Accounting for Stock Options

1. Introduction to Stock Options

1.1 Definition and Types of Stock Options

What Are Stock Options?

Stock options are financial instruments that give an employee or investor the right, but not the obligation, to buy or sell shares of a company’s stock at a predetermined price (known as the exercise or strike price) within a specified time period.

They are widely used as a form of equity compensation to align the interests of employees and shareholders, incentivizing employees to contribute to the company’s growth and success.

Mind Map: Stock Options Overview

Types of Stock Options

-

Non-Qualified Stock Options (NSOs)

- Can be granted to employees, directors, contractors, and others.

- Taxed as ordinary income upon exercise.

- Simpler regulatory requirements.

-

Incentive Stock Options (ISOs)

- Only granted to employees.

- Potential for favorable tax treatment (capital gains) if holding period requirements are met.

- Subject to specific IRS rules and limitations.

-

Employee Stock Purchase Plans (ESPPs)

- Allow employees to purchase stock at a discount, often through payroll deductions.

- May have qualified and non-qualified versions.

Mind Map: Types of Stock Options

Example 1: Non-Qualified Stock Option

Sarah, a software engineer at a tech company, receives 1,000 NSOs with an exercise price of $10 per share. After 3 years, the stock price rises to $30. When Sarah exercises her options, she pays $10,000 (1,000 shares x $10) and can immediately sell the shares at $30,000, realizing a gain of $20,000. The $20,000 is taxed as ordinary income.

Example 2: Incentive Stock Option

John, an employee at the same company, is granted 1,000 ISOs at $10 per share. He exercises the options when the stock price is $30 but holds the shares for more than one year after exercise and two years after the grant date. When he sells at $50, the $40,000 gain ($50 - $10 x 1,000) is taxed at the lower capital gains rate.

Summary

Stock options are versatile equity instruments that come in various types, each with distinct tax and regulatory implications. Understanding these differences is crucial for accurate accounting and effective financial analysis.

This foundational knowledge sets the stage for deeper exploration of accounting practices and valuation methods in subsequent sections.

1.2 Importance of Stock Options in Corporate Finance

Stock options play a pivotal role in corporate finance, serving as a strategic tool for aligning the interests of employees, management, and shareholders. Their importance extends beyond mere compensation, influencing company performance, capital structure, and investor relations.

Why Stock Options Matter

- Incentivizing Performance: Stock options motivate employees and executives to work towards increasing the company’s stock price, directly linking compensation to company success.

- Attracting and Retaining Talent: Especially in competitive industries like tech and finance, stock options are a key part of compensation packages that attract top talent and reduce turnover.

- Cash Flow Management: Unlike direct salary increases, stock options allow companies to conserve cash while still offering valuable rewards.

- Aligning Interests: By giving employees a stake in the company, stock options align their interests with those of shareholders.

Mind Map: Importance of Stock Options in Corporate Finance

Example 1: Tech Startup Using Stock Options to Attract Talent

A tech startup with limited cash resources offers stock options to its early employees. Instead of paying high salaries, the company grants options that vest over four years. This approach helps the startup attract skilled developers who are motivated to contribute to the company’s growth, knowing their equity stake could be valuable if the company goes public or is acquired.

Example 2: Executive Compensation and Performance Alignment

A publicly traded company grants stock options to its CEO as part of the compensation package. The options vest only if the company meets specific performance targets, such as revenue growth and stock price appreciation. This structure ensures the CEO’s incentives are closely tied to shareholder value creation.

Mind Map: Benefits of Stock Options for Companies

Real-World Impact

Stock options have been instrumental in the success stories of many tech giants like Google and Facebook, where early employees benefited significantly from equity compensation. This not only rewarded employees but also fostered a culture of ownership and accountability.

Summary

Stock options are more than just a compensation mechanism; they are a strategic financial tool that impacts corporate governance, talent management, and financial planning. Understanding their importance helps accountants and equity analysts evaluate company strategies and financial health more effectively.

1.3 Overview of Accounting Challenges with Stock Options

Accounting for stock options presents unique challenges due to the complexity of valuation, timing, and regulatory requirements. Understanding these challenges is crucial for accountants and equity analysts to ensure accurate financial reporting and compliance.

Key Accounting Challenges

Valuation Challenges

- Fair Value Estimation: Determining the fair value of stock options at grant date is complex because options are derivative instruments whose value depends on multiple variables.

- Model Selection: Common models include Black-Scholes and the Binomial model. Choosing the appropriate model affects the accuracy of valuation.

- Assumptions & Inputs: Volatility, risk-free rate, expected life, and dividend yield must be estimated, often based on historical data or market conditions.

Example: A tech startup grants options to employees. The accountant uses the Black-Scholes model but struggles to estimate volatility due to limited trading history. They decide to use industry benchmarks to approximate volatility, documenting assumptions carefully.

Timing Challenges

- Grant Date Identification: The grant date is when the company and employee have a mutual understanding of the option terms. Delays or ambiguities can complicate this.

- Vesting Period: Stock options typically vest over time or upon performance milestones, requiring expense recognition to be spread accordingly.

- Expense Recognition: Determining the correct period over which to recognize compensation expense requires careful tracking of vesting schedules.

Example: An employee receives options with a 4-year vesting schedule. The company must recognize the expense evenly over those 4 years, adjusting for any forfeitures if the employee leaves early.

Regulatory Compliance Challenges

- IFRS 2 vs ASC Topic 718: Different accounting standards have nuanced differences in treatment, especially around measurement and disclosure.

- Disclosure Requirements: Companies must provide detailed notes on stock option plans, assumptions used, and expense recognized.

Example: A multinational company must reconcile differences between IFRS and US GAAP when consolidating financial statements, ensuring disclosures meet both standards.

Complexity in Modifications and Tax Implications

- Modifications & Cancellations: Changes to option terms after grant date require remeasurement and additional accounting entries.

- Tax Implications: Timing and amount of tax deductions may differ from expense recognition, requiring deferred tax accounting.

- Multiple Vesting Conditions: Performance and market conditions complicate the estimation of expense and require ongoing reassessment.

Example: A company reprices underwater options to motivate employees. This triggers additional expense recognition and requires careful documentation and compliance with accounting standards.

Summary Mind Map

By understanding these challenges and applying best practices with clear documentation and appropriate models, accountants and equity analysts can improve the accuracy and transparency of stock option accounting.

1.4 Real-World Example: Stock Options in a Tech Startup

To better understand how stock options work in practice, let’s explore a detailed example involving a fictional tech startup, “Innovatech,” which uses stock options as a key part of its employee compensation strategy.

Company Background

- Innovatech is a 3-year-old startup specializing in AI-driven software solutions.

- It has 50 employees, including engineers, sales, and management.

- To attract and retain talent, Innovatech grants stock options to employees as part of their compensation package.

Stock Option Grant Details

- Grant Date: January 1, 2024

- Number of Options Granted: 10,000 options to a senior engineer

- Exercise Price: $5 per share (equal to the fair market value at grant date)

- Vesting Schedule: 4 years with a 1-year cliff (25% after 1 year, then monthly vesting)

- Expiration: 10 years from grant date

Mind Map: Stock Option Components

Step 1: Determining Fair Value at Grant Date

Innovatech uses the Black-Scholes model to estimate the fair value of each option at the grant date. Key inputs include:

- Current stock price: $5

- Exercise price: $5

- Expected life: 6 years (based on expected employee behavior)

- Volatility: 40% (derived from comparable companies)

- Risk-free rate: 3%

- Dividend yield: 0%

Calculated fair value per option: $3.00

Total fair value of options granted: 10,000 x $3.00 = $30,000

Step 2: Expense Recognition Over Vesting Period

Since the options vest over 4 years, Innovatech recognizes the compensation expense evenly over this period, assuming no forfeitures.

- Annual expense = $30,000 / 4 = $7,500

Example Journal Entry (Year 1):

| Date | Account | Debit | Credit |

|---|---|---|---|

| 31-Dec-24 | Compensation Expense | $7,500 | |

| 31-Dec-24 | Additional Paid-in Capital | $7,500 |

Step 3: Vesting and Forfeitures

If the employee leaves after 18 months, only 37.5% of the options have vested (25% after 1 year + 12.5% over 6 months). The company will recognize expense only for the vested portion.

