Fixed Asset Accounting

1. Introduction to Fixed Asset Accounting

1.1 Definition and Importance of Fixed Assets

Definition of Fixed Assets

Fixed assets, also known as tangible assets or property, plant, and equipment (PP&E), are long-term physical assets that a company acquires for use in its operations and not for resale. These assets are expected to provide economic benefits over multiple accounting periods, typically more than one year.

Key characteristics of fixed assets:

- Tangible in nature (physical form)

- Used in the production or supply of goods and services

- Not intended for immediate sale

- Provide benefits over a long period

Mind Map: Definition of Fixed Assets

Importance of Fixed Assets

Fixed assets are critical for the operational capacity and financial health of a business, especially in manufacturing and finance sectors. Their importance can be summarized as follows:

- Operational Backbone: Fixed assets like machinery, equipment, and buildings are essential for producing goods or delivering services.

- Capital Investment: Represent significant capital investments that impact a company’s balance sheet and financial stability.

- Depreciation and Cost Allocation: Fixed assets are depreciated over their useful lives, allowing companies to allocate costs systematically and match expenses with revenues.

- Collateral for Financing: Often used as collateral to secure loans or financing.

- Tax Implications: Depreciation of fixed assets affects taxable income and tax planning.

- Asset Management: Proper accounting and management help in budgeting, maintenance planning, and replacement decisions.

Mind Map: Importance of Fixed Assets

Example 1: Fixed Asset Identification in a Manufacturing Company

Consider a manufacturing company that purchases a new CNC machine for $150,000. This machine is expected to be used in production for 10 years.

- The CNC machine is a fixed asset because:

- It is tangible and physical.

- It will be used in operations, not sold.

- It provides economic benefits over multiple years.

This asset will be recorded on the balance sheet and depreciated over its useful life.

Example 2: Fixed Assets in a Finance Company

A finance company invests in office buildings and computer hardware.

- Office buildings are fixed assets because they are long-term physical assets used to conduct business.

- Computer hardware, while sometimes considered equipment, qualifies as fixed assets if used over multiple years.

Proper accounting for these assets ensures accurate financial reporting and compliance with accounting standards.

Summary

Understanding the definition and importance of fixed assets is foundational for accountants and financial controllers. It ensures accurate recording, valuation, and management of these critical resources, directly impacting financial statements, operational efficiency, and strategic decision-making.

1.2 Overview of Fixed Asset Accounting Principles

Fixed asset accounting is a critical component of financial management, especially for accountants and financial controllers in the finance and manufacturing sectors. It involves the systematic recording, valuation, depreciation, and reporting of tangible long-term assets that a company uses in its operations. Understanding the core principles ensures accuracy in financial statements and compliance with accounting standards.

Core Principles of Fixed Asset Accounting

- Recognition: Fixed assets are recognized when it is probable that future economic benefits will flow to the entity and the cost of the asset can be reliably measured.

- Initial Measurement: Assets are initially recorded at cost, which includes purchase price and any costs directly attributable to bringing the asset to working condition.

- Depreciation: Systematic allocation of the depreciable amount of an asset over its useful life.

- Impairment: Assets must be reviewed regularly for impairment to ensure carrying amounts do not exceed recoverable amounts.

- Derecognition: Removal of an asset from the books when disposed of or no longer expected to provide economic benefits.

Mind Map: Fixed Asset Accounting Principles

Detailed Explanation with Examples

-

Recognition

- Principle: An asset should be recognized if it is probable that future economic benefits will flow to the company and the cost can be measured reliably.

- Example: A manufacturing company purchases a new CNC machine. Since the machine will be used in production for several years and the purchase cost is known, it qualifies as a fixed asset.

-

Initial Measurement

- Principle: Fixed assets are recorded at cost, including purchase price and any costs necessary to prepare the asset for use.

- Example: The CNC machine cost $100,000. Additional costs include $5,000 for installation and $2,000 for transportation. The total recorded cost is $107,000.

-

Depreciation

- Principle: Depreciation allocates the cost of the asset over its useful life to reflect usage and wear.

- Example: The CNC machine has an estimated useful life of 10 years with a residual value of $7,000. Using straight-line depreciation:

- Depreciable amount = $107,000 - $7,000 = $100,000

- Annual depreciation = $100,000 / 10 = $10,000

-

Impairment

- Principle: If the asset’s carrying amount exceeds its recoverable amount, an impairment loss must be recognized.

- Example: After 5 years, newer technology makes the CNC machine less efficient. Its recoverable amount is now estimated at $40,000, but its carrying amount is $57,000. An impairment loss of $17,000 is recorded.

-

Derecognition

- Principle: When an asset is sold, scrapped, or no longer provides economic benefits, it should be removed from the books.

- Example: The CNC machine is sold for $35,000 after 7 years. The carrying amount at the time is $27,000. The company recognizes a gain of $8,000 ($35,000 - $27,000).

Mind Map: Fixed Asset Lifecycle in Accounting

Summary

Understanding these principles helps accountants and financial controllers maintain accurate asset records, comply with accounting standards such as IFRS and GAAP, and provide stakeholders with reliable financial information. Applying these principles consistently ensures transparency and supports strategic decision-making in asset management.

1.3 Role of Accountants and Financial Controllers in Fixed Asset Management

Fixed asset management is a critical function within finance and manufacturing sectors, and accountants and financial controllers play pivotal roles in ensuring accuracy, compliance, and strategic oversight. Their responsibilities span from acquisition to disposal, encompassing valuation, depreciation, and reporting.

Key Responsibilities of Accountants and Financial Controllers

Detailed Role Breakdown

-

Asset Recognition and Classification

- Accountants identify and classify fixed assets according to company policy and accounting standards.

- Example: When a manufacturing company purchases a new CNC machine, the accountant ensures it is recorded under machinery assets and not expensed.

-

Initial Measurement and Recording

- Accountants record the acquisition cost, including purchase price, taxes, shipping, and installation.

- Example: For a newly acquired assembly line, the accountant compiles all related costs to determine the asset’s capitalized value.

-

Depreciation Management

- Accountants calculate depreciation using appropriate methods (e.g., straight-line, units of production).

- Financial controllers review and approve depreciation policies to align with financial strategy.

- Example: Calculating monthly depreciation for a manufacturing robot using the declining balance method.

-

Policy Development and Enforcement

- Financial controllers develop fixed asset policies covering capitalization thresholds, depreciation methods, and asset lifecycle management.

- Accountants ensure adherence to these policies in day-to-day accounting.

-

Internal Controls and Audit Preparation

- Controllers implement controls to prevent asset misappropriation.

- Accountants prepare documentation and schedules for internal and external audits.

- Example: Conducting a quarterly physical verification of assets and reconciling with the fixed asset register.

-

Financial Reporting and Compliance

- Controllers oversee the preparation of fixed asset disclosures in financial statements.

- Accountants ensure compliance with IFRS, GAAP, and tax regulations.

Mind Map: Workflow Interaction Between Accountants and Financial Controllers

Practical Example: Managing Fixed Assets in a Manufacturing Firm

Scenario: A manufacturing company acquires a new packaging machine costing $150,000.

-

Accountant’s Role:

- Records the asset at $150,000 plus $10,000 shipping and installation.

- Classifies it under machinery.

- Calculates monthly straight-line depreciation over 10 years.

-

Financial Controller’s Role:

- Reviews and approves the capitalization.

- Ensures the depreciation method aligns with company policy.

- Monitors budget impact and reports to senior management.

This collaboration ensures accurate financial records and strategic asset utilization.

Summary

Accountants and financial controllers complement each other in fixed asset management. Accountants focus on precise record-keeping, calculations, and compliance, while financial controllers emphasize policy, oversight, and strategic alignment. Together, they safeguard asset integrity and support informed decision-making.

1.4 Common Challenges in Fixed Asset Accounting

Fixed asset accounting is a critical function for accountants and financial controllers, especially in the finance and manufacturing sectors. However, it comes with a variety of challenges that can impact accuracy, compliance, and financial reporting. Understanding these challenges and how to address them is essential for effective fixed asset management.

Key Challenges Overview

Data Management Challenges

Maintaining accurate and up-to-date fixed asset records is foundational but often problematic.

