Management Accounting Principles

1. Introduction to Management Accounting

1.1 Definition and Scope of Management Accounting

Definition: Management Accounting is the process of preparing management reports and accounts that provide accurate and timely financial and statistical information required by managers to make day-to-day and short-term decisions. Unlike financial accounting, which focuses on historical data and external reporting, management accounting is primarily concerned with internal decision-making and future planning.

Scope of Management Accounting: Management accounting covers a broad range of activities that support managerial functions such as planning, controlling, decision-making, and performance evaluation. The scope can be broadly categorized as follows:

- Cost Accounting: Recording, classification, and allocation of costs to products or services.

- Budgeting and Forecasting: Preparing detailed financial plans and predicting future financial outcomes.

- Performance Measurement: Using financial and non-financial metrics to evaluate business performance.

- Decision Support: Providing relevant data and analysis to aid managerial decisions.

- Financial Analysis: Analyzing financial statements and ratios to assess business health.

- Risk Management: Identifying and managing financial risks.

Mind Map: Definition and Scope of Management Accounting

Practical Example: Management Accounting in Action

Scenario: A medium-sized manufacturing company, “ABC Manufacturing,” wants to improve its profitability and operational efficiency.

-

Cost Accounting: ABC Manufacturing tracks direct material, direct labor, and overhead costs for each product line to understand profitability.

-

Budgeting: The management team prepares a detailed budget for the upcoming year, including sales forecasts, production costs, and capital expenditures.

-

Performance Measurement: Monthly variance reports compare actual costs and revenues against budgets to identify areas needing attention.

-

Decision Support: When considering launching a new product, management accounting provides cost-volume-profit analysis to determine the break-even point and expected profitability.

-

Financial Analysis: Ratio analysis helps management assess liquidity and solvency to ensure the company can meet its obligations.

This integrated approach helps ABC Manufacturing make informed decisions, control costs, and plan for sustainable growth.

Mind Map: Practical Example - ABC Manufacturing

Summary

Management Accounting is a vital internal function that equips managers with the financial and statistical insights needed to steer their organizations effectively. Its scope is comprehensive, covering cost management, budgeting, performance evaluation, decision support, financial analysis, and risk management. By leveraging management accounting principles, companies can enhance decision-making, optimize resource use, and achieve strategic objectives.

1.2 Differences Between Financial and Management Accounting

Management accounting and financial accounting are two essential branches of accounting that serve different purposes, audiences, and use distinct methodologies. Understanding their differences is crucial for accountants, especially management accountants who often bridge the gap between these two fields.

Key Differences at a Glance

Purpose

- Financial Accounting: Primarily focused on providing a clear and standardized view of the company’s financial health to external stakeholders such as investors, creditors, and regulatory bodies.

- Management Accounting: Focuses on providing detailed financial and non-financial information to internal management to aid in planning, controlling, and decision-making.

Example: A company’s financial accountant prepares an annual report showing overall profitability for shareholders, while the management accountant prepares a departmental cost report to help managers control expenses.

Audience

- Financial Accounting: External users including shareholders, banks, tax authorities, and regulatory agencies.

- Management Accounting: Internal users such as CEOs, department heads, and operational managers.

Example: The CFO uses financial accounting reports to communicate with investors, whereas the production manager uses management accounting reports to optimize manufacturing processes.

Time Orientation

- Financial Accounting: Historical focus, reporting on past financial performance.

- Management Accounting: Both historical and forward-looking, including forecasts and budgets.

Example: Financial accounting reports last quarter’s sales figures; management accounting prepares sales forecasts for the next quarter.

Regulatory Requirements and Standards

- Financial Accounting: Must comply with Generally Accepted Accounting Principles (GAAP), International Financial Reporting Standards (IFRS), or other regulatory frameworks.

- Management Accounting: No mandatory standards; reports are customized to meet internal needs.

Example: Financial statements must follow IFRS guidelines, while management accounting reports can vary widely in format and content.

Frequency and Reporting

- Financial Accounting: Reports are typically prepared on a fixed schedule (quarterly, annually).

- Management Accounting: Reports can be generated as frequently as needed (daily, weekly, monthly).

Example: A financial accountant prepares quarterly income statements; a management accountant may prepare weekly cost variance reports.

Level of Detail

- Financial Accounting: Provides aggregated data summarizing the entire organization.

- Management Accounting: Provides detailed, segmented data often broken down by product line, department, or project.

Example: Financial accounting shows total company revenue; management accounting breaks down revenue by product category.

Focus and Content

- Financial Accounting: Focuses on financial results and position, including balance sheets, income statements, and cash flow statements.

- Management Accounting: Includes financial data plus operational metrics such as production efficiency, customer satisfaction, and cost control.

Example: Financial accounting reports net income; management accounting analyzes cost per unit and customer acquisition costs.

Mind Map: Summary of Differences

Practical Example: Comparing Reports

| Aspect | Financial Accounting Report | Management Accounting Report |

|---|---|---|

| Report Type | Annual Financial Statements | Monthly Budget vs Actual Report |

| Audience | External Investors | Internal Department Managers |

| Content | Summary of revenues, expenses, assets, liabilities | Detailed breakdown of departmental costs and variances |

| Purpose | Compliance and external communication | Performance monitoring and decision support |

| Frequency | Annually, Quarterly | Monthly, Weekly, or as needed |

Conclusion

While both financial and management accounting deal with financial data, their objectives, audiences, and methodologies differ significantly. Management accountants must understand these differences to effectively translate financial data into actionable insights for internal decision-making, ensuring the organization’s strategic and operational goals are met.

1.3 Role of Management Accountants in Corporate Finance

Management accountants play a pivotal role in corporate finance by bridging the gap between financial data and strategic decision-making. Their expertise goes beyond traditional bookkeeping and financial reporting, focusing on providing insights that drive business growth, efficiency, and profitability.

Core Responsibilities of Management Accountants in Corporate Finance

Decision Support

Management accountants provide critical financial insights that help management make informed decisions. They prepare detailed budgets and forecasts, analyze financial trends, and assess risks associated with various business initiatives.

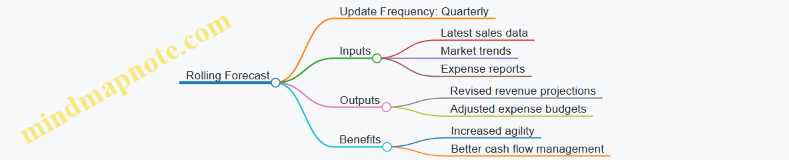

Example: A management accountant at a manufacturing company creates a rolling forecast that helps the company adjust production schedules based on fluctuating demand, ensuring optimal inventory levels and cost efficiency.

Cost Management

They analyze and classify costs to identify areas where the company can reduce expenses without compromising quality. Techniques like Activity-Based Costing (ABC) help allocate overheads more accurately.

Example: In a retail chain, the management accountant uses ABC to identify that certain store locations incur disproportionately high utility costs, prompting targeted energy-saving initiatives.

Performance Measurement

Management accountants develop and monitor Key Performance Indicators (KPIs) and conduct variance analysis to evaluate business performance against budgets and benchmarks.

Example: A management accountant at a service firm tracks customer acquisition cost and profit margins monthly, enabling the marketing team to optimize campaigns for better ROI.

Strategic Planning

They assist in evaluating capital investments, pricing strategies, and long-term financial plans to align with corporate objectives.

Example: Before launching a new product line, the management accountant conducts a Net Present Value (NPV) analysis to determine the project’s profitability and advises the executive team accordingly.

Compliance & Reporting

Management accountants ensure internal financial reports comply with corporate policies and regulatory requirements while upholding ethical standards.

Example: In a publicly traded company, the management accountant prepares internal reports that support external financial disclosures, ensuring accuracy and compliance with regulatory frameworks.

Summary Mind Map: Role of Management Accountants in Corporate Finance

In conclusion, management accountants are essential to corporate finance as they provide actionable financial insights, support strategic initiatives, and ensure sound financial management. Their role is integral to driving sustainable business success through informed decision-making and efficient resource management.

