Capital Budgeting for Accountants

1. Introduction to Capital Budgeting

1.1 Definition and Importance of Capital Budgeting

Capital budgeting is the process by which a business evaluates and selects long-term investment projects that are expected to generate returns over multiple years. It involves analyzing potential expenditures or investments in assets such as new machinery, buildings, technology upgrades, or product development to determine their profitability and alignment with the company’s strategic goals.

Why is Capital Budgeting Important?

Capital budgeting is crucial because it helps organizations allocate scarce resources efficiently, ensuring that funds are invested in projects that maximize shareholder value and support sustainable growth. Poor capital budgeting decisions can lead to wasted resources, missed opportunities, and financial distress.

Key Objectives of Capital Budgeting:

- Evaluate the profitability and risks of long-term investments

- Prioritize projects based on financial and strategic criteria

- Ensure optimal use of capital to maximize returns

- Support strategic planning and growth initiatives

Mind Map: Definition and Importance of Capital Budgeting

Example 1: Evaluating a New Machine Purchase

A manufacturing company considers purchasing a new machine costing $500,000. The machine is expected to increase production efficiency, resulting in additional cash inflows of $120,000 per year for 6 years. The company must decide whether this investment is worthwhile.

- Step 1: Identify initial investment: $500,000

- Step 2: Estimate annual cash inflows: $120,000

- Step 3: Determine project lifespan: 6 years

- Step 4: Analyze using capital budgeting techniques (covered later)

This example shows the fundamental role of capital budgeting in guiding investment decisions by quantifying expected benefits against costs.

Mind Map: Example - New Machine Purchase

Example 2: Software Upgrade Project

A financial services firm plans to upgrade its client management software at a cost of $200,000. The upgrade is expected to reduce administrative costs by $50,000 annually and improve client retention, indirectly increasing revenues by $30,000 per year for 5 years.

- Initial Investment: $200,000

- Annual Savings and Revenue Increase: $80,000 ($50,000 + $30,000)

- Project Duration: 5 years

This example highlights that capital budgeting is not only about direct cash inflows but also about cost savings and strategic benefits.

Mind Map: Example - Software Upgrade

Summary

Capital budgeting is a cornerstone of financial planning and decision-making for accountants and financial planners. It ensures that investments are carefully evaluated for their potential to generate value over time, balancing costs, benefits, and risks. By mastering capital budgeting, accountants can provide critical insights that drive sustainable business growth.

1.2 Role of Accountants in Capital Budgeting Decisions

Capital budgeting is a critical process for organizations to evaluate and select long-term investment projects. Accountants play a pivotal role in ensuring that these decisions are financially sound, compliant, and aligned with the company’s strategic goals. Their involvement spans from data preparation to analysis, reporting, and advising management.

Key Responsibilities of Accountants in Capital Budgeting

- Data Collection & Validation: Accountants gather historical financial data, estimate future cash flows, and verify the accuracy of cost and revenue projections.

- Cost Analysis: They identify relevant costs, distinguish between sunk and incremental costs, and ensure all financial aspects are considered.

- Financial Modeling: Accountants build and maintain models to calculate Net Present Value (NPV), Internal Rate of Return (IRR), Payback Period, and other metrics.

- Risk Assessment: They assist in analyzing risks through sensitivity and scenario analyses, helping management understand potential outcomes.

- Tax & Regulatory Compliance: Accountants incorporate tax implications, depreciation methods, and regulatory requirements into the budgeting process.

- Reporting & Communication: They prepare clear, concise reports and presentations to communicate findings and recommendations to stakeholders.

Mind Map: Role of Accountants in Capital Budgeting

Example 1: Data Collection and Cost Analysis

A manufacturing company is considering purchasing new machinery. The accountant collects the following data:

- Initial cost of machinery: $500,000

- Installation costs: $50,000

- Expected increase in annual revenue: $150,000

- Incremental operating costs: $40,000 per year

- Existing machinery salvage value: $30,000 (considered sunk cost)

The accountant identifies that the salvage value of the old machinery is a sunk cost and should not influence the decision. They focus on incremental costs and revenues to estimate cash flows accurately.

Example 2: Financial Modeling and Risk Assessment

For the same machinery purchase, the accountant builds an NPV model assuming a discount rate of 10% over 5 years. They also perform sensitivity analysis:

- Base case NPV: $120,000

- If annual revenue increases drop by 20%, NPV reduces to $60,000

- If operating costs increase by 15%, NPV reduces to $80,000

This analysis helps management understand how changes in assumptions impact project viability.

Mind Map: Financial Modeling and Risk Assessment

Example 3: Reporting and Communication

After completing the analysis, the accountant prepares a report summarizing:

- Project description and assumptions

- Detailed cash flow projections

- NPV, IRR, and Payback Period results

- Sensitivity and scenario analysis outcomes

- Recommendations based on financial and strategic considerations

They present this report to the finance committee, using charts and graphs to illustrate key points, ensuring non-financial managers understand the implications.

Summary

Accountants are essential in capital budgeting by providing accurate financial data, performing rigorous analysis, assessing risks, ensuring compliance, and communicating results effectively. Their expertise enables organizations to make informed investment decisions that support long-term growth and profitability.

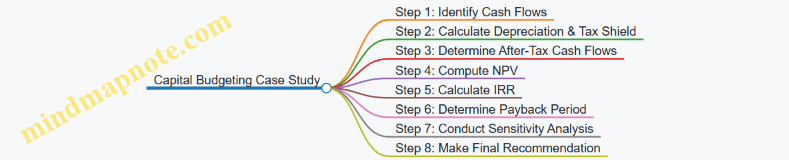

1.3 Overview of Capital Budgeting Process with Practical Examples

Capital budgeting is a systematic approach used by accountants and financial planners to evaluate and select long-term investment projects that align with a company’s strategic goals. The process ensures that capital is allocated efficiently to projects that maximize shareholder value.

Key Steps in the Capital Budgeting Process

Below is a mind map illustrating the primary stages involved in capital budgeting:

Step 1: Identification of Investment Opportunities

Accountants work closely with other departments to identify potential projects, such as purchasing new machinery, expanding operations, or launching new products.

Example: A manufacturing firm identifies the opportunity to invest in an automated packaging machine to reduce labor costs.

Step 2: Evaluation of Cash Flows

This involves estimating all relevant cash inflows and outflows associated with the project.

- Initial Investment: Cost of purchasing and installing the machine.

- Operating Cash Flows: Savings from reduced labor costs and maintenance expenses.

- Terminal Cash Flows: Salvage value of the machine at the end of its useful life.

Example:

- Initial Investment: $500,000

- Annual Operating Savings: $120,000

- Project Life: 5 years

- Salvage Value: $50,000

Step 3: Assessment of Project Viability

Accountants apply various techniques to assess whether the project adds value.

Example:

- Using a discount rate of 10%, calculate NPV:

- Present value of savings over 5 years + salvage value - initial investment

Step 4: Risk Analysis

Accountants analyze uncertainties affecting cash flows.

Example:

- Sensitivity analysis shows that if annual savings drop to $90,000, NPV remains positive, indicating project robustness.

Step 5: Decision Making

Based on the analysis, management decides to approve, reject, or modify the project.

Example:

- The project is approved due to positive NPV and acceptable payback period.

Step 6: Implementation and Monitoring

Accountants track actual cash flows and compare them to projections to ensure project success.

Example:

- Quarterly reviews show labor cost savings aligning with forecasts.

Summary Mind Map of the Capital Budgeting Process

By following this structured process, accountants ensure that capital budgeting decisions are well-informed, transparent, and aligned with the company’s financial objectives.

1.4 Common Challenges Accountants Face in Capital Budgeting

Capital budgeting is a critical process that requires precision, foresight, and collaboration. Accountants play a pivotal role in ensuring that capital budgeting decisions are financially sound and aligned with organizational goals. However, several challenges can complicate this process. Below, we explore these common challenges with detailed explanations, examples, and mind maps to aid understanding.

Challenge 1: Accurate Estimation of Cash Flows

Estimating future cash flows is inherently uncertain. Accountants must differentiate between relevant and irrelevant cash flows, avoid including sunk costs, and anticipate changes in working capital.

Example: A company plans to invest in new machinery costing $500,000. The accountant must estimate incremental cash inflows from increased production and factor in additional maintenance costs. Overestimating inflows can lead to approving unprofitable projects.

Mind Map:

Challenge 2: Selecting the Appropriate Discount Rate

Choosing the right discount rate is crucial as it affects the present value of future cash flows. Accountants often struggle to determine the Weighted Average Cost of Capital (WACC) or adjust for project-specific risks.

Example: For a high-risk project, using the company’s average WACC may undervalue risk, leading to poor investment decisions. Accountants need to adjust the discount rate to reflect project risk properly.

