International Taxation for Accountants

1. Introduction to International Taxation

1.1 Overview of International Taxation Principles

International taxation governs how countries tax income, assets, and transactions that cross their borders. For accountants and tax advisors, understanding these principles is crucial to ensure compliance, optimize tax liabilities, and advise clients effectively.

Key Principles of International Taxation

- Residence-Based Taxation: Countries tax residents on their worldwide income.

- Source-Based Taxation: Countries tax income generated within their borders, regardless of the taxpayer’s residence.

- Double Taxation: Occurs when the same income is taxed by two or more jurisdictions.

- Double Taxation Avoidance: Mechanisms such as tax treaties and unilateral relief to prevent double taxation.

- Permanent Establishment (PE): A fixed place of business in a foreign country that creates taxable presence.

- Transfer Pricing: Pricing of transactions between related entities across borders to ensure arm’s length standards.

Mind Map: Core Concepts of International Taxation

Residence-Based Taxation Explained

Residence-based taxation means a country taxes individuals or entities based on their residency status. Residents are taxed on their global income, while non-residents are taxed only on income sourced within that country.

Example:

- An accountant advising a client who is a resident of Germany but earns rental income from a property in Spain must consider that Germany taxes the client on worldwide income, while Spain taxes the rental income sourced within its territory.

Source-Based Taxation Explained

Source-based taxation focuses on taxing income generated within a country, regardless of the taxpayer’s residency.

Example:

- A US company earns royalties from licensing software to a company in India. India may impose withholding tax on the royalty payments as source-based taxation.

Double Taxation and Avoidance Mechanisms

Double taxation arises when two countries tax the same income. To mitigate this, countries enter into Double Taxation Avoidance Agreements (DTAAs) or provide unilateral relief such as foreign tax credits.

Example:

- A Canadian resident receives dividends from a US company. Both Canada and the US may tax the dividend. The Canada-US tax treaty reduces withholding tax rates and Canada allows a foreign tax credit to avoid double taxation.

Mind Map: Double Taxation Avoidance Mechanisms

Practical Example: Applying Residence and Source Principles

Scenario:

- Maria is a resident of France and works remotely for a company in the UK. She earns salary income from the UK company.

Analysis:

- France taxes Maria on her worldwide income (residence-based).

- The UK may tax her salary as the source country.

- The France-UK tax treaty determines which country has taxing rights and how double taxation is avoided.

Best Practice:

- Accountants should review residency status, source of income, and applicable tax treaties to advise clients accurately.

Summary

Understanding international taxation principles helps accountants navigate complex cross-border tax scenarios. Key concepts like residence, source, double taxation, and avoidance mechanisms form the foundation for effective tax planning and compliance.

For further reading, consider exploring OECD’s Model Tax Convention and local tax authority guidelines.

1.2 Importance of International Taxation for Accountants and Tax Advisors

International taxation is a critical area of expertise for accountants and tax advisors due to the increasing globalization of business activities. As companies expand across borders, understanding the complex web of tax laws, treaties, and compliance requirements becomes essential to optimize tax liabilities, ensure compliance, and mitigate risks.

Why International Taxation Matters

- Global Business Expansion: Multinational corporations operate in multiple jurisdictions, each with its own tax regulations.

- Complex Compliance Requirements: Different countries have unique tax filing, reporting, and withholding obligations.

- Risk Management: Incorrect tax treatment can lead to penalties, double taxation, or disputes with tax authorities.

- Tax Efficiency: Proper planning can reduce overall tax burden through treaty benefits, transfer pricing strategies, and tax credits.

- Client Advisory: Accountants and tax advisors play a pivotal role in guiding clients through international tax challenges.

Mind Map: Importance of International Taxation for Accountants

Practical Example 1: Advising a Client Expanding into Multiple Countries

Scenario: A mid-sized technology firm headquartered in the US plans to open subsidiaries in Germany and India.

Importance: The accountant must understand the tax residency rules, withholding tax rates on royalties, and transfer pricing requirements in both countries to:

- Avoid double taxation through applicable tax treaties.

- Ensure proper documentation for intercompany transactions.

- Advise on permanent establishment risks.

Mind Map: Key Considerations for Multinational Expansion

Practical Example 2: Managing Double Taxation Risk for an Expatriate Employee

Scenario: An accountant advises a client who is an employee working temporarily in France but remains a tax resident in Canada.

Importance: Understanding the tax treaty between Canada and France helps:

- Determine which country has taxing rights on employment income.

- Apply foreign tax credits to avoid double taxation.

- Comply with reporting obligations in both countries.

Mind Map: Managing Double Taxation for Expatriates

Summary

For accountants and tax advisors, mastering international taxation is not optional but essential. It enables them to provide comprehensive advice, ensure compliance, and help clients navigate the complexities of cross-border taxation efficiently and ethically.

1.3 Key Terminology and Concepts in Cross-Border Taxation

Understanding international taxation requires familiarity with specific terminology and foundational concepts that govern how taxes are applied across different jurisdictions. This section breaks down essential terms and concepts with clear explanations, mind maps, and practical examples to help accountants and tax advisors navigate cross-border tax scenarios effectively.

Key Terminology

- Tax Residency: The status determining in which country an individual or entity is subject to tax on worldwide income.

- Source of Income: The location or jurisdiction where income is generated or deemed to arise.

- Permanent Establishment (PE): A fixed place of business through which the business of an enterprise is wholly or partly carried out, triggering tax obligations in that jurisdiction.

- Double Taxation: The imposition of tax by two or more jurisdictions on the same income or economic activity.

- Double Taxation Avoidance Agreement (DTAA): A treaty between countries to prevent double taxation and fiscal evasion.

- Withholding Tax: A tax deducted at source on payments such as dividends, interest, and royalties made to non-residents.

- Transfer Pricing: Pricing of transactions between related entities across borders to allocate income and expenses appropriately.

- Controlled Foreign Corporation (CFC): A foreign company controlled by residents of another country, subject to specific anti-deferral tax rules.

Mind Map: Core Concepts in Cross-Border Taxation

Concept Explanations with Examples

-

Tax Residency

- Definition: Determines which country has the right to tax an individual or company on their global income.

- Example: An accountant advising a client who works in Germany for 8 months and in France for 4 months needs to determine the client’s tax residency. Since the client spends more than 183 days in Germany, Germany is likely the tax residence, meaning worldwide income is taxable there.

-

Source of Income

- Definition: The jurisdiction where income is considered to have originated.

- Example: A company headquartered in Canada sells goods in Mexico. The profits from sales in Mexico are sourced in Mexico and may be subject to Mexican tax.

-

Permanent Establishment (PE)

- Definition: A business presence in a foreign country that creates tax obligations.

- Example: A UK company has a warehouse in Spain where goods are stored and sold. This warehouse constitutes a PE in Spain, so the UK company must pay Spanish taxes on profits attributable to that PE.

-

Double Taxation and DTAA

- Definition: When two countries tax the same income; treaties help avoid this.

- Example: A US company receives dividends from a subsidiary in India. Without a treaty, both countries might tax the dividends. Under the US-India DTAA, withholding tax rates are reduced, and foreign tax credits may apply.

-

Withholding Tax

- Definition: Tax deducted at source on cross-border payments.

- Example: A French company pays royalties to a software developer in the UK. France withholds 15% tax on the payment, which may be reduced under the France-UK tax treaty.

-

Transfer Pricing

- Definition: Pricing transactions between related entities to reflect market conditions.

- Example: A parent company in Japan sells components to its subsidiary in Brazil. The price must be set at arm’s length to avoid shifting profits and tax base erosion.

-

Controlled Foreign Corporation (CFC)

- Definition: Foreign entities controlled by residents to prevent tax deferral.

- Example: A US parent company owns 80% of a subsidiary in the Cayman Islands. US CFC rules may require the parent to include certain income of the subsidiary in its taxable income immediately.

Mind Map: Tax Residency Determination

Practical Example: Applying Tax Residency Rules

Scenario: Sarah, a consultant, spends 200 days in Country A and 165 days in Country B during a tax year. She has a permanent home in Country B but her main economic interests are in Country A.

