Accounting for Government Grants

1. Introduction to Government Grants

1.1 Definition and Types of Government Grants

Government grants are financial awards provided by government bodies to organizations, institutions, or individuals to support specific projects, activities, or general operations without the expectation of repayment. These grants are designed to promote public welfare, stimulate economic growth, support research and innovation, and assist in community development.

Definition of Government Grants

A government grant is a non-repayable fund or product disbursed by one party (government) to a recipient, often to carry out a public purpose or stimulate activities aligned with government policies. Unlike loans, grants do not require repayment, but they often come with conditions or performance requirements.

Mind Map: Definition of Government Grants

Types of Government Grants

Government grants can be broadly categorized based on their purpose, conditions, and the nature of the recipient. Understanding these types helps accountants and financial managers apply the correct accounting treatment.

-

Capital Grants

- Purpose: To finance the acquisition, construction, or improvement of fixed assets.

- Example: A grant to build a new public library or upgrade government office buildings.

-

Revenue Grants

- Purpose: To support operating expenses or specific programs.

- Example: Funding for community health programs or educational initiatives.

-

Project Grants

- Purpose: To fund specific projects with defined objectives and timelines.

- Example: A grant for a renewable energy pilot project.

-

General Support Grants

- Purpose: To provide broad financial support without strict usage restrictions.

- Example: Block grants to local governments for general use.

-

Conditional Grants

- Purpose: Provided with specific conditions or performance targets.

- Example: Grants that require job creation or environmental compliance.

-

Unconditional Grants

- Purpose: Provided without any specific conditions attached.

- Example: A grant given to support general administrative costs.

Mind Map: Types of Government Grants

Examples Illustrating Types of Government Grants

-

Capital Grant Example: The Department of Transportation awards a $5 million grant to a city government to construct a new bridge. This grant is capital in nature because it finances a long-term asset.

-

Revenue Grant Example: A health department receives a $500,000 grant to fund vaccination programs during a public health campaign. This grant supports ongoing operational expenses.

-

Project Grant Example: An environmental agency is granted $1 million to conduct a two-year study on water quality in local rivers.

-

General Support Grant Example: A local municipality receives a block grant of $2 million to allocate across various departments as needed.

-

Conditional Grant Example: A government provides a grant to a manufacturing company contingent upon the creation of 100 new jobs within two years.

-

Unconditional Grant Example: A cultural institution receives funding to cover administrative costs without any specific usage restrictions.

Best Practice Tip:

When accounting for government grants, clearly identify the type of grant at the outset. This classification influences recognition, measurement, and disclosure. Maintaining detailed documentation on the grant’s purpose and conditions ensures compliance and accurate financial reporting.

This foundational understanding of government grants sets the stage for deeper exploration into recognition criteria, measurement, and accounting treatments in subsequent sections.

1.2 Importance of Accurate Accounting for Government Grants

Accurate accounting for government grants is crucial for government financial managers and accountants to ensure transparency, compliance, and effective resource management. Government grants often come with specific conditions and reporting requirements, making precise accounting essential to avoid financial misstatements, penalties, or loss of future funding.

Why Accurate Accounting Matters

- Compliance with Regulations: Government grants are subject to strict regulatory frameworks such as IFRS, GASB, or local government accounting standards. Accurate accounting ensures adherence to these rules.

- Transparency and Accountability: Proper recording and reporting of grant funds build trust with stakeholders, including taxpayers, grantors, and oversight bodies.

- Financial Management: Accurate accounting helps in budgeting, forecasting, and monitoring the use of grant funds to achieve intended outcomes.

- Audit Readiness: Detailed and accurate records simplify audits and reduce the risk of findings or sanctions.

- Sustainability of Funding: Demonstrating proper use of funds increases the likelihood of securing future grants.

Mind Map: Importance of Accurate Accounting for Government Grants

Practical Example 1: Compliance and Reporting

A city government receives a $2 million grant to improve public transportation infrastructure. The grant requires quarterly reports detailing expenditures and progress. Accurate accounting ensures that all expenses are properly categorized and documented, enabling the city to submit timely and accurate reports. Failure to do so could result in penalties or grant clawbacks.

Practical Example 2: Transparency and Stakeholder Trust

A state health department receives multiple grants for pandemic response. By maintaining clear and accurate accounting records, the department can transparently show how funds were allocated to testing, vaccination, and public education. This transparency fosters public trust and supports the department’s reputation.

Mind Map: Consequences of Inaccurate Accounting

Practical Example 3: Audit Readiness

A government agency managing environmental grants undergoes an external audit. Because the agency maintained meticulous records of grant receipts, expenditures, and compliance with grant conditions, the audit is completed smoothly with no adverse findings. This success enhances the agency’s credibility and supports future grant applications.

Summary

Accurate accounting for government grants is not just a regulatory requirement but a foundational practice that supports effective governance, financial integrity, and sustainable funding. By understanding its importance and implementing best practices, accountants and financial managers can safeguard public resources and contribute to successful government programs.

1.3 Overview of Regulatory Frameworks and Standards

Government grants accounting is governed by a variety of regulatory frameworks and standards designed to ensure transparency, consistency, and accountability in financial reporting. Understanding these frameworks is essential for accountants and government financial managers to correctly recognize, measure, present, and disclose government grants.

Key Regulatory Frameworks and Standards

-

International Financial Reporting Standards (IFRS)

- IFRS specifically addresses government grants under IAS 20 - Accounting for Government Grants and Disclosure of Government Assistance.

- IAS 20 provides guidance on recognition, measurement, and disclosure of grants.

-

Governmental Accounting Standards Board (GASB)

- GASB Statement No. 33 covers accounting and financial reporting for nonexchange transactions, including government grants.

- GASB standards are primarily used by U.S. state and local governments.

-

Federal Accounting Standards Advisory Board (FASAB)

- FASAB issues standards for federal entities in the United States.

- It provides guidance on grants and cooperative agreements.

-

National and Local Government Accounting Standards

- Many countries have their own public sector accounting standards (e.g., IPSAS - International Public Sector Accounting Standards).

- Local governments may have additional regulations or policies.

-

Grantor-Specific Regulations

- Some grants come with specific accounting and reporting requirements dictated by the grantor agency.

Mind Map: Regulatory Frameworks for Government Grants

IFRS - IAS 20 Highlights

- Recognition: Grants recognized when there is reasonable assurance that the entity will comply with conditions and the grant will be received.

- Measurement: Grants measured at fair value.

- Presentation: Grants related to assets can be presented as deferred income or deducted from the asset’s carrying amount.

- Disclosure: Nature, extent, and conditions of grants must be disclosed.

Example:

A government agency receives a $500,000 grant to purchase new IT equipment. Under IAS 20, the agency recognizes the grant when it is reasonably assured and measures it at fair value. The grant is presented as deferred income and amortized over the useful life of the equipment.

GASB Statement No. 33 Highlights

- Nonexchange Transactions: Grants are nonexchange transactions where the government gives or receives value without directly receiving equal value in return.

- Recognition: Revenue recognized when eligibility requirements are met.

- Types of Eligibility Requirements: Time requirements, reimbursement, and contingencies.

- Presentation: Revenues reported in the period when eligibility is met.

Example:

A city receives a grant to fund a public transportation project. The grant requires the city to spend funds within a fiscal year. The city recognizes revenue as expenses are incurred, matching grant revenue with related costs.

Mind Map: Key Accounting Concepts in Government Grants

Practical Example: Navigating Multiple Standards

A government financial manager at a regional authority must account for a $1 million grant received from a federal agency. The grant is subject to both national public sector accounting standards and specific federal grantor requirements.

Steps Taken:

- Review national accounting standards to identify recognition and measurement principles.

- Consult federal grant guidelines for reporting and compliance requirements.

- Apply IAS 20 principles for recognition and measurement if applicable.

- Ensure disclosures meet both national standards and grantor requirements.

- Document all decisions and maintain audit trails.

This integrated approach ensures compliance, transparency, and accuracy.

Summary

Understanding the regulatory frameworks and standards applicable to government grants is foundational for proper accounting. Familiarity with IFRS (IAS 20), GASB, FASAB, and local standards helps ensure grants are accounted for consistently and transparently. Additionally, recognizing grantor-specific requirements and integrating them into accounting practices is a best practice for government financial managers.

1.4 Common Challenges in Accounting for Government Grants

Accounting for government grants presents unique challenges that can impact the accuracy and transparency of financial reporting. Understanding these challenges is essential for accountants and government financial managers to ensure compliance and effective management.

Mind Map: Common Challenges in Accounting for Government Grants

Recognition Issues

One of the most frequent challenges is determining the appropriate timing and conditions for recognizing a government grant. Grants may be conditional, requiring certain performance milestones or compliance with specific terms before recognition is allowed.

Example: A government agency receives a grant to build a public park, but the grant is only payable upon completion of certain construction milestones. Recognizing the grant income before these milestones are met would be premature and could misstate financial results.

Best Practice: Maintain detailed documentation of grant conditions and monitor progress regularly to ensure recognition aligns with fulfillment of conditions.

Measurement Difficulties

Measuring the value of government grants can be complex, especially when grants are provided in non-monetary forms such as land, equipment, or services.

Example: A municipality receives donated land from the government as a grant. Determining the fair value of the land at the time of receipt requires professional appraisal and may vary significantly depending on market conditions.

Best Practice: Engage qualified valuation experts and apply consistent valuation methodologies to ensure accurate measurement.

Compliance and Documentation

Ensuring compliance with grant conditions and maintaining comprehensive documentation is critical for audit readiness and avoiding penalties.

Example: A government department receives a grant for educational programs with strict reporting requirements. Failure to document expenditures properly can lead to grant clawbacks or reputational damage.

Best Practice: Implement robust record-keeping systems and conduct periodic internal audits to verify compliance.

Presentation and Disclosure

Properly classifying and disclosing government grants in financial statements is essential for transparency and stakeholder trust.

Example: A grant intended for capital asset acquisition is mistakenly presented as revenue in the income statement, distorting the financial position.

Best Practice: Follow applicable accounting standards (e.g., IPSAS, IFRS) carefully and provide clear disclosures about the nature, amount, and conditions of grants.

Internal Controls

Weak internal controls can lead to mismanagement or misstatement of government grants.

Example: Lack of segregation of duties results in unauthorized use of grant funds for unrelated expenses.

Best Practice: Establish clear internal control procedures including segregation of duties, approval workflows, and regular reconciliations.

Coordination Across Departments

Government grants often involve multiple departments, which can create communication gaps and inconsistent accounting treatments.

Example: The finance department records a grant differently than the project management office, leading to discrepancies in reports.

Best Practice: Develop standardized accounting policies and facilitate regular inter-departmental meetings to align practices.

Summary

Accounting for government grants requires careful attention to recognition timing, accurate measurement, strict compliance, transparent presentation, strong internal controls, and effective coordination. By anticipating and addressing these common challenges, accountants and financial managers can ensure that government grants are accounted for accurately and responsibly.

1.5 Practical Example: Identifying a Government Grant in a Municipal Budget

Understanding how to identify government grants within a municipal budget is a foundational skill for accountants and financial managers in the public sector. This example will guide you through the process, using a typical municipal budget scenario.

Step 1: Understand the Source and Nature of Funds

Government grants are funds provided by higher levels of government (federal, state, or provincial) to municipalities for specific or general purposes. These funds are typically non-repayable but may come with conditions.

Mind Map: Sources of Government Grants

Step 2: Review the Municipal Budget Document

Municipal budgets often categorize revenues by source. Look for line items labeled as “Grants,” “Intergovernmental Revenues,” or similar.

Example:

| Revenue Source | Amount (USD) |

|---|---|

| Property Taxes | 5,000,000 |

| Sales Taxes | 2,000,000 |

| Federal Grants | 1,200,000 |

| State Grants | 800,000 |

| Service Charges | 1,500,000 |

Here, the “Federal Grants” and “State Grants” lines indicate government grants.

Step 3: Identify the Purpose and Conditions

Each grant should have an associated purpose and possibly conditions attached.

Mind Map: Grant Characteristics

Example:

- Federal Grant of $1,200,000 for road infrastructure improvements, requiring quarterly progress reports.

- State Grant of $800,000 for environmental cleanup, with a spending deadline within 12 months.

Step 4: Confirm the Grant Classification

Determine if the grant is capital (for asset acquisition or improvement) or revenue (for operational expenses).

Example:

- The federal grant for road infrastructure is a capital grant.

- The state grant for environmental cleanup is a revenue grant.

Step 5: Document and Record the Grant

Proper documentation includes grant agreements, correspondence, and budget notes.

Best Practice: Maintain a centralized grant register with details such as:

- Grantor

- Amount

- Purpose

- Conditions

- Recognition criteria

Mind Map: Grant Documentation

Summary Example: Identifying a Government Grant

| Step | Action Taken | Example Outcome |

|---|---|---|

| 1. Source Identification | Found “Federal Grants” and “State Grants” in budget | $1,200,000 and $800,000 identified as grants |

| 2. Purpose Review | Reviewed grant agreements | Infrastructure and environmental cleanup purposes |

| 3. Condition Check | Noted reporting and spending conditions | Quarterly reports and 12-month spending deadline |

| 4. Classification | Classified grants as capital or revenue | Federal = capital; State = revenue |

| 5. Documentation | Created entries in grant register | Centralized record for tracking |

This practical example illustrates how accountants and government financial managers can systematically identify and classify government grants within a municipal budget, ensuring compliance and accurate financial reporting.

2. Recognition Criteria for Government Grants

2.1 When to Recognize a Government Grant

Recognizing a government grant at the appropriate time is crucial for accurate financial reporting and compliance. The recognition point determines when the grant is recorded in the financial statements, impacting income, assets, and liabilities.

Key Principles for Recognition

- Probable Receipt: The entity must have reasonable assurance that it will receive the grant.

- Compliance with Conditions: The entity must comply with any attached conditions or be reasonably certain it will comply.

- Reliable Measurement: The amount of the grant can be measured reliably.

Mind Map: Criteria for Recognizing a Government Grant

Timing Considerations

- At Grant Approval: Some grants are recognized when the government formally approves the grant and communicates it to the entity.

- Upon Fulfillment of Conditions: If the grant is conditional, recognition occurs only when conditions are met.

- Over Time: For grants related to income, recognition may be spread over periods matching the related expenses.

Practical Example 1: Recognizing a Capital Grant for Building Renovation

A city government receives a $500,000 grant to renovate a public library. The grant is approved and communicated in January, but the renovation will take six months.

- Recognition Approach: The grant is recognized as income over the six-month renovation period, matching the expense recognition.

- Reasoning: The grant is conditional on renovation progress; recognizing it upfront would misstate income.

Mind Map: Timing of Recognition Based on Grant Type

Practical Example 2: Recognizing an Unconditional Operating Grant

A government agency receives an unconditional grant of $200,000 to support general operations for the fiscal year.

- Recognition Approach: The entire amount is recognized as income when the grant is received or receivable since there are no conditions.

- Reasoning: No restrictions or performance obligations exist, so recognition is immediate.

Best Practice Tips

- Maintain clear documentation of grant agreements, approvals, and conditions.

- Establish internal controls to track compliance with grant conditions.

- Collaborate with legal and compliance teams to interpret grant terms.

- Use consistent policies for recognition to ensure comparability.

Mind Map: Best Practices for Grant Recognition

By understanding when to recognize government grants, accountants and financial managers can ensure compliance with accounting standards such as IAS 20 or relevant government accounting frameworks, leading to transparent and reliable financial statements.

2.2 Conditions and Contingencies Affecting Recognition

When accounting for government grants, understanding the conditions and contingencies attached to the grant is critical for accurate recognition. These factors determine whether and when a grant can be recognized as income or as an asset, ensuring compliance with accounting standards such as IFRS and GASB.

What Are Conditions and Contingencies?

- Conditions: Specific requirements or obligations that the recipient must fulfill to qualify for the grant or to retain the grant funds.

- Contingencies: Events or circumstances that may affect the entitlement to the grant, often dependent on future outcomes.

Why Are They Important?

- They affect the timing of recognition.

- Failure to meet conditions may require repayment or reversal of recognized income.

- They influence disclosure requirements.

Mind Map: Conditions and Contingencies Affecting Recognition

Common Types of Conditions

- Use Restrictions: Funds must be used for a specified purpose.

- Performance Milestones: Completion of certain activities or phases.

- Reporting Requirements: Submission of financial or progress reports.

- Matching Contributions: Recipient must provide a certain amount of funding.

- Compliance with Laws: Adherence to legal or environmental standards.

Mind Map: Examples of Conditions

Recognition Implications

- Grant recognized only when conditions are met:

- If conditions are not yet met, the grant is recognized as a liability or deferred income.

- Partial fulfillment:

- Proportionate recognition may be appropriate.

- Failure to meet conditions:

- May require reversal of recognized amounts.

Practical Example 1: Infrastructure Grant with Milestone Conditions

A government agency receives a $5 million grant to build a community center. The grant agreement specifies:

- $2 million payable upon completion of the foundation.

- $3 million payable upon final completion.

- Quarterly progress reports must be submitted.

Accounting Treatment:

- Recognize $2 million as income when the foundation is completed and verified.

- Recognize the remaining $3 million upon final completion.

- Until milestones are met, amounts are recorded as deferred income.

Practical Example 2: Grant with Use Restriction and Reporting Condition

A city receives a $500,000 grant to fund environmental cleanup, with the condition that funds are used exclusively for hazardous waste removal and that annual reports are submitted.

Accounting Treatment:

- Recognize the grant as income only when expenditures for hazardous waste removal occur.

- Maintain records to demonstrate compliance with use restrictions.

- If reporting is delayed or incomplete, recognition may be deferred.

Mind Map: Recognition Process Considering Conditions

Best Practices

- Thoroughly review grant agreements to identify all conditions and contingencies.

- Maintain detailed documentation of how and when conditions are met.

- Implement monitoring systems to track compliance and milestones.

- Coordinate with legal and compliance teams to understand implications of non-fulfillment.

- Use clear accounting policies to handle partial fulfillment and contingencies.

Summary

Conditions and contingencies are pivotal in determining the timing and amount of government grant recognition. Proper identification, documentation, and monitoring ensure compliance and accurate financial reporting, ultimately supporting transparency and accountability in government financial management.

2.3 Distinguishing Between Capital and Revenue Grants

Understanding the distinction between capital and revenue grants is crucial for accurate accounting and financial reporting in government entities. This section explores the characteristics, accounting treatments, and practical examples to help accountants and government financial managers correctly classify and handle these grants.

What Are Capital Grants?

Capital grants are funds provided by the government to finance the acquisition, construction, or improvement of long-term assets. These grants are typically used for infrastructure projects, buildings, equipment, or other capital expenditures.

Key Characteristics:

- Intended for purchasing or improving fixed assets

- Often non-recurring and substantial in amount

- Benefits extend over multiple accounting periods

What Are Revenue Grants?

Revenue grants are funds given to support the day-to-day operational expenses or specific programs. These grants help cover costs such as salaries, supplies, or service delivery.

Key Characteristics:

- Intended for operational or revenue expenses

- Usually recurring and smaller in amount

- Benefits realized within the current accounting period

Mind Map: Distinguishing Capital vs Revenue Grants

Accounting Treatment Differences

| Aspect | Capital Grants | Revenue Grants |

|---|---|---|

| Purpose | Acquisition or improvement of fixed assets | Support operational expenses |

| Recognition | Deferred income or deducted from asset cost | Recognized immediately as income |

| Impact on Financials | Affects balance sheet and amortized over time | Affects income statement in current period |

| Examples | Grant for new school building | Grant for community health program |

Practical Examples

Example 1: Capital Grant

A government agency receives a $2 million grant to build a new public library. The grant is used exclusively for construction costs.

- Classification: Capital grant

- Accounting treatment: The grant is recorded as deferred income and recognized in the income statement over the useful life of the library building (e.g., 20 years) through amortization.

Example 2: Revenue Grant

A city council receives a $500,000 grant to fund a local arts program for the current fiscal year.

- Classification: Revenue grant

- Accounting treatment: The grant is recognized as income in the current fiscal year to match the expenses of running the arts program.

Mind Map: Accounting Workflow for Capital vs Revenue Grants

Best Practices

- Document the grant purpose clearly: Ensure grant agreements specify whether funds are for capital or revenue purposes.

- Align accounting treatment with grant conditions: Follow regulatory standards such as IPSAS 23 or IFRS requirements.

- Use consistent classification: Avoid misclassification to maintain transparency and compliance.

- Provide clear disclosures: In financial statements, disclose the nature and accounting treatment of grants.

Summary

Distinguishing between capital and revenue grants hinges on the purpose and timing of benefits. Capital grants relate to long-term assets and are recognized over the asset’s life, while revenue grants support operational costs and are recognized immediately. Proper classification ensures accurate financial reporting and compliance with accounting standards.

2.4 Best Practice: Documentation and Evidence for Recognition

Accurate documentation and robust evidence are fundamental to the proper recognition of government grants. This ensures compliance with accounting standards, facilitates audit processes, and supports transparency and accountability within government financial management.

Why Documentation and Evidence Matter

- Verification: Confirms the existence and terms of the grant.

- Compliance: Ensures adherence to regulatory and accounting standards.

- Audit Trail: Provides clear records for internal and external audits.

- Transparency: Builds trust with stakeholders and grantors.

Key Documentation Components

Mind Map: Documentation and Evidence for Grant Recognition

Best Practices for Documentation

-

Maintain a Centralized Grant File:

- Store all relevant documents in a dedicated digital or physical folder.

- Include grant agreements, correspondence, financial records, and reports.

-

Record Grant Terms Clearly:

- Highlight recognition criteria stipulated in the agreement.

- Note any conditions or contingencies affecting recognition.

-

Track Receipt of Funds:

- Use bank statements and accounting entries to confirm amounts received.

- Reconcile received funds against grant schedules.

-

Document Internal Approvals:

- Obtain formal sign-offs from authorized personnel before recognizing grants.

-

Regularly Update Performance Evidence:

- Keep records of progress reports and compliance with grant conditions.

-

Use Standardized Templates:

- Develop templates for grant documentation to ensure consistency.

Practical Example: Recognizing a Grant for Infrastructure Development

Scenario: A city government receives a $2 million grant to build a new community center. The grant agreement states that funds will be disbursed in three installments upon meeting specific construction milestones.

Documentation Steps:

- Grant Agreement: Signed contract detailing milestones and payment schedule.

- Correspondence: Emails confirming milestone approvals.

- Financial Records: Bank statements showing receipt of each installment.

- Internal Approvals: City council resolution authorizing acceptance and recognition of the grant.

- Performance Reports: Engineering reports confirming milestone completion.

Recognition:

- Upon receipt of the first installment and verification of milestone completion, the grant is recognized as deferred income.

- As construction progresses and milestones are met, portions of the grant are recognized as income in the financial statements.

Mind Map: Example - Infrastructure Grant Recognition Process

By following these documentation best practices, government accountants and financial managers can ensure that grant recognition is accurate, defensible, and aligned with both internal policies and external standards.

2.5 Practical Example: Recognizing a Grant for Infrastructure Development

Scenario Overview

A local government receives a government grant of $5 million to develop a new public transportation infrastructure project. The grant is intended to cover construction costs and is subject to specific conditions, including project milestones and reporting requirements.

Step 1: Identify the Grant and Its Nature

- Type of Grant: Capital grant for infrastructure development

- Grantor: State government

- Purpose: Construction of new bus terminals and related facilities

- Conditions: Completion of milestones, submission of progress reports, and use of funds exclusively for construction

Step 2: Assess Recognition Criteria

According to accounting standards (e.g., IPSAS 23 or IAS 20), recognition of a government grant requires:

- Reasonable assurance that the entity will comply with conditions attached to the grant

- Reasonable assurance that the grant will be received

Since the local government has signed a formal agreement and has a history of compliance, recognition is appropriate.

Step 3: Determine Measurement

- The grant amount is $5 million.

- The grant is measured at fair value, which is the nominal amount since it is a non-repayable grant.

Step 4: Accounting Treatment

- The grant is related to an asset (infrastructure).

- It will be recognized as deferred income and amortized over the useful life of the asset.

Mind Map: Recognizing a Government Grant for Infrastructure Development

Step 5: Journal Entries Example

| Date | Account | Debit ($) | Credit ($) |

|---|---|---|---|

| Upon grant receipt | Bank (Cash) | 5,000,000 | |

| Upon grant receipt | Deferred Grant Income | 5,000,000 |

As construction progresses and assets are capitalized:

| Date | Account | Debit ($) | Credit ($) |

|---|---|---|---|

| Capitalization | Infrastructure Asset | X | |

| Capitalization | Bank (Cash) or Payables | X |

Amortization of grant income over asset life (e.g., 20 years):

| Date | Account | Debit ($) | Credit ($) |

|---|---|---|---|

| Annual | Deferred Grant Income | 250,000 | |

| Annual | Grant Income (P&L) | 250,000 |

Step 6: Best Practices

- Maintain clear documentation of grant agreements and conditions.

- Monitor compliance with milestones and reporting requirements.

- Coordinate with project managers to align accounting recognition with project progress.

- Regularly review deferred income balances and amortization schedules.

Additional Mind Map: Best Practices in Grant Recognition

Summary

Recognizing a government grant for infrastructure development involves verifying eligibility, measuring the grant, and applying the appropriate accounting treatment. By following these steps and best practices, government financial managers ensure transparency, compliance, and accurate financial reporting.

This example demonstrates how to integrate accounting standards with practical project management considerations, providing a clear framework for recognizing and accounting for government grants in infrastructure projects.

3. Measurement of Government Grants

3.1 Initial Measurement: Fair Value and Present Value Concepts

When accounting for government grants, the initial measurement is a critical step that determines how the grant is recognized in the financial statements. Two fundamental concepts underpin this measurement: Fair Value and Present Value.

Understanding Fair Value

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

- Key Characteristics:

- Market-based measurement

- Reflects current market conditions

- Assumes an orderly transaction

Mind Map: Fair Value Concept

Example: Measuring a Non-Cash Grant

A government grants a municipality equipment valued at $100,000. The municipality should recognize the equipment and the grant at the fair value of the equipment received, which is $100,000, assuming no restrictions or conditions affect the measurement.

Understanding Present Value

Present value (PV) is the current worth of a future sum of money or stream of cash flows given a specified rate of return (discount rate).

- Key Characteristics:

- Time value of money concept

- Discounts future cash flows to current value

- Requires selection of an appropriate discount rate

Mind Map: Present Value Concept

Example: Measuring a Grant with Repayment Condition

A government grant of $50,000 is receivable in two years, but the recipient must repay it if certain conditions are not met. To measure the grant initially, the recipient discounts the $50,000 to its present value using an appropriate discount rate (e.g., 5%).

Calculation:

PV = $50,000 / (1 + 0.05)^2 = $45,351

The grant is initially recognized at $45,351.

Integrating Fair Value and Present Value in Grant Accounting

Mind Map: Initial Measurement Process

Best Practice Tips

- Always document the basis for fair value or present value measurement.

- Use market data and expert valuations where possible.

- Select discount rates that reflect the entity’s credit risk and market conditions.

- Review and update assumptions if conditions change before recognition.

Practical Example: Municipality Grant for Building Renovation

A municipality receives a grant of $200,000 to be paid in two installments: $100,000 immediately and $100,000 in one year. There is no repayment condition.

- Immediate $100,000 is recognized at fair value: $100,000.

- The $100,000 receivable in one year is discounted at 4%:

PV = $100,000 / (1 + 0.04)^1 = $96,154

- Total grant recognized initially: $100,000 + $96,154 = $196,154.

This ensures the grant is accurately reflected in the financial statements considering the time value of money.

By understanding and correctly applying fair value and present value concepts, accountants and government financial managers can ensure transparent, accurate, and compliant reporting of government grants.

3.2 Subsequent Measurement and Adjustments

Subsequent measurement of government grants involves the ongoing accounting treatment after the initial recognition and measurement. This step is crucial to ensure that the financial statements accurately reflect the impact of the grant over time, particularly when conditions change or when the grant is linked to specific assets or income.

Key Concepts in Subsequent Measurement

- Amortization of Grants Related to Assets: When a grant is related to an asset, it is typically recognized as deferred income and amortized over the useful life of the asset.

- Recognition of Income: Grants related to income are recognized in profit or loss over the periods necessary to match them with the related costs.

- Adjustments for Changes in Conditions: If conditions attached to the grant change or are not met, adjustments may be required, including potential repayments.

Mind Map: Subsequent Measurement Overview

Amortization of Grants Related to Assets

When a government grant is received for the purchase or construction of a fixed asset, the grant is initially recognized as deferred income (liability) and then systematically recognized as income over the asset’s useful life.

Example: A government grant of $500,000 is received to build a new public library. The library is expected to have a useful life of 25 years.

- Initial recognition: $500,000 deferred income.

- Annual amortization: $500,000 / 25 = $20,000 recognized as income each year.

Mind Map: Amortization Process

Recognition of Grants Related to Income

Grants that compensate for expenses or losses should be recognized in the same period as the related costs to ensure proper matching.

Example: A government grant of $100,000 is awarded to cover training expenses for government employees in the current fiscal year.

- The grant is recognized as income in the same period when the training expenses are incurred.

- If training expenses are $80,000, the grant income recognized is $80,000 to match the expense.

- The remaining $20,000 is recognized when additional eligible expenses occur or deferred if conditions apply.

Mind Map: Income-Related Grants

Adjustments Due to Changes in Conditions or Repayment

Sometimes, grants come with conditions that, if unmet, require repayment or adjustment of the recognized amounts.

Example: A grant of $200,000 is provided to a government agency to create 50 new jobs within two years. After one year, only 30 jobs have been created.

- The agency must reassess the grant recognition.

- If conditions are unlikely to be met, a portion of the grant may need to be reversed or disclosed as a liability.

- This adjustment ensures the financial statements reflect the true economic benefit.

Mind Map: Adjustments and Repayments

Practical Example: Subsequent Measurement in Action

Scenario: A local government receives a $1 million grant to purchase firefighting equipment with a useful life of 10 years. The grant requires the equipment to be used exclusively for firefighting services.

- Year 1:

- Recognize $1 million as deferred income.

- Amortize $100,000 as grant income.

- Year 3:

- Equipment is repurposed partially for non-firefighting activities.

- The government reassesses the grant conditions.

- Adjust deferred income and recognize a liability for the portion related to non-compliance.

This example highlights the importance of continuous monitoring and adjustment to ensure compliance and accurate financial reporting.

Best Practices for Subsequent Measurement and Adjustments

- Maintain detailed schedules linking grants to assets and expenses.

- Regularly review grant conditions and compliance status.

- Document all adjustments with clear rationale.

- Coordinate with legal and compliance teams for condition interpretation.

- Use consistent amortization methods aligned with asset depreciation.

By following these principles and practices, accountants and government financial managers can ensure that government grants are measured and reported accurately throughout their lifecycle, providing transparency and accountability to stakeholders.

3.3 Handling Grants with Repayment Conditions

Government grants with repayment conditions present unique accounting challenges. These grants require the recipient to repay the grant amount, either partially or fully, if certain conditions are not met. Proper accounting treatment ensures compliance with standards and accurate financial reporting.

Understanding Repayment Conditions

Repayment conditions typically arise when grants are contingent on:

- Failure to meet performance targets

- Non-compliance with grant terms

- Early termination of the grant project

- Change in use of the grant funds

These conditions create a potential liability for the recipient.

Accounting Treatment Overview

The key accounting considerations include:

- Initial recognition of the grant

- Recognition of a liability for the repayment obligation

- Measurement of the liability

- Subsequent adjustments based on fulfillment or breach of conditions

Mind Map: Accounting for Grants with Repayment Conditions

Example 1: Infrastructure Grant with Clawback Clause

Scenario: A local government receives a $1 million grant to build a community center. The grant includes a clause requiring repayment if the center is sold within 5 years.

Accounting Treatment:

- Initially, recognize the $1 million as deferred income.

- Recognize a contingent liability for the repayment obligation.

- If the government decides to sell the center in year 3, recognize the repayment liability and reduce income accordingly.

Mind Map:

Example 2: Research Grant with Performance Milestones

Scenario: A government agency awards a $500,000 research grant payable in installments, with repayment required if milestones are not met.

Accounting Treatment:

- Recognize grant income as milestones are achieved.

- If a milestone is missed, recognize a liability for the repayment amount.

- Adjust financial statements to reflect the likelihood of repayment.

Mind Map:

Best Practices

- Thorough Documentation: Maintain clear records of all grant terms and repayment conditions.

- Regular Monitoring: Continuously assess compliance with grant conditions.

- Conservative Recognition: Recognize liabilities promptly when repayment becomes probable.

- Transparent Disclosure: Clearly disclose repayment conditions and potential liabilities in financial statements.

Summary

Handling grants with repayment conditions requires a careful balance between recognizing income and potential liabilities. By following a structured approach and using clear documentation, government entities can ensure compliance and maintain transparent financial reporting.

3.4 Best Practice: Using Valuation Experts and Consistent Methods

Accurately measuring government grants is critical to ensure compliance with accounting standards and to present a true and fair view of financial statements. One of the best practices in this area is to engage valuation experts and adopt consistent valuation methods. This approach helps mitigate risks related to misvaluation, enhances transparency, and supports audit readiness.

Why Use Valuation Experts?

- Specialized Knowledge: Valuation experts possess deep understanding of market conditions, asset-specific factors, and regulatory requirements.

- Objective Assessment: They provide an independent and unbiased valuation, reducing the risk of internal bias.

- Complex Grants: Some grants involve assets or conditions that require sophisticated valuation techniques beyond routine accounting.

- Compliance Assurance: Experts ensure that valuations comply with relevant accounting standards such as IFRS, GASB, or IPSAS.

Consistent Valuation Methods

Consistency in applying valuation methods is essential for comparability across reporting periods and entities. Common valuation methods include:

- Market Approach: Uses prices and other relevant information generated by market transactions.

- Income Approach: Converts future amounts (cash flows or income) to a single current amount using a discount rate.

- Cost Approach: Based on the current replacement cost of an asset, less depreciation.

Mind Map: Valuation Experts and Consistent Methods

Practical Example 1: Valuing a Grant for Renewable Energy Equipment

A government agency receives a grant to purchase solar panels. The grant amount is based on the fair value of the equipment. To ensure accurate measurement:

- The agency hires a valuation expert specializing in renewable energy assets.

- The expert uses the market approach, comparing prices of similar solar panels recently sold.

- The valuation is documented and reviewed by the finance team.

- Consistent application of this method is maintained for all future equipment grants.

This approach ensures the grant is recorded at a fair value reflecting current market conditions.

Practical Example 2: Measuring a Grant with Repayment Conditions

A local government receives a grant for community development, repayable if certain milestones are not met. The valuation expert:

- Applies the income approach, discounting expected cash flows considering the probability of repayment.

- Works closely with legal and project teams to understand conditions.

- Provides a valuation report that guides the accounting treatment.

The finance team applies this consistent method for similar conditional grants, ensuring comparability.

Tips for Implementing Best Practices

- Engage Experts Early: Involve valuation professionals during grant negotiation or acceptance.

- Develop Valuation Policies: Establish clear policies outlining preferred methods and documentation requirements.

- Train Staff: Ensure accountants understand valuation principles and when to seek expert advice.

- Maintain Documentation: Keep detailed records of valuation reports, assumptions, and methodologies.

- Review Regularly: Periodically reassess valuation methods to reflect changes in market conditions or regulations.

By integrating valuation experts and consistent methods into the accounting process for government grants, organizations can enhance accuracy, compliance, and stakeholder trust.

3.5 Practical Example: Measuring a Grant for Technology Upgrade

When a government entity receives a grant specifically aimed at upgrading technology infrastructure, accurately measuring the grant is crucial for proper accounting and reporting. This example will guide you through the steps and considerations involved in measuring such a grant.

Step 1: Identify the Nature and Terms of the Grant

- Is the grant a lump sum or disbursed in installments?

- Are there any conditions or performance obligations attached?

- Does the grant cover full or partial costs?

Example: A government agency receives a $500,000 grant to upgrade its IT systems. The grant is disbursed in two installments: $300,000 upfront and $200,000 upon completion of the upgrade.

Step 2: Determine Initial Measurement

- The grant should be measured at fair value at the date of receipt or when the grant becomes receivable.

- If payment is deferred, consider the present value of future payments.

Example: Since the grant is paid in installments, the agency calculates the present value of the second installment ($200,000) discounted at an appropriate rate (e.g., 3%).

Mind Map: Initial Measurement of Technology Upgrade Grant

Step 3: Recognize the Grant in Financial Statements

- Recognize the grant as income over the periods necessary to match it with the related costs.

- If the grant relates to an asset, it may be recognized as deferred income and amortized over the asset’s useful life.

Example: The agency decides to recognize the grant as deferred income and amortize it over 5 years, matching the expected useful life of the upgraded technology.

Step 4: Adjust for Any Conditions or Repayments

- If the grant has conditions that may not be met, recognize a liability or adjust the measurement accordingly.

- Monitor for any repayments or clawbacks.

Example: The grant requires the agency to maintain the upgraded system for at least 3 years. Failure to do so could result in repayment. The agency sets up controls to monitor compliance.

Mind Map: Adjustments and Conditions

Step 5: Disclosure and Reporting

- Disclose the grant amount, measurement basis, and any conditions in the financial statements.

- Provide narrative on how the grant impacts financial position and performance.

Example: In the notes to financial statements, the agency discloses the $500,000 grant, its recognition as deferred income, amortization policy, and conditions attached.

Summary Table: Measuring a Technology Upgrade Grant

| Step | Action | Example Detail |

|---|---|---|

| Identify Grant Terms | Review agreement and payment schedule | $500,000 in two installments |

| Initial Measurement | Calculate fair value and present value | Discount second installment at 3% |

| Recognition | Recognize as deferred income | Amortize over 5 years |

| Adjust for Conditions | Monitor compliance and potential repayments | Maintain system for 3 years |

| Disclosure | Report measurement and conditions | Notes in financial statements |

This practical example highlights the importance of understanding the terms of the grant, applying appropriate measurement techniques, and ensuring transparent reporting. By following these steps, government accountants and financial managers can ensure compliance and provide stakeholders with clear, reliable information about technology upgrade grants.

4. Presentation and Disclosure Requirements

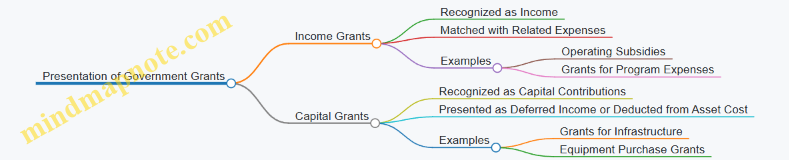

4.1 Presentation in Financial Statements: Income vs. Capital

When accounting for government grants, one of the critical considerations is how to present these grants in the financial statements. The presentation typically falls into two broad categories: income-related grants and capital-related grants. Understanding the distinction and appropriate presentation ensures transparency, compliance with accounting standards, and provides stakeholders with clear insights into the financial health and funding sources of the government entity.

Mind Map: Presentation of Government Grants in Financial Statements

Income Grants

Definition: Grants provided to support operational costs or specific program expenses.

Presentation:

- Recognized as income in the statement of financial performance (income statement).

- Matched with the expenses they are intended to offset, following the matching principle.

Example: A government agency receives a $500,000 grant to fund a community outreach program. The grant is recognized as income over the period the program expenses are incurred.

Best Practice: Maintain detailed schedules linking grant income to related expenses to ensure proper matching and avoid misstatements.

Mind Map: Income Grants Presentation

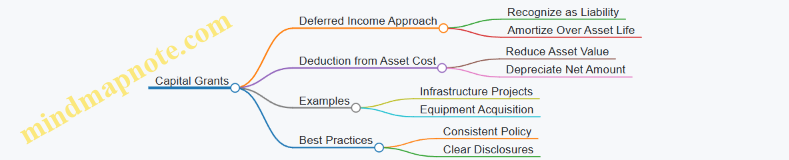

Capital Grants

Definition: Grants provided to acquire or construct long-term assets such as buildings, infrastructure, or equipment.

Presentation Options:

-

Deferred Income Approach:

- Recognize the grant as deferred income (liability) on the balance sheet.

- Amortize the income to the statement of financial performance over the useful life of the related asset.

-

Deduction from Asset Cost:

- Reduce the carrying amount of the asset by the grant amount.

- Depreciation is charged on the net amount.

Example: A city government receives a $2 million grant to build a new public library. The grant is recorded as deferred income and amortized over the 40-year useful life of the library building.

Best Practice: Choose a consistent presentation policy and disclose it clearly in the notes to the financial statements.

Mind Map: Capital Grants Presentation

Integrated Example: Income vs. Capital Grant Presentation

Scenario: A government financial manager oversees two grants:

- A $300,000 grant to fund staff salaries for a social welfare program (income grant).

- A $1 million grant to purchase new firefighting equipment (capital grant).

Accounting Treatment:

- The $300,000 is recognized as income in the period when salaries are paid, matching the expense.

- The $1 million grant is recorded as deferred income and amortized over the equipment’s 10-year useful life.

Financial Statement Impact:

- Income Statement shows $300,000 grant income matching salary expenses.

- Balance Sheet shows deferred income liability of $1 million initially, reducing over 10 years.

Summary

| Aspect | Income Grants | Capital Grants |

|---|---|---|

| Purpose | Support operational/program expenses | Fund acquisition/construction of assets |

| Financial Statement | Recognized as income | Deferred income or deduction from asset cost |

| Matching Principle | Yes, matched with related expenses | Amortized over asset’s useful life |

| Examples | Program subsidies, operational costs | Infrastructure, equipment grants |

| Best Practices | Detailed tracking, periodic recognition | Consistent policy, clear disclosures |

By carefully distinguishing between income and capital grants and presenting them appropriately, government accountants and financial managers can ensure compliance, enhance transparency, and provide meaningful financial information to stakeholders.

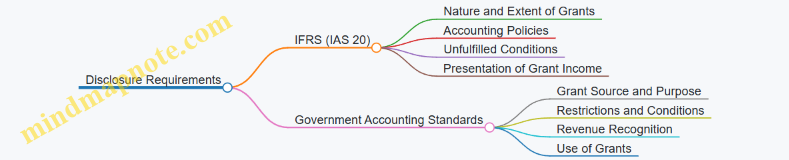

4.2 Disclosure Requirements Under IFRS and Government Accounting Standards

Accounting for government grants requires transparent and comprehensive disclosure to ensure stakeholders understand the nature, extent, and impact of grants on financial statements. Both IFRS and various government accounting standards provide specific requirements to guide these disclosures.

Key Disclosure Requirements Under IFRS (IAS 20)

- Nature and Extent of Grants Recognized: Entities must disclose the types of government grants received and their significance to the financial statements.

- Accounting Policy: Clear explanation of the accounting policies adopted for government grants, including the methods of recognition and measurement.

- Unfulfilled Conditions: Details of any unfulfilled conditions or contingencies attached to government grants that have not been recognized.

- Grant Income Presentation: How grant income is presented in the financial statements (e.g., deducted from related expenses or shown separately).

Government Accounting Standards Disclosure Requirements

Government accounting standards, such as GASB (Governmental Accounting Standards Board) in the U.S. or IPSAS (International Public Sector Accounting Standards), emphasize:

- Grant Source and Purpose: Disclosure of the source of grants and the intended purpose or program supported.

- Restrictions and Conditions: Information on any restrictions or conditions attached to the grants.

- Grant Revenue Recognition: Timing and basis of recognizing grant revenue.

- Use of Grants: How grants have been utilized during the reporting period.

Mind Map: Disclosure Requirements Overview

Best Practice: Integrating Disclosures into Financial Statements

- Use clear, concise language avoiding technical jargon.

- Provide quantitative data alongside qualitative explanations.

- Include tables summarizing grants received, recognized income, and unfulfilled conditions.

- Cross-reference disclosures with notes on related assets or expenses.

Practical Example 1: IFRS-Compliant Disclosure in a Government Agency Annual Report

Note X: Government Grants

During the year, the agency received government grants totaling $5 million, primarily to support infrastructure development and community programs. Grants are recognized when there is reasonable assurance that the agency will comply with the conditions attached and the grants will be received.

| Grant Type | Amount Received | Amount Recognized | Unfulfilled Conditions |

|---|---|---|---|

| Infrastructure Grant | $3,000,000 | $2,500,000 | $500,000 |

| Community Program | $2,000,000 | $2,000,000 | $0 |

The agency presents grant income as a separate line item in the statement of comprehensive income.

Mind Map: Example Disclosure Structure

Practical Example 2: GASB Disclosure for a City Government

Note 8: Government Grants and Contributions

The City received several grants from federal and state governments during the fiscal year 2023, amounting to $12 million. These grants are restricted for specific purposes including public safety, transportation, and environmental projects.

The City recognizes grant revenue when eligibility requirements are met. As of year-end, $1.2 million of grant funds remain unspent and are reported as deferred inflows of resources.

| Grant Program | Amount Received | Recognized Revenue | Deferred Inflows |

|---|---|---|---|

| Public Safety | $4,000,000 | $3,800,000 | $200,000 |

| Transportation | $5,000,000 | $4,700,000 | $300,000 |

| Environmental | $3,000,000 | $3,000,000 | $0 |

Mind Map: GASB Disclosure Elements

Summary

Proper disclosure under IFRS and government accounting standards enhances transparency and accountability in the use of government grants. By clearly communicating the nature, extent, conditions, and financial impact of grants, accountants and financial managers help stakeholders make informed decisions and maintain trust.

Additional Tips

- Regularly review updates to IFRS and local government accounting standards.

- Collaborate with auditors to ensure disclosures meet compliance requirements.

- Use visual aids like tables and mind maps in reports to improve clarity.

4.3 Best Practice: Transparent Reporting to Stakeholders

Transparent reporting is essential in government grant accounting to build trust, ensure accountability, and facilitate informed decision-making among stakeholders such as government officials, auditors, taxpayers, and grantors. This section explores best practices for transparent reporting, supported by clear examples and mind maps to visualize key concepts.

Why Transparent Reporting Matters

- Enhances credibility and public trust.

- Ensures compliance with regulatory requirements.

- Facilitates effective monitoring and evaluation of grant usage.

- Helps prevent misuse or misallocation of funds.

Key Elements of Transparent Reporting

-

Clear Disclosure

- Clearly state the nature, amount, and purpose of each government grant.

- Disclose any conditions or restrictions attached to the grant.

-

Timely Reporting

- Provide reports aligned with financial periods (quarterly, annually).

- Ensure stakeholders receive information promptly to support decision-making.

-

Consistent Presentation

- Use standardized formats and terminology.

- Maintain consistency across reports to enable comparability.

-

Detailed Notes

- Include explanatory notes on accounting policies, measurement methods, and any changes.

- Highlight significant judgments or estimates related to grants.

-

Stakeholder Communication

- Tailor reports to the needs of different stakeholders.

- Use accessible language and visual aids where appropriate.

Mind Map: Components of Transparent Reporting

Practical Example 1: Disclosing a Multi-Year Grant in Annual Reports

Scenario: A government agency receives a $5 million multi-year grant for environmental conservation.

Best Practice Reporting:

- Income Statement: Recognize grant income proportionally over the grant period.

- Balance Sheet: Present any unspent grant funds as deferred income or liabilities.

- Notes to Financial Statements: Describe the grant’s purpose, duration, conditions, and recognition policy.

- Supplementary Report: Include performance indicators such as hectares conserved or projects completed.

Outcome: Stakeholders can clearly see how the grant funds are being utilized over time and the agency’s progress toward objectives.

Mind Map: Example Reporting Structure for Multi-Year Grant

Practical Example 2: Transparent Reporting in a Local Government Grant

Scenario: A city government receives a grant to upgrade public transportation infrastructure.

Best Practice Reporting:

- Clear Disclosure: Report the grant amount and specify that funds are restricted to transportation projects.

- Timely Updates: Provide quarterly progress reports to the city council and public.

- Consistent Presentation: Use the same reporting format each quarter to track spending and progress.

- Detailed Notes: Explain any delays or changes in project scope affecting grant usage.

Outcome: The public and oversight bodies remain informed, reducing the risk of mismanagement and increasing support for the project.

Mind Map: Stakeholder-Focused Reporting Approach

Tips for Implementing Transparent Reporting

- Develop standardized templates for grant reporting.

- Train accounting and finance teams on disclosure requirements.

- Use visual aids like charts and graphs to enhance understanding.

- Establish regular communication channels with stakeholders.

- Incorporate feedback mechanisms to improve reporting quality.

Transparent reporting is not just a regulatory obligation but a strategic tool that strengthens governance and public confidence. By following these best practices, government accountants and financial managers can ensure that grant information is presented clearly, accurately, and comprehensively to all stakeholders.

4.4 Practical Example: Disclosing a Multi-Year Grant in Annual Reports

Disclosing a multi-year government grant in annual financial reports requires clarity, transparency, and adherence to accounting standards such as IFRS or GASB. This section provides a detailed example of how a government entity should present and disclose such grants, supported by mind maps to visualize the process.

Understanding Multi-Year Grants

Multi-year grants are funds provided by the government that span multiple fiscal years. Proper disclosure involves:

- Recognizing the grant income over the period it relates to

- Presenting the grant in financial statements appropriately

- Providing detailed notes explaining the nature, conditions, and timing of the grant

Mind Map: Key Disclosure Elements for Multi-Year Grants

Example Scenario

Entity: City Public Health Department

Grant: Multi-Year Public Health Improvement Grant

Grant Details:

- Total Amount: $5,000,000

- Duration: 5 years (2022-2026)

- Purpose: Enhance community health services and infrastructure

- Conditions: Annual performance targets and expenditure restrictions

Step 1: Recognition of Grant Income

The department recognizes grant income on a systematic basis over the grant period, matching the expenses incurred. For example:

| Year | Grant Income Recognized | Expenses Incurred |

|---|---|---|

| 2022 | $1,000,000 | $950,000 |

| 2023 | $1,000,000 | $1,050,000 |

| 2024 | $1,000,000 | $1,000,000 |

| 2025 | $1,000,000 | $1,000,000 |

| 2026 | $1,000,000 | $1,000,000 |

Step 2: Presentation in Financial Statements

- Statement of Financial Position: Any unspent grant funds at year-end are reported as deferred income (liability) or grant receivable (asset).

- Statement of Activities: Grant income is presented separately or disclosed in notes to show the contribution from government grants.

Mind Map: Financial Statement Presentation

Step 3: Notes to Financial Statements Example

Note X: Government Grants

The City Public Health Department has been awarded a multi-year grant totaling $5,000,000 from the State Health Agency to support community health services from 2022 through 2026. The grant is recognized on a systematic basis over the grant period to match related expenses.

As of December 31, 2023, the department has recognized $2,000,000 in grant income and incurred $2,000,000 in related expenses. Unspent grant funds amounting to $500,000 are recorded as deferred income.

The grant is subject to annual performance targets and expenditure restrictions. Management monitors compliance through internal controls and regular reporting to the grantor.

Step 4: Best Practices Summary

- Clearly identify the grant and its terms in disclosures.

- Recognize income systematically over the grant period.

- Present unspent funds appropriately as liabilities or assets.

- Provide detailed notes explaining conditions, restrictions, and compliance.

- Use visuals such as tables and mind maps to enhance clarity.

This practical example demonstrates how government financial managers and accountants can effectively disclose multi-year grants, ensuring transparency and compliance with accounting standards while providing stakeholders with a clear understanding of the grant’s financial impact.

4.5 Case Study: Presentation Differences in Various Government Entities

Government entities vary widely in their structure, reporting requirements, and stakeholder expectations. These differences significantly impact how government grants are presented in their financial statements. This case study explores presentation variations across three common types of government entities: Central Government, Local Government, and Government Agencies.

Mind Map: Factors Influencing Presentation of Government Grants

Central Government Presentation

Context: Central governments typically follow IPSAS or similar international standards and often have complex, multi-source grants.

Presentation Approach:

- Grants are often presented separately in the Statement of Financial Performance (Income Statement) as either “Government Grants” or under a specific line item such as “Grants and Subsidies Received.”

- Capital grants related to assets are recognized as deferred income and amortized over the useful life of the asset.

- Detailed disclosures include grant conditions, unfulfilled obligations, and multi-year commitments.

Example: The Ministry of Infrastructure receives a $100 million capital grant for highway construction.

- The grant is initially recorded as deferred income on the balance sheet.

- Each year, amortization of the grant income is recognized corresponding to the depreciation expense of the constructed highway.

- Notes disclose the grant’s purpose, conditions, and expected completion timeline.

Local Government Presentation

Context: Local governments often follow GASB or national public sector accounting standards, with a focus on transparency to local taxpayers.

Presentation Approach:

- Grants are usually reported in the governmental funds financial statements as “Intergovernmental Revenues.”

- Capital grants may be reported as revenue when the related capital asset is acquired or constructed.

- Emphasis on fund accounting means grants are often segregated by fund to show restricted vs. unrestricted usage.

Example: A city government receives a $5 million grant for park renovation.

- The grant is recorded as revenue in the Capital Projects Fund when the funds are available and spent.

- The financial statements include a schedule of grant revenues and expenditures by fund.

- Notes highlight restrictions on grant use and any unspent balances.

Government Agencies Presentation

Context: Agencies may have hybrid reporting requirements, sometimes following accrual accounting but with specific donor or grantor-imposed presentation rules.

Presentation Approach:

- Grants are often presented as “Grant Income” or “Contributions” in the Statement of Activities.

- Conditional grants are disclosed separately, with recognition deferred until conditions are met.

- Agencies may provide segmented reporting to satisfy multiple stakeholders.

Example: A public health agency receives a $2 million grant conditioned on achieving vaccination targets.

- The grant is recognized as income only when vaccination milestones are met.

- The agency discloses the unfulfilled conditions and potential repayment obligations.

- A segmented report shows grant income by program area.

Mind Map: Presentation Elements by Entity Type

Key Takeaways

- Entity type drives presentation: Central governments emphasize accrual and amortization, local governments focus on fund accounting and transparency, agencies prioritize conditional recognition and segmented reporting.

- Disclosure requirements vary: More complex entities provide detailed notes on conditions and multi-year commitments.

- Examples help illustrate: Real-world grants show how accounting policies translate into financial statement presentation.

Practical Exercise

Consider a $10 million grant received by each entity type for similar infrastructure projects. Draft a brief presentation outline for each entity’s financial statements, highlighting differences in recognition, presentation, and disclosure.

This case study demonstrates the importance of tailoring grant presentation to the entity’s accounting framework, stakeholder needs, and grant conditions to ensure clarity, compliance, and transparency.

5. Accounting Treatment for Different Types of Grants

5.1 Grants Related to Assets: Recognition and Amortization

Government grants related to assets are funds provided to acquire, construct, or improve long-term assets such as buildings, infrastructure, equipment, or land. Proper accounting treatment ensures that these grants are recognized accurately and amortized systematically over the useful life of the related asset.

Key Concepts

- Recognition: The grant should be recognized when there is reasonable assurance that the entity will comply with the conditions attached and the grant will be received.

- Presentation: Grants related to assets can be presented either by deducting the grant from the carrying amount of the asset or by recognizing it as deferred income.

- Amortization: If recognized as deferred income, the grant is amortized to profit or loss over the asset’s useful life, matching the depreciation expense.

Mind Map: Grants Related to Assets

Recognition Approaches

-

Deducting from Asset Carrying Amount

- The grant reduces the asset’s book value.

- Depreciation is charged on the net amount.

-

Deferred Income Approach

- Grant recognized as a liability (deferred income).

- Amortized to income statement over asset’s life.

Practical Example 1: Deducting Grant from Asset

A government agency receives a $500,000 grant to purchase new IT equipment costing $2,000,000. The equipment has a useful life of 5 years.

-

Accounting treatment:

- Asset recorded at $1,500,000 ($2,000,000 - $500,000).

- Annual depreciation = $1,500,000 / 5 = $300,000.

-

Journal entries:

- On purchase:

- Dr Equipment $2,000,000

- Cr Cash/Payables $1,500,000

- Cr Government Grant (deferred income) $500,000 (if using deferred income approach)

- If deducting grant from asset, credit Government Grant is not recorded separately.

- On purchase:

Practical Example 2: Deferred Income Approach

Using the same example, if the grant is recognized as deferred income:

-

Initial recognition:

- Dr Equipment $2,000,000

- Cr Cash/Payables $1,500,000

- Cr Deferred Government Grant $500,000

-

Annual amortization:

- Dr Deferred Government Grant $100,000 ($500,000 / 5 years)

- Cr Other Income $100,000

-

Depreciation expense:

- Dr Depreciation Expense $400,000 ($2,000,000 / 5 years)

- Cr Accumulated Depreciation $400,000

This method keeps the asset at full cost but recognizes the grant income over the asset’s life.

Mind Map: Amortization Process

Best Practices

- Consistent Policy: Choose one presentation method and apply consistently across similar grants.

- Documentation: Maintain detailed records of grant agreements, conditions, and asset details.

- Review Useful Life: Periodically reassess asset useful life and adjust amortization accordingly.

- Internal Controls: Ensure controls are in place to track grant receipts and related asset accounting.

Summary

Accounting for government grants related to assets requires careful recognition, presentation, and amortization to reflect the economic reality. Whether reducing the asset’s carrying amount or recognizing deferred income, the key is to match the grant income with the asset’s depreciation to provide transparent and accurate financial reporting.

5.2 Grants Related to Income: Matching Income with Expenses

Government grants related to income are financial awards provided to support the operational expenses of an entity, rather than the acquisition or construction of fixed assets. The key accounting principle here is to match the grant income with the related expenses to reflect a true and fair view of the financial performance during the reporting period.

Understanding Income-Related Grants

Income-related grants are typically intended to subsidize costs such as salaries, research expenses, or program delivery costs. These grants are recognized as income over the periods necessary to match them with the related costs that they are intended to compensate.

Best Practice: Matching Principle

The matching principle requires that grant income should be recognized in the same period as the expenses it is meant to offset. This ensures that financial statements accurately reflect the net cost of operations.

Mind Map: Matching Income-Related Grants with Expenses

Accounting Approaches

-

Deferred Income Approach: The grant is initially recorded as deferred income (liability) and recognized as income systematically over the periods in which the related expenses are incurred.

-

Direct Offset Approach: The grant income is directly offset against the related expenses in the income statement, reducing the expense amount.

The choice between these approaches depends on the accounting framework and organizational policy.

Practical Example 1: Research Grant Matching

Scenario: A government agency awards a $100,000 grant to a university to fund a two-year research project. The university incurs research expenses evenly over the two years.

Accounting Treatment:

- The university records the $100,000 grant as deferred income initially.

- Each year, $50,000 is recognized as income to match the $50,000 research expenses incurred.

Journal Entries:

| Period | Debit | Credit | Description |

|---|---|---|---|

| Year 1 | Cash/Bank | Deferred Income | Receipt of grant |

| Year 1 | Deferred Income | Grant Income | Recognize income matching expenses |

| Year 1 | Research Expense | Cash/Bank | Research costs incurred |

| Year 2 | Deferred Income | Grant Income | Recognize income matching expenses |

| Year 2 | Research Expense | Cash/Bank | Research costs incurred |

Mind Map: Research Grant Accounting Flow

Practical Example 2: Training Program Subsidy

Scenario: A local government receives a $30,000 grant to subsidize employee training costs during the fiscal year.

Accounting Treatment:

- The government directly offsets the grant income against the training expenses.

Journal Entries:

| Debit | Credit | Description |

|---|---|---|

| Training Expense | Cash/Bank | Payment for training services |

| Cash/Bank | Grant Income | Recognition of grant income |

This approach simplifies accounting by reducing the net expense reported.

Mind Map: Direct Offset Approach

Key Considerations and Best Practices

- Detailed Expense Tracking: Maintain granular records of expenses related to the grant to ensure accurate matching.

- Regular Reconciliation: Periodically reconcile deferred income balances with incurred expenses.

- Clear Policies: Establish and document accounting policies for grant income recognition.

- Transparent Disclosure: Disclose the nature, amount, and accounting treatment of grants in financial statements.

Summary