Mind Map:

Challenge 3: Incorporating Risk and Uncertainty

Capital budgeting involves forecasting over multiple years, exposing estimates to uncertainty. Accountants must use techniques like sensitivity analysis, scenario analysis, or simulations to manage risk.

Example: A financial planner uses sensitivity analysis to test how changes in sales volume affect project NPV, helping the company understand potential downside risks.

Mind Map:

Challenge 4: Aligning Capital Budgeting with Strategic Goals

Sometimes, financially attractive projects may not align with the company’s long-term strategy. Accountants must balance quantitative analysis with qualitative factors.

Example: An accountant evaluates a project with a strong NPV but that conflicts with the company’s sustainability goals. The decision requires integrating strategic considerations beyond numbers.

Mind Map:

Challenge 5: Handling Tax Implications and Regulatory Constraints

Tax laws and regulations can significantly impact project cash flows. Accountants must accurately incorporate depreciation methods, tax shields, and compliance costs.

Example: A project’s profitability improves when accelerated depreciation is applied, but accountants must ensure compliance with tax regulations to avoid penalties.

Mind Map:

Challenge 6: Data Quality and Availability

Reliable data is the foundation of sound capital budgeting. Accountants often face incomplete, outdated, or inconsistent data, which can skew analysis.

Example: An accountant receives sales forecasts from different departments with conflicting assumptions, complicating cash flow projections.

Mind Map:

Challenge 7: Communicating Complex Analysis to Stakeholders

Accountants must present capital budgeting results clearly to non-financial managers and executives, ensuring understanding and buy-in.

Example: Using visual aids like charts and simplified summaries helps accountants explain why a project with a longer payback period is still worthwhile.

Mind Map:

Summary Mind Map: Common Challenges in Capital Budgeting for Accountants

By understanding and proactively addressing these challenges, accountants can enhance the accuracy and effectiveness of capital budgeting decisions, ultimately contributing to better financial outcomes and strategic success.

2. Understanding Cash Flows in Capital Budgeting

2.1 Identifying Relevant Cash Flows: Incremental and Sunk Costs

In capital budgeting, correctly identifying relevant cash flows is crucial for making sound investment decisions. Two fundamental concepts accountants must understand are incremental cash flows and sunk costs.

What are Incremental Cash Flows?

Incremental cash flows represent the additional cash inflows or outflows that occur as a direct result of undertaking a project. These are the cash flows that would not exist if the project were not pursued.

- Why are they important?

- They help isolate the true financial impact of the project.

- Only incremental cash flows should be included in capital budgeting analysis.

Example: Imagine a company considering purchasing a new machine that will increase production and sales.

- Current sales: $500,000/year

- Expected sales with new machine: $650,000/year

- Incremental sales revenue: $150,000/year

The $150,000 is the incremental cash inflow attributable to the new machine.

What are Sunk Costs?

Sunk costs are past expenditures that have already been incurred and cannot be recovered. These costs should not influence the decision-making process because they remain the same regardless of the project outcome.

- Why exclude sunk costs?

- Including sunk costs can lead to biased or irrational decisions.

- Capital budgeting focuses on future cash flows, not past expenses.

Example: A company spent $50,000 last year on market research for a product. Now, they are deciding whether to launch the product.

- The $50,000 is a sunk cost and should be ignored in the capital budgeting analysis.

Mind Map: Relevant vs. Irrelevant Cash Flows

Mind Map: Components of Incremental Cash Flows

Practical Example: Incremental Cash Flow Identification

Scenario: A company is evaluating a project to launch a new product line.

| Item | Amount ($) | Relevant? | Reason |

|---|---|---|---|

| Market research expenses (last year) | 30,000 | No (Sunk Cost) | Already incurred, unrecoverable |

| New equipment purchase | 200,000 | Yes | Initial investment outlay |

| Additional raw materials cost | 50,000 annually | Yes | Incremental operating expense |

| Existing factory rent | 100,000 annually | No | Unchanged by project |

| Incremental sales revenue | 300,000 annually | Yes | Additional revenue generated |

| Opportunity cost of land | 40,000 annually | Yes | Foregone rental income if land used |

Explanation:

- The $30,000 market research is a sunk cost and excluded.

- The $200,000 equipment purchase is an initial outlay and included.

- Additional raw materials and incremental sales are included as operating cash flows.

- Existing rent is unchanged and excluded.

- Opportunity cost is relevant and should be included.

Best Practices for Accountants

- Always separate past costs from future costs.

- Focus on cash flows, not accounting profits. Non-cash expenses like depreciation are considered only for tax effects.

- Include opportunity costs as they represent real economic sacrifices.

- Exclude allocated overhead unless it changes due to the project.

- Document assumptions clearly to support cash flow identification.

By mastering the identification of incremental and sunk costs, accountants can ensure that capital budgeting analyses reflect the true economic impact of investment decisions, leading to better resource allocation and improved corporate financial health.

2.2 Estimating Initial Investment Outlays with Example Calculations

Estimating the initial investment outlay is a critical step in capital budgeting. It represents the total upfront cost required to start a project, including all expenditures necessary to get the asset ready for use. For accountants, accurately calculating this figure ensures that the project’s feasibility is properly assessed and that subsequent cash flow projections are reliable.

Components of Initial Investment Outlay

The initial investment outlay typically includes:

- Purchase Price of Asset: The cost to acquire the fixed asset.

- Installation and Delivery Costs: Expenses related to transporting and setting up the asset.

- Working Capital Requirements: Additional funds needed to support the project’s operations (e.g., inventory, receivables).

- Training and Start-up Costs: Costs to train staff or initiate production.

- Less Salvage Value of Old Asset (if replacement): If the project involves replacing an existing asset, the salvage value reduces the initial outlay.

Mind Map: Components of Initial Investment Outlay

Step-by-Step Example Calculation

Scenario:

A company plans to purchase new machinery to increase production capacity. The details are as follows:

| Item | Cost (USD) |

|---|---|

| Purchase Price of Machinery | 150,000 |

| Delivery and Installation | 10,000 |

| Initial Increase in Inventory | 5,000 |

| Increase in Accounts Receivable | 3,000 |

| Increase in Accounts Payable | (2,000) |

| Training Costs | 2,000 |

| Salvage Value of Old Machine | (20,000) |

Step 1: Calculate Net Working Capital Increase

Net Working Capital (NWC) = Increase in Inventory + Increase in Accounts Receivable - Increase in Accounts Payable

NWC = 5,000 + 3,000 - 2,000 = 6,000

Step 2: Calculate Total Initial Investment Outlay

Initial Outlay = Purchase Price + Delivery & Installation + Training + NWC - Salvage Value of Old Asset

Initial Outlay = 150,000 + 10,000 + 2,000 + 6,000 - 20,000 = 148,000

Mind Map: Example Calculation Breakdown

Important Considerations and Best Practices

-

Include All Relevant Costs: Accountants should ensure all costs necessary to bring the asset into operational condition are included.

-

Exclude Financing Costs: Interest and other financing expenses are not part of the initial outlay but are considered separately.

-

Working Capital Changes: Only incremental changes in working capital related to the project should be included.

-

Salvage Value of Old Assets: When replacing assets, subtract the expected salvage value to reflect the net cash outflow.

-

Documentation: Maintain detailed records of all assumptions and calculations for audit and review purposes.

Additional Example: Software Implementation Project

| Item | Cost (USD) |

|---|---|

| Software License Fee | 80,000 |

| Hardware Upgrades | 15,000 |

| Installation and Testing | 7,000 |

| Staff Training | 5,000 |

| Increase in Working Capital | 4,000 |

Calculation:

Initial Outlay = 80,000 + 15,000 + 7,000 + 5,000 + 4,000 = 111,000

This example highlights that initial investment outlays are not limited to physical assets but also include intangible assets and related costs.

Summary

Estimating the initial investment outlay accurately is foundational for capital budgeting. By systematically identifying all relevant costs and incorporating working capital changes and salvage values, accountants can provide a clear picture of the upfront investment required. Using structured approaches and examples helps ensure consistency and reliability in these estimates.

2.3 Operating Cash Flows: Forecasting and Adjustments

Operating cash flows (OCF) represent the cash generated from the core business operations of a project or investment. For accountants involved in capital budgeting, accurately forecasting and adjusting operating cash flows is critical to evaluating the viability and profitability of capital projects.

What are Operating Cash Flows?

Operating cash flows are the net cash inflows and outflows resulting from the day-to-day operations related to a capital project. They exclude financing and investing cash flows but include revenues, operating expenses, taxes, and changes in working capital.

Key Components of Operating Cash Flows

Forecasting Operating Cash Flows: Step-by-Step Approach

-

Estimate Incremental Revenues

- Identify additional sales generated by the project.

- Example: A new machine increases production by 10,000 units sold at $50 each, so incremental revenue = 10,000 × $50 = $500,000.

-

Estimate Incremental Operating Expenses

- Include direct costs like materials, labor, and overhead.