1.4 Overview of Key Management Accounting Principles

Management accounting is built on a set of core principles that guide accountants and finance professionals in providing relevant, timely, and accurate information to support managerial decision-making. Understanding these principles helps ensure that management accounting practices align with organizational goals and promote effective resource utilization.

Key Principles of Management Accounting

Below is a mind map that summarizes the foundational principles:

Principle 1: Relevance

Management accounting information should be directly applicable to the decisions at hand. For example, a management accountant preparing a cost analysis for a product line should focus on costs that will change with production volume, ignoring sunk costs.

Example: A company is deciding whether to discontinue a product. Relevant costs include variable manufacturing costs and avoidable fixed costs. Sunk costs like past research expenses are irrelevant.

Principle 2: Accuracy and Reliability

While perfect accuracy is often impossible, management accounting strives for reliable data to build trust.

Example: When calculating overhead allocation, using a consistent and well-documented method ensures reliability, such as applying machine hours consistently across production departments.

Principle 3: Timeliness

Information must be delivered promptly to influence decisions effectively.

Example: A monthly budget variance report delivered within the first week of the following month allows managers to take corrective actions swiftly.

Principle 4: Cost-Benefit Consideration

The cost of gathering and processing information should not exceed the expected benefits.

Example: Instead of tracking every minor expense, a company may group small costs into a single category to reduce administrative effort.

Principle 5: Consistency

Using consistent accounting methods over time enables meaningful comparisons.

Example: If a company uses absorption costing one year, switching to variable costing the next without reconciliation can confuse performance analysis.

Principle 6: Flexibility

Management accounting systems should adapt to different managerial needs and changing environments.

Example: During a market downturn, a company might shift focus from growth metrics to cost control metrics in its reports.

Principle 7: Objectivity

Information should be free from bias to maintain integrity.

Example: An accountant should report unfavorable budget variances honestly, even if it reflects poorly on their department.

Principle 8: Confidentiality

Sensitive financial data must be protected to prevent misuse.

Example: Salary cost reports should be restricted to HR and senior management only.

Principle 9: Future Orientation

Management accounting emphasizes forecasting and planning rather than just historical reporting.

Example: Preparing a rolling forecast that updates sales projections quarterly to guide production planning.

Principle 10: Integration

Management accounting should be integrated with other business functions like marketing, operations, and HR.

Example: Collaborating with the sales team to develop pricing strategies based on cost data and market demand.

Summary Mind Map

Summary: Management Accounting Principles Mind Map

By adhering to these principles, management accountants can provide actionable insights that help organizations optimize performance, control costs, and achieve strategic objectives.

1.5 Practical Example: How Management Accounting Supports Decision Making in a Manufacturing Firm

Management accounting plays a crucial role in helping manufacturing firms make informed decisions by providing relevant, timely, and accurate financial and non-financial information. This section illustrates how management accounting principles are applied in a manufacturing setting to support decision-making processes.

Scenario Overview

Imagine a mid-sized manufacturing firm, “ABC Manufacturing,” that produces electronic components. The management team needs to decide whether to launch a new product line, optimize production costs, and improve overall profitability.

Step 1: Cost Analysis and Classification

Management accountants begin by classifying costs related to the new product:

- Direct Materials: Raw materials specifically used for the new product.

- Direct Labor: Wages paid to workers assembling the product.

- Manufacturing Overhead: Indirect costs such as factory rent, utilities, and depreciation.

This classification helps in understanding the cost structure and estimating the product’s profitability.

Step 2: Budgeting and Forecasting

The management accountant prepares a budget forecast for the new product, including expected sales volume, production costs, and marketing expenses.

- Sales Forecast: 10,000 units at $50 each.

- Material Cost: $15 per unit.

- Labor Cost: $10 per unit.

- Overhead Allocation: $5 per unit.

- Marketing Expenses: $20,000 fixed.

This budget helps management anticipate cash flows and profitability.

Step 3: Cost-Volume-Profit (CVP) Analysis

Using CVP analysis, management accountants calculate the break-even point and profit potential.

- Contribution Margin per Unit: $50 - ($15 + $10 + $5) = $20

- Break-even Units: $20,000 / $20 = 1,000 units

This shows that the firm needs to sell at least 1,000 units to cover fixed marketing expenses.

Step 4: Decision Making

With this information, management can:

- Assess whether the sales forecast is realistic.

- Determine pricing strategies to maximize profit.

- Identify cost control opportunities in materials or labor.

- Decide to proceed with the product launch if projected profits meet company targets.

Step 5: Performance Measurement

After launch, management accountants track actual costs and revenues against the budget to analyze variances.

- Material Cost Variance: Actual vs Standard cost.

- Labor Efficiency Variance: Actual hours vs standard hours.

This continuous monitoring helps in taking corrective actions.

Summary

Through cost classification, budgeting, CVP analysis, and performance measurement, management accounting equips ABC Manufacturing with the necessary insights to make data-driven decisions. This integrated approach minimizes risks and maximizes profitability.

Additional Example: Optimizing Production Scheduling

Management accountants analyze machine hours and labor availability to schedule production efficiently, balancing demand and capacity.

By aligning production schedules with cost data, the firm reduces overtime costs and inventory holding expenses.

This practical example demonstrates how management accounting principles are embedded in everyday decision-making within a manufacturing firm, providing a clear roadmap for accountants and management alike.

2. Cost Concepts and Classifications

2.1 Understanding Fixed, Variable, and Mixed Costs

Management accounting hinges on a clear understanding of cost behavior. Knowing how costs behave relative to changes in production or sales volume is essential for budgeting, forecasting, and decision-making. This section explores three fundamental cost types: fixed, variable, and mixed costs, with practical examples and mind maps to clarify each concept.

Fixed Costs

Definition: Fixed costs are expenses that remain constant in total regardless of changes in the level of production or sales volume within a relevant range.

Characteristics:

- Do not fluctuate with production volume.

- Incurred even if production is zero.

- Examples include rent, salaries of permanent staff, insurance, and depreciation.

Example: A company rents a factory for $10,000 per month. Whether it produces 1,000 units or 10,000 units, the rent remains $10,000.

Mind Map:

Variable Costs

Definition: Variable costs change in direct proportion to changes in production or sales volume.

Characteristics:

- Total variable costs increase as production increases.

- Cost per unit remains constant.

Example: A bakery spends $2 on ingredients for each loaf of bread. If it bakes 100 loaves, the total ingredient cost is $200; if it bakes 500 loaves, the cost is $1,000.

Mind Map:

Mixed Costs (Semi-Variable Costs)

Definition: Mixed costs contain both fixed and variable components. Part of the cost remains constant regardless of activity level, while another part varies with production volume.

Characteristics:

- Fixed portion is incurred even if production is zero.

- Variable portion fluctuates with production.

Example: A utility bill includes a fixed monthly charge of $100 plus $0.05 per kWh of electricity used. If the company uses 1,000 kWh, the total cost is $100 + (1,000 x $0.05) = $150.

Mind Map:

Practical Example: Classifying Costs in a Retail Business

| Cost Item | Type | Explanation |

|---|---|---|

| Store Rent | Fixed | Monthly rent remains constant regardless of sales volume. |

| Sales Commissions | Variable | Paid as a percentage of sales; increases with sales volume. |

| Electricity Bill | Mixed | Fixed monthly charge plus variable charge based on usage. |

| Salaries (Managers) | Fixed | Salaries paid regardless of store performance. |

| Packaging Materials | Variable | Cost increases with the number of products sold. |

Summary Mind Map

Understanding these cost behaviors enables management accountants to prepare accurate budgets, forecast costs effectively, and make informed pricing and production decisions. By integrating these principles with real-world examples, accountants can better communicate cost implications to management and support strategic planning.

2.2 Direct vs Indirect Costs: Definitions and Examples

Definitions

Direct Costs: Direct costs are expenses that can be directly traced to a specific cost object, such as a product, department, or project. These costs are incurred specifically for the production of goods or services and can be easily identified and measured.

Indirect Costs: Indirect costs, on the other hand, are expenses that cannot be directly traced to a single cost object. They are incurred for multiple cost objects and are often allocated based on a reasonable basis. These costs support the overall operations but are not directly linked to production.

