Accounting for Business Restructuring

1. Introduction to Business Restructuring Accounting

1.1 Understanding Business Restructuring: Definitions and Types

Business restructuring is a strategic process undertaken by companies to significantly modify their operational, financial, or organizational structure. The goal is often to improve efficiency, address financial difficulties, adapt to market changes, or prepare for growth opportunities.

Definition of Business Restructuring

Business restructuring involves reorganizing the legal, ownership, operational, or other structures of a company. This can include changes in debt arrangements, asset reallocation, workforce adjustments, or shifts in business focus.

Example: A manufacturing company facing declining sales may restructure by closing underperforming plants and shifting production to more cost-effective locations.

Types of Business Restructuring

Business restructuring can be broadly categorized into several types, each with distinct objectives and accounting implications:

Business Restructuring Types Mind Map

Operational Restructuring

Focuses on improving the efficiency of business operations.

- Example: A retail chain reduces its store count and automates inventory management to cut costs.

- Accounting Impact: Recognition of restructuring costs such as severance pay and asset impairments.

Financial Restructuring

Involves modifying the company’s capital structure to improve liquidity or solvency.

- Example: A company refinances its high-interest debt with lower-interest loans and issues new equity to strengthen its balance sheet.

- Accounting Impact: Changes in debt valuation, recognition of refinancing costs, and equity transactions.

Organizational Restructuring

Changes in the company’s ownership or business units.

- Example: A corporation spins off a subsidiary to focus on core business areas.

- Accounting Impact: Derecognition of assets/liabilities, gain or loss on disposal, and consolidation adjustments.

Legal Restructuring

Actions taken to comply with legal requirements or to protect the company during financial distress.

- Example: Filing for bankruptcy protection to reorganize debts.

- Accounting Impact: Recognition of provisions, impairment of assets, and disclosure requirements.

Integrated Example: Mid-Sized Tech Company Restructuring

A mid-sized technology company faced with declining profits undertakes a comprehensive restructuring:

- Operational: Lays off 15% of staff and closes two underperforming offices.

- Financial: Refinances existing debt to reduce interest expenses.

- Organizational: Sells a non-core business unit.

- Legal: Renegotiates supplier contracts to improve terms.

Each of these actions requires careful accounting treatment to ensure accurate financial reporting and compliance.

Summary Mind Map

Understanding these definitions and types lays the foundation for effective accounting practices throughout the restructuring process.

1.2 The Role of Accountants and Restructuring Advisors

In the complex process of business restructuring, accountants and restructuring advisors play pivotal roles that ensure financial accuracy, regulatory compliance, and strategic guidance. Their collaboration is essential to navigate the financial, operational, and legal challenges that arise during restructuring.

Key Responsibilities of Accountants in Restructuring

- Financial Assessment and Analysis: Evaluate the company’s current financial health, identify liabilities, assets, and cash flow constraints.

- Cost Recognition and Allocation: Accurately identify restructuring costs and ensure they are recorded in the appropriate accounting periods.

- Provisioning and Liabilities: Establish and monitor provisions for restructuring-related liabilities such as severance, lease terminations, and asset impairments.

- Compliance and Reporting: Ensure adherence to accounting standards (e.g., IFRS, GAAP) and prepare transparent financial disclosures.

- Internal Controls and Audit Support: Maintain robust controls to prevent errors or fraud and support internal/external audits.

Key Responsibilities of Restructuring Advisors

- Strategic Planning: Develop and recommend restructuring strategies aligned with business objectives.

- Stakeholder Management: Liaise with creditors, investors, employees, and regulators to facilitate smooth restructuring.

- Operational Restructuring: Advise on operational changes such as divestitures, downsizing, or process improvements.

- Financial Modeling and Forecasting: Create models to predict outcomes of restructuring scenarios.

- Risk Management: Identify and mitigate risks associated with restructuring activities.

Mind Map: Roles and Interactions of Accountants and Restructuring Advisors

Example 1: Collaborative Cost Recognition

Scenario: A manufacturing company plans to close one of its plants as part of restructuring.

- The accountant calculates the estimated severance pay, lease termination penalties, and asset write-downs, ensuring these costs are recognized in the correct accounting period.

- The restructuring advisor provides the timeline and strategic rationale for the closure, helping the accountant understand when costs will be incurred.

Outcome: Together, they ensure that the financial statements accurately reflect the restructuring costs, providing stakeholders with a clear picture.

Mind Map: Cost Recognition Workflow

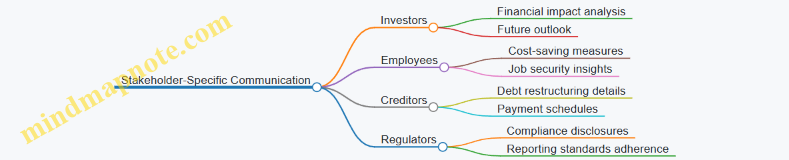

Example 2: Stakeholder Communication Support

Scenario: During a corporate restructuring, management needs to communicate financial impacts to investors.

- The accountant prepares detailed financial reports and disclosures highlighting restructuring expenses and provisions.

- The restructuring advisor crafts the narrative explaining the strategic benefits and expected outcomes.

Outcome: The combined effort results in transparent, credible communication that builds investor confidence.

Mind Map: Stakeholder Communication Roles

Summary

Accountants and restructuring advisors each bring specialized expertise that, when integrated, drive successful business restructuring. Accountants focus on the precise financial mechanics and compliance, while restructuring advisors provide strategic direction and stakeholder engagement. Their partnership ensures restructuring efforts are both financially sound and strategically effective.

1.3 Overview of Accounting Standards Relevant to Restructuring

Business restructuring involves complex accounting considerations governed by various accounting standards. Understanding these standards ensures accurate recognition, measurement, and disclosure of restructuring activities.

Key Accounting Standards for Restructuring

-

IFRS (International Financial Reporting Standards)

- IAS 37: Provisions, Contingent Liabilities and Contingent Assets

- IAS 36: Impairment of Assets

- IFRS 3: Business Combinations (when restructuring occurs post-acquisition)

- IAS 19: Employee Benefits

-

US GAAP (Generally Accepted Accounting Principles)

- ASC 420: Exit or Disposal Cost Obligations

- ASC 360: Property, Plant, and Equipment (Impairment)

- ASC 712: Compensation—Nonretirement Postemployment Benefits

Mind Map: Accounting Standards Landscape for Restructuring

IAS 37: Provisions, Contingent Liabilities and Contingent Assets

-

Purpose: Defines when and how to recognize provisions, including restructuring provisions.

-

Recognition Criteria: A provision is recognized when:

- There is a present obligation (legal or constructive) as a result of a past event.

- It is probable that an outflow of resources will be required to settle the obligation.

- The amount can be reliably estimated.

-

Example: A company decides to close a manufacturing plant. It has a legal obligation to pay severance to employees and dismantle equipment.

- The company recognizes a restructuring provision for estimated severance costs and dismantling expenses.

- The provision is measured at the best estimate of the expenditure required.

ASC 420: Exit or Disposal Cost Obligations (US GAAP)

-

Scope: Addresses costs associated with exit or disposal activities, including restructuring.

-

Recognition: Liabilities are recognized when the entity has committed to an exit plan and can reasonably estimate costs.

-

Example: A corporation announces a plant closure and commits to a detailed plan. It recognizes a liability for employee termination benefits and lease termination costs.

IAS 36: Impairment of Assets

-

Purpose: Ensures assets are carried at no more than their recoverable amount.

-

Relevance to Restructuring: Restructuring often triggers impairment tests for assets related to the restructuring.

-

Example: After announcing a restructuring, a company tests its machinery for impairment. The recoverable amount is lower than carrying value, so an impairment loss is recognized.

IAS 19: Employee Benefits

-

Termination Benefits: Recognized when the entity is demonstrably committed to a termination plan.

-

Measurement: Based on the best estimate of the cost to settle the obligation.