- Inaccurate Asset Records: Errors in asset descriptions, acquisition dates, or costs can lead to misstatements.

- Missing Documentation: Lack of purchase invoices or contracts complicates verification.

- Asset Tagging Issues: Without proper tagging or identification, assets can be lost or misclassified.

Example: A manufacturing company purchased a new CNC machine but failed to record the installation costs separately. This led to an understatement of the asset’s capitalized cost and incorrect depreciation calculations.

Depreciation Challenges

Choosing and applying the correct depreciation method and useful life is complex.

- Selecting Appropriate Methods: Different assets may require different methods (e.g., straight-line vs. units of production).

- Calculating Useful Life: Estimating the useful life can be subjective and varies by asset type.

- Handling Changes in Estimates: Adjusting depreciation when asset usage or condition changes.

Example: A financial controller used straight-line depreciation for a manufacturing robot, but the asset’s usage varied significantly year to year. Switching to units of production method improved expense matching but required recalculations and adjustments.

Asset Valuation Challenges

Ensuring assets are valued correctly at acquisition and over time.

- Initial Measurement Errors: Omitting incidental costs like freight or installation.

- Revaluation Complexity: Deciding when and how to revalue assets in compliance with standards.

- Impairment Identification: Detecting when assets have lost value due to obsolescence or damage.

Example: An obsolete manufacturing line was not impaired timely, causing overstated asset values and misleading financial statements.

Compliance Challenges

Staying compliant with evolving accounting standards and tax regulations.

- Adhering to Accounting Standards: IFRS and GAAP have nuanced requirements.

- Tax Regulation Changes: Depreciation methods and asset classifications may differ for tax purposes.

- Audit Readiness: Ensuring documentation and processes withstand external audits.

Example: A finance team missed updates to tax depreciation rules, resulting in penalties and restatements.

Asset Tracking Challenges

Physically tracking assets to prevent loss and ensure accurate records.

- Physical Verification Discrepancies: Differences between records and actual assets.

- Asset Movement and Transfers: Tracking assets moved between locations or departments.

- Theft and Loss Prevention: Implementing controls to reduce asset loss.

Example: During a physical audit, several laptops were unaccounted for due to poor tagging and transfer documentation.

Disposal and Derecognition Challenges

Properly accounting for asset disposals to reflect true financial position.

- Proper Gain/Loss Calculation: Correctly calculating and recording gains or losses on disposal.

- Documentation of Disposal: Maintaining evidence such as sale agreements or scrapping records.

- Timing of Derecognition: Ensuring assets are removed from books at the right time.

Example: A manufacturing firm sold an old machine but delayed derecognition, causing depreciation to be overstated in subsequent periods.

Summary Mind Map

By recognizing these common challenges and applying best practices such as rigorous documentation, regular physical audits, and consistent depreciation policies, accountants and financial controllers can enhance the accuracy and reliability of fixed asset accounting within their organizations.

1.5 Example: Identifying Fixed Assets in a Manufacturing Company

Identifying fixed assets accurately is a crucial step in fixed asset accounting, especially in a manufacturing environment where the variety and scale of assets can be extensive. Fixed assets are tangible items that a company uses in its operations and expects to use for more than one accounting period. These assets are not intended for resale but for production or administrative purposes.

Key Characteristics of Fixed Assets:

- Tangible physical substance

- Used in operations

- Expected to provide economic benefit over multiple years

- Not intended for immediate sale

Mind Map: Identifying Fixed Assets in Manufacturing

Example Scenario:

Company: ABC Manufacturing Ltd.

Situation: The finance team is tasked with identifying which purchases and existing items qualify as fixed assets for the upcoming financial year.

Step 1: Review Purchase Records and Asset Register

- New purchase: CNC machine costing $120,000

- Office chairs costing $300 each

- Factory land acquisition

- Software licenses for design tools

- Delivery truck purchase

Step 2: Apply Fixed Asset Criteria

- CNC machine: Tangible, used in production, cost above capitalization threshold ($5,000), expected life >1 year → Fixed Asset

- Office chairs: Tangible, used in operations, cost $300 each (below threshold), expected life >1 year → Typically expensed unless grouped

- Factory land: Tangible, used in operations, indefinite useful life → Fixed Asset

- Software licenses: Intangible asset, not fixed asset

- Delivery truck: Tangible, used in operations, cost above threshold → Fixed Asset

Step 3: Grouping Low-Cost Items

- Office chairs purchased in bulk (e.g., 50 chairs at $300 each = $15,000) may be capitalized as a group if company policy allows.

Mind Map: Decision Flow for Fixed Asset Identification

Additional Examples:

| Asset Type | Cost | Tangible | Used in Operations | Capitalization Threshold | Fixed Asset? | Notes |

|---|---|---|---|---|---|---|

| Industrial Oven | $75,000 | Yes | Yes | $5,000 | Yes | Used in production |

| Office Printer | $1,200 | Yes | Yes | $5,000 | No | Below threshold, expensed |

| Factory Land | $500,000 | Yes | Yes | N/A | Yes | Land is not depreciated |

| Software License | $20,000 | No | Yes | N/A | No | Intangible asset, treated separately |

| Forklift | $25,000 | Yes | Yes | $5,000 | Yes | Used in material handling |

Summary:

In manufacturing companies, fixed assets typically include land, buildings, machinery, vehicles, and certain grouped low-cost items. The identification process involves evaluating whether the asset is tangible, used in operations, and exceeds the capitalization threshold. Proper identification ensures accurate financial reporting and compliance with accounting standards.

By following this structured approach and using clear policies, accountants and financial controllers can streamline fixed asset identification and maintain reliable asset records.

2. Fixed Asset Classification and Recognition

2.1 Criteria for Asset Recognition

Fixed asset recognition is a fundamental step in fixed asset accounting. Proper recognition ensures that only qualifying assets are recorded on the balance sheet, reflecting the company’s true financial position. This section explores the essential criteria for recognizing an asset, supported by mind maps and practical examples tailored for accountants and financial controllers in the finance and manufacturing sectors.

What is Asset Recognition?

Asset recognition refers to the process of identifying and recording an item as a fixed asset in the accounting records. It involves evaluating whether an item meets specific criteria to be capitalized rather than expensed immediately.

Core Criteria for Asset Recognition

According to accounting standards such as IFRS and GAAP, an asset should be recognized when it meets the following criteria:

- Probable Future Economic Benefits: The asset is expected to generate future economic benefits for the company.

- Control: The company has control over the asset, meaning it can restrict others from using it.

- Cost Measurability: The cost of the asset can be measured reliably.

Mind Map: Criteria for Asset Recognition

Detailed Explanation of Each Criterion

Probable Future Economic Benefits

The asset must be expected to contribute to the company’s cash flows, either directly or indirectly. For manufacturing companies, this could be machinery that increases production output or reduces labor costs. For finance companies, it might be office equipment that supports operational efficiency.

Example: A manufacturing firm purchases a new CNC machine expected to increase production by 20%. Since this machine will generate additional revenue, it meets the probable future economic benefits criterion.

Control

The company must have the ability to use the asset and restrict others from using it. Control is usually established through legal ownership or contractual rights.

Example: A finance company leases office space with an option to purchase. Until the purchase option is exercised, the company does not have control over the building and should not recognize it as a fixed asset.

Cost Measurability

The cost of the asset must be reliably measurable. This includes the purchase price and any costs directly attributable to bringing the asset to working condition.

Example: A manufacturing company buys a machine for $100,000 and pays $5,000 for installation and testing. Both amounts are measurable and should be included in the asset’s cost.

Mind Map: Examples of Asset Recognition

Practical Example: Applying Recognition Criteria

Scenario: A manufacturing company acquires a delivery truck for $50,000. The truck is expected to be used for 5 years to deliver products, increasing customer satisfaction and reducing third-party logistics costs.

- Probable Future Economic Benefits: Yes, through cost savings and improved delivery.

- Control: Yes, the company owns the truck.

- Cost Measurability: Yes, purchase price and registration fees are documented.

Conclusion: The truck qualifies as a fixed asset and should be recognized on the balance sheet.