Mind Map: Understanding Direct and Indirect Costs

Characteristics Comparison

| Aspect | Direct Costs | Indirect Costs |

|---|---|---|

| Traceability | Directly traceable to cost object | Not directly traceable |

| Examples | Raw materials, direct labor | Rent, utilities, administrative costs |

| Variability | Usually variable with production | Usually fixed or semi-variable |

| Accounting Treatment | Charged directly to product cost | Allocated using cost drivers |

Examples of Direct Costs

-

Raw Materials in Manufacturing:

- Steel used in car manufacturing.

- Fabric used in garment production.

-

Direct Labor:

- Wages paid to assembly line workers.

- Salaries of machine operators.

-

Manufacturing Supplies:

- Nuts, bolts, and screws used in product assembly.

Examples of Indirect Costs

-

Factory Overhead:

- Electricity to run the factory lighting.

- Maintenance costs of machinery.

-

Administrative Expenses:

- Salaries of HR and accounting staff.

- Office rent and utilities.

-

Depreciation:

- Depreciation on factory building and equipment.

Practical Example: Direct vs Indirect Costs in a Bakery

| Cost Item | Type | Explanation |

|---|---|---|

| Flour | Direct Cost | Flour is directly used in baking bread and can be traced to each batch. |

| Baker’s Wages | Direct Cost | Wages paid to bakers who make the bread directly. |

| Oven Electricity | Indirect Cost | Electricity powers the oven but is shared across all products. |

| Rent for Bakery Premises | Indirect Cost | Rent supports the entire bakery operation, not just one product. |

Mind Map: Allocating Costs in a Bakery

Best Practices for Management Accountants

- Accurate Identification: Clearly distinguish between direct and indirect costs to improve cost control and pricing strategies.

- Appropriate Allocation Bases: Use logical and consistent bases (e.g., machine hours, labor hours) to allocate indirect costs fairly.

- Regular Review: Periodically review cost classifications to reflect changes in operations or production methods.

Summary

Understanding the distinction between direct and indirect costs is fundamental for accurate product costing, budgeting, and financial analysis. Direct costs are easily traceable and variable with production, while indirect costs support overall operations and require allocation. Proper classification ensures better decision-making and financial transparency.

2.3 Product Costs vs Period Costs

Understanding the distinction between product costs and period costs is fundamental in management accounting as it impacts inventory valuation, cost control, and profitability analysis.

Definition and Overview

- Product Costs: These are costs that are directly associated with the production of goods. They include all costs necessary to create a product and prepare it for sale.

- Period Costs: These costs are not tied directly to production and are expensed in the period in which they are incurred.

Mind Map: Product Costs vs Period Costs

Detailed Explanation

| Aspect | Product Costs | Period Costs |

|---|---|---|

| Definition | Costs incurred to create a product | Costs incurred outside production activities |

| Accounting Treatment | Capitalized as inventory, expensed when sold | Expensed immediately in the income statement |

| Examples | Raw materials, direct labor, factory overhead | Marketing expenses, administrative salaries |

| Impact on Financials | Affect cost of goods sold and inventory values | Affect operating expenses and net income |

Practical Examples

-

Manufacturing Company Example

- Product Costs:

- Steel used in car frames

- Wages of assembly line workers

- Depreciation of factory equipment

- Period Costs:

- Advertising expenses for new car model

- Salaries of corporate office staff

- Product Costs:

-

Retail Business Example

- Product Costs:

- Purchase price of inventory

- Shipping costs to warehouse

- Period Costs:

- Store rent

- Sales staff salaries

- Product Costs:

Mind Map: Accounting Treatment Flow

Best Practices

- Accurate Classification: Ensure costs are properly classified to avoid misstating inventory or expenses.

- Consistent Application: Apply the same classification method consistently for comparability.

- Use Examples for Training: Use real-life examples to train accounting teams on classification.

Summary

Product costs are integral to the manufacturing process and are capitalized as inventory until the product is sold. Period costs are associated with time periods and are expensed immediately. Correctly distinguishing between these costs ensures accurate financial reporting and better management decision-making.

2.4 Cost Behavior Analysis and Its Importance

What is Cost Behavior Analysis?

Cost behavior analysis is the study of how costs change in response to variations in a company’s level of activity. Understanding cost behavior helps management accountants predict how costs will change with changes in production volume, sales, or other business activities.

Types of Cost Behavior

Costs generally behave in three main ways:

- Fixed Costs: Costs that remain constant regardless of activity level.

- Variable Costs: Costs that vary directly with the level of activity.

- Mixed Costs: Costs that have both fixed and variable components.

Why is Cost Behavior Analysis Important?

- Budgeting and Forecasting: Helps create accurate budgets by predicting how costs will change.

- Cost Control: Identifies which costs can be controlled or influenced.

- Pricing Decisions: Assists in setting prices by understanding cost structures.

- Profit Planning: Helps forecast profits at different activity levels.

Mind Map: Overview of Cost Behavior Analysis

Fixed Costs Explained

Fixed costs remain unchanged within a relevant range of activity. For example, a company pays $5,000 monthly rent regardless of whether it produces 1,000 or 10,000 units.

Example:

- Rent expense of $5,000/month.

- Production increases from 1,000 to 2,000 units.

- Rent remains $5,000, so cost per unit decreases from $5 to $2.50.

Variable Costs Explained

Variable costs change in direct proportion to activity levels.

Example:

- Raw material cost is $3 per unit.

- Producing 1,000 units costs $3,000.

- Producing 2,000 units costs $6,000.

Mixed Costs Explained

Mixed costs have a fixed base plus a variable component.

Example:

- Utility bill = $200 fixed + $0.10 per unit produced.

- Producing 1,000 units: $200 + (1,000 x $0.10) = $300.

- Producing 2,000 units: $200 + (2,000 x $0.10) = $400.

Mind Map: Examples of Cost Behavior

Practical Example: Cost Behavior Analysis in a Bakery

A bakery produces cakes and wants to analyze its cost behavior.

| Cost Type | Description | Cost Behavior |

|---|---|---|

| Rent | Monthly bakery rent | Fixed |

| Flour | Cost per kg of flour | Variable |

| Electricity | Base charge + usage per hour | Mixed |

- Rent: $2,000/month (fixed)

- Flour: $1.50/kg (variable)

- Electricity: $100 base + $5 per hour used

If the bakery operates 100 hours and uses 500 kg of flour:

- Rent = $2,000

- Flour = 500 kg x $1.50 = $750

- Electricity = $100 + (100 x $5) = $600

Total Costs = $2,000 + $750 + $600 = $3,350

If the bakery increases operation to 150 hours and 700 kg of flour:

- Rent = $2,000 (fixed)

- Flour = 700 x $1.50 = $1,050

- Electricity = $100 + (150 x $5) = $850

Total Costs = $2,000 + $1,050 + $850 = $3,900

This analysis helps the bakery predict how costs will increase with production and operating hours.

Summary

Cost behavior analysis is a foundational principle in management accounting that enables accountants and managers to understand how costs react to changes in business activity. By classifying costs into fixed, variable, and mixed categories and analyzing their behavior, organizations can make informed decisions on budgeting, pricing, and cost control.

Additional Mind Map: Importance of Cost Behavior Analysis in Decision Making

2.5 Practical Example: Classifying Costs in a Retail Business

In a retail business, understanding and classifying costs accurately is crucial for effective management accounting. This helps in pricing, budgeting, and profitability analysis. Let’s explore how costs can be classified with clear examples and mind maps.

Step 1: Identify Cost Types

Retail businesses typically incur various costs. These can be broadly categorized as:

- Fixed Costs: Costs that remain constant regardless of sales volume.

- Variable Costs: Costs that fluctuate directly with sales volume.

- Mixed Costs: Costs that have both fixed and variable components.

Mind Map: Cost Types in Retail

Step 2: Direct vs Indirect Costs

- Direct Costs: Costs that can be directly traced to a product or service.

- Indirect Costs: Costs that cannot be directly traced to a single product.

In retail:

- Direct Costs: Purchase cost of inventory (COGS)

- Indirect Costs: Store rent, utilities, administrative salaries

Mind Map: Direct and Indirect Costs

Step 3: Product Costs vs Period Costs

- Product Costs: Costs related to acquiring or producing inventory.

