Financial Planning for Retirement

1. Introduction to Retirement Financial Planning

1.1 Understanding the Importance of Early Retirement Planning

Retirement planning is a critical financial process that ensures individuals can maintain their desired lifestyle once they stop working. Starting early offers numerous advantages, including the power of compounding, greater flexibility, and reduced stress. This section explores why early retirement planning is essential and provides practical examples and mind maps to illustrate key concepts.

Why Start Early?

- Compounding Growth: The earlier you start saving and investing, the more time your money has to grow exponentially.

- Flexibility: Early planning allows for adjustments over time, accommodating life changes or unexpected events.

- Lower Monthly Savings: Starting early means you can save smaller amounts regularly rather than large sums later.

- Risk Management: Longer timelines allow for more aggressive investment strategies initially, gradually shifting to conservative ones.

- Peace of Mind: Early planning reduces anxiety about financial security in retirement.

Mind Map: Benefits of Early Retirement Planning

Example 1: The Power of Compounding

Consider two individuals, Alice and Bob:

- Alice starts saving $300/month at age 25.

- Bob starts saving $300/month at age 35.

Assuming an average annual return of 7%, by age 65:

- Alice’s savings: Approximately $700,000

- Bob’s savings: Approximately $350,000

Despite both saving the same monthly amount, Alice ends up with double the retirement savings due to starting 10 years earlier.

Mind Map: Comparing Early vs. Late Starters

Example 2: Flexibility in Retirement Planning

Jane began saving for retirement at 28 but faced a job loss at 40, reducing her savings temporarily. Because she started early, she was able to pause contributions for a few years and then increase them later without jeopardizing her retirement goals.

In contrast, Mark started saving at 40 and faced the same job loss at 50. With less time to recover, Mark had to significantly increase his savings rate and delay retirement.

Mind Map: Impact of Life Events on Retirement Planning

Summary

Starting retirement planning early is not just about saving money; it’s about creating a sustainable, flexible, and stress-reduced path to financial independence. The examples and mind maps above illustrate how time, consistency, and adaptability are your greatest allies in building a secure retirement.

Actionable Tip

If you haven’t started retirement planning yet, begin today—even small contributions can grow significantly over time. Use budgeting tools to allocate a portion of your income towards retirement savings and review your plan annually to stay on track.

1.2 Key Retirement Goals and Objectives

Retirement planning begins with clearly defining your goals and objectives. These goals serve as the foundation for all financial decisions and strategies you will implement. Understanding what you want to achieve in retirement helps you tailor your savings, investments, and risk management accordingly.

Why Define Retirement Goals?

- Provides direction and motivation for saving and investing.

- Helps estimate the amount of money needed to sustain your desired lifestyle.

- Enables prioritization of financial decisions and trade-offs.

Common Retirement Goals

- Maintain a Comfortable Lifestyle

- Cover daily living expenses without financial stress.

- Continue hobbies, travel, and leisure activities.

- Ensure Healthcare and Long-Term Care Coverage

- Plan for medical expenses and potential long-term care needs.

- Leave a Legacy

- Provide for heirs or charitable causes.

- Debt Freedom

- Enter retirement with minimal or no debt obligations.

- Tax Efficiency

- Minimize taxes on retirement income and withdrawals.

Mind Map: Key Retirement Goals

Setting SMART Goals

To make your retirement goals actionable, apply the SMART criteria:

- Specific: Clearly define what you want.

- Measurable: Quantify your goals.

- Achievable: Ensure they are realistic.

- Relevant: Align with your values and priorities.

- Time-bound: Set a timeline.

Example: Instead of “I want to travel in retirement,” say “I want to allocate $5,000 annually for travel starting at age 65.”

Example: Defining Retirement Objectives for Sarah, a Financial Planner

Sarah, age 45, wants to retire at 65. Her key objectives:

- Maintain her current lifestyle, estimated at $60,000/year in today’s dollars.

- Allocate $7,000/year for travel and hobbies.

- Ensure healthcare costs are covered, budgeting $8,000/year.

- Pay off her mortgage before retirement.

- Leave $100,000 to her children as inheritance.

By defining these objectives, Sarah can calculate the total retirement corpus needed and design her savings and investment plan accordingly.

Mind Map: Sarah’s Retirement Objectives

Aligning Goals with Financial Planning

Each goal translates into financial targets:

- Lifestyle & Travel: Determine annual withdrawal amounts.

- Healthcare: Include insurance premiums and out-of-pocket expenses.

- Debt Freedom: Plan accelerated payments.

- Legacy: Incorporate estate planning strategies.

Example: Impact of Goal Setting on Savings Rate

If Sarah needs $75,000/year in retirement (lifestyle + travel + healthcare) and expects 25 years in retirement, she can estimate her required retirement fund. Assuming a 4% safe withdrawal rate:

Required Fund = $75,000 / 0.04 = $1,875,000

Knowing this, she can calculate how much to save monthly considering her current savings and expected investment returns.

Summary

Defining clear, realistic retirement goals and objectives is the cornerstone of successful retirement planning. Using mind maps helps visualize and organize these goals, while examples like Sarah’s illustrate how to translate ambitions into actionable financial plans.

1.3 Common Retirement Planning Challenges and How to Overcome Them

Retirement planning is a complex process that often presents several challenges. Understanding these common obstacles and learning how to effectively address them can significantly improve the likelihood of a comfortable and secure retirement.

Common Challenges in Retirement Planning

Procrastination and Lack of Early Planning

Challenge: Many individuals delay retirement planning due to competing priorities or a false sense of having plenty of time.

How to Overcome:

- Start with small, manageable steps such as setting up automatic contributions to retirement accounts.

- Use simple tools to visualize the impact of early savings.

Example: Sarah, age 30, starts saving $200 monthly in a retirement account with an average 7% return. By age 65, she accumulates approximately $380,000. If she delays saving until age 40, even increasing contributions to $400 monthly, she ends up with about $230,000. Early action clearly benefits her retirement corpus.

Underestimating Retirement Expenses and Inflation

Challenge: Many retirees underestimate how much income they will need, especially considering inflation and healthcare costs.

How to Overcome:

- Use inflation-adjusted calculators to estimate future expenses.

- Include healthcare and long-term care costs in budgeting.

Example: John plans for $40,000 annual expenses today. Assuming 3% inflation, in 20 years, his expenses could rise to nearly $72,000 annually. Without adjusting his plan, John risks a significant shortfall.

Managing Investment Risks and Market Volatility

Challenge: Market downturns can erode retirement savings, especially if withdrawals begin during a bear market.

How to Overcome:

- Diversify investments across asset classes.

- Gradually shift to more conservative allocations as retirement nears.

- Maintain an emergency fund to avoid forced withdrawals during downturns.

Example: Emma, 5 years from retirement, adjusts her portfolio from 80% stocks to 50% stocks and 50% bonds. During a market correction, her portfolio declines less than a fully equity portfolio, preserving capital.

Unexpected Healthcare and Long-Term Care Costs

Challenge: Healthcare expenses often rise with age and can be unpredictable.

How to Overcome:

- Plan for Medicare premiums, supplemental insurance, and out-of-pocket costs.

- Consider long-term care insurance or alternative funding strategies.

- Use Health Savings Accounts (HSAs) if eligible.

Example: Mark underestimated his healthcare costs and faced a $50,000 long-term care expense. By purchasing a long-term care insurance policy earlier, he could have mitigated this financial burden.

Behavioral Biases Impacting Decision-Making

Challenge: Emotional reactions, such as panic selling or overconfidence, can derail retirement plans.

How to Overcome:

- Establish a clear, written retirement plan.

- Work with financial advisors to maintain discipline.

- Use systematic withdrawal plans to reduce emotional decision-making.

Example: During a market dip, Lisa panicked and sold her investments at a loss. Later, she missed the market rebound. With a disciplined plan, she could have avoided this costly mistake.

Carrying Debt into Retirement

Challenge: High debt levels reduce cash flow and increase financial stress.

How to Overcome:

- Prioritize paying down high-interest debt before retirement.

- Avoid accumulating new debt as retirement approaches.

Example: Tom enters retirement with a mortgage and credit card debt, limiting his monthly disposable income. By aggressively paying off his credit card debt 5 years prior, he improved his retirement cash flow.

Complex Tax Planning and Withdrawal Strategies

Challenge: Improper tax planning can lead to higher taxes and reduced retirement income.

How to Overcome:

- Understand tax implications of different account types (Traditional IRA, Roth IRA, 401(k)).

- Plan withdrawals to minimize tax brackets and Required Minimum Distributions (RMDs).

