Strategic Cost Management

1. Introduction to Strategic Cost Management

1.1 Understanding the Fundamentals of Cost Management

Cost management is a critical discipline within finance and manufacturing that focuses on planning, controlling, and reducing business expenses to maximize profitability and operational efficiency. At its core, cost management ensures that resources are used effectively to achieve organizational goals without unnecessary expenditure.

What is Cost Management?

Cost management involves a series of processes that help organizations estimate, allocate, and control costs throughout the lifecycle of a product or service. It encompasses budgeting, cost control, cost reduction, and cost forecasting.

Key Components of Cost Management

Why is Cost Management Important?

- Profitability: Helps maintain or increase profit margins by managing expenses.

- Resource Allocation: Ensures optimal use of resources.

- Decision-Making: Provides data-driven insights for strategic decisions.

- Competitive Advantage: Enables pricing strategies and cost leadership.

Types of Costs in Cost Management

Understanding the types of costs is fundamental to managing them effectively.

Example: Understanding Cost Types in a Manufacturing Setting

Imagine a factory producing electronic gadgets:

- Fixed Costs: The monthly rent of the factory is $10,000, which remains constant regardless of production volume.

- Variable Costs: Each gadget requires $15 worth of raw materials; producing more gadgets increases this cost.

- Semi-Variable Costs: Electricity bills vary with production but have a base charge.

- Direct Costs: Components like microchips and screens directly tied to each unit.

- Indirect Costs: Factory manager’s salary and maintenance expenses.

The Cost Management Cycle

Practical Example: Cost Management in Action

A manufacturing company sets a budget of $500,000 for raw materials for the quarter. During the quarter, actual spending is tracked weekly. At mid-quarter, the company notices a 10% overspend due to supplier price increases. Using variance analysis, the cost manager identifies the issue and negotiates better terms with suppliers and adjusts production schedules to optimize material usage, bringing costs back in line with the budget.

Summary

Understanding the fundamentals of cost management equips accountants and cost managers with the tools to plan, monitor, and control costs effectively. By classifying costs correctly and following a structured cost management cycle, organizations can improve profitability and maintain competitive advantage.

Next up: 1.2 The Role of Strategic Cost Management in Finance and Manufacturing

1.2 The Role of Strategic Cost Management in Finance and Manufacturing

Strategic Cost Management (SCM) plays a pivotal role in both finance and manufacturing sectors by enabling organizations to optimize costs while aligning with their long-term business objectives. Unlike traditional cost control, which focuses on short-term expense reduction, SCM integrates cost considerations into strategic decision-making processes, ensuring sustainable profitability and competitive advantage.

Why is Strategic Cost Management Important?

- Aligns Costs with Business Strategy: Ensures that cost structures support the company’s strategic goals.

- Enhances Decision-Making: Provides detailed cost insights that inform pricing, product mix, and investment decisions.

- Drives Continuous Improvement: Encourages ongoing analysis and refinement of cost drivers.

- Supports Competitive Advantage: Helps companies reduce waste and improve efficiency to outperform competitors.

Mind Map: Role of Strategic Cost Management

Strategic Cost Management in Finance

In finance, SCM helps accountants and cost managers to:

- Develop Accurate Budgets: By understanding cost drivers, finance teams can create realistic budgets that reflect operational realities.

- Perform Variance Analysis: Identifying deviations from planned costs enables timely corrective actions.

- Optimize Capital Allocation: Ensures funds are invested in projects with the best cost-benefit profiles.

- Improve Financial Reporting: Detailed cost insights improve transparency and compliance.

Example: A multinational manufacturing company’s finance team used SCM to analyze overhead costs across different plants. By identifying plants with disproportionately high indirect costs, they reallocated resources and renegotiated service contracts, resulting in a 10% reduction in overhead expenses.

Strategic Cost Management in Manufacturing

In manufacturing, SCM focuses on controlling and reducing production-related costs without compromising quality:

- Optimizing Production Processes: Identifying bottlenecks and inefficiencies to reduce cycle times and costs.

- Inventory Management: Implementing Just-In-Time (JIT) to minimize holding costs.

- Supplier Cost Management: Collaborating with suppliers to reduce material costs.

- Product Design Influence: Incorporating cost considerations early in product development to avoid expensive redesigns.

Example: A car manufacturer applied SCM principles by adopting lean manufacturing techniques. They mapped their value stream and eliminated non-value-adding activities, reducing production costs by 12% while maintaining product quality.

Integrated Role Across Finance and Manufacturing

SCM bridges finance and manufacturing by fostering collaboration and shared goals:

- Finance provides cost data and analysis to manufacturing teams.

- Manufacturing offers operational insights to finance for better forecasting.

- Joint initiatives such as cost reduction programs and investment appraisals ensure alignment.

Mind Map: Integrated SCM Benefits

Summary

Strategic Cost Management is essential for accountants and cost managers in finance and manufacturing to drive cost efficiency, support strategic goals, and maintain competitiveness. By understanding and managing costs strategically, organizations can achieve sustainable growth and operational excellence.

1.3 Key Objectives and Benefits of Strategic Cost Management

Strategic Cost Management (SCM) is a vital approach that goes beyond traditional cost control by aligning cost management efforts with the overall strategic goals of an organization. It enables finance professionals and cost managers in manufacturing to make informed decisions that enhance competitiveness, profitability, and operational efficiency.

Key Objectives of Strategic Cost Management

-

Optimize Cost Efficiency

- Identify and eliminate non-value-added activities

- Streamline processes to reduce waste and inefficiencies

-

Enhance Decision-Making

- Provide accurate cost data for pricing, budgeting, and investment decisions

- Support scenario analysis and forecasting

-

Align Costs with Strategic Goals

- Ensure cost structures support long-term business objectives

- Facilitate cost leadership or differentiation strategies

-

Improve Profitability and Competitiveness

- Reduce product and operational costs without compromising quality

- Enable competitive pricing and margin improvement

-

Drive Continuous Improvement

- Foster a culture of cost awareness and accountability

- Encourage innovation in cost-saving initiatives

Benefits of Strategic Cost Management

-

Better Resource Allocation

- Resources are directed to high-impact areas, improving ROI

-

Increased Transparency and Control

- Clear visibility into cost drivers and variances

-

Enhanced Collaboration Across Departments

- Cross-functional teams work together to identify cost-saving opportunities

-

Risk Mitigation

- Early identification of cost-related risks and proactive management

-

Sustainable Cost Reduction

- Focus on long-term cost improvements rather than short-term cuts

Mind Map: Objectives of Strategic Cost Management

Mind Map: Benefits of Strategic Cost Management

Practical Example: Strategic Cost Management in Action

Scenario: A mid-sized manufacturing company producing automotive parts was facing shrinking profit margins due to rising raw material costs and inefficient production processes.

Application of SCM:

- Cost Driver Analysis: The cost manager identified that excessive machine downtime and high scrap rates were major cost drivers.

- Process Optimization: Implemented lean manufacturing principles to reduce downtime by scheduling preventive maintenance and improving operator training.

- Supplier Collaboration: Negotiated with suppliers for better pricing and just-in-time delivery to reduce inventory holding costs.

- Decision Support: Used detailed cost data to adjust product pricing strategically without losing market competitiveness.

Outcome: Within one year, the company reduced overall production costs by 12%, improved profit margins by 8%, and enhanced operational efficiency.

Strategic Cost Management is not just about cutting costs; it is about managing costs intelligently to support and drive the strategic vision of the company. For accountants and cost managers, mastering SCM means becoming a strategic partner in the organization’s success.

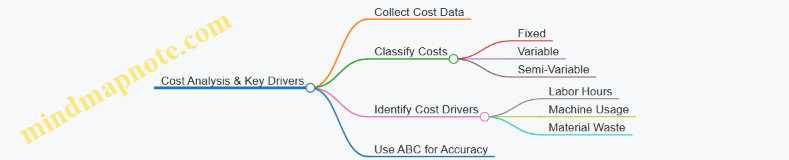

1.4 Overview of Cost Behavior and Cost Drivers with Practical Examples

Understanding cost behavior and cost drivers is fundamental for accountants and cost managers aiming to optimize financial performance in manufacturing and finance sectors. This section explores these concepts with clear explanations, mind maps, and practical examples.

What is Cost Behavior?

Cost behavior refers to how costs change in response to variations in business activity levels. It helps managers predict costs and make informed decisions.

