Cash Flow Management

1. Introduction to Cash Flow Management

1.1 Understanding Cash Flow: Definition and Importance

Cash flow is the movement of money into and out of a business over a specific period. It represents the actual liquidity available to a company to meet its obligations, invest in growth, and sustain operations. Unlike profit, which is an accounting measure of earnings, cash flow focuses solely on the cash that is physically received and paid out.

Why is Cash Flow Important?

- Liquidity Management: Ensures the business can pay its bills, salaries, and suppliers on time.

- Business Sustainability: Positive cash flow is critical for ongoing operations and avoiding insolvency.

- Investment and Growth: Cash availability allows for reinvestment in new projects, inventory, or technology.

- Creditworthiness: Lenders and investors assess cash flow to gauge financial health.

Mind Map: Core Concepts of Cash Flow

Example 1: Retail Store Cash Flow Scenario

Imagine a retail store that sells seasonal products. During the holiday season, the store experiences high sales, resulting in significant cash inflows. However, it also needs to purchase inventory in advance and pay staff salaries and rent, which are cash outflows.

- December: High sales generate $100,000 in cash inflows.

- November: The store spends $60,000 on inventory and $20,000 on operating expenses.

If the store does not manage its cash flow properly, it might run out of cash before the holiday sales peak, even though it is profitable on paper.

Mind Map: Cash Flow Example Breakdown

Example 2: Financial Controller Perspective

A financial controller in a retail company monitors cash flow daily to ensure there is enough liquidity to cover payroll and supplier payments. They use cash flow statements and forecasting tools to anticipate periods of tight cash availability and arrange for short-term credit lines if necessary.

- Best Practice: Regularly updating cash flow forecasts based on actual sales and expenses.

- Benefit: Avoids surprises and enables proactive management.

Mind Map: Role of Financial Controller in Cash Flow

Summary

Understanding cash flow is fundamental for accountants and financial controllers in finance and retail sectors. It goes beyond profit to focus on the actual cash available, which determines a company’s ability to operate, grow, and survive. By mastering cash flow concepts and monitoring, professionals can ensure their organizations remain financially healthy and agile.

1.2 Key Components of Cash Flow: Inflows and Outflows

Effective cash flow management starts with a clear understanding of its two fundamental components: cash inflows and cash outflows. These elements represent the movement of money into and out of a business, and managing them well is critical for maintaining liquidity and financial health.

Cash Inflows

Cash inflows are the funds received by a business. They increase the cash balance and provide the resources needed to cover expenses, invest, and grow.

Common Sources of Cash Inflows:

- Sales Revenue: Money received from selling goods or services.

- Accounts Receivable Collections: Payments collected from customers who previously bought on credit.

- Loans and Financing: Funds obtained through borrowing.

- Asset Sales: Cash generated from selling company assets.

- Investment Income: Dividends, interest, or returns from investments.

Mind Map: Cash Inflows

Example:

A retail store sells $50,000 worth of merchandise in a month. Of this, $35,000 is collected immediately, and $15,000 is on credit to be collected next month. Additionally, the store receives a $2,000 loan from the bank to support expansion.

- Immediate cash inflow: $35,000

- Accounts receivable expected next month: $15,000

- Loan proceeds: $2,000

Cash Outflows

Cash outflows represent the money leaving the business. These are expenses and payments that reduce the cash balance.

Common Types of Cash Outflows:

- Operating Expenses: Rent, utilities, salaries, marketing, and other day-to-day costs.

- Cost of Goods Sold (COGS): Payments to suppliers for inventory or raw materials.

- Loan Repayments: Principal and interest payments on borrowed funds.

- Capital Expenditures: Purchases of long-term assets like equipment or property.

- Taxes and Fees: Government levies and compliance costs.

Mind Map: Cash Outflows

Example:

Continuing with the retail store example, the business pays $20,000 to suppliers for inventory, $8,000 in salaries, $3,000 in rent, and $1,000 in utilities during the month. It also repays $500 in loan interest.

- Supplier payments: $20,000

- Salaries: $8,000

- Rent: $3,000

- Utilities: $1,000

- Loan interest: $500

Integrated Example: Monthly Cash Flow Snapshot

| Description | Amount (USD) | Type |

|---|---|---|

| Sales collected | 35,000 | Inflow |

| Accounts receivable (next month) | 15,000 | Inflow (future) |

| Loan proceeds | 2,000 | Inflow |

| Supplier payments | 20,000 | Outflow |

| Salaries | 8,000 | Outflow |

| Rent | 3,000 | Outflow |

| Utilities | 1,000 | Outflow |

| Loan interest | 500 | Outflow |

Net cash flow for the month:

= (35,000 + 2,000) - (20,000 + 8,000 + 3,000 + 1,000 + 500) = 37,000 - 32,500 = $4,500 positive cash flow

Why Understanding Inflows and Outflows Matters

- Liquidity Management: Knowing when cash comes in and goes out helps avoid shortfalls.

- Planning and Forecasting: Accurate categorization improves cash flow projections.

- Decision Making: Helps prioritize payments and manage credit terms.

- Identifying Problem Areas: For example, slow receivables or high expenses.

Summary

Understanding cash inflows and outflows is foundational for accountants and financial controllers in finance and retail sectors. By categorizing and monitoring these components, professionals can maintain healthy cash balances, plan effectively, and support business sustainability.

1.3 The Role of Cash Flow Management in Finance and Retail

Cash flow management is a critical function that ensures a business has enough liquidity to meet its obligations, invest in growth, and navigate uncertainties. In both finance and retail sectors, effective cash flow management plays a pivotal role in maintaining operational stability and driving strategic decisions.

Why Cash Flow Management Matters in Finance and Retail

- Liquidity Maintenance: Ensures the business can pay suppliers, employees, and creditors on time.

- Operational Continuity: Prevents disruptions caused by cash shortages.

- Investment and Growth: Frees up resources for expansion, marketing, and technology upgrades.

- Risk Mitigation: Helps anticipate and manage financial risks.

Mind Map: Core Roles of Cash Flow Management

Role in Finance Sector

In finance, cash flow management is foundational. Financial controllers and accountants rely on it to:

- Monitor and report liquidity positions.

- Manage working capital effectively.

- Ensure compliance with financial regulations.

- Support budgeting and forecasting activities.

Example: A financial controller at a mid-sized investment firm uses cash flow reports to decide when to liquidate short-term assets to cover upcoming liabilities, avoiding penalties and maintaining creditworthiness.

Role in Retail Sector

Retail businesses face unique cash flow challenges due to:

- High volume of daily transactions.

- Seasonal fluctuations in sales.

- Inventory management complexities.

Effective cash flow management helps retailers:

- Optimize inventory purchases to avoid overstocking or stockouts.

- Manage supplier payments to maintain good relationships.

- Plan for seasonal demand spikes.

Example: A retail store manager implements a cash flow forecast to align inventory purchases with expected holiday season sales, preventing excess stock and improving cash availability.

Mind Map: Cash Flow Management in Retail

Integrated Example: Finance and Retail Collaboration

Consider a retail chain expanding to new locations. The finance team and retail managers collaborate on cash flow management:

- Finance team provides cash flow forecasts highlighting available capital.

- Retail managers adjust inventory and staffing plans based on cash availability.

- Both teams monitor actual cash flow against forecasts to make real-time adjustments.

This integrated approach ensures the expansion is financially sustainable and operationally smooth.

Summary

Cash flow management acts as the lifeblood of both finance and retail organizations. It supports day-to-day operations, strategic initiatives, and risk mitigation. For accountants and financial controllers, mastering cash flow management means enabling their organizations to thrive even in volatile market conditions.

1.4 Common Cash Flow Challenges Faced by Accountants and Financial Controllers

Cash flow management is a critical responsibility for accountants and financial controllers, especially in the finance and retail sectors where cash inflows and outflows can be highly variable. Despite best efforts, several common challenges often arise that can complicate maintaining a healthy cash flow.

Key Challenges:

Delayed Receivables

One of the most frequent challenges is delayed customer payments. For example, a retail business might invoice customers with net 30 terms, but many customers pay late, causing cash inflows to be unpredictable.

Example: A retail chain issues invoices totaling $100,000 monthly but only collects $70,000 on time. This 30% delay forces the finance team to scramble for short-term financing or delay supplier payments.

