Financial Restructuring for Accountants

1. Introduction to Financial Restructuring

1.1 Understanding Financial Restructuring: Definitions and Scope

Financial restructuring is a strategic process undertaken by companies to reorganize their financial assets, liabilities, and capital structure to improve liquidity, solvency, and overall financial health. It often occurs when a company faces financial distress or aims to optimize its financial framework for growth and sustainability.

Definition of Financial Restructuring

Financial restructuring involves revising the composition of a company’s debt and equity, renegotiating terms with creditors, and sometimes altering ownership structures to restore financial stability. It is distinct from operational restructuring, which focuses on improving business operations.

Scope of Financial Restructuring

The scope covers a wide range of activities including:

- Debt rescheduling or refinancing

- Debt-for-equity swaps

- Asset sales to raise capital

- Capital injection from new or existing investors

- Modification of loan covenants

- Negotiation with creditors and stakeholders

Mind Map: Core Components of Financial Restructuring

Why Financial Restructuring is Important

- Restore Liquidity: Ensures the company has enough cash flow to meet short-term obligations.

- Improve Solvency: Reduces debt burden to sustainable levels.

- Enhance Creditworthiness: Positions the company better for future financing.

- Support Strategic Goals: Aligns financial structure with long-term business objectives.

Example 1: Debt Restructuring in a Retail Chain

A retail chain facing declining sales and high-interest debt negotiated with its lenders to extend loan maturities and reduce interest rates. This improved cash flow allowed the company to invest in e-commerce, stabilizing operations and avoiding bankruptcy.

Example 2: Debt-for-Equity Swap in a Manufacturing Firm

A manufacturing company burdened by excessive debt converted a portion of its debt into equity held by creditors. This reduced interest expenses and aligned creditors’ interests with the company’s success, enabling operational turnaround.

Mind Map: Typical Triggers for Financial Restructuring

Summary

Financial restructuring is a critical tool for accountants and restructuring advisors to help companies navigate financial challenges. Understanding its definitions and scope enables professionals to identify when restructuring is necessary and what strategies to employ for optimal outcomes.

1.2 The Role of Accountants and Restructuring Advisors

Financial restructuring is a complex process that requires the expertise of various professionals, among whom accountants and restructuring advisors play pivotal roles. Their combined skills ensure that distressed companies can navigate financial challenges effectively, maintain compliance, and optimize outcomes for all stakeholders.

Key Responsibilities of Accountants in Financial Restructuring

- Financial Analysis and Diagnosis: Accountants analyze financial statements to identify distress signals such as liquidity shortages, covenant breaches, or declining profitability.

- Cash Flow Management: They monitor and forecast cash flows to ensure the company can meet its obligations during restructuring.

- Accounting Treatment and Reporting: Accountants ensure that all restructuring transactions are accurately recorded and disclosed according to relevant accounting standards.

- Tax Implications: They assess the tax consequences of restructuring actions to optimize tax efficiency.

- Compliance and Controls: Maintaining internal controls and compliance with regulatory requirements throughout the restructuring process.

Key Responsibilities of Restructuring Advisors

- Strategic Planning: Advisors develop restructuring strategies tailored to the company’s unique challenges and goals.

- Stakeholder Negotiation: They act as intermediaries between the company, creditors, investors, and other stakeholders to negotiate terms.

- Operational Improvements: Identifying cost-saving measures and operational efficiencies to improve financial health.

- Legal and Regulatory Guidance: Advisors work closely with legal teams to navigate insolvency laws and restructuring frameworks.

- Implementation Support: Overseeing the execution of restructuring plans and adjusting strategies as needed.

Mind Map: Roles and Responsibilities

How Accountants and Restructuring Advisors Collaborate

The collaboration between accountants and restructuring advisors is essential for a successful restructuring process. Accountants provide the financial data, analysis, and compliance framework that advisors use to craft and negotiate restructuring plans.

-

Example: In a retail company facing declining sales and mounting debt, accountants identify cash flow shortfalls and covenant breaches. Restructuring advisors then use this data to negotiate debt rescheduling with creditors while recommending operational changes such as store closures and inventory optimization.

-

Example: For a manufacturing firm, accountants prepare detailed financial models forecasting post-restructuring scenarios. Advisors leverage these models to convince stakeholders of the viability of a debt-for-equity swap.

Mind Map: Collaboration Workflow

Practical Example: Turnaround of a Mid-Sized Technology Company

Scenario: A technology company experiences rapid revenue decline due to market disruption and struggles to service its debt.

- Accountants’ Role: They conduct a thorough review of financial statements, identify liquidity gaps, and prepare cash flow forecasts highlighting critical periods.

- Restructuring Advisors’ Role: Using the accountants’ analysis, advisors propose a refinancing plan involving extended maturities and partial debt forgiveness.

- Outcome: The company successfully negotiates with creditors, implements cost-cutting measures, and stabilizes operations.

This example illustrates how accountants provide the factual financial foundation, while restructuring advisors drive strategic negotiations and operational changes.

Best Practices for Accountants and Restructuring Advisors

- Maintain clear and continuous communication to ensure alignment.

- Use transparent and realistic financial data to build trust with stakeholders.

- Stay updated on regulatory changes affecting restructuring.

- Document all decisions and assumptions thoroughly.

- Foster a collaborative environment that leverages the strengths of both roles.

In summary, accountants and restructuring advisors are complementary forces in financial restructuring. Accountants bring precision, compliance, and financial insight, while restructuring advisors contribute strategic vision, negotiation skills, and operational expertise. Together, they form the backbone of successful restructuring initiatives.

1.3 Key Objectives and Benefits of Financial Restructuring

Financial restructuring is a critical process aimed at improving a company’s financial health and ensuring long-term sustainability. For accountants and restructuring advisors, understanding the core objectives and benefits is essential to guide businesses through challenging periods effectively.

Key Objectives of Financial Restructuring

Financial restructuring focuses on several primary goals that help stabilize and revitalize a company’s financial standing:

- Improve Liquidity and Cash Flow

- Reduce Debt Burden

- Optimize Capital Structure

- Enhance Operational Efficiency

- Restore Stakeholder Confidence

- Ensure Compliance and Risk Mitigation

Below is a mind map illustrating these objectives:

Benefits of Financial Restructuring

When executed effectively, financial restructuring delivers multiple benefits that can transform a distressed company into a viable and competitive entity.

-

Improved Financial Stability

- Example: A manufacturing company facing cash shortages restructured its debt by extending payment terms, which improved liquidity and allowed uninterrupted operations.

-

Enhanced Creditworthiness

- Example: After restructuring, a retail chain improved its debt-to-equity ratio, leading to better credit ratings and easier access to financing.

-

Increased Operational Flexibility

- Example: A service provider reduced fixed costs through operational restructuring, enabling quicker adaptation to market changes.

-

Preservation of Business Value

- Example: By negotiating with creditors and avoiding bankruptcy, a technology firm preserved its brand reputation and customer base.

-

Stakeholder Alignment and Confidence

- Example: Transparent communication during restructuring helped a construction company maintain investor trust and secure additional funding.

-

Long-Term Growth Potential

- Example: Post-restructuring, a healthcare provider reinvested savings into innovation, driving sustainable growth.

Here is a mind map summarizing these benefits:

Integrated Example: Retail Chain Restructuring

Scenario: A mid-sized retail chain was struggling with high debt levels and declining cash flow due to changing consumer habits and increased competition.

Objectives Applied:

- Reduced debt burden by negotiating with creditors for extended payment terms.

- Improved liquidity through better inventory management and accelerated receivables.

- Enhanced operational efficiency by closing underperforming stores.

- Restored stakeholder confidence with regular transparent updates.

Benefits Realized:

- Stabilized cash flow allowed continued operations without layoffs.

- Improved credit rating enabled access to new financing for digital transformation.

- Stakeholders remained supportive, preventing forced liquidation.

Best Practices for Accountants

- Conduct thorough financial diagnostics to identify restructuring needs.

- Engage all stakeholders early to align objectives.

- Use clear, data-driven communication to build trust.

- Monitor progress continuously and adjust strategies as needed.

