Risk Management for Accountants

1. Introduction to Risk Management in Accounting

1.1 Understanding Risk: Definitions and Types Relevant to Accountants

What is Risk?

Risk, in the context of accounting and finance, refers to the possibility of an event or condition that may negatively impact an organization’s financial health, operations, or reputation. It represents uncertainty about outcomes that can lead to losses or missed opportunities.

Key Definitions:

- Risk: The effect of uncertainty on objectives.

- Risk Management: The process of identifying, assessing, and controlling threats to an organization’s capital and earnings.

- Risk Appetite: The amount and type of risk an organization is willing to pursue or retain.

Types of Risks Relevant to Accountants

Accountants face a variety of risks that can affect financial reporting, compliance, and operational efficiency. Understanding these categories helps in designing effective controls and mitigation strategies.

Mind Map: Types of Risks Relevant to Accountants

Detailed Explanation of Each Risk Type with Examples

-

Financial Risks

- Market Risk: Exposure to losses due to changes in market prices, such as interest rates or foreign exchange rates.

- Example: An accountant managing foreign currency transactions may face losses if exchange rates fluctuate unexpectedly.

- Credit Risk: Risk that a debtor will not fulfill their financial obligations.

- Example: Accounts receivable aging shows overdue payments, increasing the risk of bad debts.

- Liquidity Risk: Risk that the company cannot meet short-term financial demands.

- Example: Insufficient cash flow to pay suppliers on time, causing operational disruptions.

- Market Risk: Exposure to losses due to changes in market prices, such as interest rates or foreign exchange rates.

-

Operational Risks

- Process Failures: Errors or inefficiencies in accounting processes.

- Example: Incorrect data entry leading to misstated financial reports.

- Human Errors: Mistakes made by staff due to lack of training or oversight.

- Example: An accountant accidentally posts a transaction twice.

- System Failures: IT system crashes or software bugs affecting accounting data.

- Example: Accounting software downtime during month-end closing.

- Process Failures: Errors or inefficiencies in accounting processes.

-

Compliance Risks

- Regulatory Non-Compliance: Failure to adhere to laws, regulations, or standards.

- Example: Missing deadlines for tax filings resulting in penalties.

- Taxation Errors: Incorrect tax calculations or reporting.

- Example: Misclassifying expenses leading to underpayment of taxes.

- Regulatory Non-Compliance: Failure to adhere to laws, regulations, or standards.

-

Fraud Risks

- Asset Misappropriation: Theft or misuse of company assets.

- Example: An employee creating fake vendor invoices to divert funds.

- Financial Statement Fraud: Deliberate misrepresentation of financial information.

- Example: Inflating revenue figures to meet targets.

- Corruption: Bribery or unethical behavior influencing financial decisions.

- Example: Accepting kickbacks from suppliers.

- Asset Misappropriation: Theft or misuse of company assets.

-

Reputational Risks

- Public Disclosure Issues: Negative publicity from financial misstatements.

- Example: A restatement of earnings causing loss of investor confidence.

- Ethical Violations: Breaches of professional ethics damaging credibility.

- Example: An accountant ignoring conflicts of interest.

- Public Disclosure Issues: Negative publicity from financial misstatements.

Mind Map: Risk Management Process for Accountants

Example Scenario: Understanding Risk in Accounts Payable

- Risk Identified: Duplicate payments due to manual invoice processing.

- Impact: Financial loss and strained supplier relationships.

- Mitigation: Implement automated invoice matching and approval workflows.

- Outcome: Reduced errors and improved control over cash outflows.

Summary

Understanding the various types of risks relevant to accountants is foundational for effective risk management. By categorizing risks into financial, operational, compliance, fraud, and reputational, accountants can better identify vulnerabilities and apply targeted controls. Integrating these insights into daily accounting practices helps safeguard organizational assets and maintain financial integrity.

1.2 The Importance of Risk Management in Accounting and Finance

Risk management is a critical discipline within accounting and finance that ensures organizations can identify, assess, and mitigate potential threats that could impact financial accuracy, compliance, and overall business sustainability. Without effective risk management, accountants and finance professionals expose their organizations to financial losses, reputational damage, regulatory penalties, and operational disruptions.

Why Risk Management Matters in Accounting and Finance

- Accuracy and Integrity of Financial Reporting: Ensures that financial statements are free from material misstatements, whether due to error or fraud.

- Regulatory Compliance: Helps organizations adhere to laws and regulations such as SOX, IFRS, GAAP, and tax codes.

- Fraud Prevention and Detection: Protects assets by identifying vulnerabilities and implementing controls to prevent fraudulent activities.

- Operational Continuity: Minimizes disruptions caused by financial mismanagement or external risks.

- Stakeholder Confidence: Builds trust among investors, creditors, and regulators through transparent and reliable financial practices.

Mind Map: Importance of Risk Management in Accounting and Finance

Practical Example 1: Preventing Financial Misstatements

A mid-sized manufacturing company failed to implement proper risk management controls around revenue recognition. As a result, their quarterly financial reports included premature revenue entries, leading to overstated earnings. This misstatement was discovered during an external audit, causing a restatement of earnings, loss of investor confidence, and regulatory scrutiny.

By integrating risk management practices such as detailed process reviews, segregation of duties, and automated controls, the company could have detected and prevented these errors early, preserving financial integrity.

Mind Map: Risk Management Controls to Prevent Misstatements

Practical Example 2: Ensuring Compliance with Sarbanes-Oxley (SOX)

A publicly traded company faced significant penalties due to non-compliance with SOX requirements. The accounting team lacked a formal risk assessment process and failed to document internal controls adequately.

Implementing a risk management framework allowed the company to identify compliance gaps, design controls to address them, and maintain detailed documentation. This proactive approach not only avoided penalties but also improved the efficiency of external audits.

Mind Map: Risk Management and Regulatory Compliance

Summary

Risk management in accounting and finance is indispensable for safeguarding the accuracy of financial information, ensuring regulatory compliance, preventing fraud, and maintaining operational stability. By embedding risk management into daily accounting practices, professionals can protect their organizations from costly errors and build a foundation of trust with stakeholders.

Key Takeaways

- Risk management reduces the likelihood of financial errors and fraud.

- Compliance with regulations is streamlined through structured risk processes.

- Effective controls and monitoring enhance operational resilience.

- Transparent risk reporting strengthens stakeholder confidence.

In the next sections, we will explore how to identify, assess, and mitigate these risks with practical tools and best practices tailored for accountants.

1.3 Overview of Risk Management Frameworks and Standards

Risk management frameworks and standards provide structured approaches for identifying, assessing, managing, and monitoring risks. For accountants, understanding these frameworks is essential to embed risk management into daily processes and ensure compliance with industry best practices.

Key Risk Management Frameworks and Standards Relevant to Accountants

-

COSO Enterprise Risk Management (ERM) Framework

- Developed by the Committee of Sponsoring Organizations of the Treadway Commission (COSO).

- Focuses on integrating risk management with strategy and performance.

- Widely used in financial reporting and internal control environments.

-

ISO 31000: Risk Management – Guidelines

- An international standard providing principles, framework, and process for managing risk.

- Flexible and applicable across industries, including accounting and finance.

-

COBIT (Control Objectives for Information and Related Technologies)

- Framework for IT governance and management.

- Important for accountants managing risks related to IT systems and data integrity.

-

Sarbanes-Oxley Act (SOX) Compliance Framework

- U.S. regulation focusing on internal controls over financial reporting.

- Requires rigorous risk assessment and control documentation.

-

Basel Accords (Basel II and III)

- International banking regulations addressing risk management in financial institutions.

- Relevant for accountants working in banking and financial services.

Mind Map: COSO ERM Framework

Example: An accounting team uses the COSO ERM framework to align their risk appetite with the organization’s strategic goals. They identify risks related to revenue recognition and design controls to mitigate those risks, reporting findings regularly to senior management.

Mind Map: ISO 31000 Risk Management Process

Example: An accountant applies ISO 31000 by first understanding the regulatory environment (establish context), identifying risks such as compliance breaches, analyzing their impact, and implementing mitigation strategies like automated compliance checks.