Main types of cost behavior:

- Fixed Costs: Costs that remain constant regardless of production volume.

- Variable Costs: Costs that vary directly with production volume.

- Semi-Variable (Mixed) Costs: Costs that have both fixed and variable components.

Mind Map: Types of Cost Behavior

Practical Examples of Cost Behavior

-

Fixed Cost Example:

- A manufacturing plant pays $10,000 monthly rent regardless of how many units it produces. Whether producing 1,000 or 10,000 units, rent remains $10,000.

-

Variable Cost Example:

- Raw material cost is $5 per unit. Producing 1,000 units costs $5,000; producing 2,000 units costs $10,000.

-

Semi-Variable Cost Example:

- Electricity bill includes a $500 fixed charge plus $0.10 per kWh used. If the plant uses 4,000 kWh, total cost = $500 + (4,000 x $0.10) = $900.

What are Cost Drivers?

Cost drivers are factors that cause changes in the cost of an activity. Identifying cost drivers helps in managing and controlling costs effectively.

Common cost drivers in manufacturing and finance:

- Production volume

- Number of setups

- Machine hours

- Number of purchase orders

- Inspection hours

Mind Map: Common Cost Drivers

Practical Examples of Cost Drivers

-

Production Volume as a Cost Driver:

- More units produced increase raw material consumption and direct labor hours.

-

Machine Hours as a Cost Driver:

- Maintenance costs increase with more machine operating hours.

-

Number of Setups as a Cost Driver:

- Each production setup requires labor and downtime, increasing setup costs.

-

Number of Purchase Orders as a Cost Driver:

- More purchase orders increase administrative costs in the finance department.

Integrated Example: Applying Cost Behavior and Cost Drivers

A company manufactures widgets. The following costs are observed:

- Rent: $12,000/month (Fixed Cost)

- Raw materials: $4/unit (Variable Cost, driven by production volume)

- Machine maintenance: $1,000 base + $50 per 100 machine hours (Semi-Variable Cost, driven by machine hours)

- Setup costs: $200 per setup (Variable Cost, driven by number of setups)

Scenario:

- Production volume: 2,000 units

- Machine hours: 400 hours

- Number of setups: 5

Cost calculation:

- Rent: $12,000

- Raw materials: 2,000 units x $4 = $8,000

- Machine maintenance: $1,000 + (400/100 x $50) = $1,000 + $200 = $1,200

- Setup costs: 5 x $200 = $1,000

Total Cost: $12,000 + $8,000 + $1,200 + $1,000 = $22,200

This example shows how understanding cost behavior and drivers enables accurate cost estimation and better budgeting.

Summary

- Cost behavior helps predict how costs change with activity levels.

- Cost drivers identify what causes costs to change.

- Combining both concepts allows for precise cost control and strategic decision-making.

For accountants and cost managers, mastering these concepts with practical application is key to driving efficiency and profitability in finance and manufacturing sectors.

1.5 Case Study: How a Manufacturing Firm Reduced Costs by 15% Using Strategic Cost Management

Background

A mid-sized manufacturing firm specializing in consumer electronics faced increasing pressure from competitors and shrinking profit margins. The CFO tasked the finance and cost management teams to implement a strategic cost management initiative aimed at reducing overall costs by at least 15% within one fiscal year without compromising product quality.

Step 1: Comprehensive Cost Analysis

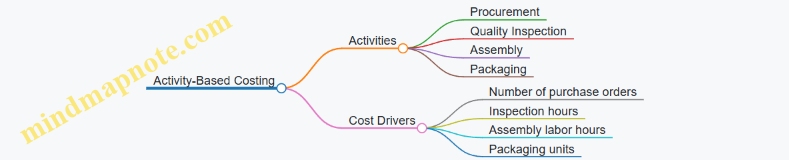

The firm began by mapping out all cost elements using Activity-Based Costing (ABC) to identify high-cost activities and cost drivers.

Mind Map: Cost Analysis Using ABC

Example:

- The ABC analysis revealed that machine setup times were disproportionately high, causing increased labor and downtime costs.

Step 2: Cost Planning and Target Setting

Using insights from the cost analysis, the team set specific cost reduction targets for each department aligned with overall strategic goals.

Mind Map: Cost Planning and Target Setting

Example:

- The production department was tasked with reducing machine setup time by 20%, translating into labor cost savings.

Step 3: Implementing Cost Control Measures

The firm introduced several best practices:

- Lean Manufacturing: Streamlined workflows to eliminate waste.

- Just-In-Time (JIT) Inventory: Reduced inventory holding costs.

- Supplier Negotiations: Leveraged volume discounts and long-term contracts.

Mind Map: Cost Control Measures

Example:

- By adopting JIT, the firm reduced raw material inventory by 30%, freeing up working capital and reducing storage costs.

Step 4: Monitoring and Continuous Improvement

The firm established KPIs and regular variance analysis to track cost performance.

Mind Map: Monitoring and Continuous Improvement

Example:

- Monthly variance reports highlighted a spike in utility costs; investigation led to implementing energy-saving equipment, reducing utility expenses by 8%.

Results

- Overall cost reduction achieved: 15.3%

- Improved production efficiency by 18%

- Inventory turnover improved by 25%

- Enhanced supplier relationships leading to better payment terms

Key Takeaways

- Strategic cost management requires a holistic approach combining analysis, planning, implementation, and monitoring.

- Activity-Based Costing is invaluable for pinpointing cost drivers.

- Lean and JIT principles can significantly reduce waste and inventory costs.

- Continuous monitoring ensures sustainability of cost savings.

This case exemplifies how accountants and cost managers in manufacturing can drive significant cost savings through strategic initiatives integrated across departments.

2. Cost Analysis and Classification Techniques

2.1 Direct vs Indirect Costs: Definitions and Examples

Understanding Direct Costs

Direct costs are expenses that can be directly traced to a specific cost object, such as a product, project, or department. These costs are incurred exclusively for that particular item and vary in direct proportion to the level of production or activity.

Examples of Direct Costs:

- Raw materials used in manufacturing a product

- Direct labor wages for workers assembling a product

- Components or parts purchased specifically for a product

Mind Map: Direct Costs

Understanding Indirect Costs

Indirect costs are expenses that cannot be directly traced to a single cost object. Instead, they support multiple products, projects, or departments and are often called overhead costs. These costs are necessary for overall operations but are allocated across different cost centers.

Examples of Indirect Costs:

- Factory rent and utilities

- Salaries of supervisors and maintenance staff

- Depreciation of equipment used across multiple products

- Office supplies and administrative expenses

Mind Map: Indirect Costs

Key Differences Between Direct and Indirect Costs

| Aspect | Direct Costs | Indirect Costs |

|---|---|---|

| Traceability | Easily traced to a specific product | Cannot be traced to a single product |

| Variability | Varies directly with production | Often fixed or semi-variable |

| Examples | Raw materials, direct labor | Rent, utilities, administrative salaries |

Practical Example in Manufacturing

Consider a company manufacturing custom furniture:

- Direct Costs: Wood, nails, varnish, and wages paid to carpenters working on a specific table.

- Indirect Costs: Factory rent, electricity, salaries of security personnel, and depreciation on woodworking machines.

The cost accountant allocates indirect costs proportionally to each product line based on machine hours or labor hours.

Mind Map: Direct vs Indirect Costs Overview

Best Practice for Accountants and Cost Managers

- Accurate Identification: Clearly distinguish direct from indirect costs to improve cost allocation accuracy.

- Use Activity-Based Costing (ABC): Helps allocate indirect costs based on actual activities driving the costs.

- Regular Review: Periodically review cost classifications as operational changes may shift cost behavior.

Summary

Understanding the distinction between direct and indirect costs is fundamental for effective cost management. It enables precise cost tracking, budgeting, and pricing decisions, especially in manufacturing environments where cost control is critical.

2.2 Fixed, Variable, and Semi-Variable Costs Explained with Manufacturing Scenarios

Understanding the nature of costs is fundamental for accountants and cost managers in manufacturing. Costs can be broadly classified into three categories: fixed, variable, and semi-variable (also called mixed costs). Each type behaves differently with changes in production volume, and recognizing these behaviors helps in budgeting, forecasting, and strategic decision-making.

Fixed Costs

Definition: Fixed costs remain constant in total regardless of the level of production or output within a relevant range.