Understanding these objectives and benefits equips accountants and restructuring advisors to design effective, tailored restructuring plans that not only rescue companies from distress but also position them for future success.

1.4 Common Triggers for Financial Restructuring

Financial restructuring is often initiated in response to specific triggers that indicate a company is facing financial distress or strategic challenges. Recognizing these triggers early enables accountants and restructuring advisors to act proactively, minimizing losses and preserving value. Below, we explore the most common triggers, supported by practical examples and mind maps to visualize their interconnections.

Key Triggers Overview

Cash Flow Problems

Cash flow issues are among the most immediate and visible triggers. When a company struggles to meet its short-term obligations—such as payroll, supplier payments, or interest expenses—it signals liquidity distress.

Example: A mid-sized manufacturing company experienced delayed customer payments and rising inventory costs, leading to a negative cash flow. The accountant identified this early and recommended restructuring the payment terms with suppliers and negotiating a short-term loan to bridge the gap.

Excessive Debt Burden

High levels of debt relative to earnings or assets can strain a company’s financial flexibility. When debt servicing consumes a disproportionate share of cash flow, restructuring becomes necessary.

Example: A retail chain expanded aggressively using debt financing. After a downturn in sales, the company struggled with interest payments. The restructuring advisor proposed debt rescheduling and partial debt forgiveness to restore viability.

Breach of Debt Covenants

Debt agreements often include covenants—financial or operational conditions that must be met. Breaching these covenants can trigger defaults and accelerate debt repayment demands.

Example: A technology firm breached its EBITDA covenant due to unexpected R&D expenses. Early detection by the accounting team led to renegotiation with lenders, avoiding default.

Declining Revenues and Profitability

Sustained revenue decline or shrinking profit margins can erode a company’s financial foundation, necessitating restructuring to realign costs and operations.

Example: An apparel company faced declining sales due to changing consumer preferences. The restructuring plan included product line rationalization and cost optimization.

Market Disruption and Competitive Pressure

New entrants, technological advances, or shifts in consumer behavior can disrupt markets, forcing companies to restructure to remain competitive.

Example: A print media company confronted digital disruption. The restructuring involved pivoting to digital platforms and downsizing print operations.

Mergers, Acquisitions, and Divestitures

Strategic transactions often require financial restructuring to integrate operations, optimize capital structure, or divest non-core assets.

Example: Following an acquisition, a healthcare provider restructured its debt and consolidated financial reporting to improve efficiency.

Regulatory Changes

New laws or compliance requirements can increase costs or restrict operations, triggering the need for restructuring.

Example: A chemical manufacturer faced stricter environmental regulations, prompting investment in cleaner technologies and restructuring of capital expenditures.

Technological Obsolescence

Failure to keep pace with technology can render products or processes obsolete, impacting financial performance.

Example: An electronics firm with outdated product lines restructured by investing in R&D and divesting legacy assets.

Economic Downturns and Industry Crises

Broader economic recessions or sector-specific crises can reduce demand and access to capital.

Example: During an economic recession, a construction company restructured its debt and renegotiated contracts to survive reduced project pipelines.

Natural Disasters and Unforeseen Events

Events such as pandemics, floods, or geopolitical instability can disrupt operations and financial stability.

Example: A hospitality group impacted by a pandemic restructured leases and deferred debt payments to maintain liquidity.

Summary Mind Map

By understanding these common triggers, accountants and restructuring advisors can better anticipate challenges, design timely interventions, and guide companies through successful financial restructuring processes.

1.5 Overview of Restructuring Types: Operational, Financial, and Strategic

Financial restructuring is a multifaceted process that involves different approaches depending on the company’s specific challenges and goals. Understanding the three primary types of restructuring—Operational, Financial, and Strategic—is essential for accountants and restructuring advisors to tailor effective solutions. Below is a detailed overview of each type, complemented by mind maps and practical examples.

Operational Restructuring

Operational restructuring focuses on improving the efficiency and effectiveness of a company’s core business operations. This type aims to reduce costs, optimize processes, and enhance productivity without necessarily altering the company’s financial structure.

Key Components:

Example: A mid-sized manufacturing company facing declining margins undertakes operational restructuring by automating its assembly line and renegotiating supplier contracts. This reduces labor costs by 15% and improves production speed, helping restore profitability.

Financial Restructuring

Financial restructuring involves reorganizing the company’s capital structure to improve liquidity, reduce debt burden, or better align financing with business needs. This often includes renegotiating debt terms, refinancing, or equity infusion.

Key Components:

Example: A retail chain struggling with high-interest loans negotiates with creditors to extend loan maturities and reduce interest rates. Simultaneously, it sells underperforming stores to generate cash, stabilizing its financial position.

Strategic Restructuring

Strategic restructuring is a broader approach that redefines the company’s long-term direction, business model, or market focus. It often involves mergers and acquisitions, divestitures, or entering new markets.

Key Components:

Example: A technology firm shifts from hardware manufacturing to software services by divesting its hardware division and acquiring a cloud services company. This strategic pivot positions the firm for future growth in a high-demand sector.

Integrated Mind Map of Restructuring Types

Summary

For accountants and restructuring advisors, recognizing these restructuring types helps in diagnosing the root causes of financial distress and crafting tailored solutions. Often, successful restructuring involves a combination of these approaches, requiring a holistic understanding and coordinated execution.

By integrating operational efficiency improvements, financial reorganization, and strategic realignment, companies can navigate challenges and emerge stronger in competitive markets.

1.6 Case Study: A Mid-Sized Company’s Journey Through Financial Restructuring

Background

ABC Manufacturing, a mid-sized company specializing in automotive parts, faced severe financial distress due to declining sales, increased raw material costs, and inefficient operations. The company’s liquidity was strained, and it struggled to meet debt obligations, prompting the need for a comprehensive financial restructuring.

Initial Assessment

The restructuring team, including accountants and advisors, conducted a thorough assessment:

- Financial Statement Analysis: Revealed shrinking profit margins and negative cash flows.

- Debt Structure Review: High-interest short-term loans with restrictive covenants.

- Operational Inefficiencies: Excess inventory and outdated production processes.

Mind Map: Initial Assessment

Developing the Restructuring Strategy

The team prioritized objectives:

- Improve liquidity and cash flow.

- Renegotiate debt terms.

- Streamline operations to reduce costs.

Example:

- Negotiated with lenders to extend loan maturities and reduce interest rates by 2%.

- Implemented just-in-time inventory to cut holding costs.

Mind Map: Restructuring Strategy

Implementation and Monitoring

- Cash Flow Forecasting: Developed weekly cash flow models to monitor liquidity.

- Cost Reduction: Reduced overhead by 15% through workforce optimization and supplier renegotiations.

- Reporting: Monthly updates to stakeholders ensured transparency.

Example:

- Using a rolling 13-week cash flow forecast, the team identified potential shortfalls early and arranged bridge financing.

Mind Map: Implementation & Monitoring

Outcome

Within 12 months, ABC Manufacturing stabilized its finances:

- Debt obligations restructured with improved terms.

- Positive cash flow restored.

- Operational efficiency increased, reducing costs by 20%.

This case highlights the critical role of accountants in diagnosing issues, crafting strategies, and ensuring disciplined execution.

Key Takeaways

- Early detection of financial distress through detailed analysis is vital.

- Integrated financial and operational restructuring yields better results.

- Transparent communication with stakeholders builds trust and facilitates negotiations.

- Dynamic financial modeling supports proactive decision-making.

This case study exemplifies how mid-sized companies can navigate complex financial challenges with a structured, best-practice approach to restructuring.

2. Assessing Financial Health and Identifying Issues

2.1 Analyzing Financial Statements for Restructuring Needs

Financial statements are the primary tools accountants and restructuring advisors use to assess a company’s financial health and identify the need for restructuring. This section details how to analyze these statements effectively, highlighting key indicators and providing practical examples.

Key Financial Statements to Analyze

- Balance Sheet: Snapshot of assets, liabilities, and equity at a point in time.

- Income Statement (Profit & Loss Statement): Shows revenues, expenses, and profitability over a period.