Example: Anna strategically converts portions of her Traditional IRA to a Roth IRA during low-income years, reducing future RMDs and tax liabilities.

Summary Mind Map of Solutions

By proactively addressing these challenges with clear strategies and practical examples, accountants and financial planners can guide clients toward a more secure and confident retirement.

1.4 Example: Comparing Retirement Outcomes with Early vs. Late Planning

Planning for retirement early versus starting late can dramatically affect the financial security and lifestyle you enjoy in your golden years. This section explores these differences through clear examples and mind maps to illustrate the impact of timing on retirement outcomes.

Mind Map: Early vs. Late Retirement Planning

Example Scenario:

Profile:

- Age at start of planning: Early Planner (25 years old), Late Planner (45 years old)

- Retirement age: 65

- Annual contribution: Early Planner saves $5,000/year, Late Planner saves $12,000/year

- Expected annual return: 7%

Calculations:

| Planner | Years Contributing | Annual Contribution | Total Contributions | Estimated Retirement Savings |

|---|---|---|---|---|

| Early Planner | 40 | $5,000 | $200,000 | ~$1,073,000 |

| Late Planner | 20 | $12,000 | $240,000 | ~$524,000 |

Note: Calculations assume contributions made at year-end and a consistent 7% return.

Interpretation:

- The Early Planner, despite contributing less annually and a smaller total amount, accumulates more than double the retirement savings of the Late Planner due to the power of compounding over a longer period.

- The Late Planner must save more than twice as much annually to approach the Early Planner’s retirement fund but still ends up with less due to fewer compounding years.

Mind Map: Impact of Compound Interest Over Time

Additional Example: Monthly Savings Needed to Reach $1,000,000 by Age 65

| Starting Age | Monthly Savings Needed (7% Return) |

|---|---|

| 25 | ~$330 |

| 35 | ~$620 |

| 45 | ~$1,350 |

This table highlights how delaying retirement savings significantly increases the amount needed to save monthly.

Summary:

- Start Early: Even modest savings grow substantially over time.

- Start Late: Requires much higher savings and carries more risk.

- Best Practice: Encourage clients to begin retirement planning as early as possible to maximize benefits.

Practical Tip for Financial Planners:

Use this example to motivate clients who may procrastinate on retirement savings. Visual aids like mind maps and concrete numbers help illustrate the tangible benefits of early planning.

This example underscores the critical importance of timing in retirement financial planning, providing a compelling case for early and consistent savings.

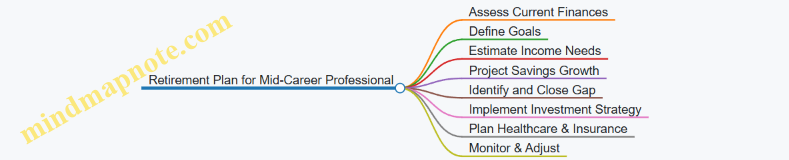

2. Assessing Your Current Financial Situation

2.1 Creating a Comprehensive Financial Inventory

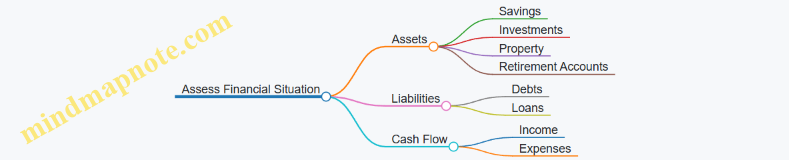

Creating a comprehensive financial inventory is a foundational step in effective retirement planning. It involves gathering and organizing all your financial information to get a clear picture of your current financial standing. This inventory helps identify your assets, liabilities, income sources, and expenses, enabling you to make informed decisions about your retirement goals.

What is a Financial Inventory?

A financial inventory is a detailed list of all your financial accounts, assets, debts, income streams, and recurring expenses. It acts like a financial snapshot, allowing you to understand where you stand today and what resources you have to support your retirement.

Why is it Important?

- Clarity: Knowing exactly what you own and owe helps you plan realistically.

- Goal Setting: Helps define achievable retirement goals based on your net worth.

- Risk Management: Identifies gaps or risks in your financial picture.

- Efficiency: Streamlines decision-making and tax planning.

Components of a Comprehensive Financial Inventory

Below is a mind map illustrating the key components:

Step-by-Step Process to Create Your Financial Inventory

-

Gather Financial Statements: Collect recent statements for bank accounts, investment accounts, retirement plans, insurance policies, and debts.

-

List All Assets: Document the current value of each asset. For investments, use the latest market value; for real estate, use appraised or estimated market value.

-

List All Liabilities: Include outstanding balances on mortgages, loans, credit cards, and other debts.

-

Identify Income Sources: Note all current sources of income, including salary, rental income, dividends, and any other cash inflows.

-

Track Expenses: Review bank statements and bills to categorize and estimate monthly expenses.

-

Compile Insurance and Estate Documents: List all relevant policies and legal documents.

-

Calculate Net Worth: Subtract total liabilities from total assets.

Example: Building a Simple Financial Inventory

Meet Sarah, a 45-year-old financial planner preparing for retirement.

-

Assets:

- Checking Account: $5,000

- Savings Account: $20,000

- 401(k) Balance: $150,000

- Roth IRA: $50,000

- Primary Residence: $350,000

- Car: $15,000

-

Liabilities:

- Mortgage Balance: $200,000

- Credit Card Debt: $3,000

-

Income Sources:

- Salary: $85,000/year

- Rental Income: $12,000/year

-

Expenses:

- Mortgage Payment: $1,500/month

- Utilities: $300/month

- Food & Transportation: $800/month

- Entertainment & Travel: $400/month

-

Insurance:

- Health Insurance Premiums: $400/month

- Life Insurance Cash Value: $10,000

-

Net Worth Calculation:

- Total Assets = $5,000 + $20,000 + $150,000 + $50,000 + $350,000 + $15,000 = $590,000

- Total Liabilities = $200,000 + $3,000 = $203,000

- Net Worth = $590,000 - $203,000 = $387,000

Sarah now has a clear financial inventory that she can use to project her retirement savings needs and plan accordingly.

Tips for Maintaining Your Financial Inventory

- Update your inventory at least annually or after major financial events.

- Use financial software or spreadsheets to organize and track your data.

- Keep digital and physical copies of important documents secure but accessible.

- Review your inventory with a financial planner to identify opportunities and risks.

By systematically creating and maintaining a comprehensive financial inventory, accountants and financial planners can guide their clients toward more accurate and personalized retirement plans, ensuring a smoother transition into retirement years.

2.2 Calculating Net Worth and Its Role in Retirement Planning

What is Net Worth?

Net worth is the difference between your total assets and total liabilities. It represents your overall financial health and is a critical starting point for retirement planning.

Why is Net Worth Important in Retirement Planning?

- Baseline Measurement: Helps you understand where you currently stand financially.

- Goal Setting: Allows you to set realistic retirement savings goals.

- Progress Tracking: Enables you to monitor growth over time.

- Debt Management: Highlights liabilities that need to be addressed before retirement.

How to Calculate Net Worth

Formula:

Net Worth = Total Assets - Total Liabilities

Step 1: List Your Assets

Assets include anything you own that has value. Examples:

- Cash and cash equivalents (checking/savings accounts)

- Investments (stocks, bonds, mutual funds, retirement accounts)

- Real estate (primary residence, rental properties)

- Personal property (vehicles, jewelry, collectibles)

- Business ownership interest

Step 2: List Your Liabilities

Liabilities are debts or financial obligations. Examples:

- Mortgage balances

- Credit card debt

- Student loans

- Auto loans

- Personal loans

Step 3: Calculate Net Worth

Subtract total liabilities from total assets.

Mind Map: Components of Net Worth Calculation

Example 1: Simple Net Worth Calculation

| Category | Amount (USD) |

|---|---|

| Checking Account | 10,000 |

| Savings Account | 15,000 |

| 401(k) Retirement Plan | 120,000 |

| Primary Residence | 300,000 |

| Car | 20,000 |

| Mortgage Balance | (200,000) |

| Credit Card Debt | (5,000) |

| Auto Loan | (10,000) |

Calculation:

Total Assets = 10,000 + 15,000 + 120,000 + 300,000 + 20,000 = 465,000

Total Liabilities = 200,000 + 5,000 + 10,000 = 215,000

Net Worth = 465,000 - 215,000 = 250,000

Role of Net Worth in Retirement Planning

-

Determining Retirement Readiness:

- Compare your net worth to your target retirement savings.

- Helps identify if you need to increase savings or adjust retirement age.

-

Asset Allocation Decisions:

- Understanding the composition of assets helps in planning investment strategies.