Best Practice Tips for Accountants and Financial Controllers

- Establish clear thresholds for capitalization to avoid ambiguity.

- Maintain detailed documentation supporting each asset’s recognition.

- Regularly review asset recognition policies to align with current accounting standards.

- Train staff involved in asset acquisition to understand recognition criteria.

By rigorously applying these criteria, finance and manufacturing professionals can ensure accurate and compliant fixed asset accounting, leading to better financial reporting and asset management.

2.2 Categories of Fixed Assets in Manufacturing and Finance

Fixed assets are long-term tangible assets that a company uses in its operations to generate income. In both manufacturing and finance sectors, categorizing fixed assets correctly is crucial for accurate accounting, depreciation, and financial reporting.

Categories of Fixed Assets

Fixed assets can be broadly categorized into the following types:

- Property, Plant, and Equipment (PPE)

- Furniture and Fixtures

- Vehicles

- Land and Buildings

- Leasehold Improvements

- Computer Equipment and Software

Let’s explore these categories with a focus on their relevance to manufacturing and finance industries.

Mind Map: Fixed Asset Categories Overview

Property, Plant, and Equipment (PPE)

Manufacturing:

- Includes heavy machinery, production lines, conveyor belts, and specialized tools.

- Example: A stamping press used in an automotive parts factory.

Finance:

- Typically includes office equipment like computers and servers, but may also include data centers.

- Example: High-performance servers used for financial trading platforms.

Best Practice: Maintain detailed asset registers specifying asset type, location, and usage to ensure proper classification.

Land and Buildings

Manufacturing:

- Factory buildings, warehouses, and land used for production.

- Example: A manufacturing plant building where assembly lines are housed.

Finance:

- Office buildings, branch locations, and land for corporate offices.

- Example: Headquarters building for a financial services firm.

Best Practice: Separate land from buildings in accounting records since land is not depreciable.

Furniture and Fixtures

Manufacturing:

- Workbenches, storage racks, and factory office furniture.

- Example: Ergonomic chairs and desks in the factory’s administrative office.

Finance:

- Office desks, chairs, filing cabinets, and conference room furniture.

- Example: Executive office furniture in a financial controller’s office.

Best Practice: Track furniture separately to apply appropriate depreciation rates.

Vehicles

Manufacturing:

- Delivery trucks, forklifts, and company cars used for logistics.

- Example: Forklifts used to move raw materials within the factory.

Finance:

- Company cars for executives, vehicles used for client visits.

- Example: Fleet of cars used by financial advisors.

Best Practice: Maintain usage logs to justify asset classification and depreciation.

Leasehold Improvements

Manufacturing:

- Modifications to leased factory spaces such as installing specialized ventilation or electrical systems.

- Example: Installing heavy-duty power outlets for machinery.

Finance:

- Office renovations, partitions, and custom lighting.

- Example: Building a secure server room in a leased office.

Best Practice: Capitalize leasehold improvements separately and amortize over the lease term.

Computer Equipment and Software

Manufacturing:

- Computers controlling machinery, CAD software licenses.

- Example: CNC machine controllers and design software.

Finance:

- Financial reporting software, trading platforms, and office computers.

- Example: Accounting software licenses and high-end workstations.

Best Practice: Distinguish between hardware (capitalized) and software (capitalized or expensed based on cost and useful life).

Mind Map: Example - Manufacturing Fixed Asset Categories

Mind Map: Example - Finance Fixed Asset Categories

Practical Example

Scenario: A manufacturing company purchases a new stamping press for $500,000, installs it for $50,000, and buys a delivery truck for $80,000.

- The stamping press and installation costs are recorded under “Machinery & Equipment” (PPE).

- The delivery truck is recorded under “Vehicles”.

Accounting Treatment:

- Both assets are capitalized and depreciated according to their useful lives.

- Installation costs are included in the asset cost basis.

Why Classification Matters:

- Different asset categories may have different depreciation methods or useful lives.

- Accurate classification ensures compliance with accounting standards and tax regulations.

Summary

Correctly categorizing fixed assets in manufacturing and finance sectors helps streamline asset management, ensures accurate financial reporting, and supports compliance with accounting standards. Using clear categories and examples enables accountants and financial controllers to maintain precise records and apply best practices effectively.

2.3 Capital vs Expense: Understanding Thresholds

In fixed asset accounting, one of the critical decisions accountants and financial controllers face is determining whether a cost should be capitalized as a fixed asset or expensed immediately. This decision impacts not only the balance sheet but also the income statement, affecting profitability and tax calculations.

What is Capitalization?

Capitalization refers to recording a cost as an asset on the balance sheet rather than an expense on the income statement. Capitalized costs are then depreciated over the asset’s useful life.

What is an Expense?

An expense is a cost that is recognized immediately in the income statement, reducing the net income for the period.

Understanding Thresholds

A capitalization threshold is a pre-determined monetary limit set by an organization to decide whether a purchase should be capitalized or expensed. Costs below this threshold are expensed immediately, while those above are capitalized.

Why Are Thresholds Important?

- Materiality: Avoids capitalizing insignificant costs that complicate bookkeeping.

- Consistency: Ensures uniform treatment of similar transactions.

- Compliance: Aligns with accounting standards and tax regulations.

Mind Map: Capital vs Expense Decision Factors

Example 1: Applying Capitalization Threshold in a Manufacturing Company

Scenario: A manufacturing company has set a capitalization threshold of $5,000.

- Purchase of a new machine part costing $4,800

- Purchase of a new conveyor belt costing $12,000

Accounting Treatment:

- The $4,800 machine part is expensed immediately since it is below the threshold.

- The $12,000 conveyor belt is capitalized and added to fixed assets.

Mind Map: Example 1 Breakdown

Example 2: Capital vs Expense Based on Useful Life

Scenario: A finance company buys office furniture costing $6,000.

- The furniture is expected to last 8 years.

Accounting Treatment:

- Since the cost exceeds the threshold and the useful life is more than one year, the cost is capitalized and depreciated over 8 years.

If the same company buys office supplies costing $6,000 but expected to be used up within 6 months, the cost would be expensed immediately despite exceeding the threshold.

Mind Map: Example 2 Useful Life Consideration

Best Practices for Setting and Applying Thresholds

- Define Clear Policies: Document thresholds and criteria for capitalization.

- Review Annually: Adjust thresholds based on inflation and company size.

- Train Staff: Ensure accounting and procurement teams understand policies.

- Use Examples: Provide real-life scenarios to guide decision-making.

- Leverage Technology: Use accounting software to automate threshold checks.

Summary

Understanding the distinction between capital and expense based on thresholds is essential for accurate financial reporting. The decision hinges on cost amount, useful life, nature of the expenditure, and organizational policies. Applying these principles consistently helps maintain compliance and provides clearer insights into company financial health.

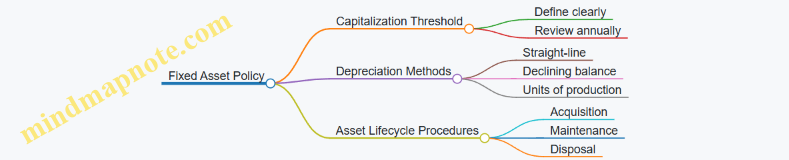

2.4 Best Practice: Establishing a Fixed Asset Policy

Establishing a comprehensive fixed asset policy is a cornerstone of effective fixed asset accounting. It ensures consistency, accuracy, and compliance across the organization, especially in sectors like manufacturing and finance where asset management is critical.

Why Establish a Fixed Asset Policy?

- Standardization: Provides uniform guidelines for asset recognition, classification, depreciation, and disposal.

- Control: Helps prevent asset misappropriation and ensures proper documentation.

- Compliance: Aligns with accounting standards (IFRS, GAAP) and tax regulations.

- Efficiency: Streamlines processes and reduces errors.

Key Components of a Fixed Asset Policy

Step-by-Step Guide to Establishing Your Fixed Asset Policy

-

Define Asset Recognition Criteria:

- Set minimum capitalization thresholds (e.g., $5,000 for machinery).

- Clarify what qualifies as a fixed asset versus an expense.

-

Classify Assets Clearly:

- Categorize assets by type (e.g., machinery, vehicles, computers).