-

Example: A company offers voluntary early retirement packages. The expected cost is recognized as a liability when the offer is accepted.

Practical Example Integrating Standards

Scenario:

A company decides to restructure by closing one of its divisions, resulting in employee layoffs, asset disposals, and contract terminations.

| Accounting Aspect | Relevant Standard | Action Taken |

|---|---|---|

| Recognition of restructuring costs | IAS 37 / ASC 420 | Recognize provisions/liabilities for severance, contract termination, and dismantling costs. |

| Asset impairment | IAS 36 / ASC 360 | Test assets for impairment and recognize losses if recoverable amount is lower. |

| Employee termination benefits | IAS 19 / ASC 712 | Recognize termination benefits when commitment to plan exists. |

Mind Map: Applying Accounting Standards in a Restructuring Scenario

Summary

Understanding and applying the relevant accounting standards is critical for accurate and compliant financial reporting during business restructuring. Both IFRS and US GAAP provide detailed guidance on recognizing provisions, liabilities, impairments, and employee benefits related to restructuring activities. Accountants and restructuring advisors must carefully evaluate the facts and circumstances to determine when and how to apply these standards, ensuring transparent and reliable financial statements.

1.4 Importance of Accurate Accounting in Restructuring Processes

Accurate accounting during business restructuring is critical for ensuring transparency, compliance, and informed decision-making. Restructuring often involves complex financial transactions, cost allocations, and reporting requirements that, if mishandled, can lead to misstatements, regulatory penalties, or misguided strategic decisions.

Why Accurate Accounting Matters

- Regulatory Compliance: Restructuring activities must comply with accounting standards such as IFRS and GAAP. Accurate accounting ensures that provisions, impairments, and costs are recognized properly.

- Stakeholder Confidence: Investors, creditors, and employees rely on accurate financial information to assess the company’s health and future prospects.

- Effective Decision-Making: Management depends on precise accounting data to evaluate restructuring impacts and adjust strategies accordingly.

- Tax Implications: Proper accounting affects tax liabilities and opportunities for deductions related to restructuring costs.

- Audit Readiness: Transparent and well-documented accounting facilitates smoother audits and reduces the risk of financial restatements.

Mind Map: Key Reasons for Accurate Accounting in Restructuring

Example 1: Misstated Severance Costs Impacting Financial Statements

A company undergoing restructuring underestimated severance costs by excluding certain employee benefits. This led to an understatement of restructuring liabilities by $500,000 in the financial statements. As a result, the company faced regulatory scrutiny and had to restate its earnings, damaging investor confidence.

Lesson: Accurate estimation and recording of all restructuring-related costs, including fringe benefits, is essential.

Mind Map: Components of Accurate Restructuring Cost Accounting

Example 2: Transparent Reporting Builds Stakeholder Trust

During a large-scale restructuring, a company provided detailed disclosures about the nature, timing, and expected costs of restructuring activities in its financial statements. This transparency reassured investors and creditors, helping maintain the company’s credit rating and access to capital.

Lesson: Clear and comprehensive disclosure of restructuring accounting enhances stakeholder confidence.

Mind Map: Benefits of Accurate Accounting in Restructuring

Summary

Accurate accounting in restructuring processes is not just a compliance exercise but a strategic enabler. It ensures that all costs and liabilities are properly recognized and reported, supports effective communication with stakeholders, and provides management with reliable data to navigate the complexities of restructuring successfully.

By integrating best practices and maintaining rigorous accounting standards, accountants and restructuring advisors can significantly contribute to the success and sustainability of the restructuring effort.

1.5 Case Study: A Mid-Sized Company’s Restructuring Journey

Background

ABC Manufacturing Ltd., a mid-sized company specializing in automotive parts, faced significant market pressure due to increased competition and rising operational costs. To remain competitive, the company embarked on a comprehensive restructuring plan aimed at streamlining operations, reducing costs, and repositioning its product portfolio.

Restructuring Objectives

- Reduce operational costs by 15% within 12 months

- Divest non-core business units

- Optimize workforce size

- Improve cash flow and liquidity

Mind Map: Key Components of ABC Manufacturing’s Restructuring

Step 1: Identifying Restructuring Costs

ABC Manufacturing identified the following restructuring costs:

- Severance payments for 50 employees

- Lease termination penalties for one facility

- Costs related to asset impairments on machinery

Example:

The company calculated severance pay based on contractual obligations: 3 months’ salary per employee. For 50 employees with an average monthly salary of $4,000, the total severance cost was:

50 employees x $4,000 x 3 months = $600,000

Step 2: Accounting for Provisions

The company recognized a restructuring provision for expected costs that met recognition criteria under IFRS:

- Present obligation from detailed formal plan

- Reliable estimate of costs

Example:

ABC Manufacturing recorded a provision of $600,000 for severance and $150,000 for lease termination penalties.

Journal entry:

| Account | Debit | Credit |

|---|---|---|

| Restructuring Expense | $750,000 | |

| Provision for Restructuring | $750,000 |

Step 3: Asset Write-Downs

Machinery in the divested unit was impaired due to reduced market value.

Example:

Book value: $1,200,000

Recoverable amount: $800,000

Impairment loss: $400,000

Journal entry:

| Account | Debit | Credit |

|---|---|---|

| Impairment Loss | $400,000 | |

| Accumulated Depreciation | $400,000 |

Step 4: Financial Reporting and Disclosure

ABC Manufacturing disclosed the restructuring costs and provisions in the notes to the financial statements, explaining:

- Nature and reason for restructuring

- Amounts recognized in the period

- Expected timing of cash outflows

Example Disclosure Extract:

“During the fiscal year, the company initiated a restructuring plan to improve operational efficiency. Restructuring expenses of $750,000 were recognized, primarily relating to employee termination benefits and lease penalties. The company expects to settle these obligations within the next 12 months.”

Mind Map: Accounting Flow for ABC Manufacturing’s Restructuring

Lessons Learned

- Early identification and measurement of costs ensure accurate financial reporting.

- Clear documentation supports provision recognition and audit processes.

- Transparent disclosures build stakeholder trust during restructuring.

This case study illustrates how accountants and restructuring advisors can apply best practices in real-world scenarios, ensuring compliance and clarity throughout the restructuring journey.

2. Planning and Preparing for Restructuring Accounting

2.1 Identifying Financial and Operational Triggers for Restructuring

Business restructuring is often initiated in response to specific financial and operational triggers that indicate the need for change. Recognizing these triggers early allows accountants and restructuring advisors to plan and implement effective restructuring strategies that align with the company’s goals.

Financial Triggers

Financial triggers are indicators related to a company’s financial health that suggest restructuring may be necessary. These include:

- Declining Profit Margins: Continuous reduction in profit margins signals inefficiencies or increased costs.

- Cash Flow Problems: Persistent negative cash flow or liquidity issues that threaten operational viability.

- High Debt Levels: Excessive leverage causing financial strain or inability to meet debt obligations.

- Poor Return on Assets (ROA): Assets not generating expected returns, indicating underutilization.

- Negative Earnings Before Interest and Taxes (EBIT): Consistent losses at the operating level.

Example:

A manufacturing company experiences a 15% year-over-year decline in profit margins over three consecutive quarters, coupled with increasing accounts payable and delayed supplier payments. These financial signs trigger a review for potential restructuring.

Operational Triggers

Operational triggers relate to inefficiencies or changes in the business environment impacting operations:

- Outdated Technology or Processes: Legacy systems causing delays and higher costs.

- Overcapacity or Underutilization: Facilities or workforce not aligned with current demand.

- Market Changes: Shifts in customer preferences or competitive landscape.

- Regulatory Changes: New laws requiring operational adjustments.

- Management or Organizational Issues: Ineffective leadership or structural misalignment.

Example:

A retail chain notices declining foot traffic due to the rise of e-commerce, leading to underutilized stores and excess inventory. This operational trigger prompts consideration of store closures and supply chain restructuring.