-

Debt Reduction Priorities:

- High liabilities can erode retirement security; planning to reduce debt is essential.

-

Cash Flow Planning:

- Knowing liquid assets available for emergencies or unexpected expenses.

Mind Map: Net Worth in Retirement Planning

Example 2: Using Net Worth to Adjust Retirement Goals

Scenario: Jane is 45 years old with a net worth of $300,000. She wants to retire at 65 with $1,000,000 saved.

- Current savings rate: $10,000/year

- Estimated annual return: 6%

Analysis:

- Using a future value calculator, Jane’s current net worth and savings will grow to approximately $600,000 in 20 years.

- There is a $400,000 shortfall.

Action:

- Increase annual savings to $16,000 to meet the $1,000,000 goal.

- Alternatively, delay retirement by 3-4 years.

Tips for Accountants and Financial Planners

- Encourage clients to update their net worth statements annually.

- Use net worth as a communication tool to illustrate progress.

- Integrate net worth analysis with cash flow and investment reviews.

- Highlight the impact of liabilities on retirement security.

Summary

Calculating net worth is a foundational step in retirement planning. It provides a clear snapshot of financial health, informs goal setting, and guides strategic decisions around saving, investing, and debt management. Regularly revisiting net worth helps ensure clients stay on track toward a secure retirement.

2.3 Understanding Cash Flow and Expense Tracking

Effective retirement planning hinges on a clear understanding of your cash flow — the money coming in versus the money going out — and diligent expense tracking. This section breaks down these concepts with practical examples and visual mind maps to help you grasp how to manage your finances for a secure retirement.

What is Cash Flow?

Cash flow is the net amount of cash being transferred into and out of your financial accounts over a specific period, typically monthly. Positive cash flow means you have surplus funds after expenses, which can be saved or invested for retirement. Negative cash flow indicates you are spending more than you earn, which can jeopardize your retirement goals.

Why is Cash Flow Important for Retirement Planning?

- Determines how much you can save toward retirement.

- Helps identify unnecessary expenses to cut back.

- Ensures you maintain liquidity for emergencies.

- Assists in forecasting retirement income needs.

Mind Map: Components of Cash Flow

Expense Tracking: The Foundation of Cash Flow Management

Expense tracking is the process of recording all your expenditures to understand where your money goes. This is crucial for retirement planning because it:

- Reveals spending patterns.

- Highlights areas to reduce expenses.

- Helps set realistic retirement budgets.

Methods for Expense Tracking

- Manual Tracking: Using spreadsheets or notebooks.

- Mobile Apps: Tools like Mint, YNAB (You Need A Budget), or Personal Capital.

- Bank Statements: Reviewing monthly statements to categorize expenses.

Example: Monthly Cash Flow Tracking

| Category | Amount ($) |

|---|---|

| Income | |

| Salary | 5,000 |

| Investment Income | 200 |

| Rental Income | 800 |

| Total Income | 6,000 |

| Expenses | |

| Mortgage | 1,200 |

| Utilities | 300 |

| Groceries | 600 |

| Transportation | 400 |

| Entertainment | 250 |

| Insurance | 350 |

| Miscellaneous | 200 |

| Total Expenses | 3,300 |

| Net Cash Flow | 2,700 |

In this example, the individual has a positive net cash flow of $2,700, which can be allocated toward retirement savings or investments.

Mind Map: Expense Tracking Process

Best Practices for Cash Flow and Expense Tracking

- Be Consistent: Track expenses daily or weekly to avoid missing data.

- Categorize Accurately: Use meaningful categories to identify spending habits.

- Review Regularly: Monthly reviews help adjust budgets and savings goals.

- Use Technology: Leverage apps for automation and reminders.

Example: Using Expense Tracking to Increase Retirement Savings

Consider Jane, who tracked her expenses for three months and discovered she was spending $300 monthly on dining out. By reducing this to $150, she freed up $150 per month. Over 20 years, investing this amount at a 6% annual return could grow to approximately $66,000, significantly boosting her retirement nest egg.

Mind Map: Impact of Expense Reduction on Retirement Savings

Summary

Understanding cash flow and tracking expenses are foundational steps in retirement financial planning. They provide clarity on your financial health, empower you to make informed decisions, and ultimately help you build a sustainable retirement plan.

By integrating these practices into your routine, you can confidently manage your finances and work toward a comfortable retirement.

2.4 Example: Building a Personal Financial Dashboard for Retirement Readiness

Creating a personal financial dashboard is an effective way to visualize and track your financial health as you prepare for retirement. This dashboard consolidates key financial metrics, helping you make informed decisions and adjust your plan as needed.

What is a Financial Dashboard?

A financial dashboard is a centralized tool that displays your financial data in an organized, easy-to-understand format. It typically includes your assets, liabilities, income, expenses, savings progress, and investment performance.

Key Components of a Retirement Financial Dashboard

- Net Worth Overview

- Income vs. Expenses

- Retirement Savings Progress

- Investment Allocation

- Debt Status

- Projected Retirement Income

Mind Map: Components of a Personal Financial Dashboard

Step-by-Step Example: Building Your Dashboard

Step 1: Gather Financial Data

Collect all relevant financial information including bank statements, investment accounts, loan balances, monthly income, and expenses.

Step 2: Calculate Net Worth

List all assets and liabilities. Subtract total liabilities from total assets to get your net worth.

Example:

- Assets:

- Savings: $50,000

- Investments: $150,000

- Home Equity: $200,000

- Liabilities:

- Mortgage: $120,000

- Credit Card Debt: $5,000

Net Worth = ($50,000 + $150,000 + $200,000) - ($120,000 + $5,000) = $275,000

Step 3: Track Income and Expenses

Create a monthly summary of all income sources and categorize expenses as fixed (e.g., mortgage, utilities) and variable (e.g., dining out, entertainment).

Example:

- Monthly Income: $6,000

- Fixed Expenses: $3,000

- Variable Expenses: $1,000

- Savings Rate: $2,000 (Income - Expenses)

Step 4: Monitor Retirement Savings Progress

Track balances in retirement accounts and calculate the percentage of your retirement goal achieved.

Example:

- Retirement Goal: $1,000,000

- Current Savings: $200,000

- Progress: 20%

Step 5: Visualize Investment Allocation

Use pie charts or bar graphs to display how your investments are distributed across asset classes.

Example:

- Stocks: 60%

- Bonds: 30%

- Cash: 10%

Step 6: Assess Debt Status

List outstanding debts with balances and monthly payments to understand their impact on your cash flow.

Step 7: Project Retirement Income

Estimate monthly income from Social Security, pensions, annuities, and planned withdrawals.

Example:

- Social Security: $1,500/month

- Pension: $1,000/month

- Investment Withdrawals: $2,000/month

- Total Projected Income: $4,500/month

Mind Map: Monthly Financial Snapshot

Tools to Build Your Dashboard

- Spreadsheet Software: Excel or Google Sheets with templates for net worth and budgeting.

- Financial Apps: Personal Capital, Mint, or YNAB for automated tracking.

- Custom Dashboards: Use data visualization tools like Tableau or Power BI for advanced users.

Benefits of Using a Financial Dashboard

- Provides a clear snapshot of your financial health.

- Helps identify spending leaks and savings opportunities.

- Enables regular monitoring and adjustments to your retirement plan.

- Facilitates communication with financial advisors.

Final Thought

Building and maintaining a personal financial dashboard empowers you to stay on track for retirement readiness. Regular updates and reviews ensure that you can adapt your plan to changing circumstances and confidently move toward your retirement goals.

3. Setting Realistic Retirement Goals

3.1 Defining Desired Retirement Lifestyle and Expenses

Planning for retirement begins with a clear understanding of the lifestyle you want to lead once you stop working. Defining your desired retirement lifestyle helps you estimate the expenses you will incur and ensures your financial plan aligns with your goals. This section explores how to identify and quantify your retirement lifestyle preferences, supported by mind maps and practical examples.

Understanding Retirement Lifestyle

Your retirement lifestyle encompasses how you want to spend your time, where you want to live, and the activities and comforts you want to maintain or acquire. It can vary widely from person to person, depending on interests, health, family situation, and financial resources.

Mind Map: Components of Retirement Lifestyle

Estimating Retirement Expenses

Once you have identified the components of your desired lifestyle, the next step is to estimate the associated expenses. This process involves:

- Listing all categories of expenses you expect to incur.

- Researching typical costs for each category, considering inflation.

- Adjusting for changes such as paid-off mortgages or increased healthcare needs.