- Vested portion fair value = 10,000 x 37.5% x $3.00 = $11,250

- Expense recognized until termination date = $11,250

Mind Map: Expense Recognition Timeline

Step 4: Exercise of Options

If the employee exercises 3,000 vested options at $5 per share when the market price is $12:

- Cash received: 3,000 x $5 = $15,000

- Market value of shares issued: 3,000 x $12 = $36,000

Journal Entry:

| Date | Account | Debit | Credit |

|---|---|---|---|

| Exercise Date | Cash | $15,000 | |

| Exercise Date | Additional Paid-in Capital | $21,000 | |

| Exercise Date | Common Stock (par value) | $3,000 | |

| Exercise Date | Equity (APIC - Options) | $33,000 |

Note: Par value assumed $1 per share for illustration.

Summary Table: Key Figures

| Item | Value |

|---|---|

| Options Granted | 10,000 |

| Exercise Price | $5 |

| Fair Value per Option (BSM) | $3 |

| Total Fair Value | $30,000 |

| Vesting Period | 4 years |

| Annual Expense | $7,500 |

| Vested at 18 months | 37.5% (3,750) |

| Expense Recognized at 18 mo | $11,250 |

| Options Exercised | 3,000 |

| Cash Received on Exercise | $15,000 |

Conclusion

This example illustrates the practical steps accountants and equity analysts take to measure, recognize, and report stock options in a startup environment. By understanding the grant terms, applying valuation models, and carefully tracking vesting and exercises, professionals can ensure accurate financial reporting and compliance with accounting standards.

2. Regulatory Framework and Standards

2.1 Overview of IFRS 2 and ASC Topic 718

Accounting for stock options is governed primarily by two major standards depending on the jurisdiction: IFRS 2 (International Financial Reporting Standard 2) and ASC Topic 718 (Accounting Standards Codification Topic 718) under US GAAP. Both standards aim to ensure transparent and consistent reporting of share-based payments, but they have nuanced differences in scope, measurement, and disclosure requirements.

Mind Map: Key Components of IFRS 2 and ASC Topic 718

IFRS 2: Key Highlights

- Scope: Applies to all share-based payment transactions, including equity-settled, cash-settled, and transactions with cash alternatives.

- Measurement: For equity-settled awards, fair value is measured at the grant date and is not remeasured subsequently. For cash-settled awards, fair value is remeasured at each reporting date.

- Expense Recognition: The total fair value of the award is recognized as an expense over the vesting period, reflecting the service received.

- Disclosure: Requires detailed disclosures about the nature and extent of share-based payment arrangements, how fair value was determined, and the effect on profit or loss.

Example: IFRS 2 Equity-Settled Stock Option

A company grants 1,000 stock options to an employee on January 1, 2024. The fair value per option at grant date is $10, and the options vest over 4 years.

- Total fair value: 1,000 x $10 = $10,000

- Annual expense recognized: $10,000 / 4 = $2,500

Journal entry each year:

Dr. Employee Compensation Expense $2,500

Cr. Equity - Stock Options $2,500

ASC Topic 718: Key Highlights

- Scope: Covers all share-based payments to employees, including stock options, restricted stock units, and other equity instruments.

- Measurement: Fair value is measured at grant date using an option pricing model (e.g., Black-Scholes). Unlike IFRS, equity awards are not remeasured after grant.

- Expense Recognition: Expense is recognized over the requisite service period, using either straight-line or graded vesting methods.

- Disclosure: Requires disclosures about the nature and terms of awards, assumptions used in valuation, and the effect on earnings per share (EPS).

Example: ASC 718 Graded Vesting Expense

A company grants 1,000 options vesting 25% each year over 4 years. Fair value per option is $12.

- Total fair value: 1,000 x $12 = $12,000

- Expense recognized each year (graded vesting):

- Year 1: 25% x $12,000 = $3,000

- Year 2: 25% x $12,000 = $3,000

- Year 3: 25% x $12,000 = $3,000

- Year 4: 25% x $12,000 = $3,000

Journal entry each year:

Dr. Compensation Expense $3,000

Cr. Additional Paid-in Capital $3,000

Mind Map: Differences Between IFRS 2 and ASC Topic 718

Best Practices for Compliance

- Understand the jurisdictional requirements: Apply IFRS 2 for international entities and ASC 718 for US-based or SEC registrants.

- Use appropriate valuation models: Black-Scholes or binomial models are common; ensure assumptions are documented.

- Maintain detailed records: Track grant dates, vesting conditions, modifications, and exercises.

- Regularly review disclosures: Ensure transparency and completeness to satisfy auditors and regulators.

This foundational understanding of IFRS 2 and ASC Topic 718 sets the stage for deeper exploration of grant date accounting, vesting conditions, and expense recognition in subsequent sections.

2.2 Key Differences Between IFRS and US GAAP in Stock Option Accounting

Stock option accounting under IFRS and US GAAP shares many similarities but also exhibits important differences that accountants and equity analysts must understand to ensure accurate financial reporting. This section explores these key differences with clear examples and mind maps to facilitate comprehension.

Overview Mind Map

Measurement of Fair Value at Grant Date

IFRS:

- Requires measurement of the fair value of the equity instruments granted at the grant date.

- Uses the “fair value” approach, often employing option pricing models like Black-Scholes or Monte Carlo simulations.

- If the fair value cannot be reliably estimated, the intrinsic value method can be used, but this is rare.

US GAAP:

- Also requires fair value measurement at grant date.

- Primarily uses the Black-Scholes or lattice models.

- Intrinsic value method was eliminated for most awards after the adoption of ASC 718.

Example: A company grants 1,000 stock options with a grant date fair value of $10 per option.

- Under both IFRS and US GAAP, the total compensation cost is $10,000.

Treatment of Vesting Conditions

| Aspect | IFRS (IFRS 2) | US GAAP (ASC 718) | |

|---|---|---|---|

| Service Conditions | Required to be met for vesting | Required to be met for vesting | |

| Performance Conditions | Separated into market and non-market conditions - Market conditions: included in fair value at grant date - Non-market conditions: accounted for by adjusting expense based on probability | Similar treatment - Market conditions: included in fair value - Non-market conditions: accounted for by adjusting expense based on probability | |

| Cancellations | Treated as forfeitures when they occur | Treated as forfeitures when they occur |

Mind Map:

Example: A company grants options with a performance condition tied to revenue growth (non-market). Initially, management estimates a 70% chance of meeting the target.

- IFRS and US GAAP: Expense recognized is adjusted as the probability estimate changes.

Modifications and Repricing

IFRS:

- If the modification increases the fair value or changes the vesting conditions, incremental expense is recognized.

- The incremental fair value is the difference between the modified and original fair value at the modification date.

US GAAP:

- Similar approach; incremental fair value is recognized as additional compensation cost.

- Requires reassessment of vesting conditions and fair value.

Example: Original option fair value: $8 Modified option fair value: $12

- Incremental expense: $4 per option recognized over the remaining vesting period.

Expense Recognition and Forfeitures

IFRS:

- Expense recognized over the vesting period based on grant date fair value.

- Forfeitures are accounted for as they occur; no upfront estimation.

US GAAP:

- Expense recognized over the vesting period.

- Forfeitures can be estimated upfront and adjusted, or accounted for as they occur (policy choice).

Mind Map:

Example: A company grants options vesting over 4 years with a total fair value of $40,000.

- IFRS: Recognize $10,000 expense each year, adjusting for actual forfeitures.

- US GAAP: If estimating 10% forfeitures upfront, recognize $9,000 expense per year, adjusting if actual forfeitures differ.

Tax Effects

IFRS:

- Deferred tax recognized for temporary differences.

- No specific guidance on tax benefits from stock options; local tax laws apply.

US GAAP:

- Requires recognition of deferred tax assets and valuation allowances.

- Excess tax benefits from stock option exercises are recognized in equity.

Summary Table of Key Differences

| Topic | IFRS (IFRS 2) | US GAAP (ASC 718) |

|---|---|---|

| Fair Value Measurement | Fair value at grant date, intrinsic value rarely used | Fair value at grant date, intrinsic value method eliminated |

| Vesting Conditions | Market conditions included in fair value; non-market adjusted | Same as IFRS |

| Forfeitures | Accounted as they occur | Estimate upfront or as they occur |

| Modifications | Incremental fair value recognized | Incremental fair value recognized |

| Tax Effects | Deferred tax assets/liabilities recognized; local tax laws apply | Deferred tax assets/liabilities recognized; excess tax benefits recorded in equity |

Understanding these differences is crucial for accountants and equity analysts working across jurisdictions or with multinational companies. Accurate application ensures compliance, transparent reporting, and informed decision-making.