Examples in Manufacturing:

- Factory rent

- Salaries of permanent staff

- Depreciation of machinery

- Property taxes

Scenario: A manufacturing plant pays $10,000 monthly rent for its facility. Whether the plant produces 1,000 units or 10,000 units, the rent remains $10,000.

Mind Map:

Variable Costs

Definition: Variable costs change in direct proportion to the level of production.

Examples in Manufacturing:

- Raw materials

- Direct labor (if paid hourly or per unit)

- Packaging costs

- Utilities directly tied to production (e.g., electricity for machines)

Scenario: If producing one widget requires $5 worth of raw materials, producing 1,000 widgets will cost $5,000 in raw materials, and producing 2,000 widgets will cost $10,000.

Mind Map:

Semi-Variable (Mixed) Costs

Definition: Semi-variable costs have both fixed and variable components. They remain partially fixed but vary with production volume beyond a certain threshold.

Examples in Manufacturing:

- Utility bills (fixed base charge + variable usage charge)

- Maintenance costs (fixed contract fee + variable repair costs)

- Salaries with overtime (fixed salary + overtime pay)

Scenario: A factory pays a monthly electricity bill with a fixed charge of $1,000 plus $0.10 per kWh consumed. If production increases, electricity usage and thus the variable portion of the bill increase.

Mind Map:

Integrated Example: Widget Manufacturing Plant

| Cost Type | Description | Cost Behavior Example |

|---|---|---|

| Fixed Cost | Factory rent | $10,000/month regardless of output |

| Variable Cost | Raw materials | $5 per widget produced |

| Semi-Variable | Electricity bill | $1,000 fixed + $0.10 per kWh consumed |

Scenario:

-

Producing 1,000 widgets:

- Rent: $10,000

- Raw materials: 1,000 x $5 = $5,000

- Electricity: $1,000 + (8,000 kWh x $0.10) = $1,000 + $800 = $1,800

- Total Cost: $16,800

-

Producing 2,000 widgets:

- Rent: $10,000

- Raw materials: 2,000 x $5 = $10,000

- Electricity: $1,000 + (15,000 kWh x $0.10) = $1,000 + $1,500 = $2,500

- Total Cost: $22,500

Why This Matters for Cost Managers and Accountants

- Budgeting: Knowing which costs are fixed or variable helps create more accurate budgets.

- Pricing: Understanding cost behavior aids in setting prices that cover costs and ensure profitability.

- Cost Control: Variable and semi-variable costs offer opportunities for cost reduction through efficiency improvements.

- Break-Even Analysis: Differentiating costs is essential for calculating break-even points and profit margins.

Summary Mind Map

This detailed understanding of cost behavior, supported by manufacturing scenarios and mind maps, equips cost managers and accountants to make informed strategic decisions that optimize cost efficiency and profitability.

2.3 Activity-Based Costing (ABC): Principles and Implementation Steps

Introduction to Activity-Based Costing (ABC)

Activity-Based Costing (ABC) is a refined costing methodology that assigns overhead and indirect costs to specific activities related to production or service delivery. Unlike traditional costing methods that allocate costs broadly, ABC provides a more accurate picture by linking costs to the actual activities that generate them.

This approach is particularly valuable in manufacturing and finance sectors where overheads are significant and diverse.

Principles of Activity-Based Costing

- Cost Drivers Identification: Recognize the factors that cause costs to be incurred.

- Activity Analysis: Break down the production or service process into discrete activities.

- Cost Assignment: Allocate costs to activities based on resource consumption.

- Product/Service Costing: Assign activity costs to products or services based on their usage of activities.

Mind Map: Principles of ABC

Implementation Steps of ABC

-

Identify and Define Activities:

- List all activities involved in the production or service process.

- Example: In a manufacturing plant, activities could include machining, assembly, quality inspection, and packaging.

-

Assign Resource Costs to Activities:

- Collect all indirect costs and assign them to the identified activities.

- Example: Electricity, maintenance, and salaries of support staff allocated to machining or assembly.

-

Determine Cost Drivers for Each Activity:

- Identify measurable factors that cause the cost of each activity.

- Example: Number of machine hours for machining, number of inspections for quality control.

-

Collect Activity Data:

- Measure the quantity of each cost driver consumed by different products or services.

- Example: Product A requires 10 machine hours; Product B requires 5.

-

Calculate Activity Rates:

- Divide total activity cost by total cost driver units.

- Example: Total machining cost $100,000 / 10,000 machine hours = $10 per machine hour.

-

Assign Costs to Products/Services:

- Multiply activity rates by the cost driver units consumed by each product.

- Example: Product A machining cost = 10 machine hours * $10 = $100.

-

Analyze and Use the Information:

- Use the detailed cost information for pricing, cost control, and process improvement.

Mind Map: ABC Implementation Steps

Practical Example: ABC in a Manufacturing Scenario

Company: XYZ Electronics

Situation: XYZ manufactures two products: Product Alpha and Product Beta.

| Activity | Total Cost | Cost Driver | Total Driver Units |

|---|---|---|---|

| Machining | $150,000 | Machine Hours | 15,000 hours |

| Assembly | $90,000 | Assembly Hours | 9,000 hours |

| Quality Inspection | $60,000 | Number of Inspections | 3,000 inspections |

Product Usage:

| Product | Machine Hours | Assembly Hours | Inspections |

|---|---|---|---|

| Alpha | 9,000 | 6,000 | 2,000 |

| Beta | 6,000 | 3,000 | 1,000 |

Calculations:

- Machining Rate = $150,000 / 15,000 = $10 per machine hour

- Assembly Rate = $90,000 / 9,000 = $10 per assembly hour

- Inspection Rate = $60,000 / 3,000 = $20 per inspection

Cost Assigned:

-

Product Alpha:

- Machining: 9,000 * $10 = $90,000

- Assembly: 6,000 * $10 = $60,000

- Inspection: 2,000 * $20 = $40,000

- Total Overhead Cost = $190,000

-

Product Beta:

- Machining: 6,000 * $10 = $60,000

- Assembly: 3,000 * $10 = $30,000

- Inspection: 1,000 * $20 = $20,000

- Total Overhead Cost = $110,000

This detailed costing helps XYZ Electronics understand the true cost drivers and allocate overheads more precisely than traditional methods.

Best Practices for Implementing ABC

- Start with a pilot project focusing on a few products or departments.

- Use software tools to collect and analyze activity data efficiently.

- Engage cross-functional teams to accurately identify activities and drivers.

- Regularly update cost drivers and activity data to reflect operational changes.

- Use ABC insights to drive process improvements and cost reduction initiatives.

Summary

Activity-Based Costing offers a powerful framework for accountants and cost managers to gain granular insights into cost behavior. By linking costs to activities and their drivers, ABC enables more accurate product costing, better pricing decisions, and targeted cost management strategies.

2.4 Practical Example: Applying ABC to Identify High-Cost Activities in an Assembly Line

Activity-Based Costing (ABC) is a powerful tool that helps organizations allocate overhead costs more accurately by identifying activities that drive costs and assigning expenses based on actual consumption. This section walks through a practical example of applying ABC in a manufacturing assembly line to pinpoint high-cost activities.

Step 1: Identify Activities in the Assembly Line

Before assigning costs, we first list all the key activities involved in the assembly line process. For example:

- Component inspection

- Assembly

- Quality testing

- Packaging

- Material handling

- Machine setup

- Maintenance

Mind Map: Assembly Line Activities

Step 2: Assign Resource Costs to Activities

Next, we allocate the total overhead costs to each activity based on resource consumption such as labor hours, machine hours, and materials used.

| Activity | Labor Hours | Machine Hours | Overhead Cost Allocation |

|---|---|---|---|

| Component Inspection | 100 | 20 | $5,000 |

| Assembly | 500 | 300 | $25,000 |

| Quality Testing | 150 | 50 | $7,500 |

| Packaging | 200 | 30 | $6,000 |

| Material Handling | 120 | 40 | $4,000 |

| Machine Setup | 80 | 60 | $3,500 |

| Maintenance | 60 | 70 | $2,000 |

Step 3: Determine Cost Drivers and Measure Activity Consumption

Identify appropriate cost drivers for each activity. For example:

