Payroll Management for Accountants

1. Introduction to Payroll Management

1.1 Understanding Payroll: Definition and Importance

Payroll is the process by which employers pay an employee for the work they have completed. It encompasses calculating wages, withholding taxes and deductions, and distributing payments to employees. For accountants, mastering payroll is crucial because it directly affects financial accuracy, compliance, and employee satisfaction.

What is Payroll?

Payroll includes all activities involved in compensating employees, such as:

- Calculating gross wages based on hours worked or salary

- Deducting taxes, benefits, and other withholdings

- Issuing payments via checks, direct deposits, or other methods

- Maintaining records for legal and tax purposes

Mind Map: Components of Payroll

Why is Payroll Important?

- Legal Compliance: Payroll must comply with tax laws and labor regulations to avoid penalties.

- Financial Accuracy: Payroll affects the company’s financial statements and cash flow.

- Employee Satisfaction: Timely and accurate payment builds trust and morale.

- Data for Decision Making: Payroll data helps in budgeting, forecasting, and strategic planning.

Example: Impact of Payroll Errors

Imagine a company where an accountant miscalculates overtime pay for 50 employees over a month. Each employee is underpaid by $100. This results in $5,000 owed to employees, potential fines for non-compliance, and decreased employee trust. Correcting this requires additional administrative effort and may damage the company’s reputation.

Mind Map: Importance of Payroll

Practical Example: Payroll in Action

Consider an accountant managing payroll for a mid-sized company with 100 employees. Each pay period, they:

- Collect timesheets and verify hours

- Calculate gross pay including overtime and bonuses

- Deduct taxes and benefits accurately

- Process payments via direct deposit

- Generate payroll reports for management

By following best practices and using payroll software, the accountant ensures compliance, accuracy, and employee satisfaction.

In summary, understanding payroll is foundational for accountants. It is not just about paying employees but managing a complex process that impacts legal compliance, financial health, and workforce morale.

1.2 Roles and Responsibilities of Accountants in Payroll

Accountants play a crucial role in payroll management, ensuring that employees are paid accurately and on time while maintaining compliance with legal and financial regulations. Their responsibilities span from data management to reporting and auditing.

Key Roles of Accountants in Payroll

- Payroll Calculation and Processing: Accountants calculate gross pay, deductions, taxes, and net pay.

- Compliance and Regulatory Adherence: Ensuring payroll complies with tax laws, labor regulations, and company policies.

- Record Keeping and Documentation: Maintaining accurate payroll records for audits and future reference.

- Reporting and Analysis: Generating payroll reports for management and tax authorities.

- Internal Controls and Fraud Prevention: Implementing controls to prevent errors and fraud.

- Communication: Coordinating with HR, finance, and employees regarding payroll queries.

Mind Map: Roles of Accountants in Payroll

Detailed Responsibilities with Examples

-

Payroll Calculation and Processing

Accountants ensure that each employee’s pay is calculated correctly based on hours worked, salary, bonuses, commissions, and deductions.

Example:

- An accountant calculates an employee’s monthly salary of $4,000, adds a $500 performance bonus, deducts $300 for taxes and $200 for benefits, resulting in a net pay of $4,000 + $500 - $300 - $200 = $4,000.

-

Compliance and Regulatory Adherence

Accountants stay updated with tax codes and labor laws to ensure payroll compliance.

Example:

- When new tax legislation increases social security contributions, the accountant updates payroll software settings to reflect the new rates, avoiding penalties.

-

Record Keeping and Documentation

Maintaining detailed payroll records is essential for audits and legal compliance.

Example:

- An accountant organizes payroll registers monthly, ensuring all payslips, tax filings, and employee contracts are stored securely and can be retrieved easily.

-

Reporting and Analysis

Accountants prepare reports that summarize payroll expenses and tax liabilities.

Example:

- Generating a quarterly payroll cost report that breaks down expenses by department helps management control budgets.

-

Internal Controls and Fraud Prevention

Implementing checks and balances to prevent payroll fraud.

Example:

- Segregating duties so that the person who approves timesheets is different from the one processing payroll reduces the risk of ghost employees.

-

Communication

Accountants act as a bridge between HR, employees, and management.

Example:

- Addressing an employee’s query about an unexpected deduction by reviewing payroll records and explaining the reason clearly.

Mind Map: Payroll Calculation Responsibilities

Summary

Accountants are the backbone of payroll management, ensuring accuracy, compliance, and transparency. By combining technical skills with effective communication and internal controls, they safeguard the payroll process and contribute to organizational success.

1.3 Overview of Payroll Systems and Processes

Payroll systems and processes form the backbone of efficient payroll management. They ensure employees are paid accurately and on time while maintaining compliance with legal requirements. This section provides a comprehensive overview of the typical payroll systems and the step-by-step processes involved, enriched with mind maps and practical examples.

What is a Payroll System?

A payroll system is a combination of software, procedures, and controls used to calculate, distribute, and record employee compensation. It automates many tasks, reduces errors, and ensures compliance with tax and labor laws.

Key Components of Payroll Systems

Payroll System Components Mind Map

Payroll Processes: Step-by-Step

Payroll Process Mind Map

Example: Manual Payroll Process for a Small Business

- Data Collection: The payroll manager collects timesheets from employees every two weeks.

- Calculation: Using a spreadsheet, the manager calculates gross pay based on hours worked and hourly rates.

- Deductions: Taxes and benefits are manually subtracted.

- Payment: The manager issues checks to employees.

- Reporting: Payroll summaries are prepared for accounting and tax purposes.

Challenges: Time-consuming, prone to errors, difficult to maintain compliance.

Example: Automated Payroll System in a Mid-Sized Company

- Employee Data Input: Employees enter their hours via an online portal integrated with biometric attendance.

- Automated Calculation: Payroll software calculates salaries, taxes, and deductions automatically.

- Direct Deposit: Payments are processed electronically to employees’ bank accounts.

- Reporting: The system generates payslips and files tax reports electronically.

Benefits: Increased accuracy, time savings, improved compliance.

Integrating Payroll with Other Systems

Payroll systems often integrate with HR management, accounting, and time-tracking software to streamline data flow and reduce duplication.

Payroll Integration Mind Map

Summary

Understanding payroll systems and processes is crucial for accountants managing payroll. Whether using manual methods or automated software, the goal remains the same: accurate, timely, and compliant payroll management. Mind maps help visualize the components and workflow, while real-world examples illustrate practical applications.

1.4 Common Payroll Terminologies Explained with Examples

Understanding payroll terminology is crucial for accountants and payroll managers to ensure accurate processing and compliance. Below are some of the most common payroll terms, explained with easy-to-understand examples and mind maps to visualize their relationships.

Gross Pay

Definition: The total earnings of an employee before any deductions are made.

Example: If an employee earns $20 per hour and works 40 hours in a week, their gross pay is:

Gross Pay = $20 × 40 = $800

Net Pay

Definition: The amount an employee takes home after all deductions (taxes, benefits, etc.) are subtracted from the gross pay.

Example: If the employee’s gross pay is $800 and total deductions amount to $200, then:

Net Pay = $800 - $200 = $600

Deductions

Definition: Amounts subtracted from gross pay, including taxes, retirement contributions, insurance premiums, and other withholdings.

Example: Common deductions include:

- Federal Income Tax

- Social Security Tax

- Health Insurance Premiums

Payroll Taxes

Definition: Taxes that employers are required to withhold from employees’ paychecks and/or pay on behalf of employees.

Example:

- Employee Portion: Social Security (6.2%), Medicare (1.45%)

- Employer Portion: Matches employee Social Security and Medicare contributions

Overtime Pay

Definition: Additional pay for hours worked beyond the standard workweek, usually calculated at 1.5 times the regular hourly rate.

Example: If the regular hourly rate is $20, overtime pay is:

Overtime Rate = $20 × 1.5 = $30 per hour

If the employee worked 5 overtime hours:

Overtime Pay = 5 × $30 = $150

Benefits

Definition: Non-wage compensations provided to employees, such as health insurance, retirement plans, and paid time off.

Example: An employer may contribute $200 monthly to an employee’s health insurance plan.

Pay Period

Definition: The recurring length of time over which employee time is recorded and paid.

Example: Common pay periods include weekly, biweekly (every 2 weeks), semimonthly (twice a month), and monthly.