Additional Resources

- IFRS Foundation: IFRS 2 Share-based Payment

- FASB Accounting Standards Codification Topic 718

End of Section 2.2

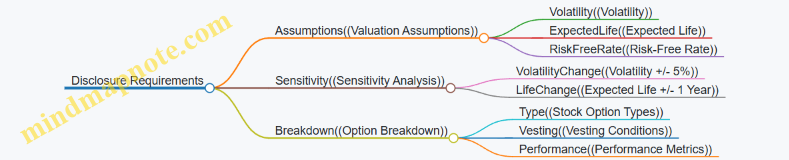

2.3 Disclosure Requirements and Compliance Best Practices

Accounting for stock options involves rigorous disclosure requirements designed to ensure transparency and provide stakeholders with a clear understanding of the company’s equity compensation plans. Compliance with these requirements not only fulfills regulatory obligations but also enhances investor confidence.

Key Disclosure Requirements

-

Description of the Stock Option Plan:

- Terms and conditions

- Eligibility criteria

- Vesting schedules

-

Number and Weighted Average Exercise Price:

- Outstanding options at the beginning and end of the period

- Options granted, exercised, forfeited, or expired during the period

-

Fair Value Measurement:

- Methodology used (e.g., Black-Scholes, Monte Carlo)

- Assumptions such as volatility, risk-free rate, expected life

-

Expense Recognition:

- Total compensation cost recognized during the period

- Unrecognized compensation cost and expected amortization period

-

Impact on Financial Statements:

- Effect on net income and earnings per share (EPS)

-

Tax Effects:

- Deferred tax assets or liabilities related to stock options

Compliance Best Practices Mind Map

Example: Disclosure Note for a Public Company

Note X: Stock-Based Compensation

The Company grants stock options to employees under its 2020 Equity Incentive Plan. Options generally vest over four years and expire ten years from the grant date.

| Description | Number of Options | Weighted Average Exercise Price ($) |

|---|---|---|

| Outstanding at January 1, 2023 | 1,000,000 | 15.00 |

| Granted during 2023 | 200,000 | 20.00 |

| Exercised during 2023 | (150,000) | 14.50 |

| Forfeited during 2023 | (50,000) | 16.00 |

| Outstanding at December 31, 2023 | 1,000,000 | 16.50 |

The fair value of options granted during 2023 was estimated using the Black-Scholes model with the following assumptions:

- Expected volatility: 30%

- Risk-free interest rate: 2.5%

- Expected life: 6 years

- Dividend yield: 0%

Stock-based compensation expense recognized in 2023 amounted to $3.2 million, with $1.8 million remaining to be recognized over the next three years.

The Company has recognized deferred tax assets of $0.9 million related to stock options.

Mind Map: Disclosure Components Breakdown

Summary

Effective disclosure of stock options requires a comprehensive approach combining detailed documentation, consistent valuation methodologies, and transparent communication. By adhering to best practices and regulatory requirements, accountants and equity analysts can ensure accurate reporting that supports informed decision-making by investors and other stakeholders.

2.4 Example: Preparing Disclosures for a Public Company

When preparing disclosures related to stock options for a public company, transparency and compliance with regulatory requirements are paramount. Disclosures provide stakeholders with insights into the nature, terms, and financial impact of stock option plans.

Key Disclosure Areas for Stock Options

Mind Map: Stock Option Disclosure Components

Example Disclosure Extract for a Public Company

Stock Option Plan

The Company maintains a stock option plan to attract, retain, and motivate employees and directors. Under the plan, options are granted with an exercise price equal to the market price on the grant date. Options generally vest over four years and expire ten years after the grant date.

Accounting Policies

Stock options are measured at fair value on the grant date using the Black-Scholes option pricing model. Compensation expense is recognized on a straight-line basis over the vesting period, adjusted for estimated forfeitures.

Stock Option Activity

| Description | Number of Options | Weighted Average Exercise Price |

|---|---|---|

| Outstanding at Jan 1 | 1,200,000 | $15.00 |

| Granted | 300,000 | $20.00 |

| Exercised | (150,000) | $14.00 |

| Forfeited | (50,000) | $18.00 |

| Outstanding at Dec 31 | 1,300,000 | $16.50 |

Fair Value Assumptions

- Expected volatility: 35%

- Risk-free interest rate: 2.5%

- Expected term: 6 years

- Dividend yield: 1.2%

Compensation Expense

Total stock-based compensation expense recognized for the year was $3.5 million. As of December 31, $2.1 million of unrecognized compensation cost related to non-vested options is expected to be recognized over a weighted-average period of 2.8 years.

Tax Effects

The Company recorded a deferred tax asset of $0.9 million related to stock option deductions expected upon exercise. Tax benefits realized from option exercises during the year totaled $1.2 million.

Best Practices for Preparing Disclosures

- Be Clear and Concise: Use straightforward language to explain complex terms.

- Use Tables and Charts: Summarize option activity and assumptions visually.

- Update Regularly: Reflect changes in plans, assumptions, and regulations.

- Coordinate with Legal and Tax Teams: Ensure accuracy and compliance.

- Provide Context: Explain how stock options impact financial performance.

By following these guidelines and using the example above as a template, accountants and equity analysts can prepare comprehensive, compliant, and insightful stock option disclosures for public companies.

3. Grant Date Accounting

3.1 Identifying the Grant Date and Its Significance

The grant date is a critical concept in accounting for stock options. It is the date on which the company and the employee have a mutual understanding of the terms and conditions of the stock option award. This date marks the point at which the fair value of the stock options is measured and from which the expense recognition period begins.

Why is the Grant Date Important?

- Establishes the fair value measurement point

- Determines the start of the vesting period for expense recognition

- Sets the contractual terms and conditions of the award

- Impacts financial reporting and tax treatment

Mind Map: Key Aspects of the Grant Date

Determining the Grant Date

The grant date is typically identified as the date when all of the following conditions are met:

- Approval by the Board of Directors or Compensation Committee: The stock option plan or award must be formally approved.

- Communication to the Employee: The employee must be informed of the award and its terms.

- No Further Negotiations: The terms are fixed and not subject to change.

If these conditions occur on different dates, the grant date is the earliest date when all are satisfied.

Mind Map: Steps to Identify Grant Date

Example 1: Simple Grant Date Identification

Scenario:

- March 1: Board approves stock option plan.

- March 5: Employee receives grant letter.

- March 10: Employee accepts terms.

Grant Date: March 10, because this is when all conditions are met — approval, communication, and acceptance.

Example 2: Complex Scenario with Delayed Acceptance

Scenario:

- April 1: Board approves award.

- April 3: Employee notified.

- April 15: Employee negotiates minor changes.

- April 20: Final terms agreed.

Grant Date: April 20, as the terms were not finalized until this date.

Significance in Accounting

- Fair Value Measurement: The stock option’s fair value is measured at the grant date using valuation models such as Black-Scholes or Monte Carlo simulations.

- Expense Recognition: The total compensation cost is recognized over the vesting period starting from the grant date.

- Financial Reporting: Accurate identification ensures compliance with IFRS 2 and ASC 718 standards.

Mind Map: Grant Date and Accounting Impact

Best Practices

- Maintain clear documentation of board approvals and employee communications.

- Confirm mutual agreement on terms before finalizing the grant date.

- Use consistent internal controls to identify and record the grant date.

- Train accounting and HR teams on the importance of the grant date.

By properly identifying the grant date, accountants and equity analysts ensure accurate valuation and reporting of stock options, which is essential for transparent financial statements and regulatory compliance.

3.2 Measuring Fair Value at Grant Date

Measuring the fair value of stock options at the grant date is a critical step in the accounting process. It determines the total compensation cost that will be recognized over the vesting period. The fair value reflects the estimated value of the option based on various assumptions and valuation models.

Key Concepts in Fair Value Measurement

- Grant Date: The date on which the company and the employee agree to the stock option terms.

- Fair Value: The estimated price at which the option would be exchanged in an arm’s length transaction.

