Treasury Management for Accountants

1. Introduction to Treasury Management

1.1 Understanding the Role of Treasury in Finance and Banking

Treasury management plays a pivotal role in the financial health and operational efficiency of organizations within the finance and banking sectors. It involves managing an organization’s liquidity, funding, risk, and financial investments to ensure stability and support strategic goals.

What is Treasury Management?

Treasury management refers to the process of overseeing an organization’s cash flow, investments, and financial risk. It ensures that the company has enough liquidity to meet its obligations while optimizing the use of its financial resources.

Key Functions of Treasury in Finance and Banking

- Cash Management: Monitoring and optimizing daily cash inflows and outflows to maintain liquidity.

- Risk Management: Identifying and mitigating financial risks such as currency fluctuations, interest rate changes, and credit risks.

- Funding and Capital Management: Securing appropriate funding sources and managing capital structure.

- Investment Management: Managing short-term and long-term investments to maximize returns within risk tolerance.

- Bank Relationship Management: Maintaining effective relationships with banks and financial institutions.

Mind Map: Core Responsibilities of Treasury

Why is Treasury Important in Finance and Banking?

Treasury acts as the nerve center for financial operations, ensuring that funds are available when needed and that risks are managed proactively. In banking, treasury functions also support regulatory compliance and capital adequacy requirements.

Example 1: Treasury’s Role in a Bank

A commercial bank’s treasury department manages the bank’s liquidity to ensure it can meet withdrawal demands, invests excess funds in safe instruments, and hedges interest rate risks to protect profitability. Accountants working closely with treasury help reconcile cash positions and ensure accurate financial reporting.

Example 2: Treasury in a Corporate Finance Team

In a corporate setting, treasury forecasts cash flow to avoid shortfalls, negotiates credit lines with banks, and invests surplus cash in low-risk instruments. Accountants provide historical financial data and assist in preparing cash flow statements that inform treasury decisions.

Mind Map: Interaction Between Treasury and Accounting

Best Practice: Collaboration Between Treasury and Accounting

Effective treasury management depends on timely and accurate financial information from accounting. Regular communication and integrated systems between these functions help in:

- Improving cash flow forecasting accuracy

- Enhancing risk management through better data

- Streamlining reporting and compliance

Example: Integrated Treasury and Accounting Workflow

A company implements an integrated ERP system where treasury and accounting share real-time data. This integration enables the treasury team to update cash forecasts daily based on actual receipts and payments recorded by accounting, reducing forecast errors by 20%.

In summary, understanding the role of treasury within finance and banking is crucial for accountants and treasury analysts alike. It ensures that financial resources are managed optimally, risks are mitigated, and organizational goals are supported through sound financial practices.

1.2 Key Responsibilities of Accountants in Treasury Management

Accountants play a pivotal role in treasury management by ensuring accurate financial data, compliance, and effective cash and risk management. Their responsibilities span from daily cash monitoring to strategic financial planning, bridging the gap between accounting and treasury functions.

Core Responsibilities

-

Cash Management and Forecasting

- Monitoring daily cash balances

- Preparing cash flow forecasts

- Ensuring liquidity for operational needs

-

Bank Reconciliation and Relationship Management

- Reconciling bank statements with ledger accounts

- Coordinating with banks for transactions and fee negotiations

-

Risk Management Support

- Assisting in identifying financial risks

- Supporting hedging activities with accurate accounting entries

-

Compliance and Controls

- Ensuring adherence to regulatory requirements

- Implementing internal controls to prevent fraud

-

Reporting and Analysis

- Preparing treasury-related financial reports

- Analyzing treasury performance metrics

-

Collaboration and Communication

- Acting as a liaison between treasury and other departments

- Supporting audit and regulatory reviews

Mind Map: Accountants’ Responsibilities in Treasury Management

Example 1: Cash Flow Forecasting

Scenario: An accountant at a manufacturing firm prepares a rolling 13-week cash flow forecast to ensure the company maintains sufficient liquidity.

Process:

- Collects data on expected receivables and payables.

- Incorporates seasonal sales trends.

- Updates forecast weekly to reflect actual cash movements.

Outcome: The company avoids overdrafts and optimizes short-term investments.

Example 2: Bank Reconciliation

Scenario: An accountant reconciles monthly bank statements with the general ledger.

Process:

- Identifies timing differences such as outstanding checks.

- Investigates discrepancies like unrecorded bank fees.

- Adjusts accounting records accordingly.

Outcome: Accurate cash balances are reported, supporting reliable treasury decisions.

Mind Map: Cash Flow Forecasting Process

Example 3: Supporting Hedging Activities

Scenario: The treasury team decides to hedge foreign currency exposure using forward contracts.

Accountant’s Role:

- Records the initial recognition of the forward contract.

- Monitors mark-to-market valuations.

- Ensures compliance with accounting standards (e.g., IFRS 9 or ASC 815).

Outcome: Accurate financial statements reflecting hedging effectiveness.

Mind Map: Compliance and Controls

Summary

Accountants in treasury management serve as the backbone for accurate financial data, risk mitigation, and regulatory compliance. Their proactive involvement in cash management, reconciliation, risk support, and reporting ensures the treasury function operates efficiently and aligns with the organization’s financial strategy.

1.3 Overview of Treasury Functions: Cash, Risk, and Investment Management

Treasury management is a critical function within any finance or banking organization, especially for accountants who play a pivotal role in ensuring financial stability and operational efficiency. The core treasury functions can be broadly categorized into three main areas: Cash Management, Risk Management, and Investment Management. Each of these functions interlinks to support the organization’s liquidity, safeguard assets, and optimize returns.

Mind Map: Treasury Functions Overview

Cash Management

Cash management involves the monitoring, analyzing, and optimizing of a company’s cash flows to ensure sufficient liquidity for day-to-day operations while minimizing idle cash.

Key Activities:

- Cash Flow Forecasting: Predicting inflows and outflows to avoid liquidity shortages.

- Liquidity Management: Maintaining an optimal cash balance to meet obligations without holding excessive idle cash.

- Payment Processing: Efficient handling of payments to vendors, employees, and other stakeholders.

Example: A retail company experiences seasonal spikes in sales during the holiday season. The treasury team, with input from accountants, prepares a rolling 13-week cash forecast that anticipates increased cash inflows from sales and schedules vendor payments accordingly to maintain liquidity.

Mind Map: Cash Management

Risk Management

Risk management in treasury focuses on identifying, measuring, and mitigating financial risks that can impact the company’s cash flows and financial position.

Types of Risks:

- Currency Risk: Exposure due to fluctuations in foreign exchange rates.

- Interest Rate Risk: Impact of changing interest rates on debt and investments.

- Credit Risk: Risk of counterparty default.

Best Practice: Developing a comprehensive risk management framework that includes policies for hedging and regular risk assessments.

Example: A multinational corporation has receivables in euros but reports in USD. To protect against adverse currency movements, the treasury team uses forward contracts to lock in exchange rates, ensuring predictable cash flows.

Mind Map: Risk Management

Investment Management

Investment management within treasury involves the strategic allocation of surplus cash into short-term, low-risk instruments to generate additional income without compromising liquidity.

Key Elements:

- Short-Term Investments: Instruments like treasury bills, commercial paper, and money market funds.

- Portfolio Diversification: Spreading investments to reduce risk.

- Yield Optimization: Balancing risk and return to maximize earnings.

Example: An accounting team collaborates with treasury to establish an investment policy that limits investments to high-quality, short-term instruments. They diversify the portfolio across government securities and highly rated commercial paper, achieving a steady yield while preserving capital.

Mind Map: Investment Management

Integrated Example: How These Functions Work Together

Consider a manufacturing firm with global operations:

- The cash management team forecasts cash needs for raw material purchases and payroll.

- The risk management team identifies exposure to currency fluctuations due to overseas suppliers and hedges accordingly.

- The investment management team invests excess cash from efficient cash flow management into short-term instruments to earn additional income.

Accountants play a crucial role by providing accurate financial data, ensuring compliance, and supporting treasury decisions with detailed reporting.