- Period Costs: Costs that are expensed in the period incurred.

In retail:

- Product Costs: Purchase price of goods, shipping fees for inventory

- Period Costs: Advertising, rent, office salaries

Mind Map: Product vs Period Costs

Example Scenario: “FashionHub” Retail Store

FashionHub is a retail clothing store. Below is a breakdown of their monthly costs:

| Cost Item | Amount ($) | Classification |

|---|---|---|

| Store Rent | 5,000 | Fixed, Indirect, Period Cost |

| Salaries (Sales Staff) | 8,000 | Fixed, Indirect, Period Cost |

| Inventory Purchase | 20,000 | Variable, Direct, Product Cost |

| Sales Commissions | 2,000 | Variable, Direct, Period Cost |

| Utilities (Electricity) | 1,200 | Mixed, Indirect, Period Cost |

| Packaging Materials | 1,000 | Variable, Direct, Product Cost |

| Advertising | 3,000 | Fixed, Indirect, Period Cost |

Analysis:

-

Fixed Costs: Store Rent, Salaries, Advertising

-

Variable Costs: Inventory Purchase, Sales Commissions, Packaging

-

Mixed Costs: Utilities (part fixed, part variable)

-

Direct Costs: Inventory Purchase, Packaging, Sales Commissions (linked to sales)

-

Indirect Costs: Rent, Salaries, Utilities, Advertising

-

Product Costs: Inventory Purchase, Packaging

-

Period Costs: Rent, Salaries, Advertising, Utilities, Sales Commissions

Visualizing the Classification

Why This Classification Matters

- Pricing: Knowing direct costs helps set product prices that cover costs and generate profit.

- Budgeting: Fixed and variable cost separation aids in creating flexible budgets.

- Cost Control: Identifying indirect costs helps management focus on overhead reduction.

- Profitability Analysis: Product vs period cost distinction ensures accurate profit measurement.

Summary

Classifying costs in a retail business like FashionHub provides clarity on how expenses behave and relate to sales. This classification supports better decision-making, budgeting, and financial control.

By applying these principles and using mind maps, management accountants can communicate cost structures effectively to stakeholders and improve overall business performance.

3. Costing Methods and Techniques

3.1 Job Costing: Principles and Application

Job costing is a fundamental management accounting technique used to assign costs to specific jobs or projects. It is especially useful in industries where products or services are customized or produced in small batches, such as construction, consulting, or custom manufacturing.

Principles of Job Costing

- Cost Accumulation: Costs are accumulated separately for each job.

- Direct and Indirect Costs: Direct materials, direct labor, and a fair share of overhead are assigned to each job.

- Job Cost Sheet: A document that records all costs related to a particular job.

- Cost Control: Monitoring costs against budgets or estimates to control expenses.

Mind Map: Job Costing Principles

Application of Job Costing

- Identify the Job: Define the specific project or order.

- Estimate Costs: Predict direct materials, labor, and overhead.

- Track Actual Costs: Record all costs incurred during the job.

- Allocate Overhead: Apply overhead costs based on a predetermined rate.

- Analyze Results: Compare actual costs to estimates for performance evaluation.

Practical Example: Custom Furniture Manufacturing

Scenario: A custom furniture company receives an order for a bespoke dining table.

- Direct Materials: Wood, varnish, hardware.

- Direct Labor: Hours spent by carpenters and finishers.

- Overhead: Factory rent, utilities allocated based on labor hours.

Job Cost Sheet Snapshot:

| Cost Element | Estimated Cost | Actual Cost | Variance |

|---|---|---|---|

| Direct Materials | $1,200 | $1,250 | +$50 |

| Direct Labor | $800 | $750 | -$50 |

| Overhead | $400 | $420 | +$20 |

| Total | $2,400 | $2,420 | +$20 |

This detailed tracking helps management assess profitability and identify areas for cost control.

Mind Map: Job Costing Application Steps

Best Practices for Job Costing

- Maintain detailed and accurate job cost sheets.

- Use technology (e.g., ERP systems) to automate cost tracking.

- Regularly review cost variances to improve estimates.

- Train staff on the importance of accurate data entry.

Additional Example: Consulting Firm

A consulting firm uses job costing to track hours and expenses for each client project.

- Direct Labor: Consultant hours billed.

- Direct Expenses: Travel, materials.

- Overhead: Allocated based on billable hours.

This enables precise billing and profitability analysis per client.

Summary

Job costing is an essential principle in management accounting that enables organizations to assign costs accurately to individual jobs, facilitating better cost control, pricing decisions, and profitability analysis. By applying job costing principles with detailed tracking and analysis, management accountants can provide valuable insights that drive business success.

3.2 Process Costing: When and How to Use It

What is Process Costing?

Process costing is a management accounting technique used to allocate costs to mass-produced, homogeneous products that pass through a series of continuous processes or departments. Unlike job costing, which tracks costs for individual jobs or batches, process costing averages costs over all units produced during a period.

When to Use Process Costing

Process costing is ideal in industries where:

- Production is continuous or repetitive.

- Products are indistinguishable from each other.

- Costs are accumulated by process or department rather than by individual job.

Common industries using process costing:

- Chemicals

- Food and beverages

- Textiles

- Petroleum refining

- Paper manufacturing

How Process Costing Works

Costs are collected for each process or department for a specific period. These costs include:

- Direct materials

- Direct labor

- Manufacturing overhead

The total costs are then divided by the number of units produced to find the cost per unit.

Mind Map: Process Costing Overview

Step-by-Step Process Costing Example

Scenario: A company manufactures bottled fruit juice. The production involves two processes: Mixing and Bottling.

| Process | Costs Incurred (Monthly) | Units Produced |

|---|---|---|

| Mixing | $50,000 | 10,000 |

| Bottling | $30,000 | 10,000 |

Step 1: Calculate Cost per Unit for Each Process

- Mixing: $50,000 / 10,000 units = $5 per unit

- Bottling: $30,000 / 10,000 units = $3 per unit

Step 2: Total Cost per Unit

- $5 (Mixing) + $3 (Bottling) = $8 per bottled juice unit

Interpretation: Each bottle of juice costs $8 to produce through both processes.

Mind Map: Process Costing Calculation

Best Practices in Process Costing

- Accurate Tracking of Costs by Department: Ensure all direct materials, labor, and overhead are properly assigned to each process.

- Consistent Measurement of Output: Units produced must be measured consistently to avoid distortions in unit cost.

- Use of Equivalent Units: When production is partially complete, calculate equivalent units to fairly assign costs.

- Regular Reconciliation: Periodically reconcile costs to identify discrepancies early.

Example: Handling Equivalent Units

Suppose in the Bottling process, 10,000 units are started, but only 8,000 are fully completed by month-end. The remaining 2,000 units are 50% complete.

Calculating Equivalent Units:

- Completed units = 8,000

- Partially completed units = 2,000 x 50% = 1,000

- Total equivalent units = 8,000 + 1,000 = 9,000

If the bottling cost is $30,000:

- Cost per equivalent unit = $30,000 / 9,000 = $3.33

This method ensures costs are fairly allocated between completed and in-process units.

Mind Map: Equivalent Units in Process Costing

Summary

Process costing is a vital tool for management accountants in industries with continuous production. By understanding when and how to apply process costing, accountants can provide accurate cost information to support pricing, budgeting, and performance evaluation.

Additional Practical Example

Industry: Paper Manufacturing

- Multiple processes: Pulping, Pressing, Drying

- Monthly costs and units tracked per process

- Use of equivalent units for in-progress inventory

Outcome: Enables management to identify cost drivers and optimize each process for cost efficiency.

This comprehensive understanding of process costing, supported by clear examples and mind maps, equips management accountants to implement best practices effectively.

3.3 Activity-Based Costing (ABC): A Detailed Approach

Overview: Activity-Based Costing (ABC) is a costing methodology that assigns overhead and indirect costs to related products and services by identifying cost drivers. Unlike traditional costing methods that allocate overhead based on a single volume measure (like labor hours or machine hours), ABC recognizes the complexity of overhead costs and assigns them more accurately based on the activities that generate those costs.