Mind Map: Sarbanes-Oxley (SOX) Compliance Framework

Example: To comply with SOX, an accounting department documents all financial reporting controls, performs regular risk assessments on these controls, and schedules internal audits to ensure controls are effective and risks are minimized.

Practical Integration Example

Imagine a mid-sized company’s accounting team implementing risk management:

- They adopt ISO 31000 as the overarching framework to guide their risk management process.

- For financial reporting risks, they integrate COSO ERM principles to ensure alignment with organizational strategy.

- To meet regulatory requirements, they follow SOX compliance guidelines for internal controls.

- For IT-related risks impacting accounting data, they use COBIT to manage and monitor IT controls.

This multi-framework approach ensures comprehensive coverage of risks from operational to regulatory and technological domains.

Summary

Understanding and applying these frameworks helps accountants:

- Establish a consistent approach to risk management.

- Align risk management with organizational objectives.

- Comply with regulatory requirements.

- Improve internal controls and reduce the likelihood of errors or fraud.

By integrating frameworks like COSO ERM, ISO 31000, and SOX, accountants can build resilient processes that proactively manage risks and support sound financial governance.

1.4 Common Risks Faced by Accountants: Financial, Operational, Compliance, and Fraud

Accountants operate in a complex environment where various types of risks can impact the accuracy, reliability, and integrity of financial information. Understanding these risks is crucial for effective risk management. Below, we explore the four primary categories of risks faced by accountants: Financial, Operational, Compliance, and Fraud. Each section includes mind maps and practical examples to illustrate these risks.

Financial Risks

Financial risks relate to errors or misstatements in financial reporting, which can lead to incorrect decision-making, financial losses, or reputational damage.

Mind Map: Financial Risks

Example: A company prematurely recognizes revenue from a large contract before delivery is complete. This inflates the current period’s revenue and misleads stakeholders about the company’s financial health. An accountant failing to identify this risk could contribute to misstated financial statements.

Operational Risks

Operational risks stem from failures in internal processes, people, or systems that affect the day-to-day accounting activities.

Mind Map: Operational Risks

Example: An accountant manually enters invoice data into the accounting system. Due to fatigue and lack of double-checking, several invoices are entered with incorrect amounts. This causes discrepancies in accounts payable and delays in vendor payments.

Compliance Risks

Compliance risks arise from failing to adhere to laws, regulations, and internal policies, potentially resulting in fines, penalties, or legal action.

Mind Map: Compliance Risks

Example: An accounting team misses the deadline for submitting quarterly tax returns due to poor scheduling and lack of reminders. This results in penalties and interest charges from tax authorities.

Fraud Risks

Fraud risks involve intentional acts to deceive or manipulate financial information for personal or organizational gain.

Mind Map: Fraud Risks

Example: An employee creates fake vendor accounts and submits fraudulent invoices for payment. Without proper segregation of duties and verification controls, these payments go unnoticed, leading to financial loss.

Summary Mind Map: Common Risks Faced by Accountants

Practical Takeaway

Accountants should maintain vigilance across all these risk areas by implementing strong internal controls, continuous monitoring, and regular training. For instance, automating invoice processing with validation checks can reduce operational errors, while regular compliance audits help avoid regulatory penalties. Recognizing fraud red flags and fostering an ethical culture are also essential to mitigate fraud risks effectively.

By understanding and addressing these common risks, accountants can safeguard the integrity of financial information and support sound business decision-making.

1.5 Case Study: How Poor Risk Management Led to Financial Misstatement

Introduction

In this case study, we explore a real-world example where inadequate risk management practices within an accounting department led to significant financial misstatements. Understanding the root causes and consequences helps accountants and risk managers appreciate the critical need for robust risk controls.

Background

A mid-sized manufacturing company, “ABC Manufacturing,” experienced a major financial restatement due to errors in revenue recognition and inventory valuation. The accounting team lacked proper risk identification and mitigation strategies, which allowed errors to go undetected for several quarters.

Mind Map: Root Causes of Financial Misstatement

Detailed Analysis

-

Lack of Internal Controls

- The accounting department did not segregate duties properly. The same individual was responsible for recording sales and reconciling accounts receivable.

- Example: A single employee could manipulate sales records without independent verification, increasing the risk of misstated revenue.

-

Insufficient Risk Identification

- The team failed to identify risks related to recognizing revenue before delivery was complete, violating revenue recognition principles.

- Example: Sales were recorded prematurely to meet quarterly targets, inflating revenue figures.

-

Inadequate Training

- Staff were not trained on the latest accounting standards (e.g., ASC 606), leading to incorrect application.

- Example: Inventory valuation methods were outdated, causing overstatement of assets.

-

Weak Communication

- Risk issues found during audits were not escalated to senior management promptly.

- Example: Early warning signs in audit reports were ignored, delaying corrective action.

Mind Map: Consequences of Poor Risk Management

Outcome

- The company was forced to restate its financials for the past two years.

- The SEC launched an investigation, resulting in fines.

- Several executives, including the CFO, resigned.

- Shareholders filed lawsuits citing misleading financial information.

Lessons Learned and Best Practices

-

Implement Strong Internal Controls: Segregate duties and establish independent review processes.

- Example: Separate the roles of sales recording and account reconciliation.

-

Regular Risk Identification: Continuously assess accounting processes for new or evolving risks.

- Example: Use risk registers updated quarterly.

-

Ongoing Training: Keep accounting staff updated on standards and fraud indicators.

- Example: Conduct quarterly workshops on ASC 606 and fraud detection.

-

Effective Communication: Ensure timely reporting of risks to senior management.

- Example: Establish a formal risk escalation protocol.

Summary

This case study highlights how poor risk management can directly lead to financial misstatements with severe legal, financial, and reputational consequences. Accountants and risk managers must proactively identify, assess, and mitigate risks to safeguard the integrity of financial reporting.

Additional Example: Early Detection Through Risk Analytics

By implementing data analytics tools, ABC Manufacturing could have detected unusual revenue spikes and inventory discrepancies early, prompting investigations before misstatements became material.

This proactive approach exemplifies best practice in integrating technology with risk management.

2. Identifying Risks in Accounting Processes

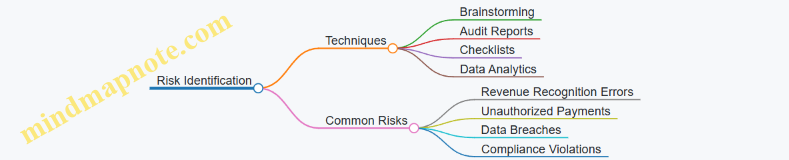

2.1 Risk Identification Techniques: Checklists, Brainstorming, and Interviews

Risk identification is the foundational step in effective risk management. For accountants, accurately identifying risks ensures that potential issues are addressed before they escalate into financial or compliance problems. This section explores three widely used techniques: Checklists, Brainstorming, and Interviews, each supported by practical examples and mind maps to clarify their application.

Checklists

Checklists are structured lists of potential risks tailored to specific accounting processes or environments. They help ensure that common and known risks are systematically considered.

Why use Checklists?

- Provide a comprehensive overview of typical risks

- Standardize risk identification across teams

- Save time by leveraging past knowledge

Example: Consider an accountant responsible for accounts payable. A checklist might include:

- Duplicate payments

- Unauthorized vendor additions

- Invoice mismatches

- Late payment penalties

- Fraudulent invoices

Mind Map: Checklist for Accounts Payable Risks

Using this checklist, accountants can systematically verify each risk area during process reviews.

Brainstorming

Brainstorming involves gathering a group of stakeholders to generate a wide range of potential risks through open discussion. This technique encourages creativity and uncovers risks that might not be obvious.

Best Practices for Brainstorming:

- Include diverse participants (e.g., accountants, auditors, risk managers)

- Encourage all ideas without immediate judgment

- Use a facilitator to keep the session focused

- Document all risks identified

Example: During a brainstorming session for the month-end closing process, participants might identify risks such as:

- Data entry errors due to manual processes

- Incomplete reconciliations

- System downtime delaying closing

- Misinterpretation of new accounting standards

Mind Map: Brainstorming Risks for Month-End Closing

This collaborative approach helps uncover both technical and operational risks.