- Cash Flow Statement: Tracks cash inflows and outflows, highlighting liquidity.

Mind Map: Components of Financial Statements and Their Importance

Step 1: Assess Liquidity and Working Capital

- Current Ratio = Current Assets / Current Liabilities

- Quick Ratio = (Current Assets - Inventories) / Current Liabilities

Example: A retail company has current assets of $500,000 and current liabilities of $600,000, resulting in a current ratio of 0.83. This indicates potential liquidity issues, signaling a restructuring need.

Step 2: Evaluate Profitability Trends

- Analyze gross profit margin, operating margin, and net profit margin over multiple periods.

- Declining margins may indicate operational inefficiencies or pricing pressures.

Example: A manufacturing firm’s net profit margin dropped from 8% to 2% over three years due to rising raw material costs and inefficient production processes.

Step 3: Examine Solvency and Leverage

- Debt-to-Equity Ratio = Total Debt / Shareholders’ Equity

- Interest Coverage Ratio = EBIT / Interest Expense

Example: A technology company has a debt-to-equity ratio of 3.5 and an interest coverage ratio below 1.5, indicating high leverage and difficulty servicing debt.

Step 4: Analyze Cash Flow Patterns

- Focus on operating cash flow to assess if core business generates sufficient cash.

- Negative operating cash flow over consecutive periods is a red flag.

Example: A service provider reports positive net income but consistently negative operating cash flow, suggesting earnings quality issues.

Mind Map: Key Ratios and Their Interpretation

Step 5: Identify Non-Recurring Items and Accounting Anomalies

- Look for one-time gains/losses, write-offs, or unusual expenses that may distort financial health.

Example: A company shows a large one-time gain from asset sales, inflating net income and masking underlying operational losses.

Integrated Example: Analyzing a Mid-Sized Company’s Financial Statements

Scenario: “ABC Manufacturing” shows declining sales, increasing debt, and shrinking cash reserves.

Analysis:

- Current ratio dropped from 1.5 to 0.9 over two years.

- Net profit margin decreased from 6% to 1%.

- Debt-to-equity ratio increased from 1.2 to 2.8.

- Operating cash flow turned negative in the last four quarters.

Conclusion: These indicators collectively suggest liquidity stress, profitability erosion, and solvency risk, signaling the need for financial restructuring.

Best Practices for Accountants

- Perform trend analysis over multiple periods rather than relying on a single snapshot.

- Use a combination of ratios and cash flow analysis for a holistic view.

- Cross-verify financial data with operational realities and market conditions.

- Document findings clearly to support restructuring recommendations.

By mastering financial statement analysis, accountants can proactively identify restructuring needs, enabling timely interventions that preserve value and stabilize organizations.

2.2 Identifying Cash Flow Challenges and Liquidity Risks

Understanding and identifying cash flow challenges and liquidity risks is critical for accountants and restructuring advisors to effectively manage financial restructuring processes. Cash flow problems often precede insolvency, making early detection essential.

What is Cash Flow and Liquidity?

- Cash Flow: The movement of money into and out of a business, representing operational, investing, and financing activities.

- Liquidity: The ability of a company to meet its short-term obligations using its liquid assets.

Common Causes of Cash Flow Challenges

- Declining sales or revenue

- Delayed receivables

- Increased operational costs

- High debt servicing requirements

- Poor inventory management

Mind Map: Causes of Cash Flow Challenges

Identifying Liquidity Risks

Liquidity risk arises when a company cannot convert assets to cash quickly enough to cover short-term liabilities.

Key indicators include:

- Current Ratio: Current Assets / Current Liabilities (Ideal > 1)

- Quick Ratio: (Current Assets - Inventory) / Current Liabilities (More stringent liquidity measure)

- Cash Conversion Cycle: Time taken to convert inventory and receivables into cash

Mind Map: Liquidity Risk Indicators

Practical Example 1: Retail Business with Seasonal Cash Flow Issues

Scenario: A retail company experiences strong sales during the holiday season but struggles to cover expenses in off-peak months.

Identification:

- Cash flow statements show negative cash flow in Q2 and Q3.

- Current ratio drops below 1 during these months.

- Inventory levels remain high, tying up cash.

Action:

- Implement better inventory management.

- Negotiate payment terms with suppliers.

- Establish a revolving credit facility for off-peak liquidity.

Practical Example 2: Service Company Facing Delayed Receivables

Scenario: A consulting firm has many clients with extended payment terms, causing delays in cash inflows.

Identification:

- Accounts receivable days increase from 30 to 75 days.

- Quick ratio declines steadily.

- Cash reserves deplete to cover payroll and rent.

Action:

- Introduce stricter credit policies.

- Offer early payment discounts.

- Use factoring services to accelerate cash inflows.

Best Practices for Identifying Cash Flow and Liquidity Issues

- Regular Monitoring: Weekly cash flow forecasts and monthly liquidity ratio analysis.

- Scenario Planning: Stress test cash flows under different business conditions.

- Stakeholder Communication: Early discussions with lenders and suppliers when risks are identified.

- Technology Use: Implement cash flow management software for real-time insights.

Mind Map: Best Practices for Managing Cash Flow and Liquidity Risks

By systematically identifying cash flow challenges and liquidity risks through these methods and examples, accountants and restructuring advisors can proactively design strategies to stabilize and improve a company’s financial health.

2.3 Evaluating Debt Structures and Covenant Compliance

Financial restructuring often begins with a thorough evaluation of a company’s existing debt structure and its compliance with debt covenants. For accountants and restructuring advisors, understanding these elements is critical to identifying risks and opportunities for negotiation.

Understanding Debt Structures

Debt structures refer to the composition, terms, and conditions of a company’s borrowings. These can include various types of debt such as:

- Senior Debt: Typically secured and has priority in repayment.

- Subordinated Debt: Lower priority, often unsecured.

- Revolving Credit Facilities: Flexible borrowing up to a limit.

- Term Loans: Fixed amount borrowed with a repayment schedule.

- Convertible Debt: Debt that can convert into equity under certain conditions.

Each type of debt has unique characteristics affecting cash flow, risk, and restructuring options.

Debt Covenants: Definition and Importance

Debt covenants are contractual clauses lenders impose to protect their interests. They can be:

- Financial Covenants: Requirements related to financial metrics (e.g., Debt-to-EBITDA ratio, Interest Coverage Ratio).

- Non-Financial Covenants: Restrictions on asset sales, dividend payments, or additional borrowing.

Covenant breaches can trigger defaults, accelerating repayment or forcing renegotiations.

Mind Map: Components of Debt Structure and Covenants

Evaluating Debt Structures: Step-by-Step

-

Inventory All Debt Instruments: Compile a detailed list including principal amounts, interest rates, maturity dates, and security.

-

Analyze Repayment Schedules: Understand timing and amounts of principal and interest payments.

-

Assess Interest Terms: Fixed vs. floating rates, and potential impact on cash flows.

-

Identify Intercreditor Agreements: Priority among creditors can affect restructuring options.

-

Review Convertible Features: Potential dilution or conversion impacts.

Evaluating Covenant Compliance

-

Gather Latest Financial Statements: Use the most recent and accurate data.

-

Calculate Covenant Ratios: For example, Debt-to-EBITDA, Interest Coverage, and Current Ratio.

-

Compare Against Covenant Thresholds: Identify any breaches or approaching limits.

-

Understand Waivers or Amendments: Check if lenders have granted any temporary relief.

-

Assess Implications of Breaches: Potential defaults, penalties, or renegotiation triggers.

Mind Map: Evaluating Covenant Compliance Process

Practical Example: Retail Chain Debt Evaluation

Scenario: A retail chain has the following debt:

- $50 million senior secured term loan, 6% fixed interest, maturing in 5 years.

- $20 million revolving credit facility with a 4.5% floating rate.

- Debt covenants include:

- Debt-to-EBITDA ≤ 3.0x

- Interest Coverage Ratio ≥ 4.0x

Step 1: Review latest financials:

- EBITDA: $18 million

- Interest expense: $3.5 million

Step 2: Calculate ratios:

- Debt-to-EBITDA = ($50M + $20M) / $18M = 3.89x (breach)

- Interest Coverage = $18M / $3.5M = 5.14x (compliant)

Step 3: Identify breach of Debt-to-EBITDA covenant.