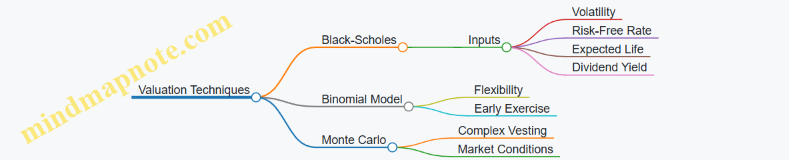

- Valuation Models: Mathematical models used to estimate the fair value, such as Black-Scholes or Binomial models.

Mind Map: Factors Influencing Fair Value Measurement

Valuation Models Overview

-

Black-Scholes Model

- Most commonly used for plain vanilla options.

- Assumes European-style exercise (only at expiration).

- Inputs: stock price, exercise price, time to expiration, volatility, risk-free rate, dividends.

-

Binomial Model

- Suitable for American-style options (exercisable anytime).

- Can incorporate complex features like early exercise and varying vesting conditions.

Example: Calculating Fair Value Using Black-Scholes Model

Scenario:

- Grant Date: Jan 1, 2024

- Current Stock Price: $50

- Exercise Price: $50

- Expected Life: 5 years

- Volatility: 30% (annualized)

- Risk-Free Rate: 3%

- Expected Dividends: 1% yield

Step-by-Step Calculation:

- Calculate d1 and d2:

\[ d1 = \frac{\ln(\frac{S}{K}) + (r - q + \frac{\sigma^2}{2})T}{\sigma \sqrt{T}} \]

\[ d2 = d1 - \sigma \sqrt{T} \]

Where:

- \(S\) = Current stock price = 50

- \(K\) = Exercise price = 50

- \(r\) = Risk-free rate = 0.03

- \(q\) = Dividend yield = 0.01

- \(\sigma\) = Volatility = 0.30

- \(T\) = Time to expiration = 5

- Calculate the option price:

\[ C = S e^{-qT} N(d1) - K e^{-rT} N(d2) \]

Where \(N(d)\) is the cumulative distribution function of the standard normal distribution.

- Result:

Using a calculator or spreadsheet, the fair value \(C\) is approximately $11.23 per option.

Mind Map: Steps to Measure Fair Value at Grant Date

Best Practices for Measuring Fair Value

- Use Market Data: Whenever possible, use observable market inputs such as stock price and volatility.

- Document Assumptions: Clearly document all assumptions used in the valuation model.

- Update Inputs for Modifications: If terms change, re-measure fair value accordingly.

- Leverage Technology: Use specialized software to reduce errors and improve efficiency.

Additional Example: Impact of Volatility on Fair Value

| Volatility | Fair Value (per option) |

|---|---|

| 20% | $7.85 |

| 30% | $11.23 |

| 40% | $15.60 |

Insight: Higher volatility increases the fair value of the stock option because it raises the probability of favorable stock price movements.

Summary

Measuring fair value at the grant date is foundational to stock option accounting. By understanding the inputs and applying appropriate valuation models, accountants and equity analysts can ensure accurate and compliant financial reporting.

3.3 Best Practices for Documenting Grant Date Assumptions

Documenting grant date assumptions is a critical step in the accounting for stock options. Accurate and comprehensive documentation ensures transparency, facilitates audit processes, and supports consistent application of valuation models. Below are best practices, supported by mind maps and examples, to help accountants and equity analysts effectively document these assumptions.

Key Elements to Document at Grant Date

- Grant Date Identification: Clearly specify the exact date when the stock options are granted.

- Option Terms: Include exercise price, vesting schedule, expiration date, and any special terms.

- Fair Value Assumptions: Document all inputs used in valuation models such as volatility, risk-free rate, expected life, and dividend yield.

- Employee Data: Number of options granted, employee classifications, and expected forfeiture rates.

- Market Conditions: Any market-based vesting conditions or performance criteria.

Mind Map: Components of Grant Date Assumptions

Best Practice #1: Use Standardized Templates

Create and use standardized documentation templates for all stock option grants. This ensures consistency and completeness across different grants and reporting periods.

Example:

| Field | Description | Example Value |

|---|---|---|

| Grant Date | Date options are granted | 2024-05-01 |

| Exercise Price | Price at which options can be exercised | $25.00 |

| Vesting Schedule | Timeline for vesting | 25% per year over 4 years |

| Expected Volatility | Estimated stock price volatility | 35% |

| Risk-Free Rate | Treasury yield for expected life | 2.5% |

| Expected Life | Expected option life in years | 6 years |

| Dividend Yield | Expected dividend rate | 1.2% |

| Forfeiture Rate | Estimated employee forfeiture | 5% |

Best Practice #2: Include Rationale for Assumptions

For each assumption, provide a brief rationale or source to justify the chosen value. This is especially important for subjective inputs like volatility and expected life.

Example:

- Volatility: Based on historical stock price data over the past 3 years.

- Expected Life: Derived from historical exercise behavior of employees in similar roles.

- Forfeiture Rate: Estimated from prior year’s employee turnover statistics.

Mind Map: Documenting Rationale for Assumptions

Best Practice #3: Maintain Version Control and Audit Trail

Keep track of all versions of grant date assumption documents, including updates and approvals. This helps in audits and when assumptions need to be revisited.

Example:

- Document version: v1.0

- Prepared by: Jane Doe

- Date: 2024-05-01

- Reviewed by: John Smith

- Date of review: 2024-05-03

Any changes to assumptions after initial documentation should be logged with reasons and dates.

Best Practice #4: Use Visual Aids to Summarize Assumptions

Incorporate charts or mind maps in documentation to provide a quick overview of key assumptions and their interrelations.

Example Mind Map: Summary of Grant Date Assumptions

Best Practice #5: Align Assumptions with Company Policies and Market Conditions

Ensure that assumptions reflect current company policies, market conditions, and any recent changes in employee behavior or economic environment.

Example: If the company has recently changed its dividend policy to increase payouts, update the dividend yield assumption accordingly.

Summary

Documenting grant date assumptions thoroughly and clearly is essential for accurate stock option accounting. Using standardized templates, providing rationale, maintaining version control, employing visual aids, and aligning assumptions with real-world conditions are best practices that enhance reliability and audit readiness.

By following these best practices, accountants and equity analysts can ensure that the valuation of stock options is well-supported, transparent, and compliant with accounting standards.

3.4 Example: Calculating Grant Date Fair Value Using Black-Scholes Model

Understanding the fair value of stock options at the grant date is critical for accurate accounting and financial reporting. The Black-Scholes model is one of the most widely used methods for estimating this fair value. Below, we will walk through a detailed example, supported by mind maps to clarify the process.

What is the Black-Scholes Model?

The Black-Scholes model is a mathematical formula used to estimate the theoretical price of European-style options. It takes into account several variables to calculate the option’s fair value.

Key Inputs for Black-Scholes Model

Mind Map: Black-Scholes Model Inputs

Step-by-Step Calculation Example

Scenario:

- Current Stock Price (S): $50

- Exercise Price (K): $55

- Time to Expiration (T): 3 years

- Risk-Free Interest Rate (r): 4% (0.04)

- Volatility (σ): 30% (0.30)

- Dividend Yield (q): 2% (0.02)

Step 1: Calculate d1 and d2

Formulas:

\[ d_1 = \frac{\ln(\frac{S}{K}) + (r - q + \frac{\sigma^2}{2})T}{\sigma \sqrt{T}} \]

\[ d_2 = d_1 - \sigma \sqrt{T} \]

Calculations:

- \( \ln(\frac{50}{55}) = \ln(0.9091) = -0.0953 \)

- \( (0.04 - 0.02 + \frac{0.30^2}{2}) \times 3 = (0.02 + 0.045) \times 3 = 0.195 \)

- Numerator for d1: \( -0.0953 + 0.195 = 0.0997 \)

- Denominator for d1: \( 0.30 \times \sqrt{3} = 0.30 \times 1.732 = 0.5196 \)

Thus,

\[ d_1 = \frac{0.0997}{0.5196} = 0.192 \]

\[ d_2 = 0.192 - 0.5196 = -0.3276 \]

Step 2: Calculate N(d1) and N(d2)

N(d) is the cumulative distribution function of the standard normal distribution.

