Effective Financial Reporting

1. Introduction to Financial Reporting

1.1 Understanding Financial Reporting: Purpose and Importance

Financial reporting is a fundamental process in the finance and corporate sectors, serving as the backbone for communicating a company’s financial health and performance to various stakeholders. It involves the systematic preparation and presentation of financial statements that reflect the economic activities of an organization over a specific period.

Purpose of Financial Reporting

The primary purposes of financial reporting include:

- Providing Information for Decision Making: Enables investors, creditors, and management to make informed decisions.

- Accountability and Stewardship: Helps stakeholders assess how well management has utilized resources.

- Compliance: Ensures adherence to regulatory requirements and accounting standards.

- Performance Measurement: Tracks financial performance against goals and benchmarks.

- Transparency: Builds trust by providing clear, accurate, and timely financial data.

Importance of Financial Reporting

Financial reporting is crucial because it:

- Facilitates investment decisions by providing insights into profitability, liquidity, and solvency.

- Supports credit assessments by lenders evaluating risk.

- Assists management in strategic planning and operational control.

- Enhances market confidence through transparency and accountability.

- Enables regulatory bodies to monitor compliance and protect public interest.

Mind Map: Purpose and Importance of Financial Reporting

Example 1: Decision Making

Consider a company, ABC Corp, planning to expand its operations. The management reviews the latest financial reports to assess cash flow and profitability before committing to new investments. Accurate financial reporting provides the data needed to evaluate whether the expansion is financially viable.

Example 2: Accountability

A nonprofit organization receives donations and must report how funds are utilized. Transparent financial reporting assures donors that their contributions are used effectively, fostering trust and encouraging future support.

Mind Map: Stakeholders and Their Needs

Example 3: Compliance

A publicly traded company must prepare financial statements in accordance with IFRS or GAAP. Failure to comply can result in penalties and loss of investor confidence. For instance, XYZ Ltd. faced regulatory fines due to late submission of audited reports, highlighting the importance of timely and compliant financial reporting.

Summary

Understanding the purpose and importance of financial reporting equips accountants and financial controllers to produce reports that not only meet regulatory standards but also add strategic value to their organizations. Clear, accurate, and timely financial information is essential for sustaining business growth, maintaining stakeholder trust, and ensuring long-term success.

1.2 Key Stakeholders and Their Reporting Needs

Financial reporting serves a diverse group of stakeholders, each with unique interests and requirements. Understanding these stakeholders and tailoring reports to meet their needs is critical for effective communication and decision-making.

Key Stakeholders in Financial Reporting

Internal Stakeholders

a) Management

- Needs: Detailed, timely, and actionable financial data to make strategic and operational decisions.

- Example: A financial controller prepares monthly profit and loss statements highlighting cost centers to help management identify areas for cost reduction.

b) Employees

- Needs: Information on company performance and stability, often related to job security and bonus calculations.

- Example: Annual reports include summarized financial highlights and commentary on company growth to reassure employees.

c) Board of Directors

- Needs: Comprehensive financial reports with risk assessments and forecasts to oversee governance and strategic direction.

- Example: Quarterly financial dashboards with KPIs and variance analysis are presented during board meetings.

External Stakeholders

a) Investors

- Needs: Transparent and accurate financial statements to assess profitability, growth potential, and risks.

- Example: Public companies publish audited annual reports including earnings per share (EPS) and dividend information to attract and retain investors.

b) Creditors (Banks, Lenders)

- Needs: Financial health indicators, liquidity ratios, and cash flow statements to evaluate creditworthiness.

- Example: A bank reviews the cash flow statement and debt-to-equity ratio before approving a loan.

c) Regulators

- Needs: Compliance with accounting standards and legal requirements to ensure market integrity.

- Example: Companies submit financial reports adhering to IFRS or GAAP standards to regulatory bodies like the SEC.

d) Customers and Suppliers

- Needs: Assurance of company stability and ability to fulfill contracts.

- Example: A supplier reviews a company’s financial statements to decide on extending credit terms.

e) Public and Community

- Needs: General understanding of company impact, especially for large corporations affecting local economies.

- Example: Sustainability reports integrated with financial data demonstrate corporate social responsibility.

Mind Map: Stakeholder Reporting Needs

Integrated Example: Tailoring Reports for Multiple Stakeholders

Scenario: A mid-sized manufacturing company is preparing its quarterly financial report.

- For management, the report includes detailed cost breakdowns and variance analysis.

- For the board, an executive summary highlights risks and strategic opportunities.

- For investors, the report emphasizes earnings growth and dividend policy.

- For creditors, liquidity ratios and cash flow forecasts are provided.

- For employees, a simplified summary with company performance highlights is shared.

This approach ensures each stakeholder receives relevant information in a format that supports their decision-making.

Summary

Recognizing the diverse needs of financial reporting stakeholders is essential. By customizing reports—whether through content detail, format, or frequency—accountants and financial controllers can enhance transparency, trust, and the overall value of financial communication.

1.3 Overview of Financial Statements: Balance Sheet, Income Statement, Cash Flow Statement

Financial statements are the cornerstone of effective financial reporting. They provide a structured way to present a company’s financial performance and position to stakeholders. The three primary financial statements are the Balance Sheet, Income Statement, and Cash Flow Statement. Each serves a unique purpose and together they offer a comprehensive picture of a company’s financial health.

Mind Map: Financial Statements Overview

Balance Sheet

The Balance Sheet, also known as the Statement of Financial Position, provides a snapshot of a company’s financial position at a specific point in time. It lists assets, liabilities, and equity, following the fundamental accounting equation:

Assets = Liabilities + Equity

- Assets: Resources owned by the company expected to bring future economic benefits.

- Liabilities: Obligations the company owes to outside parties.

- Equity: The residual interest in the assets after deducting liabilities, representing owners’ claims.

Example:

Imagine a company, ABC Corp, at year-end has:

- Cash: $50,000

- Accounts Receivable: $30,000

- Equipment: $120,000

- Accounts Payable: $40,000

- Long-term Debt: $80,000

- Owner’s Equity: $80,000

The balance sheet would look like:

| Assets | Amount | Liabilities & Equity | Amount |

|---|---|---|---|

| Cash | $50,000 | Accounts Payable | $40,000 |

| Accounts Receivable | $30,000 | Long-term Debt | $80,000 |

| Equipment | $120,000 | Owner’s Equity | $80,000 |

| Total Assets | $200,000 | Total Liabilities & Equity | $200,000 |

Mind Map: Balance Sheet Components

Income Statement

The Income Statement, or Profit & Loss Statement, summarizes revenues and expenses over a period, showing the company’s profitability.

- Revenues: Income earned from normal business operations.

- Expenses: Costs incurred to generate revenues.

- Net Income: Revenues minus expenses, indicating profit or loss.

Example:

For the same ABC Corp, during the fiscal year:

- Sales Revenue: $300,000

- Cost of Goods Sold (COGS): $180,000

- Operating Expenses: $70,000

- Interest Expense: $10,000

- Tax Expense: $15,000

Calculation:

- Gross Profit = Sales Revenue - COGS = $120,000

- Operating Income = Gross Profit - Operating Expenses = $50,000

- Net Income = Operating Income - Interest Expense - Tax Expense = $25,000

| Description | Amount |

|---|---|

| Sales Revenue | $300,000 |

| Cost of Goods Sold | $180,000 |

| Gross Profit | $120,000 |

| Operating Expenses | $70,000 |

| Operating Income | $50,000 |

| Interest Expense | $10,000 |

| Tax Expense | $15,000 |

| Net Income | $25,000 |

Mind Map: Income Statement Structure

Cash Flow Statement

The Cash Flow Statement details the inflows and outflows of cash during a period, categorized into three activities:

- Operating Activities: Cash flows from core business operations.

- Investing Activities: Cash flows from buying or selling assets.

- Financing Activities: Cash flows from borrowing, repaying debt, or equity transactions.