- According to the physical presence test, Sarah is a tax resident of Country A (over 183 days).

- However, Country B may claim residency based on her permanent home.

- Tax treaties often provide tiebreaker rules considering permanent home, center of vital interests, habitual abode, and nationality.

Best Practice: Accountants should carefully analyze residency criteria and treaty provisions to determine correct tax residency and avoid double taxation.

This foundational knowledge equips accountants and tax advisors to confidently interpret international tax rules and apply them in real-world scenarios, ensuring compliance and optimized tax outcomes for their clients.

1.4 Understanding Tax Jurisdictions and Tax Residency

International taxation hinges critically on the concepts of tax jurisdictions and tax residency. For accountants and tax advisors, mastering these concepts is essential to correctly determine tax obligations and optimize tax planning for clients operating across borders.

What is a Tax Jurisdiction?

A tax jurisdiction refers to the geographic area or territory where a government has the authority to impose taxes. This can be a country, state, province, or municipality. Each jurisdiction has its own tax laws, rates, and regulations.

Key Points:

- Jurisdictions define where income, assets, or activities are taxable.

- Multiple jurisdictions can claim taxing rights on the same income, leading to double taxation.

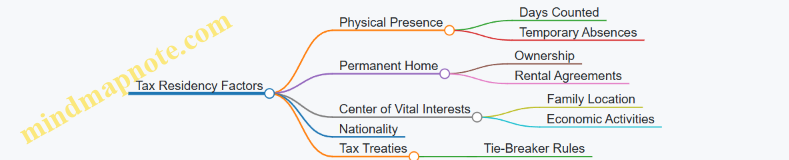

What is Tax Residency?

Tax residency determines the jurisdiction(s) where an individual or entity is considered a resident for tax purposes. Residency status affects the scope of taxable income and the application of tax treaties.

Common Criteria for Tax Residency:

- Physical presence (e.g., spending more than 183 days in a country)

- Permanent home or habitual abode

- Center of vital interests (personal and economic ties)

- Citizenship (in some jurisdictions)

Mind Map: Tax Jurisdictions and Tax Residency

Residency Rules for Individuals: Examples

Example 1: Physical Presence Test

- John, a consultant, spends 190 days in Country A during a calendar year.

- Country A’s tax law states that individuals spending more than 183 days are tax residents.

- John is considered a tax resident of Country A and must report worldwide income there.

Example 2: Center of Vital Interests

- Maria lives 120 days in Country B and 245 days in Country C.

- She owns a home and her family lives in Country B, where she also works part-time.

- Despite spending fewer days in Country B, her center of vital interests is Country B.

- She is a tax resident of Country B.

Residency Rules for Entities: Examples

Example 3: Place of Incorporation vs. Place of Effective Management

- Company X is incorporated in Country D but its board meetings and key management decisions occur in Country E.

- Country D taxes based on incorporation; Country E taxes based on effective management.

- Company X may be considered a resident in both jurisdictions, triggering potential double taxation.

Best Practices for Accountants and Tax Advisors

- Conduct thorough residency analyses: Evaluate all relevant criteria, not just physical presence.

- Document residency status: Maintain clear records to support residency claims.

- Review tax treaties: Use treaties to resolve dual residency and avoid double taxation.

- Monitor changes: Residency status can change with travel patterns or business operations.

Practical Example: Determining Tax Residency for a Multinational Employee

Scenario:

Emma is an employee of a multinational corporation. She is originally from Country F but has been on a 9-month assignment in Country G. She maintains a home in Country F and her family lives there. Country G’s tax law considers individuals residents if they stay more than 183 days.

Analysis:

- Emma spent approximately 270 days in Country G, exceeding the 183-day threshold.

- However, her permanent home and family remain in Country F.

- According to Country G, Emma is a tax resident due to physical presence.

- Country F may also consider her a resident due to permanent home and family ties.

Resolution:

- Refer to the tax treaty between Country F and Country G.

- The treaty’s tie-breaker rules prioritize permanent home and center of vital interests.

- Emma is likely a tax resident of Country F, with limited tax obligations in Country G.

Best Practice:

- Document Emma’s travel and living arrangements.

- Advise Emma on tax filing obligations in both countries.

- Utilize the treaty to claim relief from double taxation.

Understanding tax jurisdictions and residency is foundational for effective international tax advisory. By applying these principles with clear examples and mind maps, accountants can better navigate complex cross-border tax scenarios and provide accurate, compliant advice.

1.5 Practical Example: Determining Tax Residency for a Multinational Employee

Determining tax residency is a critical step for accountants and tax advisors when managing multinational employees. Tax residency affects which country has the right to tax the employee’s global income and influences compliance obligations.

Key Factors in Determining Tax Residency

The criteria for tax residency vary by country but generally include:

- Physical Presence Test: Number of days spent in the country (commonly 183 days rule).

- Permanent Home Test: Whether the employee has a permanent home available in the country.

- Center of Vital Interests: Location of personal and economic ties.

- Habitual Abode: Where the employee usually lives.

- Nationality: Sometimes used as a tiebreaker.

Mind Map: Tax Residency Determination Criteria

Example Scenario

Employee: John Smith

Countries involved: Country A and Country B

Facts:

- John spent 120 days in Country A and 150 days in Country B during the tax year.

- He owns a home in Country A but rents an apartment in Country B.

- His immediate family (spouse and children) live in Country A.

- His main employment income is from a company based in Country B.

Step-by-Step Residency Analysis

-

Physical Presence Test:

- John does not meet the 183-day threshold in either country.

-

Permanent Home Test:

- John owns a home in Country A (permanent home available).

- He rents in Country B (temporary accommodation).

-

Center of Vital Interests:

- Family is in Country A.

- Economic interests (employment) are in Country B.

-

Habitual Abode:

- John spends more days in Country B (150 days) than Country A (120 days).

-

Nationality:

- John is a citizen of Country A.

Mind Map: Residency Decision for John Smith

Applying Tax Treaty Tie-Breaker Rules

If both countries claim John as a tax resident, the tax treaty between Country A and Country B will apply tie-breaker rules, typically in the following order:

- Permanent home

- Center of vital interests

- Habitual abode

- Nationality

In John’s case, the permanent home and center of vital interests are both in Country A, so he would be considered a resident of Country A for tax purposes.

Best Practice Tips for Accountants

- Gather Comprehensive Data: Collect detailed information on days spent, home ownership, family location, and economic ties.

- Understand Local Rules: Each country may have unique residency criteria.

- Review Relevant Tax Treaties: Always check applicable treaties for tie-breaker provisions.

- Document Analysis: Maintain clear records of residency determinations for audit defense.

- Communicate with Clients: Explain implications of residency status on tax obligations.

Summary

Determining tax residency for multinational employees requires a holistic approach considering multiple factors. Using structured analysis and tax treaty provisions helps ensure accurate residency status, minimizing risks of double taxation or non-compliance.

2. Double Taxation and Tax Treaties

2.1 What is Double Taxation and Why Does It Occur?

Double taxation is a fundamental concept in international taxation that refers to the same income or financial transaction being taxed by two or more different jurisdictions. This can lead to an increased tax burden on taxpayers, especially individuals and multinational corporations operating across borders.

Understanding Double Taxation

Double taxation typically arises in two main forms:

- Jurisdictional Double Taxation: When two or more countries claim taxing rights over the same income or transaction.

- Economic Double Taxation: When the same income is taxed multiple times at different stages or entities, such as corporate profits being taxed at the company level and again when distributed as dividends to shareholders.

Why Does Double Taxation Occur?

Double taxation occurs primarily due to differences in national tax laws, definitions of tax residency, and the scope of taxable income. Key reasons include:

- Conflicting Tax Residency Rules: Countries may have different criteria for determining tax residency, causing an individual or company to be considered resident in multiple countries.

- Source vs. Residence Taxation: Some countries tax income based on where it is earned (source), while others tax based on the taxpayer’s residence.

- Lack of Coordination Between Tax Authorities: Without agreements or treaties, countries independently apply their tax laws, leading to overlapping claims.