Using standard normal tables or a calculator:

- N(d1) = N(0.192) ≈ 0.576

- N(d2) = N(-0.328) ≈ 0.372

Step 3: Calculate the Option Price (C)

Formula:

\[ C = S e^{-qT} N(d_1) - K e^{-rT} N(d_2) \]

Calculations:

- \( S e^{-qT} = 50 \times e^{-0.02 \times 3} = 50 \times e^{-0.06} = 50 \times 0.9418 = 47.09 \)

- \( K e^{-rT} = 55 \times e^{-0.04 \times 3} = 55 \times e^{-0.12} = 55 \times 0.8869 = 48.78 \)

Therefore,

\[ C = 47.09 \times 0.576 - 48.78 \times 0.372 = 27.13 - 18.15 = 8.98 \]

Fair Value of the Stock Option at Grant Date = $8.98

Mind Map: Black-Scholes Calculation Flow

Practical Best Practices

- Use Reliable Market Data: Ensure volatility and risk-free rates are sourced from credible market data providers.

- Document Assumptions: Maintain clear documentation of all assumptions used in the model.

- Review and Update Regularly: Volatility and other inputs may change; update calculations if there is a significant delay between grant and reporting.

- Leverage Software Tools: Many accounting and financial software packages automate Black-Scholes calculations, reducing manual errors.

Additional Example: Impact of Volatility on Option Value

| Volatility | Option Fair Value ($) |

|---|---|

| 20% | 5.45 |

| 30% | 8.98 |

| 40% | 13.50 |

Higher volatility increases the option’s fair value, reflecting greater uncertainty and potential upside.

This example demonstrates how accountants and equity analysts can apply the Black-Scholes model to estimate the grant date fair value of stock options, ensuring compliance with accounting standards and supporting accurate financial reporting.

4. Vesting Conditions and Their Impact

4.1 Types of Vesting Conditions: Service and Performance

Vesting conditions are critical components in stock option agreements that determine when an employee earns the right to exercise their stock options. Understanding the types of vesting conditions is essential for accurate accounting and financial reporting.

Overview of Vesting Conditions

Vesting conditions generally fall into two broad categories:

- Service Vesting Conditions: Require the employee to remain employed for a specified period.

- Performance Vesting Conditions: Depend on achieving specific performance targets or milestones.

These conditions affect the timing and amount of expense recognition in the financial statements.

Mind Map: Types of Vesting Conditions

Service Vesting Conditions

Service vesting requires employees to stay with the company for a certain period before their options vest.

- Cliff Vesting: All options vest at once after a specified period (e.g., 4 years).

- Graded Vesting: Options vest gradually over time (e.g., 25% per year over 4 years).

Example:

An employee is granted 1,000 stock options with a 4-year graded vesting schedule (25% each year). After 2 years, 500 options have vested.

Accounting Implication: Expense is recognized proportionally over the vesting period based on the fair value at grant date.

Performance Vesting Conditions

Performance vesting depends on meeting specific targets, which can be classified as market or non-market conditions.

Market Conditions

Market conditions relate to the company’s stock price or market indices and affect the option’s fair value.

- Examples: Stock price reaching $50, or outperforming a benchmark index.

Accounting Treatment: Market conditions are factored into the fair value at grant date and do not affect the expense recognition pattern.

Example:

Options vest only if the company’s stock price exceeds $50 within 3 years. The fair value at grant date incorporates this condition using option pricing models.

Non-Market Conditions

Non-market conditions depend on operational or financial targets unrelated to stock price.

- Examples: Achieving $100M revenue, launching a new product, or hitting EPS targets.

Accounting Treatment: Expense recognition is adjusted based on the probability of achieving these targets, and the expense is revised if expectations change.

Example:

An employee’s options vest only if the company achieves $100M revenue in the fiscal year. Initially, the probability is estimated at 70%, so 70% of the expense is recognized. If the probability changes, the expense is adjusted accordingly.

Mind Map: Accounting Impact of Vesting Conditions

Integrated Example: Combining Service and Performance Vesting

Company XYZ grants 2,000 stock options to an employee with the following conditions:

- Vesting over 4 years (service condition)

- Options vest only if the company achieves a 10% revenue growth target each year (non-market performance condition)

Step 1: Determine fair value at grant date (assuming $10 per option).

Step 2: Estimate probability of meeting revenue targets (initially 80%).

Step 3: Expense recognition over 4 years:

- Annual expense = 2,000 options × $10 × 80% ÷ 4 = $4,000

Step 4: Adjust expense if probability changes:

- If probability drops to 50% in year 3, reduce remaining expense accordingly.

Best Practices

- Clearly document vesting conditions in grant agreements.

- Regularly reassess probabilities for non-market conditions.

- Use appropriate valuation models that incorporate market conditions.

- Maintain detailed tracking of employee service periods and performance milestones.

Understanding the nuances of service and performance vesting conditions ensures accurate stock option accounting and compliance with regulatory standards.

4.2 Accounting for Market vs. Non-Market Conditions

When accounting for stock options, understanding the distinction between market and non-market vesting conditions is crucial because they affect how and when compensation expense is recognized.

Definitions

- Market Conditions: Conditions related to the market price of the company’s stock, such as achieving a target share price or relative total shareholder return (TSR).

- Non-Market Conditions: Conditions unrelated to market performance, typically service conditions (e.g., continued employment) or performance conditions based on operational targets (e.g., revenue growth, EBITDA).

Key Accounting Principles

| Condition Type | Measurement Basis | Expense Recognition | Adjustments Over Time |

|---|---|---|---|

| Market | Fair value at grant date, including market condition | Recognized regardless of whether market condition is met | No adjustment for failure to meet market condition; expense remains unchanged |

| Non-Market | Fair value at grant date, excluding non-market condition | Recognized based on probability of satisfying condition | Adjusted for changes in probability of meeting condition |

Mind Map: Market vs. Non-Market Conditions

Detailed Explanation

Market Conditions

Market conditions are factored into the grant date fair value of the stock options using valuation models such as Black-Scholes or Monte Carlo simulations. Because these conditions are inherently uncertain and tied to stock price movements, accounting standards require that the entire compensation cost be recognized over the vesting period regardless of whether the market condition is ultimately met.

Example:

A company grants options with a market condition that the stock price must reach $100 within 3 years. The grant date fair value, which includes this market condition, is $15 per option.

- The company will recognize the full compensation expense based on the $15 fair value over the vesting period.

- If the stock price never reaches $100, the expense is not reversed.

Non-Market Conditions

Non-market conditions are not included in the grant date fair value calculation. Instead, the fair value is measured assuming these conditions will be met. The expense recognized is adjusted over the vesting period based on the probability of satisfying these conditions.

Example:

A company grants options with a service condition requiring 3 years of employment and a performance condition requiring $10 million in revenue growth.

- The grant date fair value is calculated without considering the revenue target.

- Initially, the company estimates a 70% chance of meeting the revenue target.

- Compensation expense is recognized based on this probability.

- If the probability changes to 90% in year 2, the expense is adjusted upward accordingly.

Mind Map: Example Walkthrough

Best Practices

- Clearly identify and classify vesting conditions at grant date.

- Use appropriate valuation models that incorporate market conditions accurately.

- Regularly update estimates of non-market condition probabilities and adjust expense accordingly.

- Document assumptions and changes thoroughly for audit and disclosure purposes.

Summary Table

| Aspect | Market Conditions | Non-Market Conditions |

|---|---|---|

| Included in Fair Value? | Yes | No |

| Expense Recognition Basis | Full grant date fair value over vesting | Adjusted for probability of achievement |

| Subsequent Adjustments | No | Yes |

| Examples | Stock price targets, TSR | Service period, revenue targets |

By understanding and applying these distinctions, accountants and equity analysts can ensure accurate and compliant accounting for stock options, reflecting the true economic impact of equity compensation.

4.3 Best Practices for Tracking and Updating Vesting Conditions

Tracking and updating vesting conditions accurately is crucial for ensuring the correct accounting treatment of stock options. Vesting conditions determine when employees earn the right to exercise their options, impacting expense recognition and financial reporting.

Key Best Practices for Tracking and Updating Vesting Conditions

- Establish Clear Documentation: Maintain detailed records of all vesting schedules, including service and performance conditions.

- Use Automated Tracking Systems: Implement software solutions to monitor vesting milestones and trigger updates.

- Regularly Review Performance Conditions: Since performance-based vesting can change, periodic reassessment is essential.