Withholding Allowance

Definition: A claim made by employees on their W-4 form to reduce the amount of tax withheld from their paycheck.

Example: An employee claiming 2 allowances will have less federal income tax withheld compared to someone claiming 0.

Garnishment

Definition: A legal process where a portion of an employee’s earnings is withheld for payment of a debt.

Example: If an employee owes child support, the court may order 25% of their net pay to be garnished.

Direct Deposit

Definition: Electronic transfer of an employee’s net pay directly into their bank account.

Example: Instead of receiving a paper check, the employee’s $600 net pay is deposited automatically every payday.

Mind Maps

Payroll Components Mind Map

Tax Withholding Mind Map

Overtime Calculation Mind Map

Summary Table of Terms and Examples

| Term | Definition | Example |

|---|---|---|

| Gross Pay | Total earnings before deductions | $20/hr × 40 hrs = $800 |

| Net Pay | Earnings after deductions | $800 - $200 = $600 |

| Deductions | Amounts subtracted from gross pay | Taxes, insurance premiums |

| Payroll Taxes | Taxes withheld and employer contributions | Social Security 6.2%, Medicare 1.45% |

| Overtime Pay | Pay for hours worked beyond standard time | $20 × 1.5 × 5 hrs = $150 |

| Benefits | Non-wage compensations | Employer health insurance contribution |

| Pay Period | Timeframe for payroll calculation | Biweekly |

| Withholding Allowance | Employee claim to reduce tax withholding | Claiming 2 allowances on W-4 |

| Garnishment | Court-ordered wage withholding | 25% of net pay for child support |

| Direct Deposit | Electronic payment method | Net pay deposited into bank account |

By mastering these common payroll terms and understanding their practical applications, accountants and payroll managers can ensure smoother payroll operations and better communication with employees and stakeholders.

2. Legal and Regulatory Framework

2.1 Key Payroll Laws and Compliance Requirements

Payroll management is deeply intertwined with a variety of laws and regulations designed to protect employees and ensure fair compensation. For accountants, understanding these laws is crucial to maintaining compliance, avoiding penalties, and fostering trust within the organization.

Overview of Key Payroll Laws

Below is a mind map summarizing the major payroll-related laws and compliance areas every accountant should be familiar with:

Detailed Breakdown with Examples

Wage and Hour Laws

Fair Labor Standards Act (FLSA) governs minimum wage, overtime pay, recordkeeping, and youth employment standards.

-

Example: If an employee works 45 hours in a week, the first 40 hours are paid at the regular rate, and the extra 5 hours must be paid at 1.5 times the regular hourly rate.

-

Best Practice: Use time-tracking software to accurately record hours and automatically calculate overtime to ensure compliance.

Taxation Laws

Accountants must withhold the correct amount of federal and state income taxes, Social Security, Medicare, and unemployment taxes.

-

Example: For an employee earning $1,000 weekly, calculate:

- Federal income tax withholding based on IRS tax tables

- Social Security tax at 6.2% ($62)

- Medicare tax at 1.45% ($14.50)

-

Best Practice: Regularly update payroll tax tables and use payroll software that integrates tax calculations to minimize errors.

Employee Benefits and Deductions

Certain deductions like retirement contributions, health insurance premiums, and court-ordered garnishments must be handled carefully.

-

Example: An employee opts for a 5% 401(k) contribution. For a $2,000 paycheck, $100 is deducted pre-tax.

-

Best Practice: Maintain clear documentation of employee elections and legal orders to ensure accurate deductions.

Reporting and Recordkeeping

Employers must file quarterly and annual payroll reports with agencies such as the IRS and DOL.

-

Example: Filing Form 941 quarterly to report federal tax withholdings.

-

Best Practice: Establish a calendar with deadlines and automate report generation to avoid late filings.

Anti-Discrimination Laws

Payroll must be free from discrimination based on gender, race, or other protected classes.

-

Example: Ensuring equal pay for employees performing the same job regardless of gender.

-

Best Practice: Conduct periodic payroll audits to detect and correct any pay disparities.

Mind Map: Compliance Workflow for Payroll Management

Real-World Example: Avoiding Compliance Pitfalls

Scenario: A mid-sized company failed to withhold overtime pay correctly, paying employees their regular hourly rate for all hours worked.

Consequence: The company faced a Department of Labor investigation and was required to pay back wages plus penalties.

Lesson: Implementing automated overtime calculations and regular payroll audits can prevent costly compliance failures.

Summary

Understanding and adhering to key payroll laws is foundational for accountants managing payroll. Leveraging best practices such as automation, regular training, and thorough documentation helps ensure compliance and protects the organization from legal risks.

2.2 Taxation Rules Affecting Payroll: Income Tax, Social Security, and More

Payroll taxation is a critical aspect of payroll management that accountants must master to ensure compliance and accuracy. This section breaks down the key taxation rules affecting payroll, including income tax, social security contributions, and other mandatory deductions, supported by clear examples and mind maps to facilitate understanding.

Overview of Payroll Taxes

Payroll taxes are taxes imposed on employers and employees, usually calculated as a percentage of the salaries that employers pay their staff. These taxes fund government programs such as social security, healthcare, and unemployment benefits.

Mind Map: Key Payroll Tax Components

Income Tax Withholding

Income tax is deducted from employees’ gross wages based on tax brackets and personal allowances.

Best Practice:

Use up-to-date tax tables and software to calculate withholding accurately.

Example:

An employee earns $4,000 monthly. The income tax rate is progressive:

- 10% on first $1,000

- 15% on next $2,000

- 20% on remaining $1,000

Calculation:

- Tax on first $1,000 = $100

- Tax on next $2,000 = $300

- Tax on last $1,000 = $200

- Total Income Tax Withheld = $600

Social Security Contributions

Social security taxes fund retirement, disability, and survivor benefits.

Mind Map: Social Security Contributions

Best Practice:

Ensure both employee and employer contributions are calculated and reported correctly.

Example:

If the social security tax rate is 6.2% for both employee and employer, and the employee’s monthly salary is $5,000 with a contribution cap of $7,000 per month:

- Employee Contribution = 6.2% × $5,000 = $310

- Employer Contribution = 6.2% × $5,000 = $310

Total social security tax = $620

Medicare Tax and Other Deductions

Medicare tax is another mandatory payroll tax, often calculated at a flat rate.

Example:

Medicare tax rate is 1.45% on all wages.

For the same $5,000 salary:

- Medicare Tax = 1.45% × $5,000 = $72.50

Other deductions such as unemployment insurance or local taxes vary by jurisdiction and must be accounted for accordingly.

Handling Tax Exemptions and Allowances

Employees may have exemptions or allowances that reduce taxable income.

Example:

An employee claims a $500 monthly allowance.

Gross Salary: $4,000

Taxable Income = $4,000 - $500 = $3,500

Income tax is then calculated on $3,500 instead of $4,000.

Multi-Jurisdictional Payroll Tax Considerations

For companies operating in multiple states or countries, payroll taxes can vary significantly.

Best Practice:

Maintain updated knowledge of local tax laws and use payroll software capable of handling multi-jurisdictional tax calculations.

Summary Mind Map: Payroll Taxation Workflow

Final Example: Complete Payroll Tax Calculation

Employee Details:

- Monthly Salary: $4,500

- Allowance: $300

- Social Security Rate: 6.2%

- Medicare Rate: 1.45%

- Income Tax Brackets:

- 10% on first $1,000

- 15% on next $2,000

- 20% on remaining

Step 1: Calculate Taxable Income $4,500 - $300 = $4,200

Step 2: Income Tax Calculation

- 10% on $1,000 = $100

- 15% on $2,000 = $300

- 20% on $1,200 = $240

- Total Income Tax = $640

Step 3: Social Security 6.2% × $4,500 = $279

Step 4: Medicare 1.45% × $4,500 = $65.25

Step 5: Total Deductions $640 + $279 + $65.25 = $984.25

Net Pay: $4,500 - $984.25 = $3,515.75

By understanding and applying these taxation rules with careful calculation and compliance, accountants can ensure accurate payroll management that meets legal requirements and supports organizational financial health.