Mind Map: Causes of Double Taxation

Mind Map: Effects of Double Taxation

Practical Example 1: Individual Tax Residency Conflict

Consider an expatriate, John, who lives and works in Country A but maintains a home and family in Country B. Both countries consider John a tax resident based on their domestic rules:

- Country A taxes John on his worldwide income because he works there.

- Country B taxes John on worldwide income because he is considered resident due to family ties.

Without relief, John’s income could be taxed twice, once by each country.

Practical Example 2: Corporate Double Taxation on Dividends

A multinational corporation, CorpX, earns profits in Country X and pays corporate income tax there. When CorpX distributes dividends to its parent company in Country Y, Country Y also taxes those dividends as income. This results in the same profits being taxed twice:

- First at the corporate level in Country X.

- Then at the shareholder level in Country Y.

Best Practices to Address Double Taxation

- Utilize Double Taxation Avoidance Agreements (DTAAs): These treaties allocate taxing rights and provide relief mechanisms.

- Apply Foreign Tax Credits: Taxpayers can often credit taxes paid abroad against domestic tax liabilities.

- Understand Residency Rules Thoroughly: Properly determining residency can prevent unintended double taxation.

- Engage in Proactive Tax Planning: Structuring transactions and operations to minimize overlapping tax exposure.

By understanding the causes and implications of double taxation, accountants and tax advisors can better assist clients in navigating complex international tax environments and optimizing their tax positions.

2.2 Overview of Double Taxation Avoidance Agreements (DTAAs)

Double Taxation Avoidance Agreements (DTAAs) are bilateral treaties between two countries aimed at preventing the same income from being taxed twice. These agreements play a critical role in international taxation by providing clarity on taxing rights, reducing tax barriers to cross-border trade and investment, and promoting economic cooperation.

What is a DTAA?

A DTAA is a treaty signed between two countries to allocate taxing rights on various types of income such as business profits, dividends, interest, royalties, and capital gains. It ensures that taxpayers do not pay tax on the same income in both countries or receive relief for taxes paid abroad.

Objectives of DTAAs

- Avoid double taxation of income

- Prevent tax evasion and avoidance

- Promote cross-border trade and investment

- Provide a framework for cooperation between tax authorities

Key Features of DTAAs

- Residence and Source Rules: Defines which country has the right to tax income based on residence or source.

- Tax Credit or Exemption Methods: Mechanisms to relieve double taxation.

- Reduced Withholding Tax Rates: On dividends, interest, and royalties.

- Non-Discrimination Clauses: Ensures nationals or enterprises of one country are not discriminated against in the other.

- Exchange of Information: Facilitates sharing of tax information between countries.

Mind Map: Core Components of a DTAA

Methods to Avoid Double Taxation Under DTAAs

- Exemption Method: Income taxed in one country is exempted in the other.

- Credit Method: Tax paid in the source country is credited against tax payable in the residence country.

Practical Example: Applying DTAA to Avoid Double Taxation on Dividends

Scenario:

- A company in Country A owns shares in a company in Country B.

- Country B imposes a 15% withholding tax on dividends.

- Country A taxes dividends received by its residents at 25%.

- A DTAA between Country A and Country B reduces withholding tax on dividends to 5%.

Application:

- The company receives dividends worth $100,000.

- Country B withholds 5% tax = $5,000.

- Country A taxes the dividend at 25% = $25,000.

- To avoid double taxation, Country A allows a tax credit of $5,000.

- Net tax paid in Country A = $25,000 - $5,000 = $20,000.

- Total tax paid = $5,000 (Country B) + $20,000 (Country A) = $25,000.

Without DTAA, withholding tax could have been 15%, increasing total tax paid.

Mind Map: Example of Dividend Taxation Under DTAA

Best Practices for Accountants and Tax Advisors Regarding DTAAs

- Identify Applicable DTAA: Always verify if a DTAA exists between the countries involved.

- Understand Treaty Provisions: Carefully analyze relevant articles for income type and relief methods.

- Documentation: Maintain proof of residence and eligibility to claim treaty benefits.

- Withholding Tax Compliance: Ensure correct withholding tax rates are applied.

- Claim Relief Timely: Assist clients in claiming tax credits or exemptions as per treaty.

Additional Example: Interest Income Under DTAA

Scenario:

- An individual resident in Country X receives interest from a bond issued in Country Y.

- Country Y’s domestic withholding tax on interest is 20%.

- The DTAA between Country X and Country Y reduces withholding tax to 10%.

Application:

- Interest received: $50,000

- Withholding tax deducted in Country Y: $5,000 (10%)

- Country X taxes interest at 15%, but allows credit for tax paid in Country Y.

- Tax in Country X: $7,500 (15% of $50,000) minus $5,000 credit = $2,500 net tax.

- Total tax paid: $5,000 + $2,500 = $7,500.

Without DTAA, withholding tax would be $10,000, increasing total tax burden.

Summary

DTAAs are essential tools for accountants and tax advisors managing cross-border taxation. They provide clarity, reduce tax burdens, and help clients comply with international tax laws. Understanding their provisions and practical application ensures effective tax planning and compliance.

2.3 How to Interpret and Apply Tax Treaties

Tax treaties, also known as Double Taxation Avoidance Agreements (DTAAs), are bilateral agreements between two countries that aim to prevent the same income from being taxed twice. For accountants and tax advisors, correctly interpreting and applying these treaties is crucial to optimizing tax liabilities for clients engaged in cross-border activities.

Understanding the Structure of Tax Treaties

Most tax treaties follow the OECD Model Tax Convention or the UN Model Tax Convention, and typically include the following key components:

- Preamble: States the purpose of the treaty.

- Definitions: Clarifies terms like resident, permanent establishment, dividends, interest, royalties.

- Allocation of Taxing Rights: Specifies which country has the right to tax certain types of income.

- Relief Methods: Explains how double taxation is relieved (exemption or credit).

- Exchange of Information: Provisions for cooperation between tax authorities.

- Non-Discrimination: Ensures taxpayers are not discriminated against based on nationality or residency.

Mind Map: Key Elements of a Tax Treaty

Step-by-Step Approach to Interpreting Tax Treaties

- Identify the Residency of the Taxpayer: Determine the country of residence as per the treaty definition.

- Determine the Nature of Income: Classify the income (e.g., business profits, dividends, royalties).

- Check for Permanent Establishment (PE): For business profits, ascertain if a PE exists in the source country.

- Apply the Relevant Article: Refer to the specific article in the treaty that governs the income type.

- Determine Taxing Rights: Understand which country has the primary right to tax and any limitations.

- Apply Relief Methods: Use exemption or credit methods to avoid double taxation.

- Consider Withholding Tax Rates: Apply reduced rates if specified.

- Review Anti-Abuse Provisions: Ensure the treaty benefits are not denied due to treaty abuse.

Mind Map: Interpreting a Tax Treaty

Practical Example 1: Applying a Tax Treaty on Dividends

Scenario: A company resident in Country A receives dividends from a subsidiary in Country B. Without a treaty, Country B would withhold tax at 30% on dividends.

Application:

- Check the tax treaty between Country A and Country B.

- The treaty limits withholding tax on dividends to 10%.

- Country B withholds 10% instead of 30%, reducing tax cost.

- Country A allows a foreign tax credit for the 10% withholding tax.

Result: The investor pays a maximum of 10% withholding tax instead of 30%, and double taxation is avoided by crediting the withholding tax against Country A’s tax liability.

Practical Example 2: Business Profits and Permanent Establishment

Scenario: An IT consulting firm resident in Country X provides services in Country Y but has no fixed place of business there.

Application:

- According to the treaty, business profits are taxable only in Country X unless the firm has a PE in Country Y.

- Since no PE exists, Country Y cannot tax the income.

Result: The firm’s income is only taxed in Country X, avoiding double taxation and unnecessary tax in Country Y.

Tips and Best Practices

- Always verify the latest version of the tax treaty, as protocols and amendments may change provisions.

- Use official commentary and OECD guidelines to interpret ambiguous treaty language.

- Document the application of treaty benefits thoroughly to support claims during audits.