Best Practice: Implement automated invoicing and reminders, and consider early payment discounts to encourage timely payments.

Unpredictable Sales

Retail sales often fluctuate due to seasonality or market trends, making cash flow forecasting difficult.

Example: A fashion retailer experiences a surge in sales during holiday seasons but sees a steep decline in the off-season, leading to cash shortages.

Best Practice: Use historical sales data to build seasonal cash flow models and maintain a cash reserve for low-sales periods.

High Inventory Costs

Excess inventory ties up cash that could be used elsewhere.

Example: A retailer stocks up on winter apparel but fails to sell it all, resulting in s and cash flow strain.

Best Practice: Adopt just-in-time inventory practices and monitor inventory turnover ratios closely.

Expense Management

Unexpected or poorly controlled expenses can disrupt cash flow.

Example: A retail store faces sudden equipment repair costs that were not budgeted, forcing a cash outflow spike.

Best Practice: Maintain an emergency fund and regularly review expense categories to identify cost-saving opportunities.

Financing Constraints

Access to affordable financing is often limited, especially for smaller businesses.

Example: A financial controller struggles to secure a line of credit due to strict lending criteria, limiting the company’s ability to smooth cash flow gaps.

Best Practice: Build strong banking relationships early and explore alternative financing options like invoice factoring.

Poor Forecasting

Inaccurate or outdated cash flow forecasts can lead to misinformed decisions.

Example: A company relies on quarterly forecasts that do not reflect recent market changes, resulting in unexpected cash shortages.

Best Practice: Implement rolling forecasts updated monthly or weekly using real-time data.

Supplier Payment Terms

Short payment terms or penalties for late payments can pressure cash outflows.

Example: A retailer must pay suppliers within 15 days but only collects from customers in 30 days, creating a cash flow mismatch.

Best Practice: Negotiate extended payment terms or stagger payments to better align with receivables.

Economic Uncertainty

Inflation, regulatory changes, or economic downturns can unpredictably impact cash flow.

Example: Rising costs due to inflation increase operating expenses, squeezing cash reserves.

Best Practice: Conduct scenario planning and maintain flexible budgets to adapt quickly.

Summary Mind Map

By understanding these common challenges and applying best practices with practical examples, accountants and financial controllers can better anticipate issues and maintain a healthy cash flow, ensuring business stability and growth.

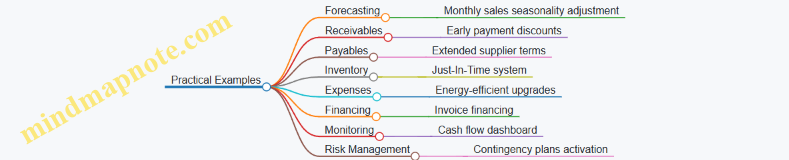

1.5 Overview of Best Practices in Cash Flow Management

Effective cash flow management is essential for maintaining the financial health of any business, especially within the finance and retail sectors. This section provides an integrated overview of best practices, supported by clear examples and mind maps to help accountants and financial controllers implement these strategies with confidence.

Best Practices Mind Map

Forecasting

Best Practice: Develop accurate cash flow forecasts to anticipate cash shortages or surpluses.

Example: A retail chain uses historical sales data and seasonal trends to create monthly forecasts. For instance, during the holiday season, they anticipate increased cash inflows and adjust inventory purchases accordingly.

Receivables Management

Best Practice: Set clear payment terms and encourage early payments to accelerate cash inflows.

Example: An accounting firm offers a 2% discount if clients pay invoices within 10 days instead of the standard 30 days. This incentivizes quicker payments and improves cash availability.

Payables Management

Best Practice: Negotiate extended payment terms with suppliers without damaging relationships.

Example: A retail store negotiates 60-day payment terms instead of 30 days with key suppliers, allowing more time to convert inventory into sales before paying.

Inventory Control

Best Practice: Optimize inventory levels to free up cash tied in stock.

Example: Implementing a Just-In-Time (JIT) inventory system, a retailer reduces excess stock, lowering storage costs and improving cash flow.

Expense Management

Best Practice: Regularly review expenses to identify and eliminate unnecessary costs.

Example: A financial controller audits monthly expenses and identifies redundant software subscriptions, canceling them to save cash.

Financing

Best Practice: Use short-term financing options strategically to bridge cash flow gaps.

Example: A retail business uses invoice financing to access cash immediately after sales, rather than waiting for customer payments.

Monitoring & Reporting

Best Practice: Track key cash flow metrics and create real-time dashboards for proactive management.

Example: A finance team develops a dashboard showing daily cash inflows and outflows, enabling quick decisions to avoid overdrafts.

Risk Management

Best Practice: Prepare contingency plans and use scenario analysis to manage cash flow risks.

Example: During an economic downturn, a retailer models worst-case cash flow scenarios and establishes a reserve fund to cover three months of expenses.

Integrated Example Mind Map

By integrating these best practices, accountants and financial controllers can create a robust cash flow management system that not only ensures liquidity but also supports strategic growth and operational efficiency.

2. Cash Flow Forecasting Techniques

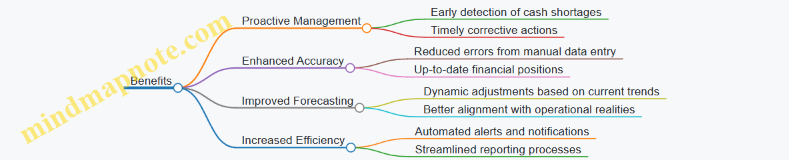

2.1 Importance of Accurate Cash Flow Forecasting

Accurate cash flow forecasting is a cornerstone of effective financial management, especially for accountants and financial controllers in the finance and retail sectors. It enables businesses to anticipate cash shortages or surpluses, make informed decisions, and maintain financial stability.

Why Accurate Cash Flow Forecasting Matters

- Ensures Liquidity: Helps maintain sufficient cash to meet day-to-day obligations such as payroll, supplier payments, and operational expenses.

- Supports Strategic Planning: Provides insights into when to invest, expand, or hold back based on projected cash availability.

- Avoids Financial Distress: Early identification of cash shortfalls allows proactive measures like securing financing or adjusting expenses.

- Improves Stakeholder Confidence: Demonstrates financial control to investors, lenders, and management.

- Optimizes Working Capital: Balances receivables, payables, and inventory to maximize cash efficiency.

Mind Map: Key Benefits of Accurate Cash Flow Forecasting

Example 1: Avoiding a Cash Shortfall in Retail

A mid-sized retail chain used historical sales data to forecast cash inflows and outflows for the upcoming quarter. The forecast revealed a potential cash shortfall in July due to seasonal inventory purchases and slower sales. Armed with this insight, the financial controller arranged a short-term line of credit and negotiated extended payment terms with suppliers. As a result, the company maintained smooth operations without disruption.

Example 2: Strategic Investment Timing

An accounting team at a finance company used accurate cash flow forecasting to identify a surplus expected in Q4. Instead of letting the cash sit idle, the team advised management to invest in upgrading IT infrastructure. This timely decision improved operational efficiency and positioned the company for growth.

Mind Map: Consequences of Inaccurate Cash Flow Forecasting

Practical Tips for Enhancing Forecast Accuracy

- Use multiple data sources including sales trends, payment histories, and market conditions.

- Update forecasts regularly to reflect actual performance and changing circumstances.

- Involve cross-functional teams to gather comprehensive input.

- Incorporate seasonal and cyclical factors relevant to retail and finance.

- Leverage forecasting software with predictive analytics capabilities.

Example 3: Regular Forecast Updates in Practice

A financial controller at a retail company updated the cash flow forecast weekly instead of monthly. This practice allowed the team to quickly identify a sudden drop in receivables due to delayed customer payments. Prompt action was taken to accelerate collections, preventing a potential cash crunch.

Accurate cash flow forecasting is not just a financial exercise; it is a strategic tool that empowers accountants and financial controllers to safeguard the financial health of their organizations and seize growth opportunities with confidence.

2.2 Short-term vs Long-term Cash Flow Forecasting

Cash flow forecasting is a critical tool for accountants and financial controllers to ensure that a business maintains sufficient liquidity to meet its obligations. Understanding the distinction between short-term and long-term cash flow forecasting is essential for effective financial planning and risk management.

