Financial Software Training for Accountants

1. Introduction to Financial Software

1.1 Understanding the Role of Financial Software in Modern Accounting

Financial software has revolutionized the accounting profession by automating routine tasks, improving accuracy, and providing real-time financial insights. For accountants, mastering these tools is essential to streamline workflows, ensure compliance, and support strategic decision-making.

What is Financial Software?

Financial software refers to computer programs designed to manage and process financial transactions, generate reports, and support accounting functions such as bookkeeping, payroll, budgeting, and auditing.

Why Financial Software is Critical in Modern Accounting

- Automation of Repetitive Tasks: Reduces manual data entry and human error.

- Real-Time Reporting: Enables timely financial analysis and decision-making.

- Regulatory Compliance: Helps maintain up-to-date tax codes and audit trails.

- Data Integration: Connects with other business systems for seamless workflows.

- Scalability: Supports growing business needs from small firms to large enterprises.

Mind Map: Core Roles of Financial Software in Accounting

Example: Automating Bank Reconciliation

Scenario: An accountant manually reconciles bank statements with company records, which takes hours and is prone to errors.

With Financial Software:

- The software imports bank transactions automatically.

- Matches transactions with recorded entries.

- Flags discrepancies for review.

Benefit: Saves time, reduces errors, and provides instant reconciliation reports.

Mind Map: Benefits of Financial Software for Accountants

Example: Real-Time Financial Reporting

Scenario: A CFO needs up-to-date financial reports to make quick investment decisions.

With Financial Software:

- Reports are generated instantly from live data.

- Custom dashboards highlight key performance indicators.

Benefit: Enables proactive management and better financial planning.

The Accountant’s Evolving Role with Financial Software

Financial software shifts accountants from data entry clerks to strategic advisors by:

- Allowing focus on analysis rather than manual tasks.

- Facilitating scenario planning and forecasting.

- Enhancing communication with stakeholders through clear reports.

Mind Map: Accountant’s Role Transformation

Summary

Understanding the role of financial software is foundational for accountants aiming to enhance productivity and add value. By automating routine tasks, ensuring compliance, and providing actionable insights, financial software empowers accountants to become key contributors to business success.

1.2 Overview of Popular Financial Software Tools (QuickBooks, Xero, SAP, Oracle Financials)

Financial software tools have revolutionized the way accountants manage financial data, streamline processes, and generate reports. Understanding the strengths and typical use cases of popular financial software is essential for accountants to select and utilize the right tool effectively.

QuickBooks

Overview: QuickBooks, developed by Intuit, is widely used by small to medium-sized businesses for its user-friendly interface and comprehensive accounting features.

Key Features:

- Invoicing and payments

- Expense tracking

- Payroll management

- Tax preparation

- Financial reporting

Best Practice Example: A freelance accountant managing multiple small business clients uses QuickBooks to automate invoicing and track expenses, reducing manual errors and saving time.

Mind Map:

Xero

Overview: Xero is a cloud-based accounting software popular for its real-time collaboration features and integration capabilities.

Key Features:

- Bank reconciliation

- Multi-currency support

- Inventory management

- Project tracking

- Mobile app access

Best Practice Example: An accounting team in a startup uses Xero to collaborate in real-time, enabling seamless updates and instant access to financial data from anywhere.

Mind Map:

SAP Financials

Overview: SAP Financials is part of the SAP ERP suite, designed for large enterprises requiring complex financial management and integration with other business processes.

Key Features:

- General ledger and accounts management

- Asset accounting

- Financial consolidation

- Compliance and risk management

- Advanced analytics

Best Practice Example: A multinational corporation uses SAP Financials to consolidate financial data across subsidiaries, ensuring compliance with international accounting standards.

Mind Map:

Oracle Financials

Overview: Oracle Financials is a comprehensive financial management solution within Oracle’s ERP Cloud, tailored for enterprises needing robust financial controls and automation.

Key Features:

- Accounts payable and receivable

- Cash management

- Expense management

- Financial reporting and analytics

- Compliance and audit support

Best Practice Example: A system administrator configures Oracle Financials to automate expense approvals and generate audit-ready reports, reducing manual workload and improving compliance.

Mind Map:

Summary Table

| Software | Target Users | Key Strengths | Example Use Case |

|---|---|---|---|

| QuickBooks | Small to Medium Biz | User-friendly, Invoicing | Freelance accountant automating invoicing |

| Xero | Small to Medium Biz | Real-time collaboration, Cloud | Startup team collaborating remotely |

| SAP Financials | Large Enterprises | Complex financial consolidation | Multinational consolidating subsidiaries |

| Oracle Financials | Large Enterprises | Automation, Compliance | Automating expense approvals and audit reporting |

Understanding these tools’ capabilities and ideal use cases helps accountants and system administrators make informed decisions about which software aligns best with their organizational needs and workflows.

1.3 Key Features and Functionalities Accountants Should Know

Financial software has become an indispensable tool for accountants, streamlining complex processes and enhancing accuracy. Understanding the key features and functionalities is essential for maximizing efficiency and ensuring compliance. Below, we explore these core features with easy-to-understand examples and mind maps to visualize their interconnections.

Core Features Overview

Chart of Accounts Management

The Chart of Accounts (CoA) is the backbone of any accounting system. It categorizes all financial transactions into accounts such as assets, liabilities, equity, income, and expenses.

Example:

- Setting up a CoA with categories like “Cash,” “Accounts Receivable,” “Sales Revenue,” and “Office Supplies Expense.”

- Ensuring each account has a unique code for easy identification.

Best Practice: Regularly review and update the CoA to reflect organizational changes, avoiding clutter and confusion.

Transaction Recording and Data Entry

Accurate and timely recording of transactions is critical. Financial software typically provides forms or templates to enter invoices, bills, payments, and receipts.

Example:

- Recording a client payment of $1,000 received via bank transfer.

- Entering a vendor invoice for office supplies worth $200.

Best Practice: Use validation rules and dropdown menus to minimize errors during data entry.

Bank Reconciliation

This feature allows accountants to match the company’s financial records with bank statements to identify discrepancies.

Example:

- Reconciling a bank statement showing a $500 deposit with the recorded sales income.

Best Practice: Perform bank reconciliations monthly to catch errors or fraudulent transactions early.

Financial Reporting

Generating reports such as Profit & Loss, Balance Sheet, and Cash Flow Statements is a fundamental function.

Example:

- Creating a monthly Profit & Loss report to review revenue and expenses.

Best Practice: Customize reports to focus on key performance indicators relevant to your business.

Automation of Recurring Transactions

Automating repetitive tasks such as monthly rent payments or subscription fees saves time and reduces errors.

Example:

- Setting up an automatic monthly journal entry for depreciation expense.

Best Practice: Review automated entries periodically to ensure accuracy.

Integration Capabilities

Modern financial software often integrates with payroll, CRM, ERP, and banking systems to provide a seamless workflow.

Example:

- Syncing payroll data directly into the accounting system to automate salary expense recording.

Best Practice: Test integrations thoroughly before going live to avoid data inconsistencies.

Security and User Permissions

Protecting sensitive financial data is paramount. Software allows setting role-based access controls.

Example:

- Restricting access to payroll data only to HR and senior accountants.

Best Practice: Regularly update user permissions and enforce strong password policies.

Summary

Understanding these key features empowers accountants to leverage financial software effectively. From managing the Chart of Accounts to automating recurring transactions and ensuring data security, mastering these functionalities leads to improved accuracy, compliance, and productivity.

By integrating these best practices and examples into daily workflows, accountants can transform their financial management processes and add greater value to their organizations.

1.4 Best Practices for Selecting the Right Financial Software: Case Study Examples

Selecting the right financial software is critical for accountants to streamline workflows, improve accuracy, and ensure compliance. This section explores best practices for making an informed choice, supported by real-world case studies and mind maps to visualize the decision-making process.

Best Practices for Selecting Financial Software

Define Your Business Needs

- Identify core accounting functions required (e.g., invoicing, payroll, tax management).

- Consider industry-specific requirements.

- Assess scalability for future growth.