- Be mindful of anti-abuse rules such as the Principal Purpose Test (PPT) which may deny treaty benefits.

Mind Map: Best Practices for Applying Tax Treaties

By mastering the interpretation and application of tax treaties, accountants and tax advisors can effectively reduce tax burdens for their clients, ensure compliance, and navigate complex cross-border tax scenarios with confidence.

2.4 Best Practices for Utilizing Tax Treaties to Minimize Tax Burden

International tax treaties are powerful tools for accountants and tax advisors to help clients reduce their overall tax liabilities and avoid double taxation. Understanding how to effectively utilize these treaties requires a strategic approach, careful analysis, and compliance with treaty provisions.

Best Practices Overview

- Thoroughly Analyze Treaty Provisions: Each tax treaty has unique clauses regarding income types, withholding tax rates, residency definitions, and dispute resolution mechanisms.

- Confirm Residency Status: Ensure the taxpayer qualifies as a resident under the treaty to benefit from treaty provisions.

- Leverage Reduced Withholding Tax Rates: Apply treaty rates on dividends, interest, and royalties instead of domestic rates.

- Utilize Treaty Tie-Breaker Rules: Resolve dual residency conflicts to avoid double taxation.

- Claim Treaty Benefits Properly: Follow procedural requirements such as submitting residency certificates and treaty forms.

- Monitor Anti-Abuse Provisions: Be aware of limitation on benefits (LOB) clauses to ensure eligibility.

- Coordinate with Domestic Tax Laws: Align treaty benefits with local tax regulations and compliance.

Mind Map: Utilizing Tax Treaties Effectively

Example 1: Applying Reduced Withholding Tax on Dividends

Scenario: A US-based company receives dividends from its subsidiary in Germany. The domestic German withholding tax rate on dividends is 26.375%, but the US-Germany tax treaty reduces this rate to 15%.

Best Practice Steps:

- Verify that the US company qualifies as a resident under the treaty.

- Obtain a valid residency certificate from the US tax authorities.

- Submit the residency certificate and treaty claim form to the German tax authorities.

- Apply the 15% treaty withholding tax rate instead of the domestic 26.375%.

- Report the dividend income and withholding tax on the US company’s tax return.

Outcome: The US company saves 11.375% in withholding tax, reducing its overall tax burden.

Mind Map: Dividend Withholding Tax Reduction Process

Example 2: Resolving Dual Residency Using Tie-Breaker Rules

Scenario: An individual holds residency in both Canada and the UK, creating potential double taxation issues.

Best Practice Steps:

- Identify dual residency status under domestic laws.

- Refer to the Canada-UK tax treaty tie-breaker rules, which consider factors such as permanent home, center of vital interests, habitual abode, and nationality.

- Determine the primary residency country based on the tie-breaker hierarchy.

- Apply the treaty provisions accordingly to avoid double taxation.

Outcome: The individual is recognized as a resident of the UK for treaty purposes, preventing double taxation on worldwide income.

Mind Map: Tie-Breaker Rule Application

Additional Tips

- Keep Updated on Treaty Changes: Tax treaties can be renegotiated or amended; staying current ensures optimal application.

- Document Everything: Maintain thorough records of residency certificates, treaty claims, and correspondence.

- Coordinate with Multijurisdictional Teams: Collaboration helps navigate complex treaty networks.

- Educate Clients: Inform clients about treaty benefits and compliance requirements to avoid surprises.

By integrating these best practices, accountants and tax advisors can effectively leverage international tax treaties to minimize clients’ tax burdens while ensuring compliance and reducing risks.

2.5 Practical Example: Applying a Tax Treaty to Avoid Double Taxation on Dividends

Introduction

When a company or individual receives dividends from a foreign country, they may face taxation both in the source country (where the dividend is paid) and in their country of residence. Double Taxation Avoidance Agreements (DTAAs) help mitigate this by reducing withholding tax rates or providing credits.

This section walks through a practical example of applying a tax treaty to avoid double taxation on dividends, illustrating best practices and key considerations.

Scenario Overview

- Resident Country: Country A

- Source Country: Country B

- Investor: Company X, resident in Country A

- Dividend Income: $100,000 paid by a company in Country B to Company X

- Domestic withholding tax rate in Country B: 15%

- Tax treaty withholding tax rate on dividends: 5%

- Corporate tax rate in Country A: 25%

Step 1: Identify Applicable Tax Treaty and Withholding Tax Rate

- Check if Country A and Country B have a tax treaty.

- Confirm the treaty’s dividend withholding tax rate (usually found in the treaty’s article on dividends).

Step 2: Apply Reduced Withholding Tax Rate

- Instead of the domestic 15%, Country B applies the treaty rate of 5%.

- Withholding tax withheld = $100,000 * 5% = $5,000

Step 3: Report Dividend Income in Resident Country

- Company X reports the full $100,000 dividend income.

- Country A taxes the dividend at 25% corporate tax rate.

- Tax on dividend = $100,000 * 25% = $25,000

Step 4: Claim Foreign Tax Credit to Avoid Double Taxation

- Company X claims a foreign tax credit for the $5,000 withheld in Country B.

- Net tax payable in Country A = $25,000 - $5,000 = $20,000

Step 5: Documentation and Compliance Best Practices

- Obtain and maintain a residency certificate from Country A.

- Submit treaty benefit claim forms to Country B’s tax authorities to apply reduced withholding.

- Keep detailed records of dividend payments, withholding tax certificates, and foreign tax credits claimed.

- Coordinate with tax advisors to ensure compliance with both countries’ regulations.

Additional Example: No Tax Treaty Scenario

- If no treaty exists, the full 15% withholding tax applies.

- Foreign tax credit in Country A remains $15,000.

- Net tax payable in Country A = $25,000 - $15,000 = $10,000.

However, the higher withholding reduces cash flow upfront, and administrative burden may increase.

Summary Table

| Step | Action | Amount (USD) |

|---|---|---|

| Dividend Income | Received from Country B | 100,000 |

| Withholding Tax (Treaty) | 5% of dividend | 5,000 |

| Tax Payable in Country A | 25% of dividend | 25,000 |

| Foreign Tax Credit | Withholding tax paid in Country B | 5,000 |

| Net Tax Payable in Country A | Tax Payable - Foreign Tax Credit | 20,000 |

Key Takeaways

- Always verify the existence and terms of tax treaties before dividend payments.

- Proper documentation is critical to claim treaty benefits.

- Foreign tax credits prevent double taxation but do not reduce withholding tax upfront.

- Coordinated tax planning can improve cash flow and compliance.

References

- OECD Model Tax Convention on Income and on Capital

- Country A and Country B’s Double Taxation Avoidance Agreement

- Local tax authority guidelines on foreign tax credits and withholding tax

This practical example demonstrates how accountants and tax advisors can leverage tax treaties to minimize double taxation on dividends, ensuring compliance and optimizing tax outcomes for their clients.

3. Transfer Pricing Fundamentals

3.1 Introduction to Transfer Pricing and Its Importance

Transfer pricing refers to the rules and methods for pricing transactions within and between enterprises under common ownership or control. Because multinational companies operate across different tax jurisdictions, transfer pricing determines how profits and expenses are allocated among subsidiaries, impacting the taxable income reported in each country.

Why is Transfer Pricing Important?

- Tax Compliance: Ensures companies comply with local tax laws and avoid penalties.

- Profit Allocation: Helps allocate profits fairly among countries where business activities occur.

- Avoidance of Double Taxation: Proper transfer pricing reduces the risk of the same income being taxed twice.

- Prevention of Tax Evasion: Prevents manipulation of prices to shift profits to low-tax jurisdictions.

Mind Map: Key Concepts of Transfer Pricing

Mind Map: Transfer Pricing Stakeholders

Common Transfer Pricing Methods

- Comparable Uncontrolled Price (CUP) Method

- Compares price charged in a controlled transaction to price charged in a comparable uncontrolled transaction.

- Resale Price Method

- Starts with the resale price to an independent party, subtracting an appropriate gross margin.

- Cost Plus Method

- Adds an appropriate markup to the costs incurred by the supplier.