Summary

Understanding the interconnected treasury functions of cash, risk, and investment management equips accountants with the knowledge to support effective treasury operations. By integrating best practices and real-world examples, accountants can enhance liquidity management, mitigate financial risks, and optimize returns, ultimately contributing to the organization’s financial health.

1.4 Best Practice: Aligning Treasury Objectives with Corporate Financial Goals

Aligning treasury objectives with the broader corporate financial goals is fundamental for ensuring that treasury activities support the overall business strategy and enhance organizational value. For accountants involved in treasury management, this alignment helps in optimizing cash flow, managing risks effectively, and supporting strategic investments.

Why Alignment Matters

- Ensures treasury activities contribute directly to profitability and liquidity.

- Facilitates better decision-making by linking treasury metrics to corporate KPIs.

- Enhances communication between treasury, finance, and executive leadership.

Key Steps to Achieve Alignment

Detailed Explanation of Alignment Strategies

-

Regular Communication

- Establish frequent meetings between treasury and finance/accounting teams.

- Share updates on cash positions, risk exposures, and funding needs.

-

Integrated Planning

- Incorporate treasury forecasts into corporate budgeting and financial planning.

- Use rolling forecasts to adapt to changing business conditions.

-

Performance Metrics

- Define KPIs that reflect both treasury efficiency and corporate financial health (e.g., cash conversion cycle, cost of capital).

- Monitor and report these KPIs regularly to stakeholders.

-

Technology Integration

- Use integrated Treasury Management Systems (TMS) that connect with accounting software.

- Automate data sharing to reduce errors and improve timeliness.

Example 1: Aligning Cash Management with Profitability Goals

A manufacturing company sets a corporate goal to improve profitability by reducing working capital. The treasury team aligns by optimizing cash flow through tighter receivables collection and inventory management. Accountants support this by providing accurate aging reports and forecasting cash inflows.

Example 2: Risk Management Alignment with Corporate Stability

A financial services firm aims to stabilize earnings by minimizing foreign exchange risk. Treasury implements hedging strategies using forward contracts. Accountants ensure proper documentation and accounting treatment of these derivatives, aligning risk management with corporate financial reporting.

Practical Tips for Accountants

- Participate actively in treasury planning sessions to understand objectives.

- Develop reports that translate treasury data into corporate financial insights.

- Advocate for systems that integrate treasury and accounting data.

- Continuously update skills on treasury instruments and accounting standards.

By embedding treasury objectives within the framework of corporate financial goals, accountants can drive more cohesive financial management, reduce risks, and support sustainable growth.

1.5 Example: How a Mid-Sized Company Integrates Treasury and Accounting Teams

In many mid-sized companies, treasury and accounting functions often operate in silos, which can lead to inefficiencies, miscommunication, and suboptimal cash management. Integrating these teams can enhance collaboration, improve cash visibility, and streamline financial operations. Below is a detailed example illustrating how a mid-sized company successfully integrated its treasury and accounting teams.

Company Background

- Industry: Manufacturing

- Annual Revenue: $150 million

- Employees: 500

- Existing Situation: Treasury managed cash forecasting and bank relationships; accounting handled payments, reconciliations, and financial reporting separately.

Objectives of Integration

- Improve accuracy and timeliness of cash flow forecasts.

- Enhance communication between treasury and accounting.

- Reduce manual data entry and reconciliation errors.

- Align treasury activities with accounting periods and reporting.

Integration Approach

Step 1: Establishing Communication Channels

- Weekly Cross-Functional Meetings: Treasury and accounting teams meet every Monday to review cash positions, upcoming payments, and forecast updates.

- Shared Dashboards: Implemented a cloud-based dashboard accessible to both teams showing real-time cash balances, forecast variances, and payment schedules.

Step 2: Data Integration

- Unified ERP System: Both teams use the same ERP platform, ensuring that payment data, bank statements, and cash transactions are recorded and visible to both.

- Real-Time Data Access: Treasury can view accounting entries as they are posted, enabling more accurate and timely cash forecasting.

Step 3: Process Alignment

- Joint Cash Flow Forecasting: Treasury leads the forecast but incorporates input from accounting on expected receivables and payables.

- Coordinated Month-End Close: Treasury provides cash position data early to accounting to assist with accurate financial reporting.

Step 4: Defining Roles and Responsibilities

- Treasury focuses on liquidity management, bank relationships, and risk mitigation.

- Accounting handles payment processing, reconciliations, and statutory reporting.

- Clear boundaries reduce duplication and ensure accountability.

Step 5: Leveraging Technology

- Implemented a Treasury Management System (TMS) integrated with ERP.

- Automated daily cash position reports generated and shared with both teams.

Example Scenario: Cash Forecasting Collaboration

| Date | Accounting Input (Expected Payments) | Treasury Forecast Adjustment | Final Forecasted Cash Position |

|---|---|---|---|

| Week 1 | $2M outgoing payments | Adjusted for early collections | $5M available |

| Week 2 | $1.5M incoming receivables | Adjusted for delayed receivables | $3.8M available |

- Accounting provides detailed payment schedules.

- Treasury adjusts forecast based on market conditions and bank confirmations.

- Result: Forecast accuracy improved by 15% within first quarter.

Benefits Realized

- Improved Forecast Accuracy: Better visibility and collaboration reduced surprises.

- Faster Month-End Close: Coordinated processes shortened close by 2 days.

- Reduced Errors: Automated data sharing minimized manual entry mistakes.

- Enhanced Decision-Making: Real-time dashboards enabled proactive cash management.

Summary Mind Map

This example demonstrates that by fostering collaboration, aligning processes, and leveraging technology, mid-sized companies can effectively integrate treasury and accounting teams to achieve stronger financial control and operational efficiency.

2. Cash Management Fundamentals

2.1 Importance of Cash Flow Forecasting for Accountants

Cash flow forecasting is a critical component of treasury management that enables accountants to predict the inflows and outflows of cash over a specific period. Accurate cash flow forecasts help organizations maintain liquidity, optimize working capital, and avoid costly shortfalls or excesses.

Why Cash Flow Forecasting Matters for Accountants

- Liquidity Management: Ensures the company has enough cash to meet its obligations without holding excessive idle funds.

- Decision Making: Provides data-driven insights for investment, financing, and operational decisions.

- Risk Mitigation: Identifies potential cash shortages early, allowing proactive measures.

- Stakeholder Confidence: Builds trust with banks, investors, and management through transparent financial planning.

Mind Map: Key Benefits of Cash Flow Forecasting

Role of Accountants in Cash Flow Forecasting

Accountants play a pivotal role in gathering accurate financial data, analyzing historical trends, and collaborating with treasury teams to produce reliable forecasts. Their expertise in understanding the timing of receivables, payables, and other cash movements ensures the forecast reflects the true financial position.

Example 1: Monthly Cash Flow Forecast for a Retail Company

A retail company experiences seasonal sales peaks during the holiday season. The accountant prepares a monthly cash flow forecast by:

- Reviewing historical sales data from the last three years.

- Adjusting for expected increases in inventory purchases before the peak season.

- Factoring in payment terms with suppliers and customers.

This forecast helps the treasury team arrange short-term financing to cover increased inventory costs without disrupting operations.

Mind Map: Steps in Creating a Cash Flow Forecast

Example 2: Weekly Cash Flow Forecast for a Manufacturing Firm

A manufacturing firm with tight supplier payment schedules uses weekly cash flow forecasts to:

- Monitor daily cash positions.

- Schedule payments to suppliers to maximize available cash.

- Identify days when cash balances might dip below the minimum required.

The accountant integrates accounts receivable aging reports and upcoming payroll schedules to ensure accuracy.

Best Practices for Accountants in Cash Flow Forecasting

- Use Rolling Forecasts: Continuously update forecasts to reflect actual performance and new information.

- Collaborate Across Departments: Work closely with sales, procurement, and operations for timely data.

- Leverage Technology: Utilize treasury management systems or spreadsheet models for automation.