Example:

ABC Corp’s cash flows for the year:

- Cash received from customers: $280,000

- Cash paid to suppliers and employees: $210,000

- Purchase of equipment: $30,000

- Proceeds from issuing shares: $20,000

- Dividends paid: $5,000

Cash Flow from Operating Activities = $280,000 - $210,000 = $70,000

Cash Flow from Investing Activities = -$30,000

Cash Flow from Financing Activities = $20,000 - $5,000 = $15,000

Net Increase in Cash = $70,000 - $30,000 + $15,000 = $55,000

| Activity | Amount |

|---|---|

| Operating Activities | $70,000 |

| Investing Activities | -$30,000 |

| Financing Activities | $15,000 |

| Net Increase in Cash | $55,000 |

Mind Map: Cash Flow Statement Components

Summary

Understanding these three financial statements is essential for accountants and financial controllers to prepare accurate reports, analyze financial health, and communicate effectively with stakeholders. Integrating best practices such as clear presentation, reconciliation, and timely reporting ensures these statements fulfill their purpose.

1.4 Regulatory Frameworks and Standards: IFRS, GAAP, and Beyond

Financial reporting is governed by a variety of regulatory frameworks and standards designed to ensure consistency, transparency, and comparability of financial statements across organizations and jurisdictions. Understanding these frameworks is essential for accountants and financial controllers to prepare compliant and reliable reports.

Key Financial Reporting Frameworks

- IFRS (International Financial Reporting Standards)

- GAAP (Generally Accepted Accounting Principles)

- Other Regional and Industry-Specific Standards

IFRS (International Financial Reporting Standards)

IFRS is a globally recognized set of accounting standards developed by the International Accounting Standards Board (IASB). It is widely adopted in over 140 countries, including the European Union, Australia, and many parts of Asia and Africa.

Key Features:

- Principles-based approach

- Emphasis on fair value measurement

- Focus on transparency and comparability

Example: A multinational corporation preparing consolidated financial statements uses IFRS to ensure that its financial reports are consistent and comparable across all countries where it operates.

GAAP (Generally Accepted Accounting Principles)

GAAP refers to the accounting standards used primarily in the United States, governed by the Financial Accounting Standards Board (FASB). GAAP is more rules-based compared to IFRS.

Key Features:

- Detailed rules and guidelines

- Emphasis on historical cost

- Strong regulatory oversight by the SEC (Securities and Exchange Commission)

Example: A US-based publicly traded company follows GAAP to comply with SEC regulations and provide detailed disclosures to investors.

Mind Map: Overview of IFRS vs GAAP

Other Regulatory Frameworks and Standards

- Local GAAPs: Many countries have their own GAAPs that may differ from IFRS or US GAAP.

- Industry-Specific Standards: Certain industries such as banking, insurance, and oil & gas have additional reporting requirements.

- Regulatory Bodies: Examples include the SEC (US), FCA (UK), and ESMA (EU).

Example: A financial institution in the UK must comply with IFRS as well as additional reporting requirements set by the Financial Conduct Authority (FCA).

Mind Map: Regulatory Bodies and Their Roles

Harmonization and Convergence Efforts

There have been ongoing efforts to reduce differences between IFRS and GAAP to facilitate cross-border investment and reporting.

Example: The IFRS and FASB have collaborated on projects such as revenue recognition and lease accounting to align standards.

Practical Example: Choosing the Right Framework

A mid-sized company expanding internationally must decide whether to adopt IFRS or continue with local GAAP. By analyzing the benefits of IFRS—such as easier access to foreign investment and simplified consolidation—they opt for IFRS adoption.

Summary

Understanding the regulatory frameworks and standards is critical for effective financial reporting. Accountants and financial controllers must stay updated on changes and ensure compliance to maintain credibility and support strategic decision-making.

1.5 Common Challenges in Financial Reporting

Financial reporting is a critical function for accountants and financial controllers, but it is fraught with challenges that can impact accuracy, compliance, and stakeholder trust. Understanding these common hurdles helps professionals anticipate issues and implement best practices to overcome them.

Mind Map: Common Challenges in Financial Reporting

Data Accuracy and Integrity

One of the most fundamental challenges is ensuring the accuracy and completeness of financial data. Errors can arise from manual data entry, missing transactions, or poor integration between systems.

Example: A financial controller noticed discrepancies between the general ledger and subsidiary ledgers during reconciliation. Upon investigation, it was found that some sales invoices were not entered into the system due to a manual entry backlog, leading to understated revenue figures.

Best Practice: Implement automated data validation checks and reconciliation processes to catch inconsistencies early. For instance, using software that flags missing entries or mismatched balances can reduce human error.

Compliance and Regulatory Changes

Financial reporting standards such as IFRS and GAAP are frequently updated, and companies operating across multiple jurisdictions face the added complexity of differing local requirements.

Example: A multinational corporation struggled to comply with the new lease accounting standard (IFRS 16) because different subsidiaries interpreted the rules differently, delaying the consolidated reporting.

Best Practice: Maintain a dedicated compliance team or subscribe to regulatory update services. Regular training sessions for the reporting team ensure everyone understands new requirements and applies them consistently.

Complexity of Financial Transactions

Certain transactions, such as revenue recognition, intercompany eliminations, and foreign currency translations, add layers of complexity that can lead to errors if not handled properly.

Example: During consolidation, intercompany sales were not eliminated, resulting in inflated revenue and expenses on the consolidated financial statements.

Best Practice: Develop clear policies and automated workflows for complex transactions. Use consolidation software that automatically eliminates intercompany transactions and applies currency translation adjustments.

Timeliness and Efficiency

The pressure to close books quickly at month-end or quarter-end can lead to rushed processes and mistakes.

Example: An accounting team manually compiled reports from multiple spreadsheets, causing delays and last-minute corrections that impacted report reliability.

Best Practice: Adopt integrated financial reporting tools that streamline data aggregation and report generation. Establish a standardized close calendar and assign clear responsibilities to improve efficiency.

Transparency and Disclosure

Providing clear, comprehensive disclosures is essential for stakeholder trust but can be challenging when balancing detail with readability.

Example: A company’s financial notes lacked sufficient explanation of significant accounting estimates, leading to investor confusion and questions during earnings calls.

Best Practice: Use plain language and standardized templates for disclosures. Include examples or scenarios to clarify complex accounting policies.

Technology Limitations

Outdated or incompatible systems can hinder data accuracy, reporting speed, and security.

Example: A firm relying on legacy accounting software faced frequent data export errors and lacked real-time reporting capabilities.

Best Practice: Invest in modern, cloud-based financial reporting platforms that offer automation, integration, and enhanced security features.

Summary Mind Map: Overcoming Challenges in Financial Reporting

By proactively addressing these common challenges with practical strategies and examples, accountants and financial controllers can enhance the reliability, clarity, and timeliness of their financial reports, ultimately supporting better business decisions and regulatory compliance.

2. Preparing Accurate Financial Statements

2.1 Best Practices for Data Collection and Validation

Effective financial reporting begins with the foundation of accurate and reliable data. Data collection and validation are critical steps that ensure the integrity of financial statements. This section explores best practices for collecting and validating financial data, supported by practical examples and mind maps to visualize the process.

Key Principles of Data Collection

- Accuracy: Ensure data is recorded correctly without errors.

- Completeness: Collect all relevant data to avoid gaps.

- Timeliness: Gather data promptly to maintain relevance.

- Consistency: Use standardized formats and definitions.

- Traceability: Maintain audit trails to verify data sources.

Mind Map: Data Collection Best Practices

Step-by-Step Best Practices for Data Collection

-

Identify Data Sources:

- List all internal and external sources relevant to financial reporting.

- Example: For accounts payable, sources include vendor invoices, purchase orders, and payment records.

-

Standardize Data Formats:

- Use consistent templates and coding systems.

- Example: Date formats standardized to YYYY-MM-DD across all reports.

-

Automate Where Possible:

- Use software tools to extract and consolidate data.

- Example: Integration of ERP with reporting tools to auto-import ledger entries.