2.3 Handling Employee Benefits and Statutory Deductions

Managing employee benefits and statutory deductions is a critical part of payroll management for accountants. Proper handling ensures compliance with legal requirements and maintains employee satisfaction. This section breaks down the key components, best practices, and examples to help accountants navigate this complex area.

Understanding Employee Benefits

Employee benefits are non-wage compensations provided to employees in addition to their normal wages or salaries. These can include health insurance, retirement plans, paid time off, and more.

Common Types of Employee Benefits:

Example:

- An employer offers a health insurance plan where the company pays 70% of the premium and the employee pays 30%. The accountant must deduct the employee’s portion from payroll and report the employer’s contribution appropriately.

Statutory Deductions Explained

Statutory deductions are mandatory payroll deductions required by law. These typically include income tax withholding, social security contributions, unemployment insurance, and other government-mandated contributions.

Key Statutory Deductions:

Example:

- For an employee earning $4,000 monthly, the accountant calculates federal income tax withholding based on IRS tax tables, deducts 6.2% for Social Security, and 1.45% for Medicare. The employer matches Social Security and Medicare contributions.

Best Practices for Handling Benefits and Deductions

-

Maintain Up-to-Date Knowledge of Laws: Payroll laws and contribution rates can change frequently. Accountants should subscribe to official updates.

-

Accurate Record-Keeping: Keep detailed records of all deductions and employer contributions for audits and employee queries.

-

Clear Communication with Employees: Provide transparent payslips showing all deductions and benefits.

-

Automate Calculations Where Possible: Use payroll software to reduce errors.

-

Regular Reconciliation: Periodically reconcile payroll deductions with payments made to government agencies and benefit providers.

Example Scenario: Calculating Payroll Deductions Including Benefits

Employee Details:

- Gross Salary: $5,000/month

- Health Insurance Premium: $400 (Employer pays $280, Employee pays $120)

- 401(k) Contribution: 5% of gross salary (Employee elected)

- Federal Income Tax: Calculated as $600

- Social Security: 6.2% of gross salary

- Medicare: 1.45% of gross salary

Step-by-Step Calculation:

| Item | Calculation | Amount ($) |

|---|---|---|

| Gross Salary | 5,000 | |

| Employee Health Insurance | Employee portion | 120 |

| 401(k) Contribution | 5% of 5,000 | 250 |

| Federal Income Tax | Given | 600 |

| Social Security | 6.2% of 5,000 | 310 |

| Medicare | 1.45% of 5,000 | 72.50 |

| Total Deductions | 120 + 250 + 600 + 310 + 72.50 | 1,352.50 |

| Net Pay | 5,000 - 1,352.50 | 3,647.50 |

Employer Contributions:

- Health Insurance: $280

- Social Security: $310 (matches employee)

- Medicare: $72.50 (matches employee)

Mind Map: Payroll Deductions Workflow

Tips for Accountants

- Always verify employee benefit elections before processing payroll.

- Use checklists to ensure all statutory deductions are applied correctly.

- Stay informed about deadlines for remitting deducted amounts to avoid penalties.

- Provide training sessions for HR and payroll staff on benefits and deductions.

By integrating these best practices and examples, accountants can effectively manage employee benefits and statutory deductions, ensuring accuracy, compliance, and employee trust.

2.4 Case Study: Avoiding Penalties Through Compliance Best Practices

In payroll management, compliance with legal and regulatory requirements is critical to avoid costly penalties and maintain organizational reputation. This case study explores how a mid-sized company successfully implemented payroll compliance best practices to steer clear of penalties.

Background

Company: TechSolutions Inc.

Industry: IT Services

Employees: 250

Challenge: Frequent changes in payroll tax laws and benefits regulations led to missed deadlines and errors in payroll tax filings, resulting in fines and employee dissatisfaction.

Compliance Challenges Faced

- Late submission of payroll tax returns

- Incorrect calculation of statutory deductions

- Incomplete documentation for employee benefits

- Lack of regular updates on changing regulations

Best Practices Implemented

Establishing a Compliance Calendar

TechSolutions created a detailed payroll compliance calendar that included all critical deadlines for tax filings, payments, and reporting.

Example: The payroll team set reminders two weeks before each deadline, ensuring ample time for review and corrections.

Regular Training and Updates

The company scheduled quarterly training sessions for payroll staff to stay updated on new laws and regulations.

Example: After a recent update in social security contribution rates, the team quickly adapted payroll calculations, avoiding underpayment penalties.

Automated Payroll Software with Compliance Features

TechSolutions invested in payroll software that automatically updated tax tables and generated compliance reports.

Example: The software flagged a discrepancy in employee tax withholding, allowing correction before submission.

Internal Audits and Review Processes

Monthly internal audits were introduced to verify payroll accuracy and compliance.

Example: An audit uncovered a misclassification of an employee’s exempt status, which was promptly corrected.

Results Achieved

- Zero penalties or fines in the following fiscal year

- Improved accuracy in payroll tax filings

- Enhanced employee trust and satisfaction

- Streamlined payroll process with reduced manual errors

Key Takeaways

- Maintaining a detailed compliance calendar ensures deadlines are met.

- Continuous education keeps payroll teams informed and prepared.

- Leveraging technology reduces human error and enhances compliance.

- Regular internal audits help detect and correct issues proactively.

Summary Mind Map

By integrating these best practices, accountants and payroll managers can significantly reduce the risk of penalties and ensure smooth payroll operations.

3. Payroll Data Collection and Management

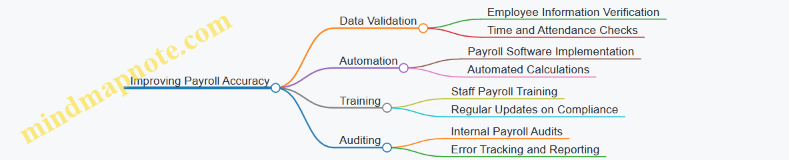

3.1 Gathering Accurate Employee Information

Accurate employee information is the foundation of effective payroll management. Without precise data, payroll calculations can be incorrect, leading to compliance issues, employee dissatisfaction, and financial discrepancies. This section explores best practices for gathering and maintaining accurate employee information, supported by practical examples and mind maps to visualize the process.

Why Accurate Employee Information Matters

- Ensures correct salary and benefits calculation

- Facilitates compliance with tax and labor laws

- Enables timely and accurate tax filings

- Prevents payroll errors and disputes

Key Employee Information to Collect

Best Practices for Gathering Employee Information

-

Use Standardized Forms:

- Provide new hires with a comprehensive onboarding form covering all necessary data.

- Example: A digital form that employees complete before their first payroll cycle.

-

Verify Data Accuracy:

- Cross-check information like SSN against official documents.

- Example: Requesting a copy of a government-issued ID during onboarding.

-

Update Information Regularly:

- Encourage employees to report changes immediately (e.g., address, marital status).

- Example: Annual employee self-service portal updates.

-

Secure Data Storage:

- Store sensitive information in encrypted databases with restricted access.

- Example: Using payroll software with built-in security protocols.

-

Train HR and Payroll Staff:

- Ensure personnel understand the importance of accurate data collection.

- Example: Regular training sessions on data privacy and accuracy.

Example Scenario: Onboarding a New Employee

Step 1: Employee receives an onboarding packet including a digital form to fill out personal, tax, and banking details.

Step 2: HR reviews submitted forms and verifies SSN and tax withholding status.

Step 3: Payroll team inputs data into the payroll system, flags any missing or inconsistent information.

Step 4: Employee confirms data accuracy via a self-service portal before the first paycheck.

Step 5: Payroll processes salary based on verified data, ensuring compliance and accuracy.

Mind Map: Employee Onboarding Data Flow

Tips for Accountants and Payroll Managers

- Establish clear communication channels with HR to ensure data accuracy.

- Implement periodic audits of employee data to catch discrepancies early.

- Use technology to automate data validation where possible.

By following these best practices and leveraging structured data collection methods, accountants and payroll managers can significantly reduce payroll errors and enhance overall payroll efficiency.

3.2 Timekeeping and Attendance Tracking Best Practices

Accurate timekeeping and attendance tracking are foundational to effective payroll management. For accountants and payroll managers, ensuring that employee hours are recorded correctly not only guarantees timely and accurate payments but also helps maintain compliance with labor laws and company policies.

Why Timekeeping and Attendance Matter

- Ensures employees are paid for the exact hours worked.

