Financial Reporting for Nonprofits

1. Introduction to Nonprofit Financial Reporting

1.1 Understanding the Purpose and Importance of Financial Reporting

Financial reporting is a fundamental aspect of nonprofit management that ensures transparency, accountability, and informed decision-making. Unlike for-profit organizations, nonprofits rely heavily on public trust and donor confidence, making accurate and clear financial reporting essential.

Why Financial Reporting Matters for Nonprofits

- Transparency: Demonstrates how funds are used, building trust with donors, grantors, and the public.

- Accountability: Shows that the organization is responsible for managing resources effectively and ethically.

- Compliance: Meets regulatory requirements from bodies such as the IRS, FASB, and state authorities.

- Decision-Making: Provides management and boards with critical financial data to guide strategy and operations.

- Fundraising: Helps attract and retain donors by showing financial health and stewardship.

Mind Map: Purpose of Financial Reporting in Nonprofits

Example: Transparency in Action

Consider a local animal shelter that receives donations from the community. By publishing an annual financial report showing how donations are spent—such as on veterinary care, food, and shelter maintenance—they reassure donors that their contributions are making a tangible impact. This transparency often leads to increased donations and community support.

Key Components of Financial Reporting

- Statement of Financial Position: Snapshot of assets, liabilities, and net assets.

- Statement of Activities: Shows revenues and expenses over a period.

- Statement of Cash Flows: Tracks cash inflows and outflows.

Mind Map: Key Components of Nonprofit Financial Reports

Example: Accountability Through Reporting

A nonprofit focused on education publishes quarterly financial reports to its board. When the board notices an unexpected increase in fundraising expenses, they can investigate and adjust strategies accordingly. This ongoing accountability helps prevent mismanagement and ensures resources are used effectively.

Summary

Financial reporting in nonprofits is not just a regulatory requirement but a strategic tool that fosters trust, supports compliance, and drives better organizational outcomes. By understanding its purpose and importance, nonprofit managers and accountants can create reports that truly reflect the organization’s mission and financial health.

1.2 Key Differences Between Nonprofit and For-Profit Financial Reporting

Financial reporting for nonprofits differs significantly from for-profit organizations due to their distinct missions, funding sources, and regulatory requirements. Understanding these differences is crucial for accountants and nonprofit managers to ensure accurate, transparent, and compliant financial statements.

Mind Map: Key Differences Between Nonprofit and For-Profit Financial Reporting

Purpose and Mission

- Nonprofits exist to fulfill a mission or public benefit, so financial reporting focuses on accountability and stewardship of resources.

- For-profits focus on profitability and maximizing shareholder value.

Example: A nonprofit animal shelter reports how donations are used to care for animals, while a for-profit pet store reports sales and profits.

Financial Statements Structure

| Aspect | Nonprofit Financial Statements | For-Profit Financial Statements |

|---|---|---|

| Primary Statements | Statement of Financial Position, Statement of Activities, Statement of Cash Flows | Balance Sheet, Income Statement, Statement of Cash Flows |

| Net Assets / Equity | Net assets categorized by donor restrictions | Equity includes stock, retained earnings |

Example:

- Nonprofit’s Statement of Activities shows changes in net assets by restriction category.

- For-profit’s Income Statement shows net income or loss.

Net Assets vs. Equity

Nonprofits classify net assets based on donor-imposed restrictions:

- Unrestricted Net Assets: No donor restrictions, available for general use.

- Temporarily Restricted Net Assets: Use limited by time or purpose.

- Permanently Restricted Net Assets: Principal must be maintained permanently.

For-profits report equity as ownership interest, including:

- Common stock

- Additional paid-in capital

- Retained earnings

Example: A nonprofit receives a $50,000 grant restricted for educational programs (temporarily restricted net assets). A for-profit reports retained earnings accumulated from prior years’ profits.

Revenue Recognition

- Nonprofits: Revenue often comes from contributions, grants, fundraising events, and membership dues. Recognition depends on donor restrictions and conditions.

- For-profits: Revenue is primarily from sales of goods or services, recognized when earned and realizable.

Example: A nonprofit receives a pledge of $10,000 to be used next year; it records this as temporarily restricted revenue until the funds are used. A for-profit recognizes revenue when a product is delivered.

Expense Classification

Nonprofits categorize expenses to demonstrate resource allocation:

- Program Services: Directly related to mission activities.

- Management and General: Administrative costs.

- Fundraising: Costs to solicit contributions.

For-profits classify expenses as:

- Cost of goods sold

- Selling, general, and administrative expenses

Example: A nonprofit spends $30,000 on a community outreach program (program services), $10,000 on office rent (management), and $5,000 on fundraising events.

Regulatory and Reporting Requirements

- Nonprofits: Must comply with FASB ASC 958, file IRS Form 990 annually, and adhere to donor restrictions.

- For-profits: Follow GAAP and, if public, SEC regulations.

Example: A nonprofit files Form 990 to disclose financial information publicly, promoting transparency to donors.

Summary Table of Key Differences

| Feature | Nonprofit | For-Profit |

|---|---|---|

| Primary Objective | Mission fulfillment and public accountability | Profit maximization and shareholder value |

| Financial Statements | Statement of Financial Position, Activities, Cash Flows | Balance Sheet, Income Statement, Cash Flows |

| Equity/Net Assets | Classified by donor restrictions | Shareholders’ equity |

| Revenue Sources | Contributions, grants, fundraising | Sales, services |

| Expense Reporting | Program, management, fundraising | Cost of goods sold, operating expenses |

| Regulatory Filings | IRS Form 990, FASB ASC 958 | GAAP, SEC filings (if public) |

Practical Example: Comparing Financial Reporting for a Nonprofit and a For-Profit

Scenario: Both organizations receive $100,000.

-

Nonprofit: Receives $100,000 grant restricted for youth programs.

- Records as temporarily restricted revenue.

- Expenses related to youth programs classified under program services.

- Reports net assets reflecting the restriction.

-

For-Profit: Sells products generating $100,000 revenue.

- Recognizes revenue when products are delivered.

- Expenses include cost of goods sold and operating expenses.

- Reports net income impacting retained earnings.

This example illustrates how the same amount of money is treated differently in financial reporting based on organizational type and purpose.

By understanding these key differences, nonprofit accountants and managers can prepare financial reports that accurately reflect their organization’s financial health, comply with regulations, and build trust with stakeholders.

1.3 Overview of Regulatory Requirements and Standards (FASB, GASB, IRS)

Nonprofit organizations operate under a unique set of regulatory requirements and accounting standards designed to ensure transparency, accountability, and proper stewardship of funds. Understanding these frameworks is essential for accountants and nonprofit managers to produce accurate financial reports and maintain compliance.

Key Regulatory Bodies and Standards

-

FASB (Financial Accounting Standards Board)

- Sets the Generally Accepted Accounting Principles (GAAP) for most nonprofits.

- Governs financial reporting for private nonprofit organizations.

-

GASB (Governmental Accounting Standards Board)

- Establishes accounting and financial reporting standards for government entities and certain nonprofits that are considered governmental or quasi-governmental.

-

IRS (Internal Revenue Service)

- Oversees tax-exempt status and requires annual filings such as Form 990.

- Enforces compliance with tax laws and public disclosure requirements.

Mind Map: Regulatory Framework for Nonprofit Financial Reporting

FASB Standards for Nonprofits

The FASB’s Accounting Standards Codification (ASC) Topic 958 specifically addresses nonprofit organizations. Key elements include:

- Statement of Financial Position: Classifies net assets into three categories — unrestricted, temporarily restricted, and permanently restricted.

- Statement of Activities: Reports revenues and expenses, showing changes in net assets.

- Statement of Cash Flows: Provides cash inflows and outflows categorized by operating, investing, and financing activities.

Example:

A nonprofit receives a $50,000 grant restricted for a specific program. Under FASB ASC 958, this amount is recorded as temporarily restricted net assets until used for the designated purpose.

Mind Map: FASB ASC 958 Key Components

GASB Standards and Applicability

GASB standards apply primarily to government entities and nonprofits that function as governmental units (e.g., public hospitals, universities). These standards emphasize fund accounting and accountability to the public.

Example:

A public university reports its financials under GASB standards, using fund accounting to separate restricted funds from general operating funds.