Mind Map: Expense Estimation Process

Example 1: Defining Lifestyle and Expenses for a Moderate Retirement

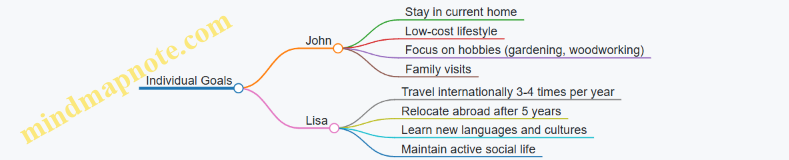

Profile: Jane, 60 years old, plans to retire at 65. She wants to live comfortably in her current home, travel twice a year, and maintain an active social life.

| Expense Category | Estimated Monthly Cost | Notes |

|---|---|---|

| Housing | $1,200 | Mortgage paid off, includes utilities |

| Food & Groceries | $600 | Eating mostly at home |

| Transportation | $300 | Owns a car, occasional rideshare |

| Healthcare | $400 | Insurance premiums + out-of-pocket |

| Leisure & Travel | $500 | Saving monthly for two trips a year |

| Social & Family | $200 | Gifts, dining out |

| Miscellaneous | $150 | Clothing, hobbies |

| Total Monthly | $3,350 |

Jane uses this estimate to calculate her annual expenses ($40,200) and adjusts her retirement savings goal accordingly.

Example 2: Mind Map for Jane’s Retirement Budget

Tips for Accountants and Financial Planners

- Encourage clients to think beyond basic expenses and include discretionary spending that impacts quality of life.

- Use mind maps as visual tools during client meetings to help them organize their thoughts.

- Provide realistic examples tailored to clients’ demographics and preferences.

- Factor in inflation and unexpected costs to avoid underestimating expenses.

Summary

Defining your desired retirement lifestyle is the foundation of effective retirement planning. By breaking down lifestyle components and estimating related expenses, you create a realistic financial target. Utilizing mind maps and concrete examples facilitates clearer communication and better decision-making for both planners and clients.

3.2 Estimating Retirement Income Needs Using Inflation Adjustments

Estimating retirement income needs accurately is a cornerstone of effective financial planning. One of the most critical factors to consider is inflation — the gradual increase in prices over time, which erodes purchasing power. Without accounting for inflation, retirees risk underestimating the amount of income needed to maintain their desired lifestyle.

Understanding Inflation and Its Impact

Inflation refers to the rate at which the general level of prices for goods and services rises, leading to a decrease in the purchasing power of money. For example, if inflation averages 3% per year, something that costs $10,000 today will cost approximately $13,439 in 10 years.

Why is this important?

- Retirement can last 20-30 years or more.

- Fixed income streams lose value over time if not adjusted.

- Healthcare and housing costs often rise faster than average inflation.

Step-by-Step Process to Estimate Retirement Income Needs with Inflation

-

Calculate Current Annual Expenses

- Include housing, food, healthcare, travel, leisure, taxes, insurance, and other personal expenses.

-

Project Future Expenses Adjusted for Inflation

- Use an assumed inflation rate (commonly 2-3%) to estimate expenses at retirement and beyond.

-

Determine Retirement Duration

- Estimate years in retirement (e.g., from age 65 to 90 = 25 years).

-

Adjust Income Needs Year-by-Year

- Increase expenses each year by the inflation rate to maintain purchasing power.

-

Calculate Total Retirement Income Required

- Sum the inflation-adjusted expenses over the retirement period.

Mind Map: Estimating Retirement Income Needs with Inflation

Example 1: Simple Inflation Adjustment Calculation

Scenario:

- Current annual expenses: $50,000

- Expected retirement age: 65

- Current age: 55

- Inflation rate: 3% per year

- Retirement duration: 25 years

Step 1: Calculate expenses at retirement (in 10 years):

\[ Future\ Expense = Current\ Expense \times (1 + Inflation)^{Years} \]

\[ = 50,000 \times (1 + 0.03)^{10} = 50,000 \times 1.3439 = 67,195 \]

Step 2: Calculate inflation-adjusted expenses for each year of retirement (year 1 to 25), increasing by 3% annually.

Step 3: Sum all yearly expenses to find total needed over retirement.

This can be simplified using the formula for the sum of a geometric series:

\[ Total = Future\ Expense \times \frac{(1 - (1 + Inflation)^{Retirement\ Years})}{1 - (1 + Inflation)} \]

Plugging in values:

\[ Total = 67,195 \times \frac{1 - (1.03)^{25}}{1 - 1.03} = 67,195 \times 43.82 = 2,945,000 \]

So, approximately $2.95 million is needed to cover 25 years of inflation-adjusted expenses starting at $67,195 in year one.

Example 2: Using a Spreadsheet or Financial Calculator

A financial planner can build a spreadsheet with columns for each retirement year, calculating the expense for that year by multiplying the previous year’s expense by (1 + inflation rate). This allows for dynamic adjustments and scenario analysis.

| Year | Expense ($) |

|---|---|

| 1 | 67,195 |

| 2 | 69,211 |

| 3 | 71,287 |

| … | … |

| 25 | 139,497 |

Sum all values for total income needed.

Best Practices

- Use conservative inflation estimates: While historical averages are around 2-3%, some costs like healthcare may rise faster.

- Review and update regularly: Inflation rates and expenses can change; revisit your plan annually.

- Consider variable inflation: Some expenses inflate differently; separate categories can improve accuracy.

- Plan for contingencies: Unexpected expenses or higher inflation periods can occur.

Mind Map: Best Practices for Inflation Adjusted Retirement Planning

Summary

Estimating retirement income needs using inflation adjustments ensures that retirees maintain their purchasing power throughout retirement. By systematically projecting expenses, applying realistic inflation rates, and planning for a long retirement horizon, financial planners can help clients build robust and resilient retirement plans.

For accountants and financial planners, incorporating inflation into retirement income projections is essential to provide clients with realistic expectations and actionable strategies.

3.3 Incorporating Healthcare and Long-Term Care Costs

Healthcare and long-term care expenses are among the most significant and often underestimated costs in retirement planning. Properly accounting for these costs ensures retirees maintain their quality of life without financial strain.

Why Healthcare and Long-Term Care Costs Matter

- Healthcare costs tend to rise faster than inflation.

- Unexpected medical events can drastically impact retirement savings.

- Long-term care (LTC) is not typically covered by Medicare.

- Planning ahead reduces the risk of depleting assets prematurely.

Components of Healthcare and Long-Term Care Costs

Estimating Healthcare Costs in Retirement

- According to Fidelity, a 65-year-old couple retiring today may need approximately $300,000 to cover healthcare expenses in retirement.

- Consider inflation: healthcare inflation averages 5-6% annually, higher than general inflation.

Example:

John and Mary, both age 65, estimate their annual healthcare costs as follows:

- Medicare premiums: $4,500

- Out-of-pocket medical expenses: $3,000

- Prescription drugs: $2,000

- Supplemental insurance: $1,500

Total annual healthcare cost estimate: $11,000

Adjusting for 5% annual inflation, after 20 years, their healthcare costs could exceed $29,000 per year.

Planning for Long-Term Care (LTC) Costs

- LTC services include assistance with daily living activities such as bathing, dressing, and eating.

- Average costs vary by care type and location:

- In-home care: $25-$30 per hour

- Assisted living facility: $4,000 per month

- Nursing home care: $7,500 per month

Example:

Susan plans to purchase LTC insurance with a daily benefit of $150 for 3 years. This coverage would help offset potential nursing home costs estimated at $7,500/month.

Strategies to Incorporate Healthcare and LTC Costs into Retirement Planning

Using Health Savings Accounts (HSAs)

- HSAs offer triple tax advantages: contributions are tax-deductible, grow tax-free, and withdrawals for qualified medical expenses are tax-free.

- HSAs can be used to save pre-retirement for healthcare costs in retirement.

Example:

Mark contributes $3,650 annually to his HSA for 10 years, earning an average 6% return. By retirement, he could accumulate over $45,000 tax-free to cover healthcare expenses.

Example Scenario: Incorporating Healthcare and LTC Costs into a Retirement Plan

Client Profile:

- Age: 60

- Retirement Age: 67

- Current Savings: $500,000

- Expected Retirement Duration: 25 years

Healthcare Planning Steps:

- Estimate annual healthcare costs starting at $10,000 with 5% inflation.

- Allocate $50,000 of savings specifically for healthcare and LTC.

- Purchase LTC insurance with a $150 daily benefit.

- Maximize HSA contributions for the next 7 years.

- Include healthcare costs in the overall retirement budget.

Outcome: By proactively incorporating these costs, the client reduces the risk of unexpected healthcare expenses derailing their retirement plan.

Key Takeaways

- Always plan for healthcare and LTC costs as part of retirement.