- Helps track overtime and leaves accurately.

- Supports compliance with wage and hour laws.

- Provides data for performance and productivity analysis.

Best Practices for Timekeeping and Attendance Tracking

Choose the Right Timekeeping System

- Manual Timesheets: Simple but prone to errors and manipulation.

- Punch Cards/Clocks: Traditional but less flexible.

- Digital Time Tracking Software: Automated, reduces errors, integrates with payroll.

Example: A mid-sized company switched from manual timesheets to a biometric time clock system. This reduced buddy punching and improved accuracy by 30%.

Establish Clear Attendance Policies

- Define work hours, break times, and overtime rules.

- Communicate policies clearly to all employees.

- Include rules for tardiness, absenteeism, and leave reporting.

Example: A company implemented a policy requiring employees to notify their manager at least 1 hour before their shift if they are going to be late or absent, reducing unreported absences by 40%.

Regularly Audit Time Records

- Conduct weekly or monthly reviews of time logs.

- Look for inconsistencies or unusual patterns.

- Verify overtime approvals.

Example: An accountant noticed repeated overtime entries without approval and flagged it for management review, preventing potential payroll fraud.

Integrate Attendance Tracking with Payroll Systems

- Automate data transfer to reduce manual entry errors.

- Use software that syncs attendance with payroll calculations.

Example: A company integrated its attendance software with payroll, reducing payroll processing time by 25% and minimizing errors.

Train Employees and Managers

- Provide training on how to use timekeeping systems.

- Educate on the importance of accurate time reporting.

Example: After training sessions, a company saw a 15% reduction in timekeeping errors reported by payroll.

Mind Maps

Mind Map 1: Components of Effective Timekeeping

Mind Map 2: Benefits of Accurate Attendance Tracking

Mind Map 3: Common Challenges and Solutions

Practical Example: Implementing a Digital Timekeeping System

Scenario: A company with 150 employees was struggling with inaccurate manual timesheets leading to payroll discrepancies and employee dissatisfaction.

Steps Taken:

- Selected a cloud-based time tracking software with biometric verification.

- Developed clear attendance policies and communicated them via workshops.

- Integrated the timekeeping system with existing payroll software.

- Trained employees and managers on system usage.

- Established monthly audits of time records.

Outcome:

- Payroll errors reduced by 80%.

- Payroll processing time shortened by 30%.

- Employee satisfaction improved due to transparency.

Summary

Accurate timekeeping and attendance tracking are critical for smooth payroll management. By choosing the right system, setting clear policies, auditing regularly, integrating systems, and training staff, accountants can ensure payroll accuracy and compliance while minimizing errors and fraud.

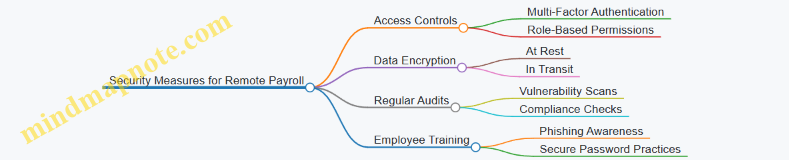

3.3 Managing Payroll Data Confidentiality and Security

Payroll data contains highly sensitive information such as employee salaries, social security numbers, bank details, and tax information. Protecting this data is critical to maintaining employee trust, complying with legal requirements, and preventing financial fraud or identity theft. In this section, we will explore best practices for managing payroll data confidentiality and security, supported by clear examples and mind maps to illustrate key concepts.

Why Payroll Data Security Matters

- Prevents unauthorized access to sensitive employee information.

- Ensures compliance with data protection laws like GDPR, HIPAA, or local regulations.

- Protects the organization from financial penalties and reputational damage.

Best Practices for Payroll Data Confidentiality and Security

Access Control

- Principle of Least Privilege: Only authorized personnel should access payroll data.

- Role-Based Access: Define roles such as Payroll Manager, Accountant, HR, and restrict data access accordingly.

Data Encryption

- Encrypt payroll data both at rest and in transit.

- Use secure protocols (e.g., HTTPS, SFTP) for data transmission.

Secure Storage

- Store payroll data on secure servers with firewalls and intrusion detection.

- Avoid storing sensitive data on local or unsecured devices.

Regular Audits and Monitoring

- Conduct periodic audits to detect unauthorized access or anomalies.

- Use logging to track who accessed or modified payroll data.

Employee Training

- Train payroll and HR staff on data privacy policies and security protocols.

- Promote awareness about phishing and social engineering attacks.

Data Backup and Recovery

- Maintain encrypted backups of payroll data.

- Have a disaster recovery plan to restore data securely in case of loss.

Mind Map: Payroll Data Confidentiality and Security Best Practices

Example 1: Implementing Role-Based Access Control (RBAC)

Scenario: A mid-sized company has a payroll team of five people, but only two should have full access to employee salary details.

Solution:

- Define roles: Payroll Manager (full access), Payroll Assistant (limited access), HR (access to employee personal info but not salary).

- Use payroll software that supports RBAC.

- Regularly review access rights and update when roles change.

Outcome: Sensitive salary data is protected from unnecessary exposure, reducing risk of internal data leaks.

Example 2: Encrypting Payroll Data in Transit

Scenario: Payroll data is sent monthly from the HR department to the accounting team via email.

Risk: Emails can be intercepted, exposing sensitive data.

Solution:

- Use secure file transfer methods such as SFTP or encrypted email services.

- Alternatively, share payroll reports via a secure, password-protected portal.

Outcome: Data remains confidential during transmission, preventing unauthorized interception.

Mind Map: Payroll Data Breach Prevention Workflow

Example 3: Responding to a Payroll Data Breach

Scenario: An employee’s payroll file was accidentally emailed to the wrong recipient.

Steps Taken:

- Immediately notify IT and management.

- Contact the unintended recipient to delete the email and confirm deletion.

- Inform affected employees if personal data was exposed.

- Review and update email policies to prevent recurrence.

- Conduct refresher training on data handling.

Outcome: Quick action minimized damage and reinforced data security culture.

Summary

Managing payroll data confidentiality and security requires a multi-layered approach combining technology, policies, and employee awareness. By implementing access controls, encryption, secure storage, regular audits, and training, accountants can safeguard sensitive payroll information effectively.

Remember, protecting payroll data is not just about compliance—it’s about maintaining trust and integrity within the organization.

3.4 Example: Implementing a Secure Payroll Data Management System

Managing payroll data securely is critical for accountants to protect sensitive employee information and ensure compliance with data protection regulations. This section provides a detailed example of how to implement a secure payroll data management system, incorporating best practices and practical steps.

Step 1: Identify Payroll Data Types and Sensitivity

Understanding what data you handle is the first step. Payroll data typically includes:

- Employee personal information (name, address, SSN, bank details)

- Salary and wage details

- Tax information

- Attendance and leave records

- Benefits and deductions

Step 2: Establish Access Controls

Limit access to payroll data based on roles. For example:

- Payroll Managers: Full access to payroll processing data

- Accountants: Access to payroll reports and tax data

- HR Staff: Access to employee personal and attendance data

- IT Staff: Limited access for system maintenance only

Example:

Use role-based access control (RBAC) in your payroll software to ensure employees only see data necessary for their role.

Step 3: Encrypt Payroll Data

Encrypt sensitive data both at rest and in transit.

- Use database encryption for stored payroll records.

- Ensure SSL/TLS protocols protect data during transmission.

Example:

Encrypt employee bank account numbers and social security numbers in the database to prevent unauthorized access.

Step 4: Implement Secure Data Backup and Recovery

Regular backups protect against data loss.

- Schedule automated encrypted backups.

- Store backups in secure, offsite locations.

- Test recovery procedures periodically.

Example:

Set up nightly encrypted backups of payroll data to a secure cloud storage provider with multi-factor authentication.

Step 5: Maintain Audit Trails and Monitoring

Track all access and changes to payroll data.

- Enable logging of user activities.

- Review logs regularly for suspicious activity.

Example:

Use payroll software features to generate audit reports showing who accessed or modified payroll records and when.

Step 6: Train Employees on Data Security

Educate payroll and HR staff about:

- Importance of data confidentiality

- Recognizing phishing attempts

- Secure password practices

Example:

Conduct quarterly training sessions on payroll data security policies and procedures.