- Communicate Changes Promptly: Any modifications to vesting terms should be documented and communicated to accounting and HR teams.

- Integrate Cross-Functional Collaboration: Ensure coordination between finance, HR, and legal departments for consistent updates.

- Maintain Audit Trails: Keep logs of all changes to vesting conditions for compliance and audit purposes.

Mind Map: Tracking Vesting Conditions

Mind Map: Updating Vesting Conditions

Example 1: Tracking Service-Based Vesting

Scenario: An employee is granted stock options with a 4-year vesting schedule, vesting 25% each year.

Best Practice Application:

- Use an automated equity management system to track each anniversary date.

- The system sends alerts one month before each vesting date.

- HR confirms employee status (active, terminated) before vesting is recognized.

- Accounting records expense monthly based on the vesting schedule.

Outcome: Accurate, timely expense recognition and reduced risk of errors.

Example 2: Updating Performance-Based Vesting Conditions

Scenario: A company grants stock options with vesting contingent on achieving a revenue target within 2 years.

Best Practice Application:

- Finance team monitors quarterly revenue against targets.

- At the end of year 1, revenue is below target; the company revises the vesting probability to 50%.

- Accounting adjusts the cumulative expense recognized to date accordingly.

- All changes are documented and communicated to stakeholders.

Outcome: Reflects realistic expense recognition aligned with performance outcomes.

Summary

Tracking and updating vesting conditions requires a structured approach combining clear documentation, automation, frequent reviews, and cross-functional collaboration. By implementing these best practices, accountants and equity analysts can ensure accurate financial reporting and compliance.

4.4 Example: Adjusting Expense for Performance-Based Vesting

Performance-based vesting conditions require that certain performance targets be met before stock options vest. These conditions affect the expense recognition because the probability of meeting these targets can change over time, requiring adjustments to the recognized compensation expense.

Understanding Performance-Based Vesting Adjustments

When accounting for performance-based stock options, companies must estimate the likelihood that the performance conditions will be met at each reporting date. This probability estimate directly impacts the amount of expense recognized.

If the probability changes, the cumulative expense recognized to date must be adjusted accordingly.

Mind Map: Key Concepts in Adjusting Expense for Performance-Based Vesting

Example Scenario

Company ABC grants 10,000 stock options to an employee with a 3-year vesting period, contingent on achieving a revenue growth target.

- Grant date fair value per option: $15

- Vesting period: 3 years

- Performance condition: Revenue growth of 10% per year

At the grant date, management estimates a 60% probability that the target will be met.

Step 1: Initial Expense Recognition

- Total fair value = 10,000 options × $15 = $150,000

- Probability-adjusted fair value = $150,000 × 60% = $90,000

- Annual expense over 3 years = $90,000 / 3 = $30,000 per year

Journal entry each year:

Dr. Compensation Expense $30,000

Cr. Additional Paid-in Capital - Stock Options $30,000

Step 2: Reassessment at Year 2

At the end of year 2, management revises the probability to 80% based on updated revenue forecasts.

- Revised total fair value = $150,000 × 80% = $120,000

- Cumulative expense to recognize by year 2 = $120,000 × (2/3) = $80,000

- Expense recognized to date = $30,000 (Year 1) + $30,000 (Year 2) = $60,000

- Additional expense to recognize in Year 2 = $80,000 - $60,000 = $20,000

Journal entry for Year 2 adjustment:

Dr. Compensation Expense $20,000

Cr. Additional Paid-in Capital - Stock Options $20,000

Total expense recognized at the end of Year 2 is $80,000.

Step 3: Final Year Expense

At the end of Year 3, the performance target is met, confirming the 80% probability estimate.

- Total expense to recognize = $120,000

- Expense recognized to date = $80,000

- Expense for Year 3 = $120,000 - $80,000 = $40,000

Journal entry:

Dr. Compensation Expense $40,000

Cr. Additional Paid-in Capital - Stock Options $40,000

Mind Map: Journal Entries Over Vesting Period

Key Takeaways

- Performance-based vesting requires continuous probability assessment.

- Expense adjustments reflect changes in estimated likelihood of achieving targets.

- Proper documentation of assumptions and changes is critical for audit and disclosure.

- Transparent communication in financial statements enhances stakeholder understanding.

This example illustrates how accountants and equity analysts should approach the dynamic nature of performance-based vesting conditions, ensuring expenses are accurately reflected in financial reporting.

5. Expense Recognition and Amortization

5.1 Calculating Total Compensation Cost

Calculating the total compensation cost of stock options is a fundamental step in accounting for equity-based compensation. This cost represents the fair value of the stock options granted to employees and must be recognized as an expense over the vesting period.

Key Concepts in Calculating Total Compensation Cost

- Grant Date Fair Value: The estimated value of stock options at the grant date, typically calculated using option pricing models such as Black-Scholes or a binomial model.

- Number of Awards Granted: The total number of stock options granted to employees.

- Vesting Period: The time over which employees earn the right to exercise their stock options.

- Forfeiture Rate: The estimated percentage of options expected to be forfeited before vesting.

Mind Map: Components of Total Compensation Cost

Step-by-Step Calculation Process

-

Determine the Grant Date Fair Value per Option

- Use an appropriate option pricing model.

- Input relevant assumptions (e.g., stock price, volatility).

-

Calculate the Total Fair Value of the Award

- Multiply the fair value per option by the number of options granted.

-

Adjust for Expected Forfeitures

- Multiply the total fair value by (1 - forfeiture rate).

-

Allocate Expense Over the Vesting Period

- Recognize the adjusted total compensation cost as an expense on a straight-line basis over the vesting period.

Mind Map: Calculation Workflow

Example: Calculating Total Compensation Cost

Scenario:

- Company ABC grants 10,000 stock options to employees.

- Grant date fair value per option (calculated via Black-Scholes): $15.

- Vesting period: 4 years.

- Estimated forfeiture rate: 10%.

Calculation:

-

Total fair value before forfeiture adjustment:

- 10,000 options × $15 = $150,000

-

Adjust for forfeitures:

- $150,000 × (1 - 0.10) = $135,000

-

Annual expense recognition:

- $135,000 ÷ 4 years = $33,750 per year

Interpretation: Company ABC will recognize $33,750 as stock option compensation expense each year over the 4-year vesting period.

Mind Map: Example Breakdown

Best Practices

- Use Reliable Valuation Models: Ensure assumptions like volatility and risk-free rate are based on current and relevant market data.

- Regularly Update Forfeiture Estimates: Adjust expense recognition if actual forfeitures differ significantly from estimates.

- Document Assumptions Clearly: Maintain transparency for auditors and stakeholders.

- Coordinate with HR: To track actual grants, forfeitures, and exercises accurately.

By following these steps and best practices, accountants and equity analysts can accurately calculate and recognize the total compensation cost associated with stock option grants, ensuring compliance and clear financial reporting.

5.2 Expense Recognition Over the Vesting Period

Expense recognition for stock options is a critical accounting process that ensures the compensation cost is matched with the period in which employees earn their awards. This section breaks down how to recognize expense over the vesting period with clear explanations, mind maps, and practical examples.

Understanding the Vesting Period

The vesting period is the timeframe during which employees must provide service to earn the right to exercise their stock options. Expense recognition aligns with this period to reflect the cost of compensation accurately.

Key Principles of Expense Recognition

- Total Compensation Cost: Determined at the grant date as the fair value of the stock options.

- Expense Allocation: This total cost is recognized as an expense over the vesting period.

- Straight-Line Method: Most common approach, spreading expense evenly unless service is non-linear.

- Adjustments: For forfeitures or changes in vesting conditions, expense recognition is adjusted accordingly.

Mind Map: Expense Recognition Process

Step-by-Step Example

Scenario:

- Grant Date: Jan 1, 2024

- Number of Options Granted: 1,000

- Fair Value per Option at Grant Date: $10

- Vesting Period: 4 years (service-based, straight-line)

- Estimated Forfeiture Rate: 5%

Step 1: Calculate Total Compensation Cost

Total fair value = 1,000 options × $10 = $10,000

Adjusting for forfeitures:

Expected options to vest = 1,000 × (1 - 0.05) = 950

Adjusted total compensation cost = 950 × $10 = $9,500

Step 2: Allocate Expense Over Vesting Period

Annual expense = $9,500 ÷ 4 years = $2,375 per year

Step 3: Record Expense Each Year

| Year | Expense Recognized | Cumulative Expense |

|---|---|---|

| 2024 | $2,375 | $2,375 |

| 2025 | $2,375 | $4,750 |

| 2026 | $2,375 | $7,125 |

| 2027 | $2,375 | $9,500 |

Mind Map: Adjusting for Forfeitures

Handling Changes in Vesting Conditions

If vesting conditions change (e.g., acceleration or extension), the expense recognition schedule must be updated to reflect the new vesting period or conditions.