- Transactional Net Margin Method (TNMM)

- Examines net profit relative to an appropriate base (e.g., costs, sales).

- Profit Split Method

- Divides combined profits from controlled transactions according to each party’s contribution.

Practical Example: Transfer Pricing in Action

Scenario: A parent company in the USA sells raw materials to its subsidiary in Germany. The parent charges $100 per unit. German tax authorities question whether this price reflects an arm’s length price.

Step 1: Identify comparable uncontrolled transactions (e.g., sales of similar raw materials between independent parties).

Step 2: Suppose comparable sales range from $95 to $105 per unit.

Step 3: Since $100 falls within this range, the price is considered arm’s length.

Best Practice: Document the comparability analysis and pricing rationale to support the transfer price in case of audits.

Mind Map: Transfer Pricing Documentation Best Practices

Summary

Transfer pricing is a critical area for accountants and tax advisors working with multinational clients. Understanding its principles, methods, and documentation requirements helps ensure compliance, optimize tax positions, and mitigate risks associated with international taxation.

By applying clear examples and maintaining thorough documentation, professionals can effectively manage transfer pricing challenges and support their clients’ global operations.

3.2 Arm’s Length Principle Explained

The Arm’s Length Principle (ALP) is a foundational concept in international taxation and transfer pricing. It requires that transactions between related parties (such as subsidiaries of a multinational corporation) be conducted as if they were between independent, unrelated parties, each acting in their own best interest.

This principle ensures that profits are allocated fairly among different tax jurisdictions, preventing profit shifting and tax base erosion.

What is the Arm’s Length Principle?

- Definition: The price or terms of a transaction between related parties should be the same as those that would have been agreed upon between independent entities under comparable circumstances.

- Objective: To ensure that taxable income is not artificially shifted to low-tax jurisdictions through manipulated transfer prices.

Key Components of the Arm’s Length Principle

Mind Map: Factors to Consider in Applying ALP

Transfer Pricing Methods Under ALP

- Comparable Uncontrolled Price (CUP) Method

- Resale Price Method

- Cost Plus Method

- Transactional Net Margin Method (TNMM)

- Profit Split Method

Each method aims to approximate the price or margin that would have been agreed upon by independent parties.

Practical Example 1: Applying ALP to an Intercompany Sale

Scenario: A parent company in Germany sells electronic components to its subsidiary in Brazil. The subsidiary then sells finished products in the local market.

Issue: The German parent sets the transfer price significantly below market value to reduce taxable income in Germany and increase profits in Brazil.

Application of ALP:

- Identify comparable uncontrolled transactions where similar components are sold between independent companies.

- Use the CUP method to determine an arm’s length price.

- Adjust the transfer price to reflect the market-based price.

Outcome: The tax authorities may adjust the taxable income in Germany and Brazil to reflect the arm’s length price, ensuring fair taxation.

Practical Example 2: Functional Analysis for ALP

Scenario: A multinational pharmaceutical company transfers intellectual property (IP) rights from its US parent to its subsidiary in India.

Functional Analysis:

- Functions performed: R&D, marketing, manufacturing

- Assets used: Patents, trademarks

- Risks assumed: Market risk, product liability

Application: The transfer price for the IP license fee must reflect the value of the functions performed and risks borne by each party.

Outcome: Using the Profit Split Method, profits are allocated based on the relative contributions of each entity, ensuring compliance with ALP.

Summary

The Arm’s Length Principle is essential for fair taxation in international business. Accountants and tax advisors must:

- Conduct thorough functional analyses

- Identify and select appropriate comparables

- Choose the correct transfer pricing method

- Document their approach comprehensively

By doing so, they help multinational enterprises comply with tax regulations and avoid disputes with tax authorities.

3.3 Documentation and Compliance Requirements

International transfer pricing regulations require companies to maintain thorough documentation to justify that their intercompany transactions are conducted at arm’s length. This section covers the key documentation types, compliance timelines, and best practices to ensure adherence to global standards.

Key Documentation Types

- Master File: Provides a high-level overview of the multinational enterprise (MNE) group, including organizational structure, business operations, intangibles, intercompany financial activities, and overall transfer pricing policies.

- Local File: Contains detailed information specific to the local entity, including related party transactions, financial data, and transfer pricing analyses relevant to that jurisdiction.

- Country-by-Country Report (CbCR): Summarizes the global allocation of income, taxes paid, and certain indicators of economic activity among tax jurisdictions.

Mind Map: Transfer Pricing Documentation Components

Compliance Timelines and Jurisdictional Variations

- Most countries require submission of transfer pricing documentation contemporaneously with tax filings or within a specified period after the fiscal year-end.

- Deadlines vary; for example, India requires documentation within 30 days of filing the tax return, while the US requires documentation upon IRS request.

- Penalties for non-compliance can include fines, adjustments, and increased audit risk.

Best Practices for Documentation and Compliance

- Maintain Consistency: Ensure that transfer pricing policies are consistently applied and documented across jurisdictions.

- Regular Updates: Update documentation annually or whenever significant business changes occur.

- Robust Benchmarking: Use reliable and recent data for comparability analyses.

- Clear and Concise Presentation: Documentation should be easy to understand for tax authorities.

- Centralized Record-Keeping: Use digital platforms to store and manage documentation securely.

Practical Example: Preparing a Local File for a European Subsidiary

Scenario: A German subsidiary sells components to its US parent company. To comply with German transfer pricing rules, the accountant must prepare a local file.

Steps:

- Collect detailed information on the German subsidiary’s functions, assets, and risks.

- Document all intercompany sales transactions, including contracts and invoices.

- Perform a benchmarking study using comparable companies to justify the pricing.

- Summarize financial results and reconcile with transfer pricing policies.

- Compile the documentation in German and ensure it is ready for submission with the tax return.

Mind Map: Best Practices for Transfer Pricing Compliance

Additional Example: Consequences of Inadequate Documentation

A Canadian subsidiary failed to provide adequate transfer pricing documentation for its intercompany service fees. During an audit, the tax authority imposed a significant adjustment increasing taxable income by CAD 2 million and levied penalties amounting to 10% of the adjustment. This example highlights the importance of timely and comprehensive documentation to mitigate audit risks and financial penalties.

By adhering to these documentation and compliance requirements, accountants and tax advisors can effectively manage transfer pricing risks and support their clients in meeting international tax obligations.

3.4 Best Practices for Preparing Transfer Pricing Documentation

Transfer pricing documentation is a critical component for multinational enterprises (MNEs) to demonstrate compliance with the arm’s length principle and avoid disputes or penalties. Proper documentation supports the pricing of intercompany transactions and provides tax authorities with transparency.

Key Objectives of Transfer Pricing Documentation

- Demonstrate that transfer prices are consistent with the arm’s length principle.

- Provide evidence to support pricing methodologies.

- Facilitate tax audits and reduce the risk of adjustments.

- Ensure compliance with local and international regulations.

Best Practices for Preparing Transfer Pricing Documentation

Understand Local Jurisdiction Requirements

- Each country may have specific documentation requirements (e.g., content, format, deadlines).

- Stay updated on local rules to avoid penalties.

Prepare a Master File and Local File

- Master File: Provides an overview of the MNE group, its global business operations, transfer pricing policies, and allocation of income/tax.

- Local File: Contains detailed information on specific intercompany transactions relevant to the local entity.

Conduct a Thorough Functional Analysis

- Identify the functions performed, assets used, and risks assumed by each related party.

- This analysis supports the selection of the most appropriate transfer pricing method.

Select and Apply the Most Appropriate Transfer Pricing Method

- Common methods include Comparable Uncontrolled Price (CUP), Resale Price, Cost Plus, Transactional Net Margin Method (TNMM), and Profit Split.

- Justify the choice of method with supporting data.

Benchmarking Analysis

- Use reliable and comparable data sources to identify arm’s length ranges.

- Document the selection criteria for comparables.

Maintain Consistency and Update Regularly

- Ensure consistency between documentation and actual pricing policies.

- Update documentation annually or when significant changes occur.

Include Supporting Evidence

- Contracts, invoices, intercompany agreements, and financial statements.