Summary Example Scenario

Company ABC implemented a secure payroll data management system by:

- Classifying payroll data and restricting access using RBAC.

- Encrypting all sensitive data fields in their payroll database.

- Using SSL/TLS for all payroll software communications.

- Scheduling nightly encrypted backups stored in a secure cloud environment.

- Enabling detailed audit logs and reviewing them weekly.

- Providing regular security training to payroll and HR teams.

As a result, Company ABC reduced the risk of data breaches, ensured compliance with GDPR and other regulations, and improved employee trust in payroll processes.

By following these steps and examples, accountants can effectively implement a secure payroll data management system that safeguards sensitive information and supports organizational compliance.

4. Payroll Calculation and Processing

4.1 Step-by-Step Payroll Calculation Methods

Payroll calculation is a critical task for accountants and payroll managers, ensuring employees are paid accurately and on time. This section breaks down the process into clear, manageable steps, supported by mind maps and practical examples.

Step 1: Gather Employee Information

- Employee ID

- Pay rate (hourly or salary)

- Hours worked (regular and overtime)

- Tax withholding details

- Benefits and deductions

Example: John Doe, Employee ID 1234, is paid $20/hour. He worked 40 regular hours and 5 overtime hours this pay period.

Step 2: Calculate Gross Pay

- For hourly employees: (Regular Hours × Hourly Rate) + (Overtime Hours × Overtime Rate)

- For salaried employees: Fixed salary amount per pay period

Overtime Rate: Typically 1.5 times the hourly rate.

Example: John’s gross pay:

- Regular Pay = 40 × $20 = $800

- Overtime Pay = 5 × ($20 × 1.5) = 5 × $30 = $150

- Total Gross Pay = $800 + $150 = $950

Step 3: Calculate Deductions

- Mandatory Deductions:

- Federal and state income tax

- Social Security tax

- Medicare tax

- Voluntary Deductions:

- Health insurance premiums

- Retirement contributions

- Union dues

Example: From John’s $950 gross pay:

- Federal tax withheld: $100

- Social Security (6.2%): $58.90

- Medicare (1.45%): $13.78

- Health insurance: $50

Total deductions = $100 + $58.90 + $13.78 + $50 = $222.68

Step 4: Calculate Net Pay

- Net Pay = Gross Pay - Total Deductions

Example: John’s net pay = $950 - $222.68 = $727.32

Step 5: Verify and Document

- Double-check calculations

- Record payroll in accounting system

- Generate payslips

Example: After calculating John’s net pay, the accountant verifies the figures and inputs the data into the payroll software, then issues a payslip showing gross pay, deductions, and net pay.

Summary Mind Map

By following these steps, accountants can ensure accurate payroll processing, reduce errors, and maintain compliance with tax and labor regulations.

4.2 Handling Overtime, Bonuses, and Commissions with Examples

Payroll management often involves complex calculations beyond base salary, such as overtime pay, bonuses, and commissions. Proper handling of these components ensures employee satisfaction and compliance with labor laws.

Overtime Pay

Definition: Overtime pay is the additional compensation employees receive for hours worked beyond their standard work schedule, typically over 40 hours per week in many jurisdictions.

Best Practices:

- Understand local labor laws regarding overtime eligibility and rates.

- Track employee hours accurately using reliable timekeeping systems.

- Calculate overtime pay at the correct rate (e.g., 1.5x regular hourly wage).

- Communicate overtime policies clearly to employees.

Example:

An employee earns $20/hour and works 45 hours in a week. The overtime rate is 1.5 times the regular rate.

- Regular pay: 40 hours x $20 = $800

- Overtime pay: 5 hours x ($20 x 1.5) = 5 x $30 = $150

- Total weekly pay = $800 + $150 = $950

Mind Map:

Bonuses

Definition: Bonuses are additional compensation awarded to employees, often based on performance, company profits, or special occasions.

Best Practices:

- Define clear criteria for bonus eligibility.

- Decide on bonus types: discretionary, performance-based, or holiday bonuses.

- Document bonus policies and communicate them transparently.

- Ensure bonuses are processed timely and accurately.

Example:

A company offers a quarterly performance bonus of 10% of the employee’s quarterly salary if sales targets are met. An employee with a quarterly salary of $12,000 meets the target.

- Bonus = 10% x $12,000 = $1,200

Mind Map:

Commissions

Definition: Commissions are payments made to employees, usually sales staff, based on the amount or value of sales they generate.

Best Practices:

- Establish clear commission structures (e.g., flat rate, tiered percentages).

- Track sales accurately and in real-time.

- Clarify timing of commission payments (monthly, quarterly).

- Integrate commission calculations with payroll systems.

Example:

A salesperson earns a 5% commission on all sales. In a month, they generate $50,000 in sales.

- Commission = 5% x $50,000 = $2,500

If the company uses a tiered commission:

- First $30,000 at 5% = $1,500

- Remaining $20,000 at 7% = $1,400

- Total commission = $1,500 + $1,400 = $2,900

Mind Map:

Integrated Example: Calculating Payroll with Overtime, Bonus, and Commission

Scenario:

- Base hourly wage: $25

- Hours worked: 50 hours (10 hours overtime)

- Overtime rate: 1.5x

- Quarterly bonus: 8% of quarterly base salary ($12,000)

- Commission: 4% on sales of $40,000

Calculations:

- Regular pay: 40 x $25 = $1,000

- Overtime pay: 10 x ($25 x 1.5) = 10 x $37.5 = $375

- Bonus (monthly portion): 8% x $12,000 / 3 = $320

- Commission: 4% x $40,000 = $1,600

Total pay for the month:

$1,000 + $375 + $320 + $1,600 = $3,295

Summary

Handling overtime, bonuses, and commissions requires clear policies, accurate tracking, and precise calculations. Using examples and mind maps helps accountants and payroll managers visualize and implement best practices effectively.

4.3 Managing Deductions and Reimbursements Accurately

Managing deductions and reimbursements is a critical component of payroll processing that ensures employees are paid correctly while maintaining compliance with legal and organizational policies. Accurate handling of these elements prevents payroll errors, employee dissatisfaction, and potential legal issues.

Key Concepts in Deductions and Reimbursements

- Deductions: Amounts subtracted from an employee’s gross pay, which may be mandatory (taxes, social security) or voluntary (retirement contributions, health insurance premiums).

- Reimbursements: Payments made to employees to cover business-related expenses they incurred, such as travel or office supplies.

Mind Map: Managing Deductions and Reimbursements

Best Practices for Managing Deductions

-

Classify Deductions Correctly:

- Separate mandatory from voluntary deductions.

- Example: Federal income tax withholding is mandatory, while contributions to a company-sponsored charity are voluntary.

-

Stay Updated on Legal Requirements:

- Tax rates and deduction limits can change annually.

- Example: Adjusting Social Security tax deductions when the wage base limit changes.

-

Obtain Employee Authorization:

- Voluntary deductions require written consent.

- Example: Employees must sign enrollment forms for health insurance premiums deducted from payroll.

-

Automate Calculations:

- Use payroll software to reduce manual errors.

- Example: Software automatically calculates retirement plan contributions based on a percentage of gross pay.

-

Reconcile Deductions Regularly:

- Cross-check payroll deductions with payments made to tax authorities or benefit providers.

- Example: Monthly reconciliation of health insurance premiums deducted vs. amounts remitted to the insurance company.

Best Practices for Managing Reimbursements

-

Define Clear Reimbursement Policies:

- Specify eligible expenses, submission deadlines, and required documentation.

- Example: Travel expenses must be submitted within 30 days with original receipts.

-

Require Proper Documentation:

- Receipts, invoices, or approval emails should accompany reimbursement requests.

- Example: An employee submits a taxi receipt for reimbursement.

-

Implement Approval Workflows:

- Supervisors or finance teams should verify and approve reimbursements before processing.

- Example: Manager approval required for any reimbursement over $100.

-

Separate Reimbursements from Payroll Deductions:

- Process reimbursements as separate payments to avoid tax complications.

- Example: Reimbursement for office supplies is paid as a separate transaction, not deducted from salary.

-

Use Payroll Software Features:

- Many payroll systems support reimbursement tracking and reporting.

- Example: Automated alerts for pending reimbursement approvals.