- Scenario Analysis: Prepare multiple forecasts based on different assumptions (e.g., best case, worst case).

Mind Map: Best Practices for Accountants

Summary

Cash flow forecasting is indispensable for accountants involved in treasury management. By mastering forecasting techniques and integrating best practices, accountants can significantly contribute to the financial health and strategic agility of their organizations.

2.2 Techniques for Accurate Cash Flow Projections

Accurate cash flow projections are essential for effective treasury management. They enable accountants and treasury analysts to anticipate liquidity needs, avoid shortfalls, and optimize the use of surplus cash. Below, we explore several proven techniques to improve the accuracy of cash flow forecasting, accompanied by mind maps and practical examples.

Key Techniques for Accurate Cash Flow Projections

Historical Data Analysis

Using historical cash flow data is the foundation of most projection techniques. By analyzing past inflows and outflows, accountants can identify recurring patterns and seasonal fluctuations.

Example: A retail company notices that cash inflows spike during November and December due to holiday sales. By analyzing the last three years of data, the treasury team adjusts the cash flow forecast to expect a 30% increase in cash receipts during these months.

Rolling Forecasts

A rolling forecast continuously updates the cash flow projection by adding a new period as the current period ends. This approach keeps the forecast horizon constant and incorporates the latest actual data.

Example: A manufacturing firm updates its cash flow forecast every week. When actual cash receipts from customers are received, the forecast for the upcoming weeks is adjusted accordingly, improving accuracy and responsiveness.

Scenario Analysis

Scenario analysis involves creating multiple cash flow projections based on different assumptions about future events. This helps in understanding the range of possible outcomes and preparing for uncertainties.

Example: An exporter projects cash flows under three scenarios:

- Base case: Stable currency exchange rates

- Best case: Favorable currency appreciation leading to higher cash inflows

- Worst case: Currency depreciation causing lower inflows

This enables the treasury to plan hedging strategies accordingly.

Collaboration with Departments

Cash flow depends on many operational factors. Collaborating with sales, procurement, and other departments ensures that forecasts reflect real-time business conditions.

Example: The treasury team holds monthly meetings with sales and accounts receivable teams to update expected customer payment dates, improving the timing accuracy of cash inflows.

Use of Technology

Modern Treasury Management Systems (TMS) and accounting software can automate data collection, reduce manual errors, and provide advanced analytics.

Example: A company integrates its ERP system with a TMS, enabling automatic extraction of invoice due dates and payment schedules. Predictive analytics then highlight potential cash shortfalls two weeks in advance.

Summary Mind Map

By applying these techniques in combination, accountants and treasury analysts can significantly enhance the accuracy of cash flow projections, enabling better liquidity management and strategic decision-making.

2.3 Best Practice: Implementing Rolling Cash Forecasts

What is a Rolling Cash Forecast?

A rolling cash forecast is a dynamic tool that continuously updates cash flow projections over a fixed future period, typically 13 weeks or 12 months. Unlike static forecasts, which are created once and become outdated, rolling forecasts are regularly refreshed (weekly or monthly) to reflect the latest financial data and business conditions.

Why Use Rolling Cash Forecasts?

- Improved Accuracy: Frequent updates reduce forecasting errors.

- Enhanced Liquidity Management: Enables proactive cash management decisions.

- Better Risk Mitigation: Early identification of potential cash shortfalls.

- Supports Strategic Planning: Aligns short-term cash needs with long-term goals.

Key Components of a Rolling Cash Forecast

Steps to Implement a Rolling Cash Forecast

- Define the Forecast Horizon: Decide on the period (e.g., 13 weeks) that balances detail with manageability.

- Collect Historical Data: Gather past cash inflows and outflows to identify patterns.

- Identify Key Drivers: Sales cycles, payment terms, seasonality, and other factors affecting cash.

- Build the Forecast Model: Use spreadsheets or treasury management systems to map inflows and outflows.

- Set Update Frequency: Typically weekly for short-term forecasts.

- Review and Adjust: Incorporate actual results and revise assumptions regularly.

Example: Rolling Cash Forecast for a Retail Company

A retail company uses a 13-week rolling cash forecast updated every Monday. Here’s how it works:

- Week 1: Forecast created using historical sales data, expected supplier payments, and payroll schedules.

- Week 2: Actual cash inflows from Week 1 are recorded; forecast for Week 14 is added.

- Adjustments: Unexpected supplier discounts or delayed customer payments are incorporated.

This process allows the treasury team and accountants to maintain a real-time view of cash availability, enabling timely decisions such as negotiating payment terms or arranging short-term financing.

Practical Tips for Accountants

- Automate Data Collection: Use accounting software integration to pull real-time data.

- Collaborate Across Departments: Engage sales, procurement, and operations for accurate inputs.

- Use Scenario Analysis: Model best-case, worst-case, and most-likely cash flow scenarios.

- Communicate Regularly: Share forecast updates with treasury and management teams.

Example: Scenario Analysis in Rolling Forecast

By incorporating scenario analysis, accountants can prepare the treasury for potential cash shortages or surpluses, ensuring the company remains financially agile.

Summary

Implementing rolling cash forecasts is a best practice that empowers accountants to provide timely, accurate cash flow insights. Through continuous updates, collaboration, and scenario planning, organizations can optimize liquidity management and support strategic financial decisions.

2.4 Example: Using Historical Data to Predict Seasonal Cash Flow Variations

Seasonal cash flow variations are common in many industries, where certain periods of the year experience predictable increases or decreases in cash inflows and outflows. For accountants involved in treasury management, leveraging historical data to forecast these variations is essential for maintaining liquidity and optimizing working capital.

Understanding Seasonal Cash Flow Patterns

Seasonality refers to periodic fluctuations in cash flow driven by factors such as holidays, weather, industry cycles, or customer behavior. Recognizing these patterns allows treasury teams to anticipate cash shortages or surpluses.

Step-by-Step Example: Predicting Seasonal Cash Flow Using Historical Data

-

Collect Historical Cash Flow Data

- Gather monthly cash inflows and outflows for the past 3-5 years.

- Ensure data is clean and categorized consistently.

-

Identify Seasonal Trends

- Analyze the data to detect recurring patterns.

- Use visualization tools like line charts or seasonal subseries plots.

-

Calculate Seasonal Indices

- Determine average cash flow for each month.

- Calculate the ratio of each month’s average to the overall average (seasonal index).

-

Adjust Forecasts Based on Seasonal Indices

- Apply seasonal indices to base cash flow forecasts to reflect expected variations.

-

Validate and Refine Forecasts

- Compare forecasts with actual cash flows periodically.

- Adjust seasonal indices as needed.

Mind Map: Seasonal Cash Flow Forecasting Process

Practical Example: Retail Company Cash Flow Seasonality

Scenario: A retail company experiences higher sales during November and December due to holiday shopping, resulting in increased cash inflows. Conversely, January and February see lower sales.

-

Historical Data Snapshot (Monthly Cash Inflows in $000s):

Month Year 1 Year 2 Year 3 Average January 500 520 480 500 February 480 470 490 480 March 600 620 610 610 … … … … … November 1200 1250 1300 1250 December 1500 1550 1600 1550 -

Overall Monthly Average: Sum all monthly averages and divide by 12.

-

Seasonal Index Calculation Example:

- Overall average = 900 (example value)

- November index = 1250 / 900 ≈ 1.39

- December index = 1550 / 900 ≈ 1.72

- January index = 500 / 900 ≈ 0.56

-

Applying Seasonal Indices: If the base forecast for November cash inflow next year is $1,000, applying the index:

- Adjusted forecast = 1,000 × 1.39 = $1,390

Mind Map: Retail Company Seasonal Cash Flow Example

Additional Best Practices

- Use Rolling Historical Periods: Update seasonal indices regularly to capture recent trends.

- Combine with Business Insights: Adjust forecasts for known events (e.g., new product launches).

- Leverage Software Tools: Utilize spreadsheet functions or treasury management systems for automation.

By systematically using historical data and seasonal indices, accountants can provide treasury teams with more accurate cash flow forecasts, enabling proactive liquidity management and strategic decision-making.