Step 4: Discuss with lenders about possible waiver or restructuring options.

Best Practices for Accountants

- Maintain an up-to-date debt register with all terms and covenants.

- Regularly monitor covenant compliance, ideally monthly or quarterly.

- Use scenario analysis to anticipate covenant breaches under stress.

- Communicate early with lenders when breaches are anticipated.

- Document all covenant calculations and communications for audit trails.

Summary

Evaluating debt structures and covenant compliance is foundational in financial restructuring. Accountants must combine technical financial analysis with proactive communication to manage risks and facilitate successful restructuring outcomes.

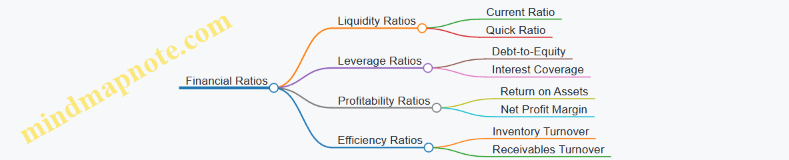

2.4 Using Financial Ratios to Diagnose Distress

Financial ratios are essential tools for accountants and restructuring advisors to quickly assess the financial health of a company and identify early signs of distress. These ratios condense complex financial data into understandable metrics that reveal liquidity, solvency, profitability, and operational efficiency.

Key Financial Ratios to Diagnose Distress

Below is a mind map summarizing the main categories of financial ratios used for diagnosing distress:

Liquidity Ratios

These ratios measure a company’s ability to meet short-term obligations.

-

Current Ratio = Current Assets / Current Liabilities

- Example: A current ratio below 1 indicates the company may struggle to pay short-term debts.

- Example: Company A has current assets of $500,000 and current liabilities of $600,000, so current ratio = 0.83, signaling liquidity concerns.

-

Quick Ratio = (Current Assets - Inventory) / Current Liabilities

- More conservative than current ratio, excludes inventory which may not be easily liquidated.

-

Cash Ratio = Cash and Cash Equivalents / Current Liabilities

- The most stringent liquidity measure.

Solvency Ratios

These assess long-term financial stability and debt burden.

-

Debt to Equity Ratio = Total Debt / Shareholders’ Equity

- High ratio indicates heavy reliance on debt financing.

- Example: Company B has $2 million debt and $1 million equity, ratio = 2.0, which may be risky.

-

Interest Coverage Ratio = EBIT / Interest Expense

- Measures ability to cover interest payments.

- Example: Company C has EBIT of $300,000 and interest expense of $150,000, ratio = 2.0, borderline for distress.

-

Debt to Assets Ratio = Total Debt / Total Assets

- Indicates what portion of assets is financed by debt.

Profitability Ratios

Declining profitability can signal distress.

-

Net Profit Margin = Net Income / Revenue

- Shrinking margins may indicate operational issues.

-

Return on Assets (ROA) = Net Income / Total Assets

- Shows efficiency in asset utilization.

-

Return on Equity (ROE) = Net Income / Shareholders’ Equity

- Declining ROE can signal poor returns to investors.

Efficiency Ratios

Operational efficiency impacts financial health.

-

Inventory Turnover = Cost of Goods Sold / Average Inventory

- Low turnover may indicate excess inventory or weak sales.

-

Receivables Turnover = Net Credit Sales / Average Accounts Receivable

- Low turnover suggests collection problems.

-

Asset Turnover = Revenue / Average Total Assets

- Low ratio indicates inefficient use of assets.

Integrated Example: Diagnosing Distress in a Retail Company

Company XYZ Financial Snapshot:

- Current Assets: $400,000

- Inventory: $150,000

- Current Liabilities: $500,000

- Total Debt: $1,200,000

- Shareholders’ Equity: $600,000

- EBIT: $100,000

- Interest Expense: $80,000

- Net Income: $20,000

- Revenue: $2,000,000

- Cost of Goods Sold: $1,200,000

- Average Inventory: $140,000

- Net Credit Sales: $1,800,000

- Average Accounts Receivable: $300,000

- Average Total Assets: $2,000,000

Calculations:

- Current Ratio = 400,000 / 500,000 = 0.8 (Below 1, liquidity concern)

- Quick Ratio = (400,000 - 150,000) / 500,000 = 0.5 (More alarming liquidity issue)

- Debt to Equity = 1,200,000 / 600,000 = 2.0 (High leverage)

- Interest Coverage = 100,000 / 80,000 = 1.25 (Very low, risk of default)

- Net Profit Margin = 20,000 / 2,000,000 = 1% (Very thin margin)

- Inventory Turnover = 1,200,000 / 140,000 ≈ 8.57 (Healthy turnover)

- Receivables Turnover = 1,800,000 / 300,000 = 6 (Moderate collection efficiency)

Interpretation:

- Liquidity ratios indicate Company XYZ may struggle to meet short-term obligations.

- High debt levels and low interest coverage ratio suggest solvency risk.

- Profit margin is very thin, signaling operational challenges.

- Inventory turnover is healthy, but receivables turnover could improve.

This comprehensive ratio analysis flags Company XYZ as financially distressed and in need of restructuring.

Best Practices for Using Financial Ratios

- Always analyze ratios in context: compare with industry benchmarks and historical trends.

- Use a combination of ratios rather than relying on a single metric.

- Supplement ratio analysis with qualitative information such as management discussions and market conditions.

- Regularly update ratio calculations to monitor changes over time.

Mind Map: Best Practices for Ratio Analysis

By mastering the use of financial ratios, accountants and restructuring advisors can effectively diagnose distress early, enabling timely interventions that can save companies from deeper financial troubles.

2.5 Practical Example: Spotting Warning Signs in a Retail Business

Financial restructuring often begins with recognizing early warning signs that indicate distress within a company. For accountants and restructuring advisors, the ability to identify these signals promptly can make the difference between a manageable turnaround and a full-blown crisis. In this section, we explore a practical example of spotting warning signs in a retail business, supported by mind maps and clear illustrations.

Background: RetailCo

RetailCo is a mid-sized retail chain specializing in apparel and accessories with 50 stores nationwide. Over the past two years, the company has faced increasing competition, changing consumer preferences, and rising operational costs.

Step 1: Analyzing Financial Statements

Key Areas to Focus:

- Declining sales revenue

- Shrinking gross profit margins

- Increasing operating expenses

- Deteriorating cash flow

- Rising debt levels

Mind Map: Key Financial Indicators to Monitor

Example:

RetailCo’s sales revenue dropped by 12% over the last fiscal year, while gross margins shrank from 45% to 38%. Operating expenses increased by 8%, primarily due to higher rent and wages. Cash flow statements show negative cash flow from operations for three consecutive quarters.

Step 2: Identifying Cash Flow Challenges and Liquidity Risks

Cash flow is the lifeblood of any retail business. Negative cash flow over extended periods signals trouble.

Mind Map: Cash Flow Warning Signs

Example:

RetailCo’s accounts payable days have increased from 30 to 60 days, indicating delayed payments to suppliers. Meanwhile, accounts receivable days decreased slightly, but overall cash reserves have fallen by 40%.

Step 3: Evaluating Debt Structure and Covenant Compliance

High leverage and covenant breaches can trigger creditor actions.

Mind Map: Debt and Covenant Monitoring

Example:

RetailCo has a $10 million revolving credit facility with covenants requiring a minimum debt service coverage ratio (DSCR) of 1.25. Recent financials show a DSCR of 0.9, indicating a breach.