- Component Inspection: Number of inspections

- Assembly: Number of units assembled

- Quality Testing: Number of tests performed

- Packaging: Number of packages

- Material Handling: Number of material moves

- Machine Setup: Number of setups

- Maintenance: Machine hours

Example data for a month:

| Activity | Cost Driver | Quantity Consumed |

|---|---|---|

| Component Inspection | Number of inspections | 1,000 |

| Assembly | Units assembled | 5,000 |

| Quality Testing | Number of tests | 1,200 |

| Packaging | Number of packages | 4,800 |

| Material Handling | Number of moves | 900 |

| Machine Setup | Number of setups | 40 |

| Maintenance | Machine hours | 500 |

Step 4: Calculate Activity Cost Rates

Activity Cost Rate = Overhead Cost Allocation / Quantity Consumed

| Activity | Overhead Cost Allocation | Quantity Consumed | Activity Cost Rate (per unit) |

|---|---|---|---|

| Component Inspection | $5,000 | 1,000 | $5.00 |

| Assembly | $25,000 | 5,000 | $5.00 |

| Quality Testing | $7,500 | 1,200 | $6.25 |

| Packaging | $6,000 | 4,800 | $1.25 |

| Material Handling | $4,000 | 900 | $4.44 |

| Machine Setup | $3,500 | 40 | $87.50 |

| Maintenance | $2,000 | 500 | $4.00 |

Step 5: Assign Activity Costs to Products

Assume the assembly line produces two products: Product A and Product B.

| Activity | Product A Consumption | Product B Consumption |

|---|---|---|

| Component Inspection | 600 inspections | 400 inspections |

| Assembly | 3,000 units | 2,000 units |

| Quality Testing | 700 tests | 500 tests |

| Packaging | 2,800 packages | 2,000 packages |

| Material Handling | 600 moves | 300 moves |

| Machine Setup | 25 setups | 15 setups |

| Maintenance | 300 machine hours | 200 machine hours |

Calculate total overhead cost per product:

-

Product A:

- Component Inspection: 600 x $5.00 = $3,000

- Assembly: 3,000 x $5.00 = $15,000

- Quality Testing: 700 x $6.25 = $4,375

- Packaging: 2,800 x $1.25 = $3,500

- Material Handling: 600 x $4.44 = $2,664

- Machine Setup: 25 x $87.50 = $2,187.50

- Maintenance: 300 x $4.00 = $1,200

- Total = $31,926.50

-

Product B:

- Component Inspection: 400 x $5.00 = $2,000

- Assembly: 2,000 x $5.00 = $10,000

- Quality Testing: 500 x $6.25 = $3,125

- Packaging: 2,000 x $1.25 = $2,500

- Material Handling: 300 x $4.44 = $1,332

- Machine Setup: 15 x $87.50 = $1,312.50

- Maintenance: 200 x $4.00 = $800

- Total = $20,069.50

Step 6: Analyze Results and Identify High-Cost Activities

From the activity cost rates and product cost assignments, we observe:

- Machine Setup has the highest cost rate ($87.50 per setup), indicating setups are very expensive.

- Quality Testing and Component Inspection also have relatively high cost rates.

- Product A consumes more setups and inspections, leading to higher overhead costs.

Mind Map: High-Cost Activities and Insights

Best Practices Illustrated

- Use precise cost drivers: Choosing relevant drivers like number of setups or inspections ensures accurate cost allocation.

- Segment costs by activity: Helps identify specific areas where cost reduction efforts should focus.

- Compare product consumption: Understand which products consume more costly activities to guide pricing or process improvement.

- Continuous monitoring: Regularly update ABC data to reflect changes in production or process.

Summary

Applying ABC in the assembly line revealed that machine setup activities are disproportionately expensive. By focusing on reducing setup times or frequency, the company can achieve significant cost savings. Similarly, optimizing quality testing and inspection processes can further enhance cost efficiency. This example demonstrates how ABC provides actionable insights beyond traditional costing methods, empowering accountants and cost managers to make strategic decisions aligned with operational realities.

2.5 Cost Allocation Methods and Best Practices in Finance Departments

Cost allocation is a critical process in finance departments, especially within manufacturing and finance sectors, where accurately assigning indirect costs to cost objects (products, departments, projects) impacts decision-making, pricing, and profitability analysis. This section explores common cost allocation methods, best practices, and practical examples to help accountants and cost managers optimize their cost allocation processes.

Understanding Cost Allocation

Cost allocation involves distributing indirect costs (overheads) to different cost centers or products based on a rational and consistent basis. Unlike direct costs, indirect costs cannot be traced directly to a single product or service.

Common Cost Allocation Methods

Direct Allocation Method

- Allocates service department costs directly to production departments without allocating costs between service departments.

Step-Down (Sequential) Method

- Allocates service department costs to other service and production departments sequentially, recognizing some inter-service department support.

Reciprocal Method

- Recognizes mutual services among all service departments and allocates costs accordingly using simultaneous equations.

Activity-Based Costing (ABC)

- Allocates costs based on activities that drive costs, providing more accurate cost assignment.

Mind Map: Cost Allocation Methods

Best Practices in Cost Allocation for Finance Departments

-

Choose the Most Appropriate Method Based on Complexity and Accuracy Needs

- For simple organizations, direct allocation may suffice.

- For complex operations, ABC or reciprocal methods provide better accuracy.

-

Use Relevant Cost Drivers

- Identify cost drivers that closely relate to the consumption of resources (e.g., machine hours, labor hours).

-

Maintain Transparency and Consistency

- Document allocation bases and methods clearly.

- Apply methods consistently across periods to enable comparability.

-

Leverage Technology

- Use ERP and costing software to automate allocation calculations and reduce errors.

-

Regularly Review and Update Allocation Bases

- Ensure cost drivers remain relevant as business processes evolve.

-

Engage Cross-Functional Teams

- Collaborate with production, operations, and finance teams to validate allocation assumptions.

Example 1: Direct Allocation Method in a Manufacturing Plant

Scenario: A manufacturing plant has two service departments: Maintenance and Cafeteria, and two production departments: Assembly and Packaging.

- Maintenance costs: $100,000

- Cafeteria costs: $50,000

Using the direct method, Maintenance and Cafeteria costs are allocated directly to Assembly and Packaging based on labor hours.

| Department | Labor Hours | % of Total Labor Hours | Maintenance Allocation | Cafeteria Allocation |

|---|---|---|---|---|

| Assembly | 6,000 | 60% | $60,000 | $30,000 |

| Packaging | 4,000 | 40% | $40,000 | $20,000 |

Outcome:

- Assembly absorbs $90,000 of service costs.

- Packaging absorbs $60,000 of service costs.

Mind Map: Direct Allocation Example

Example 2: Step-Down Method

Scenario: Same departments as above, but Maintenance provides some services to Cafeteria.

- Maintenance costs: $100,000

- Cafeteria costs: $50,000

Step 1: Allocate Maintenance costs to Cafeteria, Assembly, Packaging based on service usage:

- Cafeteria: 20%

- Assembly: 50%

- Packaging: 30%

| Department | Allocation % | Amount Allocated |

|---|---|---|

| Cafeteria | 20% | $20,000 |

| Assembly | 50% | $50,000 |

| Packaging | 30% | $30,000 |

Step 2: Add allocated Maintenance costs to Cafeteria costs:

- Cafeteria new cost = $50,000 + $20,000 = $70,000

Step 3: Allocate Cafeteria costs to Assembly and Packaging based on labor hours:

- Assembly: 60%

- Packaging: 40%

| Department | Allocation % | Amount Allocated |

|---|---|---|

| Assembly | 60% | $42,000 |

| Packaging | 40% | $28,000 |

Final Allocation:

- Assembly: $50,000 (Maintenance) + $42,000 (Cafeteria) = $92,000

- Packaging: $30,000 (Maintenance) + $28,000 (Cafeteria) = $58,000

Mind Map: Step-Down Allocation Example

Example 3: Activity-Based Costing (ABC) in Finance Department

Scenario: A finance department supports three business units: Retail, Wholesale, and Online Sales. The finance department incurs costs related to:

- Invoice processing

- Financial reporting

- Payroll processing

Step 1: Identify activities and cost pools:

- Invoice processing: $120,000

- Financial reporting: $80,000

- Payroll processing: $100,000

Step 2: Identify cost drivers:

- Invoice processing: Number of invoices

- Financial reporting: Number of reports

- Payroll processing: Number of employees

Step 3: Collect activity data:

| Business Unit | Invoices | Reports | Employees |

|---|---|---|---|

| Retail | 3,000 | 10 | 50 |

| Wholesale | 2,000 | 8 | 30 |

| Online Sales | 5,000 | 12 | 20 |

Step 4: Calculate cost driver rates:

- Invoice processing rate = $120,000 / (3,000+2,000+5,000) = $12 per invoice

- Financial reporting rate = $80,000 / (10+8+12) = $2,666.67 per report

- Payroll processing rate = $100,000 / (50+30+20) = $1,000 per employee

Step 5: Allocate costs:

| Business Unit | Invoice Cost | Reporting Cost | Payroll Cost | Total Cost |

|---|---|---|---|---|

| Retail | $36,000 | $26,666.70 | $50,000 | $112,666.70 |

| Wholesale | $24,000 | $21,333.36 | $30,000 | $75,333.36 |

| Online Sales | $60,000 | $32,000.04 | $20,000 | $112,000.04 |

Mind Map: ABC Cost Allocation Example

Summary

Effective cost allocation in finance departments ensures accurate cost visibility and supports strategic decision-making. Selecting the right allocation method depends on organizational complexity, accuracy requirements, and available data. Incorporating best practices such as using relevant cost drivers, maintaining transparency, leveraging technology, and engaging stakeholders will enhance the cost allocation process.