Mind Map: Example Workflow for Deductions and Reimbursements

Practical Example 1: Calculating Deductions

Scenario:

- Employee gross salary: $5,000

- Mandatory deductions:

- Federal Income Tax: $500

- Social Security: 6.2% of $5,000 = $310

- Medicare: 1.45% of $5,000 = $72.50

- Voluntary deductions:

- 401(k) contribution: 5% of $5,000 = $250

- Health insurance premium: $150

Calculation:

- Total deductions = $500 + $310 + $72.50 + $250 + $150 = $1,282.50

- Net pay = $5,000 - $1,282.50 = $3,717.50

Best Practice: Use payroll software to automate these calculations and generate payslips reflecting each deduction clearly.

Practical Example 2: Processing a Reimbursement

Scenario:

- Employee submits a reimbursement request for a business trip taxi fare of $45.

- Submission includes a valid receipt.

- Manager approves the request.

Process:

- Employee submits reimbursement form with receipt.

- Payroll team verifies documentation.

- Manager approves the expense.

- Payroll processes reimbursement as a separate payment in the next payroll cycle.

- Employee receives reimbursement without tax deductions.

Best Practice: Maintain a reimbursement log and track approvals to ensure audit readiness.

Summary

Accurate management of deductions and reimbursements requires clear policies, proper documentation, employee communication, and leveraging payroll technology. Accountants must ensure compliance with legal requirements while maintaining transparency and accuracy to foster trust and avoid costly errors.

4.4 Practical Example: Calculating Payroll for a Multi-State Workforce

Managing payroll for employees working across multiple states can be complex due to varying state tax laws, wage regulations, and benefit requirements. This section provides a detailed, step-by-step example to help accountants navigate these challenges effectively.

Key Considerations for Multi-State Payroll Calculation

- State Income Tax Variations: Each state may have different withholding rates and rules.

- Local Taxes: Some cities/counties impose additional taxes.

- Wage and Hour Laws: Minimum wage and overtime rules can differ.

- Unemployment Insurance (UI) Rates: Vary by state and employer experience.

- Benefits and Deductions: State-mandated benefits may apply differently.

Step 1: Collect Employee Work Location Data

| Employee | State(s) Worked | Hours Worked per State |

|---|---|---|

| Alice | California (CA) | 40 |

| Bob | Texas (TX) | 30 |

| Bob | New York (NY) | 10 |

| Carol | Florida (FL) | 40 |

Step 2: Determine Gross Pay per State

Assuming hourly wages:

- Alice: $25/hr in CA

- Bob: $20/hr

- Carol: $22/hr

| Employee | State | Hours | Hourly Rate | Gross Pay |

|---|---|---|---|---|

| Alice | CA | 40 | $25 | $1,000 |

| Bob | TX | 30 | $20 | $600 |

| Bob | NY | 10 | $20 | $200 |

| Carol | FL | 40 | $22 | $880 |

Step 3: Calculate State Income Tax Withholding

Each state has different withholding rates. For simplicity:

- CA: 6%

- TX: No state income tax

- NY: 5%

- FL: No state income tax

| Employee | State | Gross Pay | State Tax Rate | Tax Withheld |

|---|---|---|---|---|

| Alice | CA | $1,000 | 6% | $60 |

| Bob | TX | $600 | 0% | $0 |

| Bob | NY | $200 | 5% | $10 |

| Carol | FL | $880 | 0% | $0 |

Step 4: Calculate Other Deductions

- Social Security: 6.2% on total gross pay

- Medicare: 1.45% on total gross pay

Calculate total gross pay per employee:

- Alice: $1,000

- Bob: $600 + $200 = $800

- Carol: $880

| Employee | Total Gross Pay | Social Security (6.2%) | Medicare (1.45%) |

|---|---|---|---|

| Alice | $1,000 | $62 | $14.50 |

| Bob | $800 | $49.60 | $11.60 |

| Carol | $880 | $54.56 | $12.76 |

Step 5: Calculate Net Pay

Net Pay = Gross Pay - State Tax - Social Security - Medicare

| Employee | Gross Pay | State Tax | Social Security | Medicare | Net Pay |

|---|---|---|---|---|---|

| Alice | $1,000 | $60 | $62 | $14.50 | $863.50 |

| Bob | $800 | $10 | $49.60 | $11.60 | $728.80 |

| Carol | $880 | $0 | $54.56 | $12.76 | $812.68 |

Mind Map: Multi-State Payroll Calculation Process

Example Scenario Summary

Alice works full-time in California, where state income tax applies. Bob splits his time between Texas (no state income tax) and New York (withholding applies). Carol works in Florida, which has no state income tax. This example demonstrates how to allocate wages and calculate taxes accordingly.

Best Practices Highlighted

- Accurate Time Tracking: Ensure hours are correctly allocated to each state.

- Stay Updated on State Laws: Tax rates and regulations can change annually.

- Use Payroll Software: Automate calculations to reduce errors.

- Maintain Clear Documentation: For audits and compliance verification.

This practical example equips accountants with a clear framework to handle payroll calculations for employees working across multiple states, ensuring compliance and accuracy.

5. Payroll Software and Automation

5.1 Evaluating Payroll Software Options for Accountants

Selecting the right payroll software is critical for accountants to ensure accuracy, compliance, and efficiency in payroll management. This section explores key evaluation criteria, common features, and practical examples to help accountants make informed decisions.

Key Criteria for Evaluating Payroll Software

Detailed Breakdown of Evaluation Criteria

-

Features

- Automation: Does the software automate tax calculations, direct deposits, and payslip generation?

- Tax Compliance: Is it updated regularly to comply with local, state, and federal tax laws?

- Reporting: Are there customizable reports for payroll summaries, tax filings, and audit trails?

- Integration: Can it seamlessly integrate with accounting software like QuickBooks or ERP systems?

- User Interface: Is the software user-friendly for accountants with varying technical skills?

-

Cost

- Consider upfront costs, monthly or annual subscription fees, and any additional charges for extra features or users.

-

Security

- Look for strong encryption, role-based access controls, and reliable backup systems to protect sensitive payroll data.

-

Support

- Evaluate the availability of customer support, training materials, and frequency of software updates.

-

Scalability

- Ensure the software can grow with your organization, supporting more employees, locations, or complex payroll scenarios.

Example: Comparing Two Popular Payroll Software Options

| Feature | PaySoft Pro | EasyPayroll Plus |

|---|---|---|

| Automation | Full automation of payroll runs | Partial automation, manual inputs |

| Tax Compliance | Real-time tax updates | Quarterly manual updates |

| Reporting | Customizable, exportable reports | Standard reports only |

| Integration | Integrates with major accounting tools | Limited integration options |

| User Interface | Intuitive, dashboard view | Basic interface, steeper learning curve |

| Cost | $50/month + $5/employee | $30/month flat rate |

| Security | AES 256-bit encryption, 2FA | Standard encryption, no 2FA |

| Support | 24/7 live chat and phone support | Email support only |

| Scalability | Supports up to 500 employees | Best for small businesses (<100 employees) |

Practical Example: How an Accountant Chooses Payroll Software

Scenario: Jane is an accountant managing payroll for a mid-sized company with 200 employees across three states. She needs software that handles multi-state tax compliance, integrates with their existing accounting system, and offers strong security.

- Jane lists her priorities: tax compliance, integration, scalability, and support.

- She narrows options to PaySoft Pro and EasyPayroll Plus.

- After evaluating features and costs, Jane chooses PaySoft Pro because it offers real-time tax updates, seamless integration, and 24/7 support, which are critical for her company’s complexity.

Summary

Evaluating payroll software involves balancing features, cost, security, support, and scalability. Accountants should map their organization’s specific needs against software capabilities, leveraging demos, trials, and peer reviews. Using mind maps to visualize criteria can streamline the decision-making process and ensure the selected software aligns with both current and future payroll demands.

5.2 Benefits of Automating Payroll Processes

Automating payroll processes offers numerous advantages that streamline operations, reduce errors, and improve overall efficiency for accountants and payroll managers. Below, we explore the key benefits with detailed explanations, mind maps, and practical examples.

Key Benefits of Payroll Automation

Enhanced Accuracy

Manual payroll processing is prone to errors such as miscalculations of hours, incorrect tax deductions, or missed benefits. Automation uses predefined rules and formulas to calculate salaries, taxes, and deductions accurately.