Example: If the vesting period shortens from 4 years to 2 years after 1 year, the remaining expense must be recognized over the next year instead of the remaining 3 years.

Practical Tips and Best Practices

- Use robust tracking systems to monitor vesting and forfeitures.

- Regularly review forfeiture estimates and update expense accordingly.

- Document assumptions and changes in vesting conditions clearly.

- Coordinate with HR and legal teams to understand performance conditions.

Summary

Expense recognition over the vesting period ensures that stock option compensation costs are matched with the employee service period. Using clear estimates, adjusting for forfeitures, and updating for changes in vesting conditions are essential for accurate financial reporting.

5.3 Handling Modifications and Cancellations

Stock option modifications and cancellations are common events that can significantly impact the accounting treatment of stock-based compensation. Proper handling ensures accurate expense recognition and compliance with accounting standards such as ASC 718 and IFRS 2.

What Constitutes a Modification?

A modification occurs when the terms or conditions of an existing stock option award are changed. This can include:

- Changing the exercise price

- Extending the exercise period

- Altering vesting conditions

- Increasing the number of options granted

What Constitutes a Cancellation?

A cancellation happens when an option is terminated before it is exercised or vested, either voluntarily by the employee or by the company.

Mind Map: Handling Modifications and Cancellations

Accounting Treatment for Modifications

When a stock option is modified, the company must:

- Determine the fair value of the modified award at the modification date.

- Compare this fair value to the fair value of the original award immediately before the modification.

- Recognize any incremental compensation cost resulting from the modification over the remaining vesting period.

Key Point: The incremental cost is the difference between the fair value of the modified award and the original award.

Example: Modification of Exercise Price

Scenario:

- Original grant: 1,000 options with an exercise price of $50.

- Fair value at grant: $15 per option.

- After 1 year, the exercise price is reduced to $40 due to market conditions.

- Fair value of modified options at modification date: $20 per option.

- Remaining vesting period: 2 years.

Calculation:

- Incremental fair value = $20 - $15 = $5 per option

- Total incremental cost = 1,000 options * $5 = $5,000

- Recognize $5,000 over the remaining 2 years ($2,500 per year).

Accounting Treatment for Cancellations

When options are cancelled, the company must:

- Immediately recognize any unrecognized compensation cost related to the cancelled options.

- Reverse any previously recognized expense if applicable.

If the cancellation is accompanied by a replacement award, the accounting treatment depends on whether the replacement award is considered a modification or a new grant.

Example: Cancellation of Unvested Options

Scenario:

- 500 options granted with a fair value of $10 each.

- Vesting period: 4 years.

- After 2 years, 200 unvested options are cancelled.

- Previously recognized expense for cancelled options: 200 options * $10 * (2/4) = $1,000.

Accounting:

- Recognize the remaining unrecognized expense immediately: 200 options * $10 * (2/4) = $1,000.

- Total expense recognized for cancelled options: $2,000.

Best Practices for Handling Modifications and Cancellations

- Documentation: Maintain detailed records of all modifications and cancellations, including rationale and approval.

- Internal Controls: Implement controls to track changes and ensure timely and accurate accounting.

- Communication: Inform stakeholders, including auditors and equity analysts, about significant modifications or cancellations.

- Regular Review: Periodically review stock option plans to identify potential modifications or cancellations early.

Summary

Handling modifications and cancellations requires careful re-measurement and immediate recognition of incremental costs or remaining expenses. Using clear documentation, robust controls, and transparent communication helps ensure compliance and accurate financial reporting.

5.4 Example: Amortizing Stock Option Expense in Financial Statements

Amortizing stock option expense involves recognizing the total compensation cost related to stock options over the vesting period. This ensures that the expense is matched with the period in which employees earn the options.

Key Concepts Mind Map

Step-by-Step Example

Scenario:

A tech company grants 10,000 stock options to an employee on January 1, 2024. The options vest over 4 years with a straight-line vesting schedule (25% each year). The fair value of each option at the grant date is $15.

Step 1: Calculate Total Compensation Cost

- Total Compensation Cost = Number of Options × Fair Value per Option

- = 10,000 × $15 = $150,000

Step 2: Determine Annual Expense

- Vesting Period = 4 years

- Annual Expense = Total Compensation Cost ÷ Vesting Period

- = $150,000 ÷ 4 = $37,500 per year

Step 3: Record Expense Each Year

| Year | Expense Recognized | Cumulative Expense |

|---|---|---|

| 2024 | $37,500 | $37,500 |

| 2025 | $37,500 | $75,000 |

| 2026 | $37,500 | $112,500 |

| 2027 | $37,500 | $150,000 |

Step 4: Journal Entry Example (Year 1)

| Account | Debit | Credit |

|---|---|---|

| Stock-based Compensation Expense | $37,500 | |

| Additional Paid-in Capital (APIC) - Stock Options | $37,500 |

Mind Map: Journal Entry Flow

Adjusting for Forfeitures

If the employee leaves after 2 years and forfeits unvested options, the company needs to adjust the expense accordingly.

- Vested options after 2 years = 10,000 × 50% = 5,000

- Total compensation cost to recognize = 5,000 × $15 = $75,000

- Expense recognized over 2 years = $75,000 ÷ 2 = $37,500 per year

Revised Cumulative Expense Table:

| Year | Expense Recognized | Cumulative Expense |

|---|---|---|

| 2024 | $37,500 | $37,500 |

| 2025 | $37,500 | $75,000 |

No expense is recognized in years 3 and 4 due to forfeiture.

Practical Tips and Best Practices

- Consistent Methodology: Use a consistent amortization method (usually straight-line) unless a different method better reflects the pattern of employee service.

- Forfeiture Estimates: Regularly update forfeiture estimates and adjust expense accordingly.

- Documentation: Maintain clear documentation of grant dates, vesting schedules, and assumptions.

- System Integration: Utilize accounting software to automate amortization schedules and journal entries.

By following this approach, accountants and equity analysts can accurately amortize stock option expenses, ensuring compliance with accounting standards and providing transparent financial reporting.

6. Tax Implications and Accounting

6.1 Tax Deductibility of Stock Options

Understanding the tax deductibility of stock options is crucial for accountants and equity analysts to accurately assess the financial impact of equity-based compensation on a company’s tax position. This section explores the principles, rules, and practical examples related to the tax treatment of stock options.

Overview

Stock options provide employees the right to purchase company shares at a predetermined price. From a tax perspective, the timing and amount of deductible expenses for the company depend on the type of stock option granted and the jurisdiction’s tax laws.

Types of Stock Options and Their Tax Treatment

-

Non-Qualified Stock Options (NQSOs)

- Taxable to the employee at exercise

- Employer receives a tax deduction equal to the amount included in the employee’s income

-

Incentive Stock Options (ISOs)

- Generally no tax deduction for the employer unless a disqualifying disposition occurs

Mind Map: Tax Deductibility of Stock Options

Timing of Tax Deduction

For NQSOs, the employer’s tax deduction typically arises at the time the employee exercises the option. The deductible amount is the difference between the fair market value (FMV) of the stock at exercise and the exercise price paid by the employee.

For ISOs, the employer generally does not get a tax deduction unless the employee sells the stock before meeting specific holding period requirements (a disqualifying disposition).

Example 1: Tax Deductibility for NQSOs

Scenario:

- Employee granted NQSOs with an exercise price of $20 per share.

- At exercise, FMV is $50 per share.

- Employee exercises 1,000 options.

Calculation:

- Tax Deductible Amount = (FMV - Exercise Price) × Number of Options

- = ($50 - $20) × 1,000 = $30,000

Implication:

- Employer can claim a tax deduction of $30,000 in the year of exercise.

Example 2: Tax Treatment for ISOs

Scenario:

- Employee granted ISOs with an exercise price of $15.

- FMV at exercise is $40.

- Employee exercises 500 options but holds the shares.