- Example: Materials cost $20 per unit, labor $10 per unit, so total variable cost = 10,000 × ($20 + $10) = $300,000.

-

Calculate Earnings Before Interest and Taxes (EBIT)

- EBIT = Incremental Revenue – Incremental Operating Expenses – Depreciation.

- Example: Depreciation on new equipment is $50,000.

- EBIT = $500,000 – $300,000 – $50,000 = $150,000.

-

Calculate Taxes

- Apply tax rate to EBIT.

- Example: Tax rate = 30%, so taxes = $150,000 × 30% = $45,000.

-

Calculate Net Operating Profit After Taxes (NOPAT)

- NOPAT = EBIT – Taxes = $150,000 – $45,000 = $105,000.

-

Add Back Non-Cash Charges (Depreciation)

- Depreciation is a non-cash expense, so add it back.

- OCF before working capital changes = NOPAT + Depreciation = $105,000 + $50,000 = $155,000.

-

Adjust for Changes in Working Capital

- Increase in working capital is a cash outflow; decrease is a cash inflow.

- Example: Inventory increases by $10,000, accounts payable increases by $5,000, net working capital change = $10,000 – $5,000 = $5,000 outflow.

-

Calculate Final Operating Cash Flow

- OCF = $155,000 – $5,000 = $150,000.

Mind Map: Forecasting Operating Cash Flows

Adjustments to Operating Cash Flows

Accountants must make several adjustments to ensure OCF reflects the true incremental cash impact of the project:

- Exclude sunk costs: Past costs that cannot be recovered should not be included.

- Include opportunity costs: The value of the next best alternative foregone.

- Adjust for inflation: Reflect realistic price and cost changes over time.

- Consider changes in working capital: Properly forecast increases or decreases in inventory, receivables, and payables.

- Non-operating revenues/expenses: Exclude any cash flows unrelated to core operations.

Example: Adjusting Operating Cash Flows

A company plans to launch a new product line. The initial forecast shows:

- Incremental revenue: $1,000,000

- Operating expenses (excluding depreciation): $600,000

- Depreciation: $100,000

- Tax rate: 25%

- Increase in inventory: $20,000

- Increase in accounts payable: $10,000

- Sunk cost (market research already paid): $50,000

Step 1: Exclude sunk cost.

Step 2: Calculate EBIT = $1,000,000 – $600,000 – $100,000 = $300,000.

Step 3: Calculate taxes = $300,000 × 25% = $75,000.

Step 4: Calculate NOPAT = $300,000 – $75,000 = $225,000.

Step 5: Add back depreciation = $225,000 + $100,000 = $325,000.

Step 6: Calculate net working capital change = $20,000 (inventory increase) – $10,000 (payables increase) = $10,000 outflow.

Step 7: Final OCF = $325,000 – $10,000 = $315,000.

Mind Map: Adjustments to Operating Cash Flows

Best Practices for Accountants in Forecasting OCF

- Use conservative and realistic assumptions.

- Collaborate with operational managers for accurate data.

- Regularly update forecasts to reflect market changes.

- Document all assumptions and adjustments clearly.

- Utilize spreadsheet models with scenario analysis capabilities.

By mastering the forecasting and adjustment of operating cash flows, accountants can provide invaluable insights that enhance capital budgeting decisions, ensuring projects selected contribute positively to the company’s financial health.

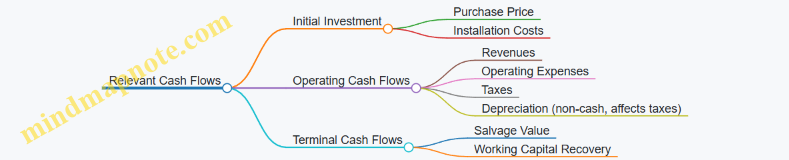

2.4 Terminal Cash Flows and Salvage Value Considerations

Understanding Terminal Cash Flows

Terminal cash flows represent the net cash inflows or outflows that occur at the end of a project’s life. These cash flows are critical in capital budgeting because they often include the recovery of working capital, the salvage value of assets, and any costs associated with project termination.

Components of Terminal Cash Flows

- Salvage Value: The estimated residual value of an asset at the end of its useful life.

- Recovery of Net Working Capital: The release of working capital invested in the project.

- Costs of Disposal or Decommissioning: Expenses related to shutting down or cleaning up.

Mind Map: Terminal Cash Flows Components

Salvage Value Considerations

Salvage value is the expected selling price of an asset after its useful life. It can be:

- Positive Salvage Value: Asset can be sold for cash.

- Zero Salvage Value: Asset has no resale value.

- Negative Salvage Value: Costs are incurred to dispose of the asset (e.g., environmental cleanup).

Example 1: Calculating Salvage Value Impact

A company buys machinery for $100,000 with a 5-year life. At the end of 5 years, the machine can be sold for $15,000. The company estimates a $2,000 cost for dismantling.

- Salvage Value = $15,000 - $2,000 = $13,000

- This $13,000 is included as a positive terminal cash inflow.

Tax Implications on Salvage Value

When an asset is sold, the difference between the salvage value and the book value results in a gain or loss, which affects taxes.

Example 2: Tax Effect on Salvage Value

Continuing Example 1:

- Book value at end of year 5 = $0 (fully depreciated)

- Salvage value = $15,000

- Gain on sale = $15,000

- Tax rate = 30%

Tax on gain = $15,000 * 30% = $4,500

After-tax salvage value = $15,000 - $4,500 = $10,500

Mind Map: Tax Impact on Salvage Value

Recovery of Net Working Capital

At the start of a project, working capital (e.g., inventory, receivables) is often invested and tied up. At project end, this capital is typically recovered.

Example 3: Working Capital Recovery

- Initial working capital investment: $20,000

- At project end, this $20,000 is released and considered a cash inflow in terminal cash flows.

Disposal or Decommissioning Costs

Some projects require costs to close or clean up, which should be accounted for as terminal cash outflows.

Example 4: Environmental Cleanup

A manufacturing plant must spend $5,000 to clean up hazardous materials at project end. This $5,000 is a terminal cash outflow.

Comprehensive Terminal Cash Flow Example

A company completes a 4-year project with the following details:

- Salvage value of equipment: $12,000

- Book value at end of project: $4,000

- Tax rate: 25%

- Recovery of working capital: $10,000

- Disposal costs: $1,500

Step 1: Calculate gain on sale

- Gain = $12,000 - $4,000 = $8,000

- Tax on gain = $8,000 * 25% = $2,000

Step 2: After-tax salvage value

- $12,000 - $2,000 = $10,000

Step 3: Calculate terminal cash flow

- After-tax salvage value: $10,000

- Recovery of working capital: $10,000

- Disposal costs: -$1,500

Total terminal cash flow = $10,000 + $10,000 - $1,500 = $18,500

Mind Map: Comprehensive Terminal Cash Flow Calculation

Best Practices for Accountants

- Always include tax effects when calculating salvage value.

- Ensure working capital recovery is accounted for as a positive cash flow.

- Include any disposal or environmental costs as terminal cash outflows.

- Use conservative estimates for salvage value to avoid overestimating terminal cash flows.

- Document assumptions clearly for audit and review purposes.

By carefully estimating terminal cash flows, accountants can provide more accurate and realistic capital budgeting analyses, ultimately supporting better investment decisions.

2.5 Best Practices for Accurate Cash Flow Estimation

Accurate cash flow estimation is critical in capital budgeting because it directly impacts the reliability of investment appraisals and financial decisions. Accountants play a pivotal role in ensuring that cash flow projections are realistic, comprehensive, and aligned with the company’s strategic goals.

Key Best Practices

Identify Relevant Cash Flows

- Include only incremental cash flows directly attributable to the project.

- Exclude sunk costs that have already been incurred.

- Consider opportunity costs of resources used.

Use Conservative and Realistic Assumptions

- Base forecasts on historical data and market research.

- Avoid overly optimistic revenue or cost estimates.

- Factor in possible delays or cost overruns.

Separate Operating, Investing, and Financing Cash Flows

- Operating cash flows: revenues and expenses from core operations.

- Investing cash flows: initial capital outlay and asset disposals.

- Financing cash flows: loans, equity injections, and dividends (usually excluded from project cash flows).

Incorporate Tax Effects and Depreciation

- Calculate tax shields from depreciation.

- Adjust cash flows for corporate tax impacts.

Regularly Update Cash Flow Estimates

- Revise projections as new information becomes available.

- Use rolling forecasts to reflect changing market conditions.

Document Assumptions and Methodologies

- Maintain transparency for audit and review.

- Facilitate communication with stakeholders.

Mind Map: Best Practices for Accurate Cash Flow Estimation

Example 1: Estimating Cash Flows for a New Machine Purchase

Scenario: A manufacturing company plans to purchase a new machine costing $500,000. The machine is expected to increase annual revenues by $150,000 and increase operating costs by $40,000. The machine will be depreciated straight-line over 5 years with no salvage value. The corporate tax rate is 30%.