Step 4: Using Financial Ratios to Diagnose Distress

Ratios provide a quick snapshot of financial health.

| Ratio | RetailCo Current | Industry Benchmark | Interpretation |

|---|---|---|---|

| Current Ratio | 0.8 | 1.5 | Poor liquidity |

| Quick Ratio | 0.5 | 1.0 | Insufficient liquid assets |

| Debt-to-Equity Ratio | 3.2 | 1.5 | High leverage |

| Interest Coverage Ratio | 1.1 | 3.0 | Weak ability to cover interest |

| Gross Profit Margin | 38% | 45% | Declining profitability |

Step 5: Additional Operational Warning Signs

- Inventory buildup leading to increased holding costs

- Declining foot traffic and customer engagement

- Increasing employee turnover

Mind Map: Operational Warning Signs

Example:

RetailCo’s inventory turnover ratio decreased from 6 to 3 times per year, signaling overstocking. Customer surveys reveal dissatisfaction with product variety and store experience.

Summary: Integrated Warning Signs Mind Map

Conclusion

By systematically analyzing RetailCo’s financial statements, cash flows, debt structure, ratios, and operational metrics, accountants and restructuring advisors can spot early warning signs of distress. This proactive approach enables timely intervention through financial restructuring strategies, potentially saving the business from insolvency.

Best Practice Tips

- Regularly monitor key financial ratios and cash flow metrics.

- Maintain open communication with management to understand operational challenges.

- Use integrated financial and operational data to form a comprehensive view.

- Document findings clearly to support restructuring decisions.

This practical example demonstrates how accountants can apply analytical skills and best practices to detect warning signs early, setting the stage for effective financial restructuring.

2.6 Best Practices for Early Detection and Proactive Measures

Early detection of financial distress is critical for accountants and restructuring advisors to intervene effectively and implement proactive measures that can prevent full-blown crises. This section outlines best practices supported by practical examples and mind maps to help visualize key concepts.

Best Practices for Early Detection

Continuous Financial Monitoring

- Regularly review financial statements (balance sheet, income statement, cash flow).

- Track key financial ratios such as liquidity ratios, leverage ratios, and profitability ratios.

- Use dashboards or automated alerts to flag unusual trends.

Cash Flow Analysis

- Monitor cash inflows and outflows weekly or monthly.

- Identify negative cash flow trends early.

- Forecast short-term cash needs to avoid liquidity crunch.

Debt Covenant Compliance Checks

- Regularly verify compliance with loan covenants.

- Engage with lenders proactively if breaches appear imminent.

Stakeholder Communication

- Maintain open communication lines with management, creditors, and investors.

- Early dialogue can facilitate collaborative problem-solving.

Benchmarking and Industry Analysis

- Compare company performance against industry peers.

- Identify deviations signaling potential distress.

Use of Technology and Analytics

- Implement financial analytics tools for anomaly detection.

- Use predictive models to forecast distress probabilities.

Proactive Measures

Early Cost Control Initiatives

- Identify non-essential expenses for reduction.

- Implement efficiency programs before cash flow deteriorates.

Restructuring Debt Terms

- Negotiate with creditors to extend maturities or reduce interest rates.

- Consider refinancing options early.

Asset Management

- Evaluate underperforming or non-core assets for sale.

- Improve working capital management.

Strategic Operational Adjustments

- Adjust production or service levels to market demand.

- Optimize supply chain and inventory.

Scenario Planning

- Develop multiple financial scenarios to prepare for uncertainties.

- Use these scenarios to guide decision-making.

Mind Maps

Mind Map 1: Early Detection Framework

Mind Map 2: Proactive Measures to Prevent Financial Distress

Practical Examples

Example 1: Retail Chain Early Warning

A regional retail chain noticed a gradual decline in its current ratio over three consecutive quarters. The accounting team implemented weekly cash flow monitoring and discovered increasing delays in receivables collection. By proactively renegotiating payment terms with suppliers and accelerating receivables through early payment discounts, the company avoided liquidity issues and stabilized operations.

Example 2: Manufacturing Firm Debt Covenant Breach Prevention

A manufacturing company was approaching a debt covenant breach due to lower EBITDA margins. The accountants flagged this early through covenant compliance checks. They worked with management to reduce discretionary spending and negotiated a temporary covenant waiver with lenders, preventing a default and allowing time to improve profitability.

Example 3: Technology Startup Scenario Planning

A tech startup used financial modeling tools to create best-case, base-case, and worst-case scenarios for cash runway. Early detection of a potential shortfall led the finance team to initiate cost-cutting measures and seek bridge financing, ensuring continued operations without disruption.

Summary

Early detection and proactive measures are essential to successful financial restructuring. Accountants and restructuring advisors should embed continuous monitoring, effective communication, and strategic planning into their workflows. Leveraging technology and real-world examples enhances the ability to identify risks early and act decisively to protect the company’s financial health.

3. Developing a Restructuring Strategy

3.1 Setting Clear Objectives and Priorities

Setting clear objectives and priorities is a foundational step in any financial restructuring process. For accountants and restructuring advisors, this clarity ensures that all efforts are aligned, measurable, and focused on restoring financial health while maintaining stakeholder confidence.

Why Setting Objectives Matters

- Provides a roadmap for decision-making

- Aligns stakeholders on common goals

- Helps prioritize limited resources effectively

- Enables measurement of progress and success

Key Types of Objectives in Financial Restructuring

- Liquidity Improvement: Ensuring sufficient cash flow to meet short-term obligations.

- Debt Reduction: Reducing overall debt burden through refinancing, rescheduling, or write-offs.

- Operational Efficiency: Cutting costs and optimizing processes to improve profitability.

- Stakeholder Confidence: Maintaining transparent communication and trust.

- Long-term Viability: Positioning the company for sustainable growth post-restructuring.

Mind Map: Setting Clear Objectives and Priorities

Practical Example: Setting Objectives for a Retail Chain Facing Financial Distress

Scenario: A regional retail chain is experiencing declining sales and increasing debt. The company needs to restructure to avoid insolvency.

Step 1: Define Clear Objectives

- Restore positive cash flow within 6 months.

- Reduce outstanding debt by 25% through negotiations.

- Cut operational costs by 15% without compromising customer experience.

- Improve supplier payment terms to enhance liquidity.

- Maintain employee morale and minimize layoffs.

Step 2: Prioritize Objectives

- Immediate liquidity improvement to avoid default.

- Debt restructuring to reduce financial burden.

- Operational cost reduction.

- Stakeholder communication to maintain confidence.

Step 3: Develop Action Plan

- Negotiate with creditors for extended payment terms.

- Implement targeted cost-saving initiatives (e.g., energy savings, renegotiated leases).

- Launch internal communication campaigns to keep employees informed.

Mind Map: Prioritizing Objectives in the Retail Chain Example

Best Practices for Setting Objectives and Priorities

- Be Specific and Measurable: Objectives should have clear metrics (e.g., reduce debt by $2M in 12 months).

- Time-Bound: Set realistic deadlines to create urgency and track progress.

- Align with Stakeholders: Ensure objectives reflect the interests of creditors, management, and employees.

- Flexible but Focused: Be ready to adjust priorities as new information emerges but avoid scope creep.

- Document and Communicate: Maintain a written plan and share it with relevant parties to foster accountability.

By setting clear objectives and priorities early in the restructuring process, accountants and restructuring advisors can create a focused, actionable plan that guides all subsequent efforts and maximizes the chances of a successful turnaround.

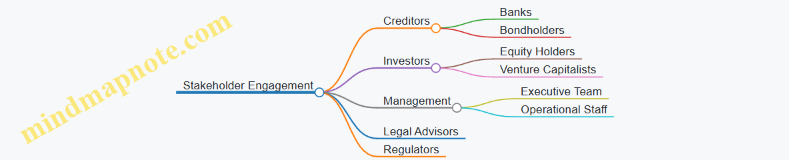

3.2 Engaging Stakeholders: Creditors, Investors, and Management

Engaging stakeholders effectively is a cornerstone of successful financial restructuring. Accountants and restructuring advisors must foster transparent communication, build trust, and align interests among creditors, investors, and management to create a collaborative environment for restructuring initiatives.

Understanding Stakeholder Roles and Interests

Each stakeholder group has unique priorities and concerns:

- Creditors: Seek repayment or restructuring terms that minimize losses.

- Investors: Interested in preserving or enhancing value and future growth prospects.

- Management: Focused on operational continuity and long-term viability.

Recognizing these perspectives helps tailor communication and negotiation strategies.