By applying these methods and examples, accountants and cost managers can improve cost control, pricing strategies, and overall financial performance within manufacturing and finance sectors.

3. Cost Planning and Budgeting Strategies

3.1 Developing Cost Plans Aligned with Business Strategy

Strategic cost planning is the process of creating detailed cost plans that directly support and align with an organization’s overall business strategy. For accountants and cost managers in finance and manufacturing sectors, this alignment ensures that cost management efforts contribute to achieving long-term goals such as market expansion, product innovation, operational efficiency, and profitability.

Why Align Cost Plans with Business Strategy?

- Ensures resource allocation supports strategic priorities.

- Prevents cost-cutting measures that undermine growth or quality.

- Facilitates proactive decision-making and risk management.

- Enhances communication between finance, operations, and leadership.

Key Steps to Develop Cost Plans Aligned with Business Strategy

-

Understand the Business Strategy

- Review strategic documents: vision, mission, objectives.

- Identify key strategic drivers (e.g., market share growth, cost leadership, product differentiation).

-

Identify Cost Drivers Linked to Strategic Objectives

- Map activities and processes that impact strategic goals.

- Prioritize cost elements that influence competitive advantage.

-

Set Cost Targets Based on Strategic Priorities

- Define acceptable cost levels for products, departments, or projects.

- Balance cost reduction with quality and innovation needs.

-

Develop Detailed Cost Plans

- Break down costs by categories: materials, labor, overhead, R&D.

- Incorporate timing and resource availability.

-

Integrate Cost Plans with Operational Plans

- Coordinate with production schedules, procurement, and sales forecasts.

-

Monitor and Adjust Plans Continuously

- Use KPIs and variance analysis to track performance.

- Adapt plans to changing market or internal conditions.

Mind Map: Developing Cost Plans Aligned with Business Strategy

Example 1: Aligning Cost Plan with a Market Expansion Strategy

Scenario: A manufacturing company aims to expand into new geographic markets over the next 3 years.

- Strategic Objective: Increase market share by 20% in emerging markets.

- Cost Planning Implications:

- Increase marketing and distribution costs in target regions.

- Invest in localized product adaptations (R&D costs).

- Scale up production capacity (capital expenditure).

- Control overhead by optimizing existing facilities.

Cost Plan Highlights:

- Allocate 15% higher budget for marketing in year 1.

- Budget for new tooling and design changes.

- Plan phased capital investments aligned with sales forecasts.

This alignment ensures the cost plan supports growth without jeopardizing financial stability.

Example 2: Cost Plan Supporting a Cost Leadership Strategy

Scenario: A manufacturing firm wants to become the lowest-cost producer in its segment.

- Strategic Objective: Reduce total production costs by 10% within 12 months.

- Cost Planning Implications:

- Identify high-cost activities through Activity-Based Costing.

- Invest in automation to reduce labor costs.

- Negotiate better terms with suppliers.

- Optimize inventory to reduce holding costs.

Cost Plan Highlights:

- Set aggressive cost reduction targets for raw materials and labor.

- Allocate budget for technology upgrades.

- Implement tighter controls on overhead spending.

This cost plan directly supports the strategic goal of cost leadership.

Mind Map: Example 2 - Cost Leadership Strategy Cost Plan

Best Practices for Accountants and Cost Managers

- Collaborate closely with strategic planners and operational managers.

- Use data-driven approaches like ABC and variance analysis.

- Communicate cost plan assumptions and impacts clearly to stakeholders.

- Regularly revisit cost plans as business strategies evolve.

- Leverage technology for real-time cost tracking and forecasting.

By developing cost plans that are tightly aligned with business strategy, finance and manufacturing professionals can ensure that cost management is not just a control function but a strategic enabler driving sustainable competitive advantage.

3.2 Zero-Based Budgeting vs Traditional Budgeting: Pros, Cons, and Examples

Introduction

Budgeting is a critical process in strategic cost management, especially for accountants and cost managers in finance and manufacturing sectors. Two widely used budgeting approaches are Zero-Based Budgeting (ZBB) and Traditional Budgeting. Understanding their differences, advantages, and drawbacks helps organizations choose the right method for cost control and resource allocation.

What is Traditional Budgeting?

Traditional budgeting, also known as incremental budgeting, uses the previous period’s budget as a base and adjusts it for the new period by adding or subtracting a percentage based on expected changes.

- Key Characteristics:

- Starts from last year’s budget

- Incremental adjustments (e.g., inflation, growth)

- Focus on historical data

Example:

A manufacturing plant had a maintenance budget of $100,000 last year. For the new year, the budget is increased by 5% to account for inflation, resulting in a $105,000 budget.

Mind Map: Traditional Budgeting

What is Zero-Based Budgeting (ZBB)?

Zero-Based Budgeting requires building the budget from scratch (zero base) every period, justifying every expense as if starting anew.

- Key Characteristics:

- No reliance on previous budgets

- Justify all expenses

- Focus on activities and outcomes

Example:

A manufacturing company decides to implement ZBB for its logistics department. Instead of automatically increasing last year’s $200,000 budget, each expense (fuel, maintenance, labor) must be justified based on current needs and efficiency targets.

Mind Map: Zero-Based Budgeting

Pros and Cons Comparison

| Aspect | Traditional Budgeting | Zero-Based Budgeting |

|---|---|---|

| Ease of Implementation | Simple, less time-consuming | Complex, requires significant effort |

| Cost Control | May perpetuate inefficiencies | Encourages cost optimization |

| Flexibility | Less flexible, based on historical data | Highly flexible, adapts to current priorities |

| Employee Engagement | Lower, often seen as routine | Higher, requires involvement in justification |

| Data Requirements | Minimal, uses existing data | Extensive, needs detailed activity analysis |

Mind Map: Pros and Cons Comparison

Practical Examples in Manufacturing and Finance

Example 1: Traditional Budgeting in a Manufacturing Plant

- The plant uses last year’s budget as a base.

- Maintenance costs increased by 3% due to inflation.

- No detailed review of individual cost drivers.

- Result: Some outdated equipment maintenance costs persist, limiting cost savings.

Example 2: Zero-Based Budgeting in Finance Department

- The finance team builds the budget from zero.

- Each expense, such as software subscriptions and training, is justified.

- Unused or redundant subscriptions are cut.

- Result: 10% cost reduction and better alignment with strategic priorities.

When to Use Which Method?

-

Traditional Budgeting:

- Stable environments with predictable costs

- Limited resources for detailed budgeting

- When speed and simplicity are priorities

-

Zero-Based Budgeting:

- When cost reduction is a strategic priority

- In dynamic or rapidly changing environments

- When inefficiencies need to be identified and eliminated

Best Practices for Accountants and Cost Managers

- Combine both methods: Use traditional budgeting for routine expenses and ZBB for discretionary or high-impact areas.

- Leverage technology to streamline ZBB data collection and analysis.

- Engage cross-functional teams to justify costs and identify savings.

- Regularly review and update budgeting assumptions.

Summary

Zero-Based Budgeting and Traditional Budgeting each have unique strengths and challenges. Understanding these helps finance and manufacturing professionals implement the best approach tailored to their organizational needs, driving strategic cost management and operational efficiency.