Step 1: Calculate Incremental Operating Cash Flows

- Incremental Revenue: $150,000

- Incremental Operating Costs: $40,000

- Incremental Earnings Before Depreciation and Tax (EBDT): $110,000

- Depreciation Expense: $500,000 / 5 = $100,000

- Earnings Before Tax (EBT): $110,000 - $100,000 = $10,000

- Tax (30%): $10,000 * 0.30 = $3,000

- Net Income: $7,000

- Add back Depreciation (non-cash): $100,000

- Operating Cash Flow: $7,000 + $100,000 = $107,000

Step 2: Initial Investment Outlay

- Machine Cost: $500,000 (Year 0 cash outflow)

Step 3: Summary of Cash Flows

| Year | Cash Flow ($) |

|---|---|

| 0 | -500,000 |

| 1-5 | +107,000 |

Best Practice Notes:

- Only incremental revenues and costs are included.

- Depreciation is used to calculate tax but added back to cash flow.

- Tax effects are incorporated.

- Salvage value is zero, simplifying terminal cash flow.

Example 2: Adjusting for Opportunity Cost

Scenario: The company owns land worth $200,000 that will be used for the new machine installation. The land could otherwise be sold.

Adjustment: Include opportunity cost as a cash outflow in Year 0.

| Year | Cash Flow ($) | |

|---|---|---|

| 0 | -700,000 | <– $500,000 machine + $200,000 opportunity cost |

| 1-5 | +107,000 |

Best Practice Notes:

- Opportunity cost of the land is included because using it for the project means forgoing its sale.

Mind Map: Example 1 & 2 Cash Flow Estimation Process

Additional Tips for Accountants

- Cross-verify with multiple departments: Collaborate with production, sales, and marketing teams to validate assumptions.

- Use scenario analysis: Prepare best-case, worst-case, and most-likely cash flow estimates.

- Leverage software tools: Utilize Excel templates or specialized budgeting software for accuracy and efficiency.

- Review historical project data: Use past project outcomes to benchmark and improve estimates.

By following these best practices, accountants can provide reliable cash flow estimates that form the foundation for sound capital budgeting decisions, reducing risks and enhancing the strategic value of investments.

3. Time Value of Money Concepts for Accountants

3.1 Understanding Present Value and Future Value

Capital budgeting fundamentally relies on the concept of the time value of money (TVM), which states that a dollar today is worth more than a dollar in the future due to its potential earning capacity. Two core concepts within TVM are Present Value (PV) and Future Value (FV). Understanding these concepts is essential for accountants when evaluating investment projects.

What is Present Value (PV)?

Present Value is the current worth of a future sum of money or stream of cash flows given a specified rate of return (discount rate). It answers the question: “How much is a future amount worth today?”

What is Future Value (FV)?

Future Value is the amount of money an investment made today will grow to at a specified interest rate over a period of time. It answers the question: “How much will a current amount be worth in the future?”

Mind Map: Time Value of Money Concepts

Formulas and Explanation

-

Future Value (FV): \[ FV = PV \times (1 + r)^n \]

-

Present Value (PV): \[ PV = \frac{FV}{(1 + r)^n} \]

Where:

- \(PV\) = Present Value

- \(FV\) = Future Value

- \(r\) = interest or discount rate per period

- \(n\) = number of periods

Example 1: Calculating Future Value

Scenario: An accountant wants to know how much $10,000 invested today will be worth in 5 years if the annual interest rate is 6%.

Calculation:

\[ FV = 10,000 \times (1 + 0.06)^5 = 10,000 \times 1.3382 = 13,382 \]

Interpretation: The investment will grow to $13,382 in 5 years.

Example 2: Calculating Present Value

Scenario: A project promises to pay $15,000 five years from now. The company’s required rate of return is 8%. What is the present value of that future payment?

Calculation:

\[ PV = \frac{15,000}{(1 + 0.08)^5} = \frac{15,000}{1.4693} = 10,212.96 \]

Interpretation: The $15,000 payment in 5 years is worth $10,212.96 today.

Mind Map: Present Value and Future Value Relationship

Practical Tips for Accountants

- Always use the appropriate discount rate reflecting project risk and opportunity cost.

- Be consistent with the time period units (years, months).

- Use financial calculators or Excel functions like

=PV(),=FV()to reduce errors. - Remember that PV helps in comparing different projects with cash flows occurring at different times.

Excel Example

To calculate Present Value in Excel:

=PV(rate, nper, pmt, [fv], [type])

For Example 2:

=PV(8%, 5, 0, 15000)

This will return approximately -10212.96 (negative sign indicates cash outflow).

Summary

Understanding Present Value and Future Value is critical for accountants involved in capital budgeting. These concepts allow for the comparison of cash flows occurring at different times by adjusting for the time value of money, enabling more informed and accurate investment decisions.

3.2 Discount Rates: Determining the Appropriate Rate

Determining the appropriate discount rate is a critical step in capital budgeting because it directly impacts the present value of future cash flows and ultimately the investment decision. The discount rate reflects the opportunity cost of capital, risk, and the time value of money.

What is a Discount Rate?

The discount rate is the rate used to convert future cash flows into their present value. It represents the minimum return an investor expects to earn to compensate for the risk and time value of money.

Key Factors Influencing the Discount Rate

- Cost of Capital: The weighted average cost of capital (WACC) is often used as the discount rate.

- Risk Premium: Additional return required for the riskiness of the project.

- Inflation: Expected inflation affects the nominal discount rate.

- Opportunity Cost: Return foregone by investing in the project instead of an alternative.

Mind Map: Components Influencing Discount Rate

Common Approaches to Determine Discount Rate

-

Weighted Average Cost of Capital (WACC)

- Combines cost of debt and cost of equity weighted by their proportions in the capital structure.

- Example:

- Cost of Debt = 5%

- Cost of Equity = 10%

- Debt = 40%, Equity = 60%

- WACC = (0.4 * 5%) + (0.6 * 10%) = 2% + 6% = 8%

-

Cost of Equity (Using CAPM)

- Capital Asset Pricing Model (CAPM): Cost of Equity = Risk-Free Rate + Beta * Market Risk Premium

- Example:

- Risk-Free Rate = 3%

- Beta = 1.2

- Market Risk Premium = 6%

- Cost of Equity = 3% + 1.2 * 6% = 3% + 7.2% = 10.2%

-

Adjusting for Project-Specific Risk

- Add a risk premium to WACC or cost of equity to reflect unique project risks.

Mind Map: Calculating WACC

Example: Determining Discount Rate for a Capital Project

Scenario: A company is evaluating a new project. The company’s capital structure consists of 50% debt and 50% equity. The cost of debt is 6%, the corporate tax rate is 30%, and the cost of equity calculated via CAPM is 12%. The project has additional risk, so a 2% risk premium is added.

Step 1: Calculate after-tax cost of debt:

\[ Rd_{after\ tax} = Rd \times (1 - Tc) = 6\% \times (1 - 0.3) = 4.2\% \]

Step 2: Calculate WACC:

\[ WACC = (E/V) \times Re + (D/V) \times Rd_{after\ tax} = 0.5 \times 12\% + 0.5 \times 4.2\% = 6\% + 2.1\% = 8.1\% \]

Step 3: Add project-specific risk premium:

\[ Discount\ Rate = WACC + Risk\ Premium = 8.1\% + 2\% = 10.1\% \]

Thus, the appropriate discount rate for this project is 10.1%.

Mind Map: Steps to Determine Discount Rate

Best Practices for Accountants

- Use Market Values: Always use market values of debt and equity rather than book values for capital structure.

- Update Inputs Regularly: Risk-free rates, betas, and market premiums can change; keep them current.

- Consider Project Specifics: Adjust discount rates for unique risks related to the project or industry.

- Document Assumptions: Maintain clear documentation of assumptions and sources for transparency.

- Leverage Software Tools: Use Excel or financial software to automate calculations and reduce errors.

Summary

Determining the appropriate discount rate is a blend of art and science. It requires understanding the company’s cost of capital, the risk profile of the project, and market conditions. Accountants play a vital role in ensuring that the discount rate used in capital budgeting reflects the true opportunity cost and risk, enabling sound investment decisions.

3.3 Practical Examples of Discounting Cash Flows

Discounting cash flows is a fundamental concept in capital budgeting that allows accountants and financial planners to determine the present value of future cash inflows and outflows. This process accounts for the time value of money — the idea that a dollar today is worth more than a dollar in the future due to its earning potential.

Mind Map: Key Concepts in Discounting Cash Flows

Example 1: Single Future Cash Flow Discounting

Scenario: A company expects to receive $10,000 one year from now. The discount rate is 8%.

Calculation:

\[ PV = \frac{10,000}{(1 + 0.08)^1} = \frac{10,000}{1.08} = 9,259.26 \]

Interpretation: The present value of $10,000 received one year from now at an 8% discount rate is approximately $9,259.26 today.