Mind Map: GASB Focus Areas

IRS Requirements for Nonprofits

The IRS governs tax-exempt organizations under Section 501(c)(3) and other subsections. Key reporting requirements include:

- Form 990: Annual information return detailing financial activities, governance, and compliance.

- Public Disclosure: Financial statements and Form 990 must be publicly available.

- Unrelated Business Income Tax (UBIT): Tax on income from activities unrelated to the nonprofit’s mission.

Example:

A nonprofit hosting a fundraising event sells merchandise unrelated to its mission. The income generated may be subject to UBIT and must be reported accordingly.

Mind Map: IRS Compliance Essentials

Integrated Example: Applying Standards in Practice

Scenario:

A nonprofit organization receives a $100,000 unrestricted donation, a $75,000 grant restricted for educational programs, and incurs $50,000 in program expenses and $20,000 in fundraising expenses.

- Under FASB ASC 958, the $100,000 is recorded as unrestricted net assets.

- The $75,000 grant is recorded as temporarily restricted net assets until spent.

- Expenses are classified between program and fundraising services in the Statement of Activities.

- The nonprofit files Form 990 with the IRS, disclosing these transactions and their impact on net assets.

This integrated approach ensures compliance with accounting standards and regulatory requirements while providing transparent financial reporting to stakeholders.

Summary

Understanding the roles of FASB, GASB, and IRS in nonprofit financial reporting enables organizations to:

- Prepare accurate and compliant financial statements.

- Maintain tax-exempt status and meet public disclosure obligations.

- Enhance transparency and accountability to donors, boards, and regulators.

Accountants and nonprofit managers should stay current with updates from these bodies to ensure ongoing compliance and best practices in financial reporting.

1.4 Common Financial Statements in Nonprofits: Statement of Financial Position, Activities, and Cash Flows

Nonprofit organizations rely on three primary financial statements to communicate their financial health, performance, and cash management. Understanding these statements is essential for accountants and nonprofit managers to ensure transparency, compliance, and informed decision-making.

Overview of the Three Core Financial Statements

Nonprofit Financial Statements Mind Map

Statement of Financial Position (Balance Sheet Equivalent)

This statement provides a snapshot of the nonprofit’s financial condition at a specific point in time. It details what the organization owns (assets), what it owes (liabilities), and the residual interest (net assets).

Key Components:

- Assets: Cash, accounts receivable, investments, property, equipment.

- Liabilities: Accounts payable, accrued expenses, notes payable.

- Net Assets: Classified as unrestricted, temporarily restricted, and permanently restricted.

Example:

| Statement of Financial Position | Amount ($) |

|---|---|

| Assets | |

| Cash | 50,000 |

| Accounts Receivable | 15,000 |

| Equipment | 35,000 |

| Total Assets | 100,000 |

| Liabilities | |

| Accounts Payable | 10,000 |

| Notes Payable | 20,000 |

| Total Liabilities | 30,000 |

| Net Assets | |

| Unrestricted | 40,000 |

| Temporarily Restricted | 20,000 |

| Permanently Restricted | 10,000 |

| Total Net Assets | 70,000 |

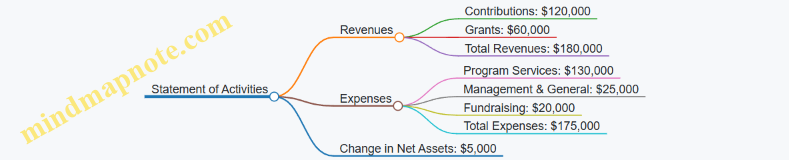

Statement of Activities (Income Statement Equivalent)

This statement shows the nonprofit’s financial performance over a period, detailing revenues and expenses and how net assets have changed.

Key Components:

- Revenues: Contributions, grants, program service fees, investment income.

- Expenses: Program services, management and general, fundraising.

- Change in Net Assets: Difference between total revenues and expenses.

Example:

| Statement of Activities | Amount ($) |

|---|---|

| Revenues | |

| Contributions | 120,000 |

| Grants | 80,000 |

| Program Service Fees | 30,000 |

| Investment Income | 5,000 |

| Total Revenues | 235,000 |

| Expenses | |

| Program Services | 150,000 |

| Management and General | 40,000 |

| Fundraising | 25,000 |

| Total Expenses | 215,000 |

| Change in Net Assets | 20,000 |

Statement of Cash Flows

This statement reports the cash inflows and outflows categorized by operating, investing, and financing activities, helping assess liquidity and cash management.

Key Components:

- Operating Activities: Cash received from donations, grants, payments for expenses.

- Investing Activities: Purchase or sale of equipment or investments.

- Financing Activities: Borrowing or repayment of loans.

Example:

| Statement of Cash Flows | Amount ($) |

|---|---|

| Operating Activities | |

| Cash received from donors | 200,000 |

| Cash paid for expenses | (180,000) |

| Net Cash from Operating Activities | 20,000 |

| Investing Activities | |

| Purchase of equipment | (10,000) |

| Sale of investments | 5,000 |

| Net Cash from Investing Activities | (5,000) |

| Financing Activities | |

| Loan proceeds | 15,000 |

| Loan repayments | (5,000) |

| Net Cash from Financing Activities | 10,000 |

| Net Increase in Cash | 25,000 |

Mind Map: Relationship Between Financial Statements

Best Practice Tips

- Consistency: Use consistent classifications across statements to improve clarity.

- Transparency: Clearly distinguish between restricted and unrestricted net assets.

- Reconciliation: Regularly reconcile cash flows with bank statements and the statement of financial position.

- Narrative: Supplement financial statements with notes explaining significant changes or unusual items.

By mastering these three core financial statements, nonprofit accountants and managers can provide stakeholders with a clear and comprehensive picture of the organization’s financial health and stewardship.

1.5 Best Practice: Establishing a Financial Reporting Calendar with Real-World Examples

Establishing a financial reporting calendar is a foundational best practice for nonprofits aiming to maintain transparency, ensure compliance, and facilitate strategic decision-making. A well-structured calendar helps nonprofit accountants and managers anticipate deadlines, allocate resources efficiently, and communicate financial information consistently to stakeholders.

Why Establish a Financial Reporting Calendar?

- Consistency: Ensures reports are generated regularly and on time.

- Accountability: Assigns clear responsibilities for each reporting task.

- Compliance: Helps meet regulatory and grant-related deadlines.

- Transparency: Provides stakeholders with predictable updates.

- Efficiency: Reduces last-minute rushes and errors.

Key Components of a Financial Reporting Calendar

Step-by-Step Guide to Creating Your Calendar

-

Identify Reporting Requirements:

- Internal (Board meetings, management reviews)

- External (IRS filings, grant reports, donor updates)

-

Define Reporting Periods:

- Monthly, quarterly, annually

- Align with fiscal year and grant cycles

-

Set Deadlines:

- Include preparation, review, and distribution dates

-

Assign Responsibilities:

- Specify who collects data, prepares reports, reviews, and distributes

-

Integrate Tools:

- Use software like QuickBooks Nonprofit, Sage Intacct, or Excel templates

- Set calendar reminders and alerts

-

Communicate Calendar:

- Share with finance team, program managers, and board members

-

Review and Update:

- Adjust calendar based on feedback and changing requirements

Real-World Example 1: Small Local Nonprofit

Organization: Community Food Bank

- Monthly: Prepare and review financial statements by the 10th of each month.

- Quarterly: Submit grant financial reports by the 15th following quarter end.

- Annually: Complete IRS Form 990 and audited financial statements by March 31.

- Responsibilities:

- Accountant prepares reports.

- Executive Director reviews.

- Board Treasurer receives reports.

Real-World Example 2: Mid-Sized Education Nonprofit

Organization: Youth Learning Initiative

- Monthly: Financial statements and budget variance analysis by the 7th.

- Bi-Monthly: Cash flow forecast updates.

- Quarterly: Board financial package including narrative explanations by the 20th.

- Semi-Annual: Internal control review and risk assessment.

- Annually: External audit and IRS filings.

Tips for Maintaining an Effective Reporting Calendar

- Use Shared Calendars: Google Calendar or Outlook for team visibility.

- Automate Reminders: Set automated alerts for upcoming deadlines.

- Regular Check-Ins: Monthly meetings to review progress and address bottlenecks.