2.5 Managing Liquidity: Balancing Cash Reserves and Investment

Effective liquidity management is a cornerstone of treasury management, especially for accountants who need to ensure that the organization maintains sufficient cash to meet its short-term obligations while optimizing returns on excess cash through investments. Striking the right balance between cash reserves and investments safeguards the company’s operational stability and enhances financial performance.

Understanding Liquidity Management

Liquidity management involves maintaining an optimal level of cash and liquid assets that can be quickly converted to cash without significant loss of value. Too much cash sitting idle results in opportunity cost, while too little cash can lead to liquidity shortfalls and operational disruptions.

Key Components of Liquidity Management

Liquidity Management Mind Map

Best Practice: Establishing Liquidity Thresholds

Accountants should work with treasury teams to define minimum cash reserve levels based on:

- Average daily operating expenses (e.g., 30-60 days of expenses)

- Unexpected cash needs or emergencies

- Regulatory or contractual liquidity requirements

This threshold acts as a safety net, ensuring the company can cover liabilities without needing to liquidate investments prematurely.

Example: Calculating Cash Reserve Needs

A company has average monthly operating expenses of $900,000. The treasury team sets a liquidity threshold of 45 days of expenses.

- Daily operating expense = $900,000 / 30 = $30,000

- Cash reserve needed = $30,000 * 45 = $1,350,000

The company maintains at least $1.35 million in cash or highly liquid assets to meet short-term obligations.

Balancing Investments with Liquidity Needs

Once the cash reserve threshold is set, excess cash can be allocated to short-term investments that provide better returns while maintaining liquidity.

Investment Options for Treasury

- Money Market Funds: Highly liquid, low risk, moderate returns.

- Treasury Bills: Government-backed, short maturities, low risk.

- Certificates of Deposit (CDs): Fixed terms, slightly higher returns, but less liquid.

Mind Map: Investment Decision Factors

Example: Investment Allocation Strategy

A treasury team has $5 million in excess cash after maintaining liquidity reserves. They decide to allocate:

- $2 million in money market funds for immediate liquidity

- $2 million in 3-month Treasury bills for slightly higher yield

- $1 million in 6-month CDs to maximize returns with moderate liquidity

This diversified approach balances liquidity with return optimization.

Monitoring and Adjusting Liquidity

Continuous monitoring of cash flow forecasts and daily cash positions is essential. Accountants should collaborate with treasury analysts to:

- Update cash forecasts regularly to reflect changing business conditions

- Adjust investment allocations if liquidity needs increase or decrease

- Use automated treasury management systems to track liquidity metrics

Example: Responding to Unexpected Cash Outflows

If a company faces an unexpected large payment, such as a tax liability of $500,000, the treasury team can quickly liquidate money market funds or short-term Treasury bills without penalty to meet the obligation, preserving operational continuity.

Summary

Managing liquidity effectively requires accountants to:

- Understand and calculate appropriate cash reserve levels

- Collaborate on investment strategies that respect liquidity needs

- Monitor cash flows and adjust allocations dynamically

By balancing cash reserves and investments thoughtfully, companies can maintain financial stability while enhancing returns on idle cash.

2.6 Example: Daily Cash Position Reporting and Decision Making

Effective daily cash position reporting is a cornerstone of treasury management that empowers accountants and treasury analysts to make informed decisions about liquidity, funding, and investment opportunities. This section explores how to implement daily cash position reporting with practical examples and mind maps to visualize the process.

What is Daily Cash Position Reporting?

Daily cash position reporting involves tracking all cash inflows and outflows to determine the net cash available at the end of each business day. This report helps in assessing whether the company has sufficient liquidity to meet its obligations or if excess cash can be invested.

Key Components of Daily Cash Position Report

- Opening Cash Balance: Cash available at the start of the day.

- Cash Inflows: Collections from customers, loan proceeds, investment maturities.

- Cash Outflows: Payments to suppliers, payroll, loan repayments.

- Closing Cash Balance: Net cash available at the end of the day.

Mind Map: Daily Cash Position Reporting Workflow

Practical Example: Daily Cash Position Report

| Description | Amount (USD) |

|---|---|

| Opening Cash Balance | 1,200,000 |

| Cash Inflows | 500,000 |

| Cash Outflows | 650,000 |

| Closing Cash Balance | 1,050,000 |

Interpretation:

- The company started with $1.2 million.

- Collected $500,000 from customers.

- Paid $650,000 in expenses.

- Ending cash is $1.05 million, indicating a net cash outflow of $150,000 for the day.

Decision Making Based on Daily Cash Position

-

Liquidity Assessment:

- Is $1.05 million sufficient to cover upcoming payments?

- Check forecasted cash needs for the next 3 days.

-

Investment Opportunity:

- If surplus cash exceeds minimum thresholds, consider short-term investments.

-

Funding Needs:

- If cash falls below minimum operating levels, plan for short-term borrowing.

-

Adjust Forecasts:

- Update cash flow forecasts based on actual inflows/outflows.

Mind Map: Decision-Making Process from Daily Cash Report

Example Scenario: Using Daily Cash Position to Optimize Working Capital

A treasury analyst notices that the daily cash position consistently ends above $1 million, while the company’s minimum operating cash requirement is $800,000. The analyst recommends placing the excess $250,000 in a 30-day treasury bill to earn interest rather than leaving it idle in the operating account.

Outcome:

- Additional interest income generated.

- Improved cash utilization.

- Treasury and accounting teams collaborate to monitor maturity and reinvestment.

Tools and Automation Tips

- Use Treasury Management Systems (TMS) or ERP modules to automate data collection and report generation.

- Set up alerts for cash balances falling below thresholds.

- Integrate bank feeds for real-time cash position updates.

Summary

Daily cash position reporting is a vital practice that enables accountants and treasury analysts to maintain liquidity control, optimize cash usage, and support strategic financial decisions. By combining structured reporting with clear decision-making frameworks, organizations can enhance their treasury effectiveness and financial stability.

3. Bank Relationship Management

3.1 Understanding Banking Products Relevant to Treasury

Treasury management relies heavily on a variety of banking products designed to optimize liquidity, manage risk, and streamline payments. For accountants working closely with treasury teams, understanding these products is essential to ensure effective cash management and financial control.

Key Banking Products in Treasury Management

Detailed Overview and Examples

1. Cash Management Accounts

-

Operating Accounts: These are the primary accounts used for daily transactions. They provide liquidity and are essential for managing payables and receivables.

Example: A company maintains an operating account with its bank to handle payroll disbursements and supplier payments. The accountant reconciles this account daily to ensure accuracy.

-

Sweep Accounts: These accounts automatically transfer excess funds into higher-yield investment accounts overnight, maximizing interest earnings.

Example: At the end of each business day, any balance above $100,000 in the operating account is swept into a money market account, earning better interest.

-

Zero Balance Accounts (ZBA): These accounts maintain a zero balance by automatically transferring funds from a master account to cover disbursements.

Example: A company uses ZBAs for its regional offices. When an office issues a payment, funds are automatically transferred from the central master account, simplifying cash control.

2. Payment Services

-

Wire Transfers: Fast, secure electronic transfers used for large or urgent payments.

Example: An accountant initiates a wire transfer to pay an overseas supplier, ensuring the payment clears within 24 hours.

-

Automated Clearing House (ACH): Batch processing of payments, typically used for payroll or vendor payments.

Example: Payroll is processed via ACH, enabling the company to pay hundreds of employees efficiently.

-

Lockbox Services: Banks collect and process incoming payments on behalf of the company, accelerating cash inflows.

Example: Customer checks are sent directly to the bank’s lockbox, where they are processed and deposited, reducing the company’s collection time.

-

Remote Deposit Capture: Allows businesses to scan and deposit checks electronically without visiting the bank.

Example: The accounting team scans received checks daily and deposits them remotely, speeding up cash availability.

3. Credit Facilities

-

Revolving Credit Lines: Flexible borrowing options to manage short-term liquidity needs.