- Use mind maps to visualize cost components and planning strategies.

- Leverage insurance, HSAs, and budgeting to manage these expenses.

- Regularly update estimates to reflect changes in health and market conditions.

3.4 Example: Crafting a Retirement Budget Based on Lifestyle Choices

Crafting a retirement budget tailored to your desired lifestyle is a crucial step in ensuring financial security and peace of mind during your retirement years. This example will guide you through the process using clear steps, mind maps, and practical illustrations.

Step 1: Define Your Retirement Lifestyle

Your lifestyle choices directly influence your retirement expenses. Consider factors such as travel frequency, hobbies, housing preferences, and healthcare needs.

Mind Map: Defining Retirement Lifestyle

Step 2: Estimate Monthly and Annual Expenses

Break down your expenses into categories aligned with your lifestyle choices.

| Expense Category | Monthly Estimate | Annual Estimate |

|---|---|---|

| Housing (Mortgage, Taxes, Maintenance) | $1,200 | $14,400 |

| Utilities (Electricity, Water, Internet) | $300 | $3,600 |

| Food (Groceries + Dining Out) | $600 | $7,200 |

| Healthcare (Insurance, Medications) | $400 | $4,800 |

| Travel (Average per month) | $500 | $6,000 |

| Hobbies & Leisure | $200 | $2,400 |

| Transportation (Fuel, Maintenance) | $250 | $3,000 |

| Miscellaneous | $150 | $1,800 |

| Total | $4,600 | $55,200 |

Step 3: Adjust for Inflation and Unexpected Costs

Plan for inflation (typically 2-3% annually) and unexpected expenses such as home repairs or medical emergencies.

Mind Map: Adjusting Budget for Inflation & Contingencies

Example: If you expect a 3% inflation rate, your $55,200 annual budget will increase approximately to $56,856 next year.

Step 4: Calculate Required Retirement Income

Using the annual expense estimate, determine the income you need to sustain your lifestyle.

Example:

- Annual Expenses: $55,200

- Expected Inflation Adjustment: 3%

- Adjusted Annual Expenses Year 1: $56,856

Consider taxes and other deductions to finalize the net income requirement.

Step 5: Create a Retirement Budget Mind Map

Mind Map: Retirement Budget Overview

Step 6: Example Scenario

Meet Jane and Mark:

- They plan to retire in 5 years.

- They want to travel twice a year internationally and take local trips quarterly.

- They plan to downsize their home, reducing housing costs.

- They enjoy golfing and dining out occasionally.

Budget Breakdown:

| Category | Monthly Cost | Notes |

|---|---|---|

| Housing | $1,000 | Downsized home |

| Utilities | $250 | Reduced space |

| Food | $700 | Dining out included |

| Healthcare | $500 | Includes supplemental insurance |

| Travel | $600 | Saving monthly for trips |

| Hobbies & Leisure | $300 | Golf club membership |

| Transportation | $200 | Less commuting |

| Miscellaneous | $150 | Buffer for unexpected expenses |

| Total | $3,700 |

Annual Total: $44,400

They plan to adjust this budget yearly for inflation and unexpected costs.

Final Tips:

- Regularly review and update your budget to reflect lifestyle changes.

- Use budgeting tools or apps to track expenses.

- Consider consulting a financial planner to align your budget with your overall retirement plan.

By following this structured approach and tailoring your budget to your lifestyle, you can confidently prepare for a financially secure and fulfilling retirement.

4. Understanding Retirement Income Sources

4.1 Social Security Benefits: Maximizing and Timing Strategies

Social Security benefits are a cornerstone of retirement income for many Americans. Understanding how to maximize these benefits and strategically time your claims can significantly impact your financial security in retirement. This section explores best practices, timing strategies, and practical examples to help you optimize your Social Security benefits.

Understanding Social Security Benefits

Social Security benefits are calculated based on your highest 35 years of earnings, adjusted for inflation. The amount you receive depends on your age at the time you start claiming benefits.

- Full Retirement Age (FRA): The age at which you are entitled to 100% of your Social Security benefits, typically between 66 and 67, depending on your birth year.

- Early Retirement: You can claim benefits as early as age 62, but your monthly benefit will be reduced.

- Delayed Retirement: Delaying benefits past FRA up to age 70 increases your monthly benefit through delayed retirement credits.

Mind Map: Social Security Claiming Strategies

Best Practices for Maximizing Social Security Benefits

-

Delay Claiming Benefits if Possible

- Delaying benefits from FRA to age 70 increases your monthly payment by approximately 8% per year.

- Example: If your FRA benefit is $1,500/month, delaying to 70 increases it to about $1,980/month.

-

Coordinate with Your Spouse

- Use spousal benefits to maximize household income.

- Example: One spouse claims early spousal benefits while the higher earner delays to 70.

-

Consider Health and Longevity

- If you have health issues or a shorter life expectancy, early claiming might make sense.

- Conversely, if you expect to live into your 80s or beyond, delaying benefits is advantageous.

-

Understand Tax Implications

- Social Security benefits may be taxable depending on your total income.

- Plan withdrawals from other accounts to minimize tax impact.

-

Use the ‘File and Suspend’ Strategy (if applicable)

- Although limited by recent legislation, some scenarios still allow strategic filing and suspending.

Mind Map: Factors Influencing Social Security Timing

Example 1: Delaying Benefits to Maximize Income

Scenario: Jane is 66 (FRA) and eligible for $2,000/month Social Security. She is in good health and expects to live into her 90s.

- If Jane claims at 66, she receives $2,000/month.

- If Jane delays until 70, her benefit increases by 32% (8% per year for 4 years), resulting in $2,640/month.

Outcome: Over 20 years, delaying benefits results in approximately $153,600 more in total benefits.

Example 2: Coordinated Spousal Claiming

Scenario: John and Mary are married. John’s FRA benefit is $2,500/month; Mary’s is $1,200/month.

- Mary claims spousal benefits at 62 (50% of John’s FRA benefit = $1,250), while John delays until 70 to maximize his benefit.

- John’s benefit grows to $3,300/month by delaying.

Outcome: Household income is optimized by combining early spousal benefits with delayed higher earner benefits.

Practical Tips for Accountants and Financial Planners

- Use Social Security calculators to model different claiming ages and scenarios.

- Educate clients on the trade-offs between early and delayed claiming.

- Review client health and family longevity history to tailor strategies.

- Coordinate Social Security planning with overall retirement income and tax strategies.

Summary

Maximizing Social Security benefits requires a strategic approach considering timing, health, spousal benefits, and tax implications. By leveraging delaying strategies and coordinating with spouses, retirees can significantly enhance their retirement income and financial security.

4.2 Employer-Sponsored Retirement Plans (401(k), 403(b), etc.)

Employer-sponsored retirement plans are among the most common and effective vehicles for building retirement savings. These plans, such as 401(k)s and 403(b)s, offer tax advantages, potential employer matching contributions, and automated payroll deductions that make saving easier and more consistent.

What Are Employer-Sponsored Retirement Plans?

- 401(k) Plans: Offered primarily by private-sector employers, allowing employees to contribute a portion of their salary pre-tax or as Roth (after-tax) contributions.

- 403(b) Plans: Similar to 401(k)s but designed for employees of public schools, certain non-profits, and tax-exempt organizations.

- 457 Plans: Available to some government and non-profit employees, with unique withdrawal rules.

Key Features and Benefits

- Tax Advantages: Contributions reduce taxable income (traditional) or grow tax-free (Roth).

- Employer Match: Many employers match a percentage of employee contributions, effectively providing free money.

- Automatic Payroll Deductions: Simplifies saving by deducting contributions directly from paychecks.

- Higher Contribution Limits: Compared to IRAs, allowing accelerated savings.

Mind Map: Employer-Sponsored Retirement Plans Overview

Contribution Limits and Employer Match

For 2024, the IRS allows employees to contribute up to $23,000 to 401(k) and 403(b) plans (including catch-up contributions for those 50 and older). Employer matches vary but commonly match 50% of contributions up to 6% of salary.

Example:

- Employee salary: $80,000

- Employee contributes 6% = $4,800

- Employer matches 50% of 6% = 3% = $2,400

- Total annual contribution = $7,200

This employer match is essentially a 50% immediate return on the employee’s contribution, significantly boosting retirement savings.

Investment Options Within Employer Plans

Most plans offer a variety of investment options, including:

- Target-Date Funds: Automatically adjust asset allocation based on expected retirement year.

- Mutual Funds: Stocks, bonds, balanced funds.

- Stable Value or Money Market Funds: Lower risk, lower return.

Employees should choose investments aligned with their risk tolerance and retirement timeline.