- Document assumptions and adjustments made.

Use Clear and Concise Language

- Avoid overly technical jargon.

- Make documentation accessible for tax authorities and internal stakeholders.

Mind Map: Transfer Pricing Documentation Best Practices

Practical Example: Preparing Transfer Pricing Documentation for an Intercompany Sale

Scenario: A manufacturing subsidiary in Country A sells components to a related distribution company in Country B. The transfer price must comply with the arm’s length principle.

Step 1: Functional Analysis

- Manufacturing subsidiary performs production and quality control.

- Distribution company handles marketing, sales, and inventory risks.

Step 2: Select Transfer Pricing Method

- Resale Price Method chosen because the distributor resells products to unrelated customers.

Step 3: Benchmarking

- Identify comparable distributors in Country B.

- Analyze gross margins to establish arm’s length range.

Step 4: Documentation Content

- Master File: Overview of the MNE group and global transfer pricing policy.

- Local File: Details of the intercompany sale, functional analysis, method selection, benchmarking data, and contracts.

Step 5: Supporting Evidence

- Sales contracts between subsidiaries.

- Financial statements.

- Market research reports for comparables.

Step 6: Review and Update

- Documentation is reviewed annually to reflect changes in business or regulations.

By following these best practices, accountants and tax advisors can prepare robust transfer pricing documentation that withstands scrutiny and supports effective tax compliance.

3.5 Practical Example: Calculating Arm’s Length Price for Intercompany Sale

Introduction

In transfer pricing, the Arm’s Length Principle requires that transactions between related entities be priced as if they were between independent parties under similar circumstances. Calculating the arm’s length price for an intercompany sale ensures compliance and minimizes tax risks.

Step-by-Step Approach to Calculate Arm’s Length Price

-

Identify the Controlled Transaction

- Intercompany sale of goods or services

-

Select the Most Appropriate Transfer Pricing Method

- Comparable Uncontrolled Price (CUP) Method

- Resale Price Method

- Cost Plus Method

- Transactional Net Margin Method (TNMM)

- Profit Split Method

-

Search for Comparable Uncontrolled Transactions

- External market prices

- Internal comparable transactions

-

Adjust Comparables for Differences

- Product differences

- Contractual terms

- Economic circumstances

-

Determine the Arm’s Length Range and Price

Mind Map: Transfer Pricing Method Selection

Practical Example Scenario

Company A (Parent) sells electronic components to its subsidiary, Company B, at an intercompany price. The goal is to determine the arm’s length price for this sale.

- Product: Electronic components

- Quantity: 10,000 units

- Cost to Company A: $50 per unit

- Comparable uncontrolled sales found:

- Company C sells similar components to unrelated parties at $70 per unit

- Adjustments needed for volume and contract terms

Applying the Cost Plus Method

- Determine Cost Base: $50 per unit

- Identify Appropriate Markup: Comparable companies earn a gross margin of 30%

- Calculate Arm’s Length Price:

- Price = Cost + (Cost × Markup)

- Price = $50 + ($50 × 0.30) = $65 per unit

Mind Map: Cost Plus Method Calculation

Applying the Comparable Uncontrolled Price (CUP) Method

- Comparable Price: $70 per unit from Company C

- Adjustments: Volume discount of 5% due to larger quantity

- Adjusted Price:

- $70 - (5% of $70) = $66.50 per unit

Mind Map: CUP Method Calculation

Conclusion: Determining the Arm’s Length Range

- Cost Plus Method Price: $65/unit

- CUP Method Price: $66.50/unit

Arm’s Length Range: $65 - $66.50 per unit

Company A and B can set the intercompany sale price within this range to comply with transfer pricing regulations.

Best Practices

- Use multiple methods to cross-verify results.

- Document all assumptions and adjustments clearly.

- Regularly update comparables to reflect market changes.

- Maintain detailed transfer pricing documentation.

This example illustrates how accountants and tax advisors can pragmatically apply transfer pricing principles to calculate arm’s length prices, ensuring compliance and minimizing tax risks.

4. Permanent Establishment (PE) Rules

4.1 Defining Permanent Establishment in International Tax Law

Permanent Establishment (PE) is a fundamental concept in international taxation that determines when a business has a taxable presence in a foreign country. Understanding PE is crucial for accountants and tax advisors because it triggers tax obligations in jurisdictions where a multinational enterprise (MNE) operates.

What is a Permanent Establishment?

A Permanent Establishment is generally defined as a fixed place of business through which the business of an enterprise is wholly or partly carried on. The concept is primarily governed by Article 5 of the OECD Model Tax Convention, which serves as a guideline for many countries’ tax treaties.

Key Elements of PE:

- Fixed Place: There must be a physical location with a certain degree of permanence.

- Business Activity: The enterprise must conduct business activities through that place.

- Duration: The presence should not be temporary; usually, a minimum period is considered.

Mind Map: Core Elements of Permanent Establishment

Types of Permanent Establishment

- Fixed Place PE: A physical location such as an office, factory, or workshop.

- Agency PE: When a dependent agent has authority to conclude contracts on behalf of the enterprise.

- Construction PE: A building site or construction project lasting beyond a specified duration (commonly 12 months).

Mind Map: Types of Permanent Establishment

Practical Examples

Example 1: Fixed Place PE

A German company opens an office in Brazil where it employs staff to negotiate and conclude contracts. The office is used continuously for over a year.

- Analysis: The office is a fixed place of business.

- Conclusion: The German company has a PE in Brazil and must pay Brazilian corporate tax on income attributable to that PE.

Example 2: Agency PE

A French company sells products in Canada through a dependent sales agent who has authority to negotiate and finalize contracts on behalf of the company.

- Analysis: The agent’s authority and dependency create an agency PE.

- Conclusion: The French company is taxable in Canada on income related to the agent’s activities.

Example 3: Construction PE

An Indian construction firm undertakes a building project in the UK lasting 14 months.

- Analysis: The project exceeds the 12-month threshold.

- Conclusion: The firm has a construction PE in the UK and must comply with UK tax obligations.

Exclusions and Exceptions

Certain activities do not create a PE even if conducted through a fixed place of business. These generally include:

- Storage, display, or delivery of goods

- Use of facilities solely for purchasing or collecting information

- Activities that are preparatory or auxiliary in nature

Mind Map: Activities Excluded from PE Definition

Best Practices for Accountants and Tax Advisors

- Review Contracts and Business Operations: Identify if the client’s activities abroad meet PE criteria.

- Assess Physical Presence: Determine if there is a fixed place of business.

- Evaluate Agent Relationships: Check if agents have authority to bind the company.

- Monitor Project Durations: Track construction or installation projects for PE thresholds.

- Document Activities: Maintain clear records to support PE status or exclusions.

Summary

Permanent Establishment is a key concept that triggers tax liabilities in foreign jurisdictions. Accountants must carefully analyze the nature, location, and duration of business activities abroad to determine PE status. Applying the OECD guidelines and local tax treaty provisions helps ensure compliance and optimize tax positions.

4.2 Types of Permanent Establishments and Their Tax Implications

Permanent Establishment (PE) is a critical concept in international taxation, as it determines when a business has sufficient presence in a foreign country to be subject to tax there. Understanding the different types of PEs and their tax implications helps accountants and tax advisors manage cross-border tax risks effectively.

Types of Permanent Establishments

Below is a detailed breakdown of the main types of PEs recognized under the OECD Model Tax Convention and many domestic tax laws, along with their tax implications.

Fixed Place of Business PE

This is the most common type of PE and arises when a company has a fixed physical location through which it carries out business activities.

- Examples include:

- Office

- Branch

- Factory

- Workshop

Tax Implications:

- Profits attributable to the fixed place of business are taxable in the host country.

- Requires proper allocation of income and expenses to the PE.

Mind Map:

Example: A German company opens an office in France where it negotiates and concludes contracts. This office constitutes a fixed place of business PE in France, and the profits attributable to this office are taxable in France.

Construction or Installation PE

This PE arises from a building site, construction, assembly, or installation project lasting more than a specified period (usually 6-12 months).

Tax Implications:

- Income from the construction project is taxable in the host country.