Mind Map: Financial Triggers for Restructuring

Mind Map: Operational Triggers for Restructuring

Integrated Mind Map: Identifying Restructuring Triggers

Best Practice: Early Detection and Continuous Monitoring

- Establish key financial and operational KPIs relevant to your industry.

- Use dashboards to monitor these KPIs in real-time.

- Conduct periodic reviews with cross-functional teams to interpret data.

- Document triggers and potential impacts to inform restructuring decisions.

Example:

An accounting team sets up a dashboard tracking cash conversion cycle, debt-to-equity ratio, and inventory turnover. When the cash conversion cycle extends beyond 90 days, it triggers a deeper operational review, leading to a restructuring plan focused on improving working capital.

Summary

Identifying financial and operational triggers is a foundational step in the restructuring process. By understanding and monitoring these indicators, accountants and restructuring advisors can proactively recommend restructuring actions that mitigate risks and position the company for sustainable success.

2.2 Establishing a Restructuring Accounting Framework

Establishing a robust restructuring accounting framework is essential to ensure that all financial aspects of a restructuring initiative are accurately captured, reported, and managed. This framework acts as the backbone for consistent accounting treatment, compliance with relevant standards, and transparent communication with stakeholders.

Key Components of a Restructuring Accounting Framework

Below is a mind map illustrating the core components:

Step-by-Step Approach to Establish the Framework

-

Define Objectives and Scope

- Clarify the goals of the restructuring accounting framework.

- Determine which restructuring activities and costs will be covered.

-

Assign Roles and Responsibilities

- Identify key personnel: accountants, restructuring advisors, finance managers.

- Establish decision-making and approval hierarchies.

-

Develop Accounting Policies

- Align with IFRS (e.g., IAS 37) or US GAAP standards.

- Specify recognition criteria for restructuring costs and provisions.

-

Design Cost Identification and Tracking Processes

- Create cost categories.

- Set up cost centers or project codes in accounting systems.

-

Establish Provision Recognition and Measurement Procedures

- Define how and when provisions are recognized.

- Develop estimation methods for uncertain costs.

-

Implement Reporting and Disclosure Protocols

- Determine internal and external reporting requirements.

- Prepare templates for financial statement notes.

-

Integrate Systems and Controls

- Configure ERP or accounting software to capture restructuring transactions.

- Set up controls to ensure data accuracy and completeness.

-

Train Staff and Communicate Framework

- Conduct training sessions.

- Provide documentation and support materials.

Example: Framework Implementation in a Manufacturing Company

Scenario: A manufacturing company plans to close one of its plants and relocate operations. The finance team needs a restructuring accounting framework to manage related costs.

- Governance: CFO appoints a restructuring accounting lead and forms a cross-functional team.

- Policies: The team adopts IFRS guidelines and defines severance pay and asset impairment recognition.

- Cost Tracking: New cost centers for plant closure, employee termination, and equipment write-down are created.

- Provisioning: Provisions for lease termination and environmental cleanup are estimated based on contracts and expert assessments.

- Reporting: Monthly internal reports and quarterly disclosures are established.

- Systems: ERP configured to tag restructuring costs.

- Training: Workshops conducted for accounting and HR teams.

Mind Map: Cost Identification & Classification

Practical Example: Recognizing Severance Costs

- Situation: Company decides to lay off 50 employees.

- Action: Calculate severance pay based on contractual obligations.

- Accounting Treatment: Recognize severance costs as a liability and expense in the period when the restructuring plan is communicated and employees are notified.

- Documentation: Maintain termination letters, severance agreements, and board approvals.

Summary

Establishing a restructuring accounting framework ensures clarity, consistency, and compliance throughout the restructuring process. By integrating governance, policies, cost tracking, provisioning, reporting, and systems, organizations can effectively manage the financial complexities of restructuring initiatives.

2.3 Best Practice: Creating a Restructuring Accounting Checklist

Creating a comprehensive restructuring accounting checklist is a critical best practice that ensures all financial aspects of a restructuring initiative are systematically identified, tracked, and managed. This checklist acts as a roadmap for accountants and restructuring advisors to maintain accuracy, compliance, and transparency throughout the process.

Why Use a Restructuring Accounting Checklist?

- Consistency: Ensures uniform treatment of restructuring items across periods and teams.

- Compliance: Helps adhere to accounting standards such as IFRS and GAAP.

- Efficiency: Streamlines data collection and reporting.

- Risk Mitigation: Reduces the chance of missing key accounting entries or disclosures.

Key Components of a Restructuring Accounting Checklist

Restructuring Accounting Checklist Mind Map

Example: Sample Restructuring Accounting Checklist for a Manufacturing Company

| Checklist Item | Description | Responsible Party | Status |

|---|---|---|---|

| Identify restructuring triggers | Review financials and operational inefficiencies | CFO / Restructuring Team | Completed |

| Define restructuring scope | Determine departments and assets affected | Project Manager | In Progress |

| Estimate employee termination costs | Calculate severance and benefits | HR / Accounting | Pending |

| Assess asset impairments | Review fixed assets for impairment indicators | Accounting / Valuation Team | Pending |

| Document provision assumptions | Prepare detailed notes on assumptions used | Accounting | Pending |

| Record journal entries | Post restructuring costs and provisions | Accounting | Pending |

| Prepare financial statement notes | Draft disclosures related to restructuring | Accounting / Legal | Pending |

| Coordinate tax treatment | Confirm tax deductibility and deferred tax impacts | Tax Department | Pending |

| Monitor actual vs. budgeted costs | Track and report variances | Restructuring Team | Ongoing |

Practical Example: Using the Checklist to Record Employee Termination Benefits

- Identify: HR provides a list of employees affected and severance packages.

- Estimate: Accounting calculates total termination benefits based on contracts.

- Provision Recognition: Confirm that the termination plan meets criteria for provision recognition under IFRS.

- Documentation: Attach HR communications and legal approvals as evidence.

- Journal Entry: Debit restructuring expense and credit provision liability.

- Disclosure: Include details in financial statement notes.

- Monitoring: Track actual payments and adjust provisions accordingly.

By systematically following a restructuring accounting checklist, accountants and restructuring advisors can ensure that all financial elements are accurately captured and reported, reducing risk and enhancing stakeholder confidence.

2.4 Coordinating Between Finance, Legal, and Operational Teams

Effective coordination between finance, legal, and operational teams is critical during business restructuring to ensure seamless accounting practices, compliance, and operational continuity. Each team brings unique expertise and perspectives that, when aligned, contribute to a successful restructuring process.

Why Coordination Matters

- Finance Team: Responsible for accurate accounting, budgeting, forecasting, and financial reporting related to restructuring costs.

- Legal Team: Ensures compliance with laws and regulations, manages contracts, employee agreements, and potential litigation risks.

- Operational Team: Implements restructuring plans on the ground, manages workforce changes, and oversees operational adjustments.

Lack of coordination can lead to misstatements in financial reports, legal penalties, or operational disruptions.

Mind Map: Coordination Workflow

Best Practices for Coordination

-

Establish Cross-Functional Steering Committee

- Include representatives from finance, legal, and operations.

- Hold weekly meetings to review progress, risks, and issues.

-

Define Clear Roles and Responsibilities

- Use RACI (Responsible, Accountable, Consulted, Informed) matrices.

- Example: Finance is responsible for cost tracking; legal is accountable for compliance.

-

Implement Shared Documentation Platforms

- Use cloud-based tools (e.g., SharePoint, Google Drive) for real-time updates.

- Maintain version control on restructuring plans and financial data.

-

Develop Integrated Timelines and Milestones

- Align financial reporting deadlines with legal compliance dates and operational milestones.

-

Use Scenario Planning and Joint Risk Assessments

- Collaborate on identifying potential financial, legal, and operational risks.

- Develop mitigation strategies collectively.

Mind Map: Best Practices for Coordination

Example: Coordinating Severance Payment Accounting

Scenario: A company plans to lay off 100 employees as part of restructuring. Coordination is needed to ensure proper accounting and legal compliance.