Example: During seasonal slowdowns, the company draws on its revolving credit line to cover operating expenses.

-

Term Loans: Fixed amount loans with scheduled repayments, often used for capital expenditures.

Example: The company finances new equipment with a 5-year term loan.

-

Overdraft Protection: Allows accounts to temporarily go negative to avoid payment failures.

Example: An unexpected large payment triggers overdraft protection, preventing bounced checks.

4. Investment Products

-

Money Market Accounts: Low-risk, highly liquid accounts offering better interest than operating accounts.

Example: Surplus cash is parked in a money market account to earn interest while remaining accessible.

-

Certificates of Deposit (CDs): Fixed-term deposits with higher interest rates but limited liquidity.

Example: The treasury invests $500,000 in a 6-month CD to earn higher returns on idle cash.

-

Treasury Bills and Bonds: Government securities used for safe, longer-term investments.

Example: To diversify investments, the company purchases 1-year Treasury bills.

5. Foreign Exchange Services

-

Spot Contracts: Immediate currency exchange at current rates.

Example: Paying an international supplier in euros using a spot contract to lock in the exchange rate.

-

Forward Contracts: Agreements to exchange currency at a future date at a predetermined rate, hedging against currency fluctuations.

Example: The company enters a forward contract to pay a supplier in 3 months, protecting against adverse currency movements.

-

Currency Options: Contracts giving the right, but not obligation, to exchange currency at a set rate.

Example: The treasury buys a currency option to hedge potential currency risk while retaining flexibility.

6. Risk Management Tools

-

Interest Rate Swaps: Agreements to exchange fixed and floating interest payments to manage interest rate exposure.

Example: The company swaps a floating rate loan for a fixed rate to stabilize interest expenses.

-

Hedging Instruments: Various derivatives used to mitigate financial risks.

Example: Using options and futures to hedge commodity price risk impacting cash flow.

Mind Map Summary

Treasury Banking Products Mind Map

Conclusion

For accountants supporting treasury functions, a solid grasp of these banking products enables better collaboration, improved cash flow management, and enhanced financial risk mitigation. By integrating these products strategically, companies can optimize liquidity, reduce costs, and safeguard financial stability.

3.2 Best Practice: Negotiating Bank Fees and Services

Negotiating bank fees and services is a critical skill for accountants involved in treasury management. Effective negotiation can significantly reduce costs and improve the quality of banking services, directly impacting the company’s bottom line.

Why Negotiating Bank Fees Matters

- Banks charge fees for various services: account maintenance, wire transfers, overdrafts, cash handling, foreign exchange, and more.

- These fees can add up to substantial amounts, especially for companies with high transaction volumes.

- Negotiating better terms helps optimize treasury costs and frees up cash for other strategic uses.

Key Steps in Negotiating Bank Fees and Services

Detailed Breakdown

-

Preparation

- Research: Analyze your current bank fees and compare them with other banks’ offerings. Use industry benchmarks to understand what is reasonable.

- Usage Analysis: Gather data on your transaction volumes, types of services used, and frequency. This information strengthens your negotiating position.

-

Negotiation Strategy

- Prioritize Needs: Identify which services are essential and which fees are negotiable.

- Bundle Services: Banks often offer discounts if you consolidate multiple services with them.

- Leverage Competition: Use offers from other banks as leverage to negotiate better terms.

-

Communication

- Approach negotiations as a partnership rather than a confrontation.

- Clearly communicate your company’s needs and growth plans.

- Build a strong relationship with your bank representative.

-

Follow-up

- After negotiation, review the new fee schedule carefully.

- Monitor bank statements regularly to ensure fees are applied correctly.

- Schedule periodic reviews to renegotiate as your business evolves.

Example 1: Reducing Wire Transfer Fees

A mid-sized manufacturing company noticed wire transfer fees were eating into their treasury budget. The accountant prepared a detailed report showing monthly wire volumes and compared fees from three competing banks. During negotiation, they:

- Highlighted their consistent transaction volume.

- Requested a volume discount on wire fees.

- Bundled wire transfers with cash management services.

Result: The bank agreed to reduce wire transfer fees by 25% and waived monthly account maintenance fees, saving the company $15,000 annually.

Example 2: Negotiating Foreign Exchange Fees

An exporter frequently dealt with foreign currency transactions. The treasury accountant:

- Analyzed FX transaction costs.

- Negotiated a tiered fee structure based on transaction size.

- Requested preferential rates for high-volume months.

Result: The company secured a 0.1% reduction in FX fees, which translated into $30,000 in annual savings.

Mind Map: Negotiation Tactics

Tips for Accountants

- Keep detailed records of all banking fees and services.

- Regularly benchmark fees against market standards.

- Engage with multiple banks to maintain competitive tension.

- Involve treasury and finance leadership in negotiations.

- Use technology tools to track and analyze banking costs.

By mastering the art of negotiating bank fees and services, accountants can significantly enhance treasury efficiency and contribute to the financial health of their organizations.

3.3 Example: Comparing Bank Fee Structures to Optimize Costs

When managing treasury functions, one critical aspect accountants and treasury analysts must focus on is understanding and optimizing bank fee structures. Different banks offer varying fee schedules depending on services, transaction volumes, and account types. By comparing these fees carefully, organizations can significantly reduce banking costs and improve overall treasury efficiency.

Understanding Common Bank Fees

Before diving into comparison, it’s important to recognize typical bank fees that impact treasury management:

- Account Maintenance Fees: Monthly or annual charges for maintaining accounts.

- Transaction Fees: Charges per transaction, such as wire transfers, ACH payments, or check processing.

- Cash Handling Fees: Fees for deposits or withdrawals of cash.

- Overdraft Fees: Charges for overdrawing accounts.

- Foreign Exchange Fees: Costs related to currency conversion.

- Service Fees: Charges for additional services like positive pay, fraud protection, or treasury management systems.

Mind Map: Bank Fee Components

Step-by-Step Example: Comparing Fees Across Three Banks

| Fee Type | Bank A | Bank B | Bank C |

|---|---|---|---|

| Monthly Maintenance | $50 | $30 | $40 |

| Wire Transfer (Domestic) | $20 per transfer | $15 per transfer | $25 per transfer |

| ACH Payment | $0.10 per item | $0.15 per item | $0.05 per item |

| Check Processing | $0.50 per check | $0.40 per check | $0.60 per check |

| Cash Deposit Fees | $0 (up to $100k) | $0 (up to $50k) | $0 (up to $75k) |

| Overdraft Fee | $35 per occurrence | $30 per occurrence | $40 per occurrence |

Scenario:

A company processes the following monthly transactions:

- 10 wire transfers

- 1,000 ACH payments

- 500 checks

- Cash deposits totaling $80,000

- No overdrafts

Calculations:

-

Bank A:

- Maintenance: $50

- Wire Transfers: 10 x $20 = $200

- ACH Payments: 1,000 x $0.10 = $100

- Checks: 500 x $0.50 = $250

- Cash Deposit: $0 (within free limit)

- Total: $50 + $200 + $100 + $250 + $0 = $600

-

Bank B:

- Maintenance: $30

- Wire Transfers: 10 x $15 = $150

- ACH Payments: 1,000 x $0.15 = $150

- Checks: 500 x $0.40 = $200

- Cash Deposit: $0 (within free limit)

- Total: $30 + $150 + $150 + $200 + $0 = $530

-

Bank C:

- Maintenance: $40

- Wire Transfers: 10 x $25 = $250

- ACH Payments: 1,000 x $0.05 = $50

- Checks: 500 x $0.60 = $300

- Cash Deposit: $0 (within free limit)

- Total: $40 + $250 + $50 + $300 + $0 = $640

Analysis:

- Bank B offers the lowest total monthly fees ($530) despite higher ACH fees because of lower maintenance and wire transfer fees.

- Bank A is the most expensive overall ($600), mainly due to higher wire transfer and check fees.

- Bank C has the cheapest ACH fees but higher wire transfer and check fees, resulting in the highest total cost ($640).