- Document Processes: Maintain SOPs linked to calendar events.

- Flexibility: Allow buffer days for unexpected delays.

By implementing a financial reporting calendar tailored to your nonprofit’s size and complexity, you create a rhythm that supports accuracy, transparency, and trust with your stakeholders. This best practice not only streamlines internal workflows but also strengthens your organization’s financial stewardship.

Summary Mindmap:

2. Chart of Accounts and Fund Accounting

2.1 Designing a Chart of Accounts for Nonprofits: Principles and Examples

A well-structured Chart of Accounts (CoA) is the backbone of accurate and meaningful financial reporting for nonprofits. It organizes financial transactions into categories that reflect the organization’s activities, funding sources, and compliance requirements. This section will guide you through the principles of designing an effective CoA tailored for nonprofits, supported by practical examples and mind maps to visualize the structure.

Principles of Designing a Chart of Accounts for Nonprofits

-

Simplicity and Clarity

- Keep the CoA straightforward to avoid confusion.

- Use clear, descriptive account names.

-

Segmentation by Fund and Program

- Differentiate accounts based on restricted vs. unrestricted funds.

- Separate programmatic expenses from administrative and fundraising costs.

-

Compliance with Reporting Standards

- Align account categories with FASB standards (e.g., net asset classes).

- Ensure IRS Form 990 reporting requirements are met.

-

Scalability and Flexibility

- Design the CoA to accommodate organizational growth and new programs.

- Allow room for additional accounts without restructuring.

-

Consistency

- Maintain consistent account numbering and naming conventions.

- Facilitate easy comparison across periods.

Mind Map: High-Level Structure of a Nonprofit Chart of Accounts

Example: Sample Chart of Accounts Numbering System

| Account Number | Account Name | Description |

|---|---|---|

| 1000 | Assets | All asset accounts |

| 1100 | Cash and Cash Equivalents | Checking and savings accounts |

| 1200 | Accounts Receivable | Money owed to the nonprofit |

| 1300 | Prepaid Expenses | Payments made in advance |

| 1500 | Fixed Assets | Long-term assets like equipment |

| 2000 | Liabilities | All liability accounts |

| 2100 | Accounts Payable | Amounts owed to vendors |

| 2200 | Accrued Expenses | Expenses incurred but not yet paid |

| 3000 | Net Assets | Equity accounts reflecting fund balances |

| 3100 | Unrestricted Net Assets | Funds without donor restrictions |

| 3200 | Temporarily Restricted Net Assets | Funds with time or purpose restrictions |

| 3300 | Permanently Restricted Net Assets | Endowment or permanently restricted funds |

| 4000 | Revenue | Income sources |

| 4100 | Contributions | Donations received |

| 4200 | Grants | Grant income |

| 4300 | Program Service Revenue | Fees for services provided |

| 4400 | Investment Income | Interest, dividends |

| 5000 | Expenses | Costs incurred |

| 5100 | Program Services | Direct program costs |

| 5200 | Management and General | Administrative expenses |

| 5300 | Fundraising | Costs related to fundraising activities |

Example: Designing Fund-Specific Accounts

To track restricted funds separately, nonprofits often append fund codes to account numbers or create sub-accounts.

| Account Number | Account Name | Description |

|---|---|---|

| 4100-01 | Contributions - General Fund | Unrestricted contributions |

| 4100-02 | Contributions - Education Fund | Temporarily restricted for education |

| 4100-03 | Contributions - Endowment Fund | Permanently restricted contributions |

This approach allows for detailed reporting on fund usage without mixing balances.

Mind Map: Expense Classification in the Chart of Accounts

Practical Example: Nonprofit XYZ’s Chart of Accounts Snapshot

Assets:

- 1010 Cash - Operating Account

- 1020 Cash - Grant Fund

- 1200 Accounts Receivable - Donations

Liabilities:

- 2010 Accounts Payable

- 2100 Accrued Payroll

Net Assets:

- 3110 Unrestricted Net Assets

- 3210 Temporarily Restricted - Building Fund

Revenue:

- 4110 Contributions - General

- 4120 Contributions - Capital Campaign

- 4200 Government Grants

Expenses:

- 5110 Program Services - Community Outreach

- 5120 Program Services - Education

- 5210 Management and General

- 5310 Fundraising Events

Summary

Designing a Chart of Accounts for nonprofits requires balancing clarity, compliance, and flexibility. By segmenting accounts according to fund restrictions and program activities, nonprofits can produce transparent and insightful financial reports that meet stakeholder and regulatory expectations. Using consistent numbering and naming conventions, along with thoughtful categorization, ensures that financial data is both accurate and actionable.

For further reading, consider exploring sample CoA templates from nonprofit accounting software providers or consulting the FASB Accounting Standards Codification (ASC) Topic 958 for nonprofit organizations.

2.2 Understanding Fund Accounting and Its Impact on Reporting

Fund accounting is a specialized accounting system used by nonprofits to ensure and demonstrate compliance with donor restrictions and legal requirements. Unlike for-profit entities that focus primarily on profitability, nonprofits must track resources according to their purpose and restrictions. This is where fund accounting plays a critical role.

What is Fund Accounting?

Fund accounting segregates resources into different “funds” based on their intended use. Each fund is treated as a separate accounting entity with its own set of accounts.

Key Characteristics:

- Ensures accountability by tracking restricted and unrestricted resources separately.

- Helps organizations report financial position and activities clearly.

- Supports compliance with donor-imposed restrictions and grant requirements.

Types of Funds in Nonprofit Accounting

Nonprofits typically classify funds into three broad categories:

- Unrestricted Funds: Resources without donor-imposed restrictions, available for general operations.

- Temporarily Restricted Funds: Resources restricted by donors for a specific purpose or time period.

- Permanently Restricted Funds: Resources that must be maintained permanently, typically endowments.

Impact of Fund Accounting on Financial Reporting

Fund accounting affects how financial statements are prepared and presented. It ensures transparency and accountability by showing how resources are used according to donor intentions.

Example: A nonprofit receives a $50,000 grant restricted for a youth education program (temporarily restricted fund). Fund accounting requires this grant to be tracked separately from general donations. When the grant is spent on the program, the restriction is released, and the funds move from temporarily restricted to unrestricted net assets.

Practical Example: Fund Accounting in Action

Scenario: The “Helping Hands” nonprofit has the following funds:

- General Fund (Unrestricted): Covers daily operations.

- Building Fund (Temporarily Restricted): For renovating the community center.

- Endowment Fund (Permanently Restricted): Principal must be preserved.

Transactions:

- Received $100,000 unrestricted donation.

- Received $200,000 grant restricted for building renovation.

- Spent $50,000 on renovation.

Accounting Treatment:

- Record $100,000 in the General Fund.

- Record $200,000 in the Building Fund.

- When $50,000 is spent, recognize expense in Building Fund and reduce temporarily restricted net assets accordingly.

Reporting Impact:

- The Statement of Financial Position shows net assets by fund type.

- The Statement of Activities reports revenues and expenses separately for each fund.

Mind Map: Fund Accounting Workflow

Best Practices for Fund Accounting

- Clearly Define Fund Categories: Establish clear policies on fund classification.

- Use Accounting Software with Fund Tracking: Automate segregation and reporting.

- Regularly Review Fund Restrictions: Ensure compliance with donor requirements.

- Train Staff and Board: Ensure understanding of fund accounting principles.

Summary

Fund accounting is essential for nonprofits to maintain transparency, meet regulatory requirements, and honor donor restrictions. By segregating resources into funds and reporting accordingly, nonprofits build trust and demonstrate responsible stewardship of resources.

For nonprofit managers and accountants, mastering fund accounting is a foundational skill that directly impacts the quality and credibility of financial reporting.

2.3 Best Practice: Segregating Restricted and Unrestricted Funds with Sample Account Setups

Introduction

In nonprofit financial reporting, correctly segregating restricted and unrestricted funds is critical to ensure transparency, compliance, and accurate financial management. Restricted funds are those given with donor-imposed limitations on their use, while unrestricted funds can be used at the organization’s discretion.

Proper segregation helps nonprofits demonstrate accountability to donors and stakeholders and ensures resources are used according to their intended purposes.

Understanding Fund Restrictions

- Unrestricted Funds: Resources available for general operations or any purpose.

- Temporarily Restricted Funds: Funds restricted by donors for a specific purpose or time period.

- Permanently Restricted Funds: Endowments or funds that must be maintained intact indefinitely, with only earnings available for use.

Mind Map: Types of Funds and Their Characteristics

Best Practice: Segregating Funds in the Chart of Accounts

To effectively segregate funds, nonprofits should design their chart of accounts to clearly differentiate between unrestricted and restricted funds. This can be done by assigning distinct account number ranges or prefixes for each fund type.

Sample Account Setup

| Account Number | Account Name | Fund Type | Description |

|---|---|---|---|

| 1000 | Assets - Unrestricted | Unrestricted | Cash, receivables, and other assets available for general use |

| 1100 | Assets - Temporarily Restricted | Temporarily Restricted | Assets restricted for specific programs or time periods |

| 1200 | Assets - Permanently Restricted | Permanently Restricted | Endowment principal and related assets |

| 2000 | Liabilities - Unrestricted | Unrestricted | General liabilities |

| 2100 | Liabilities - Temporarily Restricted | Temporarily Restricted | Liabilities related to restricted funds |

| 3000 | Net Assets - Unrestricted | Unrestricted | Net assets without donor restrictions |

| 3100 | Net Assets - Temporarily Restricted | Temporarily Restricted | Net assets with donor-imposed restrictions |

| 3200 | Net Assets - Permanently Restricted | Permanently Restricted | Net assets to be maintained permanently |

Example: Chart of Accounts Segment for Fund Segregation

Example Scenario: Recording a Temporarily Restricted Grant

Scenario: Your nonprofit receives a $50,000 grant restricted for a youth education program.

Journal Entry:

| Account | Debit | Credit |

|---|---|---|

| 1100 Assets - Temporarily Restricted (Cash) | $50,000 | |

| 3100 Net Assets - Temporarily Restricted | $50,000 |

When the funds are spent on the program:

| Account | Debit | Credit |

|---|---|---|

| Program Expense | $50,000 | |

| 1100 Assets - Temporarily Restricted (Cash) | $50,000 |

And to release the restriction:

| Account | Debit | Credit |

|---|---|---|

| 3100 Net Assets - Temporarily Restricted | $50,000 | |

| 3000 Net Assets - Unrestricted | $50,000 |

This sequence ensures the grant is tracked separately until spent and then reclassified appropriately.

Mind Map: Fund Segregation Process

Additional Tips

- Use Subaccounts: For large nonprofits, create subaccounts under each fund type to track individual grants or donations.

- Regular Reconciliation: Periodically reconcile fund balances to ensure accuracy.

- Clear Documentation: Maintain donor agreements and restriction details to support fund classification.

Summary

Segregating restricted and unrestricted funds is essential for nonprofit accountability. By designing a clear chart of accounts and following consistent recording practices, nonprofits can provide transparent financial reports that meet donor and regulatory expectations.

This best practice, supported by structured account setups and clear examples, empowers accountants and nonprofit managers to maintain financial integrity and build stakeholder trust.

2.4 Case Study: Implementing Fund Accounting in a Mid-Sized Nonprofit Organization

Introduction

Fund accounting is a cornerstone of nonprofit financial management, ensuring that resources are tracked and reported according to donor restrictions and organizational purposes. This case study explores how a mid-sized nonprofit, “GreenFuture Initiative,” successfully implemented fund accounting to enhance transparency, compliance, and financial control.

Background of GreenFuture Initiative

- Mission: Environmental conservation and education

- Annual Budget: $5 million

- Programs: Community Outreach, Research Grants, Educational Workshops

- Funding Sources: Government grants, private donations, corporate sponsorships

Challenges Before Implementation

- Difficulty segregating restricted and unrestricted funds

- Inconsistent reporting to donors and grantors

- Limited visibility into program-specific financial performance

- Manual tracking leading to errors and inefficiencies

Objectives for Fund Accounting Implementation

- Establish clear segregation of funds according to donor restrictions

- Improve accuracy and timeliness of financial reports

- Enable program managers to monitor their budgets effectively

- Ensure compliance with FASB standards and grant requirements

Step 1: Designing the Chart of Accounts

GreenFuture restructured their chart of accounts to reflect fund accounting principles.

Mind Map: Chart of Accounts Structure

Example:

- Account 1001: Cash - Unrestricted

- Account 1002: Cash - Temporarily Restricted (e.g., grant funds for Research Grants)

Step 2: Setting Up Fund Classes in Accounting Software

GreenFuture used QuickBooks Nonprofit edition, creating fund classes to track each funding source and restriction.

Mind Map: Fund Classes Setup

Example:

- A $50,000 grant received for Research Grants is recorded under the “Research Grant Fund” class.

Step 3: Recording Transactions with Fund Restrictions

Each transaction is tagged with the appropriate fund class to maintain segregation.

Example Transaction:

- Received $20,000 donation unrestricted: Debit Cash - Unrestricted, Credit Contributions - Unrestricted

- Spent $5,000 on Educational Workshops funded by the Education Sponsorship Fund: Debit Educational Workshops Expense, Credit Cash - Temporarily Restricted

Step 4: Reporting and Analysis

GreenFuture generated fund-specific financial statements, enabling clear visibility.

Mind Map: Fund Reporting Components

Example:

- The Statement of Activities for the Research Grant Fund shows $100,000 revenue and $80,000 expenses, indicating $20,000 net increase in temporarily restricted net assets.

Step 5: Training and Ongoing Monitoring

- Conducted workshops for accounting and program staff on fund accounting principles

- Established monthly fund reconciliation and reporting cycles

Outcomes and Benefits

- Enhanced transparency to donors and grantors through clear fund reporting

- Improved compliance with grant restrictions and accounting standards

- Empowered program managers with accurate financial data for decision-making

- Reduced errors and streamlined financial close process

Summary Mind Map: Fund Accounting Implementation Process

Final Thoughts

Implementing fund accounting can seem complex, but as GreenFuture Initiative’s experience shows, a structured approach with clear objectives, proper tools, and staff engagement leads to successful adoption. This foundation supports financial integrity and strengthens stakeholder trust.

3. Preparing the Statement of Financial Position

3.1 Components of the Statement of Financial Position Explained

The Statement of Financial Position, often referred to as the Balance Sheet in for-profit organizations, is a critical financial statement for nonprofits. It provides a snapshot of the organization’s financial health at a specific point in time by detailing what the nonprofit owns (assets), what it owes (liabilities), and the net assets (equity) that represent the residual interest in the assets after liabilities are deducted.

Understanding each component is essential for accurate reporting and informed decision-making. Below, we break down the main components with explanations, examples, and mind maps to visualize their relationships.

Main Components:

Assets

Assets represent resources owned or controlled by the nonprofit that are expected to provide future economic benefits.

Example:

- Cash and Cash Equivalents: Money in checking accounts or petty cash.

- Accounts Receivable: Pledges from donors expected to be received.

- Property, Plant, and Equipment: Buildings, office equipment, and vehicles used in operations.

Mind Map:

Example Scenario:

A nonprofit has $50,000 in cash, $20,000 in pledges receivable, and owns a building valued at $200,000. These would be recorded under assets accordingly.

Liabilities

Liabilities are obligations the nonprofit must settle in the future, such as debts or unpaid bills.

Example:

- Accounts Payable: Invoices from vendors for office supplies.

- Accrued Expenses: Salaries earned by employees but not yet paid.

- Deferred Revenue: Grants received but not yet earned.

Mind Map:

Example Scenario:

If the nonprofit owes $10,000 to suppliers and has a $100,000 mortgage on its building, these amounts are recorded as liabilities.

Net Assets

Net assets represent the difference between assets and liabilities and reflect the nonprofit’s equity. They are classified based on donor-imposed restrictions.

- Without Donor Restrictions: Funds available for general use.

- With Donor Restrictions: Funds restricted for specific purposes or time periods.

- Permanently Restricted: Funds that must be maintained permanently, such as endowments.

Mind Map:

Example:

A nonprofit has $150,000 in unrestricted net assets, $50,000 temporarily restricted for a new program, and $100,000 permanently restricted as an endowment.

Integrated Example: Statement of Financial Position Snapshot

| Assets | Amount | Liabilities & Net Assets | Amount |

|---|---|---|---|

| Current Assets | Current Liabilities | ||

| Cash and Cash Equivalents | $50,000 | Accounts Payable | $10,000 |

| Accounts Receivable | $20,000 | Accrued Expenses | $5,000 |

| Prepaid Expenses | $3,000 | Deferred Revenue | $15,000 |

| Non-Current Assets | Long-term Liabilities | ||

| Property, Plant & Equipment | $200,000 | Mortgage Payable | $100,000 |

| Total Assets | $273,000 | Total Liabilities | $130,000 |

| Net Assets | |||

| Without Donor Restrictions | $150,000 | ||

| With Donor Restrictions (Temp.) | $50,000 | ||

| Permanently Restricted | $100,000 | ||

| Total Net Assets | $300,000 |

Note: In this example, total net assets plus liabilities exceed total assets because of timing or valuation differences; in practice, these must balance. This highlights the importance of accurate classification and reconciliation.

Summary

Understanding the components of the Statement of Financial Position helps nonprofit accountants and managers accurately report financial status, comply with regulations, and communicate effectively with stakeholders. Using clear classifications and examples ensures transparency and supports strategic planning.

For further reading, consider exploring how these components interact with other financial statements such as the Statement of Activities and Cash Flow Statement.

3.2 Best Practice: Classifying Assets and Liabilities with Practical Examples

Proper classification of assets and liabilities is fundamental to accurate nonprofit financial reporting. It ensures transparency, aids in compliance, and provides stakeholders with a clear understanding of the organization’s financial health.

Understanding Asset Classification

Assets are resources owned or controlled by the nonprofit that provide future economic benefits. They are generally classified into current and non-current (long-term) assets.

- Current Assets: Expected to be converted into cash or used up within one year.

- Non-Current Assets: Held for longer than one year, often used in operations.

Mind Map: Asset Classification

Practical Example: Asset Classification

| Asset Item | Classification | Explanation |

|---|---|---|

| Cash in Checking Account | Current Asset | Readily available for operations |

| Pledge Receivable (due in 6 months) | Current Asset | Expected to be collected within one year |

| Office Building | Non-Current Asset | Used for operations, held long-term |

| Prepaid Insurance | Current Asset | Benefits to be realized within the year |

| Endowment Fund Investments | Non-Current Asset | Held for long-term growth and income generation |

Understanding Liability Classification

Liabilities represent obligations the nonprofit must settle. Like assets, liabilities are classified as current and long-term.

- Current Liabilities: Obligations due within one year.

- Long-Term Liabilities: Obligations due beyond one year.

Mind Map: Liability Classification

Practical Example: Liability Classification

| Liability Item | Classification | Explanation |

|---|---|---|

| Accounts Payable | Current Liability | Amounts owed to vendors, payable within 30 days |

| Deferred Grant Revenue | Current Liability | Funds received but not yet earned, due within year |

| Mortgage Payable | Long-Term Liability | Debt on property, payable over 15 years |

| Accrued Payroll | Current Liability | Salaries earned but not yet paid |

Best Practices for Classification

- Review Timing: Always consider the expected timing of cash flows to determine current vs. non-current.

- Use Clear Definitions: Align classifications with FASB ASC 958 standards for nonprofits.

- Consistent Application: Apply classifications consistently across reporting periods.

- Document Assumptions: Keep detailed notes on classification decisions for audit trails.

- Reassess Regularly: Periodically review classifications, especially for long-term receivables or liabilities.

Integrated Example: Statement of Financial Position Snapshot

| Assets | Amount (USD) | Liabilities and Net Assets | Amount (USD) |

|---|---|---|---|

| Current Assets | Current Liabilities | ||

| Cash and Cash Equivalents | 150,000 | Accounts Payable | 40,000 |

| Accounts Receivable | 60,000 | Accrued Expenses | 15,000 |

| Prepaid Expenses | 10,000 | Deferred Revenue | 25,000 |

| Non-Current Assets | Long-Term Liabilities | ||

| Property, Plant & Equipment | 500,000 | Mortgage Payable | 300,000 |

| Long-Term Investments | 200,000 | ||

| Total Assets | 920,000 | Total Liabilities | 380,000 |

| Net Assets | 540,000 |

Summary

Correct classification of assets and liabilities enhances the clarity and usefulness of nonprofit financial statements. By following the outlined best practices and using clear examples, nonprofit accountants and managers can ensure accurate reporting that supports organizational transparency and stakeholder trust.

3.3 Handling Net Assets: Unrestricted, Temporarily Restricted, and Permanently Restricted

Nonprofit organizations classify their net assets into three main categories to provide clarity on the availability and restrictions of resources. Understanding these classifications is essential for accurate financial reporting and transparency to stakeholders.

What Are Net Assets?

Net assets represent the difference between total assets and total liabilities of a nonprofit. They indicate the residual interest in the organization’s resources after obligations are met.

Categories of Net Assets

-

Unrestricted Net Assets

- Resources without donor-imposed restrictions.

- Can be used at the discretion of the nonprofit for any purpose.

- Examples: General operating funds, board-designated funds.

-

Temporarily Restricted Net Assets

- Resources subject to donor-imposed restrictions that will expire with time or by fulfilling certain conditions.

- Examples: Grants restricted for a specific program or capital campaign, funds restricted until a future date.

-

Permanently Restricted Net Assets

- Resources that donors require to be maintained permanently.

- Only the income generated from these assets can be used, not the principal.

- Examples: Endowment funds where the principal is preserved.

Mind Map: Overview of Net Assets

Best Practice: Clear Segregation and Reporting

Maintaining clear segregation of net assets in accounting systems and financial statements ensures transparency and compliance. Use specific ledger accounts for each category and regularly review restrictions with legal counsel or donor agreements.

Example 1: Recording a Temporarily Restricted Grant

Scenario: A nonprofit receives a $50,000 grant restricted for a youth education program to be used within the next fiscal year.

Accounting Treatment:

- Record $50,000 as an increase in Temporarily Restricted Net Assets.

- When funds are spent on the program, reclassify the amount from Temporarily Restricted to Unrestricted net assets to reflect the expiration of the restriction.

Journal Entries:

| Date | Account | Debit | Credit |

|---|---|---|---|

| Receipt | Cash | 50,000 | |

| Receipt | Temporarily Restricted Net Assets | 50,000 | |

| Expense | Program Expense | 20,000 | |

| Expense | Cash | 20,000 | |

| Reclassification | Temporarily Restricted Net Assets | 20,000 | |

| Reclassification | Unrestricted Net Assets | 20,000 |

Mind Map: Temporarily Restricted Net Assets Lifecycle

Example 2: Managing Permanently Restricted Endowment

Scenario: A donor gives $100,000 to establish an endowment where the principal must remain intact, but the nonprofit can use the investment income.

Accounting Treatment:

- Record $100,000 as Permanently Restricted Net Assets.

- Investment income earned (e.g., $5,000) is recorded as Temporarily Restricted or Unrestricted depending on donor stipulations.

Journal Entries:

| Date | Account | Debit | Credit |

|---|---|---|---|

| Receipt | Cash | 100,000 | |

| Receipt | Permanently Restricted Net Assets | 100,000 | |

| Investment Income | Cash | 5,000 | |

| Investment Income | Temporarily Restricted Net Assets | 5,000 |

When the income is used:

| Date | Account | Debit | Credit |

|---|---|---|---|

| Expense | Program Expense | 5,000 | |

| Expense | Cash | 5,000 | |

| Reclassification | Temporarily Restricted Net Assets | 5,000 | |

| Reclassification | Unrestricted Net Assets | 5,000 |

Mind Map: Permanently Restricted Net Assets and Income Use

Practical Tips for Accountants and Nonprofit Managers

- Review donor agreements carefully to determine the nature of restrictions.

- Maintain separate ledger accounts for each net asset category.

- Communicate clearly in financial statements the amounts and nature of restrictions.

- Use footnotes to explain any significant donor restrictions or changes.

- Regularly reconcile and reclassify net assets as restrictions expire or conditions are met.

Summary Table: Net Assets at a Glance

| Net Asset Type | Description | Example Use Case | Accounting Treatment |

|---|---|---|---|

| Unrestricted | No donor restrictions | General operations | Recorded as unrestricted net assets |

| Temporarily Restricted | Donor restrictions expire with time/purpose | Program-specific grants | Recorded as temporarily restricted; reclassified when restrictions expire |

| Permanently Restricted | Principal must be maintained permanently | Endowment funds | Recorded as permanently restricted; income recorded separately and used accordingly |

By mastering the handling of net assets, nonprofit accountants and managers can ensure accurate financial reporting that reflects the organization’s fiduciary responsibilities and builds trust with donors and stakeholders.

3.4 Example Walkthrough: Preparing a Statement of Financial Position for a Community Charity

Preparing a Statement of Financial Position (also known as the Balance Sheet) is a critical step in nonprofit financial reporting. It provides a snapshot of the organization’s financial health at a specific point in time by listing its assets, liabilities, and net assets.

Step 1: Understand the Components

The Statement of Financial Position consists of three main sections:

- Assets: What the organization owns or controls

- Liabilities: What the organization owes

- Net Assets: The residual interest in the assets after deducting liabilities, categorized by restrictions

Mind Map: Components of Statement of Financial Position

Step 2: Gather Financial Data for the Community Charity

Let’s consider “Helping Hands Community Charity,” which operates locally to provide food and shelter. Below is the summarized financial data as of December 31, 2023:

| Item | Amount (USD) |

|---|---|

| Cash and Cash Equivalents | 50,000 |

| Accounts Receivable | 15,000 |

| Prepaid Rent | 5,000 |

| Property and Equipment (net) | 120,000 |

| Accounts Payable | 10,000 |

| Accrued Expenses | 7,000 |

| Deferred Revenue | 8,000 |

| Notes Payable (Long-Term) | 40,000 |

| Unrestricted Net Assets | 90,000 |

| Temporarily Restricted Assets | 35,000 |

| Permanently Restricted Assets | 0 |

Step 3: Classify and Organize the Data

-

Assets:

- Current Assets:

- Cash and Cash Equivalents: $50,000

- Accounts Receivable: $15,000

- Prepaid Rent: $5,000

- Long-Term Assets:

- Property and Equipment (net): $120,000

- Current Assets:

-

Liabilities:

- Current Liabilities:

- Accounts Payable: $10,000

- Accrued Expenses: $7,000

- Deferred Revenue: $8,000

- Long-Term Liabilities:

- Notes Payable: $40,000

- Current Liabilities:

-

Net Assets:

- Unrestricted: $90,000

- Temporarily Restricted: $35,000

- Permanently Restricted: $0

Step 4: Construct the Statement of Financial Position

Helping Hands Community Charity

Statement of Financial Position

As of December 31, 2023

| ASSETS | LIABILITIES & NET ASSETS | ||

|---|---|---|---|

| Current Assets: | Current Liabilities: | ||

| Cash and Cash Equivalents | 50,000 | Accounts Payable | 10,000 |

| Accounts Receivable | 15,000 | Accrued Expenses | 7,000 |

| Prepaid Rent | 5,000 | Deferred Revenue | 8,000 |

| Total Current Assets | 70,000 | Total Current Liabilities | 25,000 |

| Long-Term Assets: | Long-Term Liabilities: | ||

| Property and Equipment (net) | 120,000 | Notes Payable | 40,000 |

| Total Long-Term Assets | 120,000 | Total Long-Term Liabilities | 40,000 |

| Total Assets | 190,000 | Total Liabilities | 65,000 |

| Net Assets: | |||

| Unrestricted | 90,000 | ||

| Temporarily Restricted | 35,000 | ||

| Permanently Restricted | 0 | ||

| Total Net Assets | 125,000 | ||

| Total Liabilities & Net Assets | 190,000 |

Step 5: Review and Analyze

- Balance Check: Total Assets ($190,000) = Total Liabilities + Net Assets ($65,000 + $125,000)

- Net Asset Composition: Majority unrestricted, indicating flexibility in fund usage.

- Liabilities: Current liabilities are manageable relative to current assets.

Best Practice Tips

- Use Clear Classifications: Separate current and long-term assets/liabilities for clarity.

- Reconcile Accounts: Ensure all balances come from reconciled general ledger accounts.

- Disclose Restrictions: Clearly identify net asset restrictions to comply with donor requirements.

- Regular Updates: Prepare this statement monthly or quarterly to monitor financial position.

Additional Mind Map: Preparing Statement of Financial Position

This example walkthrough demonstrates how nonprofit accountants and managers can prepare a clear, compliant, and insightful Statement of Financial Position that reflects the true financial standing of their organization.

3.5 Common Pitfalls and How to Avoid Them

Financial reporting for nonprofits is critical for transparency, compliance, and informed decision-making. However, several common pitfalls can undermine the quality and reliability of these reports. Below, we explore these pitfalls along with practical strategies and examples to avoid them.

Pitfall 1: Misclassification of Net Assets

Description: Nonprofits must classify net assets into unrestricted, temporarily restricted, and permanently restricted categories. Misclassification can mislead stakeholders about the organization’s financial health.

How to Avoid:

- Understand donor restrictions clearly.

- Maintain detailed documentation for each contribution.

- Use fund accounting to segregate resources.

Example: A nonprofit received a $50,000 donation restricted for building renovation. Recording it as unrestricted inflates available funds and may cause overspending.

Mind Map:

Pitfall 2: Incomplete or Inaccurate Revenue Recognition

Description: Recognizing revenue prematurely or failing to recognize conditional contributions can distort financial results.

How to Avoid:

- Follow FASB ASC 958 guidelines for revenue recognition.

- Identify conditions attached to grants and contributions.

- Record revenue only when conditions are substantially met.

Example: A grant requires submission of a progress report before funds are released. Recording the full amount upon grant award rather than upon meeting conditions inflates revenue.

Mind Map:

Pitfall 3: Poor Expense Allocation

Description: Expenses must be properly allocated among program services, management, and fundraising. Misallocation affects program efficiency metrics and donor trust.

How to Avoid:

- Develop clear criteria for expense classification.

- Use time tracking and cost allocation methods.

- Review allocations regularly.

Example: Administrative salaries charged entirely to program services without justification can misrepresent program costs.

Mind Map:

Pitfall 4: Neglecting Reconciliation and Review Processes

Description: Failing to reconcile accounts or review financial statements can lead to errors going undetected.

How to Avoid:

- Implement monthly bank and ledger reconciliations.

- Conduct internal reviews before finalizing reports.

- Use checklists to ensure completeness.

Example: Unreconciled bank accounts led to unnoticed duplicate payments, causing cash shortages.

Mind Map:

Pitfall 5: Inadequate Disclosure and Transparency

Description: Insufficient notes and disclosures reduce stakeholder confidence and may violate reporting standards.

How to Avoid:

- Include comprehensive notes explaining accounting policies, restrictions, and contingencies.

- Follow FASB disclosure requirements.

- Review disclosures with auditors.

Example: A nonprofit failed to disclose a significant pending lawsuit, which later affected donor trust.

Mind Map:

Summary Table of Common Pitfalls and Solutions

| Pitfall | Cause | Consequence | Best Practice to Avoid | Example Scenario |

|---|---|---|---|---|

| Misclassification of Net Assets | Poor donor restriction understanding | Misleading financial position | Fund accounting, clear documentation | Recording restricted donation as unrestricted |

| Inaccurate Revenue Recognition | Ignoring grant conditions | Overstated revenue | Follow FASB ASC 958, review agreements | Recognizing conditional grant prematurely |

| Poor Expense Allocation | Lack of clear policies | Misleading program costs | Define allocation criteria, time tracking | Charging admin salaries fully to programs |

| Neglecting Reconciliation | Time constraints, no procedures | Undetected errors, financial loss | Monthly reconciliations, checklists | Duplicate payments due to unreconciled accounts |

| Inadequate Disclosure | Lack of awareness | Reduced transparency | Comprehensive notes, auditor review | Not disclosing pending lawsuit |

By proactively addressing these common pitfalls through clear policies, regular training, and robust internal controls, nonprofit accountants and managers can ensure accurate, transparent, and compliant financial reporting that builds trust with donors, boards, and regulators.

4. Preparing the Statement of Activities

4.1 Understanding Revenue Recognition in Nonprofits

Revenue recognition is a fundamental aspect of nonprofit financial reporting. It determines when and how revenue is recorded in the financial statements, ensuring transparency and accuracy in reflecting the organization’s financial health.

What is Revenue Recognition?

Revenue recognition is the accounting principle that dictates the specific conditions under which income becomes realized or realizable and earned, and thus recorded in the financial statements.

In nonprofits, revenue can come from various sources such as donations, grants, membership fees, program service fees, and fundraising events. Each source may have different recognition criteria.

Key Principles of Revenue Recognition for Nonprofits

- Earned vs. Received: Revenue is recognized when earned, not necessarily when cash is received.

- Conditional vs. Unconditional Contributions: Conditional contributions are recognized only when conditions are met.

- Restricted vs. Unrestricted Funds: Revenue classification depends on donor-imposed restrictions.

Mind Map: Revenue Recognition Overview

Types of Revenue and Recognition Examples

-

Unconditional Contributions

- Recognized immediately when the promise to give is received.

- Example: A donor pledges $10,000 with no restrictions. The nonprofit recognizes $10,000 as revenue upon pledge.

-

Conditional Contributions

- Recognized only when conditions are substantially met.

- Example: A grant of $50,000 is awarded contingent on completing a community project. Revenue is recognized as project milestones are met.

-

Program Service Fees

- Recognized when services are performed.

- Example: A nonprofit charges $100 per workshop attended. Revenue is recognized after each workshop.

-

Membership Dues

- Recognized over the membership period.

- Example: A $120 annual membership fee is recognized as $10 per month over 12 months.

-

Fundraising Events

- Gross revenue recognized less direct costs.

- Example: A gala raises $30,000 in ticket sales with $5,000 in direct event expenses. Net revenue recognized is $25,000.

Mind Map: Conditional vs. Unconditional Contributions

Best Practice: Documenting Revenue Recognition Policies

- Clearly define revenue categories and recognition criteria in the accounting policies.

- Maintain documentation of donor restrictions and conditions.

- Regularly review contracts and grant agreements for revenue recognition triggers.

Example Scenario: Recognizing a Government Grant

A nonprofit receives a $100,000 government grant to provide educational services over 12 months. The grant is conditional on delivering monthly reports and meeting service targets.

- Recognition Approach: Revenue is recognized monthly as services are delivered and reporting requirements are met.

- Accounting Entry: Each month, recognize $8,333 as revenue (100,000 / 12).

Summary

Understanding revenue recognition in nonprofits ensures that financial statements accurately reflect the timing and nature of income. Proper classification between conditional and unconditional contributions, as well as restricted and unrestricted funds, is essential for compliance and transparency.

For nonprofit accountants and managers, mastering revenue recognition principles helps maintain trust with donors, comply with regulations, and provide meaningful financial insights to stakeholders.

4.2 Best Practice: Reporting Contributions and Grants with Illustrative Examples

Effective reporting of contributions and grants is essential for nonprofits to maintain transparency, meet compliance requirements, and build trust with donors and stakeholders. This section outlines best practices for accurately recognizing, classifying, and reporting these revenues, supported by illustrative examples and mind maps to clarify the concepts.

Understanding Contributions and Grants

- Contributions: Voluntary, unconditional transfers of cash or other assets to a nonprofit. Can be restricted or unrestricted.

- Grants: Funds provided by government agencies, foundations, or corporations, often with specific conditions or reporting requirements.

Key Principles for Reporting Contributions and Grants

- Recognition: Contributions and grants should be recognized as revenue when received or unconditionally promised.

- Restrictions: Identify whether funds are unrestricted, temporarily restricted, or permanently restricted.

- Disclosure: Clearly disclose the nature, amount, and restrictions of contributions and grants in financial statements.

Mind Map: Reporting Contributions and Grants

Step-by-Step Best Practice Guide

-

Identify the Type of Contribution or Grant

- Example: A $50,000 grant from a foundation to support a new program for one year.

-

Determine Restrictions

- Is the grant restricted to a specific purpose or time period?

- Example: The $50,000 grant is temporarily restricted for program expenses in 2024.

-

Record the Contribution or Grant

- Debit Cash or Pledges Receivable

- Credit Revenue in the appropriate net asset class

-

Track and Monitor Usage

- Ensure expenses align with restrictions

-

Report in Financial Statements

- Show revenue under the correct net asset category

- Provide notes explaining restrictions and conditions

Illustrative Example 1: Unrestricted Contribution

Scenario: A donor gives $10,000 with no restrictions.

Accounting Entry:

- Debit Cash $10,000

- Credit Unrestricted Contribution Revenue $10,000

Reporting:

- Recognized as unrestricted revenue in the Statement of Activities.

- No restrictions disclosed in notes.

Illustrative Example 2: Temporarily Restricted Grant

Scenario: A government grant of $100,000 restricted for building renovations to be used within two years.

Accounting Entry at Receipt:

- Debit Cash $100,000

- Credit Temporarily Restricted Revenue $100,000

When Expenses Are Incurred:

- Debit Temporarily Restricted Net Assets $X

- Credit Unrestricted Net Assets $X

Reporting:

- Initially reported as temporarily restricted revenue.

- Released from restriction as expenses occur.

- Notes detail the restriction and timeline.

Mind Map: Accounting Flow for Temporarily Restricted Grants

Illustrative Example 3: Conditional Contribution

Scenario: A pledge of $25,000 contingent on the nonprofit raising matching funds.

Best Practice:

- Do not recognize revenue until conditions are substantially met.

Accounting Treatment:

- No entry until matching funds are raised.

- Once conditions met, record as revenue.

Reporting:

- Disclose nature of conditions in notes.

Tips for Accurate Reporting

- Maintain detailed donor and grant agreements.

- Use fund accounting to segregate restricted funds.

- Regularly review and update restriction statuses.

- Coordinate with program managers to verify fund usage.

By following these best practices and leveraging clear documentation and classification, nonprofits can ensure their financial reports accurately reflect contributions and grants, enhancing credibility and supporting effective stewardship of resources.

4.3 Expense Classification: Program Services, Management, and Fundraising

Proper expense classification is crucial for nonprofit financial reporting as it provides transparency to donors, grantors, and stakeholders about how funds are being utilized. Nonprofits typically categorize expenses into three main categories: Program Services, Management and General, and Fundraising. Each category serves a distinct purpose and helps demonstrate the organization’s commitment to its mission and operational efficiency.

Expense Categories Overview

Program Services Expenses

These expenses are directly related to carrying out the nonprofit’s mission and programs. They include costs that are essential for delivering services or products to beneficiaries.

Examples:

- Salaries for teachers in an education nonprofit

- Supplies for a food bank

- Costs of running a health clinic

Best Practice: Track program expenses separately by program to provide detailed insights into resource allocation.

Example: A youth mentorship nonprofit spends $50,000 on mentor stipends, $10,000 on educational materials, and $5,000 on transportation for mentees. All these are classified under Program Services.

Management and General Expenses

These expenses support the overall administration and management of the organization but are not directly tied to any specific program or fundraising activity.

Examples:

- Executive director’s salary

- Accounting and audit fees

- Office rent and utilities

Best Practice: Maintain clear documentation to justify these expenses as necessary for organizational operations.

Example: The nonprofit pays $12,000 annually for accounting services and $8,000 for office rent. These costs are allocated to Management and General.

Fundraising Expenses

Fundraising expenses are costs incurred to raise money for the organization. This includes staff salaries dedicated to fundraising, event costs, and marketing.

Examples:

- Salaries of development officers

- Costs of organizing fundraising events

- Printing and mailing solicitation letters

Best Practice: Track fundraising expenses carefully to evaluate the cost-effectiveness of campaigns.

Example: A nonprofit spends $20,000 on a gala event, including venue rental, catering, and promotional materials. These are recorded as Fundraising expenses.

Mind Map: Detailed Expense Examples

Integrating Expense Classification into Financial Statements

Nonprofits report these expenses on the Statement of Activities, often breaking down expenses by category and sometimes by program. This classification helps stakeholders assess how efficiently the organization uses its resources.

Example Table:

| Expense Category | Amount ($) |

|---|---|

| Program Services | 150,000 |

| Management and General | 40,000 |

| Fundraising | 30,000 |

This breakdown clearly shows the nonprofit’s focus on program delivery while maintaining necessary administrative and fundraising activities.

Summary

- Program Services: Directly support the mission.

- Management and General: Support overall operations.

- Fundraising: Support resource development.

Accurate classification enhances transparency, builds donor trust, and ensures compliance with reporting standards.

Additional Example: Expense Classification in Action

Scenario: A nonprofit focused on environmental conservation incurs the following expenses in a quarter:

- $25,000 on habitat restoration supplies

- $10,000 on salaries for field biologists

- $5,000 on office rent

- $3,000 on accounting fees

- $7,000 on a fundraising dinner event

- $2,000 on promotional flyers

Classification:

- Program Services: $35,000 (supplies + salaries)

- Management and General: $8,000 (rent + accounting)

- Fundraising: $9,000 (event + flyers)

This clear classification helps the nonprofit communicate its financial stewardship effectively to stakeholders.

4.4 Example: Creating a Statement of Activities for a Youth Education Nonprofit

Creating a Statement of Activities is a critical step in nonprofit financial reporting. It provides a clear picture of the organization’s revenues and expenses over a specific period, showing how resources are used to fulfill its mission. In this section, we’ll walk through an example for a Youth Education Nonprofit, illustrating best practices with detailed examples and mind maps.

Understanding the Statement of Activities

The Statement of Activities reports changes in net assets by detailing revenues, gains, expenses, and losses. For nonprofits, it typically categorizes net assets into:

- Unrestricted

- Temporarily Restricted

- Permanently Restricted

Revenues and expenses are reported by their nature and function, often broken down into program services, management/general, and fundraising.

Step 1: Identify Revenue Sources

For a Youth Education Nonprofit, common revenue sources include:

- Contributions and Donations

- Grants (government and private foundations)

- Program Service Fees (e.g., tuition, workshop fees)

- Fundraising Events

- In-kind Donations

Example:

| Revenue Source | Amount (USD) | Restriction Type |

|---|---|---|

| Individual Donations | 150,000 | Unrestricted |

| Government Grant | 100,000 | Temporarily Restricted |

| Program Fees | 50,000 | Unrestricted |

| Fundraising Event | 30,000 | Unrestricted |

| Foundation Grant | 75,000 | Permanently Restricted |

Step 2: Categorize Expenses

Expenses should be classified by function:

- Program Services: Direct costs related to youth education programs

- Management and General: Administrative expenses

- Fundraising: Costs to raise funds

Example:

| Expense Category | Amount (USD) |

|---|---|

| Program Services | 220,000 |

| Management & General | 40,000 |

| Fundraising | 25,000 |

Step 3: Prepare the Statement of Activities

Below is a simplified example of the Statement of Activities for the Youth Education Nonprofit for the fiscal year ending 2023.

| Description | Unrestricted | Temporarily Restricted | Permanently Restricted | Total |

|---|---|---|---|---|

| Revenues and Support | ||||

| Contributions and Donations | 150,000 | 150,000 | ||

| Government Grants | 100,000 | 100,000 | ||

| Program Service Fees | 50,000 | 50,000 | ||

| Fundraising Events | 30,000 | 30,000 | ||

| Foundation Grants | 75,000 | 75,000 | ||

| Net Assets Released from Restrictions | 90,000 | (90,000) | 0 | |

| Total Revenues and Support | 320,000 | 10,000 | 75,000 | 405,000 |

| Expenses | ||||

| Program Services | 220,000 | 220,000 | ||

| Management & General | 40,000 | 40,000 | ||

| Fundraising | 25,000 | 25,000 | ||

| Total Expenses | 285,000 | 285,000 | ||

| Change in Net Assets | 35,000 | 10,000 | 75,000 | 120,000 |

Step 4: Visualizing the Statement of Activities with Mind Maps

Using mind maps helps visualize the flow and classification of revenues and expenses.

Statement of Activities Mind Map

Step 5: Best Practices Illustrated

- Clear Classification: Ensure revenues and expenses are accurately categorized by restriction and function.

- Net Assets Released from Restrictions: Reflect when restricted funds are used, moving amounts from temporarily restricted to unrestricted.

- Transparency: Provide notes explaining significant grants or restrictions.

- Consistent Terminology: Use terms aligned with FASB standards for clarity.

Additional Example: Narrative Explanation

“During fiscal year 2023, the Youth Education Nonprofit received $100,000 in government grants restricted for after-school program expansion. Of this, $90,000 was utilized, releasing the restriction and supporting program services. The organization also secured a $75,000 permanently restricted foundation grant to establish an endowment fund for scholarships. Total expenses of $285,000 were primarily dedicated to program services, reflecting our commitment to delivering quality educational programs to youth.”

By following this structured approach, nonprofit accountants and managers can create comprehensive, transparent, and compliant Statements of Activities that effectively communicate financial performance to stakeholders.

4.5 Integrating Narrative Explanations to Enhance Transparency

Narrative explanations in nonprofit financial reporting play a crucial role in providing context, clarifying numbers, and building trust with stakeholders such as donors, board members, and grantors. While financial statements present quantitative data, narratives help explain the “why” and “how” behind the numbers, making reports more accessible and meaningful.

Why Use Narrative Explanations?

- Clarify Complex Transactions: Explain unusual or one-time events (e.g., large grants, asset sales).

- Highlight Program Impact: Connect financial data to mission outcomes.

- Increase Accountability: Show how funds were used responsibly.

- Build Stakeholder Confidence: Transparent communication fosters trust.

Key Components of Effective Narrative Explanations

Best Practices for Integrating Narratives

- Start with a Summary: Provide an overview of the financial performance and key highlights.

- Explain Revenue Sources: Describe major funding streams and any restrictions.

- Detail Expense Allocation: Clarify how expenses support programs vs. administrative costs.

- Discuss Changes and Trends: Explain significant increases or decreases compared to prior periods.

- Use Real Examples: Illustrate points with concrete, relatable examples.

- Incorporate Visuals: Use charts or infographics to complement the narrative.

Example Narrative Explanation

“In FY2023, our nonprofit received a $500,000 grant from the Green Earth Foundation, restricted specifically for our urban tree planting program. This represents a 25% increase in program revenue compared to FY2022. The grant enabled us to plant 10,000 trees across five neighborhoods, directly contributing to our mission of improving urban air quality. Administrative expenses remained steady at 12% of total expenses, reflecting our ongoing commitment to efficient operations. The increase in program expenses aligns with the expanded scope of the tree planting initiative.”

Mind Map: Example Narrative Breakdown

Tips for Accountants and Nonprofit Managers

- Collaborate with program staff to gather impact stories and data.

- Use simple language; avoid accounting jargon.

- Tailor narratives to the audience’s level of financial literacy.

- Review narratives for accuracy and consistency with financial data.

- Update narratives regularly to reflect current activities and financial status.

Visual Example: Combining Narrative with a Pie Chart

Narrative: “Program services accounted for 78% of total expenses, underscoring our focus on mission-driven activities. Fundraising and administrative costs were 15% and 7%, respectively, reflecting prudent resource management.”

This narrative paired with a pie chart showing these percentages helps stakeholders quickly grasp expense distribution.

Summary

Integrating narrative explanations into nonprofit financial reports transforms raw data into a compelling story of impact and stewardship. By following best practices and using clear examples, nonprofits can enhance transparency, foster trust, and strengthen relationships with their stakeholders.

5. Cash Flow Reporting and Management

5.1 Importance of Cash Flow Statements in Nonprofit Financial Health

Cash flow statements are a critical component of financial reporting for nonprofits, providing a clear picture of how cash moves in and out of the organization. Unlike profit-focused businesses, nonprofits prioritize sustainability and mission delivery, making cash flow management essential to ensure ongoing operations and program success.

Why Cash Flow Statements Matter for Nonprofits

- Liquidity Insight: Cash flow statements reveal the organization’s ability to meet short-term obligations such as payroll, rent, and vendor payments.

- Operational Sustainability: They help nonprofits understand if they have enough cash to continue their programs without interruption.

- Donor and Grantor Confidence: Transparent cash flow reporting builds trust with donors and grantors by demonstrating responsible financial stewardship.

- Decision-Making Tool: Provides management and boards with actionable data to plan for future expenses, fundraising needs, or investment opportunities.

- Early Warning System: Identifies potential cash shortages before they become crises, allowing proactive measures.

Mind Map: Key Benefits of Cash Flow Statements for Nonprofits

Components of a Nonprofit Cash Flow Statement