- Finance: Calculates severance costs, accrues expenses in the correct period, and forecasts cash flow impact.

- Legal: Reviews severance agreements to ensure compliance with labor laws and minimizes litigation risk.

- Operations: Communicates layoffs to employees, manages exit processes, and ensures operational continuity.

Coordination Steps:

- Legal provides templates for severance agreements to finance and operations.

- Finance shares cost estimates and accrual schedules with legal and operations.

- Operations provides timelines for employee exits to finance for accurate period reporting.

- Weekly meetings track progress, resolve discrepancies, and update all teams.

Mind Map: Severance Payment Coordination Example

Additional Tips

- Use Clear Communication Language: Avoid jargon when possible to ensure all teams understand key points.

- Document Decisions: Keep records of all decisions and agreements to support audit trails.

- Leverage Technology: Utilize project management tools (e.g., Asana, Trello) to track tasks and deadlines.

By fostering strong collaboration between finance, legal, and operational teams, organizations can navigate the complexities of restructuring accounting more effectively, reduce risks, and improve transparency throughout the process.

2.5 Example: Setting Up a Restructuring Accounting Team in a Corporate Environment

Setting up a restructuring accounting team is a critical step in ensuring that the financial aspects of business restructuring are managed efficiently and accurately. This example will walk through the key components, roles, responsibilities, and best practices involved in establishing such a team within a corporate environment.

Key Objectives of the Restructuring Accounting Team

- Accurately capture and report restructuring costs

- Ensure compliance with accounting standards (IFRS, GAAP)

- Coordinate with cross-functional teams (legal, HR, operations)

- Provide timely financial insights to management and stakeholders

Step 1: Define Team Structure and Roles

Example:

- Team Lead / Manager: Oversees the entire restructuring accounting process, liaises with senior management.

- Senior Accountant: Handles complex accounting treatments, ensures compliance.

- Cost Analysts: Track and analyze restructuring expenses.

- Provision Specialists: Manage recognition and adjustments of provisions.

- Tax Accountant: Coordinates tax implications and filings.

- Data Analyst: Supports data collection and reporting.

- IT/ERP Specialist: Ensures systems support restructuring accounting needs.

- Compliance Officer: Monitors adherence to regulations and internal policies.

Step 2: Establish Communication Channels

Example:

- Weekly meetings to review restructuring cost updates and challenges.

- Collaborative workshops with HR to align on employee termination benefits accounting.

- Use of cloud-based platforms (e.g., SharePoint, Google Drive) for document sharing.

Step 3: Develop Accounting Policies and Procedures

Example:

- Policy states severance payments are recognized when a formal plan is approved and communicated.

- Provisions for facility closure costs require documented management commitment and reliable estimates.

Step 4: Implement Systems and Tools

Example:

- Configure the ERP system to create a dedicated restructuring cost center to segregate expenses.

- Develop dashboards that track actual vs budgeted restructuring costs in real-time.

Step 5: Training and Continuous Improvement

- Conduct training sessions on restructuring accounting standards and internal policies.

- Encourage feedback loops to identify process bottlenecks.

- Regularly update the team on regulatory changes and best practices.

Real-World Scenario Example

Company: XYZ Corp, a multinational manufacturing firm undergoing a major restructuring to streamline operations.

Action:

- XYZ Corp formed a restructuring accounting team led by a senior finance manager.

- The team included accountants specializing in cost tracking, provisions, and tax.

- They established weekly coordination meetings with HR and legal to align on employee-related costs.

- The ERP system was updated to track restructuring expenses separately.

- Policies were documented to ensure consistent recognition of restructuring costs.

- Monthly reports were generated for the executive committee to monitor financial impact.

Outcome:

- Improved accuracy in capturing restructuring costs.

- Enhanced transparency and timely reporting.

- Better compliance with accounting standards and tax regulations.

Summary

Setting up a restructuring accounting team requires careful planning of team roles, communication strategies, accounting policies, and system integrations. By following these best practices and learning from real-world examples, companies can ensure their restructuring efforts are financially well-managed and compliant.

3. Recognizing and Measuring Restructuring Costs

3.1 Types of Restructuring Costs: Direct vs Indirect

When a business undergoes restructuring, understanding the nature of costs involved is crucial for accurate accounting and financial reporting. Restructuring costs can broadly be classified into Direct Costs and Indirect Costs. This distinction helps accountants and restructuring advisors allocate expenses properly, ensuring compliance with accounting standards and providing clear insights into the financial impact of restructuring.

Mind Map: Overview of Restructuring Costs

Direct Costs

Direct costs are expenses that are explicitly and clearly attributable to the restructuring event. These costs are typically identifiable, measurable, and directly linked to the restructuring activities.

Common Examples of Direct Costs:

-

Employee Termination Benefits: Severance pay, pension contributions, and other benefits paid to employees who are laid off as part of the restructuring.

-

Contract Termination Costs: Penalties or fees paid to terminate leases, supplier contracts, or service agreements early.

-

Asset Write-Downs and Impairments: Reducing the book value of assets that are no longer useful or have lost value due to restructuring (e.g., closing a manufacturing plant).

-

Relocation Expenses: Costs incurred when moving operations, such as transportation of equipment or employee relocation allowances.

Example 1: Severance Pay Calculation

A company decides to lay off 20 employees as part of its restructuring. Each employee is entitled to 3 months of severance pay, with an average monthly salary of $4,000.

- Severance Pay = 20 employees × 3 months × $4,000 = $240,000

This $240,000 is a direct restructuring cost and should be recognized in the period when the restructuring plan is approved and communicated.

Indirect Costs

Indirect costs are less tangible and not directly attributable to restructuring but arise as a consequence of the process. These costs are often harder to quantify and may include opportunity costs or inefficiencies.

Common Examples of Indirect Costs:

-

Lost Productivity: Disruptions caused by restructuring may reduce workforce efficiency temporarily.

-

Management Time: Time spent by senior management on planning and executing restructuring instead of regular business activities.

-

Training and Recruitment: Costs related to hiring new employees or retraining remaining staff to adapt to new roles.

-

Temporary Operational Inefficiencies: Increased operational costs due to process changes or system upgrades.

Example 2: Management Time Cost Estimation

Senior management spends approximately 200 hours over 3 months on restructuring activities. If the average fully loaded hourly cost of management time is $150:

- Management Time Cost = 200 hours × $150 = $30,000

While important for internal decision-making, this cost is typically not recognized as a restructuring provision under accounting standards but should be monitored for internal reporting.

Mind Map: Direct vs Indirect Costs Comparison

Best Practice Tips for Accountants and Restructuring Advisors

-

Separate Direct and Indirect Costs: Maintain clear documentation distinguishing direct costs eligible for provision recognition from indirect costs.

-

Use Clear Criteria for Recognition: Follow accounting standards (e.g., IFRS IAS 37 or US GAAP ASC 420) to determine which costs qualify as restructuring provisions.

-

Document Assumptions and Estimates: For costs like severance pay or contract termination, keep detailed calculations and approvals.

-

Monitor Indirect Costs Internally: Even if not recognized in financial statements, track indirect costs to assess restructuring impact on operations.

-

Communicate with Stakeholders: Provide transparent explanations about the nature of restructuring costs and their treatment.

By understanding and categorizing restructuring costs into direct and indirect, accountants and restructuring advisors can ensure accurate financial reporting and provide valuable insights during the restructuring process.

3.2 Accounting for Employee Termination Benefits

Employee termination benefits are a critical component of restructuring costs and require careful accounting to ensure compliance with relevant standards and accurate financial reporting. This section explores the principles, best practices, and practical examples to help accountants and restructuring advisors manage these benefits effectively.

What Are Employee Termination Benefits?