Mind Map: Stakeholder Engagement Framework

Best Practices for Engaging Stakeholders

-

Early Involvement: Involve key stakeholders early to build trust and reduce resistance.

-

Clear Communication: Use straightforward language and provide regular updates on financial status and restructuring progress.

-

Tailored Messaging: Address specific concerns of each stakeholder group to demonstrate understanding and empathy.

-

Negotiation Preparation: Equip yourself with accurate data and realistic proposals to facilitate constructive discussions.

-

Conflict Management: Anticipate disagreements and prepare mediation strategies to maintain momentum.

-

Documentation: Keep detailed records of communications and agreements to ensure accountability.

Example: Engaging Creditors in a Retail Chain Restructuring

A regional retail chain facing liquidity issues initiated restructuring by first mapping out its creditor base:

- Secured creditors: Local banks holding mortgage on store properties.

- Unsecured creditors: Suppliers and service providers.

The restructuring team scheduled separate meetings:

- With secured creditors, they proposed refinancing terms backed by improved cash flow forecasts.

- With unsecured creditors, they negotiated extended payment terms and partial debt forgiveness.

Regular joint creditor meetings were held to update on progress and build consensus. This approach reduced creditor anxiety and secured necessary support.

Mind Map: Communication Channels and Techniques

Engaging Investors: Example from a Technology Startup

A tech startup with venture capital investors faced a cash crunch. The management team:

- Held a detailed briefing explaining the financial challenges and proposed restructuring plan.

- Shared revised financial models projecting recovery timelines.

- Invited investors to participate in strategy workshops, fostering ownership and trust.

This proactive engagement helped secure bridge financing and aligned investor expectations.

Management Engagement: Aligning Internal Teams

Successful restructuring requires management buy-in:

- Conduct workshops to explain restructuring objectives and roles.

- Encourage open dialogue to surface operational challenges.

- Establish cross-functional teams to implement restructuring initiatives.

Mind Map: Stakeholder Engagement Timeline

Summary

Engaging creditors, investors, and management through structured communication, tailored messaging, and collaborative negotiation is essential for effective financial restructuring. By applying these best practices and learning from real-world examples, accountants and restructuring advisors can drive successful outcomes that satisfy all parties involved.

3.3 Designing Debt Restructuring Plans: Refinancing, Rescheduling, and Haircuts

Financial restructuring often hinges on effectively redesigning a company’s debt obligations to restore liquidity and ensure long-term viability. Accountants and restructuring advisors play a critical role in crafting debt restructuring plans that balance the interests of creditors and the company. This section explores three primary strategies: refinancing, rescheduling, and haircuts, with clear examples and mind maps to illustrate each.

Refinancing: Replacing Old Debt with New Debt

Refinancing involves replacing existing debt with new debt, often under more favorable terms such as lower interest rates, extended maturities, or improved covenants. This strategy can reduce immediate cash flow burdens and improve financial stability.

Mind Map: Refinancing Process

Example: A mid-sized technology startup had a $5 million loan at an 8% interest rate due in 2 years. The company negotiated refinancing with its bank to replace this with a $5 million loan at 5% interest, extending the maturity to 5 years. This reduced annual interest payments and improved cash flow, allowing the company to invest in growth.

Rescheduling: Adjusting Payment Terms Without Changing Debt Amount

Rescheduling modifies the timing of debt repayments, such as extending maturities or changing installment schedules, without altering the principal amount owed. This provides immediate relief by spreading payments over a longer period.

Mind Map: Rescheduling Components

Example: A retail chain facing temporary cash flow issues negotiated with creditors to reschedule its $10 million debt from a 3-year repayment period to 6 years. This halved the annual repayment amount, easing liquidity pressures while maintaining the original principal.

Haircuts: Reducing the Principal or Interest Obligations

A haircut refers to creditors agreeing to reduce the principal amount owed or the interest rate, effectively writing off a portion of the debt. This is often used in distressed situations where full repayment is unlikely.

Mind Map: Haircuts Explained

Example: A manufacturing company burdened with $20 million in debt negotiated a 30% principal haircut with its creditors, reducing the debt to $14 million. Creditors accepted this to avoid the company’s bankruptcy, which would have resulted in even lower recoveries.

Integrating Strategies: A Holistic Approach

Often, restructuring plans combine refinancing, rescheduling, and haircuts to tailor solutions that best fit the company’s circumstances.

Mind Map: Integrated Debt Restructuring Plan

Example: A manufacturing firm facing severe liquidity issues implemented a combined plan: it refinanced $8 million of its debt at a lower interest rate, rescheduled $5 million to extend maturity from 3 to 7 years, and negotiated a 20% principal haircut on the remaining $7 million. This comprehensive approach restored financial stability and satisfied creditor concerns.

Best Practices for Designing Debt Restructuring Plans

- Thorough Financial Analysis: Understand cash flow projections and debt servicing capacity.

- Stakeholder Communication: Engage creditors early and transparently.

- Scenario Planning: Use financial models to test different restructuring options.

- Legal Review: Ensure compliance with contractual and regulatory requirements.

- Documentation: Maintain clear records of agreements and terms.

By mastering these strategies and applying them thoughtfully, accountants and restructuring advisors can design debt restructuring plans that maximize recovery, preserve business value, and support sustainable financial health.

3.4 Operational Restructuring: Cost Reduction and Efficiency Improvements

Operational restructuring focuses on improving the internal processes and cost structures of a company to enhance profitability and sustainability. For accountants and restructuring advisors, understanding how to identify inefficiencies and implement cost-saving measures is crucial. This section explores best practices, practical examples, and mind maps to guide you through operational restructuring.

Key Objectives of Operational Restructuring

- Streamline business processes to reduce waste

- Optimize resource allocation

- Improve productivity and operational efficiency

- Reduce fixed and variable costs

- Enhance overall financial health

Mind Map: Operational Restructuring Focus Areas

Best Practices with Examples

-

Workforce Optimization

- Practice: Conduct a skills and roles assessment to identify redundancies and gaps.

- Example: A mid-sized manufacturing company reduced labor costs by 15% through voluntary retirement programs and cross-training employees to cover multiple roles, avoiding layoffs while maintaining productivity.

-

Supply Chain Management

- Practice: Negotiate better terms with suppliers and optimize inventory levels to reduce carrying costs.

- Example: A retail chain implemented just-in-time inventory, reducing warehouse storage costs by 20%, while renegotiating contracts with key suppliers to secure volume discounts.

-

Overhead Cost Reduction

- Practice: Consolidate office locations and renegotiate leases to lower fixed costs.

- Example: A service firm consolidated three regional offices into one central location, saving $500,000 annually in rent and utilities.

-

Process Automation and Technology Integration

- Practice: Adopt automation tools for repetitive tasks such as invoicing and payroll.

- Example: An accounting firm implemented automated billing software, reducing manual errors and cutting processing time by 40%.

-

Lean Management Principles

- Practice: Apply lean methodologies to identify and eliminate waste in workflows.

- Example: A logistics company mapped its delivery process and eliminated redundant steps, improving delivery times by 25% and reducing fuel costs.

Mind Map: Steps to Implement Operational Restructuring

Practical Example: Operational Restructuring in a Mid-Sized Manufacturing Firm

Situation: The company faced declining margins due to high production costs and inefficient processes.

Actions Taken:

- Conducted a comprehensive process audit revealing bottlenecks in assembly lines.

- Introduced lean manufacturing techniques, including 5S workplace organization.

- Automated inventory tracking to reduce stockouts and excess inventory.

- Negotiated better rates with raw material suppliers.

- Reduced overtime by optimizing shift schedules.

Results:

- Production costs decreased by 18% within 12 months.

- On-time delivery improved by 30%.

- Employee satisfaction increased due to clearer roles and reduced overtime.

Summary

Operational restructuring is a critical lever for improving a company’s financial health by targeting cost reduction and efficiency improvements. Accountants and restructuring advisors should leverage process analysis, workforce optimization, technology, and supplier management to drive sustainable change. Using structured frameworks and real-world examples helps ensure practical and effective implementation.