Mind Map: Decision Factors for Bank Selection

Best Practice Tips:

- Regularly Review Fee Structures: Banks may update fees annually; schedule reviews to ensure continued cost optimization.

- Negotiate Fees: Use volume data to negotiate discounts or fee waivers.

- Consolidate Transactions: Group payments or deposits to reduce transaction counts and fees.

- Leverage Technology: Use treasury management systems to monitor fees in real-time.

Real-World Example:

A treasury analyst at a manufacturing firm noticed that wire transfer fees were a significant cost driver. By analyzing transaction patterns and comparing fee structures, they negotiated with their primary bank to reduce wire fees by 25% in exchange for committing to a minimum monthly transaction volume. This negotiation saved the company approximately $15,000 annually.

By systematically comparing bank fee structures and understanding transaction profiles, accountants and treasury analysts can make informed decisions that optimize banking costs and enhance treasury efficiency.

3.4 Managing Multiple Banking Relationships Efficiently

Managing multiple banking relationships is a critical aspect of treasury management that allows organizations to optimize liquidity, reduce risk, and negotiate better terms. For accountants and treasury analysts, understanding how to efficiently coordinate and leverage these relationships can lead to improved cash management and cost savings.

Why Manage Multiple Banking Relationships?

- Diversification of Risk: Avoid dependency on a single bank to mitigate operational or credit risk.

- Access to Varied Services: Different banks may offer specialized products or better rates.

- Negotiation Leverage: Multiple relationships create competitive pressure for better fees and services.

- Geographical Reach: Global companies benefit from local banking expertise.

Best Practices for Managing Multiple Banking Relationships

Centralize Cash Management

Centralizing cash management across multiple banks allows accountants to have a consolidated view of cash positions, improving forecasting accuracy and liquidity management.

Example: A multinational corporation uses a Treasury Management System (TMS) that aggregates real-time balances from five different banks. This enables the treasury team to identify surplus cash in one bank and initiate interbank transfers to cover shortfalls elsewhere, reducing the need for external borrowing.

Standardize Banking Processes

Standardizing payment formats, approval workflows, and reporting templates across banks reduces complexity and errors.

Example: An accounting team implements a uniform payment approval process for all banks, using a centralized payment factory model. This ensures consistent controls and faster processing times regardless of the banking partner.

Regular Performance and Fee Reviews

Conduct quarterly reviews of banking fees, service levels, and transaction volumes to identify cost-saving opportunities.

Example: A treasury analyst compares monthly bank statements and notices one bank charges higher wire transfer fees. After renegotiation, the bank agrees to a reduced fee tier based on volume commitments.

Maintain Strong Communication and Relationship Management

Assign dedicated relationship managers and schedule regular meetings to discuss service improvements and upcoming needs.

Example: The treasury team holds bi-annual meetings with each bank’s relationship manager to review service quality, discuss new product offerings, and plan for upcoming cash flow changes.

Leverage Technology for Integration and Automation

Integrate bank accounts into treasury platforms to automate reconciliations, cash positioning, and reporting.

Example: An accounting department uses APIs to connect their ERP system with multiple banks, enabling automatic retrieval of bank statements and reconciliation, reducing manual effort by 70%.

Risk Management Across Banks

Spread transactional and credit risk by diversifying banking partners and monitoring exposure.

Example: A treasury analyst monitors daily transaction limits and credit exposure per bank, ensuring no single bank holds excessive risk or liquidity concentration.

Summary Table: Managing Multiple Banking Relationships

| Practice | Description | Example |

|---|---|---|

| Centralize Cash Management | Consolidate cash visibility and control | Use TMS for real-time balances across 5 banks |

| Standardize Processes | Uniform payment and reporting workflows | Centralized payment factory model |

| Performance & Fee Reviews | Regularly analyze fees and negotiate | Reduced wire transfer fees after quarterly review |

| Relationship Management | Maintain communication with bank contacts | Bi-annual meetings with relationship managers |

| Technology Integration | Automate reconciliations and reporting | API connections for automatic bank statement retrieval |

| Risk Management | Diversify and monitor bank exposure | Daily transaction limit monitoring |

By adopting these best practices, accountants and treasury analysts can efficiently manage multiple banking relationships, optimize cash flow, reduce costs, and mitigate risks, ultimately contributing to stronger treasury performance and corporate financial health.

3.5 Example: Streamlining Payment Processes Across Banks

Managing payments efficiently across multiple banking partners is a critical aspect of treasury management for accountants. Streamlining these processes reduces operational risk, improves cash flow visibility, and cuts transaction costs.

Why Streamline Payment Processes?

- Reduce manual errors: Automating and standardizing payment workflows minimizes human mistakes.

- Improve reconciliation: Centralized data helps reconcile payments faster.

- Enhance cash visibility: Consolidated payment schedules improve forecasting accuracy.

- Optimize banking fees: Efficient routing can reduce transaction charges.

Mind Map: Key Components of Streamlined Payment Processes

Practical Example: Implementing a Centralized Payment Hub

Scenario: A multinational company uses three different banks for its treasury operations. Each bank has a separate payment portal, leading to duplicated efforts, delayed payments, and difficulty in tracking payment statuses.

Solution: The treasury team implements a centralized payment hub integrated with their ERP and accounting systems.

Steps Taken:

- Integration: Connect the ERP system with the centralized payment platform that supports multiple bank APIs.

- Standardization: Adopt ISO 20022 payment formats to ensure compatibility.

- Automation: Set up automated workflows for payment approvals based on payment size and vendor.

- Scheduling: Use batch processing to group payments by due dates and priority.

- Monitoring: Real-time dashboards track payment status across all banks.

- Reconciliation: Automated matching of payments with invoices reduces manual reconciliation time by 60%.

Outcome:

- Payment processing time reduced from 3 days to same-day execution.

- Errors in payment instructions dropped by 80%.

- Treasury staff freed up to focus on strategic tasks rather than manual payment entry.

Mind Map: Benefits Realized from Streamlining Payments

Additional Example: Payment Routing to Optimize Fees

Context: The company notices that some banks charge higher fees for international wire transfers.

Action: Using the centralized payment platform, the treasury team configures payment routing rules:

- Domestic payments go through Bank A with the lowest domestic fees.

- International payments under $50,000 route through Bank B with competitive fees.

- Larger international payments route through Bank C, which offers better exchange rates.

Result: This routing strategy reduces overall payment fees by 15% annually.

Summary

Streamlining payment processes across multiple banks involves centralizing payment operations, standardizing formats, automating workflows, and optimizing payment routing. For accountants in treasury roles, adopting these best practices leads to improved efficiency, cost savings, and enhanced control over cash flows.

By leveraging technology and thoughtful process design, treasury teams can transform payment management from a manual, error-prone task into a strategic function that supports broader financial goals.

4. Treasury Risk Management

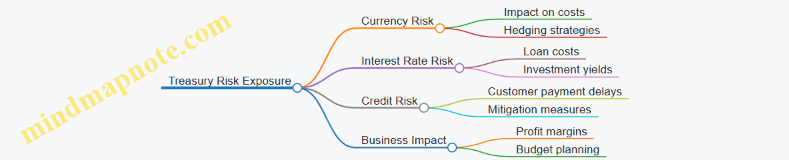

4.1 Identifying Financial Risks: Currency, Interest Rate, and Credit Risk

Effective treasury management begins with a clear understanding of the financial risks that can impact an organization’s liquidity, profitability, and overall financial health. For accountants involved in treasury functions, identifying and categorizing these risks is crucial for implementing appropriate mitigation strategies.

Overview of Key Financial Risks

-

Currency Risk (Foreign Exchange Risk)

- Arises from fluctuations in exchange rates when dealing with multiple currencies.

- Impacts companies with international operations, imports/exports, or foreign investments.

-

Interest Rate Risk

- The risk that changes in interest rates will affect the cost of borrowing or the return on investments.

- Important for companies with variable-rate debt or interest-sensitive assets.

-

Credit Risk

- The risk of loss due to a counterparty’s failure to meet its financial obligations.