Example 2: Multiple Future Cash Flows

Scenario: A project will generate cash inflows of $5,000 at the end of each year for 3 years. The discount rate is 10%.

Step-by-step Calculation:

| Year | Cash Flow | Discount Factor (10%) | Present Value |

|---|---|---|---|

| 1 | $5,000 | 1 / (1+0.10)^1 = 0.9091 | $4,545.45 |

| 2 | $5,000 | 1 / (1+0.10)^2 = 0.8264 | $4,132.23 |

| 3 | $5,000 | 1 / (1+0.10)^3 = 0.7513 | $3,756.62 |

Total Present Value:

\[ PV = 4,545.45 + 4,132.23 + 3,756.62 = 12,434.30 \]

Interpretation: The total present value of these future cash inflows is $12,434.30.

Mind Map: Discounting Multiple Cash Flows

Example 3: Discounting Uneven Cash Flows

Scenario: A project has the following expected cash inflows:

- Year 1: $3,000

- Year 2: $4,500

- Year 3: $6,000

The discount rate is 12%.

Calculation:

| Year | Cash Flow | Discount Factor (12%) | Present Value |

|---|---|---|---|

| 1 | $3,000 | 0.8929 | $2,678.70 |

| 2 | $4,500 | 0.7972 | $3,587.40 |

| 3 | $6,000 | 0.7118 | $4,270.80 |

Total Present Value:

\[ PV = 2,678.70 + 3,587.40 + 4,270.80 = 10,536.90 \]

Mind Map: Steps to Discount Uneven Cash Flows

Example 4: Using Excel for Discounting Cash Flows

Scenario: Using the uneven cash flows from Example 3, calculate the present value using Excel.

Excel Formula:

- Use the

PVfunction or manual discounting:

=PV(rate, nper, pmt, [fv], [type])

Since cash flows are uneven, use manual discounting:

| Year | Cash Flow | Formula in Excel | Result |

|---|---|---|---|

| 1 | $3,000 | =3000/(1+12%)^1 | $2,678.57 |

| 2 | $4,500 | =4500/(1+12%)^2 | $3,587.30 |

| 3 | $6,000 | =6000/(1+12%)^3 | $4,270.80 |

Sum the results for total PV.

Practical Tips for Accountants:

- Always confirm the timing of cash flows (beginning or end of period).

- Use consistent discount rates reflecting project risk.

- Double-check calculations with financial calculators or Excel.

- Document assumptions clearly for audit trails.

By mastering discounting cash flows through these practical examples, accountants can confidently evaluate investment opportunities and contribute to sound capital budgeting decisions.

3.4 Impact of Inflation and Risk on Discount Rates

Capital budgeting decisions rely heavily on discount rates to evaluate the present value of future cash flows. Two critical factors that influence the choice and adjustment of discount rates are inflation and risk. Understanding their impact helps accountants and financial planners make more accurate and realistic project evaluations.

Understanding Inflation and Its Effect on Discount Rates

Inflation represents the general increase in prices over time, which erodes the purchasing power of money. When inflation is present, future cash flows must be adjusted to reflect their real value.

- Nominal Discount Rate includes inflation.

- Real Discount Rate excludes inflation.

Relationship:

\[ (1 + \text{Nominal Rate}) = (1 + \text{Real Rate}) \times (1 + \text{Inflation Rate}) \]

Example:

Suppose the real discount rate is 5%, and expected inflation is 3%. The nominal discount rate would be:

\[ (1 + 0.05) \times (1 + 0.03) - 1 = 1.05 \times 1.03 - 1 = 1.0815 - 1 = 8.15\% \]

This means future cash flows should be discounted at 8.15% to reflect both the time value of money and inflation.

Mind Map: Inflation Impact on Discount Rates

Understanding Risk and Its Effect on Discount Rates

Risk reflects the uncertainty of achieving expected cash flows. Higher risk projects require higher discount rates to compensate investors for bearing that risk.

- Risk-Free Rate: The return on a riskless investment (e.g., government bonds).

- Risk Premium: Additional return required to compensate for risk.

Adjusted Discount Rate:

\[ \text{Discount Rate} = \text{Risk-Free Rate} + \text{Risk Premium} \]

Example:

- Risk-Free Rate = 4%

- Risk Premium for project = 6%

Discount Rate = 4% + 6% = 10%

This 10% rate reflects both the time value of money and compensation for risk.

Mind Map: Risk Impact on Discount Rates

Combining Inflation and Risk in Discount Rate Calculation

When both inflation and risk are considered, the discount rate is adjusted to reflect the real rate, inflation, and risk premium.

Stepwise approach:

- Determine the real risk-free rate.

- Add expected inflation to get the nominal risk-free rate.

- Add risk premium to reflect project-specific risk.

Example:

- Real risk-free rate = 2%

- Expected inflation = 3%

- Risk premium = 5%

Calculate nominal risk-free rate:

\[ (1 + 0.02) \times (1 + 0.03) - 1 = 5.06\% \]

Add risk premium:

\[ 5.06\% + 5\% = 10.06\% \]

So, the discount rate used to evaluate the project is approximately 10.06%.

Mind Map: Combined Impact of Inflation and Risk

Practical Example: Adjusting Discount Rate for Inflation and Risk

An accountant is evaluating a capital project with the following data:

- Real risk-free rate: 3%

- Expected inflation: 4%

- Project risk premium: 7%

Step 1: Calculate nominal risk-free rate

\[ (1 + 0.03) \times (1 + 0.04) - 1 = 1.03 \times 1.04 - 1 = 1.0712 - 1 = 7.12\% \]

Step 2: Add risk premium

\[ 7.12\% + 7\% = 14.12\% \]

Interpretation:

The accountant should use a discount rate of approximately 14.12% when discounting future cash flows for this project to properly account for inflation and risk.

Best Practices for Accountants

- Always distinguish between real and nominal cash flows and discount rates.

- Use market data to estimate inflation and risk premiums realistically.

- Adjust discount rates consistently with the nature of cash flows (nominal vs. real).

- Document assumptions clearly for transparency and audit purposes.

By carefully considering inflation and risk in discount rate calculations, accountants can ensure more accurate capital budgeting decisions that reflect true economic value and project uncertainty.

3.5 Using Financial Calculators and Excel for Time Value of Money

Understanding the Time Value of Money (TVM) is crucial for accountants involved in capital budgeting. While the concepts of present value (PV) and future value (FV) can be calculated manually, using financial calculators and Excel significantly improves accuracy and efficiency.

Financial Calculators for TVM

Financial calculators are specialized tools designed to handle TVM calculations quickly. Popular models include the Texas Instruments BA II Plus and the HP 12C.

Key Functions:

- N: Number of periods

- I/Y: Interest rate per period

- PV: Present value

- PMT: Payment (if any)

- FV: Future value

Example 1: Calculating Future Value

An accountant wants to find the future value of $10,000 invested for 5 years at an annual interest rate of 6%, compounded annually.

Steps on a financial calculator:

- Enter N = 5

- Enter I/Y = 6

- Enter PV = -10,000 (cash outflow)

- Enter PMT = 0 (no periodic payments)

- Compute FV

Result: FV ≈ $13,382.26

Excel for TVM Calculations

Excel offers built-in functions that simplify TVM computations, making it an indispensable tool for accountants.

Common Excel Functions:

- FV(rate, nper, pmt, [pv], [type])

- PV(rate, nper, pmt, [fv], [type])

- NPER(rate, pmt, pv, [fv], [type])

- RATE(nper, pmt, pv, [fv], [type])

Example 2: Calculating Present Value in Excel

Suppose you expect to receive $15,000 in 4 years. The discount rate is 7% annually. What is the present value?

Formula:

=PV(7%, 4, 0, 15000)

Result:

$11,716.29

Example 3: Calculating Number of Periods

You invest $5,000 today at 5% interest compounded annually. How many years until it grows to $7,000?

Formula:

=NPER(5%, 0, -5000, 7000)

Result:

Approximately 7.1 years

Mind Maps in

Mind Map 1: Financial Calculator TVM Workflow

Mind Map 2: Excel TVM Functions Overview

Mind Map 3: Best Practices for Using Excel and Calculators in TVM

Practical Tips for Accountants

- Always clarify whether interest rates are nominal or effective.

- Use consistent compounding periods across all calculations.

- When dealing with annuities or uneven cash flows, consider using Excel’s NPV and XNPV functions.

- Leverage Excel’s Data Tables feature to perform sensitivity analysis on TVM variables.

By mastering financial calculators and Excel for TVM, accountants can streamline capital budgeting analyses, reduce errors, and provide more insightful financial recommendations.