3.5 Integrating Financial and Operational Strategies

Financial restructuring is not solely about adjusting the numbers on a balance sheet or renegotiating debt terms. To achieve sustainable recovery, accountants and restructuring advisors must integrate financial strategies with operational improvements. This holistic approach ensures that the company not only survives immediate financial distress but also builds a stronger foundation for future growth.

Why Integration Matters

- Financial strategies focus on capital structure, liquidity management, and creditor negotiations.

- Operational strategies target cost efficiency, process optimization, and revenue enhancement.

When these two areas work in tandem, companies can:

- Align cost-cutting measures with core business priorities.

- Ensure cash flow improvements are supported by operational realities.

- Avoid short-term fixes that undermine long-term viability.

Mind Map: Integration of Financial and Operational Strategies

Practical Example: Manufacturing Firm Restructuring

Scenario: A mid-sized manufacturing company is facing liquidity issues due to declining sales and high fixed costs. The company has significant short-term debt coming due.

Financial Strategy:

- Negotiate debt rescheduling to extend maturities.

- Improve cash flow forecasting to better manage liquidity.

- Plan asset sales of non-core equipment to raise cash.

Operational Strategy:

- Implement workforce optimization by reducing overtime and streamlining shifts.

- Improve supply chain efficiency by renegotiating supplier contracts and consolidating vendors.

- Introduce lean manufacturing principles to reduce waste.

Integration:

- The debt rescheduling plan is contingent on achieving cost savings from workforce and supply chain initiatives.

- Cash flow forecasts incorporate expected savings from operational changes and proceeds from asset sales.

- Regular cross-functional meetings are held to ensure financial targets and operational milestones are aligned.

Outcome:

- The company successfully extends debt maturities, avoiding default.

- Operational improvements reduce monthly expenses by 15%, improving liquidity.

- Stakeholders gain confidence due to transparent and coordinated restructuring efforts.

Best Practices for Integration

- Cross-Functional Collaboration: Establish teams including finance, operations, and strategy to ensure alignment.

- Unified KPIs: Develop metrics that reflect both financial health and operational performance.

- Scenario Planning: Use financial models that incorporate operational assumptions and vice versa.

- Transparent Communication: Keep all stakeholders informed about how operational changes impact financial outcomes.

- Continuous Monitoring: Track progress regularly and adjust strategies as needed.

Mind Map: Best Practices for Integration

Additional Example: Retail Chain Facing Declining Margins

Financial Strategy:

- Restructure vendor payment terms to improve cash flow.

- Reduce debt interest costs through refinancing.

Operational Strategy:

- Optimize inventory management to reduce holding costs.

- Close underperforming stores and focus on high-margin locations.

Integration:

- Cash flow improvements from vendor term changes support operational investments in inventory systems.

- Store closures are timed to coincide with debt refinancing milestones.

Result:

- Improved liquidity and profitability.

- Enhanced operational efficiency aligned with financial goals.

By weaving financial and operational strategies together, accountants and restructuring advisors can create robust, actionable plans that address both immediate financial pressures and long-term business viability.

3.6 Example: Crafting a Restructuring Plan for a Manufacturing Firm

In this section, we will walk through a practical example of how accountants and restructuring advisors can craft a comprehensive financial restructuring plan for a manufacturing firm facing financial distress. This example integrates best practices, clear explanations, and mind maps to visualize the process.

Background

Company: ABC Manufacturing Ltd.

Industry: Automotive parts manufacturing

Situation: ABC Manufacturing has experienced declining sales due to supply chain disruptions and increased competition. The company is struggling with high debt levels, liquidity issues, and operational inefficiencies.

Step 1: Initial Assessment and Diagnosis

- Financial Analysis: Review of financial statements reveals:

- High leverage ratio (Debt/Equity = 3.5)

- Negative operating cash flow for 3 consecutive quarters

- Breach of debt covenants with key lenders

- Operational Issues: Inefficient production lines causing high costs

- Stakeholder Concerns: Creditors demanding repayment, employees worried about job security

Step 2: Define Objectives

- Stabilize cash flow and improve liquidity

- Reduce debt burden through negotiations

- Improve operational efficiency to reduce costs

- Restore stakeholder confidence

Step 3: Develop Restructuring Strategy

Mind Map: Restructuring Strategy Components

Financial Restructuring Example:

- Negotiate with lenders to extend debt maturities by 3 years

- Seek partial debt forgiveness of 20% to reduce principal

- Explore new financing options with lower interest rates

Operational Restructuring Example:

- Implement lean manufacturing techniques to reduce waste

- Consolidate underutilized production lines

- Introduce automation in repetitive tasks to improve efficiency

Step 4: Financial Modeling and Forecasting

- Build a cash flow forecast incorporating:

- Revised debt repayment schedule

- Cost savings from operational improvements

- Projected sales recovery based on market analysis

Mind Map: Financial Modeling Focus Areas

Example: The base case projects positive cash flow within 12 months post-restructuring, assuming a 15% reduction in operating costs and a 10% sales increase.

Step 5: Stakeholder Negotiations

- Prepare detailed financial reports and restructuring plan presentations

- Highlight benefits to creditors, such as improved likelihood of repayment

- Address employee concerns with clear communication about job security and changes

Step 6: Implementation Plan

- Assign project leads for financial and operational initiatives

- Set milestones for debt negotiations, cost reduction targets, and cash flow monitoring

- Establish regular reporting cadence to stakeholders

Mind Map: Implementation Plan

Summary

This example demonstrates how accountants and restructuring advisors can systematically approach a manufacturing firm’s financial restructuring by combining financial analysis, strategic planning, stakeholder management, and operational improvements. Using mind maps helps visualize complex interrelated components, ensuring no critical area is overlooked.

Key Takeaways

- Start with a thorough financial and operational diagnosis

- Define clear, measurable objectives

- Integrate financial and operational restructuring strategies

- Use financial modeling to forecast outcomes and support negotiations

- Engage stakeholders transparently and proactively

- Develop a detailed implementation plan with clear responsibilities and timelines

By following these steps and leveraging tools like mind maps, restructuring professionals can craft effective, actionable plans that guide distressed manufacturing firms back to financial health.

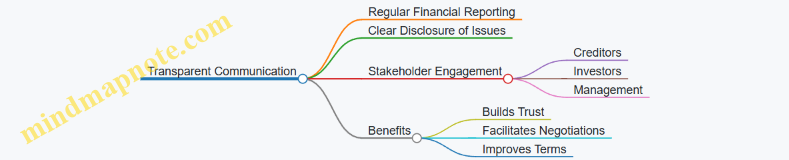

3.7 Best Practices for Communication and Transparency

Effective communication and transparency are critical components of a successful financial restructuring process. They help build trust among stakeholders, reduce uncertainty, and facilitate smoother negotiations and implementation. Below is a detailed guide on best practices, supported by mind maps and practical examples.

Key Principles of Communication and Transparency

- Clarity: Use simple, jargon-free language to explain complex financial concepts.

- Consistency: Ensure messages are consistent across all channels and stakeholders.

- Timeliness: Provide updates regularly and promptly to avoid misinformation.

- Honesty: Be upfront about challenges and realistic about outcomes.

- Engagement: Encourage two-way communication to address concerns and gather feedback.

Mind Map: Core Elements of Effective Communication in Restructuring

Best Practice 1: Develop a Comprehensive Communication Plan

Description: A communication plan outlines who communicates what, to whom, when, and how.

Example: A restructuring advisor for a mid-sized manufacturing company created a communication calendar detailing weekly updates to creditors, monthly town halls with employees, and quarterly reports to investors. This plan ensured everyone received relevant information at appropriate intervals, reducing rumors and anxiety.

Best Practice 2: Use Visual Tools to Enhance Understanding

Description: Visual aids such as charts, graphs, and flow diagrams help stakeholders grasp complex financial data.

Example: During negotiations, the accountant presented a flowchart showing the debt restructuring timeline and impact on cash flow. This visual helped creditors understand the phased repayment plan clearly.

Mind Map: Visual Communication Tools

Best Practice 3: Foster Open Dialogue and Feedback

Description: Create forums for stakeholders to ask questions and express concerns.