- Duration thresholds vary by jurisdiction and treaty.

Mind Map:

Example: A Canadian engineering firm undertakes a 10-month construction project in Brazil. Since the project exceeds the 6-month threshold, the firm has a construction PE in Brazil and must pay tax on profits attributable to this project.

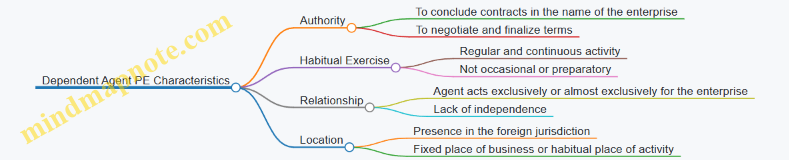

Agency PE

Occurs when a dependent agent has authority to conclude contracts on behalf of the foreign enterprise.

- Dependent agent: an individual or entity acting under the control of the foreign company.

- Independent agents (e.g., brokers) generally do not create a PE.

Tax Implications:

- The foreign company is taxed on profits attributable to contracts concluded by the agent.

Mind Map:

Example: A Japanese company appoints a sales representative in Italy who regularly signs contracts on its behalf. This creates an agency PE in Italy, and the Japanese company must pay tax on income generated through these contracts.

Service PE

Some treaties recognize a service PE when services are performed in a country for a certain period (e.g., more than 183 days within 12 months).

Tax Implications:

- Income attributable to services performed in the host country is taxable there.

Mind Map:

Example: An Australian consultancy provides advisory services in South Africa for 200 days in a year. This triggers a service PE, and South Africa can tax the income attributable to these services.

Subsidiary PE (Special Cases)

While a subsidiary is generally a separate legal entity, in some cases, a subsidiary’s activities can create a PE for the parent company, especially if the subsidiary acts as an agent.

Tax Implications:

- Parent company may be taxed on profits attributable to the subsidiary’s activities if agency PE rules apply.

Mind Map:

Example: A US parent company’s wholly owned subsidiary in Mexico signs contracts on behalf of the parent. The parent company may have an agency PE in Mexico.

Summary Mind Map: Types of PE and Tax Implications

Best Practices for Accountants and Tax Advisors

- Identify PE early: Analyze client activities in foreign jurisdictions to detect potential PEs.

- Understand treaty provisions: Review relevant tax treaties for specific PE definitions and thresholds.

- Document activities: Maintain detailed records of foreign operations, contracts, and agent roles.

- Allocate profits correctly: Use transfer pricing principles to attribute profits to the PE.

- Monitor duration thresholds: Especially for construction and service PEs.

Additional Practical Example

Scenario: A UK-based software company sends a team to Germany for 7 months to install and customize software at a client’s premises.

Analysis:

- The installation activity may create a construction or installation PE if the treaty threshold is exceeded.

- The company must evaluate the local treaty and domestic law to determine if a PE exists.

- If a PE exists, profits attributable to this activity are taxable in Germany.

This example highlights the importance of understanding PE types and their tax consequences to advise clients properly and ensure compliance.

4.3 Identifying PE Risks for Multinational Clients

Permanent Establishment (PE) is a critical concept in international taxation that determines whether a business has a taxable presence in a foreign jurisdiction. For accountants and tax advisors, identifying PE risks is essential to ensure compliance and optimize tax liabilities for multinational clients.

What Constitutes a Permanent Establishment?

A PE generally refers to a fixed place of business through which the business of an enterprise is wholly or partly carried on. Common examples include offices, branches, factories, and construction sites.

Key Factors to Identify PE Risks

- Fixed Place of Business: Is there a physical location with a degree of permanence?

- Duration: Does the activity last beyond a certain period (usually 6-12 months depending on jurisdiction)?

- Business Activity: Are core business activities being conducted at the location?

- Dependent Agents: Are there agents acting on behalf of the company with authority to conclude contracts?

Mind Map: Core Elements of PE Risk Identification

Best Practices for Identifying PE Risks

-

Conduct a Thorough Business Activity Review: Analyze the client’s operations in each jurisdiction to determine if activities go beyond preparatory or auxiliary.

-

Map Physical Presence: Document all locations where the client has employees, offices, or other facilities.

-

Evaluate Contractual Authority: Identify any agents or employees with authority to negotiate or conclude contracts.

-

Review Duration of Activities: Track how long activities have been conducted in the foreign jurisdiction.

-

Leverage Local Tax Laws and Treaties: Understand specific PE definitions and thresholds in relevant tax treaties.

Practical Example 1: Sales Representative Creating PE Risk

Scenario: A multinational company appoints a sales representative in Country A. The representative has authority to negotiate and conclude contracts on behalf of the company.

Analysis: Since the agent has authority to conclude contracts habitually, this creates a dependent agent PE in Country A.

Implication: The company may be subject to corporate tax in Country A on profits attributable to the PE.

Practical Example 2: Temporary Construction Site

Scenario: A construction company from Country B undertakes a project in Country C lasting 10 months.

Analysis: Many tax treaties consider construction sites as PEs if they last more than 6-12 months. Since the project exceeds this threshold, a PE is created.

Implication: The company must report and pay tax on income attributable to the construction site in Country C.

Mind Map: Steps to Assess PE Risk for a Client

Summary

Identifying PE risks requires a detailed understanding of the client’s international footprint, activities, and local tax laws. By systematically evaluating physical presence, agent authority, duration, and business activities, accountants can proactively manage PE exposure and ensure compliance.

For further reading, refer to OECD Model Tax Convention Article 5 on Permanent Establishment and local tax authority guidelines.

4.4 Best Practices for Managing and Mitigating PE Exposure

Managing Permanent Establishment (PE) exposure is critical for multinational corporations to avoid unexpected tax liabilities and compliance risks. Below are best practices that accountants and tax advisors should follow, along with practical examples and mind maps to visualize the concepts.

Best Practices for Managing and Mitigating PE Exposure

-

Understand the PE Definitions in Relevant Jurisdictions and Treaties

- Carefully analyze domestic tax laws and applicable Double Taxation Avoidance Agreements (DTAAs) to identify what constitutes a PE.

- Pay special attention to agency PE, construction PE, and service PE definitions.

-

Conduct a Thorough PE Risk Assessment

- Map out business activities in each jurisdiction.

- Identify any fixed place of business, dependent agents, or significant economic presence.

- Use checklists to assess potential PE triggers.

-

Structure Business Activities to Avoid PE Creation

- Limit the duration and nature of activities in foreign jurisdictions.

- Use independent agents instead of dependent agents.

- Avoid fixed places of business or ensure they fall outside PE definitions.

-

Implement Robust Contractual Arrangements

- Clearly define the role and independence of agents.

- Specify that agents do not have authority to conclude contracts on behalf of the company.

-

Monitor and Document Activities Continuously

- Maintain detailed records of personnel, contracts, and business operations abroad.

- Document the nature and duration of activities to demonstrate absence of PE.

-

Engage in Proactive Communication with Tax Authorities

- Where uncertainty exists, seek advance rulings or clarifications.

- Use mutual agreement procedures (MAP) to resolve PE disputes.

-

Leverage Technology for PE Monitoring

- Use software tools to track employee locations, contract signings, and business presence.

Mind Map: Managing and Mitigating PE Exposure

Practical Example 1: Avoiding PE through Independent Agent Usage

Scenario: A US-based software company wants to expand sales in Germany. Instead of sending employees who might create a PE, the company contracts with an independent German sales agent.

Best Practice Applied: The company ensures the agent operates independently, does not have authority to conclude contracts, and is responsible for their own expenses.

Outcome: Since the agent is independent and does not create a dependent agent PE, the US company avoids having a PE in Germany, thus minimizing tax exposure.

Practical Example 2: Monitoring Construction PE Duration

Scenario: A Canadian construction firm undertakes a project in Brazil expected to last 10 months.

Best Practice Applied: The firm monitors the project duration carefully. Since Brazilian tax law defines a construction PE as lasting more than 6 months, the firm plans to split the project into two phases with a break exceeding 6 months.