Example: A mid-sized company switched to an automated payroll system that calculates overtime pay based on actual logged hours. Previously, manual calculations led to frequent underpayments. Post-automation, payroll errors dropped by 90%, improving employee trust.

Significant Time Savings

Automated payroll systems drastically reduce the time spent on repetitive tasks like data entry, calculations, and report generation.

Example: An accounting team that used to spend 3 days processing payroll now completes it within a few hours using automation. This freed up time for strategic financial planning.

Improved Compliance

Payroll automation software is regularly updated to reflect changes in tax laws and labor regulations, helping organizations stay compliant and avoid costly penalties.

Example: When a new tax regulation was introduced, an automated payroll system instantly updated the tax tables. The company avoided penalties that competitors faced due to delayed manual updates.

Cost Efficiency

Reducing manual labor and minimizing errors translates into cost savings. Additionally, automation reduces the risk of fines from non-compliance.

Example: A company saved over $15,000 annually by automating payroll, cutting down on overtime hours spent by payroll staff and avoiding late tax filing fees.

Enhanced Data Security

Automated payroll systems often include encryption, role-based access, and audit trails, protecting sensitive employee information.

Example: After implementing an automated payroll solution with multi-factor authentication, a firm reduced data breach risks and complied with GDPR requirements.

Increased Employee Satisfaction

Automation ensures employees are paid accurately and on time, with easy access to digital payslips and tax documents.

Example: Employees at a remote-first company appreciated receiving instant electronic payslips, reducing payroll inquiries and improving transparency.

Summary Mind Map

Automating payroll processes empowers accountants and payroll managers to focus on higher-value activities, reduces risks, and enhances the overall payroll experience for employees and the organization alike.

5.3 Integrating Payroll Software with Accounting Systems

Integrating payroll software with accounting systems is a crucial step for accountants and payroll managers aiming to streamline financial processes, reduce errors, and ensure accurate reporting. This integration allows seamless data flow between payroll and accounting, eliminating manual data entry and improving overall efficiency.

Why Integration Matters

- Accuracy: Automated data transfer reduces human errors in payroll entries.

- Efficiency: Saves time by eliminating duplicate data entry.

- Compliance: Ensures payroll expenses and liabilities are correctly recorded for audits and tax filings.

- Real-time Reporting: Provides up-to-date financial insights.

Key Components of Integration

Common Integration Methods

-

API-Based Integration

- Payroll software and accounting systems communicate via APIs.

- Example: QuickBooks Payroll API syncing with QuickBooks Accounting.

-

File-Based Integration

- Export payroll data as CSV/Excel files and import into accounting software.

- Example: Exporting payroll journal entries from ADP and importing into Sage.

-

Middleware Solutions

- Third-party tools act as a bridge to synchronize data.

- Example: Using Zapier or Workato to connect Gusto Payroll with Xero Accounting.

Step-by-Step Example: Integrating Gusto Payroll with Xero Accounting

-

Setup API Access:

- Obtain API keys from both Gusto and Xero.

-

Map Data Fields:

- Match payroll categories (e.g., wages, taxes) to corresponding accounting ledger accounts.

-

Configure Automation:

- Schedule daily or weekly syncs for payroll transactions.

-

Test Integration:

- Run a test payroll cycle and verify journal entries in Xero.

-

Go Live:

- Enable full automation after successful testing.

Best Practices for Successful Integration

Real-World Example: How a Mid-Sized Company Improved Payroll Accuracy

Scenario: A mid-sized company was manually entering payroll data into their accounting system, leading to frequent errors and delayed financial reports.

Solution: They implemented an API-based integration between their payroll software (Paychex) and accounting system (NetSuite).

Outcome:

- Reduced payroll data entry errors by 90%.

- Cut down payroll processing time by 50%.

- Improved financial reporting accuracy and timeliness.

Troubleshooting Common Integration Issues

| Issue | Cause | Solution |

|---|---|---|

| Data Mismatch | Incorrect field mapping | Review and correct mapping settings |

| Sync Failures | API connection errors | Check API credentials and network |

| Duplicate Entries | Overlapping sync schedules | Adjust sync frequency and settings |

| Security Concerns | Unencrypted data transfer | Enable encryption and secure protocols |

Integrating payroll software with accounting systems is a strategic move that empowers accountants and payroll managers to maintain accurate financial records, ensure compliance, and optimize operational workflows. By following best practices and leveraging modern integration methods, organizations can achieve a seamless and efficient payroll-accounting ecosystem.

5.4 Case Example: Streamlining Payroll with Automation Tools

In today’s fast-paced business environment, payroll automation has become essential for accountants aiming to improve accuracy, save time, and ensure compliance. This case example demonstrates how a mid-sized company successfully streamlined its payroll process by integrating automation tools.

Background

Company: TechSolutions Inc.

Industry: IT Services

Employees: 250

Challenge: Manual payroll processing was time-consuming, error-prone, and compliance updates were difficult to track.

Step 1: Identifying Pain Points

- Manual data entry causing frequent errors

- Delays in payroll processing due to multiple approval layers

- Difficulty in tracking tax law changes and applying them correctly

- Lack of integration between payroll and accounting systems

Step 2: Selecting the Right Automation Tools

TechSolutions chose a cloud-based payroll software with the following features:

- Automated tax calculations and updates

- Direct integration with accounting software (e.g., QuickBooks)

- Employee self-service portal for payslips and leave requests

- Time and attendance tracking integration

Step 3: Implementation Process

- Migrated existing employee data into the new system

- Configured payroll rules including overtime, bonuses, and deductions

- Trained payroll and HR teams on software usage

- Set up automated payroll schedules and notifications

Step 4: Results Achieved

- Time Saved: Payroll processing time reduced from 3 days to 4 hours per cycle

- Error Reduction: Payroll errors dropped by 90%

- Compliance: Automated tax updates ensured 100% compliance with local laws

- Employee Satisfaction: Employees accessed payslips instantly via the portal

Mind Map: Payroll Automation Implementation

Example: Automated Overtime Calculation

Before automation, overtime was manually calculated using timesheets, often leading to miscalculations. With the new system:

- Employees clock in/out via integrated time tracking

- System automatically flags overtime hours beyond 40 hours/week

- Overtime pay is calculated at 1.5x regular rate and added to payroll

Example Calculation:

| Employee | Regular Hours | Overtime Hours | Regular Pay Rate | Overtime Pay Rate | Total Pay |

|---|---|---|---|---|---|

| John Doe | 40 | 5 | $20/hour | $30/hour | (40x20)+(5x30) = $950 |

Example: Integration with Accounting Software

The payroll system automatically exports payroll expenses to the accounting software daily, categorizing expenses by department and project.

Benefits:

- Eliminates manual journal entries

- Real-time financial reporting

- Simplifies audit trails

Best Practices Highlighted

- Choose scalable software to accommodate company growth

- Ensure integration capabilities to reduce duplicate data entry

- Train staff thoroughly to maximize tool benefits

- Leverage employee self-service to reduce administrative queries

This case example illustrates how automation tools can transform payroll management for accountants, enabling them to focus on strategic financial tasks rather than manual processing.

6. Payroll Reporting and Documentation

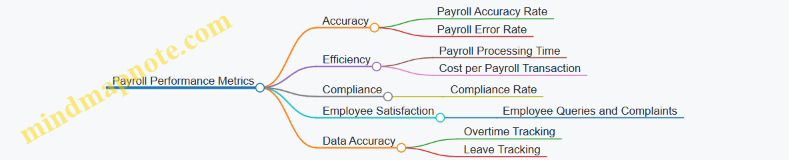

6.1 Essential Payroll Reports Every Accountant Should Generate

Payroll reports are vital tools that help accountants maintain accuracy, ensure compliance, and provide transparency in payroll management. Generating the right reports regularly enables proactive decision-making and simplifies audits. Below is a detailed overview of the essential payroll reports every accountant should generate, complete with mind maps and practical examples.

Payroll Summary Report

Purpose: Provides an overview of total payroll expenses for a specific period, including gross pay, deductions, and net pay.