Evaluate Software Features

- Compare features like automation, reporting capabilities, integration options.

- Prioritize user-friendly interfaces.

Consider Budget and Total Cost of Ownership

- Include licensing, implementation, training, and maintenance costs.

Check Vendor Reputation and Support

- Review customer feedback and support responsiveness.

Test with a Trial or Demo

- Hands-on testing to assess usability and fit.

Ensure Compliance and Security

- Verify software meets regulatory standards and has robust security.

Mind Map: Financial Software Selection Process

Case Study 1: Small Accounting Firm Choosing QuickBooks Online

Background: A small accounting firm with 10 employees needed software to manage client invoicing, payroll, and tax filing.

Approach:

- Defined needs: cloud access, multi-user support, payroll integration.

- Compared QuickBooks Online, Xero, and FreshBooks.

- Evaluated pricing plans and customer reviews.

- Conducted 30-day free trials.

Outcome:

- Selected QuickBooks Online for its comprehensive payroll features and ease of use.

- Resulted in 25% reduction in invoicing errors and improved client satisfaction.

Example Mind Map for this Case:

Case Study 2: Mid-Sized Finance Department Implementing SAP

Background: A mid-sized company with complex financial reporting and multi-currency transactions needed an enterprise-grade solution.

Approach:

- Mapped out detailed requirements including compliance with international accounting standards.

- Prioritized integration with existing ERP and CRM systems.

- Engaged vendor for a tailored demo.

Outcome:

- Chose SAP Financials for robust multi-currency support and integration capabilities.

- Training program reduced transition time by 40%.

Example Mind Map:

Practical Example: Comparing Features with a Decision Matrix

| Feature | QuickBooks Online | Xero | SAP Financials |

|---|---|---|---|

| Cloud-Based | Yes | Yes | Yes |

| Multi-Currency Support | Limited | Moderate | Extensive |

| Payroll Integration | Built-in | Add-on | Built-in |

| User Interface | Intuitive | User-friendly | Complex |

| Reporting | Basic to Advanced | Advanced | Enterprise-grade |

| Price Range | Low | Medium | High |

Using this matrix helps accountants weigh options based on their priorities.

Summary

Selecting the right financial software requires a structured approach:

- Clearly define needs

- Evaluate features and costs

- Test software hands-on

- Consider vendor support and compliance

Using mind maps and decision matrices can simplify complex decisions, while case studies provide practical insights into how others have successfully navigated the process.

1.5 Setting Up Your Financial Software Environment: Step-by-Step Guide

Setting up your financial software environment correctly from the start is crucial for ensuring smooth accounting operations, accurate data management, and efficient workflows. This section will guide you through the essential steps to configure your financial software, illustrated with mind maps and practical examples.

Step 1: Define Your Accounting Structure

Before diving into software setup, clearly outline your accounting structure, including your chart of accounts, departments, and reporting needs.

Example:

- For a small business, your chart of accounts might include basic categories like Cash, Accounts Receivable, Sales Revenue, and Office Supplies.

Step 2: Install and Configure the Software

- Download and install the latest version of your chosen financial software.

- Configure initial settings such as company name, fiscal year start/end dates, currency, and tax settings.

Example:

- Setting the fiscal year start date to January 1 and end date to December 31.

- Enabling VAT if your business operates in a VAT-registered country.

Step 3: Set Up Users and Permissions

Assign roles and permissions to team members to ensure data security and proper workflow.

Example:

- An accountant role with full access to data entry and report generation.

- An auditor role with view-only permissions.

Step 4: Customize the Chart of Accounts

Tailor the chart of accounts to match your business needs.

- Add, edit, or remove accounts.

- Group accounts logically for reporting.

Example:

- Adding a new account under Expenses for “Software Subscriptions”.

Step 5: Import or Enter Opening Balances

To ensure accurate financial reporting, input your opening balances.

- Import data from previous accounting systems or spreadsheets.

- Manually enter balances if starting fresh.

Example:

- Importing a CSV file containing the closing balances from last year.

Step 6: Configure Bank Feeds and Payment Gateways

Link your bank accounts and payment systems for automatic transaction imports.

Example:

- Connecting your checking account to automatically import daily transactions.

Step 7: Set Up Reporting Templates and Alerts

Customize reports and set alerts for important financial events.

Example:

- Setting an alert to notify the accountant when invoices are overdue by 30 days.

Step 8: Test the Setup with Sample Transactions

Before going live, enter sample transactions to verify that everything works as expected.

- Record a sample invoice.

- Process a payment.

- Generate reports.

Example:

- Creating a sample sales invoice for $1,000 and recording a payment against it.

Summary Mind Map

By following these steps, accountants can ensure their financial software environment is optimized for accuracy, security, and efficiency. Proper setup reduces errors, saves time, and lays the foundation for effective financial management.

2. Mastering Basic Financial Software Operations

2.1 Navigating the User Interface: Tips for Efficiency

Navigating the user interface (UI) of financial software efficiently is crucial for accountants to save time, reduce errors, and improve overall productivity. This section will guide you through best practices for mastering the UI, supported by clear examples and mind maps to visualize key concepts.

Understanding the Layout

Most financial software platforms follow a similar UI structure, typically including:

- Dashboard: Overview of key financial metrics and shortcuts.

- Navigation Menu: Access to modules like Invoices, Expenses, Reports, and Settings.

- Work Area: Where detailed data entry and report generation happen.

- Notifications/Alerts: Important updates or warnings.

Mind Map: Typical Financial Software UI Layout

Tip 1: Customize Your Dashboard for Quick Access

Most software allows customization of the dashboard. Prioritize widgets or shortcuts you use most frequently.

Example:

In QuickBooks, you can add widgets like “Unpaid Invoices” and “Bank Account Balances” to your dashboard. This reduces the need to navigate multiple menus.

Mind Map: Dashboard Customization

Tip 2: Use Keyboard Shortcuts to Speed Up Navigation

Learning keyboard shortcuts can drastically reduce the time spent clicking through menus.

Example:

In Xero, pressing Alt + N opens the “New Transaction” menu instantly.

| Software | Shortcut | Action |

|---|---|---|

| QuickBooks | Ctrl + I | Create Invoice |

| Xero | Alt + N | New Transaction |

| SAP | F8 | Execute Command |

Mind Map: Keyboard Shortcuts

Tip 3: Utilize Search and Filter Functions

When dealing with large datasets, use search bars and filters to locate transactions or reports quickly.

Example:

In Oracle Financials, the search bar allows filtering by invoice number, date, or vendor name. This avoids manual scrolling.

Mind Map: Search & Filter Usage

Tip 4: Familiarize Yourself with Module Groupings

Modules are often grouped logically (e.g., Payables, Receivables, Payroll). Knowing where to find each function reduces navigation time.

Example:

In SAP, Accounts Payable and Accounts Receivable are under the “Financial Accounting” module, while budgeting is under “Controlling.”

Mind Map: Module Groupings

Tip 5: Use Favorites or Bookmarks

Mark frequently used reports or screens as favorites for one-click access.

Example:

In Xero, you can star reports like “Monthly Profit & Loss” to appear in your favorites menu.

Mind Map: Favorites & Bookmarks

Practical Example: Efficient Workflow for Creating an Invoice

- Use the dashboard shortcut or keyboard shortcut (e.g., Ctrl + I in QuickBooks).

- Use auto-fill features to populate customer details.

- Apply filters to select the correct product or service.

- Save and send invoice directly from the work area.

This workflow minimizes clicks and leverages UI features for speed.

Summary

Efficient UI navigation in financial software involves understanding the layout, customizing dashboards, mastering keyboard shortcuts, using search and filters, knowing module groupings, and leveraging favorites. By adopting these best practices, accountants can significantly improve their daily productivity and accuracy.

For further practice, try mapping your own software’s UI using the mind maps above and identify shortcuts or customization options you can implement immediately.

2.2 Data Entry Best Practices: Avoiding Common Errors with Examples

Accurate data entry is the backbone of reliable financial reporting. Even minor mistakes can cascade into significant discrepancies, affecting decision-making and compliance. This section outlines best practices to minimize errors during data entry, supported by clear examples and mind maps to visualize key concepts.

