset Life: Adjust amortization schedules if customer retention or contract terms change.

- Document Assumptions: Maintain clear records of useful life estimates and amortization methods for audit purposes.

By following these steps and considerations, accountants and financial analysts can ensure that the amortization of customer lists is accurate, compliant, and reflective of the asset’s economic value.

5.4 Best Practice: Regular Review and Adjustment of Useful Lives

Intangible assets often have estimated useful lives that can change over time due to technological advances, market conditions, or changes in business strategy. Regularly reviewing and adjusting these useful lives ensures that amortization expense reflects the asset’s actual economic benefits, maintaining accurate financial reporting and compliance with accounting standards.

Why Regular Review is Important

- Reflects Current Economic Reality: Useful life estimates made at acquisition may become outdated.

- Ensures Accurate Amortization: Prevents over- or under-amortization, which can distort profit and asset values.

- Compliance with Standards: IAS 38 and ASC 350 require periodic reassessment of useful lives.

- Supports Better Decision-Making: Provides management and analysts with reliable financial data.

Key Factors to Consider When Reviewing Useful Lives

Step-by-Step Process for Reviewing and Adjusting Useful Lives

Practical Example: Adjusting Useful Life of a Software License

Scenario: A tech company initially estimated the useful life of a software license at 5 years. After 3 years, due to rapid technological advancements and a new product launch, the software is expected to be obsolete in 1 more year instead of 2.

- Original amortization: Straight-line over 5 years

- Amortization taken: 3 years

- Remaining amortization period: Adjusted from 2 years to 1 year

Adjustment:

- Recalculate the remaining amortizable amount and amortize over the revised 1-year period.

- Update financial records and disclose the change in useful life and its impact on amortization expense.

Additional Example: Patent Useful Life Extension

Scenario: A pharmaceutical company holds a patent initially amortized over 10 years. After regulatory approval for extended use, the patent’s economic life is extended by 3 years.

- Action: Increase the useful life to 13 years.

- Effect: Decrease annual amortization expense going forward.

Best Practice: Document the regulatory change and update amortization schedules accordingly.

Best Practice Tips

- Establish a formal policy for periodic review of intangible asset useful lives.