Interviews

Interviews involve one-on-one or small group discussions with key personnel to extract detailed insights about risks from their experience and perspective.

When to Use Interviews:

- To explore complex or sensitive risk areas

- When detailed understanding of specific processes is needed

- To validate risks identified through other methods

Example: An accountant interviewing the IT team might uncover risks related to:

- Access controls to financial systems

- Backup and recovery procedures

- Cybersecurity vulnerabilities affecting accounting data

Mind Map: Interview Topics with IT for Accounting Risk

This targeted approach provides deep insights that might be missed in group sessions.

Summary Table of Techniques and Examples

| Technique | Description | Example Use Case | Key Benefit |

|---|---|---|---|

| Checklists | Structured list of known risks | Accounts payable risk identification | Comprehensive and repeatable |

| Brainstorming | Group discussion to generate diverse risks | Month-end closing risk exploration | Creative and inclusive |

| Interviews | One-on-one discussions for detailed insights | IT risk assessment for accounting systems | Deep, specialized understanding |

Practical Tip for Accountants

Combine these techniques for robust risk identification. For example, start with a checklist to cover basics, use brainstorming to explore new or emerging risks, and conduct interviews to validate and deepen understanding.

By integrating these methods, accountants can build a comprehensive risk profile that supports effective mitigation strategies.

2.2 Mapping Accounting Processes to Spot Vulnerabilities

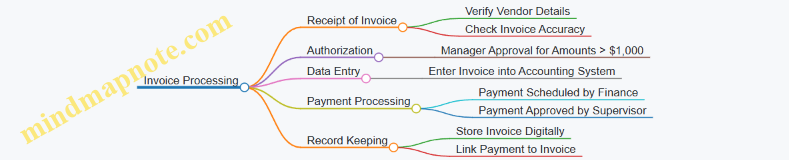

Mapping accounting processes is a critical step in identifying vulnerabilities that could lead to errors, fraud, or inefficiencies. By visually breaking down each step of an accounting workflow, accountants and risk managers can pinpoint weak spots where controls may be lacking or risks may be higher.

What is Process Mapping?

Process mapping is the creation of a visual diagram that outlines the sequence of activities, decision points, inputs, and outputs within a specific accounting process. It helps in understanding how tasks flow, who is responsible, and where potential risks might arise.

Why Map Accounting Processes?

- Identify bottlenecks and inefficiencies

- Spot control gaps and vulnerabilities

- Clarify roles and responsibilities

- Facilitate communication among teams

- Support compliance and audit readiness

Common Accounting Processes to Map

- Accounts Payable

- Accounts Receivable

- Payroll Processing

- General Ledger Closing

- Fixed Asset Management

Example Mind Map: Accounts Payable Process

Identifying Vulnerabilities in the Accounts Payable Process

| Step | Potential Vulnerabilities | Example Scenario |

|---|---|---|

| Invoice Receipt | Fake or duplicate invoices | Duplicate invoice submitted to get double payment |

| Invoice Validation | Incorrect matching or overlooked discrepancies | Invoice amount does not match purchase order but is paid anyway |

| Approval Workflow | Lack of segregation of duties | Same person submits and approves invoices |

| Payment Processing | Unauthorized payments | Payment made to a vendor not on approved list |

| Record Keeping | Missing or incomplete documentation | Invoices not properly archived, causing audit issues |

Example Mind Map: Payroll Processing

Spotting Vulnerabilities in Payroll Processing

| Step | Potential Vulnerabilities | Example Scenario |

|---|---|---|

| Employee Time Tracking | Falsified hours or buddy punching | Employee submits inflated hours; no verification |

| Payroll Calculation | Incorrect deductions or miscalculations | Tax rates not updated, leading to compliance risk |

| Approval and Verification | Lack of independent review | Payroll processed without manager approval |

| Payment Disbursement | Payments to terminated employees | Payments continue after employee leaves |

| Reporting and Compliance | Late or inaccurate tax filings | Penalties due to late submission of payroll taxes |

Best Practices for Mapping and Vulnerability Spotting

- Engage Cross-Functional Teams: Include personnel from accounting, finance, operations, and IT to get a comprehensive view.

- Use Standardized Symbols: Flowcharts, swimlane diagrams, or mind maps help maintain clarity.

- Document Roles and Responsibilities: Clearly identify who performs each step to detect segregation of duties issues.

- Incorporate Control Points: Mark where controls exist and evaluate their effectiveness.

- Review and Update Regularly: Processes evolve; keep maps current to reflect changes.

Practical Example: Mapping the General Ledger Closing Process

Vulnerabilities:

- Missing or late journal entries causing inaccurate financials

- Reconciliations not performed or reviewed

- Adjusting entries made without proper documentation

- Lack of timely approvals delaying closing

By mapping this process, accountants can identify where controls such as reconciliation checklists or approval workflows need strengthening.

Summary

Mapping accounting processes with detailed mind maps and flowcharts enables accountants and risk managers to visualize workflows, identify vulnerabilities, and implement targeted controls. Using real-world examples like accounts payable and payroll processing helps illustrate common risk points and how to address them effectively.

2.3 Practical Example: Identifying Risks in Accounts Payable and Receivable

In the accounting function, Accounts Payable (AP) and Accounts Receivable (AR) are critical processes that directly impact cash flow, financial accuracy, and operational efficiency. Identifying risks in these areas is essential to prevent financial loss, fraud, and compliance issues.

Understanding Accounts Payable Risks

Accounts Payable involves managing outgoing payments to suppliers and vendors. Common risks include duplicate payments, unauthorized payments, late payments leading to penalties, and fraud.

Mind Map: Risks in Accounts Payable

Example 1: Duplicate Payment Risk

A company processes an invoice twice due to poor invoice tracking. This results in overpayment, affecting cash flow.

Mitigation: Implement a centralized invoice tracking system with automated duplicate detection.

Understanding Accounts Receivable Risks

Accounts Receivable involves managing incoming payments from customers. Risks include delayed payments, bad debts, misapplied payments, and revenue recognition errors.

Mind Map: Risks in Accounts Receivable

Example 2: Delayed Payment Risk

A customer delays payment beyond agreed terms, causing cash flow strain.

Mitigation: Establish clear credit policies and use aging reports to monitor overdue accounts.

Step-by-Step Risk Identification in AP and AR

- Process Mapping: Document each step in AP and AR workflows to spot potential risk points.

- Stakeholder Interviews: Engage with AP/AR staff to uncover practical challenges and risk areas.

- Data Analysis: Review historical payment data for anomalies like duplicates or late payments.

- Control Review: Assess existing controls such as approval workflows and reconciliations.

Mind Map: Risk Identification Process

Integrated Example: Identifying Risks in a Mid-Sized Company’s AP Process

- Scenario: The company noticed occasional late payments and occasional vendor complaints.

- Risk Identification:

- Process mapping revealed manual invoice entry prone to errors.

- Interviews uncovered lack of segregation of duties; the same person enters and approves invoices.

- Data analysis found several duplicate payments over the last quarter.

- Control review showed no automated matching between purchase orders and invoices.

Outcome: The company prioritized implementing an automated AP system with three-way matching and segregated duties to mitigate these risks.

Summary

Identifying risks in Accounts Payable and Receivable requires a structured approach combining process analysis, stakeholder input, and data review. By mapping out risks such as duplicate payments, fraud, delayed collections, and compliance issues, accountants can design targeted controls that protect the organization’s financial health.

For further reading, consider exploring tools like risk registers and automated analytics platforms that enhance risk identification in AP and AR.

2.4 Using Data Analytics to Detect Anomalies and Potential Risks

Data analytics has become an indispensable tool for accountants aiming to enhance risk management by identifying anomalies and potential risks early in the accounting processes. By leveraging data analytics, accountants can sift through large volumes of financial data to detect patterns, outliers, and irregularities that may indicate errors, fraud, or operational inefficiencies.