Common Data Entry Errors in Financial Software

- Typographical Errors: Mistyping numbers or account codes.

- Incorrect Account Selection: Posting transactions to wrong accounts.

- Duplicate Entries: Entering the same transaction multiple times.

- Omission of Transactions: Forgetting to enter certain transactions.

- Incorrect Date Entry: Using wrong transaction dates.

Best Practices Mind Map

Double-Check Entries Immediately

Example:

An accountant enters an invoice amount as $1,250 instead of $12,500. By reviewing the entry against the original invoice before saving, the error is caught and corrected.

Tip: Use software features like confirmation prompts or review screens before finalizing entries.

Use Validation Rules and Input Masks

Many financial software tools allow setting validation rules to restrict input types or ranges.

Example:

- Setting a rule that invoice numbers must be alphanumeric and exactly 8 characters long.

- Restricting date fields to prevent future dates.

This reduces the chance of invalid data entry.

Standardize Data Entry Formats

Establishing consistent formats for dates, currency, and descriptions helps maintain uniformity.

Example:

- Always entering dates as YYYY-MM-DD.

- Using a consistent naming convention for vendors (e.g., “Acme Corp” instead of “Acme Corporation” or “Acme Co.”).

Use Templates and Recurring Entries for Repetitive Transactions

For transactions that occur regularly, templates save time and reduce errors.

Example:

- Setting up a recurring monthly rent payment entry.

- Using a purchase order template for similar supplier orders.

Cross-Check Entries Against Source Documents

Always verify data entered with original invoices, receipts, or bank statements.

Example:

Before finalizing payroll entries, compare the data with timesheets and contracts.

Avoid Duplicate Entries by Using Software Features

Many financial software solutions have built-in duplicate detection.

Example:

- QuickBooks alerts when an invoice with the same number is entered twice.

If your software lacks this, maintain a checklist or log of entered transactions.

Regularly Reconcile Accounts

Reconciliation helps identify discrepancies early.

Example:

Monthly bank reconciliation to match software entries with bank statements.

Mind Map: Error Prevention Workflow

Practical Example: Entering a Vendor Invoice

| Step | Action | Best Practice | Example |

|---|---|---|---|

| 1 | Receive invoice | Verify invoice details | Confirm invoice number, date, amount |

| 2 | Open financial software | Use vendor template | Select “Acme Corp” from standardized vendor list |

| 3 | Enter invoice data | Use validation rules | Date auto-formats to YYYY-MM-DD; amount field accepts only numbers |

| 4 | Review entry | Double-check amounts and accounts | Compare entry with invoice; confirm expense account is correct |

| 5 | Save and submit | Check for duplicate invoice numbers | Software alerts if invoice number already exists |

Summary

By implementing these data entry best practices, accountants can significantly reduce errors, improve data integrity, and streamline financial processes. Consistent use of validation, verification, and automation tools combined with regular training ensures high-quality financial data.

For further practice, consider creating your own mind maps based on your organization’s specific workflows and software capabilities to visualize and reinforce these best practices.

2.3 Managing Chart of Accounts: Practical Setup and Maintenance

Introduction

The Chart of Accounts (CoA) is the backbone of any accounting system. It organizes financial transactions into categories, making it easier for accountants to record, analyze, and report financial data accurately. Proper setup and ongoing maintenance of the CoA ensure clarity, consistency, and compliance.

What is a Chart of Accounts?

- A structured list of all accounts used in the general ledger.

- Categorizes assets, liabilities, equity, revenues, and expenses.

- Enables systematic recording and reporting.

Why Proper Management Matters

- Facilitates accurate financial reporting.

- Simplifies audit processes.

- Supports budgeting and forecasting.

- Enhances data integrity and reduces errors.

Practical Setup of Chart of Accounts

Step 1: Define Account Categories

- Assets

- Liabilities

- Equity

- Revenues

- Expenses

Step 2: Determine Account Numbering System

- Use a logical numbering scheme (e.g., 1000-1999 for Assets)

- Leave gaps for future accounts

Step 3: Create Account Names and Descriptions

- Use clear, descriptive names

- Include purpose or usage notes

Step 4: Customize Based on Business Needs

- Add sub-accounts for detailed tracking

- Align with industry standards

Step 5: Review and Approve

- Involve finance team and management

- Ensure compliance with accounting standards

Example: Sample Chart of Accounts Setup

| Account Number | Account Name | Description |

|---|---|---|

| 1000 | Cash | All cash accounts |

| 1100 | Accounts Receivable | Money owed by customers |

| 2000 | Accounts Payable | Money owed to suppliers |

| 3000 | Owner’s Equity | Owner’s investment and retained earnings |

| 4000 | Sales Revenue | Income from sales |

| 5000 | Cost of Goods Sold | Direct costs of producing goods |

| 6000 | Operating Expenses | Rent, utilities, salaries, etc. |

Mind Map: Chart of Accounts Setup

Maintenance of Chart of Accounts

Best Practices

- Regularly review accounts for relevance

- Archive or deactivate unused accounts

- Update account descriptions as needed

- Maintain consistency in naming conventions

- Document changes and approvals

Example Scenario: Adding a New Account

- Business expands to offer consulting services

- Need to track consulting revenue separately

- Steps:

- Identify appropriate category (Revenue)

- Assign new account number (e.g., 4100)

- Name it “Consulting Revenue”

- Update CoA and communicate changes

Mind Map: Chart of Accounts Maintenance

Common Pitfalls and How to Avoid Them

| Pitfall | Solution | Example |

|---|---|---|

| Overly complex CoA | Keep it simple and scalable | Avoid creating too many sub-accounts early |

| Inconsistent naming | Establish naming conventions | Use “Rent Expense” consistently, not “Office Rent” |

| No review process | Schedule regular audits | Quarterly CoA review meetings |

| Ignoring future growth | Leave numbering gaps | Number accounts in increments of 10 or 100 |

Summary

Managing the Chart of Accounts effectively is essential for accurate financial management. By following a structured setup process and maintaining it regularly, accountants can ensure their financial data is organized, reliable, and ready for reporting or audits.

Additional Resources

- QuickBooks Chart of Accounts Guide

- Xero Chart of Accounts Setup

- Best Practices for Chart of Accounts

2.4 Recording Transactions: Step-by-Step with Sample Entries

Recording transactions accurately is fundamental to maintaining reliable financial records. This section will guide you through the process of recording transactions in financial software, using clear steps and practical examples.

Step 1: Understand the Transaction Type

Before entering any data, identify the nature of the transaction. Common types include:

- Sales (Revenue)

- Purchases (Expenses)

- Payments

- Receipts

- Adjustments

Mind Map: Types of Transactions

Step 2: Gather Required Information

Ensure you have all necessary details:

- Date of transaction

- Amount

- Accounts involved (e.g., Cash, Accounts Receivable, Sales Revenue)

- Description or memo

- Supporting documents (invoices, receipts)

Step 3: Access the Transaction Entry Module

Log into your financial software and navigate to the module for entering transactions, such as “Create Invoice,” “Enter Bill,” or “Record Payment.”

Step 4: Enter Transaction Details

Input the gathered information carefully:

- Select the correct date

- Choose the appropriate accounts

- Enter the amount

- Add descriptions for clarity

Step 5: Review and Save

Double-check all entries for accuracy before saving. Many software platforms allow you to preview the transaction or run a trial balance to verify.