-

Implement Access Controls:

- Restrict data entry and editing rights to authorized personnel.

- Example: Only finance team members can update the general ledger.

-

Maintain Documentation:

- Keep detailed records of data sources and collection methods.

- Example: Store scanned copies of invoices linked to accounting entries.

Mind Map: Data Validation Techniques

Best Practices for Data Validation

-

Automated Validation Rules:

- Set rules in software to flag anomalies.

- Example: Flagging invoice amounts exceeding predefined thresholds.

-

Cross-Verification:

- Compare data across multiple sources.

- Example: Matching purchase orders with received goods and invoices.

-

Reconciliation Processes:

- Regularly reconcile accounts to identify discrepancies.

- Example: Monthly bank reconciliations to verify cash balances.

-

Exception Reporting:

- Generate reports highlighting unusual or missing data.

- Example: Report on unpaid invoices past due date.

-

Audit Trails and Approvals:

- Track changes and require approvals for adjustments.

- Example: Approval workflow for journal entry corrections.

Example: Validating Accounts Receivable Data

Scenario: The finance team collects accounts receivable data from the sales system and the general ledger.

- Step 1: Extract sales invoices from the sales system.

- Step 2: Extract accounts receivable balances from the general ledger.

- Step 3: Perform automated matching to identify invoices not recorded in the ledger.

- Step 4: Investigate discrepancies flagged by the system.

- Step 5: Reconcile differences and document adjustments.

This process ensures that reported receivables are complete and accurate, reducing the risk of misstated assets.

Summary

Adopting rigorous data collection and validation practices is essential for producing trustworthy financial reports. By combining automation, standardized procedures, and thorough manual reviews, finance professionals can minimize errors and enhance the credibility of their reporting.

For accountants and financial controllers, embedding these best practices into daily workflows not only improves report quality but also supports compliance and strategic decision-making.

2.2 Ensuring Completeness and Accuracy: Practical Checklists

Ensuring completeness and accuracy in financial reporting is fundamental to producing reliable financial statements that stakeholders can trust. This section provides practical checklists and examples to help accountants and financial controllers systematically verify that all necessary data is included and accurately represented.

Why Completeness and Accuracy Matter

- Completeness ensures no relevant financial data is omitted.

- Accuracy guarantees that the data reported reflects the true financial position.

- Both are critical to avoid misstatements, regulatory penalties, and loss of stakeholder confidence.

Practical Checklist for Ensuring Completeness

Example:

A financial controller uses this checklist during month-end close. They verify that all sales invoices for the month are recorded, check that supplier invoices received after month-end are accrued correctly, and confirm that bank reconciliations are complete. This prevents revenue or expense omissions that could distort the income statement.

Practical Checklist for Ensuring Accuracy

Example:

An accountant notices a discrepancy between the fixed asset register and the general ledger. Using the accuracy checklist, they verify depreciation calculations and discover an asset was depreciated twice. Correcting this error ensures the balance sheet reflects the true asset value.

Integrated Example: Month-End Close Process

By following this structured approach, the finance team minimizes errors and omissions, producing financial reports that are both complete and accurate.

Tips for Implementation

- Develop standardized checklists tailored to your organization’s processes.

- Use technology to automate reconciliations and data validation where possible.

- Encourage a culture of review and accountability within the finance team.

- Document all checks and approvals to maintain an audit trail.

Summary

Ensuring completeness and accuracy is not a one-time task but a continuous process supported by practical checklists and diligent review. By embedding these practices into daily routines, accountants and financial controllers can enhance the reliability of financial reports and support sound business decisions.

2.3 Example: Reconciling Bank Statements to Ensure Accuracy

Bank statement reconciliation is a fundamental best practice in financial reporting that ensures the accuracy and completeness of cash balances reported in the financial statements. It involves comparing the company’s internal cash records against the bank’s records to identify and resolve discrepancies.

Why Reconcile Bank Statements?

- Detect errors or omissions in the company’s books or the bank’s records.

- Identify fraudulent transactions or unauthorized withdrawals.

- Ensure that the cash balance reported in the financial statements is accurate.

Step-by-Step Process of Bank Reconciliation

Practical Example

Scenario:

ABC Corp’s cash ledger shows a balance of $15,000 on March 31. The bank statement for the same date shows $14,500.

Step 1: Gather Documents

- Company cash ledger balance: $15,000

- Bank statement balance: $14,500

Step 2: Identify Outstanding Items

- Outstanding checks (issued but not cleared): $1,200

- Deposits in transit (deposited but not yet reflected by bank): $700

Step 3: Adjust Bank Statement Balance

| Description | Amount | Adjusted Bank Balance |

|---|---|---|

| Bank statement balance | $14,500 | $14,500 |

| Add: Deposits in transit | $700 | $15,200 |

| Less: Outstanding checks | $1,200 | $14,000 |

Step 4: Identify Bank Charges and Errors

- Bank service fee not recorded in company books: $50

- Bank error: $100 deposit recorded twice by bank

Step 5: Adjust Company Ledger

| Description | Amount | Adjusted Company Balance |

|---|---|---|

| Company cash ledger balance | $15,000 | $15,000 |

| Less: Bank service fee | $50 | $14,950 |

| Add: Bank error correction | $100 | $15,050 |

Step 6: Final Comparison

- Adjusted bank balance: $14,000

- Adjusted company balance: $15,050

Step 7: Investigate Remaining Difference

- The remaining difference of $1,050 indicates further investigation is needed (e.g., timing differences, unrecorded transactions).

Mind Map: Common Reconciling Items

Tips for Effective Bank Reconciliation

- Perform reconciliations regularly (monthly or more frequently).

- Use reconciliation software or spreadsheets to track and document the process.

- Maintain clear documentation for all adjustments.

- Communicate discrepancies promptly with the bank.

- Train accounting staff on common reconciliation issues.

Summary

Reconciling bank statements is a critical control activity that enhances the reliability of financial reporting. By systematically comparing internal records with bank statements, accountants can detect errors, prevent fraud, and ensure that reported cash balances are accurate and trustworthy.

2.4 Handling Adjustments and Corrections with Transparency

Financial reporting is an evolving process where adjustments and corrections are inevitable. Handling these changes transparently is crucial to maintain the trust of stakeholders and ensure the accuracy of financial statements. This section explores best practices for managing adjustments and corrections, supported by clear examples and mind maps to visualize the process.

Why Transparency Matters in Adjustments and Corrections

- Builds stakeholder confidence

- Ensures compliance with accounting standards

- Prevents misinterpretation or suspicion of financial manipulation

- Facilitates audit processes

Types of Adjustments and Corrections

Mind Map: Types of Adjustments and Corrections

Best Practices for Handling Adjustments and Corrections

-

Document Every Change

- Maintain detailed records explaining why the adjustment or correction was made.

- Include dates, amounts, and responsible personnel.

-

Communicate Clearly in Financial Statements

- Use notes to the financial statements to disclose the nature and impact of adjustments.

- Highlight prior period adjustments separately.

-

Use Standardized Procedures

- Implement internal controls and approval workflows for adjustments.

- Ensure segregation of duties to reduce errors and fraud.

-

Reconcile Regularly

- Perform periodic reconciliations to detect discrepancies early.

-

Train Staff Continuously

- Keep accounting teams updated on standards and internal policies.

Example 1: Correcting a Misclassified Expense

Scenario: An expense originally recorded as an administrative cost was actually a marketing expense.

Steps Taken:

- Identify the misclassification during the monthly review.

- Reverse the original entry and record the expense under the correct account.

- Document the correction with a memo explaining the reason.

- Disclose the correction in the notes if it materially affects financial results.

Impact: This correction ensures accurate expense categorization, aiding better budget analysis and reporting.

Example 2: Prior Period Adjustment for Revenue Recognition

Scenario: Revenue from a contract was recognized prematurely in the previous financial year.

Steps Taken:

- Adjust the retained earnings account to reflect the correction of prior period revenue.

- Restate comparative financial statements if required.

- Provide detailed disclosure in the notes explaining the nature and impact of the adjustment.