Why Use ABC?

- Provides more accurate product costing

- Helps identify inefficient or non-value-adding activities

- Supports better pricing, budgeting, and cost control decisions

Core Principles of ABC

- Identify Activities: Break down the production or service process into distinct activities.

- Assign Costs to Activities: Collect overhead costs and assign them to activities based on resource consumption.

- Determine Cost Drivers: Identify measurable factors that cause the cost of each activity.

- Assign Costs to Products/Services: Use cost drivers to allocate activity costs to products or services.

Mind Map: Activity-Based Costing Process

Step-by-Step Example: ABC in a Furniture Manufacturing Company

Scenario: A furniture company produces two products: Chairs and Tables. Traditional costing allocates overhead based on direct labor hours, but management suspects this distorts product costs.

Step 1: Identify Activities and Costs

- Machine Setup: $30,000

- Quality Inspection: $20,000

- Material Handling: $10,000

- Order Processing: $15,000

Step 2: Determine Cost Drivers and Activity Volumes

| Activity | Cost Driver | Total Cost | Chairs (Volume) | Tables (Volume) |

|---|---|---|---|---|

| Machine Setup | Number of Setups | $30,000 | 100 | 50 |

| Quality Inspection | Inspection Hours | $20,000 | 200 | 300 |

| Material Handling | Material Moves | $10,000 | 400 | 100 |

| Order Processing | Number of Orders | $15,000 | 150 | 50 |

Step 3: Calculate Activity Rates

- Machine Setup Rate = $30,000 / (100 + 50) = $200 per setup

- Quality Inspection Rate = $20,000 / (200 + 300) = $40 per inspection hour

- Material Handling Rate = $10,000 / (400 + 100) = $20 per material move

- Order Processing Rate = $15,000 / (150 + 50) = $75 per order

Step 4: Assign Activity Costs to Products

| Activity | Chairs Cost (Volume × Rate) | Tables Cost (Volume × Rate) |

|---|---|---|

| Machine Setup | 100 × $200 = $20,000 | 50 × $200 = $10,000 |

| Quality Inspection | 200 × $40 = $8,000 | 300 × $40 = $12,000 |

| Material Handling | 400 × $20 = $8,000 | 100 × $20 = $2,000 |

| Order Processing | 150 × $75 = $11,250 | 50 × $75 = $3,750 |

| Total Overhead | $47,250 | $27,750 |

Step 5: Compare with Traditional Costing

- Traditional overhead allocation might have assigned costs based solely on labor hours, potentially overcosting Chairs or Tables.

Mind Map: Benefits of ABC

Best Practices for Implementing ABC

- Start with a pilot project focusing on a specific product line or department

- Engage cross-functional teams to accurately identify activities and drivers

- Use software tools to manage and analyze ABC data

- Regularly review and update cost drivers and activities

- Communicate findings clearly to management and operational teams

Additional Example: ABC in a Service Company

A consulting firm uses ABC to allocate overhead costs such as administrative support, IT services, and client onboarding.

- Activities: Client Meetings, Report Preparation, Research

- Cost Drivers: Number of Meetings, Hours Spent on Reports, Research Hours

By applying ABC, the firm discovers that certain clients consume disproportionately more resources, enabling better pricing and resource allocation.

Summary: Activity-Based Costing provides a granular and accurate approach to overhead allocation by focusing on activities and their drivers. This method helps management accountants deliver insights that improve cost control, pricing strategies, and overall organizational efficiency.

3.4 Standard Costing and Variance Analysis

Standard costing is a fundamental management accounting technique that involves assigning predetermined costs to products or services. These standard costs serve as benchmarks against which actual costs are compared to identify variances. Variance analysis then helps management understand the reasons behind cost deviations and take corrective actions.

What is Standard Costing?

Standard costing involves setting expected costs for materials, labor, and overhead based on historical data, industry standards, and efficiency targets. These standards are used for budgeting, cost control, and performance evaluation.

Benefits of Standard Costing:

- Simplifies cost control and budgeting

- Facilitates variance analysis

- Enhances decision-making

- Motivates employees by setting clear cost targets

Components of Standard Costing

Variance Analysis Overview

Variance analysis compares actual costs to standard costs to identify differences (variances). Variances are classified as favorable (costs less than standard) or unfavorable (costs more than standard).

Types of variances include:

- Material Variance (Price and Usage)

- Labor Variance (Rate and Efficiency)

- Overhead Variance (Spending and Efficiency)

Material Variance

- Material Price Variance (MPV): Difference between actual price paid and standard price, multiplied by actual quantity purchased.

- Material Usage Variance (MUV): Difference between actual quantity used and standard quantity allowed, multiplied by standard price.

Formula:

- MPV = (Actual Price - Standard Price) × Actual Quantity

- MUV = (Actual Quantity - Standard Quantity) × Standard Price

Example:

A company sets a standard price of $5 per kg for raw material and expects to use 1000 kg for production. Actual purchase was 1100 kg at $4.80 per kg.

- MPV = ($4.80 - $5.00) × 1100 = -$220 (Favorable)

- MUV = (1100 - 1000) × $5.00 = $500 (Unfavorable)

Interpretation: The company paid less per kg than expected (favorable), but used more material than the standard (unfavorable).

Labor Variance

- Labor Rate Variance (LRV): Difference between actual hourly wage and standard wage, multiplied by actual hours worked.

- Labor Efficiency Variance (LEV): Difference between actual hours worked and standard hours allowed, multiplied by standard wage rate.

Formula:

- LRV = (Actual Rate - Standard Rate) × Actual Hours

- LEV = (Actual Hours - Standard Hours) × Standard Rate

Example:

Standard labor rate is $20/hour, and standard hours for a job are 50 hours. Actual hours worked were 55 hours at $18/hour.

- LRV = ($18 - $20) × 55 = -$110 (Favorable)

- LEV = (55 - 50) × $20 = $100 (Unfavorable)

Interpretation: The company paid a lower wage rate than standard (favorable), but took more hours than planned (unfavorable).

Overhead Variance

- Variable Overhead Spending Variance: Difference between actual variable overhead and standard variable overhead based on actual hours.

- Variable Overhead Efficiency Variance: Difference between actual hours and standard hours allowed, multiplied by standard variable overhead rate.

Example:

Standard variable overhead rate is $3 per labor hour. For a job requiring 50 hours standard, actual hours were 55, and actual variable overhead cost was $170.

- Standard variable overhead = 50 × $3 = $150

- Spending Variance = $170 - (55 × $3) = $170 - $165 = $5 (Unfavorable)

- Efficiency Variance = (55 - 50) × $3 = 5 × $3 = $15 (Unfavorable)

Integrated Example: Putting It All Together

A furniture manufacturer sets the following standards for producing one table:

| Cost Element | Standard Quantity | Standard Price/Rate |

|---|---|---|

| Wood | 10 board feet | $4 per board foot |

| Labor | 5 hours | $15 per hour |

| Variable Overhead | 5 hours | $3 per hour |

Actual data for one table:

- Wood used: 12 board feet at $3.80 per board foot

- Labor hours: 6 hours at $14 per hour

- Variable overhead: $20

Calculate variances:

- Material Price Variance = (3.80 - 4.00) × 12 = -$2.40 (Favorable)

- Material Usage Variance = (12 - 10) × 4.00 = $8.00 (Unfavorable)

- Labor Rate Variance = (14 - 15) × 6 = -$6.00 (Favorable)

- Labor Efficiency Variance = (6 - 5) × 15 = $15.00 (Unfavorable)

- Variable Overhead Spending Variance = $20 - (6 × 3) = $20 - $18 = $2 (Unfavorable)

- Variable Overhead Efficiency Variance = (6 - 5) × 3 = $3 (Unfavorable)

Interpretation:

- The company saved on material price and labor rate but used more materials and labor hours than planned.

- Overhead costs were slightly higher than expected.

Best Practices for Standard Costing and Variance Analysis

- Regularly Update Standards: Reflect current market conditions and operational efficiencies.

- Investigate Significant Variances: Identify root causes to improve processes.

- Use Variance Analysis for Performance Management: Align incentives with cost control.