Example 1: Recording a Sales Invoice

Scenario: Your company sold consulting services worth $1,500 on March 15, 2024, to Client A, payment due in 30 days.

| Field | Entry |

|---|---|

| Date | 2024-03-15 |

| Customer | Client A |

| Account (Debit) | Accounts Receivable |

| Account (Credit) | Sales Revenue |

| Amount | $1,500 |

| Description | Consulting services |

Mind Map: Sales Invoice Entry

Example 2: Recording a Payment Received

Scenario: Client A pays the $1,500 invoice on April 10, 2024.

| Field | Entry |

|---|---|

| Date | 2024-04-10 |

| Customer | Client A |

| Account (Debit) | Cash/Bank |

| Account (Credit) | Accounts Receivable |

| Amount | $1,500 |

| Description | Payment for invoice |

Mind Map: Payment Received Entry

Example 3: Recording a Purchase Bill

Scenario: Your company receives a bill for office supplies worth $300 on March 20, 2024.

| Field | Entry |

|---|---|

| Date | 2024-03-20 |

| Vendor | Office Supplies Co. |

| Account (Debit) | Office Supplies Expense |

| Account (Credit) | Accounts Payable |

| Amount | $300 |

| Description | Office supplies purchase |

Mind Map: Purchase Bill Entry

Example 4: Recording a Payment Made

Scenario: You pay the $300 bill to Office Supplies Co. on April 5, 2024.

| Field | Entry |

|---|---|

| Date | 2024-04-05 |

| Vendor | Office Supplies Co. |

| Account (Debit) | Accounts Payable |

| Account (Credit) | Cash/Bank |

| Amount | $300 |

| Description | Payment for office supplies bill |

Mind Map: Payment Made Entry

Tips and Best Practices

- Always cross-check accounts: Ensure debits and credits balance.

- Use clear descriptions: This aids future audits and reviews.

- Attach supporting documents: Upload invoices or receipts when possible.

- Regularly reconcile accounts: Helps catch errors early.

- Leverage software templates: Many platforms offer templates to speed up entry.

By following these steps and using the examples provided, accountants can confidently record transactions in financial software, ensuring accuracy and compliance with accounting standards.

2.5 Generating Basic Financial Reports: Profit & Loss, Balance Sheet with Sample Data

Generating financial reports is a fundamental skill for accountants using financial software. These reports provide insights into the financial health of an organization and are essential for decision-making, compliance, and strategic planning. In this section, we’ll focus on two primary reports: the Profit & Loss (P&L) statement and the Balance Sheet. We’ll walk through best practices, sample data, and mind maps to help you understand and generate these reports effectively.

Understanding the Reports

Profit & Loss Statement (Income Statement)

- Shows revenues, expenses, and profits over a specific period.

- Helps assess operational performance.

Balance Sheet

- Snapshot of assets, liabilities, and equity at a specific point in time.

- Demonstrates financial position and stability.

Mind Map: Components of Profit & Loss Statement

Mind Map: Components of Balance Sheet

Sample Data for Report Generation

| Account | Type | Amount (USD) |

|---|---|---|

| Sales Revenue | Revenue | 150,000 |

| Service Income | Revenue | 30,000 |

| Cost of Goods Sold | Expense | 70,000 |

| Salaries Expense | Expense | 25,000 |

| Rent Expense | Expense | 10,000 |

| Utilities Expense | Expense | 5,000 |

| Depreciation Expense | Expense | 3,000 |

| Interest Expense | Expense | 2,000 |

| Cash | Current Asset | 40,000 |

| Accounts Receivable | Current Asset | 20,000 |

| Inventory | Current Asset | 15,000 |

| Property, Plant & Equip | Fixed Asset | 100,000 |

| Accumulated Depreciation | Contra Asset | (10,000) |

| Accounts Payable | Current Liability | 18,000 |

| Short-term Loans | Current Liability | 12,000 |

| Mortgage | Long-term Liability | 50,000 |

| Owner’s Equity | Equity | 90,000 |

| Retained Earnings | Equity | 45,000 |

Step-by-Step: Generating a Profit & Loss Statement

- Log into your financial software and navigate to the reporting module.

- Select the Profit & Loss report option.

- Set the reporting period (e.g., January 1 to December 31).

- Verify that all transactions are entered and categorized correctly.

- Run the report.

- Review the report output:

- Total Revenues = Sales Revenue + Service Income = $150,000 + $30,000 = $180,000

- Cost of Goods Sold = $70,000

- Gross Profit = $180,000 - $70,000 = $110,000

- Operating Expenses = Salaries + Rent + Utilities + Depreciation = $25,000 + $10,000 + $5,000 + $3,000 = $43,000

- Operating Profit = $110,000 - $43,000 = $67,000

- Interest Expense = $2,000

- Net Profit = $67,000 - $2,000 = $65,000

Example Output:

| Description | Amount (USD) |

|---|---|

| Revenues | 180,000 |

| Cost of Goods Sold | (70,000) |

| Gross Profit | 110,000 |

| Operating Expenses | (43,000) |

| Operating Profit | 67,000 |

| Interest Expense | (2,000) |

| Net Profit | 65,000 |

Step-by-Step: Generating a Balance Sheet

- Access the Balance Sheet report in your financial software.

- Choose the report date (e.g., December 31).

- Ensure all asset, liability, and equity accounts are up to date.

- Run the report.

- Analyze the report:

-

Assets:

- Current Assets = Cash + Accounts Receivable + Inventory = $40,000 + $20,000 + $15,000 = $75,000

- Fixed Assets = Property, Plant & Equipment - Accumulated Depreciation = $100,000 - $10,000 = $90,000

- Total Assets = $75,000 + $90,000 = $165,000

-

Liabilities:

- Current Liabilities = Accounts Payable + Short-term Loans = $18,000 + $12,000 = $30,000

- Long-term Liabilities = Mortgage = $50,000

- Total Liabilities = $30,000 + $50,000 = $80,000

-

Equity:

- Owner’s Equity + Retained Earnings = $90,000 + $45,000 = $135,000

-

Check: Assets ($165,000) = Liabilities ($80,000) + Equity ($135,000) = $215,000 (Mismatch indicates data entry or classification errors)

Note: In this example, the balance sheet does not balance, indicating a need to review data entries or classifications.

Example Output:

| Category | Amount (USD) |

|---|---|

| Assets | |

| - Current Assets | 75,000 |

| - Fixed Assets | 90,000 |

| Total Assets | 165,000 |

| Liabilities | |

| - Current Liabilities | 30,000 |

| - Long-term Liabilities | 50,000 |

| Total Liabilities | 80,000 |

| Equity | 135,000 |

| Total Liabilities + Equity | 215,000 |

Best Practices

- Regularly reconcile accounts to ensure data accuracy.

- Use consistent account classifications to avoid errors in reports.

- Review reports for anomalies such as imbalance in the balance sheet.

- Leverage software filters and customization to generate reports tailored to your needs.

- Export reports to Excel or PDF for sharing and further analysis.

Additional Example: Correcting the Balance Sheet

Suppose the Owner’s Equity was incorrectly entered as $90,000 instead of $50,000.

Recalculate:

- Equity = $50,000 + $45,000 = $95,000

- Liabilities + Equity = $80,000 + $95,000 = $175,000

Still not balanced with Assets ($165,000). Next, check for missing liabilities or assets or errors in accumulated depreciation.

Summary

Generating basic financial reports like the Profit & Loss statement and Balance Sheet is essential for accountants. Using financial software, you can automate much of this process, but understanding the underlying components and verifying data accuracy is critical. Practice with sample data, use mind maps to visualize report structures, and always review outputs carefully to ensure reliable financial reporting.

3. Advanced Financial Data Management

3.1 Automating Recurring Transactions: Best Practices and Use Cases

Automating recurring transactions is a critical feature in financial software that helps accountants save time, reduce errors, and maintain consistency in financial records. Recurring transactions include regular payments or receipts such as rent, subscriptions, loan repayments, and salary payments.

Why Automate Recurring Transactions?

- Time Efficiency: Automates repetitive data entry tasks.

- Accuracy: Reduces manual entry errors.

- Consistency: Ensures transactions are recorded on time.

- Improved Cash Flow Management: Helps forecast cash flow by scheduling payments.

Best Practices for Automating Recurring Transactions

-

Identify Recurring Transactions Clearly

- Review your chart of accounts to identify transactions that occur regularly.

- Examples: Monthly rent, utility bills, subscription fees.

-

Set Up Detailed Templates

- Include all necessary details: amount, frequency, payment method, accounts involved.

- Example: For a monthly rent payment of $2,000, set the amount fixed, frequency monthly, and specify the landlord’s account.