Impact: This maintains compliance with revenue recognition standards and provides stakeholders with a true picture of financial performance.

Mind Map: Process for Handling Adjustments and Corrections Transparently

Tools and Techniques to Support Transparency

- Use of accounting software with audit trails

- Version control for financial reports

- Regular internal audits and reconciliations

- Checklists for adjustments and corrections

Summary

Handling adjustments and corrections with transparency is essential for credible financial reporting. By documenting changes meticulously, communicating clearly, and following standardized procedures, accountants and financial controllers can uphold integrity and provide stakeholders with reliable financial information.

2.5 Case Study: Avoiding Common Errors in Revenue Recognition

Revenue recognition is a critical aspect of financial reporting that directly impacts an organization’s reported earnings and financial health. Errors in this area can lead to misstated financial statements, regulatory penalties, and loss of stakeholder trust. This case study explores common pitfalls in revenue recognition and demonstrates best practices to avoid them through practical examples and mind maps.

Common Errors in Revenue Recognition

Best Practices to Avoid Errors

Example Scenario: Software Company Subscription Revenue

Background: A software company sells annual subscriptions with monthly service delivery. The sales team often books revenue upfront upon contract signing, leading to premature revenue recognition.

Issue: Revenue is recorded in full at contract signing, inflating current period revenue and violating the matching principle.

Solution:

- Recognize revenue ratably over the subscription period (12 months).

- Use automated billing and revenue recognition schedules in the accounting system.

- Maintain signed contracts and delivery logs as documentation.

Mind Map:

Example Scenario: Manufacturing Company with Multiple Deliverables

Background: A manufacturing company sells machinery bundled with installation and maintenance services.

Issue: Revenue is recognized only when the machinery is shipped, ignoring the installation and maintenance components, leading to incomplete revenue recognition.

Solution:

- Identify separate performance obligations: machinery, installation, maintenance.

- Allocate transaction price based on standalone selling prices.

- Recognize revenue for each component as it is delivered or performed.

Mind Map:

Summary Checklist for Avoiding Revenue Recognition Errors

Revenue Recognition Error Prevention Checklist

- Confirm delivery or service completion before recognizing revenue

- Verify contract terms and performance obligations

- Allocate transaction price accurately among obligations

- Recognize revenue in the correct accounting period

- Maintain comprehensive supporting documentation

- Use automated systems to enforce recognition policies

- Conduct regular training and internal reviews

Conclusion

By understanding common revenue recognition errors and implementing structured policies, controls, and technology solutions, financial controllers and accountants can ensure accurate and compliant financial reporting. The examples and mind maps provided illustrate practical approaches to applying these best practices in real-world scenarios, ultimately enhancing the reliability and transparency of financial statements.

3. Enhancing Clarity and Transparency in Reporting

3.1 Using Clear Language and Consistent Terminology

Effective financial reporting hinges on the ability to communicate complex financial information in a way that is easily understood by diverse stakeholders. Using clear language and consistent terminology is essential to avoid confusion, misinterpretation, and to build trust.

Why Clear Language Matters

- Enhances comprehension: Stakeholders from non-financial backgrounds can grasp the report’s key messages.

- Reduces errors: Clear wording minimizes misinterpretation during analysis or decision-making.

- Builds credibility: Transparent communication fosters confidence in the financial data presented.

Key Principles for Clear Language

- Use simple, straightforward words instead of jargon.

- Avoid ambiguous terms or acronyms without explanation.

- Write in active voice to improve readability.

- Keep sentences concise and focused.

- Define technical terms when first introduced.

Consistent Terminology: Why It’s Critical

- Ensures uniform understanding across reports and periods.

- Facilitates easier comparison and trend analysis.

- Helps maintain compliance with accounting standards.

Mind Map: Clear Language and Consistent Terminology in Financial Reporting

Practical Examples

Example 1: Avoiding Jargon

- Instead of: “The EBITDA margin experienced a contraction due to adverse market conditions.”

- Use: “The company’s earnings before interest, taxes, depreciation, and amortization (EBITDA) margin decreased because of challenging market conditions.”

This clarifies the acronym and uses simpler language.

Example 2: Consistent Terminology Across Reports

- In Q1 report: “Net Revenue”

- In Q2 report: “Total Sales”

These terms may confuse readers if used interchangeably. Choose one term, e.g., “Net Revenue,” and use it consistently.

Example 3: Defining Technical Terms

- First mention: “Deferred Tax Assets (DTAs) represent taxes recoverable in future periods.”

- Subsequent mentions: Simply use “DTAs”.

This approach educates the reader and maintains clarity.

Mind Map: Implementation Strategies

Summary

Using clear language and consistent terminology is not just about simplifying financial reports; it is about making them accessible, trustworthy, and actionable. By applying these best practices and supporting them with style guides and training, financial controllers and accountants can significantly improve the quality and impact of their financial reporting.

3.2 Visual Aids: Charts, Graphs, and Tables for Better Understanding

Effective financial reporting hinges not only on the accuracy of data but also on how clearly that data is communicated. Visual aids such as charts, graphs, and tables transform raw numbers into intuitive insights, enabling stakeholders—especially those without deep financial expertise—to grasp key messages quickly and confidently.

Why Use Visual Aids?

- Enhance comprehension: Visuals simplify complex data sets.

- Highlight trends and patterns: Easily spot growth, decline, or anomalies.

- Support decision-making: Clear visuals provide actionable insights.

- Engage audiences: More appealing and memorable than plain text or numbers.

Common Types of Visual Aids in Financial Reporting

| Visual Aid | Purpose | Example Use Case |

|---|---|---|

| Bar Charts | Compare discrete categories or periods | Comparing quarterly revenue across business units |

| Line Graphs | Show trends over time | Tracking monthly expenses over a fiscal year |

| Pie Charts | Display proportions or percentage breakdowns | Illustrating expense distribution by category |

| Tables | Present detailed numeric data clearly | Detailed balance sheet or income statement figures |

| Waterfall Charts | Show cumulative effect of sequential values | Visualizing profit and loss components |

Mind Map: Choosing the Right Visual Aid

Example 1: Using a Bar Chart to Compare Quarterly Revenue

Imagine a company wants to demonstrate how its revenue has performed across four quarters in different regions.

| Region | Q1 Revenue | Q2 Revenue | Q3 Revenue | Q4 Revenue |

|---|---|---|---|---|

| North America | $1.2M | $1.5M | $1.7M | $2.0M |

| Europe | $900K | $1.1M | $1.3M | $1.4M |

| Asia | $700K | $850K | $900K | $1.1M |

A clustered bar chart can visually display these figures side-by-side, making it easy to compare both regionally and quarterly.

Example 2: Line Graph for Expense Trend Analysis

Tracking monthly operating expenses over a year helps identify seasonal spikes or cost-saving successes.

| Month | Operating Expenses |

|---|---|

| January | $150,000 |

| February | $140,000 |

| March | $160,000 |

| … | … |

| December | $130,000 |

Plotting these on a line graph reveals trends and helps forecast future expenses.

Example 3: Pie Chart for Expense Distribution

A company’s total expenses of $1,000,000 can be broken down as:

- Salaries: 40%

- Rent: 20%

- Marketing: 15%

- Utilities: 10%

- Miscellaneous: 15%

A pie chart visually communicates how each category contributes to overall expenses, making it easier for stakeholders to understand cost structure.

Best Practices for Using Visual Aids

- Keep it simple: Avoid clutter; focus on key data points.

- Use consistent colors: Assign colors to categories and maintain them across reports.

- Label clearly: Axes, legends, and data points should be easy to read.

- Provide context: Include titles and brief explanations.

- Avoid distortion: Ensure scales and proportions accurately reflect data.

Mind Map: Best Practices for Visual Aids

Summary

Incorporating charts, graphs, and tables into financial reports is essential for effective communication. By selecting the right visual aids and following best practices, accountants and financial controllers can ensure their reports are not only accurate but also accessible and actionable for all stakeholders.