- Assign asset codes for easy tracking.

-

Determine Valuation Methods:

- Include purchase price, taxes, installation, and transportation costs.

-

Select Depreciation Methods:

- Choose methods suitable for asset types (e.g., straight-line for buildings, units of production for machinery).

-

Set Maintenance and Repair Guidelines:

- Define when costs should be capitalized or expensed.

-

Outline Disposal Procedures:

- Establish steps for asset retirement, sale, or write-off.

-

Implement Documentation and Record-Keeping:

- Maintain an up-to-date fixed asset register.

- Keep invoices, contracts, and disposal records.

-

Schedule Regular Physical Verifications:

- Conduct annual or bi-annual asset counts.

-

Ensure Compliance:

- Align policy with current accounting standards and tax laws.

-

Assign Roles and Responsibilities:

- Define who is responsible for asset management, accounting entries, and audits.

Example: Fixed Asset Policy Excerpt for a Manufacturing Company

Capitalization Threshold: All assets with a cost of $5,000 or more and useful life exceeding one year will be capitalized.

Depreciation Method: Straight-line method over estimated useful lives:

- Machinery: 10 years

- Vehicles: 5 years

- Office Equipment: 3 years

Maintenance: Routine repairs are expensed; major upgrades extending asset life are capitalized.

Disposal: Assets disposed of must be removed from the asset register and any gain or loss recorded in the financial statements.

Practical Example: Applying the Policy

A manufacturing firm purchases a new CNC machine for $45,000. Installation costs amount to $3,000, and transportation costs are $1,000.

- Recognition: Since total cost ($49,000) exceeds the $5,000 threshold, the asset is capitalized.

- Valuation: Asset cost recorded as $49,000 (purchase + installation + transportation).

- Depreciation: Using straight-line over 10 years.

- Maintenance: Routine repairs expensed; any major upgrades capitalized.

Mind Map: Asset Lifecycle Under the Policy

Tips for Successful Policy Implementation

- Communicate Clearly: Train accounting and operational teams on the policy.

- Review Regularly: Update policy to reflect changes in regulations or business needs.

- Leverage Technology: Use fixed asset management software to enforce policy rules.

- Audit Compliance: Periodic internal audits to ensure adherence.

By establishing and rigorously following a fixed asset policy, accountants and financial controllers can enhance accuracy, improve asset control, and ensure compliance, ultimately supporting better financial decision-making within manufacturing and finance organizations.

2.5 Example: Classifying a New Machinery Purchase

When a manufacturing company purchases new machinery, correctly classifying the asset is crucial for accurate fixed asset accounting. This classification impacts depreciation, tax treatment, and financial reporting.

Step 1: Identify the Asset

- What is being purchased?

- A piece of machinery used in the production process.

- Purpose:

- To manufacture products, improve efficiency, or replace old equipment.

Step 2: Determine if the Asset Meets Recognition Criteria

According to accounting standards, an asset should be recognized if:

- It is probable that future economic benefits will flow to the entity.

- The cost of the asset can be measured reliably.

In this case, the machinery:

- Will be used for several years in production.

- Has a clear purchase price and associated costs.

Therefore, it qualifies as a fixed asset.

Step 3: Classify the Asset

Fixed assets are typically categorized into:

- Land

- Buildings

- Machinery and Equipment

- Furniture and Fixtures

- Vehicles

- Leasehold Improvements

Since this is a manufacturing machine, it falls under Machinery and Equipment.

Step 4: Assess Capitalization Threshold

Many companies set a minimum cost threshold for capitalization (e.g., $5,000). If the machinery cost exceeds this, it is capitalized; otherwise, it is expensed.

Example:

- Machinery cost: $50,000

- Installation cost: $5,000

- Total cost: $55,000

Since $55,000 > $5,000 threshold, capitalize the asset.

Step 5: Include All Relevant Costs

Capitalized cost includes:

- Purchase price

- Import duties and non-refundable taxes

- Delivery and handling

- Installation and assembly

- Testing and calibration

Example:

| Cost Component | Amount ($) |

|---|---|

| Purchase Price | 50,000 |

| Delivery | 1,000 |

| Installation | 4,000 |

| Testing | 500 |

| Total Capitalized Cost | 55,500 |

Step 6: Mind Map - Classifying New Machinery Purchase

Step 7: Accounting Treatment Example

Journal Entry on Acquisition:

| Account | Debit ($) | Credit ($) |

|---|---|---|

| Machinery & Equipment | 55,500 | |

| Accounts Payable/Cash | 55,500 |

Step 8: Additional Considerations

- Componentization: If the machinery has significant parts with different useful lives, consider separating components for depreciation.

- Leased Machinery: If the machinery is leased, different accounting treatment applies.

- Asset Tagging: Assign an asset ID for tracking.

Step 9: Summary

Classifying a new machinery purchase involves:

- Confirming it meets fixed asset recognition criteria.

- Categorizing it under machinery and equipment.

- Including all costs necessary to bring the asset to working condition.

- Applying capitalization thresholds.

- Recording the asset properly in the accounting system.

This ensures accurate financial reporting and compliance with accounting standards.

3. Asset Acquisition and Initial Measurement

3.1 Recording Asset Cost: Purchase Price and Incidental Costs

When recording fixed assets, it is crucial to accurately capture the total cost of acquisition. This includes not only the purchase price but also all incidental costs necessary to bring the asset to its intended use. Properly accounting for these costs ensures compliance with accounting standards and provides a true reflection of the asset’s value on the balance sheet.

What Constitutes Asset Cost?

- Purchase Price: The amount paid to acquire the asset, including any discounts or rebates.

- Incidental Costs: Additional expenses directly attributable to bringing the asset to working condition.

Incidental Costs Examples:

- Transportation and freight charges

- Installation and assembly costs

- Testing and calibration expenses

- Import duties and non-refundable taxes

- Professional fees (e.g., engineers, architects)

- Site preparation costs

Mind Map: Components of Asset Cost

Best Practice: Comprehensive Cost Capture

- Establish Clear Policies: Define what costs should be capitalized versus expensed.

- Document All Costs: Maintain supporting documents such as invoices, contracts, and freight bills.

- Coordinate with Procurement and Operations: Ensure all relevant incidental costs are communicated to accounting.

- Review Regularly: Periodically audit asset costs to ensure accuracy.

Example 1: Recording a New Machine Purchase

Scenario: A manufacturing company purchases a machine for $100,000. Additional costs include:

- Freight charges: $2,000

- Installation and testing: $3,000

- Import duty: $5,000

- Training for operators (expensed): $1,000

Accounting Treatment:

- Capitalize: $100,000 + $2,000 + $3,000 + $5,000 = $110,000

- Expense: $1,000 (training cost)

Journal Entry:

Dr. Fixed Asset (Machine) $110,000

Dr. Training Expense $1,000

Cr. Accounts Payable / Cash $111,000

Mind Map: Example 1 Breakdown

Example 2: Multi-Component Asset Purchase

Scenario: A finance company acquires office equipment that includes a computer system ($5,000) and specialized software ($2,000). Installation costs are $500.

Accounting Treatment:

- Capitalize computer system and installation: $5,000 + $500 = $5,500

- Software may be capitalized or expensed depending on policy and useful life.

Journal Entry:

Dr. Fixed Asset (Computer System) $5,500

Dr. Software (Intangible Asset) $2,000

Cr. Accounts Payable / Cash $7,500

Mind Map: Example 2 Breakdown

Summary

Recording the full cost of fixed assets requires careful consideration of all costs directly attributable to acquisition and preparation for use. By capturing purchase price and incidental costs accurately, accountants and financial controllers ensure assets are valued correctly, supporting reliable financial reporting and decision-making.

3.2 Treatment of Installation and Setup Costs

Installation and setup costs are critical components of the total cost of acquiring a fixed asset. Proper accounting treatment ensures that these costs are capitalized correctly, reflecting the true value of the asset on the balance sheet and enabling accurate depreciation calculations.

What Are Installation and Setup Costs?

Installation and setup costs include all expenses directly attributable to bringing the asset to its intended use. These may involve:

- Transportation and handling fees

- Assembly and installation labor

- Testing and calibration

- Site preparation

- Professional fees related to installation

Capitalization vs Expense

The key accounting principle is to capitalize costs that are necessary to prepare the asset for use, while expensing routine maintenance or operational costs.