-

Use Descriptive Naming Conventions

- Name recurring transactions clearly for easy identification (e.g., “Monthly Office Rent - April 2024”).

-

Review and Update Regularly

- Periodically check recurring transactions for changes in amounts or frequency.

- Example: If a subscription fee increases, update the recurring transaction accordingly.

-

Set Notifications and Approvals

- Configure alerts for upcoming transactions to avoid surprises.

- Use approval workflows if your software supports it.

-

Test Before Full Implementation

- Run a few cycles in a test environment or with dummy data to ensure accuracy.

-

Maintain Audit Trails

- Ensure the software logs automated transactions for audit purposes.

Mind Map: Automating Recurring Transactions

Use Case Examples

Example 1: Monthly Rent Payment Automation

- Scenario: An accounting team manages office rent payments of $2,500 due on the 1st of every month.

- Setup:

- Create a recurring transaction template:

- Amount: $2,500

- Frequency: Monthly

- Due Date: 1st of each month

- Payee: Landlord

- Account: Rent Expense

- Create a recurring transaction template:

- Outcome: The software automatically records the rent expense and schedules payment, reducing manual entry.

Example 2: Subscription Fee Automation with Variable Amounts

- Scenario: A company pays a cloud service subscription that varies based on usage.

- Setup:

- Create a recurring transaction for the base fee.

- Manually adjust the variable portion each month before finalizing.

- Best Practice: Use automation for fixed parts and manual review for variable components.

Example 3: Salary Payments Automation

- Scenario: Payroll is processed bi-weekly for 50 employees.

- Setup:

- Integrate financial software with payroll system.

- Automate salary payments as recurring transactions linked to payroll runs.

- Benefit: Minimizes errors and ensures timely salary disbursement.

Tips for Implementation

- Leverage Software Features: Many financial software platforms offer built-in recurring transaction modules—explore these thoroughly.

- Documentation: Keep detailed documentation of all recurring transaction setups.

- Training: Ensure accounting staff are trained on how to create, modify, and monitor recurring transactions.

By following these best practices and leveraging automation features, accountants can significantly streamline their workflow, reduce errors, and maintain accurate financial records with minimal manual intervention.

3.2 Handling Multi-Currency Transactions: Practical Examples

Handling multi-currency transactions is a critical skill for accountants working with international clients, vendors, or subsidiaries. Financial software often provides built-in tools to manage currency conversions, exchange rate fluctuations, and reporting in multiple currencies. This section will guide you through best practices and practical examples to effectively handle multi-currency transactions.

Understanding Multi-Currency Transactions

Multi-currency transactions occur when a business deals with financial activities involving different currencies. This can include:

- Invoicing customers in foreign currencies

- Paying suppliers abroad

- Recording foreign currency loans or investments

- Consolidating financial statements from international branches

Key Concepts

- Base Currency: The primary currency in which your accounting books are maintained.

- Foreign Currency: Any currency other than the base currency.

- Exchange Rate: The rate at which one currency is converted to another.

- Realized Gain/Loss: Profit or loss from currency exchange differences on settled transactions.

- Unrealized Gain/Loss: Currency fluctuations on outstanding balances.

Best Practices for Handling Multi-Currency Transactions

- Always set a clear base currency for your accounting system.

- Use up-to-date and reliable exchange rates; many software tools integrate with live exchange rate feeds.

- Record the exchange rate used for each transaction.

- Regularly reconcile foreign currency accounts to capture gains or losses.

- Use software features to automate currency conversion and reporting.

Mind Map: Multi-Currency Transaction Workflow

Practical Example 1: Recording a Foreign Currency Invoice

Scenario: Your company, based in the US (base currency USD), issues an invoice to a client in Europe for €1,000. The exchange rate on the invoice date is 1 EUR = 1.10 USD.

Steps:

- Create a new invoice in your financial software.

- Select EUR as the invoice currency.

- Enter the invoice amount: €1,000.

- The software automatically converts this to USD using the exchange rate 1.10, showing $1,100.

- Record the invoice.

Best Practice: Document the exchange rate used and the date to ensure audit trail clarity.

Practical Example 2: Paying a Supplier in Foreign Currency with Exchange Rate Fluctuation

Scenario: You owe a supplier €500. On the payment date, the exchange rate has changed to 1 EUR = 1.15 USD.

Steps:

- Record the accounts payable at the original invoice rate (e.g., 1.10).

- When making the payment, enter the actual payment amount in EUR and the current exchange rate (1.15).

- The software calculates the payment in USD ($575).

- The difference between the original payable amount ($550) and the payment amount ($575) is recorded as a realized exchange loss of $25.

Best Practice: Regularly update exchange rates and reconcile foreign currency payables to capture gains/losses accurately.

Mind Map: Exchange Rate Impact on Transactions

Practical Example 3: Monthly Revaluation of Foreign Currency Balances

Scenario: Your company holds a foreign currency bank account with a balance of €10,000. At month-end, the exchange rate has changed from 1.10 to 1.12.

Steps:

- The software revalues the foreign currency balance at the new rate.

- Original USD value: €10,000 x 1.10 = $11,000.

- New USD value: €10,000 x 1.12 = $11,200.

- The $200 difference is recorded as an unrealized gain.

Best Practice: Perform regular revaluations to reflect true financial position and comply with accounting standards.

Tips for Accountants Using Financial Software for Multi-Currency

- Familiarize yourself with how your software handles exchange rates and currency conversions.

- Use software features like automated exchange rate updates to minimize manual errors.

- Always verify currency settings before entering transactions.

- Maintain documentation for all exchange rates used.

- Train your team on multi-currency processes to ensure consistency.

By mastering these practices and examples, accountants can confidently manage multi-currency transactions, ensuring accuracy, compliance, and insightful financial reporting.

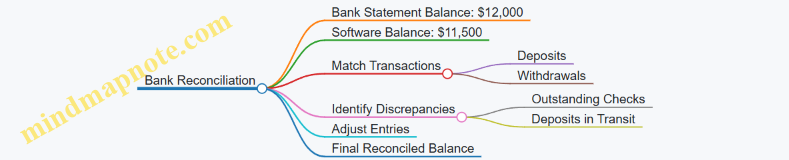

3.3 Bank Reconciliation Techniques: Stepwise Approach with Real-World Scenarios

Bank reconciliation is a critical process for accountants to ensure that the financial records in the accounting software match the bank statements. Accurate reconciliation helps identify discrepancies, prevent fraud, and maintain financial integrity.

Stepwise Approach to Bank Reconciliation

-

Gather Documents

- Collect the bank statement for the reconciliation period.

- Extract the corresponding ledger or accounting software report showing all recorded transactions.

-

Compare Opening Balances

- Verify that the opening balance on the bank statement matches the closing balance from the previous reconciliation.

-

Match Transactions

- Tick off transactions that appear both in the bank statement and accounting records.

- Identify unmatched transactions.

-

Identify Discrepancies

- Look for timing differences such as outstanding checks or deposits in transit.

- Detect errors like duplicate entries, missed transactions, or incorrect amounts.

-

Adjust Accounting Records

- Record bank fees, interest income, or direct debits not yet entered.

- Correct errors found in the accounting system.

-

Prepare Reconciliation Statement

- Summarize adjustments and reconcile the adjusted ledger balance with the bank statement balance.

-

Review and Approve

- Have a second person review the reconciliation for accuracy.

- File the reconciliation report for audit purposes.

Mind Map: Bank Reconciliation Process

Real-World Scenario Example 1: Outstanding Checks

Situation: A company issued a check for $1,200 on March 28, but the bank has not yet cleared it by March 31.

Accounting Records:

- Check recorded and deducted from the ledger.

Bank Statement:

- No record of the $1,200 check.

Action:

- Mark the $1,200 check as an outstanding check.

- Include it in the reconciliation statement as a deduction from the ledger balance.