4. Capital Budgeting Techniques and Their Application

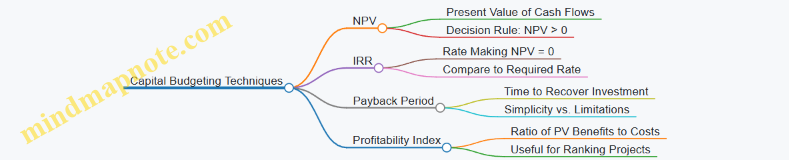

4.1 Payback Period Method: Calculation and Limitations

The Payback Period Method is one of the simplest capital budgeting techniques used by accountants and financial planners to evaluate investment projects. It measures the time required for the initial investment to be recovered from the project’s cash inflows.

What is Payback Period?

- The payback period is the length of time needed to recoup the original investment.

- It focuses on liquidity and risk by emphasizing how quickly invested capital is returned.

How to Calculate Payback Period

The payback period can be calculated in two ways depending on whether cash inflows are uniform or non-uniform.

Uniform Cash Inflows

If the project generates equal cash inflows each year, the formula is:

Payback Period = Initial Investment / Annual Cash Inflow

Example:

A company invests $50,000 in equipment expected to generate $10,000 annually.

Payback Period = $50,000 / $10,000 = 5 years

Non-Uniform Cash Inflows

When cash inflows vary each year, calculate cumulative cash flows until the initial investment is recovered.

Example:

| Year | Cash Inflow | Cumulative Cash Flow |

|---|---|---|

| 1 | $15,000 | $15,000 |

| 2 | $20,000 | $35,000 |

| 3 | $10,000 | $45,000 |

| 4 | $15,000 | $60,000 |

Initial investment = $50,000

The payback period lies between Year 3 and Year 4.

Calculation:

Amount remaining after Year 3 = $50,000 - $45,000 = $5,000

Fraction of Year 4 needed = $5,000 / $15,000 = 0.33 years

Total Payback Period = 3 + 0.33 = 3.33 years

Mind Map: Payback Period Calculation

Advantages of Payback Period Method

- Simple and easy to understand.

- Useful for assessing liquidity and risk.

- Helps in quick screening of projects.

Limitations of Payback Period Method

- Ignores the time value of money.

- Does not consider cash flows beyond the payback period.

- Does not measure overall profitability.

- Can lead to rejecting profitable long-term projects.

Mind Map: Limitations of Payback Period

Practical Example: Comparing Two Projects Using Payback Period

| Project | Initial Investment | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 |

|---|---|---|---|---|---|---|

| A | $100,000 | $30,000 | $30,000 | $30,000 | $30,000 | $30,000 |

| B | $100,000 | $50,000 | $20,000 | $15,000 | $10,000 | $5,000 |

Calculate Payback Period:

-

Project A:

- Cumulative cash flow after Year 3 = $90,000

- Amount remaining = $100,000 - $90,000 = $10,000

- Fraction of Year 4 = $10,000 / $30,000 = 0.33

- Payback Period = 3.33 years

-

Project B:

- Cumulative cash flow after Year 2 = $70,000

- Amount remaining = $100,000 - $70,000 = $30,000

- Fraction of Year 3 = $30,000 / $15,000 = 2 years (exceeds Year 3 cash flow)

- So, payback occurs during Year 4:

- After Year 3: $85,000

- Remaining: $15,000

- Fraction of Year 4 = $15,000 / $10,000 = 1.5 years (exceeds Year 4 cash flow)

- Payback occurs during Year 5:

- After Year 4: $95,000

- Remaining: $5,000

- Fraction of Year 5 = $5,000 / $5,000 = 1 year

- Total Payback Period = 2 + 1 + 1 = 4 years

Interpretation: Project A recovers investment faster (3.33 years) than Project B (4 years), so based on payback period alone, Project A might be preferred.

Best Practices for Accountants Using Payback Period

- Use payback period as a preliminary screening tool, not the sole decision criterion.

- Combine with other methods like NPV or IRR for comprehensive evaluation.

- Adjust for the time value of money by using discounted payback period if possible.

- Consider the nature of the project and industry when interpreting payback results.

Mind Map: Best Practices

In summary, the Payback Period Method offers a straightforward way for accountants to assess how quickly an investment can be recovered. While it provides valuable insights into liquidity and risk, it should be integrated with other capital budgeting techniques to ensure well-rounded investment decisions.

4.2 Net Present Value (NPV): Step-by-Step Example

Net Present Value (NPV) is one of the most widely used capital budgeting techniques. It helps accountants and financial planners evaluate the profitability of a project by calculating the present value of expected cash inflows and outflows, discounted at the project’s cost of capital.

What is NPV?

- NPV = Present Value of Cash Inflows - Present Value of Cash Outflows

- A positive NPV indicates the project is expected to add value to the firm.

- A negative NPV suggests the project may reduce firm value.

Step-by-Step Example: Evaluating a New Equipment Purchase

Scenario: A company is considering purchasing new equipment costing $100,000. The equipment is expected to generate additional cash inflows of $30,000 per year for 5 years. The company’s cost of capital is 8%. The equipment has no salvage value at the end of 5 years.

Step 1: Identify Initial Investment

- Initial Outlay = $100,000 (cash outflow at Year 0)

Step 2: Estimate Annual Cash Inflows

- Cash inflows = $30,000 per year for 5 years

Step 3: Determine the Discount Rate

- Discount rate (cost of capital) = 8%

Step 4: Calculate Present Value of Cash Inflows

Using the Present Value of Annuity formula or tables:

\[ PV = C \times \frac{1 - (1 + r)^{-n}}{r} \]

Where:

- C = annual cash inflow ($30,000)

- r = discount rate (8% or 0.08)

- n = number of years (5)

Calculation:

\[ PV = 30,000 \times \frac{1 - (1 + 0.08)^{-5}}{0.08} = 30,000 \times 3.993 = 119,790 \]

Step 5: Calculate NPV

\[ NPV = PV_{inflows} - Initial Investment = 119,790 - 100,000 = 19,790 \]

Interpretation:

Since NPV is positive ($19,790), the project is financially viable and should be accepted.

Mind Map: NPV Calculation Process

Additional Example: Project with Uneven Cash Flows

Scenario: A project requires an initial investment of $50,000. Expected cash inflows are:

- Year 1: $15,000

- Year 2: $20,000

- Year 3: $25,000

- Discount rate: 10%

Step 1: Calculate Present Value of each cash inflow:

| Year | Cash Inflow | PV Factor (10%) | Present Value |

|---|---|---|---|

| 1 | $15,000 | 0.909 | $13,635 |

| 2 | $20,000 | 0.826 | $16,520 |

| 3 | $25,000 | 0.751 | $18,775 |

Step 2: Sum of PV inflows = $13,635 + $16,520 + $18,775 = $48,930

Step 3: Calculate NPV = $48,930 - $50,000 = -$1,070

Interpretation: NPV is negative, so the project should be rejected.

Mind Map: NPV with Uneven Cash Flows

Best Practices for Accountants When Calculating NPV

- Always use the appropriate discount rate reflecting project risk.

- Include all relevant cash flows: initial outlay, operating inflows, terminal cash flows.

- Avoid including sunk costs.

- Use consistent time periods for cash flow estimation.

- Validate assumptions with stakeholders.

- Utilize Excel or financial calculators to minimize errors.

Excel Formula for NPV Calculation

For the first example:

=NPV(8%, 30000, 30000, 30000, 30000, 30000) - 100000

This formula calculates the present value of cash inflows and subtracts the initial investment.

Summary

NPV is a powerful tool for accountants to evaluate investment projects by considering the time value of money. Through clear identification of cash flows, appropriate discounting, and careful calculation, accountants can provide valuable insights that support sound capital budgeting decisions.

4.3 Internal Rate of Return (IRR): Interpretation and Practical Use

What is IRR?

The Internal Rate of Return (IRR) is the discount rate that makes the Net Present Value (NPV) of all cash flows from a particular project equal to zero. In simpler terms, it is the break-even cost of capital — the rate at which the project neither loses nor gains value.

Why is IRR Important for Accountants?

- Helps evaluate the profitability of investments.

- Provides a single percentage figure that is easy to compare against required rates of return or cost of capital.

- Assists in ranking multiple projects.

How to Calculate IRR?

IRR is found by solving the equation:

\[ NPV = \sum_{t=0}^N \frac{C_t}{(1 + IRR)^t} = 0 \]

Where:

- \(C_t\) = Cash flow at time t

- N = Project duration

Since this equation cannot be solved algebraically for IRR, iterative methods or financial calculators/software like Excel are used.

Practical Example: Calculating IRR

Scenario: A company is considering purchasing new machinery costing $100,000. The expected cash inflows over 4 years are:

- Year 1: $30,000

- Year 2: $40,000

- Year 3: $35,000

- Year 4: $20,000

Step 1: Set up cash flows

| Year | Cash Flow ($) |

|---|---|

| 0 | -100,000 |

| 1 | 30,000 |

| 2 | 40,000 |

| 3 | 35,000 |

| 4 | 20,000 |

Step 2: Use Excel or financial calculator to find IRR

In Excel, use the formula:

=IRR(values)

Where values is the range of cash flows including the initial investment.