Employee termination benefits refer to payments and other benefits provided to employees as a result of termination of employment before the normal retirement date. These may include:

- Severance pay

- Notice period payments

- Outplacement services

- Pension enhancements

- Other post-employment benefits

Accounting Standards Overview

- IFRS (IAS 19): Requires recognition of termination benefits when the entity is demonstrably committed to either terminating the employment of employees before the normal retirement date or providing termination benefits as a result of an offer made to encourage voluntary redundancy.

- US GAAP (ASC 712): Similar guidance requiring recognition when the termination benefits are probable and can be reasonably estimated.

Mind Map: Key Steps in Accounting for Employee Termination Benefits

Best Practices

- Establish a Formal Termination Plan: Document the plan clearly, including the number of affected employees, timing, and benefit amounts.

- Communicate Early and Clearly: Ensure employees are informed promptly to meet recognition criteria.

- Estimate Costs Accurately: Include all components such as severance, accrued benefits, and related taxes.

- Recognize Expense and Liability in the Correct Period: Align with accounting standards to avoid misstating financials.

- Maintain Detailed Documentation: For audit trails and future reference.

Example 1: Calculating Severance Pay

Scenario: A company plans to lay off 10 employees. Each employee is entitled to 3 months’ salary as severance. The average monthly salary is $5,000.

Calculation:

- Severance per employee = 3 months × $5,000 = $15,000

- Total severance liability = 10 employees × $15,000 = $150,000

Accounting Treatment:

- Recognize a restructuring expense of $150,000 in the period when the plan is communicated.

- Record a liability for $150,000 until payments are made.

Journal Entry:

| Account | Debit | Credit |

|---|---|---|

| Restructuring Expense | $150,000 | |

| Accrued Termination Liability | $150,000 |

Mind Map: Journal Entries for Termination Benefits

Example 2: Salary Continuation Benefits

Scenario: Instead of lump-sum severance, a company agrees to continue paying salaries for 2 months post-termination for 5 employees, each earning $4,000 monthly.

Calculation:

- Total salary continuation = 5 employees × 2 months × $4,000 = $40,000

Accounting Treatment:

- Recognize the $40,000 as a liability and expense when the termination plan is communicated.

- Expense is recognized over the 2-month period as payments are made.

Journal Entries:

- At recognition:

| Account | Debit | Credit |

|---|---|---|

| Restructuring Expense | $40,000 | |

| Accrued Termination Liability | $40,000 |

- Monthly payment (each month):

| Account | Debit | Credit |

|---|---|---|

| Accrued Termination Liability | $20,000 | |

| Cash/Bank | $20,000 |

Common Challenges

- Estimating Costs for Voluntary Redundancies: Uncertainty in employee acceptance rates.

- Timing of Recognition: Ensuring the plan is sufficiently detailed and communicated.

- Tax Implications: Differing tax treatments can affect net costs.

Summary

Accounting for employee termination benefits requires a clear understanding of the termination plan, accurate cost estimation, and timely recognition in financial statements. By following best practices and leveraging detailed examples, accountants and restructuring advisors can ensure compliance and provide transparent reporting during business restructuring.

3.3 Best Practice: Allocating Costs to the Correct Accounting Periods

Accurately allocating restructuring costs to the correct accounting periods is critical to ensure financial statements fairly represent the company’s financial position and performance. Misallocation can lead to misstated earnings, regulatory issues, and misinformed decision-making.

Key Principles for Cost Allocation

- Matching Principle: Expenses should be recognized in the same period as the related revenues or events that triggered them.

- Accrual Basis Accounting: Costs must be recorded when incurred, not necessarily when paid.

- Materiality: Focus on significant restructuring costs that impact financial statements materially.

Mind Map: Steps to Allocate Restructuring Costs Correctly

Example 1: Employee Severance Costs

A company announces on December 15 that it will lay off 50 employees effective January 31. Severance payments will be made in February.

- When to recognize the cost?

- According to IAS 37, a constructive obligation arises when the company has a detailed formal plan and has communicated it to affected employees.

- Since the announcement was made in December and employees were informed, the obligation exists in December.

- Severance costs should be accrued in December, even though payments occur in February.

Accounting Entry in December:

| Account | Debit | Credit |

|---|---|---|

| Restructuring Expense | $500,000 | |

| Provision for Severance | $500,000 |

Payment in February:

| Account | Debit | Credit |

|---|---|---|

| Provision for Severance | $500,000 | |

| Cash | $500,000 |

Mind Map: Timing Considerations for Severance Costs

Example 2: Asset Write-Downs

A company decides in Q4 to close a manufacturing plant. The plant’s book value is $2 million, but the recoverable amount is estimated at $1.2 million.

- When to recognize the impairment?

- The impairment loss should be recognized in the period when the decision is made and supported by evidence.

- If the decision and supporting data are available in Q4, the write-down is recorded in Q4.

Accounting Entry in Q4:

| Account | Debit | Credit |

|---|---|---|

| Impairment Loss | $800,000 | |

| Accumulated Depreciation | $800,000 |

Mind Map: Allocating Asset Write-Downs

Practical Tips for Accountants and Restructuring Advisors

- Maintain Detailed Documentation: Keep records of management decisions, communications, and approvals to support timing of cost recognition.

- Regularly Review Provisions: Update estimates and adjust provisions as new information becomes available.

- Coordinate with Legal and HR: Ensure alignment on timing of obligations, especially for employee-related costs.

- Use Clear Accounting Policies: Define and communicate policies on restructuring cost recognition to ensure consistency.

By following these best practices and applying the matching and accrual principles, accountants and restructuring advisors can ensure restructuring costs are allocated accurately, providing stakeholders with transparent and reliable financial information.

3.4 Practical Example: Calculating Severance Pay and Related Expenses

When a company undergoes restructuring, one of the most significant costs is severance pay to employees who are laid off. Accurately calculating severance pay and related expenses is crucial for proper accounting and financial reporting.

Step 1: Identify Eligible Employees

- Determine which employees are affected by the restructuring.

- Review employment contracts and company policies to understand severance entitlements.

Step 2: Understand Severance Pay Components

- Basic Severance Pay: Usually based on tenure and salary.

- Accrued Benefits: Unused vacation, bonuses, or other owed compensation.

- Additional Benefits: Outplacement services, extended health benefits, etc.

Step 3: Calculate Severance Pay

-

Formula example:

Severance Pay = (Monthly Salary) x (Number of Months of Severance Based on Tenure) -

Example:

Employee Monthly Salary Years of Service Severance Months Severance Pay John Doe $5,000 4 4 $20,000

Step 4: Calculate Related Expenses

- Accrued Vacation Pay: Calculate unused vacation days multiplied by daily pay rate.

- Bonus Pay: If applicable, pro-rated bonuses.

- Other Benefits: Estimate costs for extended health coverage or outplacement.

Step 5: Aggregate Total Severance Costs

- Sum severance pay and all related expenses for each employee.

Mind Map: Severance Pay Calculation Process

Example Scenario

Company ABC is restructuring and needs to calculate severance pay for three employees:

| Employee | Monthly Salary | Years of Service | Unused Vacation Days | Bonus Eligibility | Additional Benefits Cost |

|---|---|---|---|---|---|

| Alice Smith | $6,000 | 5 | 10 | Yes | $1,000 |

| Bob Jones | $4,500 | 3 | 5 | No | $500 |

| Carol Lee | $7,000 | 7 | 15 | Yes | $1,200 |

Company Policy: 1 month severance per year of service.

Calculations:

-

Alice Smith:

- Severance Pay = $6,000 x 5 = $30,000

- Vacation Pay = (Monthly Salary / 22 working days) x 10 days = ($6,000 / 22) x 10 ≈ $2,727

- Bonus (assume $3,000 pro-rated) = $3,000

- Additional Benefits = $1,000

- Total Severance Cost = $30,000 + $2,727 + $3,000 + $1,000 = $36,727

-

Bob Jones:

- Severance Pay = $4,500 x 3 = $13,500

- Vacation Pay = ($4,500 / 22) x 5 ≈ $1,023

- Bonus = $0

- Additional Benefits = $500

- Total Severance Cost = $13,500 + $1,023 + $0 + $500 = $15,023

-

Carol Lee:

- Severance Pay = $7,000 x 7 = $49,000

- Vacation Pay = ($7,000 / 22) x 15 ≈ $4,773

- Bonus (assume $4,000 pro-rated) = $4,000

- Additional Benefits = $1,200

- Total Severance Cost = $49,000 + $4,773 + $4,000 + $1,200 = $58,973

Mind Map: Example Scenario Breakdown

Best Practices for Accounting Severance Pay

- Document Assumptions: Clearly record the basis for severance calculations.