Example: A retail chain undergoing restructuring held weekly Q&A sessions with employees and suppliers. This openness helped identify operational issues early and built goodwill.

Best Practice 4: Maintain Documentation and Transparency

Description: Keep detailed records of all communications and decisions to ensure accountability.

Example: An accounting team maintained a shared digital repository of all restructuring communications, meeting minutes, and financial reports accessible to key stakeholders. This transparency minimized disputes and confusion.

Mind Map: Communication Channels and Documentation

Best Practice 5: Tailor Communication to Stakeholder Needs

Description: Different stakeholders require different levels of detail and types of information.

Example: Investors received detailed financial models and forecasts, while employees were given summaries focusing on job security and operational changes. Creditors were provided with legal and financial restructuring terms.

Summary

Effective communication and transparency are not one-time tasks but ongoing commitments throughout the restructuring journey. By implementing structured plans, leveraging visual tools, encouraging open dialogue, maintaining thorough documentation, and tailoring messages, accountants and restructuring advisors can significantly improve stakeholder confidence and the likelihood of a successful restructuring outcome.

4. Legal and Regulatory Considerations

4.1 Understanding Insolvency Laws and Their Impact

Insolvency laws form the legal framework that governs the process when a company or individual is unable to meet their financial obligations. For accountants and restructuring advisors, a solid understanding of these laws is crucial to navigate financial distress situations effectively and to advise clients on the best course of action.

What is Insolvency?

Insolvency occurs when an entity cannot pay its debts as they fall due or when its liabilities exceed its assets. Insolvency laws provide mechanisms to address this situation, either through restructuring, liquidation, or other legal remedies.

Key Objectives of Insolvency Laws

- Protect creditors’ rights

- Maximize value of the insolvent estate

- Provide fair and orderly resolution

- Facilitate business rescue where possible

Mind Map: Core Concepts of Insolvency Laws

Types of Insolvency Procedures

-

Bankruptcy: Typically applies to individuals or sole proprietors, involving court-ordered liquidation of assets to repay creditors.

-

Administration: A process designed to rescue the company as a going concern or achieve better returns for creditors than liquidation.

-

Receivership: Appointment of a receiver to take control of certain assets, often by secured creditors.

-

Liquidation: The winding up of a company’s affairs, selling assets to pay creditors, and ultimately dissolving the company.

Example: Impact of Insolvency Laws on a Manufacturing Company

ABC Manufacturing Ltd. faced severe cash flow problems due to declining sales and high debt servicing costs. The company was balance sheet insolvent, with liabilities exceeding assets.

- Step 1: The board appointed an administrator under insolvency laws to assess options.

- Step 2: The administrator proposed a restructuring plan involving debt rescheduling and operational cost cuts.

- Step 3: Creditors voted to accept the plan, avoiding liquidation.

- Step 4: The company emerged from administration with improved financial health.

This example highlights how insolvency laws can facilitate business rescue rather than immediate liquidation.

Mind Map: Stakeholders and Their Roles in Insolvency

Best Practices for Accountants Regarding Insolvency Laws

- Stay updated on jurisdiction-specific insolvency regulations.

- Conduct early financial distress detection to advise timely interventions.

- Collaborate closely with legal advisors and insolvency practitioners.

- Maintain transparent and accurate financial records.

- Educate clients on potential outcomes and legal implications.

Summary

Understanding insolvency laws is essential for accountants and restructuring advisors to guide distressed companies through complex legal processes. By leveraging insolvency frameworks effectively, professionals can help maximize creditor recoveries and preserve business value where possible.

4.2 Navigating Bankruptcy Procedures and Alternatives

Bankruptcy procedures can be complex and vary significantly by jurisdiction, but understanding the core concepts and alternatives is essential for accountants and restructuring advisors. This section explores the key bankruptcy processes, their implications, and alternative strategies to bankruptcy, all illustrated with practical examples and mind maps to enhance comprehension.

Understanding Bankruptcy Procedures

Bankruptcy is a legal process designed to help financially distressed companies either liquidate their assets to pay creditors or reorganize their debts to continue operations. The two most common types of bankruptcy for corporations are:

- Liquidation Bankruptcy (e.g., Chapter 7 in the U.S.): The company ceases operations, and a trustee sells assets to pay creditors.

- Reorganization Bankruptcy (e.g., Chapter 11 in the U.S.): The company restructures its debts and operations under court supervision to regain profitability.

Mind Map: Bankruptcy Procedures Overview

Key Steps in Bankruptcy Proceedings

- Filing the Petition: The company or creditors file a petition initiating bankruptcy.

- Automatic Stay: Immediate halt on creditor actions to collect debts.

- Appointment of Trustee or Debtor in Possession: Oversees asset management.

- Creditors’ Meeting: Stakeholders discuss claims and restructuring plans.

- Plan of Reorganization or Liquidation: Proposal for debt repayment or asset distribution.

- Court Approval and Implementation: Finalization and execution of the plan.

Example:

A mid-sized manufacturing firm facing insolvency files for Chapter 11 to reorganize. The company submits a restructuring plan reducing debt by 40%, extending maturities, and negotiating new supplier contracts. Creditors approve the plan, allowing the firm to continue operations and return to profitability within 18 months.

Mind Map: Bankruptcy Process Flow

Alternatives to Bankruptcy

Bankruptcy is often a last resort due to its cost, time, and reputational impact. Alternatives include:

- Out-of-Court Workouts: Informal negotiations with creditors to restructure debt without court involvement.

- Debt-for-Equity Swaps: Creditors exchange debt claims for equity stakes in the company.

- Pre-Packaged Bankruptcy: The company negotiates a restructuring plan with creditors before filing, expediting the process.

- Assignment for the Benefit of Creditors (ABC): A state-level alternative to liquidation where assets are assigned to a third party to liquidate and distribute proceeds.

Example:

A retail chain struggling with debt opts for an out-of-court workout. Accountants help develop a cash flow forecast demonstrating viability post-restructuring. Creditors agree to extend payment terms and reduce interest rates, avoiding bankruptcy and preserving business value.

Mind Map: Bankruptcy Alternatives

Best Practices for Accountants and Restructuring Advisors

- Early Assessment: Identify financial distress signs early to explore alternatives before bankruptcy.

- Stakeholder Communication: Maintain transparent dialogue with creditors, management, and legal counsel.

- Accurate Financial Modeling: Provide realistic forecasts to support restructuring proposals.

- Legal Coordination: Work closely with legal advisors to understand jurisdiction-specific procedures.

- Documentation: Keep meticulous records to support claims and plans.

Summary

Navigating bankruptcy procedures requires a comprehensive understanding of legal frameworks and strategic alternatives. Accountants play a critical role in analyzing financial data, preparing restructuring plans, and advising stakeholders. By leveraging alternatives when appropriate, companies can often avoid the costs and disruptions of formal bankruptcy, preserving value and enabling recovery.

For further reading, consider exploring jurisdiction-specific bankruptcy codes and recent case studies highlighting successful restructurings.

4.3 Compliance Requirements for Accountants in Restructuring

Financial restructuring is a complex process that requires accountants to adhere strictly to various compliance requirements to ensure transparency, accuracy, and legal conformity. This section explores the critical compliance obligations accountants must observe during restructuring engagements, supported by practical examples and mind maps to clarify key concepts.

Key Compliance Areas for Accountants in Restructuring

Regulatory Compliance

Accountants must ensure all restructuring activities comply with relevant accounting frameworks such as IFRS (International Financial Reporting Standards) or GAAP (Generally Accepted Accounting Principles). For example, IFRS 9 outlines how to account for financial instruments, including modifications to debt terms during restructuring.

Example: A company undergoing debt rescheduling must evaluate whether the modification results in derecognition of the original debt and recognition of a new financial liability or just an adjustment to the existing one, following IFRS 9 guidelines.

Additionally, compliance with insolvency laws is crucial. Accountants need to understand jurisdiction-specific rules that affect restructuring, such as creditor priority and reporting obligations.

Financial Reporting

Accurate financial reporting is essential to reflect the true financial position post-restructuring.