What is Short-term Cash Flow Forecasting?

Short-term cash flow forecasting typically covers a period ranging from daily up to 3 months. It focuses on immediate cash inflows and outflows, helping businesses manage day-to-day liquidity needs.

Key Characteristics:

- Time horizon: Daily, weekly, or monthly (up to 3 months)

- Focus on operational cash movements

- Helps avoid short-term cash shortages

- Supports tactical decisions like managing payables and receivables

Example: A retail store forecasts cash flow for the next 30 days to ensure it can pay suppliers on time and cover payroll. It tracks daily sales, expected customer payments, and upcoming bills.

What is Long-term Cash Flow Forecasting?

Long-term cash flow forecasting extends beyond 3 months, often up to 1-3 years or more. It is strategic in nature, used for planning major investments, financing, and growth initiatives.

Key Characteristics:

- Time horizon: Quarterly, annually, or multi-year

- Focus on strategic financial planning

- Helps in capital budgeting and financing decisions

- Incorporates assumptions about market trends, expansion, and economic conditions

Example: A retail chain prepares a 2-year cash flow forecast to evaluate the feasibility of opening new stores and securing a loan. It includes projected sales growth, capital expenditures, and debt repayments.

Mind Map: Short-term vs Long-term Cash Flow Forecasting

Integrating Both Forecasts for Effective Cash Flow Management

While short-term forecasts help manage immediate liquidity, long-term forecasts provide a roadmap for sustainable growth. Combining both approaches allows financial controllers to balance operational needs with strategic goals.

Example: A financial controller uses a rolling 13-week short-term forecast to monitor weekly cash positions and a 3-year long-term forecast to plan for upcoming capital investments. When the short-term forecast signals a cash crunch, they adjust payment schedules or seek short-term financing, while the long-term forecast guides decisions on store openings.

Practical Example: Short-term vs Long-term Forecasting in a Retail Business

Scenario: A mid-sized retail company experiences seasonal fluctuations. During the holiday season, cash inflows spike, but inventory purchases and staffing costs also increase.

- Short-term Forecast: The accountant prepares a weekly cash flow forecast for the next 12 weeks to ensure sufficient cash for inventory purchases and holiday payroll.

- Long-term Forecast: The financial controller develops a 3-year forecast considering expansion into new markets and the impact of e-commerce trends.

Outcome: By monitoring short-term cash flow, the company avoids overdrafts during peak season. The long-term forecast helps secure financing for new store openings, aligning growth with cash availability.

Summary Table: Differences Between Short-term and Long-term Cash Flow Forecasting

| Aspect | Short-term Forecasting | Long-term Forecasting |

|---|---|---|

| Time Horizon | Daily to 3 months | 3 months to several years |

| Focus | Operational liquidity | Strategic financial planning |

| Data Used | Actual cash transactions, sales | Assumptions, projections, trends |

| Purpose | Manage immediate cash needs | Plan investments and financing |

| Frequency | Weekly or daily updates | Quarterly or annual updates |

| Example | 30-day cash flow for payroll | 3-year forecast for expansion |

Tips for Accountants and Financial Controllers

- Use short-term forecasts to identify cash shortages early and take corrective actions such as adjusting payment terms or securing short-term credit.

- Develop long-term forecasts to support strategic decisions and communicate financial needs to stakeholders.

- Regularly update both forecasts to reflect actual performance and changing market conditions.

- Leverage software tools that integrate short-term and long-term forecasting for seamless cash flow management.

By mastering both short-term and long-term cash flow forecasting, finance professionals in retail and other sectors can ensure their organizations remain financially healthy and well-prepared for future challenges and opportunities.

2.3 Step-by-Step Guide to Building a Cash Flow Forecast

Building a reliable cash flow forecast is essential for accountants and financial controllers to anticipate liquidity needs, manage working capital, and make informed financial decisions. This step-by-step guide will walk you through the process of creating an effective cash flow forecast, complete with practical examples and mind maps to visualize the workflow.

Step 1: Define the Forecast Period

Decide the time horizon for your forecast. Common periods include:

- Short-term: Weekly or monthly forecasts (ideal for operational cash flow management)

- Long-term: Quarterly or annual forecasts (useful for strategic planning)

Example: A retail business preparing for seasonal sales might use a weekly forecast for the next 3 months.

Step 2: Gather Historical Cash Flow Data

Collect past cash inflows and outflows data to identify trends and seasonality.

Example: Review the last 12 months of bank statements, sales reports, and expense records.

Step 3: Identify Cash Inflows

List all sources of cash receipts, such as:

- Customer payments (sales revenue)

- Loan proceeds

- Asset sales

- Interest income

Example: A retail store expects $50,000 in sales revenue monthly, with 70% collected within the same month and 30% in the following month.

Step 4: Identify Cash Outflows

List all expected cash payments, including:

- Supplier payments

- Payroll

- Rent and utilities

- Loan repayments

- Taxes

- Capital expenditures

Example: Monthly supplier payments total $30,000, payroll is $15,000, and rent is $5,000.

Step 5: Estimate Timing of Cash Flows

Determine when cash inflows and outflows will occur to avoid timing mismatches.

Example: Customer payments are received 30 days after invoicing; supplier payments are due within 45 days.

Step 6: Build the Forecast Model

Create a spreadsheet or use software to map inflows and outflows over the forecast period.

Mind Map: Cash Flow Forecast Model Structure

Example: Using the data, calculate net cash flow for each month and update the closing cash balance accordingly.

Step 7: Incorporate Assumptions and Adjustments

Document assumptions such as payment delays, seasonal fluctuations, or expected changes in sales.

Example: Assume a 10% increase in sales during holiday months and a 5-day delay in supplier payments.

Step 8: Validate and Review the Forecast

Cross-check the forecast against actual results periodically and adjust assumptions as needed.

Example: Compare forecasted cash inflows with actual receipts monthly to refine accuracy.

Step 9: Use the Forecast for Decision Making

Leverage the forecast to plan for:

- Managing working capital

- Scheduling payments

- Securing financing if needed

- Identifying potential cash shortages early

Example: If the forecast shows a cash shortfall in June, the financial controller arranges a short-term credit line in advance.

Practical Example: Monthly Cash Flow Forecast for a Retail Business

| Month | Opening Balance | Cash Inflows | Cash Outflows | Net Cash Flow | Closing Balance |

|---|---|---|---|---|---|

| January | $20,000 | $60,000 | $50,000 | $10,000 | $30,000 |

| February | $30,000 | $55,000 | $52,000 | $3,000 | $33,000 |

| March | $33,000 | $70,000 | $60,000 | $10,000 | $43,000 |

Note: The closing balance of each month becomes the opening balance of the next.

Additional Mind Map: Workflow for Building a Cash Flow Forecast

By following these steps and continuously refining your forecast with real data and updated assumptions, accountants and financial controllers can maintain a clear picture of their organization’s cash position, enabling proactive and confident financial management.

2.4 Using Historical Data and Trends for Forecasting

Accurate cash flow forecasting is essential for effective financial management, especially in finance and retail sectors where cash inflows and outflows can be highly variable. One of the most reliable ways to enhance the accuracy of your cash flow forecasts is by leveraging historical data and identifying trends over time. This section explores how to use historical data and trends in cash flow forecasting, supported by practical examples and mind maps.

Why Use Historical Data for Cash Flow Forecasting?

- Foundation for Predictions: Historical cash flow data provides a factual basis for estimating future cash movements.

- Identifying Patterns: Seasonal fluctuations, recurring expenses, and payment behaviors become visible.

- Improved Accuracy: Reduces guesswork by grounding forecasts in real past performance.

Steps to Use Historical Data and Trends in Forecasting

-

Collect Relevant Historical Data:

- Gather at least 12 months of cash inflow and outflow data.

- Include sales data, payment receipts, supplier payments, payroll, and other expenses.

-

Clean and Organize Data:

- Remove anomalies or one-time events that could skew trends.

- Categorize data by type (e.g., sales, operating expenses, capital expenditures).

-

Analyze Seasonal and Cyclical Trends:

- Identify months or quarters with consistently higher or lower cash flows.

- Understand industry-specific cycles (e.g., holiday sales spikes in retail).