- Use Consistent Policies: Apply company policies uniformly across all employees.

- Review Contracts: Check for any special severance clauses.

- Accrue Costs Timely: Recognize severance expenses in the period when the restructuring decision is made.

- Disclose Transparently: Include severance costs and assumptions in financial statement notes.

By following these steps and using clear examples, accountants and restructuring advisors can ensure accurate and compliant accounting for severance pay and related expenses during business restructuring.

3.5 Treatment of Asset Write-Downs and Impairments During Restructuring

When a business undergoes restructuring, one critical accounting consideration is the treatment of asset write-downs and impairments. These adjustments reflect a reduction in the recoverable value of assets, ensuring that the financial statements present a true and fair view of the company’s financial position.

Understanding Asset Write-Downs and Impairments

- Asset Write-Down: A reduction in the book value of an asset when its market value falls below its carrying amount, but the asset is still expected to generate future economic benefits.

- Asset Impairment: A more formal recognition that the carrying amount of an asset exceeds its recoverable amount, requiring an impairment loss to be recognized.

Why Asset Write-Downs and Impairments Occur During Restructuring

- Disposal or closure of business units leading to underutilized or obsolete assets.

- Changes in market conditions reducing asset value.

- Technological obsolescence.

- Strategic shifts in business focus.

Mind Map: Asset Write-Downs and Impairments in Restructuring

Best Practices for Accounting Asset Write-Downs and Impairments

- Early Identification: Regularly review assets for impairment indicators, especially during restructuring phases.

- Accurate Measurement: Use appropriate valuation techniques to determine recoverable amounts.

- Documentation: Maintain detailed records of assumptions, calculations, and decisions.

- Consistent Application: Apply accounting policies consistently across similar assets.

- Transparent Disclosure: Clearly disclose impairment losses and write-downs in financial statements.

Example 1: Write-Down of Manufacturing Equipment

Scenario: A company decides to close one of its manufacturing plants as part of restructuring. The plant’s specialized equipment has a carrying amount of $2 million. Due to the closure, the equipment’s fair value less costs to sell is estimated at $1.2 million.

Accounting Treatment:

- Recognize an impairment loss of $800,000 ($2 million - $1.2 million).

- Debit Impairment Loss (P&L) $800,000.

- Credit Equipment (Asset) $800,000.

Impact: The company’s net income decreases by $800,000, reflecting the reduced asset value.

Example 2: Impairment of Goodwill After Restructuring

Scenario: During restructuring, a business unit is downsized, and the goodwill allocated to that unit is tested for impairment. The carrying amount of goodwill is $5 million, but the recoverable amount is assessed at $3 million.

Accounting Treatment:

- Recognize an impairment loss of $2 million.

- Debit Impairment Loss (P&L) $2 million.

- Credit Goodwill $2 million.

Impact: This write-down reflects the diminished value of acquired goodwill due to restructuring.

Mind Map: Steps to Account for Asset Impairments

Additional Considerations

- Reversals: Under IFRS, impairment losses on assets (except goodwill) can be reversed if recoverable amounts increase.

- Group Reporting: Impairments may affect consolidated financial statements and require careful allocation.

- Tax Implications: Impairment losses may impact deferred tax calculations.

Summary

Accounting for asset write-downs and impairments during restructuring is essential to reflect the economic realities of the business. By following best practices and applying consistent methodologies, accountants and restructuring advisors can ensure transparent, accurate financial reporting that supports informed decision-making.

4. Accounting for Restructuring Provisions and Liabilities

4.1 Defining Provisions Under IFRS and GAAP

Understanding provisions is critical in accounting for business restructuring as they represent liabilities of uncertain timing or amount. Both IFRS and GAAP provide guidance on recognizing and measuring provisions, but there are nuanced differences.

What is a Provision?

A provision is a liability of uncertain timing or amount. It is recognized when:

- There is a present obligation (legal or constructive) as a result of a past event.

- It is probable that an outflow of resources embodying economic benefits will be required to settle the obligation.

- A reliable estimate can be made of the amount of the obligation.

Provisions Under IFRS (IAS 37)

- Scope: Covers provisions, contingent liabilities, and contingent assets.

- Recognition Criteria:

- Present obligation from a past event (obligating event).

- Probable outflow of resources.

- Reliable estimate can be made.

- Measurement: Best estimate of the expenditure required to settle the obligation.

- Examples: Restructuring provisions, warranty provisions.

Provisions Under US GAAP

- Scope: No specific standard named “provisions,” but similar concepts covered under ASC 450 (Contingencies).

- Recognition Criteria:

- Loss is probable (likely to occur).

- Loss amount can be reasonably estimated.

- Measurement: Best estimate or minimum amount in a range of loss.

- Examples: Restructuring accruals, asset retirement obligations.

Mind Map: Provisions Under IFRS and GAAP

Example 1: Recognizing a Restructuring Provision Under IFRS

Scenario: A company decides to close a manufacturing plant. The decision is communicated to employees, and the company has a detailed formal plan.

- Obligating Event: Board approval and communication to employees.

- Present Obligation: Legal or constructive obligation to pay severance and close the plant.

- Probable Outflow: Severance payments, contract termination costs.

- Reliable Estimate: Based on employee contracts and closure costs.

Accounting Treatment:

- Recognize a provision for the estimated costs in the period the decision is made.

Example 2: Recognizing a Restructuring Accrual Under US GAAP

Scenario: Similar to above, a company plans layoffs and plant closure.

- Loss is Probable: Management has committed to the plan.

- Reasonable Estimate: Severance costs can be estimated.

Accounting Treatment:

- Accrue the restructuring costs when the plan is committed and communicated.

Key Differences Summary

| Aspect | IFRS (IAS 37) | US GAAP (ASC 450) |

|---|---|---|

| Terminology | Provisions | Loss Contingencies / Accruals |

| Recognition Threshold | Probable (more likely than not) | Probable (likely to occur) |

| Measurement | Best estimate of expenditure | Best estimate or minimum in a range |

| Examples | Restructuring provisions, warranties | Restructuring accruals, asset retirement |

Best Practice Tips

- Documentation: Maintain clear evidence of the obligating event and estimates.

- Conservatism: Use prudent estimates but avoid overstatement.

- Review: Regularly reassess provisions as new information arises.

- Coordination: Work closely with legal and operational teams to identify obligations early.

By understanding these definitions and criteria, accountants and restructuring advisors can ensure accurate and compliant recognition of provisions during restructuring, providing stakeholders with transparent and reliable financial information.

4.2 Criteria for Recognizing Restructuring Provisions

Recognizing restructuring provisions accurately is critical for ensuring financial statements reflect the true economic impact of restructuring activities. Provisions are liabilities of uncertain timing or amount, and their recognition must comply with accounting standards such as IFRS (IAS 37) and US GAAP.

Key Criteria for Recognizing Restructuring Provisions

To recognize a restructuring provision, the following criteria must be met:

-

Present Obligation (Legal or Constructive)

- There must be a present obligation resulting from a past event.

- This obligation can be legal (contractual or statutory) or constructive (an established pattern of past practice or public commitment).

-

Probable Outflow of Resources

- It must be probable (more likely than not) that an outflow of resources embodying economic benefits will be required to settle the obligation.

-

Reliable Estimate of the Obligation

- The amount of the obligation can be estimated reliably.