Example Reconciliation Statement Snippet:

| Description | Amount ($) |

|---|---|

| Ledger Balance | 15,000 |

| Less: Outstanding Check | (1,200) |

| Adjusted Ledger Balance | 13,800 |

| Bank Statement Balance | 13,800 |

Real-World Scenario Example 2: Bank Fees Not Recorded

Situation: The bank statement shows a monthly service fee of $25 that was not recorded in the accounting software.

Accounting Records:

- No entry for bank fees.

Bank Statement:

- Service fee of $25 deducted.

Action:

- Record the $25 bank fee as an expense in the accounting software.

- Adjust the ledger balance accordingly.

Example Journal Entry:

| Account | Debit ($) | Credit ($) |

|---|---|---|

| Bank Fees Expense | 25 | |

| Bank Account | 25 |

Mind Map: Handling Discrepancies

Best Practices for Bank Reconciliation

- Perform Reconciliation Regularly: Monthly reconciliations reduce errors and improve accuracy.

- Use Software Automation: Many financial software tools offer bank feed integrations and automated matching.

- Maintain Clear Documentation: Keep reconciliation reports and supporting documents organized.

- Segregate Duties: Have different individuals prepare and review reconciliations to reduce fraud risk.

- Investigate Unusual Items Promptly: Address discrepancies as soon as they are identified.

Example: Using QuickBooks for Bank Reconciliation

- Import bank statements via bank feeds.

- QuickBooks automatically matches transactions.

- Review unmatched transactions and categorize them.

- Add missing bank fees or interest income.

- Generate reconciliation reports and save for audit.

By following this structured approach and leveraging real-world examples, accountants can master bank reconciliation techniques, ensuring financial data accuracy and compliance.

3.4 Managing Accounts Payable and Receivable Efficiently

Managing accounts payable (AP) and accounts receivable (AR) efficiently is critical for maintaining healthy cash flow and ensuring the financial stability of any organization. Financial software provides powerful tools to streamline these processes, reduce errors, and improve overall productivity.

Key Concepts in AP and AR Management

- Accounts Payable (AP): Money a company owes to suppliers or vendors for goods and services received.

- Accounts Receivable (AR): Money owed to a company by its customers for goods or services delivered.

Best Practices for Managing Accounts Payable

Automate Invoice Processing

- Use software features to automatically capture invoice data via OCR (Optical Character Recognition).

- Set up approval workflows to reduce manual bottlenecks.

Schedule Payments Strategically

- Prioritize payments based on due dates and early payment discounts.

- Avoid late fees by setting reminders and alerts.

Maintain Vendor Records Accurately

- Keep updated contact and payment terms for each vendor.

- Use software to track purchase orders and match them with invoices.

Regular Reconciliation

- Reconcile AP ledger with vendor statements monthly to catch discrepancies early.

Example: Automating Invoice Approval Workflow

A mid-sized company uses QuickBooks to automate invoice approvals. When an invoice is received, it is scanned and uploaded. The software routes it to the department head for approval. Once approved, the invoice is scheduled for payment on the due date, ensuring timely payment and avoiding late fees.

Best Practices for Managing Accounts Receivable

Invoice Promptly and Accurately

- Generate and send invoices immediately after delivery of goods or services.

- Use templates to ensure consistency.

Implement Clear Payment Terms

- Clearly state payment due dates, accepted payment methods, and penalties for late payments.

Use Automated Reminders

- Set up automatic email reminders for upcoming and overdue payments.

Monitor Aging Reports

- Regularly review AR aging reports to identify overdue accounts and take action.

Apply Cash Receipts Promptly

- Record payments as soon as they are received to maintain accurate records.

Example: Using AR Aging Reports to Improve Collections

An accounting team uses SAP Financials to generate weekly AR aging reports. They identify customers with invoices overdue by more than 30 days and prioritize follow-up calls. This proactive approach reduces outstanding receivables by 15% within 3 months.

Mind Maps

Mind Map 1: Accounts Payable Management

Mind Map 2: Accounts Receivable Management

Mind Map 3: Integrated AP & AR Efficiency Strategies

Practical Example: End-to-End AP and AR Workflow in Xero

- Invoice Receipt (AP): Vendor sends invoice, which is uploaded into Xero.

- Invoice Approval: Automated workflow routes invoice to finance manager.

- Payment Scheduling: Approved invoices are scheduled for payment before due date.

- Invoice Generation (AR): Upon delivery, customer invoice is generated and sent via email.

- Payment Tracking: Xero sends automatic reminders to customers.

- Cash Application: Payments received are recorded and matched against invoices.

- Reporting: Monthly AP and AR reports are generated for management review.

This integrated approach reduces manual errors, improves cash flow visibility, and enhances vendor and customer relationships.

Summary

Efficient management of accounts payable and receivable using financial software involves automation, accurate data entry, timely communication, and regular reporting. By adopting these best practices and leveraging software capabilities, accountants can significantly improve cash flow management and reduce operational risks.

3.5 Using Software to Track Budgets and Forecasts: Example Walkthrough

Tracking budgets and forecasts accurately is a critical task for accountants to ensure financial health and strategic planning. Modern financial software offers robust tools to create, monitor, and adjust budgets and forecasts dynamically. This section provides a detailed walkthrough with examples and mind maps to help you master these features.

Understanding Budgeting and Forecasting in Financial Software

Budgeting involves setting financial goals for a specific period, while forecasting predicts future financial outcomes based on historical data and assumptions. Financial software integrates these processes to provide real-time insights.

Mind Map: Key Components of Budgeting and Forecasting

Step-by-Step Example: Creating and Tracking a Budget in QuickBooks

- Set Budget Period: Choose the fiscal year or custom period.

- Select Accounts: Pick income and expense accounts relevant to the budget.

- Input Budget Amounts: Enter expected revenue and expenses for each account monthly.

- Save and Activate Budget: Confirm and enable the budget for tracking.

Example:

- Revenue Account: Sales

- January: $50,000

- February: $55,000

- Expense Account: Office Supplies

- January: $1,000

- February: $1,200

Mind Map: Budget Creation Workflow

Tracking Actuals vs Budget

Once the budget is set, the software automatically tracks actual transactions and compares them against the budgeted amounts.

Example:

- January Sales Actual: $48,000 (Budget: $50,000)

- January Office Supplies Actual: $1,100 (Budget: $1,000)

The software flags variances:

- Sales: -4% variance (under budget)

- Office Supplies: +10% variance (over budget)

Forecasting Example: Using Historical Data in Xero

- Import Historical Data: Load last 12 months of revenue and expenses.

- Set Assumptions: For example, sales growth of 5% per quarter.

- Generate Forecast: Software projects next 12 months based on assumptions.

- Adjust Scenarios: Create optimistic and pessimistic forecasts.

Example Forecast Table:

| Month | Forecasted Sales | Forecasted Expenses |

|---|---|---|

| March | $52,500 | $12,000 |

| April | $55,125 | $12,600 |

| May | $57,881 | $13,230 |

Mind Map: Forecasting Process

Best Practices for Budgeting and Forecasting in Financial Software

- Regular Updates: Keep budgets and forecasts updated with actual data.

- Use Alerts: Set notifications for significant variances.

- Scenario Planning: Prepare multiple forecasts for different business conditions.

- Collaborate: Involve relevant departments for accurate inputs.

- Leverage Dashboards: Use visual tools for quick insights.

Summary

Using financial software to track budgets and forecasts empowers accountants to maintain financial control and support strategic decisions. By following structured workflows and leveraging automation, accountants can reduce errors and improve accuracy.

For hands-on practice, try creating a sample budget in your preferred software using the steps above and analyze the actual vs budget reports after entering sample transactions.

4. Integrating Financial Software with Other Systems

4.1 Importance of Integration in Financial Workflows

Financial software integration plays a pivotal role in streamlining accounting processes and enhancing accuracy, efficiency, and decision-making. For accountants and system administrators working in finance and IT sectors, understanding the importance of integration is essential to optimize workflows and reduce manual errors.

What is Financial Software Integration?

Integration refers to the seamless connection of financial software with other business systems, such as payroll, CRM, ERP, inventory management, and banking platforms. This connectivity allows data to flow automatically between systems, eliminating the need for duplicate data entry and ensuring consistency.