- Integrate with Budgeting and Forecasting: Ensure consistency across financial planning.

Summary Mind Map

By mastering standard costing and variance analysis, management accountants can provide valuable insights that drive cost efficiency, operational improvements, and strategic decision-making.

3.5 Practical Example: Implementing Activity-Based Costing (ABC) in a Service Company

Activity-Based Costing (ABC) is a costing methodology that assigns overhead and indirect costs to related products and services by identifying cost drivers. While traditionally used in manufacturing, ABC is highly effective in service companies where overheads are significant and diverse.

Scenario Overview

Imagine a mid-sized IT consulting firm, “TechSolutions,” providing three main services:

- Software Development

- IT Support

- Training and Workshops

The firm wants to better understand the true cost of each service to improve pricing strategies and profitability.

Step 1: Identify Activities and Cost Pools

In ABC, costs are assigned to activities first, then to services based on their consumption of these activities.

Key activities at TechSolutions:

- Project Management

- Software Development

- Customer Support

- Training Preparation

- Training Delivery

- Administrative Support

Mind Map: Activities and Cost Pools

Step 2: Assign Costs to Activity Cost Pools

The firm collects overhead costs (e.g., salaries of project managers, support staff, office rent, utilities) and assigns them to the above activities based on resource usage.

| Activity | Overhead Cost ($) |

|---|---|

| Project Management | 120,000 |

| Software Development | 200,000 |

| Customer Support | 80,000 |

| Training Preparation | 40,000 |

| Training Delivery | 60,000 |

| Administrative Support | 50,000 |

Total Overhead = $550,000

Step 3: Determine Cost Drivers for Each Activity

Cost drivers are factors that cause the cost of an activity to increase or decrease.

| Activity | Cost Driver | Quantity |

|---|---|---|

| Project Management | Number of Projects | 10 |

| Software Development | Development Hours | 20,000 |

| Customer Support | Number of Support Tickets | 5,000 |

| Training Preparation | Number of Training Sessions | 15 |

| Training Delivery | Number of Training Hours | 120 |

| Administrative Support | Number of Employees | 50 |

Mind Map: Cost Drivers

Step 4: Calculate Activity Rates

Activity Rate = Overhead Cost / Cost Driver Quantity

| Activity | Overhead Cost ($) | Cost Driver Quantity | Activity Rate ($ per unit) |

|---|---|---|---|

| Project Management | 120,000 | 10 | 12,000 |

| Software Development | 200,000 | 20,000 | 10 |

| Customer Support | 80,000 | 5,000 | 16 |

| Training Preparation | 40,000 | 15 | 2,666.67 |

| Training Delivery | 60,000 | 120 | 500 |

| Administrative Support | 50,000 | 50 | 1,000 |

Step 5: Assign Costs to Services Based on Activity Consumption

Assume the following consumption data for each service:

| Service | Projects | Dev Hours | Support Tickets | Training Sessions | Training Hours | Employees |

|---|---|---|---|---|---|---|

| Software Development | 6 | 15,000 | 500 | 0 | 0 | 30 |

| IT Support | 3 | 3,000 | 4,000 | 0 | 0 | 15 |

| Training & Workshops | 1 | 2,000 | 500 | 15 | 120 | 5 |

Calculations:

-

Software Development:

- Project Management: 6 projects * $12,000 = $72,000

- Software Development: 15,000 hours * $10 = $150,000

- Customer Support: 500 tickets * $16 = $8,000

- Training Preparation: 0 * $2,666.67 = $0

- Training Delivery: 0 * $500 = $0

- Administrative Support: 30 employees * $1,000 = $30,000

- Total Overhead Assigned = $260,000

-

IT Support:

- Project Management: 3 * $12,000 = $36,000

- Software Development: 3,000 * $10 = $30,000

- Customer Support: 4,000 * $16 = $64,000

- Training Preparation: 0 * $2,666.67 = $0

- Training Delivery: 0 * $500 = $0

- Administrative Support: 15 * $1,000 = $15,000

- Total Overhead Assigned = $145,000

-

Training & Workshops:

- Project Management: 1 * $12,000 = $12,000

- Software Development: 2,000 * $10 = $20,000

- Customer Support: 500 * $16 = $8,000

- Training Preparation: 15 * $2,666.67 = $40,000

- Training Delivery: 120 * $500 = $60,000

- Administrative Support: 5 * $1,000 = $5,000

- Total Overhead Assigned = $145,000

Step 6: Analyze Results and Take Action

- Insight: Software Development consumes the largest overhead, mainly due to development hours and project management.

- Pricing: The firm can now price each service more accurately, reflecting the true overhead costs.

- Cost Control: Identify high-cost activities (e.g., training preparation) and explore efficiency improvements.

Summary Mind Map: ABC Implementation Steps

Key Takeaways

- ABC provides detailed insight into overhead consumption.

- It helps service companies allocate indirect costs more accurately.

- Enables better pricing, budgeting, and cost management decisions.

This practical example demonstrates how management accountants in service industries can leverage ABC to enhance financial clarity and strategic decision-making.

4. Budgeting and Forecasting

4.1 Types of Budgets: Operating, Capital, and Cash Budgets

Budgeting is a cornerstone of management accounting, enabling organizations to plan, control, and evaluate their financial resources effectively. Understanding the different types of budgets is essential for management accountants to tailor financial plans according to organizational needs.

Operating Budget

The operating budget is a detailed projection of all expected income and expenses related to the day-to-day operations of a business over a specific period, usually a fiscal year. It focuses on revenues, cost of goods sold, and operating expenses.

Key Components:

- Sales Revenue

- Cost of Goods Sold (COGS)

- Selling, General & Administrative Expenses (SG&A)

- Depreciation

- Operating Income

Example: A retail company forecasts sales of $1,000,000 for the next year. The cost of goods sold is estimated at 60% of sales, and operating expenses are projected at $250,000. The operating budget helps the company anticipate a gross profit of $400,000 and operating income of $150,000.

Mind Map: Operating Budget

Capital Budget

The capital budget deals with long-term investments and expenditures on assets such as property, plant, and equipment. It helps organizations plan for significant expenditures that will impact the business over multiple years.

Key Components:

- Project Identification

- Cost Estimates

- Financing Methods

- Expected Returns (NPV, IRR)

- Payback Period

Example: A manufacturing firm plans to invest $500,000 in new machinery. The capital budget will include the cost of the machinery, installation, and projected benefits such as increased production capacity and cost savings.

Mind Map: Capital Budget

Cash Budget

The cash budget forecasts cash inflows and outflows over a specific period, helping ensure the company maintains adequate liquidity to meet its obligations.

Key Components:

- Cash Receipts (from sales, loans, investments)

- Cash Disbursements (expenses, loan repayments, capital expenditures)

- Opening and Closing Cash Balances

Example: A service company expects cash collections of $200,000 in January but has payments totaling $180,000. The cash budget helps the company plan for a closing cash balance of $20,000, ensuring it can cover all expenses without liquidity issues.

Mind Map: Cash Budget

Integrated Example: Seasonal Business Budgeting

Consider a company that sells winter apparel. Its operating budget will forecast higher sales and expenses during colder months. The capital budget may include plans to purchase additional inventory racks, while the cash budget ensures sufficient liquidity during off-peak months.

Operating Budget Snapshot:

- Peak season sales in Q4: $500,000

- Off-season sales in Q2: $150,000

Capital Budget Plan:

- Invest $50,000 in new inventory shelving before Q4

Cash Budget Insight:

- Cash inflows dip in Q2, requiring short-term financing to cover expenses

This integrated approach ensures the company aligns its operational activities, investment decisions, and cash management effectively.

Best Practices for Budget Preparation

- Align budgets with strategic goals: Ensure each budget supports overall business objectives.

- Use historical data and market trends: Base forecasts on reliable data.

- Involve cross-functional teams: Gain insights from different departments.

- Review and revise regularly: Adapt budgets to changing conditions.

- Leverage technology: Use budgeting software for accuracy and efficiency.

By mastering these types of budgets and their interplay, management accountants can provide invaluable insights that drive better financial planning and organizational success.