- Common in lending, trade receivables, and investment in debt instruments.

Mind Map: Financial Risks in Treasury Management

Currency Risk Explained

Currency risk can be broken down into three types:

- Transaction Exposure: Risk from actual foreign currency transactions (e.g., paying suppliers or receiving payments in foreign currency).

- Translation Exposure: Risk from converting foreign subsidiaries’ financial statements into the parent company’s currency.

- Economic Exposure: Long-term impact of currency fluctuations on market value and competitive position.

Example:

A US-based company imports raw materials from Europe and agrees to pay €1 million in 90 days. If the euro strengthens against the dollar during this period, the company will need more dollars to fulfill the payment, increasing costs.

Best Practice:

Accountants should track currency exposures regularly and collaborate with treasury to use hedging instruments like forward contracts or options to lock in exchange rates.

Mind Map: Currency Risk Breakdown

Interest Rate Risk Explained

Interest rate risk affects both borrowing costs and investment returns. It can be categorized as:

- Repricing Risk: The risk that interest rates change when debt instruments mature or are reset.

- Basis Risk: When different interest rate indices move differently (e.g., LIBOR vs Treasury rates).

- Yield Curve Risk: Changes in the shape or slope of the yield curve affecting long-term vs short-term rates.

Example:

A company has a $10 million loan with a variable interest rate tied to LIBOR. If LIBOR rises by 1%, the company’s interest expense increases by $100,000 annually, impacting profitability.

Best Practice:

Accountants should maintain detailed schedules of debt maturities and interest rate terms, enabling treasury to consider swaps or fixed-rate borrowings to mitigate risk.

Mind Map: Interest Rate Risk Components

Credit Risk Explained

Credit risk arises when counterparties fail to fulfill their financial commitments. It includes:

- Counterparty Default: Failure to pay loans, invoices, or settle trades.

- Credit Rating Changes: Downgrades that increase borrowing costs or reduce asset values.

- Concentration Risk: Overexposure to a single counterparty or sector.

Example:

A company extends $500,000 in trade credit to a customer who later files for bankruptcy, resulting in a direct loss.

Best Practice:

Accountants should monitor aging receivables, assess counterparty creditworthiness, and work with treasury to set credit limits and provisions for doubtful debts.

Mind Map: Credit Risk Elements

Summary

For accountants supporting treasury management, identifying currency, interest rate, and credit risks involves:

- Regularly reviewing financial transactions and exposures.

- Collaborating with treasury to implement risk mitigation strategies.

- Using clear reporting and forecasting to highlight risk areas.

By understanding these risks and their practical implications, accountants can contribute significantly to safeguarding the company’s financial stability.

Additional Example: Integrated Risk Identification

A multinational firm’s accountant notices that a large portion of accounts receivable is denominated in a foreign currency with volatile exchange rates, while the company also has significant variable-rate debt. By mapping these exposures, the accountant helps treasury prioritize hedging currency risk and consider fixing interest rates to reduce overall financial risk.

4.2 Best Practice: Developing a Risk Management Framework

Developing a robust risk management framework is essential for treasury teams and accountants to systematically identify, assess, and mitigate financial risks. A well-structured framework ensures that risks such as currency fluctuations, interest rate volatility, and credit exposures are managed proactively, minimizing potential negative impacts on the organization.

Key Components of a Treasury Risk Management Framework

Step-by-Step Guide to Developing the Framework

-

Risk Identification:

- Collaborate with treasury, accounting, and finance teams to list all potential financial risks.

- Example: An accountant identifies foreign currency exposure due to international sales.

-

Risk Assessment:

- Quantify risks using metrics such as Value at Risk (VaR), sensitivity analysis, or scenario testing.

- Define the organization’s risk appetite to understand acceptable risk levels.

- Example: Calculate potential loss if exchange rates move 5% against the company’s position.

-

Risk Mitigation:

- Develop hedging strategies like forwards, options, or swaps.

- Set internal limits on exposures and require approvals for exceptions.

- Example: Use forward contracts to lock in exchange rates for upcoming foreign currency receivables.

-

Monitoring & Reporting:

- Implement systems to track risk exposures continuously.

- Generate regular reports for management and auditors.

- Example: Monthly risk dashboard showing currency exposure and hedging effectiveness.

-

Governance & Policies:

- Establish clear policies outlining risk management procedures.

- Define roles and responsibilities for treasury and accounting staff.

- Example: Treasury manager responsible for executing hedges; accountant responsible for reconciling hedge accounting entries.

Mind Map: Risk Identification and Assessment

Example: Implementing a Currency Risk Management Process

Scenario: A company has significant sales in Euros but reports in USD. The accountant notices that without hedging, a 10% depreciation of the Euro could reduce revenue by $500,000.

Action:

- The treasury team uses forward contracts to lock in exchange rates for the next quarter.

- The accountant records the hedge accounting entries to reflect the forward contracts in financial statements.

- Monthly reports track the effectiveness of the hedge, comparing actual vs. forecasted cash flows.

Outcome: The company stabilizes its revenue in USD terms, reducing earnings volatility.

Mind Map: Risk Mitigation Strategies

Final Tips for Accountants

- Collaborate closely with treasury to understand risk exposures and mitigation tools.

- Ensure accurate and timely recording of hedge transactions to maintain compliance.

- Use technology and analytics to improve risk visibility and reporting.

- Regularly review and update the risk management framework to adapt to changing market conditions.

By embedding these best practices into your treasury risk management framework, accountants can play a pivotal role in safeguarding the organization’s financial health.

4.3 Example: Hedging Currency Risk Using Forward Contracts

Currency risk, also known as foreign exchange (FX) risk, arises when a company has receivables or payables denominated in a foreign currency. Fluctuations in exchange rates can impact the value of these cash flows, potentially causing financial losses. Forward contracts are a common and effective tool used by treasury teams and accountants to hedge against this risk.

What is a Forward Contract?

A forward contract is a customized agreement between two parties to buy or sell a specific amount of foreign currency at a predetermined exchange rate on a future date. This locks in the exchange rate and eliminates uncertainty.

Mind Map: Understanding Forward Contracts for Currency Hedging

Example Scenario

Company Background:

- A US-based company expects to receive €1,000,000 from a European customer in 3 months.

- The current EUR/USD exchange rate is 1.10 (meaning 1 EUR = 1.10 USD).

- The company is concerned that the euro might depreciate against the dollar, reducing the USD value of the receivable.

Risk: If the EUR/USD rate drops to 1.05 in 3 months, the company would receive only $1,050,000 instead of $1,100,000.

Hedging Strategy:

- The company enters into a forward contract to sell €1,000,000 at the current forward rate of 1.10 USD/EUR in 3 months.

Mind Map: Hedging Process Using Forward Contracts

Step-by-Step Walkthrough

-

Exposure Identification: The accountant identifies the €1,000,000 receivable due in 3 months.

-

Risk Assessment: The treasury team evaluates FX market trends and decides to hedge to avoid downside risk.

-

Forward Contract Execution: The company enters into a forward contract with its bank to sell €1,000,000 at 1.10 USD/EUR in 3 months.

-

Outcome Scenarios:

| Scenario | Spot Rate in 3 Months | USD Amount Without Hedge | USD Amount With Hedge | Result |

|---|---|---|---|---|

| Euro depreciates to 1.05 | 1.05 | $1,050,000 | $1,100,000 | Hedge protects from loss |

| Euro appreciates to 1.15 | 1.15 | $1,150,000 | $1,100,000 | Hedge misses out on gain |

- Accounting Treatment: The forward contract is recorded as a derivative instrument. Gains or losses on the contract are recognized in the financial statements, offsetting the FX impact on the receivable.

Additional Example: Partial Hedging

Sometimes, companies choose to hedge only a portion of their exposure to balance risk and opportunity.