Result: The IRR is approximately 14.5%.

Interpretation: If the company’s required rate of return (cost of capital) is below 14.5%, this project is financially viable.

Mind Map: Understanding IRR

Best Practices for Accountants Using IRR

- Use IRR alongside NPV: IRR alone can be misleading, especially with non-conventional cash flows or mutually exclusive projects.

- Check for multiple IRRs: Projects with alternating positive and negative cash flows may have more than one IRR.

- Consider the scale of investment: A higher IRR does not always mean a better project if the project size is small.

- Reinvestment Rate Assumption: Be aware IRR assumes reinvestment at the IRR itself, which may not be realistic.

Example: Multiple IRRs Scenario

Cash Flows:

| Year | Cash Flow ($) |

|---|---|

| 0 | -100,000 |

| 1 | 230,000 |

| 2 | -132,000 |

This project has unconventional cash flows (negative, positive, then negative). When calculating IRR, you may find two IRRs (e.g., 10% and 40%). This creates ambiguity.

Mind Map: Handling Multiple IRRs

Practical Use Case: Comparing Two Projects

| Project | Initial Investment | IRR | NPV at 10% Discount Rate |

|---|---|---|---|

| A | $200,000 | 18% | $25,000 |

| B | $500,000 | 15% | $50,000 |

Decision:

- Project A has a higher IRR but lower NPV.

- Project B has a lower IRR but higher NPV.

Best Practice: Accountants should consider both IRR and NPV, and align decisions with company strategy and capital availability.

Summary

- IRR is a critical tool for evaluating capital budgeting projects.

- It provides a rate of return that can be compared against the cost of capital.

- Accountants should use IRR in conjunction with other metrics like NPV.

- Awareness of IRR limitations (multiple IRRs, reinvestment assumptions) is essential.

- Practical examples and tools like Excel simplify IRR calculation and interpretation.

Additional Resources

- Excel IRR function tutorial

- Guide to Modified Internal Rate of Return (MIRR)

- Capital budgeting case studies

4.4 Profitability Index: When and How to Use

What is the Profitability Index (PI)?

The Profitability Index (PI), also known as the Profit Investment Ratio (PIR) or Value Investment Ratio (VIR), is a capital budgeting tool that measures the relative profitability of a project. It is calculated as the ratio of the present value of future cash inflows to the initial investment.

Formula:

\[ \text{Profitability Index (PI)} = \frac{\text{Present Value of Future Cash Inflows}}{\text{Initial Investment}} \]

- A PI greater than 1 indicates that the project’s NPV is positive and it is expected to generate value.

- A PI less than 1 suggests the project should be rejected.

When to Use the Profitability Index

- Capital Rationing Situations: When a company has limited capital and must choose among multiple projects, PI helps prioritize projects by value created per unit of investment.

- Comparing Mutually Exclusive Projects: PI can assist in ranking projects when initial investments differ significantly.

- Supplement to NPV and IRR: PI provides an additional perspective especially when projects vary in scale.

How to Calculate the Profitability Index: Step-by-Step Example

Scenario: A company is considering investing in a project that requires an initial investment of $100,000. The project is expected to generate the following cash inflows over 4 years:

| Year | Cash Inflow ($) |

|---|---|

| 1 | 30,000 |

| 2 | 40,000 |

| 3 | 35,000 |

| 4 | 25,000 |

Assuming a discount rate of 10%, calculate the Profitability Index.

Step 1: Calculate Present Value (PV) of Each Cash Inflow

\[ PV = \frac{\text{Cash Inflow}}{(1 + r)^t} \]

| Year | Cash Inflow | PV Factor (10%) | Present Value ($) |

|---|---|---|---|

| 1 | 30,000 | 0.9091 | 27,273 |

| 2 | 40,000 | 0.8264 | 33,056 |

| 3 | 35,000 | 0.7513 | 26,296 |

| 4 | 25,000 | 0.6830 | 17,075 |

Step 2: Sum the Present Values

\[ \text{Total PV of Cash Inflows} = 27,273 + 33,056 + 26,296 + 17,075 = 103,700 \]

Step 3: Calculate Profitability Index

\[ PI = \frac{103,700}{100,000} = 1.037 \]

Interpretation: Since PI > 1, the project is expected to add value and should be considered for acceptance.

Mind Map: Understanding Profitability Index

Mind Map: Steps to Calculate Profitability Index

Practical Example: Choosing Between Two Projects Using PI

Project A:

- Initial Investment: $150,000

- PV of Future Cash Inflows: $180,000

Project B:

- Initial Investment: $100,000

- PV of Future Cash Inflows: $120,000

Calculate PI for both:

- Project A: PI = 180,000 / 150,000 = 1.20

- Project B: PI = 120,000 / 100,000 = 1.20

Both projects have the same PI, but Project A adds $30,000 more in absolute value (NPV). If capital is limited to $150,000, choosing Project A maximizes total value. However, if capital is limited to $100,000, only Project B can be funded.

Best Practice: Use PI alongside NPV and consider capital availability and strategic fit.

Best Practices for Accountants Using Profitability Index

- Always use an appropriate discount rate reflecting project risk.

- Combine PI with other metrics like NPV and IRR for comprehensive analysis.

- Use PI to rank projects when capital is constrained.

- Be cautious when comparing projects of vastly different sizes.

- Document assumptions and cash flow estimates clearly.

Summary

The Profitability Index is a powerful tool for accountants to evaluate and prioritize capital projects, especially under capital rationing. By understanding its calculation, interpretation, and limitations, accountants can better support strategic investment decisions.

4.5 Accounting Rate of Return (ARR): Pros and Cons

What is Accounting Rate of Return (ARR)?

The Accounting Rate of Return (ARR) is a capital budgeting metric that measures the expected profitability of an investment by comparing the average annual accounting profit to the initial investment cost. Unlike cash flow-based methods, ARR focuses on accounting profits, making it familiar and straightforward for accountants.

Formula:

\[ \text{ARR} = \left( \frac{\text{Average Annual Profit}}{\text{Initial Investment}} \right) \times 100\% \]

Where:

- Average Annual Profit = (Total Profit over project life) / (Number of years)

Example of ARR Calculation

A company is considering purchasing a machine costing $100,000. The machine has a useful life of 5 years with no salvage value. The expected annual accounting profits (after depreciation) are $22,000.

Calculate the ARR:

\[ \text{ARR} = \left( \frac{22,000}{100,000} \right) \times 100\% = 22\% \]

If the company’s required ARR is 18%, this project would be accepted since 22% > 18%.

Mind Map: Understanding ARR

Pros of ARR

-

Simplicity and Ease of Use

- Uses accounting data familiar to accountants.

- Easy to calculate without complex financial models.

-

Focus on Profitability

- Directly relates to profitability as shown in financial statements.

-

Useful for Preliminary Screening

- Good for quick assessments before detailed analysis.

-

Aligns with Accounting Performance Measures

- Helps link investment appraisal with financial reporting.

Cons of ARR

-

Ignores Time Value of Money

- Treats all profits equally regardless of when they occur.

- Can lead to overvaluing projects with early profits.

-

Based on Accounting Profits, Not Cash Flows

- Accounting profits include non-cash items like depreciation.

- Cash flow is a more accurate measure of project viability.

-

Influenced by Accounting Policies

- Different depreciation methods or inventory valuations affect ARR.

-

No Standard Benchmark

- Required ARR varies widely and is often arbitrary.

-

Does Not Consider Project Scale or Duration

- Two projects with different sizes or lifespans may have misleading ARR comparisons.

Mind Map: Pros and Cons of ARR

Practical Example: Comparing Two Projects Using ARR

| Project | Initial Investment | Life (years) | Total Accounting Profit | Average Annual Profit | ARR (%) |

|---|---|---|---|---|---|

| A | $150,000 | 5 | $75,000 | $15,000 | 10.0 |

| B | $100,000 | 3 | $45,000 | $15,000 | 15.0 |

- Project A has a lower ARR (10%) but longer life.

- Project B has a higher ARR (15%) but shorter life.

Decision: If only ARR is considered, Project B looks better, but this ignores cash flow timing and total returns.

Best Practices for Accountants Using ARR

- Use ARR as a supplementary tool alongside NPV and IRR.

- Adjust accounting profits to better reflect cash flows when possible.

- Be cautious of depreciation methods and their impact on ARR.

- Consider project duration and scale when interpreting ARR.

- Communicate ARR limitations clearly to stakeholders.

Summary

The Accounting Rate of Return (ARR) is a straightforward and familiar metric for accountants to evaluate investment profitability. While its simplicity is a major advantage, its failure to consider the time value of money and reliance on accounting profits limit its effectiveness as a standalone decision tool. Integrating ARR with other capital budgeting techniques and understanding its pros and cons ensures more informed and balanced investment decisions.