3.3 Rolling Budgets and Forecasting Techniques for Dynamic Manufacturing Environments

In dynamic manufacturing environments, where market conditions, raw material costs, and production demands can fluctuate rapidly, traditional static budgeting often falls short. Rolling budgets and advanced forecasting techniques provide agility and accuracy, enabling finance and cost managers to respond proactively to changes.

What is a Rolling Budget?

A rolling budget is a continuous budgeting process where a new budget period is added as the current period ends. Instead of creating a fixed annual budget, the budget “rolls” forward, typically monthly or quarterly, maintaining a consistent planning horizon.

Key Benefits:

- Flexibility to adapt to changing conditions

- Continuous monitoring and updating

- Improved accuracy in forecasting

Mind Map: Rolling Budget Fundamentals

Forecasting Techniques in Manufacturing

-

Time Series Analysis

- Uses historical data to predict future trends.

- Example: Analyzing past 12 months of production volume to forecast next quarter.

-

Causal Models

- Considers factors influencing costs, such as raw material prices or labor rates.

- Example: Forecasting costs based on projected steel price fluctuations.

-

Qualitative Forecasting

- Uses expert judgment and market intelligence.

- Example: Incorporating insights from sales and production teams about upcoming demand spikes.

-

Simulation Models

- Uses computer models to simulate different scenarios.

- Example: Simulating cost impact of supply chain disruptions.

Mind Map: Forecasting Techniques

Implementing Rolling Budgets with Forecasting: Step-by-Step Example

Scenario: A mid-sized manufacturing company produces automotive parts. Raw material costs and demand fluctuate due to market volatility.

-

Initial Budget Setup:

- Prepare a 12-month budget based on historical data and market analysis.

-

Monthly Review:

- At the end of each month, compare actual costs and volumes against the budget.

-

Forecast Update:

- Use time series analysis on the last 6 months’ data to adjust production volume forecasts.

- Incorporate causal factors such as a recent 5% increase in steel prices.

-

Budget Roll Forward:

- Drop the past month and add a new month at the end of the 12-month horizon.

- Adjust budgeted costs and revenues accordingly.

-

Communication:

- Share updated budgets with production, procurement, and finance teams for alignment.

Result: The company maintains an up-to-date budget that reflects current realities, enabling better cost control and resource allocation.

Example Mind Map: Rolling Budget Process in Manufacturing

Best Practices for Rolling Budgets and Forecasting

- Regular Data Collection: Ensure timely and accurate data inputs.

- Cross-Functional Collaboration: Involve production, procurement, and sales teams.

- Use Technology: Leverage ERP and forecasting software for automation.

- Scenario Planning: Prepare for multiple possible futures.

- Continuous Training: Equip cost managers with forecasting and budgeting skills.

Real-World Example: Dynamic Budgeting at XYZ Manufacturing

XYZ Manufacturing faced unpredictable demand due to fluctuating automotive industry trends. By implementing rolling budgets updated monthly and integrating causal forecasting models (considering raw material price indices and supplier lead times), they reduced budget variances by 30% and improved cost predictability. This allowed the finance team to advise production on cost-saving opportunities proactively.

Summary

Rolling budgets combined with robust forecasting techniques empower manufacturing finance and cost managers to navigate uncertainty effectively. By continuously updating budgets and incorporating relevant data-driven forecasts, organizations can optimize costs, improve financial agility, and support strategic decision-making.

3.4 Best Practice: Integrating Cost Planning with Production Scheduling

Integrating cost planning with production scheduling is a critical best practice for accountants and cost managers in manufacturing and finance sectors. This integration ensures that cost control measures are aligned with production activities, leading to optimized resource utilization, minimized waste, and improved profitability.

Why Integrate Cost Planning with Production Scheduling?

- Enhanced Cost Visibility: Understanding production schedules helps anticipate cost fluctuations related to labor, materials, and overhead.

- Improved Resource Allocation: Aligning budgets with production timelines ensures resources are available when needed, avoiding costly delays.

- Reduced Waste and Idle Time: Synchronization helps minimize downtime and excess inventory, reducing carrying costs.

- Better Decision-Making: Real-time cost data linked to production schedules supports proactive adjustments.

Key Components of Integration

Step-by-Step Approach to Integration

- Collaborative Planning Sessions: Involve finance, production, and supply chain teams to align cost targets with production goals.

- Develop Detailed Production Schedules: Break down production into tasks with timelines, resource requirements, and cost estimates.

- Link Cost Budgets to Production Tasks: Assign budgeted costs to each scheduled activity, including labor, materials, and overhead.

- Implement Real-Time Monitoring Tools: Use ERP or production management software to track actual costs vs. planned costs.

- Conduct Regular Variance Analysis: Identify discrepancies between planned and actual costs, analyze causes, and adjust schedules or budgets accordingly.

Practical Example: Integrating Cost Planning with Production Scheduling in an Electronics Manufacturer

Scenario: An electronics manufacturer plans to launch a new product line. The cost manager collaborates with production planners to integrate cost planning with the production schedule.

- The production schedule outlines phases: component procurement, assembly, testing, and packaging.

- Each phase is assigned a budget based on labor hours, material costs, and overhead allocation.

- Using an ERP system, the cost manager monitors real-time expenditures against the schedule.

- During assembly, a delay causes overtime labor costs to rise. The integrated system flags this variance immediately.

- The team adjusts subsequent schedules and budgets to mitigate further cost overruns.

Outcome: The proactive integration helped reduce unexpected costs by 12%, improved schedule adherence, and enhanced cross-department communication.

Mind Map: Example Workflow for Integration

Tips for Successful Integration

- Use Integrated Software Solutions: Leverage ERP or specialized cost management tools that support production scheduling.

- Maintain Clear Communication Channels: Regular meetings between finance and production teams foster alignment.

- Train Teams on Cost Awareness: Educate production staff on the impact of scheduling decisions on costs.

- Establish Key Performance Indicators (KPIs): Track metrics like cost per unit, schedule adherence, and variance percentages.

By embedding cost planning directly into production scheduling, organizations can achieve a holistic view of operational efficiency, enabling smarter financial control and stronger competitive advantage.

3.5 Example: How a Cost Manager Used Budgeting to Control Overhead in a Multinational Plant

In a multinational manufacturing plant, overhead costs were steadily increasing, impacting the overall profitability of the operation. The cost manager was tasked with controlling and reducing these overheads without compromising production quality or employee satisfaction. This example illustrates how effective budgeting techniques were applied to achieve this goal.

Step 1: Understanding Overhead Components

The first step was to break down the overhead costs into manageable categories. These included:

- Utilities (electricity, water, gas)

- Maintenance and Repairs

- Administrative Salaries

- Depreciation of Equipment

- Indirect Materials and Supplies

- Facility Rent and Insurance

This classification helped in identifying which areas had the highest cost impact and potential for savings.

Step 2: Setting a Realistic Budget

The cost manager collaborated with department heads to establish a zero-based budgeting approach. Instead of relying on historical data alone, each department justified their overhead needs from scratch, ensuring that every expense was necessary and aligned with strategic goals.

Example:

- The maintenance department justified a 10% increase in budget due to new machinery requiring specialized upkeep.

- The administrative department proposed a 5% reduction by adopting digital workflows to reduce paper and printing costs.

Step 3: Implementing Budget Controls and Monitoring

To ensure adherence to the budget, the cost manager introduced monthly variance analysis reports comparing actual overhead expenses against budgeted figures.

- Variances were categorized as favorable or unfavorable.

- Immediate investigations were triggered for variances exceeding 5%.

Example:

- An unfavorable variance in electricity costs led to identifying inefficient lighting systems, prompting an upgrade to LED lighting.

Step 4: Continuous Improvement and Feedback Loop

The cost manager established quarterly review meetings with all stakeholders to discuss budget performance and identify new cost-saving opportunities.

- Feedback from production teams helped optimize machine usage schedules, reducing overtime and energy consumption.

- Administrative teams adopted cloud-based tools, cutting software licensing fees.

Results Achieved

- Overhead costs were reduced by 12% within the first year.

- Energy consumption dropped by 8% due to efficiency upgrades.

- Administrative expenses decreased by 7% through digital transformation.

- Improved budget accuracy and accountability across departments.

Key Takeaways for Accountants and Cost Managers

- Zero-Based Budgeting encourages critical evaluation of all expenses, preventing unnecessary overhead.