Mind Map: Components of Installation and Setup Costs

Best Practice: Capitalize All Directly Attributable Costs

Accountants should ensure that all costs directly related to installation and setup are capitalized as part of the asset’s cost base. This approach aligns with accounting standards such as IAS 16 and ASC 360.

Example 1: Capitalizing Installation Costs for a New Manufacturing Machine

Scenario: A manufacturing company purchases a new machine for $100,000. Additional costs include:

- Freight and handling: $5,000

- Installation labor: $3,000

- Calibration and testing: $2,000

- Training operators: $1,000

Treatment:

- Capitalize $5,000 + $3,000 + $2,000 = $10,000 as installation and setup costs

- Expense $1,000 as training is considered an operational expense

Journal Entry:

| Account | Debit | Credit |

|---|---|---|

| Fixed Asset - Machine | $110,000 | |

| Cash/Accounts Payable | $110,000 |

Mind Map: Capitalization Decision Flow

Example 2: Treatment of Site Preparation Costs

Scenario: Before installing a new piece of equipment, the company incurs $7,000 in site preparation (floor reinforcement, electrical wiring).

Treatment:

- Since these costs are necessary to prepare the asset for use, they should be capitalized as part of the asset cost.

Summary Checklist for Installation and Setup Costs

- Identify all costs directly related to installation and setup

- Verify whether each cost is necessary to bring the asset to working condition

- Capitalize all qualifying costs

- Expense costs related to training, administration, or routine maintenance

- Maintain detailed documentation and supporting invoices

By carefully distinguishing between capitalizable installation and setup costs and operational expenses, accountants and financial controllers can ensure accurate asset valuation and compliance with accounting standards.

3.3 Best Practice: Documenting Acquisition Costs with Supporting Evidence

Proper documentation of acquisition costs is a cornerstone of accurate fixed asset accounting. It ensures transparency, facilitates audits, and supports compliance with accounting standards such as IFRS and GAAP. This section outlines best practices for documenting acquisition costs, supported by practical examples and mind maps to visualize the process.

Why Document Acquisition Costs Thoroughly?

- Audit Readiness: Clear evidence supports the recorded asset value.

- Compliance: Meets regulatory and tax requirements.

- Financial Accuracy: Ensures correct capitalization and depreciation.

- Dispute Resolution: Provides proof in case of vendor or internal disputes.

Key Components of Acquisition Costs

- Purchase price (invoice amount)

- Import duties and non-refundable taxes

- Delivery and handling charges

- Installation and assembly costs

- Professional fees (e.g., architects, engineers)

- Testing and calibration expenses

Mind Map: Documenting Acquisition Costs

Best Practices for Documenting Acquisition Costs

-

Collect All Relevant Documents at Acquisition

- Ensure purchase orders, invoices, shipping documents, and contracts are gathered immediately.

- Example: When purchasing a CNC machine, collect the vendor invoice, shipping bill, installation contract, and calibration certificate.

-

Use a Standardized Asset Acquisition Form

- Create a form capturing all cost components and approvals.

- Example: A manufacturing firm uses a fixed asset acquisition checklist that includes fields for purchase price, taxes, freight, installation, and approval signatures.

-

Maintain a Centralized Repository

- Store all documents digitally in a secure, searchable system.

- Example: Financial controllers use ERP modules or document management systems to link acquisition documents directly to asset records.

-

Ensure Proper Authorization and Approval

- Document capital expenditure approvals before asset purchase.

- Example: A financial controller requires a signed capex approval form before processing the asset acquisition.

-

Tag and Register Assets Promptly

- Assign asset IDs and update fixed asset registers with acquisition details.

- Example: Upon delivery, the asset is tagged with a barcode and entered into the asset management system with acquisition cost details.

-

Reconcile Physical Assets with Documentation

- Conduct physical verification to confirm asset existence and condition.

- Example: After installation, the accounting team verifies the asset against purchase documents and updates records accordingly.

Example Scenario: Documenting Acquisition Costs for a New Manufacturing Robot

- Step 1: Receive vendor invoice for $150,000 including purchase price and non-refundable taxes.

- Step 2: Obtain freight bill showing $5,000 shipping cost.

- Step 3: Collect installation contract invoice for $10,000.

- Step 4: Secure capital expenditure approval signed by CFO.

- Step 5: Enter all costs into a fixed asset acquisition form totaling $165,000.

- Step 6: Upload all documents into the ERP system linked to the asset record.

- Step 7: Tag the robot with an asset ID and conduct physical verification.

Mind Map: Acquisition Cost Documentation Workflow

Summary

Documenting acquisition costs with comprehensive supporting evidence is essential for accurate fixed asset accounting. By following standardized processes, maintaining centralized records, and ensuring proper approvals, accountants and financial controllers can safeguard asset valuation integrity and streamline audit processes.

This practice not only supports compliance but also enhances financial transparency and operational efficiency within finance and manufacturing sectors.

3.4 Example: Accounting for a Multi-Component Asset Purchase

When a company purchases a multi-component asset, it means the asset consists of several significant parts or components, each with different useful lives or depreciation methods. Proper accounting requires identifying, valuing, and depreciating each component separately to reflect the asset’s true economic consumption.

What is a Multi-Component Asset?

A multi-component asset is a single asset made up of multiple parts that can be separately identified and have distinct useful lives or depreciation characteristics.

Example: A manufacturing machine that includes the main frame, electronic control system, and conveyor belt.

Why Separate Components?

- Different components may have different useful lives.

- Accurate depreciation expense allocation.

- Better asset management and replacement planning.

Step-by-Step Accounting Process

Practical Example

Scenario:

A manufacturing company purchases a new production machine for $120,000. The machine has three main components:

| Component | Estimated Cost | Useful Life (Years) | Depreciation Method |

|---|---|---|---|

| Main Frame | $70,000 | 10 | Straight-Line |

| Electronic Control | $30,000 | 5 | Declining Balance |

| Conveyor Belt | $20,000 | 4 | Units of Production |

Installation costs of $5,000 are incurred, allocated proportionally based on component cost.

Step 1: Allocate Installation Costs

- Total component cost = $120,000

- Installation cost allocation:

- Main Frame: (70,000 / 120,000) * 5,000 = $2,916.67

- Electronic Control: (30,000 / 120,000) * 5,000 = $1,250

- Conveyor Belt: (20,000 / 120,000) * 5,000 = $833.33

Step 2: Calculate Total Cost per Component

| Component | Cost | Installation | Total Cost |

|---|---|---|---|

| Main Frame | $70,000 | $2,916.67 | $72,916.67 |

| Electronic Control | $30,000 | $1,250 | $31,250 |

| Conveyor Belt | $20,000 | $833.33 | $20,833.33 |

Step 3: Depreciation Calculations

-

Main Frame (Straight-Line):

- Annual Depreciation = $72,916.67 / 10 = $7,291.67

-

Electronic Control (Declining Balance at 40%):

- Year 1 Depreciation = $31,250 * 40% = $12,500

- Year 2 Depreciation = ($31,250 - $12,500) * 40% = $7,500

-

Conveyor Belt (Units of Production):

- Assume total expected production = 100,000 units

- Cost per unit = $20,833.33 / 100,000 = $0.2083

- If 20,000 units produced in Year 1, depreciation = 20,000 * $0.2083 = $4,166.67

Mind Map: Depreciation Methods for Components

Journal Entries Example (Year 1)

| Date | Account | Debit | Credit |

|---|---|---|---|

| Purchase | Fixed Assets - Main Frame | $72,916.67 | |

| Purchase | Fixed Assets - Electronic Control | $31,250 | |

| Purchase | Fixed Assets - Conveyor Belt | $20,833.33 | |

| Purchase | Accounts Payable/Cash | $125,000 | |

| Depreciation Expense | Depreciation Expense - Main Frame | $7,291.67 | |

| Accumulated Depreciation | Accumulated Depreciation - Main Frame | $7,291.67 | |

| Depreciation Expense | Depreciation Expense - Electronic Control | $12,500 | |

| Accumulated Depreciation | Accumulated Depreciation - Electronic Control | $12,500 | |

| Depreciation Expense | Depreciation Expense - Conveyor Belt | $4,166.67 | |

| Accumulated Depreciation | Accumulated Depreciation - Conveyor Belt | $4,166.67 |

Best Practices Summary

- Always identify significant components separately.