-

Calculate Moving Averages and Growth Rates:

- Use moving averages to smooth out short-term fluctuations.

- Calculate month-over-month or year-over-year growth rates to project trends.

-

Incorporate External Factors:

- Adjust forecasts based on market conditions, economic indicators, or planned business changes.

-

Validate Forecasts Against Historical Outcomes:

- Compare forecasted cash flows with actual past results to refine assumptions.

Mind Map: Using Historical Data for Cash Flow Forecasting

Practical Example: Forecasting Cash Flow for a Retail Store Using Historical Data

Scenario: A retail store wants to forecast cash flow for the next quarter using the past 12 months of data.

Step 1: Data Collection

- Monthly sales revenue, supplier payments, payroll, rent, utilities, and marketing expenses were collected.

Step 2: Data Cleaning

- A one-time large equipment purchase was excluded from recurring expenses.

Step 3: Trend Analysis

- Sales showed a consistent 20% increase in November and December due to holiday shopping.

- Moving average of monthly sales was calculated to smooth fluctuations.

- Payroll expenses remained stable but increased by 10% in December due to seasonal hires.

Step 4: Forecasting

- November and December sales were projected with a 20% increase over the average monthly sales.

- Payroll expenses were adjusted upward for December.

- Supplier payments were forecasted based on average payment cycles.

Step 5: Validation

- The forecast was compared with the previous year’s actual cash flow for the same quarter, showing a 5% variance, which was acceptable.

Mind Map: Retail Store Cash Flow Forecasting Example

Additional Tips for Using Historical Data Effectively

- Use Granular Data: Weekly or daily data can reveal more precise trends than monthly aggregates.

- Segment Data by Product or Service: Different product lines may have distinct cash flow patterns.

- Incorporate Customer Payment Behavior: Analyze how quickly customers pay invoices to forecast receivables.

- Leverage Visualization Tools: Graphs and charts help identify trends and anomalies easily.

Summary

Using historical data and trends is a cornerstone of reliable cash flow forecasting. By systematically collecting, cleaning, and analyzing past cash flow data, accountants and financial controllers can create forecasts that reflect real business patterns. Incorporating seasonal trends, smoothing techniques like moving averages, and validating forecasts against actual results ensures forecasts are both realistic and actionable. This approach empowers finance professionals in retail and other sectors to make informed decisions that maintain healthy cash flow and support business growth.

2.5 Practical Example: Creating a Monthly Cash Flow Forecast for a Retail Business

Creating a monthly cash flow forecast is essential for retail businesses to anticipate cash shortages, plan for expenses, and make informed financial decisions. This section walks through a detailed, step-by-step example of building a cash flow forecast, complete with mind maps and practical illustrations.

Step 1: Gather Historical Data

Start by collecting historical data on cash inflows and outflows from previous months. This includes sales revenue, customer payments, supplier payments, operating expenses, and other cash movements.

Example:

- January sales: $50,000

- February sales: $55,000

- March sales: $52,000

- Average monthly sales: $52,333

Step 2: Identify Cash Inflows

Cash inflows typically include:

- Cash sales

- Credit sales collected

- Other income (e.g., interest, asset sales)

Mind Map: Cash Inflows

Example:

- Cash sales: 40% of total sales collected immediately

- Credit sales: 60% collected the following month

For April forecast:

- Cash sales = 40% * $53,000 (estimated sales) = $21,200

- Credit sales collected from March sales = 60% * $52,000 = $31,200

- Total cash inflows for April = $21,200 + $31,200 = $52,400

Step 3: Identify Cash Outflows

Cash outflows include:

- Payments to suppliers

- Operating expenses (rent, utilities, salaries)

- Loan repayments

- Capital expenditures

Mind Map: Cash Outflows

Example:

- Supplier payments: 50% paid in the month of purchase, 50% paid next month

- Operating expenses for April estimated at $15,000

- Loan repayment: $2,000

Supplier payments for April:

- 50% of April purchases (assumed $20,000) = $10,000

- 50% of March purchases (assumed $18,000) = $9,000

- Total supplier payments = $19,000

Total cash outflows for April = $19,000 + $15,000 + $2,000 = $36,000

Step 4: Calculate Net Cash Flow

Net cash flow = Total cash inflows - Total cash outflows

Example:

- Total inflows (April) = $52,400

- Total outflows (April) = $36,000

- Net cash flow = $52,400 - $36,000 = $16,400

Step 5: Consider Opening Cash Balance

Add the opening cash balance at the beginning of the month to the net cash flow to estimate the closing cash balance.

Example:

- Opening cash balance (April 1) = $10,000

- Closing cash balance (April 30) = $10,000 + $16,400 = $26,400

Step 6: Build the Monthly Cash Flow Forecast Table

| Description | Amount ($) |

|---|---|

| Opening Cash Balance | 10,000 |

| Cash Inflows | |

| Cash Sales | 21,200 |

| Credit Sales Collected | 31,200 |

| Total Inflows | 52,400 |

| Cash Outflows | |

| Supplier Payments | 19,000 |

| Operating Expenses | 15,000 |

| Loan Repayments | 2,000 |

| Total Outflows | 36,000 |

| Net Cash Flow | 16,400 |

| Closing Cash Balance | 26,400 |

Step 7: Analyze and Adjust

Use the forecast to identify potential cash shortfalls or surpluses. For example, if closing cash balance is projected to be low, consider:

- Negotiating extended payment terms with suppliers

- Accelerating receivables collection

- Reducing discretionary expenses

Mind Map: Cash Flow Adjustment Strategies

Summary

Creating a monthly cash flow forecast involves systematically estimating cash inflows and outflows based on historical data and expected changes. The example above demonstrates how a retail business can forecast cash flow for April, providing a clear picture of liquidity and enabling proactive financial management.

By regularly updating forecasts and integrating best practices such as early payment incentives and supplier negotiations, accountants and financial controllers can maintain healthy cash flow and support business growth.

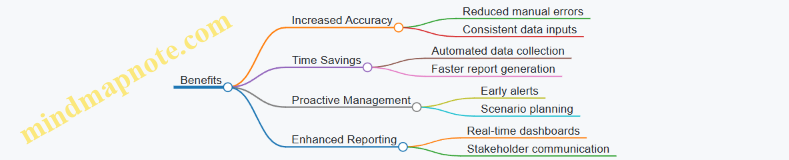

2.6 Tools and Software for Effective Cash Flow Forecasting

Effective cash flow forecasting relies heavily on the right tools and software that streamline data collection, analysis, and reporting. For accountants and financial controllers in finance and retail sectors, leveraging these technologies can significantly enhance accuracy, save time, and provide actionable insights.

Key Features to Look for in Cash Flow Forecasting Tools

- Automated Data Integration: Connects with accounting, sales, and banking systems to pull real-time data.

- Scenario Planning: Allows users to create multiple cash flow scenarios based on different assumptions.

- User-Friendly Dashboards: Visualizes cash inflows and outflows clearly for quick decision-making.

- Alerts and Notifications: Warns about potential cash shortages or overdue receivables.

- Collaboration Capabilities: Enables multiple stakeholders to contribute and review forecasts.

Popular Tools and Software Examples

| Tool Name | Description | Example Use Case |

|---|---|---|

| Float | Integrates with accounting software like Xero, QuickBooks; offers real-time cash flow views. | A retail store uses Float to monitor daily cash balances and adjust inventory purchases accordingly. |

| Fathom | Provides advanced financial analysis and forecasting with scenario modeling. | A financial controller creates multiple cash flow scenarios to prepare for seasonal sales fluctuations. |

| Pulse | Focuses on cash flow forecasting with customizable reports and alerts. | An accountant sets up alerts for overdue invoices to accelerate receivables collection. |

| PlanGuru | Offers budgeting, forecasting, and performance review tools. | A retail chain uses PlanGuru to combine sales forecasts with expense budgets for comprehensive cash flow planning. |

| Microsoft Excel + Add-ins | Widely used with customizable templates and add-ins for forecasting automation. | A financial controller builds a tailored cash flow model using Excel and automates data imports with Power Query. |

Mind Map: Selecting the Right Cash Flow Forecasting Tool

Example: Using Float for Retail Cash Flow Forecasting

- Setup: Connect Float to the retail business’s QuickBooks account.