4.2 Zero-Based Budgeting vs Incremental Budgeting

Introduction

Budgeting is a critical function in management accounting, helping organizations plan their financial resources effectively. Two popular budgeting approaches are Zero-Based Budgeting (ZBB) and Incremental Budgeting. Understanding their differences, advantages, and practical applications can help management accountants choose the best method for their organization’s needs.

What is Zero-Based Budgeting (ZBB)?

Zero-Based Budgeting is a budgeting method where every expense must be justified for each new period, starting from a “zero base.” Unlike traditional budgeting, no previous budget figures are automatically carried forward.

- Key Characteristics:

- Starts from zero every period

- Requires detailed justification for all expenses

- Focuses on activities and cost drivers

Mind Map: Zero-Based Budgeting

Example of Zero-Based Budgeting

Imagine a marketing department preparing its annual budget. Instead of using last year’s budget as a baseline, the team must justify every expense, such as:

- Advertising campaigns

- Social media management

- Event sponsorships

Each activity is evaluated for its contribution to business goals. For example, if a particular event sponsorship did not generate leads last year, it might be cut or reduced.

What is Incremental Budgeting?

Incremental Budgeting is a traditional budgeting approach where the previous year’s budget is used as a base, and adjustments are made by adding or subtracting a percentage to account for expected changes.

- Key Characteristics:

- Uses prior budget as baseline

- Adjusts for inflation, growth, or cuts

- Simple and quick to prepare

Mind Map: Incremental Budgeting

Example of Incremental Budgeting

A manufacturing company’s maintenance department had a budget of $500,000 last year. For the new year, the company expects a 5% increase in costs due to inflation and decides to increase the budget to $525,000 without detailed review of each expense.

Comparative Analysis

| Aspect | Zero-Based Budgeting (ZBB) | Incremental Budgeting |

|---|---|---|

| Starting Point | Zero, no assumptions from previous budget | Previous year’s budget |

| Focus | Justification of all expenses | Adjustments to existing budget |

| Time and Effort | High, detailed analysis required | Low, simple adjustments |

| Cost Control | Strong emphasis on eliminating waste | Risk of perpetuating inefficiencies |

| Flexibility | High, adapts to current priorities | Low, may ignore changing business conditions |

| Suitability | Organizations needing cost optimization or restructuring | Stable organizations with predictable costs |

Best Practices for Using ZBB and Incremental Budgeting

-

When to Use Zero-Based Budgeting:

- During organizational restructuring

- When cost reduction is a priority

- For departments with variable or discretionary spending

-

When to Use Incremental Budgeting:

- For stable departments with predictable expenses

- When time and resources for budgeting are limited

- For organizations with minimal changes expected

Practical Example: Choosing the Right Approach

A software company’s R&D department is launching new projects and needs to allocate funds carefully. They opt for Zero-Based Budgeting to justify each project’s funding based on potential ROI.

Conversely, their IT support department has consistent, predictable costs and uses Incremental Budgeting, increasing last year’s budget by 3% to account for inflation.

Summary

Both Zero-Based Budgeting and Incremental Budgeting have their place in management accounting. ZBB promotes cost discipline and alignment with strategic goals but requires more effort. Incremental Budgeting is simpler and faster but may overlook inefficiencies. Management accountants should assess their organization’s context and objectives to select the most appropriate budgeting method.

4.3 Forecasting Techniques for Revenue and Expenses

Forecasting revenue and expenses is a critical component of management accounting that helps organizations plan for the future, allocate resources effectively, and make informed strategic decisions. Accurate forecasting enables management accountants to anticipate financial performance, identify potential risks, and seize opportunities.

Key Forecasting Techniques

Below are some of the most widely used forecasting techniques for revenue and expenses, along with practical examples and mind maps to help visualize the concepts.

Historical Data Analysis

This technique involves analyzing past financial data to predict future revenue and expenses. It assumes that historical trends will continue unless there are significant changes in the business environment.

- Example: A retail company reviews sales data from the last three years to forecast next quarter’s revenue, adjusting for seasonal trends.

Moving Averages

Moving averages smooth out short-term fluctuations and highlight longer-term trends by averaging data points over a specific period.

- Example: A manufacturing firm calculates a 3-month moving average of raw material costs to forecast expenses for the next quarter.

Regression Analysis

Regression analysis examines the relationship between dependent variables (e.g., revenue) and one or more independent variables (e.g., marketing spend, economic indicators).

- Example: A software company uses regression analysis to forecast revenue based on historical marketing expenditure and customer acquisition rates.

Exponential Smoothing

This technique assigns exponentially decreasing weights to older data, making recent observations more influential in the forecast.

- Example: A logistics company uses exponential smoothing to forecast fuel expenses, giving more weight to recent price changes.

Scenario Analysis

Scenario analysis involves creating multiple forecasts based on different assumptions about future conditions (e.g., optimistic, pessimistic, and most likely scenarios).

- Example: A construction firm prepares revenue forecasts under three scenarios: rapid market growth, stable conditions, and economic downturn.

Delphi Method

This is a qualitative forecasting technique that relies on expert opinions gathered through multiple rounds of questionnaires to reach a consensus.

- Example: A consulting firm uses the Delphi method to forecast expenses related to new regulatory compliance requirements.

Practical Example: Forecasting Revenue for a Seasonal Business

Context: A company selling winter sports equipment wants to forecast revenue for the upcoming year.

Approach:

- Use historical sales data from the past 5 years.

- Apply moving averages to smooth seasonal spikes.

- Incorporate regression analysis with weather forecasts as an independent variable.

- Develop three scenarios (normal winter, mild winter, severe winter) to understand potential revenue variations.

Outcome:

- The company prepares a flexible revenue forecast that helps in inventory planning and budgeting marketing expenses.

Summary

Effective forecasting combines quantitative methods like moving averages and regression with qualitative approaches such as scenario and Delphi methods. Management accountants should select techniques based on data availability, business complexity, and forecasting horizon to enhance accuracy and support strategic decision-making.

4.4 Best Practices for Effective Budget Preparation

Effective budget preparation is a cornerstone of successful management accounting. It ensures that resources are allocated efficiently, financial goals are realistic, and performance can be measured accurately. Below are key best practices, supported by mind maps and practical examples, to help management accountants craft robust budgets.

Involve Key Stakeholders

Engaging department heads, project managers, and other relevant personnel ensures the budget reflects operational realities and gains broader acceptance.

Example: In a corporate finance department, involving sales and marketing teams during budget preparation helped identify realistic revenue targets and marketing expenses, reducing the risk of over-optimistic forecasts.

Use Historical Data as a Baseline

Analyzing past budgets and actual results provides a foundation for forecasting future expenses and revenues.

Example: A retail company reviewed the last three years’ sales data to adjust their budget for seasonal fluctuations, ensuring inventory purchases aligned with expected demand peaks.

Adopt a Clear Budgeting Methodology

Choose between incremental, zero-based, or flexible budgeting based on organizational needs.

Example: A startup used zero-based budgeting to justify every expense from scratch, helping control costs tightly during rapid growth phases.

Set Realistic and Measurable Objectives

Budgets should align with strategic goals and be quantifiable to track performance.

Example: A manufacturing firm set a budget objective to reduce production costs by 5% within the next fiscal year, enabling clear performance evaluation.

Incorporate Contingency Planning

Include buffers for unexpected expenses or revenue shortfalls to maintain financial stability.

Example: A technology company allocated 10% of its budget as a contingency reserve to address potential supply chain disruptions.

Leverage Technology and Tools

Use budgeting software and spreadsheets to improve accuracy, collaboration, and version control.

Example: An accounting team implemented cloud-based budgeting software allowing real-time updates and collaboration across departments.

Regularly Review and Revise Budgets

Budgets should be dynamic documents, reviewed periodically to reflect changes in business conditions.

Example: A service company conducted quarterly budget reviews, adjusting forecasts based on client acquisition rates and project pipelines.

Summary Table of Best Practices with Examples

| Best Practice | Description | Example Scenario |

|---|---|---|

| Stakeholder Involvement | Engage relevant teams for input and buy-in | Sales team contributing to revenue forecasts |

| Historical Data Usage | Use past data to inform projections | Retailer analyzing seasonal sales trends |

| Clear Budgeting Methodology | Select appropriate budgeting approach | Startup using zero-based budgeting |

| Realistic Objectives | Set measurable, aligned goals | Manufacturer targeting 5% cost reduction |

| Contingency Planning | Include buffers for uncertainties | Tech company reserving 10% for supply risks |

| Leverage Technology | Utilize software for efficiency | Cloud budgeting tools enabling collaboration |

| Regular Review | Periodically update budgets | Quarterly reviews adjusting forecasts |

By integrating these best practices, management accountants can prepare budgets that are not only accurate and comprehensive but also flexible enough to adapt to changing business environments. This approach supports better decision-making and drives organizational success.

4.5 Practical Example: Creating a Flexible Budget for a Seasonal Business

Flexible budgeting is a powerful tool for businesses that experience fluctuations in activity levels, such as seasonal businesses. Unlike static budgets, which are fixed and prepared for a single level of activity, flexible budgets adjust according to actual output or sales volume, providing a more accurate and useful framework for performance evaluation and control.

Understanding the Need for a Flexible Budget in Seasonal Businesses

Seasonal businesses, such as ski resorts, ice cream shops, or holiday decoration retailers, face significant variations in sales and costs throughout the year. Preparing a static budget based on an average or expected activity level can lead to misleading variance analysis and poor decision-making.

Example: An ice cream shop expects high sales in summer months and low sales in winter. A static budget based on average annual sales would not reflect the true cost behavior or revenue potential during peak and off-peak seasons.

Step-by-Step Process to Create a Flexible Budget

-

Identify Cost Behavior Patterns

- Separate costs into fixed, variable, and mixed categories.

- Understand how each cost behaves relative to activity levels (e.g., sales volume, units produced).

-

Determine the Activity Levels

- Define relevant activity measures (e.g., number of customers, units sold).

- Identify the range of activity levels expected during different seasons.

-

Develop Cost Formulas

- For variable costs: Cost = Variable cost per unit × Activity level

- For fixed costs: Remain constant regardless of activity within relevant range

- For mixed costs: Separate into fixed and variable components using methods like high-low or regression analysis

-

Prepare Flexible Budget at Different Activity Levels

- Create budget scenarios for low, medium, and high activity periods.

-

Analyze Variances

- Compare actual results to the flexible budget corresponding to the actual activity level to identify true variances.

Mind Map: Creating a Flexible Budget for a Seasonal Business

Detailed Example: Ice Cream Shop Seasonal Flexible Budget

| Cost Item | Cost Behavior | Cost Driver | Cost Formula / Rate |

|---|---|---|---|

| Rent | Fixed | N/A | $2,000 per month |

| Ice Cream Ingredients | Variable | Units sold | $1.50 per unit |

| Utilities | Mixed | Units sold | $500 fixed + $0.10 per unit |

| Marketing | Fixed | N/A | $300 per month |

Activity Levels (Units Sold):

- Off-Peak (Winter): 1,000 units

- Shoulder (Spring/Fall): 3,000 units

- Peak (Summer): 6,000 units

Flexible Budget Calculations:

| Season | Units Sold | Rent | Ingredients (1.5 × Units) | Utilities (500 + 0.1 × Units) | Marketing | Total Cost |

|---|---|---|---|---|---|---|

| Off-Peak | 1,000 | 2000 | 1,500 | 500 + 100 = 600 | 300 | 4,400 |

| Shoulder | 3,000 | 2000 | 4,500 | 500 + 300 = 800 | 300 | 7,600 |

| Peak | 6,000 | 2000 | 9,000 | 500 + 600 = 1,100 | 300 | 12,400 |

Mind Map: Cost Breakdown for Ice Cream Shop

Using the Flexible Budget

Suppose actual sales in summer were 5,500 units instead of the budgeted 6,000 units. The flexible budget for 5,500 units would be:

- Rent: $2,000

- Ingredients: 5,500 × $1.50 = $8,250

- Utilities: $500 + (5,500 × $0.10) = $500 + $550 = $1,050

- Marketing: $300

- Total: $2,000 + $8,250 + $1,050 + $300 = $11,600

If the actual total cost was $12,000, the variance analysis would be:

- Total Variance = Actual Cost - Flexible Budget Cost = $12,000 - $11,600 = $400 (Unfavorable)

This variance is more meaningful than comparing actual costs to a static budget based on 6,000 units, as it accounts for the actual activity level.

Best Practices for Implementing Flexible Budgets in Seasonal Businesses

- Regularly update cost behavior assumptions based on recent data.

- Use multiple activity levels to prepare a range of budget scenarios.

- Train management accountants and operational managers on interpreting flexible budget variances.

- Integrate flexible budgeting with forecasting and performance measurement systems.

Summary

Flexible budgeting allows seasonal businesses to adapt their budgets to actual activity levels, providing more accurate cost control and performance evaluation. By understanding cost behaviors, developing cost formulas, and preparing budgets for different activity levels, management accountants can support better decision-making and resource allocation throughout the seasonal cycles.

5. Performance Measurement and Management

5.1 Key Performance Indicators (KPIs) in Management Accounting

Key Performance Indicators (KPIs) are quantifiable measures that help management accountants evaluate the success of an organization or a particular activity in meeting objectives. KPIs provide critical insights into financial and operational performance, enabling informed decision-making and strategic planning.

What Are KPIs?

KPIs are metrics tailored to reflect the goals and priorities of a business. In management accounting, KPIs focus on financial health, cost control, efficiency, and profitability.

Importance of KPIs in Management Accounting

- Performance Tracking: Monitor progress against budgets and forecasts.

- Decision Support: Provide data-driven insights for operational and strategic decisions.

- Accountability: Assign responsibility by linking KPIs to departments or individuals.

- Continuous Improvement: Identify areas for cost reduction and process optimization.

Categories of KPIs in Management Accounting

Examples of Common KPIs with Explanations and Practical Use

-

Profit Margin

- Definition: Percentage of revenue remaining after all expenses.

- Formula: (Net Profit / Revenue) × 100

- Example: A company with $500,000 revenue and $100,000 net profit has a profit margin of 20%.

- Use: Helps assess overall profitability and pricing strategies.

-

Cost Variance

- Definition: Difference between budgeted and actual costs.

- Formula: Budgeted Cost - Actual Cost

- Example: If the budgeted cost for raw materials is $50,000 but actual cost is $55,000, cost variance is -$5,000 (unfavorable).

- Use: Identifies areas where costs are exceeding expectations.

-

Return on Investment (ROI)

- Definition: Measures profitability relative to invested capital.

- Formula: (Net Profit / Investment Cost) × 100

- Example: Investing $200,000 in new equipment yields $50,000 net profit, ROI = 25%.

- Use: Evaluates effectiveness of capital expenditures.

-

Inventory Turnover

- Definition: Number of times inventory is sold and replaced over a period.

- Formula: Cost of Goods Sold / Average Inventory

- Example: COGS = $600,000, Average Inventory = $150,000, Inventory Turnover = 4 times.

- Use: Indicates inventory management efficiency.

-

Budget Variance

- Definition: Difference between budgeted and actual financial outcomes.

- Formula: Budgeted Amount - Actual Amount

- Example: Operating expenses budgeted at $120,000 but actual is $110,000, variance is +$10,000 (favorable).

- Use: Helps control spending and improve forecasting accuracy.

How to Select Relevant KPIs

- Align KPIs with organizational goals.

- Ensure KPIs are measurable and actionable.

- Limit the number of KPIs to focus on critical areas.

- Review and update KPIs regularly to reflect changing priorities.

Practical Example: Using KPIs to Improve Profitability in a Retail Chain

A retail chain tracks the following KPIs monthly:

- Gross Profit Margin: To monitor pricing and cost of goods sold.

- Inventory Turnover: To reduce holding costs and avoid stockouts.

- Sales per Square Foot: To assess store productivity.

- Operating Expense Ratio: To control overhead costs.

By analyzing these KPIs, management identified that some stores had low inventory turnover and high operating expenses. Targeted actions included renegotiating supplier contracts and optimizing staffing schedules, resulting in a 5% increase in overall profit margin within six months.

Summary Mind Map