Example Scenario: Maximizing a 401(k) Plan

Scenario: Jane, age 35, earns $70,000 annually and wants to maximize her retirement savings.

- She contributes 10% of her salary ($7,000) to her 401(k).

- Her employer offers a 100% match on the first 5% of contributions.

- Employer match = 5% of $70,000 = $3,500.

Outcome: Jane’s total annual contribution is $10,500, accelerating her savings growth.

By investing in a diversified target-date fund, Jane benefits from automatic rebalancing and a risk profile that becomes more conservative as she approaches retirement.

Mind Map: Steps to Optimize Employer-Sponsored Plan Participation

Withdrawal Rules and Considerations

- Withdrawals before age 59½ typically incur a 10% penalty plus income tax (for traditional accounts).

- Required Minimum Distributions (RMDs) must begin at age 73 (as of 2024) for traditional accounts.

- Roth 401(k) withdrawals are tax-free if the account is held for at least 5 years and the participant is over 59½.

Example: Impact of Early vs. Late Enrollment

| Age Started | Annual Contribution | Employer Match | Years Contributing | Estimated Balance at 65 (7% return) |

|---|---|---|---|---|

| 25 | $6,000 | $3,000 | 40 | $1,000,000+ |

| 35 | $6,000 | $3,000 | 30 | ~$540,000 |

| 45 | $6,000 | $3,000 | 20 | ~$260,000 |

This example highlights the power of compounding and the importance of starting early.

Summary

Employer-sponsored retirement plans like 401(k)s and 403(b)s are powerful tools for retirement savings due to tax advantages, employer matches, and ease of contribution. Accountants and financial planners should encourage clients to maximize contributions, especially to capture full employer matches, select investments aligned with their goals, and understand withdrawal rules to optimize retirement outcomes.

4.3 Individual Retirement Accounts (IRA) and Roth IRAs

Individual Retirement Accounts (IRAs) are essential tools for retirement savings, offering tax advantages that can significantly impact your financial future. Understanding the differences between Traditional IRAs and Roth IRAs, their contribution limits, tax implications, and withdrawal rules is crucial for effective retirement planning.

What is an IRA?

An IRA is a personal retirement savings account that allows individuals to set aside money for retirement with tax benefits. There are two primary types:

- Traditional IRA

- Roth IRA

Both serve the purpose of retirement savings but differ mainly in tax treatment and withdrawal rules.

Mind Map: Overview of IRA Types

Contribution Limits and Eligibility (2024)

- Contribution Limit: $6,500 per year ($7,500 if age 50 or older)

- Traditional IRA: Anyone with earned income can contribute, but tax deductibility depends on income and participation in an employer plan.

- Roth IRA: Contributions are limited based on Modified Adjusted Gross Income (MAGI):

- Single filers: Phase-out starts at $138,000 and ends at $153,000

- Married filing jointly: Phase-out starts at $218,000 and ends at $228,000

Tax Treatment Comparison

| Feature | Traditional IRA | Roth IRA |

|---|---|---|

| Contributions | Potentially tax-deductible | After-tax (no deduction) |

| Earnings Growth | Tax-deferred | Tax-free |

| Withdrawals | Taxed as ordinary income | Tax-free if qualified |

| RMDs | Required starting at age 73 | No RMDs during owner’s lifetime |

Withdrawal Rules

-

Traditional IRA:

- Withdrawals before age 59½ may incur a 10% penalty plus income tax.

- RMDs must begin at age 73.

-

Roth IRA:

- Contributions can be withdrawn anytime tax- and penalty-free.

- Earnings withdrawn tax-free after age 59½ and account held for at least 5 years.

Mind Map: IRA Withdrawal Rules

Example 1: Choosing Between Traditional and Roth IRA

Scenario: Sarah, age 35, earns $70,000 annually and expects to be in a higher tax bracket at retirement.

- Traditional IRA: Contributions reduce taxable income now, but withdrawals will be taxed at a higher rate later.

- Roth IRA: Pay taxes now at a lower rate, enjoy tax-free withdrawals in retirement.

Best Practice: Sarah opts for a Roth IRA to benefit from tax-free growth and withdrawals, anticipating higher taxes in retirement.

Example 2: Maximizing IRA Contributions

Scenario: John, age 52, wants to catch up on retirement savings.

- Contribution limit for 50+ is $7,500.

- John contributes the full $7,500 to his Traditional IRA.

Best Practice: Utilizing catch-up contributions helps John accelerate savings and benefit from tax deferral.

Combining IRAs with Employer Plans

Many individuals contribute to both IRAs and employer-sponsored plans like 401(k)s.

- Contribution limits are separate.

- Diversifying between Traditional and Roth accounts can provide tax flexibility in retirement.

Mind Map: Strategic IRA Use in Retirement Planning

Summary

Individual Retirement Accounts are powerful retirement savings vehicles. By understanding the nuances of Traditional and Roth IRAs, financial planners and accountants can tailor strategies that optimize tax benefits, growth potential, and withdrawal flexibility for their clients.

Additional Resources

- IRS Publication 590-A and 590-B

- Financial planning software tools for IRA projections

- Consultation with tax professionals for personalized advice

4.4 Pension Plans and Annuities: Pros and Cons

Pension plans and annuities are two important components of retirement income planning. Understanding their benefits and drawbacks helps financial planners and accountants guide clients effectively.

What Are Pension Plans?

A pension plan is a retirement plan that provides a fixed income to retirees, typically funded by employers, employees, or both. The most common types are defined benefit plans, where the payout is predetermined based on salary and years of service.

What Are Annuities?

An annuity is a financial product sold by insurance companies designed to provide a steady income stream, often for life, in exchange for an initial lump sum or series of payments.

Mind Map: Pension Plans

Mind Map: Annuities

Pros of Pension Plans

- Guaranteed Income: Pensions provide a steady, predictable income stream, which helps retirees budget confidently.

- Employer Contributions: Many pension plans are funded partially or fully by employers, reducing the individual’s savings burden.

- Longevity Protection: Defined benefit plans often pay for life, protecting against outliving savings.

Cons of Pension Plans

- Limited Control: Employees typically have no say in how pension funds are invested.

- Underfunding Risks: Some pension plans may face funding shortfalls, potentially reducing benefits.

- Lack of Portability: Changing jobs can complicate pension benefits, especially if the new employer does not offer a comparable plan.

Pros of Annuities

- Lifetime Income: Annuities can guarantee income for life, which is valuable for managing longevity risk.

- Tax Deferral: Earnings on annuities grow tax-deferred until withdrawal.

- Flexible Options: Various payout structures (e.g., fixed, variable, immediate, deferred) allow customization.

Cons of Annuities

- Fees and Expenses: Annuities often have higher fees compared to other investment vehicles.

- Complexity: The variety of annuity products can be confusing, making it difficult to choose the right one.

- Liquidity Constraints: Many annuities impose surrender charges or penalties for early withdrawals.

Example 1: Pension Plan in Action

Scenario: Sarah has worked 30 years at a company with a defined benefit pension plan. Upon retirement, she receives $2,500 per month for life.

Benefit: Sarah can plan her monthly expenses knowing this income is guaranteed regardless of market conditions.

Consideration: If Sarah changes jobs before retirement, she might lose some benefits or have a reduced payout.

Example 2: Using an Immediate Annuity

Scenario: John has saved $300,000 and decides to purchase an immediate fixed annuity at age 65.

Outcome: He receives $1,500 per month for life, providing a predictable income stream.

Consideration: John pays fees and loses access to the lump sum, limiting liquidity.

Integrating Pension Plans and Annuities in Retirement Planning

Financial planners often recommend combining pension income with annuities to create a diversified and reliable income portfolio. For example, a client with a small or no pension might use an annuity to replicate the guaranteed income feature.

Summary Table: Pension Plans vs. Annuities

| Feature | Pension Plans | Annuities |

|---|---|---|

| Income Guarantee | Usually guaranteed for life | Can be guaranteed for life |

| Control Over Funds | Limited | Varies by product |

| Funding Source | Employer and/or employee | Individual purchase |

| Liquidity | Low | Often low, with surrender charges |

| Fees | Generally low | Can be high |

| Tax Treatment | Taxed as ordinary income | Tax-deferred growth until withdrawal |

By understanding these pros and cons, accountants and financial planners can tailor retirement strategies that optimize income security and flexibility for their clients.

4.5 Example: Combining Multiple Income Streams for a Stable Retirement

A stable retirement income often depends on diversifying income sources to reduce risk and ensure consistent cash flow. Combining multiple income streams helps retirees manage market volatility, inflation, and unexpected expenses.