- Data Sync: Automatically import historical sales, expenses, and bank transactions.

- Forecast Creation: Float generates a 13-week rolling cash flow forecast.

- Scenario Planning: The financial controller models the impact of a planned marketing campaign on cash inflows.

- Alerts: The system notifies the team of a projected cash shortfall two weeks ahead.

- Action: Adjust payment schedules and negotiate supplier terms to mitigate the shortfall.

Mind Map: Workflow Using Cash Flow Forecasting Software

Tips for Maximizing Software Effectiveness

- Regular Updates: Keep data synced daily or weekly to maintain forecast accuracy.

- Training: Ensure finance teams are trained on software features and best practices.

- Customization: Tailor dashboards and reports to highlight KPIs relevant to your retail or finance operations.

- Integration: Connect forecasting tools with ERP and CRM systems for holistic financial visibility.

- Review Cycles: Establish regular forecast review meetings to adjust assumptions and strategies.

By carefully selecting and effectively using cash flow forecasting tools, accountants and financial controllers can transform raw financial data into strategic insights, enabling proactive cash management and stronger financial health for their organizations.

3. Managing Receivables to Improve Cash Flow

3.1 Best Practices for Credit Management

Effective credit management is crucial for maintaining healthy cash flow, especially for accountants and financial controllers in the finance and retail sectors. Proper credit management ensures that your business minimizes bad debts, accelerates cash inflows, and maintains strong customer relationships.

Key Best Practices for Credit Management

Example 1: Establishing Clear Credit Policies in a Retail Business

A mid-sized retail chain sets a standard credit term of 30 days with a credit limit of $10,000 for new customers. They communicate these terms upfront during onboarding and include them on all invoices. Customers who consistently pay on time are eligible for extended terms of 45 days and higher credit limits, incentivizing good payment behavior.

Example 2: Using Credit Assessments to Minimize Risk

Before extending credit to a new wholesale customer, the finance team requests financial statements and reviews credit bureau reports. Based on the assessment, they approve a conservative credit limit of $5,000. This prevents overexposure and protects cash flow.

Example 3: Accelerating Receivables with Early Payment Discounts

A retailer offers a 2% discount if invoices are paid within 10 days instead of the usual 30. This encourages customers to pay faster, improving cash inflows. For example, a $1,000 invoice paid early nets $980 but improves liquidity significantly.

Mind Map: Credit Management Workflow

Mind Map: Benefits of Effective Credit Management

Practical Tips

- Always document credit agreements in writing.

- Use credit insurance for high-risk customers.

- Regularly communicate with customers about their account status.

- Integrate credit management with overall cash flow forecasting.

By implementing these best practices, accountants and financial controllers can significantly improve their organization’s cash flow stability and reduce the risk of payment defaults.

3.2 Setting Clear Payment Terms and Conditions

Effective cash flow management begins with establishing clear payment terms and conditions. These terms define when and how customers are expected to pay, directly impacting the timing of cash inflows. Ambiguity or poorly communicated terms can lead to delayed payments, disputes, and ultimately cash flow challenges.

Why Clear Payment Terms Matter

- Reduce Payment Delays: Clear terms set expectations upfront, minimizing confusion.

- Improve Customer Relationships: Transparent terms foster trust and professionalism.

- Enhance Cash Flow Predictability: Knowing when payments will arrive helps in forecasting.

- Mitigate Disputes: Well-defined conditions reduce disagreements over invoices.

Key Elements of Payment Terms and Conditions

Best Practices for Setting Payment Terms

-

Define Clear Due Dates: Specify exact payment deadlines (e.g., “Net 30 days” means payment due 30 days after invoice date).

-

Communicate Terms Upfront: Include terms in contracts, purchase orders, and invoices.

-

Offer Multiple Payment Options: Facilitate faster payments by accepting various methods.

-

Incorporate Incentives and Penalties: Encourage early payments with discounts (e.g., 2% off if paid within 10 days) and discourage late payments with fees.

-

Specify Currency and Taxes: Avoid confusion in international transactions by clarifying currency and tax responsibilities.

-

Provide Clear Invoicing Instructions: Detail what information invoices must contain to be processed.

-

Establish Dispute Resolution Process: Outline steps and contacts for handling payment disagreements.

Practical Example: Setting Payment Terms for a Retail Supplier

Scenario: A retail supplier wants to set payment terms that encourage timely payments while maintaining good client relationships.

- Payment Terms: Net 30 days from invoice date.

- Early Payment Discount: 2% discount if paid within 10 days.

- Late Payment Penalty: 1.5% monthly interest on overdue balances.

- Payment Methods Accepted: Bank transfer, credit card, and digital wallets.

- Invoice Frequency: Monthly, with detailed itemized invoices.

- Currency: USD, taxes included as per local regulations.

- Dispute Resolution: Customers must notify within 10 days of invoice receipt; disputes resolved within 30 days.

Outcome: This clear structure helps the supplier predict cash inflows and reduces late payments.

Mind Map: Example Payment Terms Breakdown

Additional Example: Simplified Payment Terms for Small Retailers

- Payment Due: Upon receipt of invoice.

- Payment Methods: Cash, credit card.

- No Discounts or Penalties: To keep terms simple.

- Invoice Delivery: At point of sale or via email immediately.

This approach suits small retailers with frequent, low-value transactions where simplicity aids faster payments.

Tips for Accountants and Financial Controllers

- Regularly review and update payment terms to reflect market conditions.

- Train sales and customer service teams to communicate terms clearly.

- Use automated invoicing systems to embed terms and track compliance.

- Monitor payment patterns and adjust terms or incentives accordingly.

Summary

Setting clear payment terms and conditions is a foundational best practice in cash flow management. By defining precise due dates, accepted payment methods, discounts, penalties, and dispute processes, finance professionals can reduce payment delays, improve cash flow predictability, and maintain strong customer relationships.

3.3 Strategies to Accelerate Receivables Collection

Efficient receivables collection is crucial for maintaining healthy cash flow, especially in finance and retail sectors where timely cash inflows support ongoing operations and growth. Accelerating receivables collection reduces the days sales outstanding (DSO), improves liquidity, and minimizes the risk of bad debts.

Key Strategies to Accelerate Receivables Collection

Clear and Transparent Payment Terms

Setting clear payment terms upfront helps customers understand their obligations and reduces confusion that can delay payments.

Example: A retail company includes payment terms such as “Net 30 days” and clearly states a 2% penalty for payments delayed beyond 30 days on every invoice. This clarity encourages customers to prioritize payments.

Early Payment Incentives

Offering discounts or rewards for early payments motivates customers to pay before the due date.

Example: A finance firm offers a 1.5% discount if payment is made within 10 days instead of the standard 30 days. This practice not only accelerates cash inflow but also builds goodwill.

Automated and Timely Invoicing

Automating invoicing ensures invoices are sent promptly and reduces human errors.

Example: A retail chain uses cloud-based invoicing software that automatically generates and emails invoices immediately after a sale, reducing delays caused by manual processing.

Proactive Follow-up and Reminders

Regular, polite reminders help keep payments top of mind for customers.

Example: An accounting team sets up an automated reminder system that sends an email 7 days before the due date, on the due date, and a follow-up call 7 days after if payment is not received.

Flexible Payment Options

Providing multiple payment methods and installment plans can remove barriers to payment.

Example: A retail business accepts credit cards, bank transfers, and digital wallets, allowing customers to choose their preferred payment method. They also offer installment plans for large orders, making payments manageable.

Conducting Credit Checks and Setting Limits

Assessing customer creditworthiness before extending credit reduces the risk of late or non-payment.

Example: A finance company runs credit checks on new clients and sets credit limits based on their financial health, ensuring exposure is controlled.

Efficient Dispute Resolution

Quickly addressing invoice disputes prevents delays in payment.

Example: A retail firm assigns a dedicated team to handle billing queries and disputes, responding within 24 hours to resolve issues and keep payments on track.

Summary Mind Map

By integrating these strategies, accountants and financial controllers can significantly improve cash inflows, reduce outstanding receivables, and strengthen overall cash flow management.

3.4 Practical Example: Implementing Early Payment Discounts in Retail

Early payment discounts are a strategic tool used by retailers to accelerate cash inflows by incentivizing customers or clients to pay their invoices ahead of the due date. This practice not only improves cash flow but also reduces the risk of late payments and bad debts.