Why Integration Matters in Financial Workflows

- Improved Data Accuracy: Automated data transfer reduces human errors caused by manual input.

- Time Efficiency: Saves time by minimizing repetitive tasks and accelerating processes like invoicing, reconciliation, and reporting.

- Real-Time Insights: Integrated systems provide up-to-date financial data, enabling timely decision-making.

- Regulatory Compliance: Ensures consistent and auditable data trails across systems.

- Cost Reduction: Reduces administrative overhead and potential penalties from errors or delays.

Mind Map: Benefits of Financial Software Integration

Common Integration Points in Financial Workflows

- Payroll Systems: Automatically sync employee salaries, taxes, and benefits with accounting ledgers.

- Customer Relationship Management (CRM): Link invoicing and payment status with customer accounts.

- Enterprise Resource Planning (ERP): Integrate inventory, procurement, and financial reporting.

- Banking Platforms: Enable automatic bank feeds for reconciliation.

- Tax Software: Streamline tax calculations and filings.

Example: Integration Between Accounting Software and Payroll System

Consider a mid-sized company using QuickBooks for accounting and ADP for payroll:

- Without integration, payroll data must be manually entered into QuickBooks, increasing the risk of errors.

- With integration, payroll expenses, tax withholdings, and benefits are automatically posted to the correct accounts in QuickBooks.

Benefits observed:

- Reduced payroll processing time by 40%

- Eliminated reconciliation discrepancies

- Improved accuracy in financial statements

Mind Map: Integration Points and Their Impact

Best Practices for Implementing Integration

- Assess Workflow Needs: Identify which systems require integration based on business processes.

- Choose Compatible Software: Ensure APIs or connectors are available.

- Test Thoroughly: Validate data accuracy and flow before going live.

- Train Staff: Provide training on integrated workflows to maximize benefits.

- Monitor and Maintain: Regularly review integrations for performance and update as needed.

Real-World Scenario: Avoiding Duplicate Data Entry

A financial team at a retail company struggled with duplicate data entry between their inventory system and accounting software. By integrating the two systems:

- Inventory sales automatically updated revenue accounts.

- Stock levels reflected in real-time, aiding purchasing decisions.

- Month-end closing was accelerated by 30%.

This example highlights how integration reduces manual workload and improves data reliability.

Summary

Integration in financial workflows is not just a technical enhancement but a strategic necessity. It empowers accountants and system administrators to deliver accurate, timely, and compliant financial information while optimizing operational efficiency.

By embracing integration best practices and leveraging real-world examples, finance professionals can transform their workflows and add significant value to their organizations.

4.2 Connecting Financial Software with Payroll Systems: Best Practices

Integrating financial software with payroll systems is crucial for ensuring seamless data flow, reducing manual errors, and maintaining compliance with tax and labor regulations. This section explores best practices for connecting these systems effectively, supported by clear examples and mind maps to visualize the process.

Why Integrate Financial Software with Payroll Systems?

- Accuracy: Automated data transfer reduces manual entry errors.

- Efficiency: Saves time by eliminating duplicate data entry.

- Compliance: Ensures payroll taxes and deductions are accurately reflected in financial reports.

- Real-time Reporting: Provides up-to-date financial and payroll data for decision-making.

Best Practices for Integration

Choose Compatible Systems

- Ensure your financial software and payroll system support integration either natively or via middleware.

- Example: QuickBooks Online integrates seamlessly with Gusto payroll.

Define Data Flow and Mapping

- Identify which data fields need to be synchronized (e.g., employee salaries, tax deductions, benefits).

- Map payroll data fields to corresponding financial software accounts.

Automate Data Transfer

- Use APIs or built-in connectors to automate data exchange.

- Schedule regular syncs to keep data current.

Maintain Data Security

- Use encrypted connections (e.g., HTTPS, VPN) for data transfer.

- Set role-based access controls to protect sensitive payroll information.

Test Thoroughly Before Going Live

- Run test transactions to verify data accuracy.

- Validate that payroll expenses and liabilities post correctly in financial reports.

Monitor and Audit Regularly

- Regularly review integration logs for errors.

- Reconcile payroll data with financial records monthly.

Mind Map: Connecting Financial Software with Payroll Systems

Example Scenario: Integrating QuickBooks with ADP Payroll

Step 1: Verify that QuickBooks supports integration with ADP via a third-party connector.

Step 2: Map payroll expense accounts in QuickBooks to match ADP payroll categories (e.g., wages, taxes, benefits).

Step 3: Configure the connector to automatically import payroll data after each payroll run.

Step 4: Run a test payroll cycle and verify that payroll expenses and liabilities are correctly posted in QuickBooks.

Step 5: Set up monthly reconciliation procedures to ensure ongoing accuracy.

Example: Manual Data Mapping Table

| Payroll System Field | Financial Software Account | Notes |

|---|---|---|

| Gross Pay | Salary Expense | Includes overtime and bonuses |

| Federal Tax Withheld | Payroll Tax Liability | To be remitted to tax authorities |

| Health Insurance | Employee Benefits Expense | Employer portion only |

Troubleshooting Tips

- Mismatch in Payroll Expenses: Check data mapping accuracy.

- Delayed Data Sync: Verify API credentials and scheduled sync settings.

- Security Alerts: Review access permissions and encryption protocols.

Summary

Connecting financial software with payroll systems streamlines accounting workflows and enhances accuracy. By following best practices such as choosing compatible systems, automating data transfer, and maintaining security, accountants can ensure reliable integration that supports compliance and efficient financial management.

4.3 Integrating with CRM and ERP Systems: Practical Examples

Integrating financial software with Customer Relationship Management (CRM) and Enterprise Resource Planning (ERP) systems is essential for streamlining workflows, improving data accuracy, and enabling real-time financial insights. This section explores practical examples and best practices for accountants to leverage these integrations effectively.

Why Integrate Financial Software with CRM and ERP?

- Unified Data Flow: Avoid duplicate data entry by syncing customer, sales, and financial data.

- Improved Accuracy: Reduce errors by automating data transfer between systems.

- Enhanced Reporting: Combine financial and operational data for comprehensive insights.

- Efficiency Gains: Automate invoicing, payment tracking, and order management.

Mind Map: Key Benefits of Integration

Common Integration Scenarios

-

CRM to Financial Software:

- Sync customer details, sales orders, and payment status.

- Example: Salesforce integrated with QuickBooks to automatically generate invoices when a deal is closed.

-

ERP to Financial Software:

- Transfer procurement, inventory, and payroll data.

- Example: SAP ERP feeding purchase orders and payroll expenses into Oracle Financials for consolidated accounting.

-

Bidirectional Sync:

- Updates in financial software reflect back in CRM/ERP.

- Example: Payment status updated in Xero triggers status change in HubSpot CRM.

Mind Map: Integration Workflow Example (CRM to Financial Software)

Practical Example 1: Salesforce and QuickBooks Integration

- Scenario: A mid-sized accounting firm uses Salesforce for managing client relationships and QuickBooks for bookkeeping.

- Integration Setup: Using a middleware like Zapier or a native connector, when a sales opportunity is marked “Closed Won” in Salesforce, an invoice is automatically created in QuickBooks.

- Benefits:

- Eliminates manual invoice creation.

- Ensures invoices are linked to correct clients.

- Payment status updates in QuickBooks reflect back in Salesforce, improving client communication.

Practical Example 2: SAP ERP and Oracle Financials Integration

- Scenario: A manufacturing company uses SAP ERP for inventory and procurement management and Oracle Financials for accounting.

- Integration Setup: Purchase orders and vendor payments created in SAP ERP are automatically posted to Oracle Financials.

- Benefits:

- Real-time visibility of procurement expenses.

- Simplifies month-end closing by having synchronized data.

- Reduces reconciliation time between systems.

Best Practices for Successful Integration

- Data Mapping: Clearly define how data fields correspond between systems to avoid mismatches.

- Regular Sync Schedule: Establish automated sync intervals (e.g., hourly, daily) based on business needs.

- Error Handling: Implement alerts for failed syncs or data conflicts.