Why Multiple Income Streams Matter

- Risk Reduction: If one source underperforms, others can compensate.

- Flexibility: Different income types can be accessed under varying conditions.

- Inflation Protection: Certain streams may grow with inflation.

Common Retirement Income Streams

- Social Security Benefits

- Employer-Sponsored Plans (401(k), 403(b))

- IRAs and Roth IRAs

- Pension Plans

- Annuities

- Investment Dividends and Interest

- Part-time Work or Consulting

Mind Map: Multiple Income Streams Overview

Example Scenario: The Smiths’ Retirement Income Plan

Profile: John (65) and Mary (63) Smith are planning to retire next year. They want a stable income that covers their $60,000 annual expenses.

Income Sources:

- Social Security: $24,000/year combined (John delays until 70 to increase benefits)

- 401(k) and IRA withdrawals: $20,000/year

- Pension: $10,000/year

- Dividend income from taxable investments: $6,000/year

Strategy:

- John delays Social Security to maximize benefits, relying on pension and investments initially.

- Withdrawals from 401(k) and IRA are planned to fill the gap between pension and expenses.

- Dividend income supplements cash flow and offers potential growth.

Outcome:

- Total income in early retirement: $36,000 (pension + investments)

- At age 70, Social Security benefits increase to $36,000/year, raising total income to $72,000, providing a cushion for inflation and unexpected costs.

Mind Map: Smiths’ Income Flow

Tips for Combining Income Streams Effectively

- Coordinate Timing: Delay Social Security if possible to increase benefits.

- Tax Efficiency: Withdraw from taxable accounts first to allow tax-advantaged accounts to grow.

- Maintain Liquidity: Keep some assets easily accessible for emergencies.

- Consider Inflation: Include income streams that adjust or grow with inflation.

- Review Annually: Adjust withdrawals and income sources based on market conditions and expenses.

Additional Example: Using Annuities to Stabilize Income

- Jane, 67, purchases an immediate annuity with $100,000.

- The annuity pays $6,000 annually guaranteed for life.

- Combined with Social Security ($18,000) and investment withdrawals ($16,000), Jane secures $40,000/year.

- The annuity reduces longevity risk and provides peace of mind.

By thoughtfully combining multiple income streams, retirees like the Smiths and Jane can build a resilient financial foundation that supports their lifestyle and adapts to changing circumstances.

5. Investment Strategies for Retirement

5.1 Asset Allocation and Diversification Principles

Asset allocation and diversification are foundational concepts in retirement investment strategy. They help manage risk, optimize returns, and ensure your portfolio aligns with your retirement goals and risk tolerance.

What is Asset Allocation?

Asset allocation is the process of dividing your investment portfolio among different asset categories, such as stocks, bonds, and cash. The goal is to balance risk and reward by apportioning assets according to your risk tolerance, time horizon, and investment objectives.

Key asset classes:

- Equities (Stocks): Higher growth potential but more volatile.

- Fixed Income (Bonds): Generally lower risk, provide income.

- Cash and Cash Equivalents: Lowest risk, high liquidity, but low returns.

- Alternative Investments: Real estate, commodities, etc., for further diversification.

What is Diversification?

Diversification means spreading investments within and across asset classes to reduce exposure to any single asset or risk. It helps smooth out volatility and protects your portfolio from large losses.

Diversification can be achieved by:

- Investing in different sectors (technology, healthcare, consumer goods, etc.)

- Investing across geographic regions (domestic, international, emerging markets)

- Using different investment styles (growth vs. value)

Mind Map: Asset Allocation and Diversification

Best Practices for Asset Allocation in Retirement Planning

-

Consider Your Time Horizon:

- The longer until retirement, the more you can allocate to equities for growth.

- As retirement nears, shift towards bonds and cash to preserve capital.

-

Assess Your Risk Tolerance:

- Conservative investors may prefer higher bond allocations.

- Aggressive investors may maintain higher equity exposure.

-

Rebalance Regularly:

- Periodically adjust your portfolio to maintain your target allocation.

- This prevents overexposure to any asset class due to market movements.

-

Use Target-Date Funds as a Starting Point:

- These funds automatically adjust allocation based on your expected retirement date.

Example 1: Age-Based Asset Allocation

Consider a 40-year-old planning to retire at 65 with a moderate risk tolerance.

| Asset Class | Allocation (%) |

|---|---|

| Stocks | 70 |

| Bonds | 25 |

| Cash | 5 |

At age 60, the allocation might shift to:

| Asset Class | Allocation (%) |

|---|---|

| Stocks | 40 |

| Bonds | 50 |

| Cash | 10 |

This gradual shift reduces risk as retirement approaches.

Example 2: Diversification Within Equities

Instead of investing 100% in domestic stocks, diversify:

- 50% Domestic Large-Cap Stocks

- 20% Domestic Small-Cap Stocks

- 20% International Developed Market Stocks

- 10% Emerging Market Stocks

This diversification helps reduce the impact of downturns in any single market.

Mind Map: Example Portfolio Breakdown

Summary

Asset allocation and diversification are critical to managing risk and achieving steady growth in your retirement portfolio. By thoughtfully allocating assets based on your age, risk tolerance, and goals, and diversifying within and across asset classes, you can build a resilient portfolio that supports your retirement lifestyle.

Regular reviews and rebalancing ensure your portfolio stays aligned with your evolving needs.

For financial planners and accountants advising clients, illustrating these principles with clear, relatable examples helps clients understand the importance and feel confident in their retirement strategy.

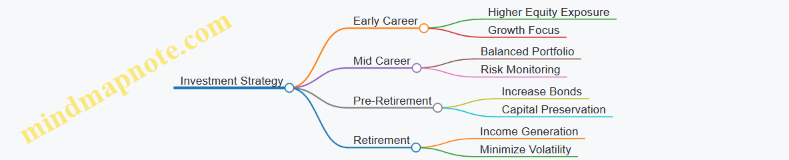

5.2 Risk Management and Adjusting Portfolio Over Time

Effective risk management is a cornerstone of successful retirement planning. As you approach retirement, your investment portfolio should evolve to reflect changing risk tolerance, time horizon, and income needs. This section explores best practices for managing risk and adjusting your portfolio over time, supported by clear examples and mind maps.

Understanding Investment Risk

Investment risk refers to the possibility that your portfolio’s returns will be lower than expected or that you could lose some of your invested capital. Common types of risks include:

- Market Risk: Fluctuations in stock and bond markets.

- Inflation Risk: The risk that inflation erodes purchasing power.

- Longevity Risk: Outliving your savings.

- Interest Rate Risk: Impact on bond prices due to changing interest rates.

Mind Map: Types of Investment Risk

Risk Tolerance and Time Horizon

Your risk tolerance is your ability and willingness to endure market fluctuations. Time horizon refers to the length of time before you need to access your funds. Generally:

- Longer Time Horizon: Higher risk tolerance, more equities.

- Shorter Time Horizon: Lower risk tolerance, more fixed income.

Example: Adjusting Risk Tolerance Over Time

John, age 40, has 25 years until retirement. He starts with 80% equities and 20% bonds. By age 60, with 5 years left, he shifts to 50% equities and 50% bonds to reduce volatility.

Portfolio Adjustment Strategies

- Glide Path Approach: Gradually reduce equity exposure as retirement nears.

- Risk Parity: Balance portfolio risk contributions rather than asset allocation percentages.

- Dynamic Rebalancing: Adjust portfolio based on market conditions and personal circumstances.

Mind Map: Portfolio Adjustment Strategies

Managing Sequence of Returns Risk

Sequence of returns risk is the danger of experiencing poor investment returns early in retirement, which can deplete savings faster.

Best Practice: Maintain a cash reserve or bond ladder to cover initial retirement expenses, reducing the need to sell equities during downturns.

Example: Sequence of Returns Risk Mitigation

Sarah retires with $1 million. She keeps 2 years of living expenses in cash and bonds, so if the market drops 20% in year one, she doesn’t have to sell stocks at a loss.

Diversification as a Risk Management Tool

Diversification spreads investments across asset classes, sectors, and geographies to reduce risk.

Example: A portfolio with U.S. stocks, international stocks, bonds, and real estate investment trusts (REITs) tends to be less volatile than one concentrated solely in domestic equities.

Mind Map: Diversification Components

Rebalancing Your Portfolio

Rebalancing involves realigning portfolio weights back to target allocations to maintain desired risk levels.

- Frequency: Annually or semi-annually.

- Threshold: When allocation drifts by more than 5%.

Example: Rebalancing

If equities grow from 60% to 70% of the portfolio, selling some equities and buying bonds brings the allocation back to 60/40, maintaining risk balance.