What is an Early Payment Discount?

An early payment discount is a reduction in the invoice amount offered to customers who pay before the agreed payment terms expire. For example, a retailer might offer a 2% discount if payment is made within 10 days instead of the usual 30 days.

Why Use Early Payment Discounts?

- Accelerate cash inflows: Improves liquidity and working capital.

- Reduce credit risk: Encourages timely payments, lowering the chance of defaults.

- Strengthen customer relationships: Provides value to customers who pay promptly.

Step-by-Step Implementation in Retail

-

Analyze Current Payment Terms and Cash Flow Needs

- Review existing payment terms and average collection periods.

- Identify cash flow gaps or periods of tight liquidity.

-

Determine Discount Rate and Time Frame

- Common practice: 2% discount if paid within 10 days (2/10 Net 30).

- Ensure discount amount balances the cost of offering it versus cash flow benefits.

-

Communicate Terms Clearly

- Update invoices to prominently display early payment discount terms.

- Inform customers via email, website, or account managers.

-

Monitor and Track Payments

- Use accounting software to track who takes advantage of discounts.

- Analyze impact on cash flow and profitability.

-

Adjust Strategy as Needed

- If uptake is low, consider increasing discount or shortening the payment window.

- If too many customers use the discount, assess impact on margins.

Mind Map: Implementing Early Payment Discounts

Example Scenario: Retail Clothing Store

Background: A retail clothing chain typically offers net 30 payment terms to wholesale buyers. The average collection period is 35 days, causing occasional cash flow shortages during peak inventory purchase periods.

Implementation:

- The financial controller proposes a 2% early payment discount if invoices are paid within 10 days.

- Invoices are updated to include: “2% discount if paid within 10 days, otherwise net 30.”

- Customers are informed via email and account managers.

Results after 3 months:

- 40% of customers take advantage of the discount.

- Average collection period reduces from 35 days to 25 days.

- Cash flow improves, enabling timely inventory purchases without additional financing.

- The cost of discounts is offset by savings on interest and improved supplier terms.

Mind Map: Example Scenario Breakdown

Additional Tips for Accountants and Financial Controllers

- Evaluate Customer Segments: Offer discounts selectively to customers with good payment history or high invoice volumes.

- Use Technology: Automate discount calculations and reminders through accounting software.

- Monitor Profit Margins: Ensure discounts do not erode profitability; consider the trade-off between margin and cash flow.

- Legal and Contractual Considerations: Ensure discount terms comply with contracts and local regulations.

Summary

Implementing early payment discounts in retail is a practical and effective cash flow management technique. By carefully designing discount terms, communicating clearly, and monitoring results, financial controllers can accelerate receivables, reduce credit risk, and ultimately strengthen the financial health of their retail operations.

3.5 Using Technology to Automate Invoicing and Follow-ups

Efficient invoicing and timely follow-ups are critical components of effective cash flow management. Manual processes can lead to delays, errors, and missed payments, which negatively impact cash inflows. Leveraging technology to automate these tasks not only reduces administrative burden but also accelerates cash collection and improves accuracy.

Benefits of Automating Invoicing and Follow-ups

- Speed: Automated systems generate and send invoices instantly after a sale or service delivery.

- Accuracy: Reduces human errors in invoice details, calculations, and data entry.

- Consistency: Ensures invoices and reminders are sent on schedule without fail.

- Tracking: Provides real-time visibility into invoice status and payment progress.

- Improved Cash Flow: Faster invoicing and follow-ups lead to quicker payments.

Key Features to Look for in Automation Tools

- Invoice creation and customization

- Automated invoice delivery (email, portal, etc.)

- Scheduled payment reminders and follow-ups

- Integration with accounting and ERP systems

- Payment gateway integration for online payments

- Reporting and analytics dashboards

Mind Map: Automating Invoicing and Follow-ups

Practical Example: Implementing Automated Invoicing in a Retail Business

Scenario: A mid-sized retail chain struggles with delayed payments due to manual invoicing and inconsistent follow-ups.

Solution: They adopt an invoicing automation tool integrated with their ERP system.

Steps Taken:

- Invoice Templates: Customized templates reflecting branding and legal requirements.

- Auto-generation: Invoices auto-created immediately after order fulfillment.

- Automated Delivery: Invoices emailed to customers instantly.

- Payment Reminders: Automated reminders sent 7 days before due date, on due date, and 7 days after if unpaid.

- Escalation: If payment is overdue by 14 days, alerts sent to the finance team for manual follow-up.

Outcome:

- Invoice processing time reduced by 70%.

- Average days sales outstanding (DSO) decreased from 45 to 30 days.

- Cash flow improved due to faster collections.

Mind Map: Retail Business Automated Invoicing Workflow

Tools and Platforms to Consider

- QuickBooks: Offers automated invoicing, reminders, and integrates with payment gateways.

- Xero: Cloud-based accounting with automated billing and follow-ups.

- FreshBooks: User-friendly invoicing automation with customizable reminders.

- Zoho Invoice: Automation with multi-channel delivery and CRM integration.

- SAP Concur: For larger enterprises needing robust automation and analytics.

Tips for Successful Automation

- Ensure data accuracy before automating to avoid errors.

- Customize messaging to maintain a professional and personal tone.

- Monitor automation reports regularly to identify bottlenecks.

- Train finance teams on using automation tools effectively.

- Combine automation with human touch for complex or high-value accounts.

By integrating technology to automate invoicing and follow-ups, accountants and financial controllers in finance and retail sectors can significantly enhance cash flow management, reduce administrative overhead, and foster better customer payment behavior.

3.6 Handling Late Payments and Bad Debts Effectively

Managing late payments and bad debts is crucial for maintaining healthy cash flow, especially in finance and retail sectors where cash inflows directly impact operational stability. This section explores practical strategies, supported by examples and mind maps, to help accountants and financial controllers minimize the risks and impacts of delayed payments and uncollectible debts.

Understanding Late Payments and Bad Debts

- Late Payments: When customers or clients fail to pay invoices by the due date.

- Bad Debts: Amounts that are deemed uncollectible after exhaustive recovery efforts.

Both can strain cash flow, increase borrowing needs, and affect profitability.

Mind Map: Causes of Late Payments and Bad Debts

Best Practices for Handling Late Payments

-

Clear Payment Terms and Communication

- Define payment deadlines, penalties, and incentives upfront.

- Example: A retail company includes a 2% early payment discount if paid within 10 days, encouraging prompt payment.

-

Automated Invoicing and Reminders

- Use software to send invoices promptly and automated reminders before and after due dates.

- Example: Financial controllers implement an automated system that sends reminders at 5 days before due date, on due date, and 3 days after.

-

Flexible Payment Options

- Offer multiple payment methods (credit card, bank transfer, digital wallets).

- Example: A retailer adds mobile payment options, reducing friction and speeding up collections.

-

Early Engagement on Overdue Accounts

- Contact customers immediately after missed payments to understand issues.

- Example: An accountant calls clients within 48 hours of a missed payment to negotiate payment plans.

-

Incentivize Early Payments and Penalize Late Ones

- Discounts for early payments and interest or fees for late payments.

- Example: A retail chain charges a 1.5% monthly late fee after 30 days overdue.

Mind Map: Steps to Manage Late Payments

Handling Bad Debts Effectively

-

Rigorous Credit Assessment Before Sale

- Evaluate customer creditworthiness using credit reports and payment history.

- Example: A financial controller requires all new retail clients to pass a credit check before extending payment terms.

-

Regular Review of Accounts Receivable Aging

- Identify overdue accounts early and classify risk levels.

- Example: Weekly reports highlight invoices overdue by 30, 60, and 90+ days for prioritized action.

-

Establish a Clear Bad Debt Policy

- Define thresholds and timelines for writing off bad debts.

- Example: Debts unpaid after 120 days with no response are reviewed for write-off.

-

Use of Collection Agencies and Legal Action

- Outsource difficult collections or pursue legal remedies when cost-effective.

- Example: A retail business engages a collection agency for debts over $5,000 unpaid after 90 days.

-

Provisioning and Financial Reporting

- Create provisions for expected bad debts to reflect realistic financial positions.