4.6 Integrating Multiple Techniques for Robust Decision Making

Capital budgeting decisions often involve significant investments with long-term implications. Relying on a single evaluation method can sometimes lead to incomplete or misleading conclusions. Integrating multiple capital budgeting techniques allows accountants and financial planners to cross-validate results, understand different dimensions of a project’s viability, and make more informed, robust decisions.

Why Integrate Multiple Techniques?

- Comprehensive Analysis: Different methods emphasize different aspects (e.g., liquidity, profitability, risk).

- Mitigate Limitations: Each technique has its own limitations; combining them compensates for weaknesses.

- Enhanced Confidence: Consistent results across methods increase decision confidence.

- Better Communication: Different stakeholders may prefer different metrics.

Common Techniques to Integrate

- Payback Period

- Net Present Value (NPV)

- Internal Rate of Return (IRR)

- Profitability Index (PI)

- Accounting Rate of Return (ARR)

Mind Map: Integrating Capital Budgeting Techniques

Practical Example: Evaluating a New Equipment Purchase

Scenario: A company is considering purchasing new machinery costing $150,000. The expected cash inflows are $40,000 annually for 5 years. The company’s discount rate is 10%.

| Year | Cash Inflow |

|---|---|

| 1 | $40,000 |

| 2 | $40,000 |

| 3 | $40,000 |

| 4 | $40,000 |

| 5 | $40,000 |

Step 1: Calculate Payback Period

- Payback Period = Initial Investment / Annual Cash Inflow = $150,000 / $40,000 = 3.75 years

Step 2: Calculate NPV

- NPV = Σ (Cash Inflow / (1 + r)^t) - Initial Investment

- Using discount rate 10%, NPV ≈ $40,000/(1.1)^1 + $40,000/(1.1)^2 + … + $40,000/(1.1)^5 - $150,000

- NPV ≈ $151,476 - $150,000 = $1,476 (positive, project adds value)

Step 3: Calculate IRR

- IRR is the rate that makes NPV = 0

- Using financial calculator or Excel IRR function, IRR ≈ 10.3%

Step 4: Calculate Profitability Index (PI)

- PI = Present Value of Cash Inflows / Initial Investment = $151,476 / $150,000 = 1.01

Step 5: Calculate Accounting Rate of Return (ARR)

- Average Annual Profit = (Total Cash Inflows - Initial Investment) / 5 = ($200,000 - $150,000) / 5 = $10,000

- ARR = Average Annual Profit / Initial Investment = $10,000 / $150,000 = 6.67%

Mind Map: Decision Insights from Multiple Techniques

Best Practices for Integration

- Start with NPV and IRR: These provide the most financially sound basis.

- Use Payback Period for Liquidity Insight: Especially important if cash availability is a concern.

- Consider Profitability Index When Capital is Limited: Helps prioritize projects.

- Use ARR for Quick Screening: But do not rely solely on it.

- Analyze Conflicting Results: Investigate why techniques differ and assess assumptions.

- Document Assumptions and Sensitivities: Transparency aids stakeholder understanding.

Summary

Integrating multiple capital budgeting techniques equips accountants with a holistic view of project viability. By combining liquidity measures, profitability metrics, and risk considerations, accountants can make balanced, well-supported recommendations that align with corporate financial goals and risk tolerance.

This approach also facilitates clearer communication with management and stakeholders, fostering trust and better decision-making outcomes.

5. Risk Analysis in Capital Budgeting

5.1 Identifying Types of Risks in Capital Projects

Capital projects inherently involve various types of risks that can impact their success, profitability, and overall feasibility. For accountants involved in capital budgeting, understanding and identifying these risks early is critical to making informed decisions and preparing appropriate mitigation strategies.

Key Types of Risks in Capital Projects

Below is a mind map illustrating the primary categories of risks typically encountered in capital budgeting:

Market Risk

Market risk refers to uncertainties related to the demand for the product or service and the prices that can be obtained.

Example: A manufacturing company budgeting for a new product line may face demand fluctuations if consumer preferences shift unexpectedly, reducing projected sales volumes.

Financial Risk

Financial risks involve changes in financial conditions such as interest rates or currency exchange rates that affect project costs or revenues.

Example: A multinational corporation investing in a foreign country may experience currency exchange risk, where depreciation of the local currency reduces the value of cash inflows when converted back.

Operational Risk

Operational risks arise from failures in internal processes, people, or systems.

Example: A project relying on a single supplier for critical components may face supply chain disruptions, delaying production and increasing costs.

Project Risk

These risks are directly related to the execution of the project, such as cost overruns and schedule delays.

Example: Unexpected geological conditions during construction can lead to increased excavation costs and extended timelines.

Regulatory Risk

Changes in laws, regulations, or government policies can affect project viability.

Example: New environmental regulations may require additional investments in pollution control equipment, increasing project costs.

Technological Risk

Risks related to the technology used in the project, including its potential obsolescence or failure.

Example: Investing in a new software system that becomes outdated quickly or fails to integrate with existing systems.

Strategic Risk

Risks arising from changes in the competitive landscape or strategic misalignment.

Example: A competitor launching a superior product shortly after project completion can reduce market share and profitability.

Integrated Example: Identifying Risks for a New Factory Investment

Consider an accountant evaluating a capital budgeting proposal for building a new factory:

- Market Risk: Demand for the factory’s products may decline due to economic downturn.

- Financial Risk: Interest rates may rise, increasing financing costs.

- Operational Risk: Delays in machinery delivery could postpone production start.

- Project Risk: Construction costs may exceed estimates due to material price increases.

- Regulatory Risk: New zoning laws might restrict factory operations.

- Technological Risk: The chosen manufacturing technology may become obsolete within a few years.

- Strategic Risk: Competitors may open factories nearby, intensifying competition.

By systematically identifying these risks, accountants can incorporate risk premiums, conduct sensitivity analyses, or recommend contingency plans.

Summary

Identifying and categorizing risks in capital projects is a foundational step in capital budgeting. Accountants should use structured approaches, such as mind maps, to ensure comprehensive risk identification. This enables better forecasting, risk mitigation, and ultimately more reliable investment decisions.

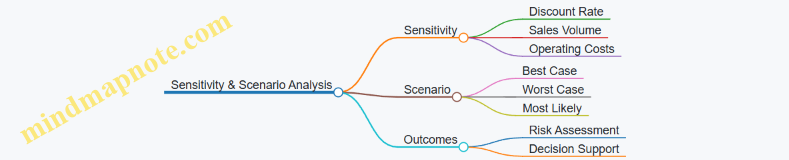

5.2 Sensitivity Analysis: Practical Example with Scenario Variations

What is Sensitivity Analysis?

Sensitivity analysis is a technique used in capital budgeting to determine how different values of an independent variable affect a particular dependent variable under a given set of assumptions. In simpler terms, it helps accountants and financial planners understand how changes in key inputs impact the outcome of a project, such as Net Present Value (NPV) or Internal Rate of Return (IRR).

Why is Sensitivity Analysis Important?

- Identifies critical variables that have the most impact on project viability.

- Helps in risk assessment by showing how sensitive a project is to changes in assumptions.

- Supports better decision-making by highlighting potential areas of concern.

Step-by-Step Practical Example

Scenario: A company is evaluating a new machine purchase project with the following base assumptions:

| Parameter | Base Value |

|---|---|

| Initial Investment | $500,000 |

| Project Life | 5 years |

| Annual Cash Inflows | $150,000 |

| Discount Rate | 10% |

Objective: Calculate the NPV and analyze how sensitive the NPV is to changes in annual cash inflows and discount rate.

Step 1: Calculate Base NPV

Using the formula:

\[ NPV = \sum_{t=1}^{n} \frac{CF_t}{(1+r)^t} - Initial\ Investment \]

Where:

- \(CF_t\) = Cash inflow at time t

- \(r\) = Discount rate

- \(n\) = Project life

Calculations:

| Year | Cash Flow | Present Value Factor (10%) | Present Value |

|---|---|---|---|

| 1 | 150,000 | 0.909 | 136,350 |

| 2 | 150,000 | 0.826 | 123,900 |

| 3 | 150,000 | 0.751 | 112,650 |

| 4 | 150,000 | 0.683 | 102,450 |

| 5 | 150,000 | 0.621 | 93,150 |

| Total PV | 568,500 |

NPV = 568,500 - 500,000 = $68,500

Step 2: Sensitivity Analysis on Annual Cash Inflows

We vary the annual cash inflows by ±20% to see the impact on NPV.

| Annual Cash Inflow | NPV Calculation (Simplified) | NPV Result |

|---|---|---|

| $120,000 (-20%) | 568,500 * (120,000 / 150,000) = 454,800 - 500,000 | -$45,200 |