- Allocate costs, including installation, proportionally.

- Use appropriate depreciation methods per component.

- Maintain detailed documentation for audit trails.

- Update fixed asset registers to reflect componentization.

This approach ensures accurate financial reporting and asset management, especially critical in manufacturing environments where machinery components have varying lifespans and usage patterns.

3.5 Handling Asset Donations and Transfers

Handling asset donations and transfers is a critical part of fixed asset accounting, especially in industries like manufacturing and finance where asset management impacts both operational efficiency and financial reporting. This section covers best practices, accounting treatments, and practical examples to help accountants and financial controllers manage these transactions effectively.

Understanding Asset Donations and Transfers

- Asset Donations: When a company donates fixed assets to another entity (e.g., charity, subsidiary, or partner), it must properly account for the removal of the asset from its books and recognize any gain or loss.

- Asset Transfers: Transfers occur when assets move between departments, divisions, or entities within the same organization, or between related parties. These transfers may or may not involve monetary consideration.

Best Practices for Handling Donations and Transfers

- Documentation: Maintain thorough documentation including transfer agreements, donation letters, and approval records.

- Valuation: Determine the fair value of the asset at the time of donation or transfer.

- Accounting Treatment: Derecognize the asset from the donor’s books and recognize any gain or loss.

- Tax Considerations: Understand the tax implications, including potential deductions for donations or taxable events for transfers.

- Internal Controls: Implement controls to ensure assets are properly authorized for donation or transfer.

Mind Map: Asset Donations and Transfers Overview

Accounting Treatment Steps

Example 1: Donating Manufacturing Equipment

Scenario: A manufacturing company donates a piece of machinery to a local technical school.

- Original cost: $100,000

- Accumulated depreciation: $60,000

- Carrying amount: $40,000

- Fair value at donation date: $45,000

Accounting entries:

- Derecognize asset and accumulated depreciation:

- Debit Accumulated Depreciation $60,000

- Credit Fixed Asset $100,000

- Recognize gain on donation:

- Debit Donation Expense or Loss $ (if any)

- Credit Gain on Disposal $5,000 (Fair value $45,000 - Carrying amount $40,000)

Note: The gain may be recognized differently depending on accounting standards and company policy.

Example 2: Transferring Assets Between Divisions

Scenario: A finance company transfers office equipment from its headquarters to a regional office.

- Carrying amount: $20,000

- Transfer price: $20,000 (no gain or loss)

Accounting entries:

-

At transferring division:

- Debit Intercompany Receivable $20,000

- Credit Fixed Asset $20,000

-

At receiving division:

- Debit Fixed Asset $20,000

- Credit Intercompany Payable $20,000

Best Practice: Ensure transfer prices reflect fair value to avoid tax or regulatory issues.

Mind Map: Accounting Workflow for Donations and Transfers

Summary

Effectively handling asset donations and transfers requires clear policies, accurate valuation, and proper accounting treatment to maintain financial integrity and compliance. By following best practices and documenting every step, accountants and financial controllers can ensure transparency and accuracy in fixed asset management.

For further reading, consider reviewing relevant accounting standards such as IAS 16 (Property, Plant and Equipment) and ASC 360 (Property, Plant, and Equipment) for US GAAP.

4. Fixed Asset Depreciation Methods

4.1 Overview of Depreciation and Its Purpose

Depreciation is a fundamental concept in fixed asset accounting that refers to the systematic allocation of the cost of a tangible fixed asset over its useful life. It reflects the wear and tear, usage, or obsolescence of an asset as it contributes to generating revenue for a business.

Why is Depreciation Important?

- Matching Principle: Depreciation aligns the expense recognition with the revenue generated by the asset, ensuring accurate profit measurement.

- Asset Valuation: It reduces the book value of the asset on the balance sheet to reflect its current worth.

- Tax Benefits: Depreciation expense can be deducted for tax purposes, reducing taxable income.

- Financial Planning: Helps in budgeting for asset replacement and maintenance.

Mind Map: Purpose of Depreciation

Types of Assets Subject to Depreciation

- Machinery and Equipment

- Buildings and Facilities

- Vehicles

- Furniture and Fixtures

Assets like land are not depreciated because they generally do not lose value over time.

How Depreciation Works: A Simple Example

Example: A manufacturing company purchases a machine for $50,000. The machine has an estimated useful life of 10 years and a residual (salvage) value of $5,000.

- Cost of the asset: $50,000

- Residual value: $5,000

- Useful life: 10 years

The depreciable amount = Cost - Residual value = $50,000 - $5,000 = $45,000

If using the straight-line method (equal expense each year), annual depreciation expense = $45,000 / 10 = $4,500

Each year, $4,500 is recorded as depreciation expense, reducing the asset’s book value accordingly.

Mind Map: Depreciation Calculation Components

Real-World Example in Manufacturing

A financial controller in a manufacturing firm oversees the depreciation of a production line conveyor system:

- Initial cost: $120,000

- Useful life: 8 years

- Residual value: $10,000

Using straight-line depreciation:

- Depreciable amount = $120,000 - $10,000 = $110,000

- Annual depreciation = $110,000 / 8 = $13,750

This annual expense is recorded in the financial statements, ensuring the cost of the conveyor system is matched with the revenue it helps generate.

Summary

Depreciation is essential for accurately reflecting the consumption of fixed assets over time. It ensures compliance with accounting principles, aids in tax planning, and supports strategic financial decisions.

By understanding its purpose and calculation, accountants and financial controllers can better manage asset costs and provide transparent financial reporting.

4.2 Common Depreciation Methods: Straight-Line, Declining Balance, Units of Production

Depreciation is a systematic allocation of the cost of a fixed asset over its useful life. Choosing the right depreciation method is crucial for accurate financial reporting and tax compliance. Below, we explore three common depreciation methods used widely in finance and manufacturing sectors: Straight-Line, Declining Balance, and Units of Production.

Mind Map: Overview of Depreciation Methods

Straight-Line Depreciation

Definition: The Straight-Line method spreads the cost of an asset evenly over its estimated useful life.

Formula: \[ \text{Annual Depreciation Expense} = \frac{\text{Cost of Asset} - \text{Residual Value}}{\text{Useful Life (years)}} \]

Example: A manufacturing company purchases a machine for $100,000 with a residual value of $10,000 and an estimated useful life of 10 years.

- Annual Depreciation = (100,000 - 10,000) / 10 = $9,000 per year

Best Practice: Use this method when the asset is expected to provide equal utility over its life, such as office furniture or buildings.

Mind Map: Straight-Line Depreciation

Declining Balance Depreciation

Definition: An accelerated depreciation method that expenses more depreciation in the early years of an asset’s life and less in later years.

Formula: \[ \text{Depreciation Expense} = \text{Book Value at Beginning of Year} \times \text{Depreciation Rate} \]

Commonly, the Double Declining Balance (DDB) method is used, which doubles the straight-line rate.

Example: Using the same machine ($100,000 cost, $10,000 residual, 10-year life):

- Straight-line rate = 1/10 = 10%

- Double declining rate = 20%

Year 1 depreciation = 100,000 x 20% = $20,000

Year 2 depreciation = (100,000 - 20,000) x 20% = $16,000

Best Practice: Ideal for assets that lose value quickly or become obsolete, such as technology or specialized manufacturing equipment.

Mind Map: Declining Balance Depreciation

Units of Production Depreciation

Definition: Depreciation based on actual usage or production output rather than time.

Formula: \[ \text{Depreciation Expense} = \left( \frac{\text{Cost} - \text{Residual Value}}{\text{Total Estimated Production}} \right) \times \text{Units Produced in Period} \]

Example: A machine costs $100,000 with a residual value of $10,000 and an estimated total production of 500,000 units.

If in Year 1, the machine produces 50,000 units:

- Depreciation Expense = ((100,000 - 10,000) / 500,000) x 50,000 = $9,000

Best Practice: Use this method for manufacturing assets where wear and tear correlate directly with usage, such as production line machinery.