Mind Map: Criteria for Recognizing Restructuring Provisions

Detailed Explanation

-

Present Obligation:

- A company must have a clear obligation to restructure. For example, if the board has approved a detailed restructuring plan and communicated it to affected parties, a constructive obligation exists.

- Example: A company announces closure of a manufacturing plant by year-end, creating a constructive obligation to pay severance and other closure costs.

-

Probable Outflow:

- The company should expect that it will have to pay costs related to the restructuring, such as employee termination benefits, contract termination penalties, or asset write-downs.

- Example: If the company expects to pay severance to 100 employees, it is probable that cash outflows will occur.

-

Reliable Estimate:

- The company must be able to estimate the costs with reasonable accuracy.

- Example: Severance pay can be calculated based on employee contracts and local labor laws.

Practical Example: Recognizing a Provision for Facility Closure

Scenario: A retail chain decides to close 5 stores due to poor performance. The board approves the closure plan on March 1st and publicly announces it on March 5th. The company expects to incur costs related to lease termination, employee severance, and asset write-downs.

Application of Criteria:

| Criterion | Application in Scenario | Result |

|---|---|---|

| Present Obligation | Board approval and public announcement create obligation | Met |

| Probable Outflow | Lease penalties, severance, asset write-downs expected | Met |

| Reliable Estimate | Lease terms known; severance calculated per contracts | Met |

Conclusion: The company should recognize a restructuring provision as of March 1st for the estimated costs.

Mind Map: Example - Facility Closure Provision

Additional Considerations

-

Exclusions:

- Future operating losses or costs associated with ongoing activities are not recognized as provisions.

- Example: Costs to run the remaining stores are not part of the provision.

-

Timing:

- Provisions should be recognized when the criteria are met, not necessarily when payments are made.

-

Documentation:

- Maintain detailed documentation of the restructuring plan, approvals, and cost estimates to support provision recognition.

By rigorously applying these criteria, accountants and restructuring advisors ensure that restructuring provisions are recognized appropriately, enhancing the transparency and reliability of financial reporting.

4.3 Best Practice: Documentation and Evidence for Provision Recognition

Proper documentation and evidence are critical when recognizing restructuring provisions to ensure compliance with accounting standards such as IFRS (IAS 37) and US GAAP. This section outlines best practices to establish a robust audit trail and support the recognition of provisions.

Key Elements of Documentation for Provision Recognition

- Detailed Description of the Restructuring Plan

- Nature and scope of restructuring activities

- Timeline and key milestones

- Management Approval Evidence

- Board resolutions or formal management sign-offs

- Minutes of meetings discussing the restructuring

- Obligating Event Identification

- Specific event triggering the obligation (e.g., contract termination, employee notification)

- Cost Estimates and Calculations

- Breakdown of expected costs (severance, lease termination, asset write-downs)

- Basis for estimates (quotes, historical data, expert opinions)

- Supporting Correspondence and Contracts

- Letters to employees or suppliers

- Termination agreements

- Accounting Judgments and Assumptions

- Rationale for recognition or non-recognition

- Discount rates applied if any

Mind Map: Documentation Components for Provision Recognition

Example: Documenting a Provision for Employee Termination Benefits

Scenario: A company plans to downsize and has formally approved a plan to terminate 50 employees.

- Restructuring Plan: Documented plan outlining the number of employees affected, timeline for termination, and expected cost savings.

- Management Approval: Board meeting minutes approving the downsizing plan dated March 15, 2024.

- Obligating Event: Notification letters sent to employees on March 20, 2024, creating a present obligation.

- Cost Estimates: Severance pay calculated based on contractual obligations and local labor laws, totaling $500,000.

- Supporting Evidence: Copies of termination letters and severance agreements.

- Accounting Judgment: Decision to recognize the provision in March 2024 financials based on the obligating event.

This documentation supports the recognition of the provision in compliance with accounting standards.

Mind Map: Example Documentation Flow for Employee Termination Provision

Additional Tips for Best Practice

- Maintain version control of all documents.

- Use standardized templates for restructuring plans and cost estimates.

- Ensure cross-functional review by finance, legal, and HR teams.

- Keep a centralized repository accessible for auditors and management.

- Regularly update documentation as new information arises or estimates change.

By following these best practices, accountants and restructuring advisors can ensure that provisions are recognized accurately and defensibly, minimizing audit risks and enhancing transparency.

4.4 Example: Recording a Provision for Facility Closure Costs

When a company decides to close a facility as part of its restructuring plan, it must recognize a provision for the associated closure costs if certain criteria are met. This section walks through an example of how to record such a provision, integrating best practices and clear explanations.

Step 1: Identify the Obligation

A provision can only be recognized when there is a present obligation (legal or constructive) as a result of a past event, and it is probable that an outflow of resources will be required to settle the obligation.

Example:

- Company XYZ decides on March 31, 2024, to close one of its manufacturing plants by September 30, 2024.

- The decision is communicated to employees and suppliers, creating a constructive obligation.

Step 2: Estimate the Costs

Estimate all direct costs related to the closure, such as:

- Employee termination benefits

- Contract termination penalties

- Decommissioning and cleanup costs

- Asset write-downs (though these are accounted separately)

Example:

- Severance pay for 50 employees: $500,000

- Contract termination penalties: $100,000

- Cleanup and decommissioning: $150,000

Total estimated closure cost: $750,000

Step 3: Measure the Provision

The provision should be measured at the best estimate of the expenditure required to settle the present obligation at the reporting date.

Step 4: Record the Provision in the Accounting System

Journal Entry Example:

| Account | Debit ($) | Credit ($) |

|---|---|---|

| Restructuring Expense | 750,000 | |

| Provision for Facility Closure | 750,000 |

This entry recognizes the restructuring expense in the income statement and the provision liability on the balance sheet.

Step 5: Disclose the Provision

In the notes to the financial statements, disclose:

- Nature of the obligation

- Expected timing of outflows

- Uncertainties about the amount or timing

Mind Map: Recording a Provision for Facility Closure Costs

Additional Example: Adjusting the Provision

Suppose by June 30, 2024, new information shows cleanup costs will be $200,000 instead of $150,000.

Adjustment Journal Entry:

| Account | Debit ($) | Credit ($) |

|---|---|---|

| Restructuring Expense | 50,000 | |

| Provision for Facility Closure | 50,000 |

This increases the provision and expense accordingly.

Best Practices Summary

- Ensure the obligation is present and clearly documented.

- Use realistic, supportable estimates for costs.

- Regularly review and adjust provisions as new information arises.

- Maintain clear audit trails for decisions and calculations.

- Provide transparent disclosures to stakeholders.

This example illustrates how accountants and restructuring advisors can systematically approach the recognition and measurement of provisions for facility closure costs, ensuring compliance with accounting standards and providing clear, actionable financial information.

4.5 Monitoring and Adjusting Provisions Over Time

In the context of business restructuring, provisions represent estimated liabilities for costs such as employee termination benefits, contract termination penalties, or facility closure expenses. However, these provisions are not static; they require continuous monitoring and adjustment to reflect the most accurate financial position of the company.

Why Monitoring and Adjusting Provisions is Critical

- Accuracy in Financial Reporting: Ensures that the financial statements reflect the current best estimate of liabilities.

- Compliance: Aligns with accounting standards such as IFRS (IAS 37) and US GAAP which require provisions to be reviewed at each reporting date.

- Decision Making: Provides management with up-to-date information to make informed decisions during restructuring.

Key Steps in Monitoring and Adjusting Provisions

Practical Example: Monitoring a Facility Closure Provision

Scenario: A company has recognized a provision of $2 million for closing one of its manufacturing plants. The initial estimate included costs for employee severance, contract terminations, and environmental cleanup.

| Reporting Date | Updated Estimate | Reason for Change | Provision Adjustment | New Provision Balance |

|---|---|---|---|---|

| Jan 1 | $2,000,000 | Initial recognition | +$2,000,000 | $2,000,000 |

| Apr 1 | $2,200,000 | Increased cleanup costs | +$200,000 | $2,200,000 |

| Jul 1 | $1,800,000 | Contract renegotiation savings | -$400,000 | $1,800,000 |

| Oct 1 | $1,800,000 | No change | $0 | $1,800,000 |

Explanation:

- At each quarter, the company reviews the provision based on new information.