3.3 Example: Simplifying Complex Financial Data for Non-Financial Stakeholders

Financial reports often contain complex data that can be overwhelming for non-financial stakeholders such as marketing teams, operations managers, or board members without a finance background. Simplifying this data is crucial to ensure clear communication, informed decision-making, and stakeholder engagement.

Key Strategies to Simplify Complex Financial Data:

- Use Plain Language: Avoid jargon and technical terms. Explain financial concepts in everyday language.

- Visualize Data: Use charts, graphs, and infographics to present numbers visually.

- Focus on Key Metrics: Highlight the most relevant figures that align with stakeholder interests.

- Provide Context: Explain what the numbers mean and why they matter.

- Summarize Insights: Offer concise takeaways or executive summaries.

Mind Map: Simplifying Financial Data for Non-Financial Stakeholders

Example Scenario:

Situation: A financial controller needs to present the quarterly financial performance to the marketing team, who have limited financial expertise.

Step 1: Identify Key Metrics Relevant to Marketing

- Revenue growth

- Marketing spend vs. sales impact

- Customer acquisition cost

Step 2: Use Visuals

- Bar chart showing revenue growth quarter-over-quarter

- Pie chart illustrating marketing budget allocation

Step 3: Provide Context and Explanation

- Explain how increased marketing spend in digital channels contributed to a 10% rise in revenue.

- Clarify what customer acquisition cost means and why it’s important.

Step 4: Summarize

- “Our focused investment in digital marketing has driven a significant increase in revenue this quarter, improving customer acquisition efficiency by 15%.”

Mind Map: Example Presentation Flow for Non-Financial Stakeholders

Additional Example: Using Analogies to Explain Financial Concepts

- Revenue: “Think of revenue as the total amount of money coming into a store from all sales, like the total cash collected at the checkout.”

- Profit Margin: “Profit margin is like the slice of the pie you get to keep after paying all the bills.”

- Cash Flow: “Cash flow is the money flowing in and out of your wallet — it’s important to have enough coming in to cover what goes out.”

Visual Example: Simplified Income Statement Snapshot

| Metric | Amount (USD) | Explanation for Non-Financial Stakeholders |

|---|---|---|

| Total Revenue | $1,000,000 | Total sales made during the quarter |

| Cost of Goods Sold | $600,000 | Cost to produce the products sold |

| Gross Profit | $400,000 | Money left after production costs |

| Operating Expenses | $250,000 | Costs like marketing, salaries, and rent |

| Net Profit | $150,000 | Final earnings after all expenses |

Explanation: “Out of every dollar earned, 40 cents remain after production costs, and after paying all other expenses, the company keeps 15 cents as profit.”

By integrating these approaches—clear language, visual aids, contextual explanations, and relatable examples—financial controllers and accountants can make complex financial data accessible and actionable for non-financial stakeholders, fostering better collaboration and strategic alignment.

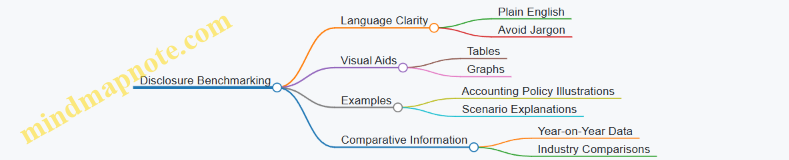

3.4 Disclosures and Notes: What to Include and How to Present

Disclosures and notes to the financial statements are essential components that provide additional context, explanations, and details that cannot be fully captured in the primary financial statements. They enhance transparency, improve understanding, and ensure compliance with accounting standards.

What to Include in Disclosures and Notes

- Accounting Policies: Description of the significant accounting policies adopted by the company (e.g., revenue recognition, depreciation methods).

- Judgments and Estimates: Key areas where management has made significant judgments or estimates (e.g., impairment testing, provisions).

- Breakdown of Financial Statement Items: Detailed breakdowns such as aging of receivables, inventory classifications, or debt maturities.

- Contingent Liabilities and Commitments: Potential obligations or guarantees that may impact the company’s financial position.

- Related Party Transactions: Details of transactions with related parties to ensure transparency.

- Subsequent Events: Events occurring after the reporting period that could affect financial statements.

- Segment Reporting: Financial information by business segment or geographic area.

- Risk Management Disclosures: Information on financial risks like credit risk, liquidity risk, and market risk.

How to Present Disclosures and Notes Effectively

- Clarity and Conciseness: Use clear, straightforward language avoiding jargon.

- Logical Organization: Group related disclosures together under clear headings.

- Cross-Referencing: Link notes to relevant line items in the financial statements.

- Use of Tables and Charts: Present complex data in tables or charts for easier comprehension.

- Consistency: Maintain consistent terminology and formatting throughout.

Mind Map: Key Components of Disclosures and Notes

Example 1: Disclosure of Accounting Policies

“Revenue is recognized when control of the goods or services is transferred to the customer, generally upon delivery. The company uses the percentage-of-completion method for long-term contracts, recognizing revenue based on the stage of completion measured by costs incurred to date relative to total estimated costs.”

This note clarifies how and when revenue is recognized, helping users understand the timing and basis of reported revenue.

Example 2: Breakdown of Debt Maturities

| Debt Instrument | Amount (USD) | Maturity Date |

|---|---|---|

| Term Loan | 1,000,000 | 31-Dec-2025 |

| Revolving Credit | 500,000 | 30-Jun-2024 |

| Bonds | 2,000,000 | 31-Dec-2027 |

This table provides stakeholders with detailed information about the company’s debt obligations, aiding in liquidity assessment.

Mind Map: Best Practices for Presenting Disclosures

Example 3: Related Party Transactions Disclosure

“During the year, the company purchased raw materials amounting to $500,000 from XYZ Ltd., a company owned by a close family member of a key management personnel. These transactions were conducted at arm’s length prices similar to those offered to unrelated parties.”

This disclosure ensures transparency about potential conflicts of interest.

Summary

Disclosures and notes are vital for providing a full picture of a company’s financial health and operations. By including comprehensive, clear, and well-organized notes, financial controllers and accountants can enhance the credibility and usefulness of financial reports, enabling stakeholders to make better-informed decisions.

3.5 Case Study: Transparent Reporting in a Multinational Corporation

Background

GlobalTech Solutions (GTS) is a multinational corporation operating in over 30 countries, specializing in technology products and services. Given its complex operations and diverse stakeholder base, transparent financial reporting is crucial for maintaining investor confidence, regulatory compliance, and internal decision-making.

Challenges Faced by GTS

- Diverse regulatory environments across countries

- Complex intercompany transactions

- Large volume of financial data from multiple subsidiaries

- Need to communicate financial results clearly to non-financial stakeholders

Transparent Reporting Practices Implemented

-

Standardized Reporting Framework Across Subsidiaries

- Adopted IFRS as the common reporting standard.

- Developed a centralized reporting manual to ensure consistency.

-

Clear and Comprehensive Disclosures

- Detailed notes on revenue recognition policies.

- Transparent reporting of foreign exchange impacts.

- Disclosure of related party transactions with clear explanations.

-

Use of Visual Aids and Summaries

- Executive summaries highlighting key financial metrics.

- Infographics to explain complex financial concepts.

-

Regular Training and Communication

- Workshops for finance teams on best reporting practices.

- Open forums for Q&A with management and auditors.

-

Technology Integration

- Implemented a cloud-based consolidation tool for real-time data.

- Automated generation of disclosures to reduce errors.

Mind Map: Transparent Reporting Components at GTS

Example: Simplifying Foreign Exchange Impact Disclosure

Before: “The company recognizes foreign exchange gains and losses in accordance with IAS 21. The net foreign exchange loss for the period was $2.5 million, primarily due to currency fluctuations in emerging markets.”

After (Transparent and Clear): “During Q1, GlobalTech Solutions experienced a net foreign exchange loss of $2.5 million. This was mainly driven by the depreciation of the Brazilian Real and South African Rand against the US Dollar. To mitigate such risks, the company employs hedging strategies detailed in Note 15.”

This approach provides clarity on the source of the loss and points stakeholders to risk management policies.

Mind Map: Communication Strategy for Non-Financial Stakeholders

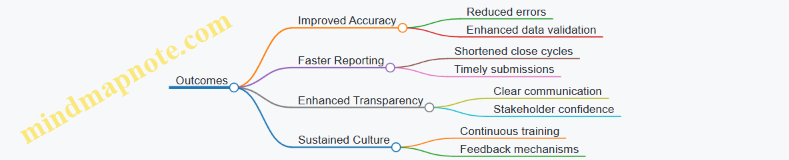

Outcomes

- Improved stakeholder trust and satisfaction as evidenced by positive feedback in investor meetings.

- Reduced audit queries related to disclosures by 30%.

- Faster month-end close process due to standardized and automated reporting.

Key Takeaways

- Transparency requires not just compliance but clarity and accessibility.

- Visual aids and plain language enhance understanding for diverse audiences.

- Continuous training and technology adoption are critical enablers.

This case study demonstrates how a multinational corporation can embed transparency into its financial reporting processes, balancing regulatory demands with stakeholder communication needs.

4. Leveraging Technology for Efficient Reporting

4.1 Financial Reporting Software: Features and Benefits

Financial reporting software has become an indispensable tool for accountants and financial controllers aiming to enhance accuracy, efficiency, and transparency in their reporting processes. This section explores the core features and benefits of such software, supported by practical examples and mind maps to illustrate key concepts.

Key Features of Financial Reporting Software

- Automated Data Integration: Seamlessly connects with ERP systems, accounting platforms, and other financial databases to pull real-time data.

- Report Templates and Customization: Offers pre-built templates for common financial statements and allows customization to meet specific organizational needs.

- Data Validation and Error Checking: Automatically detects inconsistencies, missing data, or anomalies to ensure accuracy.

- Multi-Currency and Multi-Entity Support: Facilitates consolidated reporting across different subsidiaries and currencies.

- Collaboration Tools: Enables multiple users to work on reports simultaneously with version control and audit trails.

- Regulatory Compliance Modules: Helps ensure reports meet IFRS, GAAP, or other relevant standards.

- Visualization and Dashboarding: Converts raw data into charts, graphs, and dashboards for easier interpretation.

- Security and Access Controls: Protects sensitive financial data through role-based permissions and encryption.

Benefits of Using Financial Reporting Software

- Increased Efficiency: Automation reduces manual data entry and accelerates report generation.

- Improved Accuracy: Built-in validation minimizes human errors and enhances data integrity.

- Enhanced Transparency: Clear audit trails and standardized formats build stakeholder confidence.

- Scalability: Supports growing organizations with complex reporting needs.

- Better Decision-Making: Real-time insights and visualizations empower timely strategic decisions.

- Cost Savings: Reduces reliance on external consultants and manual labor.

Mind Map: Features of Financial Reporting Software

Mind Map: Benefits of Financial Reporting Software

Practical Example: Streamlining Month-End Close with Financial Reporting Software

Scenario: A mid-sized manufacturing company struggled with a time-consuming month-end close process, involving manual data consolidation from multiple departments and spreadsheets.

Solution: They implemented a financial reporting software that integrated directly with their ERP and accounting systems.

Outcome:

- Automated data aggregation reduced the close process from 10 days to 4 days.

- Real-time validation caught discrepancies early, preventing last-minute adjustments.

- Customized dashboards provided management with instant visibility into financial performance.

This example highlights how leveraging software features can transform reporting efficiency and accuracy.

Practical Example: Ensuring Compliance with Regulatory Standards

Scenario: A multinational corporation needed to comply with both IFRS and local GAAP reporting requirements.

Solution: Using financial reporting software with built-in compliance modules, they generated parallel reports tailored to each standard.

Outcome:

- Reduced risk of non-compliance through automated standard checks.

- Simplified audit process with clear documentation and version control.

This demonstrates the software’s role in managing complex regulatory environments effectively.

In conclusion, financial reporting software offers a comprehensive suite of features that significantly benefit accountants and financial controllers by automating processes, improving accuracy, and supporting compliance. By understanding and leveraging these capabilities, finance professionals can deliver more timely, transparent, and insightful reports that drive better business outcomes.

4.2 Automating Data Collection and Report Generation

Automation in financial reporting is a game-changer for accountants and financial controllers, significantly reducing manual effort, minimizing errors, and accelerating the reporting cycle. This section explores how automating data collection and report generation can be effectively implemented, supported by practical examples and mind maps to visualize the process.

Why Automate Data Collection and Report Generation?

- Efficiency: Automates repetitive tasks, freeing up time for analysis and strategic activities.

- Accuracy: Reduces human errors in data entry and calculations.

- Timeliness: Enables faster closing cycles and more frequent reporting.

- Consistency: Standardizes data formats and reporting templates.

Key Components of Automation in Financial Reporting

Automating Data Collection

Automation begins with gathering financial data from various sources such as ERP systems, bank feeds, and cloud platforms.

- Example: Integrating your ERP system with a financial reporting tool via APIs to automatically pull trial balance data daily.

- Example: Using RPA (Robotic Process Automation) bots to extract data from legacy systems or spreadsheets.

Mind Map:

Automating Report Generation

Once data is collected and validated, the next step is generating reports automatically.

- Template-Based Reporting: Predefined templates with dynamic fields that populate automatically.

- Dynamic Dashboards: Interactive visualizations that update in real-time as data changes.

- Scheduled Reports: Reports generated and distributed automatically at set intervals (e.g., monthly, quarterly).

Example: A financial controller sets up a monthly P&L report template in a reporting software that pulls data from the ERP system and emails the report to department heads every first Monday.

Mind Map:

Practical Example: Automating Month-End Close Reporting

Scenario: A company struggles with a lengthy month-end close process involving manual data consolidation from multiple systems.

Solution:

- Data Integration: Connect ERP, payroll, and bank systems through API connectors.

- Validation Rules: Implement automated checks for missing entries and outliers.

- Report Templates: Develop standardized financial statement templates.

- Scheduling: Configure reports to generate automatically on the 2nd business day after month-end.

- Distribution: Automatically send reports to finance leadership and auditors.

Outcome: Reduced close time from 10 days to 4 days, improved accuracy, and enhanced stakeholder confidence.

Tips for Successful Automation

- Start with mapping your current manual processes.

- Identify repetitive and error-prone tasks.

- Choose tools that integrate well with your existing systems.

- Involve end-users in designing templates and dashboards.

- Regularly review and update automation rules to adapt to changes.

By embracing automation in data collection and report generation, financial controllers and accountants can transform financial reporting from a time-consuming chore into a streamlined, value-adding process.

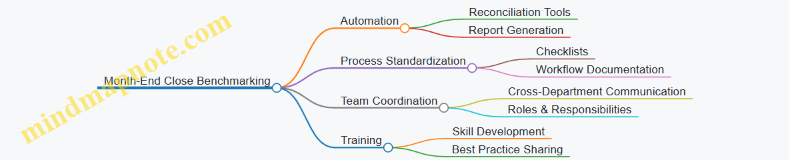

4.3 Example: Using Cloud-Based Tools to Streamline Month-End Close

Month-end close is a critical but often time-consuming process in financial reporting. Leveraging cloud-based tools can significantly improve efficiency, accuracy, and collaboration during this period. Below, we explore how cloud technology transforms month-end close with practical examples and a detailed mind map.

Why Use Cloud-Based Tools for Month-End Close?

- Real-time Data Access: Teams can access financial data anytime, anywhere.

- Collaboration: Multiple users can work simultaneously on reports.

- Automation: Routine tasks like data consolidation and reconciliations can be automated.

- Audit Trail: Cloud platforms maintain logs for compliance and review.

Mind Map: Streamlining Month-End Close with Cloud-Based Tools

Practical Example: Using Cloud-Based Tools in Action

Scenario: A mid-sized corporation traditionally takes 10 days to complete month-end close due to manual data gathering, reconciliations, and report compilation.

Implementation: They adopt a cloud-based financial close platform integrated with their ERP and bank accounts.

Step-by-Step Process:

-

Automated Data Integration: The platform automatically pulls trial balances, bank statements, and subsidiary ledgers daily.

-

Auto-Reconciliation: The system matches transactions between bank statements and ledger entries, flagging discrepancies instantly.

-

Collaborative Workflow: Accountants, controllers, and auditors access the same platform, add comments, and resolve issues in real-time.

-

Approval Automation: Managers receive notifications to approve adjustments and journal entries electronically.

-

Instant Reporting: Once reconciliations and approvals are complete, financial statements are generated automatically with pre-set templates.

Outcome:

- Month-end close time reduced from 10 days to 4 days.

- Errors reduced by 30% due to automated checks.

- Improved transparency and audit readiness.

Additional Example: Cloud-Based Close Checklist

| Task | Traditional Approach | Cloud-Based Approach | Benefit |

|---|---|---|---|

| Data Collection | Manual downloads and uploads | Automated data feeds | Saves time, reduces errors |

| Reconciliation | Manual matching in spreadsheets | Auto-reconciliation with exception flag | Faster issue identification |

| Journal Entry Approvals | Paper/email approvals | Digital workflows with notifications | Speeds up approvals |

| Report Generation | Manual compilation | One-click report generation | Consistency and speed |

| Audit Trail Maintenance | Manual record keeping | Automatic logging and version control | Enhanced compliance |

Tips for Maximizing Cloud Tool Benefits

- Choose platforms with strong ERP integration capabilities.

- Train staff on collaborative features to encourage adoption.

- Customize workflows to reflect your organization’s approval hierarchy.

- Regularly review analytics to identify bottlenecks in the close process.

By embracing cloud-based tools, financial controllers and accountants can transform the month-end close from a stressful bottleneck into a streamlined, transparent, and efficient process, enabling faster and more reliable financial reporting.

4.4 Integrating ERP Systems for Real-Time Financial Insights

Enterprise Resource Planning (ERP) systems have revolutionized how organizations manage their financial data by centralizing processes and enabling real-time insights. For accountants and financial controllers, integrating ERP systems is a critical best practice to enhance accuracy, speed, and decision-making capabilities.

What is ERP Integration?

ERP integration involves connecting various financial modules—such as general ledger, accounts payable, accounts receivable, and budgeting—within a single platform. This integration ensures seamless data flow, reduces manual entry errors, and provides a unified view of financial health.

Benefits of ERP Integration for Real-Time Financial Insights

- Centralized Data Access: All financial data is stored in one system, eliminating silos.

- Improved Accuracy: Automated data synchronization reduces errors.

- Faster Reporting: Real-time data availability accelerates report generation.

- Enhanced Decision-Making: Up-to-date insights enable proactive financial management.

- Compliance and Audit Readiness: Integrated audit trails simplify compliance.

Mind Map: Key Components of ERP Integration for Financial Reporting

How ERP Integration Works: Step-by-Step Example

Scenario: A multinational corporation wants to integrate its procurement, sales, and finance modules to get real-time visibility into cash flow and expenses.

- Data Mapping: Define how procurement invoices, sales orders, and payments map to financial accounts.

- System Configuration: Set up the ERP modules to communicate and share data automatically.

- Automation Rules: Establish triggers for automatic journal entries when invoices are approved or payments received.

- Dashboard Setup: Create real-time dashboards displaying cash flow, outstanding payables, and receivables.

- User Training: Train finance teams on accessing and interpreting real-time reports.

Outcome: The finance team can instantly see the impact of procurement and sales activities on cash flow, enabling quicker decisions on budgeting and investment.

Mind Map: Example Workflow of ERP Integration for Real-Time Financial Insights

Practical Example: Using SAP ERP for Real-Time Financial Reporting

Context: A financial controller uses SAP ERP to integrate multiple departments.

- Integration: Procurement, sales, and finance modules are linked.

- Real-Time Reporting: The controller accesses a live dashboard showing:

- Current cash position

- Outstanding invoices

- Budget variances

- Benefit: Immediate identification of cash shortages allows the company to adjust payment schedules proactively.

Tips for Successful ERP Integration

- Define Clear Objectives: Understand what real-time insights are most valuable.

- Ensure Data Quality: Clean and standardize data before integration.

- Involve Stakeholders: Collaborate across departments for smooth implementation.

- Test Thoroughly: Validate data flows and report accuracy before going live.

- Provide Training: Equip users to leverage real-time insights effectively.

Summary

Integrating ERP systems for real-time financial insights empowers accountants and financial controllers to move beyond static, historical reporting. By automating data flows and providing instant access to financial metrics, ERP integration supports agile decision-making, enhances accuracy, and drives organizational performance.

4.5 Case Study: Improving Accuracy and Speed with Automation

Introduction

In today’s fast-paced corporate environment, financial controllers and accountants face increasing pressure to deliver accurate financial reports quickly. Automation has emerged as a powerful solution to streamline financial reporting processes, reduce human error, and accelerate report generation. This case study explores how a mid-sized manufacturing company leveraged automation tools to improve both the accuracy and speed of their financial reporting.

Company Background

- Industry: Manufacturing

- Size: 500 employees

- Finance Team: 8 members

- Previous Reporting Process: Manual data entry, Excel-based reconciliations, and report compilation taking up to 10 days monthly

Challenges Before Automation

- Time-consuming manual data consolidation from multiple systems

- High risk of errors due to manual entry and formula mistakes

- Delays in month-end close affecting management decision-making

- Difficulty in maintaining audit trails and compliance documentation

Automation Strategy Implemented

The company adopted a cloud-based financial reporting software integrated with their ERP and banking systems. Key features included:

- Automated Data Extraction: Direct data feeds from ERP and bank accounts

- Pre-built Reconciliation Templates: Automated matching of transactions

- Workflow Automation: Task assignments and approval routing

- Real-time Dashboards: Instant visibility into financial metrics

Mind Map: Automation Implementation Process

Examples of Automation Impact

-

Data Accuracy Improvement:

- Before: Manual entry errors averaged 5% per report

- After: Errors reduced to less than 0.5% due to automated data feeds and validation

-

Speed of Reporting:

- Before: Month-end close took 10 days

- After: Reduced to 4 days, enabling faster management review

-

Audit Readiness:

- Automated audit trails and version control simplified external audits, reducing audit time by 30%

-

Employee Productivity:

- Finance team could focus on analysis and strategic tasks rather than data compilation

Mind Map: Benefits of Automation in Financial Reporting

Lessons Learned

- Change Management is Crucial: Early involvement of finance staff ensured smoother adoption.

- Integration Complexity: Proper planning needed to connect disparate systems.

- Continuous Training: Ongoing support helped maintain high usage and proficiency.

Conclusion

Automation transformed the company’s financial reporting by significantly improving accuracy and reducing the time required to close the books. This enabled more timely and reliable financial insights, empowering leadership to make informed decisions faster. For accountants and financial controllers, embracing automation tools is a best practice that can deliver measurable benefits in both efficiency and quality.

Final Thought

As automation technology continues to evolve, companies that proactively integrate these solutions into their financial reporting processes will maintain a competitive advantage and meet the growing demands of stakeholders with confidence.

5. Compliance and Ethical Considerations

5.1 Understanding Regulatory Compliance Requirements

Financial reporting is governed by a complex web of regulatory requirements designed to ensure transparency, accuracy, and fairness in the presentation of financial information. For accountants and financial controllers, understanding these compliance requirements is critical to avoid legal penalties, maintain stakeholder trust, and uphold the integrity of financial statements.

Key Regulatory Frameworks

- IFRS (International Financial Reporting Standards): Globally accepted standards that provide guidelines on how financial statements should be prepared and presented.

- GAAP (Generally Accepted Accounting Principles): Primarily used in the United States, GAAP outlines accounting standards and principles.

- SOX (Sarbanes-Oxley Act): U.S. legislation that mandates strict reforms to improve financial disclosures and prevent accounting fraud.

- SEC Regulations: Rules imposed by the Securities and Exchange Commission for publicly traded companies.

- Local Regulatory Bodies: Each country may have its own additional requirements, such as HMRC in the UK or ASIC in Australia.

Mind Map: Regulatory Compliance Landscape

Core Compliance Areas

- Accurate Financial Statement Preparation: Ensuring all financial data is recorded and reported according to the relevant standards.

- Timely Filing: Meeting deadlines for submission of reports to regulatory bodies.

- Disclosure Requirements: Providing all necessary notes, risk factors, and explanations.

- Internal Controls and Audit Trails: Maintaining systems to prevent fraud and errors.

- Ethical Reporting: Avoiding manipulation or misrepresentation of financial data.

Example: Compliance in Action

Scenario: A publicly traded company preparing its annual report must comply with SEC regulations and IFRS standards.

- The finance team ensures revenue recognition aligns with IFRS 15.

- All material related party transactions are disclosed in the notes.

- The report is reviewed by internal auditors to verify compliance with SOX internal control requirements.

- The filing is submitted electronically to the SEC before the deadline.

This process helps avoid penalties and maintains investor confidence.

Mind Map: Compliance Process Workflow

Practical Tips for Ensuring Compliance

- Stay Updated: Regularly monitor changes in accounting standards and regulations.

- Training: Provide ongoing education for finance teams on compliance requirements.

- Documentation: Maintain detailed records of accounting policies and decisions.

- Use Technology: Leverage compliance software to automate checks and reporting.

Example: Impact of Non-Compliance

A mid-sized company failed to disclose contingent liabilities in their financial statements as required by IFRS. Upon audit, regulators imposed fines and mandated restatement of financials, which led to a loss of investor trust and a drop in share price. This underscores the importance of thorough understanding and adherence to compliance requirements.

In summary, mastering regulatory compliance is foundational for effective financial reporting. By understanding the frameworks, following structured processes, and learning from real-world examples, financial controllers and accountants can ensure their reports meet all legal and ethical standards.

5.2 Ethical Reporting: Avoiding Manipulation and Misrepresentation

Ethical financial reporting is foundational to maintaining trust and integrity within the corporate finance environment. For accountants and financial controllers, adhering to ethical standards means presenting financial information truthfully, without distortion, manipulation, or omission that could mislead stakeholders.

Why Ethical Reporting Matters

- Builds credibility with investors, regulators, and the public.

- Ensures compliance with legal and regulatory frameworks.

- Prevents legal penalties and reputational damage.

- Supports sound decision-making based on accurate data.

Common Forms of Manipulation and Misrepresentation

Best Practices to Avoid Manipulation and Misrepresentation

-

Adhere to Accounting Standards and Policies

- Follow IFRS, GAAP, or applicable frameworks strictly.

- Use consistent accounting policies year over year.

-

Maintain Transparency in Disclosures

- Fully disclose assumptions, estimates, and judgments.

- Highlight uncertainties and risks clearly.

-

Implement Strong Internal Controls

- Segregate duties to reduce fraud risk.

- Regularly review and reconcile accounts.

-

Encourage Ethical Culture and Training

- Provide ethics training to finance teams.

- Promote whistleblower policies and anonymous reporting.

-

Engage Independent Auditors

- Use external audits to validate financial statements.

- Address auditor recommendations promptly.

Example 1: Avoiding Revenue Inflation

Scenario: A company is under pressure to meet quarterly targets and considers recognizing revenue prematurely.

Ethical Approach:

- Recognize revenue only when earned and realizable according to standards.

- Document sales contracts and delivery confirmations.

- Example: A software firm waits until the software is delivered and accepted by the client before recognizing revenue, rather than booking sales at contract signing.

Example 2: Proper Disclosure of Contingent Liabilities

Scenario: A pending lawsuit could result in a significant financial loss.

Ethical Approach:

- Disclose the nature of the lawsuit and potential financial impact in the notes.

- Avoid hiding or minimizing the risk.

- Example: A manufacturing company includes detailed notes on a product liability case, explaining the possible outcomes and estimated financial exposure.

Mind Map: Ethical Reporting Workflow

Summary

Ethical financial reporting is not just about compliance but about fostering trust and accountability. By avoiding manipulation and misrepresentation, financial controllers and accountants uphold the integrity of their organizations and contribute to a healthy financial ecosystem.

For further reading, consider exploring the IFAC Code of Ethics for Professional Accountants which provides comprehensive guidance on ethical responsibilities.

5.3 Example: Identifying and Reporting Conflicts of Interest

Conflicts of interest (COI) in financial reporting can undermine the integrity and credibility of financial statements. It is crucial for accountants and financial controllers to identify, disclose, and manage these conflicts to maintain transparency and uphold ethical standards.

What is a Conflict of Interest?

A conflict of interest occurs when an individual’s personal interests, relationships, or activities interfere with their professional duties and responsibilities, potentially influencing their judgment or actions.

Mind Map: Identifying Conflicts of Interest

Practical Example 1: Ownership in a Vendor Company

Scenario: A financial controller, Sarah, is responsible for approving payments to suppliers. She owns shares in one of the vendor companies supplying office equipment.

Identification: Sarah’s ownership interest could bias her decisions, favoring that vendor over others.

Reporting: Sarah discloses her ownership to the compliance officer and recuses herself from approving payments related to that vendor.

Outcome: The company assigns another team member to handle those transactions, ensuring impartiality.

Practical Example 2: Family Relationship Impacting Procurement

Scenario: John, an accountant, is involved in selecting a new IT service provider. His brother owns a company bidding for the contract.

Identification: John’s family relationship creates a potential COI.

Reporting: John formally declares the relationship to management and abstains from the selection process.

Outcome: The procurement team evaluates bids independently, maintaining fairness.

Mind Map: Reporting Conflicts of Interest

Best Practices for Reporting COI

- Timeliness: Report conflicts as soon as they are identified.

- Transparency: Provide full details about the nature and extent of the conflict.

- Documentation: Maintain records of disclosures and actions taken.

- Policy Adherence: Follow company policies and regulatory requirements strictly.

- Ongoing Monitoring: Regularly review potential conflicts as roles and circumstances change.

Example: Conflict of Interest Disclosure Form (Excerpt)

| Section | Details to Provide |

|---|---|

| Employee Information | Name, Position |

| Nature of Conflict | Description of personal interest or relationship |

| Impacted Activities | Specific decisions or processes affected |

| Actions Taken | Disclosure date, recusal, delegation details |

| Supervisor Acknowledgment | Signature and date |

Summary

Identifying and reporting conflicts of interest is a critical component of ethical financial reporting. By recognizing potential conflicts early and managing them through transparent disclosure and appropriate actions, accountants and financial controllers safeguard the integrity of financial information and maintain stakeholder trust.

5.4 Internal Controls to Prevent Fraud and Errors

Effective internal controls are essential to safeguard an organization’s financial integrity by preventing fraud and minimizing errors. These controls create a system of checks and balances that ensure accuracy, reliability, and compliance in financial reporting.

Key Components of Internal Controls

- Segregation of Duties (SoD): Dividing responsibilities among different employees to reduce risk of error or inappropriate actions.

- Authorization and Approval: Ensuring transactions are reviewed and approved by designated personnel.

- Reconciliation: Regularly comparing different sets of data to identify discrepancies.

- Access Controls: Restricting access to financial systems and sensitive information.

- Audit Trails: Maintaining detailed records of transactions and changes.

- Physical Controls: Safeguarding assets through locks, safes, and inventory counts.

Mind Map: Core Internal Controls to Prevent Fraud and Errors

Example 1: Segregation of Duties in Accounts Payable

In a mid-sized company, the accounts payable process is divided among three employees:

- Employee A creates purchase orders and receives goods.

- Employee B approves invoices and processes payments.

- Employee C reconciles monthly supplier statements with payments made.