Practical Example: Portfolio Adjustment Over 30 Years

| Age | Equities (%) | Bonds (%) | Cash (%) | Notes |

|---|---|---|---|---|

| 35 | 85 | 10 | 5 | High growth phase |

| 50 | 70 | 25 | 5 | Moderate risk reduction |

| 60 | 50 | 40 | 10 | Preparing for retirement |

| 65 | 40 | 50 | 10 | Retirement phase, income focus |

This gradual shift reduces exposure to volatility while ensuring growth potential early on.

Summary

- Assess and understand your risk tolerance and time horizon.

- Use diversification and rebalancing to manage risk.

- Gradually adjust your portfolio allocation as you approach retirement.

- Maintain liquidity to mitigate sequence of returns risk.

By applying these risk management strategies, financial planners can help clients build resilient portfolios that adapt to changing needs and market conditions, ensuring a more secure retirement.

5.3 Tax-Efficient Investing for Retirement Accounts

Tax-efficient investing is a critical component of maximizing retirement savings and minimizing the tax burden during both the accumulation and distribution phases. Understanding how different retirement accounts are taxed and strategically allocating assets can significantly enhance after-tax returns.

Understanding Tax Treatment of Retirement Accounts

- Traditional 401(k) and Traditional IRA: Contributions are typically pre-tax, reducing taxable income now. Taxes are paid upon withdrawal at ordinary income tax rates.

- Roth IRA and Roth 401(k): Contributions are made with after-tax dollars. Qualified withdrawals are tax-free.

- Taxable Accounts: Investments are subject to capital gains taxes when assets are sold, and dividends may be taxed annually.

Mind Map: Types of Retirement Accounts and Their Tax Characteristics

Best Practices for Tax-Efficient Investing

-

Asset Location Optimization

- Place tax-inefficient investments (e.g., bonds, REITs, actively managed funds) in tax-advantaged accounts like Traditional IRAs or 401(k)s.

- Hold tax-efficient investments (e.g., index funds, ETFs, growth stocks) in taxable accounts.

-

Utilize Roth Accounts for Growth Assets

- Since qualified withdrawals from Roth accounts are tax-free, place high-growth investments here to maximize tax-free compounding.

-

Tax-Loss Harvesting in Taxable Accounts

- Offset capital gains by selling losing investments to reduce tax liability.

-

Minimize Turnover in Taxable Accounts

- Lower transaction frequency to reduce capital gains distributions.

-

Consider Required Minimum Distributions (RMDs)

- Plan withdrawals from Traditional accounts to manage tax brackets and avoid penalties.

Mind Map: Asset Location Strategy

Example 1: Asset Location in Practice

Scenario: Sarah has $200,000 split evenly between a Traditional IRA and a taxable brokerage account. She wants to optimize tax efficiency.

- She holds $50,000 in bond funds and $50,000 in dividend-paying stocks in her Traditional IRA.

- In her taxable account, she holds $100,000 in a low-cost S&P 500 index fund.

Improvement: Sarah moves the bond funds into her Traditional IRA to shelter interest income from taxes and reallocates growth stocks to her Roth IRA (if available) or taxable account to benefit from lower capital gains tax rates.

Example 2: Roth Conversion for Tax Efficiency

Scenario: John is 55 and expects to be in a higher tax bracket in retirement. He has $150,000 in a Traditional IRA.

- He decides to convert $20,000 annually to a Roth IRA over several years.

- He pays taxes on the converted amount now at a lower rate.

- Future growth and withdrawals from the Roth IRA will be tax-free.

This strategy reduces future RMDs and potential tax burdens.

Mind Map: Tax-Efficient Withdrawal Strategy

Key Takeaways

- Understand the tax characteristics of each retirement account.

- Strategically allocate assets based on their tax efficiency.

- Use Roth accounts for investments with high growth potential.

- Employ tax-loss harvesting and minimize turnover in taxable accounts.

- Plan withdrawals to manage tax brackets and reduce tax liabilities.

By integrating these tax-efficient investing strategies, financial planners and accountants can help clients maximize their retirement wealth and enjoy a more tax-optimized retirement income.

5.4 Incorporating Dividend and Growth Stocks

Incorporating dividend and growth stocks into a retirement portfolio is a powerful strategy to balance income generation with capital appreciation. Understanding the characteristics, benefits, and risks of each type of stock can help financial planners and accountants advise clients on building a resilient and diversified portfolio tailored to their retirement goals.

What Are Dividend Stocks?

Dividend stocks are shares of companies that regularly distribute a portion of their earnings to shareholders in the form of dividends. These stocks tend to be from well-established companies with stable cash flows.

Key Characteristics:

- Provide regular income through dividends

- Typically less volatile than growth stocks

- Often belong to sectors like utilities, consumer staples, and financials

Example: A retiree invests $100,000 in a utility company paying a 4% annual dividend, generating $4,000 in steady income.

What Are Growth Stocks?

Growth stocks represent companies expected to grow earnings at an above-average rate compared to the market. These companies often reinvest earnings instead of paying dividends.

Key Characteristics:

- Focus on capital appreciation rather than income

- Higher volatility and risk

- Common in technology, biotech, and emerging industries

Example: An investor buys shares in a tech startup expecting significant price appreciation over 10 years, potentially increasing the portfolio’s value substantially.

Benefits of Combining Dividend and Growth Stocks

- Income + Growth: Dividend stocks provide cash flow, while growth stocks offer the potential for capital gains.

- Risk Mitigation: Dividend stocks tend to be more stable, balancing the higher volatility of growth stocks.

- Inflation Hedge: Growth stocks can help portfolios keep pace with inflation through price appreciation.

Mind Map: Dividend vs. Growth Stocks

How to Incorporate Dividend and Growth Stocks into Retirement Portfolios

-

Assess Risk Tolerance and Time Horizon

- Older clients or those closer to retirement may favor higher dividend allocations for income and stability.

- Younger clients can allocate more to growth stocks for long-term appreciation.

-

Determine Allocation Mix

- A common rule of thumb is to increase dividend stock allocation as retirement nears.

- Example allocation: 60% dividend stocks, 40% growth stocks for a retiree.

-

Select Quality Stocks

- Dividend stocks with a history of increasing dividends (Dividend Aristocrats).

- Growth stocks with strong earnings growth and competitive advantages.

-

Rebalance Periodically

- Adjust allocations to maintain target mix and respond to market changes.

Mind Map: Incorporation Strategy

Practical Example: Building a Balanced Retirement Portfolio

Client Profile: Jane, age 60, plans to retire in 5 years, moderate risk tolerance.

Step 1: Allocation

- 65% dividend stocks

- 35% growth stocks

Step 2: Dividend Stock Picks

- Johnson & Johnson (JNJ) – consistent dividend growth

- Procter & Gamble (PG) – stable consumer staples

Step 3: Growth Stock Picks

- Alphabet Inc. (GOOGL) – strong earnings growth

- Tesla Inc. (TSLA) – innovative technology

Step 4: Expected Outcomes

- Dividend income provides steady cash flow for expenses.

- Growth stocks offer potential portfolio appreciation to combat inflation.

Step 5: Review and Rebalance

- Annual portfolio review to adjust allocations as Jane approaches retirement.

Summary

Incorporating dividend and growth stocks allows retirees to enjoy a blend of income and capital growth. By understanding client needs, selecting quality stocks, and maintaining a disciplined approach, financial planners can help clients build portfolios that support a comfortable and sustainable retirement.

5.5 Example: Constructing a Balanced Retirement Portfolio

Constructing a balanced retirement portfolio is essential to managing risk while aiming for steady growth to support your retirement income needs. This example will guide you through the process of building a diversified portfolio tailored for a retiree or someone nearing retirement.

Step 1: Define Your Risk Tolerance and Time Horizon

- Risk Tolerance: Moderate (willing to accept some volatility for growth)

- Time Horizon: 15 years until retirement, 25+ years in retirement

Step 2: Asset Allocation Strategy

A common rule of thumb for retirees is to reduce exposure to equities and increase bonds and cash equivalents to preserve capital and generate income.

Example Allocation:

- 50% Stocks (Equities)

- 40% Bonds (Fixed Income)

- 10% Cash or Cash Equivalents

Step 3: Diversify Within Asset Classes

Stocks (50%)

- 30% U.S. Large-Cap Stocks (e.g., S&P 500 Index Funds)

- 10% U.S. Small/Mid-Cap Stocks

- 10% International Developed Markets

Bonds (40%)

- 25% U.S. Treasury Bonds (long-term and intermediate)

- 10% Investment Grade Corporate Bonds

- 5% Municipal Bonds (tax-advantaged)

Cash & Equivalents (10%)