- When cleanup costs increased, the provision was adjusted upwards.

- Contract renegotiations reduced expected costs, leading to a downward adjustment.

- Documentation is maintained for each adjustment to support audit trails.

Best Practices for Monitoring and Adjusting Provisions

Example: Adjusting Employee Termination Provisions

Initial Provision: $500,000 estimated for severance payments.

Update: After negotiations, severance packages are reduced by 10%.

Adjustment Entry:

- Debit Provision for Employee Termination Benefits $50,000

- Credit Profit & Loss $50,000 (reversal of excess provision)

This adjustment ensures the financial statements are not overstated and reflect the current expected outflow.

Summary

Monitoring and adjusting provisions over time is an essential part of restructuring accounting. It ensures that liabilities are neither understated nor overstated, maintaining the integrity of financial reporting and supporting effective management decisions. By following a structured approach with regular reviews, cross-functional collaboration, and thorough documentation, companies can manage their restructuring provisions efficiently and transparently.

5. Financial Reporting and Disclosure Requirements

5.1 Key Disclosure Requirements for Restructuring Activities

When a company undergoes restructuring, transparent and comprehensive disclosure in financial statements is crucial. This ensures stakeholders understand the financial impact, risks, and future outlook related to the restructuring process. Below, we explore the key disclosure requirements, supported by mind maps and practical examples.

Key Disclosure Areas for Restructuring Activities

Mind Map: Overview of Disclosure Requirements

Disclosure Requirements Mind Map

Example: Disclosure Note for a Restructuring Activity

XYZ Corporation undertook a restructuring plan in 2023 to streamline operations and reduce costs. The following disclosure note is an example of best practice:

Note X: Restructuring Activities

During the year ended December 31, 2023, XYZ Corporation initiated a restructuring plan aimed at consolidating manufacturing facilities and reducing workforce by 15%. The restructuring is expected to improve operational efficiency and reduce annual costs by approximately $10 million starting 2024.

Accounting Policies: Restructuring costs are recognized when a detailed formal plan is approved by management and communicated to affected employees. Provisions are measured at the best estimate of the expenditure required to settle the obligation.

Amounts Recognized:

- Employee termination benefits: $4.5 million

- Asset impairments: $2.0 million

- Contract termination costs: $1.0 million

- Other costs: $0.5 million

Provisions:

- Opening balance: $0

- Additions: $8.0 million

- Utilizations: $1.5 million

- Closing balance: $6.5 million

Timing and Uncertainties: The majority of restructuring costs are expected to be incurred within the next 12 months. Estimates are subject to change based on employee negotiations and asset disposal outcomes.

Impact on Financial Statements: The restructuring costs have been recognized in the income statement under operating expenses, resulting in a $8.0 million charge for the year.

Comparative Information: No restructuring activities were reported in the prior year.

Commitments: The company has contractual obligations related to lease terminations amounting to $0.8 million.

Mind Map: Example Disclosure Breakdown

Best Practices Summary

- Disclose the nature and rationale of restructuring clearly to provide context.

- Explain accounting policies to clarify recognition and measurement.

- Provide a detailed breakdown of costs and provisions.

- Highlight timing and uncertainties to inform about future cash flows and risks.

- Show the impact on financial statements transparently.

- Include comparative information for trend analysis.

- Disclose any commitments or contingencies related to restructuring.

- Update disclosures for subsequent events affecting restructuring.

By following these disclosure requirements and integrating clear examples, accountants and restructuring advisors can ensure that financial statements provide a full and transparent picture of restructuring activities, enhancing stakeholder confidence and compliance with accounting standards.

5.2 Best Practice: Transparent Reporting to Stakeholders

Transparent reporting during business restructuring is critical to maintaining trust and credibility with stakeholders such as investors, creditors, employees, and regulators. It ensures that all parties have a clear understanding of the financial impact, progress, and future outlook of the restructuring process.

Key Principles of Transparent Reporting

- Clarity: Use clear, jargon-free language to explain restructuring activities and their financial effects.

- Completeness: Disclose all relevant information, including assumptions, estimates, and uncertainties.

- Timeliness: Provide updates regularly to keep stakeholders informed throughout the restructuring.

- Consistency: Maintain consistent reporting formats and metrics to allow comparability over time.

Mind Map: Elements of Transparent Restructuring Reporting

Example: Transparent Disclosure in Financial Statements

A company undergoing restructuring includes the following note in its financial statements:

“During the fiscal year, the company initiated a restructuring plan aimed at streamlining operations and reducing costs. Restructuring expenses of $5 million were recognized, primarily related to employee severance and facility closures. Provisions of $3 million have been established for expected future costs. Management anticipates annual cost savings of approximately $8 million starting next fiscal year. These estimates are subject to change based on ongoing operational adjustments.”

This example demonstrates clarity by specifying amounts, completeness by detailing cost types, and future outlook by projecting savings.

Mind Map: Stakeholder-Specific Reporting Considerations

Example: Investor Presentation Slide

Slide Title: Restructuring Update and Financial Impact

- Overview of restructuring objectives

- Summary of costs incurred to date: $5M

- Expected annual savings: $8M

- Timeline for completion: 12 months

- Risks: Potential delays due to market conditions

This slide uses concise bullet points and quantifiable data to keep investors well-informed.

Best Practice Tips for Transparent Reporting

- Use Visual Aids: Charts, graphs, and timelines help stakeholders grasp complex information quickly.

- Regular Updates: Schedule quarterly or monthly updates depending on restructuring pace.

- Engage Stakeholders: Provide forums for questions and feedback to address concerns.

- Audit and Review: Ensure all reported data is verified and consistent with accounting records.

Summary

Transparent reporting is not just about compliance but fostering trust and enabling informed decision-making. By clearly communicating the financial impacts, progress, and future expectations of restructuring, accountants and restructuring advisors can help stakeholders navigate change confidently.

5.3 Example: Drafting Notes to Financial Statements on Restructuring

Drafting notes to financial statements regarding restructuring activities is a critical step to ensure transparency and compliance with accounting standards such as IFRS and GAAP. These notes provide stakeholders with detailed insights into the nature, timing, and financial impact of restructuring initiatives.

Key Components of Restructuring Notes

- Description of the Restructuring Plan: Outline the business rationale, scope, and objectives.

- Nature of Costs Recognized: Detail types of costs such as employee termination benefits, asset write-downs, and contract termination costs.

- Accounting Policies Applied: Explain how costs and provisions were recognized and measured.

- Amounts Recognized in the Reporting Period: Quantify expenses and provisions related to restructuring.

- Expected Timing of Cash Outflows: Provide estimates of when costs will be settled.

- Changes in Provisions: Reconcile opening and closing balances of restructuring provisions.

Mind Map: Structure of Restructuring Notes

Example Note to Financial Statements (Simplified)

Note X: Restructuring Activities

During the fiscal year ended December 31, 2023, the Company initiated a restructuring plan aimed at streamlining operations and reducing costs in response to market challenges. The plan involves workforce reductions, closure of two manufacturing facilities, and termination of certain contracts.

Costs Recognized:

The Company recognized restructuring expenses totaling $5.2 million, comprising:

- Employee termination benefits of $3.1 million

- Asset impairments of $1.4 million

- Contract termination costs of $0.7 million

Accounting Policies:

Restructuring costs are recognized when a detailed formal plan is approved by management and communicated to affected parties. Employee termination benefits are recognized in accordance with IAS 19 / ASC 712 when the obligation arises.

Provisions:

A restructuring provision of $4.8 million was recorded as of December 31, 2023, representing management’s best estimate of future cash outflows related to the plan. The provision is expected to be utilized over the next 12 months.

Movement in Restructuring Provisions: