Financial Statement Consolidation

1. Introduction to Financial Statement Consolidation

1.1 Understanding Consolidation: Definition and Importance

Definition of Financial Statement Consolidation: Financial statement consolidation is the process of combining the financial results of a parent company and its subsidiaries into a single set of financial statements. This unified report presents the financial position, performance, and cash flows of the entire corporate group as if it were a single economic entity.

Why is Consolidation Important?

- Provides a holistic view: Enables stakeholders to understand the overall financial health of the group rather than isolated entities.

- Regulatory compliance: Required by accounting standards such as IFRS (International Financial Reporting Standards) and GAAP (Generally Accepted Accounting Principles).

- Investment decisions: Helps investors and creditors assess the group’s consolidated risk and profitability.

- Internal management: Facilitates better decision-making by management through a comprehensive financial overview.

Mind Map: Core Concepts of Financial Statement Consolidation

Example 1: Simple Consolidation Scenario

Scenario:

- Parent Company A owns 100% of Subsidiary B.

- Parent A’s standalone net income: $1,000,000

- Subsidiary B’s standalone net income: $400,000

Without consolidation:

- Investors see two separate reports.

With consolidation:

- Combined net income reported as $1,400,000 (assuming no intercompany eliminations).

This consolidated figure gives a clearer picture of the entire group’s profitability.

Mind Map: Benefits of Consolidation for Stakeholders

Example 2: Importance of Eliminations in Consolidation

Scenario:

- Parent Company X sells inventory worth $100,000 to Subsidiary Y.

- Subsidiary Y has not sold the inventory to external parties by the reporting date.

Without elimination:

- Revenue and expenses are overstated by $100,000 in consolidated statements.

With proper elimination:

- Intercompany sales and purchases are removed to avoid double counting.

This example highlights why consolidation is critical to present accurate financials.

Summary

Financial statement consolidation is essential for presenting a true and fair view of a corporate group’s financial health. It ensures compliance, aids decision-making, and provides transparency to all stakeholders. Understanding its definition and importance lays the foundation for mastering more complex consolidation processes.

1.2 Key Stakeholders: Accountants and Financial Controllers’ Roles

Financial statement consolidation is a complex process that requires collaboration among various stakeholders. Among these, Accountants and Financial Controllers play pivotal roles in ensuring accuracy, compliance, and timely reporting. Understanding their responsibilities helps streamline consolidation and improve financial transparency.

Accountants: The Foundation of Consolidation

Accountants are responsible for the detailed preparation and recording of financial data from individual entities within a corporate group. Their tasks include:

- Data Collection: Gathering trial balances, journal entries, and supporting documents from subsidiaries.

- Reconciliation: Ensuring intercompany transactions and balances are accurately recorded.

- Adjustments: Making necessary consolidation adjustments such as eliminations and currency translations.

- Compliance: Applying relevant accounting standards (IFRS, GAAP) consistently.

Example:

An accountant at Subsidiary A identifies an intercompany sale to Subsidiary B. They record the sale and the corresponding receivable. During consolidation, this transaction must be eliminated to avoid double counting revenue.

Financial Controllers: Oversight and Strategic Management

Financial Controllers oversee the consolidation process, ensuring that the financial statements present a true and fair view. Their responsibilities include:

- Process Coordination: Managing timelines and communication between subsidiaries and the consolidation team.

- Review and Validation: Verifying the accuracy of consolidated figures and adjustments.

- Reporting: Preparing consolidated financial statements and disclosures for management and external stakeholders.

- Risk Management: Identifying and mitigating risks related to consolidation errors or compliance breaches.

Example:

A financial controller reviews the consolidated balance sheet and notices discrepancies in minority interest calculations. They coordinate with the accountants to correct the entries before finalizing the report.

Mind Maps Illustrating Roles and Responsibilities

Mind Map 1: Accountants’ Role in Consolidation

Mind Map 2: Financial Controllers’ Role in Consolidation

Mind Map 3: Collaboration Between Accountants and Financial Controllers

Integrated Example: Month-End Consolidation Cycle

Scenario: A corporate group with three subsidiaries is closing their books for the month.

- Accountants at each subsidiary prepare their financial data, ensuring all intercompany transactions are recorded.

- They submit trial balances to the consolidation team.

- The consolidation accountant performs eliminations and currency translation adjustments.

- Financial Controller reviews the consolidated data, checks for inconsistencies, and requests clarifications.

- After validation, the controller finalizes the consolidated financial statements and presents them to senior management.

This example highlights the continuous interaction and complementary roles of accountants and financial controllers in the consolidation process.

Summary

- Accountants focus on accurate data preparation, adjustments, and compliance.

- Financial Controllers oversee the consolidation process, ensuring accuracy, timeliness, and regulatory adherence.

- Effective consolidation requires strong collaboration between these roles.

- Utilizing clear communication channels and defined responsibilities enhances consolidation efficiency and reliability.

1.3 Overview of Consolidation Standards and Regulations (IFRS, GAAP)

Financial statement consolidation is governed by various accounting standards and regulations designed to ensure transparency, consistency, and comparability across entities. The two primary frameworks that accountants and financial controllers encounter globally are the International Financial Reporting Standards (IFRS) and the Generally Accepted Accounting Principles (GAAP) in the United States.

Key Objectives of Consolidation Standards

- Ensure that the financial position and performance of a group of entities are presented as a single economic entity.

- Eliminate intercompany transactions and balances to avoid double counting.

- Provide clear guidance on when and how to consolidate subsidiaries, associates, and joint ventures.

Mind Map: Consolidation Standards Overview

IFRS Consolidation Standards

IFRS 10 - Consolidated Financial Statements is the cornerstone standard for consolidation under IFRS. It defines “control” as the power to govern the financial and operating policies of an entity to obtain benefits from its activities.

Example:

Company A owns 55% of Company B’s voting shares and has the ability to appoint the majority of the board members. Under IFRS 10, Company A controls Company B and must consolidate its financial statements.

Key Points:

- Control is assessed based on power, exposure to variable returns, and the ability to use power to affect returns.

- Consolidation involves combining assets, liabilities, income, and expenses line by line.

- Non-controlling interests (minority shareholders) are presented separately in equity.

IAS 28 covers accounting for investments in associates and joint ventures using the equity method, which is not full consolidation but a proportional recognition of net assets and profits.

US GAAP Consolidation Standards

Under US GAAP, ASC 810 - Consolidation provides guidance on consolidation, focusing on two main models:

- Voting Interest Model: Similar to IFRS control concept, where majority voting rights lead to consolidation.

- Variable Interest Entity (VIE) Model: Consolidation is required if an entity has a controlling financial interest, even without majority voting rights.

Example:

Company X holds 40% voting rights in Company Y but is the primary beneficiary of Company Y’s variable interests (e.g., guarantees, significant exposure to losses/gains). Under ASC 810, Company X consolidates Company Y despite not having majority voting rights.

Key Points:

- Identification of VIEs is critical.

- Primary beneficiary consolidates the VIE.

- Similar elimination of intercompany balances and transactions.

Mind Map: Control Assessment Comparison (IFRS vs US GAAP)

Practical Example: Applying IFRS 10 vs US GAAP ASC 810

| Scenario | IFRS 10 Consolidation | US GAAP ASC 810 Consolidation |

|---|---|---|

| Majority voting rights (60%) | Consolidate | Consolidate |

| 40% voting rights + primary beneficiary status | Consolidate | Consolidate |

| 40% voting rights, no control | Equity method | Equity method |

Best Practice for Accountants and Financial Controllers

- Understand the control criteria thoroughly: Control definitions differ subtly but importantly between IFRS and US GAAP.

- Document control assessments clearly: Maintain detailed records of judgments made for consolidation decisions.

- Stay updated with standard changes: Both IFRS and US GAAP periodically update consolidation guidance.

- Use examples and case studies: Apply real-world scenarios to test consolidation decisions.

Summary

Understanding the consolidation standards and regulations is fundamental for accurate financial reporting. IFRS 10 and ASC 810 provide comprehensive frameworks but differ in control definitions and consolidation triggers. Accountants and financial controllers must carefully evaluate control, document their assessments, and apply the appropriate consolidation method to ensure compliance and reliable financial statements.