- User Training: Ensure accountants understand how integrated data flows impact their workflows.

- Security: Maintain strict access controls and data encryption during data transfer.

Mind Map: Best Practices for Integration

Troubleshooting Common Integration Issues

- Duplicate Records: Ensure unique identifiers are used in both systems.

- Data Latency: Check sync frequency and network stability.

- Field Mismatches: Review data mapping and update as systems evolve.

- Permission Errors: Verify API credentials and user permissions.

By understanding and applying these practical examples and best practices, accountants can leverage CRM and ERP integrations to enhance financial accuracy, streamline processes, and provide more strategic insights to their organizations.

4.4 Data Import and Export: Ensuring Accuracy and Consistency

Efficient data import and export processes are critical for maintaining accuracy and consistency in financial software systems. Accountants often need to transfer large volumes of data between different platforms, such as importing bank statements, exporting reports for auditors, or integrating with other business systems. This section covers best practices, common pitfalls, and practical examples to help you master data import/export operations.

Why Data Import and Export Matter

- Ensures seamless data flow between systems

- Minimizes manual data entry errors

- Saves time and improves productivity

- Supports accurate financial reporting and compliance

Best Practices for Data Import and Export

Understand the Data Structure

Before importing or exporting, review the data format requirements (CSV, XLSX, XML, JSON) and field mappings.

Clean and Validate Data

Ensure data is free from duplicates, formatting errors, and missing values to avoid corrupting your financial records.

Use Templates and Sample Files

Many financial software tools provide import templates. Use these to format your data correctly.

Backup Data Before Importing

Always create a backup of your current data to prevent loss in case of import errors.

Test with Small Data Sets

Run test imports with a small subset of data to verify accuracy before full-scale import.

Automate Where Possible

Use scheduled exports/imports or APIs to reduce manual intervention and errors.

Mind Map: Key Steps in Data Import Process

Mind Map: Common Data Export Scenarios

Practical Example 1: Importing Bank Transactions into QuickBooks

Scenario: You receive a CSV file from your bank containing monthly transactions and need to import it into QuickBooks.

Steps:

- Review CSV Format: Ensure columns like Date, Description, Amount, and Transaction Type match QuickBooks import template.

- Clean Data: Remove any blank rows or irrelevant columns.

- Backup QuickBooks Data: Export a backup before import.

- Import Using QuickBooks Import Tool: Map CSV columns to QuickBooks fields.

- Review Imported Transactions: Check for duplicates or mismatches.

- Reconcile with Bank Statement: Ensure imported data matches your bank records.

Best Practice Tip: Use QuickBooks’ built-in bank feeds feature for automated imports to reduce manual errors.

Practical Example 2: Exporting Financial Reports for Audit

Scenario: Your auditor requests detailed transaction reports for the last fiscal year.

Steps:

- Select Report Type: Choose the detailed transaction report or general ledger export.

- Set Date Range: Define the fiscal year period.

- Export Format: Choose Excel or CSV for easy review.

- Verify Data Completeness: Cross-check totals with your financial statements.

- Secure Data: Encrypt or password-protect exported files if they contain sensitive information.

Best Practice Tip: Use standardized naming conventions for exported files to maintain organization.

Mind Map: Ensuring Data Accuracy and Consistency

Troubleshooting Common Issues

| Issue | Cause | Solution |

|---|---|---|

| Import fails with error | Incorrect file format or corrupted file | Use correct template; validate file integrity |

| Data mismatch after import | Field mapping errors | Double-check field mappings before import |

| Duplicate records | Importing same data multiple times | Use import options to skip duplicates or clean data beforehand |

| Missing data in export | Filters applied incorrectly | Review export filters and parameters |

Summary

Data import and export are vital processes that require careful preparation, validation, and testing to maintain the integrity of your financial data. By following best practices and leveraging software tools effectively, accountants can ensure smooth data transfers, reduce errors, and support accurate financial management.

4.5 Troubleshooting Common Integration Issues

Integrating financial software with other systems such as payroll, CRM, or ERP can significantly streamline workflows but often comes with challenges. This section covers common integration issues accountants and system administrators face, along with practical troubleshooting steps and examples.

Common Integration Issues

- Data Mismatch or Inconsistency

- Authentication and Access Errors

- API Limitations and Timeouts

- Incorrect Data Mapping

- Synchronization Failures

- Version Compatibility Problems

Mind Map: Troubleshooting Common Integration Issues

Data Mismatch or Inconsistency

Problem: Data imported from one system does not match the expected format or values in the financial software.

Example: Customer names appear differently in CRM and accounting software, causing duplicate entries.

Best Practice:

- Establish a standardized data format before integration.

- Use data validation tools to clean data prior to import.

- Create mapping tables that define how fields correspond between systems.

Example Scenario: A company integrates their CRM with their accounting software. The CRM stores customer names as “Last, First” while the accounting software expects “First Last.” Without proper mapping, the integration creates duplicate customer profiles.

Solution: Implement a data transformation step in the integration process that re-formats names to the expected standard.

Authentication and Access Errors

Problem: Integration fails due to invalid API keys, expired tokens, or insufficient permissions.

Example: Payroll system cannot push data to financial software because the API token expired.

Best Practice:

- Regularly update and securely store API credentials.

- Assign minimal necessary permissions to integration accounts.

- Monitor authentication logs for failures.

Example Scenario: An automated payroll sync stops working after a password change on the financial software account.

Solution: Update the stored credentials in the integration middleware immediately after password changes.

API Limitations and Timeouts

Problem: Integration requests fail due to API rate limits or timeouts, especially during large data transfers.

Example: Attempting to sync thousands of invoices at once causes the API to reject requests.

Best Practice:

- Batch data transfers into smaller chunks.

- Implement retry logic with exponential backoff.

- Monitor API usage dashboards.

Example Scenario: A month-end financial close requires syncing 10,000 transactions. The integration fails halfway due to API rate limits.

Solution: Modify the integration to send data in batches of 500 transactions with pauses between batches.

Incorrect Data Mapping

Problem: Fields from one system do not correctly correspond to fields in another, causing errors or misreported data.

Example: Expense categories in ERP do not match those in financial software, leading to misclassification.

Best Practice:

- Conduct thorough field mapping analysis before integration.

- Use middleware tools that allow flexible mapping configurations.

- Test mappings with sample data.

Example Scenario: An ERP system uses numeric codes for expense categories, but the accounting software expects descriptive text.

Solution: Create a mapping dictionary that translates numeric codes into descriptive category names during data transfer.

Synchronization Failures

Problem: Scheduled or manual syncs fail intermittently or completely.

Example: Daily sync between CRM and accounting software stops unexpectedly.

Best Practice:

- Set up alerting for failed sync jobs.

- Check logs regularly to identify failure points.

- Ensure network stability and sufficient system resources.

Example Scenario: A nightly sync fails due to a temporary network outage.

Solution: Implement retry mechanisms and notify administrators when failures occur.

Version Compatibility Problems

Problem: Software updates cause integrations to break due to deprecated APIs or changed data structures.

Example: After upgrading financial software, the integration middleware throws errors.

Best Practice:

- Review release notes before upgrading.

- Test integrations in a staging environment.

- Maintain communication with software vendors.

Example Scenario: An accounting software update changes the API endpoint URLs.

Solution: Update integration configurations to reflect new endpoints before going live.

Summary Mind Map: Integration Troubleshooting Workflow

By following these troubleshooting steps and best practices, accountants and system administrators can minimize downtime and ensure smooth integration between financial software and other critical business systems.

5. Compliance, Security, and Audit Preparedness

5.1 Ensuring Regulatory Compliance Through Software Features

Regulatory compliance is a critical aspect of financial accounting. Financial software plays a pivotal role in helping accountants adhere to laws, standards, and regulations such as GAAP, IFRS, SOX, and tax codes. Leveraging built-in compliance features not only reduces risk but also streamlines audit processes and ensures data integrity.

Key Compliance Features in Financial Software

Automated Tax Calculations

Best Practice: Use software that automatically calculates taxes based on jurisdiction and transaction type to avoid manual errors.