Mind Map: Units of Production Depreciation

Summary Table of Depreciation Methods

| Method | Calculation Basis | Expense Pattern | Best Use Case |

|---|---|---|---|

| Straight-Line | Time (years) | Equal expense each year | Assets with consistent usage |

| Declining Balance | Book value x rate | Higher early, lower later | Assets losing value quickly |

| Units of Production | Usage (units produced) | Variable expense | Manufacturing equipment tied to output |

Practical Example Combining Methods

A manufacturing company has two assets:

- Asset A: Office building, $500,000 cost, 20-year life, $50,000 residual.

- Asset B: CNC machine, $200,000 cost, 10-year life, $20,000 residual, estimated 1,000,000 units production.

Asset A: Use Straight-Line

- Annual Depreciation = (500,000 - 50,000) / 20 = $22,500

Asset B: Use Units of Production

- Depreciation per unit = (200,000 - 20,000) / 1,000,000 = $0.18

- If 100,000 units produced in Year 1, Depreciation = 100,000 x 0.18 = $18,000

This approach aligns depreciation expense with asset usage and economic benefit.

By understanding and applying these depreciation methods with relevant examples, accountants and financial controllers can ensure accurate asset valuation and compliance with accounting standards.

4.3 Selecting the Appropriate Depreciation Method for Manufacturing Assets

Selecting the right depreciation method for manufacturing assets is crucial for accurately reflecting the asset’s consumption, matching expenses with revenues, and ensuring compliance with accounting standards. Different assets wear out or lose value in different ways, and choosing an appropriate method helps in better financial planning and reporting.

Key Factors to Consider When Selecting a Depreciation Method

- Nature of the Asset Usage: How the asset is utilized in production.

- Pattern of Economic Benefits: Whether the asset provides equal benefits over time or more benefits in earlier or later years.

- Maintenance and Repair Schedule: Assets with frequent repairs might have different depreciation patterns.

- Tax and Regulatory Requirements: Some jurisdictions may prescribe or favor certain methods.

- Financial Reporting Objectives: Whether the goal is to smooth expenses or reflect actual usage.

Common Depreciation Methods for Manufacturing Assets

| Method | Description | Suitability for Manufacturing Assets |

|---|---|---|

| Straight-Line (SL) | Allocates equal depreciation expense each year. | Suitable for assets with consistent usage over time. |

| Declining Balance (DB) | Accelerated method; higher expense in early years. | Suitable for assets that lose value quickly or become obsolete fast. |

| Units of Production (UoP) | Depreciation based on actual usage or output. | Ideal for machinery where wear depends on production volume. |

Mind Map: Factors Influencing Depreciation Method Choice

Mind Map: Depreciation Methods Overview

Example 1: Straight-Line Depreciation for a Manufacturing Building

Scenario: A manufacturing company purchases a factory building for $1,000,000 with an expected useful life of 40 years and no residual value.

-

Calculation:

- Annual Depreciation = Cost / Useful Life = $1,000,000 / 40 = $25,000 per year

-

Rationale: The building provides consistent economic benefits over time, making straight-line the most appropriate method.

Example 2: Declining Balance Depreciation for Manufacturing Equipment

Scenario: A company buys a specialized machine for $200,000 with a useful life of 5 years, residual value of $10,000, and expects rapid technological obsolescence.

-

Method: Double Declining Balance (DDB)

-

Rate: 2 x (1/5) = 40%

-

Year 1 Depreciation: $200,000 x 40% = $80,000

-

Year 2 Depreciation: ($200,000 - $80,000) x 40% = $48,000

-

Rationale: Accelerated depreciation matches higher expense in early years when the asset is more productive and loses value faster.

Example 3: Units of Production Depreciation for a Manufacturing Machine

Scenario: A machine costs $150,000, has an expected total production output of 300,000 units, and a residual value of $15,000.

-

Depreciation per Unit: (Cost - Residual Value) / Total Units = ($150,000 - $15,000) / 300,000 = $0.45 per unit

-

If the machine produces 50,000 units in Year 1:

- Depreciation Expense = 50,000 x $0.45 = $22,500

-

Rationale: This method aligns depreciation expense with actual usage, ideal for production-based wear and tear.

Best Practices for Selecting Depreciation Method

- Assess Asset Usage Patterns: Understand how the asset contributes to production.

- Consult Regulatory Guidelines: Ensure compliance with tax and accounting standards.

- Document the Rationale: Keep clear records explaining the chosen method.

- Review Periodically: Reassess method suitability as business conditions or asset usage changes.

- Use Consistent Methods: Avoid frequent changes to maintain comparability.

Summary

Choosing the appropriate depreciation method for manufacturing assets depends on the asset’s usage, economic benefit pattern, and regulatory environment. Straight-line is simple and effective for assets with uniform usage, declining balance suits assets with rapid obsolescence, and units of production best reflect wear based on actual output. Integrating these considerations with clear documentation and periodic review ensures accurate financial reporting and asset management.

4.4 Best Practice: Consistency and Documentation in Depreciation Policies

Maintaining consistency and thorough documentation in depreciation policies is crucial for accountants and financial controllers, especially within the finance and manufacturing sectors. This ensures accurate financial reporting, compliance with accounting standards, and facilitates audit processes.

Why Consistency Matters

- Comparability: Consistent depreciation methods allow for meaningful comparison across periods.

- Reliability: Financial statements become more reliable and trustworthy.

- Compliance: Helps meet regulatory requirements such as IFRS and GAAP.

- Audit Readiness: Simplifies audit trails and reduces risk of errors or misstatements.

Key Components of a Depreciation Policy

Best Practices for Consistency

-

Standardize Depreciation Methods Across Asset Classes

- Use the same depreciation method for similar assets (e.g., straight-line for office equipment).

- Avoid frequent changes unless justified by significant changes in asset usage or technology.

-

Define Useful Lives and Residual Values Clearly

- Establish realistic useful life estimates based on manufacturer data, industry benchmarks, and historical experience.

- Document residual values and update only when there is evidence of change.

-

Regularly Review and Approve Policies

- Schedule annual reviews to ensure policies remain aligned with business operations and accounting standards.

- Obtain approval from senior management or the finance committee.

-

Train Relevant Staff

- Ensure all accounting and finance personnel understand the depreciation policy and its application.

Best Practices for Documentation

- Maintain a formal written policy document that is accessible to all relevant personnel.

- Include step-by-step calculation examples for each depreciation method used.

- Keep a change log to track any modifications in policies, with reasons and approval signatures.

- Store supporting evidence such as manufacturer manuals, industry standards, and past asset performance data.

Example 1: Consistent Application of Straight-Line Depreciation

Scenario: A manufacturing company purchases a CNC machine costing $120,000 with an estimated useful life of 10 years and no residual value.

- Depreciation Expense per Year = $120,000 / 10 = $12,000

- Policy states straight-line method for machinery.

- Documentation includes:

- Policy excerpt specifying straight-line for machinery.

- Calculation worksheet showing annual depreciation.

- Asset register entry with purchase date, cost, useful life.

If the company later acquires a similar machine, the same method and useful life are applied, ensuring consistency.

Example 2: Documenting a Change in Useful Life

Scenario: After 5 years, the company reassesses the CNC machine’s useful life due to technological advances reducing expected usage to 8 years total.

- Remaining book value = $120,000 - (5 × $12,000) = $60,000

- Revised remaining life = 3 years

- New annual depreciation = $60,000 / 3 = $20,000

Documentation:

- Change log entry explaining the reassessment.

- Approval from finance controller.

- Updated depreciation schedule.

This example illustrates the importance of documenting changes to maintain transparency and audit readiness.

Summary

Consistency and documentation in depreciation policies are foundational to sound fixed asset accounting. They provide clarity, reduce errors, and ensure compliance. By standardizing methods, clearly defining parameters, and maintaining detailed records, accountants and financial controllers can enhance the accuracy and reliability of financial reporting.

4.5 Example: Calculating Depreciation for a Manufacturing Machine

Depreciation is a key concept in fixed asset accounting, representing the allocation of the cost of a tangible asset over its useful life. For manufacturing machines, accurate depreciation calculation ensures proper expense recognition and asset valuation.

Scenario:

A manufacturing company purchases a new machine for $120,000. The machine is expected to have a useful life of 10 years with a residual (salvage) value of $20,000 at the end of its life. The company wants to calculate depreciation expense using different methods.

Step 1: Understand the Key Variables

- Cost of Machine: $120,000

- Useful Life: 10 years

- Residual Value: $20,000

- Depreciable Amount: Cost - Residual Value = $120,000 - $20,000 = $100,000

Step 2: Depreciation Methods and Calculations

Straight-Line Depreciation

- Formula: (Cost - Residual Value) / Useful Life

- Calculation: $100,000 / 10 = $10,000 per year

Interpretation: The machine depreciates evenly by $10,000 every year.

Declining Balance Method (Double Declining)

- Formula: Book Value at Beginning of Year × (2 / Useful Life)

| Year | Beginning Book Value | Depreciation Expense | Ending Book Value |

|---|---|---|---|

| 1 | $120,000 | $120,000 × 20% = $24,000 | $96,000 |

| 2 | $96,000 | $96,000 × 20% = $19,200 | $76,800 |

| 3 | $76,800 | $76,800 × 20% = $15,360 | $61,440 |

| … | … | … | … |

Note: Depreciation continues until book value approaches residual value.

Units of Production Method

- Assumption: Machine expected to produce 100,000 units over its life.

- Formula: (Cost - Residual Value) / Total Estimated Units × Units Produced in Period

Example: If the machine produces 12,000 units in Year 1:

- Depreciation = ($100,000 / 100,000) × 12,000 = $12,000

Mind Map: Depreciation Calculation Overview

Mind Map: Straight-Line Depreciation Example

Mind Map: Declining Balance Depreciation Example

Mind Map: Units of Production Depreciation Example

Practical Tips / Best Practices:

- Choose the method that best matches asset usage: For machines with consistent usage, straight-line is simple and effective. For assets that lose value faster initially, declining balance is preferable.

- Document assumptions clearly: Useful life, residual value, and production estimates should be well supported.

- Review depreciation annually: Adjust estimates if asset usage or condition changes.

- Use software tools: Automate calculations to reduce errors and improve reporting.

Summary Table: Depreciation Expense Year 1

| Method | Depreciation Expense |

|---|---|

| Straight-Line | $10,000 |

| Declining Balance | $24,000 |

| Units of Production | $12,000 |

Each method impacts financial statements differently, affecting profit, tax, and asset book value. Accountants and financial controllers should select and apply the method that aligns with company policy and regulatory standards.

4.6 Impact of Depreciation on Financial Statements

Depreciation is a critical accounting process that systematically allocates the cost of a fixed asset over its useful life. Understanding its impact on financial statements is essential for accountants and financial controllers, especially in the manufacturing sector where fixed assets represent significant investments.

Key Financial Statements Affected by Depreciation

-

Income Statement

- Depreciation Expense reduces the reported net income.

- It is recorded as an operating expense.

-

Balance Sheet

- Accumulated Depreciation is a contra-asset account that reduces the gross fixed asset value.

- Net Book Value (Carrying Amount) = Cost of Asset - Accumulated Depreciation.

-

Cash Flow Statement

- Depreciation is a non-cash expense and added back in the operating activities section.

Mind Map: Impact of Depreciation on Financial Statements

Example 1: Depreciation Effect on Income Statement and Balance Sheet

Scenario: A manufacturing company purchases a machine for $100,000 with a useful life of 10 years and no salvage value. Using straight-line depreciation, the annual depreciation expense is $10,000.

| Year | Depreciation Expense | Accumulated Depreciation | Net Book Value |

|---|---|---|---|

| 1 | $10,000 | $10,000 | $90,000 |

| 2 | $10,000 | $20,000 | $80,000 |

Income Statement Impact:

- Each year, $10,000 is recorded as depreciation expense, reducing net income.

Balance Sheet Impact:

- The asset is shown at $100,000 less accumulated depreciation.

- After year 1, net book value is $90,000.

Cash Flow Statement Impact:

- Depreciation is added back to net income in operating activities since it is a non-cash charge.

Mind Map: Depreciation and Taxable Income

Example 2: Depreciation Impact on Taxable Income and Cash Flow

Scenario: Using the same machine, assume a corporate tax rate of 30%.

- Depreciation expense reduces taxable income by $10,000.

- Tax saving = $10,000 * 30% = $3,000.

Effect:

- The company pays $3,000 less in taxes annually due to depreciation.

- Although depreciation reduces net income, it does not reduce cash, improving cash flow.

Financial Ratios Affected by Depreciation

-

Profitability Ratios:

- Return on Assets (ROA) decreases as depreciation expense reduces net income.

-

Asset Turnover Ratios:

- Net book value decreases over time, potentially increasing asset turnover ratio.

-

Debt Covenants:

- Depreciation affects earnings and asset values, which may influence compliance with loan covenants.

Summary

Depreciation plays a pivotal role in reflecting the consumption of fixed assets over time. Its impact spans multiple financial statements, influencing reported profitability, asset values, tax liabilities, and cash flows. Properly accounting for depreciation ensures accurate financial reporting and aids in strategic decision-making for accountants and financial controllers in manufacturing and finance sectors.

5. Asset Revaluation and Impairment

5.1 Understanding Asset Revaluation: When and Why

Asset revaluation is a critical process in fixed asset accounting that involves adjusting the book value of an asset to reflect its current fair market value. This practice ensures that the financial statements present a true and fair view of the company’s asset base.

What is Asset Revaluation?

Asset revaluation is the periodic reassessment of the carrying amount of fixed assets to align with their current market value rather than historical cost. This adjustment can lead to an increase or decrease in the asset’s recorded value.

Why is Asset Revaluation Important?

- Reflects True Asset Value: Over time, asset values can fluctuate due to market conditions, wear and tear, or technological advancements. Revaluation ensures the balance sheet reflects these changes.

- Improves Financial Reporting Accuracy: Accurate asset values improve decision-making for management, investors, and creditors.

- Compliance with Accounting Standards: Some accounting frameworks (e.g., IFRS) allow or require revaluation under certain conditions.

- Tax Implications: Revaluation can impact depreciation expenses and tax liabilities.

When Should Asset Revaluation be Performed?

- Significant changes in market value are observed.

- At regular intervals as per company policy or accounting standards.

- Prior to major financial reporting events (e.g., IPO, mergers).

- When assets become obsolete or impaired.

Mind Map: Asset Revaluation Overview

Mind Map: Reasons for Asset Revaluation

Example 1: Revaluation of Manufacturing Equipment

A manufacturing company purchased a piece of machinery for $500,000 five years ago. Due to technological advancements and increased demand for similar equipment, the fair market value of this machinery has risen to $600,000.

Accounting Treatment:

- The asset’s carrying amount is increased by $100,000.

- This increase is credited to a revaluation surplus account under equity.

- Depreciation going forward will be based on the new value.

Best Practice:

- Obtain an independent professional valuation.

- Document the revaluation process and rationale.

Example 2: Revaluation Due to Impairment

A finance company owns office buildings recorded at $2 million. Due to a downturn in the real estate market, the fair value drops to $1.5 million.

Accounting Treatment:

- The asset’s carrying amount is decreased by $500,000.

- The loss is recognized in the profit and loss statement.

Best Practice:

- Conduct impairment tests regularly.

- Ensure transparency in financial disclosures.

Summary

Asset revaluation is a vital tool for maintaining accurate and compliant financial records. It helps accountants and financial controllers in the finance and manufacturing sectors to present a realistic picture of asset values, supporting better strategic decisions and regulatory adherence.

5.2 Accounting for Asset Impairment Losses

Understanding Asset Impairment

Asset impairment occurs when the carrying amount of a fixed asset exceeds its recoverable amount. This means the asset is no longer expected to generate sufficient future economic benefits to justify its book value.

Key Concepts:

- Carrying Amount: The value at which an asset is recognized on the balance sheet, net of accumulated depreciation.

- Recoverable Amount: The higher of an asset’s fair value less costs to sell and its value in use.