- Example: Monthly adjustments to the allowance for doubtful accounts based on aging analysis.

Mind Map: Bad Debt Management Framework

Practical Example: Retail Chain Handling Late Payments and Bad Debts

Scenario: A mid-sized retail chain experiences increasing late payments from wholesale clients, affecting monthly cash flow.

Actions Taken:

- Implemented automated invoicing with payment reminders.

- Introduced early payment discounts (2% if paid within 10 days).

- Conducted credit checks on new clients and reviewed terms for existing ones.

- Set up a dedicated collections team to follow up on overdue accounts within 7 days of due date.

- Established a bad debt policy to write off debts unpaid after 150 days.

Outcome:

- Reduced average days sales outstanding (DSO) from 60 to 35 days.

- Decreased bad debt write-offs by 40% within one year.

- Improved cash flow predictability and reduced reliance on short-term financing.

Summary

Effectively handling late payments and bad debts requires a proactive, structured approach combining clear policies, technology, communication, and continuous monitoring. By integrating these best practices, accountants and financial controllers can safeguard cash flow, reduce financial risks, and contribute to the overall financial health of their organizations.

4. Controlling Payables Without Jeopardizing Supplier Relationships

4.1 Understanding Payment Terms and Negotiation Techniques

Effective management of payables is crucial for maintaining healthy cash flow, especially in finance and retail sectors where timing of payments can significantly impact liquidity. Understanding payment terms and mastering negotiation techniques empower accountants and financial controllers to optimize cash outflows without damaging supplier relationships.

What Are Payment Terms?

Payment terms define the conditions under which a buyer agrees to pay a supplier for goods or services. These terms specify:

- Payment period: The number of days allowed to pay the invoice (e.g., Net 30, Net 60).

- Discounts: Incentives for early payment (e.g., 2/10 Net 30 means 2% discount if paid within 10 days, otherwise full payment due in 30 days).

- Penalties: Late payment fees or interest charges.

Mind Map: Components of Payment Terms

Common Payment Terms Explained

| Term | Description | Example |

|---|---|---|

| Net 30 | Full payment due within 30 days of invoice | Invoice dated Jan 1, due Jan 31 |

| 2/10 Net 30 | 2% discount if paid within 10 days, else full in 30 days | Pay by Jan 11 for discount, else Jan 31 full payment |

| Due on Receipt | Payment due immediately upon receiving invoice | Invoice received Jan 1, payment due immediately |

Why Are Payment Terms Important?

- Cash Flow Timing: They determine when cash leaves your business.

- Supplier Relationships: Clear terms prevent disputes.

- Negotiation Leverage: Flexible terms can improve working capital.

Negotiation Techniques to Optimize Payment Terms

Negotiating payment terms is a strategic skill. Here are some effective techniques:

- Understand Supplier Needs: Know their cash flow pressures and flexibility.

- Leverage Purchase Volume: Larger or repeat orders can justify extended terms.

- Propose Win-Win Solutions: For example, offer faster payment in exchange for discounts.

- Use Market Benchmarks: Reference industry standards to support your requests.

- Build Strong Relationships: Trust facilitates better negotiations.

- Be Transparent: Share your cash flow constraints honestly.

Mind Map: Payment Terms Negotiation Techniques

Practical Example: Negotiating Extended Payment Terms with a Supplier

Scenario: A retail company regularly orders inventory from a supplier with standard Net 15 payment terms, but the company’s cash flow cycle requires more time to convert inventory into sales.

Steps Taken:

- The financial controller reviews payment history and confirms timely payments.

- They prepare data showing consistent order volume and prompt payments.

- During negotiation, they propose extending terms to Net 45, explaining the cash flow cycle.

- To balance the supplier’s risk, they offer to increase order volume by 10%.

- Supplier agrees to Net 45 terms, improving the retailer’s cash flow without harming the supplier’s business.

Outcome: The retailer gains more breathing room to manage cash outflows, while the supplier benefits from increased sales.

Additional Tips for Negotiating Payment Terms

- Always get negotiated terms in writing.

- Review and renegotiate terms periodically.

- Consider partial payments if full extension is not possible.

- Use technology to track payment deadlines and avoid penalties.

Summary

Understanding payment terms and mastering negotiation techniques are vital for financial controllers and accountants aiming to optimize cash flow. By clearly defining terms and strategically negotiating with suppliers, businesses can improve liquidity while maintaining strong supplier relationships.

References:

- Example: 2/10 Net 30 payment term explained Investopedia

- Negotiation strategies for payment terms Harvard Business Review

4.2 Prioritizing Payments to Optimize Cash Outflows

Efficiently managing payables is crucial for maintaining a healthy cash flow, especially in finance and retail sectors where timing and relationships matter. Prioritizing payments involves strategically deciding which bills to pay first to optimize cash outflows without damaging supplier relationships or incurring penalties.

Why Prioritize Payments?

- Maintain Supplier Relationships: Timely payments ensure trust and may lead to better terms.

- Avoid Late Fees and Penalties: Prioritizing helps prevent unnecessary costs.

- Maximize Cash Availability: Delaying non-critical payments preserves cash for urgent needs.

- Leverage Discounts: Early payments can sometimes unlock discounts.

Key Factors to Consider When Prioritizing Payments

Step-by-Step Approach to Prioritize Payments

- List All Payables: Gather all outstanding invoices with due dates and terms.

- Categorize Suppliers: Identify strategic suppliers vs. less critical ones.

- Analyze Payment Terms: Note discounts, due dates, and penalties.

- Assess Cash Position: Review current and forecasted cash availability.

- Rank Payments: Prioritize based on urgency, cost implications, and relationship impact.

- Schedule Payments: Align payments with cash flow forecasts.

Practical Example: Prioritizing Payments in a Retail Business

Scenario: A retail chain has $50,000 available in cash and $70,000 in payables due this month. The payables include:

| Supplier | Amount | Due Date | Early Payment Discount | Penalty for Late Payment | Relationship Importance |

|---|---|---|---|---|---|

| Inventory Supplier | $30,000 | 10th May | 2% if paid by 5th May | 5% penalty after 10th | High |

| Utilities | $5,000 | 15th May | None | Service cut-off | Medium |

| Marketing Agency | $10,000 | 20th May | None | None | Low |

| Office Supplies | $25,000 | 25th May | 1% if paid by 20th May | 3% penalty after 25th | Medium |

Prioritization:

- Pay Inventory Supplier early to capture 2% discount and maintain strong relationship.

- Pay Utilities on or before 15th to avoid service disruption.

- Delay Office Supplies payment close to 25th to maximize cash availability but before penalty.

- Schedule Marketing Agency payment last as no penalties or discounts apply.

Mind Map: Payment Prioritization Example

Tips for Accountants and Financial Controllers

- Automate Payables Management: Use software to flag priority payments and due dates.

- Communicate with Suppliers: Negotiate payment terms where possible.

- Regularly Review Cash Flow: Adjust payment priorities based on updated forecasts.

- Document Payment Policies: Ensure consistent prioritization across teams.

By strategically prioritizing payments, finance professionals can optimize cash outflows, maintain strong supplier relationships, and improve overall financial health.

4.3 Practical Example: Negotiating Extended Payment Terms with Suppliers

Negotiating extended payment terms with suppliers is a strategic approach to improving cash flow without compromising supplier relationships. This practice allows businesses, especially in retail and finance sectors, to delay cash outflows, thereby freeing up working capital for other operational needs.

Why Negotiate Extended Payment Terms?

- Improve liquidity: More time to collect receivables before paying suppliers.

- Enhance cash flow stability: Helps manage timing mismatches between inflows and outflows.

- Build stronger supplier partnerships: Transparent negotiations can foster trust.

Step-by-Step Negotiation Process

Example Scenario: Retail Business Negotiates with Supplier

Context: A mid-sized retail chain is experiencing seasonal cash flow pressure and wants to extend payment terms from 30 to 60 days with a key supplier.

Step 1: Preparation

- The finance controller reviews the current payment schedule and cash flow forecasts.

- They identify that extending payment terms by 30 days could ease short-term cash constraints.

- Research shows the supplier has a stable financial position.

Step 2: Proposal

- The controller drafts a proposal highlighting:

- Commitment to increase order volume by 15% over the next quarter.

- Benefits of a long-term partnership.