Outcome: By structuring the project timeline, the firm avoids creating a continuous PE in Brazil, reducing permanent tax obligations.

Mind Map: PE Risk Assessment Process

Summary

Effectively managing and mitigating PE exposure requires a deep understanding of tax laws, proactive structuring of business operations, continuous monitoring, and clear documentation. By applying these best practices, accountants and tax advisors can help their clients minimize international tax risks and optimize compliance.

4.5 Practical Example: Assessing PE Status for a Sales Representative Abroad

Introduction

Permanent Establishment (PE) status is a critical concept in international taxation, as it determines whether a foreign entity has sufficient taxable presence in another country. This section provides a detailed example of assessing PE status for a sales representative working abroad, illustrating key considerations and best practices.

Scenario Overview

A multinational company, GlobalTech Inc., headquartered in Country A, sends a sales representative to Country B to promote and secure sales contracts. The company wants to determine if the sales representative’s activities create a PE in Country B, which would subject GlobalTech Inc. to corporate tax obligations there.

Step 1: Understand the Definition of PE

According to the OECD Model Tax Convention, a PE generally exists if a foreign enterprise has a fixed place of business through which it carries out business activities in another country. Additionally, a dependent agent who habitually concludes contracts on behalf of the enterprise can create a PE.

Step 2: Analyze the Sales Representative’s Activities

- Does the sales representative have a fixed place of business in Country B?

- Is the sales representative an independent agent or a dependent agent?

- Does the sales representative habitually conclude contracts or play a principal role in concluding contracts?

Mind Map: Key Factors in PE Assessment

Step 3: Apply to the Example

- The sales representative works from a rented office in Country B for 8 months.

- The representative negotiates and signs sales contracts on behalf of GlobalTech Inc.

- The representative is exclusively employed by GlobalTech Inc. and does not act independently.

Step 4: Determine PE Status

Based on the above:

- Fixed place of business: Yes (rented office)

- Dependent agent: Yes (exclusively employed)

- Habitually concludes contracts: Yes (signs contracts)

Conclusion: GlobalTech Inc. has a PE in Country B.

Step 5: Best Practices for Accountants

- Document Activities: Keep detailed records of the agent’s activities, location, and contract authority.

- Review Contracts: Clearly define the agent’s authority in contracts to manage PE risk.

- Consult Tax Treaties: Some treaties provide specific definitions or exemptions for PEs.

- Regular Assessment: Periodically reassess PE status as business operations evolve.

Additional Example: No PE Scenario

If the sales representative only performs preparatory or auxiliary activities (e.g., market research, advertising) and does not conclude contracts, even if present for a long time, no PE is created.

Mind Map: PE vs. No PE Decision Flow

Summary

Assessing PE status requires careful analysis of the agent’s role, authority, and place of business. Accountants and tax advisors should use structured frameworks and maintain thorough documentation to manage international tax risks effectively.

References

- OECD Model Tax Convention on Income and on Capital

- Country B’s domestic tax laws and relevant tax treaty with Country A

5. Cross-Border Withholding Taxes

5.1 Understanding Withholding Taxes on Dividends, Interest, and Royalties

Withholding tax (WHT) is a critical concept in international taxation, especially for accountants and tax advisors managing cross-border transactions. It refers to the tax withheld at the source on certain types of income paid to non-residents, such as dividends, interest, and royalties. Understanding how WHT works, its rates, exemptions, and treaty benefits is essential for minimizing tax leakage and ensuring compliance.

What is Withholding Tax?

Withholding tax is a mechanism used by countries to collect tax on income earned by non-residents within their jurisdiction. Instead of the recipient paying tax directly, the payer deducts the tax at source and remits it to the tax authorities.

- Purpose: Prevent tax evasion and ensure tax collection on cross-border payments.

- Commonly Withheld On: Dividends, interest, royalties, fees for technical services, and sometimes capital gains.

Mind Map: Withholding Tax Basics

Withholding Tax on Dividends

Dividends paid by a company to a foreign shareholder are often subject to withholding tax in the source country.

- Typical Rates: Vary widely, often between 5% to 30%.

- Example: Country A imposes a 15% WHT on dividends paid to non-residents.

- Treaty Impact: Tax treaties may reduce this rate, sometimes to as low as 5% or even 0%.

Example:

A company in Country A pays $10,000 in dividends to a shareholder in Country B. The domestic WHT rate is 15%, but a tax treaty between Country A and B reduces it to 5%.

- Without treaty: $10,000 x 15% = $1,500 withheld

- With treaty: $10,000 x 5% = $500 withheld

This reduces the shareholder’s tax burden and improves cross-border investment attractiveness.

Withholding Tax on Interest

Interest payments made to foreign lenders or investors are also commonly subject to withholding tax.

- Purpose: Tax the income earned by foreign creditors.

- Typical Rates: Usually lower than dividends, often around 10% or less.

- Exceptions: Some countries exempt interest on government bonds or certain bank deposits.

Example:

A multinational corporation in Country X pays $20,000 interest to a lender in Country Y. The domestic WHT rate is 10%, but a tax treaty reduces it to 0% for interest on loans exceeding 5 years.

- Without treaty: $20,000 x 10% = $2,000 withheld

- With treaty (loan > 5 years): $20,000 x 0% = $0 withheld

This encourages long-term financing from foreign lenders.

Withholding Tax on Royalties

Royalties are payments for the use of intellectual property (IP), trademarks, patents, copyrights, or know-how.

- Typical Rates: Can range from 10% to 30%, depending on the country.

- Tax Treaty Role: Often reduce rates significantly or provide exemptions.

Example:

A software company in Country M licenses its software to a company in Country N and receives $15,000 in royalties. Country N imposes a 20% WHT on royalties, but a treaty reduces it to 10%.

- Without treaty: $15,000 x 20% = $3,000 withheld

- With treaty: $15,000 x 10% = $1,500 withheld

Mind Map: Types of Income Subject to Withholding Tax

Best Practices for Accountants and Tax Advisors

- Identify Applicable WHT Rates: Always check domestic laws and applicable tax treaties.

- Review Tax Treaty Provisions: Understand reduced rates or exemptions and the conditions to qualify.

- Ensure Proper Documentation: Collect certificates of residency and treaty forms to claim benefits.

- Monitor Compliance Deadlines: Timely withholding and remittance avoid penalties.

- Plan Transactions: Structure payments to optimize WHT exposure.

Practical Example: Applying Withholding Tax on Cross-Border Dividend Payment

Scenario:

An accountant is advising a client, a company in Country Z, which plans to distribute dividends of $50,000 to a foreign shareholder in Country Q. Country Z’s domestic WHT rate on dividends is 25%. However, Country Z has a tax treaty with Country Q that reduces the WHT rate to 10%.

Steps:

- Verify the shareholder’s tax residency with a valid certificate.

- Confirm eligibility under the treaty (e.g., minimum shareholding percentage).

- Apply the reduced WHT rate of 10%.

Calculation:

- WHT = $50,000 x 10% = $5,000

- Net dividend to shareholder = $45,000

Outcome:

The shareholder benefits from treaty relief, reducing tax withheld by $7,500 compared to the domestic rate.

Summary

Understanding withholding taxes on dividends, interest, and royalties is vital for accountants and tax advisors working in international business. Proper application of domestic laws and tax treaties can significantly reduce tax costs and improve compliance. Utilizing clear documentation, staying updated on treaty changes, and advising clients on structuring payments are best practices that ensure efficient tax management.

For further reading, consult OECD’s Model Tax Convention and local tax authority guidelines on withholding taxes.

5.2 How to Apply Reduced Withholding Tax Rates under Tax Treaties

When dealing with cross-border payments such as dividends, interest, and royalties, withholding tax is often levied by the source country. However, many countries have entered into Double Taxation Avoidance Agreements (DTAAs) or tax treaties that provide for reduced withholding tax rates or exemptions to avoid double taxation and encourage cross-border investment.

Understanding the Basics

- Withholding Tax (WHT): Tax deducted at source on certain types of income paid to non-residents.

- Tax Treaty: An agreement between two countries that defines taxing rights and often reduces withholding tax rates.