- Collaborative Budgeting ensures buy-in and realistic targets from all departments.

- Regular Variance Analysis helps detect issues early and drives corrective actions.

- Continuous Feedback and Improvement foster a culture of cost consciousness and innovation.

This example demonstrates how strategic budgeting is not just about cutting costs but about aligning overhead spending with organizational goals while maintaining operational efficiency.

4. Cost Control and Monitoring Mechanisms

4.1 Establishing Cost Control Systems: Tools and Technologies

Effective cost control systems are essential for organizations aiming to manage expenses proactively and maintain profitability. In the finance and manufacturing sectors, establishing robust cost control mechanisms involves integrating the right tools and technologies that enable real-time monitoring, analysis, and corrective actions.

Key Components of Cost Control Systems

- Cost Tracking: Continuous recording of costs incurred.

- Cost Analysis: Identifying variances and their causes.

- Reporting: Clear communication of cost data to stakeholders.

- Corrective Actions: Implementing measures to control or reduce costs.

Mind Map: Components of a Cost Control System

Popular Tools and Technologies for Cost Control

-

Enterprise Resource Planning (ERP) Systems

- Integrate financial, manufacturing, and supply chain data.

- Example: SAP ERP enables real-time cost tracking across departments.

-

Activity-Based Costing (ABC) Software

- Allocates overhead costs more accurately based on activities.

- Example: A manufacturing firm used ABC software to identify costly assembly steps, leading to process redesign and 10% cost savings.

-

Variance Analysis Tools

- Compare actual costs against budgets or standards.

- Example: Using Microsoft Excel with customized variance templates to monitor monthly production costs.

-

Cost Management Dashboards

- Visualize key cost metrics in real-time.

- Example: Tableau dashboards showing raw material cost trends and alerting cost managers to spikes.

-

Inventory Management Systems

- Optimize stock levels to reduce holding costs.

- Example: Just-In-Time (JIT) inventory software reducing excess inventory by 25%.

-

Workflow Automation and Alerts

- Automate approval processes and notify managers of cost overruns.

- Example: Automated email alerts triggered when project costs exceed 90% of budget.

Mind Map: Technologies Supporting Cost Control

Example: Implementing a Cost Control System in a Manufacturing Plant

Scenario: A mid-sized manufacturing company was experiencing frequent cost overruns in production due to inefficient raw material usage and unmonitored labor costs.

Solution:

- Implemented an ERP system with integrated cost tracking modules.

- Adopted ABC software to analyze overhead allocation.

- Set up dashboards for real-time monitoring of raw material consumption and labor hours.

- Established automated alerts for cost variances exceeding 5%.

Outcome:

- Raw material waste reduced by 18% within six months.

- Labor cost variances identified early, enabling corrective scheduling.

- Overall production costs decreased by 12%, improving profit margins.

Best Practices for Establishing Cost Control Systems

- Start with Clear Objectives: Define what costs need control and why.

- Integrate Systems: Ensure seamless data flow between finance, production, and procurement.

- Train Users: Equip accountants and cost managers with skills to use tools effectively.

- Regular Review: Continuously analyze reports and refine control measures.

- Leverage Automation: Use alerts and workflows to minimize manual errors and delays.

By combining these tools and technologies with structured processes, finance and manufacturing professionals can establish cost control systems that not only monitor expenses but also drive strategic cost management initiatives.

4.2 Variance Analysis: Identifying and Addressing Cost Deviations

Variance analysis is a critical tool in strategic cost management that helps accountants and cost managers understand the differences between planned (budgeted) costs and actual costs incurred. By identifying these deviations, organizations can take corrective actions to control costs, improve efficiency, and enhance profitability.

What is Variance Analysis?

Variance analysis involves comparing actual financial performance against budgeted or standard costs to pinpoint areas where costs have deviated. These deviations, called variances, can be either favorable (costs lower than expected) or unfavorable (costs higher than expected).

Why is Variance Analysis Important?

- Enables early detection of cost overruns

- Helps in identifying inefficiencies or waste

- Supports informed decision-making

- Facilitates accountability and performance evaluation

Types of Variances in Cost Management

Step-by-Step Process of Variance Analysis

Practical Example: Material Price and Usage Variance

Scenario: A manufacturing company budgets to purchase 1,000 kg of steel at $5 per kg for $5,000. Actual purchase was 1,100 kg at $4.80 per kg, costing $5,280.

-

Material Price Variance (MPV): Measures the difference due to price change.

MPV = (Standard Price - Actual Price) x Actual Quantity

MPV = ($5.00 - $4.80) x 1,100 = $0.20 x 1,100 = $220 Favorable

-

Material Usage Variance (MUV): Measures the difference due to quantity used.

MUV = (Standard Quantity - Actual Quantity) x Standard Price

MUV = (1,000 - 1,100) x $5.00 = (-100) x $5.00 = $500 Unfavorable

Interpretation:

- The company paid less per kg than expected, saving $220.

- However, it used 100 kg more than planned, causing an extra $500 cost.

- Overall, the unfavorable usage variance outweighs the favorable price variance, indicating inefficiency in material usage.

Mind Map: Analyzing Causes of Variances

Addressing Cost Deviations: Best Practices

- Investigate Significant Variances Promptly: Focus on variances that have material impact.

- Engage Cross-Functional Teams: Collaborate with procurement, production, and finance.

- Identify Root Causes: Use tools like the 5 Whys or Fishbone diagrams.

- Implement Corrective Actions: Adjust purchasing strategies, improve training, or optimize processes.

- Update Standards if Necessary: Reflect changes in market conditions or operational realities.

- Continuous Monitoring: Establish regular variance reporting cycles.

Example: Addressing Labor Efficiency Variance

A cost manager notices an unfavorable labor efficiency variance where workers took 1,200 hours instead of the standard 1,000 hours for a batch.

- Investigation: Revealed frequent machine breakdowns causing delays.

- Action: Scheduled preventive maintenance and trained operators on quick troubleshooting.

- Result: Labor hours reduced to 1,050 in the next cycle, improving efficiency and lowering costs.

Summary

Variance analysis is an indispensable practice for accountants and cost managers to maintain control over manufacturing and financial costs. By systematically identifying, analyzing, and addressing cost deviations, organizations can drive continuous improvement and strategic cost management success.

4.3 Implementing Key Performance Indicators (KPIs) for Cost Management

Key Performance Indicators (KPIs) are essential tools for accountants and cost managers to monitor, control, and optimize costs within finance and manufacturing sectors. Properly implemented KPIs provide actionable insights that help organizations stay aligned with their strategic cost management goals.

What are KPIs in Cost Management?

KPIs are quantifiable measures that reflect the critical success factors of an organization’s cost management efforts. They help track performance against cost objectives and highlight areas requiring attention.

Why Implement KPIs for Cost Management?

- Visibility: Real-time insight into cost behavior.

- Accountability: Assign responsibility for cost control.

- Decision-Making: Data-driven strategies for cost reduction.

- Continuous Improvement: Identify trends and inefficiencies.

Key Steps to Implement KPIs for Cost Management

Common KPIs for Cost Management with Examples

| KPI Name | Description | Example in Manufacturing |

|---|---|---|

| Cost Variance | Difference between actual and budgeted costs | Actual raw material cost $105,000 vs budget $100,000 = $5,000 unfavorable variance |

| Cost per Unit Produced | Total cost divided by number of units produced | $500,000 total production cost / 10,000 units = $50 per unit |

| Overhead Cost Ratio | Overhead costs as a percentage of total costs | $200,000 overhead / $1,000,000 total cost = 20% |

| Scrap Rate | Percentage of materials wasted during production | 2% scrap rate means 2% of raw materials are wasted |

| Labor Efficiency Ratio | Actual labor hours vs standard labor hours | 950 actual hours / 1,000 standard hours = 95% efficiency |

| Inventory Turnover Ratio | How often inventory is sold and replaced | 8 times per year turnover indicates efficient inventory management |

Example: Implementing KPIs in a Manufacturing Plant

Scenario: A manufacturing plant wants to reduce costs related to raw materials and labor.

- Objective: Reduce raw material waste and improve labor productivity.

- Selected KPIs: Scrap Rate, Labor Efficiency Ratio, Cost per Unit Produced.

- Data Collection: Use ERP system to track material usage and labor hours daily.

- Target Setting: Scrap rate target set at 1.5% (down from 2%), labor efficiency target at 98%.

- Monitoring: Weekly dashboard reports shared with production managers.

- Action: Identify bottlenecks causing scrap, retrain workers, optimize workflows.

- Result: Scrap rate reduced to 1.4%, labor efficiency improved to 99%, cost per unit decreased by 5% over 6 months.

Mind Map: Example KPI Dashboard Components

Best Practices for KPI Implementation

- Align KPIs with Strategic Goals: Ensure KPIs reflect what truly impacts cost management.

- Keep KPIs Simple and Relevant: Avoid overcomplicating with too many indicators.

- Use Real-Time Data: Leverage technology for timely and accurate tracking.

- Engage Stakeholders: Involve finance, production, and procurement teams.

- Review and Update Regularly: Adapt KPIs as business needs evolve.

By integrating KPIs effectively, accountants and cost managers can transform raw data into strategic insights, driving cost efficiency and supporting sustainable growth within finance and manufacturing organizations.

4.4 Real-World Example: Using Variance Analysis to Optimize Raw Material Usage

Variance analysis is a powerful tool that helps accountants and cost managers identify differences between planned and actual costs, enabling targeted actions to optimize resource usage. In manufacturing, raw materials often represent a significant portion of total costs, making variance analysis essential for cost control and efficiency improvements.

What is Variance Analysis?

Variance analysis involves comparing actual costs to standard or budgeted costs and investigating the reasons for any deviations. It typically breaks down into:

- Material Price Variance: Difference due to paying more or less per unit of raw material.

- Material Usage Variance: Difference due to using more or less raw material than expected.

Mind Map: Components of Raw Material Variance Analysis

Real-World Example: Optimizing Raw Material Usage at ABC Manufacturing

Background: ABC Manufacturing produces automotive components. The cost manager noticed that raw material costs were consistently exceeding the budget by 8% over the last quarter.

Step 1: Conduct Variance Analysis

- Standard Cost: $50 per kg of steel

- Actual Cost: $52 per kg (Material Price Variance)

- Standard Usage: 1000 kg per batch

- Actual Usage: 1100 kg per batch (Material Usage Variance)

Calculations:

-

Material Price Variance = (Standard Price - Actual Price) x Actual Quantity

= ($50 - $52) x 1100 = -$2 x 1100 = -$2200 (Unfavorable) -

Material Usage Variance = (Standard Quantity - Actual Quantity) x Standard Price

= (1000 - 1100) x $50 = -100 x $50 = -$5000 (Unfavorable)

Total Variance: -$7,200 (Unfavorable)

Mind Map: Investigating the Causes of Variance

Step 2: Root Cause Analysis

- The price increase was due to a temporary supplier price hike.

- The usage variance was traced to increased scrap rates caused by a new machine calibration issue.

Step 3: Corrective Actions

- Negotiated with the supplier for a fixed price contract to stabilize material costs.

- Scheduled immediate maintenance and recalibration of the machine.

- Trained operators on updated machine settings to reduce errors.

Step 4: Results After Implementation

- Material price stabilized at $50/kg.

- Material usage reduced to 1020 kg per batch.

New Variance Calculations:

- Material Price Variance = ($50 - $50) x 1020 = $0

- Material Usage Variance = (1000 - 1020) x $50 = -20 x $50 = -$1000 (Significantly improved)

Mind Map: Benefits of Variance Analysis in Raw Material Optimization

Additional Example: Using Variance Analysis in a Food Manufacturing Plant

A food manufacturer noticed higher-than-expected flour consumption. Variance analysis revealed a usage variance due to inconsistent dough mixing times leading to excess flour waste. By standardizing mixing times and training staff, the plant reduced flour usage variance by 30%, saving thousands annually.

Key Takeaways

- Variance analysis breaks down cost deviations into understandable components.

- Investigating both price and usage variances provides a comprehensive view.

- Root cause analysis is critical to identify actionable issues.

- Implementing corrective actions based on variance findings can significantly reduce raw material costs.

- Regular variance analysis fosters a culture of continuous improvement and cost discipline.

By integrating variance analysis into routine cost management practices, accountants and cost managers in manufacturing can drive substantial cost savings and operational efficiencies.

4.5 Best Practice: Continuous Improvement through Cost Monitoring in Manufacturing

Continuous improvement through cost monitoring is a vital best practice for manufacturing organizations aiming to maintain competitiveness and profitability. It involves systematically tracking costs, identifying inefficiencies, and implementing incremental changes to optimize resource use and reduce waste.

Why Continuous Improvement Matters in Cost Monitoring

- Manufacturing environments are dynamic, with fluctuating raw material prices, labor costs, and operational challenges.

- Continuous improvement ensures that cost control is proactive rather than reactive.

- It fosters a culture of accountability and efficiency across departments.

Mind Map: Continuous Improvement through Cost Monitoring

Step-by-Step Approach to Implement Continuous Improvement in Cost Monitoring

-

Establish Clear Cost Metrics: Define which costs are critical to monitor, such as raw materials, labor, energy, and overhead.

-

Implement Real-Time Data Collection: Use technology like IoT sensors, ERP systems, and automated reporting to gather accurate cost data continuously.

-

Conduct Regular Variance Analysis: Compare actual costs against budgets or standards to identify deviations.

-

Perform Root Cause Analysis: Investigate the underlying reasons for cost variances, such as machine downtime or supplier price increases.

-

Develop and Implement Improvement Plans: Based on findings, initiate targeted actions like process redesign, renegotiating supplier contracts, or employee training.

-

Monitor Results and Adjust: Track the impact of changes and refine strategies accordingly.

-

Engage Teams and Foster a Cost-Conscious Culture: Encourage employee suggestions and recognize cost-saving initiatives.

Example 1: Reducing Scrap Costs in a Metal Fabrication Plant

- Situation: A metal fabrication plant noticed increasing scrap rates leading to higher material costs.

- Action: The cost management team implemented continuous monitoring of scrap rates per shift using real-time data collection.

- Analysis: Variance and root cause analysis revealed that older machines were causing defects during night shifts.

- Improvement: Scheduled preventive maintenance and operator retraining were introduced.

- Result: Scrap costs reduced by 25% within three months, improving overall cost efficiency.

Mind Map: Scrap Cost Reduction Process

Example 2: Energy Cost Optimization in a Plastic Manufacturing Facility

- Situation: Energy costs were a significant portion of overhead, fluctuating unpredictably.

- Action: The facility installed energy meters on key equipment to monitor consumption in real-time.

- Analysis: Trend analysis identified peak consumption during non-production hours.

- Improvement: Adjusted equipment schedules and implemented automated shutdown protocols.

- Result: Energy costs dropped by 18%, contributing to overall cost savings.

Mind Map: Energy Cost Monitoring and Improvement

Key Takeaways

- Continuous improvement through cost monitoring is an ongoing cycle, not a one-time event.

- Leveraging technology for real-time data collection enhances accuracy and responsiveness.

- Engaging cross-functional teams ensures comprehensive identification of cost-saving opportunities.

- Regularly reviewing and refining cost management strategies leads to sustained manufacturing efficiency and profitability.

By embedding continuous improvement into cost monitoring practices, manufacturing organizations empower accountants and cost managers to drive meaningful financial performance improvements while supporting operational excellence.

5. Strategic Cost Reduction Techniques

5.1 Value Chain Analysis for Cost Reduction Opportunities

Value Chain Analysis is a strategic tool used to identify the primary and support activities that create value for a company. By analyzing each step in the value chain, accountants and cost managers can pinpoint areas where costs can be reduced without compromising quality or customer satisfaction.

What is Value Chain Analysis?

The value chain represents the full range of activities required to bring a product or service from conception, through different phases of production, delivery to customers, and final disposal after use.

Primary Activities:

- Inbound Logistics

- Operations

- Outbound Logistics

- Marketing & Sales

- Service

Support Activities:

- Procurement

- Technology Development

- Human Resource Management

- Firm Infrastructure

Why Use Value Chain Analysis for Cost Reduction?

- Identifies cost drivers within each activity

- Highlights inefficient or redundant processes

- Helps prioritize cost reduction initiatives

- Aligns cost management with strategic business goals

Mind Map: Overview of Value Chain Analysis

Step-by-Step Approach to Value Chain Analysis for Cost Reduction

- Map the Value Chain: Document all activities involved in delivering the product/service.

- Analyze Costs: Break down costs associated with each activity.