Key Components:

- Total gross wages

- Total deductions (taxes, benefits, garnishments)

- Net pay

- Number of employees paid

Example: For March 2024, the payroll summary report shows:

- Gross wages: $150,000

- Total deductions: $45,000

- Net pay: $105,000

- Employees paid: 50

Mind Map:

Employee Earnings Report

Purpose: Details individual employee earnings, including regular hours, overtime, bonuses, and commissions.

Key Components:

- Employee name and ID

- Pay period

- Hours worked (regular and overtime)

- Earnings breakdown

Example: John Doe worked 160 regular hours and 10 overtime hours in April 2024, earning $4,000 regular pay and $375 overtime pay.

Mind Map:

Tax Liability Report

Purpose: Summarizes payroll taxes withheld and employer tax obligations.

Key Components:

- Federal income tax withheld

- Social Security and Medicare taxes

- State and local taxes

- Employer tax contributions

Example: For Q1 2024, the company withheld $20,000 in federal taxes and owes $15,000 in employer Social Security contributions.

Mind Map:

Deduction Report

Purpose: Lists all deductions taken from employee paychecks, including voluntary and involuntary deductions.

Key Components:

- Health insurance premiums

- Retirement contributions

- Wage garnishments

- Other voluntary deductions (e.g., union dues)

Example: Jane Smith had $200 deducted for health insurance and $150 for a 401(k) contribution in May 2024.

Mind Map:

Payroll Register

Purpose: A detailed report listing each employee’s pay information for a payroll period.

Key Components:

- Employee details

- Earnings

- Deductions

- Net pay

Example: The payroll register for June 2024 lists all 60 employees with their respective pay details, ensuring transparency and accuracy.

Mind Map:

Overtime Report

Purpose: Tracks overtime hours and pay to monitor labor costs and compliance with labor laws.

Key Components:

- Employee name

- Overtime hours worked

- Overtime pay

Example: Mark Lee logged 15 overtime hours in July 2024, resulting in $450 overtime pay.

Mind Map:

Leave and Absence Report

Purpose: Summarizes employee leave taken, including paid time off, sick leave, and unpaid absences.

Key Components:

- Employee name

- Type of leave

- Leave dates

- Leave balances

Example: Emily Clark took 5 days of paid vacation and 2 days of sick leave in August 2024.

Mind Map:

Best Practices for Generating Payroll Reports

- Automate Report Generation: Use payroll software to schedule and automate reports, reducing errors and saving time.

- Regular Review: Generate reports monthly or per payroll cycle to catch discrepancies early.

- Customize Reports: Tailor reports to meet organizational needs and compliance requirements.

- Secure Access: Ensure only authorized personnel can access sensitive payroll reports.

Conclusion

Generating these essential payroll reports equips accountants with the insights needed to manage payroll efficiently, ensure compliance, and support strategic financial planning. Incorporating clear examples and structured mind maps helps in understanding the components and significance of each report, making payroll management more transparent and effective.

6.2 Maintaining Accurate Payroll Records for Audits

Maintaining accurate payroll records is a critical responsibility for accountants and payroll managers, especially when preparing for audits. Audits can be internal or external and often require detailed documentation to verify compliance with tax laws, labor regulations, and company policies. Proper record-keeping not only ensures smooth audits but also helps prevent costly penalties and legal issues.

Why Accurate Payroll Records Matter

- Compliance: Demonstrates adherence to government regulations.

- Transparency: Provides clear evidence of payroll transactions.

- Dispute Resolution: Helps resolve employee payment disputes quickly.

- Audit Readiness: Facilitates efficient and successful audits.

Key Components of Payroll Records

- Employee personal information (name, address, Social Security number)

- Employment agreements and contracts

- Time and attendance records

- Payroll registers and pay slips

- Tax withholding and deduction records

- Benefits and compensation details

- Records of bonuses, commissions, and overtime

- Payroll tax filings and payment confirmations

Mind Map: Components of Accurate Payroll Records

Best Practices for Maintaining Payroll Records

- Consistency in Record-Keeping: Use standardized formats and templates for all payroll documents.

- Digital Record Management: Utilize secure payroll software to store and back up records electronically.

- Regular Updates: Update records promptly with any changes in employee status, pay rates, or deductions.

- Access Control: Restrict access to payroll data to authorized personnel only to ensure confidentiality.

- Retention Period Compliance: Retain payroll records for the legally required period (usually 3-7 years depending on jurisdiction).

- Cross-Verification: Regularly reconcile payroll records with bank statements and tax filings.

Example: Maintaining Payroll Records for Audit Preparation

Scenario: An accountant at a mid-sized company is preparing for an upcoming tax audit.

- The accountant reviews the payroll register for the past fiscal year, ensuring all employee payments are accurately recorded.

- Timekeeping records are cross-checked with payroll calculations to verify overtime payments.

- Tax withholding records are matched against submitted tax filings to confirm compliance.

- Digital backups of all payroll documents are organized by month and securely stored.

- Any discrepancies found during reconciliation are documented and corrected before the audit.

This thorough preparation helps the company pass the audit without any penalties.

Mind Map: Payroll Audit Preparation Workflow

Tips for Accountants and Payroll Managers

- Schedule periodic internal audits to catch errors early.

- Train payroll staff on compliance and record-keeping standards.

- Use checklists to ensure all necessary documents are maintained.

- Keep communication open with HR and finance teams for accurate data sharing.

By following these best practices and maintaining comprehensive, accurate payroll records, accountants can ensure their organizations are well-prepared for audits and maintain trust with employees and regulatory bodies alike.

6.3 Best Practices for Payroll Documentation and Archiving

Proper payroll documentation and archiving are critical for ensuring compliance, facilitating audits, and maintaining accurate records for both the company and employees. Below, we explore best practices with clear examples and mind maps to help accountants and payroll managers implement effective documentation strategies.

Why Payroll Documentation Matters

- Ensures legal compliance with tax authorities and labor laws.

- Provides evidence during audits or disputes.

- Facilitates accurate payroll processing and reporting.

- Helps in resolving employee queries efficiently.

Best Practices for Payroll Documentation and Archiving

-

Maintain Comprehensive Records

- Include employee personal details, tax forms, pay rates, hours worked, bonuses, deductions, and benefits.

- Example: Keep copies of Form W-4, direct deposit authorizations, and signed contracts.

-

Organize Documentation Systematically

- Use consistent file naming conventions and folder structures.

- Separate records by employee, payroll period, and document type.

- Example: Folder structure like

/Payroll/2024/Q2/EmployeeName/containing payslips, tax forms, and attendance logs.

-

Ensure Data Accuracy and Timeliness

- Update records promptly after payroll runs.

- Cross-verify data entries with source documents.

- Example: After processing payroll, reconcile hours worked with timesheets before finalizing payslips.

-

Implement Secure Storage Solutions

- Use encrypted digital storage or locked physical cabinets.

- Limit access to authorized personnel only.

- Example: Store payroll files on a secure cloud platform with role-based access controls.

-

Retain Records According to Legal Requirements

- Understand local regulations for retention periods (e.g., 3-7 years).

- Regularly review and securely dispose of outdated documents.

- Example: Retain tax forms for 7 years, then shred physical copies and delete digital files securely.

-

Backup Payroll Data Regularly

- Schedule automatic backups to prevent data loss.

- Store backups in separate physical or cloud locations.

- Example: Weekly backup of payroll database to an offsite cloud server.

-

Document Payroll Policies and Procedures

- Maintain an up-to-date payroll manual.

- Include step-by-step processes, roles, and responsibilities.

- Example: A documented procedure for handling payroll corrections and employee inquiries.

Mind Map: Payroll Documentation Best Practices

Example Scenario: Implementing Payroll Documentation in a Mid-Sized Company

Context: A company with 150 employees wants to improve its payroll documentation to prepare for an upcoming audit.

Steps Taken:

- Created a digital folder structure organized by year, quarter, and employee.

- Scanned and uploaded all historical payroll documents into a secure cloud storage with encryption.

- Established a naming convention:

EmployeeName_DocumentType_Date(e.g.,JaneDoe_Payslip_20240430.pdf). - Trained payroll staff to update records immediately after each payroll cycle.

- Set up automatic weekly backups and restricted access to payroll managers and accountants.

- Developed a payroll manual outlining documentation procedures.

Outcome:

- Audit was completed smoothly with all required documents readily available.

- Reduced time spent searching for records by 40%.