Why Use Data Analytics in Risk Detection?

- Volume Handling: Ability to analyze thousands of transactions quickly.

- Pattern Recognition: Identifies unusual trends that manual reviews may miss.

- Proactive Risk Management: Enables early detection and mitigation.

Key Techniques in Data Analytics for Risk Detection

- Descriptive Analytics: Summarizes historical data to understand what happened.

- Diagnostic Analytics: Investigates why something happened.

- Predictive Analytics: Forecasts future risks based on patterns.

- Prescriptive Analytics: Suggests actions to mitigate identified risks.

Mind Map: Data Analytics Techniques for Risk Detection

Practical Example 1: Detecting Duplicate Payments in Accounts Payable

Scenario: An accounting team suspects duplicate payments are being made to vendors.

Approach:

- Use data analytics software to scan payment records.

- Identify duplicate invoice numbers, amounts, or vendor names.

- Flag transactions with identical or near-identical attributes.

Outcome:

- Discovery of several duplicate payments totaling $15,000.

- Implementation of automated duplicate detection rules.

Practical Example 2: Anomaly Detection in Expense Reports

Scenario: Expense reports occasionally contain outlier amounts that may indicate policy violations.

Approach:

- Analyze historical expense data to establish normal spending patterns.

- Use statistical methods (e.g., Z-score) to detect outliers.

- Review flagged reports for potential misuse or errors.

Outcome:

- Identification of unusually high travel expenses submitted by a few employees.

- Reinforcement of expense policies and additional training.

Mind Map: Steps to Implement Data Analytics for Risk Detection

Best Practices for Accountants Using Data Analytics

- Start Small: Begin with high-risk areas such as cash transactions or vendor payments.

- Use Visualization: Tools like dashboards and heat maps make anomalies easier to spot.

- Collaborate with IT: Ensure proper data access and security.

- Regularly Update Models: Anomaly detection models should evolve with new data.

- Document Findings: Maintain records of detected risks and remediation steps.

Practical Example 3: Continuous Monitoring of Revenue Recognition

Scenario: A company wants to ensure revenue is recognized accurately and timely.

Approach:

- Use data analytics to monitor revenue transactions daily.

- Detect unusual spikes or drops compared to historical trends.

- Flag transactions that deviate from contract terms.

Outcome:

- Early identification of a revenue recognition error due to system misconfiguration.

- Prompt correction avoided potential financial misstatement.

Summary

Data analytics empowers accountants to move from reactive to proactive risk management by detecting anomalies and potential risks efficiently. By integrating these techniques into daily accounting workflows, organizations can safeguard financial integrity and enhance compliance.

Additional Resources

- Introduction to Data Analytics for Accountants (Online Course)

- Tools: ACL Analytics, IDEA, Power BI, Tableau

- Articles on Anomaly Detection Techniques in Finance

2.5 Best Practice: Establishing a Risk Register for Accounting Teams

A risk register is an essential tool for accountants to systematically identify, document, and manage risks within their processes. It acts as a centralized repository that helps teams track risks, assess their impact, assign ownership, and monitor mitigation efforts.

What is a Risk Register?

A risk register is a structured document or database that records all identified risks, their characteristics, and the actions taken to manage them. For accounting teams, it ensures transparency and accountability in managing financial, operational, compliance, and fraud risks.

Why Establish a Risk Register?

- Centralized Risk Tracking: Consolidates all risks in one place.

- Prioritization: Helps prioritize risks based on likelihood and impact.

- Accountability: Assigns risk owners responsible for mitigation.

- Monitoring: Tracks progress on risk mitigation activities.

- Audit Trail: Provides documentation for internal and external audits.

Key Components of a Risk Register for Accounting Teams

| Component | Description |

|---|---|

| Risk ID | Unique identifier for each risk |

| Risk Description | Clear and concise description of the risk |

| Risk Category | Classification (e.g., Financial, Operational, Compliance, Fraud) |

| Likelihood | Probability of the risk occurring (e.g., Low, Medium, High) |

| Impact | Potential effect on the organization (e.g., Low, Medium, High) |

| Risk Score | Combined score based on likelihood and impact |

| Risk Owner | Person responsible for managing the risk |

| Mitigation Actions | Steps planned or taken to reduce the risk |

| Status | Current status (e.g., Open, In Progress, Closed) |

| Review Date | Next scheduled date to review the risk |

Mind Map: Components of a Risk Register

Example: Sample Risk Register Entries for an Accounting Team

| Risk ID | Risk Description | Category | Likelihood | Impact | Risk Score | Risk Owner | Mitigation Actions | Status | Review Date |

|---|---|---|---|---|---|---|---|---|---|

| R001 | Incorrect revenue recognition | Financial | Medium | High | 8 | Senior Accountant | Implement monthly revenue review and reconciliation | In Progress | 2024-07-01 |

| R002 | Unauthorized access to accounting system | Operational | Low | High | 6 | IT Manager | Enforce multi-factor authentication and regular access audits | Open | 2024-06-15 |

| R003 | Non-compliance with new tax regulations | Compliance | High | Medium | 9 | Tax Specialist | Conduct quarterly training and update tax software | In Progress | 2024-06-30 |

| R004 | Payroll fraud | Fraud | Low | High | 6 | HR Manager | Segregate payroll duties and implement whistleblower policy | Open | 2024-07-10 |

Mind Map: Example Risk Register Entry Breakdown

Steps to Establish a Risk Register in Your Accounting Team

- Assemble a Cross-Functional Team: Include accountants, auditors, compliance officers, and IT personnel.

- Identify Risks: Use brainstorming sessions, process reviews, and historical data.

- Document Risks: Capture all relevant details in the risk register template.

- Assess Risks: Evaluate likelihood and impact to prioritize.

- Assign Risk Owners: Designate responsible individuals for each risk.

- Develop Mitigation Plans: Define clear actions to reduce risk exposure.

- Monitor and Update: Regularly review the register and update statuses.

Practical Example: Creating a Risk Register for Accounts Payable

- Risk Identification: Duplicate payments, late payments, invoice fraud.

- Risk Documentation: Each risk is entered with descriptions and categories.

- Assessment: Duplicate payments (Medium likelihood, Medium impact), late payments (High likelihood, Low impact).

- Ownership: Assign to Accounts Payable Manager.

- Mitigation: Implement invoice matching software, establish approval workflows.

Mind Map: Risk Register Process Flow

Tips for Maintaining an Effective Risk Register

- Keep it simple and user-friendly to encourage regular updates.

- Use visual dashboards to highlight high-priority risks.

- Integrate with existing accounting and audit software for automation.

- Schedule periodic reviews aligned with financial reporting cycles.

- Encourage a culture of open communication about risks.

By establishing and maintaining a comprehensive risk register, accounting teams can proactively manage risks, improve internal controls, and contribute to the overall financial health and compliance of the organization.

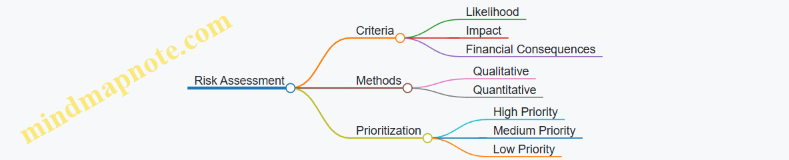

3. Risk Assessment and Prioritization

3.1 Qualitative vs Quantitative Risk Assessment Methods

Risk assessment is a critical step in the risk management process for accountants. It involves evaluating identified risks to understand their potential impact and likelihood, enabling prioritization and effective mitigation. There are two primary approaches to risk assessment: qualitative and quantitative. Both methods have unique advantages and are often used complementarily.

Qualitative Risk Assessment

Qualitative risk assessment focuses on descriptive analysis rather than numerical data. It uses subjective judgment, expert opinions, and categorization to evaluate risks.

Key Characteristics:

- Uses categories such as High, Medium, Low for likelihood and impact

- Relies on expert judgment and experience

- Easier and faster to perform

- Useful when precise data is unavailable

Common Techniques:

- Risk Matrix

- Risk Ranking

- SWOT Analysis

- Delphi Method

Example in Accounting: An accounting team identifies the risk of revenue recognition errors. Using qualitative assessment, they categorize the likelihood as “Medium” due to recent process changes and the impact as “High” because errors could lead to misstated financial statements and regulatory penalties.

Mind Map: Qualitative Risk Assessment

Quantitative Risk Assessment

Quantitative risk assessment uses numerical data and statistical models to estimate risk levels. It provides measurable and objective evaluations.

Key Characteristics:

- Uses numerical values for likelihood and impact

- Employs statistical, mathematical, or financial models

- More precise but requires reliable data

- Time-consuming and resource-intensive

Common Techniques:

- Monte Carlo Simulation

- Sensitivity Analysis

- Expected Monetary Value (EMV) Analysis

- Value at Risk (VaR)

Example in Accounting: To assess the risk of cash flow shortfalls, an accountant uses Monte Carlo simulation to model various scenarios of receivables collection delays. The simulation estimates a 15% probability that cash flow will drop below a critical threshold in the next quarter.

Mind Map: Quantitative Risk Assessment

Comparative Overview

| Aspect | Qualitative Assessment | Quantitative Assessment |

|---|---|---|

| Data Requirement | Low (expert judgment) | High (historical and statistical data) |

| Precision | Descriptive, categorical | Numerical, measurable |

| Time and Cost | Low | High |

| Use Case | Initial screening, when data is limited | Detailed analysis, when data is available |

| Example | Risk of invoice fraud categorized as High | Probability of cash flow shortfall: 15% |

Integrated Example: Assessing Risk of Accounts Payable Fraud

-

Qualitative Step:

- The accounting team holds a brainstorming session.

- They identify accounts payable fraud as a “High” impact risk with “Medium” likelihood due to recent staff turnover.

-

Quantitative Step:

- Using historical data, they analyze past fraud incidents.

- Applying EMV analysis, they estimate an average potential loss of $50,000 with a 10% probability annually.

-

Outcome:

- The combined approach helps prioritize fraud risk mitigation efforts and allocate resources effectively.

Mind Map: Integrated Risk Assessment Example

Best Practices for Accountants

- Use qualitative methods for initial risk identification and prioritization.

- Apply quantitative methods when sufficient data exists for precise analysis.

- Combine both approaches for a comprehensive risk assessment.

- Document assumptions and data sources clearly.

- Regularly update assessments to reflect changes in processes or environment.

By understanding and applying both qualitative and quantitative risk assessment methods, accountants can better identify, evaluate, and manage risks, ultimately safeguarding financial integrity and compliance.

3.2 Risk Scoring Models Tailored for Accounting Functions

Risk scoring models are essential tools that help accountants quantify and prioritize risks based on their likelihood and potential impact. Tailoring these models specifically for accounting functions ensures that the unique risks inherent in financial processes are accurately assessed and managed.

What is a Risk Scoring Model?

A risk scoring model assigns numerical values to various risk factors, allowing organizations to rank risks objectively. This helps in focusing resources on the most critical risks.

Key Components of Risk Scoring Models for Accounting:

- Likelihood (Probability): How likely is the risk event to occur?

- Impact (Severity): What is the potential financial or reputational damage?

- Detection Difficulty: How easy is it to detect the risk before it causes harm?

Mind Map: Core Elements of Risk Scoring in Accounting

Example: Risk Scoring Matrix for Revenue Recognition Errors

| Risk Factor | Score (1-5) | Description |

|---|---|---|

| Likelihood | 3 | Errors occur occasionally due to manual entries |

| Impact | 5 | Misstatements can lead to significant financial restatements |

| Detection Difficulty | 4 | Errors are often detected late in the audit process |

Total Risk Score = Likelihood x Impact x Detection Difficulty = 3 x 5 x 4 = 60

This score helps prioritize this risk over others with lower scores.

Mind Map: Steps to Build a Risk Scoring Model for Accounting

Tailoring Risk Scoring Models to Specific Accounting Functions

- Accounts Payable/Receivable: Focus on fraud risk, payment errors, and timing delays.

- Payroll: Emphasize unauthorized payments, compliance with tax laws.

- Financial Reporting: Concentrate on misstatements, compliance with accounting standards.

- Tax Accounting: Highlight risks from regulatory changes and filing errors.

Practical Example: Scoring Risk in Payroll Processing

| Risk Factor | Score (1-5) | Explanation |

|---|---|---|

| Likelihood | 2 | Payroll errors are rare due to automation |

| Impact | 4 | Errors can cause regulatory fines and employee dissatisfaction |

| Detection Difficulty | 3 | Some errors detected only during audits |

Total Risk Score = 2 x 4 x 3 = 24

This lower score compared to revenue recognition errors indicates a relatively lower priority.

Mind Map: Example Risk Scoring for Different Accounting Risks

Best Practices for Implementing Risk Scoring Models in Accounting

- Use Historical Data: Leverage past incidents and audit findings to inform likelihood and impact scores.

- Engage Experts: Include accountants, auditors, and risk managers in scoring to ensure accuracy.

- Customize Scales: Adapt scoring scales to reflect the organization’s risk appetite and industry standards.

- Regular Updates: Risk environments change; update scores periodically.

- Integrate with Risk Registers: Use scoring results to populate and prioritize entries in risk registers.

Summary

Risk scoring models tailored for accounting functions provide a structured, quantitative approach to evaluating risks. By combining likelihood, impact, and detection difficulty, accountants can prioritize risks effectively, allocate resources wisely, and strengthen internal controls.

For further reading, consider exploring tools like COSO ERM frameworks and ISO 31000 guidelines, which provide foundational principles for risk scoring and management.

3.3 Example: Assessing the Impact of Revenue Recognition Errors

Revenue recognition is a critical accounting process that directly affects financial statements and business decisions. Errors in revenue recognition can lead to misstated earnings, regulatory penalties, and loss of stakeholder trust. This section explores how to assess the impact of revenue recognition errors using practical examples and mind maps to visualize the process.

Understanding Revenue Recognition Errors

Revenue recognition errors occur when revenue is recorded in the wrong period, amount, or not in accordance with applicable accounting standards (e.g., IFRS 15 or ASC 606). Common causes include:

- Premature recognition of revenue before delivery or performance obligations are met.

- Delayed recognition causing understatement of income.

- Incorrect measurement of revenue due to pricing or contract terms misunderstanding.

Mind Map: Causes and Consequences of Revenue Recognition Errors

Step-by-Step Assessment of Impact

-

Identify the Error

- Example: A software company recognizes full revenue upon contract signing instead of over the service period.

-

Quantify the Error

- Calculate the amount of revenue recognized prematurely.

- Example: $1,200,000 recognized upfront instead of $100,000 monthly over 12 months.

-

Evaluate Financial Statement Impact

- Overstated revenue and net income in the current period.

- Understated revenue in future periods.

-

Assess Compliance and Regulatory Risks

- Potential violation of revenue recognition standards.

- Risk of audit adjustments or fines.

-

Consider Stakeholder Impact

- Investors may make decisions based on inflated earnings.

- Creditors may assess creditworthiness inaccurately.

-

Determine Corrective Actions

- Restate financial statements.

- Implement stronger internal controls.

Mind Map: Assessment Workflow for Revenue Recognition Errors

Practical Example: SaaS Company Revenue Recognition Error

Scenario: A SaaS company signs a 1-year contract for $120,000 but recognizes the entire amount as revenue immediately upon signing.

Assessment:

- Error: Premature revenue recognition.

- Quantification: $120,000 recognized upfront instead of $10,000 per month.

- Financial Impact: Current year revenue overstated by $120,000; next 11 months understated.

- Compliance Risk: Violates ASC 606 which requires revenue recognition over time as services are delivered.

- Stakeholder Impact: Investors see inflated earnings, leading to potential mispricing of stock.

Corrective Action:

- Adjust revenue recognition to a monthly basis.

- Restate financials if prior periods are affected.

- Train accounting staff on revenue recognition policies.

Example Table: Impact Analysis of Revenue Recognition Error

| Aspect | Before Correction | After Correction | Impact Description |

|---|---|---|---|

| Revenue Recognized | $120,000 upfront | $10,000 per month | Overstatement in current period |

| Net Income | Inflated by $120,000 | Adjusted to reflect actual | Earnings misrepresented |

| Compliance Status | Non-compliant with ASC 606 | Compliant | Risk of regulatory penalties reduced |

| Stakeholder Trust | Potentially damaged | Restored with transparency | Investor confidence maintained |

Best Practice Tips for Accountants

- Regularly review contracts and revenue recognition policies.

- Use automated systems to allocate revenue over time.

- Conduct periodic training on updated accounting standards.

- Implement internal audit procedures focused on revenue accounts.

- Maintain a detailed risk register to track revenue recognition risks.

By systematically assessing revenue recognition errors through identification, quantification, and impact evaluation, accountants can mitigate risks effectively and ensure accurate financial reporting.

3.4 Prioritizing Risks Based on Likelihood and Impact

Prioritizing risks is a critical step in the risk management process for accountants. It helps focus limited resources on the most significant risks that could affect financial reporting, compliance, or operational efficiency. This section will guide you through how to prioritize risks by evaluating their likelihood and impact, supported by practical examples and mind maps to visualize the process.

Understanding Likelihood and Impact

- Likelihood refers to the probability that a risk event will occur.

- Impact refers to the severity of the consequences if the risk event occurs.

Both dimensions are usually assessed qualitatively (e.g., low, medium, high) or quantitatively (e.g., probability percentages, monetary loss).

Step 1: Define Scales for Likelihood and Impact

| Scale | Likelihood Description | Impact Description |

|---|---|---|

| Low | Rare or unlikely to occur | Minor financial or operational effect |

| Medium | Possible or occasional occurrence | Moderate effect, manageable with controls |

| High | Likely or frequent occurrence | Significant effect, could threaten objectives |

Step 2: Create a Risk Matrix

A risk matrix helps visualize and prioritize risks by plotting likelihood against impact.

Risk Prioritization Matrix

| Impact \ Likelihood | Low | Medium | High |

|---|---|---|---|

| High | Medium Priority | High Priority | Critical Risk |

| Medium | Low Priority | Medium Priority | High Priority |

| Low | Low Priority | Low Priority | Medium Priority |

Mind Map: Prioritizing Risks Based on Likelihood and Impact

Step 3: Assign Risks to the Matrix

Example: Consider three risks identified in an accounting department:

-

Risk A: Revenue Recognition Error

- Likelihood: Medium (errors occur occasionally)

- Impact: High (could lead to material misstatement)

-

Risk B: Payroll Fraud

- Likelihood: Low (strong controls in place)

- Impact: Medium (financial loss but limited scope)

-

Risk C: Late Tax Filing

- Likelihood: High (tight deadlines and manual processes)

- Impact: Medium (penalties and interest)

Plotting these on the matrix:

| Risk | Likelihood | Impact | Priority |

|---|---|---|---|

| Revenue Recognition | Medium | High | High Priority |

| Payroll Fraud | Low | Medium | Low Priority |

| Late Tax Filing | High | Medium | High Priority |

Mind Map: Example Risk Prioritization

Step 4: Prioritize and Plan Responses

- Critical and High Priority Risks: Require immediate mitigation plans, such as enhanced controls, automation, or additional reviews.

- Medium Priority Risks: Should be monitored regularly and controlled through standard procedures.

- Low Priority Risks: May be accepted but reviewed periodically to ensure they do not escalate.

Practical Example: Prioritizing Risks in Accounts Payable

-

Risk: Duplicate payments

- Likelihood: Medium (manual invoice entry)

- Impact: Medium (financial loss and reconciliation issues)

- Priority: Medium

-

Risk: Unauthorized vendor setup

- Likelihood: Low (vendor onboarding controls)

- Impact: High (fraud risk)

- Priority: High

-

Risk: Late payment penalties

- Likelihood: High (complex approval workflows)

- Impact: Low (small penalties)

- Priority: Medium

This prioritization helps the accounting team focus on tightening vendor setup controls first, then improving invoice processing automation.

Summary

Prioritizing risks based on likelihood and impact enables accountants to allocate resources effectively and address the most critical risks first. Using tools like risk matrices and mind maps simplifies the visualization and communication of risk priorities.

For further reading, consider exploring risk scoring models and software tools that automate risk prioritization tailored to accounting functions.

3.5 Best Practice: Engaging Cross-Functional Teams for Comprehensive Risk Assessment

Engaging cross-functional teams in risk assessment is a best practice that significantly enhances the depth, accuracy, and effectiveness of identifying and prioritizing risks within accounting functions. By involving professionals from different departments and expertise areas, accountants can gain diverse perspectives, uncover hidden risks, and develop more robust mitigation strategies.

Why Engage Cross-Functional Teams?

- Diverse Perspectives: Different departments (e.g., finance, IT, compliance, operations) have unique insights into potential risks.

- Holistic Risk Identification: Risks often span multiple functions; collaboration ensures no risk is overlooked.

- Improved Communication: Facilitates better understanding and alignment across the organization.

- Enhanced Buy-in: Stakeholders are more likely to support risk mitigation efforts if involved early.

How to Engage Cross-Functional Teams Effectively

- Identify Relevant Stakeholders: Include representatives from accounting, internal audit, IT, legal, compliance, operations, and management.

- Define Clear Objectives: Clarify the scope and goals of the risk assessment.

- Facilitate Structured Workshops: Use guided sessions to brainstorm and evaluate risks collaboratively.

- Leverage Collaborative Tools: Utilize shared documents, risk registers, and mind maps.

- Assign Roles and Responsibilities: Ensure accountability for follow-up actions.

Example: Cross-Functional Risk Assessment Workshop

A mid-sized insurance company organized a risk assessment workshop involving the accounting team, IT security, compliance officers, and operations managers to evaluate risks in the monthly financial closing process.

- Outcome: IT highlighted system downtime risks, compliance flagged regulatory reporting deadlines, operations identified data entry bottlenecks, and accountants focused on reconciliation errors.

- Result: The team developed a prioritized risk register and agreed on mitigation steps such as system upgrades, compliance calendar integration, and process automation.

Mind Map: Cross-Functional Risk Assessment Process

Mind Map: Benefits of Cross-Functional Engagement

Practical Tips for Accountants

- Invite IT Early: Technology risks are often underestimated; IT can provide insights on system vulnerabilities.

- Include Compliance: Regulatory risks impact financial reporting and must be integrated.

- Use Visual Tools: Mind maps and flowcharts help clarify complex processes and risks.

- Document Discussions: Keep detailed notes to track risk evolution and decisions.

- Follow Up: Schedule periodic reviews to update risk assessments and monitor mitigation progress.

Additional Example: Fraud Risk Assessment

In a financial services firm, accountants collaborated with the internal audit and HR teams to assess fraud risks related to expense reimbursements.

- Cross-Functional Insights: HR provided data on employee behavior patterns, audit shared past fraud incidents, and accounting reviewed reimbursement processes.

- Outcome: The team identified gaps in approval workflows and implemented dual-approval controls, reducing fraud risk by 40% within six months.

Engaging cross-functional teams transforms risk assessment from a siloed activity into a dynamic, organization-wide effort, enabling accountants to manage risks more comprehensively and effectively.

4. Risk Mitigation Strategies for Accountants

4.1 Internal Controls: Designing and Implementing Effective Controls

Internal controls are the backbone of risk mitigation in accounting. They are processes, policies, and procedures designed to ensure the integrity of financial and accounting information, promote accountability, and prevent fraud. Effective internal controls help accountants reduce errors, detect irregularities early, and comply with regulations.

What Are Internal Controls?

Internal controls can be broadly categorized into three types:

- Preventive Controls: Designed to stop errors or fraud before they occur.

- Detective Controls: Identify and detect errors or irregularities after they have occurred.

- Corrective Controls: Actions taken to correct errors or issues once detected.

Mind Map: Types of Internal Controls

Designing Effective Internal Controls

When designing internal controls, accountants should consider the following principles:

- Segregation of Duties (SoD): No single individual should control all aspects of a financial transaction.

- Authorization and Approval: Transactions should be authorized by appropriate personnel.

- Documentation and Record Keeping: Maintain clear, complete, and accurate records.

- Physical Controls: Safeguard assets through locks, passwords, or restricted access.

- Independent Checks and Reconciliations: Regular reviews and reconciliations to detect discrepancies.

Mind Map: Principles of Designing Internal Controls

Example: Segregation of Duties in Accounts Payable

Scenario: In a mid-sized company, the accountant responsible for processing payments also approves vendor invoices and reconciles bank statements.

Risk: This concentration of duties increases the risk of fraudulent payments or undetected errors.

Control Implementation:

- Assign invoice approval to the purchasing manager.

- Assign payment processing to the accounts payable clerk.

- Assign bank statement reconciliation to an independent finance team member.

This segregation ensures no single person has control over the entire payment cycle, reducing fraud risk.

Implementing Internal Controls: Step-by-Step

- Risk Assessment: Identify key risk areas in accounting processes.

- Control Design: Develop controls tailored to mitigate identified risks.

- Documentation: Document control procedures clearly.

- Training: Educate staff on control importance and execution.

- Monitoring: Regularly review and test controls for effectiveness.

- Continuous Improvement: Update controls based on audit findings and process changes.

Mind Map: Implementing Internal Controls

Example: Authorization Controls in Expense Management

Scenario: Employees submit expense reports without manager approval.

Risk: Unauthorized or fraudulent expenses may be reimbursed.

Control Implementation:

- Require all expense reports to be approved by the employee’s direct manager before processing.

- Use an automated workflow system that blocks reimbursement until approval is logged.

This control prevents unauthorized spending and ensures accountability.

Best Practice: Use Technology to Strengthen Controls

Modern accounting software often includes built-in controls such as:

- Role-based access controls to restrict system functions.

- Automated approval workflows.

- Audit trails that log all changes and transactions.

Example: Implementing an ERP system with configurable user roles ensures that only authorized personnel can approve payments or modify financial data.

Summary

Designing and implementing effective internal controls is essential for accountants to manage risks, prevent fraud, and ensure accurate financial reporting. By applying principles like segregation of duties, authorization, documentation, and continuous monitoring — supported by real-world examples and technology — accounting teams can build a robust control environment that safeguards organizational assets and enhances trust.

For further reading, explore frameworks such as COSO Internal Control – Integrated Framework and ISO 31000 Risk Management.

4.2 Example: Segregation of Duties to Prevent Fraud

Segregation of Duties (SoD) is a fundamental internal control designed to reduce the risk of errors and fraud by ensuring that no single individual has control over all aspects of any critical financial transaction. For accountants, implementing SoD is crucial to maintaining integrity and transparency within financial processes.

What is Segregation of Duties?

Segregation of Duties means dividing responsibilities among different people to reduce the risk of error or inappropriate actions. It typically involves separating the following functions:

- Authorization

- Custody of assets

- Record keeping

- Reconciliation

Why is Segregation of Duties Important?

- Prevents fraud by limiting opportunities for manipulation

- Detects errors early by involving multiple parties

- Enhances accountability and transparency

Mind Map: Core Components of Segregation of Duties

Practical Example: Accounts Payable Process

Consider the accounts payable (AP) process, a common area vulnerable to fraud if duties are not segregated.

| Function | Role 1: Invoice Processing | Role 2: Payment Authorization | Role 3: Payment Execution | Role 4: Reconciliation |

|---|---|---|---|---|

| Receive Invoice | Yes | No | No | No |

| Verify Invoice | Yes | No | No | No |

| Approve Payment | No | Yes | No | No |

| Issue Payment | No | No | Yes | No |

| Reconcile Payments | No | No | No | Yes |

This segregation ensures that no single person can both approve and execute payments, reducing the risk of fraudulent disbursements.

Mind Map: Segregation of Duties in Accounts Payable

Additional Example: Payroll Process

In payroll, segregation of duties might look like this:

- Payroll Preparation: HR or payroll clerk prepares payroll data.

- Payroll Authorization: Manager or finance officer reviews and approves payroll.

- Payroll Disbursement: Treasury or finance team issues payments.

- Payroll Reconciliation: Internal audit or accounting reconciles payroll reports with bank statements.

This separation prevents an individual from creating fictitious employees and issuing unauthorized payments.

Mind Map: Segregation of Duties in Payroll

Best Practices for Implementing Segregation of Duties

- Identify Key Processes: Map out all financial processes and identify critical control points.

- Assign Roles Clearly: Define roles and responsibilities to avoid overlap.

- Use Technology: Employ accounting software with role-based access controls.

- Regularly Review: Conduct periodic audits to ensure SoD is maintained.

- Compensating Controls: When SoD is not feasible (e.g., small teams), implement compensating controls like increased supervision or audit trails.

Example: Using Technology to Enforce SoD

Modern ERP systems allow setting permissions so that users can only perform tasks assigned to their role. For example:

- User A can enter invoices but cannot approve payments.

- User B can approve payments but cannot create invoices.

- User C can run reconciliation reports but cannot modify transactions.

This technological segregation reduces human error and fraud risk.

Summary

Segregation of Duties is a critical control mechanism that helps accountants prevent fraud and errors by dividing responsibilities among multiple individuals. Through practical examples in accounts payable and payroll, and supported by mind maps illustrating key functions, accountants can better understand how to implement SoD effectively within their organizations.

4.3 Automation and Technology as Risk Mitigation Tools

In today’s fast-paced accounting environment, automation and technology play a crucial role in mitigating risks by reducing human error, increasing efficiency, and enhancing control mechanisms. Leveraging these tools allows accountants to focus on higher-value tasks while ensuring accuracy and compliance.

Key Benefits of Automation and Technology in Risk Mitigation

- Error Reduction: Automated calculations and data entry minimize manual mistakes.

- Consistency: Standardized processes ensure uniform application of controls.

- Real-Time Monitoring: Systems can flag anomalies instantly.

- Audit Trail: Automated logs provide transparent records for compliance.

- Efficiency: Faster processing reduces backlog and exposure to operational risks.

Mind Map: Automation and Technology in Risk Mitigation

Practical Examples

Example 1: Robotic Process Automation (RPA) in Accounts Payable

A mid-sized company implemented RPA to handle invoice processing. The bot extracts invoice data using OCR, matches it against purchase orders, and inputs it into the accounting system. This automation reduced data entry errors by 90% and ensured timely payments, mitigating the risk of late fees and supplier dissatisfaction.

Example 2: Continuous Controls Monitoring (CCM) for Expense Approvals

An organization uses CCM software to monitor expense reports in real-time. The system automatically flags expenses exceeding policy limits or duplicate submissions. This proactive approach helped the finance team detect and prevent unauthorized expenses, reducing compliance risk.

Example 3: AI-Powered Fraud Detection in Payroll

A large enterprise deployed AI tools that analyze payroll data patterns to detect anomalies such as ghost employees or unusual overtime claims. The system alerted the risk management team to suspicious entries, enabling early investigation and prevention of potential fraud.

Best Practices for Implementing Automation and Technology

- Start with Risk Assessment: Identify high-risk, repetitive tasks suitable for automation.

- Choose Scalable Solutions: Select tools that can grow with your organization’s needs.

- Integrate Systems: Ensure seamless data flow between accounting, ERP, and risk management platforms.

- Train Staff: Equip your team with skills to manage and interpret automated outputs.

- Regularly Review Controls: Continuously monitor and update automated controls to adapt to changing risks.

Mind Map: Implementation Roadmap for Automation in Risk Mitigation

By thoughtfully integrating automation and technology into accounting processes, organizations can significantly reduce operational and compliance risks. These tools not only improve accuracy and efficiency but also empower accountants and risk managers to proactively identify and address potential issues before they escalate.

4.4 Training and Awareness Programs for Risk Reduction

Effective risk management in accounting relies heavily on the knowledge, vigilance, and proactive behavior of the accounting team. Training and awareness programs are essential tools to equip accountants with the skills and mindset necessary to identify, assess, and mitigate risks before they escalate.

Why Training and Awareness Matter

- Empowers employees to recognize potential risks early.

- Reduces errors and fraud by increasing understanding of internal controls.

- Promotes a risk-aware culture that supports continuous improvement.

- Ensures compliance with regulatory requirements through up-to-date knowledge.

Key Components of Effective Training Programs

- Risk Fundamentals: Basic concepts of risk, types of risks in accounting.

- Internal Controls: How controls mitigate risks, examples of control failures.

- Fraud Awareness: Common fraud schemes, red flags, and reporting mechanisms.

- Regulatory Updates: Changes in laws and standards impacting accounting risks.

- Use of Technology: Tools and software that support risk management.

Mind Map: Components of Training and Awareness Programs

Example: Designing a Fraud Awareness Workshop

Objective: Equip accountants with the ability to detect and prevent payroll fraud.

Agenda:

- Introduction to Payroll Fraud

- Common Payroll Fraud Schemes (e.g., ghost employees, falsified hours)

- Red Flags and Warning Signs

- Case Study: Real-life Payroll Fraud Incident

- Role-playing Exercise: Identifying Fraudulent Activities

- Reporting Procedures and Whistleblower Policies

Outcome: Participants leave with practical knowledge and confidence to identify suspicious activities.

Mind Map: Payroll Fraud Awareness Workshop

Best Practices for Implementing Training Programs

- Regular Scheduling: Conduct sessions quarterly or biannually to keep knowledge fresh.

- Interactive Learning: Use workshops, quizzes, and role-playing to engage participants.

- Tailored Content: Customize training based on specific risks relevant to the accounting team.

- Leverage Technology: Use e-learning platforms and webinars for accessibility.

- Measure Effectiveness: Use feedback surveys and assessments to improve programs.

Example: Continuous Learning Through Microlearning

Microlearning delivers bite-sized training modules focused on specific risk topics, such as “Detecting Expense Report Fraud” or “Understanding SOX Controls.” These short sessions (5-10 minutes) can be delivered via mobile apps or email, allowing accountants to learn on-the-go and retain information better.

Mind Map: Microlearning Approach

Summary

Training and awareness programs are foundational to reducing risks in accounting. By combining structured workshops, interactive sessions, and innovative microlearning techniques, organizations can foster a vigilant, knowledgeable accounting team capable of proactively managing risks. Embedding these programs into the organizational culture ensures sustained risk reduction and compliance.

For accountants and risk managers, investing time and resources into comprehensive training is not just a regulatory checkbox but a strategic imperative to safeguard financial integrity and organizational reputation.

4.5 Best Practice: Continuous Monitoring and Control Testing

Continuous monitoring and control testing are critical components of an effective risk mitigation strategy in accounting. They ensure that internal controls remain effective over time, detect emerging risks early, and provide assurance that processes comply with policies and regulations.

What is Continuous Monitoring?

Continuous monitoring is an ongoing process that involves regularly reviewing and analyzing accounting activities and controls to promptly identify and address risks or control failures.

Why Continuous Monitoring Matters for Accountants

- Detects errors and fraud early

- Ensures compliance with regulatory requirements

- Enhances the reliability of financial reporting

- Supports proactive risk management

Mind Map: Continuous Monitoring in Accounting

What is Control Testing?

Control testing evaluates whether internal controls are designed effectively and operating as intended. It can be performed periodically or continuously depending on the risk profile.

Types of Control Testing

- Design Effectiveness Testing: Verifies if the control is properly designed to mitigate risks.

- Operating Effectiveness Testing: Confirms the control is functioning as intended in practice.

Mind Map: Control Testing Process

Practical Example: Continuous Monitoring and Control Testing in Accounts Payable

Scenario: An accounting team wants to reduce the risk of duplicate payments and fraudulent invoices.

Continuous Monitoring Actions:

- Implement automated software that flags duplicate invoice numbers or vendor details.

- Set up exception reports to review invoices exceeding typical amounts.

- Monitor changes in vendor master data for unauthorized updates.

Control Testing Actions:

- Periodically sample invoices and verify approval signatures.

- Test segregation of duties by reviewing who creates, approves, and pays invoices.

- Confirm reconciliations between purchase orders, invoices, and payments are performed timely.

Outcome: Early detection of anomalies reduces financial loss, and regular testing ensures controls remain effective.

Best Practices for Continuous Monitoring and Control Testing

-

Leverage Technology: Use accounting software with built-in monitoring tools and analytics to automate control checks.

-

Define Clear Metrics: Establish key risk indicators (KRIs) and control performance indicators (CPIs) to measure effectiveness.

-

Schedule Regular Reviews: Set a consistent timetable for control testing based on risk levels.

-

Document Everything: Maintain detailed records of monitoring results and testing procedures for audit trails.

-

Engage Cross-Functional Teams: Collaborate with IT, compliance, and audit teams to enhance monitoring scope.

-

Respond Promptly: Develop protocols to address control failures or risk detections immediately.

Mind Map: Best Practices for Continuous Monitoring and Control Testing

Additional Example: Monitoring Revenue Recognition Controls

Context: Revenue recognition is a high-risk area prone to manipulation.

Continuous Monitoring:

- Automated checks on timing of revenue entries relative to delivery dates.

- Exception reports for unusual revenue spikes or adjustments.

Control Testing:

- Sample contracts reviewed to ensure revenue is recognized per accounting standards.

- Verification that approvals for revenue adjustments are documented.

Result: Strengthened confidence in financial statements and reduced risk of misstatement.

Summary

Continuous monitoring and control testing form a dynamic duo in risk mitigation for accountants. By embedding these practices into daily operations, accounting teams can maintain robust internal controls, quickly identify risks, and uphold the integrity of financial reporting.

Implementing these best practices with real-world examples and leveraging technology will empower accountants to proactively manage risks and support organizational success.

5. Compliance and Regulatory Risk Management

5.1 Understanding Key Regulatory Requirements Affecting Accountants

Accountants operate in an environment heavily influenced by regulatory requirements designed to ensure transparency, accuracy, and ethical financial reporting. Understanding these regulations is crucial to managing compliance risk effectively and avoiding legal penalties or reputational damage.

Major Regulatory Frameworks Impacting Accountants

Below is a mind map illustrating the key regulatory frameworks and their core focus areas:

Financial Reporting Standards

Accountants must prepare financial statements that comply with either IFRS or GAAP, depending on jurisdiction. These standards dictate how financial transactions are recorded and reported.

Example:

A company recognizing revenue prematurely to meet quarterly targets violates GAAP revenue recognition principles, leading to restatements and penalties.

Anti-Money Laundering (AML) Regulations

Accountants often play a role in detecting and reporting suspicious financial activities.

Example:

An accountant notices unusual large cash deposits inconsistent with client business activities. Following AML regulations, they file a Suspicious Activity Report (SAR) to the relevant authority.

Tax Compliance

Accurate tax reporting and timely filing are essential to avoid fines and audits.

Example:

An accountant ensures all deductible expenses are properly documented and reported, minimizing tax liabilities while staying compliant.

Data Protection and Privacy

With increasing digitalization, accountants must safeguard sensitive financial and personal data.

Example:

Implementing encryption and access controls to protect client financial data in compliance with GDPR.

Corporate Governance Regulations

Acts like SOX impose strict internal control requirements to prevent fraud and ensure accurate financial reporting.

Example:

An accountant documents and tests internal controls over financial reporting to comply with SOX Section 404 requirements.

Audit and Assurance Standards

Accountants involved in auditing must adhere to standards ensuring independence, objectivity, and thoroughness.

Example:

Following ISA guidelines, an auditor performs risk assessments and designs audit procedures to detect material misstatements.

Integrated Example: Compliance in Practice

Scenario: An accounting firm is preparing the year-end financial statements for a publicly traded company.

- They ensure revenue recognition aligns with IFRS 15.

- Internal controls are tested and documented per SOX requirements.

- Tax filings are reviewed for accuracy and completeness.

- Client data is handled in compliance with GDPR.