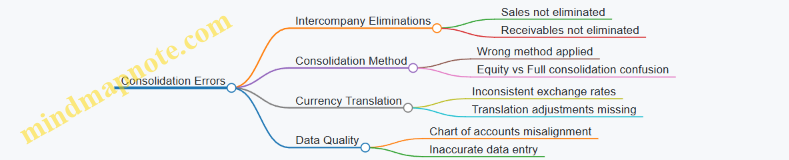

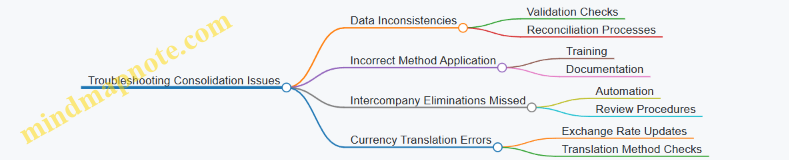

1.4 Common Challenges in Consolidation Processes

Financial statement consolidation is a complex task that involves combining financial data from multiple entities into a single set of financial statements. This process often presents several challenges that accountants and financial controllers must navigate carefully to ensure accuracy and compliance. Below, we explore the most common challenges encountered during consolidation, supported by mind maps and practical examples.

Challenge 1: Data Inconsistency and Quality Issues

One of the primary challenges is dealing with inconsistent or poor-quality data from subsidiaries or affiliated entities. Differences in accounting policies, reporting periods, or data formats can lead to errors or delays.

Mind Map: Data Inconsistency Issues

Example: A parent company consolidates financials from two subsidiaries. Subsidiary A uses straight-line depreciation, while Subsidiary B uses declining balance. Without adjusting these differences, the consolidated depreciation expense will be inaccurate.

Challenge 2: Intercompany Transactions and Eliminations

Intercompany transactions such as sales, loans, or dividends between group entities must be identified and eliminated to avoid double counting.

Mind Map: Intercompany Eliminations

Example: Subsidiary X sells inventory to Subsidiary Y for $100,000. Subsidiary Y still holds $20,000 of this inventory at period-end. The unrealized profit on this inventory must be eliminated from consolidated profit.

Challenge 3: Currency Translation and Exchange Rate Fluctuations

When consolidating foreign subsidiaries, financial statements must be translated into the parent company’s reporting currency. Exchange rate fluctuations can impact reported results.

Mind Map: Currency Translation Challenges

Example: A US parent consolidates a European subsidiary reporting in euros. The euro weakens against the dollar during the reporting period, causing translation losses that affect consolidated equity.

Challenge 4: Complex Group Structures

Groups with multiple layers of subsidiaries, joint ventures, and associates can complicate consolidation.

Mind Map: Complex Group Structures

Example: A parent owns 80% of Subsidiary A, which owns 60% of Subsidiary B. Consolidation requires proper treatment of non-controlling interests and correct elimination of intercompany transactions across multiple levels.

Challenge 5: Timing and Reporting Deadlines

Consolidation often involves tight deadlines, especially during month-end or year-end closing. Delays in receiving subsidiary data can jeopardize timely reporting.

Mind Map: Timing Challenges

Example: A subsidiary submits its financial data late due to system issues. The consolidation team must either delay the entire group reporting or proceed with estimates, risking inaccuracies.

Challenge 6: Regulatory and Compliance Differences

Different jurisdictions may have varying accounting standards and regulatory requirements, complicating consolidation.

Mind Map: Regulatory Challenges

Example: A multinational group consolidates entities reporting under IFRS and local GAAP. Reconciling these differences requires adjustments and thorough documentation to satisfy auditors.

Summary

| Challenge | Key Issue | Practical Example |

|---|---|---|

| Data Inconsistency | Different accounting policies | Depreciation methods vary across subsidiaries |

| Intercompany Eliminations | Double counting | Unrealized profit on intercompany inventory |

| Currency Translation | Exchange rate impact | Translation losses from weakening foreign currency |

| Complex Group Structures | Multi-level ownership and interests | Non-controlling interests in layered subsidiaries |

| Timing and Reporting Deadlines | Late data submission | Delayed subsidiary data affects group reporting |

| Regulatory Differences | Conflicting accounting standards | IFRS vs. local GAAP reconciliation |

By understanding these challenges and applying best practices such as early data validation, clear communication, automation of eliminations, and thorough training, accountants and financial controllers can significantly improve the efficiency and accuracy of the consolidation process.

1.5 Best Practice: Establishing a Consolidation Framework with a Real-World Example

Establishing a robust consolidation framework is a critical first step in ensuring accurate, timely, and compliant financial statement consolidation. This framework acts as the backbone for all consolidation activities, providing structure, clarity, and consistency across the group’s financial reporting.

Why Establish a Consolidation Framework?

- Consistency: Ensures uniform application of accounting policies across subsidiaries.

- Efficiency: Streamlines data collection, validation, and consolidation processes.

- Compliance: Helps meet regulatory requirements (IFRS, GAAP).

- Transparency: Facilitates clear communication between subsidiaries and corporate finance teams.

Key Components of a Consolidation Framework

Consolidation Framework Mind Map

Step-by-Step Process to Establish the Framework

-

Define Governance Structure:

- Assign clear roles for consolidation tasks (e.g., data collection, review, approval).

- Establish a consolidation committee or steering group.

-

Standardize Chart of Accounts:

- Align accounts across subsidiaries to a common structure.

- Example: All subsidiaries use “4000 - Sales Revenue” for sales to avoid confusion.

-

Implement Uniform Accounting Policies:

- Develop a policy manual covering revenue recognition, depreciation, intercompany transactions, etc.

- Example: All entities recognize revenue on delivery date.

-

Select and Configure Consolidation Tools:

- Choose software that supports multi-entity consolidation and eliminations.

- Example: Implementing SAP BPC or Oracle FCCS.

-

Develop Data Collection and Validation Procedures:

- Define timelines and formats for subsidiaries to submit financial data.

- Use automated validation checks to flag inconsistencies.

-

Design Reporting Templates and Timelines:

- Create standardized templates for consolidated financial statements.

- Set deadlines aligned with statutory reporting requirements.

-

Train Staff and Document Processes:

- Conduct workshops for subsidiaries’ finance teams.

- Maintain a consolidation manual accessible to all stakeholders.

Real-World Example: Consolidation Framework at “GlobalTech Inc.”

Background: GlobalTech Inc. is a multinational technology company with 10 subsidiaries across 5 countries. They faced challenges with inconsistent reporting timelines, misaligned charts of accounts, and frequent intercompany reconciliation issues.

Framework Implementation:

-

Governance: Established a central consolidation team with representatives from each subsidiary. Monthly consolidation committee meetings were scheduled.

-

Chart of Accounts Alignment: Rolled out a standardized chart of accounts template. Subsidiaries mapped their local accounts to the global structure.

-

Accounting Policies: Created a comprehensive policy manual. For example, all subsidiaries adopted the policy to eliminate intercompany sales and profits before consolidation.

-

Systems: Deployed Oracle FCCS for consolidation, integrated with subsidiaries’ ERP systems.

-

Data Collection: Introduced a cloud-based portal for subsidiaries to upload trial balances and supporting schedules. Automated validation rules checked for missing data and inconsistencies.

-

Reporting: Developed standardized consolidated financial statement templates with clear disclosure checklists.

-

Training: Conducted quarterly training sessions and maintained an online knowledge base.

Outcome:

- Reduced consolidation closing cycle from 15 days to 7 days.

- Improved accuracy with fewer post-close adjustments.

- Enhanced transparency and audit readiness.

Mind Map: GlobalTech Inc. Consolidation Framework

Summary

Establishing a consolidation framework is foundational for effective financial statement consolidation. By defining governance, standardizing accounts and policies, leveraging technology, and investing in training, organizations can significantly improve the accuracy, efficiency, and compliance of their consolidated financial reporting. The GlobalTech Inc. example illustrates how these best practices translate into tangible business benefits.

Quick Tips

- Start with clear roles and responsibilities.

- Align charts of accounts early.

- Automate data validation to reduce errors.

- Maintain open communication channels across subsidiaries.

- Regularly update policies and training materials.

2. Preparing for Consolidation

2.1 Gathering Financial Data from Subsidiaries and Affiliates

Gathering accurate and timely financial data from subsidiaries and affiliates is the foundational step in the consolidation process. Without reliable data, the consolidated financial statements will be flawed, potentially leading to incorrect business decisions and regulatory non-compliance.

Importance of Data Gathering

- Ensures completeness and accuracy of consolidated financial statements.

- Facilitates timely closing and reporting.

- Supports compliance with accounting standards (IFRS, GAAP).

Key Challenges

- Diverse accounting systems and formats across subsidiaries.

- Different fiscal year-ends.

- Currency differences.

- Data quality and completeness issues.

Mind Map: Components of Financial Data to Gather

Step-by-Step Best Practice for Gathering Data

-

Establish Clear Data Requirements

- Define the exact data needed (trial balances, sub-ledgers, schedules).

- Specify formats and templates to standardize submissions.

-

Set Deadlines and Communication Protocols

- Agree on submission deadlines aligned with consolidation timelines.

- Use centralized communication channels (e.g., collaboration platforms).

-

Use Standardized Templates

- Provide subsidiaries with pre-designed Excel or software templates.

- Example: A trial balance template with mandatory fields and validation rules.

-

Leverage Technology

- Employ consolidation software or ERP modules that allow direct data uploads.

- Example: Subsidiaries upload trial balances directly into a cloud platform.

-

Validate and Reconcile Data

- Perform initial checks for completeness and accuracy.

- Follow up with subsidiaries on discrepancies.

-

Document and Archive

- Keep records of received data and communications for audit trails.

Example: Gathering Data from a Subsidiary Using a Standardized Template

Scenario: A multinational corporation requires its European subsidiary to submit monthly financial data for consolidation.

Process:

- The parent company sends a standardized Excel template with predefined columns: Account Code, Account Description, Debit, Credit, Currency.

- The subsidiary fills in the trial balance and supporting schedules.

- The subsidiary submits the file via a secure cloud portal by the 5th of each month.

- The parent company’s consolidation team runs automated validation checks (e.g., debits equal credits, no missing accounts).

- Any errors trigger an automatic notification to the subsidiary for correction.

Outcome: This process reduces errors, accelerates data collection, and ensures consistency across periods.

Mind Map: Communication Workflow for Data Gathering

Tips for Accountants and Financial Controllers

- Build strong relationships with subsidiary finance teams to encourage cooperation.

- Provide training on the use of templates and data submission tools.

- Implement periodic reviews of the data gathering process to identify bottlenecks.

- Encourage transparency by sharing consolidation timelines and the impact of delays.

Summary

Gathering financial data from subsidiaries and affiliates is a critical, detail-oriented task that requires clear communication, standardized processes, and technology support. By implementing best practices such as standardized templates, defined deadlines, and validation procedures, accountants and financial controllers can ensure the consolidation process starts on a solid foundation, leading to accurate and timely consolidated financial statements.

2.2 Data Validation and Quality Checks: Practical Techniques

Ensuring the accuracy and reliability of financial data before consolidation is critical for producing trustworthy consolidated financial statements. Data validation and quality checks help identify discrepancies, errors, and inconsistencies early in the process, reducing the risk of misstatements and costly restatements.

Importance of Data Validation in Consolidation

- Prevents propagation of errors across consolidated reports.

- Ensures compliance with accounting standards.

- Enhances confidence for stakeholders relying on consolidated financials.

Practical Techniques for Data Validation and Quality Checks

Reconciliation of Trial Balances

- Compare subsidiary trial balances against the consolidated trial balance.

- Identify and investigate any variances.

Cross-Entity Data Consistency Checks

- Verify uniformity in account classifications and balances.

- Check for consistent currency usage and exchange rates.

Intercompany Transaction Validation

- Ensure intercompany sales, purchases, receivables, and payables match between entities.

- Confirm elimination of intercompany balances.

Analytical Review Procedures

- Perform ratio analysis (e.g., gross margin, current ratio) across entities to spot anomalies.

- Compare current period data with prior periods and budgets.

Automated Data Validation Rules

- Set validation rules in consolidation software (e.g., mandatory fields, range limits).

- Use exception reports to highlight data outside expected parameters.

Manual Spot Checks

- Randomly sample transactions or account balances for detailed review.

- Validate supporting documentation.

Mind Map: Data Validation Techniques

Example 1: Intercompany Transaction Validation

Scenario: Subsidiary A reports intercompany sales of $500,000 to Subsidiary B, but Subsidiary B reports intercompany purchases of only $480,000.

Validation Steps:

- Identify the $20,000 discrepancy.

- Investigate invoice records and payment confirmations.

- Correct the data in Subsidiary B’s system to reflect $500,000.

Best Practice: Implement automated matching of intercompany transactions to flag mismatches before consolidation.

Mind Map: Intercompany Transaction Validation Process

Example 2: Automated Validation Rule Implementation

Scenario: A financial controller sets up a rule in the consolidation software that flags any account balance exceeding $1 million without supporting documentation.

Outcome: During consolidation, the system flags a $1.2 million balance in a subsidiary’s account payable.

Action: The controller requests supporting invoices, discovers a data entry error, and corrects the balance to $120,000.

Benefit: Early detection prevents incorrect consolidation and potential audit issues.

Mind Map: Automated Validation Rules

Summary

Data validation and quality checks are foundational to reliable financial statement consolidation. Combining automated tools with manual review techniques ensures data integrity and minimizes errors. Accountants and financial controllers should embed these practices into their consolidation workflows to maintain accuracy and compliance.

Additional Tips

- Maintain a centralized data repository to ease validation.

- Schedule periodic training for staff on validation best practices.

- Document validation procedures for audit trails and continuous improvement.

2.3 Chart of Accounts Alignment Across Entities: Example and Best Practice

Introduction

Aligning the Chart of Accounts (CoA) across multiple entities is a critical step in the financial statement consolidation process. Without a standardized CoA, consolidating financial data becomes cumbersome, error-prone, and time-consuming. This section explores best practices for CoA alignment, supported by practical examples and mind maps to visualize the process.

Why Align the Chart of Accounts?

- Ensures consistency in financial reporting

- Simplifies consolidation and eliminates reconciliation issues

- Facilitates accurate intercompany eliminations

- Enables meaningful comparative analysis across entities

Best Practice Steps for Chart of Accounts Alignment

-

Assess Existing Charts of Accounts

- Collect CoA from all subsidiaries and affiliates

- Identify differences in account codes, naming conventions, and account groupings

-

Define a Standardized Chart of Accounts

- Create a master CoA template reflecting the parent company’s reporting requirements

- Include account codes, descriptions, and grouping hierarchy

-

Map Entity-Specific Accounts to the Master CoA

- Develop a mapping table linking local accounts to the master accounts

- Address any gaps or unique accounts with clear guidelines

-

Implement Consistent Coding and Naming Conventions

- Use uniform account numbering schemes (e.g., 1000 for Assets, 2000 for Liabilities)

- Standardize account names to avoid ambiguity

-

Test and Validate the Alignment

- Perform trial consolidations to verify mapping accuracy

- Adjust mappings based on feedback and discrepancies

-

Maintain and Update the CoA Alignment

- Establish governance for ongoing updates and changes

- Communicate changes promptly across entities

Mind Map: Chart of Accounts Alignment Process

Example: Aligning CoA for Two Entities

Entity A CoA Sample:

| Account Code | Account Name |

|---|---|

| 101 | Cash |

| 201 | Accounts Payable |

| 301 | Sales Revenue |

| 401 | Cost of Goods Sold |

Entity B CoA Sample:

| Account Code | Account Name |

|---|---|

| 1001 | Cash on Hand |

| 2001 | Payables |

| 3001 | Revenue from Sales |

| 4001 | COGS |

Master CoA Template:

| Master Code | Master Account Name |

|---|---|

| 1000 | Cash |

| 2000 | Accounts Payable |

| 3000 | Sales Revenue |

| 4000 | Cost of Goods Sold |

Mapping Table:

| Entity | Local Account Code | Local Account Name | Master Code | Master Account Name |

|---|---|---|---|---|

| A | 101 | Cash | 1000 | Cash |

| A | 201 | Accounts Payable | 2000 | Accounts Payable |

| A | 301 | Sales Revenue | 3000 | Sales Revenue |

| A | 401 | Cost of Goods Sold | 4000 | Cost of Goods Sold |

| B | 1001 | Cash on Hand | 1000 | Cash |

| B | 2001 | Payables | 2000 | Accounts Payable |

| B | 3001 | Revenue from Sales | 3000 | Sales Revenue |

| B | 4001 | COGS | 4000 | Cost of Goods Sold |

Practical Tips

- Use software tools that support CoA mapping and consolidation workflows.

- Engage finance teams from all entities early to ensure buy-in and accuracy.

- Document all mappings and changes thoroughly for audit trails.

Mind Map: Benefits of CoA Alignment

Conclusion

Aligning the Chart of Accounts across entities is foundational for efficient and accurate financial statement consolidation. By following a structured approach, leveraging mapping tables, and standardizing codes and names, accountants and financial controllers can significantly reduce consolidation complexity and improve reporting quality.

2.4 Setting Up Consolidation Software and Tools: Case Study

Setting up consolidation software and tools is a critical step in streamlining the financial statement consolidation process. This section explores a detailed case study illustrating how a mid-sized corporate finance team successfully implemented a consolidation software solution, highlighting best practices, challenges, and practical examples.

Case Study Overview: ABC Corporation

ABC Corporation is a mid-sized enterprise with 5 subsidiaries operating across different regions. The finance team faced challenges with manual consolidation, including data inconsistencies, time-consuming eliminations, and delayed reporting. To address these issues, they decided to implement a dedicated consolidation software.

Step 1: Needs Assessment and Software Selection

The team started by identifying key requirements:

- Multi-entity consolidation capability

- Intercompany eliminations automation

- Currency translation features

- Integration with existing ERP systems

- User-friendly interface for accountants and controllers

After evaluating multiple options, they selected ConsoliPro, a cloud-based consolidation tool.

Step 2: Data Preparation and Integration

The team mapped the chart of accounts across subsidiaries to ensure alignment.

Mind Map: Data Preparation Workflow

Example: Subsidiary A used account code 4001 for “Sales Revenue,” while Subsidiary B used 5001. Both were mapped to the parent company’s standard account 4000.

Step 3: Software Configuration

The team configured ConsoliPro to reflect their organizational structure:

- Defined entities and ownership percentages

- Set up intercompany transaction rules

- Configured currency translation settings

Mind Map: Software Configuration Elements

Example: Subsidiary C operates in EUR, while the parent company reports in USD. The software was set to use the current rate method for balance sheet translation and temporal method for income statement.

Step 4: Testing and Validation

Before going live, the team ran multiple test consolidations:

- Verified elimination of intercompany sales and receivables

- Checked currency translation accuracy

- Ensured minority interest calculations were correct

Mind Map: Testing Checklist

Example: A test revealed that intercompany loan interest was not eliminated properly. The team adjusted elimination rules and re-tested.

Step 5: Training and Go-Live

The finance team conducted training sessions:

- Hands-on workshops for accountants

- Detailed user manuals

- Support channels for troubleshooting

The software was then deployed for the monthly close process.

Results and Benefits

- Consolidation cycle time reduced from 10 days to 4 days

- Significant reduction in manual errors

- Improved transparency and audit trail

- Real-time consolidation reports available to management

Summary of Best Practices from the Case Study

- Conduct thorough needs assessment before software selection

- Standardize chart of accounts across entities

- Configure intercompany and currency rules carefully

- Perform rigorous testing before full deployment

- Invest in user training and support

Additional Example: Simple Consolidation Setup Mind Map

This mind map can serve as a quick reference for accountants and financial controllers when setting up consolidation software.

By following the structured approach demonstrated in this case study, finance teams can effectively implement consolidation software, improving accuracy, efficiency, and compliance in their financial reporting processes.

2.5 Best Practice: Creating a Consolidation Timeline and Checklist

Creating a well-structured consolidation timeline and checklist is essential for ensuring accuracy, efficiency, and compliance in the financial statement consolidation process. This best practice helps accountants and financial controllers manage deadlines, coordinate tasks across multiple entities, and reduce the risk of errors.

Why a Consolidation Timeline and Checklist Matter

- Improves Coordination: Aligns activities across subsidiaries and departments.

- Enhances Accuracy: Ensures all necessary steps are completed before finalizing statements.

- Facilitates Compliance: Helps meet regulatory deadlines and reporting standards.

- Reduces Stress: Provides a clear roadmap, minimizing last-minute rushes.

Key Components of a Consolidation Timeline

- Data Collection Phase

- Request financial data from subsidiaries

- Validate and reconcile data

- Preliminary Consolidation

- Align chart of accounts

- Perform initial eliminations

- Adjustments and Eliminations

- Eliminate intercompany transactions

- Adjust for minority interests

- Currency Translation

- Translate foreign subsidiaries’ financials

- Record translation adjustments

- Review and Validation

- Internal review by accounting teams

- External audit preparation

- Final Reporting

- Prepare consolidated financial statements

- Submit reports to stakeholders

Sample Consolidation Timeline (Monthly Close Cycle)

Consolidation Checklist Example

| Task | Responsible Party | Deadline | Status |

|---|---|---|---|

| Collect financial data from all subsidiaries | Subsidiary Controllers | Day 3 post-month-end | Pending |

| Validate and reconcile data | Group Accounting Team | Day 5 | Pending |

| Align chart of accounts | Financial Controller | Day 6 | Pending |

| Perform intercompany eliminations | Consolidation Specialist | Day 7 | Pending |

| Adjust for minority interests | Financial Controller | Day 8 | Pending |

| Translate foreign currency balances | Treasury Team | Day 8 | Pending |

| Internal review of consolidated statements | CFO and Controllers | Day 10 | Pending |

| Prepare final consolidated financial statements | Group Accounting Team | Day 11 | Pending |

| Submit consolidated reports to management | CFO | Day 12 | Pending |

Example Scenario: Applying the Timeline and Checklist

Company XYZ operates with three subsidiaries across different countries. The financial controller creates a timeline that starts immediately after month-end (Day 1) and ends with report submission on Day 12. Each subsidiary is assigned specific deadlines for data submission, and the group accounting team follows the checklist to track progress.

By following this timeline and checklist, Company XYZ reduces errors caused by late data submission and missed eliminations. The structured approach also helps the team prepare for the external audit smoothly.

Tips for Effective Timeline and Checklist Management

- Use project management tools (e.g., Microsoft Planner, Trello) to assign tasks and track progress.

- Schedule regular status meetings during the consolidation period.

- Build in buffer days for unexpected delays or corrections.

- Continuously update the checklist based on past consolidation cycles.

- Train all involved parties on their responsibilities and deadlines.

Mind Map: Checklist Workflow

By integrating a detailed timeline and checklist into your consolidation process, accountants and financial controllers can significantly improve the accuracy and timeliness of consolidated financial statements, ultimately supporting better decision-making and regulatory compliance.

3. Consolidation Methods and Their Applications

3.1 Full Consolidation Method Explained with Step-by-Step Example

What is the Full Consolidation Method?

The Full Consolidation Method is the most common approach used when a parent company owns more than 50% of a subsidiary, giving it control over the subsidiary’s financial and operating policies. Under this method, the parent company combines 100% of the subsidiary’s assets, liabilities, income, and expenses with its own, regardless of the percentage of ownership.

Key Features:

- 100% of subsidiary’s financials are consolidated.

- Non-controlling interests (minority interests) are recognized separately.

- Intercompany transactions and balances are eliminated.

Step-by-Step Process for Full Consolidation

Step 1: Identify Control

Control is assumed when the parent owns more than 50% of voting rights or has the power to govern the financial and operating policies of the subsidiary.

Example:

Company A owns 80% of Company B. Company A has control and must consolidate Company B’s financials fully.

Step 2: Combine Financial Statements

Add together the assets, liabilities, income, and expenses of the parent and subsidiary line by line.

Example:

| Account | Company A (Parent) | Company B (Subsidiary) | Combined Total |

|---|---|---|---|

| Cash | $500,000 | $200,000 | $700,000 |

| Accounts Payable | $300,000 | $150,000 | $450,000 |

| Revenue | $1,000,000 | $600,000 | $1,600,000 |

| Expenses | $600,000 | $400,000 | $1,000,000 |

Step 3: Eliminate Intercompany Transactions

Remove transactions between the parent and subsidiary to avoid double counting.

Example:

- Company A sold inventory worth $50,000 to Company B.

- Company B still holds $10,000 of this inventory at year-end.

Eliminate:

- Intercompany sales: $50,000

- Intercompany purchases: $50,000

- Unrealized profit on ending inventory: $10,000 * (Profit margin)

Step 4: Adjust for Non-controlling Interests (NCI)

Since the parent owns 80%, the remaining 20% belongs to minority shareholders. Their share of net assets and net income must be shown separately.

Example:

- Total equity of subsidiary: $500,000

- Net income of subsidiary: $100,000

Calculate NCI:

- Equity NCI = 20% * $500,000 = $100,000

- Income NCI = 20% * $100,000 = $20,000

Step 5: Prepare Consolidated Financial Statements

Present the combined financials after eliminations and adjustments.

Example: Consolidated Balance Sheet Extract

| Account | Amount |

|---|---|

| Cash | $700,000 |

| Accounts Payable | $450,000 |

| Equity (Parent) | $1,200,000 |

| Non-controlling Int. | $100,000 |

Example: Consolidated Income Statement Extract

| Account | Amount |

|---|---|

| Revenue | $1,550,000* |

| Expenses | $1,000,000 |

| Net Income | $550,000 |

| Less: NCI Share | $20,000 |

| Net Income Attributable to Parent | $530,000 |

*Revenue adjusted after eliminating intercompany sales.

Summary Mind Map

Practical Tips for Accountants and Financial Controllers

- Maintain detailed schedules of intercompany transactions.

- Use consolidation software to automate eliminations and NCI calculations.

- Regularly reconcile subsidiary trial balances with consolidation inputs.

- Document assumptions and ownership percentages clearly.

By following these steps and best practices, accountants and financial controllers can ensure accurate and compliant consolidated financial statements that provide a clear picture of the group’s financial health.

3.2 Equity Method: When and How to Apply with Illustrative Example

What is the Equity Method?

The equity method is an accounting technique used to record investments in associates or joint ventures where the investor has significant influence but not full control, typically defined as ownership of 20% to 50% of voting shares.

Under this method, the investment is initially recorded at cost and subsequently adjusted to recognize the investor’s share of the investee’s profits or losses, dividends received, and other comprehensive income.

When to Apply the Equity Method

- Ownership interest between 20% and 50%

- Significant influence over financial and operating policies (e.g., board representation, participation in policy decisions)

- Joint ventures where control is shared

Key Features of the Equity Method

- Investment initially recorded at cost

- Investor’s share of investee’s net income increases the carrying amount

- Dividends received reduce the carrying amount

- Adjustments for other comprehensive income and impairment losses

Mind Map: Equity Method Overview

Step-by-Step Application of the Equity Method

-

Initial Investment Recognition

- Record the investment at purchase cost.

-

Recognize Share of Investee’s Profit or Loss

- Adjust the carrying amount by the investor’s proportionate share of the investee’s net income or loss.

-

Record Dividends Received

- Dividends reduce the carrying amount of the investment.

-

Adjust for Other Comprehensive Income

- Include investor’s share of investee’s OCI items.

-

Impairment Testing

- Assess if the investment is impaired and adjust accordingly.

Illustrative Example

Scenario: Company A acquires a 30% stake in Company B for $1,000,000. During the year, Company B reports net income of $200,000 and pays dividends of $50,000.

Step 1: Initial Investment

- Debit Investment in Company B: $1,000,000

Step 2: Recognize Share of Net Income

- 30% of $200,000 = $60,000

- Increase investment by $60,000

Step 3: Record Dividends Received

- 30% of $50,000 = $15,000

- Reduce investment by $15,000

Journal Entries:

| Date | Account | Debit | Credit |

|---|---|---|---|

| Purchase | Investment in Company B | 1,000,000 | |

| Cash | 1,000,000 | ||

| Share of Income | Investment in Company B | 60,000 | |

| Equity Income (P&L) | 60,000 | ||

| Dividends | Cash | 15,000 | |

| Investment in Company B | 15,000 |

Ending Investment Balance: $1,000,000 + $60,000 - $15,000 = $1,045,000

Mind Map: Equity Method Example Flow

Best Practices for Applying the Equity Method

- Confirm Significant Influence: Evaluate qualitative and quantitative factors before applying the equity method.

- Maintain Accurate Records: Track investee’s financial results and dividends regularly.

- Timely Adjustments: Update investment carrying amounts promptly after investee’s reporting.

- Disclosure: Clearly disclose the nature of investments and method used in financial statements.

Common Pitfalls and How to Avoid Them

| Pitfall | Solution |

|---|---|

| Misclassifying investments | Assess ownership and influence carefully |

| Failing to adjust for dividends | Always reduce investment by dividends received |

| Ignoring impairment indicators | Perform regular impairment tests |

| Delayed recognition of income | Align reporting periods with investee |

Summary

The equity method is essential for accurately reflecting an investor’s share in an associate’s financial performance. By following the step-by-step process and applying best practices, accountants and financial controllers can ensure compliance and provide transparent financial reporting.

3.3 Proportionate Consolidation: Practical Use Cases

Proportionate consolidation is a method used to consolidate a company’s share of assets, liabilities, income, and expenses of a jointly controlled entity or joint venture, in proportion to its ownership interest. Unlike full consolidation, where 100% of the subsidiary’s figures are consolidated, proportionate consolidation only includes the investor’s share.

When to Use Proportionate Consolidation

- Joint ventures where control is shared equally or proportionally.

- Entities where the investor has joint control but not full control.

- Situations where IFRS 11 (Joint Arrangements) or similar standards apply.

Mind Map: Proportionate Consolidation Overview

Practical Example 1: Joint Venture in Manufacturing

Scenario: Company A owns 40% of a joint venture, JV Manufacturing Ltd., which produces automotive parts. The joint venture’s financials for the year are:

- Total Assets: $5,000,000

- Total Liabilities: $2,000,000

- Revenue: $8,000,000

- Expenses: $6,000,000

Proportionate Consolidation for Company A:

- Assets to include: 40% of $5,000,000 = $2,000,000

- Liabilities to include: 40% of $2,000,000 = $800,000

- Revenue to include: 40% of $8,000,000 = $3,200,000

- Expenses to include: 40% of $6,000,000 = $2,400,000

Company A will report these amounts in its consolidated financial statements, reflecting its economic interest in the joint venture.

Mind Map: Practical Example 1 Breakdown

Practical Example 2: Real Estate Joint Venture

Scenario: Company B holds a 50% interest in a joint venture that owns and manages commercial real estate. The joint venture’s year-end financials are:

- Assets: $10,000,000

- Liabilities: $4,000,000

- Rental Income: $1,200,000

- Operating Expenses: $400,000

Proportionate Consolidation for Company B:

- Assets: 50% of $10,000,000 = $5,000,000

- Liabilities: 50% of $4,000,000 = $2,000,000

- Rental Income: 50% of $1,200,000 = $600,000

- Operating Expenses: 50% of $400,000 = $200,000

This approach ensures Company B’s consolidated statements reflect only its share of the joint venture’s financial position and performance.

Mind Map: Practical Example 2 Breakdown

Best Practices for Proportionate Consolidation

- Accurate Ownership Percentage: Always verify the exact ownership interest to ensure correct proportional amounts.

- Consistent Data Collection: Obtain timely and accurate financial data from joint ventures.

- Intercompany Transactions: Identify and eliminate intercompany transactions between the parent and joint venture to avoid double counting.

- Clear Disclosure: Disclose the nature of joint arrangements and the consolidation method used in financial statements.

- Use of Technology: Employ consolidation software that supports proportionate consolidation to automate calculations and reduce errors.

Summary

Proportionate consolidation is a valuable method for reflecting a company’s economic interest in joint ventures. By including only the proportional share of assets, liabilities, income, and expenses, financial controllers can present a more accurate and fair view of the group’s financial position. Practical examples, like manufacturing and real estate joint ventures, illustrate how this method works in real-world scenarios.

3.4 Combining Different Methods in One Consolidated Report

In complex corporate groups, it is common to apply different consolidation methods within the same consolidated financial statement. This happens because subsidiaries, associates, and joint ventures may require different accounting treatments based on ownership percentage, control, and influence.

Why Combine Different Methods?

- Varied Ownership Structures: Some entities are fully controlled (requiring full consolidation), others are significant but not controlling interests (equity method), and some are jointly controlled (proportionate consolidation).

- Regulatory Compliance: Accounting standards such as IFRS and GAAP specify different treatments depending on the nature of the relationship.

- Accurate Financial Representation: Combining methods ensures the consolidated financial statements reflect the economic reality of the group.

Common Consolidation Methods in One Report

Step-by-Step Example

Scenario:

- Parent Company A owns 80% of Subsidiary B (full consolidation).

- Parent Company A owns 30% of Associate C (equity method).

- Parent Company A has a 50% interest in Joint Venture D (proportionate consolidation).

Step 1: Full Consolidation of Subsidiary B

- Combine 100% of B’s assets, liabilities, income, and expenses.

- Eliminate intercompany transactions between A and B.

- Recognize non-controlling interest for 20% of B’s equity and profit.

Step 2: Equity Method for Associate C

- Record initial investment at cost.

- Adjust investment value by A’s share of C’s net income or loss.

- Do not consolidate C’s individual assets or liabilities.

Step 3: Proportionate Consolidation for Joint Venture D

- Include A’s 50% share of D’s assets, liabilities, income, and expenses directly in the consolidated statements.

- Eliminate intercompany transactions between A and D.

Mind Map: Workflow for Combining Methods

Best Practices When Combining Methods

- Clear Identification of Entity Types: Maintain an updated register of subsidiaries, associates, and joint ventures.

- Consistent Application of Accounting Policies: Ensure uniform accounting principles across entities to avoid discrepancies.

- Robust Intercompany Elimination Procedures: Automate elimination entries to reduce errors.

- Transparent Disclosures: Clearly disclose the methods applied to each entity in the notes.

- Use of Consolidation Software: Leverage tools that support multiple consolidation methods within one reporting framework.

Practical Example: Consolidated Income Statement Extract

| Description | Amount (in $) |

|---|---|

| Revenue (Full Consolidation) | 5,000,000 |

| Share of Profit from Associate (Equity Method) | 300,000 |

| Share of Profit from Joint Venture (Proportionate Consolidation) | 400,000 |

| Less: Intercompany Eliminations | (200,000) |

| Consolidated Revenue | 5,500,000 |

Combining different consolidation methods in one report requires careful planning, clear documentation, and a thorough understanding of the group’s structure. By following best practices and leveraging examples like the above, accountants and financial controllers can produce accurate and compliant consolidated financial statements that truly reflect the group’s financial position.

3.5 Best Practice: Selecting the Appropriate Consolidation Method

Selecting the appropriate consolidation method is a critical step in preparing accurate and compliant consolidated financial statements. The choice depends on the nature of the relationship between the parent company and its investees, the level of control or influence, and applicable accounting standards such as IFRS or GAAP.

Key Factors to Consider When Selecting a Consolidation Method

- Control Level: Does the parent have control, joint control, or significant influence?

- Ownership Percentage: What percentage of voting rights does the parent hold?

- Nature of the Investee: Is it a subsidiary, associate, or joint venture?

- Regulatory Requirements: Which accounting standards apply?

- Purpose of the Investment: Strategic control vs. passive investment.

Mind Map: Consolidation Method Selection Criteria

Overview of Consolidation Methods

| Method | When to Use | Example Scenario |

|---|---|---|

| Full Consolidation | Parent controls >50% voting rights | Parent owns 80% of Subsidiary A |

| Equity Method | Significant influence (20%-50%) | Parent owns 30% of Associate B |

| Proportionate Consolidation | Joint control in joint ventures | Parent and Partner each own 50% of Joint Venture C |

Example 1: Full Consolidation

Scenario: ParentCo owns 75% of SubCo.

Application:

- ParentCo consolidates 100% of SubCo’s assets, liabilities, income, and expenses.

- Non-controlling interest (25%) is reported separately.

Best Practice:

- Ensure elimination of intercompany transactions.

- Adjust for minority interests.

Example 2: Equity Method

Scenario: ParentCo owns 35% of AssociateCo and has significant influence but not control.

Application:

- ParentCo records its share of AssociateCo’s net income as a single line item.

- Investment is adjusted for dividends received and share of profits/losses.

Best Practice:

- Regularly assess the level of influence.

- Monitor changes in ownership percentage.

Example 3: Proportionate Consolidation

Scenario: ParentCo and PartnerCo each own 50% of JointVentureCo.

Application:

- ParentCo includes its proportionate share (50%) of assets, liabilities, income, and expenses.

Best Practice:

- Consistently apply the method across reporting periods.

- Disclose joint control arrangements clearly.

Mind Map: Step-by-Step Decision Process

Tips for Accountants and Financial Controllers

- Maintain Documentation: Keep clear records of ownership percentages and control assessments.

- Regularly Review Relationships: Changes in ownership or agreements may require method changes.

- Use Software Tools: Leverage consolidation software to automate method application.

- Train Teams: Ensure accounting teams understand criteria and implications of each method.

By following these best practices and using structured decision-making tools like mind maps, accountants and financial controllers can confidently select the appropriate consolidation method, ensuring compliance and accuracy in financial reporting.

4. Eliminations and Adjustments in Consolidation

4.1 Intercompany Transactions: Identification and Elimination Techniques

Intercompany transactions occur when two or more entities within the same corporate group engage in financial exchanges. These transactions can include sales, loans, services, or transfers of assets. Identifying and eliminating these transactions is crucial to avoid double counting and to present a true and fair view of the consolidated financial statements.

Why Identify Intercompany Transactions?

- Prevents overstatement of revenue and expenses.

- Avoids inflated asset and liability balances.

- Ensures compliance with accounting standards (IFRS 10, ASC 810).

Types of Intercompany Transactions

Step 1: Identification Techniques

-

Review Intercompany Accounts:

- Check accounts such as “Due to/from Affiliates,” “Intercompany Payables/Receivables,” and “Intercompany Revenue/Expenses.”

-

Analyze Transaction Patterns:

- Look for repetitive transactions between group companies.

-

Use Analytical Tools:

- Employ software filters to flag intercompany transactions.

-

Cross-Entity Confirmation:

- Match transactions recorded by both entities involved.

Step 2: Elimination Techniques

-

Eliminate Intercompany Sales and Purchases:

- Remove sales revenue recorded by the selling entity and the corresponding purchase expense recorded by the buying entity.

-

Eliminate Intercompany Balances:

- Remove receivables and payables between group companies to avoid double counting.

-

Eliminate Intercompany Profits:

- Adjust for unrealized profits on inventory or fixed assets sold within the group.

-

Eliminate Intercompany Interest and Loans:

- Remove interest income and expense, and eliminate loan balances.

Practical Example

Scenario: Subsidiary A sells goods worth $100,000 to Subsidiary B. The cost of goods sold (COGS) for Subsidiary A is $70,000. At the end of the reporting period, Subsidiary B has sold only half of the inventory purchased from Subsidiary A.

Step 1: Identify Intercompany Sales and Purchases

- Subsidiary A records $100,000 as sales revenue.

- Subsidiary B records $100,000 as purchase expense.

Step 2: Eliminate Intercompany Sales and Purchases

- Eliminate $100,000 from consolidated revenue and expenses.

Step 3: Adjust for Unrealized Profit

- Inventory remaining with Subsidiary B = $50,000 (half of $100,000).

- Unrealized profit = $50,000 - (COGS proportion) = $50,000 - ($70,000 * 0.5) = $50,000 - $35,000 = $15,000.

- Reduce consolidated inventory by $15,000 to eliminate unrealized profit.

Summary:

- Revenue and expenses reduced by $100,000.

- Inventory reduced by $15,000.

Best Practice Tips

- Maintain a detailed intercompany transaction register.

- Use automated reconciliation tools to match intercompany balances.

- Perform regular intercompany confirmations between entities.

- Document all elimination entries clearly for audit trails.

Additional Mind Map: Intercompany Transaction Workflow

By systematically identifying and eliminating intercompany transactions, accountants and financial controllers ensure the integrity and accuracy of consolidated financial statements, providing stakeholders with a clear and reliable financial picture.

4.2 Intercompany Profit and Loss Adjustments with Practical Example

Understanding Intercompany Profit and Loss Adjustments

When consolidating financial statements, one critical step is eliminating intercompany profits and losses to avoid overstating the group’s financial performance. These arise when one group entity sells goods or services to another at a profit, but from the consolidated perspective, this profit is unrealized until the goods are sold to an external party.

Why Are These Adjustments Necessary?

- To prevent double counting of profits within the group.

- To ensure the consolidated financial statements reflect only profits earned from external transactions.

- To comply with accounting standards such as IFRS and GAAP.

Mind Map: Intercompany Profit and Loss Adjustments

Step-by-Step Example: Intercompany Profit Elimination

Scenario:

- Parent Company (P) sells goods to Subsidiary (S) for $150,000.

- The cost to Parent Company for these goods was $100,000.

- At the end of the reporting period, Subsidiary still holds 40% of these goods in inventory.

Goal: Eliminate unrealized profit embedded in Subsidiary’s ending inventory.

Step 1: Calculate Unrealized Profit

- Profit on sale = Selling price - Cost = $150,000 - $100,000 = $50,000

- Ending inventory held by Subsidiary = 40% of $150,000 = $60,000

- Unrealized profit in ending inventory = 40% × $50,000 = $20,000

Step 2: Adjust Consolidated Financial Statements

- Reduce Subsidiary’s inventory by $20,000 to remove unrealized profit.

- Reduce consolidated profit by $20,000 to eliminate unrealized profit from income.

Journal Entry for Elimination:

Dr. Sales Revenue (Intercompany) 150,000

Cr. Cost of Goods Sold (Intercompany) 100,000

Cr. Inventory (to eliminate unrealized profit) 20,000

Dr. Cost of Goods Sold (to adjust profit) 20,000

This entry eliminates the intercompany sales and cost of goods sold and adjusts inventory and profit to exclude unrealized profit.

Mind Map: Practical Example Breakdown

Additional Example: Intercompany Service Profit Adjustment

Scenario:

- Subsidiary provides consulting services to Parent for $30,000.

- The cost incurred by Subsidiary is $20,000.

- At period-end, services are partially completed, and $10,000 revenue is unrealized.

Adjustment:

- Eliminate unrealized revenue of $10,000 from consolidated income.

- Adjust expenses accordingly to avoid overstating profit.

Journal Entry:

Dr. Service Revenue (Intercompany) 10,000

Cr. Service Expense (Intercompany) 10,000

Best Practices for Intercompany Profit and Loss Adjustments

- Maintain Detailed Records: Track all intercompany transactions with clear documentation.

- Regular Reconciliation: Periodically reconcile intercompany accounts to identify unrealized profits.

- Automation: Use consolidation software to automate elimination entries and reduce errors.

- Clear Policies: Establish group-wide policies for intercompany pricing and profit recognition.

- Training: Ensure accounting teams understand the impact of intercompany profits on consolidation.

Summary

Intercompany profit and loss adjustments are essential to present a true and fair view of the group’s financial performance. By identifying unrealized profits and eliminating them through proper journal entries, accountants and financial controllers ensure compliance and accuracy in consolidated financial statements.

4.3 Eliminating Intercompany Balances: Step-by-Step Process

Intercompany balances arise when entities within the same corporate group transact with each other, resulting in receivables and payables that must be eliminated during consolidation to avoid double counting. Proper elimination ensures the consolidated financial statements present the group as a single economic entity.

Why Eliminate Intercompany Balances?

- Prevents inflation of assets and liabilities.

- Ensures accurate representation of the group’s financial position.

- Complies with accounting standards such as IFRS and GAAP.

Step-by-Step Process for Eliminating Intercompany Balances

Step 1: Identify Intercompany Transactions and Balances

- Collect trial balances from all subsidiaries.

- Highlight intercompany receivables and payables.

- Confirm matching balances between entities.

Example:

- Subsidiary A shows an intercompany receivable of $100,000 from Subsidiary B.

- Subsidiary B shows an intercompany payable of $100,000 to Subsidiary A.

Step 2: Verify the Accuracy and Completeness of Balances

- Reconcile intercompany accounts.

- Investigate discrepancies (e.g., timing differences, currency translation).

Example:

- Subsidiary A reports $100,000 receivable, Subsidiary B reports $98,000 payable.

- Investigate and adjust for exchange rate differences or unrecorded transactions.

Step 3: Prepare Elimination Journal Entries

- Debit intercompany payables.

- Credit intercompany receivables.

Example Journal Entry:

Dr. Intercompany Payables (Subsidiary B) $100,000

Cr. Intercompany Receivables (Subsidiary A) $100,000

Step 4: Post Elimination Entries in Consolidation Worksheet or Software

- Use consolidation tools to input elimination entries.

- Ensure entries do not affect individual entity books but adjust consolidated figures.

Step 5: Review and Validate Consolidated Balances

- Confirm intercompany balances net to zero.

- Perform analytical review to ensure no residual intercompany balances remain.

Mind Map: Eliminating Intercompany Balances

Practical Example

Scenario:

Company X owns two subsidiaries: Alpha and Beta.

- Alpha has an intercompany receivable of $50,000 from Beta.

- Beta has an intercompany payable of $50,000 to Alpha.

Step 1: Identify balances.

Step 2: Confirm both balances match exactly.

Step 3: Prepare elimination entry:

Dr. Intercompany Payables (Beta) $50,000

Cr. Intercompany Receivables (Alpha) $50,000

Step 4: Post in consolidation worksheet.

Step 5: Review consolidated balance sheet to ensure no intercompany receivables or payables remain.

Tips and Best Practices

- Maintain a detailed intercompany reconciliation schedule updated monthly.

- Use automation tools to flag mismatches early.

- Communicate regularly with subsidiaries to resolve discrepancies promptly.

- Document all elimination entries clearly for audit trails.

Additional Mind Map: Common Issues and Solutions

By following this structured approach, accountants and financial controllers can ensure accurate elimination of intercompany balances, leading to reliable consolidated financial statements that truly reflect the financial position of the entire group.

4.4 Handling Minority Interests and Non-Controlling Interests

Introduction

In financial statement consolidation, Minority Interests (MI) or Non-Controlling Interests (NCI) represent the portion of equity ownership in a subsidiary not attributable to the parent company. Properly accounting for these interests is essential to present an accurate picture of the group’s financial position and performance.

What Are Minority Interests / Non-Controlling Interests?

- Minority Interests refer to shareholders who own less than 50% of a subsidiary but still hold equity.

- Non-Controlling Interests is the preferred term under IFRS, emphasizing that these shareholders do not control the subsidiary.

Why Are They Important?

- They reflect the economic interest of outside investors in subsidiaries.

- They ensure that consolidated financial statements fairly represent both the parent’s and the minority shareholders’ stakes.

Accounting Treatment Overview

- MI/NCI is reported within equity but separately from the parent shareholders’ equity.

- Profit or loss attributable to MI/NCI is shown separately in the consolidated income statement.

- Adjustments for MI/NCI are made during consolidation to reflect their share of net assets and net income.

Mind Map: Key Concepts in Handling Minority Interests

Measurement of Minority Interests

There are two main approaches to measure NCI at acquisition:

- Fair Value Method: NCI is measured at its fair value, including goodwill attributable to NCI.

- Proportionate Share Method: NCI is measured as their proportionate share of the subsidiary’s identifiable net assets.

Example: Calculating Minority Interest at Acquisition

Scenario:

- Parent acquires 80% of Subsidiary for $800,000.

- Subsidiary’s net identifiable assets fair value: $900,000.

- Fair value of NCI (20%) estimated at $250,000.

Calculations:

- Using Proportionate Share Method:

- NCI = 20% × $900,000 = $180,000

- Using Fair Value Method:

- NCI = $250,000 (given fair value)

Implication:

- The choice affects goodwill calculation and consolidated equity.

Mind Map: Minority Interest Measurement Methods

Reporting Minority Interests in Consolidated Financial Statements

- Balance Sheet:

- NCI is presented within equity, separately from parent equity.

- Income Statement:

- Profit or loss is split between parent and NCI.

- Statement of Changes in Equity:

- Changes in NCI due to transactions or profit allocation are reflected.

Example: Reporting Minority Interests

Subsidiary’s Net Income: $100,000

- Parent owns 80%

- NCI owns 20%

Income Statement Presentation:

- Profit attributable to Parent: $80,000

- Profit attributable to NCI: $20,000

Balance Sheet Presentation:

- Total Equity = Parent Equity + NCI Equity

Mind Map: Reporting Minority Interests

Common Challenges and Best Practices

- Challenge: Correctly identifying and measuring NCI at acquisition.

- Challenge: Properly allocating profit and loss between parent and NCI.

- Challenge: Handling changes in ownership without loss of control.

Best Practices:

- Maintain detailed records of ownership percentages and changes.

- Use consolidation software to automate allocation and reporting.

- Regularly reconcile subsidiary equity with consolidated NCI.

Example: Ownership Change Without Loss of Control

Scenario:

- Parent owns 75% initially.

- Sells 10% to outside investors, now owns 65%.

Accounting Treatment:

- Recognize difference between consideration received and carrying amount of NCI as equity transaction.

- No gain or loss recognized in profit or loss.

Summary

Handling Minority Interests and Non-Controlling Interests correctly ensures transparency and accuracy in consolidated financial statements. Understanding measurement methods, proper allocation of profit and loss, and clear presentation are critical for accountants and financial controllers.

Additional Resources

- IFRS 10 – Consolidated Financial Statements

- ASC 810 – Consolidation (US GAAP)

- Practical guides on consolidation software features for NCI handling

4.5 Best Practice: Using Automation to Streamline Eliminations

Financial statement consolidation involves numerous elimination entries, especially intercompany transactions and balances. Manual processing of these eliminations can be time-consuming, error-prone, and inefficient. Automation offers a powerful solution to streamline this critical step, improving accuracy, reducing closing time, and enabling financial controllers and accountants to focus on analysis rather than data correction.

Why Automate Eliminations?

- Accuracy: Automation reduces human errors in identifying and eliminating intercompany transactions.

- Efficiency: Speeds up the consolidation process by handling repetitive tasks.

- Consistency: Ensures uniform application of elimination rules across periods and entities.

- Audit Trail: Automated systems maintain logs and documentation, facilitating audits.

Key Components of Automation in Eliminations

Step-by-Step Example: Automating Intercompany Eliminations

Scenario: A corporate group has multiple subsidiaries with intercompany sales and receivables/payables that need elimination.

-

Data Extraction: Automated data connectors pull trial balances and transaction details from each subsidiary’s ERP system daily.

-

Matching Engine: The automation tool applies matching algorithms to identify intercompany transactions based on counterparty codes, invoice numbers, and amounts.

-

Elimination Entry Generation: Once matched, the system automatically generates elimination journal entries to remove intercompany sales and balances.

-

Exception Handling: Transactions that do not match perfectly are flagged for manual review with detailed discrepancy reports.

-

Approval Workflow: Financial controllers review and approve elimination entries through an integrated workflow before posting.

-

Posting & Reporting: Approved entries are posted to the consolidation ledger, and detailed reports are generated for audit and compliance.

Practical Mind Map: Automation Workflow for Eliminations

Example: Automation Tool Impact

| Metric | Before Automation | After Automation |

|---|---|---|

| Time to Complete Eliminations | 5 days | 1 day |

| Number of Errors | 15 per period | 2 per period |

| Manual Review Effort | 40 hours | 10 hours |

This example demonstrates how automation can drastically reduce the time and errors associated with eliminations.

Tips for Successful Automation Implementation

- Define Clear Rules: Establish precise intercompany matching criteria to minimize exceptions.

- Data Standardization: Ensure consistent data formats and chart of accounts across subsidiaries.

- Pilot Testing: Start with a small group of entities to refine the automation process.

- Training: Equip accounting teams with knowledge on using automation tools effectively.

- Continuous Improvement: Regularly update rules and workflows based on feedback and evolving business needs.

Summary

Automation in the elimination process of financial consolidation is a best practice that enhances accuracy, efficiency, and transparency. By leveraging technology such as rule-based engines, workflow automation, and integration with ERP systems, accountants and financial controllers can significantly reduce manual workload and focus on strategic financial analysis.

Embracing automation not only accelerates the close process but also strengthens internal controls and audit readiness, making it an indispensable tool in modern corporate finance.

5. Currency Translation and Foreign Subsidiaries

5.1 Understanding Currency Translation in Consolidation

When consolidating financial statements of multinational corporations, one of the critical challenges is dealing with subsidiaries that operate in different currencies. Currency translation is the process of converting the financial statements of foreign subsidiaries into the parent company’s reporting currency to present a unified consolidated financial statement.

Why is Currency Translation Important?

- Ensures comparability of financial data across different countries.

- Reflects the true financial position and performance of the group.

- Complies with accounting standards such as IFRS and US GAAP.

Key Concepts in Currency Translation

- Functional Currency: The primary currency of the subsidiary’s operating environment.

- Reporting Currency: The currency in which the parent company prepares consolidated financial statements.

- Exchange Rate: The rate at which one currency is converted into another.

Mind Map: Currency Translation Overview

Common Currency Translation Methods

-

Current Rate Method

- Assets and liabilities are translated at the current exchange rate at the reporting date.

- Income statement items are translated at the average exchange rate for the period.

- Translation differences are recorded in Other Comprehensive Income (OCI).

-

Temporal Method

- Monetary assets and liabilities are translated at the current exchange rate.

- Non-monetary items are translated at historical exchange rates.

- Income statement items are translated at the rates in effect when the transactions occurred.

- Translation differences are recognized in profit or loss.

Mind Map: Currency Translation Methods

Practical Example 1: Current Rate Method

Scenario:

- Parent company currency: USD

- Subsidiary currency: EUR

- Reporting date exchange rate: 1 EUR = 1.10 USD

- Average exchange rate for the period: 1 EUR = 1.08 USD

Subsidiary Financials (EUR):

- Assets: 1,000,000 EUR

- Liabilities: 400,000 EUR

- Revenue: 500,000 EUR

- Expenses: 300,000 EUR

Translation:

- Assets = 1,000,000 EUR * 1.10 = 1,100,000 USD

- Liabilities = 400,000 EUR * 1.10 = 440,000 USD

- Revenue = 500,000 EUR * 1.08 = 540,000 USD

- Expenses = 300,000 EUR * 1.08 = 324,000 USD

Translation Adjustment:

- The difference between translated equity and net assets is recorded in OCI.

Practical Example 2: Temporal Method

Scenario:

- Same as above, but assume inventory (non-monetary) was purchased at historical rate 1 EUR = 1.05 USD.

Subsidiary Financials (EUR):

- Monetary Assets: 600,000 EUR

- Non-Monetary Assets (Inventory): 400,000 EUR

- Liabilities: 400,000 EUR

Translation:

- Monetary Assets = 600,000 EUR * 1.10 = 660,000 USD

- Non-Monetary Assets = 400,000 EUR * 1.05 = 420,000 USD

- Liabilities = 400,000 EUR * 1.10 = 440,000 USD

Translation Adjustment:

- Differences flow through profit or loss, impacting net income.

Best Practice Tips for Accountants and Financial Controllers

- Identify the functional currency accurately for each subsidiary before translation.

- Consistently apply the chosen translation method across reporting periods.

- Document exchange rates used and source them from reliable providers.

- Monitor exchange rate fluctuations and assess their impact on consolidated financials.

- Use automation tools to reduce manual errors in currency translation.

Summary

Currency translation is a fundamental step in consolidating financial statements for multinational groups. Understanding the differences between the current rate and temporal methods, and applying them correctly, ensures accurate and compliant consolidated financial reporting.

For further reading, see section 5.2 for detailed examples of translation methods and their application.

5.2 Translation Methods: Current Rate vs. Temporal Method with Examples