- If the company hedges only 50% (€500,000) of the receivable at 1.10 USD/EUR forward rate:

- If the euro depreciates to 1.05, the company receives:

- Hedged portion: €500,000 * 1.10 = $550,000

- Unhedged portion: €500,000 * 1.05 = $525,000

- Total: $1,075,000 (better than fully unhedged $1,050,000 but less than fully hedged $1,100,000)

- If the euro depreciates to 1.05, the company receives:

Mind Map: Partial Hedging Considerations

Key Best Practices for Accountants and Treasury Analysts

- Early Identification: Track foreign currency exposures as soon as contracts are signed.

- Collaboration: Work closely with treasury to align hedging strategies with accounting policies.

- Documentation: Maintain clear records of forward contracts and rationale for hedging.

- Regular Review: Monitor FX market and hedge effectiveness periodically.

- Accounting Compliance: Ensure hedge accounting rules (e.g., IFRS 9 or ASC 815) are properly applied.

By understanding and applying forward contracts effectively, accountants and treasury analysts can help their organizations mitigate currency risk, stabilize cash flows, and improve financial predictability.

4.4 Role of Accountants in Monitoring and Reporting Treasury Risks

Treasury risks encompass various financial uncertainties that can impact an organization’s liquidity, profitability, and overall financial health. Accountants play a critical role in monitoring these risks and ensuring transparent, accurate reporting to support effective decision-making.

Key Responsibilities of Accountants in Treasury Risk Monitoring

- Data Collection & Validation: Gathering accurate financial data related to cash flows, foreign exchange exposures, interest rates, and credit positions.

- Risk Identification: Collaborating with treasury teams to identify potential risks such as currency fluctuations, interest rate changes, and counterparty credit risks.

- Risk Quantification: Using accounting data to measure the magnitude and potential impact of identified risks.

- Internal Controls: Ensuring controls are in place to mitigate risks, including segregation of duties and authorization protocols.

- Reporting & Communication: Preparing timely reports that clearly communicate risk exposures and mitigation strategies to management and stakeholders.

Mind Map: Accountants’ Role in Treasury Risk Monitoring

Example 1: Monitoring Currency Risk Exposure

A multinational company has significant receivables in EUR but reports in USD. Accountants track the outstanding EUR invoices and calculate the potential impact of exchange rate fluctuations on the USD value. They prepare monthly reports showing exposure levels and collaborate with treasury to decide on hedging strategies.

Mind Map: Currency Risk Monitoring Process

Example 2: Interest Rate Risk Reporting

Accountants analyze the company’s debt portfolio, distinguishing between fixed and floating rate loans. They calculate the sensitivity of interest expenses to rate changes and prepare scenario analyses. These insights are included in treasury risk reports to inform interest rate swap decisions.

Mind Map: Interest Rate Risk Reporting

Best Practices for Accountants in Treasury Risk Reporting

- Timeliness: Deliver reports promptly to enable proactive risk management.

- Clarity: Use clear visuals like charts and dashboards to communicate complex risk data.

- Collaboration: Work closely with treasury, finance, and audit teams to ensure comprehensive risk coverage.

- Continuous Improvement: Regularly update risk models and reporting templates based on feedback and changing market conditions.

Example 3: Monthly Treasury Risk Dashboard

An accountant designs a dashboard combining currency, interest rate, and credit risk metrics. The dashboard uses color-coded indicators to highlight risk levels and trends, enabling senior management to quickly grasp the company’s risk profile and take informed actions.

Summary

Accountants are indispensable in the treasury risk management process. Through diligent data management, risk quantification, and clear reporting, they provide the foundation for effective risk mitigation strategies. Their role ensures that treasury risks are not only identified but also communicated transparently, supporting the organization’s financial stability and strategic objectives.

4.5 Example: Monthly Risk Reporting Dashboards for Senior Management

Effective risk reporting is crucial for senior management to make informed decisions and maintain oversight of the company’s treasury risks. A well-designed monthly risk reporting dashboard consolidates key risk metrics into an easily digestible format, enabling quick identification of potential issues and trends.

Objectives of a Monthly Risk Reporting Dashboard

- Provide a snapshot of the current risk exposure across currency, interest rate, and credit risks.

- Track risk mitigation activities and hedge effectiveness.

- Highlight any breaches of risk limits or policy deviations.

- Support strategic decision-making with clear, actionable insights.

Key Components of the Dashboard

Mind Map: Structure of a Monthly Risk Reporting Dashboard

Example Scenario: Implementing a Monthly Risk Reporting Dashboard

Company Background: A multinational corporation with exposure to multiple currencies, floating rate debt, and various counterparties.

Step 1: Data Collection

- Gather FX position data from treasury systems.

- Extract debt portfolio details from accounting records.

- Collect credit exposure and aging reports from accounts receivable/payable.

Step 2: Dashboard Design

- Use visualization tools (e.g., Power BI, Tableau) to create interactive charts.

- Include traffic light indicators for risk limit breaches (green = within limits, yellow = near limit, red = breach).

Step 3: Reporting and Review

- Distribute the dashboard to senior management monthly.

- Conduct a review meeting to discuss key risks and mitigation strategies.

Mind Map: Workflow for Monthly Risk Reporting

Practical Tips for Accountants

- Automate data extraction where possible to reduce errors and save time.

- Use consistent definitions and metrics month-over-month to track trends accurately.

- Collaborate closely with treasury and risk teams to ensure data accuracy.

- Tailor the dashboard complexity to the audience; senior management prefers high-level summaries with drill-down options.

Summary

A monthly risk reporting dashboard is an essential tool for accountants supporting treasury functions. By integrating key risk metrics, visual cues, and clear summaries, it empowers senior management to proactively manage financial risks and align treasury activities with corporate objectives.

5. Investment Management in Treasury

5.1 Principles of Short-Term Investment for Treasury

Short-term investments are a critical component of treasury management, enabling organizations to optimize liquidity while earning returns on idle cash. For accountants involved in treasury functions, understanding the principles behind short-term investments helps ensure funds are managed prudently, risks are minimized, and objectives aligned with corporate cash flow needs.

Key Principles of Short-Term Investment

- Liquidity: Investments must be easily convertible to cash without significant loss of value to meet unexpected cash needs.

- Safety: Preservation of principal is paramount; investments should have minimal credit and market risk.

- Yield: While safety and liquidity take precedence, maximizing returns within these constraints is important.

- Maturity Matching: Aligning investment maturities with anticipated cash flow requirements to avoid forced liquidation.

- Diversification: Spreading investments across instruments and counterparties to reduce risk.

Mind Map: Principles of Short-Term Investment

Common Short-Term Investment Instruments

- Treasury Bills (T-Bills)

- Commercial Paper

- Certificates of Deposit (CDs)

- Money Market Funds

- Repurchase Agreements (Repos)

Each instrument varies in terms of risk, liquidity, and yield, so selection depends on the organization’s specific treasury objectives.

Example 1: Maturity Matching in Practice

A company expects to pay a large supplier invoice in 45 days. The treasury team invests excess cash in a 45-day Treasury Bill rather than a 90-day CD. This ensures funds are available exactly when needed without risking early withdrawal penalties or reinvestment risk.

Example 2: Diversification to Mitigate Risk

Instead of placing all short-term funds in a single bank’s certificate of deposit, the treasury department splits investments across T-Bills, commercial paper from multiple issuers, and money market funds. This approach reduces exposure to any single counterparty default.

Mind Map: Short-Term Investment Decision Factors

Best Practice: Developing a Short-Term Investment Policy

Accountants should collaborate with treasury to establish a clear investment policy that defines:

- Eligible investment instruments

- Maximum maturity limits (commonly up to 1 year, often shorter for liquidity)

- Credit quality requirements (e.g., minimum credit ratings)

- Diversification guidelines

- Approval and monitoring procedures

This policy ensures consistent decision-making and compliance with regulatory and corporate governance standards.

Example 3: Yield Optimization within Safety Constraints

A treasury team compares yields on a 30-day commercial paper issued by a highly rated corporation versus a 30-day Treasury Bill. Although the commercial paper offers a slightly higher yield, the team evaluates the credit risk and decides to allocate 70% to T-Bills and 30% to commercial paper, balancing yield and safety.

Summary