Step 3: Communication

- The controller schedules a video call with the supplier’s account manager.

- Presents the proposal emphasizing mutual benefits.

Step 4: Negotiation

- Supplier expresses concern about cash flow impact.

- Controller offers to pay 50% of invoices within 30 days and the remaining 50% within 60 days.

- Supplier agrees to trial this arrangement for 3 months.

Step 5: Agreement

- Both parties sign an addendum to the contract reflecting the new terms.

Step 6: Follow-up

- Controller monitors payments and supplier satisfaction.

- After successful trial, full 60-day terms are adopted.

Mind Map: Negotiation Outcome Options

Additional Tips for Successful Negotiation

- Build rapport: Establish trust before discussing terms.

- Be transparent: Share legitimate reasons for requesting extension.

- Offer value: Propose incentives like larger orders or faster payments on select invoices.

- Document everything: Ensure all agreed terms are clearly recorded.

- Stay flexible: Be open to compromise to maintain good relationships.

Summary

Negotiating extended payment terms is a practical and effective method to optimize cash flow. By preparing thoroughly, communicating clearly, and offering mutual benefits, financial controllers and accountants can secure terms that support business liquidity while preserving supplier partnerships.

4.4 Leveraging Early Payment Discounts Without Straining Cash Flow

Early payment discounts are a valuable tool for improving a company’s profitability by reducing expenses. However, taking advantage of these discounts requires careful cash flow management to avoid liquidity issues. This section explores best practices and practical examples to help accountants and financial controllers leverage early payment discounts effectively without compromising cash flow stability.

Understanding Early Payment Discounts

Early payment discounts are incentives offered by suppliers to encourage buyers to pay invoices before the due date. Common terms include “2/10 net 30,” meaning a 2% discount if paid within 10 days, otherwise full payment is due in 30 days.

Benefits:

- Cost savings through reduced invoice amounts

- Strengthened supplier relationships

- Potential for improved credit terms in the future

Risks:

- Cash flow strain if payments are made too early without sufficient liquidity

- Opportunity cost of using cash that could be allocated elsewhere

Mind Map: Key Considerations for Leveraging Early Payment Discounts

Best Practices with Examples

-

Forecast Cash Flow Accurately Before Committing to Early Payments

Example: A retail company forecasts a cash inflow of $100,000 in 7 days but has an early payment discount deadline in 5 days. Instead of paying early and risking a shortfall, they negotiate with the supplier to extend the discount period by 3 days, aligning payment with cash availability.

-

Calculate the Effective Annualized Return of the Discount

Example: A supplier offers 2% discount if paid in 10 days (2/10 net 30). The cost of capital is 8% annually.

- Discount = 2%

- Days saved = 20 days (30 - 10)

- Annualized return = (2% / 98%) * (365 / 20) ≈ 37.24%

Since 37.24% > 8%, taking the discount is financially beneficial if cash is available.

-

Prioritize Payments to Suppliers Offering the Highest Discounts

Example: A financial controller reviews multiple invoices and prioritizes paying a supplier offering 3% discount over another offering 1%, maximizing savings without increasing cash outflow.

-

Use Payment Automation Tools to Ensure Timely Payments

Example: An accounting team implements an automated accounts payable system that flags invoices eligible for early payment discounts and schedules payments accordingly, reducing manual errors and missed discounts.

-

Negotiate Flexible Terms or Partial Discounts

Example: A retailer negotiates with a supplier to split payments, paying 50% early to capture half the discount and the remainder on the standard due date, easing cash flow pressure.

Mind Map: Step-by-Step Approach to Implement Early Payment Discounts

Practical Example: Retail Chain Leveraging Early Payment Discounts

Scenario: A retail chain receives invoices totaling $500,000 monthly with various early payment discount terms. The finance team forecasts cash inflows and identifies two weeks each month with surplus cash.

Actions:

- They map out all discount deadlines and prioritize payments within the surplus cash periods.

- For suppliers with high discounts but early deadlines, they negotiate extended discount periods.

- Implement an automated payment system to schedule payments precisely.

Outcome:

- The company captures $8,000 in discounts monthly without overdrawing cash accounts.

- Supplier relationships improve due to consistent and timely payments.

Summary

Leveraging early payment discounts can significantly reduce costs, but it requires a disciplined approach to cash flow management. By forecasting cash availability, prioritizing discounts with the highest returns, negotiating flexible terms, and utilizing automation, accountants and financial controllers can maximize savings without risking liquidity.

4.5 Using Payables Automation to Avoid Late Fees and Improve Accuracy

Managing payables efficiently is crucial for maintaining healthy cash flow and strong supplier relationships. Manual processes often lead to errors, missed deadlines, and late fees, which can strain finances and damage credibility. Payables automation offers a solution by streamlining invoice processing, approvals, and payments, reducing errors, and ensuring timely payments.

What is Payables Automation?

Payables automation refers to the use of software solutions to automate the entire accounts payable process—from invoice receipt and validation to approval workflows and payment execution.

Key Benefits:

- Reduces manual data entry errors

- Accelerates invoice processing times

- Ensures compliance with payment terms

- Improves cash flow visibility

- Minimizes late payment penalties

Mind Map: Benefits of Payables Automation

How Payables Automation Works

- Invoice Capture: Invoices are received electronically or scanned and converted into digital data using OCR (Optical Character Recognition).

- Validation: The system cross-checks invoice data against purchase orders and contracts to ensure accuracy.

- Approval Workflow: Automated routing sends invoices to the appropriate approvers based on predefined rules.

- Payment Scheduling: Once approved, payments are scheduled according to due dates, optimizing cash flow.

- Payment Execution: Payments are processed electronically via ACH, wire transfer, or other methods.

- Reporting: Dashboards provide real-time visibility into payables status and cash flow impact.

Practical Example: Implementing Payables Automation in a Retail Finance Department

Scenario: A retail chain was facing frequent late payment fees due to manual invoice processing delays and lost paperwork.

Solution: They implemented an accounts payable automation platform integrated with their ERP system.

Results:

- Invoice processing time reduced from 10 days to 2 days.

- Late fees dropped by 90% within the first quarter.

- Early payment discounts increased by 25% due to timely payments.

- Staff reallocated from manual data entry to strategic financial analysis.

Mind Map: Steps to Implement Payables Automation

Tips for Maximizing the Benefits of Payables Automation

- Encourage suppliers to submit electronic invoices: This reduces manual entry and speeds up processing.

- Set up automated reminders and alerts: Notify approvers of pending invoices to avoid delays.

- Leverage early payment discount opportunities: Automation helps identify and act on these promptly.

- Integrate with cash flow forecasting tools: Provides a holistic view of upcoming cash outflows.

- Regularly review and update approval workflows: Ensure they remain efficient and aligned with organizational changes.

Example Mind Map: Avoiding Late Fees Through Automation

By adopting payables automation, accountants and financial controllers in retail and finance sectors can significantly reduce errors, avoid costly late fees, and improve overall cash flow management. The integration of automation tools not only streamlines operations but also empowers teams to focus on strategic financial planning and supplier relationship management.

4.6 Balancing Payables with Cash Flow Needs in Retail Operations

Balancing payables with cash flow needs is a critical challenge for retail operations, where maintaining liquidity while honoring supplier commitments can directly impact business continuity and profitability. Effective management ensures that retailers can meet their obligations without straining their cash reserves, enabling smooth operations and fostering strong supplier relationships.

Key Considerations in Balancing Payables and Cash Flow

- Payment Terms Optimization: Negotiating favorable payment terms (e.g., net 30, net 60) to align outflows with inflows.

- Cash Flow Forecasting: Anticipating cash availability to schedule payments strategically.

- Prioritization of Payables: Identifying critical suppliers and prioritizing payments accordingly.

- Utilizing Early Payment Discounts: Weighing the benefits of discounts against cash availability.

- Automation and Scheduling: Leveraging technology to optimize payment timing and avoid late fees.

Mind Map: Balancing Payables with Cash Flow Needs

Practical Example: Scheduling Payables to Match Cash Inflows

Scenario: A retail store receives major customer payments on the 10th and 25th of each month but has supplier invoices due on the 5th, 15th, and 20th.

Approach:

- Negotiate with suppliers for payment terms that allow payment after the 10th or 25th.