Tax Implication:

- Employer does not get a tax deduction at exercise.

- If the employee sells the shares before the required holding period, the employer may claim a deduction equal to the amount included in the employee’s income.

Mind Map: Example Walkthrough for NQSOs

Jurisdictional Considerations

Tax rules vary by country. For example:

- In the United States, the Internal Revenue Code governs stock option taxation with clear distinctions between NQSOs and ISOs.

- In Canada, stock options may have different tax treatments, often with deductions available at exercise or sale.

- European countries have diverse rules, often requiring careful local tax consultation.

Best Practices for Accountants and Equity Analysts

- Maintain detailed records of grant dates, exercise dates, FMV, and exercise prices.

- Coordinate with tax advisors to understand jurisdiction-specific rules.

- Monitor employee dispositions to identify disqualifying events affecting deductibility.

- Ensure accurate timing of tax deductions in financial reporting.

Summary

Tax deductibility of stock options hinges on the option type, timing of exercise, and jurisdictional tax laws. NQSOs generally provide a clear tax deduction at exercise, while ISOs offer potential tax benefits to employees but limited deductions to employers unless certain conditions are met. Proper documentation and understanding of local tax rules are essential for accurate accounting and compliance.

6.2 Accounting for Deferred Tax Assets and Liabilities

When accounting for stock options, understanding the tax implications is crucial, especially the recognition of deferred tax assets (DTAs) and deferred tax liabilities (DTLs). These arise due to differences in the timing of expense recognition between financial accounting and tax reporting.

What Are Deferred Tax Assets and Liabilities?

- Deferred Tax Asset (DTA): Occurs when the tax deduction exceeds the book expense, leading to future tax benefits.

- Deferred Tax Liability (DTL): Occurs when the book expense exceeds the tax deduction, leading to future tax payments.

Why Do DTAs and DTLs Arise in Stock Option Accounting?

Stock options create differences because:

- For financial reporting, compensation expense is recognized over the vesting period based on the grant-date fair value.

- For tax purposes, the deduction is generally recognized when the option is exercised, and the amount is based on the intrinsic value (market price minus exercise price).

This timing and measurement difference creates temporary differences leading to DTAs or DTLs.

Mind Map: Deferred Tax Accounting for Stock Options

Step-by-Step Accounting Process

- Calculate cumulative stock-based compensation expense for financial reporting.

- Determine tax deduction amount at exercise (intrinsic value).

- Calculate the temporary difference:

- Temporary Difference = Cumulative Book Expense - Cumulative Tax Deduction

- Apply the enacted tax rate to temporary difference to find deferred tax asset or liability.

- Assess whether a valuation allowance is necessary for DTAs.

- Record journal entries to recognize deferred tax assets/liabilities.

Example 1: Recognizing Deferred Tax Asset

Scenario:

- Grant-date fair value per option: $10

- Number of options granted: 1,000

- Vesting period: 4 years

- Tax deduction per option at exercise (intrinsic value): $15

- Enacted tax rate: 30%

Year 2:

- Cumulative book expense recognized: $5,000 (500 options vested × $10 × 1 year)

- Tax deduction so far: $0 (no exercises yet)

Temporary difference:

- $5,000 (book) - $0 (tax) = $5,000

Deferred tax asset:

- $5,000 × 30% = $1,500

Journal entry:

Dr. Deferred Tax Asset 1,500

Cr. Income Tax Benefit 1,500

This DTA reflects future tax savings when options are exercised.

Example 2: Deferred Tax Liability Scenario

In rare cases where the tax deduction is less than the book expense (e.g., due to forfeitures or changes in assumptions), a deferred tax liability may arise.

Scenario:

- Cumulative book expense: $8,000

- Tax deduction so far: $10,000

Temporary difference:

- $8,000 - $10,000 = -$2,000 (negative temporary difference)

Deferred tax liability:

- $2,000 × 30% = $600

Journal entry:

Dr. Income Tax Expense 600

Cr. Deferred Tax Liability 600

Valuation Allowance Considerations

- If it is more likely than not that some or all of the deferred tax asset will not be realized (e.g., insufficient future taxable income), a valuation allowance must be recorded.

Example:

- Deferred tax asset: $1,500

- Management estimates only 70% realizability

Valuation allowance:

- $1,500 × 30% = $450

Journal entry:

Dr. Income Tax Expense 450

Cr. Valuation Allowance 450

Summary Best Practices

- Maintain detailed tracking of cumulative book expense and tax deductions.

- Regularly update assumptions and tax rates to reflect current conditions.

- Assess valuation allowance each reporting period.

- Coordinate with tax teams to ensure alignment on exercise data and tax deductions.

- Disclose deferred tax assets and liabilities clearly in financial statements.

By carefully accounting for deferred tax assets and liabilities related to stock options, accountants and equity analysts can ensure accurate financial reporting and provide stakeholders with transparent insights into the company’s tax position.

6.3 Best Practices for Coordinating Tax and Financial Reporting

Coordinating tax and financial reporting for stock options is critical to ensure compliance, optimize tax benefits, and maintain accurate financial statements. Misalignment between tax and accounting treatments can lead to errors, restatements, or missed tax deductions.

Key Best Practices

-

Early Collaboration Between Tax and Accounting Teams

- Foster communication to align assumptions, timelines, and data.

- Jointly review stock option plans and changes.

-

Consistent Documentation and Tracking

- Maintain detailed records of grant dates, vesting schedules, exercises, cancellations, and modifications.

- Track tax basis and book basis separately but reconcile regularly.

-

Understand Differences in Tax and Accounting Treatments

- Tax deductions often occur at exercise or sale, while accounting expense is recognized over the vesting period.

- Deferred tax assets/liabilities must be recorded for timing differences.

-

Use Integrated Systems and Automation

- Implement software that supports both tax and financial reporting needs.

- Automate data flow to reduce manual errors.

-

Regular Reconciliation and Review

- Periodically reconcile book expense, tax deductions, and deferred tax balances.

- Adjust deferred tax assets/liabilities for changes in tax laws or valuation allowances.

-

Stay Updated on Regulatory Changes

- Monitor updates in tax codes and accounting standards affecting stock options.

- Train teams on implications and required adjustments.

Mind Map: Coordinating Tax and Financial Reporting for Stock Options

Example 1: Reconciling Tax Deduction and Book Expense

Scenario: A company grants stock options with a fair value of $100,000 recognized as expense over 4 years. The employees exercise options in year 3, generating a tax deduction of $120,000 due to an increase in stock price.

Accounting Treatment:

- Recognize $25,000 expense per year for 4 years.

- Record deferred tax asset/liability for timing differences.

Tax Treatment:

- Deduct $120,000 in year 3 when exercised.

Best Practice:

- Maintain a deferred tax asset for the difference between book expense recognized ($75,000 by year 3) and tax deduction ($120,000).

- Reconcile deferred tax balances quarterly.

Example 2: Using Integrated Software for Coordination

Scenario: A multinational tech company uses a cloud-based equity management platform that integrates with their ERP and tax software.

Benefits:

- Real-time updates on option grants, exercises, and cancellations.

- Automated calculation of book expense and tax deductions.

- Generates reports for both accounting and tax teams.

Best Practice:

- Regularly validate data inputs.

- Schedule monthly cross-functional meetings to review reports.

Summary

Coordinating tax and financial reporting for stock options requires proactive communication, robust documentation, understanding of differing treatments, and leveraging technology. By following these best practices, organizations can ensure accurate reporting, optimize tax benefits, and reduce compliance risks.

6.4 Example: Recording Tax Effects of Stock Option Exercises

When employees exercise stock options, companies must account not only for the equity transactions but also for the related tax effects. This section provides a detailed example of how to record the tax effects arising from stock option exercises, including journal entries and a mind map to visualize the process.

Understanding the Tax Effects

When stock options are exercised, the company may receive a tax deduction equal to the intrinsic value of the options at exercise (i.e., the difference between the market price and the exercise price). This creates a deferred tax asset or reduces deferred tax liabilities, impacting the company’s tax expense.

Mind Map: Tax Effects of Stock Option Exercises

Example Scenario

- Company: Tech Solutions Inc.

- Employee stock options exercised: 10,000 options

- Exercise price per option: $15

- Market price at exercise: $25

- Tax rate: 30%

- Previously recognized compensation expense: $50,000